derivatives. basic derivatives contracts call option put option forward contract futures contract

TRANSCRIPT

Derivatives

Basic Derivatives Contracts

Call OptionPut OptionForward ContractFutures Contract

Call Options

A call option gives you the right to buy ,within a specified time period, at a specified price

The owner of the option pays a cash premium to the option seller in exchange for the right to buy

Put Option

A put option gives you the right to sell within a specified time period at a specified price

It is not necessary to own the asset before acquiring the right to sell it

Options-Terms

Spot Price - The price of the underlying asset at a certain point in time. Strike Price - the predetermined transaction price Premium - price of the option Underlying Asset - the asset that the option gives you the right to buy/sell

Stock, Commodity, Currency etc.

In the Money - A call option with a strike price that is lower than the market price of the underlying asset, or a put option with a strike price that is higher than the market price of the underlying asset.

Out of the Money - A call option with a strike price that is higher than the market price of the underlying asset, or a put option with a strike price that is lower than the market price of the underlying asset.

Call Option

The right to buy an asset (stock) at a price of $40(strike price) at a price of $200(premium)

Why? You want to capitalize on an increasing trend in the spot market (bullish).

LONG CALL

Call Option Example

You believe GOOG will rise towards the 500 level in about a month’s time. The spot rate is currently 450. You buy a GOOG Call with a one month expiry and a strike of 450. The price (premium) is 10 dollars. Let’s say in one month the price of the stock is $480.

Upside: Unlimited, and calculated by: Closing spot price – Strike price - premium = profit Ex. 480 - 450 - 10 = 20 dollars

Downside: The premium (10 dollars) which will be lost if the option is Out-of-The-Money (OTM) at expiry

Put Option

The right to sell an asset (stock) at a price of $40(strike price) at a price of $200(premium)

Why? You want to capitalize on a decreasing trend in the spot market (bearish).

LONG PUT

Put Option Example

You believe GOOG will fall towards the 400 level in about a month’s time. The spot rate is currently 450. You buy a GOOG Put with a one month expiry and a strike of 450. The price is 10 dollars. Let’s say the price of GOOG drops to $400.

Upside: Unlimited, and calculated by: Strike price – closing spot price - premium = profit Profit/Loss: 450 - 400 - 10 = 40 dollars

Downside: The premium (10 dollars) which will be lost if the option is Out-of-The-Money (OTM) at expiry

Participants in the Options Market

Four types of participants in options markets depending on the position they take:

1.) Buyers of calls (Long Position)2.) Sellers of calls (Short Position)3.) Buyers of puts (Short Position)4.) Sellers of puts (Long Position)

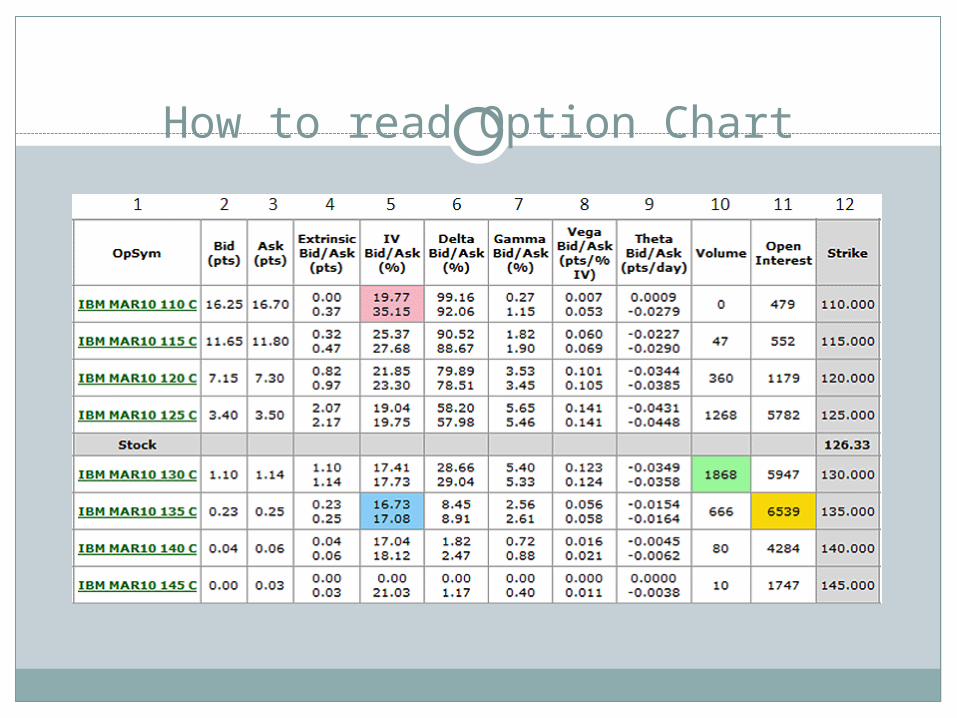

How to read Option Chart

Meanings of Columns

Column 2 – Bid (pts): The "bid" price is the latest price (premium) offered by a market maker to buy a particular option. What this means is that if you enter a "market order" to sell the March 2010, 125 call, you would sell it at the bid price of $3.40.

Column 3 – Ask (pts): The "ask" price is the latest price (premium) offered by a market maker to sell a particular option. What this means is that if you enter a "market order" to buy the March 2010, 125 call, you would buy it at the ask price of $3.50. The more active the option, typically the tighter the bid/ask spread.

Column 4 – Extrinsic Bid/Ask (pts): This column displays the amount of time premium built into the price of each option (in this example there are two prices, one based on the bid price and the other on the ask price).

Meanings of Columns

Column 5 – Implied Volatility (IV) Bid/Ask (%): This value is calculated by an option pricing model Represents the level of expected future volatility based on the current

price of the option and other known option pricing variables. Option prices increase when implied volatility increases

The higher the IV Bid/Ask (%)the more time premium is built into the price of the option and vice versa.

Column 6 – Delta Bid/Ask (%): Delta is a Greek value derived from an option pricing model and which represents the "stock equivalent position" for an option. The delta for an option can range from 0 to +/-100. The present reward/risk characteristics associated with holding a call

option with a delta of 50 is essentially the same as holding 50 shares of stock.

i.e., an option with a delta of 49.9 would gain .499 dollars for each dollar gain or loss in the underlying stock price.

Long positions delta>0, Short positions delta<0

Meanings of columns

Column 7 – Gamma Bid/Ask (%): Another Greek value derived from an option pricing model. Gamma tells you how many deltas the option will gain or lose if the

underlying stock rises by one full point. If gamma is high, need to rebalance more often since even small

changes in stock price will change delta a lot

Column 8 – Vega Bid/Ask (pts/% IV): Vega is a Greek value that indicates the amount by which the price of the option would be expected to rise or fall based solely on a one point increase in implied volatility. March 2010 125 call, if implied volatility rose one point – from 19.04%

to 20.04% Price of this option would gain $0.141. This indicates why it is

preferable to buy options when implied volatility is low You pay relatively less time premium and a subsequent rise in IV will

inflate the price of the option

Meanings of Columns

Column 9 – Theta Bid/Ask (pts/day): Theta is the Greek value that indicates how much value an option will lose with the passage of one day's time. As time goes by, time to expiration decreases, and value of a call or

put drops. Usually decreases faster at the end for a call. At present, the March 2010 125 Call will lose $0.0431 of value due

solely to the passage of one day's time Since purchased options usually decay, you lose value the longer you

hold them.

Column 10 – Volume: This simply tells you how many contracts of a particular option were traded during the latest session.

Meanings of Columns

Column 11 – Open Interest: Total number of contracts of a particular option that have been opened but have not yet been offset. Options that can still be exercised

Column 12 – Strike: Price that the buyer of that option can purchase the underlying security at if he chooses to exercise his option.

Forward Contracts

Definition: A binding agreement (obligation) to buy/sell an underlying asset in the future, at a price set today.

Custom made Traded PrivatelyIn force till maturity, making them less liquidProfit/loss is accumulated till the expiry of

contract

Futures Contracts

Essentially the same definition of a forward but with some additional features that distinguish the two

Standardized (not tailor made), allows for liquidityTraded on the futures exchangeParties can enter into opposite contracts Daily settlement of profit and loss (mark to market)Margin requirements and periodic margin calls

Margin call-A broker's demand on an investor using margin to deposit additional money or securities so that the margin account is brought up to the minimum maintenance margin

Arbitrage Example

Suppose the two year interest rates in Australia and the United States are 5.00% and 7.00%, respectively and the spot exchange rate between Australia (AUD) and the U.S. is .6200 and the two year forward rate is .6300.

However, the forward rate should be .6200e^((.07-.05)*2) Which is simply the spot rate times “e” to the interest rate difference multiplied by the time period. So there is an arbitrage (investment with no risk) opportunity.

Arbitrage Example Continued

Borrow 1,000 AUD at 5.00% for 2 years and you will have to pay back 1000e^(.05*2)= 1,105.17 AUD

Convert 1,000 AUD to $620.00 and invest @ 7.00% for two years giving you 620e^(.07*2)= $713.17

You need 1105.17AUD in 2 years so enter a forward contract at .6300$/AUD which will cost you 1105.17*.6300= $696.26

Arbitrage profit: 713.17-696.26= $16.91

METALLGESELLSCHAFT CASE

Forwards/Futures Gone Wrong

Metallgesellschaft

Early 1991 - MG Refining and Marketing (MGRM) sold forwards of barrels of petroleum The length of the contracts was generally 5-10 years Very successful because prices for petroleum were $3-

5 higher than the spot price September, 1993 - MGRM sold forward contracts on

approximately 160 million barrels Ex. customer could have contract requesting 1,000

barrels of oil a month for 10 years which would be 1,000*12*10= 120,000 barrels

Metallgesellschaft

Forward contracts exposed MGRM to the risk of rising energy prices If energy prices rose, MGRM would be obligated to

supply petroleum at a price lower than the prevailing spot price

MGRM hedged risk by: Buying long gasoline and crude oil futures

Late 1993 - Energy prices fell significantly (25%) and triggered a $900 million dollar loss

Liquidated its futures positions resulting in massive realized losses (1.3 Billion)