housing authority of st. landry...

TRANSCRIPT

^/OD

HOUSING AUTHORITY OF ST. LANDRY PARISH, LOUISIANA

AUDITED FINANCIAL REPORT

YEAR ENDED JUNE 30,20lb

Under provisions of state law, this report is a public document. A copy of the report has been submitted to the entity and other appropriate public ofilcials. The report is available for public inspection at the Baton Rouge office of the Legislative Auditor and, where appropriate, Bi the office of the parish clerk of court.

Release Date c^Mii

TABLE OF CONTENTS

FINANCIAL SECTION Page

Management's Discussion and Analysis i - vii

Independent Auditor's Report 1-2

Financial Statements:

Statement ofNet Assets 4-5

Statement of Revenues, Expenses, and Changes in Net Assets 6

Statement of Cash Flows 7-8

Notes to Financial Statements 9-16

Other Reports and Schedules:

Schedule of Expenditures of Federal Awards 18

Report on Intemal Control over Financial Reporting And on Compliance And Other Matters Based on an Audit of Financial Statements Performed in Accordance With Govemment Auditing Standards 19-20

Report on Compliance with Requirements That Could Have a Direct and Material Effect on Each Major Program And on Intemal Control over Compliance in Accordance with OMB Circular A-133 21-22

Status of Prior Audit Findings 23

Findings and Questioned Costs 24

Statement and Certification of Actual Modernization Costs 25

Financial Data Schedules 26-35

HOUSING AUTHORITY OF ST LANDRY, LOUISIANA

REQUIRED SUPPLEMENTAL INFORIMATION

MANAGEMENT DISCUSSION AND ANALYSIS (MD&A)

JUNE 30,2010

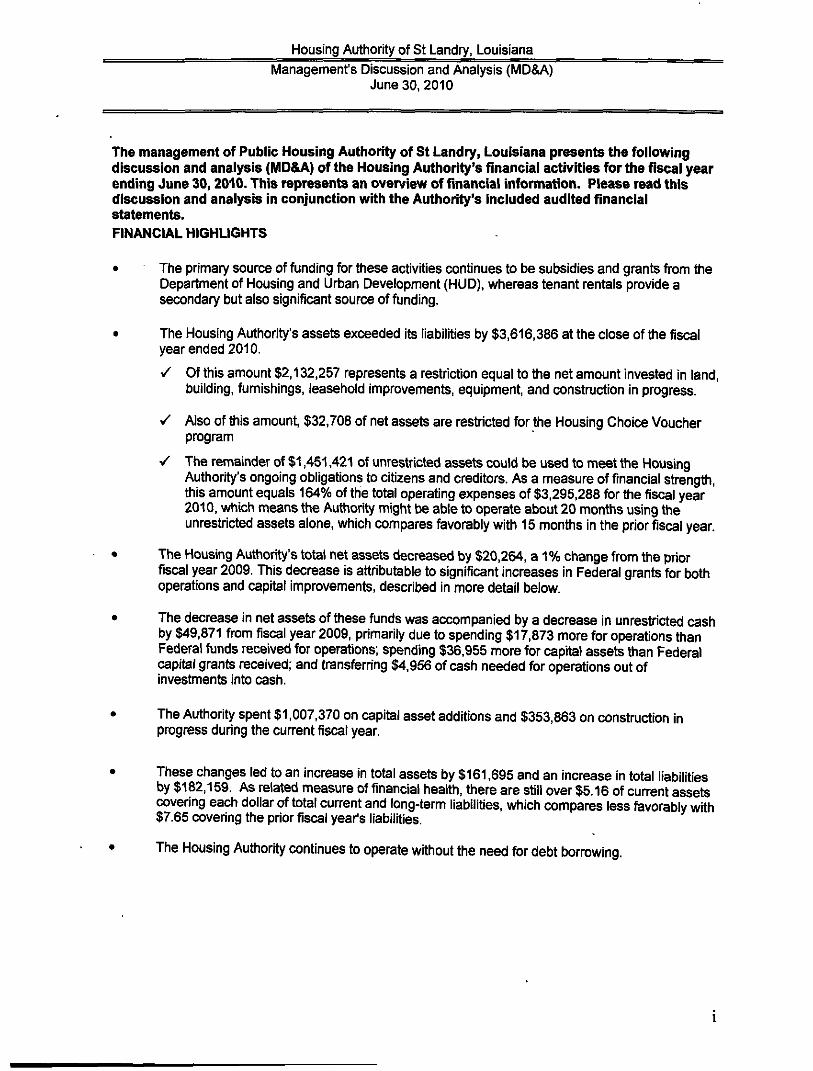

Housing Authority of St Landry, Louisiana Management's Discussion and Analysis (MD&A)

June 30, 2010

The management of Public Housing Authority of St Landry, Louisiana presents the following discussion and analysis (MD&A) ofthe Housing Authority's financial activities forthe fiscal year ending June 30,2010. This represents an overview of financial information. Please read this discussion and analysis in conjunction with the Authority's Included audited financial statements. FINANCIAL HIGHLIGHTS

• The primary source of funding for these activities continues to be subsidies and grants from the Department of Housing and Urban Development (HUD), whereas tenant rentals provide a secondary but also significant source of funding.

• The Housing Authority's assets exceeded its liabilities by $3,616,386 at the close of the fiscal year ended 2010.

• Of this amount $2,132,257 represents a restriction equal to the net amount invested In land, building, furnishings, leasehold improvements, equipment, and constmction in progress.

>/ Also of this amount, $32,708 of net assets are restricted for the Housing Choice Voucher program

•/ The remainder of $1,451,421 of unrestricted assets could be used to meet the Housing Authority's ongoing obligations to citizens and creditors. As a measure of financial strength, this amount equals 164% of the total operating expenses of $3,295,288 for the fiscal year 2010, which means the Authority might be able to operate about 20 months using the unrestricted assets alone, which compares favorably with 15 months in the prior fiscal year.

• The Housing Authority's total net assets decreased by $20,264, a 1% change from the prior fiscal year 2009. This decrease is attributable to significant increases in Federal grants for both operations and capital improvements, described in more detail below.

• The decrease In net assets of these funds was accompanied by a decrease in unrestricted cash by $49,871 from fiscal year 2009, primarily due to spending $17,873 more for operations than Federal funds received for operations; spending $36,955 more for capital assets than Federal capital grants received; and transferring $4,956 of cash needed for operations out of investments Into cash.

• The Authority spent $1,007,370 on capital asset additions and $353,863 on construction in progress during the current fiscal year.

• These changes led to an Increase in total assets by $161,695 and an increase in total liabilities by $182,159. As related measure of financial health, there are still over $5.16 of current assets covering each dollar of total current and long-term liabilities, which compares less favorably with $7.65 covering the prior fiscal year's liabilities.

• The Housing Authority continues to operate without the need for debt borrowing.

Housing Authority of St Landry, Louisiana Management's Discussion and Analysis (MD&A)

June 30, 2010

OVERVIEW OF THE FINANCIAL STATEMENTS

This MD&A is Intended to serve as an Introduction to the Housing Authority's basic financial statements. The Housing Authority Is a special-purpose government engaged in business-type activities. Accordingly, only fund financial statements are presented as the basic financial statements, comprised of two components: (1) fund financial statements and (2) a series of notes to the financial statements. These provide infomiation about the activities of the Housing Authority as a whole and present a longer-temi view of the Housing Authority's finances. This report also contains other supplemental Information in addition to the basic financial statements themselves demonstrating how projects funded by HUD have been completed, and whether there are inadequacies In the Authority's internal controls.

Reporting on the Housing Authority as a Whole

One of the most important questions asked about the Authority's finances is, "Is the Housing Authority as a whole better off, or worse off, as a result of the achievements of fiscal year 2010?" The Statement of Net Assets and the Statement of Revenues, Expenses, and Changes in Net Assets report information about the Housing Authority as a whole and about its activities in a way that helps answer this question. These statements include all assets and liabilities using the accmal basis of accounting, which Is similar to the accounting used by most private-sector companies. All of the cun-ent year's revenues and expenses are taken Into account regardless of when cash is received or paid.

Fund Financial Statements

All of the funds of the Housing Authority are reported as proprietary funds. A fund Is a grouping of related accounts that Is used to maintain control over resources that have been segregated for specific activities or objectives. The Housing Authority, like other enterprises operated by state and local govemments, uses fund accounting to ensure and demonstrate compliance with finance-related legal requirements.

The Housing Authority's financial statements report its net assets and changes In them. One can think of the Housing Authority's net assets - the difference between assets and liabilities - as one way to measure the Authority's financial health, or financial position. Over time, increases and decreases In the Authority's net assets are one indicator of whether its financial health is Improving or deteriorating. One wilj need to consider other non-financial factors, however, such as the changes in the Authority's occupancy levels or its legal obligations to HUD, to assess the overall health ofthe Housing Authority.

USING THIS ANNUAL REPORT

The Housing Authority's annual report consists of financial statements that show combined information about the Housing Authority's most significant programs:

Low Rent Public Housing Housing Choice Vouchers Public Housing Capital Fund Program DVP HOME Ownership

n

Housing Authority of St Landry, Louisiana Management's Discussion and Analysis (MD&A)

June 30, 2010

The Housing Authority's auditors provided assurance In their independent auditors' report with which this MD&A is included, that the basic financial statements are fairly stated. The auditors provide varying degrees of assurance regarding the other information Included in this report. A user of this report should read the Independent auditors' report carefully to detennine the level of assurance provided for each of the other parts of this report.

Reporting the Housing Authority's Most Significant Funds

The Housing Autiiority's financial statements provide detailed information about the most significant funds. Some fijnds are required to be established by the Department of Housing and Urban Development (HUD). However, the Housing Authority establishes other funds to help it control and manage money for particular purposes, or to show that it is meeting legal responsibilities for using grants and other money.

The Housing Authority's enterprise funds use the following accounting approach for Proprietary funds: All of the Housing Authority's services are reported in enterprise fijnds. The focus of proprietary funds is on income measurement, which, together with the maintenance of net assets. Is an important financial indicator

FINANCIAL ANALYSIS The Housing Authority's net assets were $3,616,386 as of June 30, 2010. Of this amount, $2,132,257 was invested in capital assets, and the remaining $1,451,421 was unrestricted. There was $33,266 in specific assets restricted for Housing Choice Voucher program. Also, there were $33,266 of general net assets restricted for the Housing Choice Voucher program

CONDENSED FINANCIAL STATEMENTS Condensed Balance Sheet

(Excluding Interfund Transfers) Asof June 30,2010

2010 2009

ASSETS Current assets Assets restricted for Housing Choice Voucher program. Capital assets, net of depredation

Total assets

LIABILITIES Current liabilities Non-current liabilities

Total liabilities

NET ASSETS Invested in capital assets, net of depreciation Net assets restricted for the Housing Choice Voucher program Unrestricted net assets

Total net assets

Total liabilities and net assets

$1,799,329 33,266

2,132,257

3,964,852

313,216 35.250

348.466

2,132,257

32,708 1,451,421

3,616,386

3,964,852

$1,273,940 567,431

1,961,786

3,803,157

126,507 40,000

166,507

1,961,786

567,431 1,107,433

3,636,650

3,803,157

Ul

Housing Authority of St Landry, Louisiana

Management's Discussion and Analysis (MD&A) June 30,2010

CONDENSED FINANCIAL STATEMENTS (Continued)

The net assets of these funds decreased by $20,264, or by 1 %, from those of fiscal year 2009, as explained below. In the narrative that follows, the detail factors causing this change are discussed:

Condensed Statement of Revenues, Expenses, and Changes In Fund Net Assets (Excluding Interfund Transfers) Fiscal Year Ended June 30,2010

2010 2009

OPERATING REVENUES Tenant rental revenue Other tenant revenue

Total operating revenues

OPERATING EXPENSES Federal Housing Assistance Payments (HAP) to landlords Administi-ation Maintenance and repairs Depreciation General Utilities Extraordinary repairs Tenant services

Total operating expenses

(Losses) from operations

NON-OPERATmG REVENUES Federal grants for operations Fraud Recovery Otiier non-tenant revenue Interest income

Total Non-Operating Revenues

NON-OPERATING EXPENSES

Income (loss) after non-operating revenues

OTHER CHANGES IN NET ASSETS Federal grants for capital expenditures

NET INCREASE (DECREASE) IN NET ASSETS

NET ASSETS, beginning of fiscal year

NET ASSETS, end of fiscal year

$ 233,609 13,383

246,992

2.213,932

452.830 220,026 193,045 164,010 49,704 1.450 292

3,295,289

(3,048.297)

2.626.492 14,644 1.299 5,514

2,647,949

(400,348)

380,084

(20,264)

3,636,650

3,616,386

$ 229,934 4.062

233,996

1,970,871 475,737 224,573 169,094

159,506 53,412

1,405

3.054,598

(2,820.602)

2,922,662

14,655 10,114

2,947,431

126,829

271,392

398,221

3,238,429

3,636,650

IV

Housing Autiiority of St Landry, Louisiana Management's Discussion and Analysis (MD&A)

June 30, 2010

EXPLANATIONS OF FINANCIAL ANALYSIS

Compared witii the prior fiscal year, total operating and non-operating revenues decreased $177,795, or by 5%, from a combination of larger offsetting factors. Reasons for most of this change are listed below in order of impact from greatest to least;

• Federal revenues fi'om HUD for operations decreased by $296,170, or by 10% from that of the prior fiscal year. The determination of operating grants is based in part upon operations perfomiance of prior years. This amount fiuctuates fi-om year-to-year because of the complexities of the funding formula HUD employs. Generally, this fonriula calculates an allowable expense level adjusted for Inflation, occupancy, and other factors, and then uses tills final result as a basis for determining the grant amount. The amount of rent subsidy received fi-om HUD depends upon an eligibility scale of each tenant There was a decrease in the number of eligible tenants receiving subsidies, so Housing Assistance Grants decreased accordingly, lowering the overall total.

• Federal Capital Funds from HUD increased by $108,692, or by 40% from that of the prior fiscal year. The Housing Authority was still in the process of completing projects funded from grants by HUD for fiscal years 2008 through 2009, and submitted a new grant during fiscal year 2011.

• Total tenant revenue increased by $12,996, or by 6% from that of tiie prior fiscal year, and because the amount of rent each tenant pays is based on a sliding scale of their personal income. Some tenants' personal incomes increased, so rent revenue from these tenants increased accordingly, raising the overall total. Finally, other tenant revenues (such as fees collected from tenants for late payment of rent, damages to their units, and other assessments) increased by $9,321.

• Total otiier non-operating revenue decreased by $13,356, or by 91% fi-om that of tiie prior fiscal year. There was no Other income collected this year in the Low Rent Program.

• Interest income decreased by $4,601, or by 55% fi-om that of tiie prior fiscal year, because the Authority spent available cash mostly on capital assets instead of temporary investments.

Compared with the prior fiscal year, total operating and non-operating expenses increased $240,691, or by 8%, but this also was made up of a combination of offsetting factors. Again, reasons for most of this change are listed below in order of impact from greatest to least:

• Housing Assistance Payments to landlords increased by $243,061, or by 12% from that of the prior fiscal year, because there was an Increase in the number of tenants qualifying for subsidy during the year. Consequently, revenues from HUD for these subsidies decreased by $320,849.

• Depreciation expense increased by $23,951, or by 14% from that of the prior fiscal year, because there was an increase in capital assets by $1,361,233.

• Administi^tive Expenses decreased by $22,907, or by 5% fi-om tiiat of the prior fiscal year, due to a combination of offsetting factors: Administrative staff salaries decreased by $2,699, or by 1 % and related employee benefit conti-ibutions decreased by $9,154, or by 8%; therefore, total staff salaries and benefit costs decreased by 3%. In addition, audit fees increased by $200, or by 5%, accounting fees increased by $1,095, or by 8%; thus, total outside professional fees increased by 8%. Finally, staff travel reimbursements increased by $65,228, staff training costs increased by $258, or by 46%, but sundry expenses decreased by $69,978, or by 92%; therefore, other staff administi^tive expense decreased by 5%.

V

Housing Authority of St Landry, Louisiana Management's Discussion and Analysis (MD&A)

June 30,2010

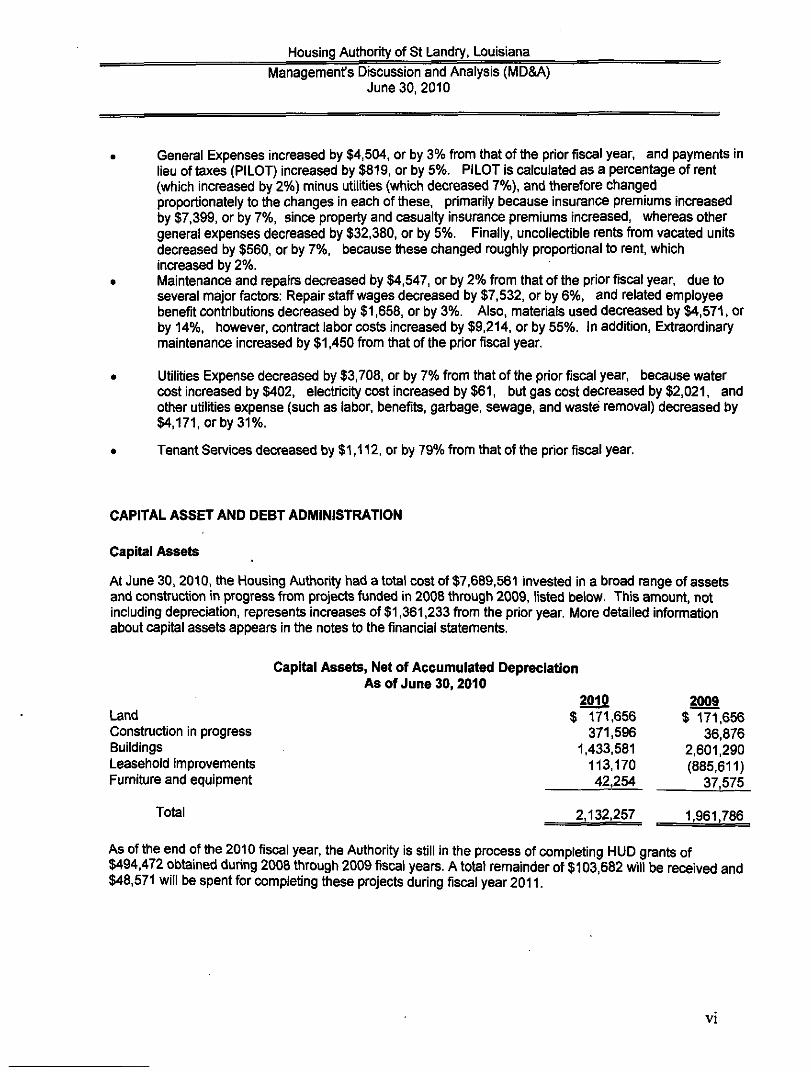

General Expenses increased by $4,504, or by 3% from tiiat of the prior fiscal year, and payments in lieu of taxes (PILOT) Increased by $819, or by 5%. PILOT is calculated as a percentage of rent (which increased by 2%) minus utilities (which decreased 7%), and therefore changed proportionately to the changes in each of these, primarily because insurance premiums increased by $7,399, or by 7%, since property and casualty insurance premiums increased, whereas otiier general expenses decreased by $32,380. or by 5%. Finally, uncollectible rents from vacated units decreased by $560, or by 7%, because these changed roughly proportional to rent, which increased by 2%. Maintenance and repairs decreased by $4,547, or by 2% from that of the prior fiscal year, due to several major factors: Repair staff wages decreased by $7,532, or by 6%, and related employee benefit contributions decreased by $1,658, or by 3%. Also, materials used decreased by $4,571, or by 14%, however, contract labor costs increased by $9,214, or by 55%. In addition. Extraordinary maintenance increased by $1,450 from that of the prior fiscal year

Utilities Expense decreased by $3,708, or by 7% from that of the prior fiscal year, because water cost Increased by $402. electricity cost increased by $61, butgascostdecreased by $2,021, and otiier utilities expense (such as labor, benefits, garisage, sewage, and waste removal) decreased by K171,orby31%.

Tenant Services decreased by $1,112, or by 79% from tiiat of the prior fiscal year.

CAPITAL ASSET AND DEBT ADMINISTRATION

Capital Assets

At June 30> 2010, tiie Housing Authority had a total cost of $7,689,561 invested In a bnsad range of assets and consti-uction in progress from projects fijnded in 2008 through 2009, listed below. This amount, not including depreciation, represents increases of $1,361,233 fi-om tiie prior year. More detailed information about capital assets appears in the notes to the financial statements.

Capital Assets, Net of Accumulated Depreciation Asof June 30,2010

2010 2009 Land $ 171,656 $ 171,656 Constmction in progress 371,596 36,876 Buildings 1,433,581 2,6o{290 Leasehold improvements 113,170 (885,611) Furniture and equipment 42,254 37,575

Total 2,132,257 1,961,786

As of tiie end of the 2010 fiscal year, tiie Authority Is still in the process of completing HUD grants of $494,472 obtained during 2008 through 2009 fiscal years. A total remainder of $103,682 will be received and $48,571 will be spent for completing these projects during fiscal year 2011.

VI

Housing Authority of St Landry, Louisiana Management's Discussion and Analysis (MD&A)

June 30,2010

Debt

The Housing Authority owes $0, long term notes payable to RRD that were used to finance buildings and equipment listed above costing $0 (or $0 net of depreciation.) As of June 30,2010, tiie Housing Authority owed $0 on these notes, of which $0 Is due cun-entiy for fiscal year 2011.

Non-current liabilities also include accrued annual vacation and sick leave due to employees. The Housing Authority has not Incurred any mortgages, leases, or bond indentures for financing capital assets or operations.

ECONOMIC FACTORS AND NEXT YEAR'S BUDGETS AND RATES

The Housing Autiiority is primarily dependent upon HUD for the funding of operations; therefore, the Housing Authority is affocted more by Federal budget than by local economic conditions. The capital budgets for the 2011 fiscal year have already been submitted to HUD for approval and no major changes are expected.

The Capital fund programs are multiple year budgets and have remained relatively stable. Capital Funds are used for the modernization of public housing properties including administrative fees involved in the modernization.

CONTACTING THE HOUSING AUTHORITY'S FINANCIAL MANAGEMENT

Our financial report is designed to provide our citizens, investors, and creditors with a general overview of the Housing Authority's finances, and to show the Housing Authority's accountability for the money it receives. If you have questions about this report, or wish to request additional financial information, contact Donna Piti e, at Public Housing Authority of St Landry, Louisiana; P.O Box 276; St Landry, LA 70589.

vn

RICHARD C . U R B A N

CERTIFIED PUBUC ACCOUNTANT

M E M B E R : OFFICE:

AMERICAN t N S T m j T H OF 1112 HEATHER DRfVE

CERTIFIED P U B U C ACCOUNTANTS OPELOUSAS. LOUISIANA 7 0 5 7 0

SOCIETY OF LOUISIANA PHONE Q3T> 942-2154

CERTIFIED P U B U C ACCOUNTANTS FAX C337> 948-3813

INDEPENDENT AUDITOR'S REPORT

To the Board of Commissioners Housing Authority of St. Landry Parish Washington, Louisiana

We have audited the accompanying basic financial statements ofthe Housing Authority of St. Landry Parish, Louisiana as of and for the year ended Jime 30,2010, as listed in the table of contents. These financial statements are the responsibility ofthe Housing Authority's management. Our responsibility is to express opinions on these financial statements based on our audit.

We conducted our audit in accordance vrith au<Hting standards generally accepted m the United States of America and the standards applicable to financial audits contained m Govemment Auditing Standards, issued by the Comptroller General ofthe United States. Those standards require that we plan and perfonn the audit to o b t ^ reasonable assurance about whether the financial statements are fi:ee of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinion.

In our opinion, the financial statements referred to above present fairly, in all material respects, tiie financial position ofthe Housing Authority of St. Landry Parish, Lomsiana, as of June 30,2010, and the respective changes in financial position and cash floors, thereof for the year then ended, in conformity with accounting principles generally accepted in the United States of America.

In accordance with Govemment Auditing Standards, we have also issued our report dated November 8,2010, on our consideration ofthe Housing Authority of St. Landry Parish, Louisiana's intemal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and otiier matters. Tbe purpose of that report is to describe the scope of our testing of intemal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on the intemal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Govemment Auditing Standards and should be considered in assessing the results of our audit.

1

The management's discussion and analysis on pages i - vii, is not a required part ofthe basic financial statements but are supplementary information required by accounting principles generally accepted in the United States of America, We have applied certain limited procedures, which consisted principally of inquiries of management regarding the methods of measurement and presentation ofthe required supplementary information. However, we did not audit the information and express no opinion on it.

Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise the Housing Authority of St. Landry Parish, Louisiana's basic financial statements. The accompanying schedule of expenditures of federal awards is presented for purposes of additional analysis as required by U.S. Office of Management and Budget Circular A-133, Audits of States, LocaJ Govemments. and Non-Profit Organizations, and is not a required part ofthe basic financial statements. The accompanying financial infonnation listed as supplemental information in the table of contents is presented for additional analysis and is not a required part ofthe financial statements ofthe Housing Authority of St. Landry Parish, Louisiana. Such infonnation has been subjected to the auditing procedures applied in the audit ofthe basic financial statements and, in our opinion, is fairly stated, in all material respects, in relation to the basic financial statements taken as a whole.

The accompanying Financial Data Schedules required by HUD are presented for purposes of additional analysis and are not a required part ofthe basic financial statements. Such information has been subjected to the auditing procedures applied in the audit ofthe basic financial statements and, in our opinion, is fairly stated in all material respects in relation to the basic financial statements taken as a whole.

MJdL Richard C. Urban, CPA

Opelousas, Louisiana November 8,2010

FINANCIAL STATEMENTS

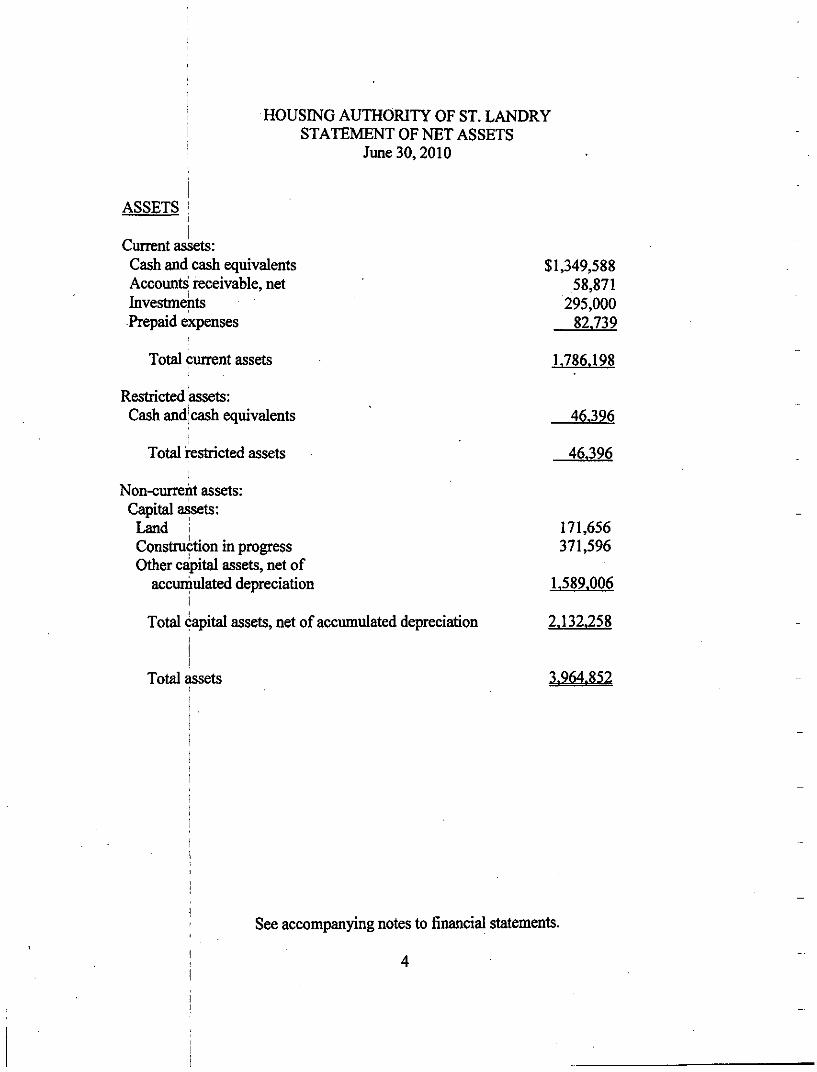

HOUSING AUTHORITY OF ST. LANDRY STATEMENT OF NET ASSETS

June 30,2010

ASSETS

Cunent assets: Cash and cash equivalents $1,349,588 Accounts receivable, net 58,871 Investments 295,000 Prepaid expenses 82.739

Total current assets 1,786.198

Restricted assets: Cash andjcash equivalents 46.396

Total restricted assets 46.396

Non-current assets: Capital assets:

Land j 171,656 Constmction in progress 371,596 Other capital assets, net of

accumulated depreciation 1,589,006 i

Total capital assets, net of accumulated depreciation 2,132.258 j

!

Total assets 3,964,852

See accompanying notes to financial statements.

4

LIABILITIES

Liabilities: Cunent liabilities:

Accounts payable $ 42,357 Payable to other govemments 18,877 Compensated absences payable 13,855 Deferred revenue 684 Otiier current liability 224.313

Total current liabilities 300.086

Liabilities payable fi'om restricted assets: Tenant security deposits 13.130

Total liabilities payable fi'om restricted assets 13.130

Non-current liabilities:

Compensated absences payable 35.250

Total non-cunent liabilities 35.250

Total liabilities 348.466

NET ASSETS Invested in capital assets, net of related debt 2,132,258 Restricted for Housing Choice Vouchers 32,708 Unrestricted 1,451.420

Total net assets 3.616.386

Total liabilities and net assets 3.964.852

HOUSING AUTHORITY OF ST. LANDRY STATEMENT OF REVENUES, EXPENSES AND

CHANGES IN NET ASSETS Year Ended June 30,2010

OPERATING REVENUES Annual contributions - Housing Assistance Payments $ 1,671,715 HUD administrative fee - Section 8 423,745 HUD administrative fee - CFP 28,941 Public housing operating subsidy 502,092 Tenant rental revenue 233,609 Otiier income 29.325

Total operating revenues 2.889.427

OPERATING EXPENSES Housing Assistance Payments 2,213,932 General and administrative 616,837 Repairs and maintenance 221,477 Utilities 49,704 Tenant services 292 Depreciation and amortization 193.046

Total operating expenses 3.295.288

Operating income (loss) ( 405,861)

NON-OPERATING REVENUE (EXPENSED Investment income

Total non-operating revenue (expense)

Income (loss) before other revenues, expenses, gains, losses

andn^sfers ( 401,034)

Capital contributions (grants) 380.770

Increase (decrease) in net assets ( 20,264)

Prior year adjustment for depreciation ( 24,951)

Net assets, beginning of year 3.661.601

Net assets, end of year

4,827

4.827

See accompanying notes to financial statements,

6

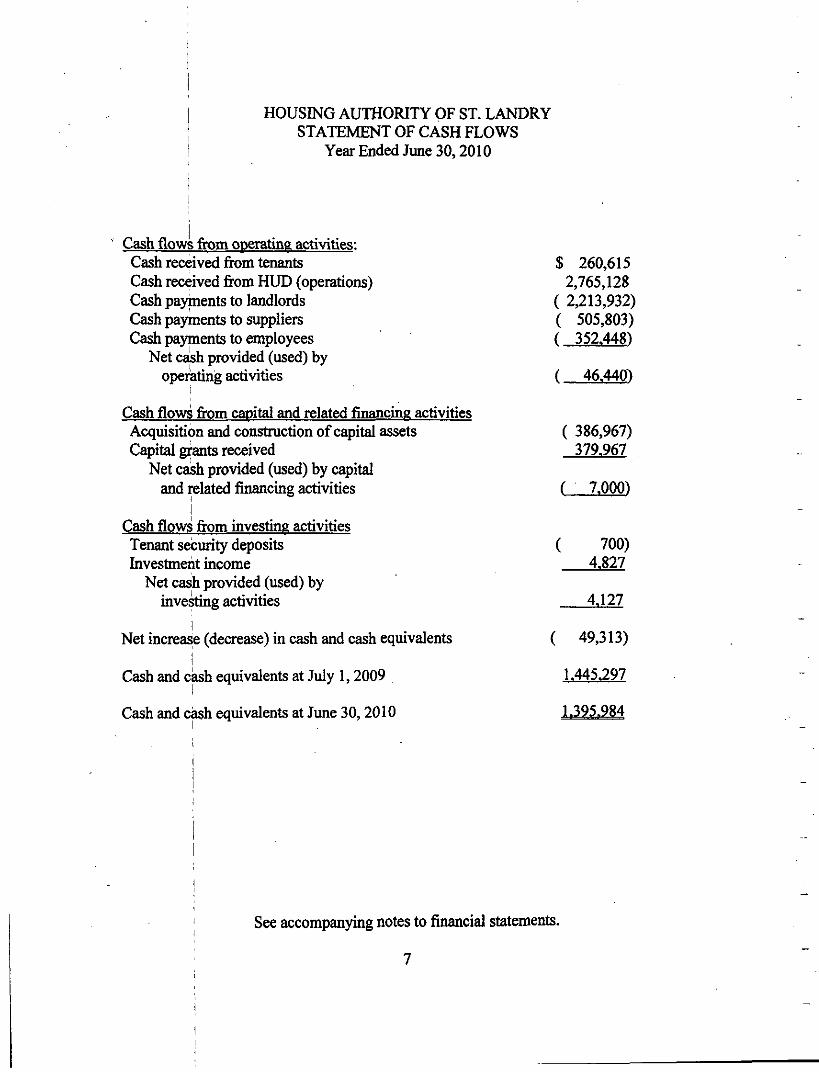

HOUSING AUTHORITY OF ST. LANDRY STATEMENT OF CASH FLOWS

Year Ended June 30,2010

Cash flows from operating activities: Cash received fiom tenants $ 260,615 Cash received fi-om HUD (operations) 2,765,128 Cash payments to landlords ( 2,213,932) Cash payments to suppliers ( 505,803) Cash payments to employees ( 352,448)

Net cash provided (used) by operating activities

Cash flows fiom capital and related financing activities Acquisition and constmction of capital assets Capital grants received

Net cash provided (used) by capital and related financing activities

Cash flows fi:om investing activities Tenant security deposits Investment income

Net cash provided (used) by investing activities

1 Net increase (decrease) in cash and cash equivalents

1 Cash and cash equivalents at July 1,2009

Cash and cash equivalents at June 30,2010

( 46,440)

( 386,967) 379,967

( 7,000)

( 700) 4,827

AMI

( 49,313)

1.445.297

1.395.984

See accompanying notes to financial statements.

7

Reconciliation of operating mcome Closs) to net cash provided (used) bv ODcrating activities:

Operating mcome (loss) Adjustments to reconcile operating

income (loss) to net cash provided (used) by operating activities: Depreciation Changes in assets and liabilities: (Increase) decrease in accounts

receivable (Increase) decrease in prepaid

expenses and other assets Increase (decrease) in accounts

payable Increase (decrease) in payable to other govemments Increase (decrease) in other liabiUty Increase (decrease) in compensated

absences payable Increase (decrease) in tenant security deposits Increase (decrease) in defened

revenue Total adjustments

Net cash provided (used) by operating activities

$( 405,861]

193,046

( 53,575)

( 8,556)

26,745 819

207,683

( 6,061) ( 700)

20 359.421

(=Jg,440)

HOUSING AUTHORITY OF ST. LANDRY PARISH Washington, Louisiana

NOTES TO FINANCIAL STATEMENTS June 30,2010

INTRODUCTION

The Housing Authority of St. Landry Parish (authority) was created by Louisiana Revised Statute (LSA-R.S.) 40.391 to engage in tiie acquisition, development, and administration of a low rent housing program to provide safe, sanitary, and affordable housing to the residents of St. Landry Parish, Louisiana,

The authority is administered by a six-member board appointed by the parish. Members ofthe board serve five-year staggered terms.

Under tiie United States Housing Act of 1937, as amended, tiie U.S. Department of Housing and Urban Development (HUD) has direct responsibility for administering low rent housing programs in the United States. Accordingly, HUD has entered into an annual contributions contract with the authority for the purpose of assisting the authority in financial the acquisition, constmction, and leasmg of housing units and to make annual contributions (subsidies) to tiie authority for the purpose of maintaining this low rent character.

NOTE 1 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Basis of Presentation

The accompanying financial statements ofthe authority have been prepared in confonnity with accounting principles generally accepted in the United States of America (GAAP) as applied to govemmental imits. The Govemmental Accoimting Standards Board (GASB) is the accepted standard setting body for establishing govemmental accounting and financial reporting principles.

Financial Reporting Entity

GASB Codification Section 2100 defines criteria for determining the govemmental reporting entity and component units that should be included within the reporting entity. Because the authority is legally separate and fiscally independent, the authority is a separate govemmental reporting entity.

The authority is a related organization ofthe Parish of St. Landry, since the parish appoints a voting majority ofthe authority's goveming board. The parish is not financially accountable for tiie authority as it cannot impose its will on the authority

NOTES TO FINANCIAL STATEMENTS (CONTINUED)

and there is no potential for the authority to provide financial benefit to, or impose fmancial burdens on, the parish. Accordingly, the authority is not a component unit of the financial reporting entity ofthe parish of St, Landry, Louisiana.

GASB Codification Section 2100 defines criteria for determining which component units should be considered part ofthe authority for financial reporting purposes. The basic criterion for including a potential component unit within the reporting entity is financial accountability. The GASB has set forth criteria to be considered in determining financial accountability. These criteria include:

1. Appointing a voting majority of an organization's goveming body, and a. The ability of the authority to impose its will on that organization and/or b. The potential for the organization to provide specific financial benefits to, or

impose specific fmancial burdens on the authority. 2. Organizations for which the autiiority does not appoint a voting majority, but are

fiscally dependent on the authority. 3. Organizations for which the reporting entity fmancial statements would be

misleading if data ofthe organization is not included because ofthe nature or significance ofthe relationship.

Based on the previous criteria, the authority has determmed that the following component unit should be considered as part ofthe authority reporting entity:

St. Landry Public Housing Corporation is a legally separate entity. The members of the authority's board of commissioners also serve as the board of directors ofthe entity. The authority has the ability to impose its vwll on the entity.

The Corporation was formed for the purpose of facilitating the development and financing of an affordable housing facility within the parish limits of St. Landry Parish. The Corporation is a partner in the developer partnership. However, since the investment limited partner owns 99+% interest in the partnership, the Corporation takes the position that eventual control ofthe partnership rests with the investment limited partnership.

The partnership has entered into loan agreements and other financing arrangements that may have incurred contingent liabilities on behalf of the Corporation, but not any that would obligate the PHA. No contingencies have been reported in the PHA financial statements.

The material Corporation financial activities are included in the PHA financials through blended presentation.

Fund Accounting

10

NOTES TO FINANCIAL STATEMENTS (CONTINUED)

The authority uses funds to report on its financial position and the results of its operations. Fund accounting is designed to demonstrate legal compliance and to aid financial management by segregating transactions relating to certain govemment fimctions or activities. A fund is a separate accounting entity with a self-balancing set of accounts.

The authority accounts for its business-type activities as proprietary funds.

Proprietary fimds are used to account for activities similar to those found in the private sector, where the determination of net income is necessary or useful to sound financiai administration. Operating income reported in proprietary fimd financial statements includes revenues and expenses related to the primary, continuing operations ofthe fund. Principal operating revenues for proprietary fimds are charges to tenants for rents or other services as well as operating subsidies received from HUD. Principal operating expenses are the costs of providing these services and include administrative expenses and depreciation of capital assets. Other revenues and expenses are classified as non-operating in the financial statements.

Basis of Accounting

The accmal basis of accountmg is utilized by proprietary fimds. Under this method, revenues are recorded when eamed and expenses are recorded at the time liabilities are incurred.

Budgets

The authority prepares its financial statements in accordance mih generally accepted accounting principles. In accordance with the provisions of its annual contributions contract with the Department of Housing and Urban Development, the authority prepares an aimual budget. This budget is prepared in conformity with the accounting practices prescribed by HUD, which is a comprehensive basis of accounting other than generally accepted accoimting principles. Because ofthe differences in accounting practices, no budgetary information is provided in this report.

The following are the budgetary practices prescribed by HUD and used by the authority:

The Executive Director prepares a proposed budget and submits same to the Board of Commissioners no later than thirty days prior to the beginning of each fiscal year. Following discussion and acceptance of tiie budget by tiie Board, it is sent to HUD for approval. Upon approval by HUD, the budget is formally adopted. Any budgetary amendments require the approval ofthe Executive Director and the Board of Commissioners. Any budgetaiy appropriations lapse at the end of each fiscal year.

11

NOTES TO FINANCIAL STATEMENTS (CONTINUED)

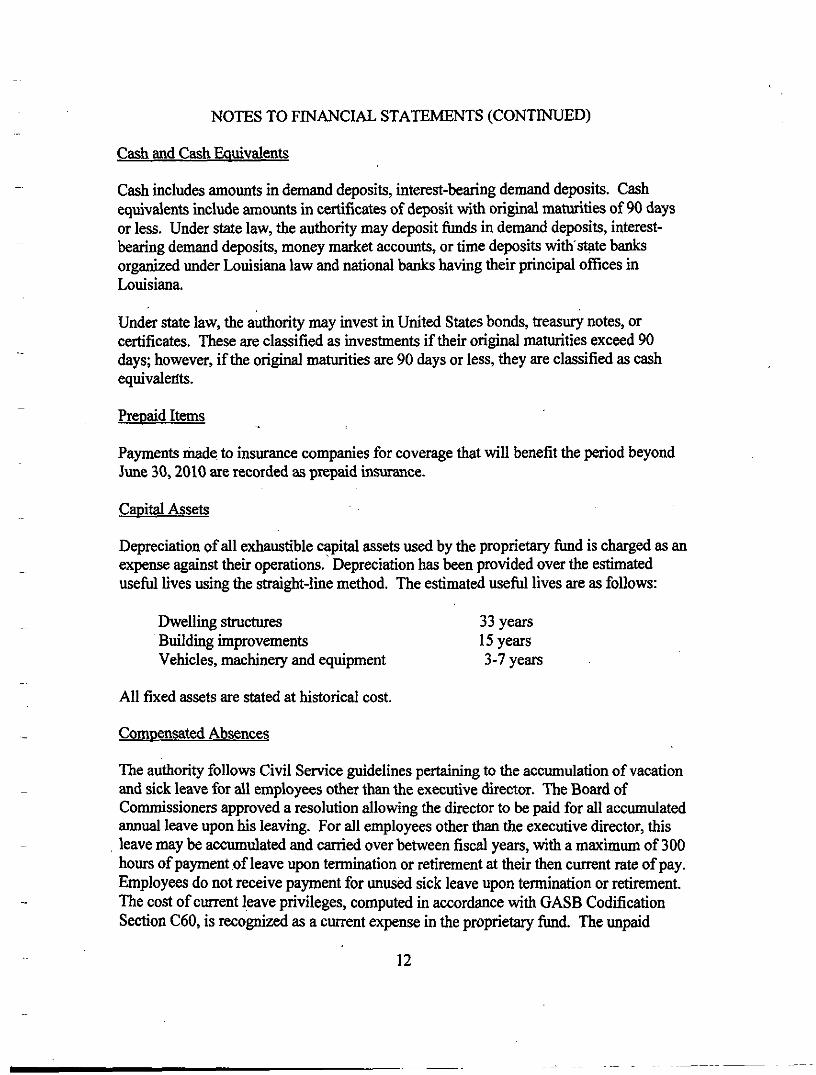

Cash and Cash Equivalents

Cash includes amounts in demand deposits, interest-bearing demand deposits. Cash equivalents include amounts in certificates of deposit with original maturities of 90 days or less. Under state law, the authority may deposit funds in demand deposits, interest-bearing demand deposits, money market accounts, or time deposits with'state banks organized under Louisiana law and national banks having their principal offices in Louisiana.

Under state law, the authority may invest in United States bonds, treasury notes, or certificates. These are classified as investments if their original maturities exceed 90 days; however, if the original maturities are 90 days or less, they are classified as cash equivalents.

Prepaid Items

Payments made to insurance companies for coverage that will benefit the period beyond June 30,2010 are recorded as prepaid insurance.

Capital Assets

Depreciation of all exhaustible capital assets used by the proprietary fimd is charged as an expense against their operations. Depreciation has been provided over the estimated usefiil lives using the straight-line method. The estimated useful lives are as follows:

Dwelling stmctures 33 years Building improvements 15 years Vehicles, machineiy and equipment 3-7 years

All fixed assets are stated at historical cost.

Compensated Absences

The authority follows Civil Service guidelines pertaining to the accumulation of vacation and sick leave for all employees other than the executive director. The Board of Commissioners approved a resolution allowing the director to be paid for all accumulated annual leave upon his leaving. For all employees other than the executive director, this leave may be accumulated and carried over between fiscal years, v^tii a maximum of 300 hours of payment of leave upon termination or retirement at their then current rate of pay. Employees do not receive payment for unused sick leave upon termination or retirement. The cost of current leave privileges, computed in accordance with GASB Codification Section C60, is recognized as a current expense in the proprietary fimd. The unpaid

12

NOTES TO FINANCIAL STATEMENTS (CONTINUED)

portion of leave privileges is recorded as a current liability in the proprietary fund.

NOTE 2 - CASH AND CASH EQUIVALENTS AND INVESTMENTS

At June 30,2010, the authority has cash and cash equivalents, and investments totaling $1,740,297 as follows:

Interest-bearing demand deposit $1,395,376 Certificates of deposit 295,000 Otiier . m

Total 1,690,984

These deposits are stated at cost, which approximates market. Under state law, these deposits must be secured by federal deposit insurance or the pledge of securities owned by the fiscal agent. The market value ofthe pledged securities plus the federal deposit insurance must at all times equal the amount on deposit vwth the fiscal agent. These securities are held in the name of the pledging fiscal agent bank in a holding or custodial bank that is mutually acceptable to both parties. At June 30,2010, the autiiority has $1,690,934 in deposits (bank balances), categorized below to reflect the amoimt of risk assumed by the authority.

GASB Category 1 $488,350 GASB Category 2 GASB Category 3 1.202,584

1,690,934

Even though the pledged securities are considered imcollateralized (Category 3) under the provisions of GASB Statement 3, Louisiana Revised Statue 39:1229 imposes a statutory requirement on the custodial bank to advertise and sell the pledged securities within 10 days of being notified by the authority that the fiscal agent has failed to pay deposited fimds upon demand.

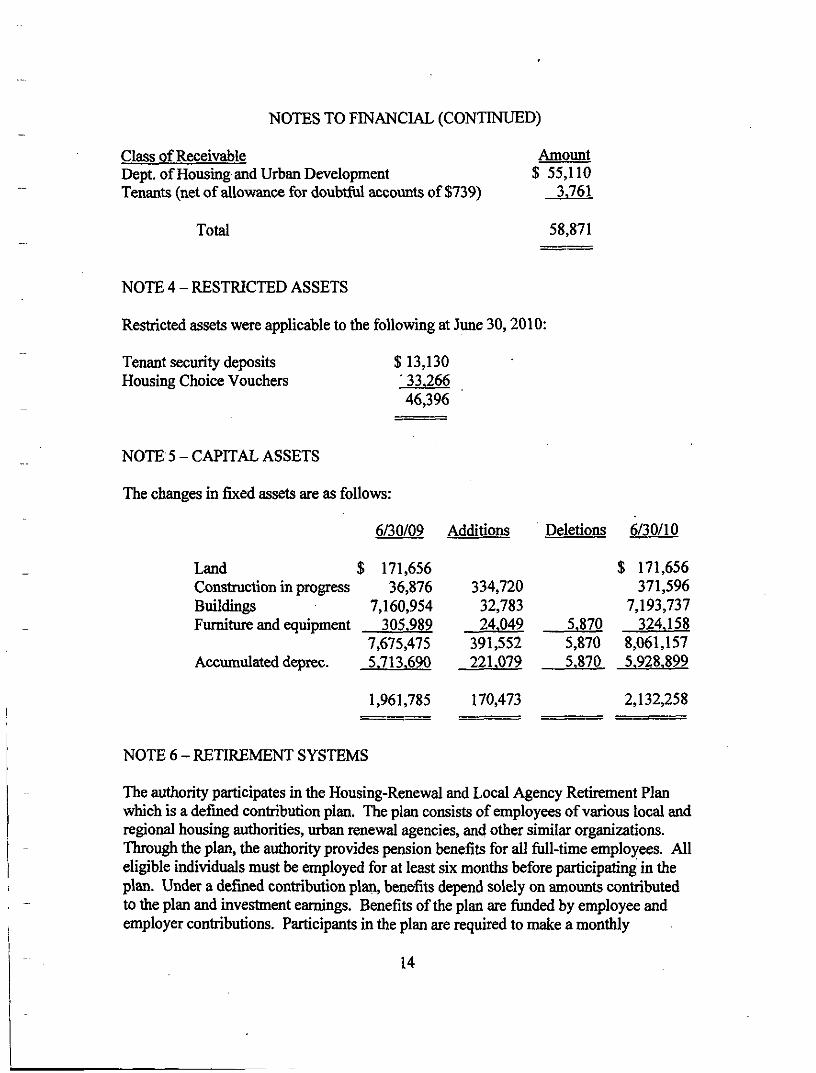

NOTE 3 - RECEIVABLES

The receivables of $58,871 at June 30,2010, are as follows:

13

NOTES TO FINANCIAL (CONTINUED)

Class of Receivable Amount Dept of Housing and Urban Development $ 55,110 Tenants (net of allowance for doubtfiil accounts of $739) 3,761

Total 58,871

NOTE 4 - RESTRICTED ASSETS

Restricted assets were applicable to the following at June 30,2010:

Tenant security deposits $13,130 Housing Choice Vouchers ' 33.266

46,396

NOTE 5 - CAPITAL ASSETS

The changes in fixed assets are as follows:

6/30/09 Additions Deletions 6/30/10

Land $ 171,656 $ 171,656 Construction in progress 36,876 334,720 371,596 Buildings 7,160,954 32,783 7,193,737 Fumiture and equipment 305.989 24.049 5.870 324.158

7,675,475 391,552 5,870 8,061,157 Accumulated deprec. 5.713.690 221.079 5.870 5.928.899

1,961,785 170,473 2,132,258

NOTE 6 - RETIREMENT SYSTEMS

The authority participates in the Housing-Renewal and Local Agency Retirement Plan which is a defined contribution plan. The plan consists of employees of various local and regional housing authorities, urban renewal agencies, and other similar organizations. Through the plan, the authority provides pension benefits for all fiill-time employees. All eligible individuals must be employed for at least six months before participating in the plan. Under a defined contribution plan, benefits depend solely on amounts contributed to the plan and investment eamings. Benefits ofthe plan are fimded by employee and employer contributions. Participants in the plan are required to make a monthly

14

NOTES TO FINANCIAL STATEMENTS (CONTINUED)

contribution of 5.5 percent of their basic (excludes overtime) compensation. The authority makes a monthly contribution equal to 8.5 percent of each participant's basic compensation. The employer contributions and eamings allocated to each participant's account are fiilly vested after one year of continuous service. Normal retirement date shall be the first day ofthe month foUovwng the employee's sixty-fifth birthday or after ten years of participation in the plan. The authority's total payroll for the fiscal year ended June 30,2010, was $352,448. The authority's contributions were made based on the total covered payroll of $352,448. The authority and the covered employees made the required contributions for the year ended June 30,2010. Employee contributions totaled $19,380 while the authority's contributions totaled $29,949 for the year ended June 30, 2010.

NOTE 7 - COMPENSATED ABSENCES

At June 30,2010, employees ofthe authority have accumulated and vested $49,105 of employee leave benefits, which is presented as both current and non-current liabilities of the proprietary fund in the balance sheet. The current portion is $13,855 while the non-current portion is $35,250. Except as discussed above, the liability has been computed in accordance with GASB Codification Section C60.

NOTE 8 - RISK MANAGEMENT

The authority is exposed to all common perils associated vnih the ownership and rental of real estate properties. To minimize loss occurrence and to transfer risk, the authority carries various commercial insurance policies including property, casualty, employee dishonesty, public official's liability, business auto and other miscellaneous policies. These policies are reviewed for adequacy by management annually. There has been no significant reduction in insurance coverages from those in the prior year. Also, there have been no significant claims that have exceeded commercial insurance coverages in the current and prior year.

NOTE 9 - FEDERAL COMPLL\NCE CONTINGENCIES

The authority is subject to possible examinations by federal regulators who determine compliance with terms, conditions, laws and regulations goveming grants given to the entity in the current and prior years. These examinations may result in required refimds by the entity to federal grantors and/or program beneficiaries. No questioned or disallowed costs were noted for inclusion in our report.

NOTE 10 - COMPENSATION OF BOARD MEMBERS

15

NOTES TO FINANCIAL STATEMENTS (CONTINUED)

The following is a list of board members and their per diem received for tiie year ended June 30,2010:

Larris Soileau $ 50 James Soileau 250 Joel Stelly 450 Sharon Reed Everett 450 Phillip Young 500 Larry Janise 500 Willie Haynes, III 500

2,700

The housing authority has discontinued paying its board members a per diem for monthly and special meetings effective May 1,2010.

16

OTHER REPORTS AND SCHEDULES

HOUSING AUTHORITY OF ST. LANDRY PARJSH SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS

Year Ended June 30,2010

Federal Grantor/ Program Title

U.S. Dept. of Housing and Urban Development

CFDA No. Federal Award Program

Received Expenditures

Direct Programs: Capital Fund Programs 14.872 Low-income HAP 14.850 Capital Fund Stimulus Grant 14.239 Housing Choice Vouchers 14.871

Total U.S. Dept. of Housing And Urban Development

Total federal assistance

Federal funds on hand, beginning of year Federal funds received Federal fimds disbursed

Federal fimds on hand, end of year

176,235 502,092 232,790

2.095,460

3.006,577

3,006,577

$ -0-3,006,577 (3.006,577)

-0-

176,235 502,092 232,790

2.095,460

3,006,577

3,006,577

The above schedule is prepared under the accrual basis of accounting.

18

RICHARD C . U R B A N

CERTrFlED PUBUC ACCOUNTANT

M E M B E R :

AMERrCAN INSTITUTE OF

CERTIRED P U B U C ACCOUrsTrANTS

SOCIETY OF LOUIStANA

CERTIFIED PUBLIC ACCOUNTANTS

O F R C E :

1112 HEATHER DRIVE

OPELOUSAS. LOUISIANA 7 0 5 7 0

PHONE Q37) 942-2154

FAX (337) 948-3813

Board of Commissioners Housing Authority of St. Landry Parish Washington, Louisiana

REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS BASED ON AN AUDIT OF

FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS

We have audited the financial statements ofthe business-type activities ofthe Housing Authority of St. Landry Parish, Louisiana, as of and for the year ended June 30,2010, which collectively comprise the Housing authority's basic financial statements and have issued our report thereon dated November 8,2010. We conducted our audit in accordance virith auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Govemment Auditing Standards, issued by the Comptroller General ofthe United States.

Intemal Control Over Financial Reporting

In planning and performing our audit, we considered the Housing Authority's intemal control over financial reporting as a basis for designing in our auditing procedures for the purpose of expressing our opinion on the financial statements, but not for the purpose of expressing an opinion on the effectiveness ofthe Housing Authority's intemal control over financial reporting. Accordingly, we do not express an opinion on the effectiveness ofthe Housing Authority's intemal control over financial reporting.

A deficiency in intemal control exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned fimctions, to prevent, or detect and conect misstatements on a timely basis. A material weakness is a deficiency, or combination of deficiencies, in intemal control, such that there is a reasonable possibility that a material misstatement ofthe entity's financial statements will not be prevented, or detected and corrected on a timely basis.

Our consideration of internal control over financial reporting was for the lunited purpose described in the first paragraph of tiiis section and was not designed to identify ail deficiencies m intemal control over financial reporting tiiat nught be deficiencies, significant deficiencies or material weaknesses. We did not identify any deficiencies in

19

intemal control over financial reporting that we consider to be material weaknesses, as defined above.

Compliance and Other Matters

As part of obtaining reasonable assurance about whether the Housing Authority of St. Landry Parish, Louisiana's financial statements are free of material misstatement, we performed tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements, noncompliance with which could have a direct and material effect on the determination of financial statement amounts. However, providing an opinion on compliance with those provisions was not an objective of our audit, and accordingly, we do not express such an opinion. The results of our tests disclosed no instances of noncompliance or other matters that are required to be reported under Government Auditing Standards.

This report is intended for the information ofthe Board of Commissioners, management, the Department of Housing and Urban Development, and the Legislative Auditor of the State of Louisiana, and is not intended to be and should not be used by anyone other than these specified parties. Under Louisiana Revised Statute 24:513, this report is distributed by the Legislative Auditor as a public document. •

Richard C. Urban, CPA

Opelousas, Louisiana November 8,2010

20

RICHARD C . U R B A N

CERTIFIED PUBLIC ACCOUNTANT

MEMBER: OFFICE:

AMERICAN INSTITUTE OF 111E HEATHER DBIN/E

CERTIFIED PUBUC ACCOUNTANTS OPELOUSAS. LOUISIANA 70570 SOCIETY OF UDUISIANA PHONE C337) 942-2154

CERTIRED PUBUC ACCOUNTANTS FAX (337> 948-3813

Board of Commissioners Housing Authority of St. Landry Parish Washington, Lomsiana

REPORT ON COMPLIANCE WITH REQUIREMENTS THAT COULD HAVE A DIRECT AND MATERIAL EFFECT ON EACH MAJOR PROGRAM AND ON

INTERNAL CONTROL OVER COMPLIANCE IN ACCORDANCE WITH OMB CIRCULAR A-133

Compliance

We have audited the compliance ofthe Housii^ Authority of St. Landry Parish, Louisiana, with the types of compliance requirements described in the U.S. Office of Management and Budget COMB) Circular A-133 Compliance Supplement that could have a direct and material effect on each of its major federal programs for the year ended June 30,2010. The Housing Authority's major federal programs are identified in the sunamary of auditor's results section ofthe accompanying schedule of findings and questioned costs. Compliance with the requirements of laws, regulations, contracts and grants applicable to each of its major federal programs is the responsibility ofthe Housing Authority's management. Our responsibility is to express an opinion on the Housing Authority's compliance based on our audit.

We conducted our audit of compliance in accordance with auditing standards generally accepted in tiie United States of America; the standanis applicable to financial audits contained in Govemment Auditing Standards, issued by tiie Comptroller General ofthe United States, and OMB Circular A-133. Those standards and OMB Circular A-133 require tiiat we plan and perfonn the audit to obtain reasonable assurance about whether noncompliance with tiie types of compliance requirements refened to above that could have a direct and material effect on a major f e d ^ program occmred. An audit includes examining, on a test basis, evidence about the Housing Authority's compliance with those reqmrements and performing such other procedures as we considered necessary in the circumstances. We believe that our audit provides a reasonable basis for our opinion. Our audit does not provide a legal detennination on tiie Housing Autiiority of St. Landry Parish, Louisiana's compliance witii tiiose requirements.

hi our opinion, the Housing Autiiority of St. Landiy Parish, Louisiana complied, in all material respects, with tiie compliance requirements referred to above tiiat could have a du^t and material effect on each of its major federal programs for tiie year ended June 30,2010.

21

Intemal Control Over Compliance

The management ofthe Housing Authority is responsible for establishing and maintaining effective intemal control over compliance with requirements of laws, regulations, contracts and grants applicable to federal programs. In planning and performing our audit, we considered the Housing Authority's intemal control over compliance with the requirements that could have a direct and material effect on a major federal program in order to determine the auditing procedures for the purpose of expressing our opinion on compliance and to test and report on internal control over compliance in accordance with OMB Circular A-133, but not for the purpose of expressing an opinion on the effectiveness of intemal control over compliance. Accordingly, we do not express an opinion on the effectiveness ofthe Housing Authority's intemal control over compliance.

A deficiency in intemal control over compliance exists when the design or operation of a control over compliance does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and conect, noncompliance with a type of compliance requirement of a federal program on a timely basis. A material weakness in intemal control over compliance is a deficiency, or combination of deficiencies, in intemal control over compliance such that there is a reasonable possibility that material noncompliance with a type of compliance requirement of a federal program will not be prevented, or detected and corrected, on a timely basis.

Our consideration of intemal control over compliance was for the limited purpose described in the first paragraph of this section and was not designed to identify all deficiencies in intemal control over compliance that might be deficiencies, significant deficiencies, or material weaknesses. We did not identify any deficiencies in intemal control over compliance that we consider to be material weaknesses, as defined above.

This report is intended for the infonnation ofthe Board of Commissioners, management, the Department of Housing and Urban Development, and the Legislative Auditor ofthe State of Louisiana, and is not intended to be used by anyone other than these specified parties. Under Louisiana Revised Stamte 24:513, tius report is distributed by the Legislative Auditor as a public document. ^ -

Richard C. Urban, CPA

Opelousas, Louisiana November 8,2010

22

HOUSING AUTHORITY OF ST. LANDRY PARISH STATUS OF PRIOR AUDIT FINDINGS

The previous audit contained no findings or questioned costs.

23

14.850 14.852 14.239

$ 502,092 2,095,460 232,790

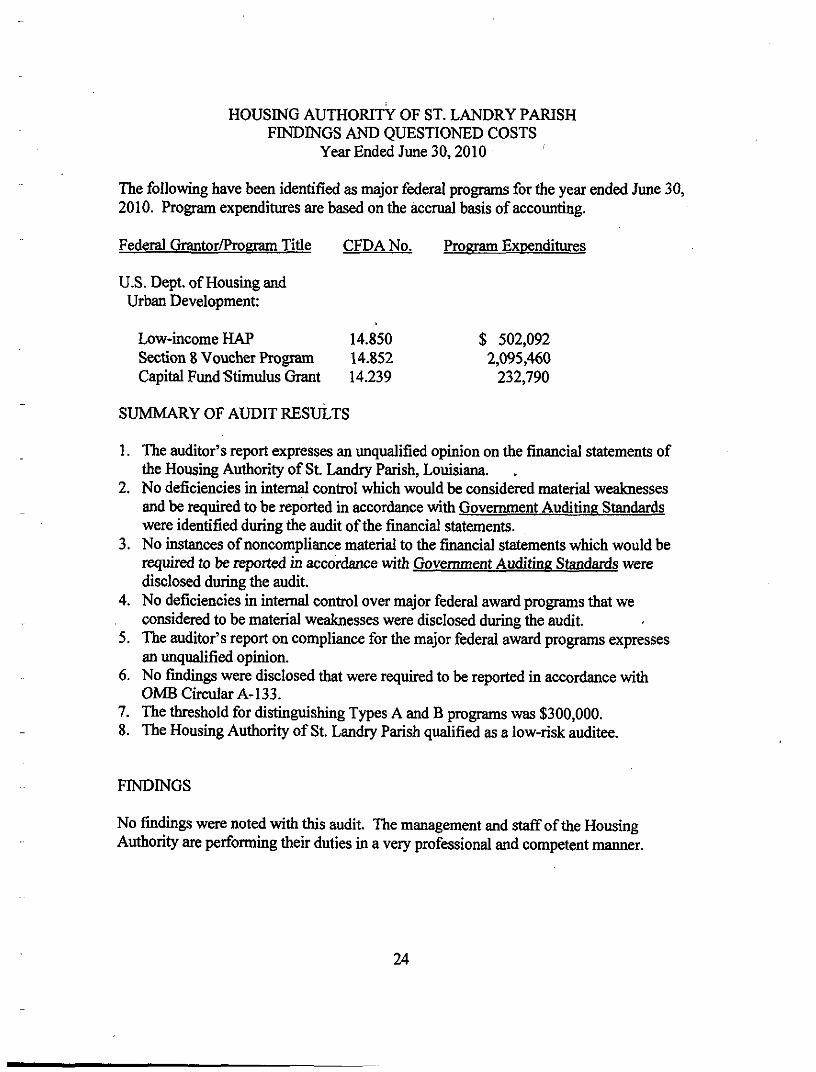

HOUSING AUTHORITY OF ST. LANDRY PARISH FINDINGS AND QUESTIONED COSTS

Year Ended June 30,2010

The following have been identified as major federal programs for the year ended June 30, 2010. Program expenditures are based on the accrual basis of accounting.

Federal Grantor/Program Title CFDA No. Program Expenditures

U.S. Dept. of Housing and Urban Development:

Low-mcome HAP Section 8 Voucher Program Capital Fund Stimulus Grant

SUMMARY OF AUDIT RESULTS

1. The auditor's report expresses an unqualified opinion on the financial statements of the Housing Authority of St. Landry Parish, Louisiana.

2. No deficiencies in intemal control which would be considered material weaknesses and be required to be reported in accordance with Govemment AucHting Standards were identified during the audit ofthe financial statements.

3. No instances of noncompliance material to the fiinancial statements which would be required to be reported in accordance with Govemment Auditing Standards were disclosed during the audit.

4. No deficiencies in intemal control over major federal award programs that we considered to be material weaknesses were disclosed during the audit.

5. The auditor's report on compliance for the major federal award programs expresses an unqualified opinion.

6. No findings were disclosed that were required to be reported in accordance with OMB Circular A-133.

7. The threshold for distinguishing Types A and B programs was $300,000. 8. The Housing Authority of St. Landry Parish qualified as a low-risk auditee.

FINDINGS

No fmdings were noted with this audit. The management and staff of the Housing Authority are performing theu' duties in a very professional and competent manner.

24

HOUSING AUTHORITY OF ST. LANDRY PARISH STATEMENT AND CERTIFICATION OF ACTUAL MODERNIZATION COSTS

At June 30,2010 :

2005 PHASE LA 48P067501-05

FUNDS APPROVED FUNDS EXPENDED

EXCESS OF FUNDS APPROVED

FUNDS ADANCED FUNDS EXPENDED

EXCESS OF FUNDS ADVANCED

$ 225,581 225.581

-0- -

$ 225,581 225.581

-0-

1. The distribution of costs by project as shown on the Final Statement of Modernization Cost submitted to HUD for approval is in agreement with the PHA's records.

2. All modernization costs have been paid and all related liabilities have been discharged through payment.

25

4 ^

O cr cn o 2. A 5"

O (A

M

TJ 3

3

cn

Q .

w

s

I

I.

w

a>

> c 3 so

a a

ro o

CT <D 0)

OD

-n 3 c a.

8 >3

Ol ro

o i a

CO o n

s i' O c

i 3

CD o < (D

3 3 (D 3

ro

> o 8

i (D

s I" CT O I

•D X >

o o

I 0)

U l

O to m

u

o

• 0 (D < 3 3

o

0) CT

ro O m w rr I

7 1 0) (0

S

o a.

m 3 a D

? £E. o 3 (D 3

« 3-

c 3

3 I %

n § s s 4A

CO

12 S S s

4A

3 S •in

4» .A U

g (D

s

Ui c CT 3 OT S2. o 3

c 3 u C o.

I .: tn W 3

a 9 a tt B 3 O o 0> 3 " 9

CO

c 3 3 »

I o c 3 *

s > CO I

z o H u z

3 "

o •3 .

n = h

CD

"D Q) 11. 3 -O

5 12 Q) 3 a

2!

-< Q)

m 3 O.

o Ol

o

O O)

26

w

u > § c 3 ff

1 CD V CO o

13 (U 0)

D c

o

o

o> M

>

§ c 3 ff u u

0

A I I

CO

o O Q)

"5

cn - J

ro u

CO

-* OD to 3

? CD

1

s

s

_ ; » . CO

o H a

a ff

^ o t n cn b) en

o cn cn

'2 t n

.. S r l

1

c

1 ff

M

_

CO IO

_& -4 O)

3

<

3 CD 3 ff

o 5'

i a c 3 en

s

«

_fc • N l • b .

o

1 a ff

S

S

_ x

-^ 0 9

O 3 3 ff 71 CD

s S' CT (D z O 3

o c 3

s

s

^ •^ ro Z o

1

1 CO S o

0) CQ CD W

s < CT t

? 3

o

1 1

D 0) (fl D c (D

s

o

. j t

-4 _ x

Z o ff Cfl

5" D) 3 CO

D) 3 a

o

u (Q CD Cfl 73 (D

8 i' CT CD

z o 3 1

o c

i 3

s

^ b

o> O

r l a O

ff

1 ff z a a o J2 3 c tD ff Q . D (D

• a

5 o

a o" 3

w

IO

_ro

u

To

_». cn 00

?

CO

a

3

o

4» O

_». o> •^ O o 3 Cfl

a o 3

3' D

i 3 (fl Cfl

t n

O)

«»

_». o> a> >

c 3 c a (D Q .

O ID •o

5 o

a 5' 3

A

K OS

cn

IO

» OD t o

. . A

a> cn IT (D 01 t f l (D CT O

a. 3 •o

1 3 CD 3 ff

t n

' o

cn

4A

W cn cn

— 1 .

a> *. •n c 3

m n c •D 3 o a

0)

3 (D

5 I

> Q .

3 3

1 3

o

5 O

o

_ k

0 ) CO

• n

c 3

m c

• D '

3 3

fl"

to

3 (D

3 1

1 3 *

( Q

(0

44 ..A

JO

5

M

SI

_ i .

cn ro 01 c a. 3'

( Q CO

«*

ca M

^

$

^ 0) • J >

r* Q} 3

V * - A - J

- J

. . A

2! o r l

1 O c 3 3

ff

«»

'%l

u u

_ k

• b

cn ^

s ff X (D O .

CB CD

•

g

s

•Jk

^ ^ ff 1 3

3 3 o c CD -n 3 3

o

IS o •"-4

s

_

CO

1

i

CO c CT 3 0) Cfl

5' 3 ^ TD

C 3 (D C

g. ff

1 t

CO

T j

5= 0) - 1

m 3 O .

O O )

c5 Q

, g

X o c CO

CQ > m c

1 ? a 5 2. 00 CO ? » X (D § Z TJ s g » S o ^ 1 - a « 5 ?2 i ^

5 o en

27

CO en o

i o

? O c 3

8 (S CL D CD

O 3 0) 3 Q.

o 1 3 m CD

CT

CO cn c»

i m cn 0)

CT

CO

s E CD Q .

3 T3 CD 3 Cfl a ff a. > CT CO CD 3

8 z o 3

o c

3 3

CD

CT

CO

o

5*

o c 3

CT 5 : (D (»

00

o c

CO

cn

CD CT c m CT 1 CO

O

a 3' o 3 Q

0) (Q a

ts cn lo l o s s

s n CO

«

s ts t n To

8 8 S

5

3

s s s s

C/) c CT 3 CO CO ?r 3

• < ' • a CD

C

r a ff P->

S m 3

a <D

DD » tt 3 8 0)

(S (D

w c 3 3 B) <3

1 CO X z —1

o ^

5

T o c CO 3 '

CQ

>

O 3.

a =? (D

"0 3 .

3 "

a CO

sr 3 U .

CO

s 01 - t m 3 a. o

IO o

o o>

28

o o

CD

s s CO

a 3 a.

n c

CO

a

Icn icn CO

- t

I ff

c

Z

a ?

IO

io c 3 3 (0 a

c 3 Q. (D (fl

^ " CD

a. -n c 3 Q . DD

m 0) 3

O cn cn

's cn

Its a

cn cn

io C 3

3

i a.

S" (fl

I (D

a. -n c 3 CL a S" 3

8

CO '

io 11

c 3 Q. OD » (D 3

I (0

ff

O 01

ff

a ff

a a 5" a ff Q. o o CT

is 1^

(D

is

5 52

n w'

s if 01

m 3 Q .

O

CO

IO

o

o

29

I CO Ico ro o o

g .

3 ' (O n

o o

3

I f CO

m 0) 3 . CD [ f l

O o o o

73

I CD

- • I ro o o o

1 (fl 3 CD 3 3

8 3 to

CO

a

5>

c;)

en o o O

I (D 3 C CD

O

o -n 3 & X CD

I •3

CO o o I D 3 8 CD Q . CO

3 g co'

2 . 5* 3

Cfl a ff X

a o. CO

u (D

10 O O

o &

CD 5" ff 3 a 3

8 3 CD

3 CD 1

• C 3 3 a 3 .

&

O 00 o o O CD

- Q i 3 3 CD a o 3

I

2 o o

I n o (D

f CD 3 c : (D

O

o 11

3 3

' J o CO

o Q O

-n o a -n CD (D

o ro o

cn CD

a 3

l<9 (D

3 (D a n (D CD

0) 3

(S CD

•NI O o>

o

g o X c o 13 X > CD

I o 3 3 ff

o cn o o

2,

a 3 ta 3_

73 S CD 3 C CD

3 fll 3

73 (D 3

^ (D < CD 3 C CD

CO c CT 3 (fl M O 3 ^ •D CD

Is Is u s s iS

s S5

t

c 3 fil c Q.

ff & ?; CO CO

n co' s •< CD 0}

- m 3 a. 0 en c5 p ro 0

m 3

•?

a CD

1 3 e CD

3 a m X

13 0 3 0 tn c 3 3 u C3

$ > go X z 3 0 z '5

X 0 c 0) 3

CQ

> C 3" 0 3 .

a 5

"0 Ql 3 . CO 3 -

a CO

r-3 a. ^ „...s

f 0 Oi

"-

30

CO CO 0 0 o o o S (D

c

CD CO

a 3 CO CD

8

S

CO CO

^ o o m 3 •o CD (D

O D CD 3

1 s 3

CT

O 3

(fl c s 5* (0

8

8

CO CO O ) o o CO

CD

v»

ID

1 OB

CD CO cn o o

CT o - 1

8

8

CO CO

.^ o o n c a

o

o

CO CO CO o o o to (0

«•

s

8 o

CO CO ro o o m ff

o'

«» p <o

p to - 4

CD CO ^ b

o o

1 ff

«» t n OD

3

Ul O -4 to

(O ro cn o o

5* ff S* 3 01 3

CO CD

3 8 CO

s s

IO to ro

CO ro .u g 3" 3 01

a CO (D

8 (A I

o CT (D

IO

M

to

CO IO Ol o o m 3 •a

(D (D

OD CD 3 a a; O o 3

CT C a o 3 CO

^ 3 01 3

CO

a> 3 8 (0

8

4» O

CO I O ro 8 71

o'

1 ff

O

CO I O

o o

3 u a CO (D

3 8 CO

CO a a 3 . CD (0

O

8

CO ro o o o

£ 01 3

s CD

3 (D 3

•n o CD

o

CD

_ O o o

§ (D

3 3

( Q

3 3 (fl'

< cS

t cn fO oa ro to

"s to

<D

•* CO

g g CT CD

M o>

O

V * cn CO

o

CD «>• 0 0

o

o 8 ff a.

(D

3 -Q>

a

o

8

CD . 1 ^

OD O o

1 a

4«

Vi J).

i

CD _k ^ O o

5" CQ

m rn X

•o CD' 3 (0 CD

8

CO

CD

^ cn o o O m o o

5? • D (D 3 CO CD CO

V * 00

o

•o

s - J

CO ^J»

cn o o m 3 •a

1 CD OD CD 3

%

8 3

CT C

5' 3 CO 1

I 3. 5" to '

1 CD

M

oa

o 00

CD

^ • f r .

O o

< CD

3 : CO 3

Q 0) 3 a.

01

5-

3 CQ

M IO

4n

13

CD ^ k

CO

-^ o OD O

o

CD •o 3 '

CQ

CD

8

o

CO - A

CO

o o

01 3 01

CO CD

3 CD

a "n

8

8

^

CO

1

CO c CT 3

CD

c 3 01 c a Q. ni

a a

I 3 C (D » 3 a !? •O a> 3 (0 » 0) c 3 3 0)

<3 - n m'

s 0)

m 3 Q .

O

CO

g M o

X o c CO

3 (Q

O

it €0 ^

Z TJ

g §. O & ? o

m 3 a •2

o a> •si

31

^ a> o o 00 01 a. a.

1 1

CD

o

8

% en g DD

Q . CD

s 1

o

01 CQ CD

o

8

CD

2 g OD U Q L

Q . CD

a 5" 3 fll 3

71 (D 3 ff

^ l o t o fO

"8 IO

CD o> CO o o 13

3 CD 3

ff 5 ' r-(D C

a 5* X

CO

CA

09

4A

CO

cn IO

o O o 3 n o

a . > CT (A CD 3

8 CO

4 * t o

t n

n cn O)

S ro § O 5

3

f 3

(0

i . ^

».

X

^ v &

o o H o

s; 5' CO

c 3 3

8 13

3 d c 3

w

t n

t o

4A

O

t n

t o

CO

o> i u o

i CD

5" t o

e: 3

8

v t

fs

CO

s

CO

cn ^ k

CO o

1 S-3 a> 3 CO

8 3 CD

O 3

«*

W

CB

CO

cn - A

IO o n 01 CT

f 3 (A C 3 3

8

i f *

t n

M

t n

CO O ) ^ k

.^ o 13 3 •a CD

3 CO

c 3 3

8

t

t "2

CO

cn o o o - 1

1 1 3

1 CD

CO (D 3

8 CO

8

o

CD cn cn o o m 3 •D O

OD CD 3 CD

o o

a 3*. 1 3 CO 1

1 3

1 a 1 CO o 3 o* 0 CO

8

8

CO

cn CO o o 13

i (D ( 0 (D 3 8 CO

i

8

8

t o cn IO o o n 5 ff a i" ( 0 (D

3. 8 0 )

O CT " 1

o O 1 a o o (0

ff

8

o

CO

cn M ^

o o 13

1 CO CD

3

8 CO

CT O -

8

8

g CD O O

H

1 01 5" ff 3 m

8

o IO - 4

o "o !3

CO

cn o o m 3 • a

1 o OD to 3 (D

O o 3 3 . C

5"

1

O 3. 3 01

«3

m

1 3 01 3

8

t

s

t t n

( D • ^

CO o o o a 3 01 •3

a> 3 ff 3 01 3

8 01

EX

o o

g. O 3 (0 O o

t

V *

ro

00

n o t o tB

S IO o o o 3. 3 01 •5

01

3 01 3

8 01 3 Q.

o Q

o 3 (fl 1

01 ff 3 . 01 CO 01 3

a O 3 CD

S CO o o

n CO o o

CO •tx - V O o O

a 3 01 •3 01 3 ' ff 3 U 3

8 m 3 a

3 §•'

r -

- 1

Ol

t f l t o t n

CO CO

o o o - 1 o

c

2

1

t

2

g

S

1

CO c CT d (fl (0 O 3 - i ^ to

c 3

r Q.

R >

CO CO

n

o 01

-< CD 01 —1

m 3 a. o o> CO o to o

m A

-e a to

9

s 3 C m 3

a

S" 3

(0 c 3 d 0) •3

5 > CO X

z o u z

• •

! >

T o c: CO 3

(Q

> C

o 3 . 'S-- 4 t

3 -CD

13

3 . ( 0 3 " o ^ CO

l -Q) 3 Q.

' ^ .—.,.

>> O <n -si ^ ^

32

o o

O • D CD

i 3

(O H

3 3

% (0

3 o n 3 .

3 0) O o < 3 3 to 3

O O

O • a CD

3 (Q

o T3 CD

5' EQ

H

3 3

I

CD O o o o

•o (D

Q Cfl

o

C 3

a m CD 3 (» (D

o o < (D

3 3 to 3

s; -n c 3 a. CO

CO

cn o o

£•

I O c 01

Q o < (D 3 3 (D 3

ff

CO CD •>! CO cn o I > H D O

CT

f

D

3 (D 3

ff

C 3 a CO

to

"i to

CO

to tn

OS OD

8

8 2

8

8

8

8

CO c CT d CO CO O 3 H »< IS c

Q.

ff

? CO

Tl

8 -< (D 01 ^ m 1 Q.

O cn ^ ^ o

m 3

•e !§ a (D

ii? 1 3 C to a 3 a

•o o 3 (A CD

e 3 d ^

S > CO X z Q H U z

T o c CO 3

CO

> c 3 -

o 3 .

o =K

5 CD "D Q) 3 . (0 3 -

a

3

n. •2 ^ ^ i ^

t o CJ>

' " '

33

I O

o z c 3 CT CD

(D 01 CO Q Q .

to O

c 3

r I CD

- J O

3 3'

f J CD

o o O CT 01 3

CO CD CA

O ( O

o O CT 01 3

CQ O CO

5'

I 3

C O " O CD O

a

I i CD

3 3 0 3 O 3

% ff

01 CT

o 3 -01 3

(Q (0 01

O CT OP 3

CQ CD CO

o § O CT 01 3

EQ CD CA

5' O O

3 3

O

u 3 . O

S" 3 . O CL

O CO

o OD

3

3. 3

CO

m c

o

(D Q. > CT

8 3 O to m a 01 3

3 [ Q

3

ff

3

c I CD 3

ff

C

>?

s" 3

3 01 3 O.

O o

o 3 Q

o CD CT 13 3 . 3 Q.

•o

a 01

i 3 ff

O o o o

I (A CO

O % o Q 3

5

5*

I CD 3 C CD

§ (D

c 3 a. CD

i

o

i 3 (U 3 O 5' ta CO

o

c CA CD CA

O

o 2 3

3 CT CD

I to 3

13

CD a Dl 3 Q .

o

Dl 3 (0

ff 3

I to 3

1 3

3 CQ 3 3 a 3 a. •V to'

a

o o so lo 3" ? 13

?

O 01 (0

CT

m

o fll (A CT

3

CD

O o OD o CO • o

(D

» ff 3 (O

01

o o cn o

3 8 (D CL (0

I CD

O

i O • a CD

CQ

-1 5 3

CD

3 3 o o o 3

•T3 O 3 CD 3

c 3

( 0

8

1 A CO

O l

o>

i

8 & g 8 8

8 fe

8 8 8

CT 3 CO (fl o 3 H •< •o CD

C

c a.

? eo CO

n

8 -< to V - I

m 3 Q.

O cn ro o IO o

m d •? € a CD

3

1 3 C » 0) 3 a m X

•a 3 (0 o 0> c 3 d 01 5

§ - > CO X

z -J u _z >

T O

c CO 3

CQ

> C 3 " O -n

a 3 -CD

•n 3 .

3 -

a (ti 1 - ^

r-Q) 3 n, •2 .—., •> o

• " " '

34

CO CO o

s "D 01

8 3 a X o c 3

(Q

-n fll

n c 3 cx Cfl

8

o

CO cn _ ! •

O

O T l U

a CD

2 ro (D

3 3 13 01

d CD 3 ff

8

8

—« O) cn o

I oi

a c a! 13 c a 01 Cfl CD

8

o

^ k

o> en o

JT CD O CT O Q.

3 T3

$ d CD 3

(0

c CT

(0

8

8

~ cn • u o n c d 5

m JD

3 CD

a

3 3

a 3 < CD

u c 01 (A CD (fl

8

8

-^ —Ik

m CO o

? 3 3 C6

m •O

c

a 1

CD

3 CQ

H c

a CT (A CD (A

^

i

.^ m IO o CD

c 3

CQ

13 C

a CT 0 1

CD (A

to c» (B '(0 03

M

to o>

cn —1

o

^ 3

? 4 m CO CD (A

8

• A

ro - s |

o

^ % i o 01 (A CT

8 tn

cn

S - 1 t f l

•A cn

1

1

ro c CT ^ $ n 3 H *< • a o c

Q.

CD

>; - X

CO

n CO

s -< CD CD

m 3 a. o o> to o IO o

m #« •

•?

1 3 C (D 0) 3 a ff

3 ta o 0) e 3 d 01 J

5 > CO X

z c;) u z '5

T 0 c cn s > h ZT

^

=S.

=f CD TJ Q) 3 . tn 3-

a 2 r fl) 3 a ^

. M .

^

^ - ^

35