general ledger and reporting system uaa – acct 316 accounting information systems dr. fred barbee

TRANSCRIPT

General Ledger and Reporting System

UAA – ACCT 316 Accounting Information Systems Dr. Fred Barbee

General Ledger and Reporting Activities

Objectives

1. To record all accounting transactions promptly and accurately.

2. To post these transactions to the proper accounts.

3. To maintain an equality of debit/credit balances among the accounts.

Objectives

4. To accommodate needed adjusting entries.

5. To generate reliable and timely financial reports pertaining to each accounting period.

Basic Activities (Processes)

1. Update the general ledger

2. Post adjusting entries

3. Prepare financial statements

4. Produce managerial reports

1. Analyze Transaction

s

2. Journalize

3. Post

4. Prepare Unadjusted

Trial Balance

5. Adjust

6. Prepare Adjusted

Trial Balance

7. Prepare Statements

8. Close

9. Prepare Post-Closing

Trial balance

10. Reverse (Optional)

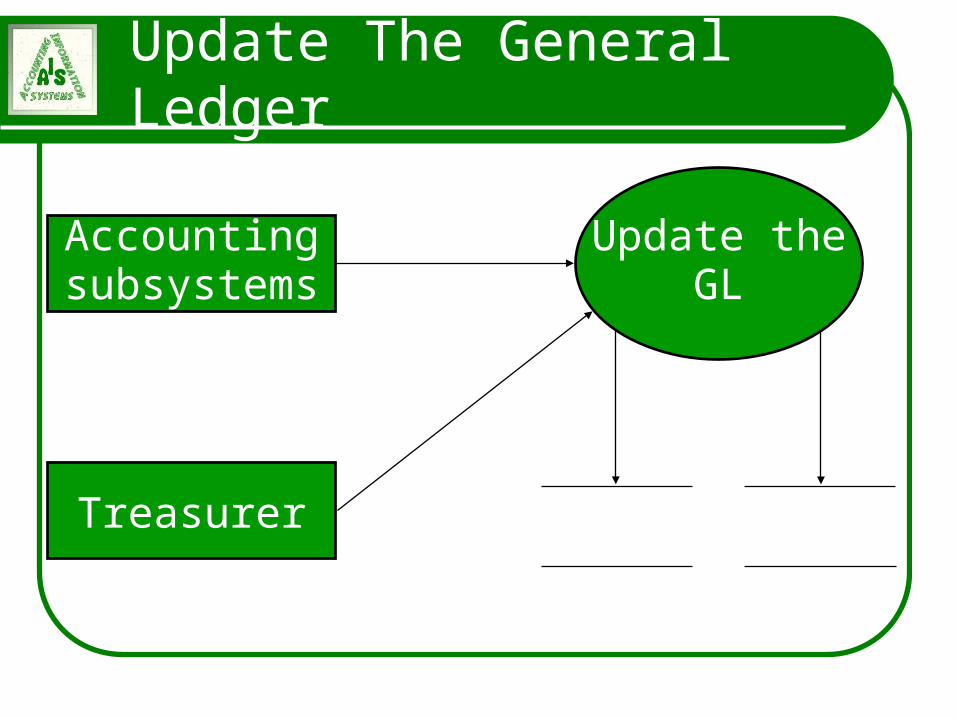

Update The General Ledger

Updating consists of posting journal entries that originated from two sources:

1. Accounting subsystems

2. The treasurer

Update The General Ledger

Accountingsubsystems

Treasurer Journal voucher

General ledger

Update theGL

Journal entry

Journal entry

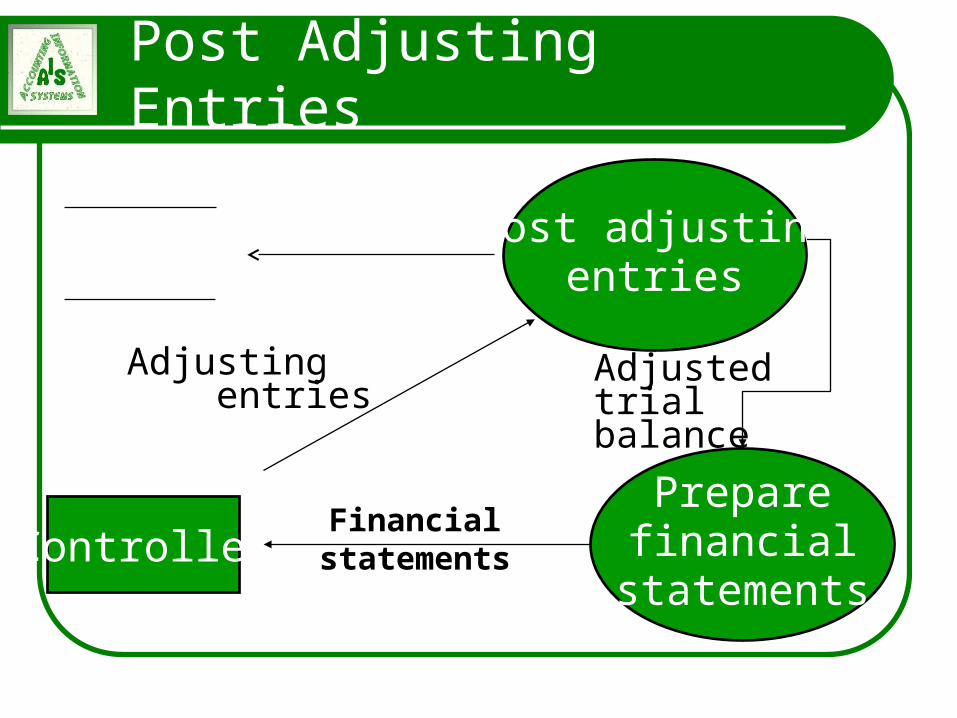

Post Adjusting Entries

The second activity in the general ledger system involves posting various adjusting entries.

Adjusting entries originate from the controller’s office, after the initial trial balance has been prepared.

Post Adjusting Entries

1. Accruals (wages payable)

2. Deferrals (rent, interest, insurance)

3. Estimates (depreciation)

4. Revaluation (change in inventory method)

5. Corrections

Post Adjusting Entries

Controller

Journal voucher

Post adjustingentries

Preparefinancial

statements

Adjusting entries

Financial statements

Adjusted trial balance

Prepare Financial Statements

The third activity in the general ledger and reporting system involves the preparation of financial statements.

The income statement is prepared first.

The balance sheet is prepared next.

The cash flows statement is prepared last.

Produce Managerial Reports

The final activity in the general ledger and reporting system involves the production of various managerial reports.

What are the two main categories of managerial reports?

1. General ledger control reports

2. Budgets

Produce Managerial Reports

Control Report Examples

– lists of journal vouchers by numerical sequence, account number, or date

– listing of general ledger account balances

Budget Examples

– operating budget

– capital expenditures budget

Produce Managerial Reports

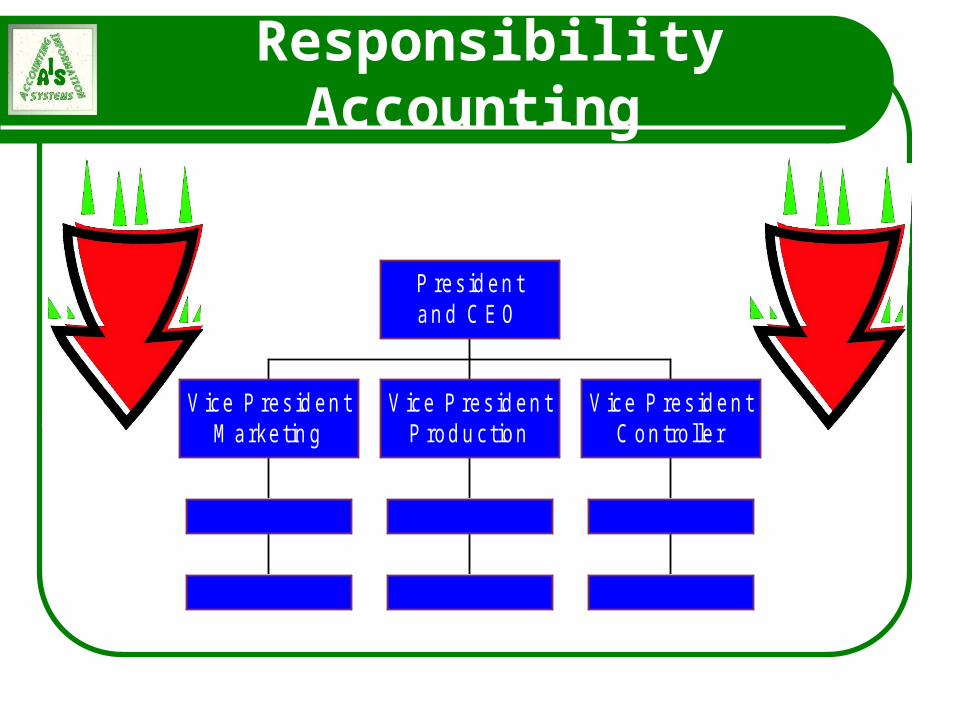

Budgets and performance reports should be developed on the basis of responsibility accounting.

Responsibility Accounting involves reporting financial results on the basis of managerial responsibilities within an organization.

Responsibility Accounting

A concept that implies that every economic event that affects the organization is the responsibility of and can be traced to an individual.

V ice P res id en tM arke tin g

V ice P res id en tP rod u c tion

V ice P res id en tC on tro lle r

P res id en tan d C E O

Responsibility Accounting

V ice P res id en tM arke tin g

V ice P res id en tP rod u c tion

V ice P res id en tC on tro lle r

P res id en tan d C E O

Installing Responsibility Accounting

Create a set of financial performance goals (budgets)

Measure and report actual performance.

Evaluate based on comparison of actual with budget.

Responsibility Accounting

Measures the results of each responsibility center and

Responsibility Accounting

compares those results with some standard or benchmark.

Heh man, that isn‘t funny! Please don’t erase that line, I’m

benchmarking!

Responsibility Centers

Responsibility Center

A segment of an organization with authority . . .

To incur and control costs

To earn revenues, and

To invest funds in assets.

Responsibility Center . . .

A responsibility center can be:

A cost center

A revenue center

A profit center

An investment center

Responsibility Centers

A Systems Perspective

A firm can be examined in the

context of Input Process Output

A firm can be examined in the

context of Input Process OutputProcessing Steps

WithinInformation Systems

Processing StepsWithin

Information Systems

Data

(Inputs)

Information

(Outputs)

DMDL

MOH

DMDL

MOH

Goods, Services,

Ideas

Goods, Services,

Ideas

WorkingCapital

EquipmentEtc.

WorkingCapital

EquipmentEtc.

Resources used . . . Capital . . . Output . . .

A firm can be examined in the

context of Input Process Output

A firm can be examined in the

context of Input Process OutputProcessing Steps

WithinInformation Systems

Processing StepsWithin

Information Systems

Data

(Inputs)

Information

(Outputs)

DMDL

MOH

DMDL

MOH

Goods, Services,

Ideas

Goods, Services,

Ideas

WorkingCapital

EquipmentEtc.

WorkingCapital

EquipmentEtc.

Resources used . . . Capital . . . Output . . .

Resources are converted through the use of working capital, equipment,

etc.

Responsibility Centers:A Systems PerspectiveResponsibility Centers:A Systems Perspective

InputInput OutputOutput Process Process

Control only this

Cost Center

Responsibility Centers:A Systems PerspectiveResponsibility Centers:A Systems Perspective

InputInput OutputOutput Process Process

Control only this

Revenue Center

Responsibility Centers:A Systems PerspectiveResponsibility Centers:A Systems Perspective

InputInput OutputOutput Process

Process

Control these

Profit Center

Responsibility Centers:A Systems PerspectiveResponsibility Centers:A Systems Perspective

InputInput OutputOutput Process

Process

Control these

Investment Center

Control Objectives, Threats & Procedures

Control Objectives

1. Updates to the general ledger are properly authorized.

2. Recorded general ledger transactions are valid.

3. Valid, authorized general ledger transactions are recorded.

Control Objectives

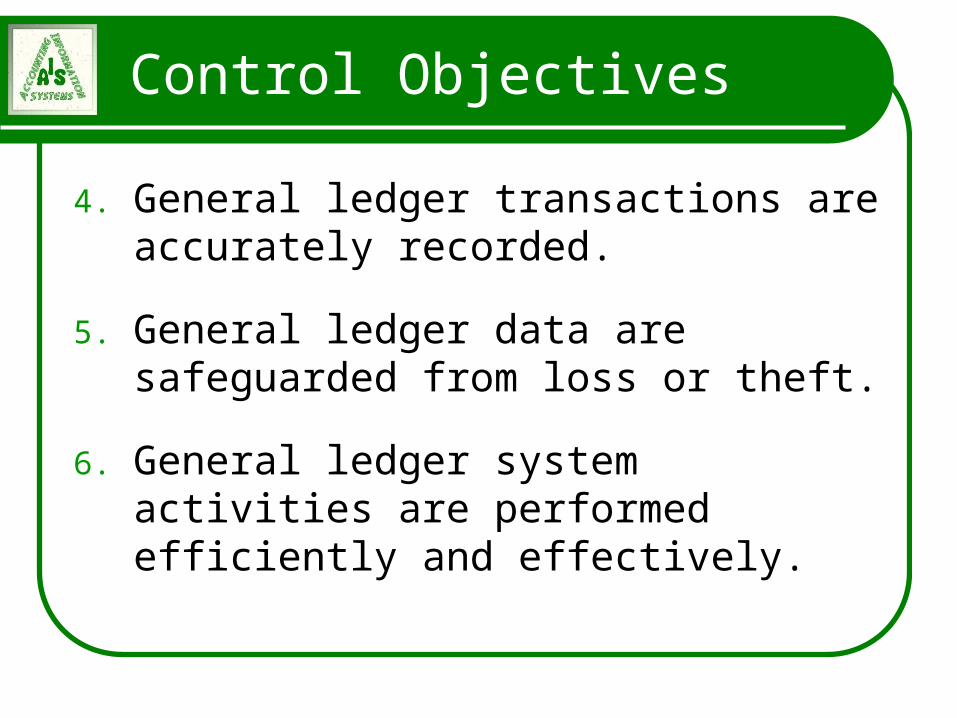

4. General ledger transactions are accurately recorded.

5. General ledger data are safeguarded from loss or theft.

6. General ledger system activities are performed efficiently and effectively.

Threats and Controls in the General Ledger and Reporting System

Process/Activity ThreatApplicable Control

Procedures

Updating the general ledger

Errors Input and processing controls; reconciliations and control reports; audit trail

Access to general ledger

Loss of confidential data and/or concealment of theft

Access controls; audit trail

Loss or destruction of the general ledger

Loss of data and assets

Backup and disaster recovery procedures

Threat 1: Errors in Updating the GL

Errors in Updating GL

Can lead to poor decision making based on erroneous information in financial performance reports.

Control procedures fall into three categories: Input edit and processing controls

Reconciliations and control reports

Maintenance of an adequate audit trail

Input Edit and Processing Controls

There are two sources of journal entries for updating the general ledger:

1. Summary journal entries from other AIS cycles

2. Direct entries made by the treasurer or controller

Input Edit and Processing Controls

Journal entries made by the treasurer and controller are original data entry.

Several types of input edit and processing controls are needed to ensure that they are accurate and complete.

Input Edit and Processing Controls

Validity Check

Field checks

Zero-balance checks

Completeness Test

Closed-loop verification

Sign Check

Input Edit and Processing Controls

Calculation run-to-run totals to verify accuracy of journal voucher batch processing

Standard adjusting entry file for recurring adjusting entries made each period

Reconciliation and Control Report

Reconciliations and control reports can detect if any errors were made during the process of updating the general ledger.

Trial Balance

Comparing the general ledger control account balances to the total balance in the corresponding ledger

Reconciliation and Control Report

The audit trail is the path of a transaction through the accounting system.

The audit trail should allow you to do three things . . .

Reconciliation and Control Report

1. Trace any transaction from its original source document to the general ledger and to any report or other document using that data.

Reconciliation and Control Report

2. Trace any item appearing in a report back through the general ledger to its original source document

3. Trace all changes in general ledger accounts from their beginning balance to their ending balance

Threat 2: Unauthorized Access to the GL

Unauthorized Access to the GL

Unauthorized access to the general ledger can result in confidential data leaks to competitors or corruption of the general ledger.

It can also provide a means for concealing the theft of assets.

Unauthorized Access to the GL

User IDs and passwords

Read-only access to the general ledger

System checks of authorization codes for each journal voucher record before posting

Threat 3: Loss or Destruction of the GL

Loss or Destruction of the GL

Adequate backup and disaster recover y procedures must be in place to protect the general ledger.

Use of internal and external file labels

Performance of regular backup of the general ledger

Integrated Data Model

Integrated Data Model

An integrated enterprise-wide data model represents a merging of separate data models.

This merging primarily involves linking each resource with the events that increase and decrease that resource.

Integrated Data Model

(1, N)

(1, 1)

Cash (1, N)

Cashdisbursements

Cashreceipts

(1, 1)

Integrated Data Model

Integrated Data Model

(1, N)

(1, 1)(1, N)

Cash

Payemployees

Issuestock

Dividendpayment

Debtpayment

Issuedebt

(1, 1)

(0, N) (0, N)

(1, 1)

(0, N)

(1, 1)

(0, N)(1, 1)

(0, N)

Integrated Data Model

Benefits of an Integrated Data Model

What are some benefits of an Integrated data model?

Improved support for decision making

Integration of financial and nonfinancial information

Improved internal reporting

Benefits of an Integrated Data Model

Development of a virtual value chain occurs in three stages.

What are these stages?

1. Visibility

2. Mirroring

3. Building new customer relationships