hvcre (high volatility commercial real estate): a primer

TRANSCRIPT

Robert AshbaughExecutive Risk Management Consultant

Sageworks

P R E S E N T E D B Y

2

3

• Risk management thought leader for institutions and examiners

• Regularly featured in national and trade media

• Loan portfolio and risk management solutions

• More than 1,000 financial institution clients

• Founded in 1998

4

This presentation may include statements that constitute “forward-looking statements” relative to publicly available industry data. Forward-looking statements often contain words such as “believe,” “expect,” “plans,” “project,” “target,” “anticipate,” “will,” “should,” “see,” “guidance,” “confident” and similar terms. There can be no assurance that any of the future events discussed will occur as anticipated, if at all, or that actual results on the industry will be as expected. Sageworks is not responsible for the accuracy or validity of this publicly available industry data, or the outcome of the use of this data relative to business or investment decisions made by the recipients of this data. Sageworks disclaims all representations and warranties, express or implied. Risks and uncertainties include risks related to the effect of economic conditions and financial market conditions; fluctuation in commodity prices, interest rates and foreign currency exchange rates. No Sageworks employee is authorized to make recommendations or give advice as to any course of action that should be made as an outcome of this data. The forward-looking statements and data speak only as of the date of this presentation and we undertake no obligation to update or revise this information as of a later date.

5

Robert Ashbaugh

Executive Risk Management Consultant

Sageworks

HVCRE: a primer

• Why do the regulators care about HVCRE loans in the first place?

• HVCRE Loans: How did we get here?

• HVCRE Loans: All loans except for what?

• The Equity Contribution

Challenges

• HVCRE Risk Management

• How much HVCRE is there?

• HVCRE Capital Requirements

Relief on the horizon?

• HR 2148 to the rescue

• FFIEC EGRPRA Section 2222

6

7

8

9

10

11

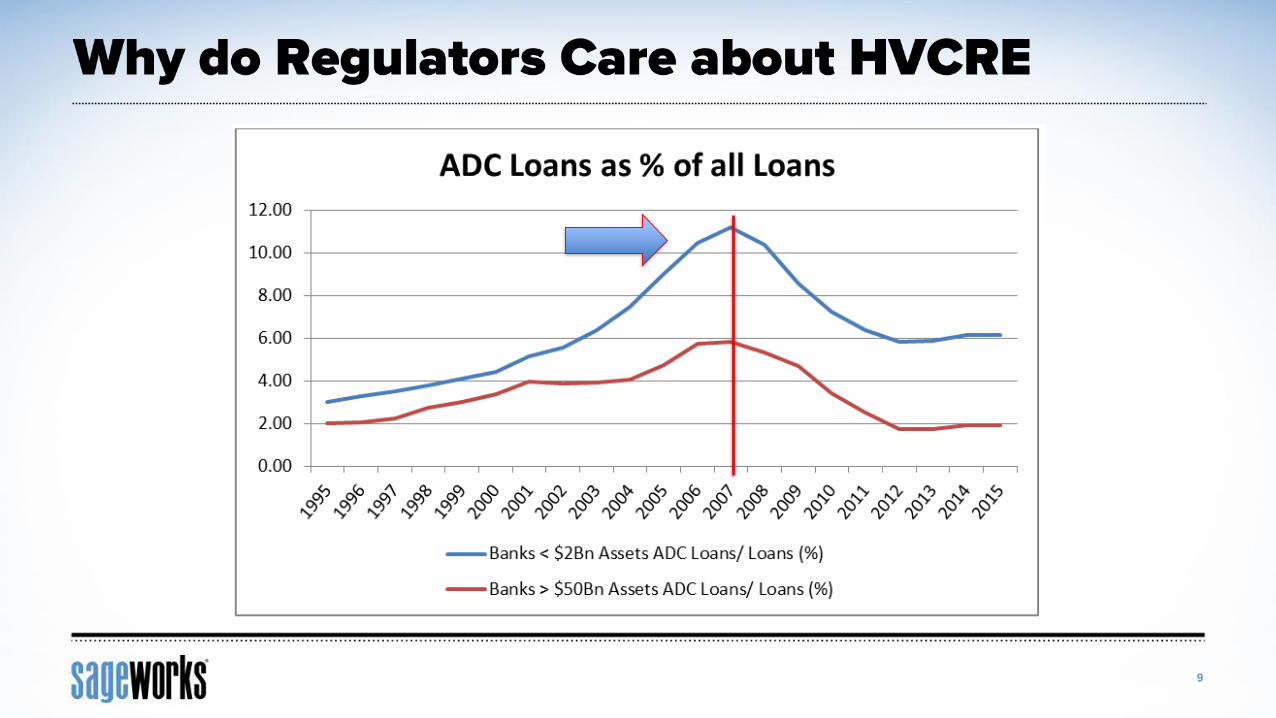

HVCRE is the result of the Basel III (2010) response to the impact of significant losses banks took on commercial real estate loans during the last recession

During the 1990s and 2000s CRE grew using CMBS and a regulatory environment that permitted lower capital requirements and did not place lending caps, merely supervisory limits

• Demand for product to feed CMBS boosted lending across the banking industry

• Limits were 100% of capital (construction) and 300% (all investor CRE)

» In 2006 31% of US banks exceed at least one limit• 23% that exceed both limits failed

• 13% that exceed the construction limit failed

• Accounted for 80% of the losses to the FDIC insurance fund

12

"a credit facility that, prior to conversion to permanent financing, finances or has financed the acquisition, development, or construction (ADC) of real property," with certain exclusions that MUST be all met:

1. LTV must be less than or equal to the maximum LTV ratio for certain types of loans

» Raw land 65%

» Land development 75%

» Non residential construction 80%

» Residential construction 85%

» Construction for improved properties 85%

2. Borrower capital contribution of 15% of the “as completed” value for the “life of the project”

3. The borrower capital contribution must be in place before bank funds are advanced and must remain in place until the loan is converted to permanent financing

13

Other exclusions:

• 1-4 Family Residential properties and the residential portion of mixed use properties

• Agricultural land loans

• Loans for

» Community development

» Public welfare

» Economic development

Be sure to have a testing process to identify potential HVCRE loans during the prospecting process

• Bankers should be familiar with the guidelines

• HVCRE loans should be specifically identified during both the pre-screen and final approval process

• Outline expectations and requirements with borrowers in advance

14

• Distributions cannot be made until the project is completed, or converted to perm

• The 15% equity contribution may take the form of cash or land, as long as the land is being used for the project

» Cash cannot come from 2nd lien financing, grants or leasing deposits

• The contribution cannot be borrowed from the bank giving the loan

» But it may be contributed from a non-bank financial or borrowed on an unsecured basis from another bank

• The contribution is based on the “as completed” value, or the expected value of the property at the time the project is completed

• Certain expenses paid by the borrower can count towards equity

» Site development

» Leasing and brokerage expenses

» Reasonable soft costs tied to the development

“Borrower needs to show skin in the game”

15

16

Loan Structuring considerations• Try to avoid HVCRE in the first place

» Simultaneous permanent loan in conjunction with the ADC loan» Be creative and know the definitions

• Define the conversion process to permanent• Equity contribution as a condition precedent

» Define and detail provisions

Define in commitment letter and loan documents:• Minimum DSCR• Define as-is LTV• Defining equity contribution

» Distributions only upon conversion to permanent financing

17

18

86 87

93

100

108 109113

117115

0

20

40

60

80

100

120

140

3/31/2015 6/30/2015 9/30/2015 12/31/2015 3/31/2016 6/30/2016 9/30/2016 12/31/2016 3/31/2017

Bill

ion

s

Total HVCRE Lending

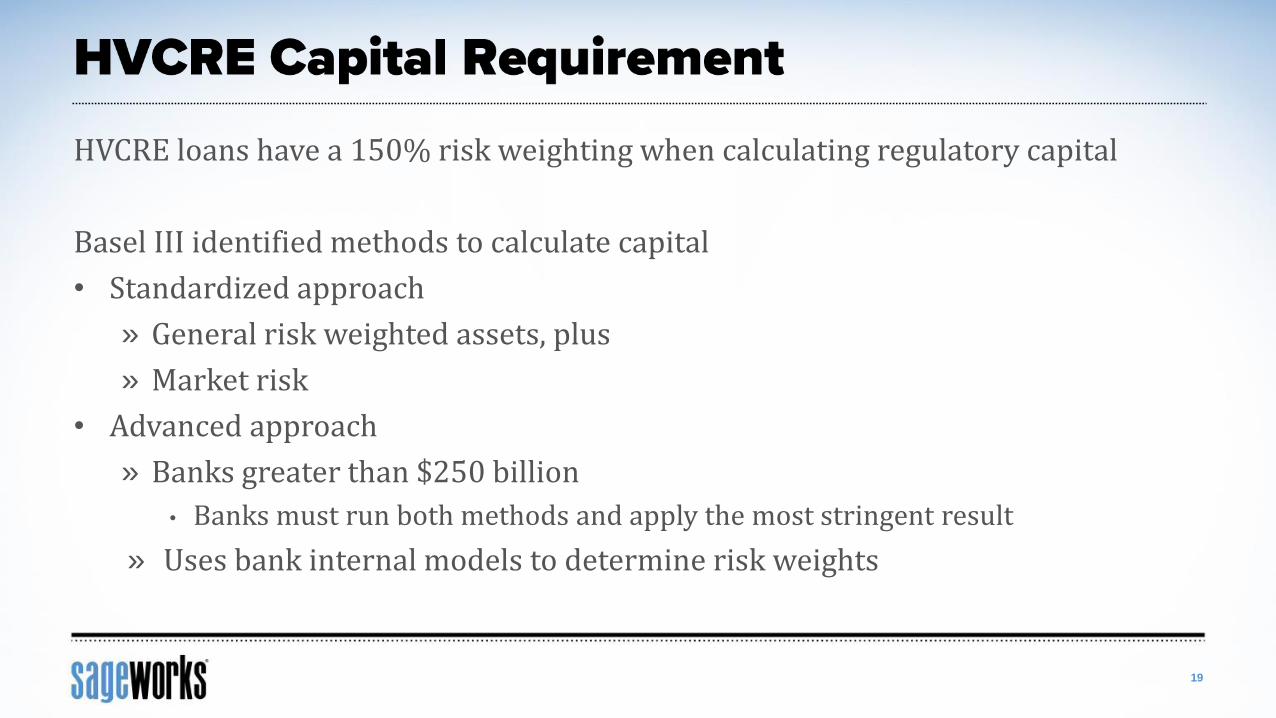

HVCRE loans have a 150% risk weighting when calculating regulatory capital

Basel III identified methods to calculate capital

• Standardized approach

» General risk weighted assets, plus

» Market risk

• Advanced approach

» Banks greater than $250 billion

• Banks must run both methods and apply the most stringent result

» Uses bank internal models to determine risk weights

19

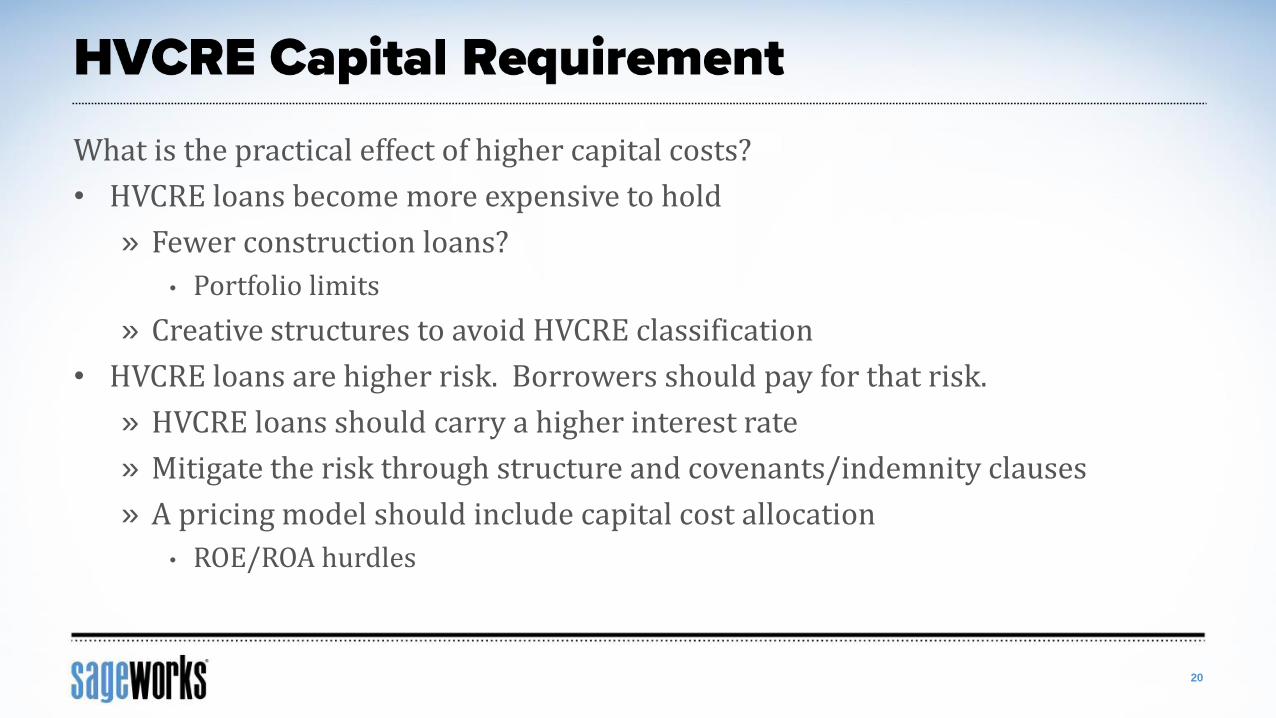

What is the practical effect of higher capital costs?

• HVCRE loans become more expensive to hold

» Fewer construction loans?

• Portfolio limits

» Creative structures to avoid HVCRE classification

• HVCRE loans are higher risk. Borrowers should pay for that risk.

» HVCRE loans should carry a higher interest rate

» Mitigate the risk through structure and covenants/indemnity clauses

» A pricing model should include capital cost allocation

• ROE/ROA hurdles

20

21

HR 2148• Bipartisan bill passed by the House on November 7 (Senate is reviewing)

• Applies to only new HVCRE loans and exempts loans originated before 2015

• HVCRE loans include loans that

» Finance or re-finances the acquisition or construction of real property

» Purpose is to develop property into income producing real property

» Will be dependent on future income proceeds

• Equity built up beyond the 15% threshold can be withdrawn

• Equity contribution is based on recent appraisal rather than purchase price

• ADC loans whose project is completed and are sufficiently cash flowing to cover debt service and expenses would become non-HVCRE loans

22

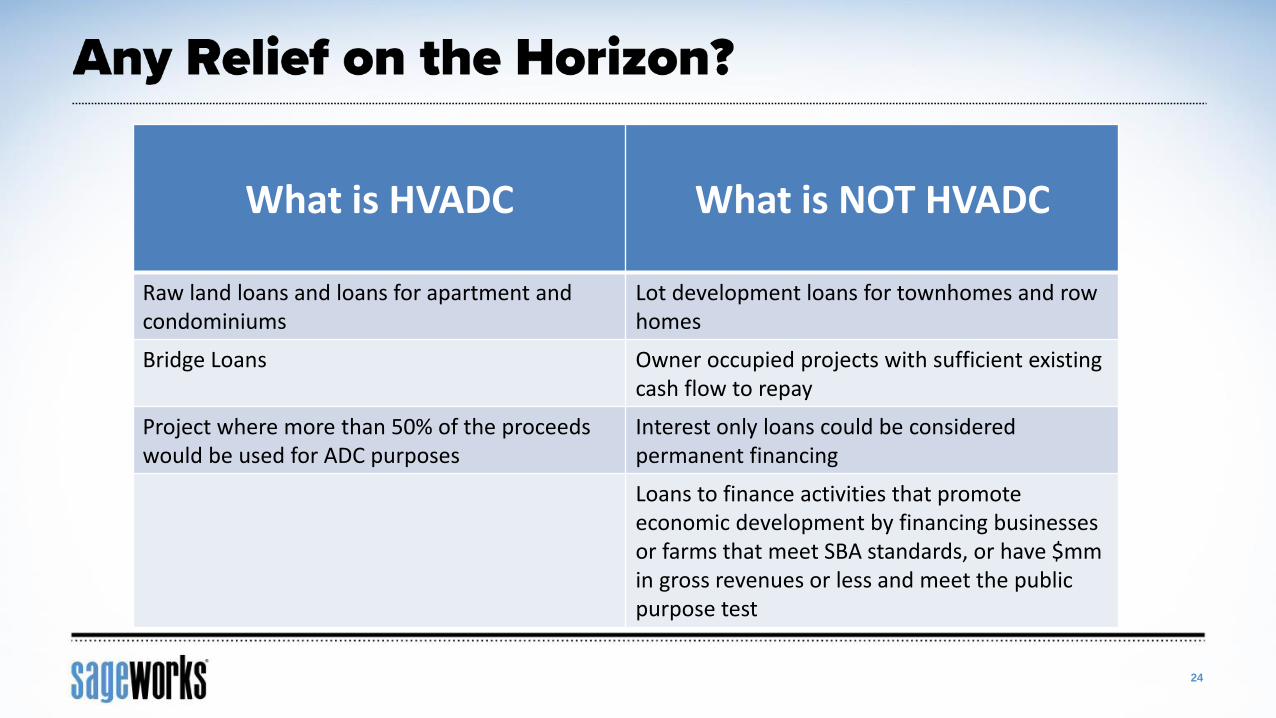

OCC, FDIC and the Federal Reserve have proposed HVADC• Proposed September 27 (60 day comment period just ended)

• Includes new loans that primarily (more than 50% used for the..) finance or refinance:

» The construction or improvement of existing buildings

» The development of land for new structures

» The purchase of vacant or developed land

• Capital charge is reduced from 150% to 130%

• Includes more loans under the rule as 15% equity contribution is eliminated

23

24

What is HVADC What is NOT HVADC

Raw land loans and loans for apartment and condominiums

Lot development loans for townhomes and row homes

Bridge Loans Owner occupied projects with sufficient existing cash flow to repay

Project where more than 50% of the proceeds would be used for ADC purposes

Interest only loans could be considered permanent financing

Loans to finance activities that promote economic development by financing businesses or farms that meet SBA standards, or have $mm in gross revenues or less and meet the public purpose test

25

• Sageworks.com – Learn about Sageworks’ risk management suite

» Sageworks Credit Analysis

» Sageworks Loan Pricing

» Sageworks ALLL

• Interested in talking with a specialist?

» Email us now: [email protected]

26

Robert AshbaughExecutive Risk Management [email protected]

SAGEWORKS LENDING SOLUTIONS

Eliminate data entry with the Electronic Tax Return Reader and core integrations

Integrated platform for the customer lifecycle

Exclusive benchmarks & risk models to support decision-making

Thought leader to help you navigate changing regulatory landscape

Responsive service & support from product experts

Insight into the best practices & templates used at 1,000+ financial institutions