general study on consumer goods industry uae 03-05-2010

TRANSCRIPT

A

PROJECT STUDY

ON

STUDY ON CONSUMER GOODS INDUSTRY IN UAE

SUBMITTED TO VINAYAKA UNIVERSITY FOR THE PARTIAL FULFILLMENT OF THE DEGREE OF MASTER OF BUSINESS

ADMINISTRATION IN MARKETING

ZACHARIA.C. GEORGE

REG. NO.

UNDER THE GUIDANCE AND SUPPORT OF

PROF. JOTHILINGAM

CAPITAL EDUCATIONAL INSTITUTE - ABU DHABI

2009 - 2010

Page 1 of 78

CERTIFICATE

This is to certify that the project work titled "STUDY ON

CONSUMER GOOD INDUSTRY IN UAE” submitted by

ZACHARIA. C GEORGE, Reg No. In partial fulfillment

of the requirement of the award of degree of Master of Business

Administration of Vinayaka University, Salem is a bonofide record

of work carried out by him under our guidance and supervision

during the year 2009. The result embodied in this record has not

been submitted to any other university or institute for the award of

any degree/diploma.

Internal Guide Director/Principal

Page 2 of 78

STUDENTS DECLARATION

I ZACHARIA.C.GEORGE Reg No: hereby

declare that the project study entitled " STUDY ON CONSUMER

GOOD IN UAE." has been prepared by me, under the supervision

and guidance of Prof. Jothilingam, Faculty Member of Capital

Institute- Abu Dhabi and now being submitted to Vinayaka

University-Salem for partial fulfillment of the university regulation

for the award of the degree of Master of Business Administration.

In further I declare that this project report is based on the original

project study under taken by me and has not formed a basis for

the award of any other degree/diploma at any other university

Place: Abu Dhabi ZACHARIA. C GEORGE Date:

Page 3 of 78

ACKNOWLEDGEMENTS

First of all, I thank my Almighty God for giving me the ability

to complete this project. I feel extremely fortunate to have the

privilege of undergoing my project study with Analysis of Rubber

Products in UAE. I would like to express my sincere thanks to

Prof. Jothilingam, my internal guide for providing indispensable

assistance during the project guidance session and thanks to him

for his assistance and useful comments. I am very grateful to our

director & Principal Mrs. Laly Joseph and the faculty members of

management department. In addition, I express my affectionate to

my beloved parents, friends & all other family members for being

so encouraging and supportive throughout the study.

Place: Abu Dhabi ZACHARIA. C GEORGE

Date:

Page 4 of 78

INTRODUCTION

1.1. UAE economy and current world economic slow down - a brief overview

It is obliviously important to analysis or study of any industry of a region or a

country, we should know their economic background and how it backing up the

industry with current situation.

Consumer goods industry has been one of the fastest growing industries in

the UAE for the past few years. Favorable government policy frameworks and active

participation of private sector have facilitated one of the world’s most desirable

consumer trade environments in terms of investments and revenue generation.

Further, burgeoning economy, balancing crude oil prices, rising purchasing power

and strong consumer confidence are strengthening the retail industry.

According to the new research report “Booming Retail Sector in UAE”, the

economic slowdown signs were almost nonexistent in UAE consumer industry and its

growth rate remained intact in 2009-2010. Surging public and private sector

consumption along with the contribution of strong industry verticals (tourism, trade,

banking, etc) are expected to help the consumer industry experience an impressive

Compound Annual Growth Rate (CAGR) of around 13% during 2010-2013.

In addition, the country’s population is highly dominated by expats. Of the total

population, UAE nationalists only account for 20% share and rest is from South Asia

and European countries. Large proportions of expatriates are mainly employed in

commerce, aviation, tourism and constriction sectors and enjoy comparatively high

Page 5 of 78

net worth. The consumer segment is fueling retail sales and encouraging new market

players for more developments.

The rapid development of modern retail infrastructure is luring consumers for

convenient shopping experience and transforming into high retail spending. Per

capita gross leasable area (GLA) surpassed 1 Sq Meter mark in 2008, which is one

of the highest in the world. We anticipate that this trend will prevail in coming years

and gradually boost the retail sales growth.

The report is an outcome of extensive research and thorough analysis of retail

industry in the UAE. It facilitates statistics and analysis of all prominent market

segments to provide deep and informative understanding of the market. The report

also examines consumer behavior scenario with respect to purchasing decisions,

spending pattern, and inclination towards domestic and foreign brands. The future

growth areas discussed in the report helps to analyze the emerging market segments

for players.

The United Arab Emirates remains one of the region's economic

powerhouses, despite the slow-down it experienced during the last 18 months. The

economy has experienced a difficult year buffeted by a large drop in oil prices along

with rapid de-leveraging and default in its corporate sector and banking sector strains

it is emerging from the crisis in a stronger position. There is clear signs of a strong

recovery process taking shape in the UAE and the region and expecting region to

recover at a faster pace compared to the US and Europe. Analysis says for a 2.1 per

cent expansion in economic activity, supported by Global economic recovery and

demand for commodities. The gradual recovery in global growth, which is being led

by Asia, will have beneficial effects for the UAE.

Page 6 of 78

The UAE economy may have reached the “bottom of this downturn” and

should see a “mild recovery” in 2010. The recent improvement in global economic

momentum, the rise in oil prices, and the stabilization in domestic markets are

helping the country’s economy to recover from a slump led by the collapse in real-

estate and energy prices.UAE retail sales seen growing 3-5% in 2010

Recent study identified as consumer industry has the best practice and

recommendations which retailers and manufacturers can implement to survive, and

even take advantage of the current downturn. It by stressing a product's value

proposition - as opposed to cheapness - maintaining marketing budgets, better

targeted product ranges, improving customer service levels and reinforcing the

quality of products are all vital to building quality and maintaining margins. It believes

that sales of food and beverage products that can be consumed within the home will

remain strong in UAE. Cosmetics sales are also forecast to benefit from sacrificial

consumption patterns as cash-strapped consumers, wanting to spend less but not

stop buying, continue to buy smaller, less expensive indulgence.

The Middle East region is booming and is now the second fastest growth area

in the world after China. Political and economic reforms across the region provide a

new dynamic business atmosphere where consumer demand and consumption is on

the rise.

1.2 OBJECTIVE OF THE PROJECT

Page 7 of 78

The main objective of the project is to conduct a general study about

consumer goods market in UAE, to analyze the general outlook of the consumer

goods industry and to study about the major competitors in the market.

It also aims at evaluating the strength and weakness of consumer goods

industry and suggesting ways to improve market share of consumer goods.

1.3 SCOPE AND SIGNIFICANCE OF THE STUDY

The scope of the is both overview level information and in-depth analysis of

consumer goods industry highlighting the major internal and external factors which

play a crucial role in the performance of the consumer goods industry in UAE

1.4 RESEARCH METHODOLOGY

The approach to this study is supply based. The trade sector and

supply sector will be considered in this study. Basically the imports constitute the

supply side of the consumer goods market. While the domestic consumption and re-

exports constitutes the demand side of the market. In addition the data that is

available with the Chamber of commerce databases and other countries databases

are used to shed light on the size and the structure of UAE consumer goods market.

Secondary data from other relevant sources has also been used.

Research methodology is considered as the nerve of the

project .Without a proper well organized research plan, it is impossible to complete

the project and reach to any conclusion. The project was based on the survey plan.

The main objective of the survey was to collect appropriate data, which work as

base for drawing conclusion and getting result. Therefore, Research methodology is

the way to systematically solve the problem. Research methodology not only deals

about the methods but also logic behind the methods used in the context of a

research study and it explains why a particular method has been used in the

preference of the other methods.

Page 8 of 78

1.5 Research Design

Research design is important primarily because of the increased complexity in the market as well as marketing approaches available to the researchers .In fact it is key to the evolution of the successful marketing strategies and programmers .It is an important tool to study the buyers behavior, consumption pattern , brand loyalty and focus market changes . A research design specifies the methods and procedures for concluding a particular study. Research design specifies methods and procedures for study.

1.6 SAMPLING METHODS The researcher had selected a reasonable number of samples for the

primary data collection. The technique selected for sampling was convenience and

availability. Type of sampling method used is random in nature

1.7SAMPLE SIZE100 customers

1.8 RESEARCH TOOLSIt provides a detailed analysis of the consumer goods industry in UAE,

including key growth trends, statistics, forecasts, and the competitive environment

including key issues facing the industry. The tool used for analyzing the primary

data collected through questionnaire was percentage system. Diagrammatic

presentation has also been done through charts.

1.9 RESEARCH AREAGeneral study of Consumer goods industry

Page 9 of 78

2. Consumer Goods

2.1. General View

The issue of consumer goods is most important in assessment of Gross

Domestic Product (GDP), basically a yearly measurement of what is purchased

(consumed), made, invested, and what is spent by the government. Economic

analysts can parse out the different types of goods that are included in the GDP, and

look at how each area is performing. So for instance, a decline in the sale of

consumer goods would indicate people aren’t spending as much on most consumer

items, which can include on food, automobiles, clothing, electronics, and a host of

other things.

Some things that would seem like consumer goods are not traditionally

classed as them. For instance, most things sold second hand aren’t consumer goods

any longer because they were already counted as final goods earlier. This would

include the resale of items like cars, clothing or jewelry. Other things that you might

purchase like parts of cars, even tires or a car battery, aren’t final goods either.

Technically, the goods used in the assembly of cars don’t represent a final product,

even though many of us have had to buy new tires for a car or replace a car’s

battery, because they may be used in the production of new items.

There’s also a classification of goods called Fast Moving Consumer Goods

(FMCG) or Consumer Packaged goods. These are items that will be sold very

quickly. Most items sold in grocery stores are FMCGs, and many small electronics

items make the list too. These things don’t always sell quickly but usually are

consumed quickly, and are usually defined because they are in contrast to what are

called durable goods, like big appliances. Simply put, a jar of strawberry jam, an

FMCG, will be consumed much more quickly than the refrigerator you place it in, a

durable good.

Another group of final goods is called Fast Moving Consumer Electronics

(FMCE). These include items like cameras, cell phones, MP3 players, and laptop

Page 10 of 78

computers. Note that desktop computers may be more likely to be considered as

durable goods, though they’re still final goods because they tend to live longer than

the average laptop.

2.2. Consumer goods: Definition

Consumer goods are alternately called final goods, and the second term

makes more sense in understanding the concept. Essentially, consumer goods are

things purchased by average customers, and will be consumed or used right away.

Any tangible commodity purchased by households to satisfy their wants and needs.

Consumer goods may be durable or nondurable

2.3. Consumer goods: Classification

Consumer goods can be classified into three type they are durable, non

durable and semi durables

3.3.1Durable goods

One that yields services or utility over time rather than being completely used

once. Most goods are therefore durable goods to a certain degree. These are goods

that can last for a long time, such as refrigerators, cars, and DVD players,[1] and

such big-ticket items should continue to be serviceable for three years, at least.

Perfectly durable goods never wear out. It has a significant life span, often defined as

three years or more, and consumption is spread over this span. Durable goods,

which can be used repeatedly or continuously for more than one year, such as motor

vehicles and major appliances. Under this category has got scope of study on varies

industry such as electronic appliance and auto mobile.

Page 11 of 78

2.3.3 Nondurable goods:

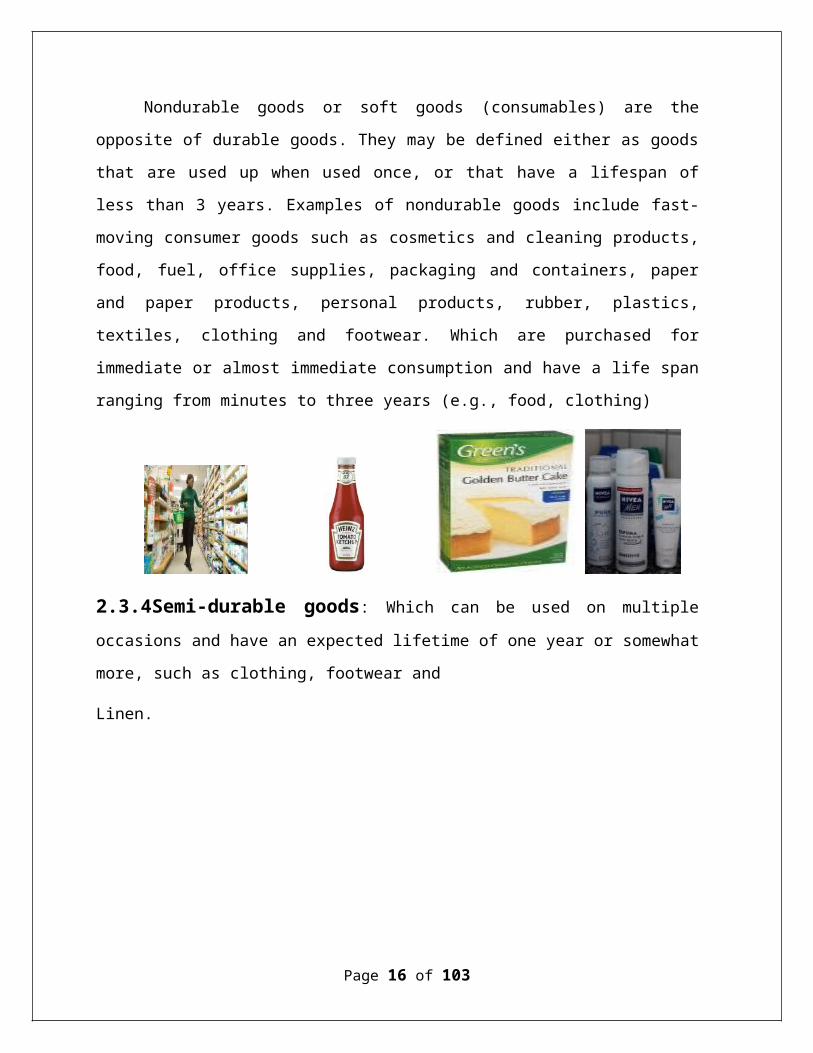

Nondurable goods or soft goods (consumables) are the opposite of durable

goods. They may be defined either as goods that are used up when used once, or

that have a lifespan of less than 3 years. Examples of nondurable goods include fast-

moving consumer goods such as cosmetics and cleaning products, food, fuel, office

supplies, packaging and containers, paper and paper products, personal products,

rubber, plastics, textiles, clothing and footwear. Which are purchased for immediate

or almost immediate consumption and have a life span ranging from minutes to three

years (e.g., food, clothing)

2.3.4Semi-durable goods: Which can be used on multiple occasions and have

an expected lifetime of one year or somewhat more, such as clothing, footwear and

Linen.

The study of consumer goods in UAE is too outsized. Therefore we can

analyze only here the market of non –durable goods and FMCG which is it self huge

and not easy to describe such short project

Page 12 of 78

3. FACTS INFLUENECING THE CONSUMER INDUSTRY

3.1. Statistical Analysis

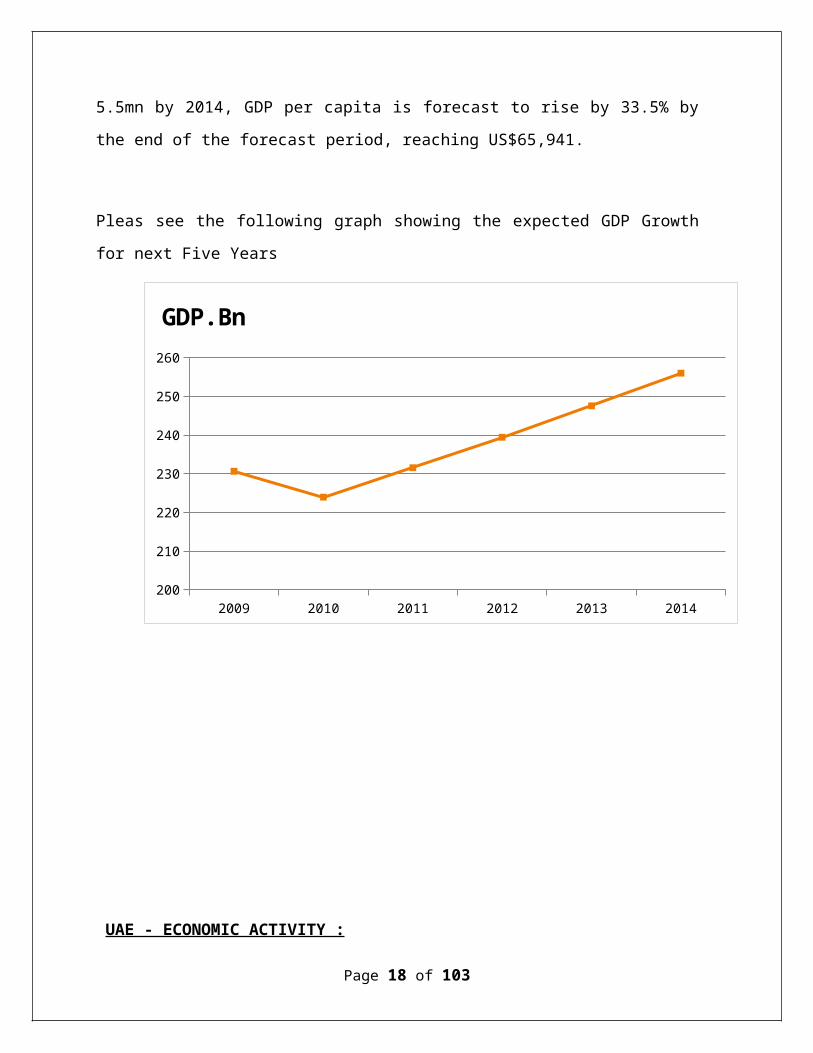

The UAE’s nominal GDP was US$230.61bn in 2009, with last year’s decline of

2.9% expected to translate into growth of 2.8% in 2010 as the economy begins to

recover. BMI predicts average annual GDP growth of 3.4% between 2009 and 2014.

With the population increasing from 4.7mn in 2009 to an estimated 5.5mn by 2014,

GDP per capita is forecast to rise by 33.5% by the end of the forecast period,

reaching US$65,941.

Pleas see the following graph showing the expected GDP Growth for next Five Years

2009 2010 2011 2012 2013 2014200

210

220

230

240

250

260

GDP.Bn

Page 13 of 78

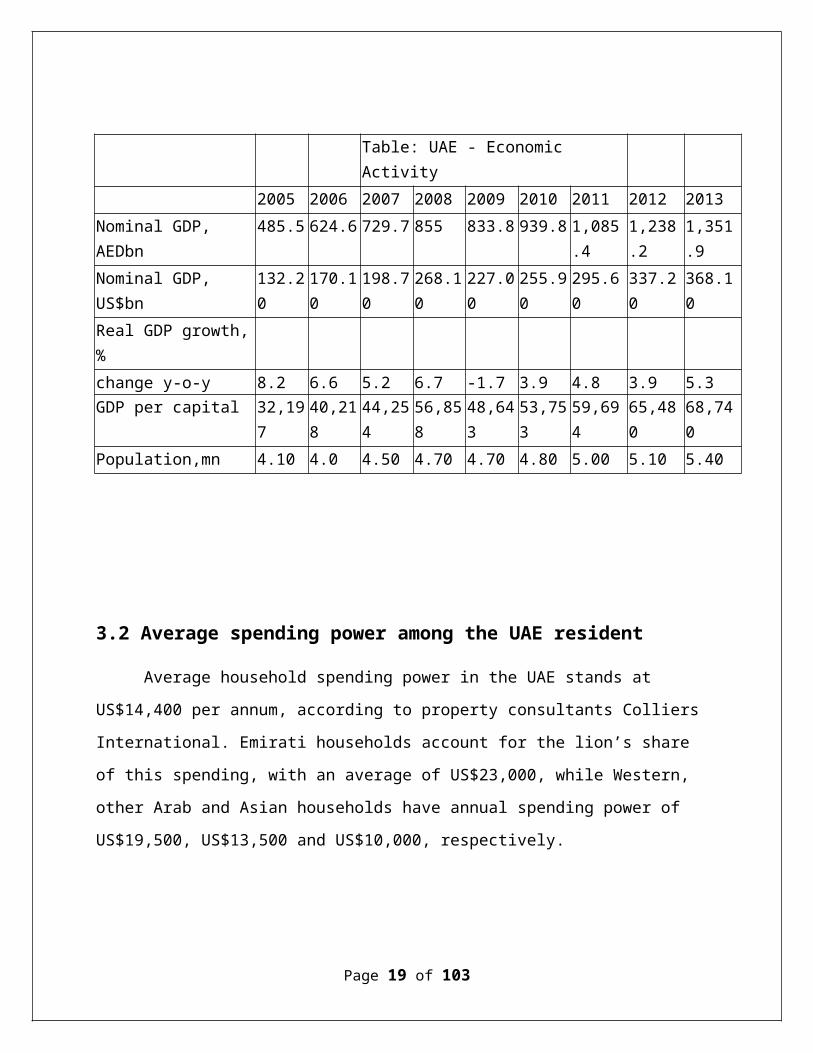

UAE - ECONOMIC ACTIVITY :

Table: UAE - Economic Activity 2005 2006 2007 2008 2009 2010 2011 2012 2013Nominal GDP, AEDbn 485.5 624.6 729.7 855 833.8 939.8 1,085.4 1,238.2 1,351.9Nominal GDP, US$bn 132.20 170.10 198.70 268.10 227.00 255.90 295.60 337.20 368.10Real GDP growth, % change y-o-y 8.2 6.6 5.2 6.7 -1.7 3.9 4.8 3.9 5.3GDP per capital 32,197 40,218 44,254 56,858 48,643 53,753 59,694 65,480 68,740Population,mn 4.10 4.0 4.50 4.70 4.70 4.80 5.00 5.10 5.40

3.2 Average spending power among the UAE resident

Average household spending power in the UAE stands at US$14,400 per

annum, according to property consultants Colliers International. Emirati households

account for the lion’s share of this spending, with an average of US$23,000, while

Western, other Arab and Asian households have annual spending power of

US$19,500, US$13,500 and US$10,000, respectively.

Page 14 of 78

UAE NatioanlAsian

WesternOther Arab 0

5,000

10,000

15,000

20,000

25,000

Spen

ding

Pow

er in

US$

3.3 factor - influencing retails selling growth

While Emiratis actively contributed to retail sales, the buying power of the

country’s expatriate residents was the major source of success, a study by UAE

research firm RNCOS said. Tourism is also a massive factor in stimulating retail

growth, with the UAE expecting more than 11mn tourists every year by 2010.

Growing urbanization is also factor in the buoyancy of the retail sector. Abu Dhabi in

particular is highly urbanized; with the Urban Planning Council (UPC) projecting that

Abu Dhabi City’s population will rise to 1.3mn by 2013. In 2005, 85.5% of the UAE’s

population was classified by the UN as urban and this is forecast to increase to

86.3% by 2010.

Page 15 of 78

Population Expatriate Tourism0

10

20

30

40

50

60

70

80

90

100

3.4 Population forecast for the next Five Years

In 2009, the UAE's population was estimated at 6 million,[3] of which just

under 20% were UAE nationals or Emiratis,[81] while the majority of the population

were expatriates.[82] The country's net migration rate stands at 22.98, the highest.

The UN describes 73% of the UAE population in 2005 as economically active,

forecast to rise to 78.6% by 2015. In 2005, just over 30% of the population was in the

crucial 20-44 age range, and this is expected to hit 57.6% by 2015.

Page 16 of 78

1963 1968 1975 1980 1985 1995 1999 2003 2009 20100

1000000

2000000

3000000

4000000

5000000

6000000

7000000

Year

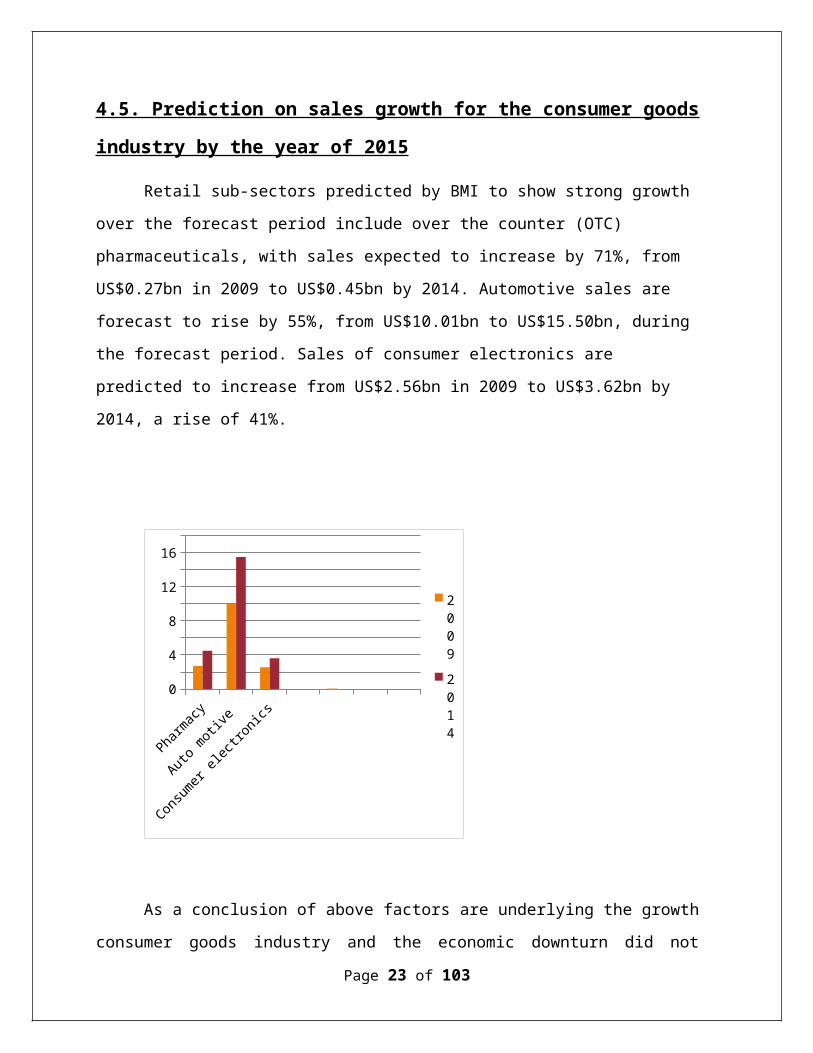

4.5. Prediction on sales growth for the consumer goods industry by the year of 2015

Retail sub-sectors predicted by BMI to show strong growth over the forecast

period include over the counter (OTC) pharmaceuticals, with sales expected to

increase by 71%, from US$0.27bn in 2009 to US$0.45bn by 2014. Automotive sales

are forecast to rise by 55%, from US$10.01bn to US$15.50bn, during the forecast

period. Sales of consumer electronics are predicted to increase from US$2.56bn in

2009 to US$3.62bn by 2014, a rise of 41%.

Page 17 of 78

Pharmacy

Auto motive

Consumer ele

ctronics

0

2

4

6

8

10

12

14

16

18

2009

2014

As a conclusion of above factors are underlying the growth consumer goods

industry and the economic downturn did not appear to have a severe impact on the

lifestyles and attitudes of consumers in the UAE. That will provide us positive out look

for the study of this industry.

Page 18 of 78

4. MAJOR PLAYERS IN THE INDUSTRY – WHOLE SALE SECTOR

4.1. UAE Consumer Market:

UAE, one of the most attractive retail destinations around the world,

represents a high potential and untapped market for Consumer good industry. With

growing awareness, surging income levels and shifts in consumer behavior, the

country’s nascent consumer goods market is fast transforming into the world’s fastest

growing consumer market. In addition, increasing population will further boost

demand for consumer goods in the country.

According to our new research report “Consumer Market has substantially

grown over the past few years and caught the attention of international players. It

showed impressive performance last year (2009), which indicates to the

nonexistence of economic slowdown effects. Aggressive marketing strategies and

consumer acceptance of branded products will enable the industry to register a

CAGR of more than 11% during 2010-2013.

The market will witness a dramatic change in competitive landscape. A large

number of international companies will foray into the lucrative UAE market with their

diversified product portfolio. This will lead players to invest huge amount of money in

product innovation and development in order to capture a significant share of the

overall market. The large untapped market in al areas is anticipated to witness

concrete market developments which will also give impetus to the consumer foods

market.

The rapid development of modern retail infrastructure is luring consumers for

convenient shopping experience and transforming into high retail spending.

Consumer goods companies are optimally utilizing this trend and executing strong

product positioning strategies to maximize their market returns.

Page 19 of 78

4.2. Market Leaders in the consumer Industry

4.2.1 Industry out look

The UAE is leading global consumer market not merely on account of its

strong growing domestic demand, but also because of its role as trading hub serving

the expanding market of whole Middle East. Located at the crossroads of Asia and

Middle East, the consumer product distributors of emirates serve a potential market

of almost 2 billion people.

4.2.1 Domestic Market

The sophisticated local market has grown strongly in recent years. The UAE

has one of the highest GDP capita in the world, due to its oil wealth. The consumer

goods market is also boosted by excellent telecommunication and information

technology infrastructure. The large expatriate community also drives market

development and helps swell a growing population.

In the last few years, the local market has steadily become more important in

relation to the re-export trade. The UAE is favorite testing ground for multinational

consumer goods vendors for new product launches and marketing initiatives.

In the last few years, the local market has steadily become more important

relation to the re-export trade. The UAE is a favorite testing ground for multinational

consumer electronics vendors for few product launches and marketing initiatives.

Over the last couple of years, the show has become more attractive to global

consumer goods companies with the rise in spending power of the region, particularly

the UAE.

Page 20 of 78

4.3 COMPANY PROSPECTS -WHOESALE

Trading partners we can classify into three types based on their trading

according to the nature of consumer goods and these are durable goods, non-

durable goods, and Semi-durable goods.

Leading players in United Arab Emirates for consumer goods industry is a

huge list. It is not easy to take all of them in such small project. Therefore, we

illustrate few companies here in this project based on the activities and types of

consumer goods handling by them.

4.3.1Kuwait Food Co. - Americana (FOOD)

Kuwait Food Co. - Americana (FOOD) is specialized in the industry of canned

and Frozen Goods, Meat and Poultry, Restaurants and Cafes. Kuwait Food

Company Americana KSC is a Kuwait-based public shareholding company engaged

in the manufacture, import, wholesale and retail of consumer food and beverage

products across Kuwait and the Arab markets. The Company is also engaged in the

operation of fast food restaurants and international franchises in Kuwait and the

Middle East. It operates over 1000 restaurants across 17 countries. Its franchises

include Hardee’s, T.G.I. Friday’s, Krispy Kreme, KFC, Pizza Hut, Baskin Robbins,

Samadi and Fish Market. Its consumer food and beverage products are

manufactured in five countries, and are marketed across the region under such brand

names as Americana Meat, Americana Cake, Farm Frites, California Garden, Heinz,

Koki, Greenland, Americana Olives, Gulfa and Beefy. The Company’s subsidiaries

include Egyptian Co. for International Touristic projects (Americana), Egypt; Gulfa for

Mineral Water, United Arab Emirates, and Al Ahlia Restaurants Co., Saudi Arabia.

Maintain a position as the 1st choice of

Page 21 of 78

4.3.1. A Subsidiaries, Associates & Joint Ventures

International Cosmetics Co.

International Fashion Co.

Kuwait Food Co.

Kuwait Food Co.

Qatar Food Co.

Al Ahlia Restaurants Co.

National Food Industries Co.

America Group for Food & Touristic Projects

Egyptian Canning Co. (Americana)

Products

Page 22 of 78

Technical Analysis-Kuwait Food Company

Page 23 of 78

4.4. New medical Centre for Trading- Cosmetics-Healthcare-Food

NMC Trading, is a 100% local organization incorporated in the UAE in 1984,

employs over 1,000 people, with 2007 turnover exceeding US$ 125 million is one of

the UAE’s leading marketing and distribution companies for prestigious international

brands.

NMC Trading is owned by the NMC Group – a multi billion dollar diversified

business conglomerate in UAE with interests in Healthcare, Financial Services,

Manufacturing, Trading, Hospitality, Retailing, Beauty Care, Information Technology,

Advertising and Real Estate

The emergence of NMC as a leading player in the trading business stems

from a simple business philosophy - "Advance forays into high potential, high growth

segments and establish a strong presence in these markets".

Armed with a mission critical plan and a team of dedicated marketing

professionals, NMC for Trading is continuously synchronizing the sales, marketing

and distribution support systems for some of the most reputed companies in the

world.

Today, the numbers speak for themselves. Twenty brands occupy premier

slots and an equal number of companies is surfacing in this list, all thanks to able

leadership and focused operational activities. The hallmark of the trading business is

the fourth P in the marketing mix - Physical Distribution.

From temperature-sensitive vaccines and life-saving drugs to ECG machines

and foetal heart monitors, the NMC markets and distributes a wide range of products.

Behind these complex operations are the ultra-modern, strategically located

warehouses and a fully computerized inventory management system.

No wonder, when it comes to logistics, the trading division is famous for its "on

time, each time, every time" deliveries.

Page 24 of 78

The trading wing has stolen the march over competitors by continuously

adding value to the brands of its trading partners, aided by participation in market

research activities to review, evaluate and propose recommendations to help identify

critical determinants in competitive trade.

In short, NMC for Trading is the gateway for establishing sound businesses in

the United Arab Emirates

The emergence of NMC as a leading player in the trading business stems

from a simple business philosophy - "Advance forays into high potential, high growth

segments and establish a strong presence in these markets".

Armed with a mission critical plan and a team of dedicated marketing

professionals, NMC for Trading is continuously synchronizing the sales, marketing

and distribution support systems for some of the most reputed companies in the

world.

Today, the numbers speak for themselves. Twenty brands occupy premier

slots and an equal number of companies is surfacing in this list, all thanks to able

leadership and focused operational activities. The hallmark of the trading business is

the fourth P in the marketing mix - Physical Distribution.

From temperature-sensitive vaccines and life-saving drugs to ECG machines

and foetal heart monitors, the NMC markets and distributes a wide range of products.

Behind these complex operations are the ultra-modern, strategically located

warehouses and a fully computerized inventory management system.

Page 25 of 78

.The trading wing has stolen the march over competitors by continuously

adding value to the brands of its trading partners, aided by participation in market

research activities to review, evaluate and propose recommendations to help identify

critical determinants in competitive trade.

In short, NMC for Trading is the gateway for establishing sound businesses in

the United Arab Emirates

4.4.1 NMC Trading: Operating Companies

The portfolio of businesses under NMC Trading has been strategically

grouped under 3 operating companies

4.4.1. A Beiersdorf Cosmetic Trading (BCT)

Product Categories and Key Brands

BCTC represents the following portfolio from Beiersdorf, Germany NIVEA Crèmes

NIVEA Body Lotions ,NIVEA Sun Care, NIVEA Face Care ,NIVEA Hair care,

NIVEA Bath Care, NIVEA Deodorants, NIVEA For Men Range, NIVEA Make Up

Range ,NIVEA Hand Care, Labello Chap Sticks, Eucerin Range, Hansaplast First Aid

Strips,NIVEA Crèmes

Page 26 of 78

f NIVEA PRODUCTS

BCTC represents the following portfolio from Beiersdorf, Germany NIVEA Crèmes

NIVEA Body Lotions ,NIVEA Sun Care, NIVEA Face Care ,NIVEA Hair care,

NIVEA Bath Care, NIVEA Deodorants, NIVEA For Men Range, NIVEA Make Up

Range ,NIVEA Hand Care, Labello Chap Sticks, Eucerin Range, Hansaplast First Aid

Strips,NIVEA Crèmes

4.4.1. B New Medical Centre for Trading (NMCT)

Product Categories

The NMT Foods Division supplies international brands of Bread Spreads,Breakfast

Cereal,Cakes (Frozen),Canned Vegetables, Chicken (chilled & frozen),Chocolates,

Coffee, Condiments, Cookies, Cooking Oil, Crabs (frozen), Curry Powders. Fries

(frozen), Fries (frozen),Fruit Juices, Honey, Instant Mixes,Jams, Masala Powders,

Noodles,Pickles & Pastes, Rice,Spices,Spices & Seasonings,Tea,Thai foods,Tuna

Vegetables (frozen)

Page 27 of 78

NMC Own Brands

Tasty

Food Factory -

BiteRite -

Principal Company Brands

McCormick (Mc Spice, Mc Thai Kitchen, Mc Pop Corn, Mc Vitasoy, Sara Lee, Lamb

Weston, Nectaflor, Droste, Nippon, Mr. Tom, Amor Di Pane, Khaza, Agri Gold, Frooti

Mac Coffee, Kracks, HiTea, Blue Ocean, Handy, Mohanlal Taste Buds

Page 28 of 78

4.5. Al Ain Dairy

The first established dairy in UAE and a leading producer of dairy products—

has expanded its quality control system at local farms and processing plant through

the establishment of two new technologies; a Food Lab System and Somatic Cell

Counter.

They have forecasted considerable business expansion during 2010 and we

want to do everything we can to ensure that health remains the top priority

throughout the production process

How they operate

Planning

Strategic planning directives are issued by the Board Executive Committee

and provide guidance throughout Al Ain Dairy’s operations. All divisions work

together to formulate independent plans which are then seamlessly integrated as a

blueprint for the company’s operations to meet set directives.

Future sales plans and projections are forecast with reference to historical

statistics, market intelligence, competitor activity and internal and external research.

The sales plan then assists the dairy in planning the raw milk supply required to meet

the sales forecast. Reference to current technical performance data is taken into

account, with consideration given to herd size development and the volume of raw

milk required from external farms. Financial planning assists all departments by

providing budgets and capital expenditure plans for the forecast activity.

Processing and production

The milk processing function is to convert the available supply of raw milk into

the products required by the sales department on a daily basis. Al Ain Dairy is

equipped with a state-of-the-art processing plant which has many process control

systems in accordance with obtaining HACCP certification. From the milking of the

Page 29 of 78

dairy cows through to the packaging of the finished product, there are many critical

control points, which includes the complete pasteurisation process and these are

continuously monitored. Production records are created and maintained throughout

the whole process, enabling total traceability on all products manufactured.

Products and packaging are analysed regularly and immediate action taken in

the event of non-conformance. All final products are subjected to physico-chemical

and microbiological examination, in addition to monitoring of aseptic points and

online processes.

Strict adherence to the UAE health law, municipality by-laws and the

international health organisations require the manufacturing of safe and healthy

products, in addition to having a good quality assurance system in place. Al Ain

Dairy’s accreditation by HACCP generates confidence from customers and the health

authorities that Al Ain Dairy’s processes meet and exceed safe and hygienic

benchmarks of an international standard.

As the first dairy in the UAE to be awarded HACCP certification, Al Ain Dairy

maintains a competitive edge over other major competing dairies in the region, whilst

offering its customers quality assurance and total peace of mind. Al Ain Dairy’s

quality assurance system has been improved to follow a structured approach by

formalising all process flows, quality control tests, formulations and by implementing

the HACCP system. The methods used are further improved by comparing Al Ain

Dairy’s processes with those of the local health authority to ensure that all

requirements are met and to assist and verify new techniques. New developments in

testing and monitoring are continually evaluated and implemented if appropriate by Al

Ain Dairy.

Page 30 of 78

Cold Chain Process

The cold chain is an essential element in the supply of fresh and safe milk.

The eight step procedure is a critical process which covers the supply of milk from

cow to consumer. The main aim of the cold chain is to keep bacterial contamination

to minimum levels and provide consumers with safe fresh milk. Temperature is a

main contributor to bacterial contamination, so strict controls have been put in place

to keep the milk at a constant temperature of four degrees centigrade (+4ºC)

throughout the whole process.

In the first stage, after the cows have been milked under hygienic conditions,

the raw milk output is examined by technicians at the processing plant. This ensures

that the milk is of the required quality and standards.

The milk is then stored in silos at a constant temperature of +4ºC before

starting the processing procedure by being treated by pasteurization. The

pasteurization process involves the milk being heat treated to destroy any harmful

bacteria present in the raw milk. The milk is then subjected to homogenization which

is a mechanical process where the milk fat is evenly distributed throughout the milk.

Page 31 of 78

Homogenization gives milk a creamy taste and stops the fat from collecting along the

top and sides of the bottle as cream.

After being treated by pasteurization and homogenization, the milk is

packaged or formulated into other dairy products prior to being stored for distribution

from the dairy to the sales depots.

The entire fleet of Al Ain Dairy vehicles is fitted with cooling units to enable the

distribution of milk from the dairy to the sales depots and in turn to the retailers at the

required temperature. Al Ain Dairy salesmen regularly monitor that retailers conform

to the requirements of the cold chain by checking and inspecting the temperatures of

the cold storage units used to display products to consumers and remedial action is

taken in the event of non-conformance.

The cold chain process ultimately provides the consumer assurance and

confidence that they are purchasing the freshest milk that has been produced, stored

and distributed under the most hygienic and controlled conditions possible.

Purchasing

Streamlined and efficient Purchasing procedures ensure that Al Ain Dairy

obtains the best quality raw materials and other production requirements in the most

timely manner. Comparative pricing and evaluation is used in all purchases made by

the dairy to guarantee procurements are being made at the most competitive prices

possible.

Products

» Milk » Yoghurt» Flavored Milk» Laban & Laban Drinks» Health & Lifestyle Products

» Desserts» Juices» Coffee Drinks» Camel Milk» Long Life Milk

Page 32 of 78

Page 33 of 78

The Al Ain Diary bags award of ISO certification to Al Ain Farms in November

2009 for planning, implementing, and maintaining a Food Safety Management

System to work across the company’s operations. Such recognitions are an

important means of encouraging local companies to elevate their production

standards to worldwide calibers.

The Al Ain Diary bags award of ISO certification to Al Ain Farms in November

2009 for planning, implementing, and maintaining a Food Safety Management

System to work across the company’s operations. Such recognitions are an

important means of encouraging local companies to elevate their production

standards to worldwide calibers.

Page 34 of 78

4.6. Al Futtaim Motors.

Considering the study on Consumer good of we have to look the Automobile

industry as well.

Al Futtaim Motors established in 1955, currently it occupies the pre-eminent

position of the largest distributor of automotive products in the Emirates, and leads

the rapid development of automobile business in the UAE, while continuing to

contribute to Toyota's worldwide growth.

Today, Al-Futtaim Motors is synonymous with Toyota and Lexus, which enjoy

undisputed leadership in the UAE in terms of the largest number of vehicles on the

road. Besides Toyota, we also hold exclusive franchises for some of the world's top

automobiles and automotive products like Hino - Japan's leading heavy-duty vehicle

manufacturer, Toyo & Chen shin/ Maxxis tyres, GS & Panasonic batteries and many

more.

To provide full back-up support to these world-class franchises, we have an

established network of showrooms and service & parts centers throughout the UAE.

The UAE's auto industry is seeing a slow recovery during the first quarter of

this year, as consumer confidence and financial lending gradually picks up, industry

experts said.

"International Expo Consults have suggested that automotive car sales are

expected to rise by an average of 19.2 per cent this year whilst car ownership is

projected to rise to 55.9 per cent in 2010 from 55.4 per cent in 2009," said Ehsan

Koman, an economist at Dubai Chamber of Commerce and Industry

Al Futtaim become benchmarks in their respective market segments, setting

unrivalled standards in the automobile industry.

A name that spells quality and value for money, Toyota enjoys a majority

market share in the highly competitive and consumer conscious UAE market. Each

Page 35 of 78

one of its wide spectrum of vehicles is a leader in its class and the first choice of

discerning consumers.

With an exhaustive range of passenger cars that is designed to satisfy every

customer and meet every possible budget, Toyota continues to dominate the UAE

roads. Be it the revolutionary Echo, sporty xA, reliable Corolla, elegant Camry, the

luxurious Avalon, the spacious Innova, the new Yaris Hatchback to the all new Yaris

Sedan, each model is a winner in its class. No need to wonder, therefore, why every

fourth passenger car in the UAE is a Toyota.

For a country that offers a unique off-road experience, Toyota has an

impressive line-up of 4 x4s. From the fun machine RAV4, to the affordable Prado, the

mighty Landcruiser and the all new Fortuner, Toyota continues to lead the way.

And that's not all. Toyota's unmatched range also includes light commercial

vehicles such as the all New HILUX pickup cabs, vans like the HIACE, and

passenger coaches like the COASTER.

Toyota engineers have worked long and hard to make the year all models

even better (a difficult job by any standards). It is this level of dedication that gives

Toyota such a strong, competitive edge. A wide choice of models which meet every

individual requirement, superior technological features and specifications, high

quality, low overall cost of ownership and legendary resale value make every Toyota

a sound investment.

Al-Futtaim Motors is the largest distributor of automobiles and automotive

products in the Emirates, with fully computerized showrooms plus fully-equipped

service workshops and parts facilities in every emirate.

An aggressive Customer Satisfaction programme, designed to enhance our

service levels right across the company, from showroom to workshop, continues to

foster Customer relationships. Our ultimate goal is to consolidate our position as the

number one distributor in the UAE by achieving new standards in customer

satisfaction.

Page 36 of 78

4.6.1 Auto sector poised to rise by 5pc in the UAE

Auto sales in the UAE are expected to rise 5 per cent between 2009 and 2010

as an easing in liquidity conditions boosts confidence in the sector, according to an

analysis by the Dubai Chamber.

A general high-level of disposable income and renewed consumer confidence

in the UAE on the back of easing liquidity conditions, provides a favourable

background for the auto sector in the coming months. Furthermore, plans for a car

production plant in the UAE could help initiate a local automotive manufacturing

industry.

Since the UAE is the fastest growing auto market in the Middle East, the

sector is in a position to expand with preliminary plans for a car production plant to

help spawn a local auto manufacturing industry already in place.

"The automotive sector was affected by the financial crisis as banks became more

cautious in granting auto loans. But with the UAE accelerating on the path to

economic recovery, banks are now being more flexible with auto financing which will

no doubt benefit the sector, fuel the demand, and ultimately increase sales, as per

Dubai Chamber Director.

The analysis disclosed that it is increasingly apparent that the UAE automotive

market is mature, with vehicle ownership rates of over 540 per 1,000 inhabitants —

a rate that exceeds most of the developing world.

Car dealers in the UAE are optimistic on the outlook for the second half of

2009 and are confident that their sales will grow though at a lower rate, in what

seems like a challenging year on the back of the global financial crisis. This is

primarily down to an easing in lending conditions with banks loosening their belts and

Page 37 of 78

imposing lowers rates and more lenient requirements on borrowers. Over 70 per cent

of new car purchases are made on credit in the UAE. Galadari Automobile's General

Manager R. Krishnan expressed a cautious optimism about the rest of 2009.

The combination of relatively high living standards, a growing population in

the UAE, as well as a resurgence in oil prices, have been the key driving forces

behind the growth in the auto sector in the UAE. Despite an expected slowdown in

auto sales this year, the outlook based on resurgence in consumer demand on the

back of a pick-up in the global economy is likely to lead to robust growth in 2010 and

beyond.

Whilst the UAE does not possess a sizable domestic automobile

manufacturing capability, its high national wealth has created a niche market for

sales of imported vehicles in recent years, and there is a large re-export trade based

on the country's regional status as a key strategic location, Dubai Chamber said. Car

ownership is expected to rise above 55 per cent this year for the first time in the

country's history. The analysis further revealed that though Abu Dhabi contributes

over 55 per cent to overall UAE GDP, its economy is dominated by the energy sector.

Thus, it is diversified Dubai that is experiencing the most rapid growth, and it has

taken a lead in the auto sector, accounting for nearly 50 per cent of the total vehicle

stock Khaleej Times

Page 38 of 78

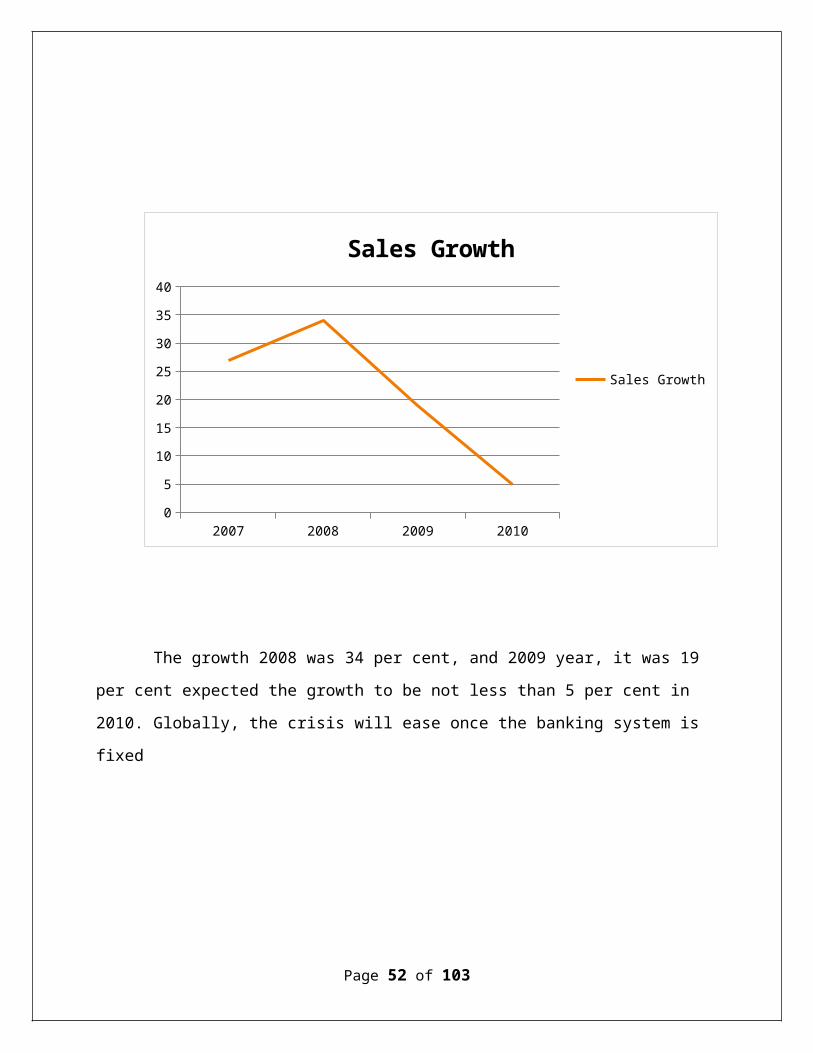

The growth 2008 was 34 per cent, and 2009 year, it was 19 per cent expected

the growth to be not less than 5 per cent in 2010. Globally, the crisis will ease once

the banking system is fixed

2007 2008 2009 20100

5

10

15

20

25

30

35

40

Sales Growth

Sales Growth

The growth 2008 was 34 per cent, and 2009 year, it was 19 per cent

expected the growth to be not less than 5 per cent in 2010. Globally, the crisis will

ease once the banking system is fixed

Page 39 of 78

4.7 JUMBO ELECTRONICS: Leader in consumer electronic products

The flagship company of the Jumbo Group, Jumbo Electronics Company Ltd. (LLC)

was founded in 1974. Jumbo is one of the leading names in the field of consumer

electronics, information technology, telecommunications, home appliances, office

automation and entertainment in the United Arab Emirates and is amongst the first

transnational corporations with a well spread out network of 30 retail stores and 9

service centres across the Emirates. Jumbos presence in the UAE encompasses the

seven Emirates of Dubai, Sharjah, Abu Dhabi, Umm Al Quwain, Ras Al Khaimah,

Fujairah and Ajman.

Jumbo is ISO 9001 certified with established systems and procedures which are

constantly tested and improved upon to best serve customer needs.

GLOBAL BRANDS A partner for the world’s leading brands, Jumbo’s extensive retail and distribution

network have made it a natural choice for manufacturers wanting to establish their

products in the growing Middle East markets. One of the largest distributors of Sony

products in the world, the company has an enviable line-up of various other

international brands in its portfolio. Jumbo is a distributor for Acer, Blackberry,

Brother, Casio, Dometic, Du, Dyson, Etisalat, Gorenje, Hewlett Packard, LG, Ricoh,

NCR, Rionet, Sennheiser, Sony, Supra, Vaio.

In addition to the above brands, the retail arm of the company also handles most of

the other well know brands including Apple, Asus, Belkin, Bit Defender, Buffalo,

Cisco, Compaq, Dell, Fujitsu, Garmin, HTC, IBM, Imation, Intel, Kasperesky, Lenovo,

Page 40 of 78

Logitech, Microsoft, Mio, Motorola, Net Apps, Netgear, Nokia, Optoma, Orion,

Packard Bell, Pixel Point, Samsung, Seagate, SCR, Sony Ericsson, Toshiba,

VMWare, Western Digital, Wincor Nixdorf.

From modest beginnings in 1974, Jumbo’s remarkable progress into becoming a

consumer electronics giant has been built with an uncompromising adherence to

quality. Jumbo’s five principal divisions - Sony, Information Technology, Telecom,

Supra and Agencies Divisions - work seamlessly with channels such as the Retail

and Corporate Sales, with support from the Central Services and Logistics, to set

new benchmarks in customer service.

Global Brands

Asus Packard Bell Vaio

Gorenje Sony

Casio Brother Nokia

Sony Ericsson Ricoh Hewlett-Packard

Page 41 of 78

Acer Toshiba Apple

Current Scenario in the Consumer Electronic Market - Analysis

The UAE is not only a leading market for consumer electronic products in the

neighboring region extending from the Indian sub-continent to East Europe, but is

also an important trading sector in the domestic non-oil economy. The total turnover

of the consumer electronics market is estimated to be almost US$2.9 billion. Most of

the demand for consumer electronics is from outside the domestic market, viz. re-

exports, tourists and travelers.

Consumer electronics trade is usually understood to include watches, still

cameras and household electrical appliances (white goods). However, the largest

amount of business is conducted in audio/visual products (brown goods), which

account for about 60-65 per cent of business. White goods being bulky do not enjoy

the same ease of transport as the former, and consequently do not have the same

re-export and "carry" potential as brown goods. The largest proportion of sales of

electronics items are "carry" sales, namely sales in the domestic market which are

"carried" by individual travellers out of the country. Industry sources estimate such

sales to have an almost 40 per cent share in sales. Such sales are known as semi-

wholesale, as "carry" individuals make dedicated trips for the purpose of purchase of

electronics, and purchase significant quantities.

Pure domestic sales are around 40 per cent as well. Mostly retail, these are for

local consumption by residents and those purchased by expatriate residents as gifts

etc. on home leave. Pure domestic demand is in fact very low, considering that the

market is already saturated. According to a report in early nineties, 90 per cent and

70 per cent of the households owned a television and Video Cassette Recorder

respectively. Only about 20 per cent of sales are officially registered direct re-exports.

The re-export markets which developed in the 70s were Iran, India and Eastern

Africa. Iran is still the most important official re-export market for the United Arab

Page 42 of 78

Emirates. East Europe and particularly the CIS were an important addition since

1989 onwards. The entry of buyers from these markets has significantly lifted the

annual volume turnover of the electronics market by up to as much as 20-25 per

cent.

UAE leading Distributors

Page 43 of 78

5.1 CALSSIFICATION OF TRADING PARTNERS IN CONSUMER GOODS INDUSTRY –REATAIL SECTOR

The UAE has been ranked eighth among the top 15 most international retail markets,

with 41 per cent of international retailers present in the emirate. The global footprint

of 250 of the world's top retailers revealed that the UAE is now ranked among the top

international retail destinations ahead of countries such as china, Singapore, Russia,

us and the Netherlands. Retailing in the UAE has changed beyond recognition in

recent years with the emergence of some of the most high-profile retail developments

anywhere in the world.

According to our latest research report "Booming Retail Sector in UAE",

offering huge potential for retail developments, the UAE is gradually becoming hub

for international retail giants. In the tough post-recession scenario, when prominent

retail markets around the world are struggling to survive, UAE retail sector has

continued to record a reasonable growth. The report projects that the retail sales in

the country are expected to remain intact and will achieve one of the highest CAGR

globally in coming years.

The report reveals that rapid development in country's modern retail

infrastructure is luring consumers for convenient shopping experience, thereby

leading to increased retail spending.

In view of the study of consumer goods industry retail outlet playing a major

role in sales and marketing.

Page 44 of 78

5.2 EMKE Group is an Abu Dhabi

The company with interests in retail shopping and other businesses, EMKE

are the developers of several supermarkets, hypermarkets, and shopping centers in

Abu Dhabi and elsewhere in the UAE and other countries in the GCC region.

Turnover of more than $2.1 billion (AED 7.7 billion) in 2008 Previous figures

(unconfirmed) $1.2 billion in 2005, $1.4 billion in 2006, $1.14 billion in 2007.

5.2.1EMKE Group shopping centers and hypermarkets in the UAE

Lulu's supermarkets and hypermarkets - in all seven emirates (Abu Dhabi,

Ajman, Dubai, Fujairah, Ras Al Khaima, Sharjah, Umm Al Quawain) and other GCC

countries. A total of 75 with the opening of one in Al Ain in August 2009.

a. Al Falah Plaza, Abu Dhabi

b. Al Raha Mall, Abu Dhabi, open 2007

c. Al Wahda Mall, Abu Dhabi, open 2007

d. Emirates General Market, Abu Dhabi

e. Khalidiyah Mall, Abu Dhabi, open 2008

f. Madinat Zayed Mall

g. Mazyad Mall, Mussafah, Abu Dhabi, open 2009

h. Lulu Center

i. Lulu Express - smaller versions of Lulu

Hypermarkets (there's one in the new Mazayad

shopping mall in Mussaffah)

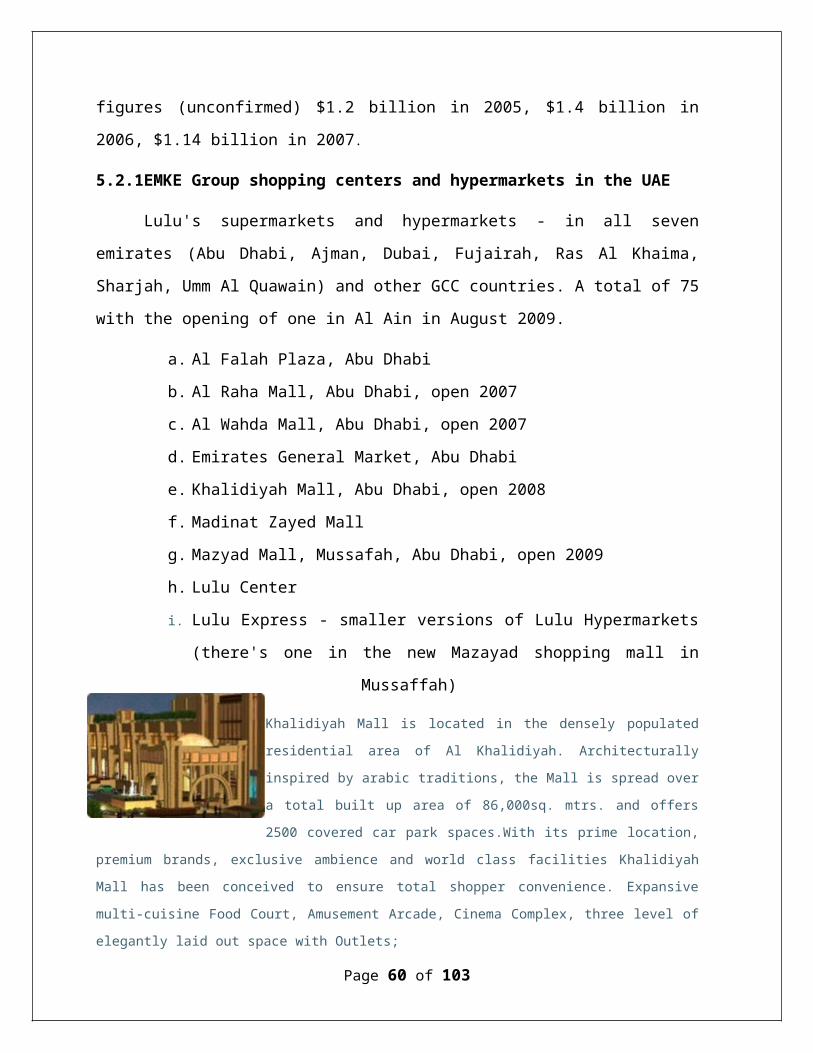

Khalidiyah Mall is located in the densely populated residential area of Al

Khalidiyah. Architecturally inspired by arabic traditions, the Mall is spread

over a total built up area of 86,000sq. mtrs. and offers 2500 covered car

park spaces.With its prime location, premium brands, exclusive ambience and world class facilities

Khalidiyah Mall has been conceived to ensure total shopper convenience. Expansive multi-cuisine

Food Court, Amusement Arcade, Cinema Complex, three level of elegantly laid out space with Outlets;

everything combines with Khalidiyah Mall to give the shoppers a uniquely

Page 45 of 78

Al Wahda Mall, located in Airport road besides the famous Al

Wahda Sports and Cultural Club stands in an area of 1.5 million

square feet and houses 152 brands, a 200,000 square feet Lulu

Hypermarket, the biggest in the city and 9 levels of covered

parking. It opened to the public on the 31st of May 2007.

5.3 Abu Dhabi Co-op Supermarkets

Year 1981, UAE saw the birth of a retailing revolution through the inception of

the first 'Abu Dhabi Co-op' supermarket. Seven committed professionals put together

their efforts to see through a 30,000sqft. supermarket and little did they know this

odyssey would turn to a $30 billion organization, employing 2,200 professionals with

primary interests in Hypermarkets, Supermarkets, Shopping malls, Retail parks &

Franchise operations.

Currently the Company is diversified into various business segments. Some

are Supermarkets, Hyper markets, Consumer goods, Distribution, Real estate,

Franchise for International Brands, Electronics Superpark, Infotech, Share

Investments and Imports.

At Abu Dhabi Co-op, customer find quality products at a reliable price. As a

leading super market chain, we provide almost all products available in the market.

We are associated with Consumer Co-operative Union of UAE, a volountery

consumer protection organization. There is a wide range of fast moving items are

made available across UAE by the union through its band name "CO OP". You may

find the product range associated with CO-OP brand here. Supermarket &

Hypermarkets

With Ten branches in Abu Dhabi and an annual turnover of Dhs. 750 Million,

Abu Dhabi Co-operative Society is the No. 1 retail chain in Abu Dhabi commanding

43% share of the retail market. Abu Dhabi Co-operative Society has retail operations

Page 46 of 78

spanning through 1.5 million sqft. The most recent Megamart Hypermarket chain is

Abu Dhabi Co-op's retail arm in emerging markets with two stores, one in Sharjah

and the other in Al Ain. Abu Dhabi Co-op is a part of the Consumer Co-operative

Union, which is also the governing body for the various Co-operatives in the UAE.

Retail Park

Mina Center the first retail park in the Middle East is established around the

principal of large retail concepts under one roof established a little away from the

hush and rush of the city. Similar to retail parks in the west, Mina Center offers

serious shopping through large concept stores offering no-frill value bargains on

reputed brands from reputed resellers.

Shopping Malls

Mina Center, Sharjah Mega Mall & Abu Dhabi Co-op shopping centers are

state of the art shopping malls of the group. Well laid out leisure and shopping

destinations the shopping malls houses reputed global retail concepts.

Franchise Operations

2XL French furnishing and home decor concept Abu Dhabi Co-op represents

the concept in the Middle East as the Master Franchisee for the French furnishing

concept XXL. 2XL offers radical design driven furnishing concepts through state of

the art stores spanning 60,000sqmtr

Page 47 of 78

5.4 Majid Al Futtaim Retail (Carrefour)

Recognized as one of the most active shopping concept developers

throughout the region, the Group first introduced the hypermarket model to the

Middle East in 1995. Majid Al Futtaim Retail manages Majid Al Futtaim

Hypermarkets, a joint venture company with the world’s second largest retailer

Carrefour, and offers shoppers the same quality, variety and value-for-money that

have made the brand a household name to millions over the world.

In the last 3 years, Majid Al Futtaim Hypermarket has opened 14 new Stores.

In the expansion of Carrefour across the region currently there are 37 hypermarkets

in the Middle East. In the coming year of 2010, Majid Al Futtaim Retail expects to

open 10 new stores.

Carrefour reputation has been built, above all, on the quality and freshness of

the products, customer service and competitive prices. Selling goods with quality

choices in food, personal care, communication, leisure, entertainment and household

goods while continually meeting the needs of local consumers in 2009, with the

ranging from needed to refrigerate food to clothes under one roof, is trendy as

shoppers pick specialized stores. Carrefour’s own retail brands are a significant

Page 48 of 78

medium for brand differentiation and customer loyalty, contributing substantially to

the organization’s growth in sales

Majid Al Futtaim Retail is honored to share the experience of Carrefour

growing with more than 13000 Employees from more than 50 different nationalities in

11 countries.

5.5 SPINNEYS DUBAI LLC

Spinney’s is one of the best known supermarket groups in the Middle East. It’s

particularly popular with British expatriates because it stocks Waitrose products.

1995 Spinney’s acquired Fine Fair Commercial Complexes, built Ramada

Supermarket & a brand new distribution center at Al Quoz. In 1997 Spinney’s center

in Umm Sequim was opened. In 1999 Spinney’s Ghubaiba was acquired from First

choice & closed its Qassimia Supermarket.

In April 1999, Ali Albwardy took 100% ownership of the Spinneys Dubai

Group.

Spinney’s group today is involved in distribution and marketing of consumer

goods and liquor products, supermarket retailing, food services, and exports of

consumer products. The group's activities extend to the entire UAE which includes

Dubai, Abu Dhabi, Sharjah, Ajman, Umm AI Qwain, Ras Al Khaimah and Fujairah.

The company operates nine supermarkets in Dubai and four in Sharjah. The

largest is at the Mercato Centre with 40,000 sq ft.area.

Spinneys imports a large proportion of its retail products and a state-of-the-art

computer system has been installed to facilitate point of sale scanning and to provide

sales and stock data.

Page 49 of 78

The retail stream of the company expects the fastest growth in future

Consumer Products Distribution & Marketing

Examples of brands represented:

Nestle -Nescafe, Nido, Maggi, Libby's, Rowntree Mackintosh etc

Kraft –Cheeses, Colgate -Toothpaste, toiletries etc,

Reckitt & Coleman,-Dettol, Pif Paf etc

Kimberly Clark -Kleenex, Huggies, Kotex etc

Nabisco -Biscuits, Jellies, Angliss Pacific -QBB Ghee

5.6 Choithram Supermarkets

Choithram Supermarket and Department Store is the best example for the

retail and whole sales sector of consumer goods industry

In UAE Choithrams have come up in convenient locations across the seven

Emirates. With its unbeatably high standard of quality and service, Choithrams has

become a name synonymous with excellence in the region today.

True to its mission of absolute customer satisfaction, Choithrams provide the

freshest fruit and vegetables and quality meats. The variety of wholesome seeded

breads, light creamy cakes and croissants are baked in store every day. And the

readymade chilled and hot meals are a great relief to a growing number of customers

who are always on the go.

The efficiency of the chain was recognized when Choithrams was awarded the

first ever "Grocer of the year" RetailME award in 2005, for overall excellence in the

Page 50 of 78

field of food retailing. It was a true testament to the competence of Choithrams in

successfully catering to the needs of a diverse population.

Choithrams- a successful enterprise

Choithrams is today a successful group with associates in diverse fields like

wholesaling, commodity brokerage, and manufacturing of edible and non-edible

items. This rich association brings to the group a huge bank of experience and

resources. Choithrams came to UAE in 1974 and has grown to a retail chain with

over 25 supermarkets in the emirates.

Choithram Supermarkets is the face of a large and successful network of

companies, T. Choithram & Sons. T. Choithram & Sons was establised in 1944 in

Sierra Leone, West Africa. Since then, it has developed into an international

company spanning Europe, North America, Africa as well as the Gulf, and remains a

private business. The trust funds and manages a group of schools and hospitals in

India and West Africa.

It was in the 70's that Choithrams came to the Gulf countries namely UAE,

Oman, Bahrain and Qatar. It brought with it international expertise, experience,

networks and communication built over 60 years in 25 countries.

Since then there has been no looking back and Choithrams is today a trusted

name and a significant contributor to the fast paced economic and social growth of

the Gulf region.

Page 51 of 78

6. Supply chain management

Supply chain management (SCM) is the management of a network of

interconnected businesses involved in the ultimate provision of product and service

packages.

Design, planning, execution, control, and monitoring of supply chain activities

with the objective of creating net value, building a competitive infrastructure,

leveraging worldwide logistics, synchronizing supply with demand, and measuring

performance globally.

In consumer goods industry SCM is the core factor to mobilize industry which

determine the growth of the market. Its make the consumer goods are turning to

consultancies to help reduce sales losses and cope with high growth by creating so-

called supply chain management networks. The primary intention of SCM is that the

product should reach the to customer in least time. Therefore SCM in basic

requirement of any industry to grab their position in the market.

Page 52 of 78

7.1. INDUSTRIAL FORECAST SCENARIO

MACROECONOMIC FORECAST:

Downturn Raises Employment Questions

We are forecasting recession for the UAE in 2009, with lower oil prices-

and reduced investment spending two of the key culprits. The downturn will bring

employment regulations to the fore, as the government balances the need to

encourage continued immigration while protecting the employment of UAE citizens.

While recently released figures from the Ministry of Economy confirmed the

UAE's strong economic expansion in 2008, we believe that government bullishness

regarding the effectiveness of its fiscal rescue package is somewhat misplaced. We

remain bearish regarding the country's growth prospects this year; indeed we are

now forecasting an outright recession, with the economy expected to contract by

1.7%. In our view, government spending will limit the downside and stave off job

losses in key sectors, but will not be sufficient to fully counteract the contraction in

trade volumes, the slowing of consumer spending on the back of population losses

and the severe cutting back of investment plans.

GOOD TIMES ARE PAST

A recent statement by Sultan bin Saeed aI-Mansouri, the UAE Minister of Economy,

put real GDP growth at 7.4% in 2008, slightly above our 6.9% estimate for the year.

While we are still awaiting a full breakdown of GDP by expenditure from the ministry

or the central bank, the minister's statement confirmed a number of key trends that

we were following throughout the year. Most important of these was the surge in oil

revenues as prices peaked in the middle of the year. Overall, the contribution of the

oil sector to GDP rose from 35.9% in 2007 to 37.9% in 2008. The second trend was

the sharp upswing in investment spending,much of which was ploughed into real

estate developments. Both these trends have already witnessed a sharp reversal. On

Page 53 of 78

the oil front, we recently raised our forecast average annual price to US$45.50/bbl for

the OPEC Basket in 2009, up from our previous figure of US$39.50/bbl. However,

this is still less than half of the 2008 average of US$95.40/bbl. Oil prices are likely to

creep up again as global demand recovers in the second half of this year and from

2010 onwards, but we believe a return to 2008 levels is unlikely in the foreseeable

future. Even by 2012, we are forecasting an average price of DS$71.50/bbl, broadly

on a par with 2007.

Lower oil prices, combined with stricter lending requirements by banks and

greater caution among investors whose fingers have been burned (or are still

getting burnt) by the collapse in real estate prices will also translate into less

exuberant investment plans. We see real growth in gross fixed capital formation

(GFCF) remaining in single digits over the next two to three years, rather than the

rates of 15-20% (or likely even higher in 2008) seen over the past three, as plans

for many real estate projects are shelved, others are scaled back and the

government begins to play more central role in infrastructure development.

ACKNOWLEDGING THE PROBLEM

While the economy ministry is painting a bullish picture, comments from

elsewhere in the ruling elite suggest that the government does recognise the

magnitude of the challenges facing the DAE economy this year. In mid-March, the

central bank governor, Sultan bin Nasser al-Suweidi, admitted that growth was likely

to slow to low single digits, or could even turn negative, this year. He promised

interest rate cuts to stimulate growth, although as is the case around the world, the

real problem is translating central bank cuts into lower market rates for consumers

and businesses. At the time of writing, the DAE interbank offered rate (AEIBOR)

stood at 2.9188%, compared with a central bank repo rate of 1 %

Another key area where the government is sitting up and taking notice is population

growth. We have long argued that a steady expansion of the population is essential

to the UAE's growth plans. Immigration, by both highly skilled white collar workers

Page 54 of 78

and unskilled laborers, has fuelled the country's recent boom. Highly skilled

migrants have brought experience and expertise in key non-oil sectors such as

financial services and construction, while laborers from south Asia have provided

the manpower for the bulk of construction projects. On top of this, steady population

expansion has driven increases in consumer spending and fuelled demand for

housing, particularly in Dubai, the first Emirate to allow foreign ownership of

property.

With many construction sites now lying untouched, large numbers of laborers

have lost their jobs and redundancies have spread to office workers in the real

estate and financial sectors. With most visas for foreign workers tied to

employment, those that lose their jobs often have only a few weeks in which to find

new employment before being forced to leave the country. The scale of recent

emigration is unknown; the ministry of labour has insisted that thousands of new

work permits are still being issued, although it is not clear what proportion of these

are simply renewals of existing permits.

In 2009, we are currently forecasting a 1% contraction in the total population

to 4.67mn. However, the government is reportedly re-examining its immigration

regulations, with a view to making it easier for unemployed expatriates to remain in

the country while they search for new jobs. Without changes to the current system,

Dubai - probably the Emirate most reliant on foreign labour - has little chance of

achieving its 3% workforce growth target in 2009 (even with these changes, we

think this figure is optimistic).

EMPLOYMENT NATIONALISM

But at the same time as it tries to retain foreign workers, the UAE is also

keen to shield its native population from the Impact of the economic downturn.

Dubai recently launched another 'Emiratisation' drive, aimed this time at increasing

the proportion of UAE citizens employed in the public sector (previous initiatives

have tended to focus on encouraging private firms to take on more local staff).

Page 55 of 78

Recent research by the UAE University found that among over 120 private

firms surveyed, less than 1% of their employees were Emirati. Figures were much

higher in the public sector, but still not high enough according to Sheikh Mohammed

bin Rashid, ruler of Dubai and the UAE's Prime Minister. Just 25% of staff at federal

authorities, and barely more than half of those employed in ministries, are UAE

citizens.

The poverty that often accompanies unemployment is not such an issue in

the UAE - the. government has always provided its citizens with a generous range

of welfare benefits, ranging from free education and healthcare to subsidised land

and loans for house building. That said, with a young population, providing enough

jobs is still a concern and job losses among Emirati staff will always be unpopular,

particularly when there are still large numbers of foreign workers still employed in

the UAE. However, until now the government has tried to tread carefully. Rules on

emiratisation have not been strictly applied, as the state recognised the tradeoff

between boosting domestic employment levels and remaining competitive.

UAE - ECONOMIC ACTIVITY :

Table: UAE - Economic Activity 2005 2006 2007 2008 2009 2010 2011 2012 2013Nominal GDP, AEDbn 485.5 624.6 729.7 855 833.8 939.8 1,085.4 1,238.2 1,351.9Nominal GDP, US$bn 132.20 170.10 198.70 268.10 227.00 255.90 295.60 337.20 368.10Real GDP growth, % change y-o-y 8.2 6.6 5.2 6.7 -1.7 3.9 4.8 3.9 5.3GDP per capital 32,197 40,218 44,254 56,858 48,643 53,753 59,694 65,480 68,740Population,mn 4.10 4.0 4.50 4.70 4.70 4.80 5.00 5.10 5.40

Page 56 of 78

8. SWOT ANALYSIS

Swot Analysis is a strategic planning method used to evaluate the

Strengths, Weakness, Opportunities and Threats involved in a project or in a

business venture. It involves specifying the objective of the business venture or

project and identifying the internal and external factors that are favourable and

unfavourable to achieving that objective. The technique is credited to Albert

Humphrey who led a research project at Stanford University in the 1960s and 1970s

using data from Fortune 500 companies. The Fortune 500 is an annual list compiled

and published

By Fortune magazine that ranks the top 500 US public corporations as

measured by their gross revenue.

Strengths and Weaknesses are internal factors that create value or destroy

value. They can include assets skills or resources that a company has its disposal,

compared to its competitors. They can be measured using internal assessments or

external benchmarking.

Opportunities and Threats are external factors that create value or destroy

value. A company cannot control them. But they are emerging from either the

competitive dynamics of the industry / market or from demographic, economic,

political, technical, social, legal or cultural factors.

8.1 SWOT ANALYSIS OF CONSUMER GOODS INDUSTRY IN UAE

STRENGTH

Rising income levels, i.e. increase in purchasing power of consumers

Large domestic market- a population of over one billion.

• Export potential

Page 57 of 78

One of the largest consumer industry in the Gulf region, accounting close to

85% of regional speeding

A trading hub serving the expanding market of Saudi Arabia & Gulf as well as

further-flung regions such as East Africa

There is government support for many projects

One of the major economy of the country

Vast customer portfolio

Marketing many brands

Good will

Location of business-loccal manufacturer

Cost advantage-manufacture supplier

New and innovative products

WEAKNESS

Piracy and parallel imports. Country’s low trade barrier contribute to a

growing problem with counterfeit or grey market goods

Regional economy very dependent on oil, despite diversification effort

in many sectors

Lack of product awareness with European consultants

Lower scope of investing in technology and achieving economies of

Page 58 of 78

scale, especially in small sectors

Low exports levels

OPPORTUNITIES

Fast growing consumer goods industries in UAE

Private label growth to enhance brand & margins

Vast untapped market

High income growth in GCC countries

Stable economy of UAE

Innovation of new products

Strategic alliances

A new international market

Wealthy domestic market offers continued growth potential

THREATS

Recession - seriously affected the construction industry all over the

world.

Decreasing petroleum products price.

Rising commodity & shipping prices

Cut- throat competition.

Non availability of reliable trade partners.

Page 59 of 78

Non availability of qualified and experienced staff.

Entry of new foreign competitors.

8.2 UAE ECONOMIC SWOT

STRENGTH

UAE is a member of GCC which as well as being a common market, is

targeting a common currency by 2012(although UAE looks, at present, unlikely to

participate)

UAE has one of the most liberal trade regimes in Gulf and aattracts

strong capital flows across the region

In common, with most gulf states, there are high number of experienced

workers at all levels of economy

UAE is progressively diversifying its economy, minimizing vulnerability

to oil price movements

WEAKNESS

UAE’s currency is pegged to dollar giving it minimal control over

monetary policy and reducing the ability to tackle inflatory pressure

Page 60 of 78

The state’s location in a volatile region means that its risk profile is to

some extent, affected by US concerns about regional militant groups and Iranian

WMD programmes could affect investor perceptions

OPPORTUNITIES

Oil prices are expected to stay high over forecast period

Economic diversification into gas, tourism, financial services & high tech

industry offers some protection against volatile oil prices

The construction, tourism and financial sectors are growing rapidly

driven by domestic and foreign investments

THREATS

Heavy subsidies on utilities and agriculture and an outdated tax system

have contributed to persistent fiscal deficits in the past,although rising oil revenues

have masked the problem in recent years