glenn r. mueller, ph.d. johns hopkins university real estate institute director, capital markets...

Post on 21-Dec-2015

216 views

TRANSCRIPT

Glenn R. Mueller, Ph.D.Johns Hopkins University

Real Estate InstituteDirector, Capital Markets & International Programs

&

Legg Mason, Inc.Real Estate Research Group

Real Estate Investment Strategist

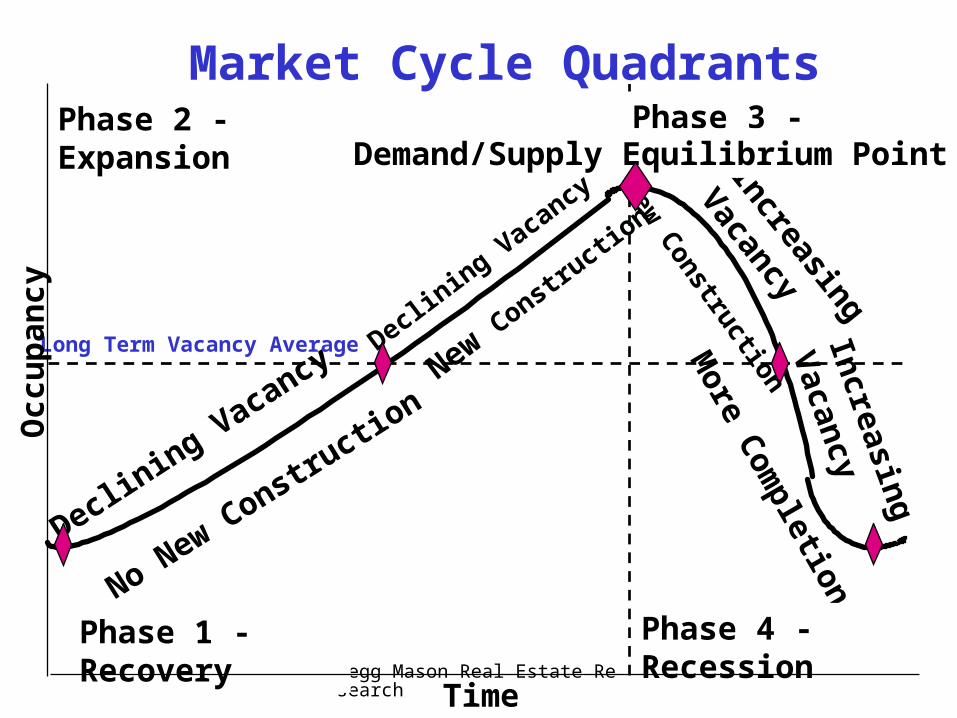

Market Cycle AnalysisMarket Cycle Analysis

Physical CyclePhysical Cycle

Demand, Supply and Vacancy Demand, Supply and Vacancy

affect Rental Growthaffect Rental Growth

Legg Mason Real Estate Research

Market Cycle Quadrants

Declining V

acancy N

ew C

onstruction

No New Constructio

n

Increasing

Vacancy

Declining Vacancy

Increasing

Vacancy

More C

ompletions

New Constr

uction

Phase 1 - Recovery

Phase 2 - Expansion

Phase 3 - Hypersupply

Phase 4 - Recession

Demand/Supply Equilibrium Point

Long Term Vacancy Average

Occ

up

ancy

Time

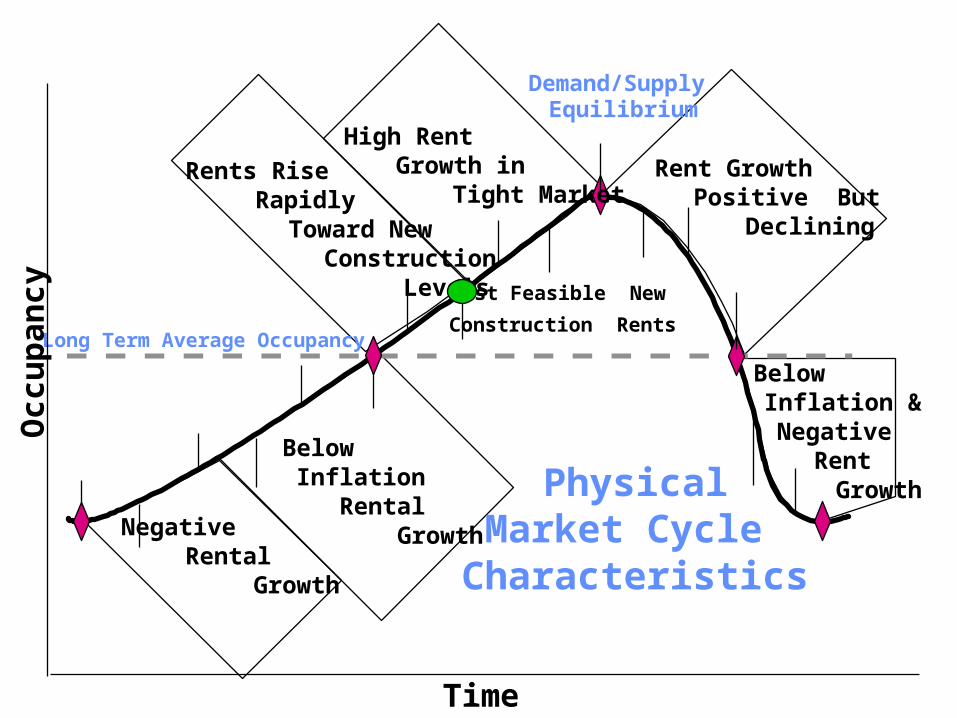

PhysicalMarket Cycle

Characteristics

Negative Rental Growth

Below Inflation Rental Growth

Rents Rise Rapidly Toward New Construction Levels

High Rent Growth in Tight Market

Demand/Supply Equilibrium

Rent Growth Positive But Declining

-Below Inflation & Negative Rent Growth

Cost Feasible New

Construction RentsLong Term Average Occupancy

Occ

up

ancy

Time

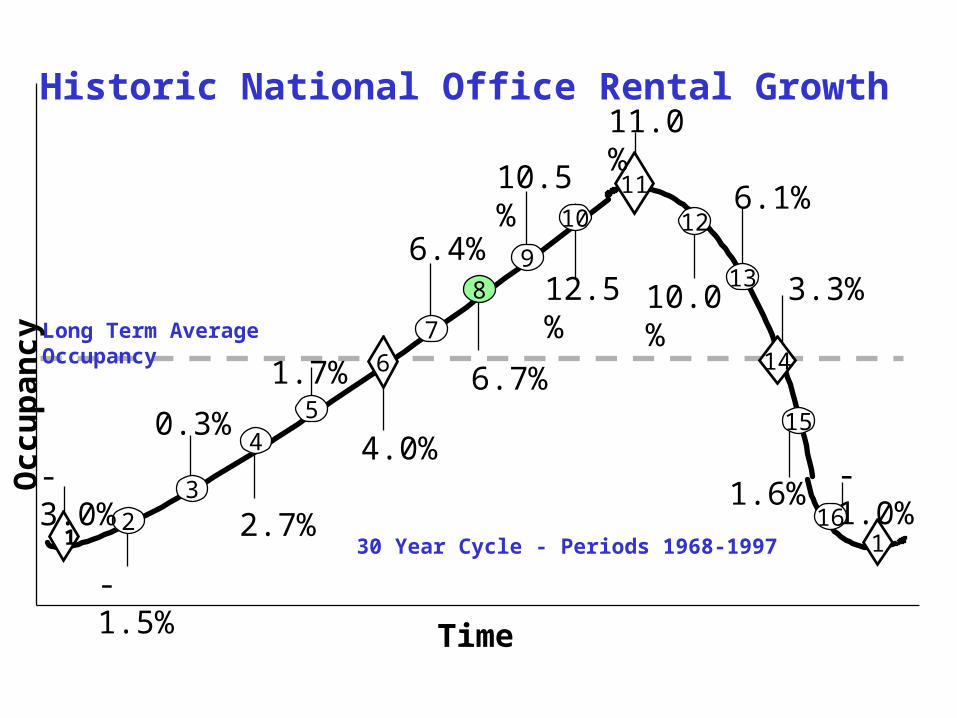

2

54

3

89

7

10

16

15

13

1

6

11

14

1

12

0.3%

2.7%

-3.0%

-1.5%

1.7%

4.0%

6.4%

11.0%

12.5%

10.5%

6.7%

-1.0%1.6%

3.3%

6.1%

10.0%

Historic National Office Rental Growth

30 Year Cycle - Periods 1968-1997

Long Term Average Occupancy

Occ

up

ancy

Time

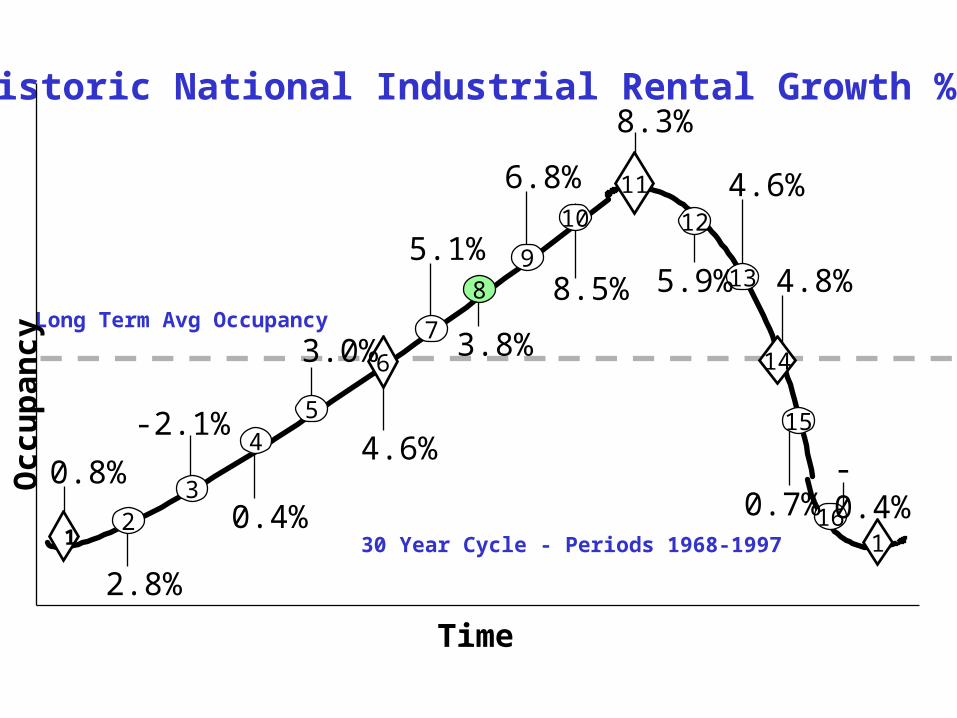

2

54

3

89

7

10

16

15

13

1

6

11

14

1

12

-2.1%

Historic National Industrial Rental Growth %

0.4%

0.8%

2.8%

3.0%

4.6%

5.1%

8.3%

8.5%

6.8%

3.8%

-0.4%0.7%

4.8%

4.6%

5.9%

30 Year Cycle - Periods 1968-1997

Long Term Avg Occupancy

Occ

up

ancy

Time

Orange County+1

Riverside+1

LT Average Occupancy

Source: Mueller, 2004

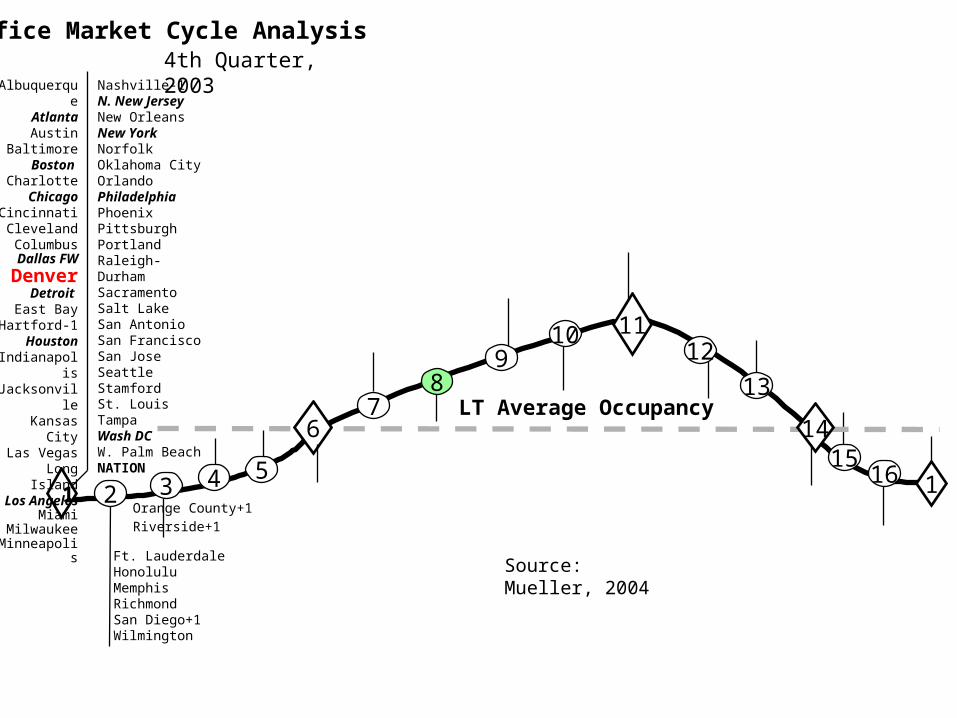

11

1467

89

1012

13

115

165432 1

Office Market Cycle Analysis4th Quarter, 2003

Nashville-1N. New JerseyNew OrleansNew YorkNorfolkOklahoma CityOrlandoPhiladelphiaPhoenixPittsburghPortlandRaleigh-DurhamSacramentoSalt LakeSan AntonioSan FranciscoSan JoseSeattleStamfordSt. LouisTampaWash DCW. Palm BeachNATION

Ft. LauderdaleHonoluluMemphisRichmondSan Diego+1Wilmington

AlbuquerqueAtlantaAustin

BaltimoreBoston

CharlotteChicago

CincinnatiClevelandColumbus

Dallas FW

DenverDetroit

East BayHartford-1

HoustonIndianapolisJacksonvilleKansas City

Las VegasLong IslandLos Angeles

MiamiMilwaukee

Minneapolis

Source: Mueller, 2004

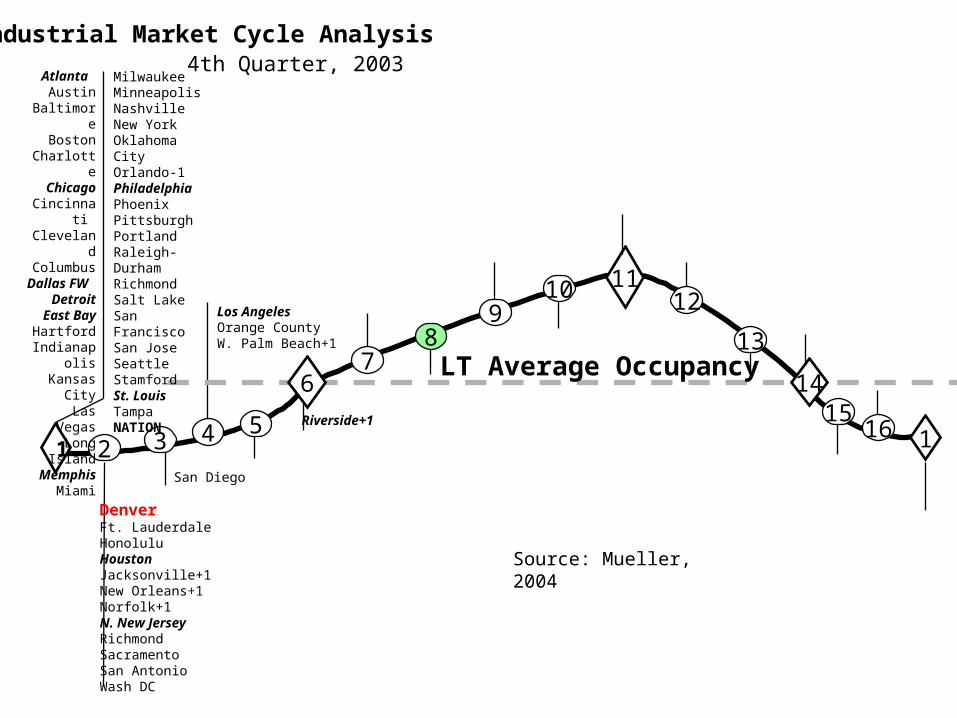

11

1467

89

10 12

13

115

165432 1

4th Quarter, 2003

LT Average Occupancy

Industrial Market Cycle Analysis

DenverFt. LauderdaleHonoluluHoustonJacksonville+1New Orleans+1Norfolk+1N. New JerseyRichmondSacramentoSan AntonioWash DC

San Diego

MilwaukeeMinneapolisNashvilleNew YorkOklahoma CityOrlando-1PhiladelphiaPhoenixPittsburghPortlandRaleigh-DurhamRichmondSalt LakeSan FranciscoSan JoseSeattleStamfordSt. LouisTampaNATION

Atlanta Austin

BaltimoreBoston

CharlotteChicago

Cincinnati ClevelandColumbus

Dallas FW Detroit

East BayHartford

IndianapolisKansas City

Las VegasLong Island

MemphisMiami

Los AngelesOrange CountyW. Palm Beach+1

Riverside+1

Source: Mueller, 2004

11

1467

89

10 12

115

165432 1BostonHonoluluSacramentoW. Palm BeachWash DC

LT Average Occupancy

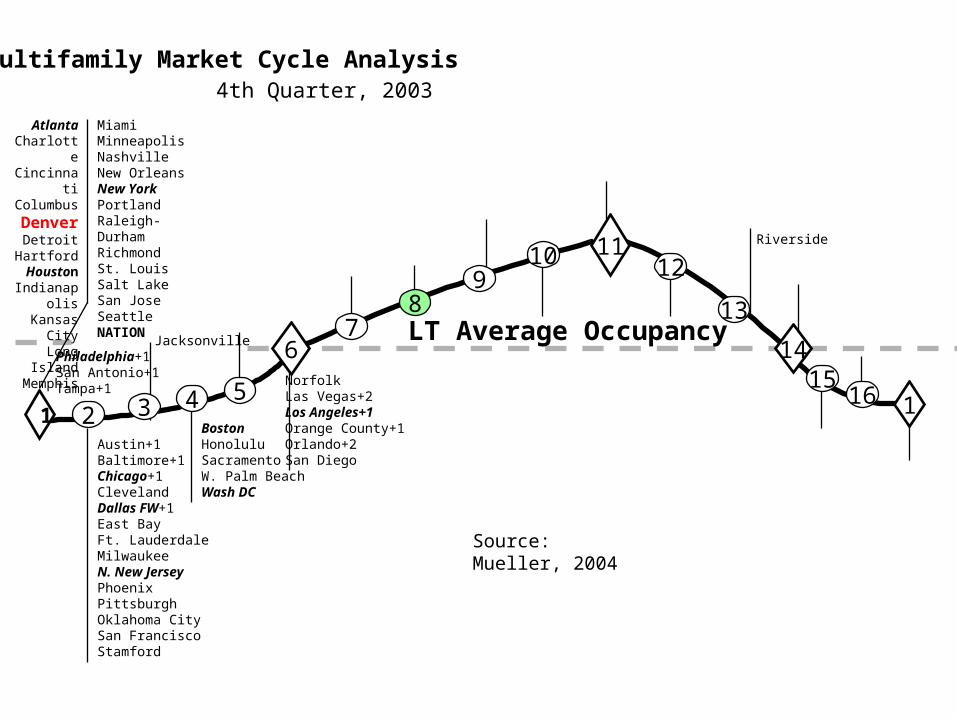

Multifamily Market Cycle Analysis4th Quarter, 2003

NorfolkLas Vegas+2Los Angeles+1Orange County+1Orlando+2San Diego

Riverside

Austin+1Baltimore+1Chicago+1ClevelandDallas FW+1East BayFt. LauderdaleMilwaukeeN. New JerseyPhoenixPittsburghOklahoma CitySan FranciscoStamford

13

AtlantaCharlotte

CincinnatiColumbus

DenverDetroit

HartfordHouston

IndianapolisKansas CityLong Island

Memphis

MiamiMinneapolisNashvilleNew OrleansNew YorkPortlandRaleigh-DurhamRichmondSt. LouisSalt LakeSan JoseSeattleNATION

Philadelphia+1San Antonio+1Tampa+1

Jacksonville

Source: Mueller, 2004

11

1467

89 12

13

115

165432 1

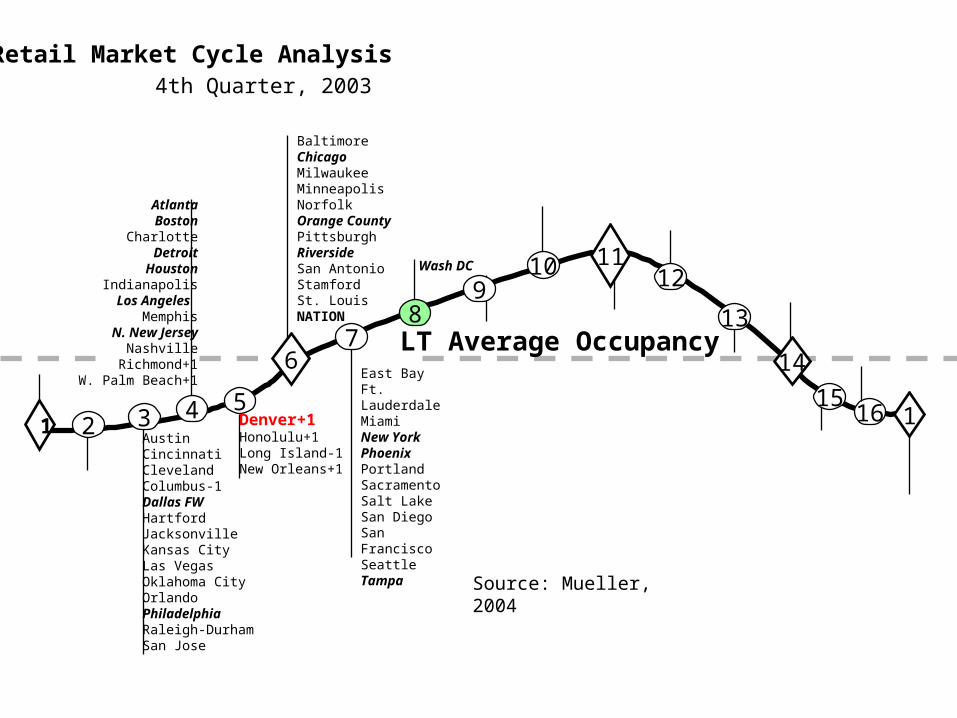

Retail Market Cycle Analysis

10

LT Average Occupancy

4th Quarter, 2003

East BayFt. LauderdaleMiamiNew YorkPhoenixPortlandSacramentoSalt LakeSan DiegoSan FranciscoSeattleTampa

BaltimoreChicagoMilwaukeeMinneapolisNorfolkOrange CountyPittsburghRiversideSan AntonioStamfordSt. LouisNATION

AustinCincinnatiClevelandColumbus-1Dallas FWHartfordJacksonvilleKansas CityLas VegasOklahoma CityOrlandoPhiladelphiaRaleigh-DurhamSan Jose

AtlantaBoston

CharlotteDetroit

HoustonIndianapolis

Los Angeles Memphis

N. New JerseyNashville

Richmond+1W. Palm Beach+1

Wash DC

Denver+1Honolulu+1Long Island-1New Orleans+1

Source: Mueller, 2004

1467

89 12

13

115

165

432 1

1110

LT Average Occupancy

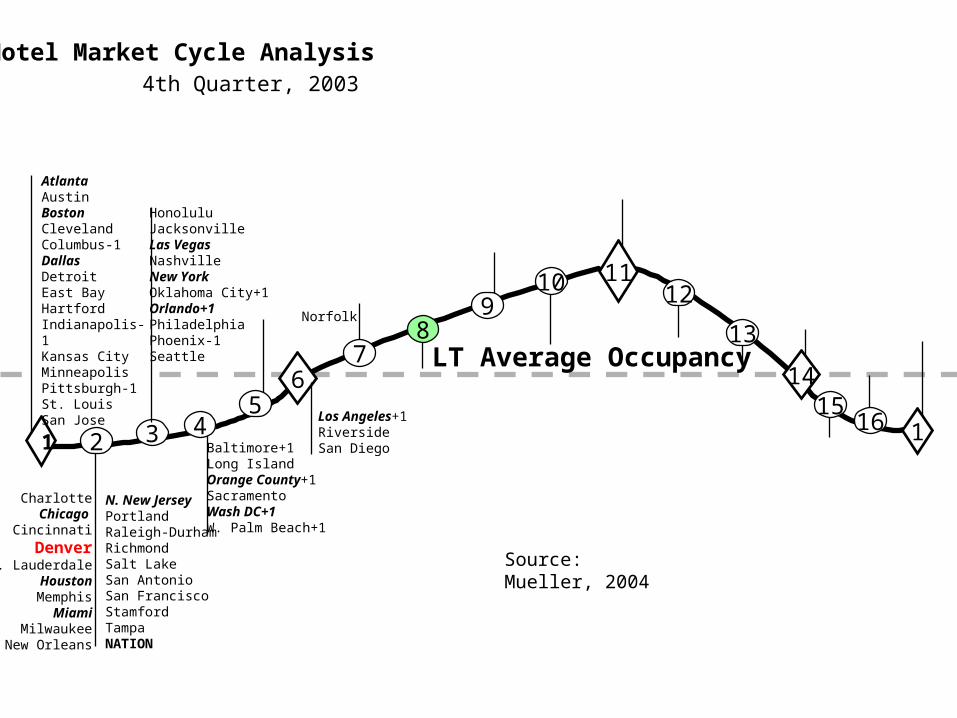

Hotel Market Cycle Analysis4th Quarter, 2003

Norfolk

HonoluluJacksonvilleLas VegasNashvilleNew YorkOklahoma City+1Orlando+1PhiladelphiaPhoenix-1Seattle

Baltimore+1Long IslandOrange County+1SacramentoWash DC+1W. Palm Beach+1

Los Angeles+1RiversideSan Diego

AtlantaAustinBostonClevelandColumbus-1DallasDetroitEast BayHartfordIndianapolis-1Kansas CityMinneapolisPittsburgh-1St. LouisSan Jose

CharlotteChicago

Cincinnati

DenverFt. Lauderdale

HoustonMemphis

MiamiMilwaukee

New Orleans

N. New JerseyPortlandRaleigh-DurhamRichmondSalt LakeSan AntonioSan FranciscoStamfordTampaNATION

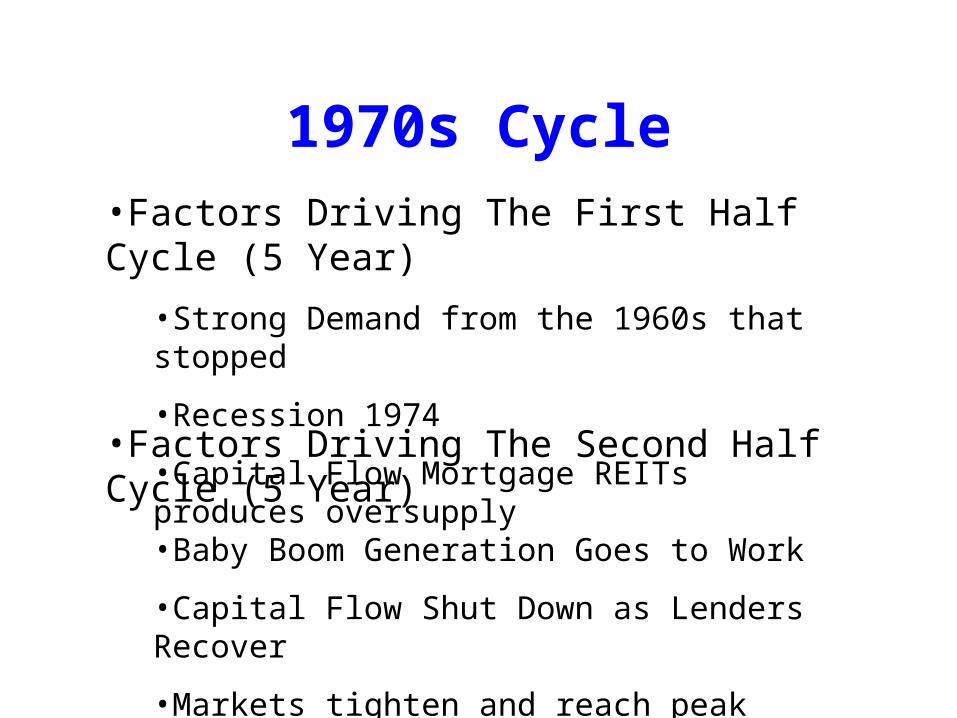

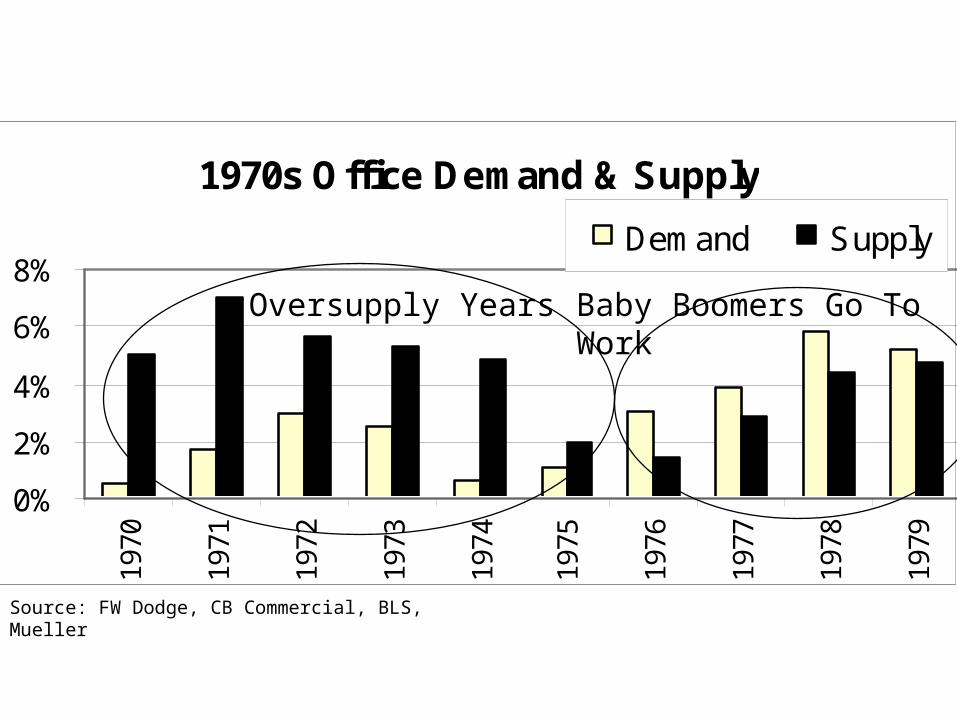

1970s Cycle•Factors Driving The First Half Cycle (5 Year)

•Strong Demand from the 1960s that stopped

•Recession 1974

•Capital Flow Mortgage REITs produces oversupply

•Factors Driving The Second Half Cycle (5 Year)

•Baby Boom Generation Goes to Work

•Capital Flow Shut Down as Lenders Recover

•Markets tighten and reach peak occupancy 1979

1970s Office Demand & Supply

0%

2%

4%

6%

8%

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

Demand Supply

Source: FW Dodge, CB Commercial, BLS, Mueller

Oversupply Years Baby Boomers Go To Work

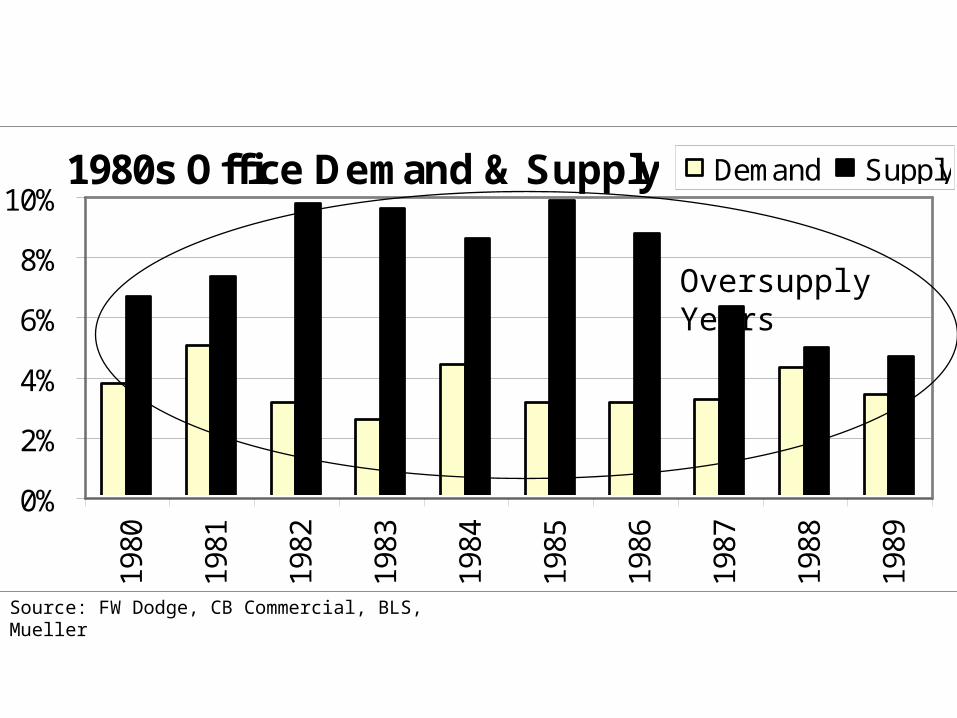

1980s Cycle•Factors Driving The First Half Cycle (5 Year)

•Tight market in 1979 pushes rents and prices up

•Tax Act of 1981 attracts taxable investors supply up

•Factors Driving The Second Half Cycle (5 Year)

•Thrift Deregulation allows capital to flow

•Inflation pushes real estate prices higher

•Tax Act of 1986 slows taxable investors, but not tax free

•Poor stock market attracts Pension & Foreign capital

•Rising R.E. prices masks poor income returns

1980s Office Demand & Supply

0%

2%

4%

6%

8%

10%

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

Demand Supply

Source: FW Dodge, CB Commercial, BLS, Mueller

Oversupply Years

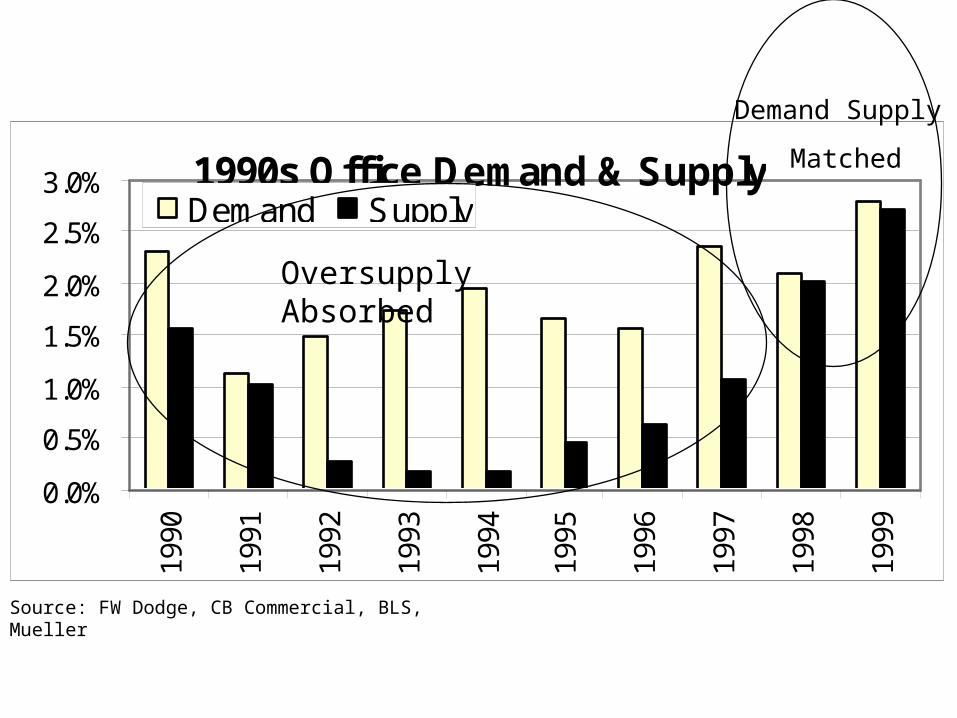

1990s Cycle•Factors Driving The First Half Cycle (5 Year)

•Moderate but stable demand growth (1991 recession minor)

•Oversupply and Foreclosures shut down construction

•Excess space absorbed - bringing markets back

•Factors Driving The Second Half Cycle (5 Year)

•Moderate Demand growth Continues

•Oversupply absorbed and return performance improves

•Construction “constrained” causing rents & prices to rise

•More efficient markets match supply to demand

1990s Office Demand & Supply

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%19

90

1991

1992

1993

1994

1995

1996

1997

1998

1999

Demand Supply

Source: FW Dodge, CB Commercial, BLS, Mueller

Oversupply Absorbed

Demand Supply

Matched

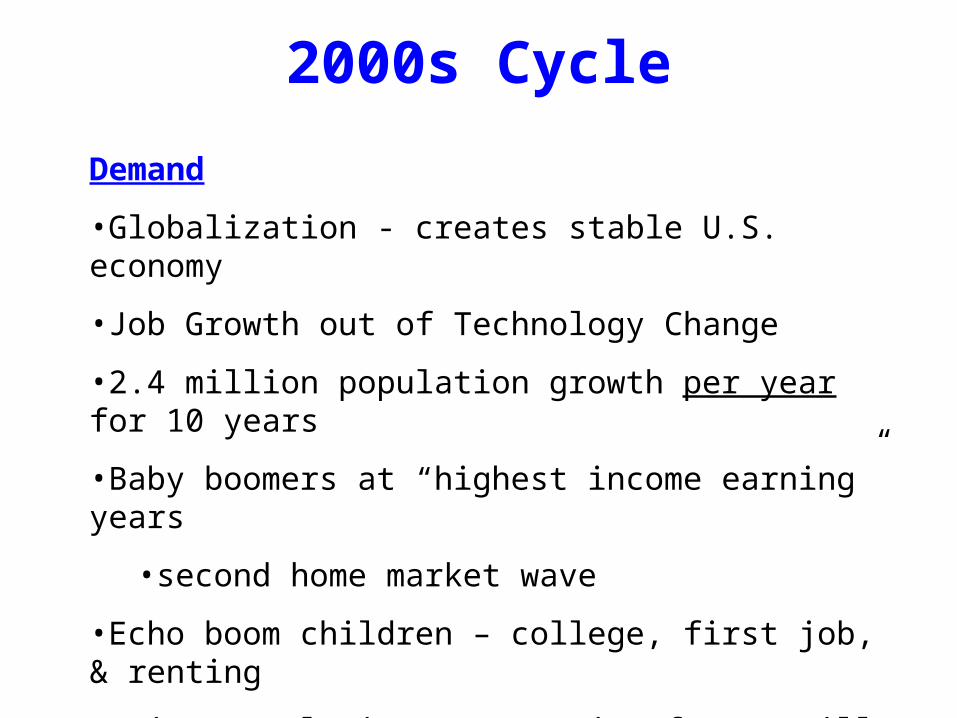

2000s Cycle

Demand

•Globalization - creates stable U.S. economy

•Job Growth out of Technology Change

•2.4 million population growth per year for 10 years

•Baby boomers at “highest income earning” years

•second home market wave

•Echo boom children – college, first job, & renting

•Aging population not a major factor till 2014

•Employment growth - determines demand - WHEN

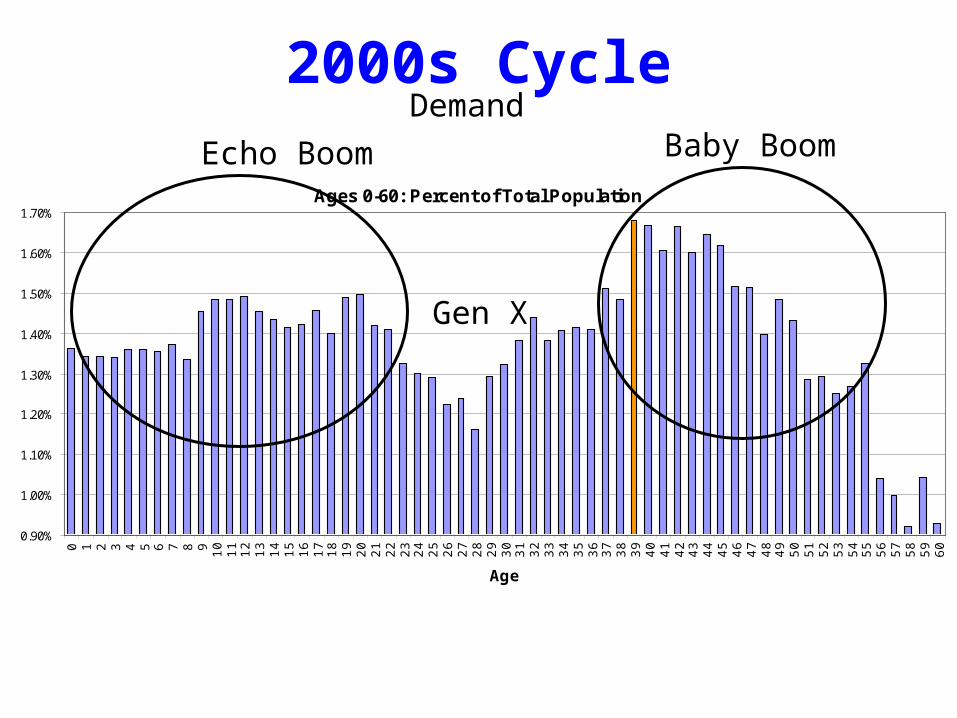

Ages 0-60: Percent of Total Population

0.90%

1.00%

1.10%

1.20%

1.30%

1.40%

1.50%

1.60%

1.70%

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 50 51 52 53 54 55 56 57 58 59 60

Age

Demand2000s Cycle

Baby BoomEcho Boom

Gen X

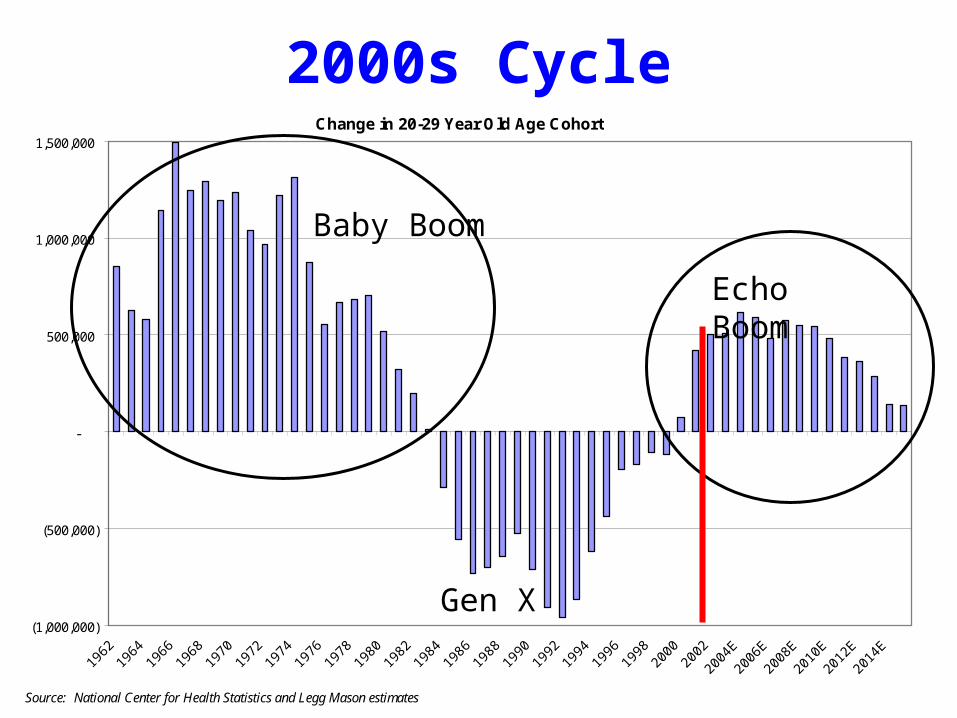

Change in 20-29 Year Old Age Cohort

(1,000,000)

(500,000)

-

500,000

1,000,000

1,500,000

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

E

2006

E

2008

E

2010

E

2012

E

2014

E

Source: National Center for Health Statistics and Legg Mason estimates

2000s Cycle

Baby Boom

Echo Boom

Gen X

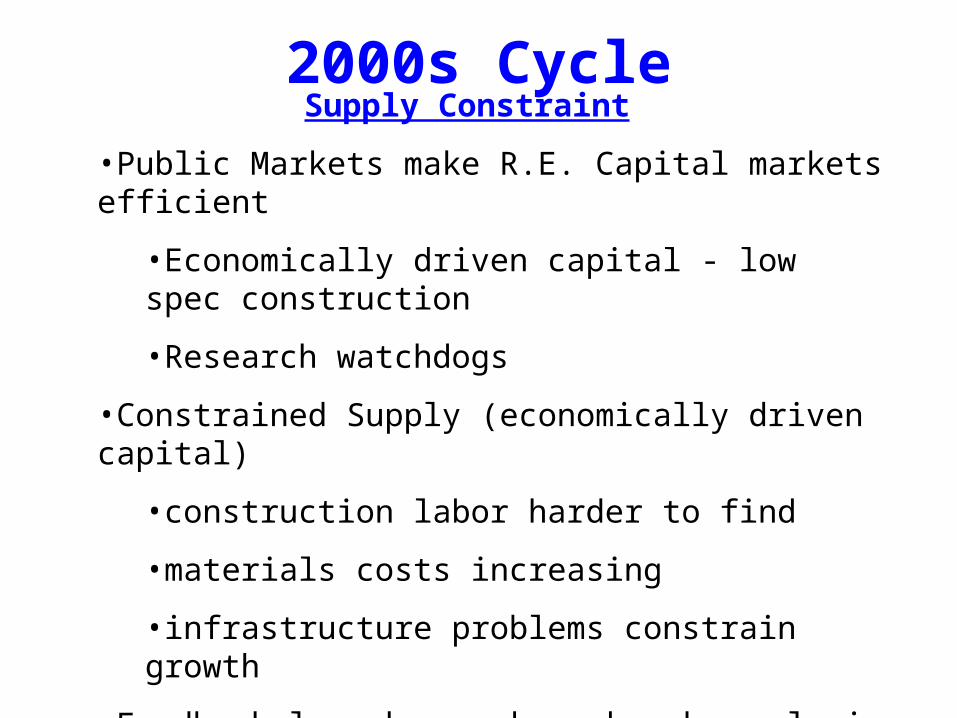

Supply Constraint

•Public Markets make R.E. Capital markets efficient

•Economically driven capital - low spec construction

•Research watchdogs

•Constrained Supply (economically driven capital)

•construction labor harder to find

•materials costs increasing

•infrastructure problems constrain growth

•Feedback loop keeps demand and supply in better balance

•greater transparency

•Faster reaction to demand slowdown

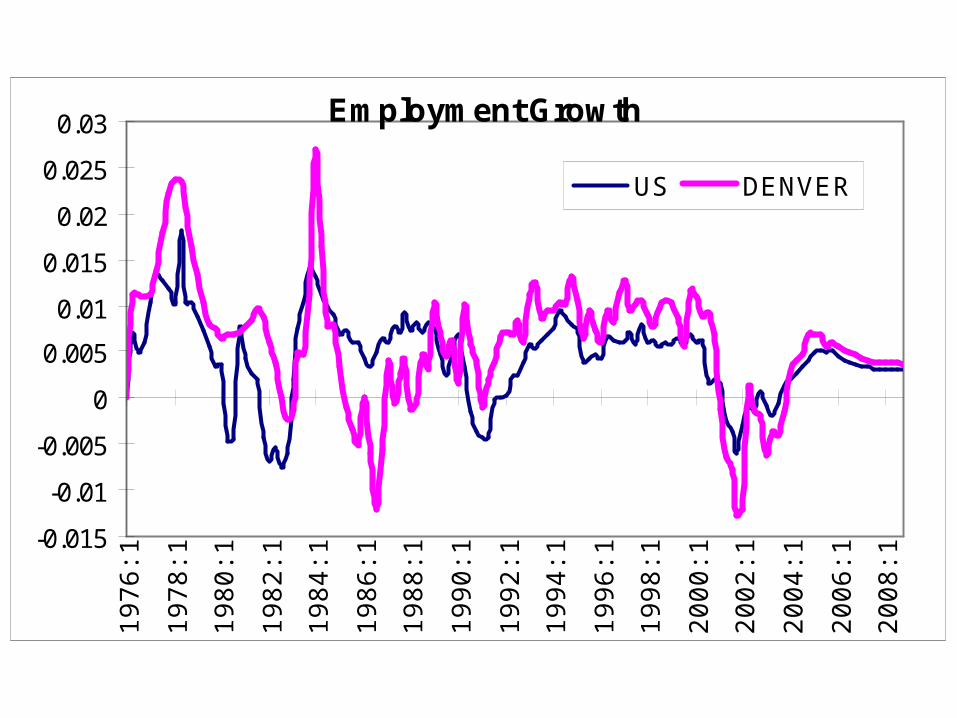

2000s Cycle

Employment Growth

-0.015

-0.01

-0.005

0

0.005

0.01

0.015

0.02

0.025

0.0319

76:1

1978

:1

1980

:1

1982

:1

1984

:1

1986

:1

1988

:1

1990

:1

1992

:1

1994

:1

1996

:1

1998

:1

2000

:1

2002

:1

2004

:1

2006

:1

2008

:1

US DENVER

Source: Mueller, 2004

11

1467

89

10 12

13

115

16432 1

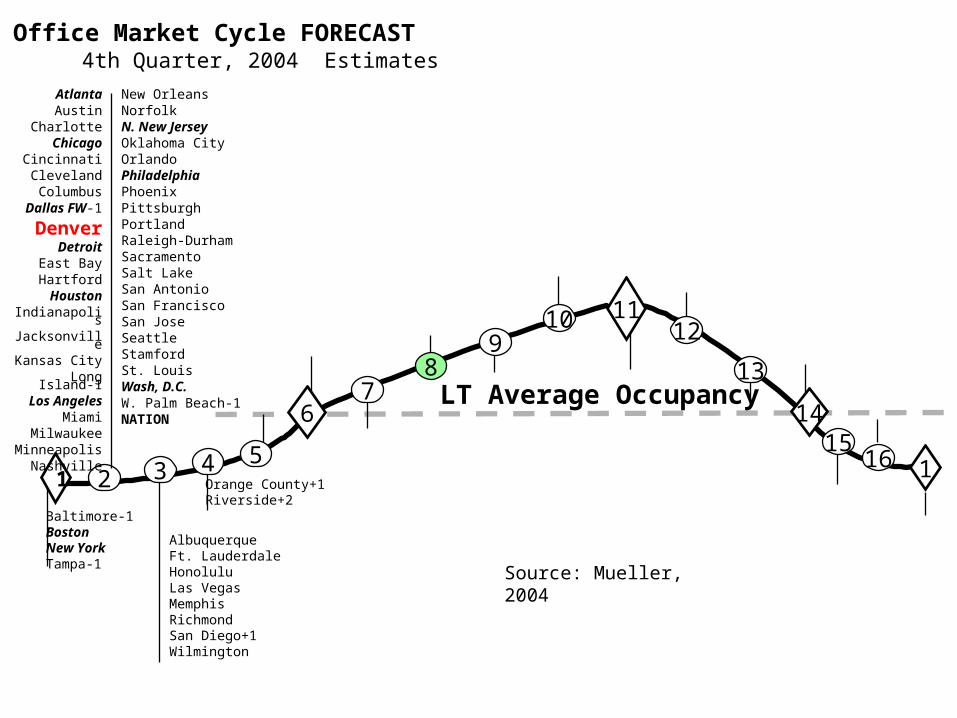

4th Quarter, 2004 Estimates

LT Average Occupancy

Office Market Cycle FORECAST

AlbuquerqueFt. LauderdaleHonoluluLas VegasMemphisRichmondSan Diego+1Wilmington

5

Baltimore-1BostonNew YorkTampa-1

Orange County+1Riverside+2

New OrleansNorfolkN. New JerseyOklahoma CityOrlandoPhiladelphiaPhoenixPittsburghPortlandRaleigh-DurhamSacramentoSalt LakeSan AntonioSan FranciscoSan JoseSeattleStamfordSt. LouisWash, D.C.W. Palm Beach-1NATION

AtlantaAustin

CharlotteChicago

CincinnatiClevelandColumbus

Dallas FW-1

DenverDetroit

East BayHartfordHouston

IndianapolisJacksonvilleKansas City

Long Island-1Los Angeles

MiamiMilwaukee

MinneapolisNashville

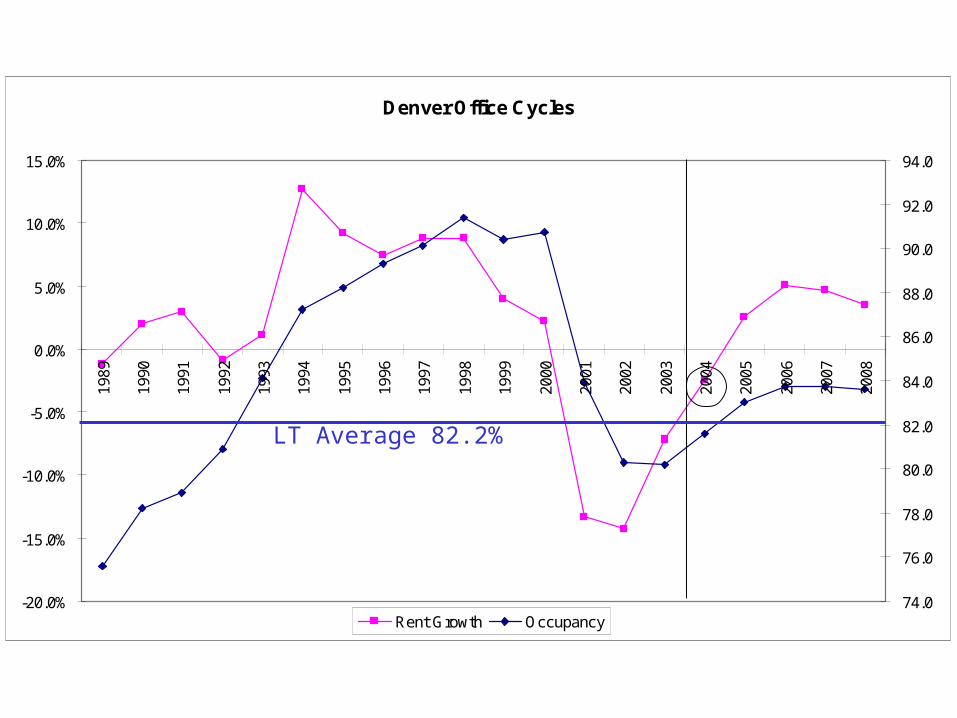

Denver Office Cycles

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

74.0

76.0

78.0

80.0

82.0

84.0

86.0

88.0

90.0

92.0

94.0

Rent Growth Occupancy

LT Average 82.2%

Source: Mueller, 2004

11

1467

89

10 12

13

115

1653 1

4th Quarter, 2004 Estimates

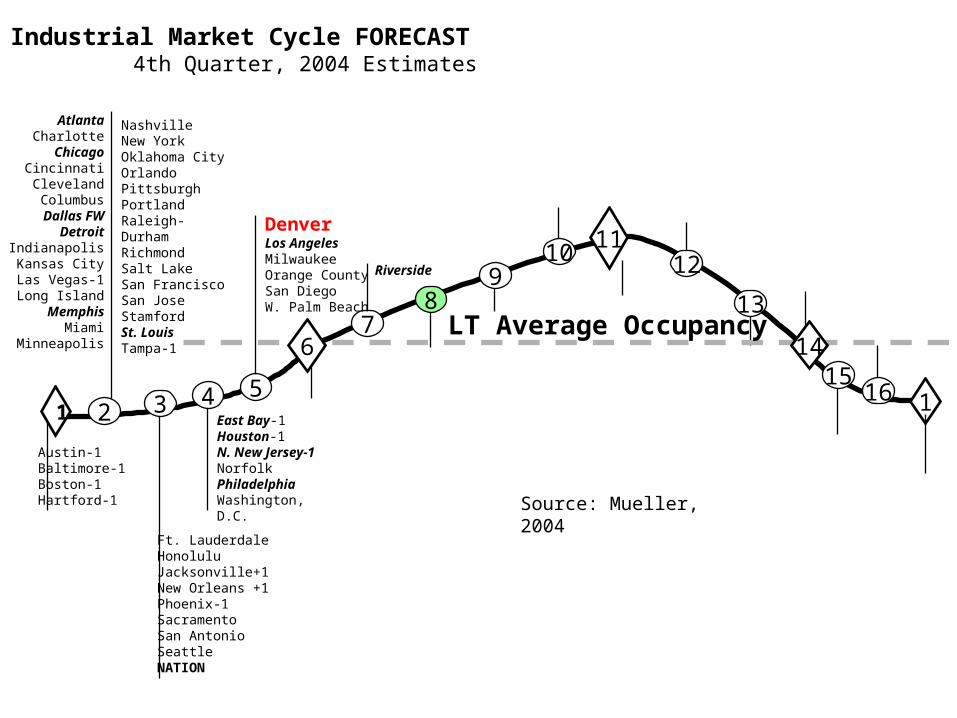

DenverLos AngelesMilwaukeeOrange CountySan DiegoW. Palm Beach

LT Average Occupancy

Industrial Market Cycle FORECAST

Riverside

4

AtlantaCharlotteChicago

CincinnatiClevelandColumbus

Dallas FWDetroit

IndianapolisKansas CityLas Vegas-1Long Island

MemphisMiami

Minneapolis

2

Ft. LauderdaleHonoluluJacksonville+1New Orleans +1Phoenix-1SacramentoSan AntonioSeattleNATION

Nashville New YorkOklahoma CityOrlandoPittsburghPortlandRaleigh-Durham RichmondSalt LakeSan FranciscoSan JoseStamfordSt. LouisTampa-1

East Bay-1Houston-1N. New Jersey-1NorfolkPhiladelphiaWashington, D.C.

Austin-1Baltimore-1Boston-1Hartford-1

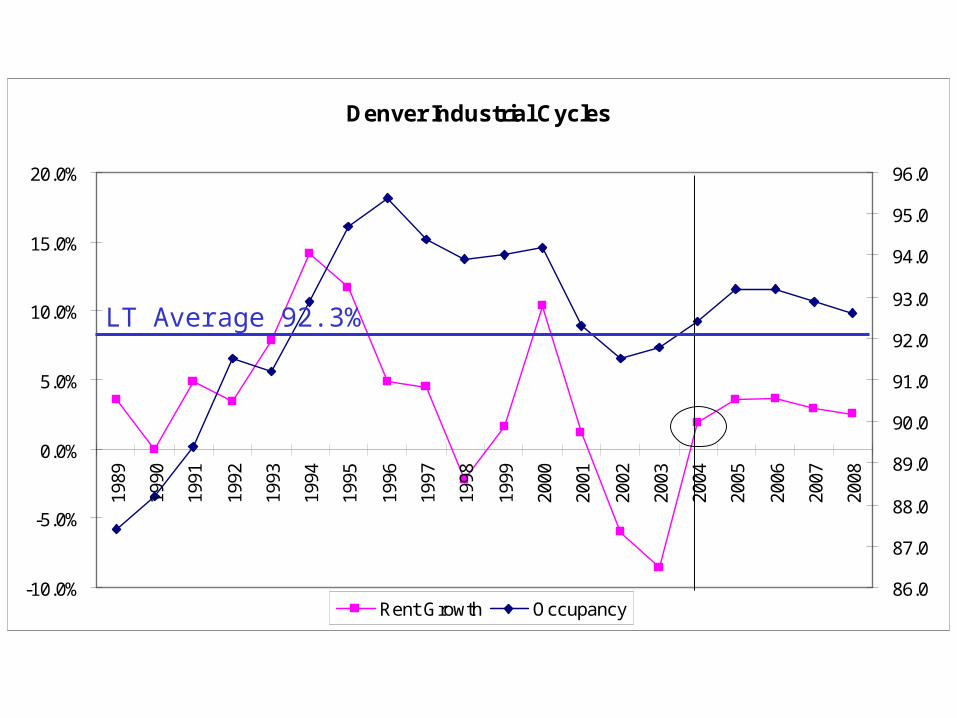

Denver Industrial Cycles

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

86.0

87.0

88.0

89.0

90.0

91.0

92.0

93.0

94.0

95.0

96.0

Rent Growth Occupancy

LT Average 92.3%

Source: Mueller, 2004

11

1467

89

10 12

13

115

16432 1

4th Quarter, 2004 Estimates

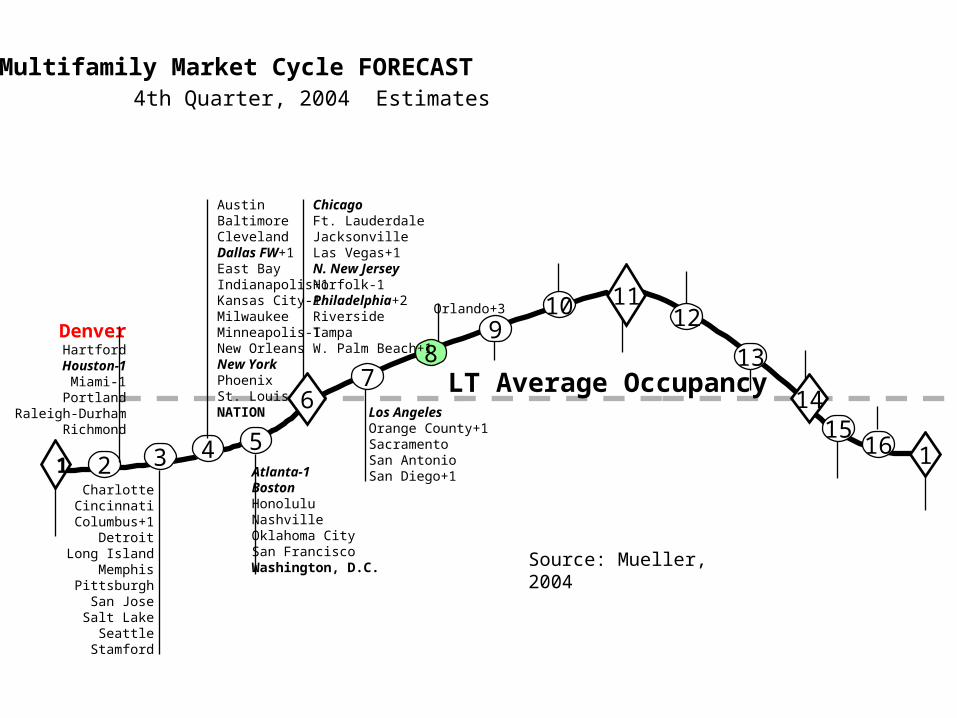

Los AngelesOrange County+1SacramentoSan AntonioSan Diego+1

LT Average Occupancy

Multifamily Market Cycle FORECAST

CharlotteCincinnati

Columbus+1Detroit

Long IslandMemphis

PittsburghSan Jose

Salt LakeSeattle

Stamford

Atlanta-1BostonHonoluluNashvilleOklahoma CitySan FranciscoWashington, D.C.

ChicagoFt. LauderdaleJacksonvilleLas Vegas+1N. New JerseyNorfolk-1Philadelphia+2RiversideTampaW. Palm Beach+1

AustinBaltimoreClevelandDallas FW+1East BayIndianapolis+1Kansas City-1MilwaukeeMinneapolis-1New OrleansNew YorkPhoenixSt. LouisNATION

DenverHartford

Houston-1Miami-1Portland

Raleigh-DurhamRichmond

5

Orlando+3

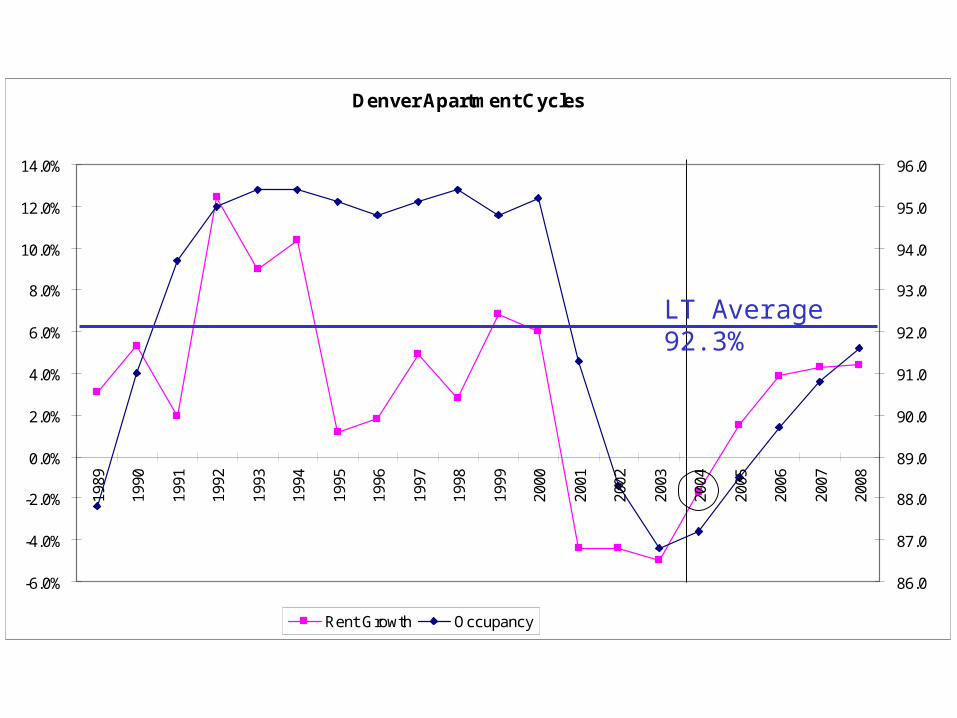

Denver Apartment Cycles

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

86.0

87.0

88.0

89.0

90.0

91.0

92.0

93.0

94.0

95.0

96.0

Rent Growth Occupancy

LT Average 92.3%

Source: Mueller, 2004

11

147

89

10 12

13

115

165432 1

4th Quarter, 2004 Estimates

Boston-1HonoluluHouston-1IndianapolisLong IslandLos AngelesNew OrleansRiversideSan Antonio-2StamfordSt. LouisW. Palm Beach+1

LT Average Occupancy

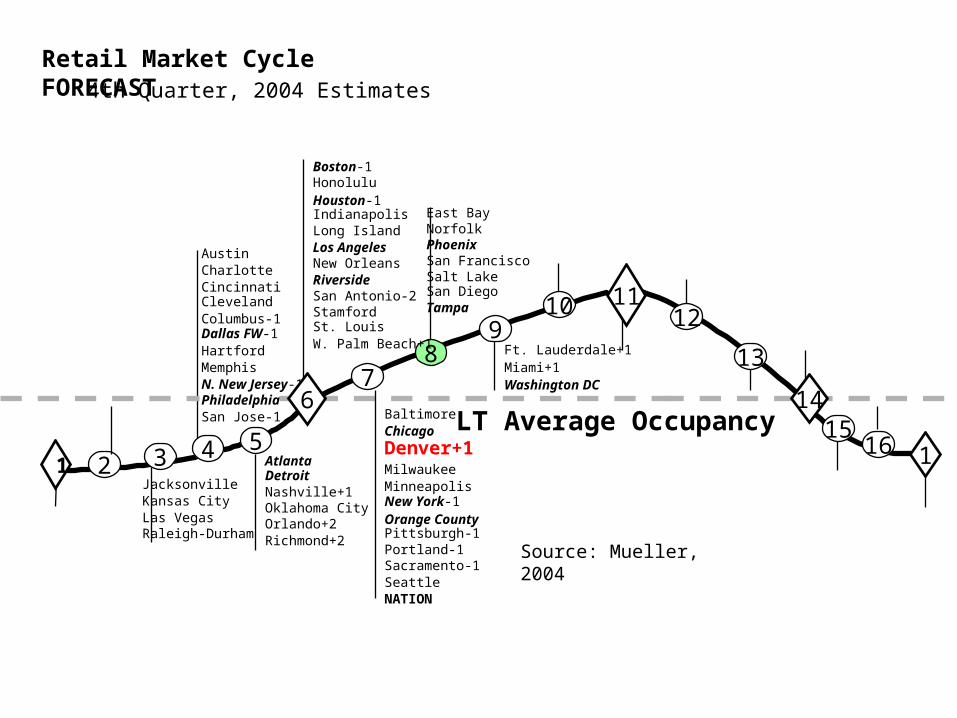

Retail Market Cycle FORECAST

AustinCharlotteCincinnatiClevelandColumbus-1Dallas FW-1HartfordMemphisN. New Jersey-1PhiladelphiaSan Jose-1

AtlantaDetroitNashville+1Oklahoma City Orlando+2Richmond+2

East BayNorfolkPhoenixSan FranciscoSalt LakeSan DiegoTampa

JacksonvilleKansas CityLas VegasRaleigh-Durham

6

Ft. Lauderdale+1Miami+1Washington DC

BaltimoreChicago

Denver+1MilwaukeeMinneapolisNew York-1Orange CountyPittsburgh-1Portland-1Sacramento-1SeattleNATION

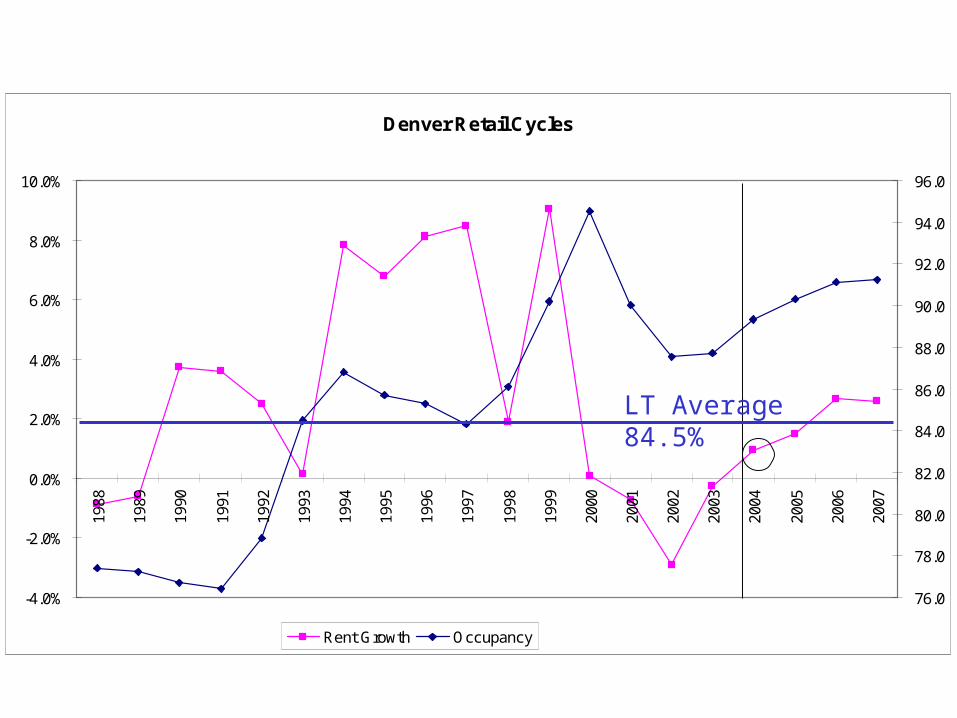

Denver Retail Cycles

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

76.0

78.0

80.0

82.0

84.0

86.0

88.0

90.0

92.0

94.0

96.0

Rent Growth Occupancy

LT Average 84.5%

Source: Mueller, 2004

11

1467

89

10 12

13

115

165432 1

4th Quarter, 2004 Estimates

LT Average Occupancy

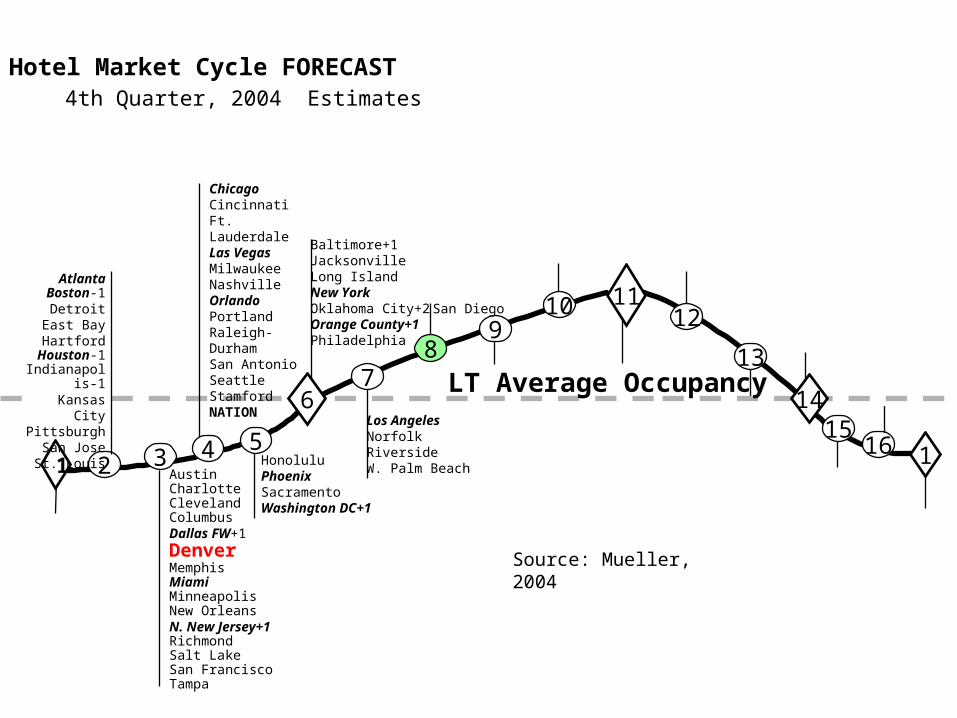

Hotel Market Cycle FORECAST

AustinCharlotteClevelandColumbusDallas FW+1

DenverMemphisMiamiMinneapolisNew OrleansN. New Jersey+1Richmond Salt LakeSan FranciscoTampa

ChicagoCincinnatiFt. LauderdaleLas VegasMilwaukeeNashvilleOrlandoPortlandRaleigh-DurhamSan AntonioSeattleStamfordNATION

HonoluluPhoenixSacramentoWashington DC+1

Baltimore+1JacksonvilleLong IslandNew YorkOklahoma City+2Orange County+1Philadelphia

AtlantaBoston-1

DetroitEast BayHartford

Houston-1Indianapolis-1

Kansas CityPittsburgh

San JoseSt. Louis

Los AngelesNorfolkRiversideW. Palm Beach

San Diego

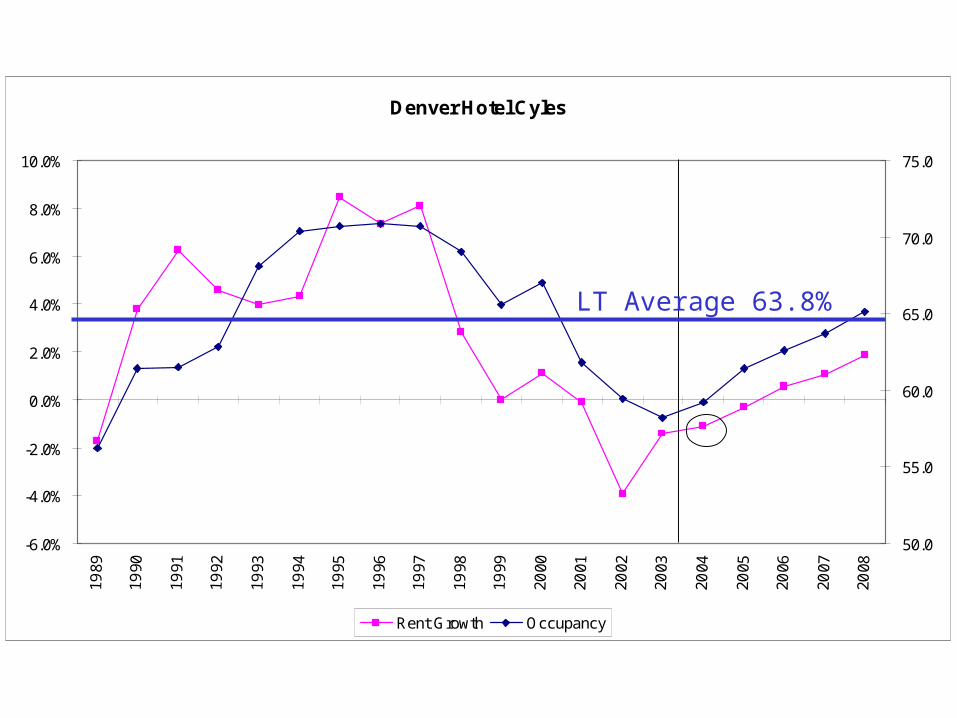

Denver Hotel Cyles

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

50.0

55.0

60.0

65.0

70.0

75.0

Rent Growth Occupancy

LT Average 63.8%

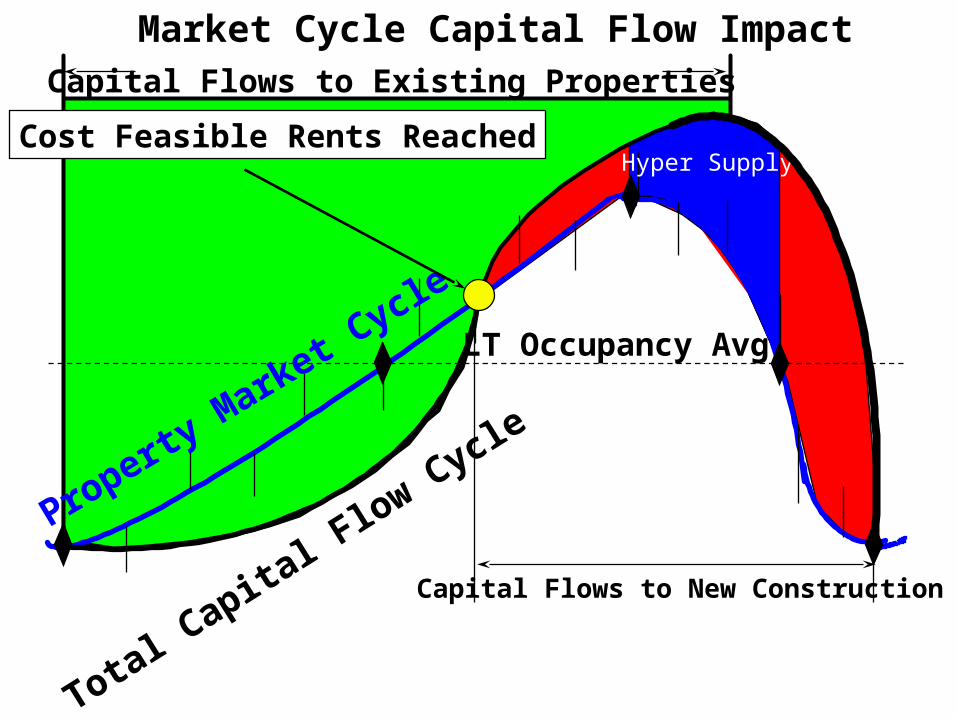

Real Estate Financial Cycles

Capital Flows

Affect Prices

Hyper Supply

LT Occupancy Avg.

Market Cycle Capital Flow Impact

Capital Flows to Existing Properties

Capital Flows to New Construction

Total Capita

l Flow CycleProperty M

arket Cycle

Cost Feasible Rents Reached

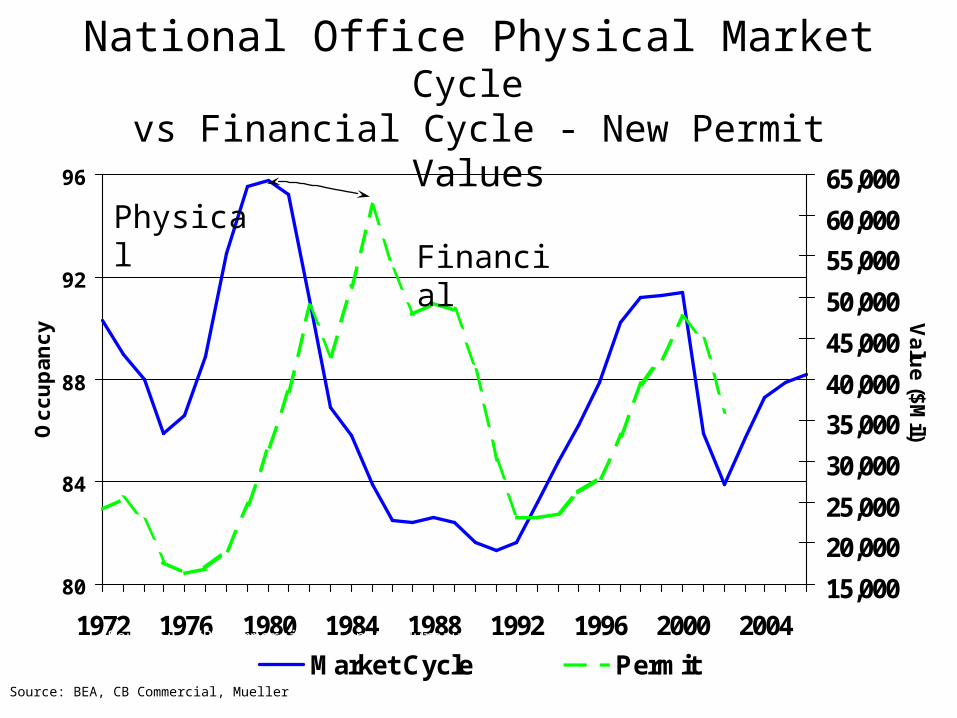

National Office Physical Market Cycle vs Financial Cycle - New Permit Values

80

84

88

92

96

1972 1976 1980 1984 1988 1992 1996 2000 2004

Oc

cu

pa

nc

y

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

60,000

65,000

Va

lue

($M

il)

Market Cycle PermitSource: CB Commercial, Census Bureau

PhysicalFinancial

Source: BEA, CB Commercial, Mueller

-10,000

-5,000

0

5,000

10,000

15,000

20,000

25,000

1970

Q1

1972

Q1

1974

Q1

1976

Q1

1978

Q1

1980

Q1

1982

Q1

1984

Q1

1986

Q1

1988

Q1

1990

Q1

1992

Q1

1994

Q1

1996

Q1

1998

Q1

2000

Q1

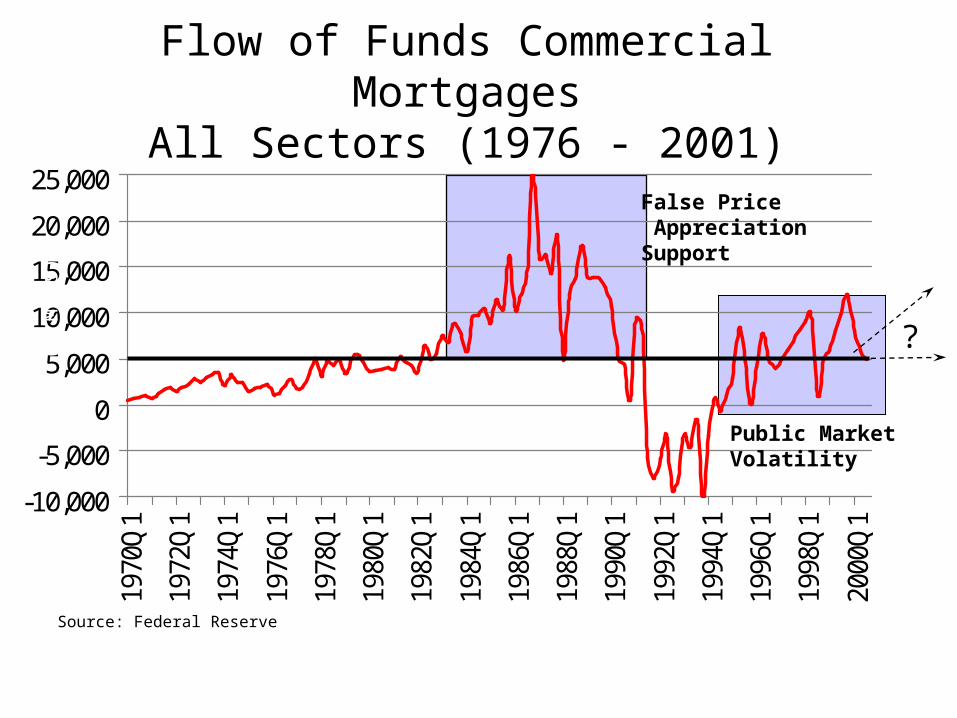

Flow of Funds Commercial MortgagesAll Sectors (1976 - 2001)

False Price AppreciationSupport

?($ M

ils)

Source: Federal Reserve

Public MarketVolatility

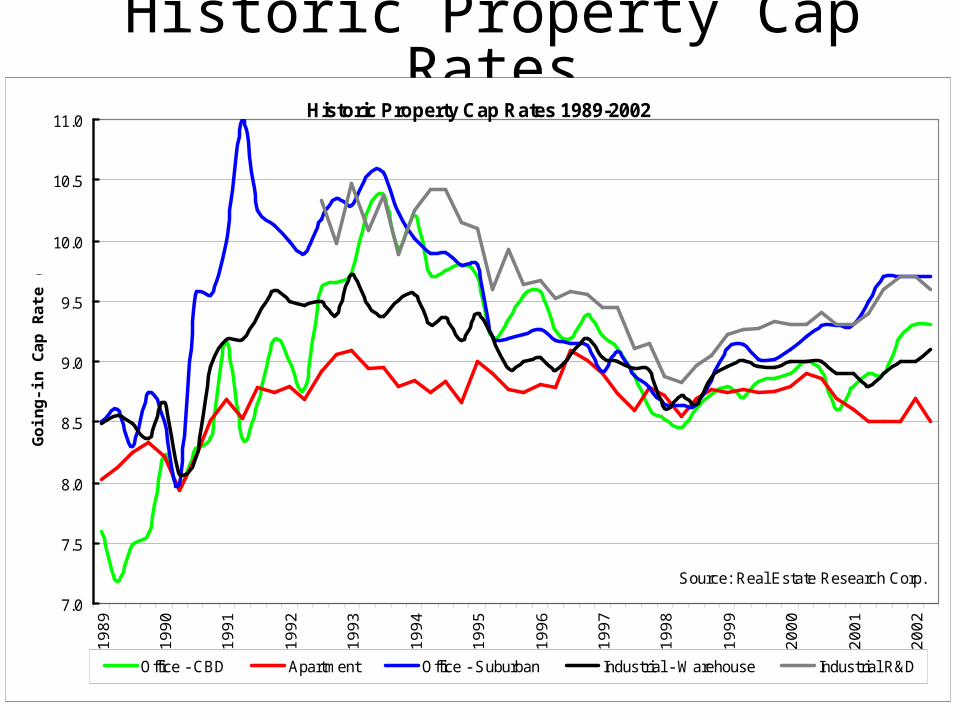

Historic Property Cap RatesHistoric Property Cap Rates 1989-2002

7.0

7.5

8.0

8.5

9.0

9.5

10.0

10.5

11.019

89

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

Go

ing

-in

Cap

Rat

e (%

)

Office - CBD Apartment Office - Suburban Industrial - Warehouse Industrial R&D

Source: Real Estate Research Corp.

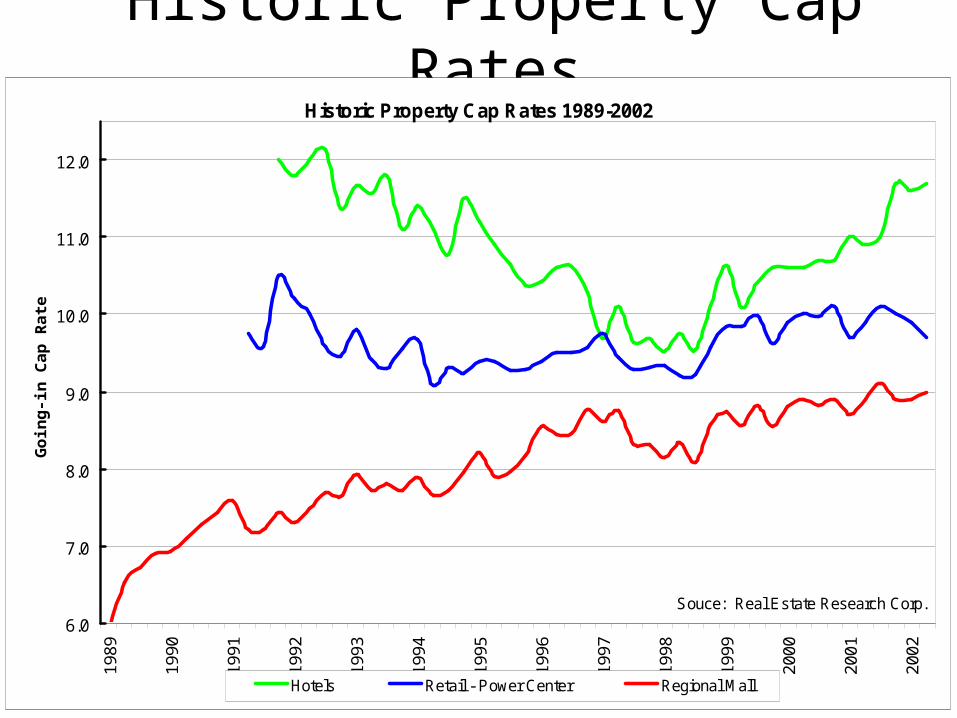

Historic Property Cap RatesHistoric Property Cap Rates 1989-2002

6.0

7.0

8.0

9.0

10.0

11.0

12.0

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

Go

ing

-in

Cap

Rat

e (%

)

Hotels Retail - Power Center Regional Mall

Souce: Real Estate Research Corp.

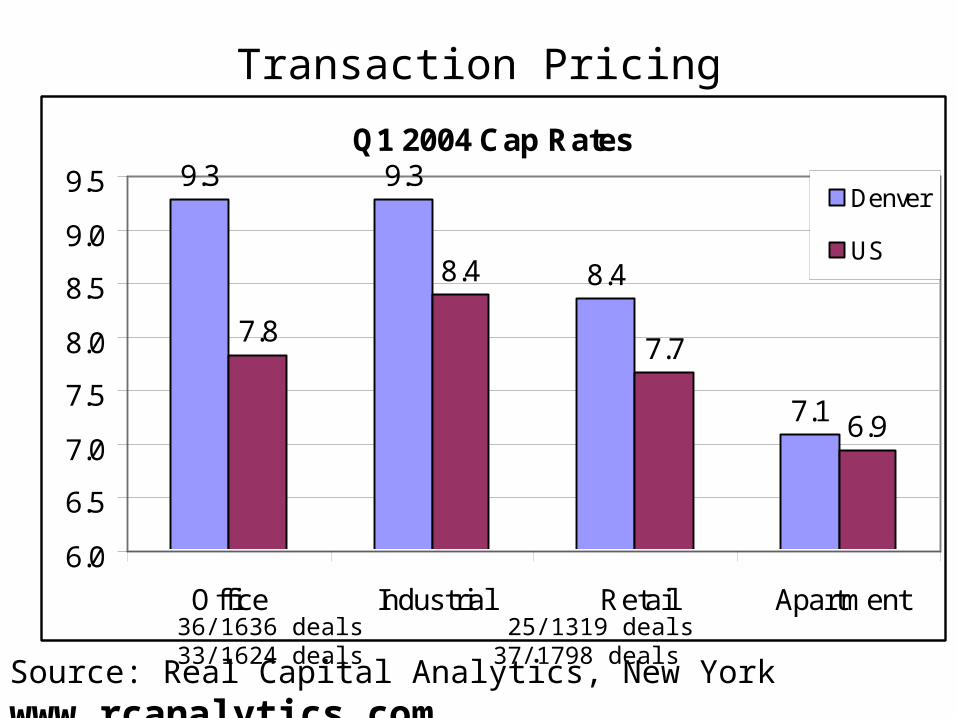

Transaction Pricing

Source: Real Capital Analytics, New York www.rcanalytics.com

Q1 2004 Cap Rates9.3 9.3

8.4

7.1

7.8

8.4

7.7

6.9

6.0

6.5

7.0

7.5

8.0

8.5

9.0

9.5

Office Industrial Retail Apartment

Denver

US

36/1636 deals 25/1319 deals 33/1624 deals 37/1798 deals

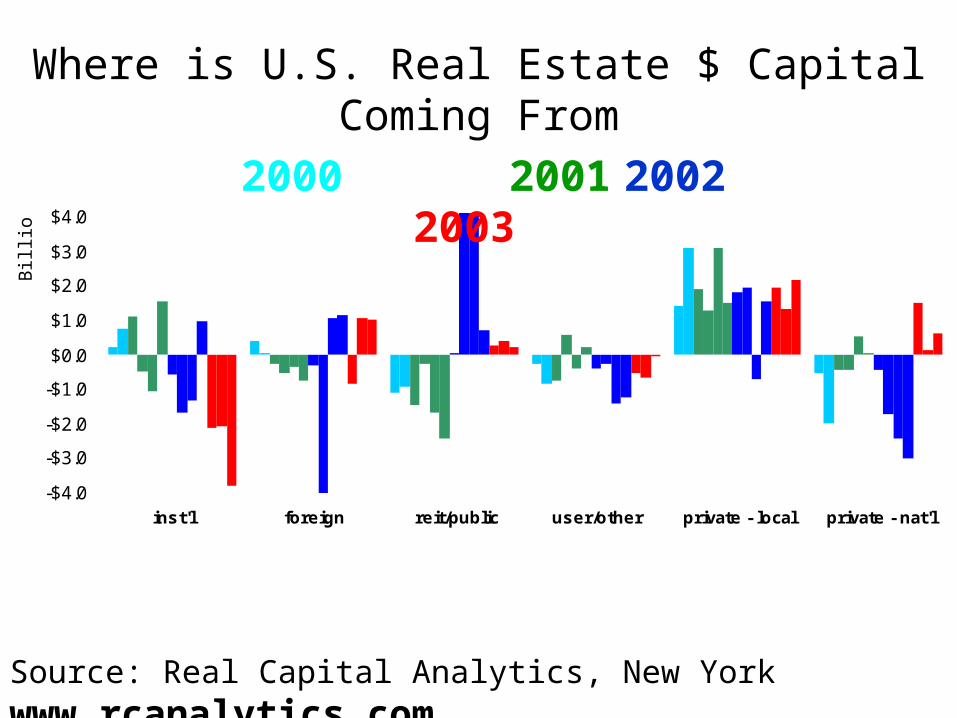

Where is U.S. Real Estate $ Capital Coming From

-$4.0

-$3.0

-$2.0

-$1.0

$0.0

$1.0

$2.0

$3.0

$4.0

inst'l foreign reit/public user/other private - local private - nat'l

Bill

ion

s

2000 2001 2002 2003

Source: Real Capital Analytics, New York www.rcanalytics.com

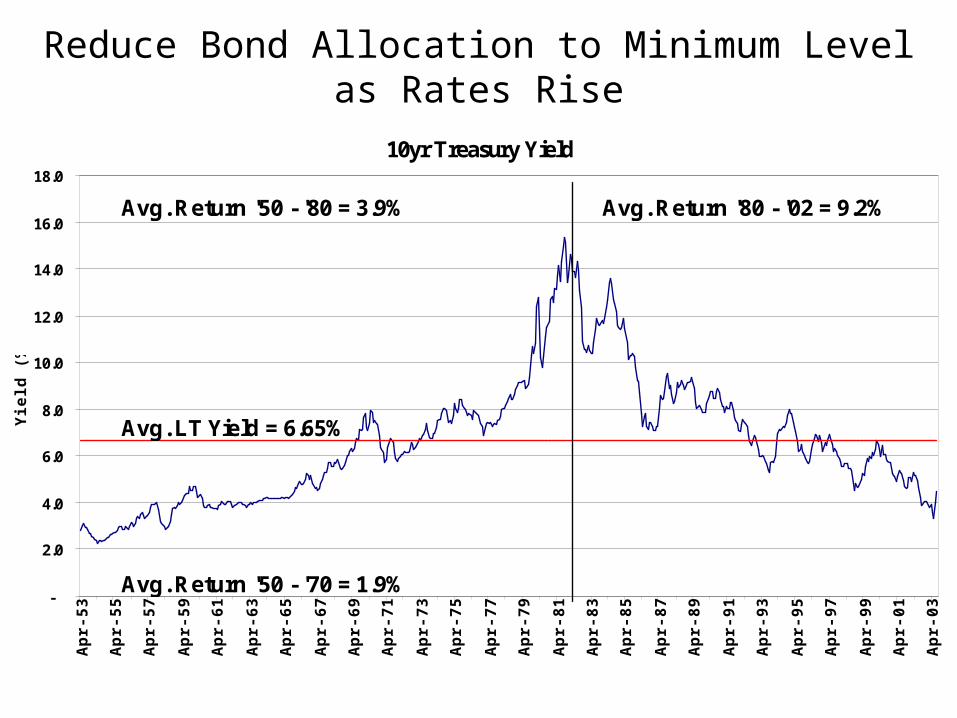

Reduce Bond Allocation to Minimum Level as Rates Rise

10yr Treasury Yield

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

Apr

-53

Apr

-55

Apr

-57

Apr

-59

Apr

-61

Apr

-63

Apr

-65

Apr

-67

Apr

-69

Apr

-71

Apr

-73

Apr

-75

Apr

-77

Apr

-79

Apr

-81

Apr

-83

Apr

-85

Apr

-87

Apr

-89

Apr

-91

Apr

-93

Apr

-95

Apr

-97

Apr

-99

Apr

-01

Apr

-03

Yie

ld (

%)

Avg. LT Yield = 6.65%

Avg. Return '50 - '70 = 1.9%

Avg. Return '80 - '02 = 9.2%Avg. Return '50 - '80 = 3.9%

2003 Physical CycleDemand & Supply Affect Vacancies Rental Growth

Demand Growth - MUCH SLOWER for How long?

Supply Slowing - how long to absorb?

Return to Growth Phase in 2006?

Wars stop progress - Create Economic Recovery after ?

2003 Financial CycleCapital Flows Affect Prices – Stock Market Fear

Real Estate the SAFEST Investment Alternative?

Interest Rates are driving investments in the short run

R E Equity – dominated by private markets (currently international)

Public Market Debt – Biggest RE Capital Source

Confidence will return in 200?