hw assignment 400 - university of texas at austin · hw: 400 course: m339d/m389d - intro ......

TRANSCRIPT

HW: 400 Course: M339D/M389D - Intro to Financial Math Page: 1 of 4

University of Texas at Austin

HW Assignment 400

A smorgasbord of problems to prep for the final exam

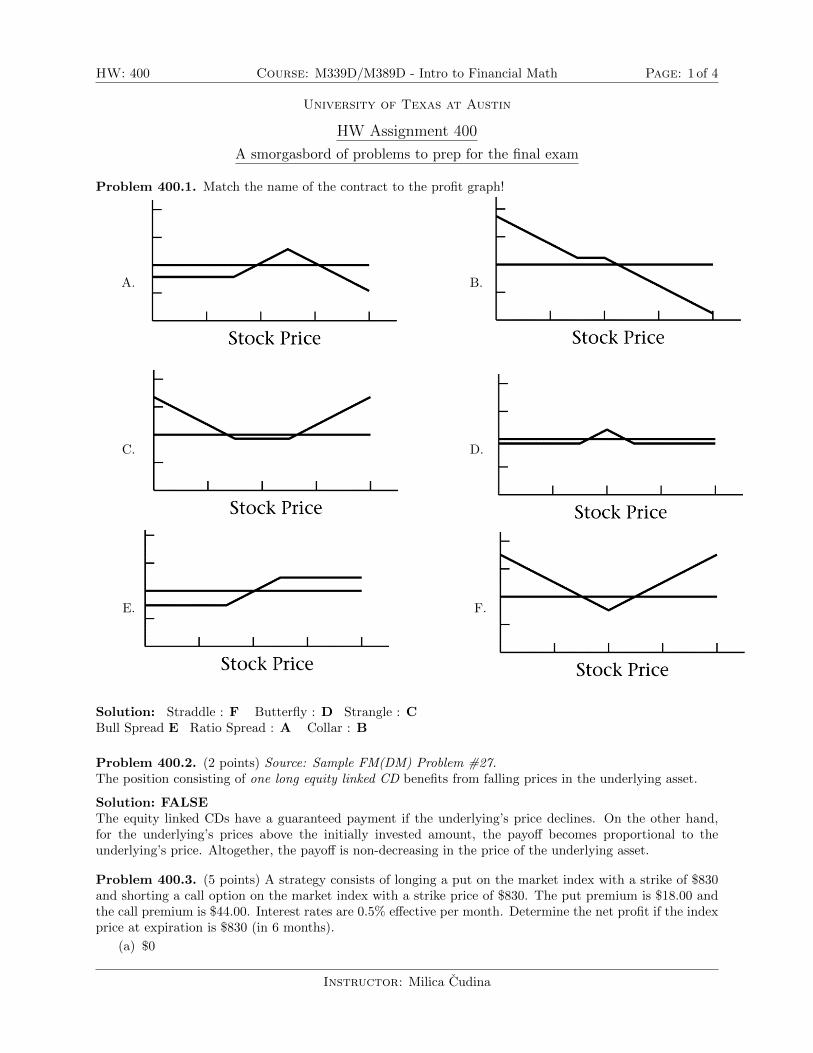

Problem 400.1. Match the name of the contract to the profit graph!

A.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 3-24

B.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 3-24

C.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 3-24

D.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 3-24

E.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 3-24

F.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 3-24

Solution: Straddle : F Butterfly : D Strangle : CBull Spread E Ratio Spread : A Collar : B

Problem 400.2. (2 points) Source: Sample FM(DM) Problem #27.The position consisting of one long equity linked CD benefits from falling prices in the underlying asset.

Solution: FALSEThe equity linked CDs have a guaranteed payment if the underlying’s price declines. On the other hand,for the underlying’s prices above the initially invested amount, the payoff becomes proportional to theunderlying’s price. Altogether, the payoff is non-decreasing in the price of the underlying asset.

Problem 400.3. (5 points) A strategy consists of longing a put on the market index with a strike of $830and shorting a call option on the market index with a strike price of $830. The put premium is $18.00 andthe call premium is $44.00. Interest rates are 0.5% effective per month. Determine the net profit if the indexprice at expiration is $830 (in 6 months).

(a) $0

Instructor: Milica Cudina

HW: 400 Course: M339D/M389D - Intro to Financial Math Page: 2 of 4

(b) $23.67 loss

(c) $26.79 gain

(d) $28.50 gain

(e) None of the above.

Solution: (c)In our usual notation, the expression for the payoff is

(K − S(T ))+ − (S(T ) −K)+ = K − S(T ) .

with K = 830. So, the payoff is 0 if S(T ) = 830.Since the profit calculation entails subtracting the future value of the initial cost, we have that the profit is

0 − (1 + 0.005)6(18 − 44) ≈ 26.79.

Problem 400.4. Source: Problem #2 from the Sample FM(DM) questions.You are given the following information:

(1) The current price to buy one share of XYZ stock is 500.(2) The stock does not pay dividends.(3) The risk-free interest rate, compounded continuously, is 6%.(4) A European call option on one share of XYZ stock with a strike price of K that expires in one year

costs $66.59.(5) A European put option on one share of XYZ stock with a strike price of K that expires in one year

costs $18.64.

Determine the strike price K.

(a) $449

(b) $452

(c) $480

(d) $559

(e) None of the above.

Problem 400.5. (5 points) Source: SoA Sample FM (DM) Problem #30.You are trying to decide whether to use forward contracts or futures contracts when committing to buy anunderlying asset at some date in the future. Which of the following is NOT a distinguishing characteristicof futures contracts, relative to forward contracts?

(a) Contracts are settled daily, and marked-to-market.

(b) Contracts are more liquid, as one can offset an obligation by taking the opposite position.

(c) Contracts are more customized to suit the buyers needs.

(d) Contracts are structured to minimize the effects of credit risk.

(e) Contracts have price limits, beyond which trading may be temporarily halted.

Solution: (c)

Problem 400.6. (5 points) Source: SoA Sample FM (DM) Problem #23.In our usual notation, you are given the following zero-coupon bond prices

P (0, 1) = 0.96154, P (0, 2) = 0.91573, P (0, 3) = 0.85770, P (0, 4) = 0.78466, P (0, 5) = 0.69656.

You enter into a 5-year interest rate swap (with a notional amount of $100,000) to pay a fixed rate and toreceive a floating rate based on future 1-year LIBOR rates. If the swap has annual payments, what is thefixed rate you should pay?

(a) 0.052

Instructor: Milica Cudina

HW: 400 Course: M339D/M389D - Intro to Financial Math Page: 3 of 4

(b) 0.057

(c) 0.067

(d) 0.072

(e) None of the above.

Solution: (d)Let us denote the fixed rate by R. Then, in our usual notation,

R =

∑5k=1 P (0, k)r0(k − 1, k)∑5

k=1 P (0, k).

We have5∑k=1

P (0, k)r0(k − 1, k) =

5∑k=1

P (0, k) · P (0, k − 1)

P (0, k)= 1 − P (0, 5) = 1 − 0.69656 = 0.30344.

Also,

5∑k=1

P (0, k) = 4.21619.

Finally, R = 0.30344/4.21619 ≈ 0.072.

Problem 400.7. (5 points)You are given that the swap prices for a one-year swap and a two-year swap are $2.25 and $2.60, respec-

tively. Assume that the zero-coupon bond yield rates for a one-year and a two-year bond are 4% and 5%,respectively.What is the forward price for a two-year forward contract on the same asset?

(a) About $2.97

(b) About $3.23

(c) About $3.47

(d) About $3.53

(e) None of the above.

Solution: (a)One year swap price and a one year forward price are the same. So, denoting the two-year forward price byf , we have

2.25/1.04 + f/1.052 = 2.60(1/1.04 + 1/1.052).

We get f ≈ 2.97.

Problem 400.8. (5 points) The current price of a non-dividend-paying stock is $75 per share. You modelthe stock price at the end of this year using a one-period binomial model under the assumption that thestock price can either increase by 1/5 of its current value or decrease by 1/5 of its current value.

A zero-coupon boon redeemable in one year for $100 currently sells for $95.What is the risk-neutral probability that the stock price will go up?

Solution: In our usual notation,

p∗ =e(r−δ)h − d

u− d=

er − d

u− d.

The conditions on the binomial asset-pricing model yield u = 1.2 and d = 0.8. The given bond price givesus that er = 100/95. So,

p∗ =10095 − 0.8

1.2 − 0.8= 0.6316..

Instructor: Milica Cudina

HW: 400 Course: M339D/M389D - Intro to Financial Math Page: 4 of 4

Problem 400.9. (5 points) The current price of a non-dividend-paying stock is $125 per share. You modelthe stock price at the end of this year using a one-period binomial model under the assumption that thestock price can either increase by $20, or decrease by $20.

The continuously compounded risk-free interest rate is given to be 0.04.What is the price of a one-year, $135-strike American call option on the above stock?

Solution: The risk-neutral probability of the stock price going up is

p∗ =125e0.04 − 105

40= 0.6275

The call option’s price is, thus,

VC(0) = e−0.04 × 0.6275 × (145 − 135) = 6.0293.

Problem 400.10. (5 points) The current price of a non-dividend-paying stock is $120 per share. You modelthe stock price at the end of this year using a one-period binomial model under the assumption that thestock price can either increase by $20, or decrease by $20.

The continuously compounded risk-free interest rate is given to be 0.04.What is the price of a one-year, $110-strike European option on the above stock?

Solution: The risk-neutral probability of the stock price going up is

p∗ =120e0.04 − 100

140 − 100= 0.6224.

The put option’s price is, thus,

VP (0) = e−0.04 × (1 − 0.6224) × (110 − 100) = 3.6276.

Instructor: Milica Cudina