health insurance aseem sapphire

TRANSCRIPT

Relax……..

WELCOME

HEALTH INSURANCEMr.Aseem.B,

MSc N,MBA,PGDHA,

Assistant Professor,

SP Fort College of Nursing,

Thiruvananthapuram

aseem.sapphire

DEFINITION• The term Health Insurance is generally used to

describe a form of insurance that pays for medical expenses. (Joshy D C, 2009).

• It is the payment for the expected costs of a group resulting from medical utilization based on the expected expenses incurred by the group. The payment can be based on community or experience rating. (Jacobs P, 2004).

•

HISTORY FOUNDATIONS

HISTORY FOUNDATIONS

• In history health insurance existed as health care provided by one’s family, tribe, or village

• During industrial revolution financial contracts for the cargo of ships developed.

• Then it moved to industrial nations, factory owners or donations from workers supplied sums of money for ill or injured workers as needed.

• In mining sickness funds began to be supplied by owners .• In addition some factory owners hired company doctors

for sick and injured.

• Early Asian Insurers–Meiji Life Assurance Company, 1888, was the

first life insurance company to open in Japan.–Cho-Sun Life Insurance Company, 1921, was

the first company capitalized and owned by Koreans– The Great Eastern Life Assurance Company

Limited was founded in Singapore in 1908.– In india oriental insurance company in

Calcutta.

PRINCIPLES OF HEALTH INSURANCE

• Health insurance is based on principles that affect the alignment of incentives around cost, quality, and access. These principles are related to concepts such as information, predictability of risk, and ways that the demand for health care may be influenced.

• Information problems and asymmetric information

• Setting premium and rating• Third party administrators• Deductables, Coinsurance• co-payment• Adverse selection• Moral hazard

Information problems and asymmetric information

INFORMATION PROBLEMS AND ASYMMETRIC INFORMATION

• Insurers (payers) have information problems. The primary reason for health insurance coverage is to protect against unpredictable risk: the costs of an unexpected illness, injury, or disability. Young and relatively healthy persons may pay health insurance premiums for years before an illness or other disorder occurs

ASYMMETRIC INFORMATION

• The problem of asymmetric information differs from information problems in that one party possesses knowledge needed to enable rational decision making that the other party lacks. Health insurers face asymmetric information when consumers do not disclose conditions such as diabetes, cardiovascular disorders, serious risk behaviors, or disabilities.

Setting premium and rating

Setting premium and rating• Health plans must make decisions about the premiums they

charge. • Experience rating : It is a method used by many traditional

indemnity health insurance plans in which premiums are based on the utilization or claims history of the group, rather than on the characteristics of the group’s population as a whole. As a result, a plan year in which a group experiences an unusual number of high-cost claims (such as AIDS cases) may result in higher premiums the following year.

• Community rating is a method in which premiums are based on the population characteristic of an entire group. In many cases, community ratings are adjusted for age and sex, and sometimes other factors as well.

Third party administrators

THIRD PARTY TRANSACTIONS• Health insurance represents a third party transaction;

in other words, a provider supplies goods or services to the consumer (patient) but bills a private or government insurance entity, which is the third party.

• As a result, consumers typically are largely unconcerned with the costs of their care, knowing that their bills are paid by another party.

• Third party transactions provide incentives to patients to utilize health care goods and services that may not be necessary, as they are not sensitive to the cost of these interventions.

DEDUCTABLES, COINSURANCE, • Deductibles represent minimum threshold payments

before a plan begins to cover health care costs. For example, there may be a $100 annual deductible for prescription medications:

• after the beneficiary pays the first $100, the insurance plan covers the remainder of the prescription medication costs for the plan year.

• Coinsurance represents a percentage of a given health care cost that is required by the insurer to be paid by the beneficiary; by comparison.

CO-PAYMENT

• co-payment represents a specific dollar amount of the given health care cost required of the beneficiary. For example, a beneficiary may be required to pay a 20% coinsurance for the inpatient hospital bed rate after the fifth inpatient day, or required to pay $20 co-payment for every visit to a primary care physician’s office.

ADVERSE SELECTION

• Adverse selection is the over-selection of a health plan based on its coverage of persons likely to have high health care costs. When the consumer is more knowledgeable about the probability of illness and health care costs than the insurer (asymmetric information), the problem of adverse selection can occur.

• For example, a health plan providing more generous coverage to persons with diabetes than competing health plans unknowingly attracts a greater proportion of diabetic beneficiaries than would be expected in the overall risk pool

MORAL HAZARD

• Moral hazard represents a plan member’s higher utilization of covered services. Unlike adverse selection, it is not that the member is primarily at higher risk for health care costs, but because these costs are covered by insurance, the member utilizes more health care goods or services than might be necessary.

• For example, a person with vision coverage might purchase new glasses more frequently, even if the eye examination indicates that the lens prescription has not changed.

HEALTH INSURANCE POLICY

• It is contract between an insurer and an individual or group, in which insurer agrees to provide, specific Health Insurance at an agreed upon premium. Depending upon the insurance policy the premium may be payable in lump sum or in installments.

AMERICAN STUDY

TYPES OF HEALTH INSURANCE

• International health insurance agencies: As a result of globalization, the international health insurance agencies have also started showing interest in the field of health insurance. This is useful for those going abroad on tourist VISA, etc.

• Insurance agencies in public sector: In India, the insurance agencies also undertake health insurance in the form of medi-claim policies

• Insurance in private sector: The private sector is playing an important role in health insurance of the people.

• Mandatory Insurance: The examples are ESI scheme, CGHS, and ECHS (Ex service Man Contributory Health Scheme).

• Employer based health insurance schemes for the employees in the private sector not covered under the ESI scheme.

• Community based health insurance: The example is Yashasvirti scheme of Karnataka government for farmers.

• Cashless health insurance: After the formation of Insurance Regulatory and Development Authority (IRDA), the cashless insurance has resulted into development of the Third Party Administrators.

SOCIAL HEALTH INSURANCE

• The SHI is based on income-determined contributions from mandatory membership of, in principal, the entire population with the government subsidizing the financially vulnerable sections.

• The existing mandatory health insurance schemes in India the Employees’ State Insurance Scheme (ESIS) and the Central Government Health Scheme (CGHS)—were first started as pilot projects in 1948 and 1954, respectively in the context of achieving universal coverage via the SHI.

CENTRAL GOVERNMENT HEALTH SCHEME (CGHS)

EMPLOYEES STATE INSURANCE

ESI SCHEME• Enacted in 1948, the Employees’ State Insurance

(ESI) Act was the first major legislation on social security in India.

• The scheme applies to power using factories employing 10 persons or more, and non-power and other specified establishments employing 20 persons or more, with employees’ earnings up to Rs 7500 per month being covered, along with their dependants.

• The current coverage stands at 84 lakh employees and 353 lakh beneficiaries across 22 States and Union Territories.

CENTRAL GOVERNMENT HEALTH SCHEME (CGHS)

• The Central Government Health Scheme (previously known as Contributory Health Service Scheme) for the Central Government employees was first introduced in New Delhi in 1954 to provide comprehensive medical care to Central Government employees.

• CGHS covers employees and retirees of the Central Government, and certain autonomous, semi-autonomous and semi-government organizations.

• It also covers Members of Parliament, governors, accredited journalists, Widows receiving family pension, Ex Governors, Ex Judges of Supreme Court and high courts and members of the general public in some specified areas.

• The families of the employees are also covered under the scheme.

CGHS

• Benefits under the scheme include medical care at all levels and home visits/care as well as free medicines and diagnostic services.

• These services are provided through public facilities (including CGHS-exclusive allopathic, ayurvedic, homeopathic and unani dispensaries) with some specialized treatment (with reimbursement ceilings) being permissible at private facilities.

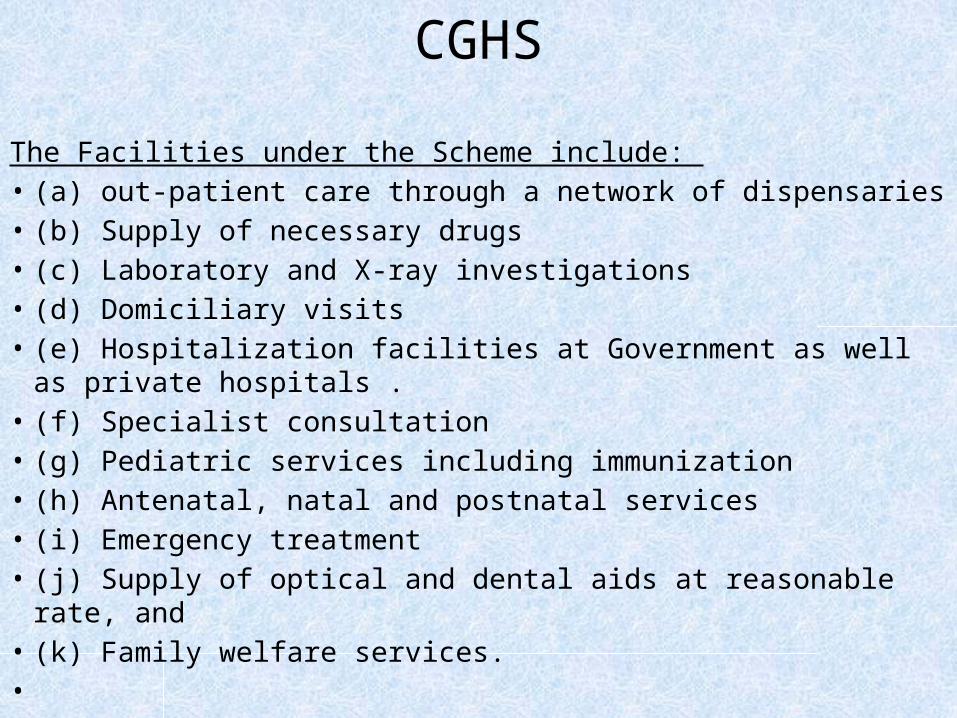

CGHS The Facilities under the Scheme include: • (a) out-patient care through a network of dispensaries • (b) Supply of necessary drugs • (c) Laboratory and X-ray investigations • (d) Domiciliary visits • (e) Hospitalization facilities at Government as well as private hospitals .• (f) Specialist consultation • (g) Pediatric services including immunization • (h) Antenatal, natal and postnatal services • (i) Emergency treatment • (j) Supply of optical and dental aids at reasonable rate, and • (k) Family welfare services. •

PRIVATE HEALTH INSURANCE

• Since the liberalization of the insurance industry in 2000 India has been promoting private players to enter the health insurance sector. With the enactment of the IRDA (Insurance regulatory authority of india), the industry now has a regulatory framework to protect the interests of policy holders.

• Some of the private are• Star health, reliance, ttk prestige, LIC, oreintal

Insurance,National insurance

STAR HEALTH

Third party administrators

THIRD PARTY ADMINISTRATORS

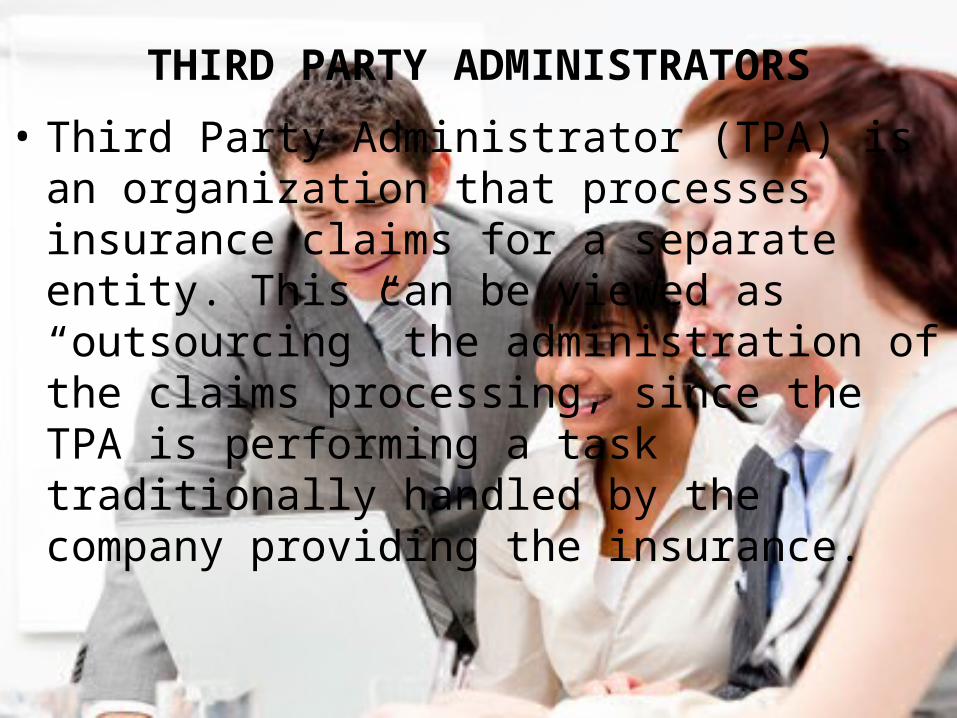

• Third Party Administrator (TPA) is an organization that processes insurance claims for a separate entity. This can be viewed as “outsourcing” the administration of the claims processing, since the TPA is performing a task traditionally handled by the company providing the insurance.

CONDITIONS FOR TPA’S

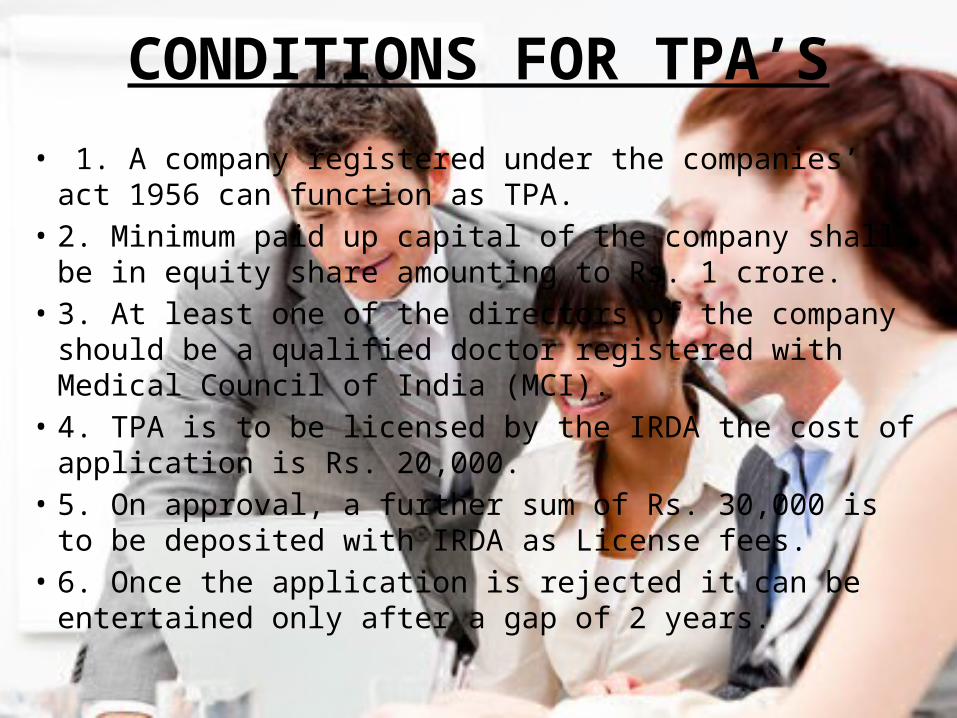

• 1. A company registered under the companies’ act 1956 can function as TPA.

• 2. Minimum paid up capital of the company shall be in equity share amounting to Rs. 1 crore.

• 3. At least one of the directors of the company should be a qualified doctor registered with Medical Council of India (MCI).

• 4. TPA is to be licensed by the IRDA the cost of application is Rs. 20,000.

• 5. On approval, a further sum of Rs. 30,000 is to be deposited with IRDA as License fees.

• 6. Once the application is rejected it can be entertained only after a gap of 2 years.

SERVICES OF TPA• 1.Benefit management: Designing tailor made

insurance scheme. • 2. Medical management: The TPAs tracks the line of

treatment & ensures genuine treatment. • 3. Issue of identity cards to the policy holders. • 4. Cashless hospitalization is ensured. • 5. Faster processing of claims.

• 6. Providing benefits like: a. Toll free telephone facility b. Provision of ambulance services c. Identification of hospital d. Attending to medical emergencies of insured persons e. Reducing work load of patients f. Quality of care g. Discounts h. Package pricing i. Priority appointments and admissions. j. Claim administration like documentation, coverage claim

submission and arranging payment for services provided.

BENEFITS OF TPA• 1. Admission to network hospital is beneficial because

one gets cashless insurance and not over charged by the hospital.

• 2. TPAs verify the treatment and ensure that the hospital charges are correct and at negotiated rates.

• 3. The TPAs are advantageous to health insurance companies also because they bring down the claims as a result of vigilant administration.

• 4. The TPAs scrutinize all the claims before settlement and can also guide patients for availing particular treatment as there are number of doctors among the employees of TPAs.

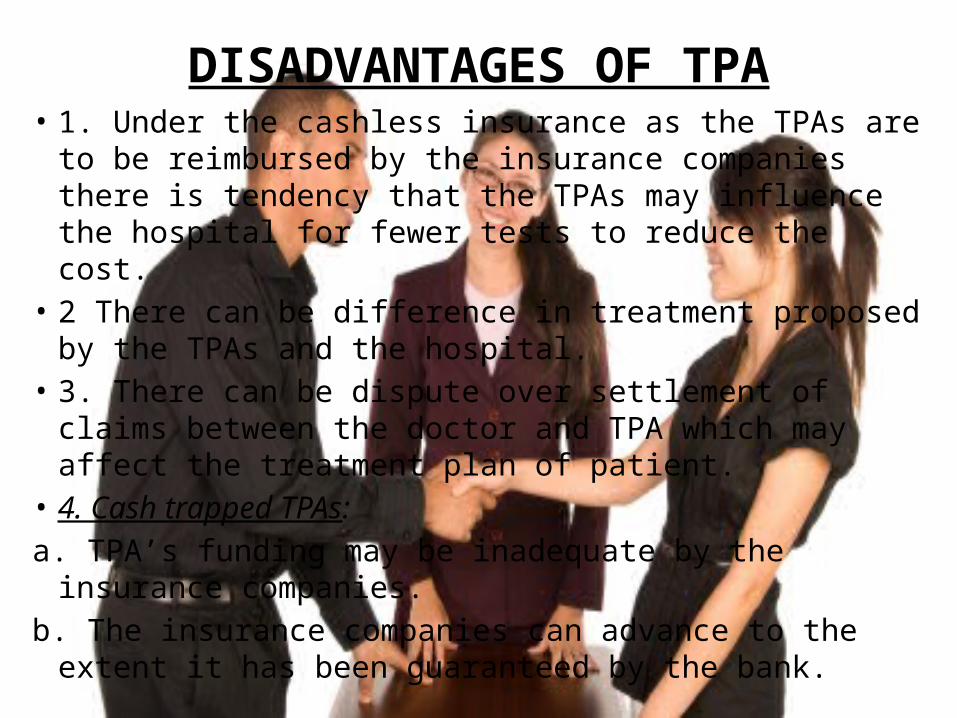

DISADVANTAGES OF TPA• 1. Under the cashless insurance as the TPAs are to be

reimbursed by the insurance companies there is tendency that the TPAs may influence the hospital for fewer tests to reduce the cost.

• 2 There can be difference in treatment proposed by the TPAs and the hospital.

• 3. There can be dispute over settlement of claims between the doctor and TPA which may affect the treatment plan of patient.

• 4. Cash trapped TPAs: a. TPA’s funding may be inadequate by the insurance companies. b. The insurance companies can advance to the extent it has

been guaranteed by the bank.

IRDA

IRDA• The IRDA was passed in December 1999 by Parliament.• The Act allows for the entry of private sector entities in

the Indian insurance sector, including health insurance, and envisages the creation of a regulatory authority.

• The IRDA is supposed to protect the interests of the policy-holders, promote efficiency in the conduct of insurance, regulate the rates and terms and conditions of the policies offered by insurers and direct the maintenance of solvency margins.

• The IRDA has wide powers for accounting and auditing insurers

COMPOSITION OF IRDA

• As per the Section 4 of IRDA Act’ 1999, Insurance Regulatory and Development Authority (IRDA. which was constituted by an act of parliament) specify the composition of Authority. The Authority is a ten member team consisting of:

• a. A Chairman; • b. Five whole-time members; • c. Four part-time members, (All appointed by the

Government of India).

Duties, Powers and Functions of IRDA • Subject to the provisions of this Act and any other law

for the time being in force, the Authority shall have the duty to regulate, promote and ensure orderly growth of the insurance business and reinsurance business.

• Issue to the applicant a certificate of registration, renew, modify, withdraw, suspend or cancel such registration.

• Protection of the interests of the policy holders in matters concerning assigning of policy, nomination by policy holders, insurable interest, settlement of insurance claim, surrender value of policy and other terms and conditions of contracts of insurance.

Duties, Powers and Functions of IRDA • Specifying the code of conduct for surveyors and loss

assessors. • Promoting efficiency in the conduct of insurance business. • Promoting and regulating professional organizations

connected with the insurance and re-insurance business. • Levying fees and other charges for carrying out the

purposes of this Act. • Regulating investment of funds by insurance companies.• Supervising the functioning of the Tariff Advisory

Committee

UNIVERSAL HEALTH INSURANCE SCHEME

UNIVERSAL HEALTH INSURANCE SCHEME- For providing financial risk protection to the poor, the

Government announced a UHIS in 2003. Under this scheme, for a premium of Rs 365 per year per person, Rs 548 for a family of five and Rs 730 for a family of seven, health care for an assured sum of Rs 30,000 was provided. BPL families were given a premium subsidy of Rs 200 per annum.

- The scheme was redesigned in May 2004 with higher subsidy and restricting eligibility to BPL families only. The subsidy was increased to Rs 200, Rs 300 and Rs 400 to individuals, families of five and seven, respectively.

- To make the scheme more saleable, the insurance companies provided for a floater clause that made any member of the family eligible as against the Mediclaim Policy which is for an individual member.

UHIS

• During 2004, the Government also provided an insurance product under which for a premium of Rs 120 the sum assured was Rs 10,000. This was, to be available only for self-help groups (SHG). However, the intake is reportedly negligible.

• The reasons for this poor intake are similar to those cited above. With the Common Minimum Programme (CMP) committed to having a UHIS, there has been much effort and debate to evolve a suitable and sustainable design.

• To expand the health insurance business, recommendations are also being made to reduce the minimum pre-qualification of Rs 100 crore equity as it will require 15 years to break even.

• Another set of recommendations is for permitting TPAs and hospitals to introduce health insurance products

COMMUNITY BASED HEALTTH INSURANCE

COMMUNITY BASED HEALTH INSURANCE

• In recent years, community health insurance (CHI) has emerged as a possible means of:

• (1) improving access to health care among the poor.• (2) protecting the poor from indebtedness and

impoverishment resulting from medical expenditures• CHI schemes involve prepayment and the pooling of

resources to cover the costs of health-related events. They are generally targeted at low-income populations, and the nature of the ‘communities’ around which they have evolved is quite diverse

HEALTH INSURANCE IN KERALA• The comprehensive Health Insurance scheme to benefit

entire Kerala was launched on October 2, 2008. Those who join the scheme will get benefit from December 1.

• The scheme will cover all the districts of the State. Government will distribute ‘Smart Cards’ to an estimated 22 lakh families expected to enroll in the scheme.

• It will cover 11.79 lakh BPL families as identified by the Planning Commission for inclusion in the centrally sponsored Rashtriya Swasthya Bima Yojana, around 10 lakh families additionally identified as BPL families by the State Government and APL families that are ready to pay the insurance premium amount

REASONS FOR POOR PENETRATION OF HEALTH INSURANCE

• Lack of regulations and control on provider behavior

• Unaffordable premiums and high claim ratios• Reluctance of the health insurance

companies to promote their products and lack of innovation

• Too many exclusions and administrative procedures.

• Inadequate supply of services• . Co-variate risks

CONCLUSION

• Insurance serves an important function in medical care. Having insurance does not protect a person against illness, but it can provide a measure of protection against the financial consequences of an illness

Thank you