gresham private equity co-investment fund. ar_web version.pdf · 2010-12-14 · private equity...

TRANSCRIPT

PRIVATE EQUITY

Annual Report 2005.

Gresham Private Equity Co-Investment Fund.A.R.S.N. 109 573 015

Responsible entityGresham Funds Management Limited.

A.B.N. 32 109 020 153

{

Gresham Private Equity is a specialist inmanagement buy-outs and targets investmentopportunities in Australiaand New Zealand.

}

Letter from the Chairman

Review of Operations

Noel Leeming Group Limited

Australian Pacific Paper Products

Financial Report

Directory

Annual Report 2005. 1

CONTENTS

2.8.3.

4.

6.

25.

Gresham Private Equity Co-Investment Fund.2

Dear Unitholder

I have pleasure in presenting the Gresham Private Equity Co-InvestmentFund’s (the “Fund’s”) Annual Report for the period ended 30 June 2005.

The Fund’s objective is to invest in established Australian and New Zealandbusinesses with enterprise values of, indicatively, up to $500 million.It targets management buy-out and buy-in opportunities, expansion capitalinjections, industry consolidations and public-to-private transactions.

In the period since inception in August 2004, the Fund has successfullymet this objective by investing in:

• the management buy-in of the Noel Leeming Group inNew Zealand; and

• the management buy-out of Australian Pacific Paper Products in Australia.

In aggregate, the Fund has invested approximately 18% of itscommitted capital in this period.This is in line with its target of investing 80% of its committed capital in the first five years of operations.

The investments have been funded by the initial instalment of $0.15 per unit made by investors at the time of the Fund’s establishment,supplemented by borrowings under a debt facility designed to bridgethe Fund’s operations between instalments. As originally foreshadowed,it is anticipated that a further instalment of between $0.30 and $0.45per unit will be made during the second year of the Fund’s operation.

During the year the Fund’s management team has been strengthenedfrom six to eight executives.The board has also altered following the recent retirement of Michael Chaney as Managing Director of Wesfarmers, and consequently as a director of Gresham PrivateEquity Limited, the Manager of the Fund. Michael Chaney remains,however, within the Gresham Group, having accepted the position of Chairman of the Manager’s parent company, Gresham PartnersHoldings Limited, from July 2005. Richard Goyder, now ManagingDirector of Wesfarmers, and Gene Tilbrook, the Finance Director of Wesfarmers, continue to work closely with the Manager on its board and investment committee.

I am pleased to advise that, following a review of its first year ofoperation, the Fund’s service fee has been reduced from 0.75% pa of committed capital to 0.50% pa of committed capital, with effectfrom 1 July 2005.This reduction has been possible due to the success of the Fund in attracting larger total investor commitments with a higher proportion of larger investors than originally estimated.

For the general information of unitholders we will be holding fourInformation Meetings as follows:

• Sydney: 4 October 2005 at 12.00 noon at The Treasury Room The Intercontinental Hotel Cnr of Bridge and Phillip Streets, Sydney

• Brisbane: 6 October 2005 at 8.30am at The Raffles Room The Stamford PlazaCnr of Edward & Margaret Streets, Brisbane

• Melbourne: 6 October 2005 at 5.30pm at The Archer RoomThe Old TreasuryLevel 2, Cnr of Collins & Spring Streets, Melbourne

• Perth: 7 October 2005 at 12.00 noon at The Duxton 1 RoomThe Duxton HotelNo.1 St Georges Terrace, Perth

If you intend to join us at one of these Information Meetings, and have not already responded, would you kindly email Jasmine McDonald-Williams at [email protected] to advise us of your attendance.

We thank you for your support and look forward to advising youfurther at the meetings.

Yours faithfully

James P GrahamChairmanGresham Funds Management LimitedResponsible Entity

LETTER FROM THE CHAIRMAN

Annual Report 2005. 3

REVIEW OF OPERATIONS

INVESTMENT REVIEW

In the period to 30 June 2005, the Manager (Gresham Private EquityLimited) invested $18.4 million of the Fund’s capital across twotransactions. In both these transactions the Fund co-invested with theinstitutional investment vehicles of Gresham Private Equity Fund 2.

• Noel Leeming Group

In August 2004, the Fund led the NZ$138.5 million managementbuy-in of New Zealand’s leading electrical appliance retailer – The Noel Leeming Group (“NLG”), backing Nick Lowe to take over as CEO once Gresham Private Equity acquired the business.

Since the acquisition, and consistent with our investment strategy,we have replaced most of the previous management team. NLG hasfocused its attention on its dual chains of electrical appliance stores – “Noel Leeming” and “Bond & Bond” – and has introduced someclear delineation between the brands through the exclusive “Fisher& Paykel” offering in its premier full service Noel Leeming stores.In addition, we have a targeted program of store refurbishment to improve sales and have also implemented a detailed cost review of the company.The under-performing “Big Byte” and “NoelLeeming Furniture” stores have been exited.

• Australian Pacific Paper Products

In June 2005, the Fund led the $75 million secondary managementbuy-out of Australian Pacific Paper Products (“APPP”) – Australia’ssecond largest disposable nappy manufacturer. APPP provides a range of disposable nappy products, led by its premium “BabyLove” brand.

The APPP management team is in the midst of the initial 100-dayplan to improve manufacturing efficiency, review the sales and marketing channels and initiate new product and technicaldevelopments.This task is being assisted by the participation of APPP’s new Chairman, Peter McLoghlin, the former CEO of the rival “Huggies” brand, who has been appointed to the position by Gresham Private Equity.

Further details of both investments are set out on the following pages.

The investment program to date has seen approximately 18% of theFund’s committed capital invested in the first year of operations.This is consistent with the Fund’s target of investing 80% of its capital overits five-year investment horizon.

NEW INVESTMENT OUTLOOK

While it is difficult to forecast the precise timing or size of our nexttransactions, we are confident that we will broadly remain on trackwith our investment program in the coming year. Our work in progressremains strong and we are working with a broad range of advisers on a number of interesting opportunities.The investment outlook has bothpositive and negative aspects. On the positive side there are a numberof interesting businesses for sale. On the negative side there is significantpricing pressure and an expectation across the private equity market of lower returns.

It is our task, on behalf of our investors, to maintain investmentdiscipline on acquisition and to subsequently take a rigorous approachto portfolio management.

The Fund continues to form part of Gresham Private Equity Fund 2,which has now completed its fund raising and has total committedcapital of $325 million. Our strategy continues to be to adopt a focusedapproach to MBOs and MBIs in the range of $100 to $500 million ofenterprise value.While we do see competition for transactions of thissize and type, it does not tend to be as intense as for larger transactions.As a result, our investments to date have been priced at multiples which should provide satisfactory returns to our investors, provided the investments are carefully managed and well exited.

INVESTMENT MANAGEMENT TEAM

The Fund’s management team has been augmented during the year witha net increase from six to eight executives. Our focus continues to be to add to the breadth of the management team through the recruitmentof executives with a diverse mix of backgrounds and skills.The teamcontinues to offer a blend of local and international experience inprivate equity, investment banking, consulting and operational roles.

CONCLUSION

We are pleased with progress to date.While the investment environmenthas its challenges, we will continue to take a diligent approach to theevaluation of investment opportunities and we remain confident ofdelivering satisfactory returns to our investors.

Gresham Private Equity Co-Investment Fund.4

In August 2004,Gresham Private Equityled the NZ$138.5 million management buy-out of Noel Leeming GroupLimited from Pacific Retail Group.

SUMMARY OF DEAL

In August 2004, Gresham Private Equity led the NZ$138.5 millionmanagement buy-out of Noel Leeming Group Limited from PacificRetail Group. Noel Leeming Group is New Zealand’s largest electricalappliance retailer, operating under the “Noel Leeming”, “Noel LeemingFurniture”, “Bond & Bond” and “Big Byte” brands.

The buy-out was led by Gresham Private Equity whose funds hold 85%of the equity, and Direct Capital Limited also invested in the transactionand has a 5% stake.The management team, led by new CEO NickLowe, also made a significant investment. Bank of Scotland provided thesenior and subordinated acquisition debt facilities for the transaction.

BACKGROUND

The Noel Leeming Group was part of Pacific Retail Group, a NZSElisted company. Pacific Retail Group announced its intention to list Noel Leeming Group in order to fund other parts of the group.However, instability in the public markets caused problems with a listing. Following a direct approach by Gresham and its advisers,all parties worked together to effect the sale.

Gresham Private Equity conducted extensive due diligence into thefinancial and legal background of Noel Leeming using Ernst & Young and Bell Gully. Gresham Private Equity has also undertaken in-depthindustry analysis through specialist retail consultants The Brackenbury Group.

Roy McKelvie and Mark Youens of Gresham Private Equity have joinedthe Board of Noel Leeming Group.

THE BUSINESS

Noel Leeming is the largest electrical appliance retailer in New Zealandwith a market share of 26%.At acquisition, it had 90 retail outletscomprising four brands, “Noel Leeming”, “Noel Leeming Furniture”,“Bond & Bond” and “Big Byte”.

“NOEL LEEMING”“Noel Leeming” is the flagship retail brand with 47 stores and over 630 employees. It strives to offer a superior standard of service and thewidest possible range of branded consumer technology and appliances.“Noel Leeming” promises its customers that it will never knowingly be undersold. Comprehensive after sales support is a critical point ofdifference to its competitors.With its significant retail footprint, “NoelLeeming” is uniquely positioned to offer its customers new technologybased products such as liquid crystal display (“LCD”) and plasma TVs, cellular phones and services, digital cameras and convergencetechnologies. Demand for these technologies is growing and isexpected to continue to drive growth in the “Noel Leeming” brand.

In May 2003, “Noel Leeming” opened its first new concept mega store,incorporating appliances, technology and furniture under one roof.Covering a retail area of 3,668m2, the store is based in the leading retailprecinct at Wairau Park on Auckland’s North Shore. Early trading hasbeen ahead of management expectations.

“BOND & BOND”With 35 stores and 320 employees, “Bond & Bond” has an emphasis on audio visual products and provides its customers with appliance,computer and electronics products in a no frills environment.

“Bond & Bond’s” product range is less extensive than the “NoelLeeming” branded store, but provides selected leading brands at thebest possible prices. It is based on a low-cost store format strategy that supports its price and value positioning. Until recently, many“Bond & Bond” stores could be found in mall and high street locations.Now they are mainly found in destination shopping areas.This isincreasing profitability by lowering rent costs and more accuratelytargeting its key demographic. Recent purchasing improvements andlowering of operating costs have allowed it to strengthen its competitiveadvantage in the sourcing and stocking of the best products at thelowest prices for its customers.

NOEL LEEMING GROUP LIMITED

Annual Report 2005. 5

MANAGEMENT

At the time of the acquisition of Noel Leeming, Nick Lowe wasappointed as the new Chief Executive Officer of the business. Nick hassignificant experience in electrical and general retailing in New Zealandand the United Kingdom.

Nick’s previous role was CEO of Farmers, New Zealand’s largestdepartment store, a role he held for four years. Before moving to New Zealand Nick worked at Dixons, Europe’s largest electricalappliance retailer, for 13 years.When he left he was Managing Directorof The Link. Prior to this he held various senior roles in marketing and operations within the Dixons empire.

Since acquisition, Bruce Cotterill has been appointed as Chairman of Noel Leeming Group. Bruce was previously the CEO of CanterburyNew Zealand, the former Regional Managing Director of Colliers Jardineand the former Managing Director of ACP Media in New Zealand.

TRANSACTION RATIONALE

We saw Noel Leeming as an attractive investment opportunity because:

• The business is the market leading electrical appliance retailer in New Zealand and is more than twice the size of its nearestcompetitor. It is the largest distributor of “Sony”, “Philips”,“Panasonic”, “Hewlett Packard” and “Electrolux” in New Zealand,enabling superior buying power, trading terms leverage and volume rebates.

• Noel Leeming has continued to grow in the face of intensecompetition.There are significant low cost operational improvementsthat will better define and deliver its offer in the respective brandsthat should deliver higher future growth.

• Nick Lowe brings to the management team a wealth of internationalelectrical appliance retailing experience balanced with six yearsworking in the New Zealand market.

• Due to the vendor’s cash requirements, there was an opportunity to buy the business at a material discount to listed peers.

• The business generates strong cash flows to service the acquisition debt.

• The strength of the brand and the scale of the business should lead to a number of exit options over our investment time horizon.

Gresham Private Equity Co-Investment Fund.6

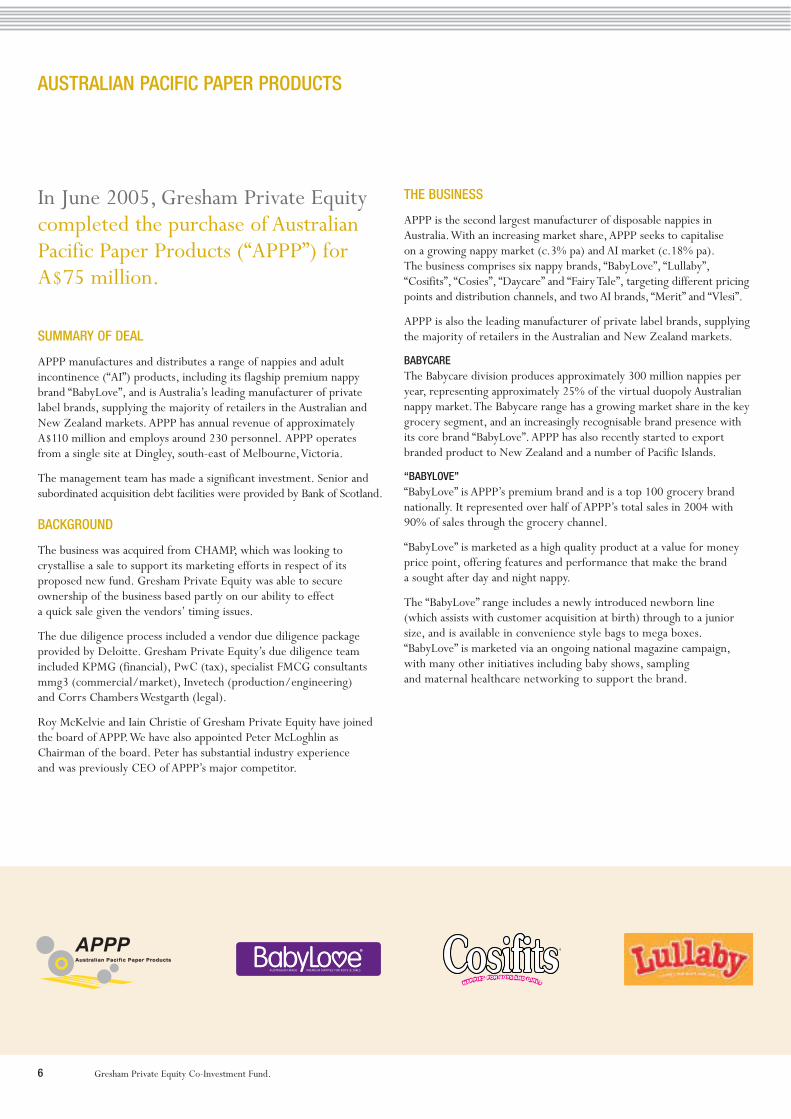

In June 2005, Gresham Private Equitycompleted the purchase of AustralianPacific Paper Products (“APPP”) forA$75 million.

SUMMARY OF DEAL

APPP manufactures and distributes a range of nappies and adultincontinence (“AI”) products, including its flagship premium nappybrand “BabyLove”, and is Australia’s leading manufacturer of privatelabel brands, supplying the majority of retailers in the Australian andNew Zealand markets. APPP has annual revenue of approximatelyA$110 million and employs around 230 personnel. APPP operates from a single site at Dingley, south-east of Melbourne,Victoria.

The management team has made a significant investment. Senior andsubordinated acquisition debt facilities were provided by Bank of Scotland.

BACKGROUND

The business was acquired from CHAMP, which was looking tocrystallise a sale to support its marketing efforts in respect of itsproposed new fund. Gresham Private Equity was able to secureownership of the business based partly on our ability to effect a quick sale given the vendors’ timing issues.

The due diligence process included a vendor due diligence packageprovided by Deloitte. Gresham Private Equity’s due diligence teamincluded KPMG (financial), PwC (tax), specialist FMCG consultants mmg3 (commercial/market), Invetech (production/engineering) and Corrs Chambers Westgarth (legal).

Roy McKelvie and Iain Christie of Gresham Private Equity have joinedthe board of APPP.We have also appointed Peter McLoghlin asChairman of the board. Peter has substantial industry experience and was previously CEO of APPP’s major competitor.

THE BUSINESS

APPP is the second largest manufacturer of disposable nappies inAustralia.With an increasing market share, APPP seeks to capitalise on a growing nappy market (c.3% pa) and AI market (c.18% pa).The business comprises six nappy brands, “BabyLove”, “Lullaby”,“Cosifits”, “Cosies”, “Daycare” and “Fairy Tale”, targeting different pricingpoints and distribution channels, and two AI brands, “Merit” and “Vlesi”.

APPP is also the leading manufacturer of private label brands, supplying the majority of retailers in the Australian and New Zealand markets.

BABYCAREThe Babycare division produces approximately 300 million nappies peryear, representing approximately 25% of the virtual duopoly Australiannappy market.The Babycare range has a growing market share in the keygrocery segment, and an increasingly recognisable brand presence withits core brand “BabyLove”. APPP has also recently started to exportbranded product to New Zealand and a number of Pacific Islands.

“BABYLOVE”“BabyLove” is APPP’s premium brand and is a top 100 grocery brandnationally. It represented over half of APPP’s total sales in 2004 with90% of sales through the grocery channel.

“BabyLove” is marketed as a high quality product at a value for moneyprice point, offering features and performance that make the brand a sought after day and night nappy.

The “BabyLove” range includes a newly introduced newborn line (which assists with customer acquisition at birth) through to a juniorsize, and is available in convenience style bags to mega boxes.“BabyLove” is marketed via an ongoing national magazine campaign,with many other initiatives including baby shows, sampling and maternal healthcare networking to support the brand.

AUSTRALIAN PACIFIC PAPER PRODUCTS

Annual Report 2005. 7

HEALTHCARE DIVISION – ADULT INCONTINENCEAPPP supplies the “Vlesi” and “Merit” brands.The size of the totalAustralian AI market is A$130 million and this is forecast to grow at c.18% pa through to 2008. Key drivers are an ageing populationcombined with increasing penetration of AI products, underpinned by product innovation and consumer education.

APPP is focused on the aged care nursing home market, selling a widerange of products for usage in incontinence care. APPP is currentlydeveloping its business across the NSW and Queensland markets, havingestablished very strong market shares in the nursing home sector in Victoria, South Australia,Western Australia and Tasmania.

MANAGEMENT

The CEO, Colin Lamond, joined APPP in 2002 and has significantmanufacturing experience with National Starch and Email Limited,and international experience with Schlumberger. Colin has a HarvardMBA and a first degree in engineering. He is supported by an able team of specialists in Manufacturing,Technical, Sales and Marketing and Finance.

Gresham has introduced Peter McLoghlin as Chairman of the board.Peter is a well known FMCG specialist, who previously ran divisions of Goodman Fielder and Kimberly Clark Australia (“KCA”).While atKCA, Peter ran the personal care division, the largest part of which was the “Huggies” nappies business. He sits on the boards of a range of companies including the Australasian arm of S.C. Johnson, the USMultinational, and Greens Foods, the listed Australian food group.

TRANSACTION RATIONALE

The attractions of this business as an investment opportunity include:

• Duopoly Market with Strong Retailer Support: APPP has a strong position in a virtual duopoly market. Retailers are sensitive to the dominance of the current market leader, KCA.

• Brand Rationalisation and New Products: Management havesuccessfully commenced the process of reducing the company’smyriad range of overlapping brands.This process is not yet completebut already a clearer, more focused marketing message is havingpositive effects on sales as well as marketing costs.

• Manufacturing Efficiency: Since 2002 the focus onmanufacturing efficiency has contributed to profit growth.APPP now has a strong manufacturing base. Our production and engineering diligence has supported the view that there are further efficiency gains to be made.

• Strong Cash Flow: The business has consistently demonstrated its ability to generate cash.

• Acquisition Pricing and Exit: Given the vendor’s externalimpetus for an exit, there was the opportunity to acquire the businessat a discount to its listed peers. In addition, timing circumstancesshould facilitate a more attractive trade exit environment in three to four years’ time. Our strategy will be to structure the company to be operationally compatible with such likely acquirers.

• Management Commitment: The Management made a significantinvestment in the business which is strong evidence of their faith inthe company’s continued growth potential.

• Impressive Leadership Augmented by a Strong Buy-inChairman: Colin Lamond has demonstrated strong leadership andhis team have delivered consistent profit improvements in each yearof his leadership.We have augmented this with a buy-in Chairmanwho was the CEO of APPP’s major competitor.

Gresham Private Equity Co-Investment Fund.8

DIRECTORS’ REPORT

The directors of Gresham Funds Management Limited (the “Company”), the Responsible Entity of the Gresham Private Equity Co-Investment Fund(the “Fund”), submit their report together with the financial report of the Fund for the financial period, from the date of registration, 29 June 2004,to 30 June 2005.

DIRECTORSThe following persons held office as directors of the Company since the date of registration and since the end of the financial period and up to thedate of this report, unless noted otherwise:

James P Graham, ChairmanRoger S Casey, Joint Managing DirectorRoy D McKelvie, Joint Managing DirectorAntony G BreuerMichael A Chaney, AO (ceased 29 June 2005)Richard J B Goyder Graham J RichGrant W Schmidt (ceased 31 March 2005)Gene T Tilbrook (appointed 29 June 2005)

PRINCIPAL ACTIVITIESThe Fund’s objective is to pursue investments in a wide range of companies predominantly in Australia and New Zealand, in conjunction with theinstitutional Gresham Private Equity Funds 2a and 2b.The Fund intends to invest in significant growth opportunities in various sectors.The majorityof the investments are expected to be management buy-outs and expansion capital.There have been no significant changes in the nature of the Fund’sactivities since commencement.

REVIEW OF OPERATIONSThere has been no change to the operation of the Fund since establishment.

For the financial period, from the date of registration, 29 June 2004, to 30 June 2005, the Fund, in conjunction with the institutional GreshamPrivate Equity Funds 2a and 2b, completed two major investments in businesses having an aggregate enterprise value on acquisition of $203 million.No change in the carrying value of these investments has been made since acquisition and accordingly the operating result for the period was a lossof $2,638,823, reflecting largely the management, operating and interest expenses incurred by the Fund.

The objective is to realise an increase in the value of the Fund’s investments in due course, which after all accumulated net operating costs producesan attractive return to unitholders.

DISTRIBUTIONSNo distributions have been paid or provided by the Fund during the period.

SIGNIFICANT CHANGESOn 16 August 2004, the Fund finalised its capital raising with unitholders providing committed capital totalling $102,020,000. Otherwise, in theopinion of the directors, there were no significant changes in the state of affairs of the Fund that occurred during the financial period under reviewnot otherwise disclosed in this report and financial statements.

MATTERS SUBSEQUENT TO BALANCE DATEExcept for the matter discussed in the financial report, no other matters or circumstances have arisen since 30 June 2005 that have significantlyaffected or may significantly affect:

(a) the operations of the Fund in future financial years; or

(b) the results of those operations in future financial years; or

(c) the state of affairs of the Fund in future financial years.

FINANCIAL REPORT

Annual Report 2005. 9

LIKELY DEVELOPMENTS AND EXPECTED RESULTS OF OPERATIONSFor reporting periods beginning on or after 1 January 2005, the Fund must comply with Australian equivalents to International Financial ReportingStandards (“AIFRS”) as issued by the Australian Accounting Standards Board.This financial report has been prepared in accordance with Australianaccounting standards and other financial reporting requirements (“Australian GAAP”) applicable for reporting periods ended 30 June 2005.

Details of the impact of the transition to AIFRS are set out in Note 17 of the financial report.

On 29 June 2005, the Responsible Entity decided to reduce the operating expenses of the Fund by lowering its service fee from the level set out in the Constitution of 0.75% to 0.50% per annum of committed capital, for the year commencing 1 July 2005.

Other than the above, there are no material changes proposed for the operation of the Fund and its investment philosophy.

VALUE OF ASSETSThe carrying value of the Fund’s assets at 30 June 2005 was $18,950,044 which is derived using the bases set out in Note 1 to the financial statements.

INDEMNIFICATION AND INSURANCE OF OFFICERS AND AUDITORDuring the financial period, no insurance premiums were paid out of the Fund in respect of any insurance cover relating to the Responsible Entityor the auditor. So long as the officers of the Responsible Entity act in accordance with the Fund’s Trust Deed and the law, they will remain fullyindemnified out of the assets of the Fund against any losses incurred whilst acting on behalf of the Fund.There is no indemnification of the auditor of the Fund out of the assets of the Fund.

ENVIRONMENTAL REGULATIONThe activities of the Fund itself are not subject to any particular or significant environmental regulations under a Commonwealth, State or Territory law.

AUDITOR’S INDEPENDENCE DECLARATIONA copy of the Auditor’s Independence Declaration as required under section 307 of the Corporations Act is set out on page 10.

This report is made out in accordance with a resolution of the directors.

James P GrahamChairman

Sydney, 27 July 2005

As lead auditor for the audit of Gresham Private Equity Co-InvestmentFund for the period ended 30 June 2005, I declare that to the best of my knowledge and belief, there have been:

a) no contraventions of the auditor independence requirements of the Corporations Act 2001 in relation to the audit; and

b) no contraventions of any applicable code of professional conduct in relation to the audit.

This declaration is in respect of Gresham Private Equity Co-InvestmentFund during the period.

AJ Loveridge SydneyPartner 27 July 2005PricewaterhouseCoopers

AUDITORS’ INDEPENDENCE DECLARATION

Gresham Private Equity Co-Investment Fund.10

Liability is limited by the Accountant’s Scheme under the Professional Standards Act 1994 (NSW).

Annual Report 2005. 11

29 June 2004 to

Note 30 June 2005$

Statement of financial performance

INVESTMENT INCOMEInterest 90,103Transaction fees 574,318Other income 21,727

Total investment income from ordinary activities 686,148

EXPENDITUREAdministration and other expenses 277,230Loan establishment, interest and line fee expenses 424,589Management fees and transaction expenses 1,953,984Service fees 669,168

Total expenditure from ordinary activities 3,324,971

Net operating loss from ordinary activities (2,638,823)

DistributionNet operating loss (2,638,823)Transfer from accumulated deficit 5(c) 2,638,823

Distributions paid –

The above statement of financial performance should be read in conjunction with the accompanying notes.

STATEMENT OF FINANCIAL PERFORMANCEfor the period 29 June 2004 to 30 June 2005

Gresham Private Equity Co-Investment Fund.12

Note 2005$

UNITHOLDERS’ FUNDSOrdinary units 5(a) 12,705,995Sponsor units 5(b) 500Accumulated deficit 5(c) (2,638,823)

TOTAL UNITHOLDERS’ FUNDS 10,067,672

CURRENT ASSETSCash 7(b) 113,255Receivables 417,827

TOTAL CURRENT ASSETS 531,082

NON-CURRENT ASSETSInvestments 6 18,418,962

TOTAL NON-CURRENT ASSETS 18,418,962

TOTAL ASSETS 18,950,044

CURRENT LIABILITIESAccounts payable 1,132,372

TOTAL CURRENT LIABILITIES 1,132,372

NON-CURRENT LIABILITIESLoan facility 8 7,750,000

TOTAL NON-CURRENT LIABILITIES 7,750,000

TOTAL LIABILITIES 8,882,372

NET ASSETS 10,067,672

The above statement of financial position should be read in conjunction with the accompanying notes.

STATEMENT OF FINANCIAL POSITIONas at 30 June 2005

Annual Report 2005. 13

29 June 2004 to

Note 30 June 2005$

CASH FLOWS FROM OPERATING ACTIVITIESInterest received 49,381Other income received 284,818Payment of borrowing costs (374,654)Payment of management fees and other expenses (1,883,323)

NET CASH OUTFLOW FROM OPERATING ACTIVITIES 7(a) (1,923,778)

CASH FLOWS FROM INVESTING ACTIVITIESPurchases of investments (18,418,962)

NET CASH OUTFLOW FROM INVESTING ACTIVITIES (18,418,962)

CASH FLOWS FROM FINANCING ACTIVITIESProceeds from issue of units 15,303,000Proceeds from loan drawdowns 7,750,000Payment of fund establishment expenses (2,597,005)

NET CASH INFLOW FROM FINANCING ACTIVITIES 20,455,995

NET INCREASE IN CASH HELD 113,255Cash at the beginning of the financial period –

CASH AT THE END OF THE FINANCIAL PERIOD 7(b) 113,255

The above statement of cash flows should be read in conjunction with the accompanying notes.

STATEMENT OF CASH FLOWSfor the period 29 June 2004 to 30 June 2005

Gresham Private Equity Co-Investment Fund.14

NOTE 1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

BASIS OF PREPARATIONThis general purpose financial report for the period from 29 June 2004 to 30 June 2005 has been prepared in accordance with the Fund’s Constitution,Accounting Standards, other authoritative pronouncements of the Australian Accounting Standards Board, Urgent Issues Group Consensus Views and theCorporations Act 2001. It has been prepared in accordance with the historical convention, except for certain assets which, as noted, are at valuation.

CASHFor the purposes of the statement of cash flows, cash includes deposits at call which are readily convertible to cash and are subject to insignificantrisk of changes in value, net of bank overdrafts, if any.

INVESTMENT INCOME AND EXPENSES Investment income and expenses are brought to account on an accruals basis. Interest revenue is recognised on a time proportionate basis that takesinto account the effective yield on the financial assets. Dividends from companies are recorded as income when the Fund’s right to receive paymentis established.

RESPONSIBLE ENTITY’S REMUNERATIONResponsible Entity’s fees have been calculated in accordance with the Fund’s Constitution.

INVESTMENTSInvestments are initially recorded at cost and are revalued by the Directors to their market value in line with industry practice as at the reportingdate. Gains and losses (realised and unrealised) are included within investment income in the statement of financial performance. Individualinvestments may take the form of a combination of equities and loans which are managed as a single investment. Foreign currency contracts may be acquired to hedge against the financial effects of movements in exchange rates as determined by the investment manager.

FOREIGN CURRENCY TRANSACTIONSForeign currency transactions are initially translated into Australian currency at the rate of exchange at the date of the transaction. At balance date,amounts receivable and payable in foreign currencies are translated to Australian currency at rates of exchange current at that date. Resultingexchange differences are brought to account in determining investment income for the year.

RECEIVABLESReceivables may include amounts for dividends, interest and securities sold where settlement has not yet occurred. Interest is accrued at thereporting date from the time of last payment. Amounts are generally received within 30 days of being recorded as receivables, with the exception of interest on certain non-current investments.

ACCOUNTS PAYABLEAccounts payable represent liabilities for amounts owing by the Fund at year end which are unpaid.The amounts are unsecured and are usually paidwithin 30 days of recognition.

GOODS AND SERVICES TAX (“GST”)The Fund qualifies for Reduced Input Tax Credits at a rate of 75%. Investment management fees and other expenses have been recognised in thestatement of financial performance inclusive of the amount of GST not recoverable from the Australian Taxation Office (“ATO”).The net amount of GST recoverable from the ATO is included in receivables in the statement of financial position. Accounts payable are inclusive of GST. Cash flowsrelating to GST are included in the statement of cash flows on a gross basis.

NOTE 2. TAXATION

Under current legislation, the Fund would not be liable to income tax to the extent that the taxable income is distributed in full to Unitholders.

NOTE 3. LIFE OF FUND

The Fund was registered on 29 June 2004 under a Constitution dated 28 June 2004 and shall terminate on the earliest to occur of:

(a) unless previously extended or determined, 30 June 2015; and

(b) the date on which the Fund is terminated by law.

NOTES TO AND FORMING PART OF THE FINANCIAL STATEMENTSfor the period 29 June 2004 to 30 June 2005

Annual Report 2005. 15

NOTE 4. NET TANGIBLE ASSET BACKING

The net tangible asset backing of each unit as at 30 June 2005 is $0.0987.

NOTE 5. UNITHOLDERS’ FUNDS

2005 2005Number $

(a) Ordinary units (refer below)

Opening balance – –Units issued at $1.00 paid to $0.15 102,020,000 15,303,000Fund establishment cost – (2,597,005)

Closing balance 102,020,000 12,705,995

As stipulated in the Fund’s Constitution, each ordinary unit represents a right to an individual share in the Fund and does not extend to a right tothe underlying assets of the Fund. Calls are made in accordance with the Constitution.

(b) Sponsor units (refer below)

Opening balance – –Units issued at $0.001 paid to $0.001 500,000 500

Closing balance 500,000 500

As stipulated in the Fund’s Constitution, sponsor units, which are held by the investment manager of the Fund, Gresham Private Equity Limited,a related body corporate of the Responsible Entity, carry an entitlement to a share of any sponsor’s unit distributions of the Fund.The sponsor’s unitdistributions are payable out of the proceeds of realised investments of the Fund.The distribution is calculated each time an investment is realisedby the Fund. Ordinary unitholders are entitled to a return equal to the Relevant Outflows of the Fund plus a preferred 8% per annum in respect of these Relevant Outflows before any sponsor’s unit distribution becomes payable. Subject to this priority return for ordinary unitholders, thesponsor’s unit distribution (if any) payable when investments are realised will generally be 20% of the profit, net of certain expenses, achieved.If the Fund’s assets were realised at their estimated fair value at balance date, there would be no resultant sponsor’s unit distribution entitlement.

(c) Accumulated deficit

Opening balance –Transfer to distribution statement (2,638,823)

Closing balance (2,638,823)

NOTE 6. INVESTMENTS

Investments at directors’ valuation– Unlisted equities 3,914,231– Unsecured loans 14,504,731

Total investments 18,418,962

NOTES TO AND FORMING PART OF THE FINANCIAL STATEMENTSfor the period 29 June 2004 to 30 June 2005 (continued)

Gresham Private Equity Co-Investment Fund.16

NOTE 7. RECONCILIATION OF NET OPERATING LOSS TO NET CASH OUTFLOW FROM OPERATING ACTIVITIES

29 June 2004 to30 June 2005

$

(a) Reconciliation of net operating loss to net cash outflow from operating activities

Net operating loss for the period (2,638,823)Change in operating assets and liabilities:Increase in receivables (417,327)Increase in accounts payable 1,132,372

Net cash outflow from operating activities (1,923,778)

(b) Components of cash

Cash as at the end of the financial year as shown in the statement of cash flows is reconciled to the statement of financial position as follows:

2005$

Cash 113,255

NOTE 8. BORROWING/FINANCING FACILITIES

The Fund has a 10 year $25,000,000 bank loan facility which commenced on 16 November 2004.The amount drawn down at 30 June 2005 was $7,750,000.

NOTE 9. REDEMPTION ARRANGEMENT

The Responsible Entity has no obligation in the Constitution to repurchase units or redeem units issued under the Constitution.

NOTES TO AND FORMING PART OF THE FINANCIAL STATEMENTSfor the period 29 June 2004 to 30 June 2005 (continued)

Annual Report 2005. 17

NOTE 10. FINANCIAL INSTRUMENTS

INTEREST RATE RISKInterest rate risk is the risk that the value of a financial instrument will fluctuate due to changes in market interest rates.

The Fund has an interest rate exposure from the holding of financial assets and liabilities in the normal course of business.The exposure to theinterest rate risk and the weighted average interest rate for each class of interest bearing financial asset and financial liability is set out as follows.

Weighted average Floating Non-interest30 June 2005 effective interest rate interest rate bearing Total

% p.a. $ $ $

Financial assetsCash 5.3 113,255 – 113,255Receivables – – 417,827 417,827Investments 11.5 4,264,939 14,154,023 18,418,962

Total financial assets 4,378,194 14,571,850 18,950,044

Financial liabilitiesAccounts payable – – 1,132,372 1,132,372Loan facility 6.3 7,750,000 – 7,750,000

Total financial liabilities 7,750,000 1,132,372 8,882,372

Net financial assets/(liabilities) (3,371,806) 13,439,478 10,067,672

CREDIT RISK EXPOSURE(i) On-balance sheet financial instruments

Credit risk is the risk that a counterparty will fail to perform obligations under a contract.The credit risk on financial assets of the Fund which havebeen recognised in the statement of financial position is the carrying amount net of any provision for doubtful debts.

(ii) Off-balance sheet financial instruments

At 30 June 2005, the Fund had no off-balance sheet financial instruments. No trading in derivative financial instruments occurred during the period.

NET FAIR VALUE OF FINANCIAL ASSETS AND LIABILITIES(i) On-balance sheet financial instruments

The Fund’s financial assets and liabilities included in the balance sheet are carried at amounts that approximate net fair value.

(ii) Off-balance sheet financial instruments

At 30 June 2005 the Fund had no off-balance sheet financial instruments.

NOTES TO AND FORMING PART OF THE FINANCIAL STATEMENTSfor the period 29 June 2004 to 30 June 2005 (continued)

Gresham Private Equity Co-Investment Fund.18

NOTES TO AND FORMING PART OF THE FINANCIAL STATEMENTSfor the period 29 June 2004 to 30 June 2005 (continued)

NOTE 10. FINANCIAL INSTRUMENTS (CONTINUED)

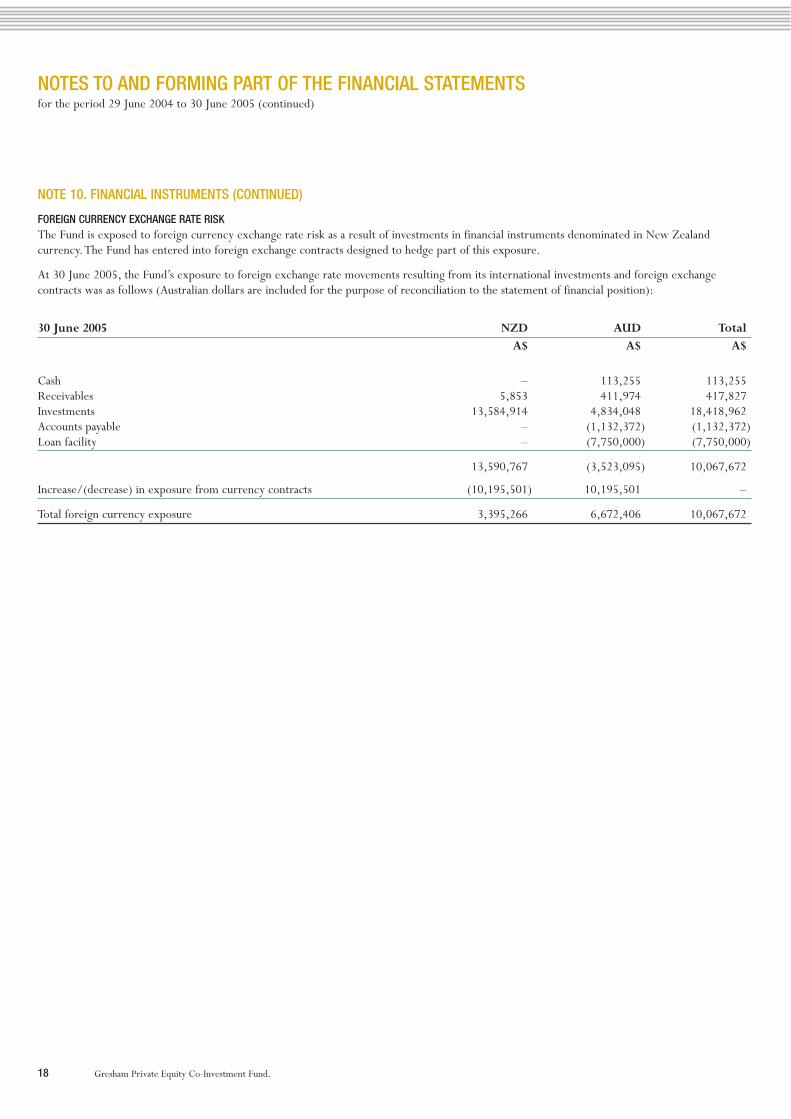

FOREIGN CURRENCY EXCHANGE RATE RISKThe Fund is exposed to foreign currency exchange rate risk as a result of investments in financial instruments denominated in New Zealandcurrency.The Fund has entered into foreign exchange contracts designed to hedge part of this exposure.

At 30 June 2005, the Fund’s exposure to foreign exchange rate movements resulting from its international investments and foreign exchangecontracts was as follows (Australian dollars are included for the purpose of reconciliation to the statement of financial position):

30 June 2005 NZD AUD TotalA$ A$ A$

Cash – 113,255 113,255Receivables 5,853 411,974 417,827Investments 13,584,914 4,834,048 18,418,962Accounts payable – (1,132,372) (1,132,372)Loan facility – (7,750,000) (7,750,000)

13,590,767 (3,523,095) 10,067,672

Increase/(decrease) in exposure from currency contracts (10,195,501) 10,195,501 –

Total foreign currency exposure 3,395,266 6,672,406 10,067,672

Annual Report 2005. 19

Directors’ and executives’ disclosures:

The Responsible Entity’s parent, Gresham Partners Limited, as the employer company for the Gresham Partners Limited group, pays theremuneration of those directors of the Responsible Entity who are employees of Gresham Partners Limited. No remuneration was paid to any director of the Responsible Entity directly out of the Fund or by the Responsible Entity. In accordance with guidance from the AustralianAccounting Standards Board, the amount of remuneration paid to directors directly by the Fund; the Responsible Entity; and the apportionedamounts of remuneration paid to directors by the Responsible Entity’s parent entity in relation to the Fund, are to be disclosed in the Fund’sfinancial report.The apportioned amounts disclosed below have been based on estimates of time spent by the relevant director on the Fund,and exclude amounts in relation to the estimated time spent by the relevant director on behalf of Gresham Private Equity Fund 2a and 2b pursuingthe identical investment opportunities of this Fund.These apportioned amounts are derived from the allocation of time used for the purposes of preparing the internal management accounts of the Gresham Partners Limited group.

NOTES TO AND FORMING PART OF THE FINANCIAL STATEMENTSfor the period 29 June 2004 to 30 June 2005 (continued)

NOTE 11. RELATED PARTIES

The Responsible Entity of the Fund is Gresham Funds Management Limited, which is incorporated and domiciled in Australia.The registered officeand principal place of business is:

Level 6175 Macquarie StreetSydney NSW 2000

The custodian of the Fund is ANZ Custodian Services Limited.

The directors of the Responsible Entity during the financial period were:

James P Graham, ChairmanRoger S Casey, Joint Managing Director Roy D McKelvie, Joint Managing Director Antony G BreuerMichael A Chaney AO (ceased 29 June 2005)Richard J B Goyder Graham J RichGrant W Schmidt (ceased 31 March 2005)Gene T Tilbrook (appointed 29 June 2005)

Transactions with related parties are set out below:

Responsible Entity’s remuneration:

29 June 2004 to

30 June 2005$

Responsible Entity’s remuneration paid or payable in accordance with the provisions of the Constitution 1,953,984

Service fee paid or payable in accordance with the provisions of the Constitution (refer Note 16) 669,168

Balances with related parties:The aggregate amounts payable to related parties by the Fund at balance date comprise:

Responsible Entity 882,937

Gresham Private Equity Co-Investment Fund.20

NOTES TO AND FORMING PART OF THE FINANCIAL STATEMENTSfor the period 29 June 2004 to 30 June 2005 (continued)

NOTE 11. RELATED PARTIES (CONTINUED)

29 June 2004 to

30 June 2005$

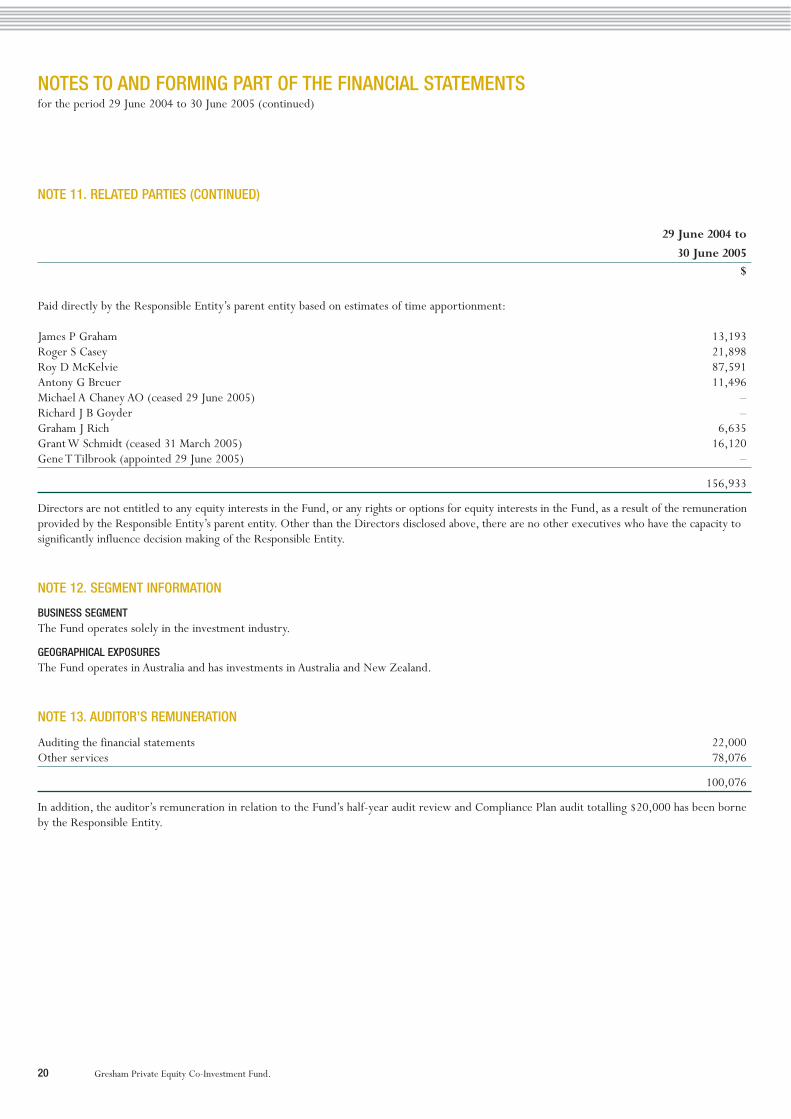

Paid directly by the Responsible Entity’s parent entity based on estimates of time apportionment:

James P Graham 13,193Roger S Casey 21,898Roy D McKelvie 87,591Antony G Breuer 11,496Michael A Chaney AO (ceased 29 June 2005) –Richard J B Goyder –Graham J Rich 6,635Grant W Schmidt (ceased 31 March 2005) 16,120Gene T Tilbrook (appointed 29 June 2005) –

156,933

Directors are not entitled to any equity interests in the Fund, or any rights or options for equity interests in the Fund, as a result of the remunerationprovided by the Responsible Entity’s parent entity. Other than the Directors disclosed above, there are no other executives who have the capacity tosignificantly influence decision making of the Responsible Entity.

NOTE 12. SEGMENT INFORMATION

BUSINESS SEGMENTThe Fund operates solely in the investment industry.

GEOGRAPHICAL EXPOSURESThe Fund operates in Australia and has investments in Australia and New Zealand.

NOTE 13. AUDITOR’S REMUNERATION

Auditing the financial statements 22,000Other services 78,076

100,076

In addition, the auditor’s remuneration in relation to the Fund’s half-year audit review and Compliance Plan audit totalling $20,000 has been borneby the Responsible Entity.

Annual Report 2005. 21

NOTES TO AND FORMING PART OF THE FINANCIAL STATEMENTSfor the period 29 June 2004 to 30 June 2005 (continued)

NOTE 14. CAPITAL COMMITMENTS

As at 30 June 2005, the Fund had no undrawn capital commitments.

NOTE 15. CONTINGENT LIABILITIES

No contingent liabilities have arisen during the period ended 30 June 2005.

NOTE 16. EVENTS OCCURRING AFTER REPORTING DATE

Following the Fund’s establishment period, the Responsible Entity has decided to reduce the service fee from 0.75% to 0.50% per annum of committed capital, commencing on 1 July 2005.The Responsible Entity will review the service fee level on an ongoing annual basis for any subsequent adjustments up or down.

NOTE 17. IMPACT OF ADOPTING AUSTRALIAN EQUIVALENTS TO INTERNATIONAL FINANCIAL REPORTING STANDARDS

For reporting periods beginning on or after 1 January 2005, the Fund must comply with Australian equivalents to International Financial ReportingStandards (“AIFRS”) as issued by the Australian Accounting Standards Board.This financial report has been prepared in accordance with Australianaccounting standards and other financial reporting requirements (“Australian GAAP”) applicable for reporting periods ended 30 June 2005.

TRANSITION MANAGEMENTThe Responsible Entity has sought advice from its external advisers and the Fund is expected to be in a position to fully comply with therequirements of AIFRS for the first time in the Fund’s financial statements for the financial year ended 30 June 2006.

To date the Responsible Entity has analysed most of the AIFRS and has identified accounting policy changes that will be required.The rules for first time adoption of AIFRS are set out in AASB 1 First Time Adoption of Australian Equivalents to International Financial Reporting Standards.In general, AIFRS accounting policies are required to be applied retrospectively to determine the opening balance sheet under AIFRS. In some cases choices of accounting policies are available, including elective exemptions to this general principle to assist in the transition to reporting under AIFRS.These choices have been analysed to determine the most appropriate accounting policy for the Fund.

Funds complying with AIFRS for the first time will be required to restate their comparative financial statements to amounts reflecting theapplication of AIFRS to that comparative period.With the exception of certain elections in AASB 1, most adjustments required on transition to AIFRS will be made, retrospectively, against opening net assets attributable to unitholders as at 1 July 2004.

IMPACT OF TRANSITION TO AIFRSThe impact of transition to AIFRS including the transitional adjustments disclosed in the reconciliations from current Australian GAAP to AIFRS,and the selection and application to AIFRS accounting policies, are based on AIFRS standards that the Responsible Entity expects to be in place,or where applicable, adopted early, when preparing the first complete AIFRS financial report.The reconciliations disclosed below assume that the Fund will apply the requirements of AASB 132 Financial Instruments: Disclosure and Presentation and AASB 139: Financial Instruments:Recognition and Measurement in the first comparative year under AIFRS.

Although the adjustments disclosed in this note are based on the Responsible Entity’s best knowledge of expected standards and interpretations,and current facts and circumstances, these may change.

Revisions to the selection and application of the AIFRS accounting policies may be required as a result of:

• changes in financial reporting requirements that are relevant to the Fund’s first complete AIFRS financial report arising from new or revisedaccounting standards or interpretations issued by the Australian Accounting Standards Board subsequent to the preparation of the 30 June 2005financial report;

• additional guidance on the application of AIFRS in a particular industry or to a particular transaction; or

• changes to the Fund’s operations.

Therefore, until the Fund prepares its first full AIFRS financial statements, the possibility cannot be excluded that the accompanying disclosures may have to be adjusted and consequently, the final reconciliations presented in the first financial report prepared in accordance with AIFRS mayvary materially from the reconciliations provided below.

Gresham Private Equity Co-Investment Fund.22

NOTE 17. IMPACT OF ADOPTING AUSTRALIAN EQUIVALENTS TO INTERNATIONAL FINANCIAL REPORTING STANDARDS (CONTINUED)

The significant changes in accounting policies and the associated transitional arrangements adopted in preparing the AIFRS reconciliations and theelections made under AASB 1 are set out below.

(a) Financial liabilities

In accordance with AASB 132, unitholders’ funds are defined as “puttable instruments” and no longer classed as equity but rather as debt.Therefore, a liability must be recognised for the fair value of the units. Unitholders’ funds are classed as debt and disclosed as “Net assetsattributable to unitholders”.

(b) Transaction costs

AASB 139 states that the initial measurement (cost) on acquisition of investments shall not include directly attributable transaction costs such as feesand commissions paid to agents. Incremental transaction costs should be expensed as incurred in the statement of financial performance.This differsfrom the current treatment where incremental transaction costs on acquisition of investments are included within initial measurement cost.

On transition to AIFRS this change will not impact net assets attributable to unitholders, however, the classification of gains and losses betweenrealised and unrealised in the statement of financial performance may differ.

(c) Financing costs

As unitholders’ funds are classed as debt under AIFRS, it will be necessary to recognise “distribution expense to unitholders” and “change in net assetvalue attributable to unitholders” in the statement of financial performance as a financing cost. In future periods, the statement of financialperformance of the Fund will disclose a nil result.

This differs from the current treatment where the net profit for the year is disclosed as available for distribution to unitholders, however, there is no impact to net assets attributable to unitholders.

The reconciliation below summarises the known or reliably estimable significant impacts on the Fund’s net asset position and net operating incomeas currently reported in the financial report for the period ended 30 June 2005 had it been prepared using AIFRS.The reconciliations have beenprepared on the assumption that the Fund will apply the requirements of AASB 132 Financial Instruments: Disclosure and Presentation and AASB139: Financial Instruments: Recognition and Measurement in the first comparative year under AIFRS.The expected financial effects of adoptingAIFRS have been shown for significant items comprising net assets in the statement of financial position and net operating income/(loss) in thestatement of financial performance with descriptions of the differences. No disclosures have been made for re-classifications within the statement of financial position and statement of financial performance that have no impact on net assets or net operating income/(loss).

Note 2005$

RECONCILIATION OF NET ASSET VALUE

Net asset value under AGAAP 10,067,672

Net assets attributable to unitholders 10,067,672Reclassification of unitholders’ funds 17(a) (10,067,672)

Net asset value under AIFRS –

RECONCILIATION OF NET OPERATING INCOME/(LOSS)

Net operating income/(loss) under AGAAP (2,638,823)Reclassification to financing costs of changes in net asset value attributable to unitholders 17(c) 2,638,823

Net operating income/(loss) under AIFRS –

NOTES TO AND FORMING PART OF THE FINANCIAL STATEMENTSfor the period 29 June 2004 to 30 June 2005 (continued)

Annual Report 2005. 23

In the Directors’ opinion:

(a) the financial statements and notes set out on pages 11 to 22 are in accordance with the Corporations Act 2001, including:

(i) complying with Accounting Standards, the Corporations Regulations 2001 and other mandatory professional reporting requirements; and

(ii) giving a true and fair view of the Fund’s financial position as at 30 June 2005 and of its performance, as represented by the results of itsoperations and its cash flows, for the financial period ended on that date; and

(b) there are reasonable grounds to believe that the Fund will be able to pay its debts as and when they become due and payable.

This declaration is made in accordance with a resolution of the Directors.

James P GrahamDirector

Sydney, 27 July 2005

DIRECTORS’ DECLARATION

Gresham Private Equity Co-Investment Fund.24

INDEPENDENT AUDIT REPORT TO THE MEMBERS OF GRESHAM PRIVATE EQUITY CO-INVESTMENT FUND

MATTERS RELATING TO THE ELECTRONIC PRESENTATION OF THE AUDITED FINANCIAL REPORTThis audit report relates to the financial report of Gresham PrivateEquity Co-Investment Fund (the fund) for the financial period ended 30June 2005 included on Gresham Private Equity Co-Investment Fundweb site.The directors of the fund’s responsible entity are responsiblefor the integrity of the Gresham Private Equity Co-Investment Fundweb site.We have not been engaged to report on the integrity of thisweb site.The audit report refers only to the financial report identifiedbelow. It does not provide an opinion on any other information whichmay have been hyperlinked to/from the financial report. If users of thisreport are concerned with the inherent risks arising from electronicdata communications they are advised to refer to the hard copy of theaudited financial report to confirm the information included in theaudited financial report presented on this web site.

AUDIT OPINIONIn our opinion, the financial report of Gresham Private Equity Co-Investment Fund:

• gives a true and fair view, as required by the Corporations Act 2001 in Australia, of the financial position of Gresham Private Equity Co-Investment Fund as at 30 June 2005, and of its performance for the period ended on that date, and

• is presented in accordance with the Corporations Act 2001, AccountingStandards and other mandatory financial reporting requirements in Australia, and the Corporations Regulations 2001.

This opinion must be read in conjunction with the rest of our audit report.

SCOPEThe financial report and directors’ responsibilityThe financial report comprises the statement of financial position,statement of financial performance, statement of cash flows, accompanyingnotes to the financial statements, and the directors’ declaration forGresham Private Equity Co-Investment Fund (the fund), for the periodended 30 June 2005.

The directors of the responsible entity of the fund are responsible for the preparation and true and fair presentation of the financial report inaccordance with the Corporations Act 2001.This includes responsibility forthe maintenance of adequate accounting records and internal controls thatare designed to prevent and detect fraud and error, and for the accountingpolicies and accounting estimates inherent in the financial report.

AUDIT APPROACHWe conducted an independent audit in order to express an opinion to the unitholders of the fund. Our audit was conducted in accordance withAustralian Auditing Standards, in order to provide reasonable assurance as to whether the financial report is free of material misstatement.Thenature of an audit is influenced by factors such as the use of professionaljudgement, selective testing, the inherent limitations of internal control,and the availability of persuasive rather than conclusive evidence.Therefore, an audit cannot guarantee that all material misstatements

have been detected. For further explanation of an audit, visit our websitehttp://www.pwc.com/au/financialstatementaudit.

We performed procedures to assess whether in all material respects the financial report presents fairly, in accordance with the CorporationsAct 2001, Accounting Standards and other mandatory financial reportingrequirements in Australia, a view which is consistent with ourunderstanding of the fund’s financial position, and its performance as represented by the results of its operations and cash flows.

We formed our audit opinion on the basis of these procedures, whichincluded:

• examining, on a test basis, information to provide evidencesupporting the amounts and disclosures in the financial report, and

• assessing the appropriateness of the accounting policies anddisclosures used and the reasonableness of significant accountingestimates made by the directors.

Our procedures include reading the other information in the AnnualReport to determine whether it contains any material inconsistencies with the financial report.

While we considered the effectiveness of management’s internalcontrols over financial reporting when determining the nature andextent of our procedures, our audit was not designed to provideassurance on internal controls.

Our audit did not involve an analysis of the prudence of businessdecisions made by directors or management.

INDEPENDENCEIn conducting our audit, we followed applicable independencerequirements of Australian professional ethical pronouncements and the Corporations Act 2001.

PricewaterhouseCoopers

AJ Loveridge SydneyPartner 27 July 2005

Liability is limited by the Accountant’s Scheme under the Professional Standards Act 1994 (NSW).

Annual Report 2005. 25

DIRECTORY

RESPONSIBLE ENTITY

GRESHAM FUNDS MANAGEMENT LIMITEDABN 32 109 020 153

Registered Office:Level 6, 175 Macquarie StreetSydney NSW 2000 AustraliaTelephone: 61 2 9221 5133Facsimile: 61 2 9223 9072

MANAGER

GRESHAM PRIVATE EQUITY LIMITEDABN 86 084 509 946

Registered Office:Level 6, 175 Macquarie StreetSydney NSW 2000 AustraliaTelephone: 61 2 9221 5133Facsimile: 61 2 9223 9072

DIRECTORS OF RESPONSIBLE ENTITY

James Graham, ChairmanRoger Casey, Joint Managing DirectorRoy McKelvie, Joint Managing DirectorTony BreuerRichard GoyderGraham RichGene Tilbrook

REGISTRY

COMPUTERSHARE INVESTOR SERVICES PTY LTDLevel 3, 60 Carrington StreetSydney NSW 2000 AustraliaTelephone: 1300 855 080Outside Australia: 61 3 9415 4000Facsimile: 61 2 8234 5050

SPONSORING BROKERS

GOLDMAN SACHS JBWERELevel 42, Governor Phillip Tower1 Farrer PlaceSydney NSW 2000 Australia

ABN AMRO MORGANSLevel 29, Riverside Centre123 Eagle StreetBrisbane QLD 4000 Australia

MACQUARIE EQUITIESLevel 18, 20 Bond StreetSydney NSW 2000 Australia

ORD MINNETTLevel 8, NAB House255 George StreetSydney NSW 2000 Australia

SOLICITORS

FREEHILLSLevel 32, MLC Centre19 Martin PlaceSydney NSW 2000 Australia

TAX ADVISER

PRICEWATERHOUSECOOPERS201 Sussex StreetSydney NSW 2000 Australia

AUDITOR

PRICEWATERHOUSECOOPERS201 Sussex StreetSydney NSW 2000 Australia

Des

igne

d an

d pr

oduc

ed b

y The

Gla

ssho

use,

Sydn

ey.