global imbal jan 23 - university of california,...

TRANSCRIPT

Glo

bal I

mba

lanc

es

Janu

ary

23rd

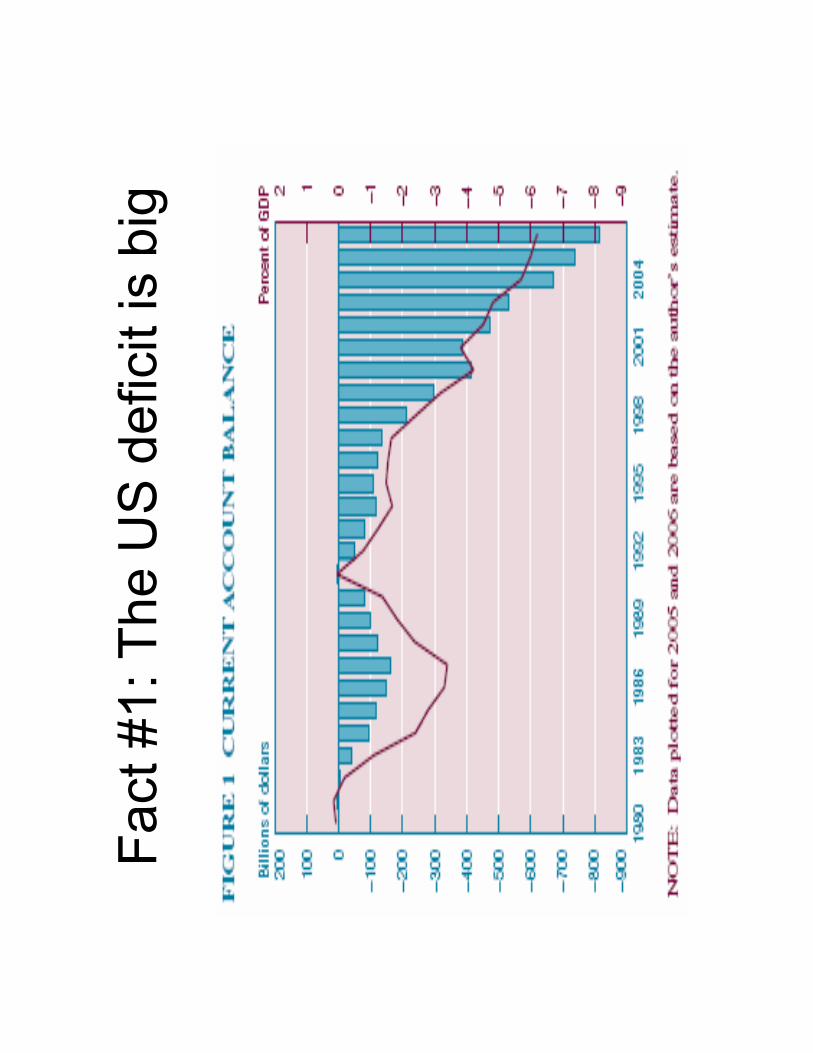

Fact

#1:

The

US

def

icit

is b

ig

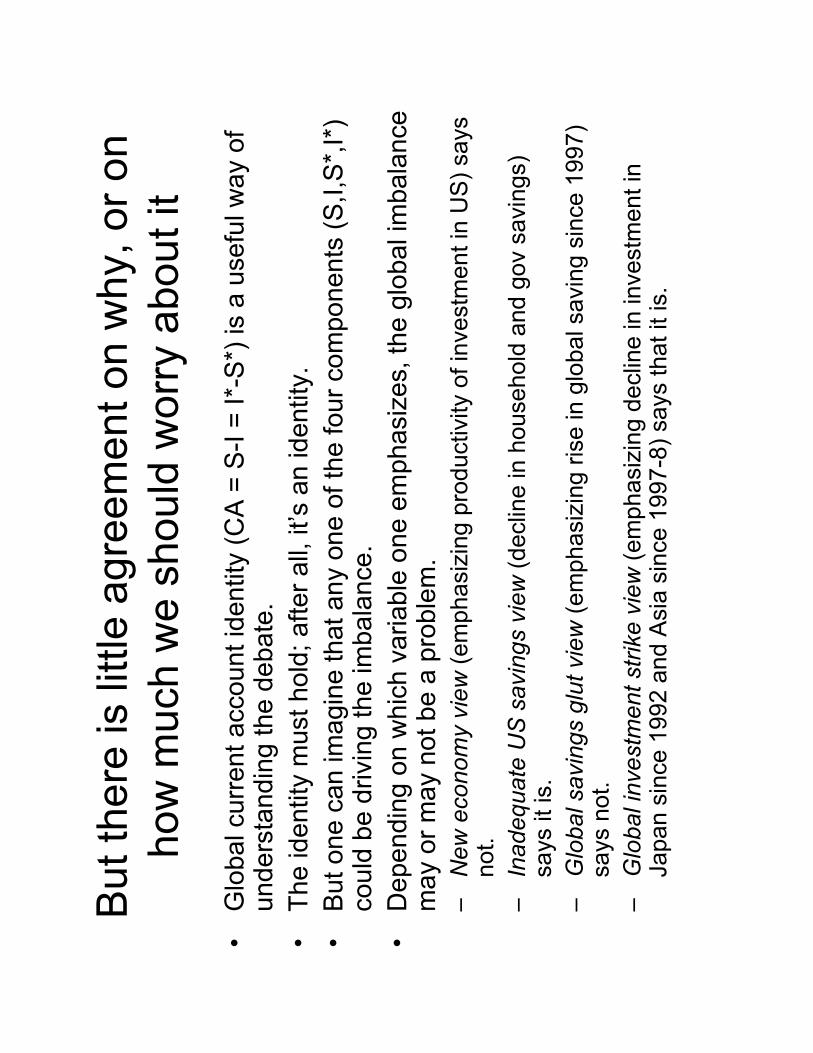

But

ther

e is

littl

e ag

reem

ent o

n w

hy, o

r on

how

muc

h w

e sh

ould

wor

ry a

bout

it•

Glo

bal c

urre

nt a

ccou

nt id

entit

y (C

A =

S-I

= I*-

S*)

is a

use

ful w

ay o

f un

ders

tand

ing

the

deba

te.

•Th

e id

entit

y m

ust h

old;

afte

r all,

it’s

an

iden

tity.

•B

ut o

ne c

an im

agin

e th

at a

ny o

ne o

f the

four

com

pone

nts

(S,I,

S*,I

*)

coul

d be

driv

ing

the

imba

lanc

e.•

Dep

endi

ng o

n w

hich

var

iabl

e on

e em

phas

izes

, the

glo

bal i

mba

lanc

em

ay o

r may

not

be

a pr

oble

m.

–N

ew e

cono

my

view

(em

phas

izin

g pr

oduc

tivity

of i

nves

tmen

t in

US

) say

s no

t.–

Inad

equa

te U

S s

avin

gs v

iew

(dec

line

in h

ouse

hold

and

gov

savi

ngs)

sa

ys it

is.

–G

loba

l sav

ings

glu

t vie

w(e

mph

asiz

ing

rise

in g

loba

l sav

ing

sinc

e 19

97)

says

not

.–

Glo

bal i

nves

tmen

t stri

ke v

iew

(em

phas

izin

g de

clin

e in

inve

stm

ent i

n Ja

pan

sinc

e 19

92 a

nd A

sia

sinc

e 19

97-8

) say

s th

at it

is.

Wha

t abo

ut th

e ne

w e

cono

my

view

?

Wha

t abo

ut th

e ne

w e

cono

my

view

?•

Yes

, U.S

. pro

duct

ivity

gro

wth

, how

ever

m

easu

red,

has

rise

n to

Eur

ope’

s.•

The

next

slid

e sh

ows

this

for l

abor

pr

oduc

tivity

…

Her

e is

som

e ad

ditio

nal d

etai

l

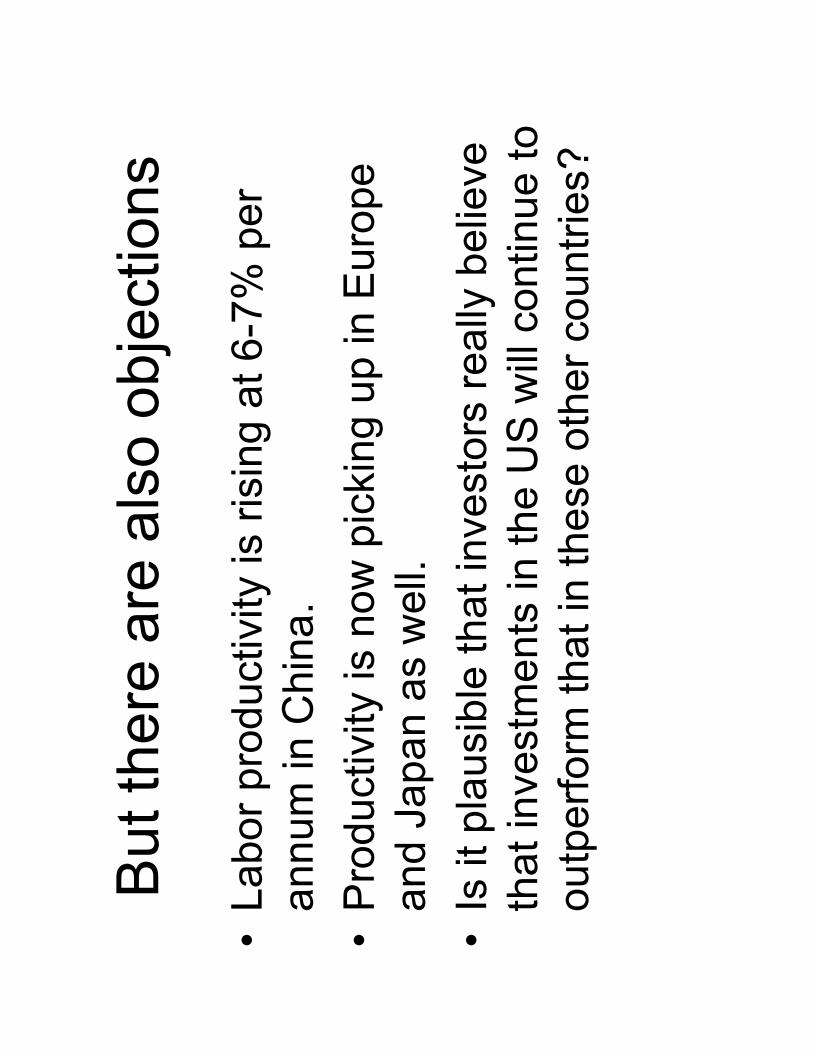

But

ther

e ar

e al

so o

bjec

tions

•La

bor p

rodu

ctiv

ity is

risi

ng a

t 6-7

% p

er

annu

m in

Chi

na.

•P

rodu

ctiv

ity is

now

pic

king

up

in E

urop

e an

d Ja

pan

as w

ell.

•Is

it p

laus

ible

that

inve

stor

s re

ally

bel

ieve

th

at in

vest

men

ts in

the

US

will

cont

inue

to

outp

erfo

rm th

at in

thes

e ot

her c

ount

ries?

And

ther

e ha

s be

en n

o in

vest

men

t sur

ge in

th

e U

nite

d S

tate

s.S

ince

the

colla

pse

of th

e H

igh

Tech

Bub

ble

in 2

000,

fore

ign

fund

s ha

ve b

een

flow

ing

mai

nly

into

deb

t, no

t int

o U

S s

tock

s as

this

st

ory

wou

ld p

redi

ct.

And

the

prin

cipl

e fo

reig

n in

vest

ors

have

bee

n fo

reig

n ce

ntra

l ban

ks, n

ot p

rivat

e fo

reig

n in

vest

ors.

Inde

ed, s

o fa

r as

we

can

tell,

fore

ign

cent

ral b

anks

ha

ve a

ccou

nted

for s

ome

75 p

erce

nt o

f fin

ance

fo

r the

US

cur

rent

acc

ount

bal

ance

in re

cent

ye

ars.

All

of th

is is

a b

it di

fficu

lt to

squ

are

with

the

New

E

cono

my

stor

y.

Wha

t abo

ut th

e in

adeq

uate

US

sa

ving

s vi

ew?

•Th

e fa

ct th

at h

ouse

hold

sav

ings

rate

s ha

ve fa

llen

to n

ear z

ero

is c

onsi

sten

t with

th

is e

mph

asis

.–

[See

the

next

slid

e]

Yes

, the

re h

as b

een

a pe

rson

al

savi

ngs

decl

ine

Two

obje

ctio

ns to

this

em

phas

is o

n lo

w U

.S. s

avin

gs•

Low

hou

seho

ld s

avin

g is

the

ratio

nal r

eact

ion

to th

e hi

gh

stoc

k m

arke

t and

hig

h ho

usin

g pr

ices

. A

nd th

e la

tter

refle

ct th

e he

alth

y fu

ndam

enta

l con

ditio

n of

the

US

ec

onom

y.–

But

this

ass

umes

the

valid

ity o

f the

new

-eco

nom

y ar

gum

ent.

•H

ouse

hold

sav

ing

is n

ot a

ll th

at m

atte

rs.

Cor

pora

tions

sa

ve to

o, a

nd c

orpo

rate

sav

ing

is a

t all-

time

high

s.–

So

the

next

gra

ph s

how

s a

mor

e co

mpr

ehen

sive

mea

sure

.–

It is

stil

l not

all

that

reas

surin

g.•

Not

e: P

rivat

e +S

&L

adds

Sta

te a

nd L

ocal

Gov

ernm

ent (

dis)

savi

ngto

ho

useh

old

and

corp

orat

e sa

ving

. Th

e ot

her s

avin

g lin

e th

en a

dds

fede

ral g

over

nmen

t (di

s)sa

ving

.

•Th

us, i

t is

hard

not

to c

oncl

ude

that

ther

e is

som

ethi

ng to

the

inad

equa

te U

.S. s

avin

gs v

iew

.

Wha

t abo

ut th

e fo

reig

n in

vest

men

t st

rike?

•It

is tr

ue th

at E

urop

ean

and

Japa

nese

in

vest

men

t hav

e be

en s

tagn

ant,

whi

le A

sian

in

vest

men

t dec

lined

afte

r 199

7 (a

fter t

he A

sian

fin

anci

al c

risis

).•

The

latte

r is

not n

eces

saril

y a

bad

thin

g, if

you

be

lieve

, as

man

y do

, tha

t muc

h of

the

inve

stm

ent o

f the

prio

r per

iod

was

rela

tivel

y in

effic

ient

.•

But

this

gen

eral

izat

ion

igno

res

Chi

na, w

here

in

vest

men

t has

bee

n ris

ing

shar

ply.

Of c

ours

e, S

* ha

s be

en ri

sing

fast

er

than

I* in

Chi

na•

This

brin

gs u

s to

the

final

“hig

h S

*” e

xpla

natio

n.•

This

is C

hairm

an B

erna

nke’

sfa

mou

s “g

loba

l sav

ings

gl

ut” s

tory

.•

With

the

wor

ld e

cono

my

grow

ing

rapi

dly,

ther

e is

lots

of

savi

ngs,

out

side

the

Uni

ted

Sta

tes

in p

artic

ular

. It

has

to

go s

omew

here

, and

it fl

ows

tow

ard

the

U.S

., fin

anci

ng

our c

urre

nt a

ccou

nt d

efic

it.•

This

sto

ry h

as th

e si

ngul

ar m

erit

of e

xpla

inin

g ho

w it

co

uld

be th

at e

ven

thou

gh th

e U

.S. i

s ru

nnin

g bi

g de

ficits

, glo

bal i

nter

est r

ates

are

low

.•

But

the

data

do

not o

bvio

usly

bea

r it o

ut.

•If

the

data

wer

e pe

rfect

, the

two

lines

co

uld

have

to

coin

cide

.•

But

they

do

not

obvi

ousl

y po

int t

o ex

cess

glo

bal s

avin

gs

as th

e dr

ivin

g fo

rce.

Whe

re d

oes

this

leav

e us

?•

It is

pro

babl

y le

ss a

ppro

pria

te to

talk

abo

ut a

glo

bal s

avin

g gl

ut th

an a

re

gion

al s

avin

g sh

ift, d

own

in th

e U

S, u

p in

the

rest

of t

he w

orld

.•

US

inve

stm

ent h

as h

eld

stea

dy, w

hile

inve

stm

ent h

as d

eclin

ed m

odes

tly in

th

e re

st o

f the

wor

ld fr

om m

id-1

990s

leve

ls.

•Fo

reig

ners

thus

may

be

will

ing

to p

ark

som

e of

thei

r sav

ings

, ofw

hich

they

ha

ve m

any,

in th

e U

.S.

To th

e ex

tent

that

this

is th

e dr

ivin

g fo

rce,

ext

erna

l de

ficits

at t

he c

urre

nt le

vel a

re s

usta

inab

le a

nd b

enig

n.–

To th

e ex

tent

that

inve

stor

s’ p

ortfo

lios

have

bee

n in

adeq

uate

ly d

iver

sifie

d in

tern

atio

nally

, fin

anci

al g

loba

lizat

ion

poin

ts in

the

sam

e di

rect

ion.

•B

ut th

e gl

obal

imba

lanc

e is

als

o be

ing

driv

en b

y th

e fa

ilure

of A

mer

ican

s to

fin

ance

inve

stm

ent i

n th

eir e

cono

my

out o

f the

ir ow

n sa

ving

s. T

o th

e ex

tent

th

at th

is is

the

driv

ing

forc

e, e

xter

nal d

efic

its a

t the

cur

rent

leve

l are

not

su

stai

nabl

e an

d be

nign

.•

This

ecl

ectic

vie

w w

ould

then

sug

gest

that

the

U.S

. can

sup

port

a hi

gher

ex

tern

al d

ebt/G

DP

ratio

than

bef

ore,

but

not

with

out l

imit.

–U

.S. d

ebt/G

DP

ratio

is c

urre

ntly

on

the

orde

r of 2

5 pe

r cen

t.–

A c

onse

nsus

vie

w w

ould

be

that

, in

the

futu

re, l

evel

s as

hig

h as

50 p

er c

ent

mig

ht b

e fe

asib

le.

So

wha

t kin

d of

adj

ustm

ent i

s ne

eded

?

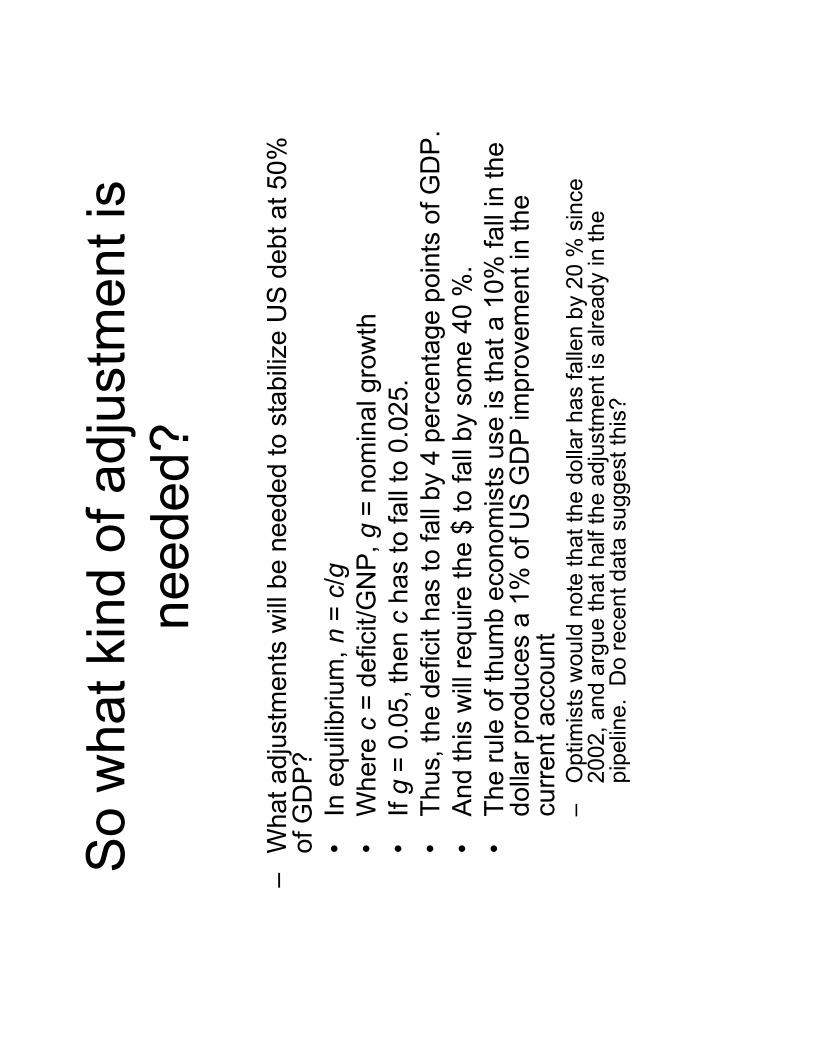

–W

hat a

djus

tmen

ts w

ill b

e ne

eded

to s

tabi

lize

US

deb

t at 5

0%

of G

DP

?•

In e

quili

briu

m, n

= c/

g•

Whe

re c

= de

ficit/

GN

P, g

= no

min

al g

row

th•

If g

= 0.

05, t

hen

cha

s to

fall

to 0

.025

.•

Thus

, the

def

icit

has

to fa

ll by

4 p

erce

ntag

e po

ints

of G

DP

.•

And

this

will

requ

ire th

e $

to fa

ll by

som

e 40

%.

•Th

e ru

le o

f thu

mb

econ

omis

ts u

se is

that

a 1

0% fa

ll in

the

dolla

r pro

duce

s a

1% o

f US

GD

P im

prov

emen

t in

the

curr

ent a

ccou

nt–

Opt

imis

ts w

ould

not

e th

at th

e do

llar h

as fa

llen

by 2

0 %

sin

ce

2002

, and

arg

ue th

at h

alf t

he a

djus

tmen

t is

alre

ady

in th

e pi

pelin

e. D

o re

cent

dat

a su

gges

t thi

s?

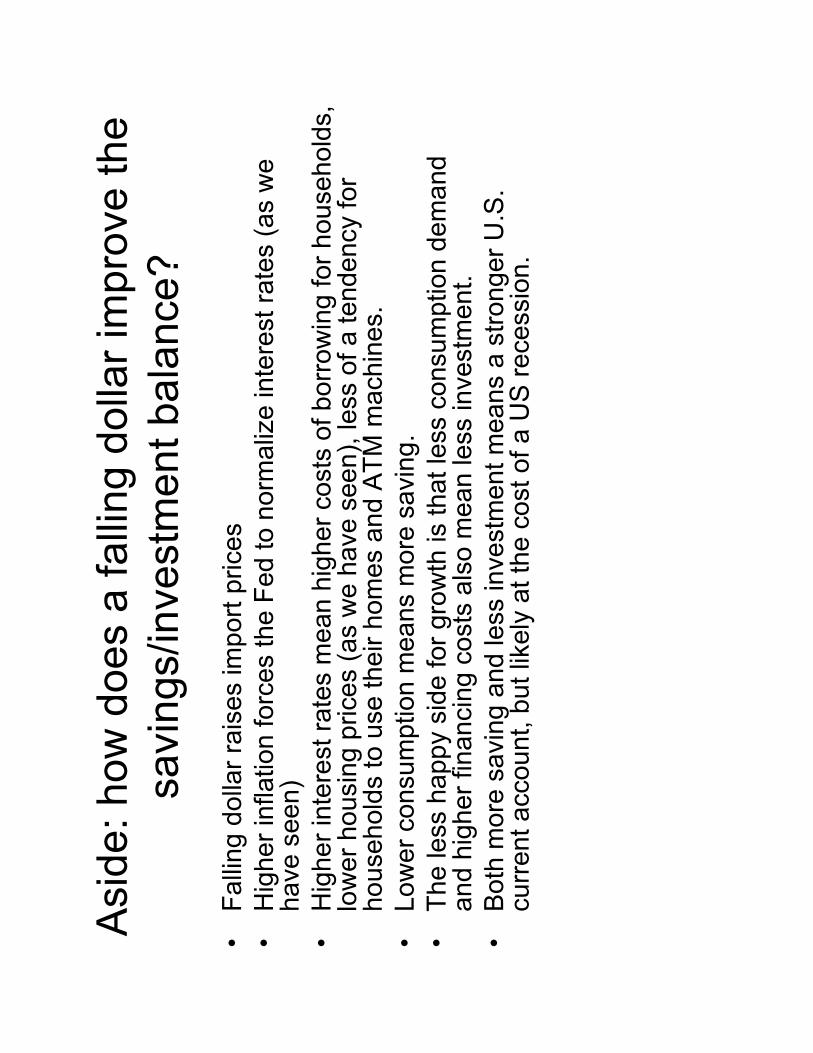

Asi

de: h

ow d

oes

a fa

lling

dolla

r im

prov

e th

e sa

ving

s/in

vest

men

t bal

ance

?

Asi

de: h

ow d

oes

a fa

lling

dolla

r im

prov

e th

e sa

ving

s/in

vest

men

t bal

ance

?•

Falli

ng d

olla

r rai

ses

impo

rt pr

ices

•H

ighe

r inf

latio

n fo

rces

the

Fed

to n

orm

aliz

e in

tere

st ra

tes

(as

we

have

see

n)•

Hig

her i

nter

est r

ates

mea

n hi

gher

cos

ts o

f bor

row

ing

for h

ouse

hold

s,

low

er h

ousi

ng p

rices

(as

we

have

see

n), l

ess

of a

tend

ency

for

hous

ehol

ds to

use

thei

r hom

es a

nd A

TM m

achi

nes.

•Lo

wer

con

sum

ptio

n m

eans

mor

e sa

ving

.•

The

less

hap

py s

ide

for g

row

th is

that

less

con

sum

ptio

n de

man

d an

d hi

gher

fina

ncin

g co

sts

also

mea

n le

ss in

vest

men

t.•

Bot

h m

ore

savi

ng a

nd le

ss in

vest

men

t mea

ns a

stro

nger

U.S

. cu

rrent

acc

ount

, but

like

ly a

t the

cos

t of a

US

rece

ssio

n.

Asi

de: “

dark

mat

ter”

•B

ut, i

f you

look

ed a

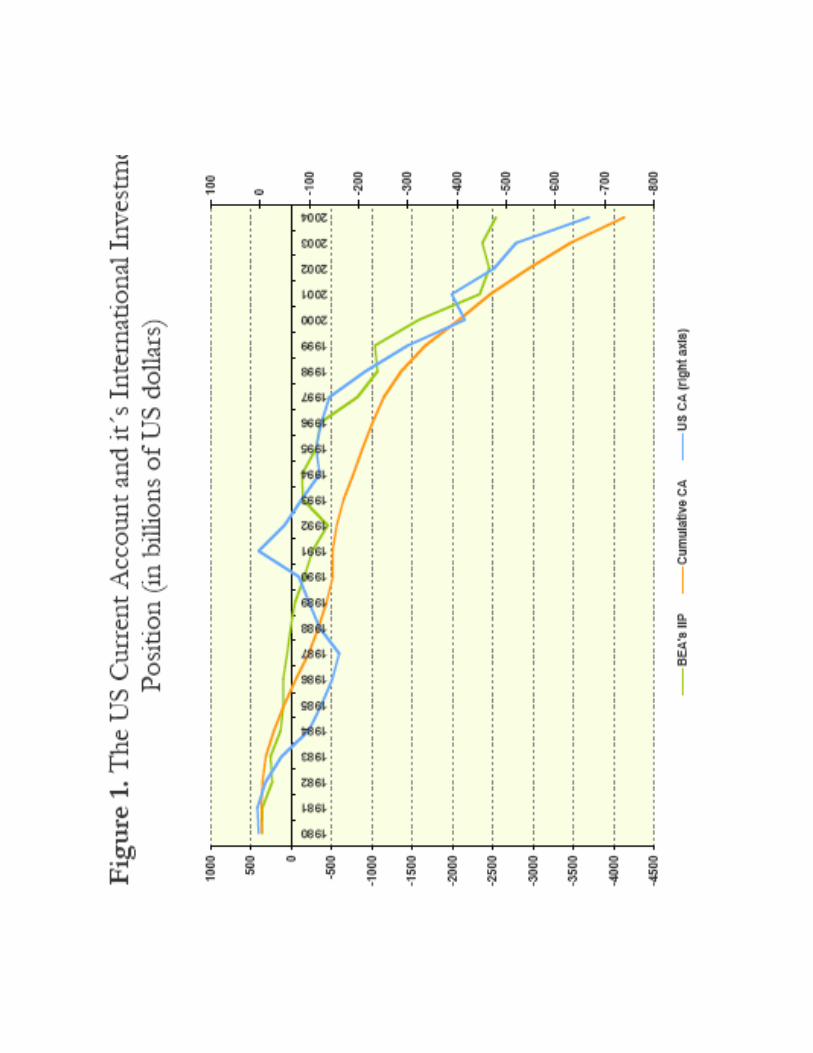

t Fig

ure

1 of

the

Chi

nn

artic

le, y

ou w

ill se

e th

at th

e U

S c

urre

nt

acco

unt h

as m

oved

into

dee

p de

ficit

rece

ntly

with

out a

lso

incr

easi

ng U

S n

et

fore

ign

debt

.

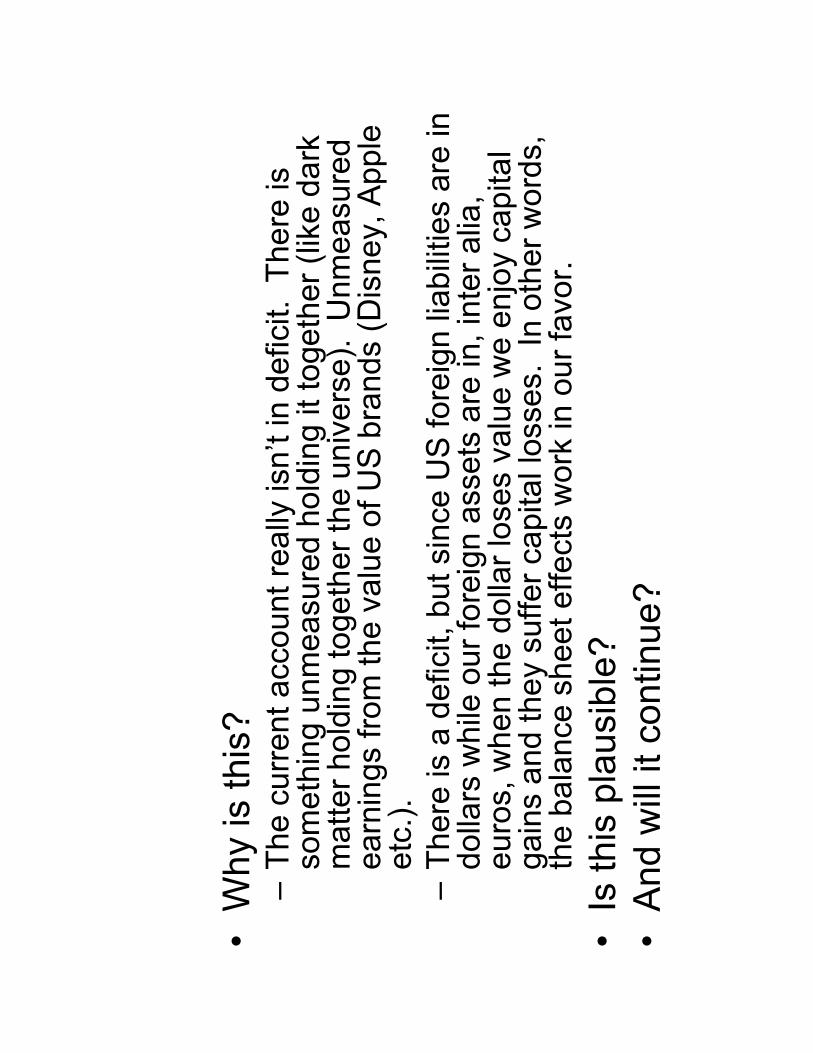

•W

hy is

this

?–

The

curr

ent a

ccou

nt re

ally

isn’

t in

defic

it. T

here

is

som

ethi

ng u

nmea

sure

d ho

ldin

g it

toge

ther

(lik

e da

rk

mat

ter h

oldi

ng to

geth

er th

e un

iver

se).

Unm

easu

red

earn

ings

from

the

valu

e of

US

bra

nds

(Dis

ney,

App

le

etc.

).–

Ther

e is

a d

efic

it, b

ut s

ince

US

fore

ign

liabi

litie

s ar

e in

do

llars

whi

le o

ur fo

reig

n as

sets

are

in, i

nter

alia

, eu

ros,

whe

n th

e do

llar l

oses

val

ue w

e en

joy

capi

tal

gain

s an

d th

ey s

uffe

r cap

ital l

osse

s. I

n ot

her w

ords

, th

e ba

lanc

e sh

eet e

ffect

s w

ork

in o

ur fa

vor.

•Is

this

pla

usib

le?

•A

nd w

ill it

con

tinue

?

Won

’t fo

reig

ners

cat

ch o

n?

•W

on’t

they

dem

and

that

we

borro

w fr

om

them

in th

eir o

wn

curre

ncie

s?–

This

will

occ

ur, i

n pr

actic

e, b

y th

eir

dive

rsify

ing

out o

f exi

stin

g do

llar b

alan

ces.

•If

so, b

alan

ce s

heet

effe

cts

won

’t au

tom

atic

ally

wor

k in

our

favo

r.•

On

thes

e an

d ot

her g

roun

ds, I

am

incl

ined

to

dis

mis

s th

e re

assu

ring

“dar

k m

atte

r vi

ew.”

If so

, the

dol

lar m

ust f

all b

y at

leas

t an

othe

r 20%

•U

S tr

ade

with

Asi

a eq

uals

US

trad

e w

ith E

urop

e to

a fi

rst a

ppro

xim

atio

n.•

So

this

can

be

acco

mpl

ishe

d ei

ther

by:

–A

20%

fall

agai

nst b

oth

the

euro

and

Asi

an c

urre

ncie

s–

Or a

10%

fall

agai

nst t

he e

uro

and

a 30

% fa

ll ag

ains

t A

sian

cur

renc

ies

(mor

e ap

prop

riate

giv

en th

e st

reng

th

of th

eir r

espe

ctiv

e ec

onom

ies)

.•

But

it im

plie

s a

“bru

tal”

40%

app

reci

atio

n of

the

euro

aga

inst

the

dolla

r if A

sian

cur

renc

ies

don’

t m

ove.

–A

nd w

heth

er A

sian

cur

renc

ies

mov

e hi

nges

on

wha

t th

e bi

g do

g, C

hina

, doe

s.

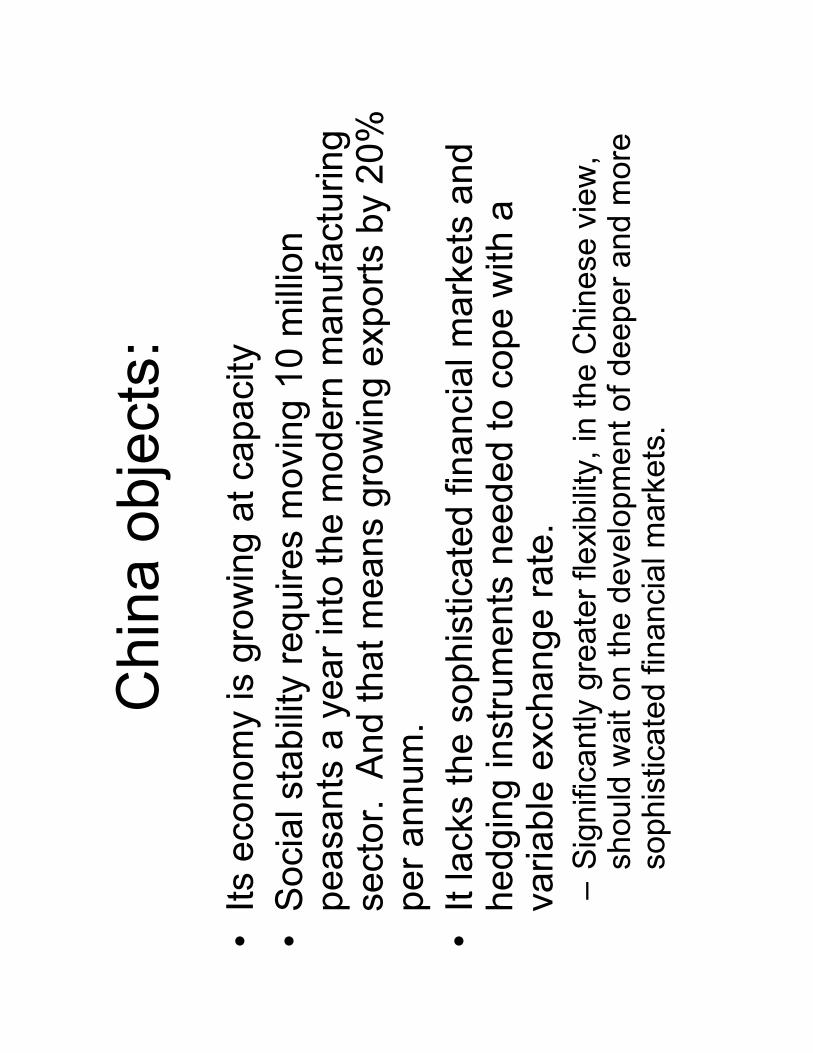

Chi

na o

bjec

ts:

•Its

eco

nom

y is

gro

win

g at

cap

acity

•S

ocia

l sta

bilit

y re

quire

s m

ovin

g 10

mill

ion

peas

ants

a y

ear i

nto

the

mod

ern

man

ufac

turin

g se

ctor

. A

nd th

at m

eans

gro

win

g ex

ports

by

20%

pe

r ann

um.

•It

lack

s th

e so

phis

ticat

ed fi

nanc

ial m

arke

ts a

nd

hedg

ing

inst

rum

ents

nee

ded

to c

ope

with

a

varia

ble

exch

ange

rate

.–

Sig

nific

antly

gre

ater

flex

ibili

ty, i

n th

e C

hine

se v

iew

, sh

ould

wai

t on

the

deve

lopm

ent o

f dee

per a

nd m

ore

soph

istic

ated

fina

ncia

l mar

kets

.

But

is th

e R

MB

in fa

ct

unde

rval

ued?

•E

cono

mis

ts, n

ot fo

r the

firs

t tim

e, d

on’t

agre

e.•

They

take

two

appr

oach

es to

ans

wer

ing

this

que

stio

n:

So

is th

e R

MB

und

erva

lued

?

•E

cono

mis

ts ta

ke tw

o ap

proa

ches

to

answ

erin

g th

is q

uest

ion:

–Th

e si

mpl

e or

aug

men

ted

PP

P a

ppro

ach

–Th

e ex

tern

al b

alan

ce a

ppro

ach

–E

very

one

know

s w

hat t

hese

are

?

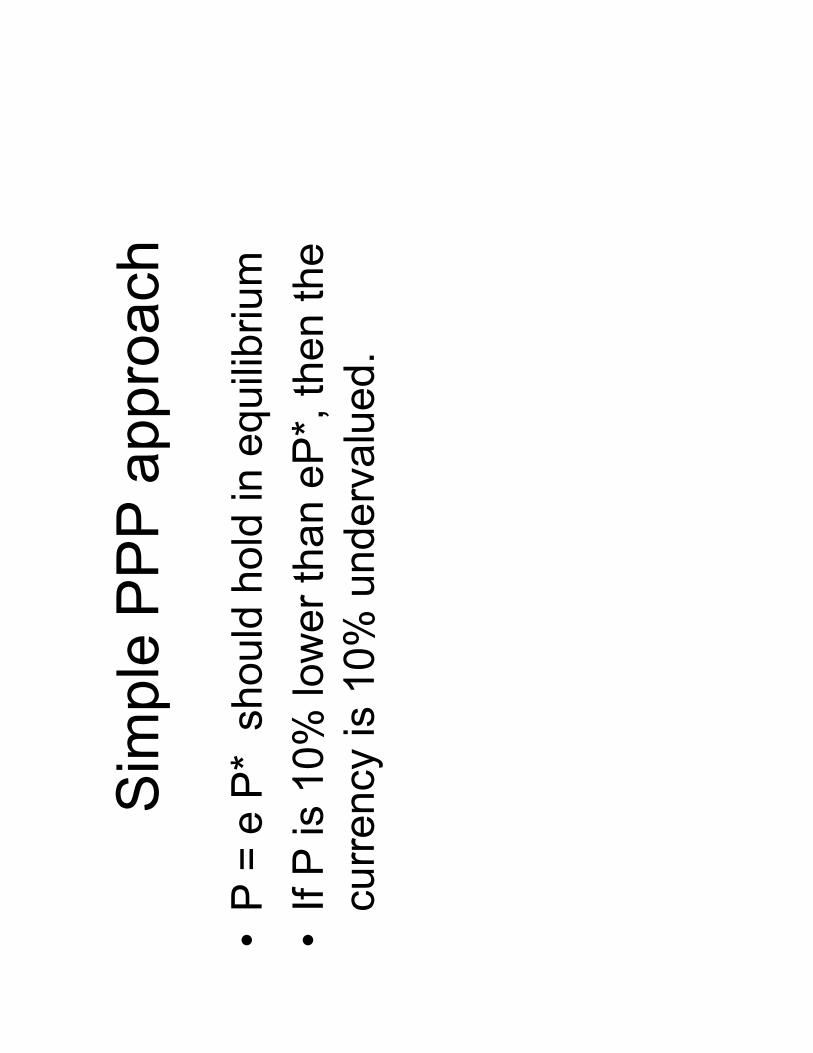

Sim

ple

PP

P a

ppro

ach

•P

= e

P*

sho

uld

hold

in e

quilib

rium

•If

P is

10%

low

er th

an e

P*,

then

the

curre

ncy

is 1

0% u

nder

valu

ed.

But

are

ther

e pr

oble

ms

with

the

sim

ple

PP

P a

ppro

ach?

But

are

ther

e pr

oble

ms

with

the

sim

ple

PP

P a

ppro

ach?

•A

bsol

ute

PP

P p

laus

ibly

hol

ds fo

r tra

ded

good

s.•

But

not

for t

rade

d go

ods.

–Th

e co

st o

f a s

hoes

hine

or a

hai

rcut

in In

dia

is m

uch

low

er th

an th

e co

st o

f a s

hoes

hine

or h

airc

ut in

A

mer

ica.

•E

very

one

unde

rsta

nds

why

?–

This

tend

ency

for t

he p

rice

of n

ontra

ded

good

s to

be

high

er w

here

inco

mes

are

hig

her e

ven

has

its o

wn

nam

e, th

e B

alas

sa-S

amue

lson

effe

ct.

–B

ut h

ow m

uch

high

er?

How

do

Chi

nn e

t al.

atte

mpt

to

ans

wer

this

?

They

use

the

augm

ente

d P

PP

ap

proa

ch•

They

regr

ess

P/e

P*

on Y

PC

/ YP

C*

•Th

is th

en g

ener

ates

the

typi

cal

(“equ

ilibriu

m”)

rela

tions

hip.

•Th

en lo

ok to

see

by

how

muc

h a

coun

try

devi

ates

from

that

to ju

dge

by h

ow fa

r its

cu

rrenc

y is

“out

of e

quilib

rium

.”

Her

e’s

the

typi

cal r

elat

ions

hip

(sol

id li

ne),

1 &

2

s.e.

ban

ds, a

nd a

ctua

l for

Chi

na.

So

they

co

nclu

de: C

hina

’s c

urre

ncy

is 4

0% to

o lo

w

Wha

t’s w

rong

with

this

pic

ture

?

Wha

t’s w

rong

with

this

pic

ture

?

•A

nsw

er d

epen

ds o

n yo

ur n

ull h

ypot

hesi

s.–

Chi

na is

stil

l with

in th

e 2

s.e.

ban

ds–

We

also

can

not r

ejec

t the

nul

l tha

t the

re

nmin

biis

0%

und

erva

lued

.–

So

the

test

is a

t bes

t ver

y w

eak.

Wha

t els

e is

wro

ng w

ith th

is

pict

ure?

Wha

t els

e is

wro

ng w

ith th

is

pict

ure?

•Th

e te

st a

ssum

es th

at n

othi

ng b

esid

es

rela

tive

inco

mes

affe

cts

rela

tive

pric

es.

•In

par

ticul

ar, a

s th

e au

thor

s ac

know

ledg

e (y

ou w

ill ha

ve h

ad to

be

a ca

refu

l rea

der t

o fin

d th

e fo

otno

te),

it as

sum

es “e

xter

nal

bala

nce”

(tha

t cur

rent

acc

ount

s ar

e in

eq

uilib

rium

).•

And

the

curre

nt a

ccou

nt b

alan

ce b

etw

een

the

US

and

Chi

na is

, in

fact

, far

from

zer

o.

So

is it

pos

sibl

e to

aug

men

t the

aug

men

ted

PP

P a

ppro

ach

to ta

ke th

is fa

ct o

n bo

ard?

So

is it

pos

sibl

e to

aug

men

t the

aug

men

ted

PP

P a

ppro

ach

to ta

ke th

is fa

ct o

n bo

ard?

•Im

agin

e re

gres

sing

P/e

P*

on Y

PC

/ YP

C*

and

also

on

the

Cur

rent

Acc

ount

Bal

ance

.•

But

the

CA

B a

nd re

lativ

e pr

ices

are

si

mul

tane

ousl

y de

term

ined

. S

o es

timat

ing

this

rela

tions

hip

is e

asie

r sai

d th

an d

one.

(D

oing

so

requ

ires

an in

stru

men

t. M

ight

be

an

inte

rest

ing

subj

ect f

or a

fina

l pap

er

for t

his

cour

se.

I hav

e th

e au

thor

s’ d

ata

set i

f you

’d li

ke to

try.

)

Alte

rnat

ive

is th

e ex

tern

al b

alan

ce

appr

oach

•W

e ha

ve a

lread

y se

en h

ow th

is w

orks

. Y

ou

mak

e as

sum

ptio

ns a

bout

:–

By

how

muc

h a

10%

dep

reci

atio

n of

the

dolla

r will

im

prov

e th

e U

.S. C

A d

efic

it (r

ecal

l: ty

pica

lly,

econ

omis

ts a

ssum

e by

1%

of U

S G

DP

)–

Wha

t CA

/GD

P ra

tio is

sus

tain

able

for t

he U

S

Rec

all:

typi

cally

eco

nom

ists

ass

ume

2.5%

, sin

ce

toge

ther

with

nom

inal

inco

me

grow

th o

f 5%

this

yie

lds

a 50

% d

ebt/G

DP

ratio

in e

quili

briu

m.

Rem

inde

r of t

he u

nder

lyin

g ar

ithm

etic

•In

equ

ilibr

ium

: n =

c/g

, whe

re:

–n

= ra

tio o

f net

ext

erna

l deb

t rel

ativ

e to

GD

P•

50%

wou

ld b

e a

very

hig

h ra

tio fo

r a c

ount

ry li

ke th

e U

nite

d S

tate

s. W

e ha

ve n

ever

see

n a

larg

e co

untry

w

ith a

ratio

that

hig

h du

ring

peac

etim

e.–

c =

curr

ent a

ccou

nt d

efic

it re

lativ

e to

GD

P

–g

= no

min

al g

row

th ra

te o

f the

eco

nom

y–

So

if g=

5 (3

% g

row

th +

2%

infla

tion)

, we

mus

t cu

t the

def

icit

to 2

1/2

% o

f GD

P fr

om it

s cu

rren

t 6

½ p

er c

ent

•Th

en to

cut

the

U.S

. def

icit

ratio

by

4 po

ints

, the

do

llar h

as to

fall

by 4

0% (h

opef

ully

, onl

y an

ad

ditio

nal 2

0%, s

ince

20%

has

alre

ady

occu

rred

).–

Not

e th

at n

ow w

e ar

e ta

lkin

g ab

out t

he d

olla

r’s v

alue

ag

ains

t all

fore

ign

curr

enci

es (i

ts “t

rade

wei

ghte

d va

lue”

), an

d no

t jus

t its

val

ue a

gain

st th

e re

nmin

bi.

–B

ut fo

r the

reas

ons

just

des

crib

ed, i

t is

hard

to

imag

ine

that

we

will

see

a s

moo

th a

djus

tmen

t with

out

Chi

nese

par

ticip

atio

n.

So

wha

t sho

uld

the

Chi

nese

do?

•M

ove

mor

e qu

ickl

y in

the

dire

ctio

n of

gre

ater

flex

ibili

ty,

and

let t

he re

nmin

biap

prec

iatio

n.•

Rea

lize

that

the

finan

cial

mar

ket d

evel

opm

ent t

hey

priz

e re

spon

ds to

ass

et m

arke

t fle

xibi

lity

(it is

not

mer

ely

a pr

econ

ditio

n).

–Th

at is

a le

sson

of J

apan

ese

expe

rienc

e in

the

1970

s.•

And

if C

hina

mov

es, t

he re

st o

f Asi

a ca

n co

ntin

ue

mov

ing.

•Th

e en

tire

burd

en w

ill n

ot fa

ll, in

this

cas

e on

Eur

ope.

•M

eanw

hile

, Chi

na a

nd o

ther

Asi

an c

ount

ries

can

stim

ulat

e de

man

d.•

And

one

can

then

at l

east

hol

d ou

t hop

e fo

r the

po

ssib

ility

of s

moo

th re

bala

ncin

g of

the

glob

al e

cono

my.