gensler indonesia - a feasibility market research

TRANSCRIPT

BU3102 Multi-Disciplinary Project

Final Report

Gensler Indonesia

Phuvadol Uewongtrakoon 12877726

Lintang Sekar Langit 12752741

Xiao Yao 12848201

Chen Yiyi 12658745

Xing Chen 12659056

Lecturer : Dr Adrian Kuah

Supervisor : Dr Wang Pengji

Table of contents

1.0 Executive summary 1

2.0 Country background 2

3.0 Strategic growth plan of Indonesia 5

3.1 MP3EI 5

3.2 Geographic focus – Jabodetabek 11

3.3 Upcoming government projects 12

4.0 Real estate market in Indonesia 14

4.1 Jakarta 14

4.2 Surabaya 17

4.3 Other promising markets 23

5.0 SWOT analysis 24

6.0 Top real estate companies in Indonesian market 26

6.1 Top architectural companies 29

6.2 Top developer companies 29

7.0 Market entry strategies 33

7.1 Collaboration with international developers 30

7.2 Cooperation with major local developers 32

8.0 References 33

9.0 Appendices 37

Appendix 1: Major architectural companies 37

Appendix 2: Major architectural companies 40

1

1.0 Executive summary

This report is a feasibility market research tailored for Gensler to enter

Indonesia; six sections are developed mainly based on official statistics, latest real

estate reports and news. Section one provides a macro-environment scan including

political, economic, social-cultural and legislative factors of Indonesia; section two is

focused on the country’s strategic growth plan, several components are highlighted

such as the geographic focus area, relevant industry, big upcoming events and

infrastructure plan because these strategies are directly linked to the development of

real estate industry.

The most important part is section three which is a comprehensive analysis of

Indonesian real estate market by geographic location. A number of major cities on

Java Island have various opportunities: residential and retail segments in outskirts of

Jakarta; retail and hotel segments in Surabaya, residential and retail segments in

Bandung and eco-friendly hotel in Yogyakarta. Moreover, a few government projects

will be developed in central Jakarta for the 2018 Asian Games and some well-known

regional developers are planning to develop integrated projects in central Jakarta.

The SWOT analysis (section four) combines all the insights from previous

sections, together with the developers list in section five, the team has come up with a

few entry strategies (section six). In addition, there is also a list of leading architect

companies in section five which may shed light on the competition of architecture

industry.

2

2.0 Country background

Indonesia is a republic country with the largest economy in Southeast Asia. It

is consists of 240 million people with GDP growth of 5.78%. Indonesia was among

the top performers during the global crisis in 2009 due to many factors such as strong

domestic demand and huge amount of natural resources (US Commercial Service,

2012). Located on the world’s major trade routes, has made Indonesia become a good

place for trading and expanding business. Moreover, more than 60 million people

coming from the low-income class are expected to join the middle class in the coming

period that will result in the increase of stronger consumer demand. Also, Indonesia is

currently working on their improvement of infrastructure such as renovation and

construction in the city, military upgrading, safety as well as security systems and

protection of sea-borne traffic.

Economic environments

Indonesia has a market-based economy where the government takes a big part.

Having a large and youthful population, it leads to huge needs of new infrastructure

projects. Thus, Indonesia is a potential market to the U.S. products and investments.

In addition, having both leader comes from business background have made

Indonesia’s economic environment more comfort to foreign investment. The new

government is planning to decrease fuel subsidies that will result in increase of funds

for infrastructure and social development ("Indonesia: Economy | Asian Development

Bank," n.d.) Similar to the U.S, Indonesia belongs to several international

organizations and forums such as the United Nations, ASEAN Regional Forum and

World Trade Organization. More than that, the Indonesian Government has enhanced

its international peacekeeping capacity, reducing greenhouse gas emissions and

adopted a leadership role in the Global Counterterrorism Forum.

3

Political environments

Indonesia’s Political environment at the moment is stable. Recent election in

June 2014 have been put Mr. Joko Widodo, a former furniture businessman and

exporter become president. He is well known as a humble figure and loved by the

people (BBC News, 2014). Indonesia bureaucracies now have been changing into

more transparent and business friendly. Even though ranked as one of the most

corrupted country, Mr. Joko Widodo slowly changed that (Wartaekonomi.co.id, 2014).

Many investors believed now is a perfect environment for foreign investor to invest in

Indonesia mostly thanks to Indonesia’s leader who are both come from businessman

background.

Socio-Culture environments

Indonesia has been well known for its agricultural and maritime section. Most

of Indonesian works as farmers. Despite having large variety of ethnics, 300+ ethnics,

they are well-known for its unity under the national motto “Unity in Diversity”.

Indonesian people are also well known for their hospitality toward foreigners.

Indonesia is the fourth most populous nation in the world after China, India and the

United States. Over two thirds of the population resides in Java, the centre of the

country's economic and political power (Merdeka.com, 2014).

Barriers

Indonesia experiences domestic development challenges, including uneven

benefits from democratic and economic progress, insubstantial institutions caused by

lack of capacity to effectively address its social service needs as well as

environmental degradation. In terms of its economic condition, there is an

implementation of protectionist laws and regulations in Indonesia and unevenly

applied legal structure. The number of corruption rate in Indonesia is also another

factor that should be monitored especially when making business in the country

(“Center for Strategic and International Studies,” n.d.). As mentioned earlier, the

4

uneven legal structure has influenced the country’s safety system such as riots happen

for protests regarding the Government’s decision.

Indonesia current economy and political conditions are considered stable, with

the new president Mr. Joko Widodo, the country’s bureaucracies has become more

transparent and business friendly. Although, Indonesia has been known as one of the

most corrupted country, Mr. Joko Widodo is slowly working to change the reputation

of the country. “President Joko Widodo aims to achieve a +7 percent (y/y) growth

figure by 2019 through the implementation of structural reforms” (Indonesia

Investment, 2014). Additionally, many investors believe that Indonesia is now a great

place to make investment. However, there could be some barriers in doing business in

the country such as its corruption rate, law and regulations as well as uneven legal

structure.

5

3.0 Strategic growth plan of Indonesia

This section starts with an overview of Indonesian Master Plan (MP3EI), and

then several areas are selected from the national development plan as they are most

likely to impact on Indonesian Real Estate Market, such as the Tourism industry, Java

economic corridor (regional economic development strategy) and The Greater Jakarta

(the plan’s geographic focus area). Other government projects in the major region are

also included.

3.1 MP3EI

The purpose of MP3EI (Acceleration and Expansion of Indonesia Economic

Development 2011-2025) is to support Indonesia’s transformation into a developed

country by 2025, meaning that millions of citizens will be pulled out from poverty,

increasing number of middle class will also represent higher purchasing power, better

access to quality education and higher living standard. The master plan will lead

Indonesia become one of the 10 major economies in the world by 2025 and it requires

7-9% real economic growth per year from now on.

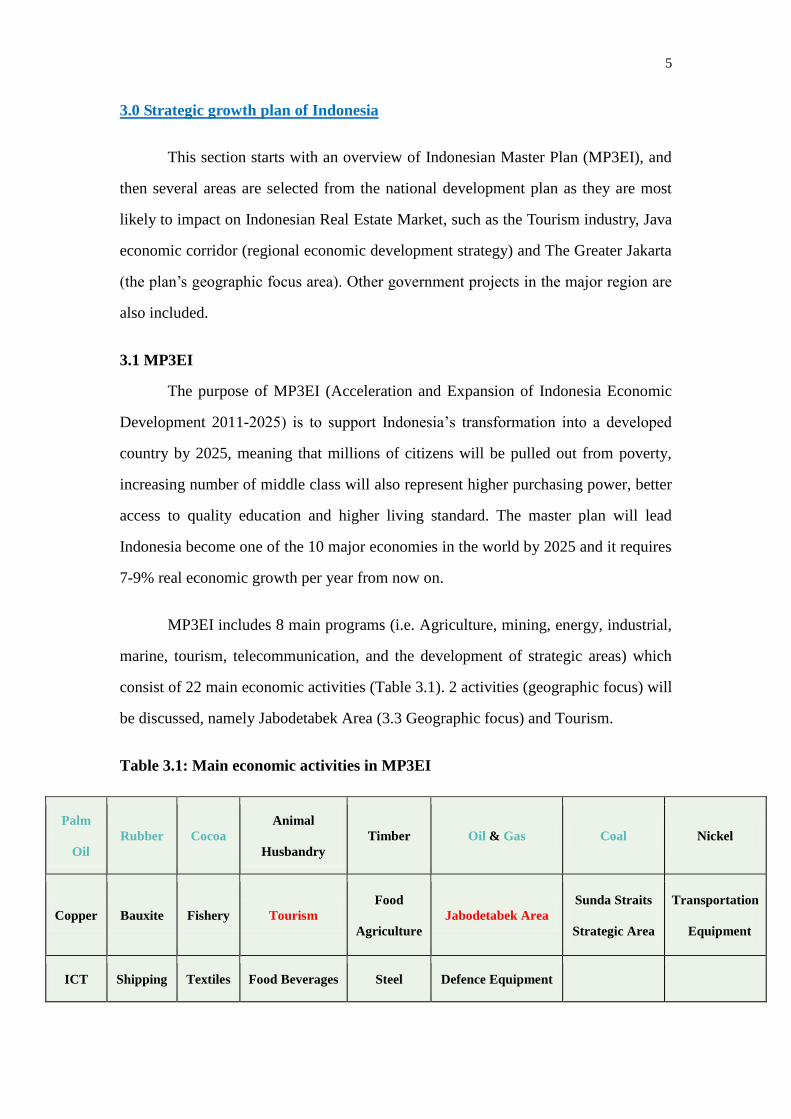

MP3EI includes 8 main programs (i.e. Agriculture, mining, energy, industrial,

marine, tourism, telecommunication, and the development of strategic areas) which

consist of 22 main economic activities (Table 3.1). 2 activities (geographic focus) will

be discussed, namely Jabodetabek Area (3.3 Geographic focus) and Tourism.

Table 3.1: Main economic activities in MP3EI

Palm

Oil

Rubber Cocoa

Animal

Husbandry

Timber Oil & Gas Coal Nickel

Copper Bauxite Fishery Tourism

Food

Agriculture

Jabodetabek Area

Sunda Straits

Strategic Area

Transportation

Equipment

ICT Shipping Textiles Food Beverages Steel Defence Equipment

6

Tourism

Fig. 3.1 Tourism industry in Indonesia

(Source: CEIC Data)

Tourism industry has been promising in Indonesia and it indicates new

investment opportunities for other associated industries, such as hospitality and retail.

In the first 5 months of the year, from January through May 2013, international tourist

arrivals to Indonesia rose by 5.79% although amidst global economic uncertainties.

This means that Indonesia is on track to achieve this year’s target of international

visitors, aimed at 8.6 million visitors. Indonesian international arrivals had a growth

of 7.65% over the same month last year. Indonesia has seen a continued increase in

visitors on account of the many events, concerts, meetings and conventions held in the

past months and are still to be held to the end of the year. On the other hand, the

domestic traveller number is increasing rapidly because of the development of

domestic transportation. As a result, more accommodation and retail space will be

needed.

7

The implementation strategy of MP3EI

1. Economic Corridors

Fig. 3.1 Indonesian economic corridors

(Source: Master plan Acceleration and Expansion of Indonesia Economic Development 2011-2025)

The 6 economic corridors are regional development plans that aim to create an

integrated and sustainable economic base, there are six economic corridors, namely:

Sumatra economic corridor, Java economic corridor, Kalimantan economic corridor,

Sulawesi economic corridor, Bali – Nusa Tenggara economic corridor, and Papua –

Kepulauan Maluku economic corridor. The development gives greater emphasis to

economic development as follows:

To emphasize the increase of productivity and value-adding on natural resource

management through the expansion and creation of a sustainable upstream and

downstream activity chain;

To focus on diverse and inclusive economic development, which connects

corridors with other regions to develop opportunities based on local potential and

specialization;

To emphasize sector and regional development synergies to enhance national,

regional and global comparative and competitive advantages;

To emphasizes integrated economic development between transportation and

logistics, as well as communications and information systems to open regional

8

access;

Will be supported with fiscal and non-fiscal incentives, ease of regulation,

licensing, and optimum public services from Central and Local Governments.

Fig. 3.1.1 Java Economic Corridor

(Source: Master plan Acceleration and Expansion of Indonesia Economic Development 2011-2025)

Java Corridor has the best economic and social conditions in relevance to

other corridors. As shown in Fig.3.1.2, Java is the most populous island in Indonesia

with a population of 143 million (57% of whole Indonesia) it has become the most

densely populated place in the world. Every region of the Java has numerous

volcanoes so that the remaining land is scarce. High population density will directly

affect the price level and development patterns of property, especially residential,

office and retail sectors (Grether & Mieszkowski, 1974).

9

Fig. 3.1.2 Indonesia population density

(Source: Encyclopaedia Britannica, 2009)

Moreover, Java is the most developed region of Indonesia with relatively stronger

transportation system to support its trading economy; the corridor contains 3 sea ports

and 6 economic centres (Jakarta, Surabaya Bandung, Semarang, Yogyakarta, and

Serang). The capital city Jakarta is located in west Java whereas the second largest

city Surabaya is located in East Java. More details about the Greater Jakarta will be

given in the next section. Surabaya--- the second largest city in Indonesia, capital and

economic heart of East Java. With a municipal population of 2.97 million (2010),

Surabaya has emerged as an important centre for business, industry and higher

education. Surabaya has one of the busiest ports in South East Asia and one

international airport, the city also acts as the gateway to the larger Gerbangkertosusila

metropolitan region, which has a population of approximately 9 million (World Bank,

2014).

Therefore Java economic corridor has the potential to serve as the benchmark

for economic changes, evolving from primary-industry focus towards being more

focused on tertiary-industry. The main focus of the Java Economic Corridor

10

development will be on Food and Beverage, Textile, and Transportation Equipment.

In addition, there is also desire to develop other economic activities such as Shipping

and Information & Communication Technology (ICT).

2. Strengthening national connectivity

Indonesia’s national connectivity is part of the global connectivity. Therefore,

the strengthening of the national connectivity has to consider Indonesia connectivity

with regional and global economic growth centres in order to enhance national

competitiveness and optimize advantages of Indonesia’s regional and global

connectivity. 4 national policy elements are included i.e. National Logistic System,

National Transportation System, Regional Development and Information &

Communication Technology (ICT). These policies were combined in order to create

an effective, efficient, and integrated national connectivity. The objects of

strengthening national connectivity are:

To connect the centres of major economic growth through “inter-modal supply

chain systems”.

To expand economic growth through accessibility improvement from the centres

of growth to the hinterland.

To distribute the benefits of economic development by improving the quality of

connectivity to the less developed, isolated and border areas in order to achieve

equitable economic development.

3. Supportive human resource capacity, science & technology

Academic education programs are designed to match the fields of the

economic development potential in each economic corridor. Create a network which

contributes to the value added chain for each commodity and sector developed in each

economic corridor. University research centres must be developed nationally as an

important part of national innovation centre.

11

3.2 Geographic focus---Jabodetabek (The Greater Jakarta)

Fig. 3.3 Jabodetabek map

The Greater Jakarta area covers three provinces, namely DKI Jakarta, Banten

and West Java (the green area shown in Fig. 3.3), specifically the three regencies of

those provinces which surround Jakarta - Bekasi and Bogor in West Java,

and Tangerang in Banten. This area controls approximately 60% of national

import-export activities, as well as more than 85% of decisions related to national

financial matters. The Greater Jakarta is the largest urban area in Southeast Asia. It is

estimated that more than 30% of Greater Jakarta residence has income of more than

approximately USD 5,000 per year.

However, the development of The Greater Jakarta is facing a series of

problems. One of the main problems in this region is high traffic congestion caused

by the current road capacity, which if far below the capacity required to accommodate

vehicle movement. Another problem is the low availability of clean water, limited

airports and seaports capacity, and hindered access to airports because of flooding

during the rainy season.

12

Future development in The Greater Jakarta

Spread business activity outside of DKI Jakarta to reduce the time of travel

between business centres in the internal Greater Jakarta;

Development of a mass transportation system that to commute from the

suburb area (to reduce air pollution, reduce fuel consumption)

Development of interconnected mass transportation network pattern that is

easily accessible to all the activities surrounding the business centres and

government;

Development of an efficient logistics network of production centres in the

region as well as with other production centres that have a close relationship;

Development of sewerage and drainage system that can overcome the

problems of environmental quality (accumulation of garbage, slums and

flood).

3.3 Upcoming government projects

Surabaya Urban Transport Corridor Development and MRT system

The Program will be targeted on an East-West corridor, and a North-South

corridor, that integrates improvements in Non-Motorized Transport (NMT), public

transport, traffic management, land-use and urban development strategies. In terms of

public transport, there will be MRT system (monorail and tram) in CBD Surabaya

(World Bank, 2014).

Jakarta-Surabaya Toll Road

Apart from the Tans-Java toll road network, Government is planning a new

project, a 775km-longtoll road along the coast from Jakarta to Surabaya (above the

sea). The aim of this project is reducing congestion on Java`s highways and

facilitating connectivity and economic development of Java Island. The

Jakarta-Surabaya toll road will connect the Tanjung Priok harbour in Jakarta to the

Tanjung Perak harbour in Surabaya. It is also planned to be extended from Jakarta to

Merak on the western tip of Java as Merak is an important trade route to Sumatra

13

Island. However, the construction date and completion date of this project is unknown

(Anatara News, 2014).

Stadiums and Athletes’ Village for 2018 Asian Games in Jakarta

The Jakarta administration will cooperate with private developers to build

several new sports stadiums for the 2018 Asian Games; the city administration is in

the process of coordinating with the central government to acquire the plots of land

for the stadiums (Asia One, 2014).

Jakarta Mass Rapid Transit (MRT)

The rail-based Jakarta MRT is expected to stretch across over 108 kilometres,

including 21.7 km for the North-South Line (from Lebak Bulus to Kampung Bandan)

and 87 km for East-West Line (from Balaraja to Cikarang). The phase 1of the project

(Lebak Bulus to Hotel Indonesia Roundabout) will be opened to the public by the first

quarter of 2018 (Jakarta Post, 2014).

6 inner-city toll roads in Jakarta

The toll roads were designed to connect all five of Jakarta’s municipalities, the

Public Works Agency and the city administration recently signed an agreement to

begin the project. 2 of 6 toll roads will start construction in few months (Jakarta Post,

2014).

These infrastructure projects will facilitate the connectivity between Jakarta

and Surabaya as well as the internal connectivity within these two cities. With the

improved transport system, residents can travel more efficiently around the city, from

urban area to suburbs. As a result, the property supply will expand to the outskirts of

Jakarta (Jakarta Post, 2014); the future transport network will also spread more

opportunities into other regions of Surabaya. According to Collier International

Research (2014), currently the occupancy rate and asking base rent in central

Surabaya is much higher than other areas of the city.

14

4.0 Real estate market in Indonesia

The real estate market has been growing rapidly in recent few years. The price

for every sector has nearly doubled since the past three years, and that is because of

the expanding middle class, low interest rate regime, national economic growth and

higher consumer confidence towards the presidential elections in 2014. The

Indonesian real estate market consists of five main sectors, i.e., residential,

commercial, retail, hotel and industrial sectors. Data from the Central Statistics

Agency (BPS) showed that the Greater Jakarta area, with a combined population of

22.6 million people, was a big market with huge opportunities that investors should be

interested in; the trend for property development in the retail and condominium

segments would be centred in the suburbs and outskirts of Jakarta (Jakarta Post, 2014).

Furthermore, Surabaya will likely to be another emerging market and an ideal

geographic focus for investors.

4.1 Jakarta

Fig 4.1.a Apartment Strata-tile

Market maintained a stable

performance. Until September 2014,

the take-up rate of existing

apartments in Jakarta reached 95%,

the take-up rate of under construction

projects was 73.2% (Fig 4.1.a). Based

on the market segment, the pre-sales

rate of middle upper class projects

achieved the highest take-up rate of

84%, followed by upper class at 78%.,

there are only two luxury apartment projects under construction, Raffles Residences

and The Langham Residences, which posted an average sales rate of 71%.

15

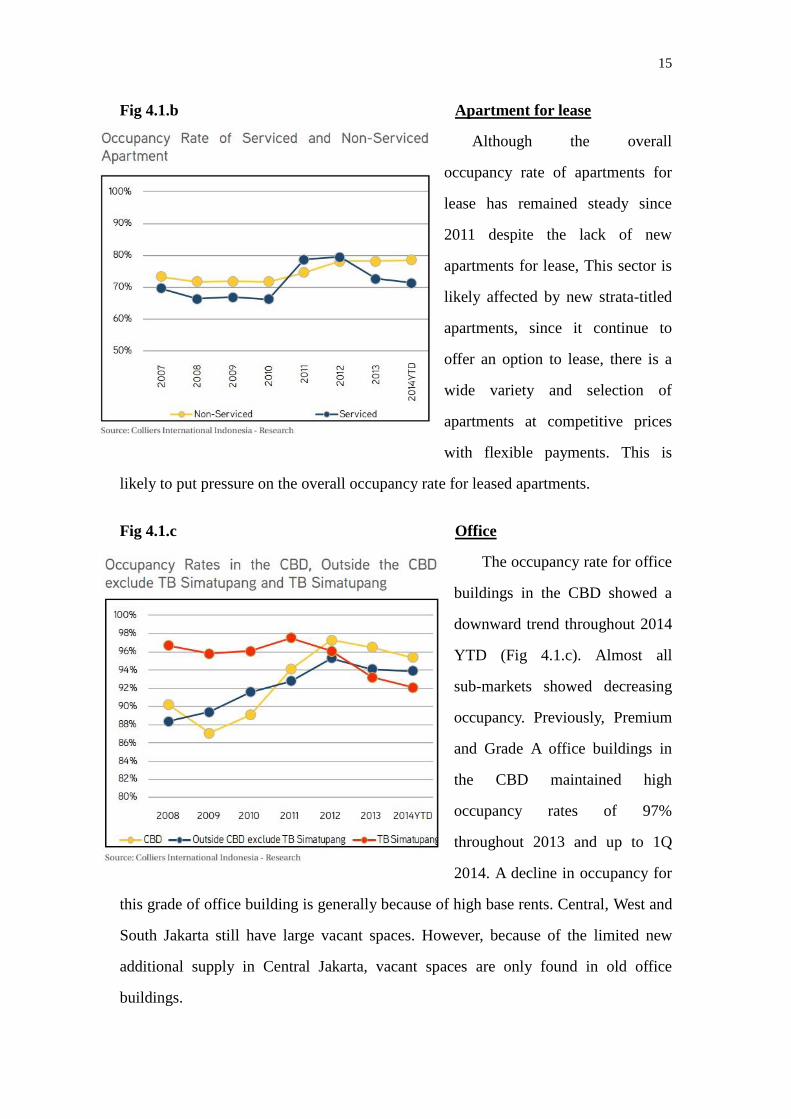

Fig 4.1.b Apartment for lease

Although the overall

occupancy rate of apartments for

lease has remained steady since

2011 despite the lack of new

apartments for lease, This sector is

likely affected by new strata-titled

apartments, since it continue to

offer an option to lease, there is a

wide variety and selection of

apartments at competitive prices

with flexible payments. This is

likely to put pressure on the overall occupancy rate for leased apartments.

Fig 4.1.c Office

The occupancy rate for office

buildings in the CBD showed a

downward trend throughout 2014

YTD (Fig 4.1.c). Almost all

sub-markets showed decreasing

occupancy. Previously, Premium

and Grade A office buildings in

the CBD maintained high

occupancy rates of 97%

throughout 2013 and up to 1Q

2014. A decline in occupancy for

this grade of office building is generally because of high base rents. Central, West and

South Jakarta still have large vacant spaces. However, because of the limited new

additional supply in Central Jakarta, vacant spaces are only found in old office

buildings.

16

Fig 4.1.d Retail in Jakarta

The upper class shopping

centres maintains an occupancy

rate of 88.3% in 3Q 2014. Large

additional supply caused

occupancy rates for shopping

centres in Jakarta to go down.

However, this does not reflect a

slowdown in demand. Indonesia

continues to attract foreign

retailers as so to expand the market. Several retail brands have been eyeing this big

market and some have confirmed the opening of their first stores in Indonesia next

year.

Fig 4.1.e Retail in Bodetabek

There was a quite large

additional supply in Bogor in

early 2014, which caused the

occupancy rate to plummet by

7.7% to 81.7% as of 1Q 2014.

Bekasi and Tangerang are the

most active areas to contribute

new shopping centers, the

average occupancy rate for

shopping centres in Bekasi and

Tangerang remained at 80 and 83%, throughout 2014. However, there will be

additional large retail supply in 2015 - 2017 which may create tighter retail

competition in the BoDeTaBek area; the occupancy level will continue to face a

challenge in the BoDeTaBek area.

17

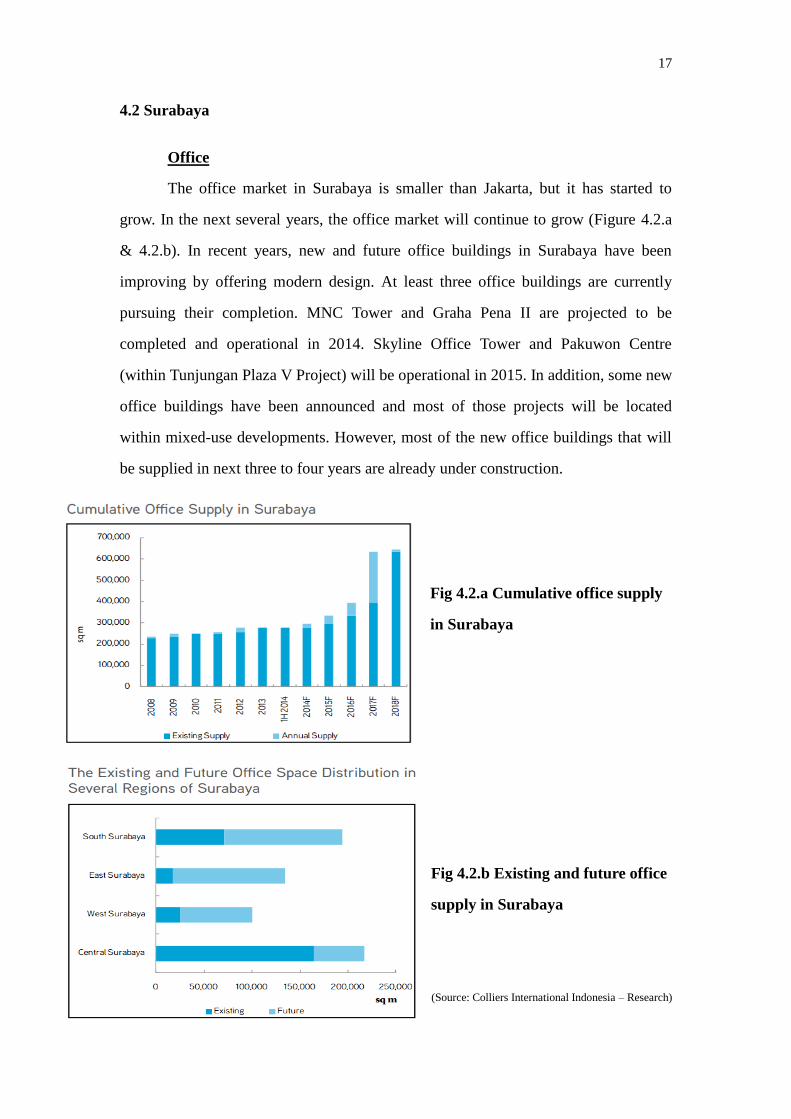

4.2 Surabaya

Office

The office market in Surabaya is smaller than Jakarta, but it has started to

grow. In the next several years, the office market will continue to grow (Figure 4.2.a

& 4.2.b). In recent years, new and future office buildings in Surabaya have been

improving by offering modern design. At least three office buildings are currently

pursuing their completion. MNC Tower and Graha Pena II are projected to be

completed and operational in 2014. Skyline Office Tower and Pakuwon Centre

(within Tunjungan Plaza V Project) will be operational in 2015. In addition, some new

office buildings have been announced and most of those projects will be located

within mixed-use developments. However, most of the new office buildings that will

be supplied in next three to four years are already under construction.

Fig 4.2.a Cumulative office supply

in Surabaya

Fig 4.2.b Existing and future office

supply in Surabaya

(Source: Colliers International Indonesia – Research)

18

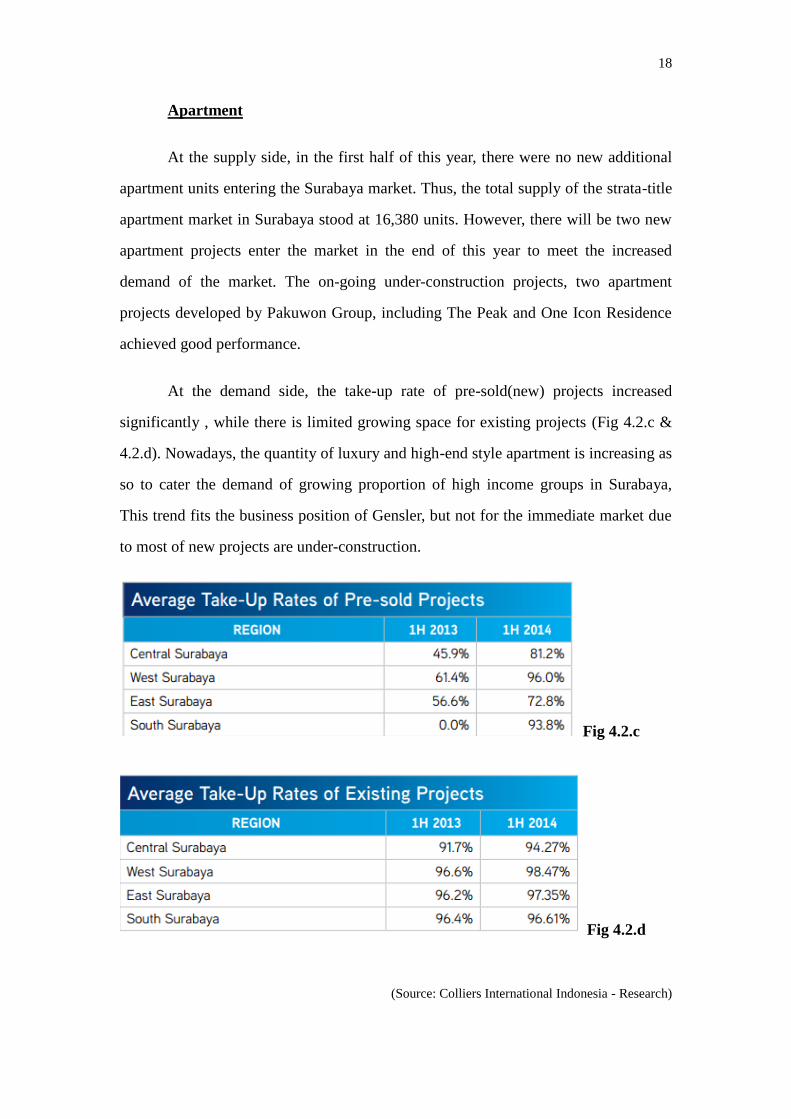

Apartment

At the supply side, in the first half of this year, there were no new additional

apartment units entering the Surabaya market. Thus, the total supply of the strata-title

apartment market in Surabaya stood at 16,380 units. However, there will be two new

apartment projects enter the market in the end of this year to meet the increased

demand of the market. The on-going under-construction projects, two apartment

projects developed by Pakuwon Group, including The Peak and One Icon Residence

achieved good performance.

At the demand side, the take-up rate of pre-sold(new) projects increased

significantly , while there is limited growing space for existing projects (Fig 4.2.c &

4.2.d). Nowadays, the quantity of luxury and high-end style apartment is increasing as

so to cater the demand of growing proportion of high income groups in Surabaya,

This trend fits the business position of Gensler, but not for the immediate market due

to most of new projects are under-construction.

Fig 4.2.c

Fig 4.2.d

(Source: Colliers International Indonesia - Research)

19

Retail

The retail sector is dramatically growing currently and will continue to grow

in the next three years. The number of new shopping centres in all market segments

starting from middle-low to upper-class is projected to grow as shown in Fig 4.2.e,

central Surabaya will contribute 31% of total future shopping space supply (Fig 4.2.f).

Fig 4.2.e

Cumulative retail space

supply in Surabaya

Fig 4.2.f

Distribution of future

retail supply in each

region in Surabaya

(Source: Colliers International Indonesia - Research)

20

Three big developers in Surabaya are in a race to provide new malls in next

three years (Pakuwon Group, Ciputra Development, LIPPO Group). No new future

malls will be completed in 2014, future retail supply seemingly will invigorate in

Surabaya starting in 2015 with the addition of almost 50,000 square metres by 2017.

Overall, the future supply is expected to be 367,750 square metres in Surabaya by

2017 with contributions from 14 new shopping centres. This projected additional

supply will amount to 8.7% annual growth for retail centres in Surabaya from 2014 to

2017.

Furthermore, the occupancy rates for shopping centres in Surabaya jumped

significantly as of 1H 2014. By growing 2.9% in a six-month period, the occupancy

rate has risen to 86.5% in 1H 2014. The occupancy has grown by 5.7% (see Fig 4.2.g).

The increasing demand for middle-upper-class shopping centres has caused rental

rates in Surabaya to grow by 10.2% in 2013 compared to previous years.

Fig 4.2.g Occupancy rates in

different regions in Surabaya

(Source: Colliers International Indonesia - Research)

21

A growth in rental rates in Surabaya was again recorded in the first half 2014

and saw significant growth of 7.8%. This growth has raised rental rates for shopping

centres in Surabaya to IDR412,679 per square metres / month as of 1H 2014 (Fig

4.2.h). Central Surabaya ranks the highest in terms of occupancy rate and rental rate

(Fig 4.2.i).

Fig 4.2.h Average asking

base rents and occupancy of

retail in Surabaya

Fig 4.2.i Occupancy and

asking base rents for each

region of Surabaya

(Source: Colliers International Indonesia - Research)

22

Moreover, retailers expect to motivate the other committed and potential

tenants to open their stores, giving the malls confidence to attract more crowds. These

retailers try to accommodate the middle- to upper-income customers, and may attract

branded retailer. These malls need designers with international perspective and

standard therefore Gensler’s capability best fits into this market.

Hotel

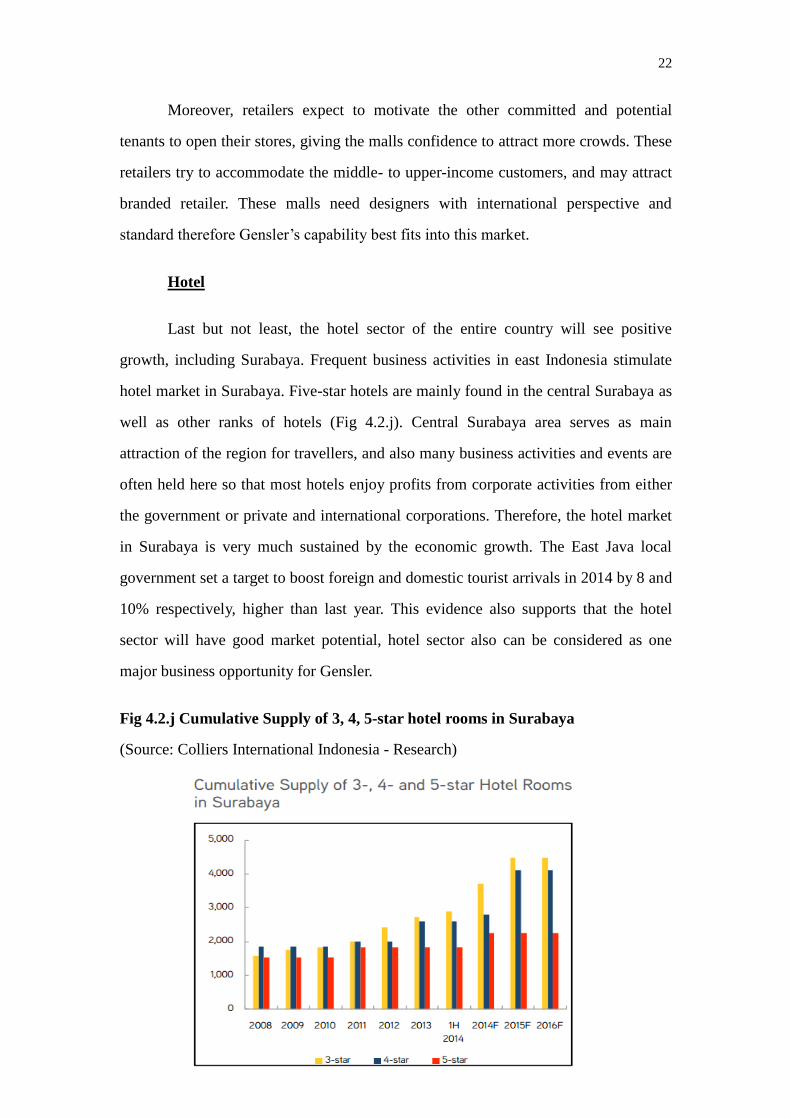

Last but not least, the hotel sector of the entire country will see positive

growth, including Surabaya. Frequent business activities in east Indonesia stimulate

hotel market in Surabaya. Five-star hotels are mainly found in the central Surabaya as

well as other ranks of hotels (Fig 4.2.j). Central Surabaya area serves as main

attraction of the region for travellers, and also many business activities and events are

often held here so that most hotels enjoy profits from corporate activities from either

the government or private and international corporations. Therefore, the hotel market

in Surabaya is very much sustained by the economic growth. The East Java local

government set a target to boost foreign and domestic tourist arrivals in 2014 by 8 and

10% respectively, higher than last year. This evidence also supports that the hotel

sector will have good market potential, hotel sector also can be considered as one

major business opportunity for Gensler.

Fig 4.2.j Cumulative Supply of 3, 4, 5-star hotel rooms in Surabaya

(Source: Colliers International Indonesia - Research)

23

4.3 Other promising markets

Real estate market in Indonesia will remain positive growth. Besides Jakarta

and Surabaya, Bandung has become increasingly attractive; the emerging middle class

in Bandung has propelled the growth of the property sector in the city, ranging from

housing complexes and apartments to malls and hotels. A few developers have already

step into this city, Bandung is also becoming more popular among local tourists as a

lifestyle destination, and the demand for accommodation is on the rise. This has also

prompted several hotel operators to develop accommodation in the area (Jakarta Post,

2014).

Another major city on Java Island, Yogyakarta has been target by a few hotel

groups, such as Melia Hotel and Achipelago. Interestingly, it is reported that a number

of hotels and malls in Yogyakarta have been accused of over-exploiting groundwater

and many have been found to not possess the proper licenses. Thus “Greener”

architect design and construction will be the new trend in this area and entire

Indonesia

24

5.0 SWOT analysis

Strengths

International famous architecture design & planning company with high

reputation.

Strong R & D capability (e.g. Xia Jun, the Executive Vice-President of Gensler,

has been taken charge of main design work in many famous design company

before join in Gensler. And he has participated in designing the world’s second

highest building - Shanghai Tower).

Offices across the USA, UK, Asia, Central America and other 30 cities.

Weaknesses

Digital technology is very important for Design Company (e.g. Aided design,

parametric modelling, simulation of construction, etc.). Young designers proficient

in digital technology, but lack of experience. Senior designers have enough

experiences, but are not skilled in digital technology, and hard to spare time to

study.

Limited managerial skills and technological stock in Indonesia.

Non-native company may be trapped in the poor business environment.

Lack of resources and know-how to enter the market. Usually entering a new

market requires certain regulatory, financial and infrastructural requirements to be

met before they can do business. Companies prefer to partner with local company

so that can lower the barriers to entry.

Opportunities

Indonesia has some largest construction companies & real estate developers in

Asia, which Gensler could corporate with and exchange knowledge with.

Resources are rich (e.g. Cheap and sufficient labour).

Relatively low entry barrier (tariff & non-tariff) as Indonesia is a member of the

Association of South East Asian Nations (ASEAN).

Positive economic environment since the GDP grows well from 2012 until now.

25

Tourism industry in emerging thereby there will be higher demand of hotels.

MP3EI—the country’s development plan favours real estate industry as the

infrastructure will be improved to facilitate traffic, logistic and connectivity within

the country.

Rapid growth of Urbanization and growing population (means more demand for

residential, office and shopping space.

Fast growing middle-class indicates higher purchasing power.

Inflation rate is relatively stable, under control as foreign companies do not want

to enter the market when the CPI grows too fast.

Threats

There are different laws in different parts of Indonesia.

Income inequality threatens the unity of this nation.

If Gensler is successful, there might be another foreign company in the same

industry invests in Indonesia and become a strong competitor.

Corruption in government of Indonesia makes the political environment complex.

Too many established competitors already - oversupply of architecture and interior

design firms in Jakarta that further drive down prices make the market even less

attractive.

Not part of “immediate strategy”. Indonesia is considered a high growth but very

low cost market and the company may have decided that it might be more

worthwhile to allocate scarce resources in markets where they can command a

premium.

26

Table 6: BCI Rating for Green Certification (BCI Asia, 2013)

6.0 Top real estate companies in Indonesian market

The BCI Asia Top Ten Awards has been awarded to developers and

architecture companies that have the highest value portfolios of projects in each full

year since 2005. For almost ten years, it has been one of the most desire awards for

design and construction industry in Asia. The BCI Asia has provided value

information that allows companies to position themselves with top stakeholders in the

industry in Asia. Since 2013, the judging criteria are based on green building ratings

and the value of projects as illustrated in the Table 6. The BCI Asia awards are

bestowed to the top ten architecture and developer companies that have the greatest

results during the last full year calendar (BCI Asia, 2013).

27

These judging criteria have been used to evaluate and determine the top ten

lists in diverse countries such as Australia, Hong Kong, China, Singapore, Thailand,

US and Indonesia. According to BCI Asia (2014), the Top Ten awards have been

bestowed to these architecture and developer companies that have the greatest

influence in Indonesian market in 2013 as stated in the Table 6.1 and Table 6.2

respectively.

28

29

6.1 Top ten architectural companies

Since the green and sustainable development agenda within Indonesia is likely

to grow significantly which creates strong opportunities for specialist architects and

construction services companies to provide developments in green and sustainable

buildings. As an indicator of growing interest, a recent seminar on Sustainable

Construction in Indonesia was organised by the Ministry of Public Works. Both

private and public clients are therefore likely to increase their demand for consultancy

services significantly in this sector (UK Trade & Investment, 2011).

According to the BCI criteria, it has shown that Airmas Asri, Anggara and

Arkonin were the top 3 architectural companies that have the most impact to the

market in terms of project value and green buildings in 2013. Their offerings are

likely to be attractive to a wide range of potential customers within Indonesia, both in

the public and private sector. Gensler could therefore classify these 3 architectures as

its main competitors in the Indonesian market in order to be prepared to compete in

the growing market of green buildings, more information about the competitors are

provided in the Appendix 1.

6.2 Top ten developer companies

As mentioned above about the growing trend of green development and

buildings, Gensler should consider the top 3 developer companies which comprising

of Agung Podomoro, Agung Sedayu, Alam Sutera as its major potential partnership

because these developers are currently dominating the market and obtain a lots of

valued and green projects in Indonesia, more information about the developers are

provided in the Appendix 2.

However, Gensler could also look at Intiland, Pakuwon Jati, Sinarmas Land

and Summarecon because one of their key focus areas are the hospitality market

which matches perfectly with the expertise of Gensler in designing the hotel sector.

30

7.0 Market entry strategies

According to the analysis of Indonesia market, Gensler may find difficulty to

set up its company in Indonesia because of laws, regulations and the complex

procedure of Indonesian government. Moreover, Gensler have never had interactions,

relationships or experiences in the Indonesian market before, it may consume a lot of

resources in terms of time and capital if Gensler choose to set up its office in

Indonesia at the first place. By doing so, Gensler might be able to operate its business,

gain awareness and succeed in the market. However, in the worst case scenario,

Gensler might not be able to do so and waste lots of its resources. The failure of

entering Indonesian market may ruin the reputation and image of Gensler

internationally.

According to Gensler, one of the objectives of entering Indonesian market is to

earn profits as fast and much as it could. Hence, it could be better for Gensler to enter

the market by using a Joint Venture or Joint Operation to collaborate with both major

international developers and major local developers that have experienced and

specialised in the Indonesian market. With the cooperation, Gensler would be able to

take advantages of the developers’ experience, expertise and connections in order to

obtain a mega project and operate the business without setting up its own company in

Indonesia.

7.1 Collaboration with international developers

In this case, Gensler should focus on CapitaLand in particular because it has

already entered the market. CapitaLand is one of Asia’s largest real estate companies.

Headquartered and listed in Singapore, the company’s businesses in real estate and

real estate fund management are focused on its core markets of Singapore and China.

The company’s diversified real estate portfolio primarily includes integrated

31

developments, shopping malls, serviced residences, offices and homes. The company

also has one of the largest real estate fund management businesses with assets located

in Asia.

CapitaLand leverages its significant asset base, real estate domain knowledge,

product design and development capabilities, active capital management strategies

and extensive market network to develop real estate products and services.

CapitaLand’s listed real estate investment trusts are Ascott Residence Trust,

CapitaCommercial Trust, CapitaMall Trust, CapitaMalls Malaysia Trust and

CapitaRetail China Trust.

CapitaLand has been operating in Indonesia since 1995 through its

wholly-owned serviced residence business unit, The Ascott Limited (Ascott), which is

the largest international serviced residence owner-operator in the country. Ascott

currently operates eight properties with about 1,800 apartment units in Jakarta,

Surabaya and Bali. Three more serviced residences comprising approximately 700

units are currently under development in Jakarta and Surabaya.

Recently, it has entered a joint venture agreement with a subsidiary of Credo

Group to develop an integrated development in Central Jakarta, Indonesia. The

integrated development, CapitaLand’s first in Indonesia, will comprise a Grade A

office tower, mid- to high-end residential units, serviced residences and supporting

retail space, spanning a total gross floor area of more than 40,000 square metres.

Estimated to be completed in 2018, construction for the development is expected to

commence in 2015. The total development cost is approximately S$220 million

(CapitaLand Limited, 2014).

In addition, most of the CapitaLand’s projects are in the high class of quality

which require high standard of architecture like Gensler. Therefore, there is potential

for Gensler to propose and cooperate with CapitaLand by using the existing

relationship between the two companies that used to collaborate in the past as a

32

referral even though there are many possible challenges and difficulties in

establishing the collaboration with the large multinational organisation.

7.2 Cooperation with major local developers

In the case of local developers, it is very essential to have some cooperation

with major local developers due to the fact that most mega projects and government

projects are acquired by the local major developers. However, since Gensler has no

significant relationship with local developers in Indonesia, it is suggested that Gensler

should propose to all the major developers as stated above in the table of top ten

developers in Indonesia in order to increase the possibility to obtain the projects as

much as it could. This could be able to help Gensler in generating profits in Indonesia.

By the collaboration with both major international and local developers in real

estate industry would be able to create more opportunities for Gensler to operate its

business and create awareness in Indonesia. After gaining enough experiences,

reputations and connections in the market, Gensler might consider setting its

wholly-owned business in order to maximize its revenues and profits in the future.

33

8.0 References

AGUNG PODOMORO LAND (APL) (n.d.). About Us, Company At Glance.

Retrieved 30 October 2014 from

http://www.agungpodomoroland.com/page/About-Us/Company-At-Glance

AGUNG PODOMORO LAND (APL) (n.d.). Annual Report 2013, Interactive

Version Online. Retrieved 30 October 2014 from

http://agungpodomoroland.com/resources/areport/apln-2013-interactive/bab02.ht

ml#2b

AGUNG PODOMORO LAND (APL) (2014, July 22). Financial Statement,

APLN 1H-2014 Financial Statements. Retrieved 30 October 2014 from

http://www.agungpodomoroland.com/pages/download.php?downloadqh=12&file

=1

Agung Sedayu Group (ASG) (n.d.). Corporate. Retrieved December 26th

2014

from http://www.agungsedayu.com/?page_id=10

Airmas Asri (n.d.). About Us. Retrieved December 15th

2014 from

http://www.airmasasri.com/information/7/about-us/en

Alam Sutera (n.d.). About Us. Retrieved December 26th

from

http://www.alam-sutera.com/about-us/4/company-profile

Anggara (n.d.). Profile. Retrieved December 15th

2014 from

http://www.anggara.co.id/profile.htm

Arkonin (n.d.). Arkonin. Retrieved December 15th

2014 from

http://www.arkonin-id.com/#/Arkonin

Anatara News (n.d.). Jakarta-Surabaya toll road plan must move forward: Minister.

Retrieved from

http://www.antaranews.com/en/news/91164/jakarta-surabaya-toll-road-plan-must-

move-forward-minister

Asia One (n.d.). Jakarta to build new stadiums for Asian Games. Retrieved from

http://news.asiaone.com/news/asia/jakarta-build-new-stadiums-asian-games

34

BBC News (2014, 22 November). Indonesian president flies economy to son’s

graduation. Retrieved from http://www.bbc.com/news/world-asia-30158409

BCI Asia (2013). Judging Criteria. Retrieved December 15th

2014 from

http://www.bcitop10.com/index.cfm/-the-award/judging-criteria/

BCI Asia (2014). Top Ten 2014 Architects – Indonesia. Retrieved December 15th

2014 from

http://www.bcitop10.com/index.cfm/top-10-architects/2014/indonesia/?countryid=

3&year=2014

BCI Asia (2014). Top Ten 2014 Developers – Indonesia. Retrieved December 15th

2014 from

http://www.bcitop10.com/index.cfm/top-10-developers/2014/indonesia/?countryid

=3&year=2014

Bradsher, K. (2013, October 15). Real Estate Heating Up in Indonesia.

Retrieved from

http://www.nytimes.com/2013/10/16/business/international/real-estate-heating-up-

in-indonesia.html?pagewanted=all&_r=3&

CapitaLand Limited (2014, November 17). CapitaLand inks joint venture for its

first integrated development in Indonesia, Media Release. Retrieved from

http://media.corporate-ir.net/media_files/IROL/13/130462/CL_NewsRelease_KSP

rime_17Nov2014.pdf

CEIC (n.d.). Promising Tourism in Indonesia Presents New Investment

Opportunities. Retrieved from

http://www.ceicdata.com/en/blog/promising-tourism-indonesia-presents-new-inve

stment-opportunities

Colliers (2014). Jakarta Property Report 3Q 2014. Retrieved from

http://www.colliers.com/-/media/B9E2A35E2D50495FA0F4F49AE99B8AA2.ash

x

Corruption in Indonesia and the 2014 Elections | Center for Strategic and

International Studies. (n.d.). Retrieved from

http://csis.org/publication/corruption-indonesia-and-2014-elections

35

Di Hadapan Pemuka Bisnis Eropa, Kadin Ingin Jokowi Hapus Hambatan Investasi

- Warta Ekonomi. (n.d.). Retrieved from

http://wartaekonomi.co.id/news/get_news_by_id/38247/di-hadapan-pemuka-bisni

s-eropa-kadin-ingin-jokowi-hapus-hambatan-investasi.html

Grether, D. M., & Mieszkowski, P. (1974). Determinants of real estate

values. Journal of Urban Economics, 1(2), 127-145.

Indonesia: Economy | Asian Development Bank. (n.d.). Retrieved from

http://www.adb.org/countries/indonesia/economy

Indonesia Investment. (2014). Indonesia Investment Coordination Board Targets

15% Investment Growth | Indonesia Investments. Retrieved from

http://www.indonesia-investments.com/news/todays-headlines/indonesia-investme

nt-coordination-board-targets-15-investment-growth/item2687

Jakarta Post (n.d.). Bandung brimming with potential. Retrieved from

http://m.thejakartapost.com/news/2014/09/19/bandung-brimming-with-potential.h

tml

Jakarta Post (n.d.). Property industry to see positive growth in 2015. Retrieved

from

http://www.thejakartapost.com/news/2014/12/26/property-industry-see-positive-gr

owth-2015.html

Jakarta Post (n.d.). Surabaya gearing up for Rp 8.6 trillion MRT project.

Retrieved from

http://www.thejakartapost.com/news/2013/12/20/surabaya-gearing-rp-86-trillion-

mrt-project.html

Jawa dan Sumatera masih jadi pusat pertumbuhan ekonomi nasional |

merdeka.com. (n.d.). Retrieved from

http://www.merdeka.com/uang/jawa-dan-sumatera-masih-jadi-pusat-pertumbuhan

-ekonomi-nasional.html

UK Trade & Investment (2011). Opportunities for UK Construction Sector

Companies in Indonesia. Retrieved from

36

http://www.architecture.com/Files/MembersOnly/MemberUpdate/UKTIIndonesia

ConstrReportAD5046.pdf

U.S. Commercial Service (2012). Doing Business in Indonesia: 2012 Country

Commercial Guide for U.S. Companies. Retrieved from

http://export.gov/indonesia/static/2012%20CCG%20Indonesia_Latest_eg_id_050

874.pdf

World Bank (n.d.) Indonesia - Surabaya Urban Transport Corridor Development

Project (English). Retrieved from

http://documents.worldbank.org/curated/en/2014/03/19352500/indonesia-surabaya

-urban-transport-corridor-development-project

37

9.0 Appendices

Appendix 1: Major architectural companies

Airmas Asri PT

Airmas Asri PT was founded in October 1988 by three principals. It has

prospered and become rapidly one of the Indonesian’s foremost architecture firms that

provide world class services on major projects to its clients by using competitive

conditions as the sole architectural consultant. Airmass has been entrusted to respond

solely for the design and development on numerous mega projects in diverse sectors

such as hospitality, shopping malls and residential. In addition, it also has cooperated

with foreign architecture firms when it is deemed to be the most beneficial to all party

on major projects (Airmas Asri, n.d.).

Philosophy

Airmas has successfully performed to provide a diversity of architectural

services to a wide range of customers. It has operated on the philosophy that

architecture is not only just about designing, it is also about creating value for clients

in order to maximise the value added to the ultimate users.

Mission

Airmas has been working closely with its clients rather than providing the

ready-made or common solutions in order to get a better understanding of their

facility needs such as budget requirements, site conditions and organisation goals.

Hence, Airmas could be able to adjust and develop its services to suit the client

projects. Over the recent years, the company has therefore been able to thrive among

the rapid change of the environment in Indonesian building industry and neighbouring

countries that have affected the market.

Recent projects

District 8 @ SCBD

Springhill Residences

38

The Gianetti at Casa Goya Park Residence

Anggara Achiteam PT

Anggara Achiteam is an architecture company providing expertise planning

and designing in every project in order to provide the best services to its clients.

Anggara has been striving to understand architectural styles in growing Asian cities

that express the fresh where international movements and domesticated styles have

been interwoven. The buildings designed by Anggara display a perfect balance of the

cohesive image between modernism and technology. Moreover, Anggara have the

experience delivering well designed sites to meet functional requirements from wide

range types of clients. It also serves and retains the long lasting relationships with its

clients in order to help firms manage their real estate portfolios (Anggara, n.d.).

Philosophy

The philosophy of Anggara is to provide a creative, convenient and

economical building design services. All aspects of Anggara architectural design have

followed this principle because Anggara believes that every architecture work is a

living organism. A building therefore is analysed and monitored by specialist staffs in

order to achieve the best outcomes (Anggara, n.d.). Nowadays, the property

development business throughout the world is a delicately tuned profession that all

issues from feasibility to final construction are needed close attentions. Hence,

Anggara has prided itself with a completed range of professional skills required with

all the resources to serve and deliver projects to clients on time and with a limited

budget in order to become one of the world most outstanding architecture companies.

Mission

Anggara aims to provide exceptional standard with the highest possible

services to a wide range of clients, regardless to their business size. It has committed

fully to clients in responding to the challenges in architecture industrial demands in

39

order to achieve its goal which is the customer satisfaction.

Recent projects:

Astra Hongkong Land Residential Development (Collaborated With

SCDA)

Bonavista Apartment

GCNM Apartment (Collaborated With SCDA)

Gudang Garam Office Tower

House of Roman Showroom Office

Arkonin PT

Arkonin was founded in 1961 and established as a design and engineering

company in 1975. Arkonin has become one of the most respected and influential

design companies in Indonesia after it has completed more than thousands of projects

covering more than millions of square meters. It has experienced in many sectors such

as offices, hotels, apartments, industrial buildings, urban design, roads, bridges and

water supply. Arkonin has provided a full range of services as a design and

engineering company (Arkonin, n.d.).

Philosophy

Arkonin has been providing trusted and innovated solutions to clients in order

to be the best design and engineering firm in Indonesia. It has been engaged in

building and environmental design producing high professional quality for both

clients and publics.

Recent projects

Gresik Sport Hall and Stadium

Kementerian Dalam Negeri RI

40

Appendix 2: Major developer companies

Agung Podomoro Land Tbk PT

APLN was established in 2004, it is a leading integrated diversified real estate

developer, mainly focus on commercial and residential segments. APLN is one of the

fastest growing and largest real estate developers in Indonesia. There are more than 70

property projects ranging from low cost to high end with majority in middle class

segment, which have been begun or completed construction by APLN group since

1973 to present (APL, n.d.).

APLN integrates a visionary approach to design with an emphasis on speedy

execution and time to market. A unique business model called Fast Churn concept

allows APLN to acquire land or firms with sizeable land which can be developed into

a 3-5 years project in order to optimise the use of capital and resources instead of

accumulate in huge land bank. The company’s sales and revenues increased from

2012 by 4.5% to reach around IDR4,900 billion in 2013. Moreover, there was an

increase about 5.5% of sales and revenues in the first half of 2014 compared to last

year (APL, 2014). At the end of 2013, the total assets raised from 2012 by 29.5% to

IDR15,195.6 billion.

APLN has succeeded in constructing high quality landmark projects such as

Podomoro City, Kuningan City and Senayan City, it therefore is being known as a

pioneer of the superblock development. The second business strategy of APLN is to

increase contribution from recurring revenues. With this strategy, the company’s

recurring revenues has significantly risen from 5.3% in 2010 to 20.5% in 2013. The

continued extension of the business to second-tier growth cities like Bandung, Bali,

and Makassar and so on is the third strategy of APLN to enlarge its business and

obtain majority of market share (APL, n.d.).

Vision

To continue to grow as an integrated property developer, to optimise value for

41

clients, business partners, shareholders and society.

Mission

To meet public needs in quality housing and commercial developments

To optimise return on investment from business partners and

shareholders

To become a developer that can deliver more value to employees

To actively support Government programs in promoting urban

development and improving the human development index

Value

Harmony: in working with clients, business partners, shareholders and

society

Passion and perseverance: optimising our efforts

Quality: maintained at every stage of development

Environmentally conscious: putting care into the environmental aspects of

every project

Recent projects

Indigo Hotel Seminyak

Madison Park at Podomoro City

Agung Sedayu Permai PT

Agung Sedayu Group (ASG) started from a small constructor firm in 1979,

their popularity had spread out through word of mouth in the first 10 years. ASG were

able to extend the business, they have improved their employee standard quality and

become more successful. In 1991, ASG was very well known after achieving the

Harco Mangga Dua, the first electronic mall in Indonesia, followed by another big

scale project in residential and apartments. With good management within the

company, ASG became stronger and managed to avoid the financial crisis in Asia due

42

to their good cooperation and strong internal financial whereas other companies failed

to do so. Since then, ASG started to do more projects including the revolution Kelapa

Gading Square with the one-step-living concept which known as one of the elite

residence in Jakarta. ASG was the one who survived during the crisis in 1997 – 1998;

they kept climbing to the top with financial stability (ASG, n.d.).

Vision

They developed a vision of becoming dynamic and innovative in creating their

product quality as they believe it as a way for developer to compete well in property

industry that keeps changing in Indonesia.

Mission

To be a property developer who gives the best quality of product on time and

cost effective

Value

Humble, professional, trust and focus

Recent projects

Bogor Valley Condotel

Casablanca East Residences 2

Alam Sutera Realty Tbk PT

PT Alam Sutera Realty Tbk was incorporated on November 3, 1993 under the

name PT Adhihutama Manunggal by Harjanto Tirtohadiguno and their families that

focus its business activities in the field of property. Company changed its name to PT

Alam Sutera Realty Tbk by deed dated 19 September 2007 no. 71 made by Misahardi

Wilamarta, SH, notary in Jakarta. At December 18, 2007 the company became a

public company with a public offering in Indonesia Stock Exchange. After more than

19 years since its founding, the company has become an integrated property developer

that focuses its business activities in the construction and management of residential,

43

commercial and industrial areas, and also the management of shopping centres,

recreation centres and hospitality (mixed used development) (Alam Sutera, n.d.).

Vision

To become the best property developer, that focuses on innovation for better

human quality of life.

Mission

To provide excellent service and an innovative product of excellent

quality in developing comfortable, safe and healthy environments for the

customer.

To provide the employee with an opportunity to develop and create

corporate culture and a value based professional working environment in

which all employees may realise their potential thus improve the

productiveness of the company.

To implement prudent governance allowing for sustainable growth of the

company for the shareholders.

To maximise the potential of each property being developed by adopting

integrated development to give high returns for the stakeholders.

Recent projects

Alam Sutera

Paddington Heights – Apartment Tower