how to reconcile an investment account

TRANSCRIPT

©2019 W

ithu

mSm

ith+B

row

n, P

C

1

©2019 WithumSmith+Brown, PC

How to Reconcile an Investment Account

©2019 W

ithu

mSm

ith+B

row

n, P

C

2

Jeremias Ramos, CPA

Tax Supervisor

Our Speaker

©2019 W

ithu

mSm

ith+B

row

n, P

C

3

Upon Completion of this course, participants will be able to:

• Be able to read a brokerage statement

• Reconcile a brokerage statement on a monthly and annual basis

• Reconcile K-1/PTP investments in a brokerage account

Learning Objectives

©2019 W

ithu

mSm

ith+B

row

n, P

C

4

Polling Question 1

©2019 W

ithu

mSm

ith+B

row

n, P

C

5

What is a Brokerage Account?

©2019 W

ithu

mSm

ith+B

row

n, P

C

6

What is a Brokerage Account?

In this section we will learn

▪ What is a brokerage account

▪ Why would a client have a brokerage account

▪ How to read a monthly account statement

©2019 W

ithu

mSm

ith+B

row

n, P

C

7

What is a Brokerage Account?

A brokerage account is a specific type of account that allows you to purchase investments.

You can open and fund a brokerage account with an investment company or brokerage firm, then use the money you’ve deposited to buy investments.

• Stocks

• Bonds

• Publicly Traded Partnerships

©2019 W

ithu

mSm

ith+B

row

n, P

C

8

What is a Brokerage Account?

Cash

Stocks

Bonds

Purchases Interest

PTPs

©2019 W

ithu

mSm

ith+B

row

n, P

C

9

What is a Brokerage Account?

Stocks

Bonds

PTPs

Cash

Opening Balance

DepositsWithdrawalsInterestDividendsPurchasesSalesChange in Market Value

Ending Balance

Summary of Activity Summary of Holdings

©2019 W

ithu

mSm

ith+B

row

n, P

C

10

Brokerage Account vs Cash Account

Brokerage Account

▪ Keep track of tax basis

▪ Report monthly and annual performance

▪ Summarizes tax reporting with 1099

▪ Can use investment advisor

Cash Account

▪ Doesn’t track investments

▪ Only reports monthly cash activity

▪ Tax reporting not summarized (tax form for every investment)

©2019 W

ithu

mSm

ith+B

row

n, P

C

11

How to Read the Statements

Every brokerage statement can be broken out into 3 main categories

1. Account Summary▪ Generally one of the first pages on the brokerage account. This

page will summarize monthly activity, current holdings, and monthly performance metrics.

2. Investment Holdings▪ Summarizes the various investments by category and keeps track

of cost basis, unrealized appreciation and fair market value

3. Transaction Detail▪ Shows the detail of transactions by transaction type and asset

category (i.e. income, deposits, purchases, sales, etc.)

©2019 W

ithu

mSm

ith+B

row

n, P

C

12

Account Summary

▪ Overview of account activity

▪ Reconciliation of opening and ending cash by transaction category

▪ Summarizes monthly income

▪ You can use this summary page to tie into your ending balances and reconcile to your Profit & Loss accounts

©2019 W

ithu

mSm

ith+B

row

n, P

C

13

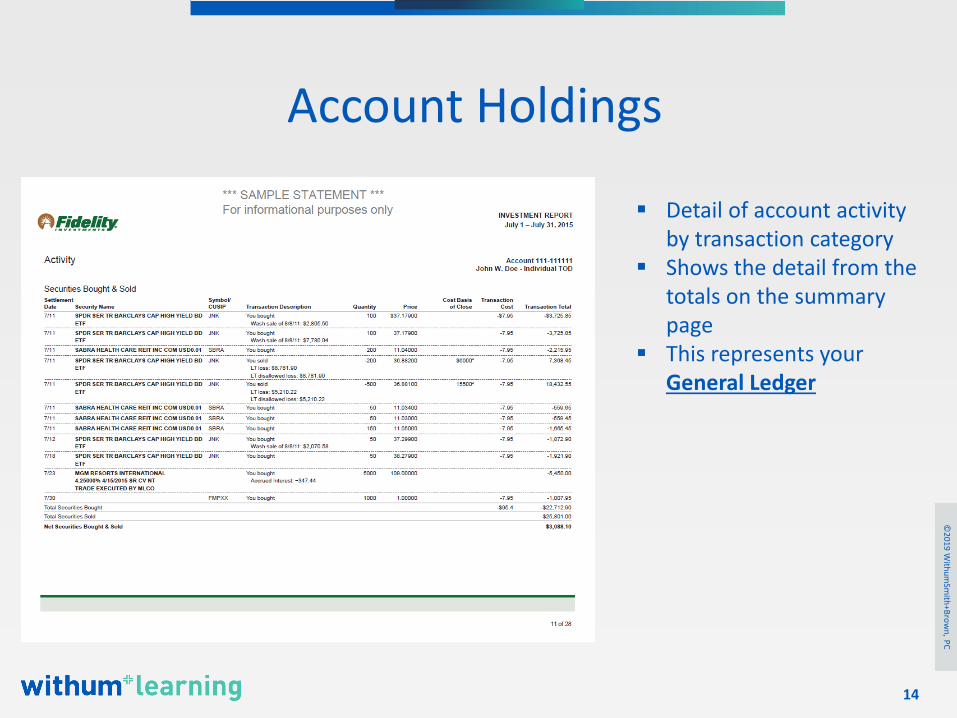

Account Holdings

▪ Overview of account holdings at the end of the month

▪ Keeps track of cost basis and unrealized gains/losses by asset category

▪ These balances represents the balances on your Balance Sheet by asset category

©2019 W

ithu

mSm

ith+B

row

n, P

C

14

Account Holdings

▪ Detail of account activity by transaction category

▪ Shows the detail from the totals on the summary page

▪ This represents your General Ledger

©2019 W

ithu

mSm

ith+B

row

n, P

C

15

Polling Question 2

©2019 W

ithu

mSm

ith+B

row

n, P

C

16

Monthly/Annual Reconciliations

©2019 W

ithu

mSm

ith+B

row

n, P

C

17

How Do I Reconcile a Brokerage

Statement?

In this section we will learn

▪ How to record monthly activity

▪ How to record adjusting journal entries

▪ How to reconcile 1099 to brokerage statements

©2019 W

ithu

mSm

ith+B

row

n, P

C

18

Start With Cash

Your cash account will fuel and be fueled by your investments.

• Interest income

• Dividend income

• Purchases of investments

• Sales of investments

• Deposits/Withdrawals

All of these transactions will hit the cash account so you can treat this activity as you would any other cash account

©2019 W

ithu

mSm

ith+B

row

n, P

C

19

Using Excel to Reconcile Cash

©2019 W

ithu

mSm

ith+B

row

n, P

C

20

Using QuickBooks to Reconcile Cash

©2019 W

ithu

mSm

ith+B

row

n, P

C

21

Reconcile Cash to the Statement

©2019 W

ithu

mSm

ith+B

row

n, P

C

22

Investment Account Journal Entries

After accounting for all the cash activity you will have to adjust for the non-cash activity

▪ Unrealized gains/losses

▪ Realized capital gain/loss adjustment

▪ Transferred in securities

▪ Other cost basis adjustments

©2019 W

ithu

mSm

ith+B

row

n, P

C

23

Unrealized Gains/Losses

Breakout asset accounts into tax cost basis and unrealized gain/loss. The total of these two will equal the ending FMV and tie to the statement. Unrealized gain or loss will be adjusted each month and the change in the account will hit the P&L

©2019 W

ithu

mSm

ith+B

row

n, P

C

24

Realized Gain/Loss Adjustment

Think of the sale of a security the same way you think about the sale of a business asset.

You will remove the tax asset from the balance sheet and net it against the proceeds to come up with a net capital gain/loss

Journal Entries:

Cash $100,000

Capital Gain/Loss $100,000

To record sale of security (already accounted for in cash activity)

Capital Gain/Loss $50,000

Stocks (Tax Basis) $50,000

To remove tax basis of asset from Balance Sheet

Unrealized Gain/Loss (P&L) $50,000

Unrealized Gain/Loss (Asset) $50,000

To remove unrealized gain/loss account from Balance Sheet

©2019 W

ithu

mSm

ith+B

row

n, P

C

25

Transfer in of Securities

If a client transfers in securities or other investments into an account (i.e. changes brokers or consolidates accounts) you will need to record the transfer in as a transfer or contribution

Stocks (Tax Basis) $20,000

Unrealized gain (Asset) $10,000

Contributions (Equity) $30,000

©2019 W

ithu

mSm

ith+B

row

n, P

C

26

Other Cost Basis Adjustments

Sometimes the cost basis will change from one statement to another with no corresponding change in cash. Nothing was sold or purchased but the broker is adjusting the cost basis.

Stocks (Tax Basis) $100

Other adjustments (P&L) $100

©2019 W

ithu

mSm

ith+B

row

n, P

C

27

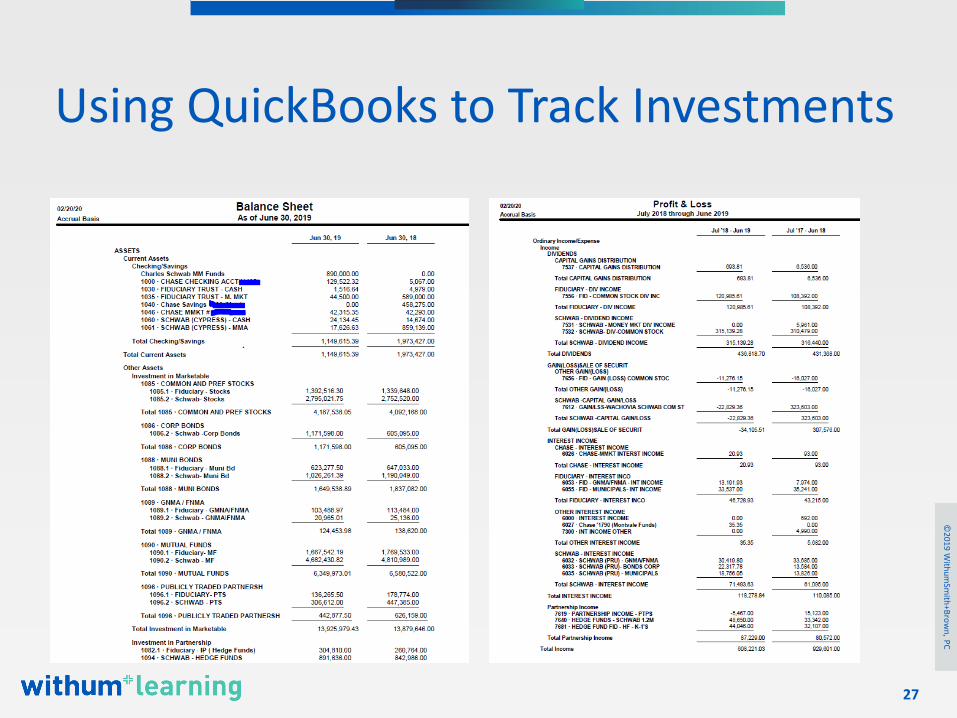

Using QuickBooks to Track Investments

©2019 W

ithu

mSm

ith+B

row

n, P

C

28

Polling Question 3

©2019 W

ithu

mSm

ith+B

row

n, P

C

29

How to Reconcile Partnership K-1s

©2019 W

ithu

mSm

ith+B

row

n, P

C

30

How Do I Reconcile

Partnership K-1s

In this section we will learn

▪ How to track partnership investments

▪ How to properly track tax cost

▪ How to report sales

©2019 W

ithu

mSm

ith+B

row

n, P

C

31

Investments in Partnership

▪ Investments in partnerships are treated differently than other investment assets.

▪ Hedge funds and publicly traded partnerships (PTPs) are often shown on the brokerage statement as “other assets” or “investments in partnerships”

▪ The taxpayer will also receive a K-1 from this investment each year that will be reported separately from the 1099

©2019 W

ithu

mSm

ith+B

row

n, P

C

32

Publicly Traded Partnerships

Publicly traded partnerships are just that –publicly traded. Investors buy shares just like they would any other publicly traded stock but PTPs are slightly different in that investors receive annual K-1s

3 things to look out for when an investment account has PTPs:1. Investment in PTPs will be shown as a

contribution on the K-1 and be picked up as tax basis on the brokerage account

2. Annual income/loss activity will impact your tax basis but won’t be shown on the brokerage account

3. Distributions may be reported as other dividends but should reduce tax basis

©2019 W

ithu

mSm

ith+B

row

n, P

C

33

Brokerage Account vs PTP Activity

Brokerage Account▪ New investment shown as

new asset▪ Distributions shown as

dividends or other deposits

▪ Income not reflected on brokerage account

▪ Sales don’t account for cost basis adjustment on brokerage account or 1099s

PTP K-1▪ New investment shown as

contribution on K-1▪ Distributions shown as a

reduction in basis on the K-1

▪ Income reported on the K-1

▪ Sales adjustments shown on the back of the PTP K-1 to account for distributions and income/losses

©2019 W

ithu

mSm

ith+B

row

n, P

C

34

PTP Journal Entries

Initial Contribution

Investment in PTP $10,000

Cash $10,000

Annual Activity

Investment in PTP $5,000

Interest $1,000

Dividends $4,000

Distributions

Cash $1,000

Investment in PTP $1,000

©2019 W

ithu

mSm

ith+B

row

n, P

C

35

Sale of PTP

▪ When there is a sale of a PTP interest the brokerage statement won’t match the K-1.

▪ Remember – the brokerage statement is only tracking initial investment and not the annual distributions and income/losses

▪ Your books will have a different tax cost than the brokerage statement so there will be a different gain/loss reported on your books vs the 1099

©2019 W

ithu

mSm

ith+B

row

n, P

C

36

Example of PTP Cost Adjustment

©2019 W

ithu

mSm

ith+B

row

n, P

C

37

Sale of PTP AJE

Cash $100,000

Capital Gain/Loss $100,000

To record proceeds from sale of PTP (in cash activity)

Capital Gain/Loss $50,000

Investment in PTP (Per 1099) $80,000

Investment in PTP (Cost Adj) $30,000

To record adjustment for sale of PTP

©2019 W

ithu

mSm

ith+B

row

n, P

C

38

Putting Everything Together

©2019 W

ithu

mSm

ith+B

row

n, P

C

39

Don’t Be Scared of Investment Accounts

▪ Reconcile cash accounts like you would any other account

▪ The Account Summary is your Profit &Loss (shows the month to date income/loss items)

▪ The Investment Holdings is your Balance Sheet (shown at tax cost basis and market value)

▪ The Account Activity is your General Ledger (reports all the activity for the month that impacts your cash and investments)

©2019 W

ithu

mSm

ith+B

row

n, P

C

40

What Did You Learn?

How to Read a Brokerage Statement

How to record monthly and yearly

activity

How to keep track of investments in Partnerships

How to reconcile an Investment Account

©2019 W

ithu

mSm

ith+B

row

n, P

C

41

Polling Question 4

©2019 W

ithu

mSm

ith+B

row

n, P

C

42

QUESTIONS OR COMMENTS?

©2019 W

ithu

mSm

ith+B

row

n, P

C

43

Thank [email protected]

Jeremias and other Withum experts are available to assist with training at your firm or organization. Email us to learn more.

@withum.com