how to leverage the small business payments toolkit · the small business payments toolkit has been...

TRANSCRIPT

How to Leverage the Small Business

Payments Toolkit

Matt Davies Payments Outreach Officer

Federal Reserve Bank of Dallas

Webinar of October 23, 2015

Mary Hughes Sr. Payments Info. Consultant

Federal Reserve Bank of Minneapolis

Logistics Call-in number: 888-625-5230 Conference code: 81415042# https://www.webcaster4.com/Webcast/Page/577/10508

Webinar You can choose to listen to the audio through your PC speakers or dial in through the

phone option. Please note: If you experience problems with the PC audio at any time, you can dial in using the number and code above.

Materials button

How we’ll take questions We will be holding questions until the end of the session, please submit them at any time

throughout the presentation via the Ask Question button in the webinar.

2

AGENDA

1) About the Small Business Payments Toolkit 2) U.S. Payment Trends 3) Brief Primer on Small Business Payment Types 4) Talking with Small Businesses about Payments 5) Educating Small Businesses about Payments Fraud

Views expressed today are those of the presenters and not the Federal Reserve Banks. The Small Business Payments Toolkit has been created by the Remittance Coalition & is intended to be used as a resource. Views expressed are not necessarily those of, & should not be attributed to, any particular Remittance Coalition participant or organization; nor are they intended to provide business or legal advice nor to promote or advocate a specific action, payment strategy, or product. Readers should consult with their own legal and business advisors.

What is the Small Business Payments Toolkit? • FREE resource to be leveraged by small business (&

their bankers & advisors) —Not copyrighted —OK to modify using Adobe Professional

• Encourages adoption of electronic B2B payments plus payment/remittance information exchanges —https://fedpaymentsimprovement.org/wp-

content/uploads/small-business-toolkit.pdf

4

Link to Toolkit

Created by the Remittance Coalition

5

Remittance Coalition

• Participation: National group of associations, small and large businesses, financial institutions, technology and software vendors, standards development organizations and others —Formed in 2011 —440+ members and growing —No dues or criteria for joining,

other than a willingness to work together

• Mission: Work together to solve problems related to processing remittance information associated with B2B payments in order to promote use of electronic payments and straight through processing (STP) ©2015 Federal Reserve Bank of Minneapolis. Materials are not to be used without consent.

6

Remittance Coalition Information

• Information about the Remittance Coalition: https://fedpaymentsimprovement.org/get-involved/remittance-coalition/

Visit the website to: Learn about activities Join the Remittance Coalition Volunteer on a project Listen to recorded webinars

©2015 Federal Reserve Bank of Minneapolis. Materials are not to be used without consent.

Contents of Small Business Payments Toolkit • Payment Types Explained • Understanding ACH • Working with Your Banker • Fraud Prevention & Mitigation Tips • Resources

— Glossaries of Payment Terms — Credit & Debit Card Resources — ACH Resources — General Small Business Resources — Fraud & Data Security Resources

7

8

Brief Primer on Small Business Payment Types

Small Business Payment Types

9

Small Business

Payments

ACH

Internet Bill Pay

Credit and Debit

Cards

Wire Transfer

Business Check

Payment Type Pros & Cons

10

Pros Cons

• Highly secure

• Near real time

• Certain delivery

• Fees charged to both parties

• Need routing & account #

Pros Cons

• Legacy System

• Widely accepted

• No need for Bank acct numbers

• Higher costs • Manual

handling • Greater

fraud frequency

Pros Cons

• Easy to use, widely accepted

• No need for routing & account #

• Costs higher –equipment & processing

• Fees incurred for reversal

Pros Cons

• Save time • Cost savings • Reduce

paper

• Some payments still via check

• Identify payee to system

Pros Cons

• Much lower fees

• Higher automation lower handling

• Much lower fraud

• ACH credit not final until settlement

• Need routing & account #

Internet Bill Pay

ACH

Business Check

Wire Transfer

Credit & Debit Cards

Comparing Payment Attributes

4%

8%

19%

19%

23%

37%

41%

53%

55%

60%

11%

57%

37%

38%

33%

38%

38%

35%

29%

28%

79%

9%

21%

5%

10%

8%

11%

7%

9%

4%

7%

27%

23%

38%

35%

17%

10%

6%

8%

9%

Best for international payments

Least costly

Best fraud protection

Most convenient

Best for working capital mgmt.

Best data accuracy

Best for avoiding duplicate payments

Easiest to integrate with AP system

Most complete remittance info.

Highest supplier acceptance

Check ACH Wires Cards

11

Source: PayStream Advisors, Electronic Payments and Card Solutions in 2015: Perceptions, Realities, and Strategies, Q3 2015.

Which payment method best represents each attribute?

©2015 Federal Reserve Bank of Minneapolis. Materials are not to be used without consent.

Top Challenges in Payments Processing

4%

12%

12%

13%

20%

25%

30%

35%

Loss from fraud

Employee confusion overcorrect payment method to use

More than one payment methodfor some suppliers

Lack of payment visibility

Duplicate payments

Missed discounts

Late payments

High processing costs

12

Challenges mostly result from manual payment management and they do not differ

between larger and small organizations.

Source: PayStream Advisors, Electronic Payments and Card Solutions in 2015: Perceptions, Realities, and Strategies, Q3 2015. ©2015 Federal Reserve Bank of Minneapolis. Materials are not to be used without consent.

U.S. Payment Trends

B2B Check Usage is Stagnant

14

0

5

10

15

20

25

30

35

2006 2009 2012

Chec

ks in

bill

ions

Number of Checks Written by Counterparty

C2C

C2B

B2C

B2B

Source: Federal Reserve Payments Studies published in 2007, 2010, and 2013. See https://www.frbservices.org/communications/payment_system_research.html for reports.

©2015 Federal Reserve Bank of Minneapolis. Materials are not to be used without consent.

Checks Are the Leading Payment Type among Businesses

Check, 66%

ACH, 20%

Wire Transfer, 8%

Cards, 6% Other, 1%

% of Payment Transactions Made by Corporations, by Payment Type

©2015 Federal Reserve Bank of Minneapolis. Materials are not to be used without consent.

15 Source: 2014 Phoenix-Hecht Treasury Management Monitor, survey of corporations with annual sales of above $20 million.

Most Organizations Use Checks for at Least Half of B2B Payments

63%

21%

3% 4%

82%

41%

15% 21%

Checks ACH Wires Cards

Used for at least 50% of B2B PaymentsUsed for at least 20% of B2B payments

What percentage of your supplier-related payments is processed using the

following methods?

16

Source: PayStream Advisors, Electronic Payments and Card Solutions in 2015: Perceptions, Realities, and Strategies, Q3 2015.

©2015 Federal Reserve Bank of Minneapolis. Materials are not to be used without consent.

Profile of Heavy Check Users

81%

27%

15%

17%

29%

40%

44%

49%

56%

64%

Have taken actions to decrease checks in past2 years

Cite high processing costs among greatestpayment challenges

Say many suppliers specifically request checks

Have not addressed check usage in past 2years

Under $100 million in annual revenue

Heavy Check Users Remainder of Repsondents

17

“Heavy users” rely on checks for at least three-quarters of their payments

Source: PayStream Advisors, Electronic Payments and Card Solutions in 2015: Perceptions, Realities, and Strategies, Q3 2015.

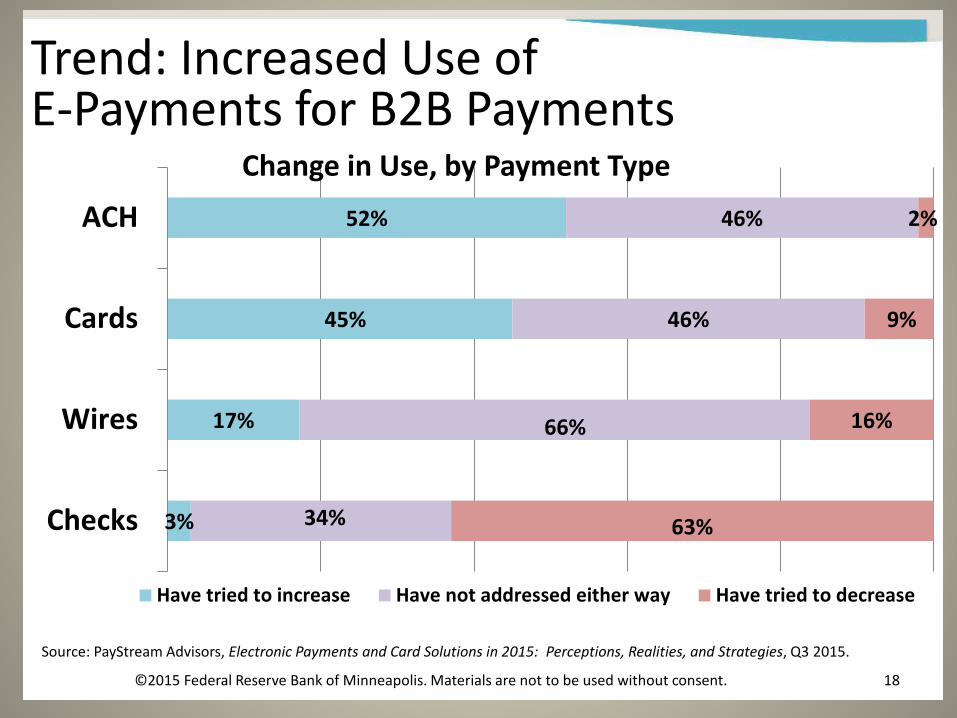

Trend: Increased Use of E-Payments for B2B Payments

3%

17%

45%

52%

34%

66%

46%

46%

63%

16%

9%

2%

Checks

Wires

Cards

ACH

Change in Use, by Payment Type

Have tried to increase Have not addressed either way Have tried to decrease

©2015 Federal Reserve Bank of Minneapolis. Materials are not to be used without consent.

18

Source: PayStream Advisors, Electronic Payments and Card Solutions in 2015: Perceptions, Realities, and Strategies, Q3 2015.

Talking with Small Businesses

Using Electronic Payments is a Smart Choice for Small Businesses

20

• Efficiency —Lower costs of payments handling —Free up staff resources

• Security — Lower risk of fraud losses

• Reliability • Strengthen customer retention by setting up recurring

payments • Direct deposit of payroll boosts employee productivity • Business growth/ increase revenue opportunities

— Some large trading partners and government contracts require acceptance of ACH payments

What Can Electronic Payments Do for Small Businesses? • Using ACH, wires and / or cards can improve cash

flow —Predictable and managed posting of transactions —Take advantage of discounts

• Offers way to impose requirements on slow-paying customers —Payment due before product/services delivered —ACH credits, wires, or cards

• Offer an incentive to pay early or to use an electronic payment method over paper

21

Talking about ACH with Small Businesses • Many small businesses already understand ACH through payroll

— Use as a starting place for discussion o Educate on fee structure and options o Talk about number of payments required to justify costs

• Discuss ACH implementation issues — Determine how to originate ACH – in-house or hire third party — Requires underwriting

o Complex authorization forms required for risk underwriting and security

o Other options (e.g. pre-fund) — Workflow and control issues

o Must manage and secure payment identity of each payee Routing/transit number

22

Advice on Working with Bankers • Small businesses should be proactive: contact bankers

about payment needs • Shop around to find the best bank with services the small

business needs, e.g., ACH origination services, remote deposit capture, merchant services, etc.

• Seek out experts at your bank • Bring information (payrolls, examples of incoming and outgoing payments,

card usage) to the meeting with your banker — Ask bank to suggest payment options best for your business

• Seek out (free) risk mitigation services and fraud prevention tools offered by your bank

• Have a discussion on prices: negotiate fees • Ask about workflow and control issues you may need to address • Ask about best practices for managing the payment identity of each payee

23

Guidance on Accepting Cards

• Accepting cards may make small businesses more competitive and may boost sales

• However, card acceptance comes with risk —The Small Business Payments Toolkit contains:

o Tips to help small business lower the risk of accepting fraudulent cards Best practices for employees who handle cards

oConsiderations to help avoid internal card fraud o Education on handling disputes and chargebacks

24

Educating Small Businesses about Payments Fraud

Payments Fraud

26

The Toolkit contains best practices & tips to help small businesses combat payment-related fraud and manage risks:

Check fraud ACH fraud Mobile banking fraud Avoid purchasing card fraud Bank services that can combat fraud Educating and training your employees to avoid payments

fraud Avoiding data breaches ….AND MUCH MORE!

All payment methods carry the risk of fraud

Small Business Fraud Prevention by Payment Type

27

Wire • Use dual control • Require form for initiation, rather than

fax or e-mail • Require call-back/voice confirmation

Check • Implement strong internal controls

and procedures around AR/AP functions

• Leverage tool and processes from your bank and service providers; enact best practices (e.g., positive pay)

• Consider not accepting checks • Limit number of checks issued

Purchasing Card • Use p-card program and tools • Monitor transaction activity Acceptance of Credit Cards • Toolkit contains tips to avoid

accepting fraudulent cards

Mobile Banking • Encryption and strong passwords • Disable wireless, Bluetooth, and NFC

when not in use • Apply patches timely • Update software/hardware • Limit access • Develop and follow policies

ACH Debit • Limit debit activity to a few accounts • Address exceptions timely • Restrict access to PC • Use out of band authentication

process ACH Credit • Use dual control • Require due diligence

Small Business

Payments

ACH

Internet Bill Pay

Credit and Debit

Cards

Wire Transfer

Business Check

Check Fraud

• Examples —Mail theft —Counterfeit checks —Alterations —Duplicate deposits

• Precautions — Implement strong internal controls

& procedures around AR/AP functions

— Leverage tools & processes from your bank and service providers; enact best practices (e.g., positive pay, reverse positive pay)

—Consider not accepting checks at all —Limit number of checks issued

28

ACH Fraud • Examples

—Unauthorized debits

—Insider fraudulent transactions

—Hacker attacks (phishing, etc.)

• Precautions ACH Debit

—Limit debit activity to a few accounts

—Address exceptions timely —Secure bank account info —Use ACH blocks, filters,

positive pay, & debit alerts ACH Credit

—Use dual control —Require due diligence of 3rd

party processors 29

What Should Small Businesses Be Doing? • Check accounts daily • Use fraud protection services

(e.g., debit blocks/filters; positive pay)

• Ensure fraud prevention and detection is an organizational objective —Set policies, establish

procedures, monitor compliance, and take action on exceptions 30

What Should Small Businesses Be Doing? continued

• Educate and train employees on fraud prevention • Implement security best practices

—Secure bank account information, lock up paper documents, limit access to sensitive online data

—Use strong passwords and change them often —Monitor and measure fraud attempts and losses

• Update defenses; best practices today may not be best practices tomorrow

31

Take Action

• The toolkit was developed as a FREE resource for you – USE IT AND SHARE IT. —Reference the toolkit when speaking

with small business customers • Version 2 of the toolkit is currently being developed

—Topics include: o EMV migration o Emerging/Alternative payments o Authorization forms o Handling ACH returns o Case studies

—Suggestions on content are welcomed! 32

Check out the Resources Pages!

• The Small Business Payments Toolkit offers links to additional information on:

• Glossaries of payment-related terminology • Credit and debit cards • ACH • General resources for small

business practitioners • Fraud and data security

33

Questions

34 ©2015 Federal Reserve Bank of Minneapolis. Materials are not to be used without consent.