garch models - lth · garch (generalized arch) i is the most common dynamics variance model. i the...

TRANSCRIPT

GARCH models

Erik Lindström

FMS161/MASM18 Financial Statistics

Erik Lindström GARCH models

Time series models

Let rt be a stochastic process.I µt = E[rt |Ft−1] is the conditional mean modeled by an AR,

ARMA, SETAR, STAR etc. model.I Having a correctly specified model for the conditional mean

allows us to model the conditional variance.I I will for the rest of the lecture assume that rt is the zero

mean returns.I σ2

t = V [rt |Ft−1] is modeled using a dynamic variancemodel.

Erik Lindström GARCH models

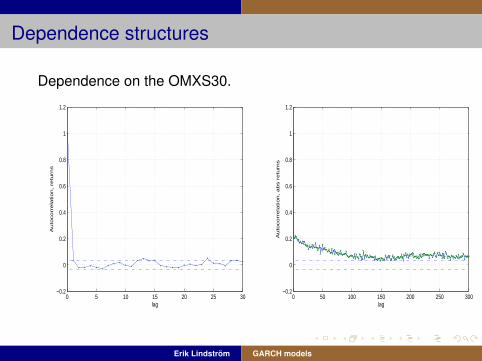

Dependence structures

Dependence on the OMXS30.

0 5 10 15 20 25 30−0.2

0

0.2

0.4

0.6

0.8

1

1.2

lag

Au

toco

rre

latio

n, re

turn

s

0 50 100 150 200 250 300−0.2

0

0.2

0.4

0.6

0.8

1

1.2

lag

Au

toco

rre

latio

n, a

bs r

etu

rns

Erik Lindström GARCH models

The ARCH family

I ARCH (1982), Bank of Sweden . . . (2003)

I GARCH (1986)

I FIGARCH (1996)

I Special cases (IGARCH, A-GARCH, GJR-GARCH,EWMA)

I EGARCH (1991)

I SW-GARCH

I GARCH in Mean (1987)

Erik Lindström GARCH models

ARCH

The ARCH (Auto Regressive Conditional Heteroscedasticity)model

I The (mean free) model is given by

rt = σtzt ,

I The conditional variance is given by

σ2t = ω +

p

∑i=1

αi r2t−i

I Easy to estimate as σ2t ∈Ft−1!

I Q : Compute cov(rt , rt−h) and cov(r2t , r

2t−h) for this model.

Erik Lindström GARCH models

ARCH, solution

I We have that E[rt ] = E[E[σtzt |Ft−1]] = E[σtE[zt |Ft−1]] = 0.I Next, we compute Cov(rt , rt−h)) as

E[σtztσt−hzt−h] = E[E[σtztσt−hzt−h|Ft−1]] =

E[σtσt−hzt−hE[zt |Ft−1]] = 0.

I Computing Cov(r2t , r

2t−h) is harder. Introduce νt = r2

t −σ2t

(white noise!). It then follows that

r2t = σ

2t + νt = ω +

p

∑i=1

αi r2t−i + νt .

The r2t is thus a . . . . . . . . . process (with heteroscedastic

noise).

Erik Lindström GARCH models

ARCH, limitations

I Large number of lags are needed to fit data.I The model is rather restrictive, as the parameters must be

bounded if moments should be finiteI (Exercise: Compute the restrictions for the ARCH(1) model

to have finite variance and kurtosis.)

Erik Lindström GARCH models

GARCH (Generalized ARCH)

I Is the most common dynamics variance model.I The conditional variance is given by

σ2t = ω +

p

∑i=1

αi r2t−i +

q

∑j=1

βjσ2t−j

I A GARCH(1,1) is often sufficent!I Conditions on the parameters.

Erik Lindström GARCH models

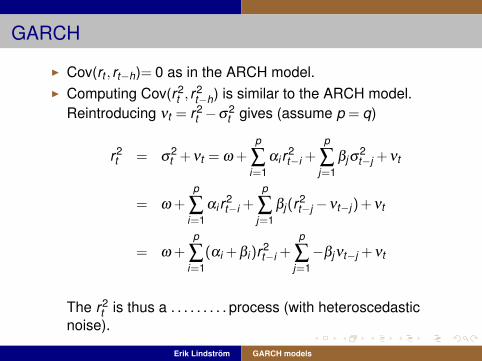

GARCH

I Cov(rt , rt−h)= 0 as in the ARCH model.I Computing Cov(r2

t , r2t−h) is similar to the ARCH model.

Reintroducing νt = r2t −σ2

t gives (assume p = q)

r2t = σ

2t + νt = ω +

p

∑i=1

αi r2t−i +

p

∑j=1

βjσ2t−j + νt

= ω +p

∑i=1

αi r2t−i +

p

∑j=1

βj(r2t−j −νt−j) + νt

= ω +p

∑i=1

(αi + βi)r2t−i +

p

∑j=1−βjνt−j + νt

The r2t is thus a . . . . . . . . . process (with heteroscedastic

noise).

Erik Lindström GARCH models

Estimation of GARCH(1,1) on OMXS30 logreturns

ω = 1.9 ·10−6, α1 = 0.0775 β1 = 0.9152

2000 2010

−0.05

0

0.05

0.1

OMXS30 logreturns

2000 2010

0.01

0.015

0.02

0.025

0.03

0.035

0.04

Extimated GARCH(1,1) vol

2000 2010

−4

−2

0

2

4

OMXS30 normalised logreturns

−4 −2 0 2 4

0.0010.0030.01 0.02 0.05 0.10 0.25 0.50 0.75 0.90 0.95 0.98 0.99

0.9970.999

Data

Pro

ba

bili

ty

NORMPLOT OMXS30 normalised logreturns

Erik Lindström GARCH models

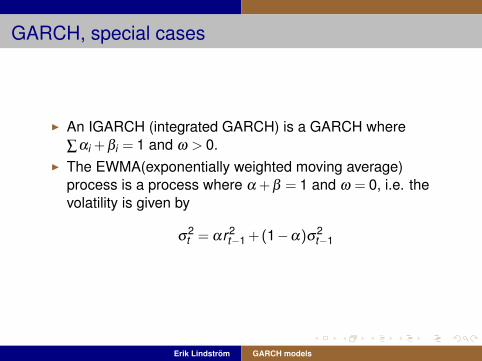

GARCH, special cases

I An IGARCH (integrated GARCH) is a GARCH where∑αi + βi = 1 and ω > 0.

I The EWMA(exponentially weighted moving average)process is a process where α + β = 1 and ω = 0, i.e. thevolatility is given by

σ2t = αr2

t−1 + (1−α)σ2t−1

Erik Lindström GARCH models

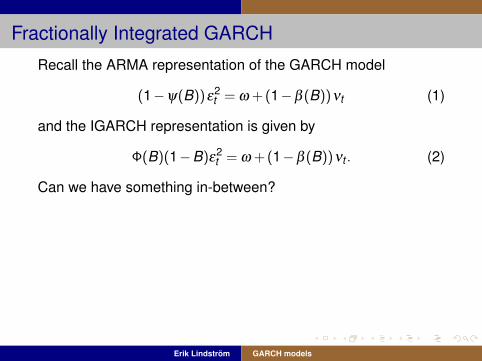

Fractionally Integrated GARCH

Recall the ARMA representation of the GARCH model

(1−ψ(B))ε2t = ω + (1−β (B))νt (1)

and the IGARCH representation is given by

Φ(B)(1−B)ε2t = ω + (1−β (B))νt . (2)

Can we have something in-between?

Yes, that is the FIGARCHmodel

Φ(B)(1−B)dε

2t = ω + (1−β (B))νt (3)

with the process having finite variance if −.5 < d < 0.5. Thefractional differentiation can be computed as

(1−B)d =∞

∑k=0

Γ(k −d)

Γ(k + 1)Γ(−d)Bk . (4)

Erik Lindström GARCH models

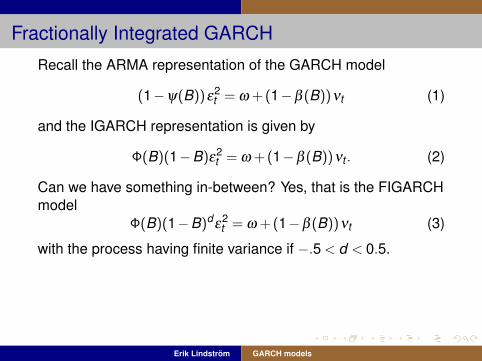

Fractionally Integrated GARCH

Recall the ARMA representation of the GARCH model

(1−ψ(B))ε2t = ω + (1−β (B))νt (1)

and the IGARCH representation is given by

Φ(B)(1−B)ε2t = ω + (1−β (B))νt . (2)

Can we have something in-between? Yes, that is the FIGARCHmodel

Φ(B)(1−B)dε

2t = ω + (1−β (B))νt (3)

with the process having finite variance if −.5 < d < 0.5.

Thefractional differentiation can be computed as

(1−B)d =∞

∑k=0

Γ(k −d)

Γ(k + 1)Γ(−d)Bk . (4)

Erik Lindström GARCH models

Fractionally Integrated GARCH

Recall the ARMA representation of the GARCH model

(1−ψ(B))ε2t = ω + (1−β (B))νt (1)

and the IGARCH representation is given by

Φ(B)(1−B)ε2t = ω + (1−β (B))νt . (2)

Can we have something in-between? Yes, that is the FIGARCHmodel

Φ(B)(1−B)dε

2t = ω + (1−β (B))νt (3)

with the process having finite variance if −.5 < d < 0.5. Thefractional differentiation can be computed as

(1−B)d =∞

∑k=0

Γ(k −d)

Γ(k + 1)Γ(−d)Bk . (4)

Erik Lindström GARCH models

EGARCH (Exponential GARCH)

I The conditional variance is given by

logσ2t = ω +

p

∑i=1

αi f (rt−i) +q

∑j=1

βj logσ2t−j

I logσ2 may be negative!I Thus no (fewer) restrictions on the parameters.

Erik Lindström GARCH models

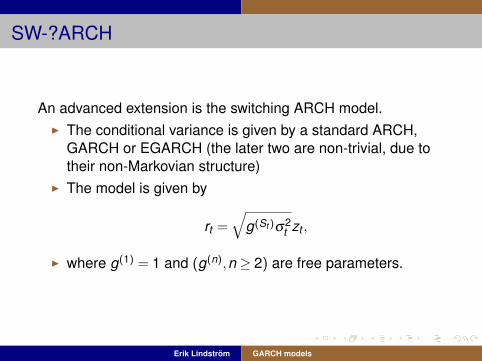

SW-?ARCH

An advanced extension is the switching ARCH model.I The conditional variance is given by a standard ARCH,

GARCH or EGARCH (the later two are non-trivial, due totheir non-Markovian structure)

I The model is given by

rt =√

g(St )σ2t zt ,

I where g(1) = 1 and (g(n),n ≥ 2) are free parameters.

Erik Lindström GARCH models

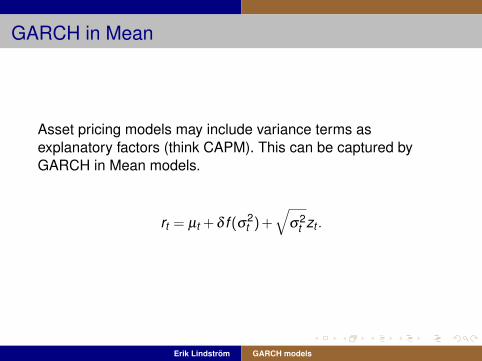

GARCH in Mean

Asset pricing models may include variance terms asexplanatory factors (think CAPM). This can be captured byGARCH in Mean models.

rt = µt + δ f (σ2t ) +

√σ2

t zt .

Erik Lindström GARCH models

Variations

Several improvements can be applied to any of the models.I Bad news tend to increase the variance more than good

news. We can replace r2t−i by

I (rt−i + γ)2 (Type I)I (|rt−i |+ cr2

t−i ) (Type II)I Replace αi with (αi + α̃i1{rt−i<0})

(GJR, Glosten-Jagannathan-Runkle).I DistributionsI Stationarity problems.

Erik Lindström GARCH models

Multivariate models

What about multivariate models?I Huge number of models.

I VEC-MVGARCH (1988)I BEKK-MVGARCH (1995)I CCC-MVGARCH (1990)I DCC-MVGARCH (2002)I STCC-MVGARCH(2005)

I Most are overparametrized.I I recommend starting with the CCC-MVGARCHI Returns: Rt = H1/2

t ZtI Ht = ∆tPc∆t where

I ∆ = diag(σt ,k )I Pc is a constant correlation matrix.

Erik Lindström GARCH models

Multivariate models

What about multivariate models?I Huge number of models.

I VEC-MVGARCH (1988)I BEKK-MVGARCH (1995)I CCC-MVGARCH (1990)I DCC-MVGARCH (2002)I STCC-MVGARCH(2005)

I Most are overparametrized.I I recommend starting with the CCC-MVGARCHI Returns: Rt = H1/2

t ZtI Ht = ∆tPc∆t where

I ∆ = diag(σt ,k )I Pc is a constant correlation matrix.

Erik Lindström GARCH models

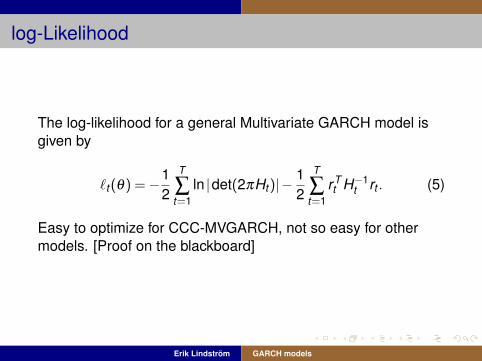

log-Likelihood

The log-likelihood for a general Multivariate GARCH model isgiven by

`t (θ) =−12

T

∑t=1

ln |det(2πHt )|−12

T

∑t=1

rTt H−1

t rt . (5)

Easy to optimize for CCC-MVGARCH, not so easy for othermodels. [Proof on the blackboard]

Erik Lindström GARCH models

Some wellknown Swedish assets

On the second computer exercise you will try to fit aCCC-MVGARCH model to this.

2005 2006 2007 2008 2009 20100

100

200

300

400

500

600

ABBAstrazeneca

B

BolidenInvestor

B

LundinMTG

B

NordeaTele2

B

Erik Lindström GARCH models