future of manufacturing in south east … of manufacturing in south east melbourne steering...

TRANSCRIPT

FUTURE OF

MANUFACTURING IN

SOUTH EAST

MELBOURNE

FUTURE OF

MANUFACTURING IN

SOUTH EAST

MELBOURNE

Steering Committee

Ian Monger (Chair)

Anita Buczkowsky

Paul Dowling

Sandra George

Rod Nelson

Project Team

Rodney Bourke

John Dean

Rodin Genoff

Tony Quick

Garry Wall

This study was commissioned by the Southern Melbourne Regional Development

Australia Committee in partnership with South East Business Networks and the

South East Melbourne Manufacturers‘ Alliance.

December 2011

Page | 3

Contents Abbreviations ........................................................................................................................ 5 1. Executive Summary ......................................................................................................... 6 2. Project objectives and methodology ................................................................................. 9

2.1 Objectives ............................................................................................................... 9 2.2 Defining manufacturing ......................................................................................... 10 2.3 Defining the region ................................................................................................ 10 2.4 Method ................................................................................................................. 10 2.5 Policy context ....................................................................................................... 11

3: Manufacturing in a Global Context ................................................................................. 13 3.1 Forces shaping the global economy ...................................................................... 13

3.1.1 Changing players in the international economy .............................................. 13 3.1.2 Rising cost of resources ................................................................................. 13 3.1.3 Reach of Information and Communications Technology (ICT). ...................... 14 3.1.4 Growth of services sector .............................................................................. 15

3.2 Pressures on the business of manufacturing ........................................................ 15 3.2.1 Origins of manufacturing organisation ............................................................ 15 3.2.2 New customers and changing demands ........................................................ 16 3.2.3 More stakeholder requirements ..................................................................... 16 3.2.4 Intense competition ........................................................................................ 16 3.2.5 The pace of innovation and development of new technologies ....................... 16

3.3 Responding to change ........................................................................................ 157 3.3.1 Flexible manufacturing ................................................................................... 18 3.3.2 Evolution in how manufacturers create value ................................................. 21 3.3.3 Customers and markets ................................................................................. 20 3.3.4 Manufacturing operations .............................................................................. 21 3.3.5 Organisation of production: Global supply chains ......................................... 21 3.3.6 Computer integrated manufacturing ............................................................... 22 3.3.7 New Enabling Technologies ........................................................................... 23

3.4 Innovation in Business Models .............................................................................. 24 3.5 Implications of technology development................................................................ 25

4: Manufacturing - the Australian Context ......................................................................... 26 4.1 Performance of Australia‘s manufacturing sector .................................................. 26 4.2 Performance of manufacturing sub-sectors ........................................................... 30 4.3 Technology ........................................................................................................... 36 4.4 Firm size ............................................................................................................... 37 4.5 Demand side issues.............................................................................................. 38 4.6 Implications for manufacturers in South East Melbourne ...................................... 40

5: Manufacturing in South East Melbourne......................................................................... 40 5.1 Characteristics of manufacturing in South East Melbourne ................................... 40

5.1.1 Importance of manufacturing in South East Melbourne ................................. 40 5.1.2 Industry profile ............................................................................................... 44 5.1.3 Sub-region characteristics............................................................................. 45 5.1.4 Evidence of change and restructuring ............................................................ 46

5.2 Managers attitudes and firm strategy: Preparing for the future ............................. 48 5.2.1 Competitive advantages ................................................................................ 48 5.2.2 Factors driving change ................................................................................... 49 5.2.3 Risks .............................................................................................................. 49 5.2.4 Firm responses to change.............................................................................. 50 5.2.5 Strategic intentions: Technology investment ................................................. 51

Page | 4

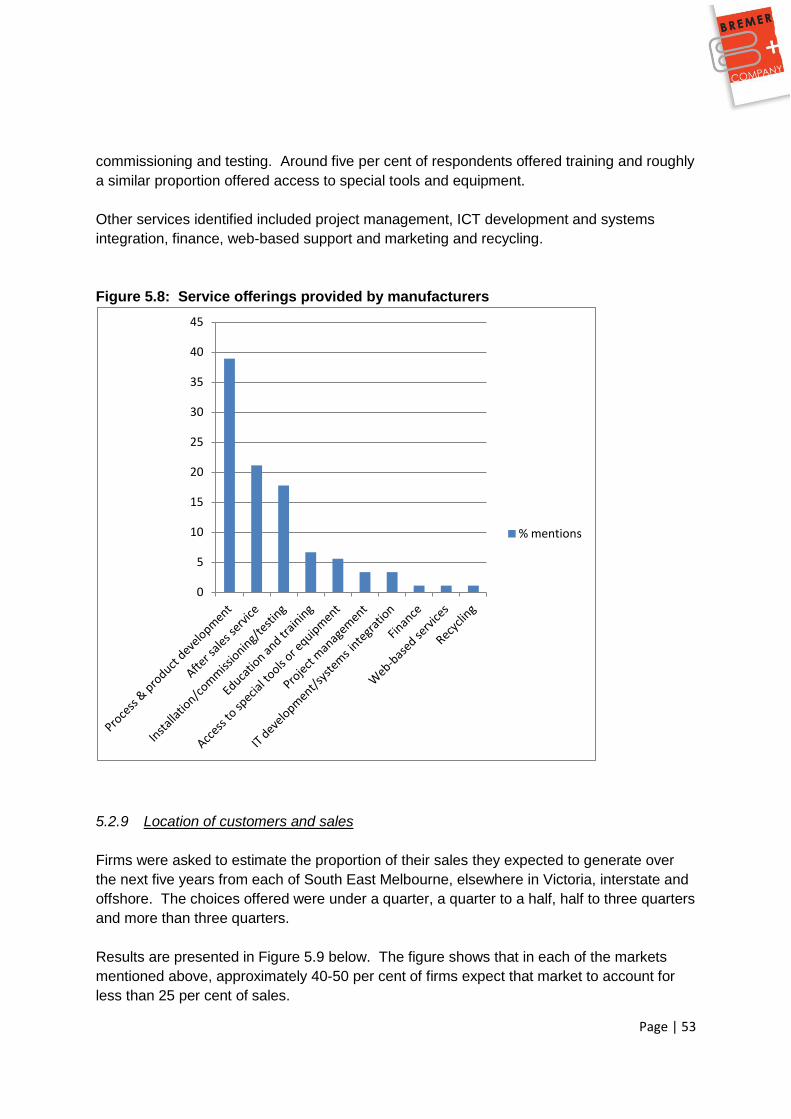

5.2.6 Strategic intentions: Capability acquisition .................................................... 52 5.2.7 Market development ...................................................................................... 52 5.2.8 Service offerings ............................................................................................ 52 5.2.9 Location of customers and sales .................................................................... 53 5.2.10 Engagement with local suppliers .................................................................... 54 5.2.11 Opportunities for local collaboration ............................................................... 55 5.2.12 Regional manufacturing leaders..................................................................... 55

5.3 Labour force issues .............................................................................................. 55 5.4 Supporting infrastructure ....................................................................................... 56

5.4.1 Economic infrastructure .................................................................................. 56 5.4.2 Public Research Organisations ...................................................................... 57 5.4.3 Education and Training .................................................................................. 57 5.4.4 Supporting organisations ................................................................................. 58

6: Findings ......................................................................................................................... 63 6.1 Forces shaping manufacturing .............................................................................. 63

6.1.1 Structural issues shaping Australian manufacturing ....................................... 63 6.1.2 Global integration of manufacturing activity .................................................... 64 6.1.3 Organisation of production ............................................................................. 64 6.1.4 Technology .................................................................................................... 65 6.1.5 Sustainability.................................................................................................. 65

6.2 Firm readiness and capabilities ............................................................................. 65 6.2.1 Firm leadership and management .................................................................. 65 6.2.2 Sources of value ............................................................................................ 67

6.3 Infrastructure ........................................................................................................ 67 6.4 Regional manufacturing leadership and morale .................................................... 68 6.5 Interfirm linkages .................................................................................................. 69 6.6 Support mechanisms ............................................................................................ 69 6.7 Education and training .......................................................................................... 70 6.8 Land supply .......................................................................................................... 70

7: Shaping the strategy – strategic considerations ............................................................. 71 7.1 Strategic options – possible elements of a strategy .............................................. 71 7.2 Overview of the strategic environment .................................................................. 72 7.3 Focus of activity .................................................................................................... 74

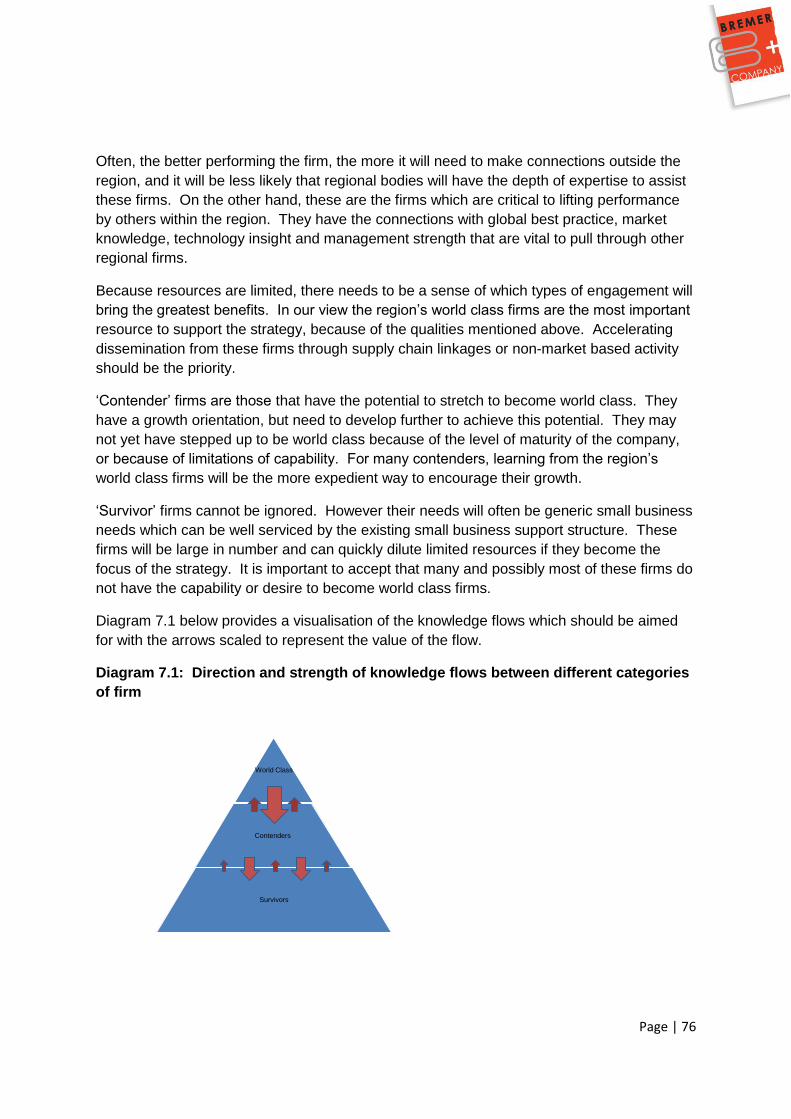

7.3.1 Firms, sectors and other commonalities ............................................................. 74 7.3.2 Knowledge flows and segmentation of firms ....................................................... 75 7.3.3 Attraction and retention of manufacturing firms .................................................. 79

7.4 Leadership ............................................................................................................ 79 7.5 Resources ............................................................................................................ 80 7.6 Timeframe ............................................................................................................. 82

8. Strategy and recommendations ..................................................................................... 83 8.1 Theme 1: Shared vision of viable manufacturing of the future.................................. 84 8.2 Theme 2: Global outlook .......................................................................................... 85

8.2.1 Global view ........................................................................................................ 85 8.2.2 Global connections ............................................................................................. 86

8.3 Theme 3: Encouraging a culture of change .......................................................... 86 8.4 Theme 4: Building on the strength of existing bodies ........................................... 87 8.5 Theme 5: Leadership and management skills ...................................................... 89 8.6 Recommended Actions ......................................................................................... 90

Page | 5

Abbreviations

ABS Australian Bureau of Statistics

AiG Australian Industry Group

ANZSIC Australian and New Zealand Standard Industrial Classification

ASX Australian Securities Exchange

BIG Business Improvement Group

CAD Central Activity District

CBD Central Business District

CGD City of Greater Dandenong

CNC Computer Numerical Control

CRC Cooperative Research Centre

CSIRO Commonwealth Scientific and Industrial Research Organisation

DBI Department of Business and Innovation

DDB Dandenong Development Board

DIISR Department of Innovation, Industry, Science and Research

EC Enterprise Connect

emp Employment

GMC Geelong Manufacturing Council

HPC High Performance Consortium

ICN Industry Capability Network

ICT Information and Communications Technology

GDP Gross Domestic Product

LGA Local Government Authority

MNC multi national corporation

nec not elsewhere classified

NIEIR National Institute for Economic and Industry Research

OECD Organisation for Economic Cooperation and Development

OHS Occupational Health and Safety

PAC Principal Activity Centres

PRO Public Research Organisation

R&D Research and Development

RDA Regional Development Australia

SEBN South East Business Networks

SEMIP South East Melbourne Innovation Precinct

SEMMA South East Melbourne Manufacturers Alliance

SME Small and Medium Enterprise

SMRDA Southern Melbourne RDA

SMRDAC Southern Melbourne RDA Committee

STRIP (Monash) Science Technology Research and Innovation Precinct

TAFE Technical and Further Education

TCF Textiles, Clothing and Footwear

VA Value Added

VCAMM Victorian Centre for Advanced Materials Manufacturing

VCEC Victorian Competition and Efficiency Commission

Page | 6

1. Executive Summary

This report is about the future of manufacturing in South East Melbourne, source of

around 40 per cent of Victoria‘s manufacturing value added. It looks beyond the

immediate business cycle to identify the issues that, if addressed, can raise the trajectory

of the region‘s manufacturing sector. It was commissioned by the Southern Melbourne

Regional Development Australia Committee in partnership with South East Business

Networks and the South East Melbourne Manufacturers‘ Alliance.

The global manufacturing sector has been reshaped over the last twenty years. Based

on the rapid change in global markets, Australian and Victorian manufacturers would

have been in for a turbulent time even if they had already been well integrated into global

manufacturing markets. As it stands, they have had to face the same changes as their

counterparts while also coping with the specific weaknesses in the structure of

Australia‘s manufacturing sector. These include legacy issues from protection, few large

indigenous manufacturers to pull through small firms, and a long tail of very small firms

with limited capabilities. The appreciation of the dollar and the volatility around it

presents yet another dimension which has some manufacturers overwhelmed.

Modern manufacturing has moved beyond the paradigm of the 1950s and 1960s and,

although it is no longer a large employer of unskilled labour, the manufacturing sector is

a vital part of the economy of South East Melbourne. There are some outstanding firms

in the region which demonstrate that regional manufacturers can take a position in global

markets, be profitable, provide highly skilled and interesting jobs, and lead innovation.

Our assessment is that a regionally-based initiative for manufacturers in South East

Melbourne can improve the prospects for firms in the region. In making this observation,

we note that there are already worthwhile initiatives in place to support manufacturers

through Commonwealth and Victorian government offerings, and those of specialist

regional bodies such as SEBN and SEMMA.

It only makes sense to proceed with a regionally-based strategy if it delivers

opportunities beyond those already in place. We see two obstacles in this regard. First,

to implement a regionally-based strategy will require a level of energy, commitment and

vision. This can only come from manufacturing leaders. Generally, the leaders of the

best firms are involved in regional bodies in only a passive way. Without their authority,

influence and credibility a strategy is unlikely to be well focused and attract interest,

support and resources from stakeholders. We see the absence of top-level industry

leadership as the primary obstacle to proceeding with a strategy. The second and

related issue is that it is not clear which of the several relevant regional bodies would be

the ‗owner‘ and primary driver of the strategy. There would need to be a clear

governance structure around the strategy, recognised and accepted by the main regional

stakeholders. We have proposed that SMRDAC should promote the strategy to

stakeholders and seek resources for its implementation, but the strategy needs to be led

by industry.

Page | 7

Active engagement of leading firms is important not only for the credibility they lend to a

strategy, but because they are potentially a fundamental resource for upgrading efforts.

The best firms will be those which are in contact with international best practice, leading

edge developments and other innovation and market information. While some of this will

be confidential, it is by engaging with other firms that the leaders, often unconsciously,

transmit this knowledge to other regional firms. However, in many cases the linkages

between firms in the region appear weak and so the transmission of knowledge and the

potential for learning is not as strong as it could be. Hollowing out of local manufacturing

supply chains is exacerbating this and increasing the sense of isolation in many firms.

Nevertheless, the project survey shows there is a reasonable base on which to build with

nearly 40 per cent of participants indicating at least one local manufacturer was a critical

supplier to their business. The ideal arrangement is a regional manufacturing community

that is well connected both through market transactions and by participation in

networking and other non-market linkages. The most useful connections are directly

between firms and not through intermediaries, although intermediaries are critical in

making some of the initial connections.

We do not recommend a sector-based strategy. Sectors make less sense in the world of

modern manufacturing as firms bundle services and products, innovate at the

intersection of disparate technologies, and supply many different types of customer and

markets. There is more chance of success in building on the strengths of world class

firms and working with firms around commonalities such as supply chains, markets,

technologies and innovation. There will potentially be many such commonalities and it

will not be possible to be involved in them all.

Many existing activities will fit within the strategy‘s framework. Any additional resources

obtained are likely to be modest. Therefore a clear sense of priorities will be needed.

Without creating difficulties arising from exclusion, we suggest the strategy should focus

primarily on the linkages between world class firms and potential leaders. A primary goal

will be to diffuse knowledge in order to expand insights and lift capabilities of firms

around management and leadership.

Any positive changes to the environment in which firms operate should be supported.

New transport, utilities, broadband and so on all have the potential to impact positively

on the performance of the manufacturing sector in South East Melbourne. However in

the short to medium term, the impact on the locational decisions and viability of existing

businesses will be minor. It does not matter how good the schools, the infrastructure,

the land supply or the tax system might be - if business leaders do not have the skills to

profitably run their business, all else is to no avail. The quality of the regional economic

environment will be of prime significance in attracting new manufacturers to the region

rather than retaining those which are already located here.

We suggest that a regional strategy should be formed around a long term focus on a set

of themes intended to lift the performance of firms. The themes we have suggested are:

Page | 8

Creating and promoting a shared vision of a viable manufacturing sector in South

East Melbourne

Expanding the global outlook for South East Melbourne manufacturers

Encouraging a culture of anticipatory change

Building on the strengths of existing bodies

Leadership and management skills

The themes are inter-related and suggest actions, some of which are a continuation of

existing activities.

Finally, it is important to recognise the business of facilitating change is a hard one.

Firms themselves are responsible for devising their strategies and managing their

businesses. The best incentives they can have is exposure to market forces,

supplemented with knowledge and information to understand what price signals mean. It

is in this latter role that regional and other bodies can be of assistance. Because

resources are limited it is important for these bodies to develop decision-making

arrangements which have the highest chance of reaping positive change. Identifying

and nurturing those firms with the potential to become leaders, introducing and

facilitating linkages between potential leaders, and other leading firms which are sources

of innovation are among the most valuable functions regional bodies can undertake. A

strategy to lift regional manufacturing performance will require a concerted effort which

will extend over many years.

Page | 9

2. Project objectives and methodology

2.1 Objectives

The brief for this project was to develop a strategy to strengthen the manufacturing

sector in South East Melbourne, to help it be more competitive and viable over the

medium to longer term. The focus of the project is on the future. The purpose in looking

at the present is to gain insights and identify trends which could be relevant to the future.

2.2 Defining manufacturing

The Australian Bureau of Statistics (ABS) defines manufacturing as:

The Manufacturing Division in the Australia and New Zealand Standard Industry

Classification (ANZSIC) includes units mainly engaged in the physical or chemical

transformation of materials, substances or components into new products (except

agriculture and construction). The materials, substances or components transformed

by units in this division are raw materials that are products of agriculture, forestry,

fishing and mining, or products of other manufacturing units. Units in the

Manufacturing Division are often described as plants, factories or mills and

characteristically use power-driven machines and other materials-handling

equipment. However, units that transform materials, substances or components into

new products by hand, or in the unit's home, are also included.

Activities undertaken by units incidental to their manufacturing activity, such as

selling directly to the consumer products manufactured on the same premises from

which they are sold, such as bakeries and custom tailors, are also included in the

division. The view excludes manufacturing activities undertaken by private individuals

or organisations whose principal activity is not manufacturing. This is because an

ANZSIC, or industry code, is allocated based on the predominant activity of an

organisation. It is important to understand this difference between manufacturing

activity and manufacturing industry as most of ABS statistics on manufacturing are

based on an industry view.

Manufacturing covers a myriad of inputs, processes and products. It embraces

production of thousands of different types of goods. These range from ships to sugar

to sheep shearing equipment, and from micro circuits to motor vehicles to medicines.

The number and complexity of the processes involved in the production of these

goods varies. The extent of transformation involved in these processes form the

basis of a view of manufacturing which differs from the standard industry, or ANZSIC,

view. Some products are simple primary product manufactures such as flour, cheese,

tanned hides and skins and pig iron. Some are simply transformed manufactures

such as basic metal shapes (billets, coils, ingots), Portland cement, basic organic

Page | 10

and inorganic chemicals (such as caustic soda). Others are moderately transformed

manufactures such as wire rods, metal pipes and tubes, basic glass, soap and

detergents, textile fabrics and tissue paper, while others are elaborately transformed

manufactures such as prefabricated metal buildings, wire products, glassware,

ceramic products, paints, medicines and perfumes.

The degree of mechanisation involved in the production process provides another

view of manufacturing. Manufacturing in Australia covers a wide range of situations

from highly mechanised production lines using robotics to simple mechanical

activities such as soft drink bottling or concrete mixing through to production of fine

jewellery by hand.

This formal definition of manufacturing, which is the basis for the vast majority of the

statistics which describe the sector, is problematic. As we discuss further in Section 3.3,

the trend is towards manufacturers bundling of services with goods and their businesses

being providers of solutions rather than transformers of materials. This makes the

question of what constitutes a manufacturer less clear. Over time many ‗manufacturing‘

firms will find the proportion of their revenue sourced from the activities defined in the

formal definition will decline.

2.3 Defining the region

The region covered in this report is that of the Southern Melbourne RDA. It comprises

ten Local Government Areas (LGAs): Port Phillip, Stonnington, Bayside, Glen Eira,

Kingston, Greater Dandenong, Cardinia, Casey, Frankston and the Mornington

Peninsula.

This area incorporates a significant part of Australia‘s manufacturing sector. There were

6,613 manufacturing businesses in this area in 2009, representing 7.2 per cent of all the

manufacturing businesses in Australia, and 34.8 per cent of all the manufacturing

businesses in Melbourne. While not covered by the Southern Melbourne Regional

Development Australia Committee (SMRDAC), Monash and Knox have strong

commercial links to the South East region. These areas too have a sizeable number of

manufacturing firms that no doubt are involved in significant trade with firms in the formal

Southern Melbourne region.

2.4 Method

The primary determinants of firm competitiveness are the capabilities, systems, plant,

resources, leadership and business model which the firm itself brings to bear in its

activities. Firm competitiveness is also influenced by aspects such as infrastructure,

availability of specialised factors, connections between firms and Public Research

Organisations (PROs), and linkages between firms themselves. Of course beyond those

factors general economic and social conditions, derived from the international economy

Page | 11

and influenced by state and Commonwealth Government actions, are important

elements of the business operating environment.

The project methodology has involved these activities:

Reviewing previous reports and existing material on manufacturing in South East

Melbourne

Identifying global trends shaping manufacturing

Analysing trends in manufacturing in Australia

Preparing a statistical profile of manufacturing in the region

Engaging senior managers in manufacturing firms, either by interview, survey or

workshop, to gauge the key aspects of their strategies for the future. This survey

and interview work focused on industry leaders and so is not intended to be

representative of all the firms in the region

Identifying hard and soft infrastructure issues in South East Melbourne

Analysing this information in the context of past and current policy trends and

bringing the key information obtained above into findings

From these stages we have proposed a strategy to lift performance at the firm level. The

strategy involves five themes that focus primarily on how regional bodies can assist firms

to upgrade and maintain and increase their competitiveness.

2.5 Policy context

The place of manufacturing in the Australian economy continues to attract government

interest, as it has done at numerous stages over the past sixty years.

In March 2011, the Victorian Government announced a review of manufacturing industry

policies. It commissioned the Victorian Competition and Efficiency Commission (VCEC)

to report on the existing program mix and propose priorities for the future. VCEC

published a draft report in June 20111 and presented its final report to Government in

September 2011. The final report and Government response was initially expected in

September 2011 but is not yet public.

The draft report set out a set of principles intended to ensure any interventions produced

a community benefit. VCEC endorsed the concept of moving programs to an

‗intelligence-based‘ approach. The thinking is that the needs of firms should be

assessed on an individual basis and assistance packaged to meet those needs, rather

than being delivered through an inventory of standardised offerings.

It is anticipated that the Government will respond to the VCEC report shortly and it is

possible that there may be opportunities for regional bodies such as SEMMA and SEBN

Page | 12

to obtain resources to pursue initiatives consistent with the strategy articulated in this

report.

The Commonwealth Government also has established a task force to map out a shared

vision for the future of Australia‘s manufacturing sector and to help strengthen local firms

as they adapt to changes in our economy, including the rise of Asia. It will identify a plan

for how best to leverage existing efforts, including government policies and programs, to

capture the opportunities and respond to the challenges facing manufacturing. The

Commonwealth has indicated that it wants to see the sector move up the value chain by

building up its skills and innovation base.

Depending on outcomes, once again there may be opportunities for regional bodies to

obtain resources to take the strategy forward.

Page | 13

3: Manufacturing in a Global Context

Many forces are shaping the global manufacturing sector. Our goal in this section is to

identify and discuss the implications of these.

3.1 Forces shaping the global economy

At the macro-level, four ‗mega-trends‘ are shaping the international economy:

3.1.1 Changing players in the international economy

Rapid economic growth outside western economies is creating new players with

considerable market power. Faster growing economies like Brazil, Russia, China and India

are having a substantial impact on global markets. It estimated that by 2025 India and China

will account for 25-40 per cent of the total world demand for goods and services, displacing

North America and Europe as the major global sources of demand.2 In addition, emerging

economies like Indonesia, Vietnam and the Ukraine are expected to become significant both

as manufacturing locations and consumer marketplaces. Some estimates indicate China‘s

GDP will be larger than that of the US by 2025 and that India will have a larger economy

than the US by 2050.

3.1.2 Rising cost of resources

The cost of resources increases both as stocks diminish. They will also increase as a price

is placed on carbon and together will affect the price of energy, waste, water and carbon-

intensive inputs into production.

Resources will become scarcer as high grade reserves are exhausted. Figures 3.1 and 3.2

below demonstrate that the quality of new finds of oil and other minerals is diminishing. The

implication is that the cost of extraction and refining becomes higher as high grade deposits

are exhausted, which means that the price of resources will rise over time.

Figure 3.1: New discoveries of oil, 1930-1950

Page | 14

Figure 3.2: Quality of discoveries of new deposits of selected ores, 1840-2005

3.1.3 Reach of Information and Communications Technology (ICT).

The pervasiveness of digital technologies and the world wide web have changed forever the

nature of information management and communication. The exponential growth of capacity

in this area is demonstrated by Moore‘s Law, coined in 1965, which proposed that the

number of transistors which could be placed in an integrated circuit would double every two

years. While industry experts expect this trend to slow or reverse by the mid 2010s, the last

fifty years have witnessed an extraordinary expansion of digital technology based on rapidly

expanding capabilities and falling costs.

Figure 3.3: Transistor counts on integrated circuits, 1971-2011

General Trend

Page | 15

3.1.4 Growth of services sector

A fourth factor is the growth of services within economies and the emergence of international

trade in services, facilitated in part by advances in information and communication

technologies. Services are the dominant sector in all OECD economies today, generally

accounting for 65-80 per cent of value added and the proportion of ‗internationally exposed‘

services continues to rise.

3.2 Pressures on the business of manufacturing

3.2.1 Origins of manufacturing organisation

Over the last century, manufacturing evolved based on high volume and mass production.

Products had standard designs and parts were interchangeable. The emphasis was on long

production runs and increasing economies of scale. Large manufacturers of complex

products like vehicles had vertically integrated businesses, processing raw materials at one

end and controlling distribution and marketing channels at the other.

Firm growth was based on increasing volume. Large inventories were used to maintain

material flows and to buffer production in the face of changes in supplier and customer

behaviour. Manufacturers relied on mass markets, but production facilities were primarily

regionally focused.

Production followed a sequential process of product conception, engineering, manufacturing,

marketing, sales, and after sales service. The entire process, together with a variety of

services, was undertaken in stand-alone production facilities. Inside the factory, machinery

and equipment were stationary and heavily reliant on manual labour. Each process had a

limited number of variations.

Organisations ran along Taylorist principles of scientific management. Production flexibility

was gained simply by expanding or contracting production lines, by adding or subtracting

people who were to carry out specific tasks and could easily be replaced. It was the job of

management experts to plan and make decisions, and of workers simply to carry them out.

Static job assignments were given to workers on the shop floor. Each worker was trained for

a small number of tasks and given responsibility for a particular machine, process, or

function along the production line. Tasks were conventional and repetitive. Even in smaller

enterprises, responsibilities were usually clearly divided between management and workers

on one hand, and among workers on the other. Quality was the job of inspectors who

reviewed operations periodically. Performance benchmarks were defined internally, most

commonly by accounting departments. Problems were identified primarily as a result of

customer complaints.

This situation has been revolutionised. The challenges of the global business environment

have made traditional manufacturing increasingly obsolete. More flexible production systems

Page | 16

have emerged together with quality-oriented business practices that aim to serve customers

better and at lower costs.

3.2.2 New customers and changing demands

Emerging markets are creating new sources of rapidly growing demand for products and

services on the part of consumers and businesses alike. At the same time consumer tastes

in established markets are not static, and needs are becoming more specific and at the

same time more diverse. Aging populations, changing life patterns, higher incomes leading

to changes in consumption preferences, immigration and other demographic trends are

opening new markets and closing old ones. Innovation is also driving change in customer

needs and expectations. Demand is for greater variety, better quality, performance and

service, at lower cost.

3.2.3 More stakeholder requirements Manufacturers, and other businesses, must observe a growing set of requirement set not

only by customers but by other stakeholders – the ‗social license to operate‘. They must

deliver returns to their investors and value to shareholders as well as meet responsibilities to

their employees and the communities in which they operate. Manufacturers also have to

respond to more and more stringent requirements set by governments and other regulating

agencies. These rules cover the way companies are run, the nature of their goods and

services and the way they are produced, the health, safety and security of employees and

the public at large, as well as current and future impacts on the environment.

3.2.4 Intense competition

Manufacturers are facing intense competition in their efforts to defend and grow market

shares. Globalisation of markets reaches as far as individual customers through electronic

commerce which provides the ability to source products, services, innovation and

technologies on a global basis. Geographic proximity is diminishing as a competitive

advantage.

The emergence of highly populated and rapidly industrialising economies like China and

India, with relatively low labour costs, has shifted patterns of production across industries on

a global basis and disrupted established production systems.

3.2.5 The pace of innovation and development of new technologies

New and improved products and processes are being brought to market at a more rapid

pace. The application of information and communication technologies has revolutionised

control and information systems in manufacturing. This has allowed more outsourcing,

integration, automation and remote management of production processes. The rate of

change continues to accelerate as a result of new and transformational applications of

software programming, computing and information technologies, biotechnology, micro- and

Page | 17

nano- technologies, new materials, energy technologies, sensors, robotics, and to more

advanced machining, measuring, and automated systems.

Technology is contributing to fundamental changes in the processes of innovation. Some

examples:

‗eScience‘ is being used by companies such as Rolls-Royce to draw on wide ranging

expertise;

Virtual reality is being applied in fashion and clothing industries to improve consumer

choice;

Simulation and modelling is being deployed to predict the effects of products;

Rapid prototyping using 3D printers opens up the prospect of digital fabrication, using

fabrication laboratories to by-pass existing manufacturers3; and

Mixed reality simulation to streamline prototyping such as in the design of the Boeing

787 Dreamliner.4

The pace of innovation has been assisted by growth in production and trade in intermediate

products - that is, products that are designed to be incorporated into or combined with a final

product. So, for example, in the motor vehicle sector it is common to see innovation being

led by component manufacturers – parking sensors, electronic monitoring and control,

lighting, and so on. It is increasingly common for innovation to be outsourced to component

suppliers with their own highly specialised knowledge available for the innovation effort.

3.2.6 Commoditisation and the integration of global markets

Prices of manufactured goods are set in global markets and determined by global supply

and demand. For most manufacturing sectors today, intense competition and excess

capacity are driving down prices, but the cost of raw materials is rising as demand increases

and supply becomes scarcer. The ‗commodity threshold‘ continues to creep up as products,

technologies and features that were previously reserved for premium products and markets

become expected in standard offerings. Base model computers and mobile phones, cars

and other products have all become commodities that manufacturers seek to differentiate

with brands, bundling with services and continual innovation. Production must be highly

efficient for firms to remain relevant.

3.3 Responding to change

Over the last thirty years manufacturers have been moving toward increased flexibility,

higher quality standards, and greater responsiveness to the needs of a larger array of

customer segments.

World-class competitiveness requires product differentiation, flexible and lean production

systems, and supply chains and business networks aligned to deliver value to customers at

Page | 18

competitive costs. Contemporary manufacturing is characterised by innovation and the

ability to make a variety of high value products. The objective is rapid response to variable

and changing customer demands.

3.3.1 Flexible manufacturing

Flexible manufacturing processes are adaptable and reconfigurable for short, low volume

production runs. The emphasis is on process change and product diversification. But

economies of scale are still important. As products become more specialised, manufacturers

have looked to high volume customers and increasingly to international markets to provide

sufficient volumes.

Time has become a key competitive factor, in addition to product costs, quality, and

performance. Manufacturers are reducing human effort in the factory, their stock of

inventories, the space it takes to manufacture, and the time it takes to get products out the

door. Their objective is to cut changeover times from hours to minutes, avoid downtimes for

repair, simplify the information systems that track the flow of materials and industrial

processes, and arrange manufacturing processes into cells that both increase flow

efficiencies and are capable of achieving regularly changing rather than constant production

schedules. Lean management methods are pervasive across manufacturing systems and

help in eliminating waste.

Flexible manufacturing involves minimal inventories. Materials and components are received

and goods supplied just in time, or as required – and manufacturers pay a steep penalty if

they are unable to when they cannot. Processing, fabrication, and assembly technologies

are automated and integrated through computer networks such as in additive manufacturing

or 3D printing. Product differentiation is achieved through design and quality assurance,

logistics and distribution systems, financing and after-sales service and there is a premium

on customer service.

Organisational design in flexible manufacturing is flat with horizontal management methods.

There are complex communication systems to integrate all of the product development,

production, and services functions that go into meeting customer demand. There has to be

direct communication among senior managers, marketing, design, engineering, and

manufacturing operations personnel. In flexible manufacturing systems, communication

systems extend beyond the firm and are integrated across supply chains and business

networks.

Teams of multi-skilled workers are empowered with responsibilities to make operating

decisions, assure quality standards, and solve problems as they arise. On-the-job training is

a necessity to improve technical skills, maintain quality, and increase flexibility.

Quality products, processes, and procedures are essential to meet customer requirements.

Flexible manufacturing requires that quantifiable quality controls apply to all aspects of the

Page | 19

business – from corporate governance to operations and financial management to supply

chains, production, information systems, and preventative maintenance.

The rate of change is increasing exponentially and because of this it is more difficult for

manufacturers to catch up if they have missed earlier waves of change.

3.3.2 Evolution in how manufacturers create value

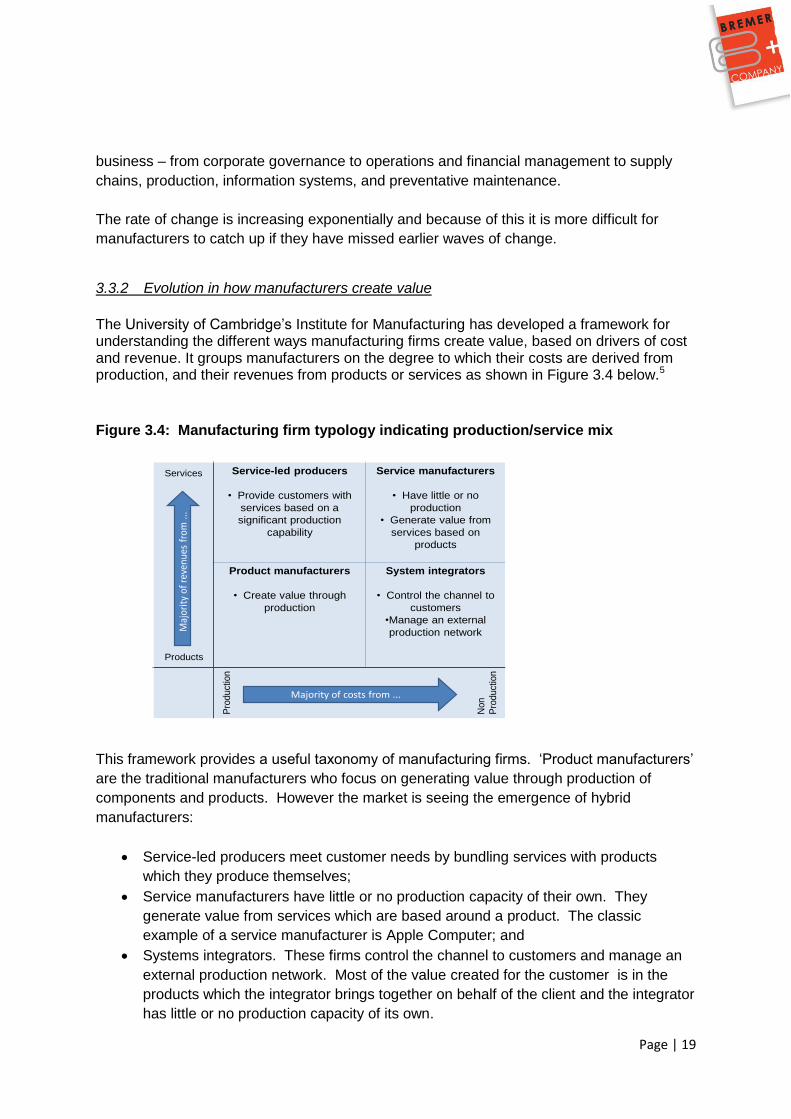

The University of Cambridge‘s Institute for Manufacturing has developed a framework for understanding the different ways manufacturing firms create value, based on drivers of cost and revenue. It groups manufacturers on the degree to which their costs are derived from production, and their revenues from products or services as shown in Figure 3.4 below.5

Figure 3.4: Manufacturing firm typology indicating production/service mix

This framework provides a useful taxonomy of manufacturing firms. ‗Product manufacturers‘

are the traditional manufacturers who focus on generating value through production of

components and products. However the market is seeing the emergence of hybrid

manufacturers:

Service-led producers meet customer needs by bundling services with products

which they produce themselves;

Service manufacturers have little or no production capacity of their own. They

generate value from services which are based around a product. The classic

example of a service manufacturer is Apple Computer; and

Systems integrators. These firms control the channel to customers and manage an

external production network. Most of the value created for the customer is in the

products which the integrator brings together on behalf of the client and the integrator

has little or no production capacity of its own.

Service-led producers

• Provide customers with

services based on a

significant production

capability

Service manufacturers

• Have little or no

production

• Generate value from

services based on

products

Product manufacturers

• Create value through

production

System integrators

• Control the channel to

customers

•Manage an external

production network

Pro

duct

ion

Non

Pro

duct

ion

Majority of costs from ...

Products

Services

Maj

orit

y of

rev

enue

s fr

om ..

.

Page | 20

Services (design, quality assurance, installation, training, financing, after-sales services,

remote monitoring, disposal, etc) can each be distinguishing elements in adding customer

value. To provide these services will often require collaborative arrangements between

manufacturers and services firms such as those in software, IT and electronics.

These developments challenge the traditional notion of a manufacturer as being in the

businesses of the physical or chemical transformation of materials, as outlined in the ABS

definition in Section 2.2. The activities which distinguish a manufacturer are becoming much

less clear. Meanwhile the need to acquire new skills in accessing technology and

collaborating is becoming more urgent.

3.3.3 Customers and markets

Manufacturers will continue to compete on delivering customer value at lower and lower

prices. That will reinforce the trend towards individual products meeting individual needs –

and increase opportunities for packaging of services with products. Competitive cost

structures will be needed to ensure that customisation is commercially viable - the ultimate

goal is the competitive batch of one.

Mass customisation will entail businesses tailoring product functionality, design, and service

to satisfy individual customer requirements, but also making differentiated products at high

speed and in high volume production runs in order to keep unit costs to a minimum. Digital

manufacturing allows a high volume production run of ‗cousin‘ products using the same

feedstock and tooling, with unique customisation of batches of one within the production run.

Manufacturers will have to accelerate flexibility through continuous innovation and shorter

production runs that can accommodate changing and more specialised customer

requirements together with shorter product life cycles.

Mass customisation will require further changes within the business of manufacturing.

Information systems will need to quickly identify customer specifications, turn them into work

orders, and create pull systems throughout supply chains and production processes.

Cost increases can no longer automatically be passed on to customers. Manufacturers

have to focus on delivering customer value at the lowest possible cost, knowing that

customers can source globally. Returns are maximised by meeting new or more specific

customer needs quickly, rather than by increasing production volumes and selling more of

the same product. As noted above, packaging of services with the product can be an

important aspect of strategies to escape the effects of commoditisation.

Page | 21

3.3.4 Manufacturing operations

Customer-pull systems are replacing production-push manufacturing which means systems

can be reconfigured quickly for shorter production runs. Greater variability is allowing for

greater control over product and production defects through quantitative methods of quality

assurance. Processes are more highly automated, controlled and integrated through

advanced information and communication technologies which may also allow remote

operation of plant.

Process efficiency and cost reductions are being driven throughout manufacturing

businesses, from materials handling and production processes to information systems and

supply chain logistics. Time has become the driving consideration in profitability. Companies

are striving to reduce wait times, down times, and the time required for product and process

changeovers.

Strategies for growth are coming to rely on product and process innovation, not simply

adding volume. Consequently innovation is permeating organisations and is understood as

a broad concept, no longer solely as a technical activity, the province of research and

development and engineering departments. Innovation is important on the shop floor, in

purchasing and logistics, in marketing and design, as well as in management systems.

Workers are part of the innovation effort and their work has become more knowledge-

intensive with greater flexibility for individual decision making. Workers need a higher level

of technical skills and experience, so they can engage in problem solving, multi-tasking,

teaming and collaboration.

3.3.5 Organisation of production: Global supply chains

Manufacturers are increasingly serving customers around the globe and are restructuring

their operations, production systems, and supply chains to achieve this. They will continue to

seek the rapidly expanding markets of emerging economies. E-business technologies will

allow manufacturers to connect anywhere at any time with customers around the world. In

Australia the national broadband is expected to provide a platform for significant expansion

in the use of digital technologies by manufacturers across a wide range of business

functions.

As market reach expands, production and services will be sourced on a global basis to take

advantage of the best skills, technologies, and cost structures. This will allow firms to

increase their profit margins while offering customers higher value at lower price.

In the classic integrated manufacturing businesses of the early twentieth century, such as

the Ford Motor Company, most of what was needed was produced by the company. At one

stage Ford produced its own steel and owned its own forests. However, over time integrated

production has evolved into systems with tiers of suppliers with their own supply chains and

value networks. With globalisation, specialisation, and advances in information technology,

Page | 22

supply chains stretch internationally and are intermingled, with firms participating in many

supply chains. Where once firms competed with each other, now it is supply chains that

compete and innovation takes place at all it levels and stages. Companies are participating

in consortia, strategic alliances, and joint ventures to leverage their resources and expertise

and create opportunities for new product and market development.

While larger businesses are expanding their operations around the world, at the same time

they are consolidating investment in research, design, engineering, and other key decision-

making functions in one or only a few locations. Few if any Australian owned-firms are large

―primes‖. The vast majority of Australian manufacturers are either in the lower reaches of

the supply chain or have relatively small niche positions in markets for consumer products.

In global production, Australian manufacturers need to move from supply chains oriented

toward the Australian market to global supply chains.

3.3.6 Computer integrated manufacturing

The manufacturing systems of the future will embody the intelligence of advanced software

applications, modelling and simulation capabilities. They will be built around integrated

systems of human and artificial intelligence – allowing for the specification, communication,

and technical translation of exact customer expectations; the application of machine

intelligence, expert systems, and neural networks in production; and the design,

coordination, and integration of complex production, logistics, and business systems. Future

production systems are being planned on the basis of virtual engineering and virtual

factories: Computer automated technologies are allowing manufacturers to combine design,

engineering, testing, scheduling, production, maintenance, quality assurance, services, and

supply chain management into single processes. Manufacturing capabilities will then depend

on the efficient management of information and the rapid translation of that information into

production systems.

The ‗factory‘ will become an information network. Customers will participate in the design

and testing of products in accordance with their specific needs. Virtual reality will play a key

role in permitting customer participation in design and engineering. Intelligent equipment,

sensors, robotics, and smart materials will help to control quality and process flows.

Customer requirements will be communicated to computer-integrated and mobile machining,

processing, and material delivery systems. Computer integrated factories will allow for

machines and production cells to automatically reconfigure themselves on the production

floor in response to new orders or new product variations. Purchasing and scheduling will

take place automatically as orders are received. Machines will be capable of producing a

wide variety of products and parts. Fully automated systems will allow for continuous ―lights-

out‖ production, and people will be employed to maintain, program, schedule, and plan

processes of change. Virtual engineering processes will integrate simulation, modelling,

analysis, testing, diagnostic, and analytical technologies in design, production, and control

functions affecting all aspects of manufacturing.

Page | 23

Manufacturers will be able to control, repair, and service their products remotely. Smart

engineering systems will increase the degree of flexibility and speed up cycle times

significantly. They will integrate and simplify manufacturing processes. They will be the key

to making customisation commercially viable.

ICT and related technologies have provided the capabilities that make flexible, automated

production systems, global supply chains, and global customer reach possible. New

applications of information and communication technologies will continue to revolutionise

manufacturing activity, including the use of advanced modelling and simulation, artificial

intelligence, digital imaging, high density data storage, and virtual reality.

3.3.7 New Enabling Technologies

Other advanced technologies will also transform future manufacturing capabilities, including:

Biotechnology and genetics. Manufacturers are already working with biomaterials,

creating bio-products, and using bio-processes as a result of advances in the science

of genomics.

Nano-technology. Molecular engineering is allowing manufacturers to build things

from their most basic atomic structures up.

Micro-machining. Techniques that exist for producing devices and mechanical parts,

whose size can be measured in microns, will enable greater precision, sensitivity,

and flexibility in micro production processes.

Metrology. Advanced measurement systems will allow for greater precision in

production and process control.

Mechatronics. Systems that integrate sensors, actuators, and control functions in one

intelligent system will improve product precision, performance, efficiency, and ease of

use.

New materials. The development of new materials from bio-materials and advanced

polymers, to light weight composites and superconductive materials are providing

manufacturers with a capacity to develop new and improved products and processes

that can get the job done better for customers at much lower costs.

Smart Materials. Smart materials change shape, colour, form, phase, electric and

magnetic fields, temperature, optical qualities, and other characteristics in response

to external stimuli. Designers will be able to use smart materials to set new standards

in meeting customer needs, as well as simplify products, add features, reduce

material use, and lower the expense of product specialisation. Future smart materials

will be capable of self-diagnosis, repair, and learning.

Fuel Cells and Alternative Energy. Hydrogen fuel cells, solar energy, and nuclear

applications will be used in products and processes as alternative energy sources.

Integrated technologies. Future manufacturing capabilities will be expanded even

more by the integration of these technologies.

Page | 24

3.4 Innovation in business models

Advances in electronics, information and communication technologies, computing

capabilities, software programming, and e-business networks are already revolutionising the

business of manufacturing. While drivers of production technology are important, perhaps

the more significant change is in the manufacturing business model itself.

Business models are the ‗recipe‘ of how a firm plans to generate and capture value – the

firm‘s value proposition, the customer segments it targets, the distribution channels it uses,

how it generates sales, its systems to control costs and how it configures its resources. For

many years manufacturers were able to work within a static business model. But all the

developments outlined earlier require revision of business models, sometimes

fundamentally. The ability to reinvent the business to exploit new technologies, changes in

supply chain arrangements, e-commerce and new channels to customers all point to the

need to be able evolve the firm‘s business model. In many cases this will involve the

acquisition of new capabilities and competencies.

3.5 Implications of technological developments for manufacturers in South East

Melbourne

As illustrated above the implications of these technologies are expected to be pervasive,

touching most aspects of modern life. The impacts on manufacturers in South East

Melbourne will vary, depending on the sectors they operate in. Developments in

biotechnologies, for example, may have a greater effect on food and beverage producers

than on a manufacturer of air circulation equipment for commercial buildings, although even

this cannot be certain with biotechnologies having increasing application in air and water

filtration systems.

Perhaps the broadest impact on manufacturing in South East Melbourne over the next

decade or so will come from a cluster of technologies known as Cleantech. The application

of these technologies is driven by resource constraints (raw materials, energy and water),

community concerns about pollution, and associated policy instruments such as carbon

pricing, waste disposal charges, and recycling legislation (return, recycle, re-use).

Cleantech technologies are expected to affect the way goods are made, the materials used

in manufacturing, the way goods are distributed and sold, and just as importantly the way the

goods are perceived and used by the purchasers, as well as the way they are disposed of.

Energy in particular has a pervasive impact. Energy efficiency is a driver in transport and in

buildings as well as in manufacturing processes. Building design, materials, equipment and

techniques are being pushed by the thermal properties of construction materials in striving

for reduced energy consumption and smaller carbon footprints. Lightweight materials, such

as composites and light metals, are driving change in the manufacture of transport

components. Low emission, energy efficiency and alternative fuels are accelerating

changes in vehicle powertrain systems – from combustion systems, to hybrid vehicles, to

hydrogen and fuel cells, to electric and battery operated vehicles. However, these changes

Page | 25

are occurring at a global scale and only manufacturers who are both technologically

advanced and enjoy a high echelon position in the automotive value chain can expect to

participate in and benefit from these developments. Smart materials, deploying

nanotechnologies, with the capacity to transform themselves and perform a range of

functions, are also expected to be significant in industries as diverse as clothing and textile

products, fine chemicals, surface finishes and coatings, pharmaceuticals and personal

healthcare, building materials, printing and packaging, and transport.

Digital technology is another technology grouping with the potential to transform South East

Melbourne manufacturers. Much of the discussion earlier in this section was on the

combined impact of these technologies and other technologies to trigger changes in the

production processes and the products produced. What is less well understood is that digital

technologies will enable small and medium (SME) manufacturers in South East Melbourne

to transform downstream processes such as delivering high value services and moving up

the value chain. In effect broadband opens the possibility for manufacturers in South East

Melbourne of competing more effectively and extending their reach into international

markets. It is expected to enable them to leverage changes in areas like the business model

(new product offerings - value add services and customer solutions), administration,

customer relationships (sales and marketing), and managing assets and resources.

Page | 26

4: Manufacturing - the Australian Context

In Section 3 we reviewed the key drivers shaping manufacturing on a global basis. This

section is concerned with outlining the underlying trends in Australia‘s manufacturing sector.

This provides the backdrop to consider manufacturing in South East Melbourne.

4.1 Performance of Australia’s manufacturing sector

At the end of 2008-09 there were 91,400 manufacturing businesses in Australia, a three per

cent decline over the previous financial year6. These 91,400 manufacturing businesses

represent about 4.5 per cent of the total 2,050,000 businesses operating in Australia at that

time.

It‘s common to talk of the ‗decline‘ of manufacturing in Australia. It is true that measured as

a proportion of Gross Domestic Product (GDP), manufacturing output peaked in the late

1960s and early 1970s at around 30 per cent of industry value added. However, since then

manufacturing output has continued to grow, but at a lower rate than that of other sectors. It

is this pattern – relatively slower growth of manufacturing, rather than absolute decline -

which drives the change in position of manufacturing in the Australian economy. Chart 4.1

below shows the output of the manufacturing and mining sectors since 1991. Aside from the

disturbance in 2009 from which the sector is still recovering, manufacturing output continues

to increase, up by about 30 per cent over the last twenty years.

Chart 4.1

While output from the manufacturing sector continues to increase, the slower growth with

respect to services and, more recently, mining, means that its relative importance has

declined. Services sector output has come to account for nearly 80 per cent of industry

value added, as shown in Chart 4.2 below which traces contributions to value added from

1991 to the present.

Page | 27

However it should also be noted that changes in production systems means that data

collections tend to understate the overall contribution of manufacturing. As businesses have

become more specialised and focused on core competencies they have outsourced various

activities. This is true in manufacturing as much as elsewhere and so activities which are

now outsourced – for example, logistics, some office functions, specialised technical inputs –

are counted as services outputs where previously they were included as manufacturing

value added because they were performed ―in-house‖.

Chart 4.2

Chart 4.3 shows a similar pattern in terms of employment in the various sectors.

Manufacturing employment has declined from around 14 per cent of the workforce in 1991 to

around 8.5 per cent today. Services employment has increased from around 79 to 86 per

cent, mining has increased to 2 per cent, and, like manufacturing, agriculture has fallen from

5.5 to 2.8 percent.

In absolute terms, the pattern of the past twenty years has been that around 1 million people

have been employed in the manufacturing sector, as shown in Chart 4.4 below. This

number has fallen away after the global financial crisis and it remains to be seen whether

these jobs will be recovered by the manufacturing sector, or the labour will be permanently

transferred to services and mining. Employment in the services sector has grown from

around 6 million people to nearly 10 million over this time.

Page | 28

Chart 4.3

Chart 4.4

Table 4.1 below aggregates this data and provides a measure of overall sectoral productivity

as a ratio of the percentage of industry value added divided by the percentage of

employment for each sector (VA/Emp) for 1991 and 2011. The table shows a small increase

in the sectoral productivity of manufacturing, and a large increase in the productivity of the

agricultural sector. Productivity of the services sector remains constant and there is,

interestingly, a decline in productivity in the mining sector.

Page | 29

Table 4.1: Composition of employment and industry value added, Australia, 1991-

2011

1991 2011

% Emp %VA VA/Emp % Emp % VA VA/Emp

Agriculture 5.5 2.5 0.5 2.8 3.2 1.1

Mining 1.2 11.5 9.6 2.0 10.0 5.0

Manufacturing 13.8 14.7 1.1 8.5 10.0 1.2

Services 79.4 71.0 0.9 86.3 77.2 0.9

Source: Bremer+Company based on Thomson Reuters Datastream

Chart 4.5 below provides another dimension on productivity performance. The chart shows

the value added created for each dollar spent on labour in Victorian manufacturing against a

dollar spent on labour in the Australian mining sector. Over the last ten years, each dollar of

labour in Victorian manufacturing is associated with value added of around $1.80 to $1.90.

The same dollar spent in mining is associated with value added of between $4.00 and $6.50.

This demonstrates the power of the mining sector in being able to pull resources from other

sectors, and its capacity to pay higher wages.

Chart 4.5: Value added generated by a dollar of labour input – Victorian

manufacturing and Australian mining

Page | 30

4.2 Performance of manufacturing sub-sectors

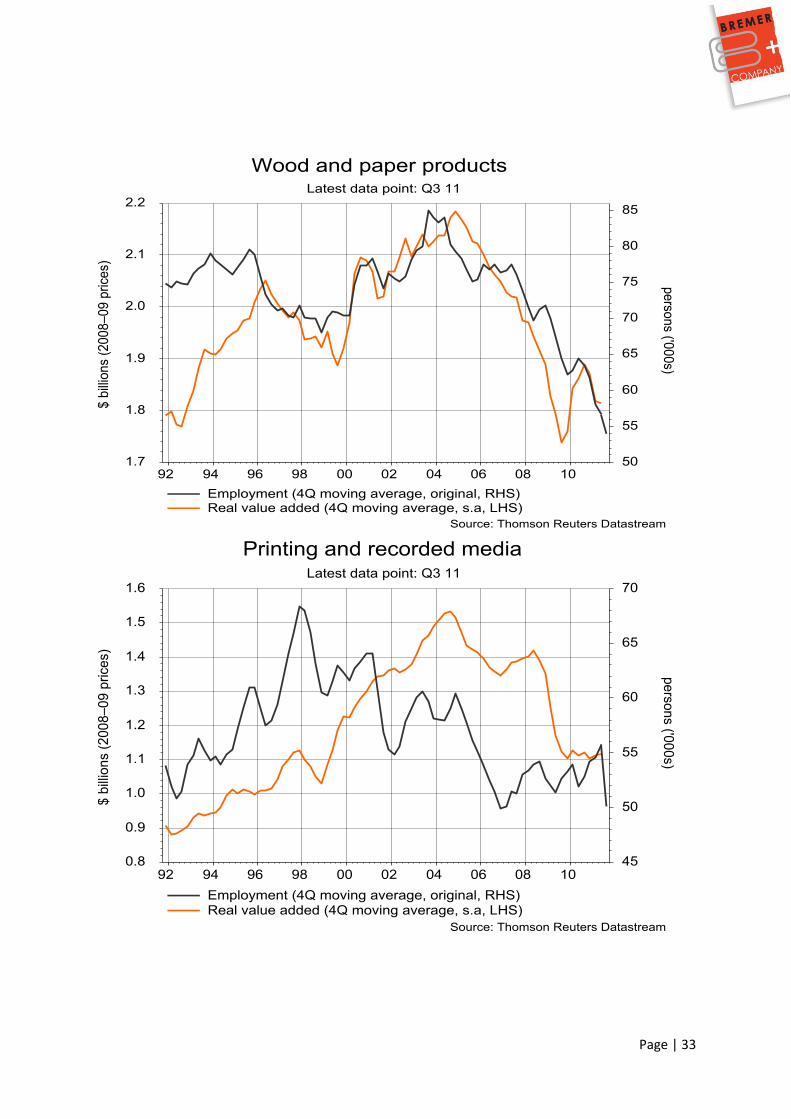

Table 4.2 below summarises the performance of the primary manufacturing sub-sectors from

1991 to 2011. Data for each sub-sector is shown in Charts 4.6 – 4.13 on the following

pages. Unfortunately the data is highly aggregated, which masks a richer and more

interesting picture of the dynamics within each sub-sector. The data shows that value added

in all sectors expanded, except Textiles, Clothing and Other Manufacturing (largely furniture)

which contracted by about half. Growth in Wood and Paper Products was very small.

The sectors with the largest proportional growth were Non-metallic Mineral Products –

largely building materials, followed by Equipment and Machinery and then Metal Products.

In terms of employment, the only sector with growth was Food, Beverage and Tobacco

manufacturing. The largest falls were in Textiles, Clothing and Other Manufacturing, Non-

metallic mineral products and Wood and Paper.

An important measure is Value Added per employee, which gives an indication of the overall

productivity of each sub-sector. The sector with the highest value added is Petroleum, Coal,

Plastics and Rubber, which tend to be characterised by capital intensive operations with high

throughput. Next is Metal Products, followed by Non-metallic Mineral Products. Over the

twenty year period under review, the sub-sectors with the greatest increase in value added

per employee are Non-metallic Mineral Products (up 161 per cent), Machinery and

Equipment (up 82 per cent) and Metal Products, up 78 per cent. These are also the sectors

with the largest proportional growth, as noted above. However it does not follow that

workers displaced from one sector can automatically move to another as the skill

requirements are unlikely to be similar, aside from any locational issues.

The data illustrates the differing performance of the various sub-sectors. Further on in the

report we discuss the importance of avoiding dealing with the manufacturing sector as a

homogeneous set of firms. While some issues in the economic environment impact in

similar ways across the sub-sectors, different drivers are shaping performance in each. The

trajectories and prospects of the sub-sectors differ. And even within declining sectors such

as Textiles, Clothing and Other Manufacturing, firms can be found with performance which

runs against the sectoral trend. These firms are not lucky. They have strategies which

capitalise on the evolving realities of the market place together with management and

operational capabilities to continue delivering value to the customer.

Page | 31

Table 4.2: Australian manufacturing employment and value added, 1991-2011

Emp 1991

Emp 2011

% Change

VA 1991

VA 2011

% Change

VA/worker 1991

VA/ worker 2011

% Change

000s 000s $b $b

Food, beverage and tobacco 184 229 24% 4.15 5.65 36% $ 22,554

$ 24,672

9

Textiles, clothing and other manufacturing

178 96 -46% 2.1 1.05 -50% $ 11,798

$ 10,938

-7

Wood and paper products 75 54 -28% 1.79 1.82 2% $ 23,867

$ 33,704

41

Printing and recorded media 54 50 -7% 0.9 1.1 22% $ 16,667

$ 22,000

32

Petroleum, coal, chemical and rubber 98 86 -12% 4.2 5 19% $ 42,857

$ 58,140

36

Non metallic mineral products 54 37.5 -31% 0.76 1.38 82% $ 14,074

$ 36,800

161

Metal products 185 149 -19% 4.4 6.3 43% $ 23,784

$ 42,282

78

Machinery and equipment 239 206 -14% 3.5 5.5 57% $ 14,644

$ 26,699

82

1067 907.5 21.8 27.8

Source: Bremer+Company, based on Thomson Reuters Datastream

Page | 32

Page | 33

Page | 34

Page | 35

Page | 36

Two other aspects of Australia‘s manufacturing sector bear consideration – the level of

technology, and firm size.

4.3 Technology

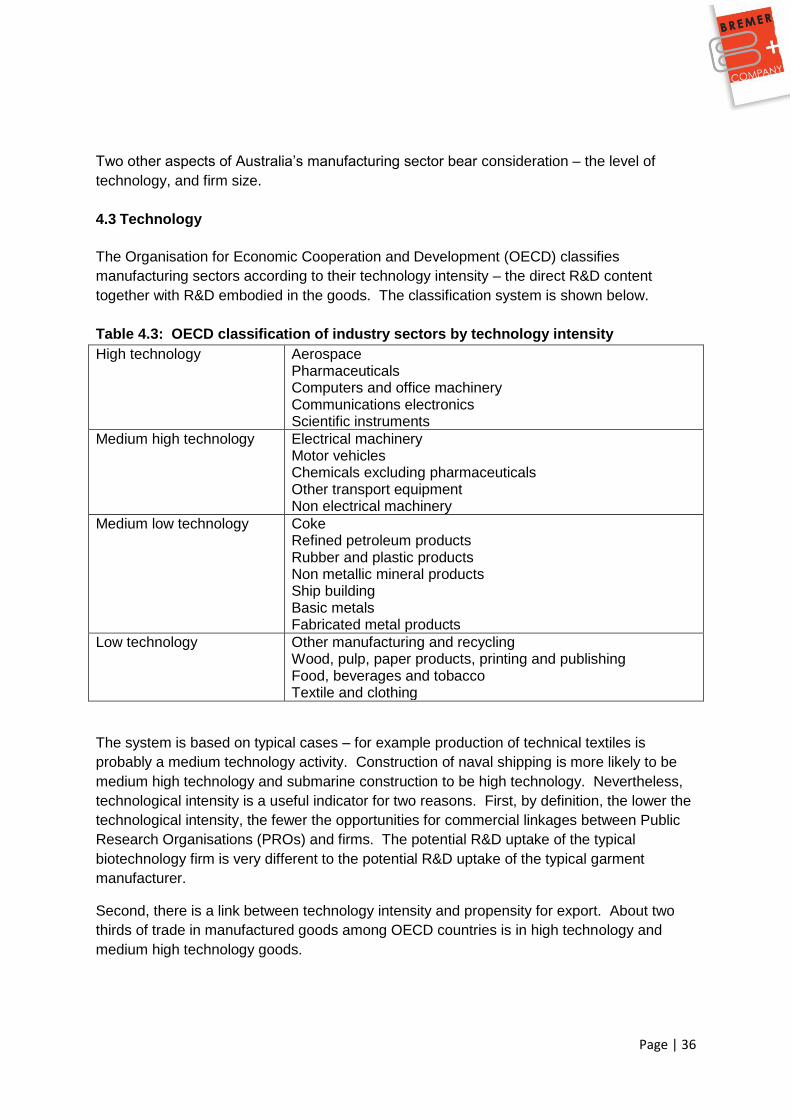

The Organisation for Economic Cooperation and Development (OECD) classifies

manufacturing sectors according to their technology intensity – the direct R&D content

together with R&D embodied in the goods. The classification system is shown below.

Table 4.3: OECD classification of industry sectors by technology intensity

High technology Aerospace Pharmaceuticals Computers and office machinery Communications electronics Scientific instruments

Medium high technology Electrical machinery Motor vehicles Chemicals excluding pharmaceuticals Other transport equipment Non electrical machinery

Medium low technology Coke Refined petroleum products Rubber and plastic products Non metallic mineral products Ship building Basic metals Fabricated metal products

Low technology Other manufacturing and recycling Wood, pulp, paper products, printing and publishing Food, beverages and tobacco Textile and clothing

The system is based on typical cases – for example production of technical textiles is

probably a medium technology activity. Construction of naval shipping is more likely to be

medium high technology and submarine construction to be high technology. Nevertheless,

technological intensity is a useful indicator for two reasons. First, by definition, the lower the

technological intensity, the fewer the opportunities for commercial linkages between Public

Research Organisations (PROs) and firms. The potential R&D uptake of the typical

biotechnology firm is very different to the potential R&D uptake of the typical garment

manufacturer.

Second, there is a link between technology intensity and propensity for export. About two

thirds of trade in manufactured goods among OECD countries is in high technology and

medium high technology goods.

Page | 37

4.4 Firm size

Australian firms generally, and manufacturing firms in particular, are small in comparison

with foreign counterparts. Fortune‘s Global 5007 ranks the world‘s largest corporations

based on revenue – admittedly an indicator of limited utility. The 2011 list includes nine

firms which are listed on the ASX. The largest – Rio Tinto (which is also listed in London

and New York) ranks at 140 by revenue. The list includes the other big miner – BHP (159),

the conglomerate Wesfarmers (183), retailer Woolworths (184), financial services

Commonwealth Bank of Australia (249), Westpac (254), National Australia Bank (266) and

Australia New Zealand Bank (338) and telecoms firm Telstra (441). Around one third of the

firms on the global list are manufacturers.

Another perspective can be obtained from company listings on the ASX. In the top 100 firms

there are 15 manufacturers (soon to be 14 with the takeover of Fosters Group), as shown in

Table 4.4 below. The largest manufacturer, ranking at 14th in terms of market capitalisation,

is CSL, with a market capitalisation of around $16b. None of these firms has its

headquarters in South East Melbourne and only Bluescope (presently) has a manufacturing

operation there.

Table 4.4: Manufacturing firms in ASX Top 100 by capitalisation, 4/10/2011

Ma

rket

cap

italizati

on

04/1

0/2

011

Ran

k

04/1

0/2

011

Secto

r

Reg

iste

red

off

ice

CSL $15.7b 14 Biotech / pharma Melbourne

Orica $8.7b 26 Chemicals / explosives Melbourne

Fosters Group $10.2b 20 Beverages Melbourne

Amcor $8.3b 27 Packaging Melbourne

Coca Cola Amatil $9.0b 25 Beverages Sydney

Resmed $4.6b 46 Therapeutic devices Sydney

Cochlear $2.7b 71 Therapeutic devices Sydney

Boral $2.4b 78 Building materials Sydney

Caltex $2.9b 66 Petrochemicals Sydney

Campbell Bros $2.7b 70 Chemicals (and services) Brisbane

OneSteel $1.7b o/s Materials - steel Sydney

UGL $1.9b 93 Transport equipment Sydney