hindustan petroleum corporation limited - petrotechpetrotech.in/uploadfiles/speakerprofiles/hpcl_ m...

TRANSCRIPT

Questions

1

Hindustan Petroleum

Corporation Limited

New Delhi

December 6, 2016

- M K Surana

Questions

2

Plan of Presentation

1 Hydrocarbon Industry : Outlook

2 Impact of Renewables

3 Reducing environmental footprint

Questions

3

Global Energy Mix : 2015

Oil is the world’s leading fuel, contributing to ~ 33% of

global energy consumption of 13,147 mtoe

Units in mtoeSource : BP Statistical Review 2016

Global Energy consumption

10 Year CAGR = 2.3% ; Growth in 2015 = 1.0%

Questions

4

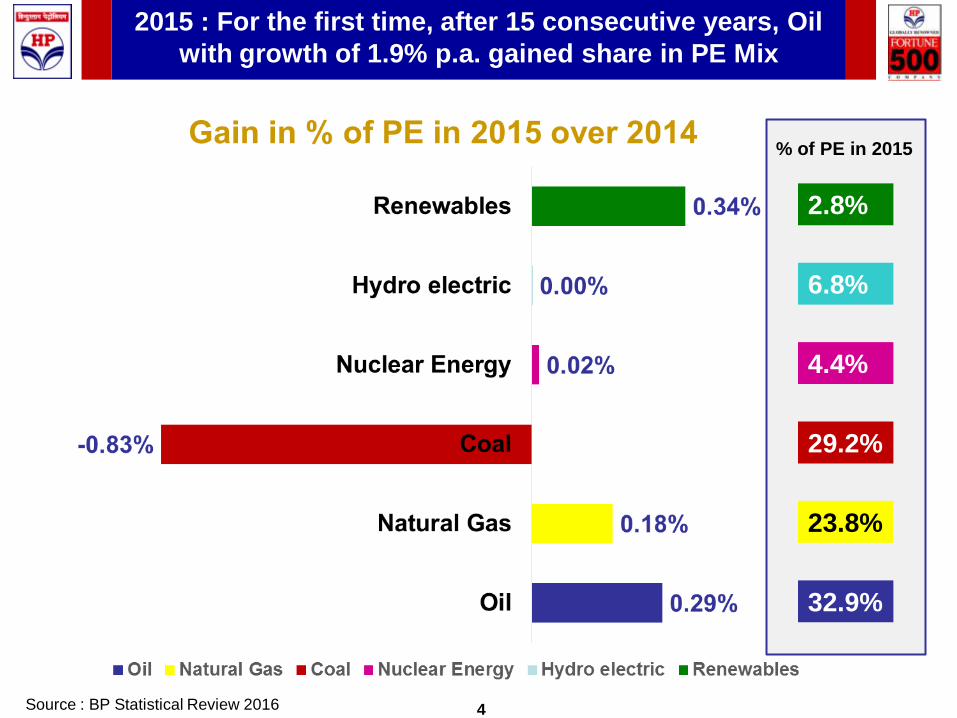

2015 : For the first time, after 15 consecutive years, Oil

with growth of 1.9% p.a. gained share in PE Mix

32.9%

23.8%

29.2%

4.4%

6.8%

2.8%

% of PE in 2015

Source : BP Statistical Review 2016

Questions

5

Key Global Trends witnessed in 2015

• Weakening energy demand due to decline in China growth, slow recovery

in Europe and shift of fuel mix from Coal to Natural gas in US power sector.

• Increased Supply, due to rapid technology and productivity gains driving

strong growth in US Oil output and growth in other Oil producers like Iraq,

Iran and Saudi Arabia.

• OPEC continued to leave output targets unchanged resulting in rise in Oil

inventories globally.

• Sharp fall in energy prices across Oil, Natural Gas and Coal.

• Non-Fossil fuels grew on the back of growth in new entrants of Solar and

Wind in Power sector, with China becoming the largest generator of Solar

Power.

• Technology costs particularly for wind and solar power have decreased

justifying investments in new capacities.

• Carbon Emissions from energy use witnessed the slowest growth in the

past 2 decades.

Source: Bloomberg, BP Statistical review 2016, Team Analysis

Questions

6

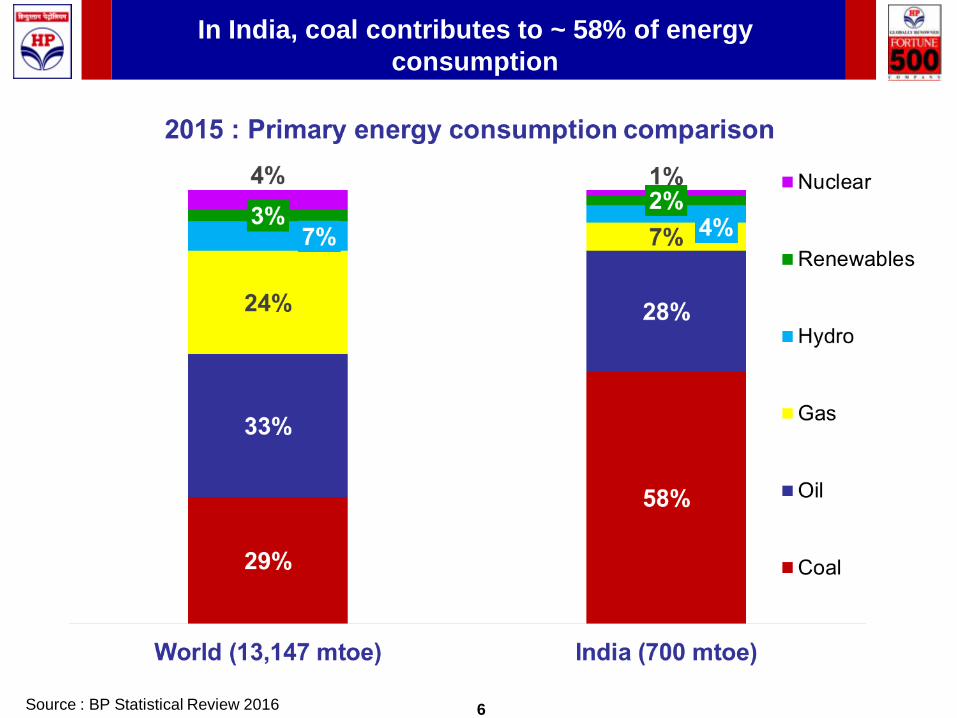

In India, coal contributes to ~ 58% of energy

consumption

Source : BP Statistical Review 2016

Questions

7

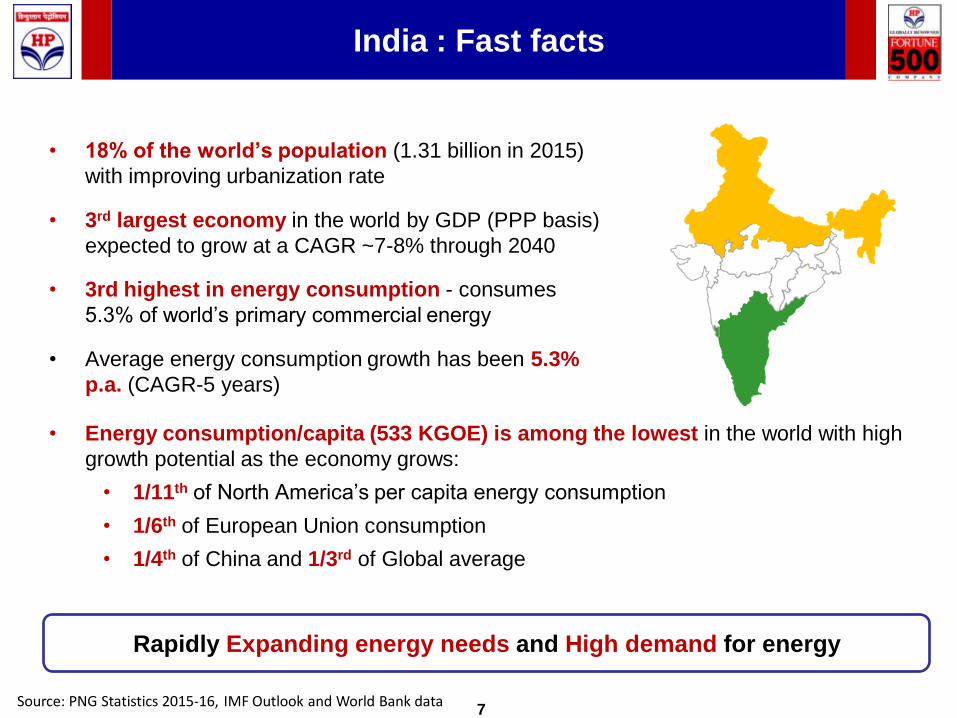

India : Fast facts

• 18% of the world’s population (1.31 billion in 2015)

with improving urbanization rate

• 3rd largest economy in the world by GDP (PPP basis)

expected to grow at a CAGR ~7-8% through 2040

• 3rd highest in energy consumption - consumes

5.3% of world’s primary commercial energy

• Average energy consumption growth has been 5.3%

p.a. (CAGR-5 years)

Rapidly Expanding energy needs and High demand for energy

• Energy consumption/capita (533 KGOE) is among the lowest in the world with high

growth potential as the economy grows:

• 1/11th of North America’s per capita energy consumption

• 1/6th of European Union consumption

• 1/4th of China and 1/3rd of Global average

Source: PNG Statistics 2015-16, IMF Outlook and World Bank data

Questions

8

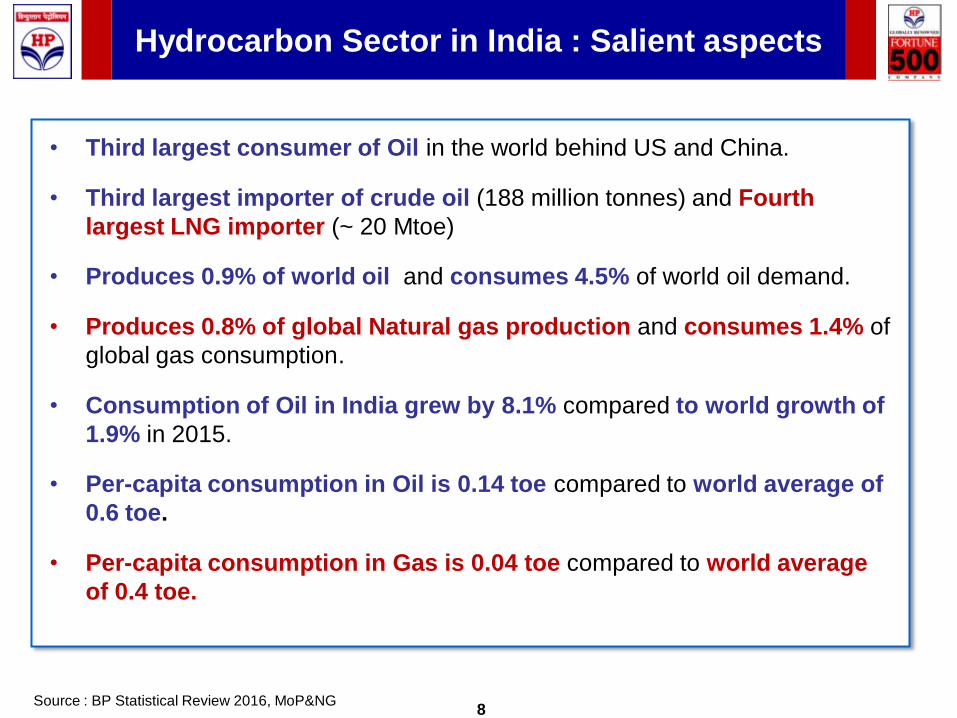

Hydrocarbon Sector in India : Salient aspects

Source : BP Statistical Review 2016, MoP&NG

• Third largest consumer of Oil in the world behind US and China.

• Third largest importer of crude oil (188 million tonnes) and Fourth

largest LNG importer (~ 20 Mtoe)

• Produces 0.9% of world oil and consumes 4.5% of world oil demand.

• Produces 0.8% of global Natural gas production and consumes 1.4% of

global gas consumption.

• Consumption of Oil in India grew by 8.1% compared to world growth of

1.9% in 2015.

• Per-capita consumption in Oil is 0.14 toe compared to world average of

0.6 toe.

• Per-capita consumption in Gas is 0.04 toe compared to world average

of 0.4 toe.

Questions

9

Government of India Initiatives driving Growth

FDI Liberalization• Construction

• Civil Aviation

• Defence

• Financial Services

• Oil & Gas

Policy Instruments • PMUY, DBTK, Perform Achieve and Trade (PAT) scheme

• RPO, Electricity to every household by 2019

• Pro-market, Pro-growth Reforms

• GST Framework under process

Government Initiatives

Make in India• Promoting India’s production/ manufacturing sector

• Improving investment and innovation landscape

• Start up India, Digital India, Skill India

Questions

10

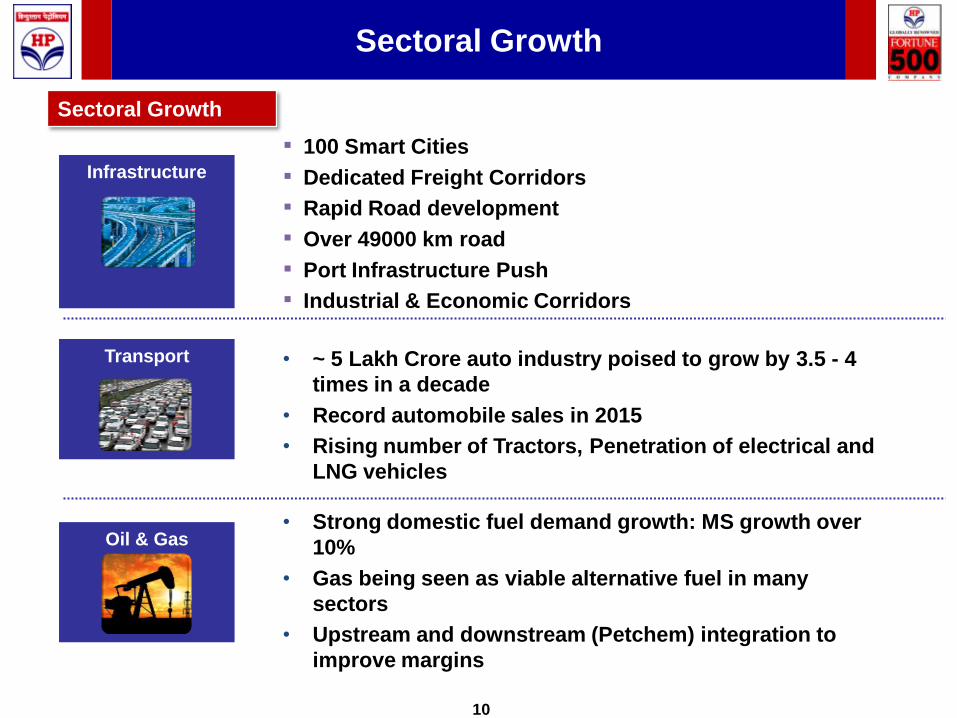

Sectoral Growth

Sectoral Growth

Oil & Gas• Strong domestic fuel demand growth: MS growth over

10%

• Gas being seen as viable alternative fuel in many

sectors

• Upstream and downstream (Petchem) integration to

improve margins

Infrastructure

▪ 100 Smart Cities

▪ Dedicated Freight Corridors

▪ Rapid Road development

▪ Over 49000 km road

▪ Port Infrastructure Push

▪ Industrial & Economic Corridors

Transport • ~ 5 Lakh Crore auto industry poised to grow by 3.5 - 4

times in a decade

• Record automobile sales in 2015

• Rising number of Tractors, Penetration of electrical and

LNG vehicles

Questions

11

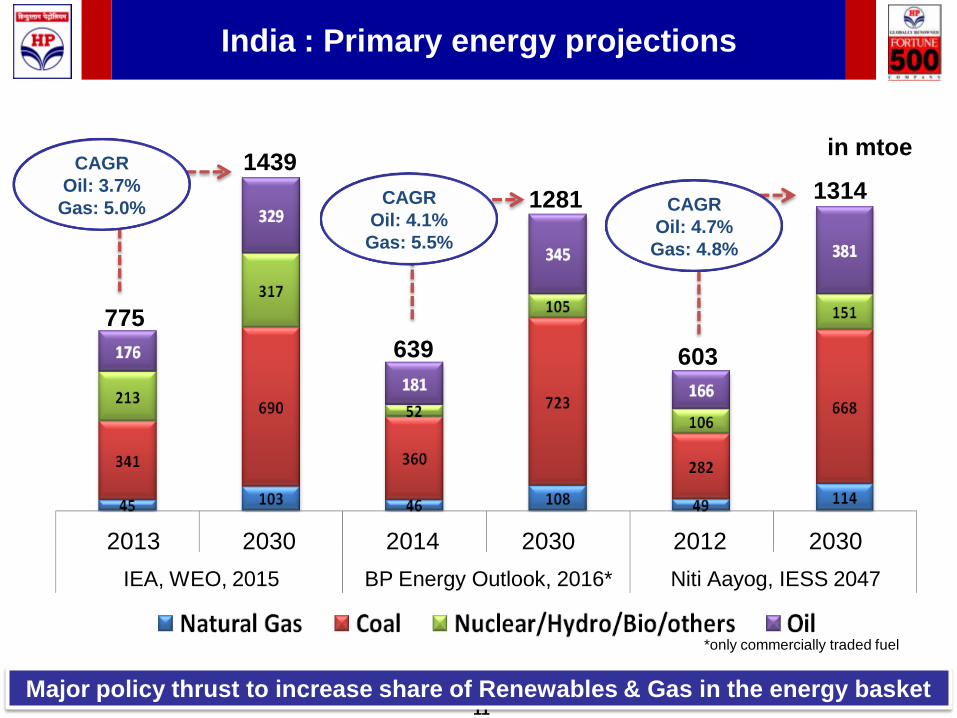

India : Primary energy projections

IEA, WEO, 2015 BP Energy Outlook, 2016* Niti Aayog, IESS 2047

2013 2030 2014 2030 2012 2030

775

1439

1281

639

1314

603

in mtoe

Major policy thrust to increase share of Renewables & Gas in the energy basket

CAGR

Oil: 3.7%

Gas: 5.0%CAGR

Oil: 4.1%

Gas: 5.5%

CAGR

Oil: 4.7%

Gas: 4.8%

*only commercially traded fuel

Questions

12

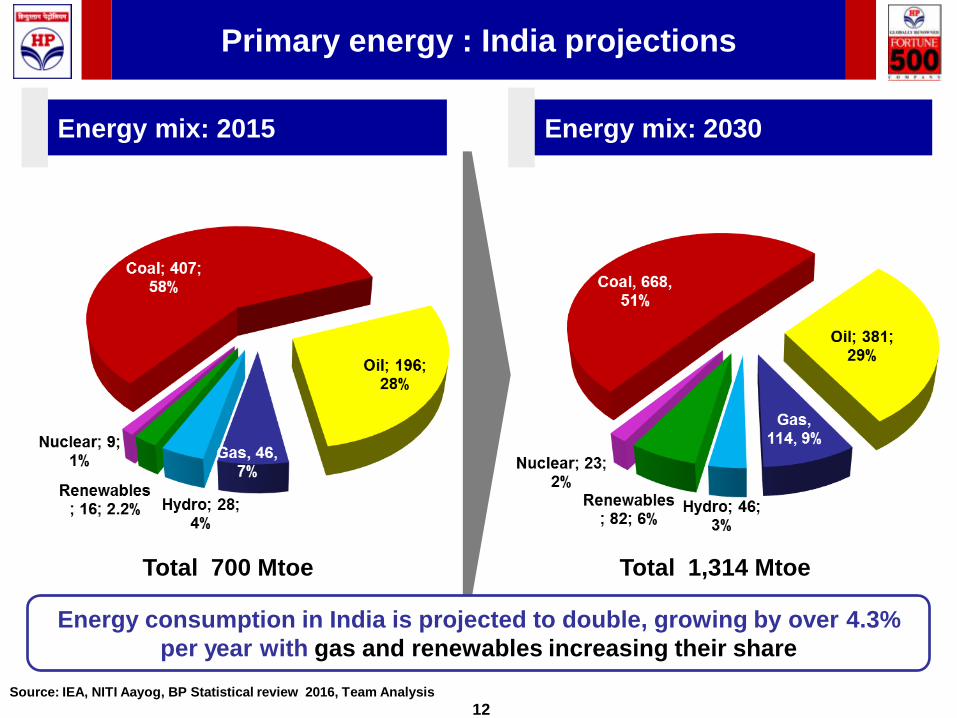

Primary energy : India projections

Source: IEA, NITI Aayog, BP Statistical review 2016, Team Analysis

Energy mix: 2015 Energy mix: 2030

Total 700 Mtoe Total 1,314 Mtoe

Energy consumption in India is projected to double, growing by over 4.3%

per year with gas and renewables increasing their share

Questions

13

Global oil outlook for 2030

SOURCE: BP statistics 2016, McKinsey, Team Analysis

Growth

Projections

2014-30 CAGR %

• Global Energy Perspective : 0.8%

• BP : 1.1%

• IEA- WEO : 0.9%

Global Oil demand is projected to grow at CAGR of 0.8% to 1.1% p.a.

to reach ~ 107 to 112 mbpd to by 2030

• Gas to become the fastest growing fossil fuel, spurred on strong supply growth,

particularly of US shale gas and LNG and supportive environmental policies

• Global Oil demand to increase substantially with growing use in Asia for both

transport and industry

• Oil demand to be driven by strong growth in emerging Asian markets met by

increased supply from the American Continent and OPEC

• China and India to consume most of the incremental oil demand and Oil

consumption in OECD economies continue to decline

Questions

14

Plan of Presentation

1 Hydrocarbon Industry : Outlook

2 Impact of Renewables

3 Reducing environmental foot print

Questions

15

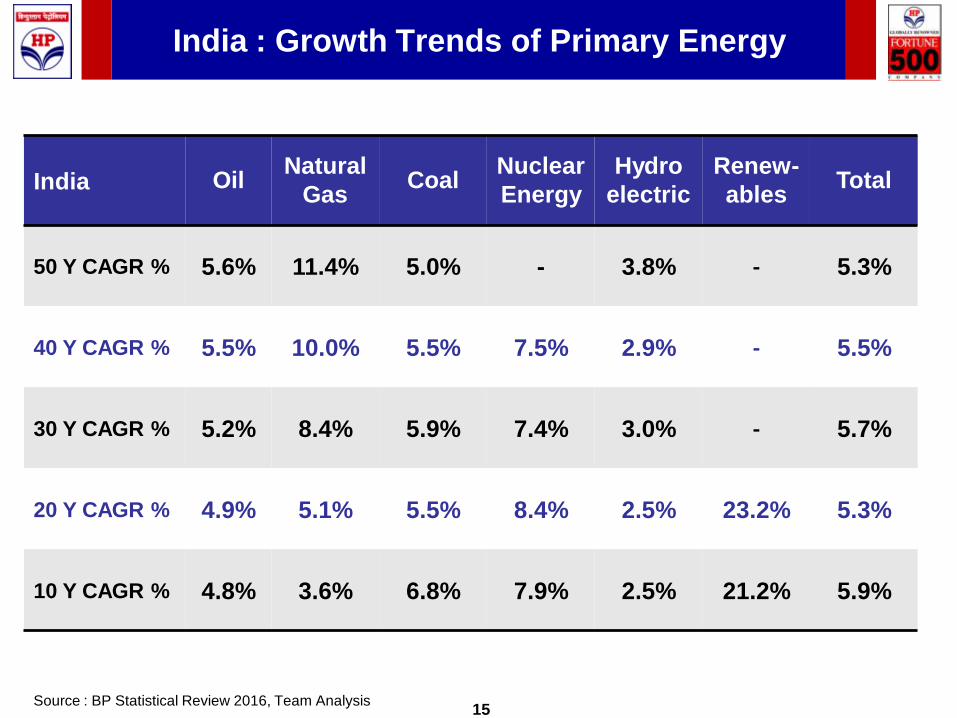

India : Growth Trends of Primary Energy

India OilNatural

GasCoal

Nuclear

Energy

Hydro

electric

Renew-

ablesTotal

50 Y CAGR % 5.6% 11.4% 5.0% - 3.8% - 5.3%

40 Y CAGR % 5.5% 10.0% 5.5% 7.5% 2.9% - 5.5%

30 Y CAGR % 5.2% 8.4% 5.9% 7.4% 3.0% - 5.7%

20 Y CAGR % 4.9% 5.1% 5.5% 8.4% 2.5% 23.2% 5.3%

10 Y CAGR % 4.8% 3.6% 6.8% 7.9% 2.5% 21.2% 5.9%

Source : BP Statistical Review 2016, Team Analysis

Questions

16

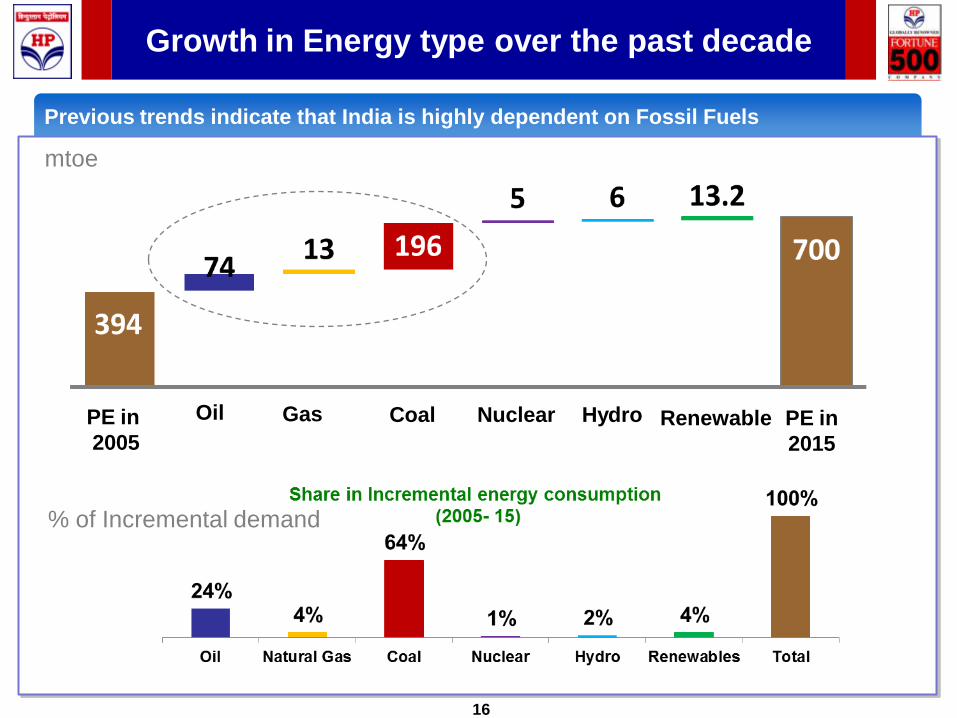

Growth in Energy type over the past decade

Previous trends indicate that India is highly dependent on Fossil Fuels

mtoe

GasPE in

2005

Oil Coal Nuclear Hydro Renewable PE in

2015

% of Incremental demand

Questions

17

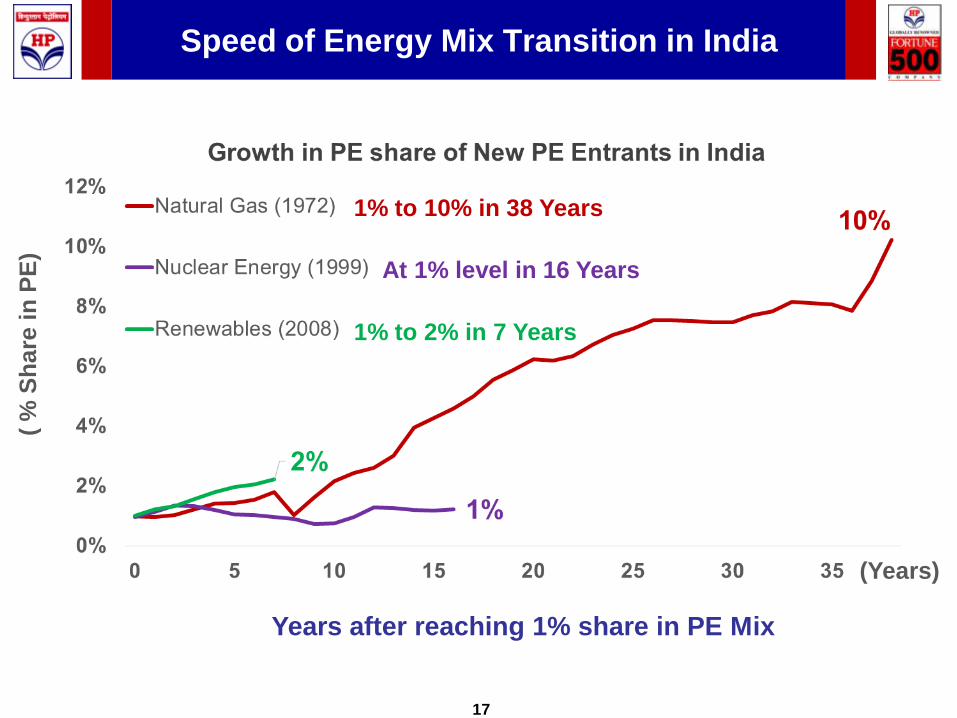

Speed of Energy Mix Transition in India

Years after reaching 1% share in PE Mix

1% to 10% in 38 Years

At 1% level in 16 Years

1% to 2% in 7 Years

(Years)

( %

Sh

are

in

PE

)

Questions

18

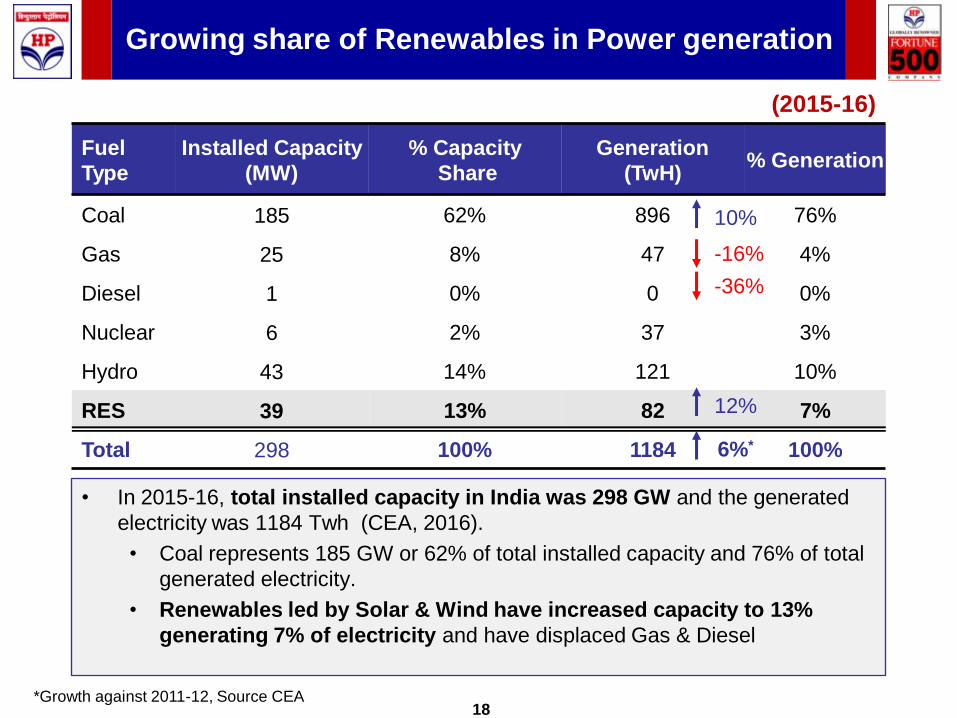

Growing share of Renewables in Power generation

Fuel

Type

Installed Capacity

(MW)

% Capacity

Share

Generation

(TwH)% Generation

Coal 185 62% 896 76%

Gas 25 8% 47 4%

Diesel 1 0% 0 0%

Nuclear 6 2% 37 3%

Hydro 43 14% 121 10%

RES 39 13% 82 7%

Total 298 100% 1184 100%

(2015-16)

• In 2015-16, total installed capacity in India was 298 GW and the generated

electricity was 1184 Twh (CEA, 2016).

• Coal represents 185 GW or 62% of total installed capacity and 76% of total

generated electricity.

• Renewables led by Solar & Wind have increased capacity to 13%

generating 7% of electricity and have displaced Gas & Diesel

-16%

-36%

10%

12%

6%*

*Growth against 2011-12, Source CEA

Questions

19

Hydrocarbon fuels will continue to play an important

role in India

Significant rise in passenger vehicle ownership and

affordability of air travel will propel the transport fuels and

lubricants demand.

LPG to witness a high growth with policies aimed at providing

cleaner cooking fuels and encouraging a move away from solid

biomass for cooking.

Industrial consumption of oil & gas products to grow

significantly with rising energy demand from Industries on the

back of thrust on manufacturing sector from Make in India.

Gas demand to increase due to demand from end use sectors

like power generation, transport, Fertilisers, Petrochemicals etc.

and strengthening of regasification & supply infrastructure.

e-SV

Questions

20

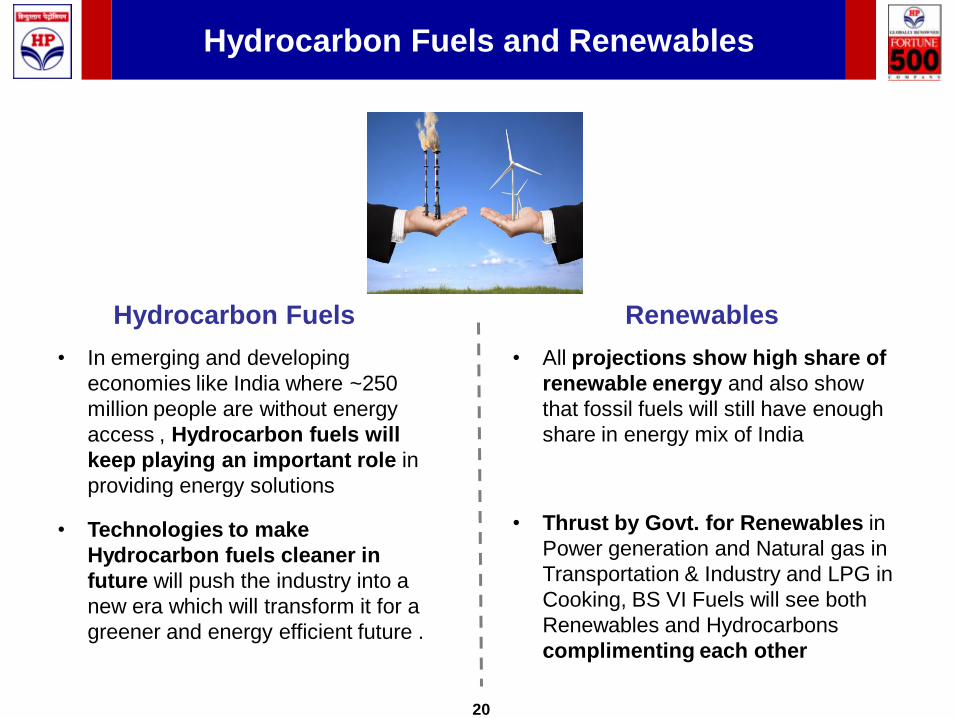

Hydrocarbon Fuels and Renewables

• In emerging and developing

economies like India where ~250

million people are without energy

access , Hydrocarbon fuels will

keep playing an important role in

providing energy solutions

• Technologies to make

Hydrocarbon fuels cleaner in

future will push the industry into a

new era which will transform it for a

greener and energy efficient future .

• All projections show high share of

renewable energy and also show

that fossil fuels will still have enough

share in energy mix of India

• Thrust by Govt. for Renewables in

Power generation and Natural gas in

Transportation & Industry and LPG in

Cooking, BS VI Fuels will see both

Renewables and Hydrocarbons

complimenting each other

Hydrocarbon Fuels Renewables

Questions

21

Plan of Presentation

1 Hydrocarbon Industry : Outlook

2 Impact of Renewables

3 Reducing environmental foot print

Questions

23

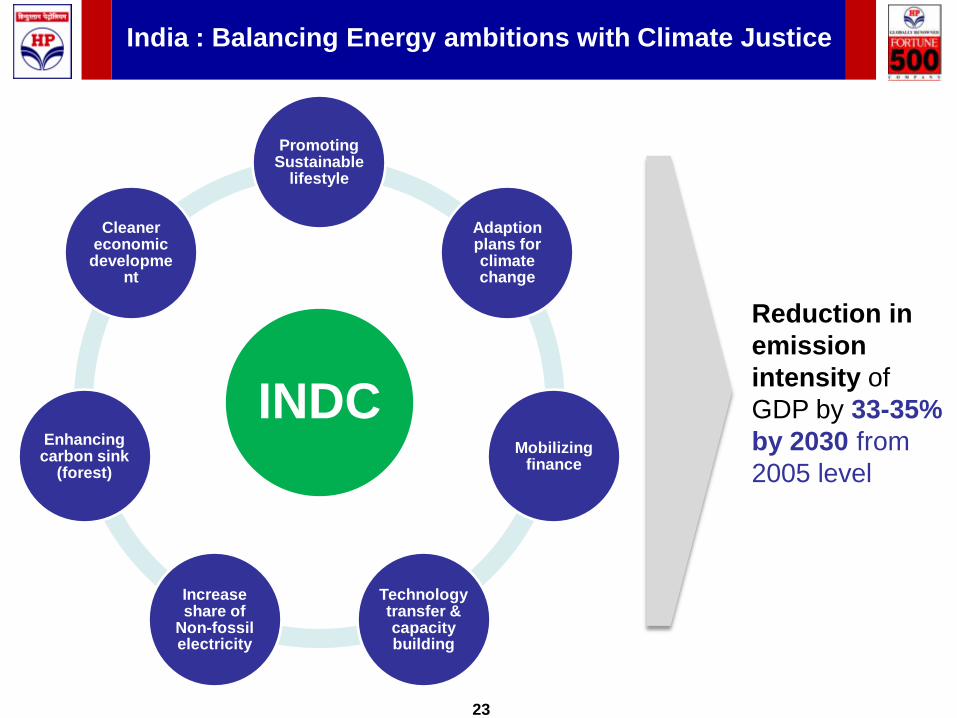

India : Balancing Energy ambitions with Climate Justice

INDC

Promoting Sustainable

lifestyle

Adaption plans for climate change

Mobilizing finance

Technology transfer & capacity building

Increase share of

Non-fossil electricity

Enhancing carbon sink

(forest)

Cleaner economic

development

Reduction in

emission

intensity of

GDP by 33-35%

by 2030 from

2005 level

Questions

24

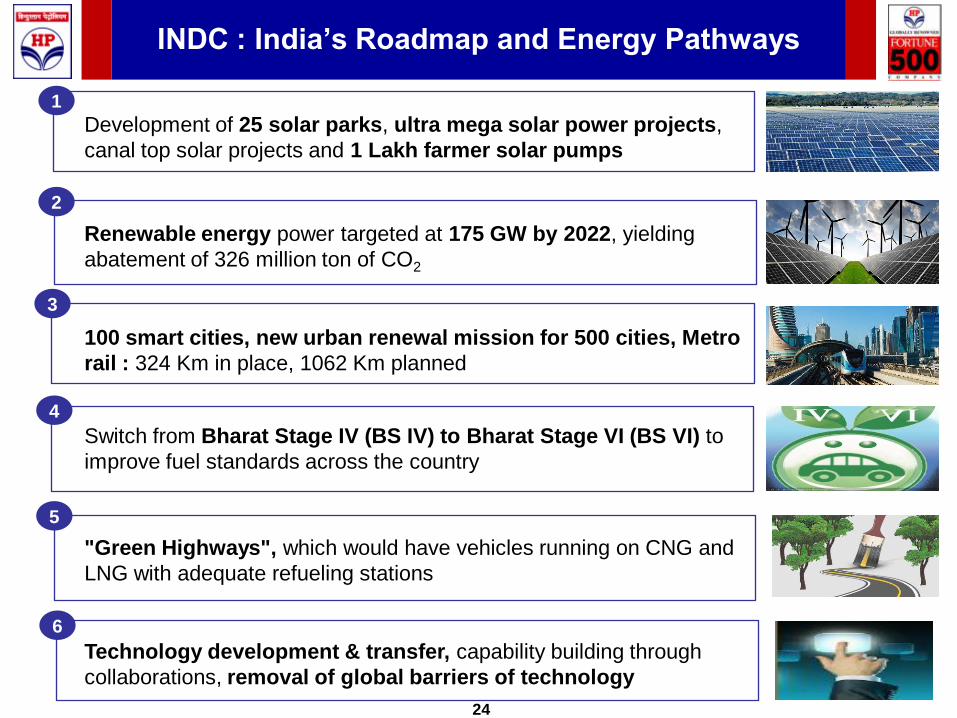

INDC : India’s Roadmap and Energy Pathways

1

2

3

4

5

6

Development of 25 solar parks, ultra mega solar power projects,

canal top solar projects and 1 Lakh farmer solar pumps

Renewable energy power targeted at 175 GW by 2022, yielding

abatement of 326 million ton of CO2

100 smart cities, new urban renewal mission for 500 cities, Metro

rail : 324 Km in place, 1062 Km planned

Switch from Bharat Stage IV (BS IV) to Bharat Stage VI (BS VI) to

improve fuel standards across the country

"Green Highways", which would have vehicles running on CNG and

LNG with adequate refueling stations

Technology development & transfer, capability building through

collaborations, removal of global barriers of technology

Questions

25

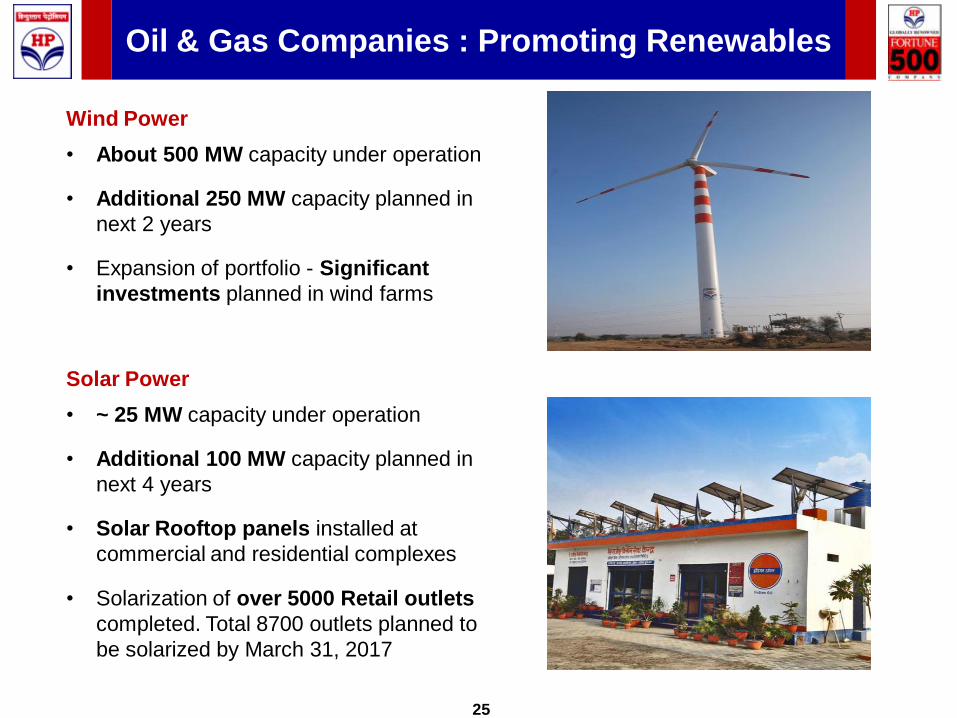

Oil & Gas Companies : Promoting Renewables

Wind Power

• About 500 MW capacity under operation

• Additional 250 MW capacity planned in

next 2 years

• Expansion of portfolio - Significant

investments planned in wind farms

Solar Power

• ~ 25 MW capacity under operation

• Additional 100 MW capacity planned in

next 4 years

• Solar Rooftop panels installed at

commercial and residential complexes

• Solarization of over 5000 Retail outlets

completed. Total 8700 outlets planned to

be solarized by March 31, 2017

Questions

26

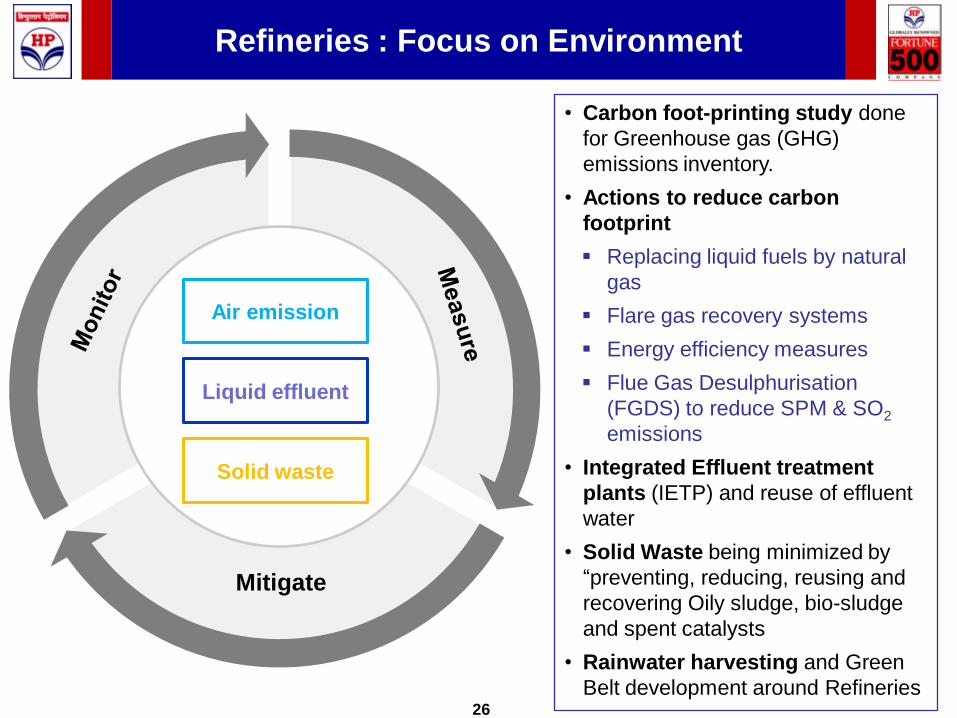

Refineries : Focus on Environment

Mitigate

• Carbon foot-printing study done

for Greenhouse gas (GHG)

emissions inventory.

• Actions to reduce carbon

footprint

Replacing liquid fuels by natural

gas

Flare gas recovery systems

Energy efficiency measures

Flue Gas Desulphurisation

(FGDS) to reduce SPM & SO2

emissions

• Integrated Effluent treatment

plants (IETP) and reuse of effluent

water

• Solid Waste being minimized by

“preventing, reducing, reusing and

recovering Oily sludge, bio-sludge

and spent catalysts

• Rainwater harvesting and Green

Belt development around Refineries

Air emission

Liquid effluent

Solid waste

Questions

27

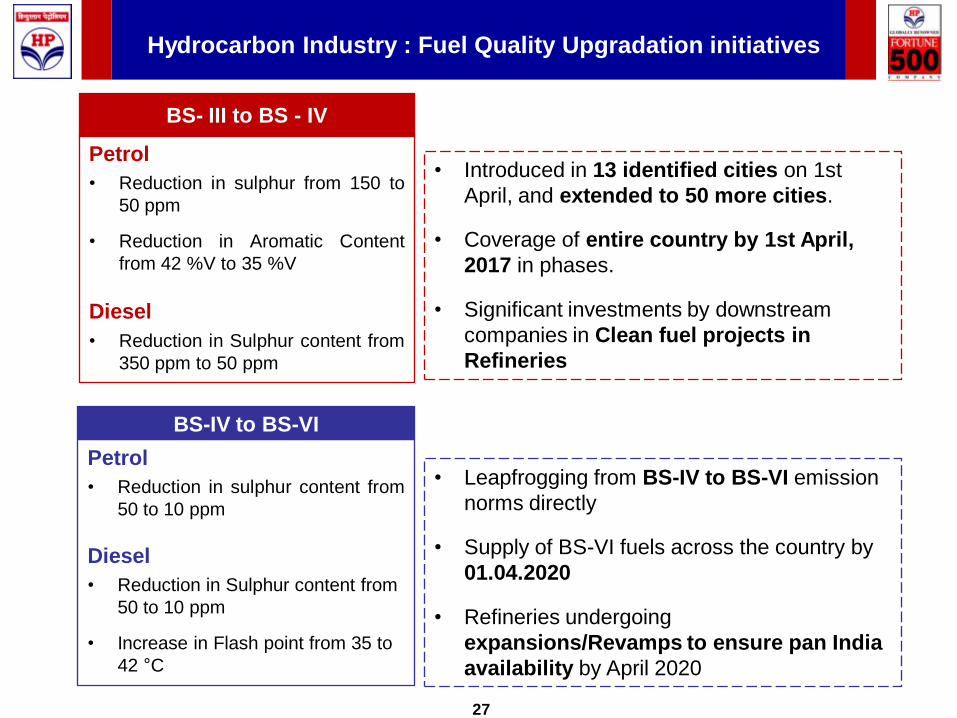

Hydrocarbon Industry : Fuel Quality Upgradation initiatives

Petrol

• Reduction in sulphur from 150 to

50 ppm

• Reduction in Aromatic Content

from 42 %V to 35 %V

Diesel

• Reduction in Sulphur content from

350 ppm to 50 ppm

BS- III to BS - IV

Petrol

• Reduction in sulphur content from

50 to 10 ppm

Diesel

• Reduction in Sulphur content from

50 to 10 ppm

• Increase in Flash point from 35 to

42 °C

BS-IV to BS-VI

• Introduced in 13 identified cities on 1st

April, and extended to 50 more cities.

• Coverage of entire country by 1st April,

2017 in phases.

• Significant investments by downstream

companies in Clean fuel projects in

Refineries

• Leapfrogging from BS-IV to BS-VI emission

norms directly

• Supply of BS-VI fuels across the country by

01.04.2020

• Refineries undergoing

expansions/Revamps to ensure pan India

availability by April 2020

Questions

28

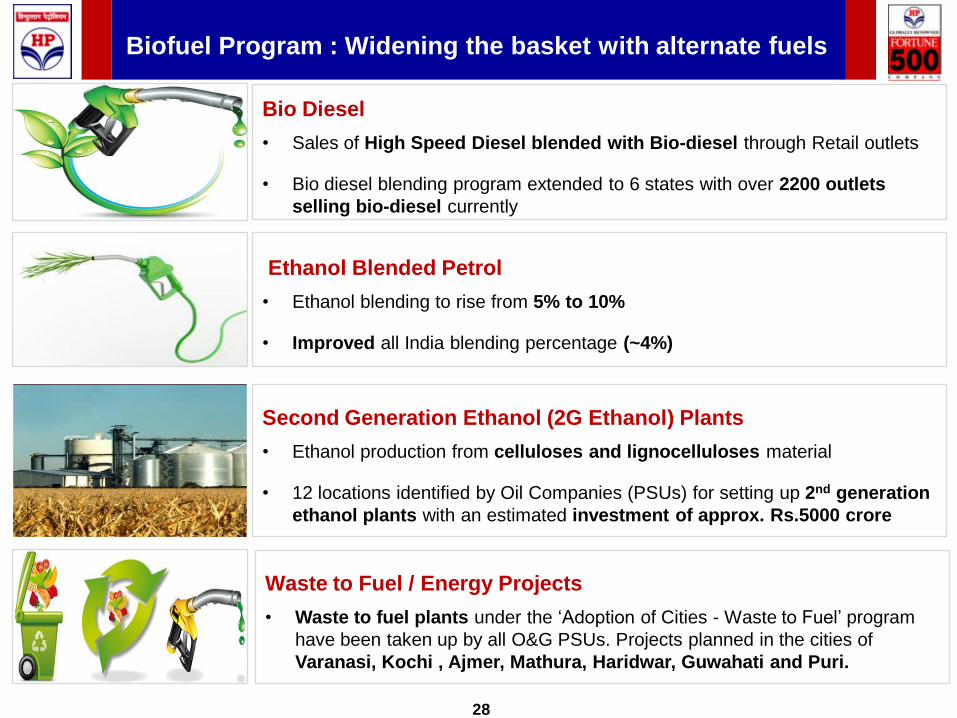

Biofuel Program : Widening the basket with alternate fuels

Bio Diesel

• Sales of High Speed Diesel blended with Bio-diesel through Retail outlets

• Bio diesel blending program extended to 6 states with over 2200 outlets

selling bio-diesel currently

Second Generation Ethanol (2G Ethanol) Plants

• Ethanol production from celluloses and lignocelluloses material

• 12 locations identified by Oil Companies (PSUs) for setting up 2nd generation

ethanol plants with an estimated investment of approx. Rs.5000 crore

Ethanol Blended Petrol

• Ethanol blending to rise from 5% to 10%

• Improved all India blending percentage (~4%)

Waste to Fuel / Energy Projects

• Waste to fuel plants under the ‘Adoption of Cities - Waste to Fuel’ program

have been taken up by all O&G PSUs. Projects planned in the cities of

Varanasi, Kochi , Ajmer, Mathura, Haridwar, Guwahati and Puri.

Questions

29

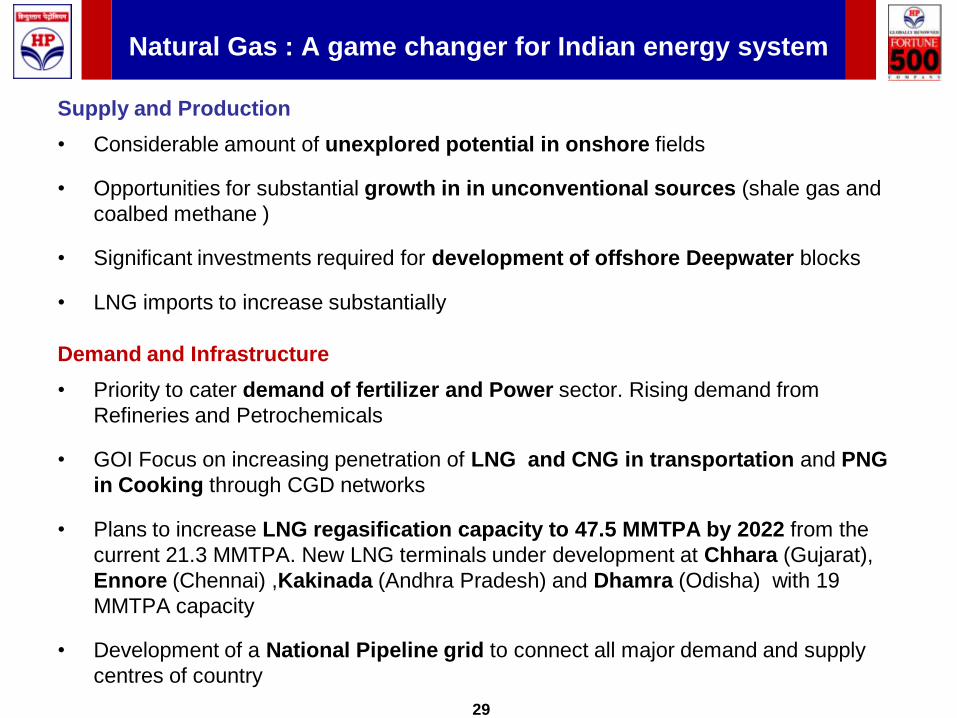

Natural Gas : A game changer for Indian energy system

Supply and Production

• Considerable amount of unexplored potential in onshore fields

• Opportunities for substantial growth in in unconventional sources (shale gas and

coalbed methane )

• Significant investments required for development of offshore Deepwater blocks

• LNG imports to increase substantially

Demand and Infrastructure

• Priority to cater demand of fertilizer and Power sector. Rising demand from

Refineries and Petrochemicals

• GOI Focus on increasing penetration of LNG and CNG in transportation and PNG

in Cooking through CGD networks

• Plans to increase LNG regasification capacity to 47.5 MMTPA by 2022 from the

current 21.3 MMTPA. New LNG terminals under development at Chhara (Gujarat),

Ennore (Chennai) ,Kakinada (Andhra Pradesh) and Dhamra (Odisha) with 19

MMTPA capacity

• Development of a National Pipeline grid to connect all major demand and supply

centres of country

Questions

30

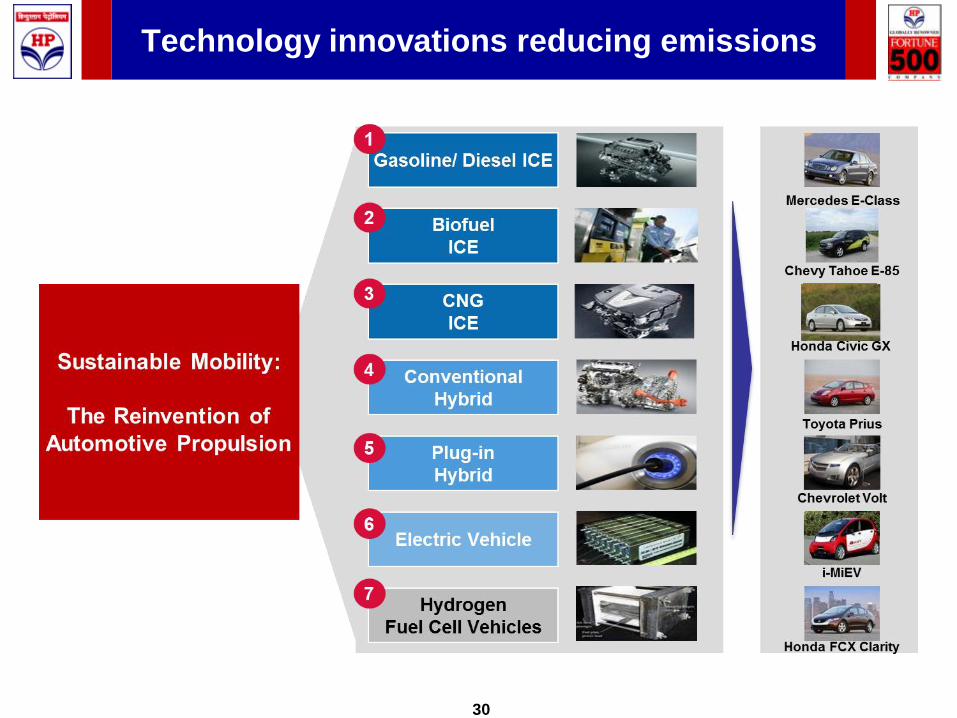

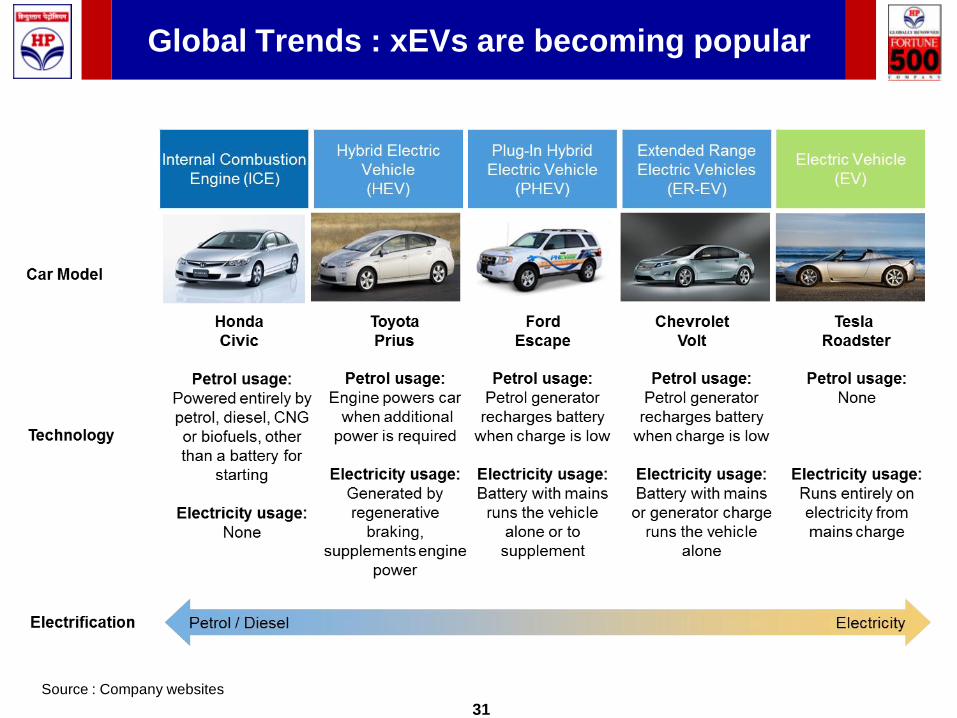

Technology innovations reducing emissions

Questions

31

Global Trends : xEVs are becoming popular

Source : Company websites

Questions

32

In Conclusion

• Energy consumption in India is projected to double, growing by a CAGR of 4.3%

per year to reach ~ 1314 mtoe by 2030.

• The energy mix is projected to change with Renewables & Gas increasing the

share and Oil holding steady.

• Fossil fuels remain the dominant source of energy powering the Indian economy,

providing around 84% of the growth in energy demand (Coal – 43%, Oil – 30% and

Gas -11%) between 2015 to 2030 and accounting for about 89% of total energy

supply in 2030 (down from 93% in 2015).

• Gas is seen to be increasingly used in the industrial sector and for power

generation. Liquid fuels continue to dominate in the Transport sector.

• Among non-fossil fuels, renewables (including biofuels) is projected to grow

rapidly (11.7% p.a.), increasing share in primary energy from 2% in 2015 to reach

6% by 2030.

• Renewables is seen competing with fossil fuels in Power sector directly.

• The degree of Policy measures in Carbon Emissions will see advent of Battery

operated vehicles and increased use of natural gas as vehicle fuel.

Thank you