greece: state of economy, outlook and major challenges

TRANSCRIPT

Greece: state of economy, outlook

and major challengesDimitris Malliaropulos

Bank of Greece

&

University of Piraeus

Presentation in CRETE 2017 Conference

Milos, July 12 2017

Bank of Greece, Economic Analysis and Research Department

2Bank of Greece, Economic Analysis and Research Department

1. Economic adjustment during the crisis

2. Current state of economy

3. Strengths and weaknesses of economic recovery

4. Economic outlook and risks

5. What can policy do? Preconditions for a sustainable recovery

Outline

3Bank of Greece, Economic Analysis and Research Department

Fiscal and external deficits have been eliminated and cost

competitiveness has been restored

General Government primary balance

(% of GDP, programme definition)

Source: Eurostat, Bank of Greece.

Deficit

Surplus

Current account balance (% of GDP) and

Competitiveness (Index)

Source: Bank of Greece, ECB.

4Bank of Greece, Economic Analysis and Research Department

Exports increased and tradeable sector gained a higher share in the

economy

Tradeables: agriculture, industry, business and financial services,

telecommunications and services related to tourism (transport and

accommodation and restaurants).

Non-tradeables: all else except public administration and non-market services.

Relative size of tradeable to non-

tradeable sector (index: 2010=1)

Source: Eurostat and Bank of Greece.

Exports of goods at constant prices

(index: 2009=100)

5Bank of Greece, Economic Analysis and Research Department

Source: ELSTAT.

Where do we stand now?

Recession is over but economy is trapped in stagnation since 2014

Economic recovery has faced two major

headwinds in 2016 and early 2017

1. Increased uncertainty due to delays in

closing 1st and 2nd review.

2. Fiscal over-performance: 4.2% of GDP

primary surplus in 2016 against target of

0.5% of GDP.

Real GDP increased in Q2-Q3 2016 but

turned negative in Q4. Turned +ve in Q1.

Conclusion of 2nd review in June improves short-

term outlook

Resolution of uncertainty will allow

positive momentum to continue.

Nevertheless, recovery remains fragile.

Real GDP growth decomposition

(annual % change, pp contributions)

6Bank of Greece, Economic Analysis and Research Department

Strengths

• Industry-Manufacturing

• Exports

• Labour market

Weaknesses

• Consumer

• Investment

• Banks

Major strengths and weaknesses of current recovery

7Bank of Greece, Economic Analysis and Research Department

Industry and manufacturing

Sector is expanding at healthy rates since mid-2015.

Rebound largely driven by increasing exports due to lower wage

costs and higher competitiveness.

Industrial confidence improved significantly since mid-2015.

Industrial production on an upward trend.

8Bank of Greece, Economic Analysis and Research Department

The recovery is broad-based: 17 out of 24 manufacturing sectors posted positive growth

in 2016Industrial production and industrial confidence(annual % change and balance)

Sources: ELSTAT, European Commission.

9Bank of Greece, Economic Analysis and Research Department

Exports Exports of goods increased on average by 6% annually in real

terms over the past seven years.

Exports of services (ex shipping) increased by 4% annually in

real terms over the same period.

Underperformance of Greek exports relative to peers is due to

developments in the shipping sector.

Shipping sector suffered from global supply overhang. Capital

controls also affected the sector.

Exports of services(index: 2000=100, constant prices )

Source: Eurostat Ameco. Ireland excluded from Graphs due to distortion of export data following the 2015 GDP revision.

Exports of goods(index: 2000=100, constant prices )

10Bank of Greece, Economic Analysis and Research Department

Exports of goods have benefited from increased competitiveness. Exports

of services underperformed after 2008

Shipping sector explains most of underperformance of exports,

particularly after imposition of capital controls in June 2015

11Bank of Greece, Economic Analysis and Research Department

Source: Eurostat and Bank of Greece.

Real exports of goods and services

(index: 2009=100) Euro area (147)

Greece with Shipping (114)

Underperformance of shipping

sector has cut export growth

by a whole 27 ppts!

Greece without Shipping (141)

12Bank of Greece, Economic Analysis and Research Department

Labour market

Employment is growing at healthy rates since mid-2014.

Rebound largely driven by higher job-market flexibility due to

past structural reforms.

Nevertheless, unemployment remains very high (21.7% in April).

Labour market recovery continues for the third year despite GDP

stagnating.

13Bank of Greece, Economic Analysis and Research Department

Source: ELSTAT, Labour Force Survey.

Employment

(y-o-y growth)

Employment growth turned positive since mid-2014

Net job creation is to a large extent due to increased labour market

flexibility

Source: OAED and ERGANI.

Net dependent employment flows

(cumulative net flows; number of jobs)

14Bank of Greece, Economic Analysis and Research Department

Consumers

Consumers remain pessimistic.

Disposable income still declining despite rebound in employment

due to higher taxation and lower net social transfers.

Deleveraging and dissaving continue.

Consumer confidence remains weak, holding down retail sales and

personal consumption growth

15Bank of Greece, Economic Analysis and Research Department

Sources: ELSTAT and European Commission.

Retail sales and consumer confidence(annual % change and balance)

Post-election euphoria

Disappointment

Disposable income is gradually stabilizing but remains in negative territory.

Taxation and decline in social transfers among negative drivers.

16Bank of Greece, Economic Analysis and Research Department

Source: ELSTAT and Bank of Greece calculations.

Disposable income of households and components

(annual % change; pp contributions) Private sector is creating jobs and

income

But increased taxation and cuts in net

social transfers reduce disposable

income.

Hence, job creation fails to translate into

consumption growth.

17Bank of Greece, Economic Analysis and Research Department

Sources: ECB and Bank of Greece.

Households continue deleveraging and dissaving

deleveraging

dissaving

18Bank of Greece, Economic Analysis and Research Department

Banking sector

Two key issues: liquidity, asset quality.

Bank funding conditions gradually improve, but deleveraging

continues and NPLs remain the biggest challenge.

“Credit-less recovery” not unlikely but weak and not desirable.

Urgent need to restore normal credit conditions. Tackle NPLs.

Source: Bank of Greece.

Greek banks borrowing from Eurosystem

(EUR bn; end of month)

Bank of Greece, Economic Analysis and Research Department 19

Bank funding: gradual recovery of deposits and lower dependence

on Eurosystem financing

Deposits of NFCs and households

(EUR bn; monthly flow and outstanding

amount)

Source: Bank of Greece.

Bank credit: Deleveraging of private sector continues.

NPL ratios stabilise at high levels

20Bank of Greece, Economic Analysis and Research Department

Source: Bank of Greece.

Bank credit to NFCs and households(EUR bn; outstanding amounts)

Greek commercial banks – NPL ratio(%)

Source: Bank of Greece.

21Bank of Greece, Economic Analysis and Research Department

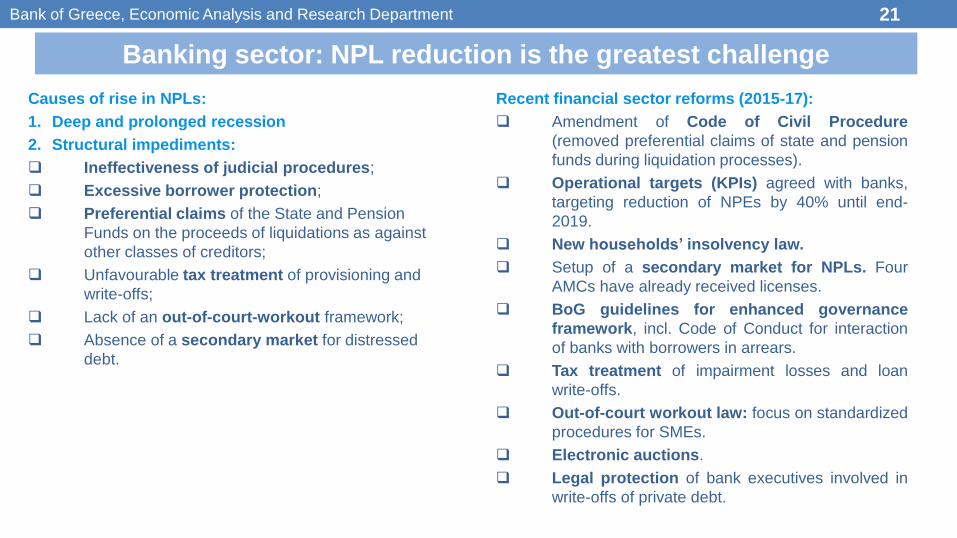

Banking sector: NPL reduction is the greatest challenge

Recent financial sector reforms (2015-17):

Amendment of Code of Civil Procedure

(removed preferential claims of state and pension

funds during liquidation processes).

Operational targets (KPIs) agreed with banks,

targeting reduction of NPEs by 40% until end-

2019.

New households’ insolvency law.

Setup of a secondary market for NPLs. Four

AMCs have already received licenses.

BoG guidelines for enhanced governance

framework, incl. Code of Conduct for interaction

of banks with borrowers in arrears.

Tax treatment of impairment losses and loan

write-offs.

Out-of-court workout law: focus on standardized

procedures for SMEs.

Electronic auctions.

Legal protection of bank executives involved in

write-offs of private debt.

Causes of rise in NPLs:

1. Deep and prolonged recession

2. Structural impediments:

Ineffectiveness of judicial procedures;

Excessive borrower protection;

Preferential claims of the State and Pension

Funds on the proceeds of liquidations as against

other classes of creditors;

Unfavourable tax treatment of provisioning and

write-offs;

Lack of an out-of-court-workout framework;

Absence of a secondary market for distressed

debt.

22Bank of Greece, Economic Analysis and Research Department

Investment and Financing

Investment declined dramatically since 2008.

80% of decline was in residential investment.

Net investment has become negative since 2011. Decline in

capital stock!

Financing conditions of NFCs gradually improving.

However, domestic saving is not sufficient to finance

investment.

Need to restore normal bank credit conditions (NPL resolution).

Need to restore access of companies to capital markets.

Need to attract FDI.

23Bank of Greece, Economic Analysis and Research Department

Private investment has declined dramatically

Sources: ECB and Bank of Greece.

Private investment (NFCs and HHs)

(% of GDP)

Investment gap

Investment of NFCs

(flows; 4-quarter moving sum; EUR mn)

Investment gap

Gross Investment declined below deprecation since 2011. Negative net investment.

Investment gap of private sector is currently EUR 15 bn p.a. (9% of GDP).

For Non-Financial Companies, investment gap is EUR 6.5 bn p.a. (3.7% of GDP).

Given rate of depreciation, even if NFCs’ gross investment increases by 8% p.a., it will take 6 years until net

investment becomes positive and 9 years until capital stock of NFCs increases to 2008 levels.

Greece needs an investment shock to avert output hysteresis.

24Bank of Greece, Economic Analysis and Research Department

Source: ECB and Bank of Greece.

External financing of NFCs is gradually improving

External financing of Non-Financial Companies

(flows; 4-quarter moving sum; EUR bn)

*includes trade credit and advances and other accounts receivable/payable.

Has deleveraging of NFCs

come to and end?

25Bank of Greece, Economic Analysis and Research Department

Economic Outlook

26Bank of Greece, Economic Analysis and Research Department

Short-term economic outlook

Growth outlook

With the conclusion of the 2nd review, positive momentum expected to continue over the short and medium term

(Real GDP growth 2017: 1.6%, 2018: 2.4%).

Public consumption and investment expected to support economic activity in 2017.

o Part of fiscal over-performance in 2016 can be used to increase expenditure or reduce taxation.

Private consumption expected to rebound modestly, driven by continuing gains in employment.

Exports expected to increase further, driven by past gains in competitiveness and stronger global growth.

o Tourism: bookings indicate strong growth in 2017. June data suggest strong rebound of both arrivals and earnings.

Upside risks

Specification of debt relief measures

QE participation

Fiscal impulse in 2017

Downside risks

Programme implementation

Fiscal mix not growth-friendly

Major stock imbalances will be a drag on growth: public debt, NPLs, unemployment

External risks (global, regional, markets)

27Bank of Greece, Economic Analysis and Research Department

Long-term economic outlook is positive

Structural reforms improve growth potential.

o OECD estimates that implemented and planned reforms are expected to boost real GDP by 13% over a 10-

year horizon. BoG has similar estimates.

o Potential growth estimated at 1.5% p.a.

Rebalancing the economy towards a “new growth model” is the great challenge

o From the demand side: Investment and exports must fill the gap of effective demand from lower public and

private consumption. Feasible.

o From the supply side: Rebalancing towards tradeable goods and services.

Note: Net profit margins are calculated as Net Operating Surplus/GVA. Source: Eurostat and Bank of Greece calculations.

28Bank of Greece, Economic Analysis and Research Department

Potential growth mainly driven by TFP.

TFP is driven by net investment

Periods of high (low) potential growth coincide with periods of high (low) TFP growth.

High correlation between TFP growth and capital accumulation (0.62).

TFP growth is related to growth of

capital stock

Sources: Eurostat Ameco and Bank of Greece.

Decomposition of potential growth

(%; bars pp contributions)

29Bank of Greece, Economic Analysis and Research Department

Sources: ELSTAT and Bank of Greece.

Potential growth to gradually converge to 1.5%+.

Drivers differ across time

Large pool of unemployed provides initial space for economy to grow.

Capital stock to continue to decline due to negative net investment until 2020.

TFP growth to gradually increase as capital stock increases and structural reforms start to pay dividends.

Potential growth projections

(%; bars pp contributions)

30Bank of Greece, Economic Analysis and Research Department

Preconditions for a sustained recovery

1. Get ownership of reforms: Delays in implementation will result in new spikes of uncertainty and a

fallback to economic stagnation.

2. Focus on growth: Having completed the fiscal consolidation required by the program, economic

policy should now focus on growth. Putting the economy on a sustainable growth path will gradually

reduce unemployment, allow households and companies to repay their debts and generate the funds

to service and gradually reduce the public debt burden.

3. Fiscal policy must stop being a drag on economic activity; the fiscal buffer created in 2016 can help

reduce taxation already in the current year; increased public investment can also provide a positive

impulse to the economy.

4. Tackle NPLs: Recent financial sector reforms must be implemented swiftly in order to tackle the

problem of high NPLs in banks’ portfolios. This will allow banks to start lending again and companies

to finance their investment projects.

5. Debt relief: European partners must specify the medium term debt relief measures to ensure

sustainability of public debt. This would help Greece return to international financial markets, abolish

capital controls and return to financial normality. Postponing the decision on debt relief further down

the road does not serve the purpose of a sustainable comeback to financial markets and a

sustainable recovery of the Greek economy.

31Bank of Greece, Economic Analysis and Research Department

Thank you for your attention