gjensidige bank presentation april 2008

TRANSCRIPT

Gjensidige Bank ASA

Presentation

Bergen, 23. April 2008

Oslo, 24 April 2008

24.04.2008 Gjensidige Bank2

Presentation team

Experience: Gjensidige Forsikring

SkandiaBanken AB, NUF

SkandiaBanken Bilfinans AS

SkandiaBanken Merkefinans AS

Vesta Forsikring/Vesta Finans

Education: Norwegian School of Management (BI)Bachelor of management, Masterprogram StrategicManagement, Project leadership

Experience: Gjensidige Forsikring SKIPPER Electronics ASSamarbeidende Revisorer ASKPMG ASGjensidige NOR Forsikring

Education: Norwegian School of ManagementNorwegian School of Economics

Tor Magne LønnumChairman of the Board

Jan Kaare Hellevang

CEO

Frank-Rune Ås

Sparebanken

Sogn og Fjordane

CFO

Experience: Lorenzen Lysaker Group

Norw. State’s Institute ofTechnology

Diary of Sogn og Fjordane

Sparebanken Sogn og Fjordane

Education: Norwegian School of Management(BI), siv. øk.

Norwegian School of Management, Masterprogram Investment and Finance

24.04.2008 Gjensidige Bank3

I. Gjensidige Forsikring - in brief

III. Cooperation with SSF

IV. Performance – key figures

V. Goals and outlook

II. Strategy and concept

Agenda

VI. Q&A

24.04.2008 Gjensidige Bank4

Norway International

General Insurance

Gross Written Premium (“GWP”) of NOK 12,987 mill (NOK 13,375 mill incl. Norwegian municipal portfolio) (85.3 per cent of Group) in 2007Staff of 2,033 (31 December 2007)Market shares (Q4 2007)1):

• Total 31.0%

• Private 30.4%

• Of which Agriculture 74.1%

• Commercial 32.7%

• Group Life (2006) 33.7%

• Marine (2006) 22.4%

Customers (Q4 2007)

• Total number of customers 1,051,000

• 956,000 customers in private and agricultural markets

• 70% of private/agricultural customers are members of loyalty or affinity programs, generating 88% of written premium

• 8% churn rate 2) for loyalty/ affinity customers (13% for all customers, 24% in the mass market)

International operations include:

• Tennant (Norway and Sweden)

• Fair and KommuneForsikring (Denmark)

• Gjensidige Baltic (formerly Parekss) and its agents (the Baltics)

GWP of NOK 2,243 mill (14.7%) in 2007Staff of 640 (31 December 2007)

Other Business Units

• Other operations include Gjensidige Pension and Savings, Gjensidige Bank and Help24 that operate in Norway

• Staff of around 787 (31 December 2007)

Gjensidige ForsikringIn brief

1) The Norwegian Financial Services Association (“FNH”), general insurance per 31-Dec-2007. Segments are based on company definitions, but drawn directly from FNH report. Marine numbers are from CFOR

2) Monthly churn rate consists of persons who were customers previous month, but with no insurance policy next month, divided on total amount of customers previous month. Yearly churn rate is computed by adding up the last twelve monthly churn rates. This definition applies throughout this presentation

24.04.2008 Gjensidige Bank5

Gjensidige ForsikringLeading position – strong brand

30,4 %28,3 %

18,1 %

12,7 %

Gjensidige If Vesta Sparebank1

74,1 %

16,5 %

7,3 %

Gjensidige If Terra

32,7 % 33,3 %

18,2 %

4,4 %

Gjensidige If Vesta Sparebank1

Market Share – Private Market Share – Commercial

Norwegian Market Share Development since 2002

Source: FNH, general insurance. The definition of Private and Commercial is adjusted to reflect Gjensidige’s business model

Of which: Agriculture

15 %

20 %

25 %

30 %

35 %

2002 2003 2004 2005 2006 2007

Gjensidige If Vesta Sparebank1

15 %

20 %

25 %

30 %

35 %

2002 2003 2004 2005 2006 2007

Gjensidige If Vesta Sparebank1

Market Share – Private Market Share – Commercial

24.04.2008 Gjensidige Bank6

NOK mill

Gross written premium

Claims ratio gen. ins.

Cost ratio gen. ins.

UW result gen. insurance

Net financial income

Profit after tax

Rating (S&P)

20062007

13,78715,727

75.9%78.6%

18.9%17.5%

669553

3,7112,820

4,0922,479

Gjensidige ForsikringStrong financial position

20,30319,017

2007 2006

Equity (NOK mill)

Pre-tax Return on Equity (%)

15.4

24.2

2007 2006

Single A Single A

24.04.2008 Gjensidige Bank7

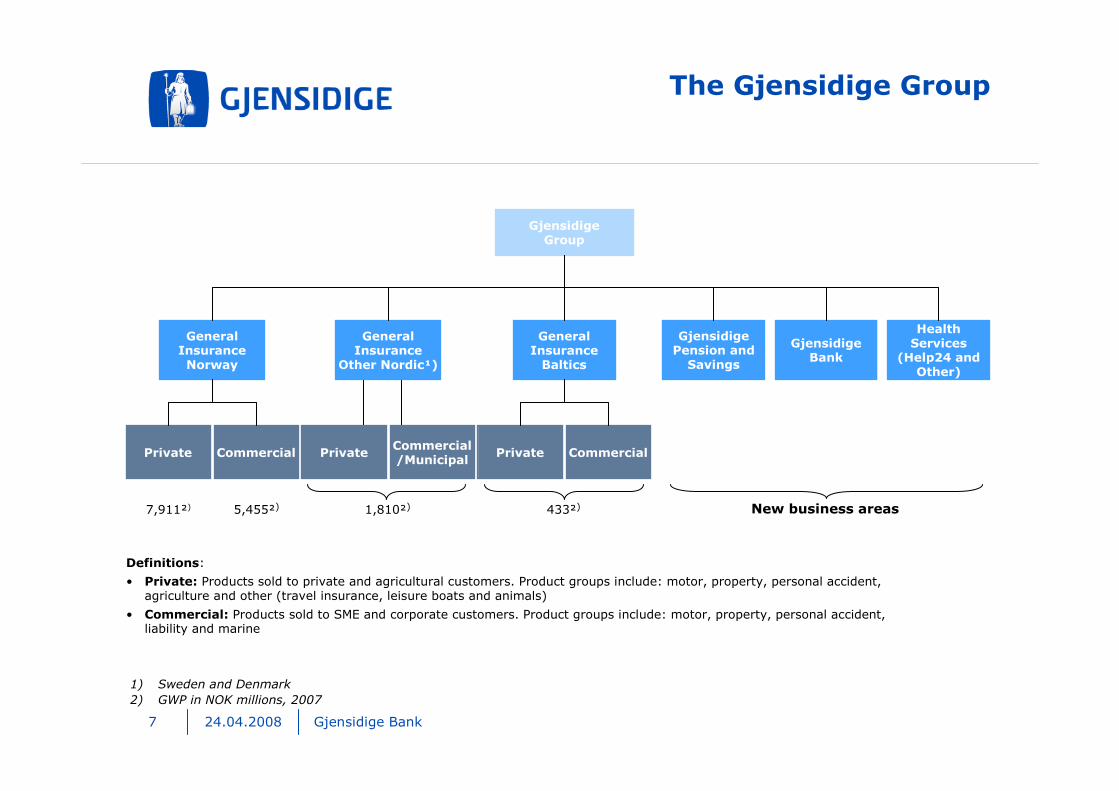

Gjensidige Group

General InsuranceNorway

Gjensidige Pension and

Savings

Gjensidige Bank

General Insurance Baltics

Health Services

(Help24 and Other)

Private Commercial Private Commercial

General Insurance

Other Nordic¹)

PrivateCommercial/Municipal

7,911²) 5,455²) 1,810²) 433²) New business areas

The Gjensidige Group

Definitions:

• Private: Products sold to private and agricultural customers. Product groups include: motor, property, personal accident, agriculture and other (travel insurance, leisure boats and animals)

• Commercial: Products sold to SME and corporate customers. Product groups include: motor, property, personal accident, liability and marine

1) Sweden and Denmark

2) GWP in NOK millions, 2007

24.04.2008 Gjensidige Bank8

Parekss(Baltics)

Gjensidige in Denmark

Help24Gjensidige Pension

and Savings

Gjensidige Bank

Geographical expansion

Broadened product range

NorwegianGeneral

September 2004 January 2006 January 2007

September 2006

March 2006—acquisition of Fair

January 2007—acquisition of KommuneForsikring

Tennant(Sweden)

August 2007

RESO(Baltics) Regulatory approval pending

Gjensidige ForsikringExpansion Strategy

Rationale:

• Broaden product offering to leverage brand and customer base

• Grow and diversify the Group through Nordic/Baltic platform

24.04.2008 Gjensidige Bank9

Gjensidige ForsikringBroadened product range - banking

Strategic Rationale

• Represents the entry to the retail banking sector

• Allows Gjensidige to:

– Offer a new range of products and services to existing clients

– Protect general insurance market share against bancassurers entering the general insurance market space

• Provides opportunity to gain new customers to broaden the group’s overall customer base

• Gjensidige Bank aims to be profitable without any financial support from the Group

24.04.2008 Gjensidige Bank10

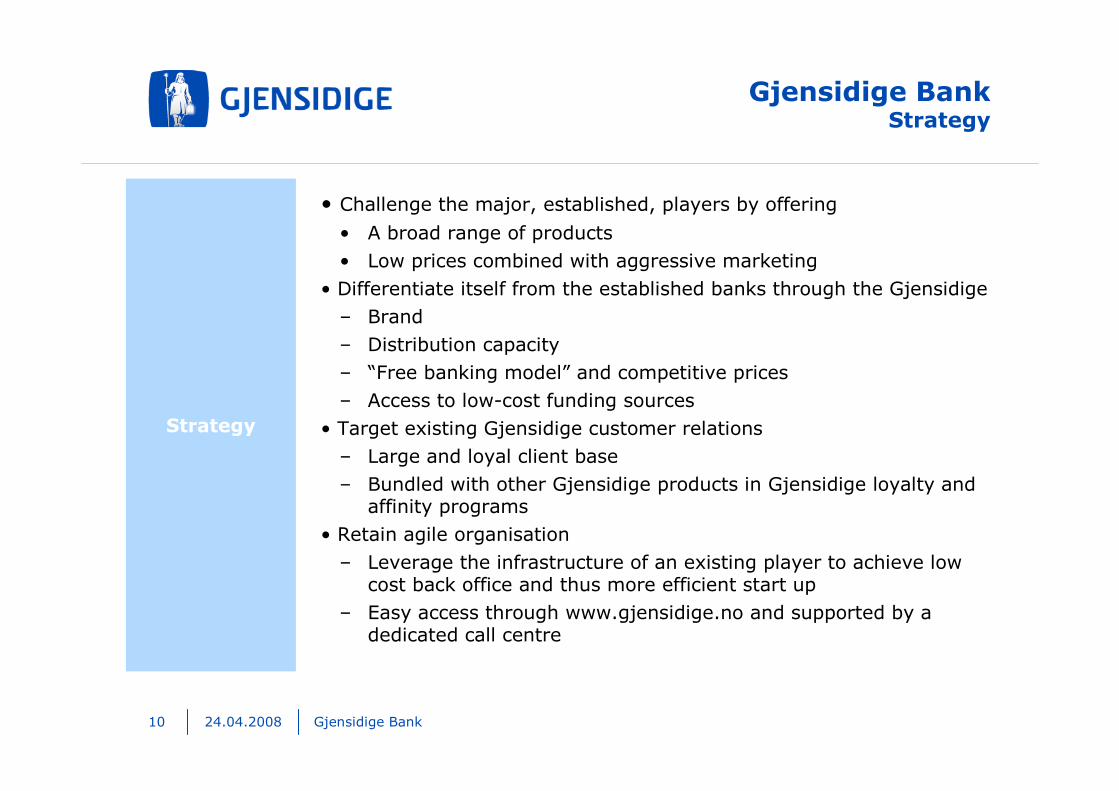

• Challenge the major, established, players by offering

• A broad range of products

• Low prices combined with aggressive marketing

• Differentiate itself from the established banks through the Gjensidige

– Brand

– Distribution capacity

– “Free banking model” and competitive prices

– Access to low-cost funding sources

• Target existing Gjensidige customer relations

– Large and loyal client base

– Bundled with other Gjensidige products in Gjensidige loyalty andaffinity programs

• Retain agile organisation

– Leverage the infrastructure of an existing player to achieve lowcost back office and thus more efficient start up

– Easy access through www.gjensidige.no and supported by a dedicated call centre

Gjensidige BankStrategy

Strategy

24.04.2008 Gjensidige Bank11

Gjensidige establishes internet bank for the retail market

• Customers meet Gjensidige Bank in the "Gjensidige Portal" www.gjensidige.no

• Internet bank with phone support from support centre in Førde

• Self-service concept with attractive terms

• Easy to use web pages which give a good customer experience

• A cost effective, modern and agile internet bank with full productspectrum

• Differentiated from other ”traditional” banks and internet banks primarily through connection with:

– Brand

– Customer base

– Distribution

• Established in co-operation with Sparebanken Sogn og Fjordane

Gjensidige BankConcept

24.04.2008 Gjensidige Bank12

Gjensidige Bank

2 jan 11 jan 12 jan 31jan 1 feb 6 feb 20 feb 15 may- 8 jun 15jul-15aug 29oct 1dec 15 dec 1 jan

Nationwidelaunch

4,000 customers

Launch for YS

Launch for other

employeesin

Gjensidige

Launch for the bank employeesand for Tekna

3,000 customers

1,000 customers

2,000 customers

2007

9,000 customers

13,000 customers

Awareness 10% Awareness 12.6% Awareness 14.6%

Launch ofadvantageprogram

18,000 customers

Autumncampaign

Launch for NITO

20,000 customers

Launch of sales through Gjensidige

branches

22,000 customers

Summercampaign

24.04.2008 Gjensidige Bank13

GjensidigeBank Holding AS

Gjensidige Bank ASA

Board

Management

Board

Management

Synergies

Mutual staff resourcesMutual research and

developmentMore power innegotiations

Gjensidige BankCooperation with SSF

Main deliveriesAccounts/bookkeeping Human Resources

Finance Foreign exchange

Legal Debt collection

Deposit department IT - Support

Property administration

24.04.2008 Gjensidige Bank14

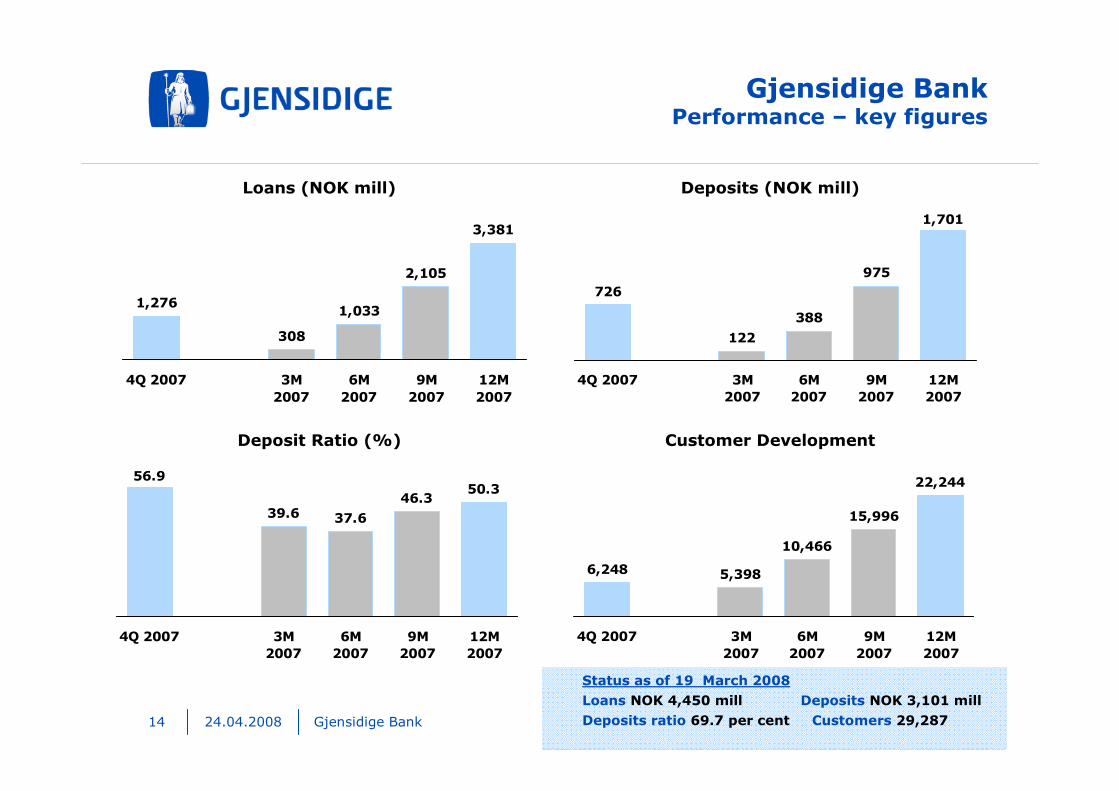

308

3,381

1,276

2,105

1,033

4Q 2007 3M2007

6M2007

9M2007

12M2007

Gjensidige BankPerformance – key figures

Loans (NOK mill) Deposits (NOK mill)

726

122

388

975

1,701

4Q 2007 3M2007

6M2007

9M2007

12M2007

50.356.9

46.3

37.639.6

4Q 2007 3M2007

6M2007

9M2007

12M2007

Deposit Ratio (%) Customer Development

22,244

6,248

15,996

10,466

5,398

4Q 2007 3M2007

6M2007

9M2007

12M2007

Status as of 19 March 2008

Loans NOK 4,450 mill Deposits NOK 3,101 mill

Deposits ratio 69.7 per cent Customers 29,287

24.04.2008 Gjensidige Bank15

Gjensidige BankGoals & Targets

Goals

Targets

It is expected that the bank will initially be loss-making as it achieves scale – results in 2007 according to plan

Growth is expected to be relatively high for the first few years, until the bank reaches a level where growth will stabilise at a more normal level, in line with the established players

In 2008 Gjensidige is targeting a quarterly run rate for customer addition between 5,000 and 6,000

• Growth in customer base 3Q: 5,530 customers

• Growth in customer base 4Q: 6,248 customers

Gjensidige Bank have earlier communicated that the bank should have a capital adequacy ratio of around 16 %, which is high compared to statutory provisions of 8 %. By the end of 2007 the bank had a capitaladequacy ratio of 20.8%. In the future the bank will put more emphasison risk profile and growth plans when deciding on level of capitaladequacy ratio, but the bank still intends to have a good margin compared to statutory provisions.1. Customers or persons registered as interested in becoming customers

1

1

24.04.2008 Gjensidige Bank16

The bank’s adopted strategy will continue and will be developed during the

coming year. There will be a special focus on product development and

the improvement of customer processes to remain competitive. Efforts

to adapt the bank to the new capital adequacy requirements (Basel II) and

enhancement of the efficiency of internal processes will continue.

In 2007 the bank decided to start a pilot project in financial distribution to

evaluate different service models that can improve the efficiency of the

Group’s distribution system. This work will continue in 2008.

Recruitment of new employees in step with the bank’s growth and development will also be a priority area in 2008.

Gjensidige BankOutlook

VI. Q&A

VI. Appendices

24.04.2008 Gjensidige Bank19

CEO

BUSINESS-

SUPPORT

(5 FTE)

SALES AND MARKETING

(13 FTE)

Jan Kåre Raae

Jan Kaare Hellevang

Frode Schanke

BUSINESS-

DEVELOPMENT

(4 FTE)

Synnøve M Ø IversenGunnar Klakegg

CREDIT

(17 FTE)

PRODUCT

(1 FTE)

Atle Kristian Hornnes

Organisation

24.04.2008 Gjensidige Bank20

Board of Directorscv

Name: Tor Magne Lønnum

Role: Chairman of the Board

Backgr: Gjensidige Forsikring, SKIPPER Electronics AS, Samarbeidende Revisorer AS, KPMG AS, Gjensidige NOR Insurance.

Edu: Norwegian School ofManagement, NorwegianSchool of Economics

Name: Arvid Andenæs

Role: Board member

Backgr: Sparebanken Sogn og Fjordane, Fokus Bank, KPMG Consulting, Sparebanken Nord Norge

Edu: Siviløkonom, Norwegian Schoolof Management (BI), Master ofManagement

Name: Ingun Ranneberg- Nilsen

Role: Board member

Backgr: Gjensidige Forsikring

Sparebanken NOR

ASM AS

Edu: Handelsøkonom (BI)

Management program (Dialog markedsføring, Elektronisk handel)Master of Technology, MBA

Name: Trond Rino Delbekk

Role: Board member (Nestleder)

Backgr: Nordea, Sparebanken NOR

Edu: Bachelor of economics, Master`s degree from the Norwegian Schoolof Management

24.04.2008 Gjensidige Bank21

Board of DirectorsCV

Name: Roger Nedrebø

Role: Board member (Employeerepresentative)

Backgr: Sparebanken Sogn og Fjordane

Edu: Diplomøkonom BI

Name: Marianne B. Einarsen

Role: Board member

Backgr: NSB, Personmarked DnB NOR,

Sparebanken NOR, Storebrand,

UNI Forsikring

Edu: Master of Mangement (BI), Diplommarkedsøkonomi BI/NMH, DH-kandidat Agder Distriktshøgskole

24.04.2008 Gjensidige Bank22

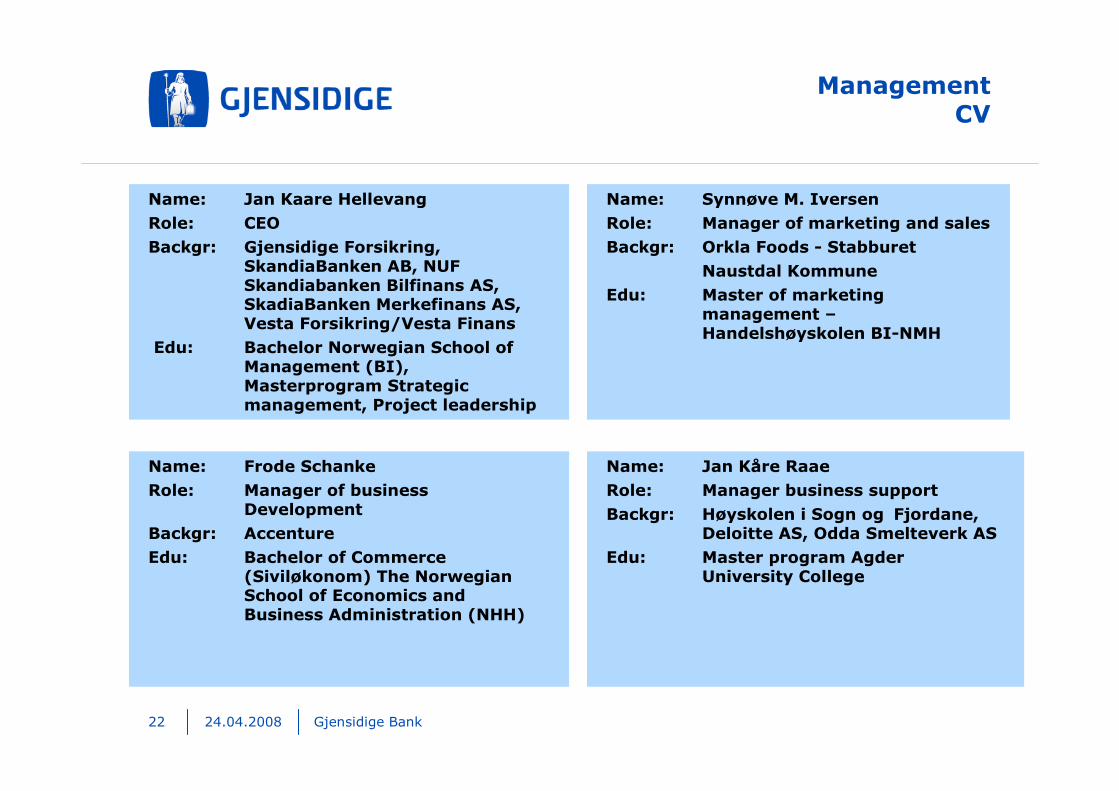

ManagementCV

Name: Jan Kåre Raae

Role: Manager business support

Backgr: Høyskolen i Sogn og Fjordane, Deloitte AS, Odda Smelteverk AS

Edu: Master program Agder University College

Name: Frode Schanke

Role: Manager of business Development

Backgr: Accenture

Edu: Bachelor of Commerce(Siviløkonom) The NorwegianSchool of Economics and Business Administration (NHH)

Name: Synnøve M. Iversen

Role: Manager of marketing and sales

Backgr: Orkla Foods - Stabburet

Naustdal Kommune

Edu: Master of marketing management –Handelshøyskolen BI-NMH

Name: Jan Kaare Hellevang

Role: CEO

Backgr: Gjensidige Forsikring, SkandiaBanken AB, NUF Skandiabanken Bilfinans AS, SkadiaBanken Merkefinans AS, Vesta Forsikring/Vesta Finans

Edu: Bachelor Norwegian School ofManagement (BI), Masterprogram Strategicmanagement, Project leadership

24.04.2008 Gjensidige Bank23

ManagementCV

Name: Gunnar Klakegg

Role: Manager Credit

Backgr: DnB NOR

Norsk Havfisk AS

Klakegg Eiendom AS

Cubus

Edu: Diplomøkonom, BI

Name: Atle Kristian Hornnes

Role: Product Manager

Backgr: Fjaler Sparebank, Dale ofNorway, Kaizen AS

Edu: Bachelor of Commerce(Siviløkonom) The NorwegianSchool of Economics and Business Administration (NHH)