fha 203k streamline. why fha 203k streamline? through the fha 203k streamline program, borrowers can...

TRANSCRIPT

FHA 203K StreamlineFHA 203K Streamline

Why FHA 203K Streamline?Why FHA 203K Streamline?

Through the FHA 203K Streamline program, borrowers can purchase or refinance their home and include the costs to renovate and repair the

home in the same loan.

If you need work done to a home and have no equity available,If you need work done to a home and have no equity available,THIS IS THE PROGRAM FOR YOU!THIS IS THE PROGRAM FOR YOU!

Target MarketsTarget Markets

Borrowers purchasing a home in need of renovationBorrowers purchasing a home in need of renovation- REOs, Foreclosures and Short Sales- Incomplete Renovations

Borrowers refinancing existing homeBorrowers refinancing existing home- Improve instead of move- Out-Dated Kitchens, Bathrooms, etc…

Program HighlightsProgram Highlights

Up to 96.50% LTV For Purchases

97.75% Maximum LTV on Rate & Term Refinances

640 Minimum FICO

Finance up to $35,000 in Renovations Costs

Program HighlightsProgram Highlights

All Work Must be Done by a qualified, and experienced, contractor

Can Not be Used for Structural Improvements or Repairs

Same Underwriting logic as a Standard FHA Loan

ImprovementsImprovements

Improvements are eligible as long as they become aImprovements are eligible as long as they become apermanent part of the property and add value, for instance:permanent part of the property and add value, for instance:

- Roofs, gutters & downspouts- Heating and Air Conditioning- Upgrade/Repair plumbing, septic, well and electrical- Replacement of flooring, windows, doors and siding- Weatherization, painting, basement waterproofing- Purchase and installation of appliances- Elimination of Health and Safety Hazards

ImprovementsImprovements

Luxury Items Are Not EligibleLuxury Items Are Not Eligible

- Swimming pools & Hot Tubs- Tennis Courts- Gazebos- Barbecue Pits- Structural Changes

Determining the ValueDetermining the Value

The LTV is based on the lesser of:

- The Sales Price or “As Is” Appraised Value PLUS the total renovation costs, or

- 110% of the “After Improved” Appraised Value (includes all work done)

PurchasePurchase

Determining Max Loan Determining Max Loan AmountAmount

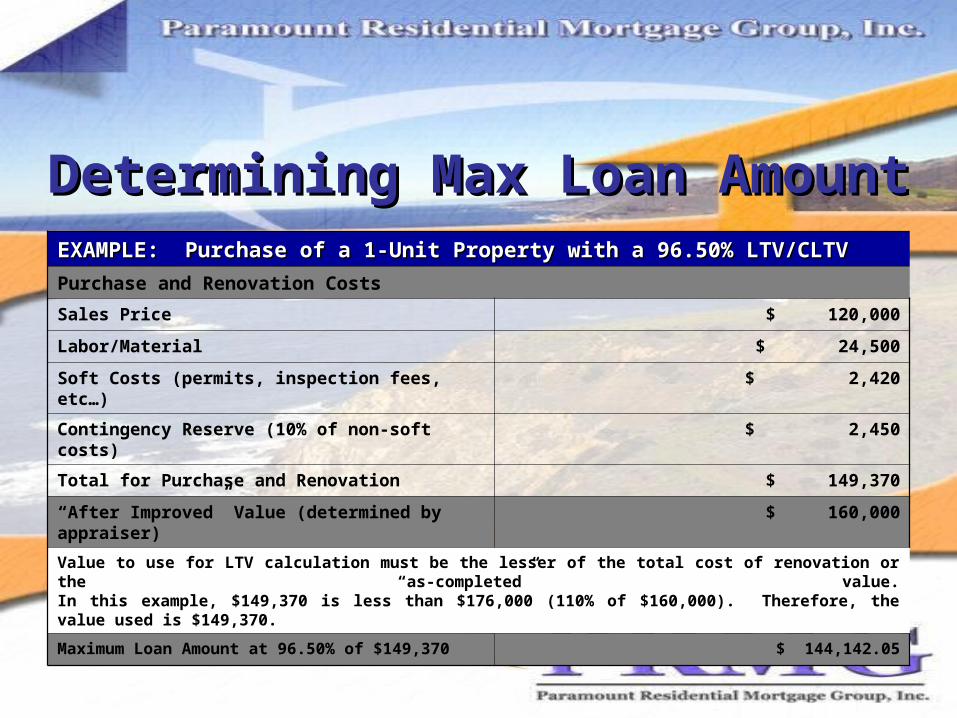

EXAMPLE: Purchase of a 1-Unit Property with a 96.50% LTV/CLTVEXAMPLE: Purchase of a 1-Unit Property with a 96.50% LTV/CLTV

Purchase and Renovation Costs

Sales Price $ 120,000

Labor/Material $ 24,500

Soft Costs (permits, inspection fees, etc…) $ 2,420

Contingency Reserve (10% of non-soft costs) $ 2,450

Total for Purchase and Renovation $ 149,370

“After Improved” Value (determined by appraiser) $ 160,000

Value to use for LTV calculation must be the lesser of the total cost of renovation or the “as-completed” value.In this example, $149,370 is less than $176,000 (110% of $160,000). Therefore, the value used is $149,370.

Maximum Loan Amount at 96.50% of $149,370 $ 144,142.05

Determining the ValueDetermining the Value

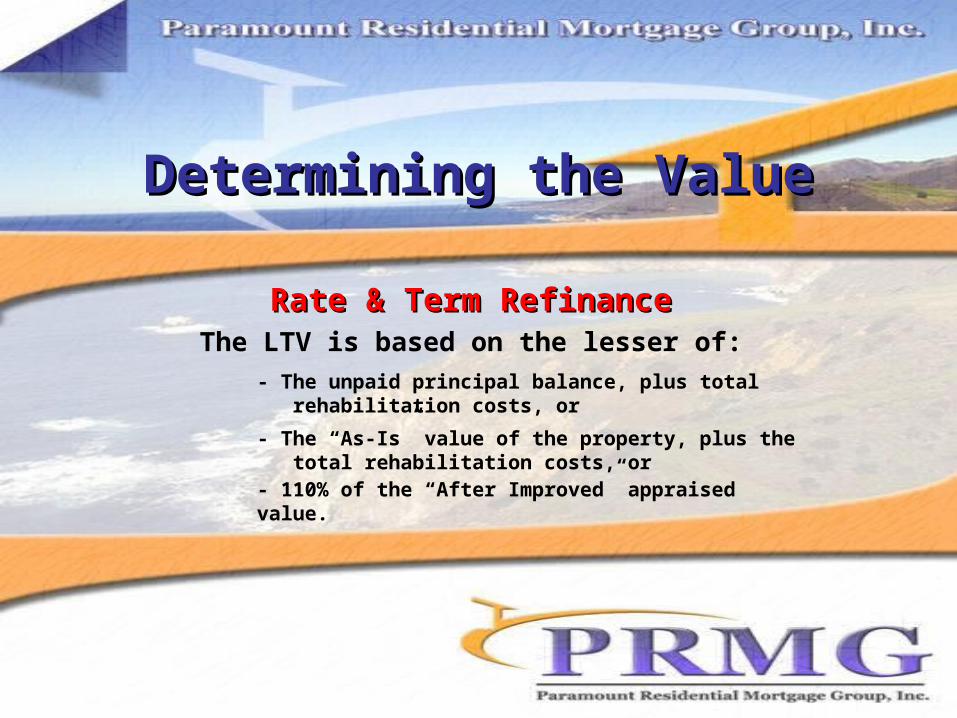

The LTV is based on the lesser of:

- The unpaid principal balance, plus total rehabilitation costs, or

- The “As-Is” value of the property, plus the total rehabilitation costs, or

Rate & Term RefinanceRate & Term Refinance

- 110% of the “After Improved” appraised value.

Determining Max Loan Determining Max Loan AmountAmount

EXAMPLE: Refinance of a 1-Unit Property with a 97.75% LTV/CLTVEXAMPLE: Refinance of a 1-Unit Property with a 97.75% LTV/CLTV

Purchase and Renovation Costs

Unpaid Principal Balance $ 120,000

“As-Is” Appraised Value (determined by appraiser) $ 130,000

Labor/Material $ 24,500

Soft Costs (permits, inspection fees, etc…) $ 2,420

Contingency Reserve (10% of non-soft costs) $ 2,450

Total for Unpaid Principal and Renovation $ 149,370

“After Improved” Value (determined by appraiser) $ 160,000

Value to use for LTV calculation must be the lesser of the Unpaid Principal + Renovation, the “As-Is” Appraised Value + Renovation, or 110% of the “After Improved Appraised Value. In this example, UP+R = $149,370,AIV+R = $159,370 and 110% of AIV = $176,000. Therefore the value used for LTV/CLTV calculation is $149,370.

Maximum Loan Amount at 97.75% of $149,370 $ 146,009.17

Draw ProcessDraw Process

Within 30 days after loan funding, 50% of the funds are disbursed.

Included with the disbursement is an instruction letter that explains how the final disbursement works.

The remainder of the funds is disbursed once ALL work is complete.

Inspections (or Certificates from Municipalities), to verify the work, may be required depending on the number of contractors working on the renovations.

Contingency ReserveContingency Reserve

10% of the cost of renovation must be put into a Contingency Reserve.(15% if utilities are not on, or if property is vacant)

The Contingency Reserve is used to cover health, safety and unplanned issues that arise during the renovation process.

If not used (after all construction is complete) the remaining amount can be applied to the principal or used to make other improvements

(additional approval is required).

Document ChecklistDocument Checklist

GFE DisclosureGFE Disclosure

Fees must be properly disclosed on the GFE

A Supplemental Origination Fee is to be included in Block 1 of the GFE:1.50% of the renovation amount, or $350, whichever is more

(recommend disclosing the max $525).

Inspections and Title Updates:Disclose a minimum of 1 each; Inspection - $110 and Title - $150

Change of Circumstance can be done when bid is received and more thanone inspection is required.

Helpful HintsHelpful Hints

Make sure that ALL parties understand the draws, how they happen and when they happen.

Title must be clear before final payment is made.

The most common cause for a delay in draw is missing a W-9.

Questions?Questions?

Let’s go get some Let’s go get some Loans!Loans!