goa stimulus report

TRANSCRIPT

8/14/2019 GOA Stimulus Report

http://slidepdf.com/reader/full/goa-stimulus-report 1/42

GAOUnited States Government Accountability Office

TestimonyBefore the Committee on HomelandSecurity and Governmental Affairs, U.S.Senate

RECOVERY ACT

As Initial ImplementationUnfolds in States andLocalities, Continued

Attention to AccountabilityIssues Is Essential

Statement of Gene L. Dodaro Acting Comptroller General of the United States

For Release on DeliveryExpected at 9:00 a.m. EDTThursday, April 23, 2009

GAO-09-631T

8/14/2019 GOA Stimulus Report

http://slidepdf.com/reader/full/goa-stimulus-report 2/42

Page 1 GAO-09-631T

Mr. Chairman, Ranking Member Collins, and Members of the Committee:

I am pleased to be here today to discuss our work examining the uses and planning by selected states and localities for funds made available by the American Recovery and Reinvestment Act of 2009 (Recovery Act). 1 TheRecovery Act is estimated to cost about $787 billion over the next several years, of which about $280 billion will be administered through states andlocalities. Funds made available under the Recovery Act are beingdistributed to states, localities, and other entities and individuals through acombination of grants and direct assistance. As you know, the stated purposes of the Recovery Act are to:

preserve and create jobs and promote economic recovery;• assist those most impacted by the recession;• provide investments needed to increase economic efficiency by

spurring technological advances in science and health;• invest in transportation, environmental protection, and other

infrastructure that will provide long-term economic benefits; and• stabilize state and local government budgets, in order to minimize and

avoid reductions in essential services and counterproductive state andlocal tax increases.

As I described in my March testimony, 2 the Recovery Act specifies several

roles for GAO including conducting bimonthly reviews of selected states’and localities’ use of funds made available under the act. 3 My statementtoday is based on our report being released today, Recovery Act: As Initial

Implementation Unfolds in States and Localities, Continued Attention to

Accountability Issues Is Essential, which is the first in a series of bimonthly reviews we will do on states’ and localities’ uses of Recovery Act funding and covers the actions taken under the Act through April 20,2009.4 Our report and our other work related to the Recovery Act can befound on our new website called Following the Money: GAO’s Oversight

of the Recovery Act, which is accessible through GAO’s home page atwww.gao.gov.

1Pub. L. No. 111-5, 123 Stat. 115 (February 17, 2009).

2 GAO-09-453T.

3Recovery Act, div. A, title IX, §901

4 GAO-09-580.

8/14/2019 GOA Stimulus Report

http://slidepdf.com/reader/full/goa-stimulus-report 3/42

8/14/2019 GOA Stimulus Report

http://slidepdf.com/reader/full/goa-stimulus-report 4/42

legislative proposals, and other state legal materials. A detailed descriptionof our scope and methodology can be found in an appendix to our report.

We conducted a performance audit for our first bimonthly review fromFebruary 17, 2009, to April 20, 2009 in accordance with generally acceptedgovernment auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide areasonable basis for our findings and conclusions based on our auditobjectives. We believe that the evidence obtained provides a reasonablebasis for our findings and conclusions based on our audit objectives.

In addition to our ongoing work on selected states’ and localities’ use of Recovery Act funding, we have completed two of the other mandatesincluded for us in the Recovery Act. First, on April 3, 2009, we announcedthe appointment of 13 members to the Health Information TechnologyPolicy Committee, a new advisory body established by the Recovery Act. Additionally, on April 16, 2009, we issued a report on the actions of theSmall Business Administration (SBA) to, among other things, increaseliquidity in the secondary market for SBA loans. 6

Summary of GAO

Findings

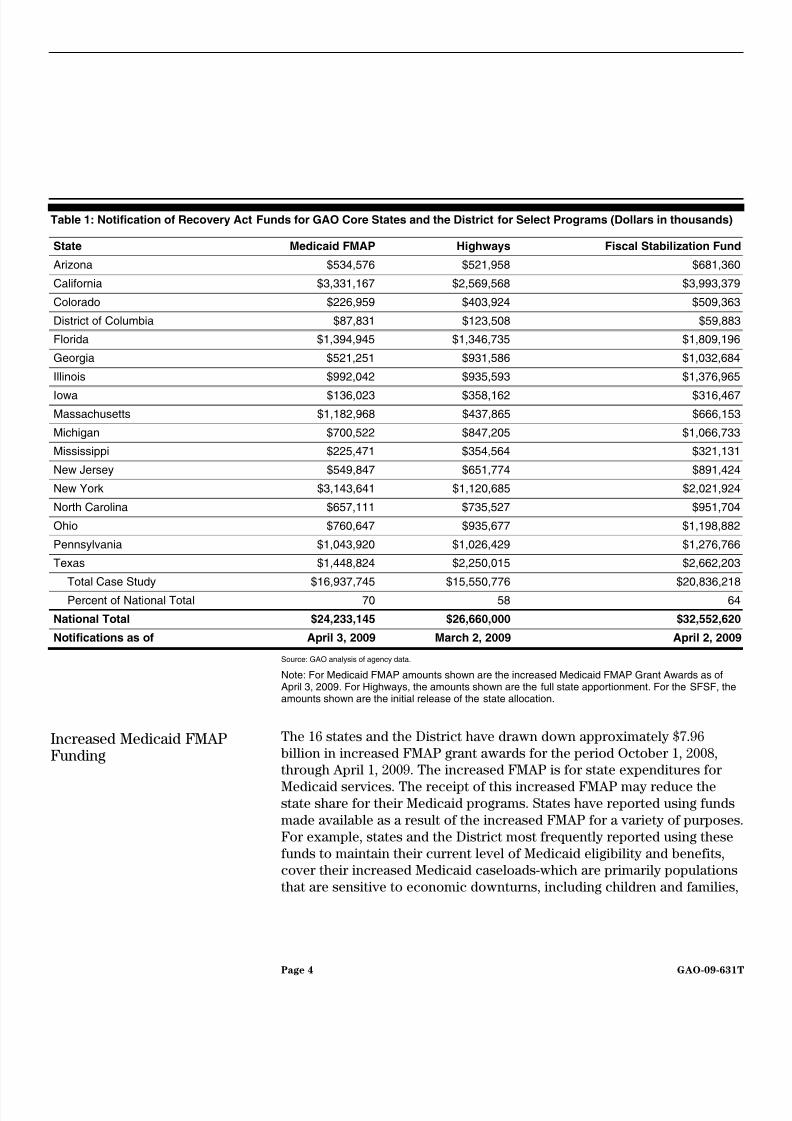

Uses of Funds About 90 percent of the estimated $49 billion Recovery Act funding to be provided to states and localities in fiscal year 2009 will be through health,transportation and education programs. Within these categories, the threelargest programs are increased Medicaid Federal Medical AssistancePercentage (FMAP) grant awards, funds for highway infrastructureinvestment, and the State Fiscal Stabilization Fund (SFSF). Table 1 showsthe breakout of funding available for these three programs in the 16selected states and the District. The Recovery Act funding for these 17 jurisdictions accounts for a little less than two-thirds of total Recovery Act

funding for these three programs.

6GAO, Small Business Administration’s Implementation of Administrative Provisions

in the American Recovery and Reinvestment Act of 2009, GAO-09-507R (Washington,D.C.: April 16, 2009).

Page 3 GAO-09-631T

8/14/2019 GOA Stimulus Report

http://slidepdf.com/reader/full/goa-stimulus-report 5/42

Table 1: Notification of Recovery Act Funds for GAO Core States and the District for Select Programs (Dollars in thousands)

State Medicaid FMAP Highways Fiscal Stabilization Fund

Arizona $534,576 $521,958 $681,360

California $3,331,167 $2,569,568 $3,993,379

Colorado $226,959 $403,924 $509,363

District of Columbia $87,831 $123,508 $59,883

Florida $1,394,945 $1,346,735 $1,809,196

Georgia $521,251 $931,586 $1,032,684

Illinois $992,042 $935,593 $1,376,965

Iowa $136,023 $358,162 $316,467

Massachusetts $1,182,968 $437,865 $666,153

Michigan $700,522 $847,205 $1,066,733

Mississippi $225,471 $354,564 $321,131

New Jersey $549,847 $651,774 $891,424

New York $3,143,641 $1,120,685 $2,021,924

North Carolina $657,111 $735,527 $951,704

Ohio $760,647 $935,677 $1,198,882

Pennsylvania $1,043,920 $1,026,429 $1,276,766

Texas $1,448,824 $2,250,015 $2,662,203

Total Case Study $16,937,745 $15,550,776 $20,836,218

Percent of National Total 70 58 64

National Total $24,233,145 $26,660,000 $32,552,620

Notifications as of April 3, 2009 March 2, 2009 April 2, 2009

Source: GAO analysis of agency data.

Note: For Medicaid FMAP amounts shown are the increased Medicaid FMAP Grant Awards as ofApril 3, 2009. For Highways, the amounts shown are the full state apportionment. For the SFSF, theamounts shown are the initial release of the state allocation.

The 16 states and the District have drawn down approximately $7.96billion in increased FMAP grant awards for the period October 1, 2008,through April 1, 2009. The increased FMAP is for state expenditures for

Medicaid services. The receipt of this increased FMAP may reduce thestate share for their Medicaid programs. States have reported using fundsmade available as a result of the increased FMAP for a variety of purposes.For example, states and the District most frequently reported using thesefunds to maintain their current level of Medicaid eligibility and benefits,cover their increased Medicaid caseloads-which are primarily populationsthat are sensitive to economic downturns, including children and families,

Increased Medicaid FMAPFunding

Page 4 GAO-09-631T

8/14/2019 GOA Stimulus Report

http://slidepdf.com/reader/full/goa-stimulus-report 6/42

and to offset their state general fund deficits, thereby avoiding layoffs andother measures detrimental to economic recovery.

States are undertaking planning activities to identify projects, obtainapproval at the state and federal level, and move them to contracting andimplementation. Some state officials told us they were focusing onconstruction and maintenance projects, such as road and bridge repairs.Before they can expend Recovery Act funds, states must reach agreementwith the Department of Transportation on the specific projects; as of April16, 2009, two of the 16 states had agreements covering more than 50 percent of their states’ apportioned funds, and three states did not have

agreement on any projects. While a few, including Mississippi and Iowahad already executed contracts, most of the 16 states were planning tosolicit bids in April or May. Thus, states generally had not yet expendedsignificant amounts of Recovery Act funds.

Highway InfrastructureInvestment

The states and the District must apply to the Department of Education forSFSF funds. Education will award funds once it determines that anapplication contains key assurances and information on how the state willuse the funds. As of April 20, applications from three states had met thatdetermination-South Dakota, and two of GAO’s sample states, Californiaand Illinois. The applications from other states are being developed andsubmitted and have not yet been awarded. The states and the Districtreport that SFSF funds will be used to hire and retain teachers, reduce the potential for layoffs, cover budget shortfalls, and restore funding cuts to programs.

State Fiscal Stabilization Fund

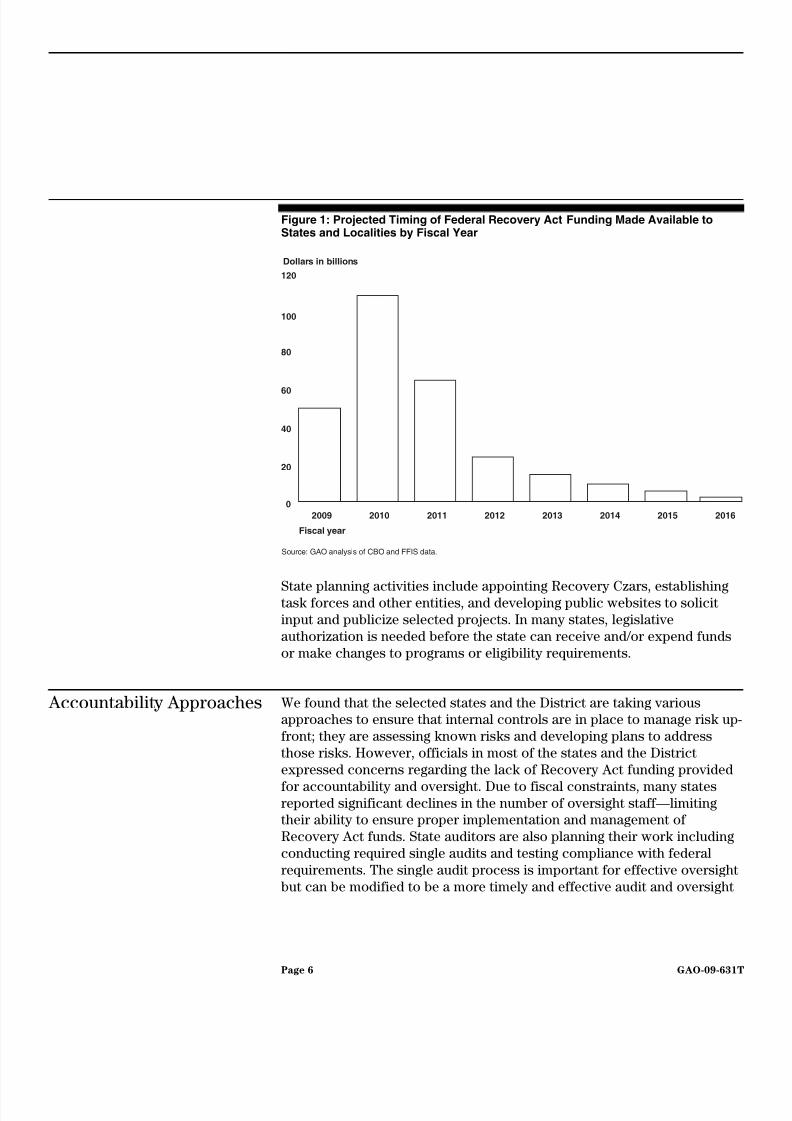

Planning continues for the use of Recovery Act funds. Figure 1 belowshows the projected timing when funds will be made available to statesand localities.

Page 5 GAO-09-631T

8/14/2019 GOA Stimulus Report

http://slidepdf.com/reader/full/goa-stimulus-report 7/42

Figure 1: Projected Timing of Federal Recovery Act Funding Made Available toStates and Localities by Fiscal Year

Source: GAO analysis of CBO and FFIS data.

0

20

40

60

80

100

120

20162015201420132012201120102009

Dollars in billions

Fiscal year

State planning activities include appointing Recovery Czars, establishingtask forces and other entities, and developing public websites to solicitinput and publicize selected projects. In many states, legislativeauthorization is needed before the state can receive and/or expend fundsor make changes to programs or eligibility requirements.

Accountability Approaches We found that the selected states and the District are taking variousapproaches to ensure that internal controls are in place to manage risk up-front; they are assessing known risks and developing plans to addressthose risks. However, officials in most of the states and the Districtexpressed concerns regarding the lack of Recovery Act funding provided

for accountability and oversight. Due to fiscal constraints, many statesreported significant declines in the number of oversight staff—limitingtheir ability to ensure proper implementation and management of Recovery Act funds. State auditors are also planning their work includingconducting required single audits and testing compliance with federalrequirements. The single audit process is important for effective oversightbut can be modified to be a more timely and effective audit and oversight

Page 6 GAO-09-631T

8/14/2019 GOA Stimulus Report

http://slidepdf.com/reader/full/goa-stimulus-report 8/42

tool for the Recovery Act and OMB is weighing options on how to modifyit.

Nearly half of the estimated spending programs in the Recovery Act will beadministered by non-federal entities. State officials suggestedopportunities to improve communication in several areas. For example,they wish to be notified when Recovery Act funds are made availabledirectly to prime recipients within their state that are not state agencies.

Plans to Evaluate Impact An important objective of the Recovery Act is to preserve and create jobs

and promote economic recovery. Officials in nine of the 16 states and theDistrict expressed concern about determining jobs created and retainedunder the Recovery Act, as well as methodologies that can be used forestimation of each.

OMB has moved out quickly to guide implementation of the Recovery Act. As OMB’s initiatives move forward, it has opportunities to build upon itsefforts to date by addressing several important issues.

GAO’sRecommendations

Accountability andTransparencyRequirements

The Director of OMB should:

• adjust the single audit process to provide for review of the design of internal controls during 2009 over programs to receive Recovery Actfunding, before significant expenditures in 2010.

• continue efforts to identify methodologies that can be used todetermine jobs created and retained from projects funded by theRecovery Act.

• evaluate current requirements to determine whether sufficient, reliableand timely information is being collected before adding further datacollection requirements.

Administrative Supportand Oversight

The Director of OMB should clarify what Recovery Act funds can be usedto support state efforts to ensure accountability and oversight.

Communications The Director of OMB should provide timely and efficient notification to (1) prime recipients in states and localities when funds are made available fortheir use, (2) states, where the state is not the primary recipient of funds,but has a state-wide interest in this information, and (3) all recipients, on

Page 7 GAO-09-631T

8/14/2019 GOA Stimulus Report

http://slidepdf.com/reader/full/goa-stimulus-report 9/42

planned releases of federal agency guidance and whether additionalguidance or modifications are expected.

We provided the Director of the Office of Management and Budget with adraft of this report for comment on April 20, 2009. OMB staff respondedthe next day, noting that in its initial review, OMB concurred with theoverall objectives of our recommendations. OMB staff also provided someclarifying information, adding that OMB will complete a more thoroughreview in a few days. We have incorporated OMB’s clarifying informationas appropriate. In addition, OMB said it plans to work with us to define the

best path forward on our recommendations and to further theaccountability and transparency of the Recovery Act. The Governors of each of the 16 states and the Mayor of the District were provided drafts forcomment on each of their respective appendixes in this report. Thosecomments are included in the appendixes.

OMB, States, andDistrict Comments onthe Draft of OurReport

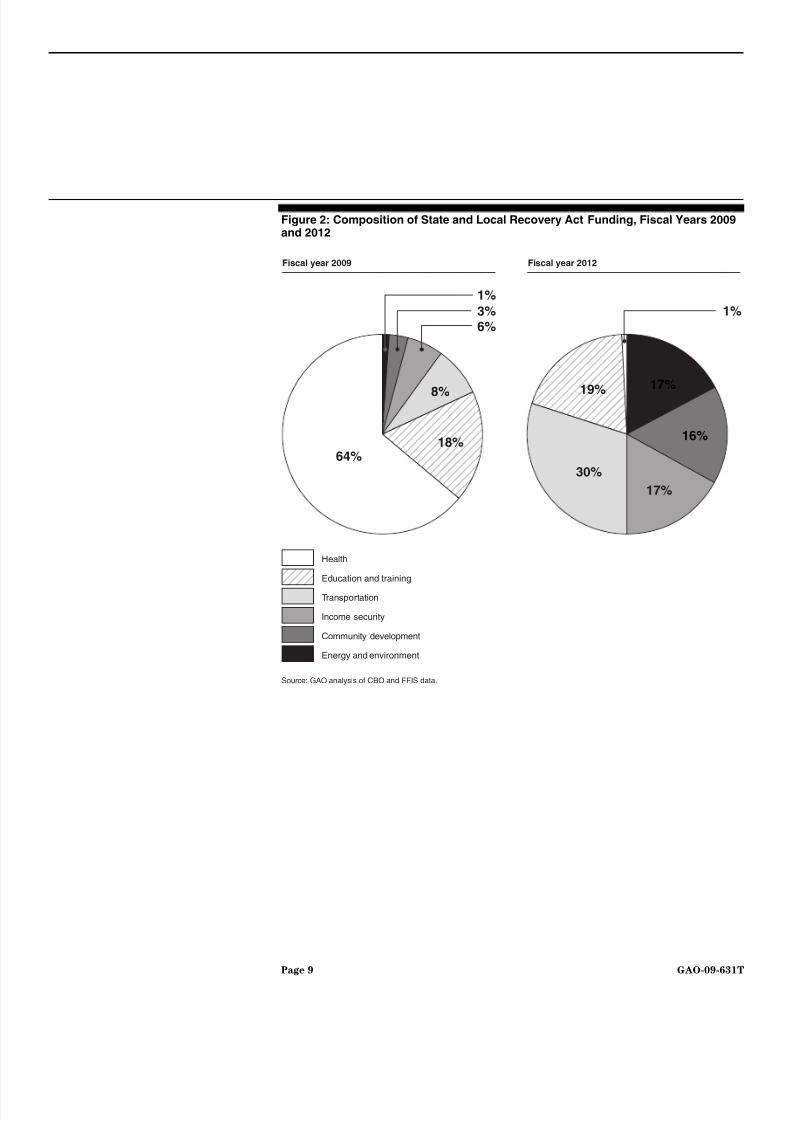

Over time, the programmatic focus of Recovery Act spending will change. As shown in figure 2, about two-thirds of Recovery Act funds expected tobe spent by states in the current 2009 fiscal year will be health-relatedspending, primarily temporary increases in Medicaid FMAP funding.Health, education, and transportation is estimated to account forapproximately 90 percent of fiscal year 2009 Recovery Act funding forstates and localities. However, by fiscal year 2012, transportation will bethe largest share of state and local Recovery Act funding. Taken together,transportation spending, along with investments in communitydevelopment, energy, and environmental areas that are geared moretoward creating long-run economic growth opportunities, will representapproximately two-thirds of state and local Recovery Act funding in 2012.

Background

Page 8 GAO-09-631T

8/14/2019 GOA Stimulus Report

http://slidepdf.com/reader/full/goa-stimulus-report 10/42

Figure 2: Composition of State and Local Recovery Act Funding, Fiscal Years 2009and 2012

Source: GAO analysis of CBO and FFIS data.

18%

8%

3%

1%

64%

30%

17%

16%

19%

17%

Health

Education and training

Transportation

Income security

Community development

Energy and environment

1%

Fiscal year 2009 Fiscal year 2012

6%

Page 9 GAO-09-631T

8/14/2019 GOA Stimulus Report

http://slidepdf.com/reader/full/goa-stimulus-report 11/42

States’ and Localities’Use of and Plans forRecovery Act FundsFocuses on Purposesof the Act and States’Fiscal Stresses

Medicaid FMAP Medicaid is a joint federal-state program that finances health care for

certain categories of low-income individuals, including children, families, persons with disabilities, and persons who are elderly. The federalgovernment matches state spending for Medicaid services according to aformula based on each state’s per capita income in relation to the nationalaverage per capita income. 7 The amount of federal assistance statesreceive for Medicaid service expenditures is known as the FMAP.

Under the Recovery Act, states are eligible for an increased FMAP forexpenditures that states make in providing services to their Medicaid populations. 8 The Recovery Act provides eligible states with an increasedFMAP for 27 months between October 1, 2008 and December 31, 2010. OnFebruary 25, 2009, CMS made increased FMAP grant awards to states, andstates may retroactively claim reimbursement for expenditures thatoccurred prior to the effective date of the Recovery Act. 9 Generally, forfiscal year 2009 through the first quarter of fiscal year 2011, the increasedFMAP, which is calculated on a quarterly basis, provides for: (1) themaintenance of states’ prior year FMAPs; (2) a general across-the-boardincrease of 6.2 percentage points in states’ FMAPs; and (3) a furtherincrease to the FMAPs for those states that have a qualifying increase inunemployment rates. For the first two quarters of 2009, the increases in

7

States may use certain sources for financing the non-federal share of Medicaidexpenditures, including contributions from political subdivisions in the state, such as citiesor counties.

8See Recovery Act, div. B, title V, § 5001 (a)-(c). U.S. territories are also eligible for an

increased FMAP subject to a different formula than states. Recovery Act div. B, title V, §5001 (d). 9 Although the effective date of the Recovery Act was February 17, 2009, states generallymay claim reimbursement for Medicaid service expenditures made on or after October 1,2008.

Page 10 GAO-09-631T

8/14/2019 GOA Stimulus Report

http://slidepdf.com/reader/full/goa-stimulus-report 12/42

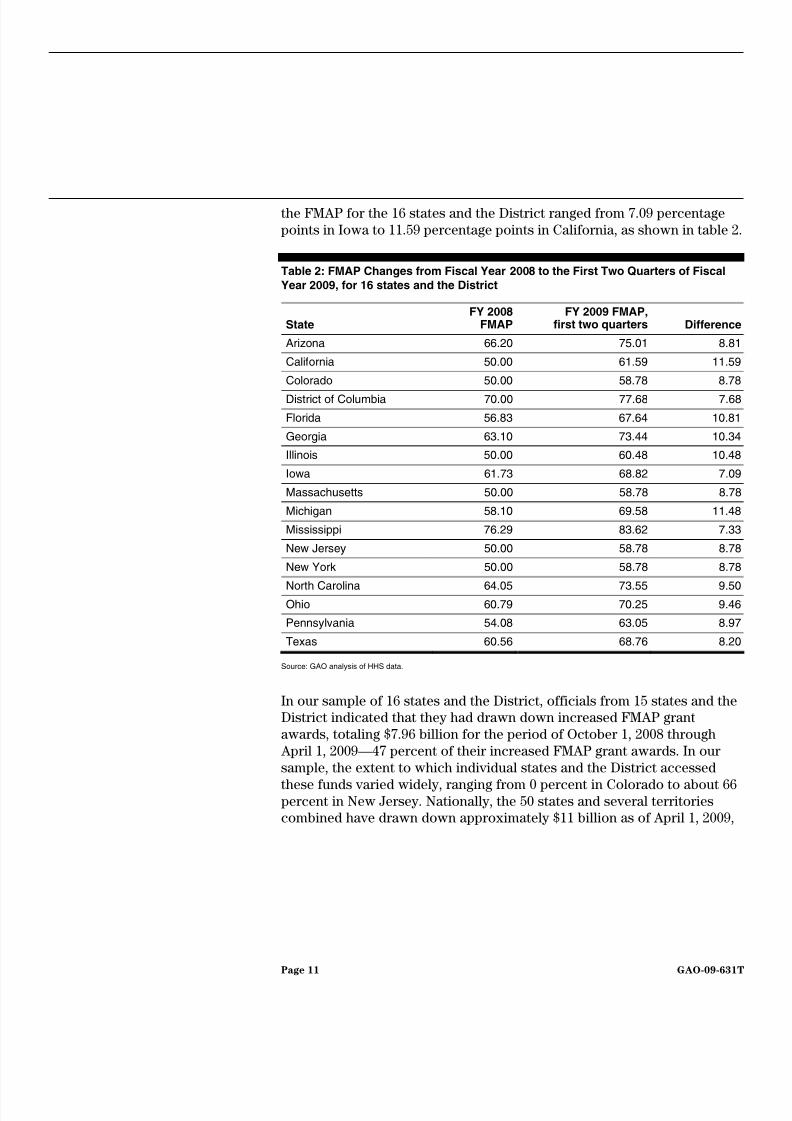

the FMAP for the 16 states and the District ranged from 7.09 percentage points in Iowa to 11.59 percentage points in California, as shown in table 2.

Table 2: FMAP Changes from Fiscal Year 2008 to the First Two Quarters of FiscalYear 2009, for 16 states and the District

StateFY 2008

FMAPFY 2009 FMAP,

first two quarters Difference

Arizona 66.20 75.01 8.81

California 50.00 61.59 11.59

Colorado 50.00 58.78 8.78

District of Columbia 70.00 77.68 7.68

Florida 56.83 67.64 10.81

Georgia 63.10 73.44 10.34

Illinois 50.00 60.48 10.48

Iowa 61.73 68.82 7.09

Massachusetts 50.00 58.78 8.78

Michigan 58.10 69.58 11.48

Mississippi 76.29 83.62 7.33

New Jersey 50.00 58.78 8.78

New York 50.00 58.78 8.78

North Carolina 64.05 73.55 9.50Ohio 60.79 70.25 9.46

Pennsylvania 54.08 63.05 8.97

Texas 60.56 68.76 8.20

Source: GAO analysis of HHS data.

In our sample of 16 states and the District, officials from 15 states and theDistrict indicated that they had drawn down increased FMAP grantawards, totaling $7.96 billion for the period of October 1, 2008 through April 1, 2009—47 percent of their increased FMAP grant awards. In oursample, the extent to which individual states and the District accessed

these funds varied widely, ranging from 0 percent in Colorado to about 66 percent in New Jersey. Nationally, the 50 states and several territoriescombined have drawn down approximately $11 billion as of April 1, 2009,

Page 11 GAO-09-631T

8/14/2019 GOA Stimulus Report

http://slidepdf.com/reader/full/goa-stimulus-report 13/42

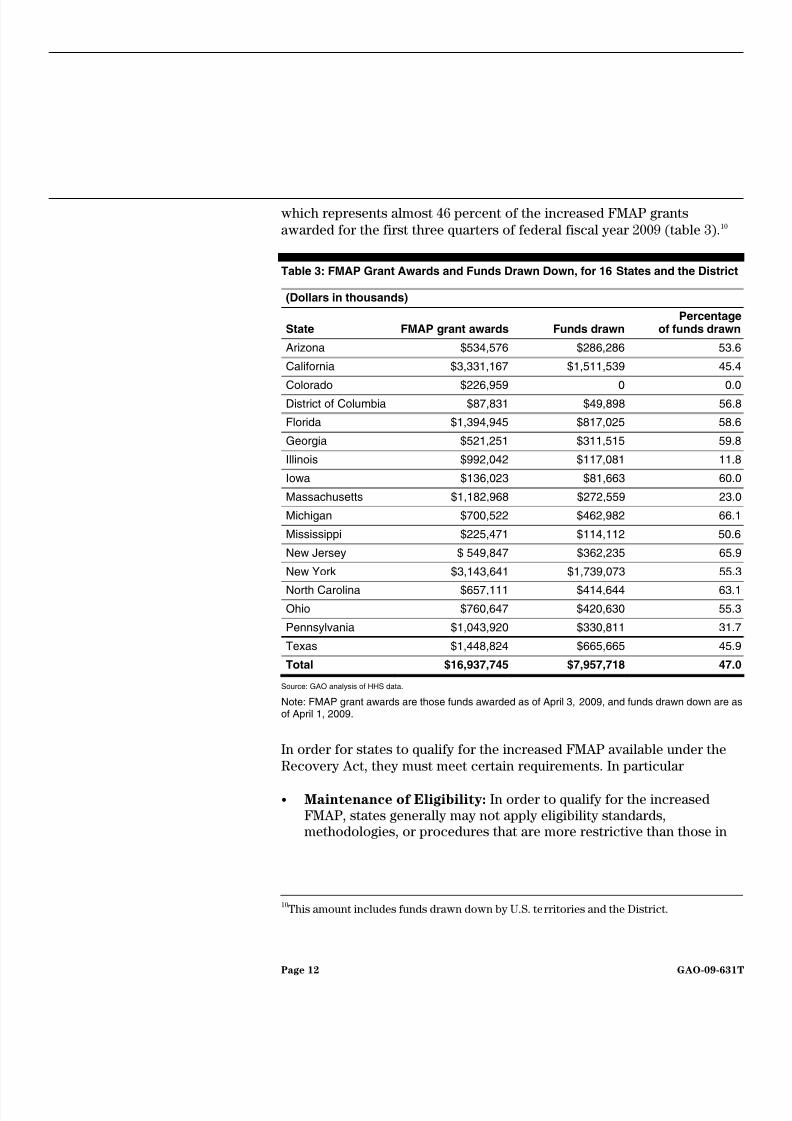

which represents almost 46 percent of the increased FMAP grantsawarded for the first three quarters of federal fiscal year 2009 (table 3). 10

Table 3: FMAP Grant Awards and Funds Drawn Down, for 16 States and the District

(Dollars in thousands)

State FMAP grant awards Funds drawnPercentage

of funds drawn

Arizona $534,576 $286,286 53.6

California $3,331,167 $1,511,539 45.4

Colorado $226,959 0 0.0

District of Columbia $87,831 $49,898 56.8

Florida $1,394,945 $817,025 58.6

Georgia $521,251 $311,515 59.8

Illinois $992,042 $117,081 11.8

Iowa $136,023 $81,663 60.0

Massachusetts $1,182,968 $272,559 23.0

Michigan $700,522 $462,982 66.1

Mississippi $225,471 $114,112 50.6

New Jersey $ 549,847 $362,235 65.9

New York $3,143,641 $1,739,073 55.3

North Carolina $657,111 $414,644 63.1Ohio $760,647 $420,630 55.3

Pennsylvania $1,043,920 $330,811 31.7

Texas $1,448,824 $665,665 45.9

Total $16,937,745 $7,957,718 47.0

Source: GAO analysis of HHS data.

Note: FMAP grant awards are those funds awarded as of April 3, 2009, and funds drawn down are asof April 1, 2009.

In order for states to qualify for the increased FMAP available under theRecovery Act, they must meet certain requirements. In particular

• Maintenance of Eligibility: In order to qualify for the increasedFMAP, states generally may not apply eligibility standards,methodologies, or procedures that are more restrictive than those in

10This amount includes funds drawn down by U.S. territories and the District.

Page 12 GAO-09-631T

8/14/2019 GOA Stimulus Report

http://slidepdf.com/reader/full/goa-stimulus-report 14/42

effect under their state Medicaid programs on July 1, 2008. 11 In

guidance to states, CMS noted that examples of restrictions of eligibility could include (1) the elimination of any eligibility groupssince July 1, 2008 or (2) changes in an eligibility determination orredetermination process that is more stringent than what was in effecton July 1, 2008. States that fail to initially satisfy the maintenance of eligibility requirements have an opportunity to reinstate their eligibilitystandards, methodologies, and procedures before July 1, 2009 andbecome retroactively eligible for the increased FMAP.

• Compliance with Prompt Payment: Under federal law states are

required to pay claims from health practitioners promptly.12

Under theRecovery Act, states are prohibited from receiving the increased FMAPfor days during any period in which that state has failed to meet thisrequirement. 13 Although the increased FMAP is not available for any

claims received from a practitioner on each day the state is not incompliance with these prompt payment requirements, the state mayreceive the regular FMAP for practitioner claims received on days of non-compliance. CMS officials told us that states must attest that theyare in compliance with the prompt payment requirement, but thatenforcement is complicated due to differences across states inmethods used to track this information. CMS officials plan to issueguidance on reporting compliance with the prompt payment

requirement and are currently gathering information from states on themethods they use to determine compliance.

• Rainy Day Funds: States are not eligible for an increased FMAP if anyamounts attributable (either directly or indirectly) to the increasedFMAP are deposited or credited into any reserve or rainy day fund of the state. 14

• Percentage Contributions from Political Subdivisions: In somestates, political subdivisions—such as cities and counties—may be

11See Recovery Act § 5001(f)(1).

12States are required to pay 90 percent of clean claims from health care practitioners within

30 days of receipt and 99 percent of these claims within 90 days of receipt. See 42 U.S.C. §1396a(a)(37)(A).

13This provision only applies to claims received after February 17, 2009, the date of

enactment of the Recovery Act. See Recovery Act § 5001(f)(2).

14This prohibition does not apply to any increase in FMAP based on maintenance of the

states’ prior year FMAPs.

Page 13 GAO-09-631T

8/14/2019 GOA Stimulus Report

http://slidepdf.com/reader/full/goa-stimulus-report 15/42

required to help finance the state’s share of Medicaid spending. Statesthat have such financing arrangements are not eligible to receive theincreased FMAP if the percentage contributions required to be madeby a political subdivision are greater than what was in place onSeptember 30, 2008. 15

In addition to meeting the above requirements, states that receive theincreased FMAP must submit a report to CMS no later than September 30,2011 that describes how the increased FMAP funds were expended, in aform and manner determined by CMS. 16 In guidance to states, CMS has

stated that further guidance will be developed for this reportingrequirement. CMS guidance to states also indicates that, for federalreimbursement, increased FMAP funds must be drawn down separately,tracked separately, and reported to CMS separately. Officials from severalstates told us they require additional guidance from CMS on trackingreceipt of increased FMAP funds and on reporting on the use of thesefunds.

The increased FMAP available under the Recovery Act is for stateexpenditures for Medicaid services. 17 However, the receipt of thisincreased FMAP may reduce the state share for their Medicaid programs.States have reported using these available funds for a variety of purposes.

In our sample, individual states and the District reported that they woulduse the funds to maintain their current level of Medicaid eligibility andbenefits, cover their increased Medicaid caseloads—which are primarily populations that are sensitive to economic downturns, including childrenand families, and to offset their state general fund deficits thereby avoidinglayoffs and other measures detrimental to economic recovery. Ten statesand the District reported using these funds to maintain program eligibility.Nine states and the District reported using these funds to maintainbenefits. Specifically, Massachusetts reported that during a previousfinancial downturn, the state limited the number of individuals eligible forsome services and reduced certain program benefits that were optional forthe state to cover. However, with the funds made available as a result of

the increased FMAP, the state did not have to make such reductions.

15This prohibition does not apply to any increase in FMAP based on maintenance of the

states’ prior year FMAPs.

16Recovery Act, div. B, title V, § 5001 (g)(1).

17Recovery Act, div. B, title V, § 5001 (a)-(c), (h)(1).

Page 14 GAO-09-631T

8/14/2019 GOA Stimulus Report

http://slidepdf.com/reader/full/goa-stimulus-report 16/42

Similarly, New Jersey reported that the state used these funds to eliminate premiums for certain children in its State Children’s Health InsuranceProgram, allowing it to retain coverage for children whose enrollment inthe program would otherwise have been terminated for non-payment of premiums.

Nine states and the District reported using these funds to cover increasesto their Medicaid caseloads, primarily to populations that are sensitive toeconomic downturns, such as children and families. For example, New Jersey indicated that these funds would help the state meet the increaseddemand for Medicaid services. According to a New Jersey official, due to

significant job losses, the state’s proposed 2010 budget would not haveaccommodated all the applicants newly eligible for Medicaid and that thefunds available as a result of the increased FMAP have allowed the state tomaintain a “safety net” of coverage for uninsured and unemployed people.Six states in our sample also reported that they used funds made availableas a result of the increased FMAP to comply with prompt paymentrequirements. Specifically, Illinois reported that these funds will permitthe state to move from a 90-day payment cycle to a 30-day payment cyclefor all Medicaid providers. Three states also reported using these funds torestore or to increase provider payment rates.

In addition, 10 states and the District indicated that the funds madeavailable as a result of the increased FMAP would help offset deficits intheir general funds. Pennsylvania reported that because funding for itsMedicaid program is derived, in part, from state revenues, programfunding levels fluctuate as the economy rises and falls. However, the statewas able to use the funds made available to offset the effects of lowerstate revenues. Arizona officials also reported that the state used fundsmade available as a result of the increased FMAP to pay down some of itsdebt and make payroll payments, thus allowing the state to avoid a seriouscash flow problem.

In our sample, many states and the District indicated that they need

additional guidance from CMS regarding eligibility for the increased FMAPfunds. Specifically, 5 states raised concerns about whether certain programmatic changes could jeopardize the state’s eligibility for thesefunds. For example, Texas officials indicated that guidance from CMS isneeded regarding whether certain programmatic changes being consideredby Texas, such as a possible extension of the program’s eligibility period,would affect the state’s eligibility for increased FMAP funds. Similarly,Massachusetts wanted clarification from CMS as to whether certainchanges in the timeframe for the state to conduct eligibility re-

Page 15 GAO-09-631T

8/14/2019 GOA Stimulus Report

http://slidepdf.com/reader/full/goa-stimulus-report 17/42

determinations would be considered a more restrictive standard. Fourstates also reported that they wanted additional guidance from CMSregarding policies related to the prompt payment requirements or changesto the non-federal share of Medicaid expenditures. For example, Californiaofficials noted that the state reduced Medicaid payments for in-homesupport services, but that counties could voluntarily choose to increasethese payments without altering the cost sharing arrangements betweenthe counties and the state. The state wants clarification from CMS onwhether such an arrangement would be allowable in light of the Recovery Act requirements regarding the percentage of contributions by politicalsubdivisions within a state toward the non-federal share of expenditures.

In response to states’ concerns regarding the need for guidance, CMS toldus that it is in the process of developing draft guidance on the prompt payment provisions in the Recovery Act. One official noted that thisguidance will include defining the term practitioner, describing the typesof claims applicable under the provision, and addressing the principlesthat are integral to determining a state’s compliance with prompt paymentrequirements. Additionally, CMS plans to have a reporting mechanism in place through which states would report compliance under this provision.With regard to Recovery Act requirements regarding political subdivisions,CMS described their current activities for providing guidance to states.Due to the variability of state operations, funding processes, and politicalstructures, CMS has been working with states on a case-by-case basis todiscuss particular issues associated with this provision and to address the particular circumstances for each state. A CMS official told us that if therewere an issue(s) or circumstance(s) that had applicability across thestates, or if there were broader themes having national significance, CMSwould consider issuing guidance.

The Recovery Act provides approximately $48 billion to fund grants tostates, localities and regional authorities for transportation projects of which the largest piece is $27.5 billion for highway and relatedinfrastructure investments. The Recovery Act largely provides for

increased transportation funding through existing programs-such as theFederal-Aid Highway Surface Transportation Program—a federallyfunded, state-administered program. Under this program, funds areapportioned annually to each state department of transportation (orequivalent) to construct and maintain roadways and bridges on thefederal-aid highway system. The Federal-Aid Highway Program refers tothe separately funded formula grant programs administered by the FederalHighway Administration (FHWA) in the U.S. Department of Transportation.

Highway InfrastructureInvestment

Page 16 GAO-09-631T

8/14/2019 GOA Stimulus Report

http://slidepdf.com/reader/full/goa-stimulus-report 18/42

Of the $27.5 billion provided in the Recovery Act for highway and relatedinfrastructure investments, $26.7 billion is provided to the 50 states forrestoration, repair, construction and other activities allowed under theFederal-Aid Highway Surface Transportation Program. Nearly one-third of these funds are required to be sub-allocated to metropolitan and otherareas. States must follow the requirements for the existing program, and inaddition, the Recovery Act requires that the Governor must certify that thestate will maintain its current level of transportation spending, and thegovernor or other appropriate chief executive must certify that the state orlocal government to which funds have been made available has completedall necessary legal reviews and determined that the projects are an

appropriate use of taxpayer funds. The certifications must include astatement of the amount of funds the state planned to expend from statesources as of the date of enactment, during the period beginning on thedate of enactment through September 30, 2010, for the types of projectsthat are funded by the appropriation.

The U.S. Department of Transportation is reviewing the Governors’certifications regarding maintaining their level of effort for highways. According to the Department, of the 16 states in our review and theDistrict, three states have submitted a certification free of explanatory orconditional language—Arizona, Michigan, and New York. Eight submitted“explanatory” certifications—certifications that used language thatarticulated assumptions used or stated the certification was based on the“best information available at the time,” but did not clearly qualify theexpected maintenance of effort on the assumptions proving true orinformation not changing in the future. Six submitted a “conditional”certification, which means that the certification was subject to conditionsor assumptions, future legislative action, future revenues, or otherconditions. 18

Recovery Act funding for highway infrastructure investment differs fromthe usual practice in the Federal-Aid Highway Program in a few importantways. Most significantly, for projects funded under the Recovery Act, the

federal share is 100 percent; typically projects require a state match of 20 percent while the federal share is typically 80 percent. Under the Recovery Act, priority is also to be given to projects that are projected to becompleted within three years. In addition, within 120 days after the

18The legal effect of such qualifications is currently being examined by the U.S. Department

of Transportation and has not been reviewed by GAO.

Page 17 GAO-09-631T

8/14/2019 GOA Stimulus Report

http://slidepdf.com/reader/full/goa-stimulus-report 19/42

apportionment by the Department of Transportation to the states (March2, 2009), 50 percent of the apportioned funds must be obligated. 19 Anyamount of this 50 percent of apportioned funding that is not obligated maybe withdrawn by the Secretary of Transportation and redistributed toother states that have obligated their funds in a timely manner.Furthermore, one year after enactment, the Secretary will withdraw anyremaining unobligated funds and redistribute them based on states’ needand ability to obligate additional funds. These provisions are applicableonly to those funds apportioned to the state and not those funds requiredby the Recovery Act to be suballocated to metropolitan, regional and localorganizations.

Finally, states are required to give priority to projects that are located ineconomically distressed areas as defined by the Public Works andEconomic Development Act of 1965, as amended. In March 2009, FHWAdirected its field offices to provide oversight and take appropriate actionto ensure that states gave adequate consideration to economicallydistressed areas in selecting projects. Specifically, field offices weredirected to discuss this issue with the states and to document its reviewand oversight of this process.

States are undertaking planning activities to identify projects, obtainapproval at the state and federal level, and move projects to contractingand implementation. However, because of the steps necessary beforeimplementation, states generally had not yet expended significant amountsof Recovery Act Funds. States are required to reach agreement with DOTon a list of projects. States will then request reimbursement from DOT asthe state makes payments to contactors working on approved projects.

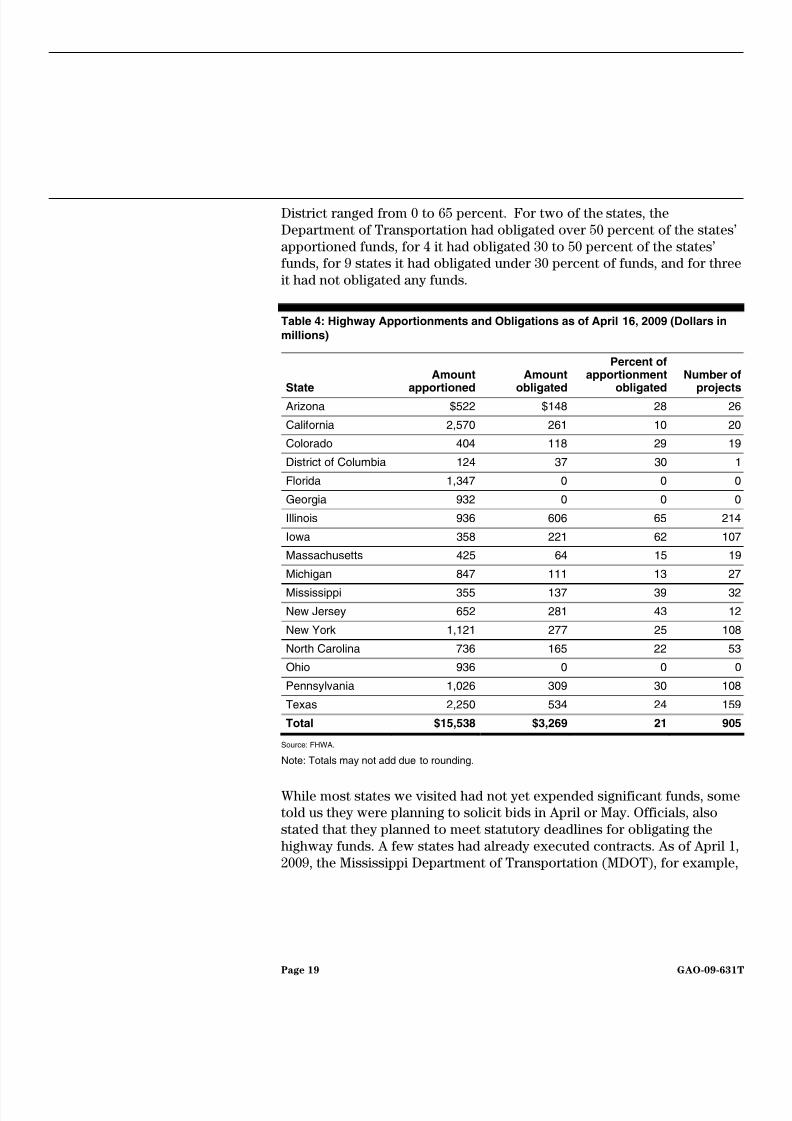

As of April 16, 2009, the U.S. Department of Transportation reported thatnationally $6.4 billion of the $26.6 billion in Recovery Act highwayinfrastructure investment funding provided to the states had beenobligated--meaning Transportation and the states had reached agreementson projects worth this amount. As shown in Table 4 below, for the

locations that GAO reviewed, the extent to which the Department of Transportation had obligated funds apportioned to the states and the

19For federal-aid highway projects, the Federal Highway Administration of the U.S.

Department of Transportation has interpreted the term obligation of funds to mean thefederal government’s contractual commitment to pay for the federal share of a project. Thiscommitment occurs at the time the federal government approves a project agreement andthe project agreement is executed.

Page 18 GAO-09-631T

8/14/2019 GOA Stimulus Report

http://slidepdf.com/reader/full/goa-stimulus-report 20/42

District ranged from 0 to 65 percent. For two of the states, theDepartment of Transportation had obligated over 50 percent of the states’apportioned funds, for 4 it had obligated 30 to 50 percent of the states’funds, for 9 states it had obligated under 30 percent of funds, and for threeit had not obligated any funds.

Table 4: Highway Apportionments and Obligations as of April 16, 2009 (Dollars inmillions)

State

Amount

apportioned

Amount

obligated

Percent ofapportionment

obligated

Number of

projectsArizona $522 $148 28 26

California 2,570 261 10 20

Colorado 404 118 29 19

District of Columbia 124 37 30 1

Florida 1,347 0 0 0

Georgia 932 0 0 0

Illinois 936 606 65 214

Iowa 358 221 62 107

Massachusetts 425 64 15 19

Michigan 847 111 13 27

Mississippi 355 137 39 32

New Jersey 652 281 43 12

New York 1,121 277 25 108

North Carolina 736 165 22 53

Ohio 936 0 0 0

Pennsylvania 1,026 309 30 108

Texas 2,250 534 24 159

Total $15,538 $3,269 21 905

Source: FHWA.

Note: Totals may not add due to rounding.

While most states we visited had not yet expended significant funds, sometold us they were planning to solicit bids in April or May. Officials, alsostated that they planned to meet statutory deadlines for obligating thehighway funds. A few states had already executed contracts. As of April 1,2009, the Mississippi Department of Transportation (MDOT), for example,

Page 19 GAO-09-631T

8/14/2019 GOA Stimulus Report

http://slidepdf.com/reader/full/goa-stimulus-report 21/42

had signed contracts for 10 projects totaling approximately $77 million. 20 These projects include the expansion of State Route 19 in easternMississippi into a four-lane highway. This project fulfills part of MDOT’s1987 Four-Lane Highway Program which seeks to link every Mississippianto a four-lane highway within 30 miles or 30 minutes. Similarly, as of April15, 2009, the Iowa Department of Transportation had competitivelyawarded 25 contracts valued at $168 million. Most often however, wefound that highway funds in the states and the District have not yet beenspent because highway projects were at earlier stages of planning,approval, and competitive contracting. For example, in Florida, theDepartment of Transportation (FDOT) plans to use the Recovery Act

funds to accelerate road construction programs in its preexisting 5-year plan which will result in some projects being reprioritized and selected forearlier completion. On April 15, 2009, the Florida Legislative BudgetCommission approved the Recovery Act-funded projects that FDOT hadsubmitted.

For the most part, states were focusing their selection of Recovery Act-funded highway projects on construction and maintenance, rather than planning and design, because they were seeking projects that would haveemployment impacts and could be implemented quickly. These includedroad repairs and resurfacing, bridge repairs and maintenance, safetyimprovements, and road widening. For example, in Illinois, theDepartment of Transportation is planning to spend a large share of itsestimated $655 million in Recovery Act funds 21 for highway and bridgeconstruction and maintenance projects in economically distressed areas,those that are shovel-ready, and those that can be completed by February2012. In Iowa, the contracts awarded have been for projects such as bridgereplacements and highway resurfacing—shovel-ready projects that couldbe initiated and completed quickly. Knowing that the Recovery Act wouldinclude opportunities for highway investment, states told us they worked

20

As of April 16, 2009, the U.S. Department of Transportation had obligated $137.0 millionfor 32 Mississippi projects.

21 According to the Federal Highway Administration, Illinois’ share of Recovery Act funds

for highway infrastructure investment is approximately $936 million. This total consists of $655 million for IDOT projects and $281 million in sub-allocations for local governments’highway projects. The $655 million to IDOT includes $627 million for IDOT to use statewideand $28 million for mandatory transportation enhancements. Transportation enhancementsinclude activities such as provision of facilities for pedestrians and bicyclists, preservationof abandoned railway corridors, acquisition of scenic easements, and historic preservation

projects.

Page 20 GAO-09-631T

8/14/2019 GOA Stimulus Report

http://slidepdf.com/reader/full/goa-stimulus-report 22/42

in advance of the legislation to identify appropriate projects. For example,in New York, the state DOT began planning to manage anticipated federalstimulus money in November 2008. A key part of New York’s DOT’sstrategy was to build on existing planning and program systems todistribute and manage the funds.

The Recovery Act provided $53.6 billion in appropriations for the StateFiscal Stabilization Fund (SFSF) to be administered by the U.S.Department of Education. The Act requires that the Secretary set aside $5billion for State Incentive Grants, referred to by the department as theReach for the Top program, and the establishment of an Innovation Fund.

The Recovery Act specifies that 81.8 percent (about $39.5 billion) is to bedistributed to states for support of elementary, secondary, and postsecondary education, and early childhood education programs. Theremaining 18.2 percent of SFSF (about $8.8 billion) is available for basicgovernment services but may also be used for educational purposes. Thesefunds are to be distributed to states by formula, with 61 percent of thestate award based on the state’s relative share of the population aged 5 to24 and 39 percent based on the state’s relative share of the total U.S. population. The Department of Education announced on April 1, 2009 thatit will award the SFSF in two phases. The first phase—$32.6 billion—represents about two-thirds of the SFSF.

State Fiscal Stabilization Fund

The states and the District must apply to the Department of Education forSFSF funds and Education must approve those applications. As of April20, 2009, applications from three states had been approved—SouthDakota, and two of GAO’s sample states, California and Illinois. Sinceapplications from other states are now being developed and submitted,they have not yet received their SFSF funds. The applications to Educationmust contain certain assurances. For example, states must assure that, ineach of fiscal years 2009, 2010, and 2011, they will maintain state supportat fiscal year 2006 levels for elementary and secondary education and alsofor public institutions of higher education (IHEs). However, the Secretaryof Education may waive maintenance of effort requirements if the state

demonstrates that it will commit an equal or greater percentage of staterevenues to education than in the previous applicable year. The stateapplication must also contain (1) assurances that the state is committed toadvancing education reform in increasing teacher effectiveness,establishing state-wide education longitudinal data systems, andimproving the quality of state academic standards and assessments; (2)baseline data that demonstrates the state’s current status in each of theeducation reform areas; and (3) a description of how the state intends touse its stabilization allocation.

Page 21 GAO-09-631T

8/14/2019 GOA Stimulus Report

http://slidepdf.com/reader/full/goa-stimulus-report 23/42

Within two weeks of receipt of an approvable SFSF application, Educationwill provide the state with 67 percent of its SFSF allocation. Under certaincircumstances, Education will provide the state with up to 90 percent of its allocation. In the second phase, Education intends to conduct a full peer review of state applications before awarding the final allocations.

After maintaining state support for education at fiscal year 2006 levels,states are required to use the education portion of the SFSF to restorestate support to the greater of fiscal year 2008 or 2009 levels forelementary and secondary education, public IHEs, and, if applicable, earlychildhood education programs. States must distribute these funds to

school districts using the primary state education formula but maintaindiscretion in how funds are allocated to public IHEs. If, after restoringstate support for education, additional funds remain, the state mustallocate those funds to school districts according to the Title I, Part Afunding formula. However, if a state’s education stabilization fundallocation is insufficient to restore state support for education, then a statemust allocate funds in proportion to the relative shortfall in state supportto public schools and IHEs. Education stabilization funds must beallocated to school districts and public IHEs and cannot be retained at thestate level.

Once stabilization funds are awarded to school districts and public IHEs,they have considerable flexibility over how they use those funds. Schooldistricts are allowed to use stabilization funds for any allowable purposeunder the Elementary and Secondary Education Act (ESEA), (commonlyknown as the No Child Left Behind Act), the Individuals with DisabilitiesEducation Act (IDEA), the Adult Education and Family Literacy Act, or thePerkins Act, subject to some prohibitions on using funds for, among otherthings, sports facilities and vehicles. In particular, because allowable usesunder the Impact Aid provisions of ESEA are broad, school districts havediscretion to use Recovery Act funding for things ranging from salaries of teachers, administrators, and support staff to purchases of textbooks,computers, and other equipment. The Recovery Act allows public IHEs to

use SFSF funds in such a way as to mitigate the need to raise tuition andfees, as well as for the modernization, renovation, and repair of facilities,subject to certain limitations. However, the Recovery Act prohibits publicIHEs from using stabilization funds for such things as increasingendowments, modernizing, renovating, or repairing sports facilities, ormaintaining equipment. According to Education officials, there are nomaintenance of effort requirements placed on local school districts.Consequently, as long as local districts use stabilization funds for

Page 22 GAO-09-631T

8/14/2019 GOA Stimulus Report

http://slidepdf.com/reader/full/goa-stimulus-report 24/42

allowable purposes, they are free to reduce spending on education fromlocal-source funds, such as property tax revenues.

States have broad discretion over how the $8.8 billion in SFSF fundsdesignated for basic government services are used. The Recovery Act provides that these funds can be used for public safety and othergovernment services and that these services may include assistance foreducation, as well as for modernization, renovation, and repairs of publicschools or IHEs, subject to certain requirements. Education’s guidance provides that the funds can also be used to cover state administrativeexpenses related to the Recovery Act. However, the Act also places

several restrictions on the use of these funds. For example, these fundscannot be used to pay for casinos (a general prohibition that applies to allRecovery Act funds), financial assistance for students to attend privateschools, or construction, modernization, renovation, or repair of stadiumsor other sports facilities.

States expected that SFSF uses by school districts and public IHEs wouldinclude retaining current staff and spending on programmatic initiatives,among other uses. Some states’ fiscal condition could affect their ability tomeet maintenance of effort (MOE) requirements in order to receive SFSFmonies, but they are awaiting final guidance from Education on procedures to obtain relief from these requirements. For example, due tosubstantial revenue shortages, Florida has cut its state budget in recent years and the state will not be able to meet the maintenance-of-effortrequirement to readily qualify for these funds. The state will apply toEducation for a waiver from this requirement; however, it is awaiting finalinstructions from Education on submission of the waiver. Florida plans touse SFSF funds to reduce the impact of any further cuts that may beneeded in the state education budget.

In Arizona, state officials expect that SFSF recipients, such as local schooldistricts, will generally use their allocations to improve the tools they useto assess student performance and determine to what extent performance

meets federal academic standards, rehire teachers that were let gobecause of prior budget cuts, retain teachers, and meet the federalrequirement that all schools have equal access to highly qualified teachers,among other things. Funds for the state universities will help themmaintain services and staff as well as avoid tuition increases. Illinoisofficials stated that the state plans to use all of the $2 billion in State FiscalStabilization funds, including the 18.2 percent allowed for governmentservices, for K-12 and higher education activities and hopes to avert layoffsand other cutbacks many districts and public colleges and universities are

Page 23 GAO-09-631T

8/14/2019 GOA Stimulus Report

http://slidepdf.com/reader/full/goa-stimulus-report 25/42

facing in their fiscal year 2009 and 2010 budgets. State Board of Educationofficials also noted that U.S. Department of Education guidance allowsschool districts to use stabilization funds for education reforms, such as prolonging school days and school years, where possible. However,officials said that Illinois districts will focus these funds on filling budgetgaps rather than implementing projects that will require long-termresource commitments. While planning is underway, most of the selectedstates reported that they have not yet fully decided how to use the 18.2 percent of the SFSF, which is discretionary.

States’ and localities’ tracking and accounting systems are critical to the

proper execution and accurate and timely recording of transactionsassociated with the Recovery Act. OMB has issued guidance to the statesand localities that provides for separate “tagging” of Recovery Act funds sothat specific reports can be created and transactions traced. Officials fromall 16 of the selected states and the District told us they have establishedor were establishing methods and processes to separately identify,monitor, track, and report on the use of Recovery Act funds they receive.Officials in some states expressed concern that the use of differentaccounting software among state agencies may make it difficult to provideconsistent and timely reporting. Others reported that their ability to trackRecovery Act funds may be affected by state hiring freezes, resulting frombudget shortfalls.

Plans to Track Recovery ActFunds

State officials reported a range of concerns regarding the federalrequirements to identify and track Recovery Act funds going to sub-recipients, localities, and other non-state entities. These concerns includetheir ability to track these funds within existing systems, uncertaintyregarding state officials’ accountability for the use of funds which do not pass through state government entities, and their desire for additionalfederal guidance to establish specific expectations on sub-recipientreporting requirements. Officials in many states expressed concern aboutbeing held accountable for funds flowing directly from federal agencies tolocalities or other recipients. Officials in some states said they would like

to at least be informed about funds provided to non-state entities, in orderto facilitate planning for their use and so they can coordinate Recovery Act activities.

Page 24 GAO-09-631T

8/14/2019 GOA Stimulus Report

http://slidepdf.com/reader/full/goa-stimulus-report 26/42

All of the 16 selected states and the District reported taking action to planfor and monitor the use of Recovery Act funding. Some states reportedthat Recovery Act planning activities for funds received by the state aredirected primarily by the governor’s office. In New York, for example, thegovernor provides program direction to the state’s departments andoffices, and he established a Recovery Act Cabinet comprised of representatives from all state agencies and many state authorities tocoordinate and manage Recovery Act funding throughout the state. InNorth Carolina, Recovery Act planning efforts are led by the newly createdOffice of Economic Recovery and Investment, which was established bythe governor to oversee the state’s economic recovery initiatives.

States’ Actions to Planfor Use of Recovery Act Funds IncludeNew and ExistingEntities andProcesses

Other states reported that their Recovery Act planning efforts were lesscentralized. In Mississippi, the governor has little influence over the stateDepartments of Education and Transportation, as they are led byindependent entities. In Texas, oversight of federal Recovery Act fundsinvolves various stakeholders, including the Office of the Governor, theOffice of the Comptroller of Public Accounts, and the State Auditor’sOffice as well as two entities established within the Texas legislaturespecifically for this purpose—the House Select Committee on FederalEconomic Stabilization Funding and the House Appropriations’Subcommittee on Stimulus. 22

Several states reported that they have appointed “Recovery Czars” oridentified a similar key official and established special offices, task forcesor other entities to oversee the planning and monitor the use of Recovery Act funds within their states. In Michigan, the governor appointed aRecovery Czar to lead a new Michigan Economic Recovery Office, whichis responsible for coordinating Recovery Act programs across all statedepartments and with external stakeholders such as GAO, the federalOMB, and others.

Some states began planning efforts before Congress enacted the Recovery Act. For example, the state of Georgia recognized the importance of

accounting for and monitoring Recovery Act funds and directed stateagencies to take a number of steps to safeguard Recovery Act funds and

22Under Texas law, the governor is the state’s chief budget officer, but the state legislature

and the Legislative Budget Board have a large role in the state’s budget process, whichoperates on a 2-year cycle. Both the governor and the Legislative Budget Board developbudget recommendations and submit budget proposals to the legislature, which adopts abudget (general appropriations bill) for the 2-year period.

Page 25 GAO-09-631T

8/14/2019 GOA Stimulus Report

http://slidepdf.com/reader/full/goa-stimulus-report 27/42

mitigate identified risks. Georgia established a small core team inDecember 2008 to begin planning for the state’s implementation of theRecovery Act. Within 1 day of enactment, the governor appointed aRecovery Act Accountability Officer, and she formed a Recovery Actimplementation team shortly thereafter. The implementation teamincludes a senior management team, officials from 31 state agencies, anaccountability and transparency support group comprised of officials fromthe state’s budget, accounting, and procurement offices, and five cross-agency implementation teams. At one of the first implementation teammeetings, the Recovery Act Accountability Officer disseminated animplementation manual to agencies, which included multiple types of

guidance on how to use and account for Recovery Act funds, and new andupdated guidance is disseminated at the weekly implementation teammeetings.

Officials in other states are using existing mechanisms rather than creatingnew offices or positions to lead Recovery Act efforts. For example, aDistrict official stated that the District would not appoint a Recovery Czar,and instead would use its existing administrative structures to distributeand monitor Recovery Act funds to ensure quick disbursement of funds. InMississippi, officials from the Governor’s office said that the state did notestablish a new office to provide statewide oversight of Recovery Actfunding, in part because they did not believe that the Recovery Act provided states with funds for administrative expenses—includingadditional staff. The Governor did designate a member of his staff to act asa Stimulus Coordinator for Recovery Act activities.

All 16 states we visited and the District have established Recovery Act websites to provide information on state plans for using Recovery funding,uses of funds to date, and, in some instances, to allow citizens to submit project proposals. For example, Ohio has created www.recovery.Ohio.gov,which represents the state’s efforts to create an open, transparent, andequitable process for allocating Recovery Act funds. The state hasencouraged citizens to submit proposals for use of Recovery Act funds,

and as of April 8, 2009, individuals and organizations from across Ohiosubmitted more than 23,000 proposals. Iowa officials indicated they wantto use the state’s recovery web site (www.recovery.Iowa.gov) to host a“dashboard” function to report updated information on Recovery Actspending that is easily searchable by the public. Also in Colorado, the state plans to create a web-based map of projects receiving recovery funds tohelp inform the public about the results of Recovery Act spending inColorado.

Page 26 GAO-09-631T

8/14/2019 GOA Stimulus Report

http://slidepdf.com/reader/full/goa-stimulus-report 28/42

8/14/2019 GOA Stimulus Report

http://slidepdf.com/reader/full/goa-stimulus-report 29/42

Internal controls include management and program policies, procedures,and guidance that help ensure effective and efficient use of resources;compliance with laws and regulations; prevention and detection of fraud,waste, and abuse; and the reliability of financial reporting. BecauseRecovery Act funds are to be distributed as quickly as possible, controlsare evolving as various aspects of the program become operational.Effective internal control is a major part of managing any organization toachieve desired outcomes and manage risk. GAO’s Standards for InternalControl include five key elements: control environment, risk assessment,control activities, information and communication, and monitoring. 23 Ourreport contains a discussion of these elements and the related effort

underway in the jurisdictions we visited.

OMB’s Circular No. A-133 sets out implementing guidelines for the singleaudit and defines roles and responsibilities related to the implementationof the Single Audit Act, including detailed instructions to auditors on howto determine which federal programs are to be audited for compliancewith program requirements in a particular year at a given grantee. TheCircular No. A-133 Compliance Supplement is issued annually to guideauditors on what program requirements should be tested for programsaudited as part of the single audit. OMB has stated that it will use itsCircular No. A-133 Compliance Supplement to notify auditors of programrequirements that should be tested for Recovery Act programs, and willissue interim updates as necessary.

Current Single AuditFocus May NotProvide TimelyOversight Informationfor Recovery ActFunds

Both the Single Audit Act and OMB Circular No. A-133 call for a “risk-based” approach to determine which programs will be audited forcompliance with program requirements as part of a single audit. Ingeneral, the prescribed approach relies heavily on the amount of federalexpenditures during a fiscal year and whether findings were reported inthe previous period to determine whether detailed compliance testing isrequired for a given program that year. 24 Under the current approach forrisk determination in accordance with Circular No. A-133, certain risks

unique to the Recovery Act programs may not receive full consideration.

23GAO, Standards for Internal Control in the Federal Government, GAO/AIMD-00-21.3.1

(Washington, D.C.: November 1999).

24The Single Audit Act requires that all major programs be audited and specifies minimum

dollar amounts and minimum proportions of federal funds expended for programs to beidentified by the auditor as major programs. See 31 U.S.C. §§ 7501.

Page 28 GAO-09-631T

8/14/2019 GOA Stimulus Report

http://slidepdf.com/reader/full/goa-stimulus-report 30/42

Recovery Act funding carries with it some unique challenges. The mostsignificant of these challenges are associated with (1) new government programs, (2) the sudden increase in funds or programs that are new forthe recipient entity, and (3) the expectation that some programs and projects will be delivered faster so as to inject funds into the economy.This makes timely and efficient evaluations in response to the Recovery Act’s accountability requirements critical. Specifically,

• new programs and recipients participating in a program for the firsttime may not have the management controls and accounting systemsin place to help ensure that funds are distributed and used in

accordance with program regulations and objectives;• Recovery Act funding that applies to programs already in operation

may cause total funding to exceed the capacity of managementcontrols and accounting systems that have been effective in past years;

• the more extensive accountability and transparency requirements forRecovery Act funds will require the implementation of new controlsand procedures; and

• risk may be increased due to the pressures of spending funds quickly.

In response to the risks associated with Recovery Act funding, the singleaudit process needs adjustment to put appropriate focus on Recovery Act programs and to provide the necessary level of accountability over thesefunds in a timely manner. The single audit process could be adjusted torequire the auditor to perform procedures such as the following as part of the routine single audit:

• provide for review of the design and implementation of internalcontrol over compliance and financial reporting for programs underthe Recovery Act;

• consider risks related to Recovery Act-related programs in determiningwhich federal programs are major programs; and

• specifically, test Recovery Act programs to determine whether theauditee complied with laws and regulations. 25

The first two items above should preferably be accomplished during 2009

before significant expenditures of funds in 2010 so that the design of internal control can be strengthened prior to the majority of those

25The Single Audit Act sets out minimum federal expenditure amounts and proportions to

use as criteria in defining which programs are to be tested for compliance with programrequirements during a single audit. OMB will need to consider those statutory criteria whenconsidering revisions to the single audit process.

Page 29 GAO-09-631T

8/14/2019 GOA Stimulus Report

http://slidepdf.com/reader/full/goa-stimulus-report 31/42

expenditures. We further believe that OMB Circular No. A-133 and/or theCircular No. A-133 Compliance Supplement could be adjusted to providesome relief on current audit requirements for low-risk programs to offsetadditional workload demands associated with Recovery Act funds.

OMB told us that it is developing audit guidance that would address theabove audit objectives. OMB also said that it is considering reevaluating potential options for providing relief from certain existing auditrequirements in order to provide some balance to the increasedrequirements for Recovery Act program auditing.

Officials in several states also expressed concerns regarding the lack of funding provided to state oversight entities, given the additional federalrequirements placed on states to provide proper accounting and ensuretransparency. Due to fiscal constraints, many states reported significantdeclines in the number of oversight staff, limiting their ability to ensure proper implementation and management of Recovery Act funds. Althoughthe majority of states reported that they lack the necessary resources toensure adequate oversight of Recovery Act funds, some states reportedthat they are either hiring new staff or reallocating existing staff for this purpose.

State and LocalCapacity to ManageRisks

Officials we interviewed in several states said the lack of funding for stateoversight entities in the Recovery Act presents them with a challenge,given the increased need for oversight and accountability. According tostate officials, state budget and staffing cuts have limited the ability of state and local oversight entities to ensure adequate management andimplementation of the Recovery Act. For example, Colorado’s stateauditor reported that state oversight capacity is limited, noting that theDepartment of Health Care Policy and Financing has had 3 controllers inthe past 4 years and the state legislature’s Joint Budget Committeerecently cut field audit staff for the Department of Human Services in half.In addition, the Colorado Department of Transportation’s deputy

controller position is vacant, as is the Department of Personnel & Administration’s internal auditor position. Colorado officials noted thatthese actions are, in part, due to the natural tendency in an economicdownturn to cut administrative expenses in an attempt to maintain program delivery levels. Our report contains more examples of capacityissues from our selected states and the District.

Although most states indicated that they lack the resources needed to provide effective monitoring and oversight, some states indicated they will

Page 30 GAO-09-631T

8/14/2019 GOA Stimulus Report

http://slidepdf.com/reader/full/goa-stimulus-report 32/42

hire additional staff to help ensure the prudent use of Recovery Act funds.For example, according to officials with North Carolina’s Governor’sCrime Commission, the current management capacity in place is notsufficient to implement the Recovery Act. Officials explained that theRecovery Act funds for the Edward Byrne Memorial Justice AssistanceGrant program have created such an increase in workload that thedepartment will have to hire additional staff to handle over the next 3 years. Officials explained that these staff will be hired for the short termsince the money will run out in 3 years. Additionally, officials explainedthat they are able to use 10 percent of the Justice Assistance Grantsfunding to pay for the administrative positions that are needed.

A number of states expressed concerns regarding the ability to trackRecovery Act funds due to state hiring freezes, resulting from budgetshortfalls. For instance, New Jersey has not increased its number of stateauditors or investigators, nor has there been an increase in fundingspecifically for Recovery Act oversight. In addition, the state hiring freezehas not allowed many state agencies to increase their Recovery Actoversight efforts. For example, despite an increase of $469 million inRecovery Act funds for state highway projects, no additional staff will behired to help with those tasks or those directly associated with theRecovery Act, such as reporting on the number of jobs created. While thestate’s Department of Transportation has committed to shift resources tomeet any expanded need for internal Recovery Act oversight, one personis currently responsible for reviewing contractor-reported payrollinformation for disadvantaged business enterprises, ensuring compliancewith Davis-Bacon wage requirements, and development of the job creationfigures. State education officials in North Carolina also said that greateroversight capacity is needed to manage the increase in federal funding.However, due to the state’s hiring freeze, the agency will be unable to usestate funds to hire the additional staff needed to oversee Recovery funds.The North Carolina Recovery Czar said that his office will work with stateagencies to authorize hiring additional staff when directly related toRecovery Act oversight.

With respect to oversight of Recovery Act funding at the local level, varying degrees of preparedness were reported by state and local officials.While the California Department of Transportation (Caltrans) officialsstated that extensive internal controls exist at the state level, there may becontrol weaknesses at the local level. Caltrans is collaborating with localentities to identify and address these weaknesses. Likewise, Coloradoofficials expressed concerns that effective oversight of funds provided to Jefferson County may be limited due to the recent termination of its

Page 31 GAO-09-631T

8/14/2019 GOA Stimulus Report

http://slidepdf.com/reader/full/goa-stimulus-report 33/42

internal auditor and the elimination of its internal control audit function. Arizona state officials expressed some concerns about the ability of rural,tribal, and some private entities such as boards, commissions, andnonprofit organizations to manage, especially if the Recovery Act does not provide administrative funding.

As recipients of Recovery Act funds and as partners with the federalgovernment in achieving Recovery Act goals, states and local units of government are expected to invest Recovery Act funds with a high level of transparency and to be held accountable for results under the Recovery

Act. As a means of implementing that goal, guidance has been issued andwill continue to be issued to federal agencies, as well as to directrecipients of funding. To date, OMB has issued two broad sets of guidanceto the heads of federal departments and agencies for implementing andmanaging activities enacted under the Recovery Act. 26 OMB has alsoissued for public comment detailed proposed standard data elements thatfederal agencies will require from all recipients (except individuals) of Recovery Act funding. 27 When reporting on the use of funds, recipientsmust show the total amount of recovery funds received from a federalagency, the amount expended or obligated to the project, and projectspecific information including the name and description of the project, anevaluation of its completion status, the estimated number of jobs createdand retained by the project, and information on any subcontracts awardedby the recipient, as specified in the Recovery Act.

State Plans to AssessRecovery Act

Spending Impact

State reactions vary widely and often include a mixture of responses to thereporting requirements. Some states will use existing federal programguidance or performance measures to evaluate impact, particularly for on-going programs. Other states are waiting for additional guidance fromfederal departments or from OMB on how and what to measure to assessimpact. While Georgia is waiting on further federal guidance, the state isadapting an existing system (used by the State Auditor to fulfill its Single Audit Act responsibilities) to help the state report on Recovery Act funds.

26See, OMB memoranda, M-09-10, Initial Implementing Guidance for the American

Recovery and Reinvestment Act of 2009, February 18, 2009, and M-09-15, Updated Implementing Guidance for the American Recovery and Reinvestment Act of 2009, April3, 2009.

27OMB, Information Collection Activities: Proposed Collection; Comment Request, Federa

Register – 74 Fed. Reg. 14824 (Apr. 1, 2009).

Page 32 GAO-09-631T

8/14/2019 GOA Stimulus Report

http://slidepdf.com/reader/full/goa-stimulus-report 34/42

The statewide web-based system will be used to track expenditures, project status, and job creation and retention. The Georgia governor isrequiring all state agencies and programs receiving Recovery Act funds touse this system. Some states indicated that they have not yet determinedhow they will assess impact.

Officials in 9 of the 16 states and the District expressed concern about thedefinitions of jobs retained and jobs created under the Recovery Act, aswell as methodologies that can be used for estimation of each. 28 Officialsfrom several of the states we met with expressed a need for clearerdefinitions of “jobs retained” and “jobs created.” Officials from a few states

expressed the need for clarification on how to track indirect jobs, 29 whileothers expressed concern about how to measure the impact of fundingthat is not designed to create jobs. Mississippi state officials suggested theneed for a clearly defined distinction for time-limited, part-time, full-time,and permanent jobs; since each state may have differing definitions of these two categories. Officials from Massachusetts expressed concern thatcontractors may overestimate the number of jobs retained and created.Some existing programs, such as highway construction, havemethodologies for estimating job creation. But other programs, existingand new, do not have job estimation methodologies.

Some of the questions that states and localities have about Recovery Actimplementation may have been answered in part via the guidance provided by OMB for the data elements as well as by guidance issued byfederal departments. For example, OMB provided draft definitions foremployment, as well as for jobs retained and jobs created via Recovery Act funding. However, OMB did not specify methodologies for estimating jobs retained and jobs created, which has been a concern for some states.Data elements were presented in the form of templates with section bysection data requirements and instructions. OMB provided a comment period during which it is likely to receive many questions and requests forclarifications from states, localities, and other entities that can be directrecipients of Recovery Act funding. OMB plans to update this guidance

28Recovery Act, § 3(a)(1). Non-federal entities receiving discretionary funds appropriated

under the Recovery Act must report on the number of jobs created and retained, amongother requirements. Mandatory and entitlement programs are excluded from thisrequirement. Recovery Act, div. A, title XV. § 1512.

29Indirect jobs are jobs created as a result of a demand for goods and services generated by

direct funding from the Recovery Act.

Page 33 GAO-09-631T

8/14/2019 GOA Stimulus Report

http://slidepdf.com/reader/full/goa-stimulus-report 35/42

again in the next 30 to 60 days. Some federal agencies have also providedguidance to the states. The Departments of Education, Housing and UrbanDevelopment, Justice, Labor, Transportation, the Corporation for NationalCommunity Service, the National Institutes of Health, and the Centers forMedicare & Medicaid Services have provided guidance for programimplementation, particularly for established programs. Although guidanceis expected, some new programs, such as Broadband Deployment Grants,are awaiting issuance of implementation instructions.

It has been a little over two months since enactment of the Recovery Act

and OMB has moved out quickly. In this period, OMB has issued two setsof guidance, first on February 18 and next on April 3, with another roundto be issued within 60 days. OMB has sought formal public comment on its April 3 guidance update and before this, according to OMB, reached outinformally to Congress, federal, state, and local government officials, andgrant and contract recipients to get a broad perspective on what is neededto meet the high expectations set by Congress and the Administration. Inaddition, OMB is standing up two new reporting vehicles, Recovery.gov,which will be turned over to the Recovery Accountability andTransparency Board and is expected to provide unprecedented publicdisclosure on the use of Recovery Act funds, and a second system tocapture centrally information on the number of jobs created or retained. As OMB’s initiatives move forward and it continues to guide theimplementation of the Recovery Act, OMB has opportunities to build uponits efforts to date by addressing several important issues.

ConcludingObservations andRecommendations:Moving Forward toClarify Recovery ActRoles andResponsibilities

These issues can be characterized broadly in three categories: (1) Accountability and Transparency Requirements, (2) AdministrativeSupport and Oversight, and (3) Communications.

Accountability andTransparency

Requirements

Recipients of Recovery Act funding face a number of implementationchallenges in this area. The Act includes many programs that are new or

new to the recipient and, even for existing programs; the sudden increasein funds is out of normal cycles and processes. Add to this the expectationthat many programs and projects will be delivered faster so as to injectfunds into the economy and it becomes apparent that timely and efficientevaluations are needed. The following are our recommendations to helpstrengthen ongoing efforts to ensure accountability and transparency.