grains eu sugarmarketunsettled afterthe end of quotas · grains ¨ strategie-grains.com oct-sept...

TRANSCRIPT

stratégiegrains®

strategie-grains.com

EU sugar market unsettledafter the end of quotas

October 25, 2018

stratégiegrains®

strategie-grains.com

100

200

300

400

500

600

700

800

900

1000

1100

Oct -06

May-07

Dec-07

Jul-08

Feb-09

Sep-09Apr-10

Nov-10

Jun-11

Jan-12

Aug -12

Mar-13

Oct -13

May-14

Dec-14

Jul-15

Feb-16

Sep-16Apr-17

Nov-17

Jun-18

RAW SUGAR

WHITE SUGAR

EU QUOTA SUGAR

EU NON QUOTA SUGAR

EU SUGAR

European prices have been collapsing for more than a year, reaching historical lows

25/10/2018 Sugar Outlook 2

§ -17% betweenOct 2017 and Aug 2018

§ Raw sugar pricedown 24% between Oct17 and Sept18

§White sugardown 12%

$/t

stratégiegrains®

strategie-grains.com

In a very heavy global market

§ Large production increases in 2017/18 in many regions of the world

§ Big increase in world stocks

§Decreasing Brazilian real value

25/10/2018 Sugar Outlook 3

-280

102454446 4677

20513

Brazil

India

EU Thailand

World

Changes in 2017/18 production compared to 2016/17 (kt raw eq.)

Dollar vs. Real value

3,13

4,19

stratégiegrains®

strategie-grains.com

European sugar beet production down in 2018/19 despite stable growing area

§ Beet roots suffered fromlate plantings and dry summer weather

25/10/2018 Sugar Outlook 4

Changes in sugar beet production between 2017 and 2018

111.7140.5

125.6

2016/17 2017/18 2018/19

EU sugar beet crop (Mt)

stratégiegrains®

strategie-grains.com

Sugar production to decrease by more than 2 Mt to 19 Mt

§ Sugar campaign started with some delay and should be shorter than last year

25/10/2018 Sugar Outlook 5

Main changes in 2018 sugar production compared to 2017 (Mt white eq.)

-950 -848

-223 -180 -177 -151

170

-2244

Fran

ce

Ger

man

y

Belg

ium

Aust

ria

Net

herla

nds

Czec

h Re

p.

Italy

Tota

l EU

stratégiegrains®

strategie-grains.com

Contrary to expectations, isoglucose production is decreasing§ Low sugar prices and higher

grain prices => isoglucose isnot competitive

§Despite the opening of a new plant in Hungary

§ 2018/19 isoglucose production close to 2017/18

25/10/2018 Sugar Outlook 6

EU production of isoglucose (kt)

780

600 600

2016/17 2017/18 2018/19

stratégiegrains®

strategie-grains.com

Domestic market more attractive thanexports§Downward trend for per

capita sugar intake but less competition thananticipated from othersweeteners

§ Industrial demand down with availabilities

§ Attractive ethanol outlet

25/10/2018 Sugar Outlook 7

31,530,9 30,7

2016/17 2017/18 2018/19

EU per capita sugar consumption (kg/year)

-75-175

156

-94

food industrial bioethanol total

Changes in 2018/19 EU sugar consumptioncompared to 2017/18 (kt white eq.)

stratégiegrains®

strategie-grains.com

EU exports forecast down, imports stable

25/10/2018 Sugar Outlook 8

14%

34%

22%

17%

10%

3%North Africa

Near andMiddle EastOther Africa

Europe outsideEUAsiancountriesOthercountries

§Countries around the Mediterranean should remain the main market for EU sugar

1607

3640

1587

2619

0500

1000150020002500300035004000

imports exports

EU imports and exports (kt white eq.)

2017/18 2018/19

stratégiegrains®

strategie-grains.com

12 %

14 %

16 %

18 %

20 %

22 %

24 %

26 %

28 %

30 %

32 %

20 0

25 0

30 0

35 0

40 0

45 0

50 0

55 0

60 0

65 0

2009/10

2010/11

2011/12

2012/13

2013/14

2014/15

2015/16

2016/17

2017/18

2018/19

raw sugar average price ($/t)stocks/ use (%)

World stocks to remain high in 2018/19

§ 2018/19 production forecastto decrease to a level close to consumption

25/10/2018 Sugar Outlook 9

9

§ Average raw sugar priceexpected close to 290 $/t

§White sugar price close to 370-380 $/t

-8270

1808

-2315 -930

-9421

Braz

il

Indi

a

EU Thai

land

Wor

ld

Changes in 2018/19 production compared to 2017/18 (kt raw eq.)

stratégiegrains®

strategie-grains.com

Oct-Sept 2017/18 2018/19carry-in stock 2.1 2.6production 21.1 18.9imports 1.6 1.6consumption 18.7 18.5exports 3.6 2.6carry-out stock 2.6 2.0stock/use ratio 11.7% 9.5%

Fragile EU balance sheet should maintain a premium for EU sugar

25/10/2018 Sugar Outlook

EU balance sheet (Mt white eq.) § World prices should continue to weight on European prices

§ EU premium maintained around50 €/t

§ 2018/19 average EU pricedecreasing to 360-370 €/t (376 €/t on average for Oct17-Aug18)

10

stratégiegrains®

strategie-grains.com

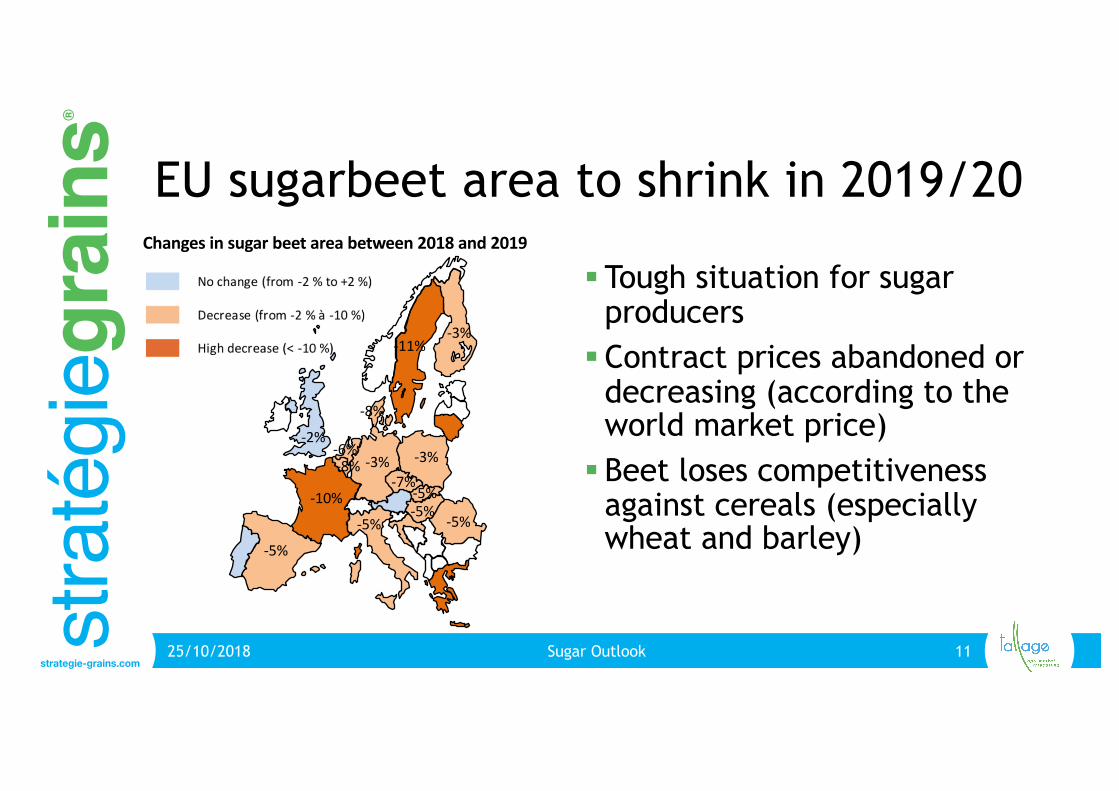

EU sugarbeet area to shrink in 2019/20

§ Tough situation for sugarproducers

§Contract prices abandoned or decreasing (according to the world market price)

§ Beet loses competitivenessagainst cereals (especiallywheat and barley)

25/10/2018 Sugar Outlook 11

Changes in sugar beet area between 2018 and 2019

-10%

-11%

-3% -3%-2%

-6%

-7%-8%

-8%

-5%

-5%-5%-5%-5%

-3%

stratégiegrains®

strategie-grains.com

First prospects for 2019/20 beet and sugar production

§ Lower area does not necessarily mean lowerproduction

§ Sugar production between17,5 Mt and 20,5 Mt

25/10/2018 Sugar Outlook 12

118

141

126 125

138

105

110

115

120

125

130

135

140

145

2017/18 2018/19 2019/20

EU sugar beet production (Mt)

Low yield = 2018

Average yield = 5-year average

Good yield = 5% above trend

stratégiegrains®

strategie-grains.com

Thank you for your attention

Any questions?

• Sugar analyst: Madeleine Breguet• Crop analysts (EU/Black Sea): Benoit Fayaud, Jean-Sébastien Jacquet, Laurine Simon

13