guide to fha streamline refinances - merrimack … to fha streamlines - google...guide to fha...

TRANSCRIPT

Guide to FHA Streamline Refinances

By J.J. Sawicki, CMPAVP Third Party Lending/Merrimack Mortgage

What is a streamline refinance?The FHA streamline refinance has become an increasingly attractive option for FHA mortgage holders. It has been available since the 1980s for insured mortgages and those who want to refinance for a number of reasons.

"Streamline" refers to the reduced amount of paperwork and approval processes needed to receive refinancing on a current FHA mortgage. There are two types of FHA streamline refinances: without appraisal and with appraisal.

Streamline refinances are designed to lower the monthly principal and interest payments on a current FHA-insured mortgage and must involve no cash back to the borrower, except for minor adjustments at closing not to exceed $500. Streamline refinances can be made with or without an appraisal

Certain standards must be met to refinance with a FHA streamline mortgage. You may be able to refinance without appraisal. However, if your new payments will be higher than the previous payments, you will need to refinance with an appraisal and undergo all the necessary credit, employment, and income verifications. Verifications will also be needed if you refinance to remove a borrower from the previous mortgage, or if you assumed the mortgage without previous credit qualifications within a time period of 6 months.

Terms of a streamline refinanceTerms of a streamline refinance are:

● The existing mortgage must be FHA insured ● The property must be a primary residence● Borrower must have made at least 6 payments on the FHA insured mortgage. On the date of case assignment, at least 6

payments must have been made and six months from the first due date have elapsed and 210 days from the closing date have elapsed

● Cash cannot be withdrawn from the equity. The max incidental cash out is $500 ● Refinancing should be for the purpose of lowering monthly P&I and MIP by at least 5% or changing the amortization● Mortgage payments must be current, and a 12-month mortgage payment history will be assessed to make sure that no

payments have been late. Per FHA, 1x30 in the past 12 months is allowed as long as the past 3 months payments have been current. However, MMC does not allow any lates in the past 12 months

● The borrower must be current on the mortgage for the month due PRIOR to the closing month● No income, asset, or employment verifications are needed to qualify. But current employment must be verified via verbal

verification of employment and one paystub showing 30 days of earnings is required● Assets are only verified if they are needed for closing● Occupancy of a former investment property < 12 months prior to the application date is not allowed● The term of the mortgage is the lesser or 30 years of the remaining term of the mortgage plus 12 years

Mortgage Insurance Premiums

UFMIP = 1.75% (Streamline refis that were endorsed prior to 5/31/09 will see a decrease of UFMIP to .01% and the annual MIP is .55 effective 6/11/12)

Annual MIP effective 1/26/15 for cases endorsed > 6/1/09 with terms of >15 years:

UFMIP RefundsMIP Refund:Effective 12/8/04, the UFMIP is only refundable if the borrower refinances their current FHA mortgage to another FHA mortgage (streamline) within the first 3 years.When the mortgage is refinanced, the premium refund is netted against the new amount due on the refinanceLoans closed 1/1/01-12/7/04, the UFMIP is refundable within the first 5 yearsLoans closed < 1/1/01, the UFMIP is refundable within the first 7 years

When doing an FHA to FHA refinance, the refund will be applied to the UFMIP on the new loan● The existing loan must be >3 years old● The loan must not be assumed● If the lender filed a claim for losses on your loan, there will be no refund

FHA Streamline WITHOUT an Appraisal“Without an appraisal” means that no appraisal is needed on the property to establish value, and no credit evaluations are needed. This type of FHA streamline refinance is the most common and eliminates the need to re-qualify because of credit history. The lender WILL look for anything that may affect their lien position. Escrow accounts must be re-established when you settle the mortgage. Checklist for FHA Streamline Without an Appraisal:

● FHA Transmittal● Initial Application with HUD Addendum (1003) It is not necessary to disclose income, assets or debts. But list borrower’s employer and

occupation● Satisfactory Case Assignment (must show names and property address as the appear on current loan)● Refinance (Netting) Authorization● CAIVRS, LDP and GSA checks● Payoff statement from current lender. Please make sure the payoff identifies the escrow account balance held by the current lender (we

will need this information to transfer impounds and calculate escrow shortages).● Verification of Mortgage● Note and HUD-1 for old FHA loan - Must show old Case Number. If Payoff Statement shows this info plus the rate, it is acceptable in

lieu of the Note● FHA and applicable disclosures● Preliminary Title Report● Proof of social security number ● Tri-merged credit report with at least one FICO required and minimum 640 FICO

Calculating the loan amount without an appraisalThe maximum base mortgage cannot exceed:

● Unpaid principal balance plus the interest charged by the servicing lender when the payoff will not be received on the first day of the month, but may not include delinquent interest, late charges or escrow shortages MINUS

The lesser of: ● Unearned UFMIP (from FHA refinance Authorization or appropriate MIP Refund Schedule) OR ● New Estimated UFMIP

Total New Mortgage Amount ● Maximum base mortgage PLUS ● New UFMIP

**Closing costs, pre-paid expenses and discount points, late changes and escrow shortages may not be finance into the new loan.

Additional Requirements :● If subordinate financing is remaining in place, the maximum CLTV/HCLTV is 100% If a borrower wishes to subordinate an existing HELOC, the maximum credit limit

must be subordinated and must be considered in the HTLTV ● Determine the LTV/CLTV based on the original appraised value of the loan being refinanced. The value is taken from the FHA Connection Case Query Screen. MMC

will run the Case Query. A copy of the Case Query screen will be available for review by the DE Underwriter. ● Term of new mortgage is the lesser of 30 years or the un-expired term of the current mortgage plus 12 years. (This is particularly important when the term of the original

loan was 15 years) ● New secondary financing is not permitted. ● A subordination agreement will condition of loan approval ● No cash back to borrower permitted (incidental minor adjustment at closing not exceeding $500.00 cash back is acceptable). ● Refinance Authorization information will be obtained at Case Number Assignment directly from FHA Connection

FHA Streamline WITH an AppraisalFHA streamline refinancing with an appraisal is similar to that without an appraisal, but with this option, the new mortgage may exceed the original loan balance if the value comes in higher. The other difference between the two is that financing with appraisal requires an appraisal assessment of the property being refinanced and re-qualification for the mortgage is necessary. Credit, employment, and income requirements will be reassessed upon refinancing with a streamline with appraisal mortgage. When you take out a FHA streamline refinance mortgage with appraisal, all closing costs can be refinanced. On streamline refinances with an appraisal, Form HUD 92564-VC (Notice to Lender/Valuation Conditions) is required, but the Homebuyer Summary is not required. FHA does not require repairs to be completed (except for lead-based paint repairs) on streamline refinances with appraisals; however, the lender may require completion of repairs as a condition of the loan.Checklist for FHA Streamline With an Appraisal:

● FHA Transmittal● Initial Application with HUD Addendum (1003) ● Satisfactory Case Assignment● Refinance (Netting) Authorization● Payoff statement from current lender – Please make sure the payoff identifies the escrow account balance held by the current lender (we will need this

information to transfer impounds and calculate escrow shortages).● Verification of Mortgage ● Note and HUD-1 for old FHA loan – Must show old Case Number. If Payoff Statement shows this info plus the rate, it is acceptable in lieu of the Note● FHA and applicable disclosures● Preliminary Title Report● Appraisal and addendums● Proof of Social Security Number● Tri-merged credit report with at least one FICO required and minimum 640 FICO

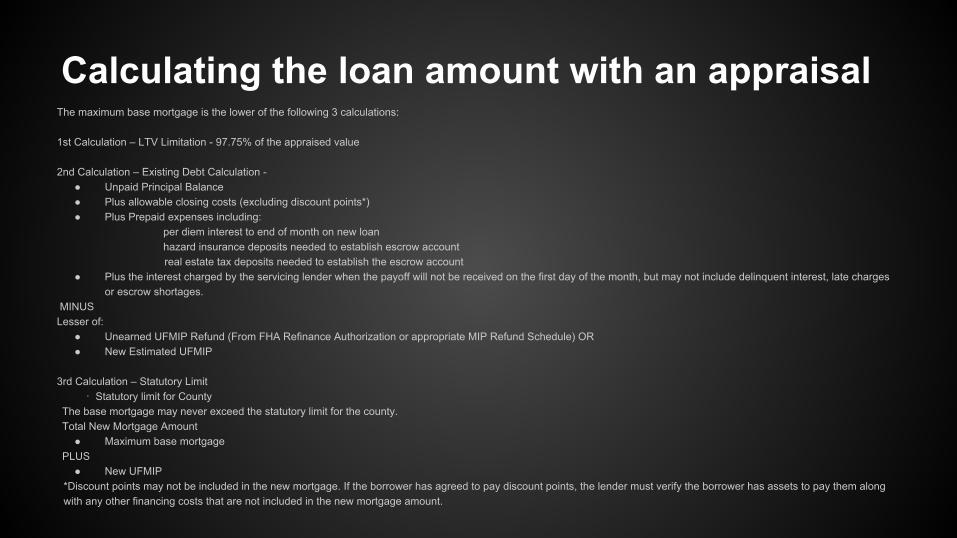

Calculating the loan amount with an appraisalThe maximum base mortgage is the lower of the following 3 calculations:

1st Calculation – LTV Limitation - 97.75% of the appraised value

2nd Calculation – Existing Debt Calculation - ● Unpaid Principal Balance ● Plus allowable closing costs (excluding discount points*) ● Plus Prepaid expenses including:

per diem interest to end of month on new loan hazard insurance deposits needed to establish escrow account

real estate tax deposits needed to establish the escrow account ● Plus the interest charged by the servicing lender when the payoff will not be received on the first day of the month, but may not include delinquent interest, late charges

or escrow shortages. MINUS Lesser of:

● Unearned UFMIP Refund (From FHA Refinance Authorization or appropriate MIP Refund Schedule) OR ● New Estimated UFMIP

3rd Calculation – Statutory Limit

· Statutory limit for County The base mortgage may never exceed the statutory limit for the county. Total New Mortgage Amount

● Maximum base mortgage PLUS

● New UFMIP *Discount points may not be included in the new mortgage. If the borrower has agreed to pay discount points, the lender must verify the borrower has assets to pay them along with any other financing costs that are not included in the new mortgage amount.

Calculating the loan amount with an appraisal (cont.)Additional Requirements

● Owner Occupied properties only ● New secondary financing is not permitted. ● May subordinate existing junior liens up to a maximum 100% CLTV/HCLTV. If a borrower wishes to subordinate

an existing HELOC, the maximum credit limit must be subordinated and must be considered in the HCLTV. ● A subordination agreement will be a condition of loan approval ● No cash back to borrower permitted except for minor adjustments at closing not exceeding $500.00 cash back. ● Refinance Authorization information will be obtained at Case Number Assignment directly from FHA Connection

and included in the loan file.

Net Tangible Benefitecond homes.

Adding or deleting individualsAdding or Deleting Individuals on Title. Individuals may be added to the title on a streamline refinance without creditworthiness review and without triggering due-on-sale clauses. Individuals can be deleted from the title on a streamline refinance only under the circumstances described in HUD 4155 Rev-5 Ch 1-12C or:

● When an assumption of a mortgage not containing a due-on-sale clause occurred more than six months previously and the assumptor can document that he or she has made the mortgage payments during this interim period; or

● Following an assumption of a mortgage in which the transferability restriction (due-on-sale clause) was not triggered, such as in a property transfer resulting from a divorce decree or by devise or descent, and the assumption or quit-claim of interest occurred more than six months previously and the remaining owner-occupant can demonstrate that he or she has made the mortgage payments during this time.

Exceptions are allowed in the following cases:

● Divorce○ Remaining spouse must have been on title by themselves for at least 6 months○ Provide a copy of the final divorce decree○ Provide 6 months cancelled checks proving they’ve been making the payments on their own

● Death○ Provide the original death certificate○ Provide 6 months cancelled checks proving they’ve been making the payments on their own

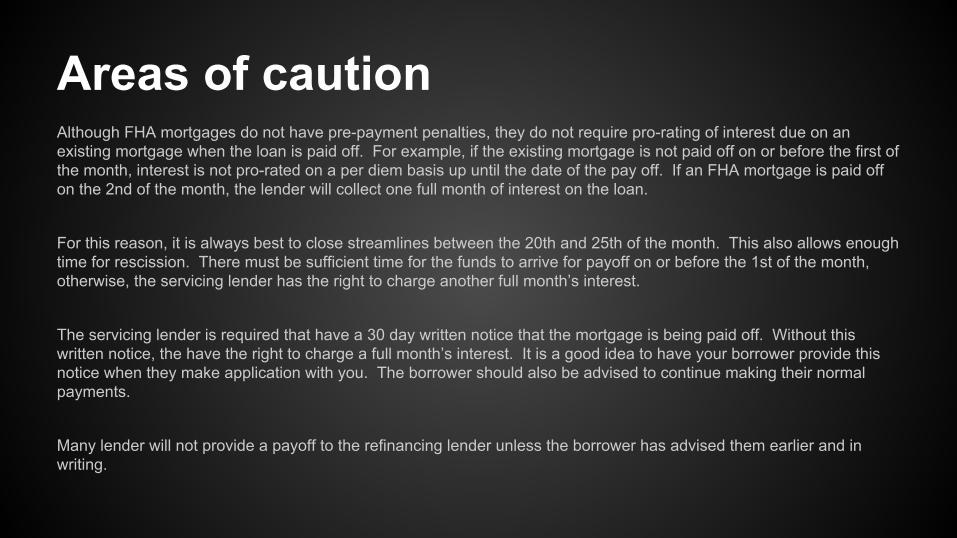

Areas of cautionAlthough FHA mortgages do not have pre-payment penalties, they do not require pro-rating of interest due on an existing mortgage when the loan is paid off. For example, if the existing mortgage is not paid off on or before the first of the month, interest is not pro-rated on a per diem basis up until the date of the pay off. If an FHA mortgage is paid off on the 2nd of the month, the lender will collect one full month of interest on the loan.

For this reason, it is always best to close streamlines between the 20th and 25th of the month. This also allows enough time for rescission. There must be sufficient time for the funds to arrive for payoff on or before the 1st of the month, otherwise, the servicing lender has the right to charge another full month’s interest.

The servicing lender is required that have a 30 day written notice that the mortgage is being paid off. Without this written notice, the have the right to charge a full month’s interest. It is a good idea to have your borrower provide this notice when they make application with you. The borrower should also be advised to continue making their normal payments.

Many lender will not provide a payoff to the refinancing lender unless the borrower has advised them earlier and in writing.

Areas of caution (cont.)Because lenders tend to calculate payoffs differently, care should be taken when the payoff is received to identify the principal balance of the loan and work from the amount to make the final calculation of the new mortgage. If escrow balances have been applied, they can be credited to the borrower on the HUD (lines 204 and 205) and should be identified as “escrows balances from previous lender”.

In the event that the lender does not credit the borrower for escrows, and makes a refund directly to the borrower after receiving the payoff on the existing loan, the borrower will need to establish new escrows at the time of closing and will be reimbursed for a portion of the escrow upon receipt of these funds.

Additional InformationAppraisal and Termite Inspection. We do not require an appraisal or termite inspection. However, the associated fees may be paid by the borrower out-of-pocket (i.e., not financed) if law, banking regulations, or its secondary market investors require the lender to obtain these services on a streamline refinance made without a FHA appraisal.

Cash-to-Close. Borrowers are not required to provide evidence of cash-to-close unless cash to close is needed.

Withdrawn Condominium Approvals. If approval of a condominium project has been withdrawn, FHA will insure only streamline refinances without appraisals for that condominium project.

"No-Cost" Refinances. "No-cost" refinances, in which the lender charges a premium interest rate to defray the borrower's closing costs and/or prepaid items, are permitted. The lender may also offer an interest-free advance of amounts equal to the present escrow balances on the existing mortgage to establish a new escrow account.

Holding Period before Eligibility. A borrower who assumed or took title subject to an FHA-insured mortgage, without being credit qualified and with the previous mortgagors receiving a release of liability, must have owned the property for at least six months before being eligible for the streamline refinance program without credit qualifying. This rule applies to mortgages that do not contain restrictions limiting the assumption only to creditworthy assumptors. Typically those mortgages were made prior to December 1989.

Seven-Unit Exemptions. An eligible investor that has a financial interest in more than seven rental units, as described in 24 CFR 203.42, may only refinance without appraisals. Subordinate Financing. Subordinate financing may remain in place, to a max 100% CLTV, against the property on streamline refinances, with or without appraisals. The borrower is not required to satisfy any outstanding subordinate liens, as long as they will clearly be subordinate to the new FHA-insured refinance mortgage to the max CLTV. Proceeding as if No Appraisal was Completed. If the appraised value is such that the borrower would be better advised to proceed as if no appraisal had been made, the appraisal may be ignored and not used

Additional Information (cont.) ARM to ARM. An ARM may be refinanced to another ARM, provided that an immediate payment reduction occurs and that the maximum interest rate of the new mortgage does not exceed the maximum interest rate of the old mortgage being refinanced. These refinances may be transacted with or without an appraisal. ARM to Fixed Rate. An ARM may be refinanced to a fixed-rate mortgage, with or without an appraisal, provided the interest rate on the new fixed-rate mortgage will be no greater than 2 percentage points above the current rate of the ARM. In addition, all mortgage payments must have been made within the month due for the past 12 months or the period the mortgage has been in force, if shorter. If the new fixed-rate mortgage will be at a rate lower than the existing rate of the ARM thus reducing the homeowner's monthly mortgage payment, the "within the month due," (i.e., not more than 30 days late), rule is not applicable. Fixed-Rate to ARM. Fixed-rate mortgages may be refinanced to a one-year ARM, with or without an appraisal, provided the interest rate of the new mortgage is at least 2 percentage points below the interest rate of the current mortgage.

203(k) to 203(b). 203(k) loans may be refinanced into a 203(b) loan after all work is complete. The rehabilitation work is considered complete by a fully executed certificate of completion, the rehabilitation escrow account has been closed with a final release, and the lender has entered the required close out information into the FHA Connection or its functional equivalent. The new mortgage will be subject to the appropriate insurance premium applicable to a new 203(b) mortgage.

Section 235 to Section 203(b). Lenders may refinance Section 235 mortgages to Section 203(b) mortgages using the streamline underwriting procedures described in paragraph 1-12. Any overpaid subsidy that has been paid by the lender to HUD and is part of the borrowers' mortgage account can be included in the Section 203(b) mortgage amount, provided the mortgage amount does not exceed the maximum mortgage permitted under paragraphs 1-12 A or 1-12 B as appropriate. Furthermore, if HUD has a junior lien that was part of the original Section 235 financing, HUD will subordinate the junior lien to the Section 203(b) mortgage that refinances the Section 235 mortgage. Too much cash at closing? This is not something that can be resolved with a principal reduction, so be prepared!