global trends sv mar17 - hotforex · outlook for the euro and eurusd japan and the yen outlook for...

TRANSCRIPT

WORLD LEADER IN FINANCIAL TRADINGwww.hotforex.com

GLOBAL TRENDS17

AN EXCLUSIVE OUTLOOK ON GLOBALMARKETS AND ECONOMIES

CONTENTS2017 Outlook - An Update

USA and the USD

Outlook for the USD Index

Europe and the EURO

Outlook for the Euro and EURUSD

Japan and the YEN

Outlook for USDJPY

UK and Sterling

Outlook for GBPUSD

The Commodity Currencies (AUD, CAD and NZD)

Gold

Outlook for Gold

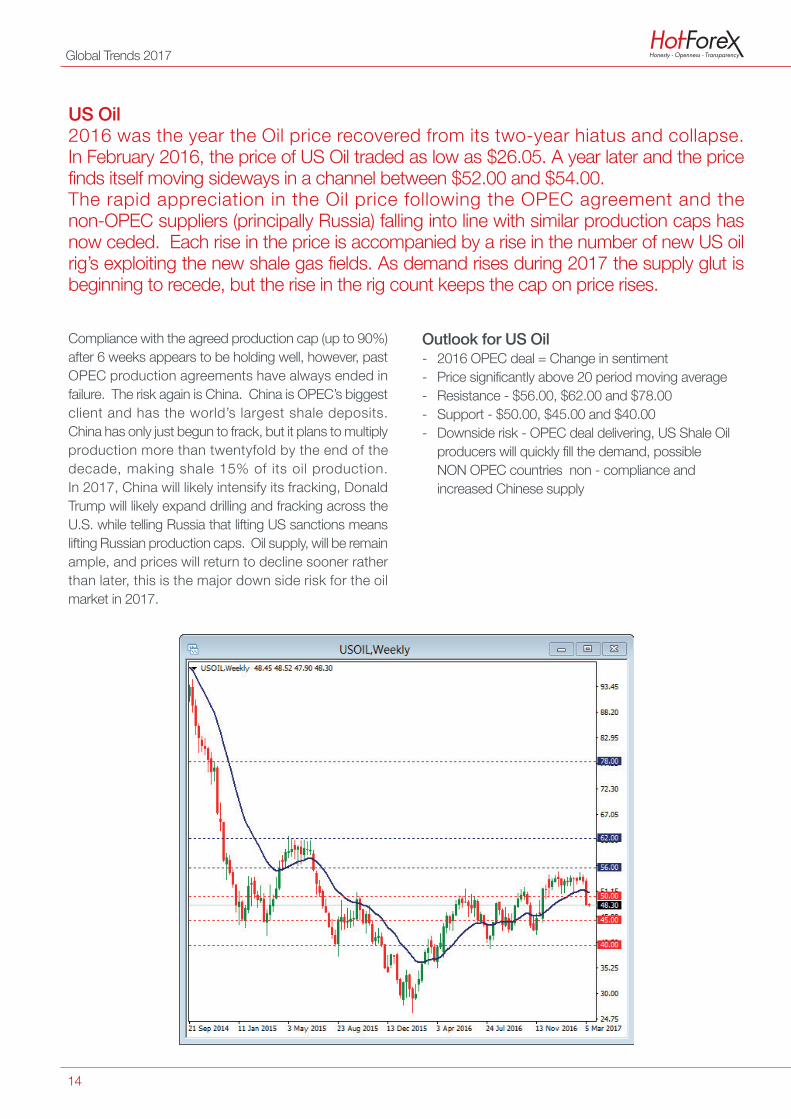

US Oil

Outlook for US Oil

Stuart Cowell - HotForex’s Senior Analyst

02

03

04

05

06

07

08

09

10

11

12

13

14

14

15

02

2017 Outlook - An Update

All the enclosed content, market data and chart information was correct as at March 11, 2017

Global Trends 2017

“Three months after the US election and a month after President Trump has assumed power, the US equity markets remain buoyant and at all-time highs. The bond market keeps on going as yields continue their trend in the opposite direction. What of 2017 and the foreign exchange (Forex) markets? What are the key stories and events likely to play out as the year rolls on?

At the end of December 2016, I published my thoughts and analysis for what I thought the first half of 2017 may hold. Today I am updating those thoughts for the remainder of 2017.

Stuart Cowell HotForex’s Senior Analyst

Global Trends 2017

03

January 2017 was a big reality check for the Index as it had one of its worst performing Januarys on record, losing over 4% in a single month. The USD had got ahead of itself and a retrace was inevitable. Also the promises of candidate Trump need the checks and balances of the US government system before they can become policy for President Trump. Although the Republicans hold majorities in both the Senate and the House of Representatives it is Congress as a whole that has to pass the Budget. Republicans will be happy to cut taxes but less enthusiastic to increase spending; their natural inclination is to cut the government budget, not to expand it. There is some distance (trillions of dollars) between what the President wants to spend and what Congress will accept. This could be the significant point of tension and risk to the USD during 2017.

Traditionally the assumption has always been that a strong dollar means a strong US economy, a break from traditional thinking may be on the cards. On a number of occasions, since taking office, the new administration have suggested that a strong dollar is impacting US growth and countries in the firing line have ranged from Japan and China to Germany. So there could be pressure to actually reduce the value of the mighty Greenback.

However, my assumption in December that USD strength will prevail remains, and the fact that we have seen strong US job numbers, although a persistently low earnings growth, adds to my view that the potential for THREE interest rate hikes this year is still tenable. Even if President Trump delivers a reduced fiscal package, the policy divergence between the USA and the rest of the world (that has been in part driving the value of the dollar north) will persist. The really new caveat has been the market’s reaction to Presidential tweets in the absence of policy and that shows no sign of slowing down. Perhaps, after the honeymoon period of the new administration is over, policy will become a little more predictable.

USA and the USD The earthquake to the establishment that was the Trump victory in the US election has seen the USD soar from expectations of tax cuts, a reduction in corporate regulation and a boost in infrastructure spending. The USD Index as I reported at year end was in a strong three-month bull run and Trump’s victory had propelled the index through the psychological 100.00 level. The move by the Federal Reserve to raise interest rates at their December meeting further propelled the USD.

Outlook for the USD Index:- Key Psychological 100 level remains key- Index at multiyear highs (last at these levels in 2003) - Resistance at 106, 115 and 121 - Support at 100, 95.70 and 92.20- Significance of the January 2017 reversal cannot be underestimated

04

Global Trends 2017

05

Global Trends 2017

The three key elections in the Netherlands (March), France (April and May) and Germany (September) where the populist nationalist parties continue to garner support will cloud the already uncertain outlook that hangs over Europe and the countries of the Eurozone. In December, the EURUSD had broken the psychological 1.0500 barrier and once again parity was on the agenda. Although the pair have staged a recovery since, the outlook remains cautious.

The first major political milestone is the March 15 Dutch election, closely followed by the UK triggering Article 50 on March 31 to start the two-year process to be the first country to ever leave the European Union. The disintegration of the Eurozone and the fracturing of the EU itself will continue to create headlines. Pressure on the Euro could become very significant in the first half of 2017, especially in the wake of strong euro sceptic votes in the Netherlands and France.

The thought of Mrs Merkel not winning the German election in September appeared preposterous only a few months ago, however, a strong official opposition (SPD) headed by the combative Martin Schulz and a significant rise in support for the AfD has also changed the mood in Germany.

Economically, ironically, the lethargic and glacial recovery in the Eurozone is showing signs of gaining momentum and even inflation is back on the agenda.

The problem remains the “two-speed” Europe with the dominant northern economies moving much faster and their southern colleagues continuing to struggle with low growth, high unemployment and resistance to key structural reforms.

The ECB remains very accommodative and the continued QE programme shows little significant signs of “tapering” as some at the central bank have been calling for. Caution ahead for the potential storm clouds gathering over Euroland.

Europe and the EUROAgain it is politics and personalities (Merkel, Le Pen and the lesser-known but potentially more significant Geert Wilders) that will dominate the economic scene in Europe and prospects for the single currency. The economic uncertainties and Black Swans could come from the Italian Banking system, (and the Euro-wide problem of very high non-performing loans), the recurring Greek debt and consequences of Brexit on the single market.

06

Global Trends 2017

Outlook for the Euro and EURUSD - Key Psychological 1.0500 level remains important - Last at these levels in 2002 - Technically Bearish - Lower half of Bollinger Band, Below 20 Period MA , Parabolic SAR - - Support at - 1.0200, 1.000 (Parity) and 0.9850- Resistance at - 1.1000, 1.1500 and 1.1850- Major Political Risk - Elections in the Netherlands, France & Germany - BREXIT - still largely unknown, more clarity by 31/3/17 following Article 50.

07

Global Trends 2017

The goal is to boost domestic demand and GDP and at the same time raise inflation to the nirvana that is 2 percent. The structural reforms which are the most problematic for Abe are the problem of poor competition, expanding trade (even more in focus with the new US President pulling the out of the Trans Pacific Partnership) and the biggest problem of all that of reforming the labour market.

The Bank of Japan was the first to push short-term interest rates below zero coining a flurry of copycat moves by central bankers as negative interest rates policy (NIRP) found favour around the world. However, the BOJ have now gone a step further and are focusing on the yield curve and have capped long-term 10-year rates on Japanese Government Bonds (JGBs) at zero.

The impact is that the widening yield gap between Japan and other parts of the world will keep pressure on the Yen.

At their recent meeting, PM Abe and President Trump agreed not to focus on currency difficulties and the thorny issue of trade. However, Japan has a huge trade surplus with the USA and with the new US administration’s focus on levelling the playing field this can only be to Japan’s disadvantage.

Japan and the YenThe Japanese economy remains sluggish even after four straight quarters of growth and a strong finish to 2016. Prime Minister Abe’s much heralded 3 arrows of fiscal expansion, monetary easing, and structural reform have more or less failed and the outlook for the Japanese Yen remains a mirror image of the prospects for the USD.

08

Global Trends 2017

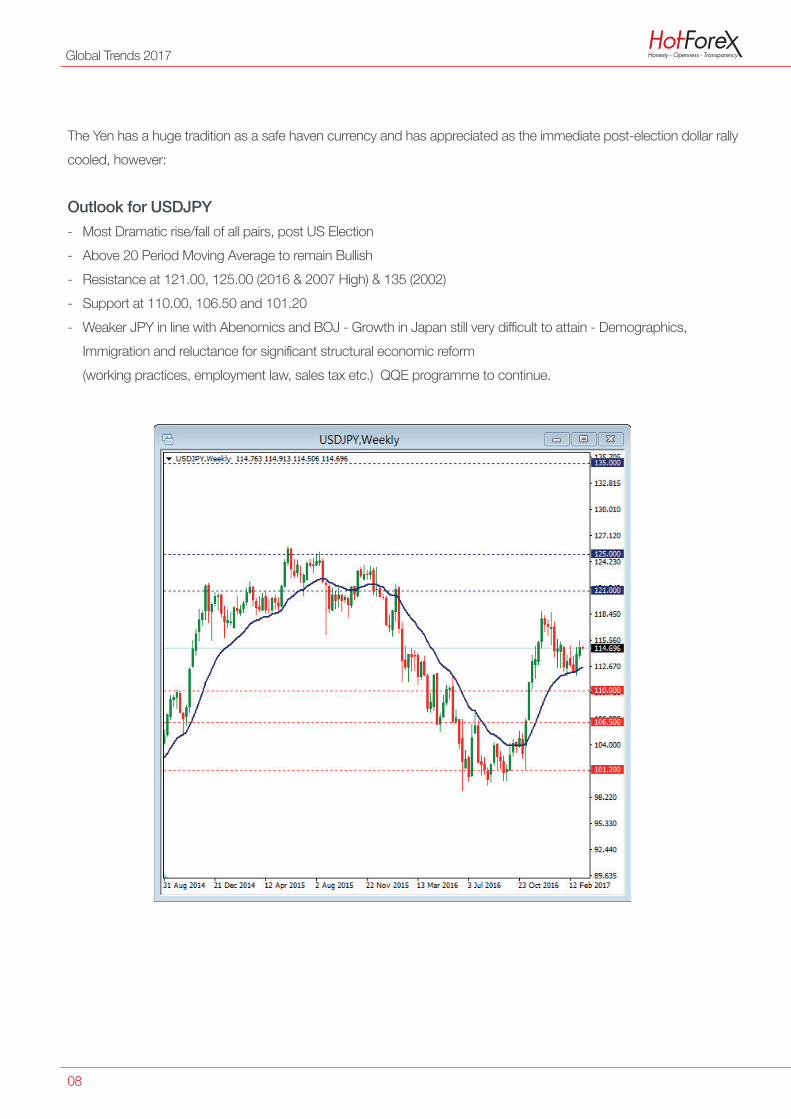

The Yen has a huge tradition as a safe haven currency and has appreciated as the immediate post-election dollar rally cooled, however:

Outlook for USDJPY - Most Dramatic rise/fall of all pairs, post US Election- Above 20 Period Moving Average to remain Bullish - Resistance at 121.00, 125.00 (2016 & 2007 High) & 135 (2002) - Support at 110.00, 106.50 and 101.20- Weaker JPY in line with Abenomics and BOJ - Growth in Japan still very difficult to attain - Demographics, Immigration and reluctance for significant structural economic reform (working practices, employment law, sales tax etc.) QQE programme to continue.

09

Global Trends 2017

The uncertainty of the Brexit process is also beginning to clarify, if only a little; the UK Parliament will get a vote on the exit plan, March 31 is the Article 50 deadline day set by PM May and talk is swirling of an earlier commence-ment of the official negotiations. PM May was the first overseas leader to meet President Trump (a backer of Brexit) and the carrot of a new bilateral trade deal to be agreed quickly. In return, the pomp and circumstance of a full UK state visit was offered to the President within months of him taking office. This is normally reserved until the second or third years of any new US administration.

UK growth and inflation are both on the rise and the risk is of a sudden unexpected spike in inflation outside of BOE estimates and well north of the 2% target. As inflation rises and earnings remain constrained by continued slack in the economy, the impact of what is actually being nego-tiated in the Brexit talks will begin to emerge by mid-year. The BOE continues to balance the need for growth and extra stimulus with the prospect of higher inflation and weak wage growth and the pressure that will put on consumption and investment. Productivity in the UK remains stubbornly low and so UK interest rates could easily move either way during the rest of 2017.

UK and SterlingSterling has fallen significantly (15-18%) against its major rivals since the EU Referendum in June 2016. UK exports are now much more competitive and imports much more expensive and as a net importer the country’s debt and balance of payments deficit have increased significantly. However, consumer and business confidence have held up well and with swift action from the Bank of England to cut interest rates in the immediate aftermath of the shock vote to leave the EU it’s been “steady ahead ” for the UK economy.

10

Global Trends 2017

Outlook for GBPUSD- Recovered 6% from 35 year lows earlier in the year - Could outperform both the EUR & JPY- 20 Period moving average (1.25000) key following recovery from significant oversold situation- Support - 1.2000, 1.1500 and 1.1000- Resistance - 1.3000, 1.3500 and 1.4200- Brexit is the REAL unknown and Sterling will remain the main indictor of its impact- BOE unlikely to act again quickly; the economy - so far has performed better than expectations but outlook is uncertain.

11

Global Trends 2017

The Chinese economy avoided a heavy landing in 2016

as the government continued its fiscal and monetary

policies aimed simply and squarely at continued

economic growth at all costs.

The risk is the credit and housing bubble that continues

to inflate and the regulation of the unique Chinese

shadow banking system. However, the key risk remains

the trade situation and the relationship with the new

US administration; this could be the possible tipping

point of 2017.

Should China slow significantly then, the major casualty

will be the Australian economy and the AUD. The rise in

the AUD has been on the back of the recovery in global

commodity prices including Coal, Copper, Gold and in

particular Iron Ore. Clearly the slowing of the world’s

second largest economy impacts other Asian

countries, many of whom are also key export markets

for Australia. China as the Yuan depreciates further is

the key catalyst in Asia and the wider global economy.

New Zealand is less exposed to China, but dependent

on Australia for many of its exports, the ripple effect will

inevitably be felt in New Zealand too. However, being a

soft commodity exporter if the slowdown in China is

realised it will be in the housing and construction sectors

that slow first (Australian Coal and Iron Ore) rather than

the milk powder and agricultural goods from New

Zealand. China takes 32% of Australian exports com-

pared to 18% of New Zealand exports.

Canada, although dependent on the energy sector,

has a more diverse economy than many appreciate.

Housing inflation remains a key risk along with the future

of trade with the USA. However, oil prices have

recovered significantly since the OPEC agreement of last

November and remain in the $50-$55 range. The fiscal

spending and expansionist policies of the new USA

administration should benefit Canada, even with

a re-negotiated trade deal. Over 70% of Canadian

exports end up in the USA and that is likely to remain

fairly stable. The CAD could become the new star

commodity currency through 2017.

The Commodity Currencies (AUD, CAD and NZD)The Australian Dollar and New Zealand dollar continue to be the best two performing currencies since the US election and so far in 2017. Both are heavily influenced by their near neighbour China; Australia to a greater extent than New Zealand and both countries central banks are becoming increasingly concerned about their respective dollar’s appreciation. However, both are unlikely to action moves in interest rates during 2017.

12

Global Trends 2017

Always a volatile asset it becomes a safe haven in uncertain times. This and the combination of concerns over future monetary policy and the explosion of negative interest rates globally drove demand. Although global demand increased overall in 2016 the two key markets of India and China saw consumer demand fall by 21% and 7% respectively. Chinese currency controls were a significant constraint on demand there.

The outlook for Gold during 2017 depends on the USD, the trade and political policies that emerge from the new Trump presidency and global demand in the key Asian emerging market economies (particularly China and India). Sentiment is also a key driver in determining gold prices. The 2017 rally, much like the January/February rally of 2016 could herald stronger prices ahead.

However, unlike last year, the 2017 rally has been accompanied by a global equity rally too, a key divergence from traditional correlations. 2017 also has similar global concerns ahead, last year it was Brexit and the US election, both although unknown, were expected to have the opposite outcomes.

This year so far, Gold has been driven in part by the uncertainty of what to expect from President Trump (particularly regarding foreign policy including Russia, China and Iran) and the political uncertainties surround-ing the elections in Europe. In such situations something usually gives; either the Gold price or Equities.

GoldThe end of the year USD rally was projecting a weak Gold price during 2017. However, the new year gold rally has been sustained and from a low of $1123 the price has rallied 10% to over $1240. 2016 was a good year for gold with demand up 2% at 4,309 tonnes; it’s highest in four years.

13

Global Trends 2017

Outlook for Gold- Remains bearish but end of Q1 important for rest of year - Above 20 period moving average so possible end of weakness - Support - 1120, 1060 and 1000 - Resistance - 1300, 1365 and 1477

14

Global Trends 2017

Compliance with the agreed production cap (up to 90%) after 6 weeks appears to be holding well, however, past OPEC production agreements have always ended in failure. The risk again is China. China is OPEC’s biggest client and has the world’s largest shale deposits. China has only just begun to frack, but it plans to multiply production more than twentyfold by the end of the decade, making shale 15% of its oil production. In 2017, China will likely intensify its fracking, Donald Trump will likely expand drilling and fracking across the U.S. while telling Russia that lifting US sanctions means lifting Russian production caps. Oil supply, will be remain ample, and prices will return to decline sooner rather than later, this is the major down side risk for the oil market in 2017.

Outlook for US Oil - 2016 OPEC deal = Change in sentiment - Price significantly above 20 period moving average - Resistance - $56.00, $62.00 and $78.00- Support - $50.00, $45.00 and $40.00- Downside risk - OPEC deal delivering, US Shale Oil producers will quickly fill the demand, possible NON OPEC countries non - compliance and increased Chinese supply

US Oil2016 was the year the Oil price recovered from its two-year hiatus and collapse. In February 2016, the price of US Oil traded as low as $26.05. A year later and the price finds itself moving sideways in a channel between $52.00 and $54.00. The rapid appreciation in the Oil price following the OPEC agreement and the non-OPEC suppliers (principally Russia) falling into line with similar production caps has now ceded. Each rise in the price is accompanied by a rise in the number of new US oil rig’s exploiting the new shale gas fields. As demand rises during 2017 the supply glut is beginning to recede, but the rise in the rig count keeps the cap on price rises.

15

With over 25 years experience working for a host of globally recognized organisations in the City of London, Stuart Cowell is a passionate advocate of keeping things simple, doing what is probable and understanding how the news, charts and sentiment work together to provide trading opportunities across all asset classes and all time frames.

Stuart has been trading the global markets since 1997 and has also run his own consultancy. He believes that knowing yourself and employing effective risk management are the keys to successful trading.

Stuart Cowell HotForex’s Senior Analyst

Global Trends 2017

Further improve your Forex trading knowledge and skills by joining our free live trading webinars https://www.hotforex.com/hf/en/trading-tools/trading-webinars.html

Compliance with the agreed production cap (up to 90%) after 6 weeks appears to be holding well, however, past OPEC production agreements have always ended in failure. The risk again is China. China is OPEC’s biggest client and has the world’s largest shale deposits. China has only just begun to frack, but it plans to multiply production more than twentyfold by the end of the decade, making shale 15% of its oil production. In 2017, China will likely intensify its fracking, Donald Trump will likely expand drilling and fracking across the U.S. while telling Russia that lifting US sanctions means lifting Russian production caps. Oil supply, will be remain ample, and prices will return to decline sooner rather than later, this is the major down side risk for the oil market in 2017.

Outlook for US Oil - 2016 OPEC deal = Change in sentiment - Price significantly above 20 period moving average - Resistance - $56.00, $62.00 and $78.00- Support - $50.00, $45.00 and $40.00- Downside risk - OPEC deal delivering, US Shale Oil producers will quickly fill the demand, possible NON OPEC countries non - compliance and increased Chinese supply

Disclaimer: The content provided in this report does not constitue investment advice, should not be viewed as an investment recommendation or as a solicitation for the purpose of buying or selling of any financial instrument. All the information provided in this report has been gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. This communication should not be reproduced or distributed without the prior written permission of the HF Markets Group.

Legal: HotForex is a unified brand name of the HF Markets Group which encompasses global licensed entities.Please visit our website for more information.

Risk Warning: Trading leveraged products such as Forex and CFDs may not be suitable for all investors as they carry a high degree of risk to your capital. Trading such products is risky and you may lose all of your investment. Before deciding to trade, you need to ensure that you understand the risks involved taking into account your investment objectives and level of experience.

Follow Stuart's daily market analysishttps://analysis.hotforex.com