homeready mortgage - meadowbrook financial … criteria are subject to the formal terms and...

TRANSCRIPT

This summary is intended for reference only. All criteria are subject to the formal terms and conditions of the Fannie Mae Selling Guide and Servicing Guide. In the event of any conflict with this document, the Selling Guide and/or Servicing Guide will govern. © 2016 Fannie Mae. Trademarks of Fannie Mae. March 21, 2016 Page 1 of 5

HomeReady® Mortgage

Designed for creditworthy, low- to moderate-income borrowers, with expanded eligibility for financing homes in designated low-income, minority, and disaster-impacted communities. HomeReady lets you lend with confidence while expanding access to credit and supporting sustainable homeownership. Key features:

Simplicity and certainty for lenders

Streamlined pricing and execution

Product features designed to align with today’s buyer demographics and support sustainable homeownership

1-Unit 2- to 4-Unit

Elig

ibili

ty

Loan Purpose Purchase or Limited Cash-out Refinance (LCOR)

Occupancy and

Property Type

1-unit principal residence, including eligible condos, co-ops,

PUDs, and manufactured housing

2- to 4-unit principal residence (no condos, co-ops, or

manufactured housing)

Manufactured

Housing

In accordance with standard MH guidelines (Desktop

Underwriter® [DU®] required; max 95% LTV/CLTV; FRMs or

7/1 and 10/1 ARMs only; no buydowns)

Not applicable

HomeStyle®

Renovation

In accordance with standard HomeStyle Renovation guidelines

(special lender approval; max LTVs/CLTVs per HomeStyle Renovation guidelines)

Borrower Income

Limits

No income limits in low-income census tracts

100% of area median income (AMI) in high-minority census tracts or designated disaster areas

80% of AMI in all other census tracts

Minimum Borrower

Contribution (own

funds)

$0

$0 for LTV/CLTV/HCLTV of 80% or less;

3% for LTV /CLTV/HCLTV > 80%

3% required if sweat equity is being used

Acceptable Sources

of Funds for Down

Payment and Closing

Costs

Gifts, grants, and Community Seconds®. Cash-on-hand for 1-unit properties only.

Any eligible loan may have more than one Community Seconds (i.e., third lien) up to the maximum 105% CLTV

(see Community Seconds fact sheet). Sweat equity is acceptable in accordance with the Selling Guide.

This summary is intended for reference only. All criteria are subject to the formal terms and conditions of the Fannie Mae Selling Guide and Servicing Guide. In the event of any conflict with this document, the Selling Guide and/or Servicing Guide will govern.

© 2016 Fannie Mae. Trademarks of Fannie Mae. March 21, 2016 Page 2 of 5

1-Unit 2- to 4-Unit E

ligib

ility

(co

ntin

ue

d)

Product 10-, 15-, 20-, or 30-year fixed-rate mortgages (FRMs)

5/1 (2/2/5 and 2/2/6 caps only), 7/1, and 10/1 adjustable-rate mortgages (ARMs)

Maximum LTV/CLTV

and Subordinate

Financing

CLTV up to 105% with eligible Community Seconds (Refer to Eligibility Matrix for details)

Other subordinate financing per the Selling Guide

Purchase:

DU Only – 97% (FRM)

DU and manual underwriting to 95% (FRM); 90% (ARM)

LCOR: DU and manual underwriting: 95% FRM; 90% (ARM)

Purchase or LCOR

2-unit: 85% FRM, 75% ARM

3- to 4-unit: 75% FRM only

Ownership of Other

Property Occupant borrower(s) may not have an ownership interest in any other residential property at the time of closing.

Non-Occupant

Borrowers

Non-occupant borrowers permitted to maximum 95% LTV in DU; 90% LTV manual with max 43% DTI for occupying borrower.

Income considered as part of qualifying income and subject to income limits. No limitation on ownership of other property for

non-occupant borrower.

Interest Rate

Buydowns 3-2-1 and 2-1 buydown structures permitted

Mortgage Insurance

(MI) Coverage and

Financed MI

25% MI coverage for LTVs 90.01−97%

Standard MI coverage for LTVs of 90% or less

MI may be financed up to the maximum LTV for the transaction, including the financed MI

(Minimum MI Coverage Option may be used with additional LLPA; the HomeReady LLPA waiver or cap does not apply).

Un

de

rwriting

Desktop

Underwriter® (DU)

(Available in DU:

target Dec 2015)

Based on the census tract and borrower income, DU will notify users when a loan casefile appears to be eligible for

HomeReady but the lender has not underwritten the loan casefile as HomeReady. Resubmit the loan casefile as a

HomeReady loan to obtain the appropriate HomeReady messaging. New Additional Data screen field will allow entering

census tract information if DU is unable to geocode the property address.

DU recommendation of Approve/Eligible required. DU will determine qualifying ratios and reserves.

Eligible in DU if at least one borrower has traditional credit and contributes more than 50% of qualifying income.

Manual Underwriting (Limited waiver of

representations and

warranties does not

apply. LTVs >95% not

Use manual underwriting if (1) the DU recommendation is other than Approve/Eligible, or

(2) there is not at least one borrower with a traditional credit history.

Benchmark qualifying ratio follows Fannie Mae standard Selling Guide (Section B3-6-02) for manual underwriting.

Representative minimum credit scores for manual underwriting (Minimum could be higher for certain reserves and debt-to-income ratios; see the Eligibility Matrix)

620 or higher, per the Eligibility Matrix 640 or higher, per the Eligibility Matrix

This summary is intended for reference only. All criteria are subject to the formal terms and conditions of the Fannie Mae Selling Guide and Servicing Guide. In the event of any conflict with this document, the Selling Guide and/or Servicing Guide will govern.

© 2016 Fannie Mae. Trademarks of Fannie Mae. March 21, 2016 Page 3 of 5

1-Unit 2- to 4-Unit U

nde

rwriting

(co

ntin

ue

d)

eligible for manual

underwriting.) Reserves for manual underwriting

Minimum none or up to 6 months, per the Eligibility Matrix

(based on credit score, DTI ratio, and FRM or ARM)

Minimum none or up to 12 months, per the Eligibility Matrix

(based on credit score, DTI ratio, and FRM or ARM)

Manual Underwriting,

Exceptions to

Minimum Credit

Score Requirements

Borrowers with nontraditional credit are eligible. In addition,

up to 30% of qualifying income may come from a borrower

for which no traditional or nontraditional credit profile can

be established.

If the borrower has a credit score below the minimum

required as a result of an insufficient traditional credit

history (“thin files”) as documented by reason codes on the

credit report, the lender may supplement the thin file with

an acceptable nontraditional credit profile. SFC 818 must

be used to identify loans with supplemented thin files (for

manually underwritten loans only).

If a borrower has a credit score below the minimum

required, but has sufficient traditional credit sources listed

on the credit report, the lender may not establish a

nontraditional credit profile to supplement the borrower’s

traditional credit history.

If the borrower’s credit history was heavily influenced by

credit deficiencies that were the result of documented

extenuating circumstances, the minimum credit score

requirement must be met (per the Eligibility Matrix), or the

credit score must be no less than 620.

Not eligible

Other Income

Boarder income (relatives or non-relatives): Up to 30% of

qualifying income; documentation for at least 9 of the most

recent 12 months (averaged over 12 months) and

documentation of shared residency for the past 12 months.

Not eligible

Accessory dwelling units: Rental income may be considered

in qualifying the borrower per rental income guidelines.

Rental income may be used as qualifying income per rental

income guidelines.

Non-Borrower

Household Income

Permitted as a compensating factor in DU only to allow a debt-to-income (DTI) ratio >45%, up to 50% (non-borrower income

is not considered qualifying income and is not applied to income limits). The following additional requirements apply:

Non-borrower income must total at least 30% of the total monthly qualifying income being used by the borrower(s). (Note:

Income from more than one non-borrower household member may be considered.)

Non-borrower household members may be relatives or non-relatives.

This summary is intended for reference only. All criteria are subject to the formal terms and conditions of the Fannie Mae Selling Guide and Servicing Guide. In the event of any conflict with this document, the Selling Guide and/or Servicing Guide will govern.

© 2016 Fannie Mae. Trademarks of Fannie Mae. March 21, 2016 Page 4 of 5

1-Unit 2- to 4-Unit

Non-borrower household income must be documented in accordance with standard Selling Guide policy based on the

income type.

Non-borrowers must sign a statement of intent to reside with the borrower for a minimum of 12 months. (See optional

Fannie Mae Form 1019.)

The income must be reflected in DU as an Other Income type of “Non-Borrower Household Income” (new income type will

be added with DU implementation). This income will not be included as qualifying income, and would not impact the DTI

ratio used in the risk assessment or displayed on the DU Underwriting Findings report.

Ho

me

ow

ners

hip

Ed

ucatio

n

Prepurchase

Homeownership

Education

Homeownership education required prior to note date for at least one borrower on all transactions (purchase and LCOR).

Must be provided through Framework, an online program approved by Fannie Mae.

$75 fee paid by the borrower to Framework for a simple, accessible online program with email support 7 days a week.

Lenders may choose to provide a credit against closing costs in accordance with Selling Guide section B3-4.1-02 (Lender

Incentives for Borrowers).

Homeownership education certificate must be retained in the mortgage file.

Although one-on-one counseling is optional for HomeReady, Framework will offer borrowers a referral to a HUD-approved

counseling agency for additional assistance. Borrowers also have the option to consult a counselor of their choice.

Post-Purchase

Support

To support sustainability, borrowers will have access to post-purchase homeownership support for the life of the loan through

Framework's homeownership advisor service.

Special Borrower

Considerations

Online education may not be appropriate for all potential home buyers. The presence of a disability, lack of Internet access,

and other issues may indicate that a consumer is better served through other education modes (e.g., in-person classroom

education, telephone conference call, etc.). In these situations, consumers should be directed to Framework’s toll-free

customer service line, from which they can be directed to a HUD-approved counseling agency that can meet their needs.The

counseling agency that handles the referral must provide a certificate of completion, and the lender must retain a copy of the

certificate in the loan file.

Previous Home-

Buyer Education

In lieu of the Framework course, Fannie Mae will allow lenders to accept a certificate of pre-purchase education/counseling

from a HUD-approved counseling agency dated within the previous six months before the loan application date and before

September 30, 2016.

Landlord Education Not Applicable

Landlord education required in accordance with Selling Guide

requirements (not available through Framework)

This summary is intended for reference only. All criteria are subject to the formal terms and conditions of the Fannie Mae Selling Guide and Servicing Guide. In the event of any conflict with this document, the Selling Guide and/or Servicing Guide will govern.

© 2016 Fannie Mae. Trademarks of Fannie Mae. March 21, 2016 Page 5 of 5

1-Unit 2- to 4-Unit

Pricin

g,

Co

mm

ittin

g,

Execu

tion

,

De

live

ry,

and S

erv

icin

g

Loan-Level Price

Adjustments (LLPAs)

Standard risk-based LLPAs waived with an LTV above 80% and a representative credit score equal to or greater than 680;

for loans outside of these parameters, standard LLPAs apply (per the LLPA matrix) with a cap of 1.50%.

(The Minimum MI Coverage Option LLPA is not waived or considered toward the cap if that option is used.)

Whole Loan

Pricing/Committing View live whole loan pricing and make commitments in Fannie Mae’s whole loan committing application

MBS Pricing and

Committing Lender base guaranty fee per MBS contract

Execution Commingle with non−HomeReady loans in whole loan commitments and MBS pools

Delivery Data Special Feature Code 900 required; set ULDD Sort ID 238 – LoanAffordableIndicator – to “True” to capture detailed

counseling information.

Servicing HomeReady loans will be serviced under the requirements for Fannie Mae’s community lending products. These Servicing

Guide requirements are currently under review by Fannie Mae, and we expect to simplify and clarify this policy for our

servicing partners.

LENDER FACT SHEET

HomeReady™ Mortgage Help meet the diverse needs of today’s buyers with HomeReady, Fannie Mae’s enhanced affordable lending product. Overview Designed for creditworthy, low- to moderate-income borrowers, with expanded eligibility for financing homes in designated low-income, minority, and disaster-impacted communities. HomeReady lets you lend with confidence while expanding access to credit and supporting sustainable homeownership.

• Simplicity and certainty for lenders • Improved pricing and execution • Product features designed to align with today’s buyer demographics and support sustainable

homeownership

Lender Benefits Enhanced Simplicity and Certainty

Borrower Benefits Accessible and Sustainable Financing

• Underwrite with confidence. Desktop

Underwriter® (DU®) offers a comprehensive credit risk assessment and eligibility determination, and automated identification of potentially HomeReady–eligible loans.

• Improved and simplified pricing is better than or equal to Fannie Mae standard loan pricing and supports a competitive borrower payment.

• Standard risk-based pricing waived for LTVs >80% with a credit score >=680 (risk-based loan-level price adjustment cap of 150 bps applies for loans outside of these parameters).

• Simplified execution. Ability to commingle standard and HomeReady loans into MBS pools and whole loan commitments.

• Low down payment. Up to 97% financing

for home purchase with many borrower flexibilities.

• Flexible sources of funds can be used for the down payment and closing costs with no minimum contribution required from the borrower’s own funds (1-unit properties).

• Conventional home financing with cancellable monthly MI (per Servicing Guide policy); reduced MI coverage requirement above 90% LTV supports competitive borrower payment.

• Homeownership education helps buyers get ready to buy a home and be prepared for the responsibilities of homeownership. The required training offers an easy-to-use, online course provided by Framework.

See next page for more about product features …

Fannie Mae’s Economic and Strategic Research group reports a “demographic sea change” in the housing market, characterized by the rise of the Millennials, increased diversity, and a growing elderly population; and

new household growth is being driven by traditionally underserved segments.

© 2015 Fannie Mae. Trademarks of Fannie Mae. September 29, 2015 Page 1 of 2

Income Eligibility (Aligned with Fannie Mae’s regulatory housing goals and may help lenders meet applicable Community Reinvestment Act goals)

Product Features

• DU will automatically identify potentially eligible loans. • Underwriting flexibilities include:

Offers an innovative new feature that supports extended family households: will consider income from a non-borrower household member as a compensating factor in DU to allow for a debt-to-income (DTI) ratio >45% to 50%.

Allows non-occupant borrowers, such as a parent. Permits rental income from an accessory dwelling unit (such as a basement apartment). Allows boarder income (updated guidelines provide documentation flexibility).

• Financing up to 97% LTV (DU is required for LTVs >95%). Borrower is not required to be a first-time buyer; purchase of one-unit principal residence (limited cash-out refi up to 95%).

• Lower MI coverage requirement than standard (25% for LTVs >90% to 97%). • Allows for nontraditional credit. • Gifts, grants, Community Seconds®, and cash-on-hand permitted as a source of funds for down

payment and closing costs. • Supports manufactured housing up to 95% and HomeStyle® Renovation (approved lenders) to 95%.

Homeownership Education and Post-Purchase Support Comprehensive homeownership education. Requires online course provided by Framework, and offers additional post-purchase support through the life of the loan to help ensure sustainable homeownership.

• Borrowers will invest 4−6 hours (average) of their time and a modest fee of $75 (paid to Framework) to learn the fundamentals of buying and owning a home, take an online test, and receive a certificate of completion.

• Although one-on-one counseling is optional for HomeReady, Framework will offer borrowers a referral to a HUD-approved counseling agency for additional assistance. Borrowers also have the option to consult a counselor of their choice.

• To further promote sustainability, borrowers will have access to post-purchase homeownership support for the life of the loan through Framework's homeownership advisor service.

Bookmark the HomeReady page for resources and updates: www.FannieMae.com/singlefamily/HomeReady

Borrower Income Eligibility 2015 Eligibility (Fannie Mae analysis using 2015 data)

No income limit: Properties in low-income census tracts 31% of census tracts

100% of AMI: Properties in high-minority census tracts and designated disaster areas 20% of census tracts

80% of AMI: All other properties 49% of all U.S. census tracts

AMI = area median income (AMI data source: FHFA)

© 2015 Fannie Mae. Trademarks of Fannie Mae. September 29, 2015 Page 2 of 2

Freddie Mac Home Possible® Mortgages

A responsible, low down payment mortgage option for first-time homebuyers and low- and moderate-income borrowers

Freddie Mac Home Possible® and Home Possible Advantage® mortgages (collectively referred to as Home Possible mortgages) offer outstanding flexibility and options to meet a variety of borrowers’ needs.

With Home Possible, you’ll capitalize on opportunities to meet the home financing needs of low- and moderate-income borrowers looking for low down payments and flexible sources of funds.

Home Possible Advantage offers more flexibility for maximum financing. This offering adopts the responsible and affordable flexibilities of Home Possible, but with additional requirements.

Purchase and no cash out refinancing.

Maximum 97 percent LTV and 105 percent TLTV ratios for Home Possible Advantage.

Mortgage insurance options.

Loan Product AdvisorSM or manual underwriting.

No reserves required for 1-unit properties.

Delivery fee cap of 0.0 percent or 1.50 percent.

Stable monthly payments with fixed-rate mortgages.

Flexible sources of funds.

Reduced mortgage insurance coverage levels for LTV ratios greater than 90 percent.

Minimum down payment of 3 percent allowed for Home Possible Advantage.

The information in this document is not a replacement or substitute for information found in the Single-Family Seller/

Servicer Guide and/or the terms of your Master Agreement and/or Master Commitment.

Borrower Profile

Publication Number 572 January 2017

Key Features

www.FreddieMac.com

You may offer this mortgage option for:

First-time homebuyers, move-up borrowers, and retirees.

Families in underserved areas.

Very low and low- to moderate-income borrowers.

This fact sheet reflects the changes announced in Single-Family Seller/Servicer Guide Bulletin 2015-21 and Bulletin 2016-8 effective for mortgages with Freddie Mac settlement dates on or after July 1, 2016.

Borrower Benefits

ORIGINATION & UNDERWRITING REQUIREMENTS

Eligible Property Types

Home Possible Home Possible Advantage

1- to 4-unit primary residences 1-unit primary residences only Condos Condos PUD PUDs Manufactured homes (with restrictions) See Guide Section A4501.6(a).

N/A

Eligible Mortgages

Home Possible mortgages eligible for purchase must be first lien mortgages that are fully amortizing. Home Possible mortgages must be conventional, conforming mortgages. Home Possible mortgages, other than mortgages secured by manufactured homes, must have an original maturity

date not greater than 30 years. Home Possible mortgages secured by manufactured homes must have a maximum original maturity not greater than

that specified in Guide Section 5703.3(d).

Home Possible Home Possible Advantage Fixed-rate mortgages Fixed-rate mortgages

7/1 and 10/1 ARMs if secured by a 1- or 2-unit primary residence

N/A

5/1 ARMs if secured by a 1- or 2-unit primary residence other than a manufactured home

N/A

Construction Conversion and Renovation Mortgages originated according to Guide Chapter 4602

Construction Conversion and Renovation Mortgages originated according to Guide Chapter 4602

Mortgages with an RHS Leveraged Second originated according to Guide Section 4205.2.

N/A

Temporary Subsidy Buydowns

Allowed for mortgages secured by 1- to 2-unit properties, other than manufactured homes (See Guide Sections 4501.5 and 4202.4).

If a mortgage with a temporary subsidy buydown plan is subject to secondary financing, including an Affordable Second® that requires repayment to begin before the due date of the 61st monthly payment under the Home Possible mortgage, the secondary financing must have a fixed interest rate.

Maximum LTV/TLTV/HTLTV Ratios

Maximum LTV/TLTV/LTV (Purchase and no cash-out refinance transactions)

Property Type LTV TLTV HTLTV Home Possible

1- to 4-unit 95% 95% 95% Manufactured home See Guide Chapter 5703.3

Home Possible Advantage 1-unit 97% 105% N/A

Minimum Borrower Contribution, and Reserves

Minimum Contribution from Borrower Personal Funds (Purchase transactions only)

Property Type Home Possible LTV/TLTV/HTLTV

ratios <= 80%

Home Possible LTV/TLTV/HTLTV

ratios >80% <= 95%

Home Possible Advantage mortgages

1-unit None None None 2- to 4-unit None 3% N/A Manufactured home None None N/A

Minimum Reserves Property Type Home Possible Home Possible Advantage

1-unit None required None required 2- to 4-units Two months N/A

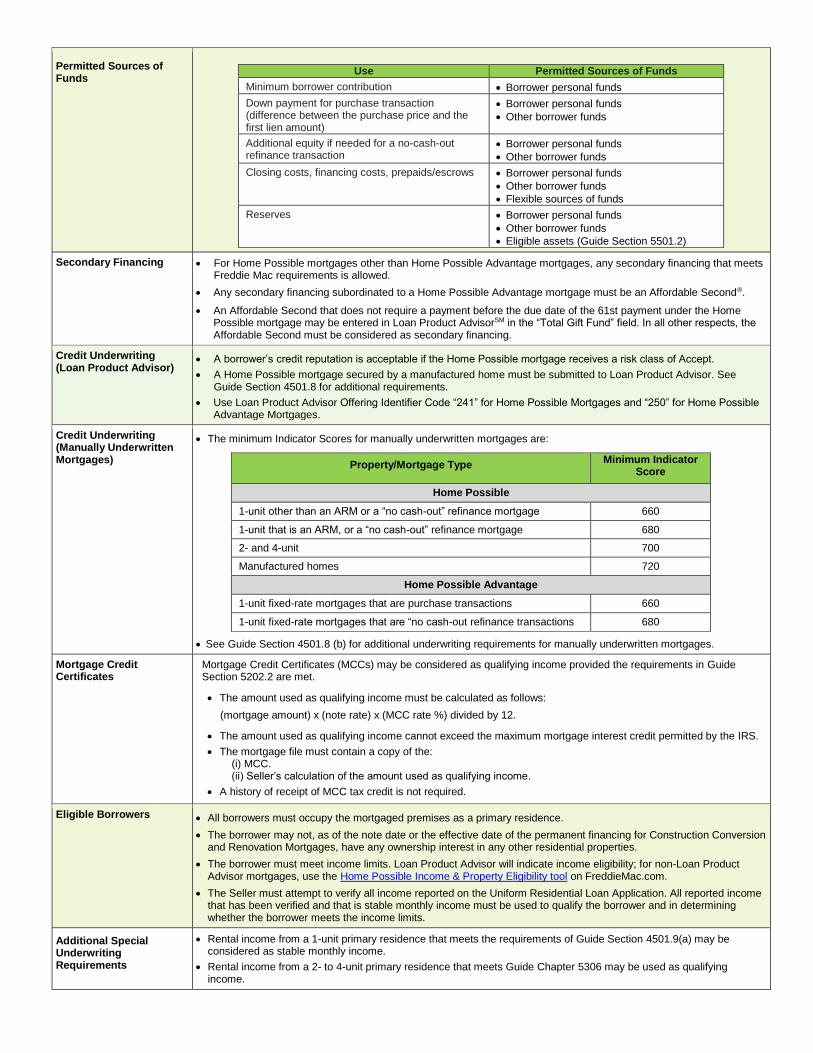

Permitted Sources of Funds

Use Permitted Sources of Funds

Minimum borrower contribution Borrower personal funds Down payment for purchase transaction (difference between the purchase price and the first lien amount)

Borrower personal funds Other borrower funds

Additional equity if needed for a no-cash-out refinance transaction

Borrower personal funds Other borrower funds

Closing costs, financing costs, prepaids/escrows Borrower personal funds Other borrower funds Flexible sources of funds

Reserves Borrower personal funds Other borrower funds Eligible assets (Guide Section 5501.2)

Secondary Financing

For Home Possible mortgages other than Home Possible Advantage mortgages, any secondary financing that meets Freddie Mac requirements is allowed.

Any secondary financing subordinated to a Home Possible Advantage mortgage must be an Affordable Second®. An Affordable Second that does not require a payment before the due date of the 61st payment under the Home

Possible mortgage may be entered in Loan Product AdvisorSM in the “Total Gift Fund” field. In all other respects, the Affordable Second must be considered as secondary financing.

Credit Underwriting (Loan Product Advisor)

A borrower’s credit reputation is acceptable if the Home Possible mortgage receives a risk class of Accept. A Home Possible mortgage secured by a manufactured home must be submitted to Loan Product Advisor. See

Guide Section 4501.8 for additional requirements. Use Loan Product Advisor Offering Identifier Code “241” for Home Possible Mortgages and “250” for Home Possible

Advantage Mortgages.

Credit Underwriting (Manually Underwritten Mortgages)

The minimum Indicator Scores for manually underwritten mortgages are:

Property/Mortgage Type Minimum Indicator Score

Home Possible 1-unit other than an ARM or a “no cash-out” refinance mortgage 660

1-unit that is an ARM, or a “no cash-out” refinance mortgage 680 2- and 4-unit 700

Manufactured homes 720

Home Possible Advantage 1-unit fixed-rate mortgages that are purchase transactions 660

1-unit fixed-rate mortgages that are “no cash-out refinance transactions 680

See Guide Section 4501.8 (b) for additional underwriting requirements for manually underwritten mortgages.

Mortgage Credit Certificates

Mortgage Credit Certificates (MCCs) may be considered as qualifying income provided the requirements in Guide Section 5202.2 are met.

The amount used as qualifying income must be calculated as follows: (mortgage amount) x (note rate) x (MCC rate %) divided by 12.

The amount used as qualifying income cannot exceed the maximum mortgage interest credit permitted by the IRS. The mortgage file must contain a copy of the:

(i) MCC. (ii) Seller’s calculation of the amount used as qualifying income.

A history of receipt of MCC tax credit is not required.

Eligible Borrowers

All borrowers must occupy the mortgaged premises as a primary residence. The borrower may not, as of the note date or the effective date of the permanent financing for Construction Conversion

and Renovation Mortgages, have any ownership interest in any other residential properties. The borrower must meet income limits. Loan Product Advisor will indicate income eligibility; for non-Loan Product

Advisor mortgages, use the Home Possible Income & Property Eligibility tool on FreddieMac.com. The Seller must attempt to verify all income reported on the Uniform Residential Loan Application. All reported income

that has been verified and that is stable monthly income must be used to qualify the borrower and in determining whether the borrower meets the income limits.

Additional Special Underwriting Requirements

Rental income from a 1-unit primary residence that meets the requirements of Guide Section 4501.9(a) may be considered as stable monthly income.

Rental income from a 2- to 4-unit primary residence that meets Guide Chapter 5306 may be used as qualifying income.

Mortgage Insurance Requirements

The standard required or custom MI coverage levels for Home Possible mortgages are as follows:

Transaction type MI coverage LTV Ratio

>80% & <85% >85% & <90% >90% & <95% >95% & <97%

Home Possible, fixed-rate, term < 20 years

Standard 6% 12% 25% 25%

Custom N/A N/A 16% 18%

Home Possible, fixed-rate, term > 20 years; ARMs; and manufactured homes1

Standard 12% 25% 25% 25%

Custom 6% 12% 16% 18%

1 Manufactured homes are limited to maximum LTV ratios of 95%.

Seller must obtain Freddie Mac's approval to sell mortgages with annual or monthly premium lender-paid mortgage insurance to Freddie Mac.

See Guide Section 4701.1 for additional MI requirements and options including custom MI.

Collateral Evaluation 1-unit primary residences: Use Form 70, Uniform Residential Appraisal Report.

Condominiums: Use Form 465, Individual Condominium Unit Appraisal Report. 2- to 4-unit primary residences: Use Form 72, Small Residential Income Property Appraisal Report.

Manufactured housing: Use Form 70B, Manufactured Home Appraisal Report.

Homebuyer and Landlord Education and Borrower Disclosure

See Guide Section 4501.12 for homeownership education and landlord education requirements related to: Borrower(s) who are all first-time homebuyers. Restrictions on parties that may provide the homeownership education. Homeownership education documentation that must be retained in the mortgage file. Acceptable types of homeownership education, including Freddie Mac CreditSmart® financial education curriculum or

CreditSmart – Steps to Homeownership Tutorial. Borrower disclosure requirements. Landlord education (2- to 4-unit primary residences) requirements for purchase transactions.

DELIVERY REQUIREMENTS

Eligible Executions

Home Possible Home Possible Advantage Servicing-Released Cash Servicing-Released Cash Servicing-Retained Cash Servicing-Retained Cash WAC ARM Cash Fixed-rate Guarantor Fixed-rate Guarantor MultiLender Swap WAC ARM Guarantor MultiLender Swap

Delivery Requirements See Guide Section 6302.14(b) for special delivery instruction for Home Possible mortgages and Guide Section 6304.34 for applicable secondary financing delivery requirements. In addition, Sellers must provide the applicable information, as outlined in Guide Section 6302.14(b), for down payment, closing costs, automated underwriting system, and borrower counseling. Sellers must deliver the following ULDD Data Points: o Loan Affordable Indicator: “true” o Loan Program Identifier: “Home Possible Mortgage” o Loan Program Identifier “Home Possible Advantage Mortgage” if applicable

If applicable, Sellers must deliver the following Investor Feature Identifiers (IFI) in ULDD Data Point IFI:

o IFI 532 (If mortgage satisfies the minimum number of payment reference requirement using noncredit payment references).

o IFI 583 (Home Possible mortgage with an Affordable Second). o IFI G18 (Home Possible mortgage with Affordable Second entered into Loan Product Advisor in "Total Gift Fund"

field).

Pooling Requirements There are no special pooling requirements for Home Possible mortgages. Refer to Guide Chapter 6202 for pooling requirements.

Mortgages may be pooled with non-Home Possible mortgages.

Delivery Fees See Guide Exhibit 19 for details on delivery fee caps and delivery fees applicable to Home Possible mortgages.

Learn more about Home Possible mortgages

Review Chapter 4501 of the Single-Family Seller/Servicer Guide.

Call 800-FREDDIE.

NMLS #176162©2015

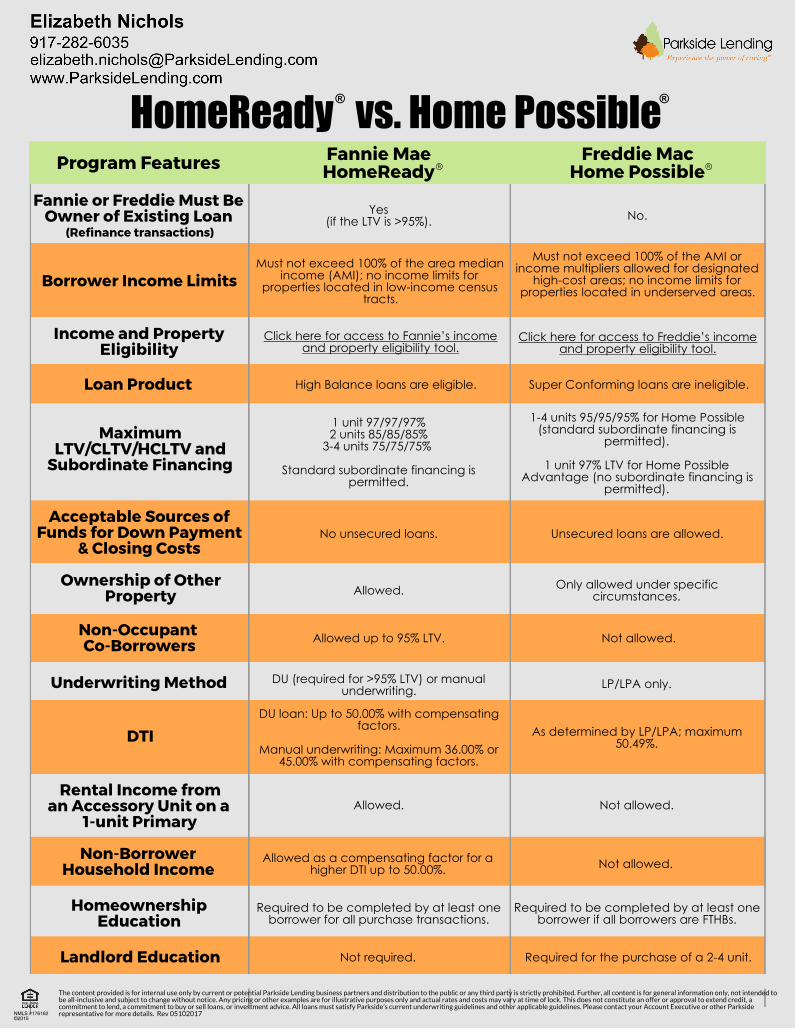

Borrower Income Limits

Income and PropertyEligibility

Loan Product

MaximumLTV/CLTV/HCLTV and

Subordinate Financing

HomeReady vs. Home Possible

Acceptable Sources ofFunds for Down Payment

& Closing Costs

® ®

Ownership of OtherProperty

Non-Occupant Co-Borrowers

Underwriting Method

DTI

Rental Income froman Accessory Unit on a

1-unit PrimaryNon-Borrower

Household Income

HomeownershipEducation

Landlord Education

Yes(if the LTV is >95%).

High Balance loans are eligible.

1 unit 97/97/97%2 units 85/85/85%

3-4 units 75/75/75%

Standard subordinate financing ispermitted.

Fannie or Freddie Must BeOwner of Existing Loan

(Refinance transactions)

Must not exceed 100% of the area median income (AMI); no income limits for

properties located in low-income census tracts.

Click here for access to Fannie’s income and property eligibility tool.

No unsecured loans.

Allowed.

Allowed up to 95% LTV.

DU (required for >95% LTV) or manualunderwriting.

DU loan: Up to 50.00% with compensatingfactors.

Manual underwriting: Maximum 36.00% or45.00% with compensating factors.

Allowed.

Allowed as a compensating factor for ahigher DTI up to 50.00%.

Required to be completed by at least oneborrower for all purchase transactions.

Not required.

No.

Must not exceed 100% of the AMI or income multipliers allowed for designated

high-cost areas; no income limits for properties located in underserved areas.

Click here for access to Freddie’s income and property eligibility tool.

Super Conforming loans are ineligible.

1-4 units 95/95/95% for Home Possible(standard subordinate financing is

permitted).

1 unit 97% LTV for Home PossibleAdvantage (no subordinate financing is

permitted).

Unsecured loans are allowed.

Only allowed under specific circumstances.

Not allowed.

LP/LPA only.

As determined by LP/LPA; maximum 50.49%.

Not allowed.

Not allowed.

Required to be completed by at least one borrower if all borrowers are FTHBs.

Required for the purchase of a 2-4 unit.

Program Features Fannie MaeHomeReady

Freddie MacHome Possible®®

The content provided is for internal use only by current or potential Parkside Lending business partners and distribution to the public or any third party is strictly prohibited. Further, all content is for general information only, not intended tobe all-inclusive and subject to change without notice. Any pricing or other examples are for illustrative purposes only and actual rates and costs may vary at time of lock. This does not constitute an offer or approval to extend credit, acommitment to lend, a commitment to buy or sell loans, or investment advice. All loans must satisfy Parkside’s current underwriting guidelines and other applicable guidelines. Please contact your Account Executive or other Parksiderepresentative for more details. Rev 05102017