growth strategies for greece and cyprus - lse home...growth strategies for greece and cyprus twitter...

TRANSCRIPT

Speakers:

Gikas Hardouvelis, Professor of Finance and Economics, University of Piraeus in Greece

Sir Christopher Pissarides, Regius Professor of Economics, LSE; Professor of European Studies, University of Cyprus

Constantinos Petrides, Minister of Interior, Cyprus

Dimitri Vayanos, Professor of Finance, LSE

Hosted by the Hellenic Observatory & School of Economics & Management, University Of Cyprus

Chair: Vassilis MonastiriotisAssociate Professor of Political Economy, LSE

Growth strategies for Greece and Cyprus

Twitter Hashtag: #LSECyprus

Reform Priorities and Outlook for Greece

Dimitri Vayanos, London School of Economics

University of Cyprus, 27 November 2018

The Book

• Website of English Edition: https://mitpress.mit.edu/books/beyond-austerity

• Website of Greek Edition: https://www.cup.gr/book/pera-apo-ti-litotita/

• Financial support by the LSE Hellenic Observatory is gratefully acknowledged

Chapters and Contributors

1. The Greek Economy 2. Greece and the Euro 3. Trade Balance

4. Product Markets 5. Privatizations 6. Labor Market 7. Financial System

8. Education 9. Healthcare 10. Taxation 11. Pensions

12. Justice System 13. Corruption 14. Public Administration Ι 15. Public Administration ΙΙ

D. Vayanos N. VettasC. Meghir C. Pissarides G. M. Angeletos H. Dellas C. Arkolakis M. GalenianosA. Doxiadis

Κ. Meghir M. Haliassos

Ν. Vettas M. Haliassos

Y. Katsoulacos C. Genakos G. Houpis V. Skreta Α. Lyberaki D. Nicolitsas M. Tsoutsoura D. VayanosG. Hardouvelis

P. Kanavos Κ. Souliotis C. Kotsogiannis C. MeghirM. Flevotomou S. Panageas P. Tinios

E. Papaioannou S. Karatza C. Azariadis Y. Ioannides M. Jacobides P. Karkatsoulis Ε. Stefopoulou

Structural Reforms in Greece—Improvements So Far

• Labour market.• Significant deregulation of a formerly over-regulated labor market.

• Product markets.• Significant deregulation and reduction of barriers to entry.

• Pensions.• Unification of a highly fragmented pension system.• Viability achieved through significant pension cuts.

• Tax administration.• Establishment of independent tax collection authority.• Fully electronic filing.

Structural Reforms in Greece—Priorities Going Forward• Reduce tax burden on productive activity.

• Move to a flat tax system, with a minimum guaranteed income and possibly EITC. • More emphasis on consumption taxes, and less on income and corporate taxes.• Multi-pillar pension system, with tight link between contributions and pensions.

• Enhance competition in product markets.• Abolish more barriers to entry. Strengthen competition authorities.• Use privatizations as a tool to enhance competition. (Not only to maximize revenue)• Facilitate NPL resolution, via bankruptcy laws and bad bank.

• Make public administration more efficient and independent.• Enshrine independence between public administration and political system.• More autonomy to organizational units (schools, universities, hospitals, courts).• More performance measurement and incentives.

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1995 2000 2005 2010 2015

Efficiency of the Public Administration

Governance Indicators, World Bank (Government Effectiveness Index)

Dependence on politicians: Quality of Government Indicators, University of Gothenburg, 2015 (“the top political leadership hires and fires senior public officials”). Efficiency of public administration: Governance Indicators, World Bank, 2015 (Government Effectiveness Index). OECD countries.

0.00

0.50

1.00

1.50

2.00

2.50

1 2 3 4 5 6 7

Effi

cien

cy o

f th

e P

ub

lic A

dm

inis

trat

ion

Dependence on Politicians

Outlook for Greece

• Limited progress, and backtracking, on many reform areas.• Greece is sliding back in competitiveness rankings, e.g., Doing Business.

• Europeans (in IMF’s absence) are turning a blind eye.

• If growth remains anaemic, a new bailout programme is likely in a few years.• Cash buffer can carry Greece for a few years.

• Market access is conditional on expectations of future growth.

Growth or Stagnation

Ahead?

Cyprus vs. Greece

Prof. Gikas Hardouveliswww.hardouvelis.gr

www.hardouvelis.com

Conference on “Growth strategies for Greece and Cyprus,” organized by The Hellenic Observatory, London School of Economics and Political Sciences

& The School of Economics and Management, University of Cyprus Nicosia, Cyprus, November 27, 2018, 18:00

University of Cyprus, Aglantzia Campus, Leventis Building , Amphitheatre B108

TABLE OF CONTENTS

Growth or Stagnation Ahead? Cyprus vs. Greece

I. A different economic trajectory following the crisis

II. The challenge of achieving lasting growth

2Gikas A. Hardouvelis

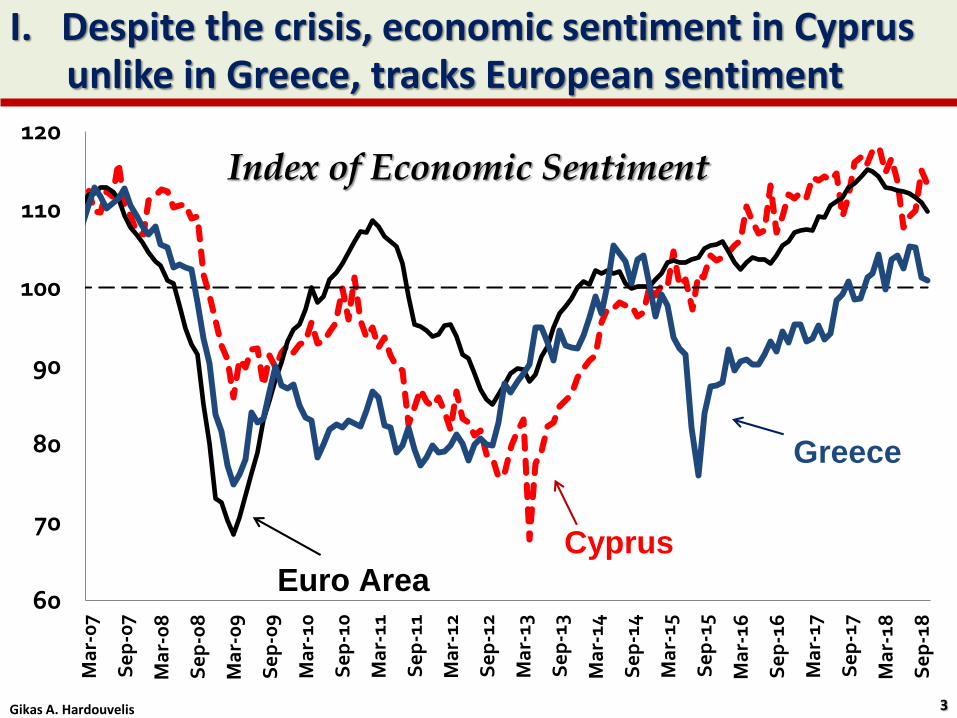

I. Despite the crisis, economic sentiment in Cyprusunlike in Greece, tracks European sentiment

60

70

80

90

100

110

120

Mar-07

Sep-07

Mar-08

Sep-08

Mar-09

Sep-09

Mar-10

Sep-10

Mar-11

Sep-11

Mar-12

Sep-12

Mar-13

Sep-13

Mar-14

Sep-14

Mar-15

Sep-15

Mar-16

Sep-16

Mar-17

Sep-17

Mar-18

Sep-18

Cyprus

Euro Area

Greece

Index of Economic Sentiment

3Gikas A. Hardouvelis

I. Small output loss and quick recovery in Cyprus, huge loss and continued stagnation in Greece

70

75

80

85

90

95

100

105

110

T0

T+

1T

+2

T+

3T

+4

T+

5T

+6

T+

7T

+8

T+

9T

+10

T+

11

T+

12

T+

13

T+

14

T+

15T

+16

T+

17

T+

18

T+

19

T+

20

T+

21

T+

22

T+

23

T+

24

T+

25

T+

26

T+

27

T+

28

T+

29

T+

30

T+

31

T+

32

T+

33

GREECE (2010Q1=100)

CYPRUS (2012Q2=100)

Cumulative GDP change

-22.2% from T0

in 15 Quarters

-22.6% from T0

in 22 Quarters

-7.9% from T0

in 9 Quarters

From 2007 Q4 to T0 Greece lost

another 5.6%Cyprus lost

another 1.0 %

Source: Eurostat, Gkionis-Hardouvelis

4Gikas A. Hardouvelis

T0 is the moment just before an MoUbegan

Lost output growth due to Crisis Phase II

I. Unemployment declines fast in Cyprus, now less than when crisis started

-5

0

5

10

15

20

T0

T+

1T

+2

T+

3T

+4

T+

5T

+6

T+

7T

+8

T+

9T

+10

T+

11

T+

12

T+

13

T+

14

T+

15

T+

16

T+

17

T+

18

T+

19

T+

20

T+

21

T+

22

T+

23

T+

24

T+

25

T+

26

T+

27

T+

28

T+

29

T+

30

T+

31

T+

32

T+

33

GREECE 2010Q1=100

CYPRUS 2012Q2=100

Source: Eurostat, Gkionis-Hardouvelis

ppts Cumulative Change in Unemployment Rate

Complete correction after 5 years in Cyprus

From 2007 to T0 Greece lost another 3.2%(8.1 →11.3)

Cyprus lost another 7.9%(3.8 → 11.7)

5Gikas A. Hardouvelis

0.10

0.15

0.20

0.25

0.302

000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

20

13

20

14

2015

2016

2017

20

18E

2019F

2020F

GREECE

CYPRUS

EA19

Investment – Output Ratio

6Gikas A. Hardouvelis

I. Investment picks up in Cyprus, not in GreeceO

ptim

istic Gre

ek fo

recastsSource: Eurostat, Gkionis-Hardouvelis

0

500

1000

1500

2000

2500

3000

3500

4000Ja

n-1

0

Ap

r-1

0

Jul-

10

Oct

-10

Jan

-11

Ap

r-1

1

Jul-

11

Oct

-11

Jan

-12

Ap

r-1

2

Jul-

12

Oct

-12

Jan

-13

Ap

r-1

3

Jul-

13

Oct

-13

Jan

-14

Ap

r-1

4

Jul-

14

Oct

-14

Jan

-15

Ap

r-1

5

Jul-

15

Oct

-15

Jan

-16

Ap

r-1

6

Jul-

16

Oct

-16

Jan

-17

Ap

r-1

7

Jul-

17

Oct

-17

Jan

-18

Ap

r-1

8

Jul-

18

Oct

-18

SPREADS GREECE VS GERMANY

SPREADS CYPRUS VS GERMANY

Source: Bloomberg

I. Markets are willing to lend to Cyprus, spreads consistently lower than Greek spreads

7Gikas A. Hardouvelis

Nov. 23,2018GGB 10-yr 4.8%CGB 10-yr 2.4%

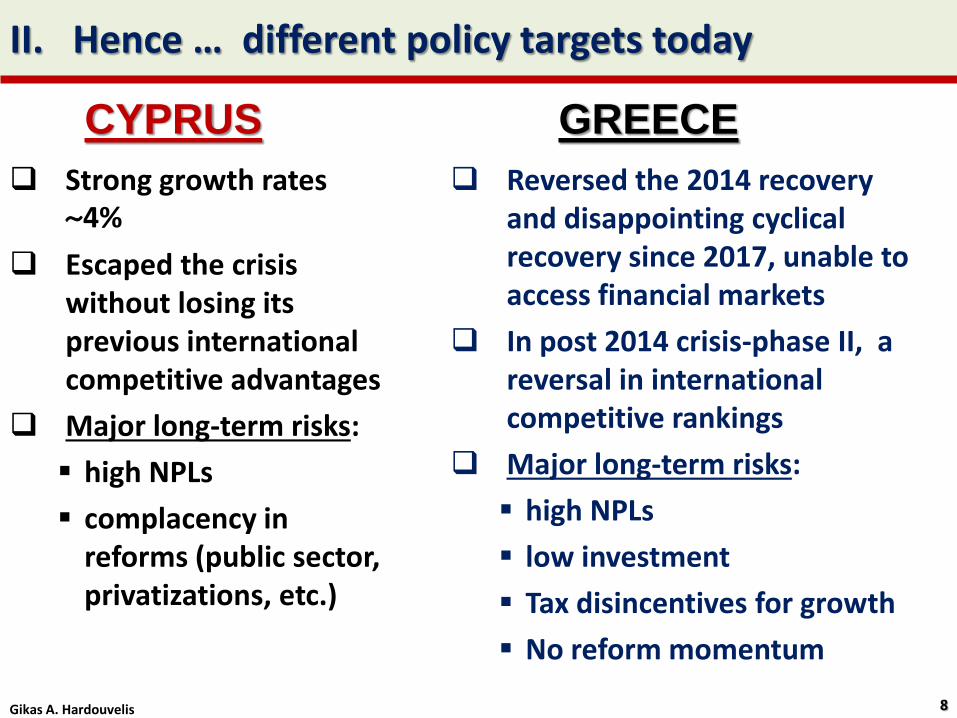

II. Hence … different policy targets today

Strong growth rates ~4%

Escaped the crisis without losing its previous international competitive advantages

Major long-term risks:

high NPLs

complacency in reforms (public sector, privatizations, etc.)

Reversed the 2014 recovery and disappointing cyclical recovery since 2017, unable to access financial markets

In post 2014 crisis-phase II, a reversal in international competitive rankings

Major long-term risks:

high NPLs

low investment

Tax disincentives for growth

No reform momentum

CYPRUS GREECE

8Gikas A. Hardouvelis

ΙΙ. Non-Performing loans: The elephant in the room

9

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

GR CY PT IT BG HR SI IE HU PL RO ES LV EU MT AT FR SK LT IS DK NL BE EE DE GB CZ NO FI SE LU

Non-Performing Exposures

(% Loans)

2018Q2

Source: European Banking authority

Huge NPE problem in Greece & Cyprus

Due to a fiscal crisis in Greece and to a recession later

Due to a banking crisis in Cyprus

Portugal, Italy next but below 10%

Gikas A. Hardouvelis

II. Other key indicators today

ConditionsGreece

2018

Cyprus

2018

Primary Balance (% GDP, ESA2010) 3.9 5.5

General Gov. Balance (% GDP) 0.6 2.8

Gross Public Debt (% GDP) 182.5 105

Current Account Balance (% GDP, 3-yr average)

-0.8 -5.0

Ease of Doing Business 68.08 71.71

REER (ULC total economy deflated,

1999Q1 = 100, 3-yr % change)-2.8 -6.6

Private Sector Debt (% GDP, 2017) 116.4 316.3

Banks Assets (% of GDP, 2018-H1) 132 336

1) Fiscal statistics: Deficit OK in both countries , Debt is high in Greece2) Competitiveness statistics: No problem yet3) Financial sector statistics: Cyprus more exposed to a shock

10Gikas A. Hardouvelis

II. Revealing Doing Business competitive rankings

11Gikas A. Hardouvelis

170 countries

II. Revealing Doing Business competitive rankings

12Gikas A. Hardouvelis

CYPRUS

GREECE

II. Revealing Doing Business competitive rankings

13Gikas A. Hardouvelis

2018 Greece Cyprus

Overall Score DTF 68.08 71.71

Starting a business 92.39 91.24

Dealing with construction permits 75.29 64.08

Getting electricity 75.97 78.35

Registering property 47.59 63.46

Getting credit 50.00 60.00

Protecting minority investors 63.33 66.67

Paying taxes 76.89 80.78

Trading across borders 93.72 88.44

Enforcing contracts 50.19 48.59

Resolving insolvency 55.39 75.45

1. Safeguard macroeconomic stability, ensure pension system is solvent

2. Clean up the banking system

3. Keep up the reform effort

Gikas A. Hardouvelis 14

ΙΙ. Concluding recipe for persistent growth

Thank youfor your attention!

www.hardouvelis.grwww.hradouvelis.com

Greece and Cyprus: Are we embarking on sustainable

growth?Christopher Pissarides

University of Cyprus and London School of Economics

University of Cyprus panel discussion, 27 November 2018

Where are we?

• Lots of progress has been made since the crash – more in Cyprus than in Greece

• We are almost out of the woods in macro aggregates

• But investment still very low, productivity stalling

• Employment improved but has not yet recovered

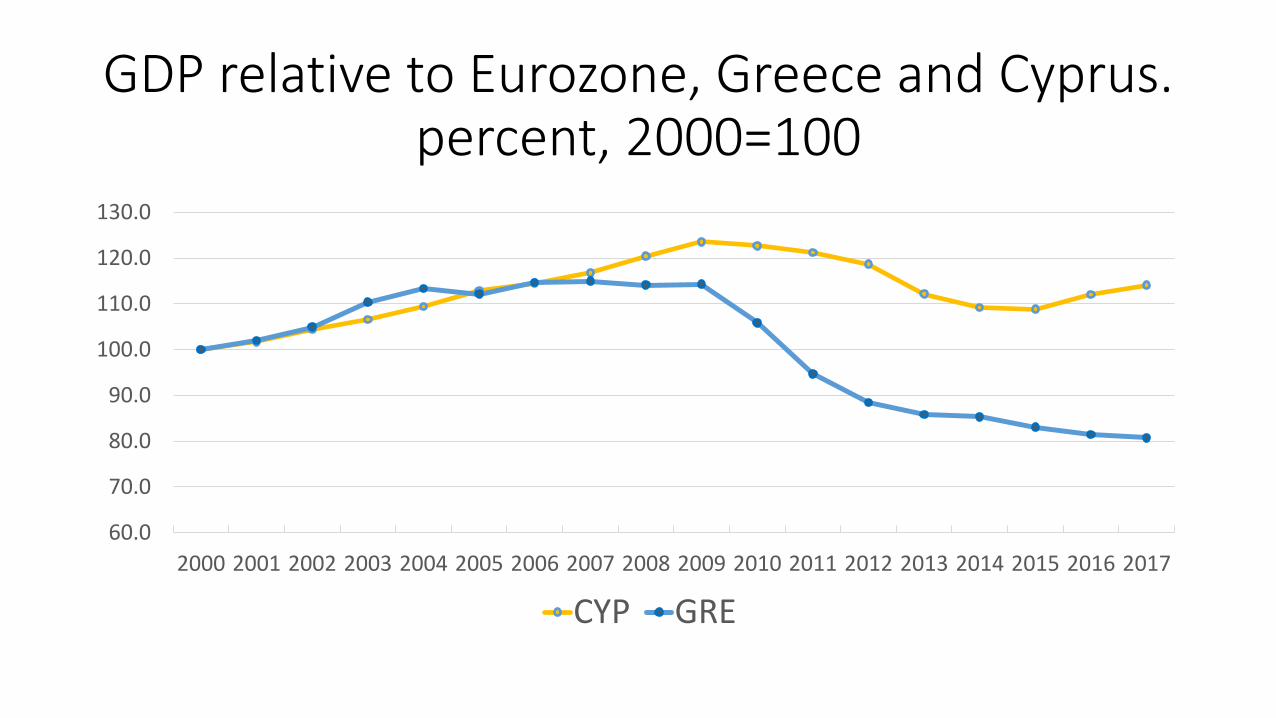

GDP relative to Eurozone, Greece and Cyprus.percent, 2000=100

60.0

70.0

80.0

90.0

100.0

110.0

120.0

130.0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

CYP GRE

Consumption, % GDP

60.0

62.0

64.0

66.0

68.0

70.0

72.0

74.0

76.0

78.0

80.0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

GRE CON CYP CON

Investment, % of GDP

0

5

10

15

20

25

30

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

GRE INV CYP INV

Labour productivity at current prices

0

1000

2000

3000

4000

5000

6000

7000

8000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

EUR 19 GRE CYP

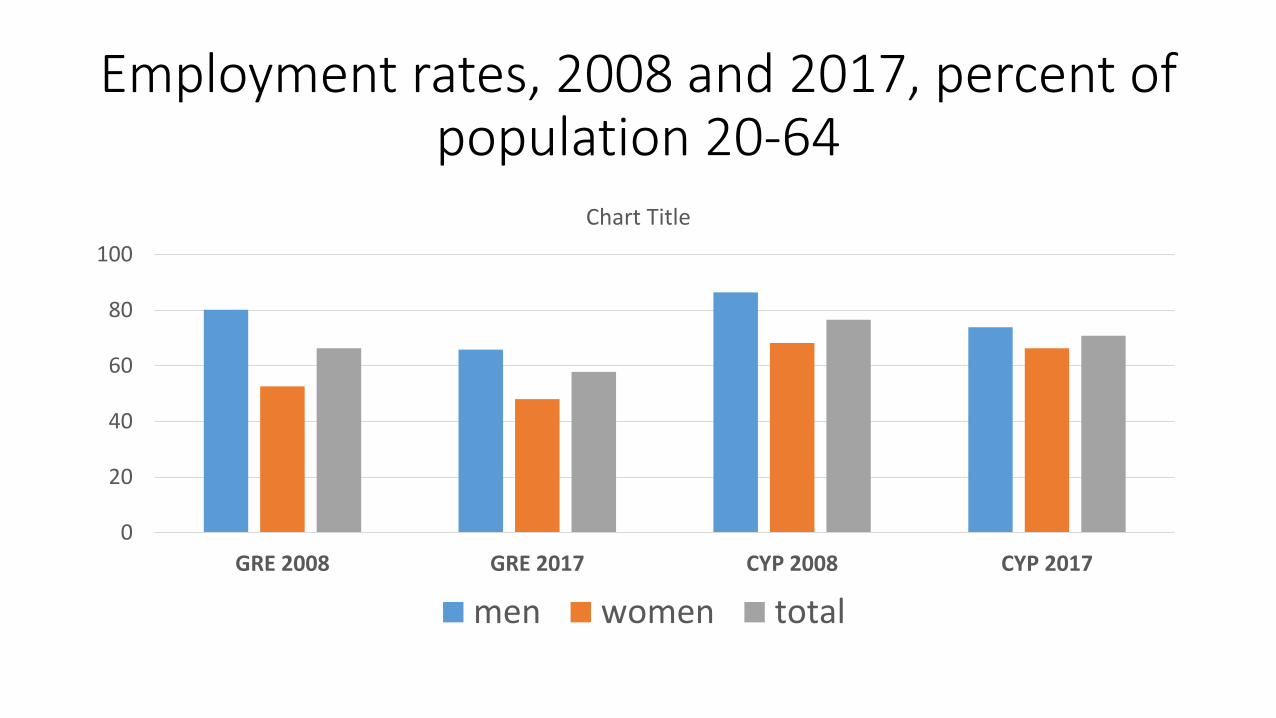

Employment rates, 2008 and 2017, percent of population 20-64

0

20

40

60

80

100

GRE 2008 GRE 2017 CYP 2008 CYP 2017

Chart Title

men women total

Sustainable growth

• New theories of growth emphasize the importance of institutions and politics in generating sustainable growth

• Both Cyprus and Greece doing very badly in institutional reform

• Worst in the European Union, and red tape is deteriorating

• Corruption prevalent, especially political

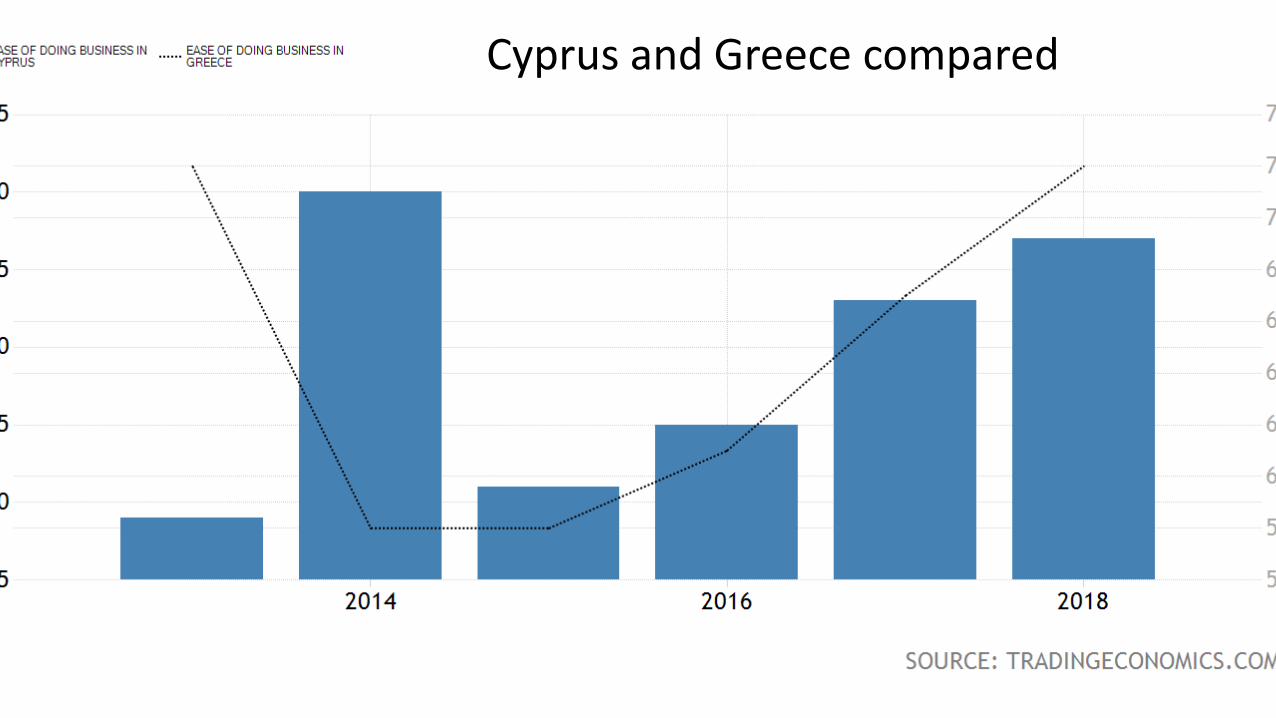

Ease of doing business, Cyprus rank, 2008-18

Cyprus and Greece compared

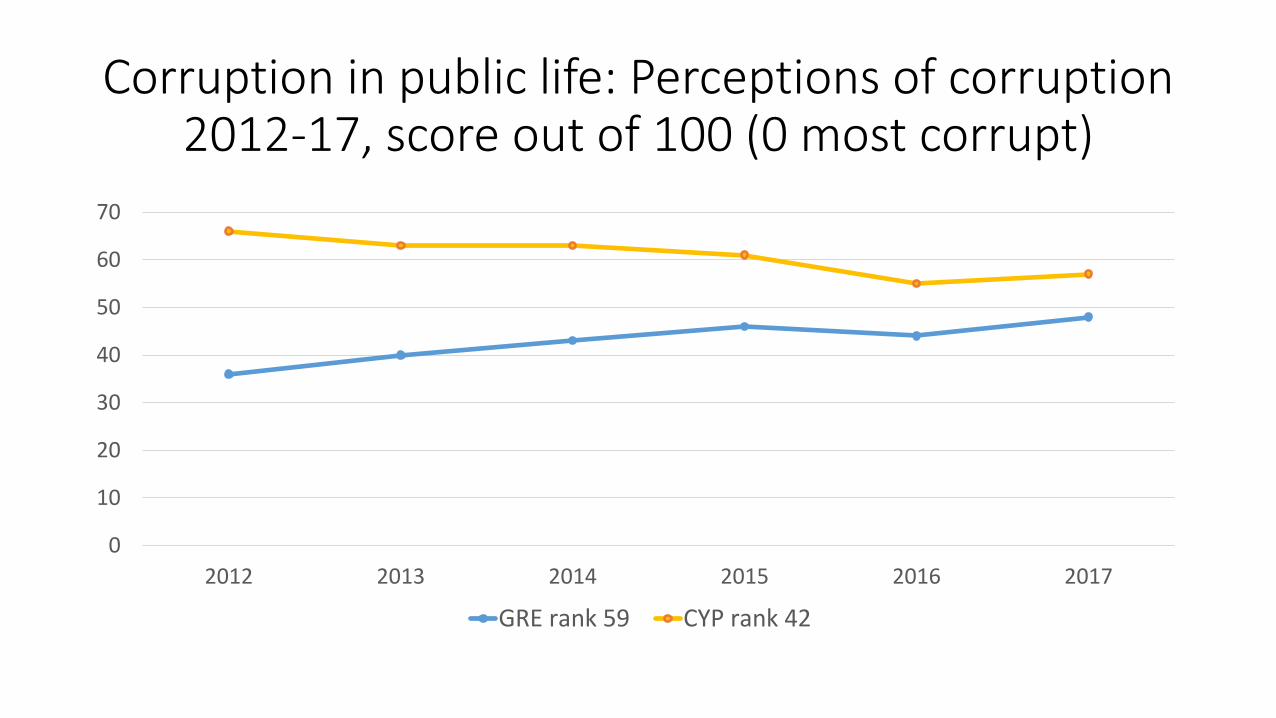

Corruption in public life: Perceptions of corruption 2012-17, score out of 100 (0 most corrupt)

0

10

20

30

40

50

60

70

2012 2013 2014 2015 2016 2017

GRE rank 59 CYP rank 42

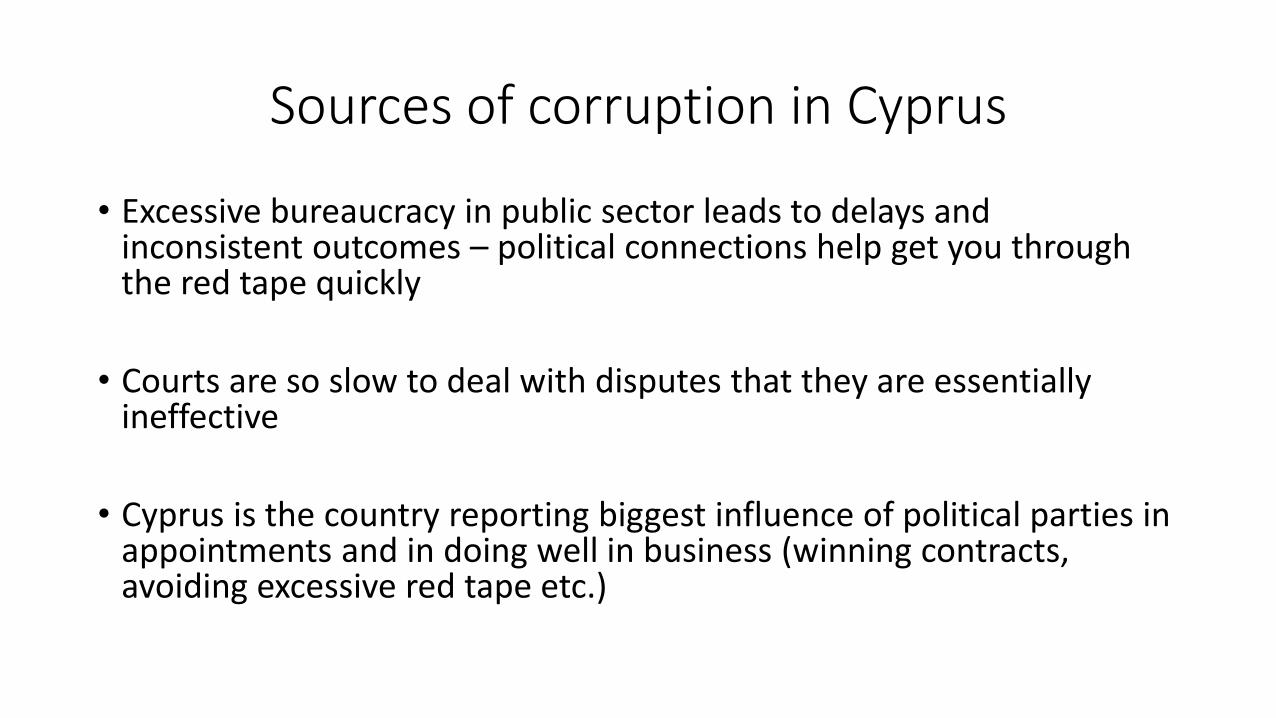

Sources of corruption in Cyprus

• Excessive bureaucracy in public sector leads to delays and inconsistent outcomes – political connections help get you through the red tape quickly

• Courts are so slow to deal with disputes that they are essentially ineffective

• Cyprus is the country reporting biggest influence of political parties in appointments and in doing well in business (winning contracts, avoiding excessive red tape etc.)

Where does one start?

• No doubt that in Cyprus the source of institutional inefficiency is the public sector – virtually nothing works quickly, with transparency and with confidence that the case has been dealt with fairly in the absence of political interference

• E.g., property titles delayed because the tax authorities consider threats in this connection as the most effective way to collect overdue taxes – in other countries the courts play that role

• Tax office responds to queries about tax owed with 6-7 years delay and then penalise you heavily for the delay in paying the taxes

Company red tape

• Red tape becoming worse, still no digital technology used. Recent report by the auditor general about tax evasion criticising dividing lines between VAT and income tax – response form the companies office and tax authorities: give us another 150 employees and we will deal with it.

• In the tourist sector (the biggest foreign exchange earner on the island) it is not clear where local authorities’ powers end and where central government ones begin. As a result, there is chaos in maintenance and issuing of permits, with detrimental results on the quality of the product (environment, licencing etc.)

Good signs – or are they?

• Most encouraging development is that people in high office started to complain in public, e.g., auditor general, attorney general, even central bank governor.

• Public who have been disgruntled but got on with their life are beginning to talk more loudly

• Hopefully progress is on its way – but it has to come from government and Parliament, which has the vested interest in preserving the status quo