futures, forward, and option contracts section 2130 · futures, forward, and option contracts...

TRANSCRIPT

Futures, Forward, and Option ContractsSection 2130.0

2130.0.1 INTRODUCTION

Effective March 1, 1983, the Board issued anamended bank holding company policy state-ment entitled ‘‘Futures, Forward and Options onU.S. Government and Agency Securities andMoney Market Instruments.’’ Bank holdingcompanies are now required to furnish writtennotification to their District Federal ReserveBanks within 10 days after financial contractactivities are begun by the parent or a nonbanksubsidiary. The policy is consistent with thejoint policy statement previously issued by thethree federal bank regulators with regard tobanks participating in financial contracts, andreflects the Board’s judgment that bank holdingcompanies, as sources of strength for their sub-sidiary banks, should not take speculative posi-tions in such activities.If a bank holding company or nonbank sub-

sidiary is taking or intends to take positions infinancial contracts, that company’s board ofdirectors should approve written policies andestablish appropriate limitations to ensure thatthe activity is conducted in a safe and soundmanner. Also, appropriate internal control andaudit procedures should be in place to monitorthe activity. The following discussion andinspection procedures apply to futures contractactivity generally, but are intended to focus spe-cifically on financial futures contracts. For adiscussion of currency futures and options andthe examination procedures for those instru-ments, see sections F and G in the Merchant andInvestment Bank Examination Manual.Information, instructions, and inspection pro-

cedures have been provided for verifying com-pliance with the Board’s policy statement. It isintended that the policy statement will ensurethat contract activities are conducted in accor-dance with safe and sound banking practices.The task of evaluating BHC contract activitiesis the responsibility of System examiners. Thefollowing information and inspection proce-dures are intended to serve as a guide for Fed-eral Reserve Bank staff in that effort.

2130.0.2 DEFINITIONS

Basis—Basis is defined as the differencebetween the futures contract price and the cashmarket price of the same underlying security,money market instrument, or commodity.Call Option—A contract that gives the buyer

(holder) the right, but not the obligation to buy

(call), a specified quantity of an underlyingsecurity, money market instrument or commod-ity at or before the stated expiration of thecontract. At expiration, if the value of the optionincreases, the holder will exercise the option orclose it at a profit. If the value of the option doesnot increase, the holder would probably let theoption expire (or close it out at a profit) and,consequently, will lose the cost (premium paid)of (for) the option. Alternatively, the option maybe sold prior to expiration.Clearing Corporation—A corporation orga-

nized to function as the clearing house for anexchange. The clearing house registers, moni-tors, matches and guarantees trades on a futuresmarket, and carries out financial settlement offutures transactions. The clearing house acts asthe central counterparty to all trades executedon the exchange. It substitutes as a seller to allbuyers and as a buyer to all sellers. In addition,the clearing corporation serves to insure that allcontracts will be honored in the event of acounterparty default.Clearing Member—A member firm of the

clearing house or corporation. Membership inclearing associations or corporations is restrictedto members of the respective commodity ex-changes, but not all exchange members areclearing house members. All trades of a non-clearing member must be registered with, andeventually settled through, a clearing member.Commodities Futures Trading Commission—

The CFTC is a federal regulatory agencycharged with regulation of futures trading in allcommodities. It has broad regulatory authorityover futures trading. It must approve all futurecontracts traded on U.S. commodity exchanges,ensure that the exchanges enforce their ownrules (which it must review and approve), anddirect an exchange to take any action needed tomaintain orderly markets whenever it believesthat an ‘‘emergency’’ exists.Contract Activities—This term is used in this

manual to refer to banking organization partici-pation in the futures, forward, standby contract,or options markets to purchase and sell U.S.government and agency securities or moneymarket instruments, foreign currencies and otherfinancial instruments.Convergence—The process by which the fu-

tures market price and the cash market price of afinancial instrument or commodity converge asthe futures contract approaches expiration.

BHC Supervision Manual December 1992Page 1

Covered Call Options—This term refers tothe issuance or sale of a call option where theoption seller owns the underlying deliverablesecurity or financial instrument.Cross Hedging—The process of hedging a

‘‘cash’’ or derivative instrument position withanother cash or derivative instrument that hassignificantly different characteristics. For exam-ple, an investor who wants to hedge the salesprice of long-term corporate bonds might hedgeby establishing a short position in a treasurybond or treasury bond futures contract, but sincethe corporate bonds cannot be delivered to sat-isfy the contract, the hedge would be a crosshedge. To be successful, the price movements ofthe hedged instrument must be highly correlatedto that of the position being hedged.Difference Check—A difference check is sent

by the party which recognizes a loss when aforward contract is closed out by the executionof an offsetting forward contract pursuant to apair-off clause. In essence, the difference checkrepresents a net cash settlement on offsettingtransactions between the same two parties andreplaces a physical delivery and redelivery ofthe underlying securities pursuant to offsettingcontracts.Financial Contract—This term is used in the

manual to refer to financial futures, forward,standby contracts, and options to purchase andsell U.S. government and agency securities,money market instruments, foreign currencyfutures and other financial instruments.Firm Forward Contract—This term is used

to describe a forward contract under which de-livery of a security is mandatory. See ‘‘StandbyContract’’ for a discussion of optional deliveryforward contracts.Forward Contracts—Over-the-counter con-

tracts for forward placement or delayed deliveryof securities in which one party agrees to pur-chase and another to sell a specified security at aspecified price for future delivery. Contractsspecifying settlement in excess of 30 days fol-lowing trade date shall be deemed to be forwardcontracts. Forward contracts are usually non-standardized and are not traded on organizedexchanges, generally have no required marginpayments, and can only be terminated by agree-ment of both parties to the transaction. The termalso applies to derivative contracts such asswaps, caps, and collars.Futures Contracts—Standardized contracts

traded on organized commodity exchanges topurchase or sell a specified financial instrument

or commodity on a future date at a specifiedprice. While futures contracts traditionally spec-ified a deliverable instrument, newer contractshave been developed that are based on variousindexes. Futures contracts based on indexes set-tle in cash and never result in delivery of anunderlying instrument; some traditional con-tracts that formerly specified delivery of anunderlying instrument have been redesigned tospecify cash settlement. New financial futurescontracts are continually being proposed andadopted for trading on various exchanges.Futures Commission Merchant (FCM)—An

FCM functions like a broker in securities. AnFCM must register with the CommoditiesFutures Trading Commission (CFTC) in orderto be eligible to solicit or accept orders to buy orsell futures contracts. The services provided byan FCM include a communications system fortransmittal of orders, and may include researchservices, trading strategy suggestions, trade exe-cution, and recordkeeping services.Financial Futures Contracts—Standardized

contracts traded on organized exchanges to pur-chase or sell a specified security, money marketinstrument, or foreign currency on a future dateat a specified price on a specified date. Futurescontracts on GNMA mortgage-backed securitiesand Treasury bills were the first interest ratefutures contracts. Other financial futures con-tracts have been developed, including contractson Eurodollars, currencies, and Euro-Rate dif-ferentials. It is anticipated that new and similarfinancial futures contracts will continue to beproposed and adopted for trading on variousexchanges.Futures Exchange—Under the Commodities

Exchange Act (CEA), a ‘‘board of trade’’ desig-nated by the Commodity Futures Trading Com-mission as a contract market. Trading occurs onthe floor of the exchange and is conducted byopen auction in designated trading areas.GNMA or GINNIE MAE—Either term is used

to refer to the Government National MortgageAssociation. Ginnie Mae is a government corpo-ration within the U.S. Department of Housingand Urban Development. In creating GNMA,Congress authorized it to grant a full faith andcredit guaranty of the U.S. government tomortgage-backed securities issued by privatesector organizations.Hedge—The process of entering transactions

that will protect against loss through compensa-tory price movement. A hedge transaction is onewhich reduces the organization’s overall levelof risk.Initial Futures Margin—In the futures mar-

ket, a deposit held by an FCM on behalf of a

Futures, Forward, and Option Contracts 2130.0

BHC Supervision Manual December 1992Page 2

client against which daily gains and losses onfutures positions are added or subtracted. Afutures margin represents a good-faith depositor performance bond to guarantee a partici-pant’s performance of contractual obligations.Interest Rate Cap—A multi-period interest

rate option for which the buyer pays the seller afee to receive, at predetermined future times, theexcess, if any, of a specified floating interest rateindex above a specified fixed per annum rate(cap or strike rate). Caps can be sold separatelyor may be packaged with an interest rate swap.Interest Rate Collar—the combination, in sin-

gle contract, of a simultaneous sale of a cap andthe purchase of a floor, or, a purchase of a capand sale of a floor. The buyer of the collar is abuyer of a cap and the seller of a floor. Byselling the floor, the collar buyer gives up thepossibility of benefiting from a decline in inter-est rates below the strike rate in the floor compo-nent. On the other hand, the fee earned in sellingthe floor lowers the cost of protection againstinterest rate reversal.Interest Rate Floor—is the reverse of an

interest rate cap. The buyer pays a premium toobtain protection against a decline in interestrates below a specified level.Long Contract—A financial contract to buy

securities or money market instruments at aspecified price on a specific future date.Long Hedge—The long hedge, also called the

anticipatory hedgeis the process by which amarket participant protects a cash or risk posi-tion by buying a futures or forward contract, i.e.taking a long financial contract position.Maintenance Margin—Maintenance margin

is the minimum level to which an equity posi-tion can decline as a result of a price declinebefore additional margin is required. In otherwords, it is the minimum margin which a cus-tomer must keep on deposit with a member atall times. Each futures contract has specifiedmaintenance margin levels. A margin call isissued when a customer’s initial margin balancefalls below the maintenance margin level speci-fied by the exchange. Maintenance margin mustbe satisfied by the deposit of cash or agreedupon cash equivalents. The amount of cash re-quired is that amount which is sufficient torestore the account balance to the initial marginlevel.Mandatory Delivery—See ‘‘Firm Forward

Contract.’’Mark-to-market—The process by which the

carrying value (market value or fair value) of afinancial instrument is revalued, and which isrecognized as the generally accepted accountingprinciple for determining profit or loss on secu-

rities positions in proprietary trading and invest-ment accounts. Futures positions are typicallymarked-to-market at the end of each tradingsession.Naked Call Option—Refers to the issuance or

sale of a call option where the option seller doesnot own the underlying deliverable security orinstrument.Open Interest—Refers to the number of

futures contracts outstanding for a given deliv-ery month in an individual futures contracts.The mechanics of futures trading require thatfor every open long futures contract there is anopen short futures contract. For example, anopen interest of 10,000 futures contracts meansthat there are 10,000 long contract holders and10,000 short contract holders.Options Contracts—Option contracts require

that the buyer of the option pay the seller (orwriter) of the option a premium for the right, butnot the obligation, to exercise an option to buy(call option) or sell (put option) the instrumentunderlying the option at a stated price (strike orexercise price) on a stated date (European styleoption) or at any time before or on the statedexpiration date (American style option). Thereare also exchange traded options contracts:(1) put and call options on futures contracts thatare traded on commodities exchanges; and(2) put and call options that specify delivery ofsecurities or money market instruments (or thatare cash settled) that are traded on securitiesexchanges. The key economic distinctionbetween options on futures and options on secu-rities, is that the party who exercises an optionon a futures contract receives a long or shortfutures position rather than accepting or makingdelivery of the underlying security or financialinstrument.Pair-Off Clause—A pair-off clause specifies

that if the same two parties to a forward contracttrade should subsequently execute an offsettingtrade (e.g. a long contract against an outstandingshort contract), settlement can be effected byone party sending the other party a differencecheck rather than having physical delivery andredelivery of securities.Par Cap—This term refers to a provision in

the contract of sale for Ginnie Mae mortgage-backed securities which restricts delivery onlyto pools which bear an interest rate sufficientlyhigh so that the securities would trade at orbelow par when computed based on the agreedto yield.Put Option—An option contract which gives

Futures, Forward, and Option Contracts 2130.0

BHC Supervision Manual December 1992Page 3

the holder the right, but not the obligation, tosell (put) a specified quantity of a financialinstrument (money market) or commodity at aspecified price on or before the stated expirationdate of the contract. If price of the underlyinginstrument occurs, the purchaser will exercise orsell the option. If a decline in price of theunderlying instrument does not occur, the optionpurchaser will let it expire and will lose only thecost (premium paid) of (for) the option.Round Turn—Commissions for executing

futures transactions are charged on a round turnbasis. A round turn constitutes opening a futuresposition and closing it out with an offsettingcontract, i.e. executing a short contract and clos-ing out the position with a long contract orvice-versa.Short Contract—A financial contract to sell

securities or money market instruments at aspecified price on a specified future date.Short Hedge—The process by which a cus-

tomer protects a cash or risk position by sellinga futures or forward contract, i.e. taking a shortfinancial contract position. The purpose of theshort hedge is to lock in a selling price.Standby Contract—Optional delivery forward

contracts on U.S. government and agency secu-rities arranged between securities dealers andcustomers that do not involve trading on orga-nized exchanges. The buyer of a standby con-tract (put option) acquires, upon paying a fee,the right to sell securities to the other party at astated price at a future time. The seller of astandby (the issuer) receives the fee, and muststand ready to buy the securities at the otherparty’s option. See the fuller discussion ofStandby Contracts under 2130.0.3.1.2)TBA (To Be Announced) Trading—TBA is

the abbreviation used in trading Ginnie Maesecurities for forward delivery when the poolnumber of securities bought or sold is ‘‘to beannounced’’ at a later date.Variation Margin—is when, in very volatile

markets, additional funds are required to bedeposited to bring the account back to its initialmargin level, while trading is in progress. Varia-tion margin requires that the needed funds bedeposited within the hour, or when reasonablypossible. If the customer does not satisfy thevariation or maintenance margin call(s), thefutures position is closed. Unlike initial margin,variation margin must be in cash. Also refer to‘‘Maintenance Margin’’.Weighted Hedge—a hedge that is used to

compensate for a greater decline in the dollar

value of a cash bond as compared to a pricedecline of an accessible T-bond futures contract.Yield Maintenance Contract—This is a for-

ward contract written with terms which main-tain the yield at a fixed rate until the deliverydate. Such a contract permits the holder of ashort forward contract to deliver a different cou-pon security at a comparable yield.

2130.0.3 FINANCIAL CONTRACTTRANSACTIONS

Futures, forward and options contracts aremerely other tools for use in asset–liability man-agement. These contracts are neither inherentlya panacea nor a speculative vehicle for use bybanks and bank holding companies. Rather, thebenefit or harm resulting from engaging infinancial contract activities results from themanner in which contracts are used. Proper utili-zation of financial contracts can reduce the risksof interest or exchange rate fluctuations. On theother hand, financial contracts can serve asleverage vehicles for speculation on ratemovements.

2130.0.3.1 Markets and Contract Trading

Forward contract (OTC) trading of GovernmentNational Mortgage Association (‘‘GNMA’’) or‘‘Ginnie Mae’’ Mortgage-Backed Securities pre-ceded exchange trading of GNMA futures con-tracts in 1975.

2130.0.3.1.1 Forward Contracts

Forward contracts are executed solely in anover-the-counter market. The party executing acontract to acquire securities on a specifiedfuture date is deemed to have a ‘‘long’’ forwardcontract; and the party agreeing to deliver secu-rities on a future date is described as a partyholding a ‘‘short’’ forward contract. Each con-tract is unique in that its terms are arrived atafter negotiation between the parties.For purposes of illustrating a forward con-

tract, assume that SMC Corporation is an origi-nator of government guaranteed mortgages andissuer of GNMA securities. SMC Corporationhas a proven ability to manage and predict thevolume of its loan originations over a timehorizon of three to four months. To assure aprofit or prevent a loss on current loan origina-tions, SMC Corporation may enter binding over-the-counter commitments to deliver 75% of its

Futures, Forward, and Option Contracts 2130.0

BHC Supervision Manual December 1992Page 4

mortgage production which will be convertedinto GNMA securities three months in thefuture. If SMC agrees to sell $3 million ofGNMA securities (11% coupon) to the WPSecurities Firm at par in three months, SMCCorporation is considered to have entered a‘‘short’’ (commitment to sell) forward contract.Conversely, WP has entered a ‘‘long’’ (commit-ment to buy) forward contract. The two partiesto the transaction are both now obligated tohonor the terms of the contract in three months,unless the contract is terminated by mutualagreement.It should be noted that executing a ‘‘short’’

forward contract is not the same as executingthe short sale of a security. Generally, a shortsale of a security is understood to represent thespeculative sale of a security which is not ownedby the seller. The short seller either purchasesthe security prior to settlement date or borrowsthe security to make delivery; however, a‘‘short’’ forward contract merely connotes theside of the contract required to make delivery ona future date. Short forward contracts should notbe considered inherently speculative, but mustbe considered in light of the facts surroundingthe contract.Forward trading can be done on a mandatory

delivery (sometimes referred to as ‘‘firm for-ward’’ contracts) basis or on an optional deliv-ery basis (‘‘standby’’ contract). With respect toa ‘‘mandatory’’ trade, the contract can also bewritten with a ‘‘pair-off’’ clause. A pair-offclause specifies that if the same two parties to atrade should subsequently execute an off-settingtrade (e.g., the banking organization executes along contract against an outstanding short con-tract), settlement can be effected by one partysending the other party a ‘‘difference check’’rather than having a physical delivery and rede-livery of securities.When a forward contract is executed by a

dealer, a confirmation letter or contract is sent tothe other party to the transaction. The contractwill disclose pertinent data about the trade, suchas the size of the trade, coupon rate, the dateupon which final delivery instructions will beissued, and the yield at which the trade waseffected. In addition, the contract letter willspecify whether it is permissible for the ‘‘short’’side of the trade to deliver a different couponsecurity at a comparable yield (‘‘yield mainte-nance contract’’) if the coupon specified in thecontract is not available for delivery. Contractswhich prohibit the delivery of securities requir-ing a premium over par are considered to have a‘‘par cap.’’ The initial contract letter generallydoes not specify which specific securities (e.g.,

GNMA mortgage-backed securities identifiedby a pool number) will be delivered. Instead,such contracts generally identify the deliverablesecurities as having been traded on a ‘‘TBA’’basis (‘‘to be announced’’). Prior to settlement,the dealer holding the short contract will send afinal confirmation to the other party specifyingthe actual securities to be delivered, accruedinterest, dollar price, settlement date, couponrate, and the method of payment.Forward contracts are not typically marked-

to-market. Both parties in a forward contract areexposed to credit risk, since either party candefault on its obligation.

2130.0.3.1.2 Standby Contracts

Standby contracts are ‘‘put options’’ that tradeover-the-counter, with initial and final confirma-tion procedures that are quite similar to those onforward transactions. Standby contracts weredeveloped to allow GNMA issuers to hedgetheir production of securities, especially ininstances where mortgage bankers haveextended loan commitments in connection withthe construction of new subdivisions. When amortgage banker agrees to finance a subdivisionwith conventional and government guaranteedmortgages it is difficult to predict the actualnumber of FHA and VA guaranteed loans whichwill be originated. Hence, it is risky for aGNMA issuer to enter mandatory forward con-tracts to deliver the entire estimated amount ofloans eligible to be pooled as GNMA securities.By entering an option contract and paying a feefor the option to ‘‘put’’ securities to anotherparty, a GNMA issuer or securities dealer ob-tains downside market protection, but remainsfree to obtain the benefits of market apprecia-tion since it can ‘‘walk away’’ from the optioncontract. In addition to the flexibility of walkingaway and selling securities at the prevailingmarket price when GNMA prices are rising, aGNMA issuer avoids the potential risk of pur-chasing mortgages or GNMA securities to covershort forward contracts in the event that produc-tion of GNMA securities falls below anticipatedlevels.When a securities dealer sells a standby con-

tract granting a GNMA issuer the right ‘‘to put’’securities to it, the dealer, in turn, will attempt topurchase a matching standby contract from aninvestor because the dealer does not want toshoulder all of the downside market risk. There

Futures, Forward, and Option Contracts 2130.0

BHC Supervision Manual December 1992Page 5

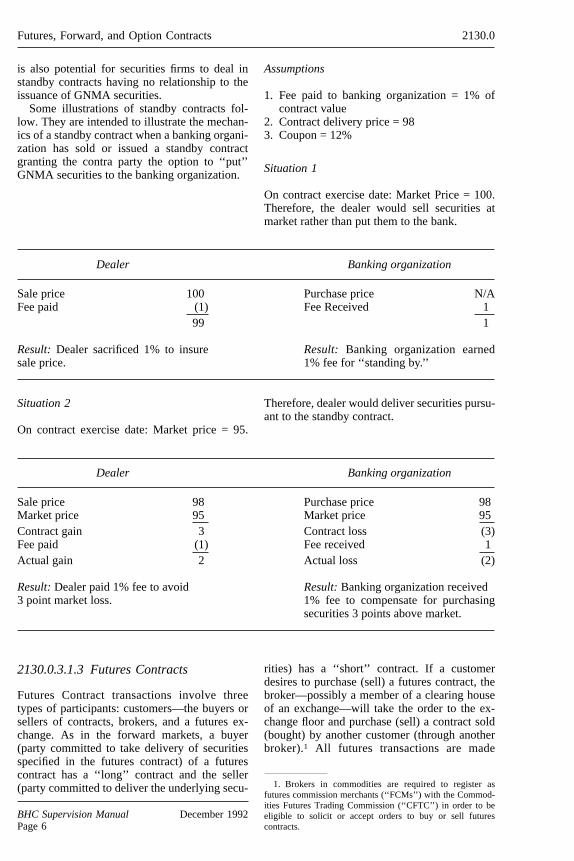

is also potential for securities firms to deal instandby contracts having no relationship to theissuance of GNMA securities.Some illustrations of standby contracts fol-

low. They are intended to illustrate the mechan-ics of a standby contract when a banking organi-zation has sold or issued a standby contractgranting the contra party the option to ‘‘put’’GNMA securities to the banking organization.

Assumptions

1. Fee paid to banking organization = 1% ofcontract value

2. Contract delivery price = 983. Coupon = 12%

Situation 1

On contract exercise date: Market Price = 100.Therefore, the dealer would sell securities atmarket rather than put them to the bank.

Dealer Banking organization

Sale price 100Fee paid (1)

99

Result:Dealer sacrificed 1% to insuresale price.

Purchase price N/AFee Received 1

1

Result: Banking organization earned1% fee for ‘‘standing by.’’

Situation 2

On contract exercise date: Market price = 95.

Therefore, dealer would deliver securities pursu-ant to the standby contract.

Dealer Banking organization

Sale price 98Market price 95Contract gain 3Fee paid (1)Actual gain 2

Result:Dealer paid 1% fee to avoid3 point market loss.

Purchase price 98Market price 95Contract loss (3)Fee received 1Actual loss (2)

Result:Banking organization received1% fee to compensate for purchasingsecurities 3 points above market.

2130.0.3.1.3 Futures Contracts

Futures Contract transactions involve threetypes of participants: customers—the buyers orsellers of contracts, brokers, and a futures ex-change. As in the forward markets, a buyer(party committed to take delivery of securitiesspecified in the futures contract) of a futurescontract has a ‘‘long’’ contract and the seller(party committed to deliver the underlying secu-

rities) has a ‘‘short’’ contract. If a customerdesires to purchase (sell) a futures contract, thebroker—possibly a member of a clearing houseof an exchange—will take the order to the ex-change floor and purchase (sell) a contract sold(bought) by another customer (through anotherbroker).1 All futures transactions are made

1. Brokers in commodities are required to register asfutures commission merchants (‘‘FCMs’’) with the Commod-ities Futures Trading Commission (‘‘CFTC’’) in order to beeligible to solicit or accept orders to buy or sell futurescontracts.

Futures, Forward, and Option Contracts 2130.0

BHC Supervision Manual December 1992Page 6

through and carried on the books of clearinghouse member brokers, who are treated by theexchange as their own customers. Hence, thereare always an equal number of long and shortcontracts outstanding, referred to as the ‘‘openinterest,’’ since the auction process requires abuyer and seller for every contract.All futures contracts are obligations of an

exchange’s clearing association or corporation,i.e. the clearing association is on the oppositeside of each long and short contract; and alltransactions are guaranteed within the resourcesof the exchange’s clearing association (on mostfutures exchanges a small fee is collected oneach transaction and placed into an insurancefund). Should an FCM default on a futurescontract, the association pays the costs of com-pleting the contract.

2130.0.4 MARGIN REQUIREMENTS

In order to insure the integrity of futures mar-kets, the clearing house requires that memberbrokers (clearing house members) deposit initialmargin in connection with new futures positionscarried for the firm, other brokers or FCMs forwhom the clearing house member clears trans-actions, and public customers. The clearinghouse members in turn require their customers—whether they are other FCMs or public custom-ers—to deposit margin.2 The FCMs generallyrequire that public customers meet initial mar-gin requirements by depositing cash, pledginggovernment securities, or obtaining irrevocablestandby letters of credit from substantial com-mercial banking organizations. Daily mainte-nance margin or variation margin calls (depositsof cash required to keep a certain minimumbalance in the margin account) based upon eachday’s closing futures prices are calculated pursu-ant to rules of the various futures exchanges,and clearing house members are required tomeet daily variation margin calls on positionscarried for customers and the firm. In turn, the

FCMs require customers to reimburse them forposting additional margin.Once a customer has executed a futures con-

tract to make or accept delivery of securities inthe future it is obligated to fulfill the terms ofthe contract. A futures contract cannot be resoldover-the-counter because futures contracts arenot transferable. However, a customer may ter-minate its obligation under a futures contracteither by making or accepting delivery of thesecurities as specified by the contract, or byexecuting an offsetting futures contract (longcontract to cancel a short contract or vice-versa)with the same broker to cancel the originalcontract on the same exchange. The overwhelm-ing majority of futures contracts are closed outby the execution of an offsetting contract priorto expiration.The key to understanding futures transactions

is the fact that futures contract prices on U.S.government and agency securities move in thesame manner as bond prices; e.g. rising interestrates result in falling futures prices and fallinginterest rates result in rising futures prices.Hence, the purchase of a futures contract(‘‘long’’ futures contract) at a price of 98 willresult in a loss if future market participantsperceive rising interest rates in the month ofcontract expiration and act accordingly; then theoffsetting of a futures contract (executing a‘‘short’’ futures contract) would have to be at alower price; e.g. 96. As in the case of anycommercial transaction, the participant has aloss if the sale price is lower than the purchaseprice, or a gain if the sale price is higher than thepurchase price.

2130.0.4.1 Variation Margin Calls

Variation margin calls for each contract andexpiration month are based upon the closingfutures exchange price. If there is a change fromthe previous day’s closing prices, the long con-tract holders will be required to post additionalmargin which will be passed through via theclearing house process to short contract holdersor vice-versa. Subsequent to the computation ofvariation margin calls, the clearing house mem-ber brokers are required to post variation marginon behalf of the clearing firm and its customeraccounts prior to commencement of the nextday’s trading. Then, the clearing brokers calltheir FCM and public customers requestingmore margin to bring the accounts up to the

2. In general, the futures exchanges set different initialmargin requirements based upon the types of activity engagedin by the customer. Margin requirements are higher for cus-tomer contracts characterized as ‘‘speculative’’ than for thosecontracts deemed to be ‘‘hedge’’ positions. The commoditiesindustry traditionally defines someone with a business needfor using the futures market as a hedger; others are defined asspeculators. Therefore, in instances where there are differentinitial hedge and speculative margin requirements, it is as-sumed that banking organizations will only be required tomeet margin required for hedgers.

Futures, Forward, and Option Contracts 2130.0

BHC Supervision Manual December 1992Page 7

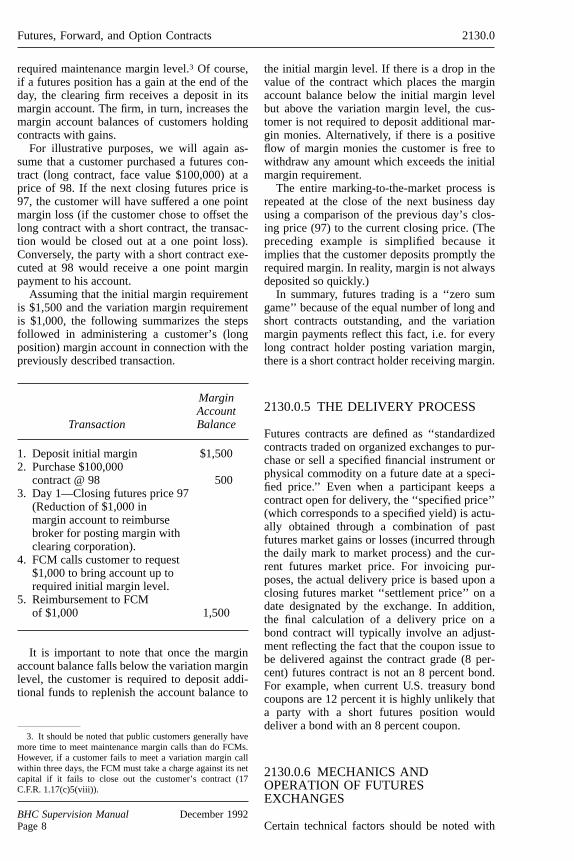

required maintenance margin level.3 Of course,if a futures position has a gain at the end of theday, the clearing firm receives a deposit in itsmargin account. The firm, in turn, increases themargin account balances of customers holdingcontracts with gains.For illustrative purposes, we will again as-

sume that a customer purchased a futures con-tract (long contract, face value $100,000) at aprice of 98. If the next closing futures price is97, the customer will have suffered a one pointmargin loss (if the customer chose to offset thelong contract with a short contract, the transac-tion would be closed out at a one point loss).Conversely, the party with a short contract exe-cuted at 98 would receive a one point marginpayment to his account.Assuming that the initial margin requirement

is $1,500 and the variation margin requirementis $1,000, the following summarizes the stepsfollowed in administering a customer’s (longposition) margin account in connection with thepreviously described transaction.

Transaction

MarginAccountBalance

1. Deposit initial margin $1,5002. Purchase $100,000

contract @ 98 5003. Day 1—Closing futures price 97

(Reduction of $1,000 inmargin account to reimbursebroker for posting margin withclearing corporation).

4. FCM calls customer to request$1,000 to bring account up torequired initial margin level.

5. Reimbursement to FCMof $1,000 1,500

It is important to note that once the marginaccount balance falls below the variation marginlevel, the customer is required to deposit addi-tional funds to replenish the account balance to

the initial margin level. If there is a drop in thevalue of the contract which places the marginaccount balance below the initial margin levelbut above the variation margin level, the cus-tomer is not required to deposit additional mar-gin monies. Alternatively, if there is a positiveflow of margin monies the customer is free towithdraw any amount which exceeds the initialmargin requirement.The entire marking-to-the-market process is

repeated at the close of the next business dayusing a comparison of the previous day’s clos-ing price (97) to the current closing price. (Thepreceding example is simplified because itimplies that the customer deposits promptly therequired margin. In reality, margin is not alwaysdeposited so quickly.)In summary, futures trading is a ‘‘zero sum

game’’ because of the equal number of long andshort contracts outstanding, and the variationmargin payments reflect this fact, i.e. for everylong contract holder posting variation margin,there is a short contract holder receiving margin.

2130.0.5 THE DELIVERY PROCESS

Futures contracts are defined as ‘‘standardizedcontracts traded on organized exchanges to pur-chase or sell a specified financial instrument orphysical commodity on a future date at a speci-fied price.’’ Even when a participant keeps acontract open for delivery, the ‘‘specified price’’(which corresponds to a specified yield) is actu-ally obtained through a combination of pastfutures market gains or losses (incurred throughthe daily mark to market process) and the cur-rent futures market price. For invoicing pur-poses, the actual delivery price is based upon aclosing futures market ‘‘settlement price’’ on adate designated by the exchange. In addition,the final calculation of a delivery price on abond contract will typically involve an adjust-ment reflecting the fact that the coupon issue tobe delivered against the contract grade (8 per-cent) futures contract is not an 8 percent bond.For example, when current U.S. treasury bondcoupons are 12 percent it is highly unlikely thata party with a short futures position woulddeliver a bond with an 8 percent coupon.

2130.0.6 MECHANICS ANDOPERATION OF FUTURESEXCHANGES

Certain technical factors should be noted with

3. It should be noted that public customers generally havemore time to meet maintenance margin calls than do FCMs.However, if a customer fails to meet a variation margin callwithin three days, the FCM must take a charge against its netcapital if it fails to close out the customer’s contract (17C.F.R. 1.17(c)5(viii)).

Futures, Forward, and Option Contracts 2130.0

BHC Supervision Manual December 1992Page 8

respect to futures markets. First, futures marketsare not totally free markets. Rules of theexchanges put artificial constraints—daily pricemovement limits—upon the amount of dailymarket movement allowed in given types offutures contracts. For example, governmentsecurities prices in the cash market will move asfar as the market participants deem necessary toreflect the ‘‘market’’ for those securities, whilethe futures market specifying delivery of theunderlying security will be constrained fromhaving the same potential unlimited marketmovement. There have been instances wherepersons desiring to close out a futures contractby executing an offsetting contract have beenunable to do so for one or more days until theexchange’s daily trading limits allowed futuresprices to ‘‘ratchet’’ up or down to the level thatreflected the true ‘‘market’’ price as perceivedby hedgers, speculators, and arbitragers.Although the preceding illustrates the basic

nature of futures price movements, do notassume that futures and cash market pricesalways move in the same direction at the samevelocity. Futures prices by definition predictfuture events, e.g., a market participant can buya futures contract to take delivery of a threemonth Treasury bill two years in the future.4

In such an instance, the holder of a long T-billfutures contract agrees to the future purchase ofa government security which has not yet beenissued. There is no reason to assume that acontract with a distant maturity will move in thesame manner as the cash market for a threemonth Treasury bill. In addition, there is a rela-tionship between the cash market price of anexisting security and the price of that security inthe futures market which is called the basis. Thebasis can vary significantly over the life of agiven futures contract. In the contract deliverymonth, the futures market price will convergetowards the cash market price (the basis ap-proaches zero), adjusted for technical factorsthat reflect the costs of processing and deliver-ing securities. If the futures market price did notconverge towards the cash market price in thedelivery month, the arbitragers would take off-setting futures and cash market positions to arbi-trage away any profitable discrepancies betweenthe two markets.

2130.0.7 COMPARISON OF FUTURES,FORWARD, AND STANDBYCONTRACTS

Excluding the fact that futures contracts aretraded on organized exchanges, there are manysimilarities between contracts. Conceptually, thecontracts are interchangeable; each type of con-tract can be utilized for hedging, speculating, orarbitrage strategies, but none of the contracts aretransferable to third parties. While engaging incontract activities allows the participants toeither assume or shift the risks of interest ratechanges associated with the security deliverableunder the contract, such contracts fail to providethe other benefits of owning the underlyingsecurity. Specifically, financial contracts do notpay interest, do not have a U.S. governmentguaranty of payment of principal at maturity,and cannot be pledged to secure public depositsor be used as collateral for repurchase agree-ments. The forward markets are perceived to bedelivery markets wherein there is a high per-centage of delivery of the underlying security.As in the case of other futures markets, the

financial futures markets were not designed tobe delivery markets. Nevertheless, there havebeen a number of instances when a relativelyhigh percentage of financial futures contractshave resulted in delivery. Some persons suggesttax reasons and the deliverable supply of securi-ties as two factors that have contributed to themuch higher delivery of securities than deliveryof physical commodities. It is, of course, alsoeasier and cheaper to make delivery of securi-ties rather than railroad carloads of grain.Trading units on futures exchanges are stan-

dardized. The standardized trading unit in aphysical commodity which may be a railroadcar of grain; the typical trading unit in a govern-ment or agency security futures contract may be$100,000 or $1 million par principal at a couponrate (on coupon issues) fixed by the exchange.On the other hand, forward and standby con-tracts are not traded in standardized unitswith given contract maturity months. Instead,forward and standby contracts are custom madeto suit the needs of the two parties to thetransaction.While all contract holders are involved with

market risks, the holders of forward and standbycontracts are especially prone to credit risk.Unlike futures contracts where the mechanics ofexchange trading provide for the futures ex-change clearing association to guaranty perfor-

4. All financial futures contracts have a number of contractexpiration months extending into the future. As the near termcontract expires, a contract with a more distant expiration dateis added.

Futures, Forward, and Option Contracts 2130.0

BHC Supervision Manual December 1992Page 9

mance of each contract, forward and standbycontracts are only as good as the entity on theother side of the contract. Anyone who reads thefinancial press should be aware that prior to thepassage of the Government Securities Act of1986, there were a number of defaults involvingforward and standby contracts. In an effort tobring increased integrity into the unregulatedforward contract markets, there has been a trendby some of the major securities dealers torequire the posting of margin in connection withforward contract trading. There are no uniformmargin requirements governing all aspects offorward contract trading, nor is there a uniformapplication of margin requirements by dealersrequiring ‘‘house’’ margin (or internal marginrequirements established and enforced by indi-vidual securities dealers). GNMA has estab-lished limited margin requirements (24 C.F.R.390.52), as described below.

2130.0.8 OPTION CONTRACTS

Subsequent to the Board’s initial adoption of apolicy statement governing futures, forward, andstandby contracts, trading of interest rate optionsbegan on organized futures and securities ex-changes. Proponents of exchange traded optionsargue that such instruments are attractive tousers because they permit the user to obtaindown side price risk protection, yet benefitfrom favorable price movement. In contrast,futures and forward contracts allow the user tolock in a specific price, but the user must forgofuture participation if the market should experi-ence an upward price movement. Furthermore,the purchaser of an option pays a one timepremium for this protection and is spared thecontingent liabilities associated with futuresmargin calls.An option is a contract that gives the buyer,

or holder, the right, but not the obligation, tobuy or sell a specified financial instrument at afixed price, called the exercise or strike price,before or at a certain future date. Some options,however do not provide for the delivery of theunderlying financial instrument and, instead, arecash settled. Moreover, in some cases, theunderlying financial instrument is an index.Options that can be exercised before or at theexpiration date are referred to as Americanoptions; if an option can be exercised only onthe expiration date, it is termed a Europeanoption.

There are two basic types of options: callsand puts. Thecall option is any option whichobligates the writer to deliver to the buyer at aset price (exercise or strike price) within a spec-ified time limit the underlying financial instru-ment. When the market price of the underlyinginstrument is above the exercise (strike) price ofthe call, the call option is ‘‘in-the-money.’’ Con-versely, when the market price of the underlyingfinancial instrument is below the exercise(strike) price of the call option, the call is ‘‘out-of-the-money.’’ When the market price of theunderlying instrument is equal to the strikeprice, the option is ‘‘at-the-money.’’ At expira-tion, the buyer will exercise the option if it is‘‘in-the-money’’ or let it expire unexercised if itis out-of-the-money. An out-of-the-money calloption has no value at expiration, since buyerswill not purchase the underlying instrument at aprice above the current market price. Prior toexpiration, the value of an ‘‘in-the-money’’ calloption is at least equal to the market value of theunderlying instrument minus the strike price.The ownership of a call provides significantleverage, but raises the breakeven price relativeto ownership of the underlying instrument.Holding the call limits the amount of potentialloss and offers unlimited potential for gains.A put optiongives the buyer the right, but not

the obligation, tosell the underlying instrumentat a specified price (exercise or strike price),before or at expiration. When the market priceof the underlying instrument is below the strikeprice of the put option, the put is ‘‘in-the-money,’’ and a put option is out-of-the-moneywhen the market price of the underlying finan-cial instrument is above the strike price of theput option. Ownership of a put option offersleveraged profitability if the market value of theunderlying instrument declines.Some portfolio managers commonly employ

‘‘covered’’ call writing strategies to gain feeincome from options written on securities heldin the portfolio. If an option position is covered,the seller owns the underlying financial instru-ment or commodity or has a futures position.For example, an option position would be ‘‘cov-ered’’ if a seller owns cash market U.S. Treasurybonds or holds a long position on a Treasurybond futures contract. Writing ‘‘covered calls’’has only limited potential for gain. Writing‘‘covered calls’’ is not a proper strategy for amarket that could rise or fall by substantialamounts. It is generally used in a flat marketenvironment.Referring to the above example, if a seller

holds neither the cash market U.S. TreasuryBonds or was not long on the Treasury bond

Futures, Forward, and Option Contracts 2130.0

BHC Supervision Manual December 1992Page 10

futures contract, the writer would have anuncovered or ‘‘naked’’ position. In suchinstances, margin would be required (by theexchange, if an exchange traded option—not thecase for an OTC option) since the seller wouldbe obligated to satisfy the terms of the optioncontract if the option buyer exercises the con-tract. The risk potential for loss in writing‘‘naked calls’’ (calls against which there are nosecurities held in portfolio) is great since theparty required to deliver must purchase the re-quired securities at current market prices. Naked‘‘covered call’’ writing is generally viewed to bespeculative since the risks are theoreticallyunlimited, particularly if it is done solely togenerate fee income.Options are purchased and traded either on

organized exchanges or in the over-the-counter(OTC) market. Option contracts follow three-month expiration cycles (example: March/June/September/December). The option contractsexpire on the Saturday following the third Fri-day in the expiration month. Thus, options areconsidered as ‘‘wasting assets’’ because theyhave a limited life since they expire on a certainday, even though it may be weeks, months, oryears from now. The expiration date is the lastday the option can be exercised. After that datethe option is worthless.Option premium valuation.The price (value)

of an option premium is determined competi-tively by open outcry auction on the tradingfloor of the exchange. The premium value isaffected by the inflow of buy and sell ordersreaching the exchange floor. The buyer of theoption pays the premium in cash to the seller ofthe option which is credited to the seller’saccount. Several factors affect the value of anoption premium, as discussed below. The optionpremium consists of two parts, ‘‘intrinsic value’’and ‘‘time value.’’ The intrinsic valueis thegross profit that would be realized upon immedi-ate exercise of the option. Stated another way, itis the amount by which the option is in-the-money. It is the higher of: the value of an optionif it is exercised today; or zero. For ‘‘in-the-money’’ call options, it is the difference betweenthe price of the underlying financial instrument,and the exercise (strike) price of the option. For‘‘in-the-money’’ put options, it is the differenceof the exercise (strike) price of the put optionand the price of the underlying financial instru-ment. The intrinsic value is zero for ‘‘at-the-money’’ or ‘‘out-of-the-money’’ options. Thetime value derives from the chance that anoption will gain intrinsic value in the future orthat its intrinsic value will increase before matu-rity of the contract. Time value is determined by

subtracting intrinsic value from the option pre-mium. For example,

Time value = Option premium− Intrinsic values

Time value = 5–10/64 − 4.00

Time value = 1.15384

The option premium is affected by severalother factors. One factor involves the compari-son of the underlying futures price versus thestrike price of the option. An option’s price isincreased the more that it is in-the-money. Asecond factor is volatility. Volatile prices of theunderlying financial instrument can help stimu-late demand for the options, thus increasing thepremium. A third factor that affects the pre-mium of an option is the time until expiration.Option premiums are subject to greater pricefluctuations because the underlying value of thefutures contract changes more with a longertime period. Other factors that affect the optionpremium are the strike rate(s) and the domesticand foreign (if applicable) interest rates.An exchange-traded option is often referred

to as a ‘‘standardized’’ option, reflecting the factthat the terms of the contract are uniform withrespect to the underlying instrument, amounts,exercise prices, and expiration dates. OTCoptions are characterized by terms and condi-tions which are unique to each transaction.Large financial institutions are often dealers incustomized interest rate or foreign exchangeoptions. For example, a banking organizationmight write a ‘‘cap,’’ or series of put option onpounds sterling to protect the dollar value of asterling denominated receivable due in one year.In this case, an option can be tailored to fit theexact needs of the buyer.Like futures contracts, contract performance

on exchange-traded options is guaranteed by theclearing corporation which interposes itself as acentral counterparty to all transactions. It substi-tutes itself as a seller to all buyers and as a buyerto all sellers. Standardization combined with theclearing corporation’s guarantee facilitates trad-ing and helps to insure liquidity in the market.The buyer or seller of an exchange-traded optionmay always close out an open position by enter-ing into an offsetting transaction, with the samestrike price and expiration date, and for thesame amount. Indeed, most exchange-tradedoptions are liquidated prior to maturity with anoffsetting transaction, rather than by exercising

Futures, Forward, and Option Contracts 2130.0

BHC Supervision Manual December 1992Page 11

the option in order to buy or sell the underlyinginstrument.Buyers of exchange-traded options are not

required to post funds to a margin accountbecause their risk is limited to the premium paidfor the option. However, writers (sellers) ofoptions are required to maintain marginaccounts because they face substantial amountsof risk. The amount of the margin variesdepending upon the volatility in the price of theoption. As the option moves closer and closer tobeing in-the-money, the writer is required todeposit more and more into his margin account,in order to guarantee his performance should theoption eventually be exercised.Options on futures contracts provide the

holder with the right to purchase (call) or sell(put) a specified futures contract at the option’sstrike price. The difference between the strikeprice on the option and the quote on the futurescontract represents the intrinsic value of theoption. Options on futures contracts differ fromtraditional options in one key way: the partywho exercises an option on a futures contractreceives a long or short futures position (de-pending on whether he is exercising a call or putoption) rather than accepting or making deliveryof the underlying security or financial instru-ment. When the holder of a call option on afutures contract exercises the option and thefutures contract is delivered, the option writermust pay the option holder the differencebetween the futures contract’s current value andthe strike price of the exercised call. The buyertakes on a long position, and the writer a shortposition in the futures contract. When a futuresput option is exercised, the holder takes on ashort futures position, and the writer a longposition. The writer of the put pays the holderthe difference between the current price of thefutures contract and the strike price of the putoption. The resultant futures position, like anyother futures position, is subject to a dailymarked-to-market valuation. In order to liqui-date the futures position, both the buyer andthe seller must undertake offsetting futurestransactions.

2130.0.8.1 Other Option Contracts

2130.0.8.1.1 Stock Index Options

A stock index option is a call or a put that isbased on a stock market index such as the S & P

500. As opposed to a regular call or put optionon equity securities where there must be a saleand delivery of shares of stock, there is nodelivery of the underlying instrument when anindex option is exercised. Rather, settlement isin cash.

2130.0.8.1.2 Foreign Currency Options

The right to buy (call) or sell (put) a quantity ofa foreign currency for a specified amount of thedomestic currency is a foreign currency option.The size of the contract is standard for eachcurrency. The contracts are quoted in cents perunit of foreign currency. As an example, onecall option for the British pound is 12,500pounds.

2130.0.8.2 Caps, Floors, and Collars

Caps, floors, and collars provide risk protectionagainst floating interest rates. The market forthese products is an outgrowth of the OTC mar-ket in fixed income (bond) options.An interest rate cap contract pays the buyer

cash if the short term interest index risesabove the strike rate in the contract in exchangefor a fee. In combination with a floating rateobligation, it effectively sets a maximum levelon interest rate payments. If market rates arebelow the cap rate, no payments are madeunder the cap agreement. Thus, the buyer of acap is able to place a ceiling on his floatingrate borrowing costs without having to foregopotential gains from any decline in marketrates.Cap agreements typically range in maturity

from 6 months to as long as 12 years, with resetdates or frequencies that are usually monthly,quarterly, or semiannual. The London InterbankOffered Rate (LIBOR) is the most widely usedreference rate for caps, floors, and collars. Otherindexes used as reference rates are commercialpaper rates, the prime interest rate, Treasury billrates, and certain tax-exempt rates. Cap feesdepend upon the cap level, the maturity of theagreement, the volatility of the index used as thereference rate, and market conditions. Thehigher the cap rate, the lower the premium.The fee is usually paid up front, but can beamortized.An interest rate floor agreement is used to

protect the overall desired rate of return associ-ated with a floating-rate asset. In accordancewith the agreement, the seller receives a fee for

Futures, Forward, and Option Contracts 2130.0

BHC Supervision Manual December 1992Page 12

the floor agreement from the holder of theunderlying asset. When interest rates fall, theholder of the floor contract is protected by theagreement, which specifies the fixed per annumrate (floor rate) that will be retained on thoseassets, at specified times during the life of theagreement, even though floating interest ratesmay decline further.An interest rate collar is a variation of a

cap-only agreement. Under this arrangement theseller of the collar, for a fee, agrees to limit thebuyer’s floating rate of interest within oneagreement by a simultaneous sale of a capand purchase of a floor, or purchase of a capand sale of a floor. When the reference rate isabove the cap rate the seller makes payments tothe buyer sufficient to return the buyer’s floatingrate interest cost to the cap rate. Conversely, thebuyer makes payments to the collar provider tobring its rate back to the floor whenever thereference rate falls below the floor rate. In effect,under a collar agreement the buyer is selling astring of call options (the floor) back to theprovider of the cap. The premium received fromselling the floor reduces the overall cost of thecap to the buyer of the collar. Thus, the pre-mium for a floor/ceiling, or collar, agreement, islower than for a cap-only agreement with thecap at the same level. This is because the floorsold to the provider of the collar has a certainvalue, which is passed along to the buyer in theform of a lower premium.The disadvantage to collars, of course, is that

they limit the buyer’s ability to profit fromdeclines in market rates below the specifiedfloor. Clearly, one’s interest rate expectationsplay an important role in determining whetheror not to use a collar agreement. It should alsobe noted that collar agreements involve creditrisk on both sides of the agreement, similar tothe credit risk considerations found in interestrate swap agreements. The buyer of the collar isexposed to the risk that the provider may defaulton payments due under the cap agreement; andthe provider of the collar is exposed to the riskthat the buyer may default on payments dueunder the floor agreement.

2130.0.9 REGULATORYFRAMEWORK

GNMA has adopted limited margin require-ments. Specifically, the GNMA margin require-ments (12 C.F.R. 390.52) require marking-to-market and the posting of maintenance

margin.5 However, the GNMA margin require-ments exclude the majority of GNMA forwardcontracts and only pertain to contracts involvingGNMA issuers with other parties.6

The Commodities Futures Trading Commis-sion (‘‘CFTC’’) is the agency authorized byCongress to supervise the trading of ‘‘commodi-ties,’’ including financial futures. Exchangeswhich trade commodities must register withthe CFTC. In addition, the various futuresexchanges must receive CFTC approval beforethey can begin trading a new futures instrument.Brokers and dealers who execute futures con-tracts for customers must register as FuturesCommission Merchants (‘‘FCM’’) with theCFTC. There are also CFTC registrationrequirements pertaining to firms engaging incommodities activities similar to an investmentadvisor or mutual fund in the securities markets.Finally, the surveillance activities of the variousfutures exchange examiners are subject to over-sight by the CFTC.With the exception of reporting requirements

concerning persons or entities with large futurespositions, the CFTC’s jurisdiction generallydoes not extend to financial institutions. Rather,the federal and state banking agencies, stateinsurance commissions, and the Office of ThriftSupervision are responsible for supervisingregulated entities’ future activities, if permitted,under statute or regulation.

2130.0.10 EXAMPLES OF CONTRACTSTRATEGIES

For purposes of reporting large positions to theCFTC a market participant defines its futureactivities as ‘‘speculative’’ or as ‘‘hedging.’’Basically, CFTC rules consider a participant tobe a hedger if certain facets of such person’sbusiness can be hedged in the futures markets;persons who do not have a business need forparticipating are deemed to be speculators. It isanticipated that bank holding companies charac-terize their contract activities as ‘‘hedging’’, orpossibly as arbitrage between various markets.

5. Initial margin requirements necessitate the pledging ofsomething of value prior to initiation of a transaction. Depos-iting maintenance margin refers to pledging something ofvalue in reaction to market movements; e.g. depositing cashrepresenting the difference between a forward contract priceand its current market value.6. See SR-625 dated July 23, 1980.

Futures, Forward, and Option Contracts 2130.0

BHC Supervision Manual December 1992Page 13

Examiners must scrutinize contract positions forpurposes of evaluating risk.The Board policy statement concerning bank

holding companies7 states:‘‘. . . the Board believes that any positions

that bank holding companies or their nonbanksubsidiaries take in financial contracts shouldreduce risk exposure, that is, not be specula-tive.’’ It should be noted, however, that a moreliberal interpretation of the policy statement hasbeen permitted for dealer subsidiaries. For ex-ample, in a government securities dealer subsid-iary, it is permissible to use related financialcontracts as a substitute trading instrument forcash market instruments. Thus, the use of finan-cial contracts is not limited solely to reducingthe risk of dealing activities.Some examples of contract strategies are pro-

vided which reduce risk when viewed in isola-tion. A definition of a financial hedge is:

‘‘to enter transactions that will protectagainst loss through a compensatory pricemovement.’’In looking at a hedge transaction in isolation,

there should be certain elements present to makea hedge workable:1. The interest rate futures or forward con-

tract utilized should have a high positive corre-lation (prices that tend to move in the samedirection with similar magnitude) with the cashposition being hedged. In other words, thefutures or forward position taken should bestructured so that an upward price movement inthe contract offsets a downward price move-ment in the cash or risk position being hedged,and vice versa.2. The type (e.g. T-bill, T-bond, etc.) and size

of the contract position8 taken should have aproportionate relationship to the cash or riskposition being hedged, so that futures gains

(losses) will approximately offset any losses(gains) on the hedged position.3. The contract position taken should have a

life which is equal to or greater than the end ofthe period during which the hedge will be out-standing. For example, if interest rate protectionwas deemed necessary for a six-month timespan, it would not ordinarily be wise to enter acontract expiring in three months.

2130.0.10.1 The Mortgage Banking PriceHedge

Assume that a mortgage banking subsidiaryagrees in June to originate mortgages at a fixedyield in the following October. Unless the loanoriginator has a forward commitment to sell theloans to a permanent investor(s), it is exposed toa decline in the principal value of mortgagesdue to a rise in interest rates between the com-mitment date and ultimate sale of the loans. Anexample of a traditional ‘‘short hedge’’ wouldbe the sale of futures contracts in an attempt toreduce the risk of price fluctuation and insure aprofitable sale of the loans. However, in follow-ing this strategy the mortgage originator alsochooses to forfeit its ability to reap a profit ifinterest rates should fall.If interest rates increased, the loss on the sale

of mortgages or a pool of mortgage-backed se-curities will probably be largely offset by a gainon the futures transaction; see example below. Ifinterest rates fall, the mortgage originator wouldgain on the resale of mortgages but lose on thefutures market transaction. Hence, in a truehedge, the hedger’s earnings are relatively unaf-fected by a change in market interest rates ineither direction.Generally accepted accounting principles

applicable to mortgage activity require thatmortgages held for resale be periodically reval-ued to the lower of cost or market (FinancialAccounting Standards Board Statement No. 65,‘‘Accounting for Certain Mortgage BankingActivities’’). Unrealized gains and losses on out-standing futures contracts are matched againstrelated mortgages or mortgage commitmentswhen the inventory is revalued to the lower ofcost or market; i.e. the lower of cost or marketvaluation is based upon a net figure includingunrealized related futures gains and losses.

2130.0.10.2 Basis

Basis is the difference between the cash (spot)price of a security (or commodity) and itsfutures price. In other words:

7. The Board’s policy statement on engaging in futures,forwards, and option contracts.8. Futures market participants engage in a practice, some-

times known as ‘‘factorweighting’’ or ‘‘overhedging,’’ to de-termine the appropriate number of futures contracts necessaryto have the proper amount of compensatory price movementagainst a hedged cash or risk position. For example, it wouldrequire 10 mortgaged-backed futures contracts (8% coupon,$100,000 face value) to hedge an inventory of $1,000,000mortgage-backed (8% coupon) securities. Alternatively, 14mortgage-backed futures contracts would be required to hedgea $1 million inventory of mortgage-backed securities with a131⁄2% coupon. Overhedging or factor weighting is necessaryin hedging securities with higher coupons than those specifiedin futures contracts (currently 8% on bond futures) becausehigher coupon securities move more in price for a givenchange in yield than lower coupons.

Futures, Forward, and Option Contracts 2130.0

BHC Supervision Manual December 1992Page 14

Basis = Spot price− Future price

For short-term and intermediate futures con-tracts, the futures price is the quoted futuresprice times an appropriate conversion factor.For short-term futures contracts the quotedfutures price is 100 less the annualized futuresinterest rate. The invoice price must be deter-mined using yield-to-price conventions for thefinancial instrument involved.Basis may be expressed in terms of prices.

Due to the complexities involved in determiningthe futures price, it is thus better to redefineprice basis using actual futures delivery pricesrather than quoted futures prices. Thus, the pricebasis for fixed income securities should be rede-fined as:

Price Basis = Spot price− Futures delivery price.

Basis may also be expressed in terms of inter-est rates. Therate basisis defined as:

Rate basis = Spot rate− Futures rate

The spot rate refers to the current rate on theinstrument that can be held and delivered on thecontract. The futures rate represents the interestrate that corresponds to the futures deliveryprice of the deliverable instrument.

The rate basis is useful in analyzing hedges ofshort-term instruments since it nets out alleffects resulting from aging. For example, if aone year T-bill has a rate of 9 percent with aprice of 85, and a 3-month T-bill has a rate of9 percent and a price of 94, the price basiswould be−9. If a cash security ages, it does notnecessarily mean that a change in the rate basishas taken place.

2130.0.10.3 Trading Account ShortHedge

Another example of a short hedge pertains tosecurities dealers that maintain bond tradingaccounts. While bonds are held ‘‘long’’ (actual-ly owned by the dealer) in trading accounts,dealers are subject to two risks. First, there isthe risk that the cost can change regardless ofwhether the funds are generated through repur-chase agreement financing or the dealer’s otherfunding sources. When there is an inverted yieldcurve (short-term interest rates are higher thanlong-term rates), trading portfolio bonds ininventory yield less than the cost of fundsrequired to carry them. Second, there is the riskthat bond market interest rates will rise, thusforcing the dollar price of bonds down.

2130.0.10.3.1 Example 1: A Perfect Short Hedge1

Month Cash Market Futures Market

June Mortgage department makes commitment to abuilder to originate $1 million of mortgages(based on current GNMA 8’s cash price) at98-28⁄32 for $988,750

Sells 10 December mortgage-backed futures at 96-8⁄32for $962,500 to yield8.59 percent

October Mortgage department originates thensells $1million of pooled mortgages to investors at aprice of 95-20⁄32, for $956,250

Loss: $32,500

Buys 10 December mortgage-backed futures at 93,for $930,000 to yield8.95 percent

Gain: $32,500

1. The effects of margin and brokerage costs on the trans-action are not considered. It should be noted that ‘‘perfecthedges’’ generally do not occur.

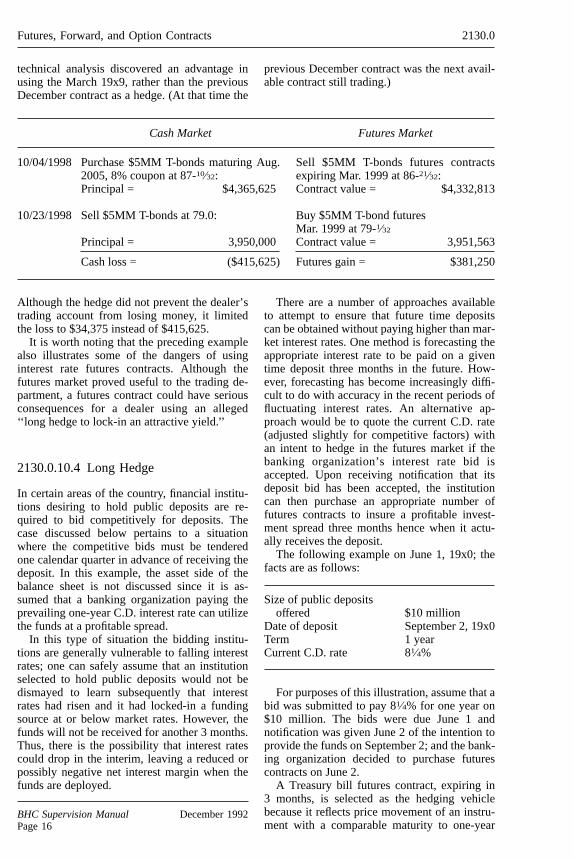

The following example pertains to a bond trad-ing account. Assume that the dealer purchasesTreasury bonds on October 4 and simulta-neously sells a similar amount of Treasury bondfutures contracts. The illustration ignores com-

mission charges and uses futures contractsmaturing in March 19x9 because the dealer’s

Futures, Forward, and Option Contracts 2130.0

BHC Supervision Manual December 1992Page 15

technical analysis discovered an advantage inusing the March 19x9, rather than the previousDecember contract as a hedge. (At that time the

previous December contract was the next avail-able contract still trading.)

Cash Market Futures Market

10/04/1998 Purchase $5MM T-bonds maturing Aug.2005, 8% coupon at 87-10⁄32:Principal = $4,365,625

Sell $5MM T-bonds futures contractsexpiring Mar. 1999 at 86-21⁄32:Contract value = $4,332,813

10/23/1998 Sell $5MM T-bonds at 79.0:

Principal = 3,950,000

Cash loss = ($415,625)

Buy $5MM T-bond futuresMar. 1999 at 79-1⁄32Contract value = 3,951,563

Futures gain = $381,250

Although the hedge did not prevent the dealer’strading account from losing money, it limitedthe loss to $34,375 instead of $415,625.It is worth noting that the preceding example

also illustrates some of the dangers of usinginterest rate futures contracts. Although thefutures market proved useful to the trading de-partment, a futures contract could have seriousconsequences for a dealer using an alleged‘‘long hedge to lock-in an attractive yield.’’

2130.0.10.4 Long Hedge

In certain areas of the country, financial institu-tions desiring to hold public deposits are re-quired to bid competitively for deposits. Thecase discussed below pertains to a situationwhere the competitive bids must be tenderedone calendar quarter in advance of receiving thedeposit. In this example, the asset side of thebalance sheet is not discussed since it is as-sumed that a banking organization paying theprevailing one-year C.D. interest rate can utilizethe funds at a profitable spread.In this type of situation the bidding institu-

tions are generally vulnerable to falling interestrates; one can safely assume that an institutionselected to hold public deposits would not bedismayed to learn subsequently that interestrates had risen and it had locked-in a fundingsource at or below market rates. However, thefunds will not be received for another 3 months.Thus, there is the possibility that interest ratescould drop in the interim, leaving a reduced orpossibly negative net interest margin when thefunds are deployed.

There are a number of approaches availableto attempt to ensure that future time depositscan be obtained without paying higher than mar-ket interest rates. One method is forecasting theappropriate interest rate to be paid on a giventime deposit three months in the future. How-ever, forecasting has become increasingly diffi-cult to do with accuracy in the recent periods offluctuating interest rates. An alternative ap-proach would be to quote the current C.D. rate(adjusted slightly for competitive factors) withan intent to hedge in the futures market if thebanking organization’s interest rate bid isaccepted. Upon receiving notification that itsdeposit bid has been accepted, the institutioncan then purchase an appropriate number offutures contracts to insure a profitable invest-ment spread three months hence when it actu-ally receives the deposit.The following example on June 1, 19x0; the

facts are as follows:

Size of public depositsoffered $10 million

Date of deposit September 2, 19x0Term 1 yearCurrent C.D. rate 81⁄4%

For purposes of this illustration, assume that abid was submitted to pay 81⁄4% for one year on$10 million. The bids were due June 1 andnotification was given June 2 of the intention toprovide the funds on September 2; and the bank-ing organization decided to purchase futurescontracts on June 2.A Treasury bill futures contract, expiring in

3 months, is selected as the hedging vehiclebecause it reflects price movement of an instru-ment with a comparable maturity to one-year

Futures, Forward, and Option Contracts 2130.0

BHC Supervision Manual December 1992Page 16

C.D., and there was no C.D. futures contracttrading. For purposes of this illustration, it isassumed that the contract offers sufficient liquid-ity to enable the banking organization to readilyoffset its open futures position when necessary.Using the bill contract is an example of ‘‘crosshedging’’ which is defined as the buying orselling of an interest rate futures contract toprotect the value of a cash position of a similar,

but not identical, instrument. This type of hedg-ing is a measured risk since the outcome of sucha transaction is a function of the price correla-tion of the instruments being hedged. At anygiven moment it is conceivable that a negativecorrelation could exist between two unlikeinstruments despite the presence of a strongcorrelation over an extended time period.

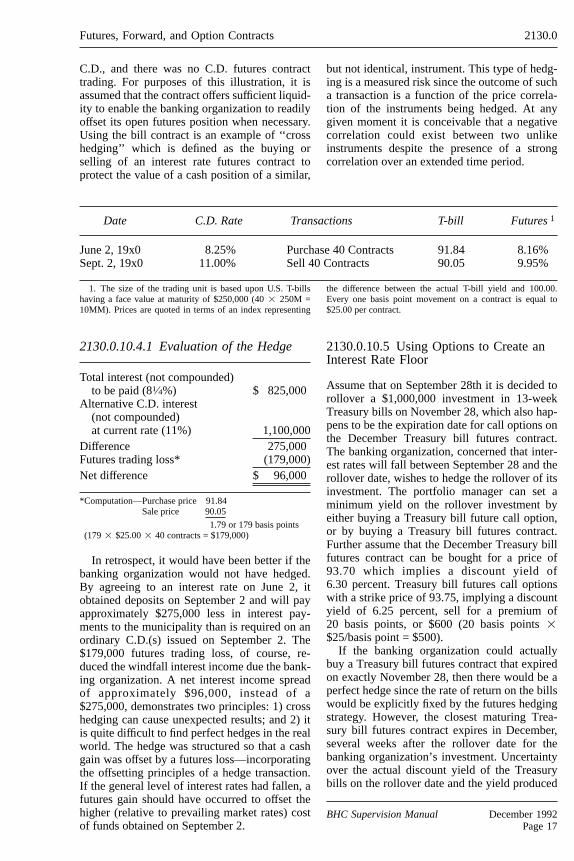

Date C.D. Rate Transactions T-bill Futures1

June 2, 19x0 8.25% Purchase 40 Contracts 91.84 8.16%Sept. 2, 19x0 11.00% Sell 40 Contracts 90.05 9.95%

1. The size of the trading unit is based upon U.S. T-billshaving a face value at maturity of $250,000 (402 250M =10MM). Prices are quoted in terms of an index representing

the difference between the actual T-bill yield and 100.00.Every one basis point movement on a contract is equal to$25.00 per contract.

2130.0.10.4.1 Evaluation of the Hedge

Total interest (not compounded)to be paid (81⁄4%) $ 825,000

Alternative C.D. interest(not compounded)at current rate (11%) 1,100,000

Difference 275,000Futures trading loss* (179,000)Net difference $ 96,000

*Computation—Purchase price 91.84Sale price 90.05

1.79 or 179 basis points(1792 $25.002 40 contracts = $179,000)

In retrospect, it would have been better if thebanking organization would not have hedged.By agreeing to an interest rate on June 2, itobtained deposits on September 2 and will payapproximately $275,000 less in interest pay-ments to the municipality than is required on anordinary C.D.(s) issued on September 2. The$179,000 futures trading loss, of course, re-duced the windfall interest income due the bank-ing organization. A net interest income spreadof approximately $96,000, instead of a$275,000, demonstrates two principles: 1) crosshedging can cause unexpected results; and 2) itis quite difficult to find perfect hedges in the realworld. The hedge was structured so that a cashgain was offset by a futures loss—incorporatingthe offsetting principles of a hedge transaction.If the general level of interest rates had fallen, afutures gain should have occurred to offset thehigher (relative to prevailing market rates) costof funds obtained on September 2.

2130.0.10.5 Using Options to Create anInterest Rate Floor

Assume that on September 28th it is decided torollover a $1,000,000 investment in 13-weekTreasury bills on November 28, which also hap-pens to be the expiration date for call options onthe December Treasury bill futures contract.The banking organization, concerned that inter-est rates will fall between September 28 and therollover date, wishes to hedge the rollover of itsinvestment. The portfolio manager can set aminimum yield on the rollover investment byeither buying a Treasury bill future call option,or by buying a Treasury bill futures contract.Further assume that the December Treasury billfutures contract can be bought for a price of93.70 which implies a discount yield of6.30 percent. Treasury bill futures call optionswith a strike price of 93.75, implying a discountyield of 6.25 percent, sell for a premium of20 basis points, or $600 (20 basis points2

$25/basis point = $500).If the banking organization could actually

buy a Treasury bill futures contract that expiredon exactly November 28, then there would be aperfect hedge since the rate of return on the billswould be explicitly fixed by the futures hedgingstrategy. However, the closest maturing Trea-sury bill futures contract expires in December,several weeks after the rollover date for thebanking organization’s investment. Uncertaintyover the actual discount yield of the Treasurybills on the rollover date and the yield produced

Futures, Forward, and Option Contracts 2130.0

BHC Supervision Manual December 1992Page 17

by the hedge is known as ‘‘basis risk,’’ the riskthat the yield on the hedge may differ from theexpected yield on the hedged item. For purposesof this example, assume that the yield on thefutures contract equals the actual discount yieldon the 13-week Treasury bills at the rolloverdate. Thus, the futures hedge in this examplewill provide an effective discount yield of6.30 percent on the rollover of the 13-weekTreasury bill investment.Assume that rates fall after September 28 and

that the discount yield on Treasury bill futurescontracts declines from 6.30 percent to 6.00 per-cent at the November 28 expiration date of theDecember Treasury bill futures options con-tract. The option to buy the Treasury bill futureswill be exercised since the strike price of 93.75is below the market price of 94.00 for theunderlying futures contract, yielding a profit of25 basis points or $625 (25 basis points2

$25/basis point). The profit must be offset by the20 basis point cost of the option, which reducesthe net profit to 5 basis points. The effectivehedged discount yield is 6.05 percent (6.00 per-cent on the 13-week Treasury bills—assumingno basis risk—plus the 5 basis point profit fromthe hedge). The option hedge produces a yieldthat is 5 basis points higher than the unhedgedyield, but 25 basis points lower than the6.30 percent yield that would have resulted fromhedging with futures.Although the option hedge resulted in a lower