fund facts 2q2021

TRANSCRIPT

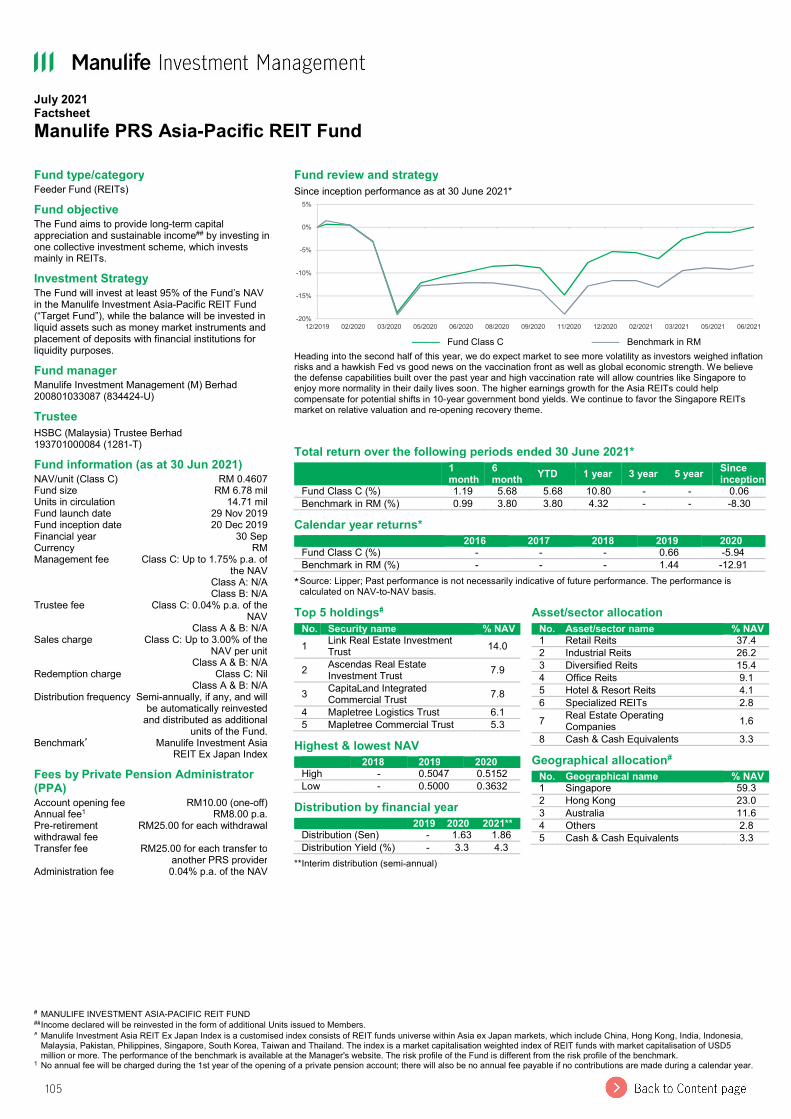

Fund Facts2Q2021

Market review and outlook

WealthStyles Income Series articles

Fund fact sheets

Income distribution

2

Content

Fund fact sheets (as at 30 June 2021)

Conventional funds

Equity

Click on a title or fund name to view respective pages

Islamic funds

Equity

Manulife Private Retirement Scheme Series

Manulife PRS NESTEGG Series: Core funds

Fixed income

Fixed income

Manulife Shariah PRS NESTEGG Series: Core funds

Manulife PRS NESTEGG Series: Non-core fund

Manulife Shariah PRS NESTEGG Series: Non-core fund

Money market

Money market

3

Market review and outlook

The race between vaccine and virusIn 2Q 2021, developed markets the likes of US and Europe continued to pull ahead in the war against Covid-19 amid accelerating vaccination campaigns. This comes about even as more contagious delta variant of the virus pushed up the global case count. The key to winning the war lies in the effectiveness of vaccine to contain hospitalization and death rates due to COVID-19, and for now, it appears that vaccines are containing fall-out from the delta variant.

Governments in most developed markets continued to ease mobility restrictions, allowing activity levels to pick up. Economic data over the last quarter has been strong, especially in the US. Although the eurozone economy contracted in 1Q 2021, leading economic indicators such as purchasing managers’ index (PMI) business surveys, have reached multi-year high in many regions, pointing to strong rebound in Europe in the second quarter.

The combination of resurging Covid-19 infections and slow vaccination progress hampered emerging markets’ effort to reopen economy, forcing many countries to return to various forms of mobility restrictions to control infections.

Malaysia experienced a new wave of infection in April 2021 and saw cases rising sharply over the next few weeks despite implementation of mobility restrictions in selected hot spots. This culminated in a nationwide lockdown in June 2021, which managed to prevent the pandemic from spiralling out of control, but still failed to bring down infection rates to targeted levels. In July 2021, large swaths of Klang Valley were placed under Enhanced Movement Control Order, which is an even stricter form of lockdown.

This latest development derailed the country’s economic recovery timeline and we see downside risks to growth as long as Covid-19 infections are not brought under control. The government indicated that it will announce a new forecast for 2021’s gross domestic product (GDP) growth in August. The silver lining is the acceleration of vaccination rate within Malaysia over the past few weeks to expedite reopening of economy and return the country to a state of normalcy. On a separate note, political uncertainty has returned with the parliament scheduled to convene end of July 2021, ahead of the 1 August expiration of the state of emergency.

More stimulus packages – termed “PEMERKASA” and “PEMULIH” were unveiled in light of the national lockdown. Although the size of the packages was large in totality, direct fiscal injection was small given limited fiscal space. Still, fiscal deficit for 2021 is likely to rise from the earlier estimated 6.0% of GDP due to larger stimulus and lower GDP growth.

Equity market review

Global equities rose in 2Q 2021 as vaccination campaigns continued to accelerate in most developed markets, especially in Europe Union, which is now catching up to the pace of the US and UK. Emerging economies continued to lag on the vaccination front, but fortunately, daily Covid-19 cases remain very low in China and it seem to have peaked in India. The prospect of more fiscal stimulus as US President Biden reached a bipartisan deal to increase infrastructure spending also boosted market sentiment.

Nevertheless, the reopening of economies and the quick rebound in activities have fuelled inflation in some countries. While the US Federal Reserve continues to see the higher inflation as transitory, it has turned slightly hawkish, admitting that tapering is being discussed. The Fed (based on dot plot projections) now expects two rate hikes in 2023, up from no rate hikes just three months ago.

For Malaysia, the FBM KLCI Index fell by 2.6% quarter-on-quarter (q-o-q) to close the quarter at a year-to-date low of 1,532.6 points. Market sentiment was dented by the reimposition of lockdowns and rising political temperature. Both average daily trading volume and values fell to the lowest levels since April 2020, with lacklustre interest from market participants. The benchmark index was dragged by the healthcare sector as glovemakers recorded steep declines, while index heavyweight plantation also underperformed. The broader market performed worse, with the FBM100 Index and FBM Small Cap Index returning -3.6% and -7.9% q-o-q respectively.

Relative to the region, the FBM KLCI Index underperformed the MSCI Asia ex-Japan Index, which gained by 3.0% during the quarter. The top performers were Vietnam (18.2%), Taiwan (8.1%) and South Korea (7.7%). Meanwhile, Malaysia (-2.6%) was the worst performer.

4

Quarter-to-date stock market performance as of 30 June 2021 (%)

US S&P 500Taiwan TWSESouth Korea KOSPIPhilippines PCOMPIndia SENSEXEuro STOXX 600China SHCOMPMSCI Asia Ex JapanHong Kong HSIThailand SETIndonesia JCIJapan TOPIXSingapore FSSTIMalaysia FBMKLCI

Source : Bloomberg as of 30 June 2021

Equity market outlook

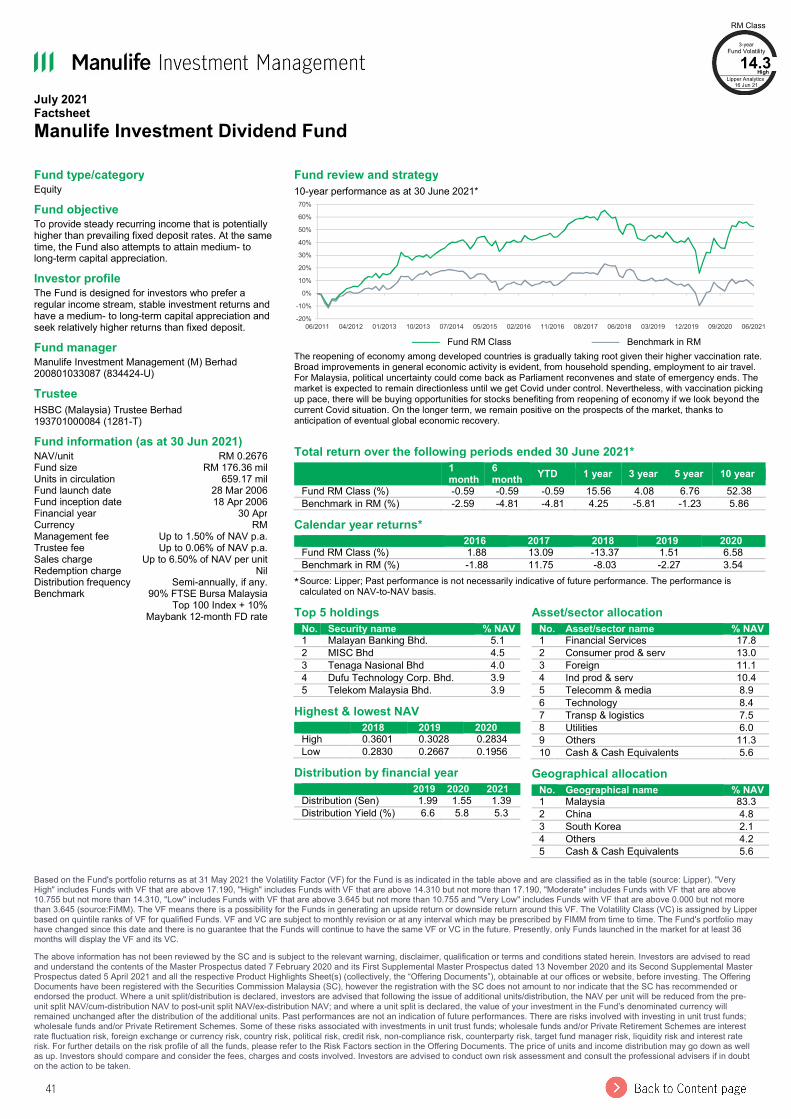

The reopening of economy among developed countries is gradually taking root given their higher vaccination rate relative to that of emerging markets. Broad improvements in general economic activity is evident, from household spending, employment to air travel. The key risk to global economic recovery would be a resurgent in Covid-19 cases caused by new virus variants, though vaccines seem to be working against them thus far.

In Malaysia, the market is expected to remain directionless until the Covid pandemic is brought under control and the political impasse is resolved. Nevertheless, with vaccination picking up pace, there will be buying opportunities for stocks benefiting from reopening of economy if we look beyond the current Covid situation. On the longer term, we remain positive on the prospects of the market, thanks to anticipation of eventual global economic recovery.

We believe key structural investment themes that we like, such as deglobalisation, digitalisation and clean energy, remain intact and will continue to anchor the basis of our investment decisions. In the current investment climate, stocks selection will be key to investment performance.

Fixed income market review

Bond markets were generally positive in 2Q 2021, as investors took a breather from the global selldown

in the first quarter. Selling pressure has dissipated and US Treasury (UST) yields retreated from highs. Towards the end of the quarter, the Fed also turned more hawkish and upped forecasts for GDP growth as well as inflation. This move sets the path towards rate normalization globally, although at a very gradual pace. Consequently, the UST yield curve flattened as short-term yields rose in anticipation of sooner rate hikes while long-term yields declined as inflationary fears faded – many view high inflation as a transitional phenomenon – and some risk-off sentiment as the delta variant of Covid-19 spread globally. Over the longer term, we believe bond yields should trend higher structurally as rates normalize.

On local shores, Bank Negara Malaysia (BNM) kept the Overnight Policy Rate (OPR) unchanged at 1.75% in July’s Monetary Policy Committee (MPC) meeting. BNM appeared to have increased their recognition of downside risks to economic growth although the MPC statement continued to sound neutral.

In line with global bond markets, Malaysian Government Securities (MGS) yields also retraced downwards in 2Q 2021. The market rebound was slight, however, as yields were still pressured upwards by expectation of economic recovery, unfavourable supply-demand dynamics and uncertainties relating to sovereign rating changes.

Credit spreads compressed quarter-on-quarter as demand for corporate bonds drove corporate bond yields lower. Credit condition appears manageable for now although we do see increasing downside risks if Covid-19 infection persists.

Fixed income market outlook

We expect BNM to maintain OPR at the current level throughout the remainder of the year as recovery prospects for Malaysia is underpinned by fiscal support and vaccination progress.

A ‘lower for longer’ theme for policy rate is likely to keep short-term yields low, with yield curve expected to remain steep as negative factors such as unfavourable supply-demand dynamics and growth expectations persist. Over the longer term, we anticipate MGS yields to continue its upward trajectory due to rate normalization as Malaysia gradually overcomes its Covid challenges. In the meantime, we anticipate rangebound MGS yields to continue providing income return and cushion from volatility for investors and market participants.

Market review and outlook (continued)

8.0% 10.0%6.0%4.0%2.0%0.0%-2.0%-4.0%

5

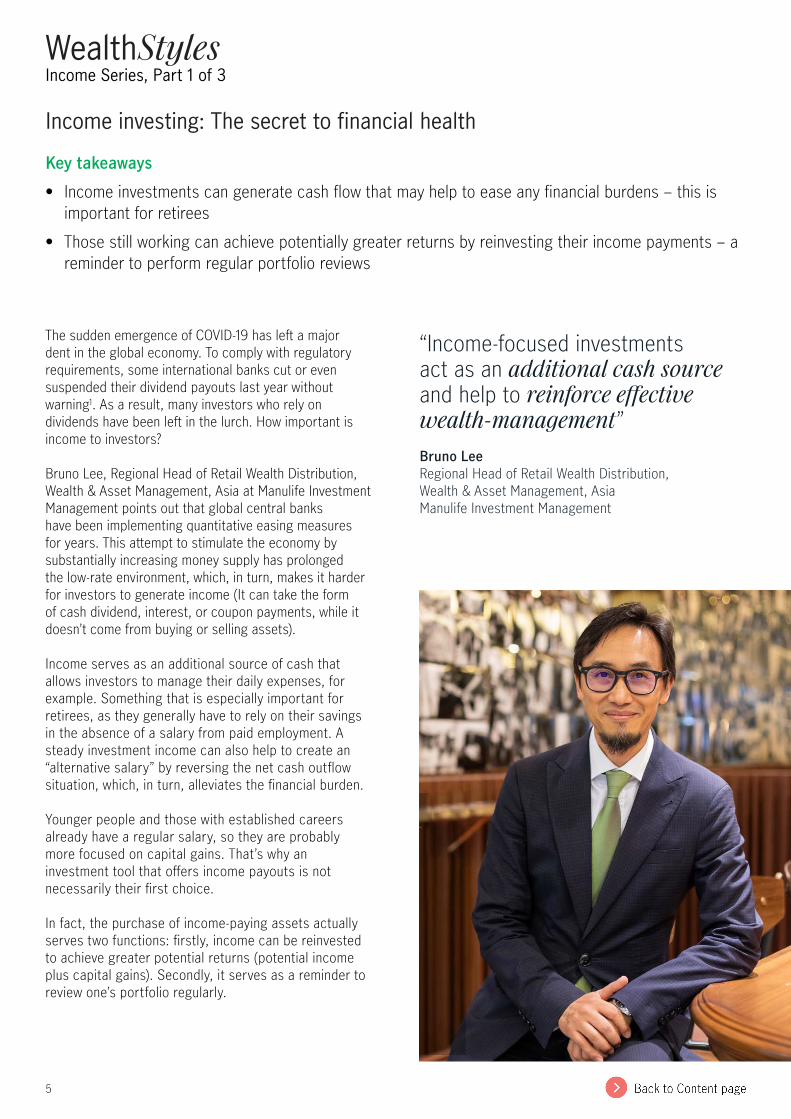

The sudden emergence of COVID-19 has left a major dent in the global economy. To comply with regulatory requirements, some international banks cut or even suspended their dividend payouts last year without warning1. As a result, many investors who rely on dividends have been left in the lurch. How important is income to investors?

Bruno Lee, Regional Head of Retail Wealth Distribution, Wealth & Asset Management, Asia at Manulife Investment Management points out that global central banks have been implementing quantitative easing measures for years. This attempt to stimulate the economy by substantially increasing money supply has prolonged the low-rate environment, which, in turn, makes it harder for investors to generate income (It can take the form of cash dividend, interest, or coupon payments, while it doesn’t come from buying or selling assets).

Income serves as an additional source of cash that allows investors to manage their daily expenses, for example. Something that is especially important for retirees, as they generally have to rely on their savings in the absence of a salary from paid employment. A steady investment income can also help to create an “alternative salary” by reversing the net cash outflow situation, which, in turn, alleviates the financial burden.

Younger people and those with established careers already have a regular salary, so they are probably more focused on capital gains. That’s why an investment tool that offers income payouts is not necessarily their first choice.

In fact, the purchase of income-paying assets actually serves two functions: firstly, income can be reinvested to achieve greater potential returns (potential income plus capital gains). Secondly, it serves as a reminder to review one’s portfolio regularly.

Income investing: The secret to financial health

Key takeaways

• Income investments can generate cash flow that may help to ease any financial burdens – this is important for retirees

• Those still working can achieve potentially greater returns by reinvesting their income payments – a reminder to perform regular portfolio reviews

WealthStylesIncome Series, Part 1 of 3

“Income-focused investments act as an additional cash source and help to reinforce effective wealth-management”Bruno LeeRegional Head of Retail Wealth Distribution, Wealth & Asset Management, AsiaManulife Investment Management

6

Regular portfolio health checks:a reminder

Investors may be unaware that besides acting as an additional cash source, income-focused investments help to reinforce effective wealth management.

Lee believes that it is common for investors to neglect wealth management due to their hectic work schedules or lifestyles. Investing in assets that offer regular dividends can, therefore, provide a cordial reminder when any payouts are made. In Lee’s experience, whenever a distribution is received, the amount is directly deposited into his cash account and he gets a notification with details of that transaction. His account balance continues to rise with each payment. This has the effect of highlighting any idle assets and, consequently, the need to review his portfolio. Lee can then decide whether reinvestment is required – a cycle that allows him to remain a disciplined investor.

Lee reveals more about his strategy: “I hold different types of funds with regular payouts. When, after a few months, the accumulated income reaches a certain level, I would consider how to reinvest the newly gained capital. For instance, I can increase my current holdings or look for investment opportunities in other equity funds during a sell-off.”

In terms of investment allocation, Lee says investors may consider taking a conservative approach for the principal coupled with flexible asset allocation according to the investor’s risk tolerance, lifecycle stage, and wealth-management objectives. As for the additional income, more aggressive investors can select higher-risk tools in the pursuit of better potential returns, as it accounts for only a small proportion of the portfolio’s total value.

Different income functions for different people

Income

Retiree Employee

Create income flow, relieve financial stress

Are expenses greater than income?

Provide additional income to cover living expenses

Reinvest income, reminds self to review portfolio regularly

Yes

No

WealthStylesIncome Series, Part 1 of 3

1 Source: Prudential Regulation Authority (PRA) of Bank of England (BoE), 31 March, 2020; European Central Bank (ECB), 28 July, 2020; Bloomberg, 14 October, 2020. The PRA of BoE requested local banks to suspend cash dividend payouts and share buybacks until 2020 year-end, and the situation will be reviewed in Q4 2020. The ECB requested regional banks to suspend cash dividend payouts and share buybacks until 1 January, 2021. Statistics from Bloomberg show that 28% of Asia Pacific companies have announced dividend suspension or cuts.

Manulife Investment Management is the global wealth and asset management segment of Manulife Financial Corporation. The information and/or analysis contained in this material have been compiled or derived from sources believed to be reliable at the time of writing but Manulife Investment Management does not make any representation as to their accuracy, correctness, usefulness or completeness and does not accept liability for any loss arising from the use hereof or the information and/or analysis contained herein. Neither Manulife Investment Management or its affiliates, nor any of their directors, officers or employees shall assume any liability or responsibility for any direct or indirect loss or damage or any other consequence of any person acting or not acting in reliance on the information contained herein.This material was prepared solely for educational and informational purposes and does not constitute a recommendation, professional advice, an offer, solicitation or an invitation by or on behalf of Manulife Investment Management to any person to buy or sell any security. Nothing in this material constitutes financial, investment, legal, accounting or tax advice, or a representation that any investment or strategy is suitable or appropriate to your individual circumstances, or otherwise constitutes a personal recommendation to you. Past performance is not an indication of future results. Investment involves risk. In considering any investment, if you are in doubt on the action to be taken, you should consult professional advisers.Proprietary Information – Please note that this material must not be wholly or partially reproduced, distributed, circulated, disseminated, published or disclosed, in any form and for any purpose, to any third party without prior approval from Manulife Investment Management.These materials have not been reviewed by, are not registered with any securities or other regulatory authority, and may, where appropriate, be distributed by the following Manulife entities in their respective jurisdictions.Malaysia: Manulife Investment Management (M) Berhad 200801033087 (834424-U). Singapore: Manulife Investment Management (Singapore) Pte. Ltd. (Company Registration Number: 200709952G). Philippines: Manulife Asset Management and Trust Corporation. Australia, South Korea and Hong Kong: Manulife Investment Management (Hong Kong) Limited in Hong Kong and has not been reviewed by the HK Securities and Futures Commission (SFC). Manulife Investment Management (Hong Kong) Limited (“Manulife”) shall cease to use your personal data in direct marketing if you make your request in writing to The Privacy Officer, 23/F, Manulife Tower, One Bay East, 83 Hoi Bun Rd, Kwun Tong, Kowloon, Hong Kong. To view Hong Kong Manulife’s Privacy Policy, please click here.If you no longer wish to receive these emails, you may unsubscribe at any time.

7

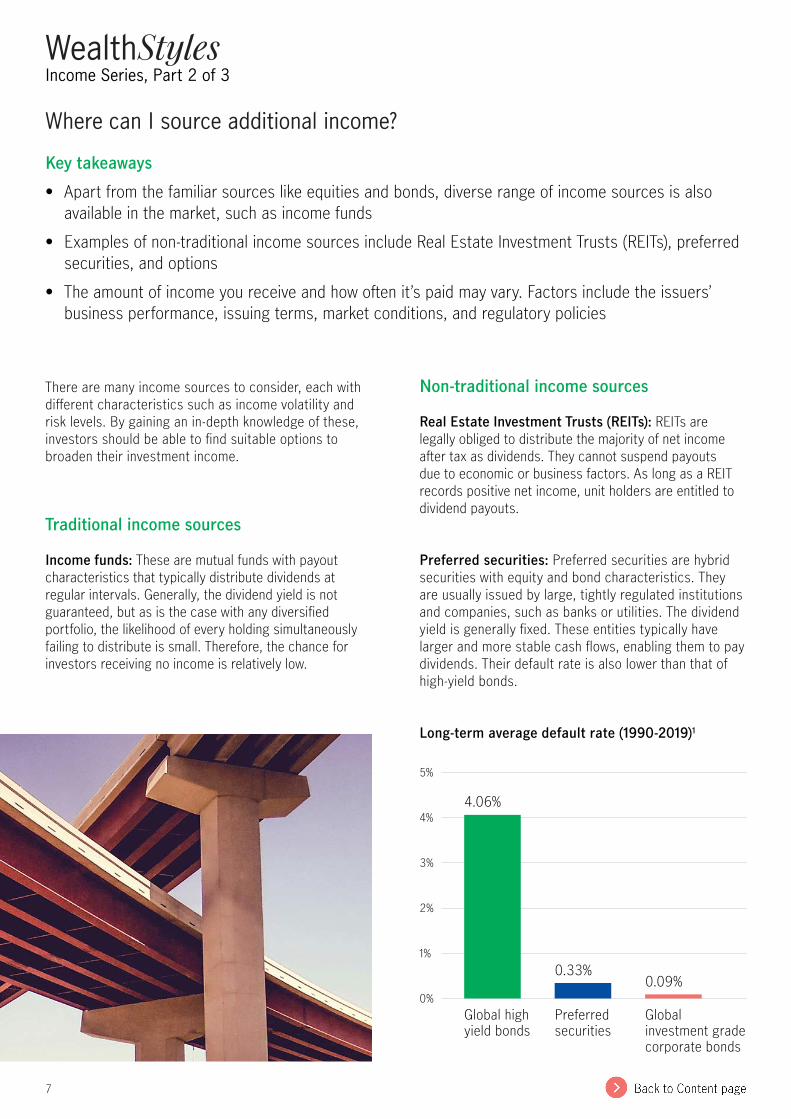

There are many income sources to consider, each with different characteristics such as income volatility and risk levels. By gaining an in-depth knowledge of these, investors should be able to find suitable options to broaden their investment income.

Traditional income sources

Income funds: These are mutual funds with payout characteristics that typically distribute dividends at regular intervals. Generally, the dividend yield is not guaranteed, but as is the case with any diversified portfolio, the likelihood of every holding simultaneously failing to distribute is small. Therefore, the chance for investors receiving no income is relatively low.

Non-traditional income sources

Real Estate Investment Trusts (REITs): REITs are legally obliged to distribute the majority of net income after tax as dividends. They cannot suspend payouts due to economic or business factors. As long as a REIT records positive net income, unit holders are entitled to dividend payouts.

Preferred securities: Preferred securities are hybrid securities with equity and bond characteristics. They are usually issued by large, tightly regulated institutions and companies, such as banks or utilities. The dividend yield is generally fixed. These entities typically have larger and more stable cash flows, enabling them to pay dividends. Their default rate is also lower than that of high-yield bonds.

Long-term average default rate (1990-2019)1

5%

4%

3%

2%

1%

0%Global high yield bonds

Preferred securities

Global investment grade corporate bonds

4.06%

0.33%0.09%

Where can I source additional income?

Key takeaways

• Apart from the familiar sources like equities and bonds, diverse range of income sources is also available in the market, such as income funds

• Examples of non-traditional income sources include Real Estate Investment Trusts (REITs), preferred securities, and options

• The amount of income you receive and how often it’s paid may vary. Factors include the issuers’ business performance, issuing terms, market conditions, and regulatory policies

WealthStylesIncome Series, Part 2 of 3

8

Options: By selling a call option or put option, investors can receive a premium (income) in advance without waiting until the option expiry date. However, it should be noted that obtaining a premium does not necessarily mean that the overall investment return is positive.

If the trend of the underlying asset deviates from expectations, i.e., the price of an asset actually rises after selling a call option, or vice versa, overall returns may be negative, as the premium may not be adequate to offset the loss on exercising an option completely.

Payout frequency: Depends on the dividend policy of a fund. Some pay dividends on a monthly basis.Income volatility: Depends on the income generated by a portfolio’s holdings

Payout frequency: Usually quarterly, semi-annually or annually Income volatility: Depends on a company’s financial situation and/or the regulatory policies

Payout frequency: Usually quarterly, semi-annually or annually Income volatility: Coupon rates vary according to bond type (e.g. government/ corporate bonds; fixed rate/ floating rate bonds), ratings, duration, and underlying assets (e.g. inflation-linked bonds)

Payout frequency: Usually quarterly, semi-annually or annually Income volatility: Legally obliged to pay dividends, but it depends on the amount of distributable income

Payout frequency: Usually quarterly, semi-annually or annually Income volatility: Paid at fixed rates

Payout frequency: Premiums are received at the beginning of the investment period Income volatility: Depends on strike prices, expiry dates, and volatility

REITs

Preferred securities

Income funds

Options

Equities

Bonds

Non-traditional income sources2

Traditional income sources2

WealthStylesIncome Series, Part 2 of 3

1 Source: Default rate of global high-yield bonds and global investment-grade bonds provided by Moody’s Investors Service, Inc. Default rate of preferred securities during 1990–2017 calculated by Wells Fargo. As Wells Fargo stopped providing the relevant information after 2017, Manulife Asset Management has calculated the annual default rate based on the ICE BofAML US All Capital Securities Index since 2018. As of 31 December, 2019. Past performance is not indicative of future performance. 2 The above material is for illustration purposes only. Distribution of dividends, the frequency of distribution and the amount/rate of dividends are not guaranteed. Positive distribution yield does not imply positive return.

Manulife Investment Management is the global wealth and asset management segment of Manulife Financial Corporation. The information and/or analysis contained in this material have been compiled or derived from sources believed to be reliable at the time of writing but Manulife Investment Management does not make any representation as to their accuracy, correctness, usefulness or completeness and does not accept liability for any loss arising from the use hereof or the information and/or analysis contained herein. Neither Manulife Investment Management or its affiliates, nor any of their directors, officers or employees shall assume any liability or responsibility for any direct or indirect loss or damage or any other consequence of any person acting or not acting in reliance on the information contained herein.This material was prepared solely for educational and informational purposes and does not constitute a recommendation, professional advice, an offer, solicitation or an invitation by or on behalf of Manulife Investment Management to any person to buy or sell any security. Nothing in this material constitutes financial, investment, legal, accounting or tax advice, or a representation that any investment or strategy is suitable or appropriate to your individual circumstances, or otherwise constitutes a personal recommendation to you. Past performance is not an indication of future results. Investment involves risk. In considering any investment, if you are in doubt on the action to be taken, you should consult professional advisers.Proprietary Information – Please note that this material must not be wholly or partially reproduced, distributed, circulated, disseminated, published or disclosed, in any form and for any purpose, to any third party without prior approval from Manulife Investment Management.These materials have not been reviewed by, are not registered with any securities or other regulatory authority, and may, where appropriate, be distributed by the following Manulife entities in their respective jurisdictions.Malaysia: Manulife Investment Management (M) Berhad 200801033087 (834424-U). Singapore: Manulife Investment Management (Singapore) Pte. Ltd. (Company Registration Number: 200709952G). Philippines: Manulife Asset Management and Trust Corporation. Australia, South Korea and Hong Kong: Manulife Investment Management (Hong Kong) Limited in Hong Kong and has not been reviewed by the HK Securities and Futures Commission (SFC). Manulife Investment Management (Hong Kong) Limited (“Manulife”) shall cease to use your personal data in direct marketing if you make your request in writing to The Privacy Officer, 23/F, Manulife Tower, One Bay East, 83 Hoi Bun Rd, Kwun Tong, Kowloon, Hong Kong. To view Hong Kong Manulife’s Privacy Policy, please click here.If you no longer wish to receive these emails, you may unsubscribe at any time.

9

Choosing the right sources of income from the wide variety of options available in the market may seem daunting to many investors. To construct an optimal investment portfolio with income exposure, Bruno Lee, Regional Head of Retail Wealth Distribution, Wealth & Asset Management, Asia at Manulife Investment Management believes that investors should first understand the risks associated with each income source then consider their own risk tolerance level and wealth-management objectives.

Diverse sources of income, differenttypes of risks

Understanding the different types of income sourcesin the market is only the first step towards generating additional cash. Therefore, to identify the suitable investment tools, it is important to consider each source of risk, one by one.

Bonds: credit risk

The most significant risk associated with corporate bonds is credit risk. This occurs when issuers cannot fulfil the terms of a bond and fail to pay coupons or return the principal on time – commonly known as a bond default. To establish the level of credit risk, investors should understand various factors, such as how the issuer performs under different economic conditions and the size of its business. It’s also helpful to know about the issuer’s profitability and financial health. The extent of these risk factors is reflected by indicators, such as credit ratings and yields, and could serve as useful reference points when investing in single bonds.

The risks related to bond funds, which invest in a basket of bonds, can be determined by assessing each bond’s investment objectives, average credit ratings, and risk indicators. Lee uses investment-grade bond funds as an example, pointing out that while these are considered less risky than high-yield bond funds, they come with a lower yield. Meanwhile, the risk (yield) of emerging-market (i.e., Asian emerging markets) bond funds is higher than bond funds from developed markets, such as Europe and the US.

Preferred securities: a combination of equity and bond risk

Some companies also issue preferred securities, which feature characteristics of both equities and bonds. Therefore, investing in preferred securities bears the risks of these two asset classes simultaneously, which could include the credit and interest-rate risk of bond investments, as well as the volatility risk of equities.

REITs: property-market risk

Real Estate Investment Trusts (REITs), which have risen to prominence in recent years, invest primarily in real estate that generates a recurring rental income. While real estate assets are generally inflation resistant, and REITs are required by law to distribute the majority of their income as dividends, investors have to bear the risks associated with property markets. These can include changes in property prices (asset-price volatility), interest rate trends, and profitability, which are all affected by geographical location, asset type, occupancy rate, and fluctuations in rental income.

Understand income-source risks before asset allocation

Key takeaways

• To master the art of asset allocation, you should understand the risks associated with each income source. Consider your attitude towards risk then establish wealth-management objectives, as this will help you to identify the most suitable asset-allocation tools

• When constructing an investment portfolio, it’s vital to diversify your investments rather than focus on a single equity, bond, or fund

WealthStylesIncome Series, Part 3 of 3

10

Multi-asset funds: risk depends on asset-class coverage

In the case of multi-asset funds, risk is determined by the various asset classes in a portfolio. Lee points out that besides investing in stocks, bonds, REITs, and preferred securities, some funds also generate income by including options. Holding these funds, therefore, means that investors have to bear the credit risk of options issuers.

Dividend yield is not the sole indicator

When selecting investment tools to help meet their personal wealth management needs, investors would generally consider factors other than risk, such as dividend levels and past performance. However, Lee notes that while some funds offer an attractive dividend income, this should not be used as the sole indicator of that fund’s selection.

Instead, attention should be paid to total returns, where dividend return is combined with a change in fund prices to provide a more comprehensive picture. “The investment return of some portfolios may not support the payment of high dividends,” observes Lee.

Diversification increases the chancesof earning income

Apart from understanding the sources of risk and total return, investors also need to evaluate their own risk profiles and choose investment tools that match their risk tolerance level. When investors plan to construct a portfolio by themselves, Lee highlights that it’s vital to remember diversification: “It’s important to diversify investments and not focus on a single equity, bond, or fund. An income-focused investment portfolio should consist of at least three-to-five different types of funds or investments.”

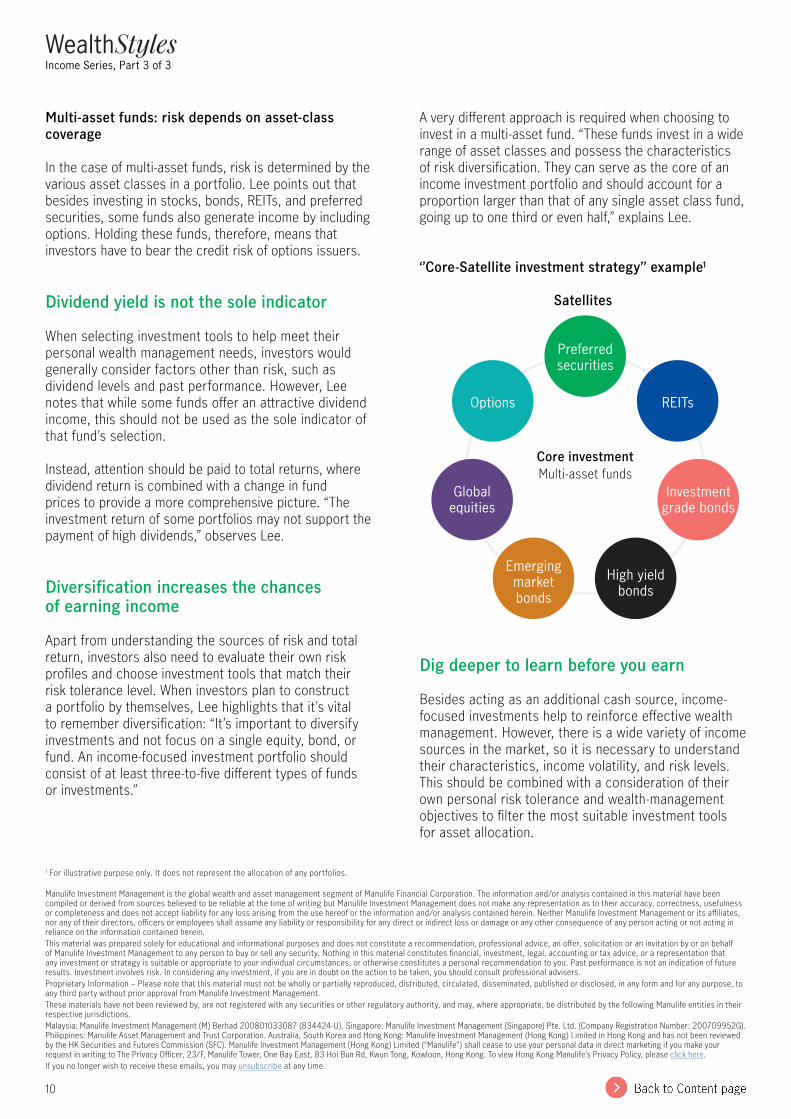

A very different approach is required when choosing to invest in a multi-asset fund. “These funds invest in a wide range of asset classes and possess the characteristics of risk diversification. They can serve as the core of an income investment portfolio and should account for a proportion larger than that of any single asset class fund, going up to one third or even half,” explains Lee.

‘’Core-Satellite investment strategy’’ example1

Satellites

Dig deeper to learn before you earn

Besides acting as an additional cash source, income-focused investments help to reinforce effective wealth management. However, there is a wide variety of income sources in the market, so it is necessary to understand their characteristics, income volatility, and risk levels. This should be combined with a consideration of their own personal risk tolerance and wealth-management objectives to filter the most suitable investment tools for asset allocation.

Core investmentMulti-asset funds

Preferred securities

REITs

Options

Global equities

Investment grade bonds

Emerging market bonds

High yield bonds

WealthStylesIncome Series, Part 3 of 3

1 For illustrative purpose only. It does not represent the allocation of any portfolios.

Manulife Investment Management is the global wealth and asset management segment of Manulife Financial Corporation. The information and/or analysis contained in this material have been compiled or derived from sources believed to be reliable at the time of writing but Manulife Investment Management does not make any representation as to their accuracy, correctness, usefulness or completeness and does not accept liability for any loss arising from the use hereof or the information and/or analysis contained herein. Neither Manulife Investment Management or its affiliates, nor any of their directors, officers or employees shall assume any liability or responsibility for any direct or indirect loss or damage or any other consequence of any person acting or not acting in reliance on the information contained herein.This material was prepared solely for educational and informational purposes and does not constitute a recommendation, professional advice, an offer, solicitation or an invitation by or on behalf of Manulife Investment Management to any person to buy or sell any security. Nothing in this material constitutes financial, investment, legal, accounting or tax advice, or a representation that any investment or strategy is suitable or appropriate to your individual circumstances, or otherwise constitutes a personal recommendation to you. Past performance is not an indication of future results. Investment involves risk. In considering any investment, if you are in doubt on the action to be taken, you should consult professional advisers.Proprietary Information – Please note that this material must not be wholly or partially reproduced, distributed, circulated, disseminated, published or disclosed, in any form and for any purpose, to any third party without prior approval from Manulife Investment Management.These materials have not been reviewed by, are not registered with any securities or other regulatory authority, and may, where appropriate, be distributed by the following Manulife entities in their respective jurisdictions.Malaysia: Manulife Investment Management (M) Berhad 200801033087 (834424-U). Singapore: Manulife Investment Management (Singapore) Pte. Ltd. (Company Registration Number: 200709952G). Philippines: Manulife Asset Management and Trust Corporation. Australia, South Korea and Hong Kong: Manulife Investment Management (Hong Kong) Limited in Hong Kong and has not been reviewed by the HK Securities and Futures Commission (SFC). Manulife Investment Management (Hong Kong) Limited (“Manulife”) shall cease to use your personal data in direct marketing if you make your request in writing to The Privacy Officer, 23/F, Manulife Tower, One Bay East, 83 Hoi Bun Rd, Kwun Tong, Kowloon, Hong Kong. To view Hong Kong Manulife’s Privacy Policy, please click here.If you no longer wish to receive these emails, you may unsubscribe at any time.

11

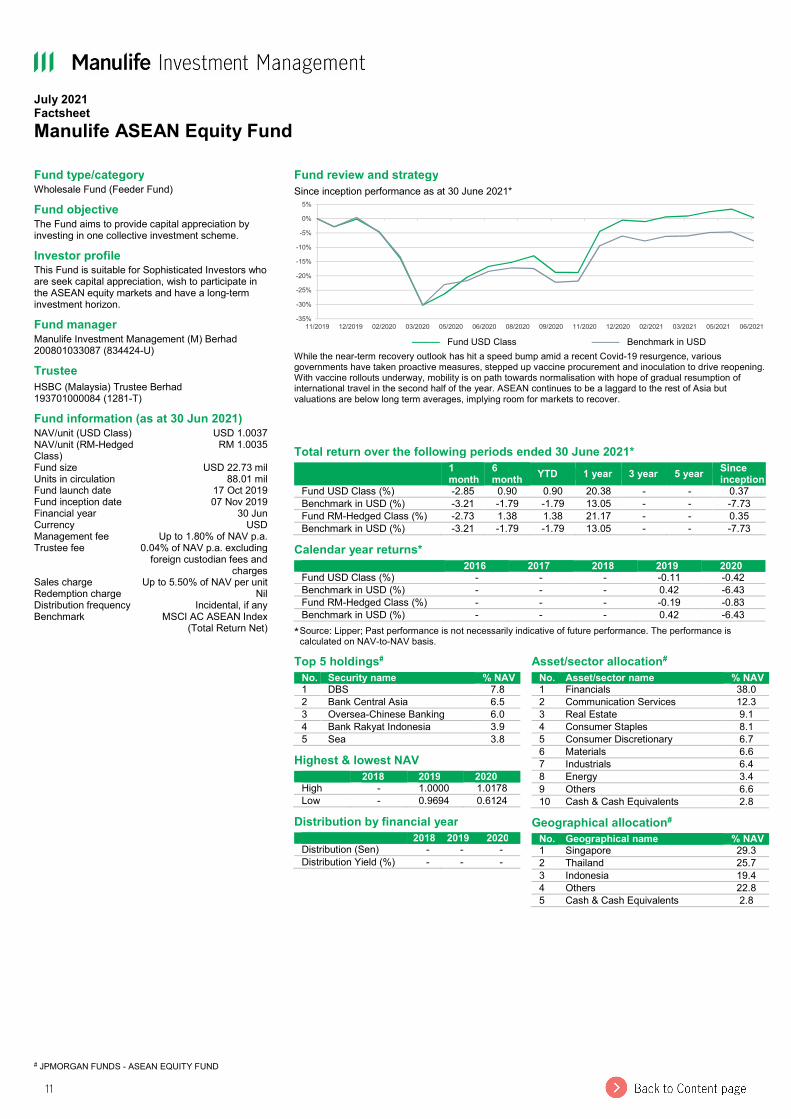

July 2021 Factsheet Manulife ASEAN Equity Fund

# JPMORGAN FUNDS - ASEAN EQUITY FUND

Fund type/category Wholesale Fund (Feeder Fund) Fund objective The Fund aims to provide capital appreciation by investing in one collective investment scheme. Investor profile This Fund is suitable for Sophisticated Investors who are seek capital appreciation, wish to participate in the ASEAN equity markets and have a long-term investment horizon. Fund manager Manulife Investment Management (M) Berhad 200801033087 (834424-U) Trustee HSBC (Malaysia) Trustee Berhad 193701000084 (1281-T) Fund information (as at 30 Jun 2021) NAV/unit (USD Class) USD 1.0037 NAV/unit (RM-Hedged Class)

RM 1.0035 Fund size USD 22.73 mil Units in circulation 88.01 mil Fund launch date 17 Oct 2019 Fund inception date 07 Nov 2019 Financial year 30 Jun Currency USD Management fee Up to 1.80% of NAV p.a. Trustee fee 0.04% of NAV p.a. excluding

foreign custodian fees and charges

Sales charge Up to 5.50% of NAV per unit Redemption charge Nil Distribution frequency Incidental, if any Benchmark MSCI AC ASEAN Index

(Total Return Net)

Fund review and strategy Since inception performance as at 30 June 2021*

——— Fund USD Class ——— Benchmark in USD

While the near-term recovery outlook has hit a speed bump amid a recent Covid-19 resurgence, various governments have taken proactive measures, stepped up vaccine procurement and inoculation to drive reopening. With vaccine rollouts underway, mobility is on path towards normalisation with hope of gradual resumption of international travel in the second half of the year. ASEAN continues to be a laggard to the rest of Asia but valuations are below long term averages, implying room for markets to recover.

Total return over the following periods ended 30 June 2021*

1 month

6 month YTD 1 year 3 year 5 year Since

inception Fund USD Class (%) -2.85 0.90 0.90 20.38 - - 0.37 Benchmark in USD (%) -3.21 -1.79 -1.79 13.05 - - -7.73 Fund RM-Hedged Class (%) -2.73 1.38 1.38 21.17 - - 0.35 Benchmark in USD (%) -3.21 -1.79 -1.79 13.05 - - -7.73

Calendar year returns* 2016 2017 2018 2019 2020

Fund USD Class (%) - - - -0.11 -0.42 Benchmark in USD (%) - - - 0.42 -6.43 Fund RM-Hedged Class (%) - - - -0.19 -0.83 Benchmark in USD (%) - - - 0.42 -6.43

* Source: Lipper; Past performance is not necessarily indicative of future performance. The performance is calculated on NAV-to-NAV basis.

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

11/2019 12/2019 02/2020 03/2020 05/2020 06/2020 08/2020 09/2020 11/2020 12/2020 02/2021 03/2021 05/2021 06/2021

Top 5 holdings# No. Security name % NAV

1 DBS 7.8 2 Bank Central Asia 6.5 3 Oversea-Chinese Banking 6.0 4 Bank Rakyat Indonesia 3.9 5 Sea 3.8

Highest & lowest NAV 2018 2019 2020

High - 1.0000 1.0178 Low - 0.9694 0.6124

Distribution by financial year 2018 2019 2020

Distribution (Sen) - - - Distribution Yield (%) - - -

Asset/sector allocation# No. Asset/sector name % NAV

1 Financials 38.0 2 Communication Services 12.3 3 Real Estate 9.1 4 Consumer Staples 8.1 5 Consumer Discretionary 6.7 6 Materials 6.6 7 Industrials 6.4 8 Energy 3.4 9 Others 6.6 10 Cash & Cash Equivalents 2.8

Geographical allocation# No. Geographical name % NAV

1 Singapore 29.3 2 Thailand 25.7 3 Indonesia 19.4 4 Others 22.8 5 Cash & Cash Equivalents 2.8

July 2021 Factsheet Manulife ASEAN Equity Fund

# JPMORGAN FUNDS - ASEAN EQUITY FUND

Fund type/category Wholesale Fund (Feeder Fund) Fund objective The Fund aims to provide capital appreciation by investing in one collective investment scheme. Investor profile This Fund is suitable for Sophisticated Investors who are seek capital appreciation, wish to participate in the ASEAN equity markets and have a long-term investment horizon. Fund manager Manulife Investment Management (M) Berhad 200801033087 (834424-U) Trustee HSBC (Malaysia) Trustee Berhad 193701000084 (1281-T) Fund information (as at 30 Jun 2021) NAV/unit (USD Class) USD 1.0037 NAV/unit (RM-Hedged Class)

RM 1.0035 Fund size USD 22.73 mil Units in circulation 88.01 mil Fund launch date 17 Oct 2019 Fund inception date 07 Nov 2019 Financial year 30 Jun Currency USD Management fee Up to 1.80% of NAV p.a. Trustee fee 0.04% of NAV p.a. excluding

foreign custodian fees and charges

Sales charge Up to 5.50% of NAV per unit Redemption charge Nil Distribution frequency Incidental, if any Benchmark MSCI AC ASEAN Index

(Total Return Net)

Fund review and strategy Since inception performance as at 30 June 2021*

——— Fund USD Class ——— Benchmark in USD

While the near-term recovery outlook has hit a speed bump amid a recent Covid-19 resurgence, various governments have taken proactive measures, stepped up vaccine procurement and inoculation to drive reopening. With vaccine rollouts underway, mobility is on path towards normalisation with hope of gradual resumption of international travel in the second half of the year. ASEAN continues to be a laggard to the rest of Asia but valuations are below long term averages, implying room for markets to recover.

Total return over the following periods ended 30 June 2021*

1 month

6 month YTD 1 year 3 year 5 year Since

inception Fund USD Class (%) -2.85 0.90 0.90 20.38 - - 0.37 Benchmark in USD (%) -3.21 -1.79 -1.79 13.05 - - -7.73 Fund RM-Hedged Class (%) -2.73 1.38 1.38 21.17 - - 0.35 Benchmark in USD (%) -3.21 -1.79 -1.79 13.05 - - -7.73

Calendar year returns* 2016 2017 2018 2019 2020

Fund USD Class (%) - - - -0.11 -0.42 Benchmark in USD (%) - - - 0.42 -6.43 Fund RM-Hedged Class (%) - - - -0.19 -0.83 Benchmark in USD (%) - - - 0.42 -6.43

* Source: Lipper; Past performance is not necessarily indicative of future performance. The performance is calculated on NAV-to-NAV basis.

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

11/2019 12/2019 02/2020 03/2020 05/2020 06/2020 08/2020 09/2020 11/2020 12/2020 02/2021 03/2021 05/2021 06/2021

Top 5 holdings# No. Security name % NAV

1 DBS 7.8 2 Bank Central Asia 6.5 3 Oversea-Chinese Banking 6.0 4 Bank Rakyat Indonesia 3.9 5 Sea 3.8

Highest & lowest NAV 2018 2019 2020

High - 1.0000 1.0178 Low - 0.9694 0.6124

Distribution by financial year 2018 2019 2020

Distribution (Sen) - - - Distribution Yield (%) - - -

Asset/sector allocation# No. Asset/sector name % NAV

1 Financials 38.0 2 Communication Services 12.3 3 Real Estate 9.1 4 Consumer Staples 8.1 5 Consumer Discretionary 6.7 6 Materials 6.6 7 Industrials 6.4 8 Energy 3.4 9 Others 6.6 10 Cash & Cash Equivalents 2.8

Geographical allocation# No. Geographical name % NAV

1 Singapore 29.3 2 Thailand 25.7 3 Indonesia 19.4 4 Others 22.8 5 Cash & Cash Equivalents 2.8

12

July 2021 Factsheet Manulife ASEAN Equity Fund Market Review The ASEAN region was flat on aggregate, with contrasting performance between markets, driven by COVID-19 infection trends. Singapore, Thailand and Malaysia saw subdued performance due to rising cases and tighter mobility restrictions, whereas the Philippines saw a strong market rebound as cases appeared to be stabilizing. Vietnam was the outlier – posting new all-time highs despite a flare up in cases. ASEAN lagged Asa ex Japan this month. Feeder Fund Review In June, the Feeder Fund posted a) -2.85% versus the benchmark return of -3.21% for its USD class; and b) -2.73% versus the benchmark return of -3.21% for its RM-Hedged class. The Fund was down but outperformed the benchmark. On a country level, stock selection was strong in Thailand and Singapore. Allocation to Vietnam also helped. On a sector level, communication services and health care were strong. On the positive side, sector allocation and stock selection in health care worked well. Being underweight the Malaysian glove makers again worked in our favour. Elsewhere in health care, the off-benchmark position in a Thailand medical services stock contributed on the back of increased hospitalization utility from the covid situation. In Singapore, a multinational technology conglomerate that own a leading e-commerce platform in Southeast Asian and Taiwan was the largest contributor on its long-term growth potential. In Vietnam, a commerce bank finally rallied after a stale price performance in the 1H2021. In Philippines, the market advanced on optimism around reopening. The COVID situation is improving locally with cases and hospitals’ bed occupancies improving. Holding a Philippines based energy company in the power sector was positive as the market starts to get comfortable around the prospects for capacity growth. A global port management company headquartered in Manila contributed as there were continual earnings and price upgrades by the market. Market Outlook While the near-term recovery outlook has hit a speed bump amid the recent Covid-19 resurgence, various governments have taken proactive measures, stepped up vaccine procurement and inoculation to drive reopening. With vaccine rollouts underway, mobility is on path towards normalisation with hope of a gradual resumption of international travel in the second half of the year. ASEAN continues to be a laggard to the rest of Asia but valuations are below long term averages, implying room for markets to recover. The structural positives for ASEAN remain unchanged through the pandemic. The region is well-placed for further supply chain diversification, and long-term structural themes such as increasing financial penetration, and tourism growth should gradually return to the fore as we move past the lockdown-induced cyclical troughs. The emergence of new economy stocks in ASEAN and potential public listings also present interesting opportunities. Meantime, we are encouraged by the positive progress in Indonesia’s Omnibus law reform, the financial health of its banking system in weathering this pandemic, and the robust growth story exhibited by Vietnam. The pace of the recovery will be uneven across the region, and active bottom-up picking remains crucial given the wide dispersion in stock fundamentals across ASEAN. We continue to be overweight companies in regions with long term growth profiles (Indonesia, Vietnam). The fund is more selective in Thailand and Singapore. Malaysia continues to be a structural underweight for the fund. Across ASEAN, we continue to prefer long-term compounders and domestic champions with attractive growth prospects, however we have been gradually positioning the portfolio more towards areas which may benefit from the eventual economic reopening. The above information has not been reviewed by the SC and is subject to the relevant warning, disclaimer, qualification or terms and conditions stated herein. Investors are advised to read and understand the contents of the Information Memorandum dated 11 February 2020 and all the respective Product Highlights Sheet(s) (collectively, the “Offering Documents”), obtainable at our offices or website, before investing. The Offering Documents have been registered with the Securities Commission Malaysia (SC), however the registration with the SC does not amount to nor indicate that the SC has recommended or endorsed the product. Where a unit split/distribution is declared, investors are advised that following the issue of additional units/distribution, the NAV per unit will be reduced from the pre-unit split NAV/cum-distribution NAV to post-unit split NAV/ex-distribution NAV; and where a unit split is declared, the value of your investment in the Fund’s denominated currency will remained unchanged after the distribution of the additional units. Past performances are not an indication of future performances. There are risks involved with investing in unit trust funds; wholesale funds and/or Private Retirement Schemes. Some of these risks associated with investments in unit trust funds; wholesale funds and/or Private Retirement Schemes are interest rate fluctuation risk, foreign exchange or currency risk, country risk, political risk, credit risk, non-compliance risk, counterparty risk, target fund manager risk, liquidity risk and interest rate risk. For further details on the risk profile of all the funds, please refer to the Risk Factors section in the Offering Documents. The price of units and income distribution may go down as well as up. Investors should compare and consider the fees, charges and costs involved. Investors are advised to conduct own risk assessment and consult the professional advisers if in doubt on the action to be taken.

13

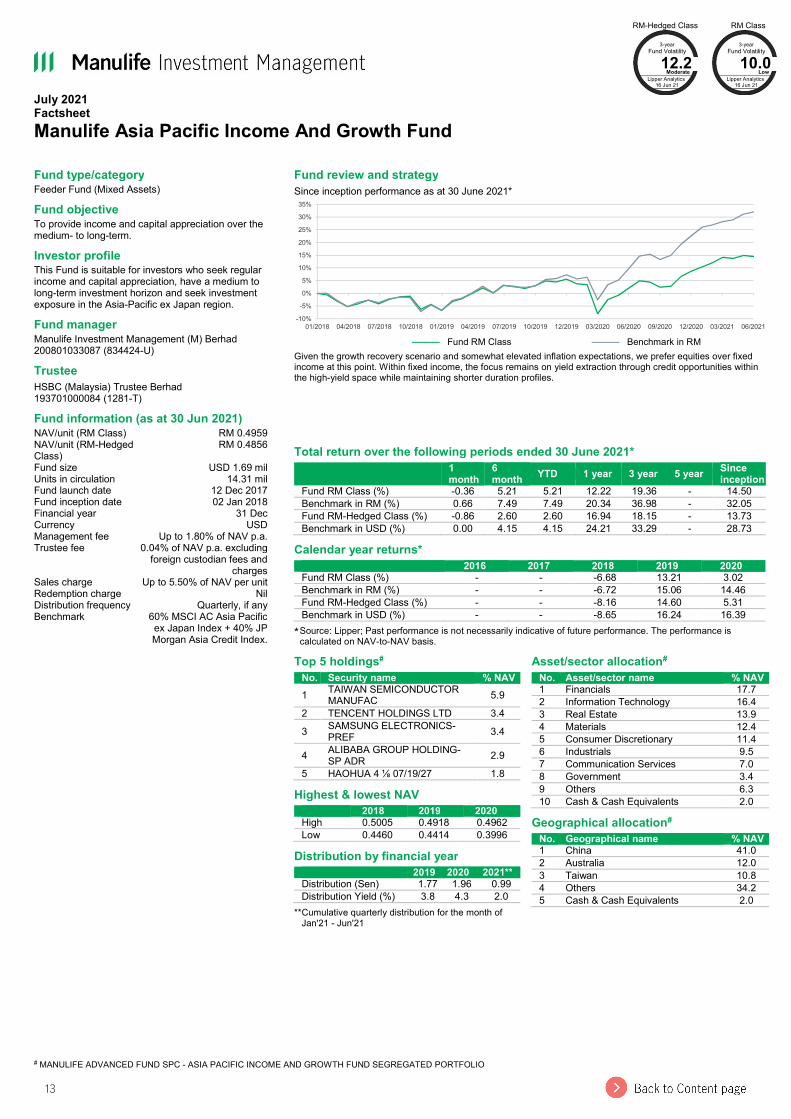

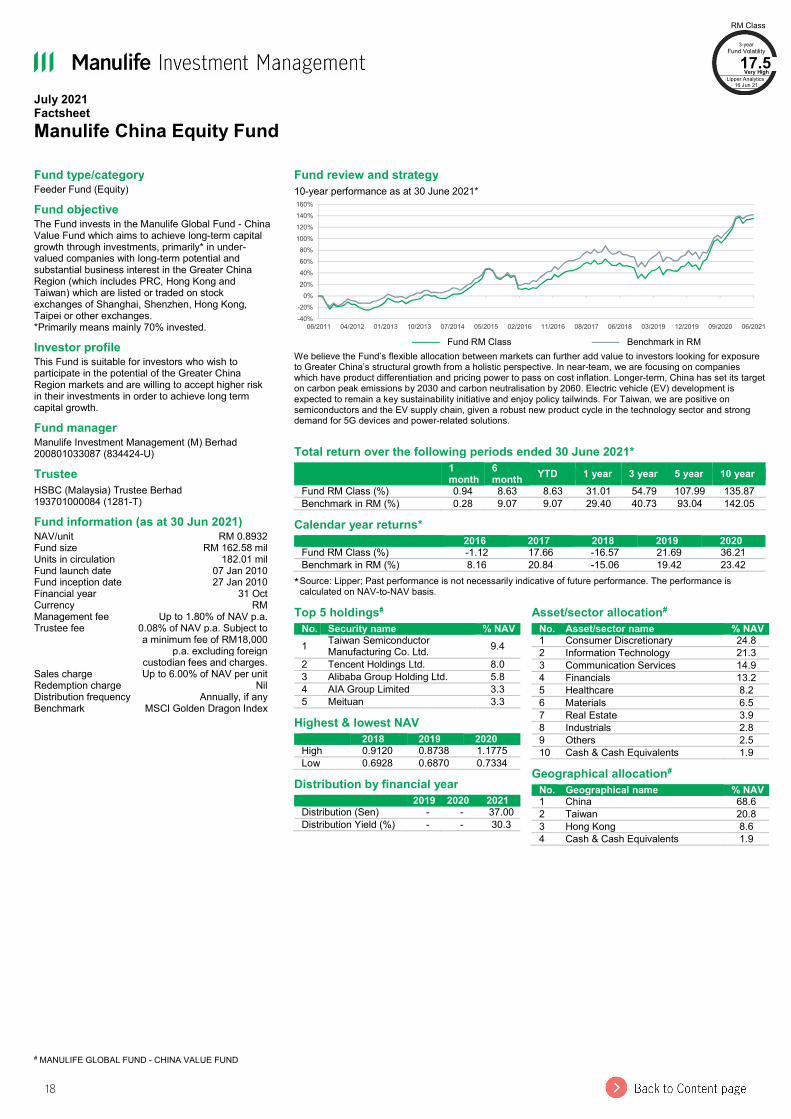

July 2021 Factsheet Manulife Asia Pacific Income And Growth Fund

# MANULIFE ADVANCED FUND SPC - ASIA PACIFIC INCOME AND GROWTH FUND SEGREGATED PORTFOLIO

Fund type/category Feeder Fund (Mixed Assets) Fund objective To provide income and capital appreciation over the medium- to long-term. Investor profile This Fund is suitable for investors who seek regular income and capital appreciation, have a medium to long-term investment horizon and seek investment exposure in the Asia-Pacific ex Japan region. Fund manager Manulife Investment Management (M) Berhad 200801033087 (834424-U) Trustee HSBC (Malaysia) Trustee Berhad 193701000084 (1281-T) Fund information (as at 30 Jun 2021) NAV/unit (RM Class) RM 0.4959 NAV/unit (RM-Hedged Class)

RM 0.4856 Fund size USD 1.69 mil Units in circulation 14.31 mil Fund launch date 12 Dec 2017 Fund inception date 02 Jan 2018 Financial year 31 Dec Currency USD Management fee Up to 1.80% of NAV p.a. Trustee fee 0.04% of NAV p.a. excluding

foreign custodian fees and charges

Sales charge Up to 5.50% of NAV per unit Redemption charge Nil Distribution frequency Quarterly, if any Benchmark 60% MSCI AC Asia Pacific

ex Japan Index + 40% JP Morgan Asia Credit Index.

Fund review and strategy Since inception performance as at 30 June 2021*

——— Fund RM Class ——— Benchmark in RM

Given the growth recovery scenario and somewhat elevated inflation expectations, we prefer equities over fixed income at this point. Within fixed income, the focus remains on yield extraction through credit opportunities within the high-yield space while maintaining shorter duration profiles.

Total return over the following periods ended 30 June 2021*

1 month

6 month YTD 1 year 3 year 5 year Since

inception Fund RM Class (%) -0.36 5.21 5.21 12.22 19.36 - 14.50 Benchmark in RM (%) 0.66 7.49 7.49 20.34 36.98 - 32.05 Fund RM-Hedged Class (%) -0.86 2.60 2.60 16.94 18.15 - 13.73 Benchmark in USD (%) 0.00 4.15 4.15 24.21 33.29 - 28.73

Calendar year returns* 2016 2017 2018 2019 2020

Fund RM Class (%) - - -6.68 13.21 3.02 Benchmark in RM (%) - - -6.72 15.06 14.46 Fund RM-Hedged Class (%) - - -8.16 14.60 5.31 Benchmark in USD (%) - - -8.65 16.24 16.39

* Source: Lipper; Past performance is not necessarily indicative of future performance. The performance is calculated on NAV-to-NAV basis.

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

01/2018 04/2018 07/2018 10/2018 01/2019 04/2019 07/2019 10/2019 12/2019 03/2020 06/2020 09/2020 12/2020 03/2021 06/2021

Top 5 holdings# No. Security name % NAV

1 TAIWAN SEMICONDUCTOR MANUFAC 5.9

2 TENCENT HOLDINGS LTD 3.4 3 SAMSUNG ELECTRONICS-

PREF 3.4

4 ALIBABA GROUP HOLDING-SP ADR 2.9

5 HAOHUA 4 ⅛ 07/19/27 1.8 Highest & lowest NAV 2018 2019 2020

High 0.5005 0.4918 0.4962 Low 0.4460 0.4414 0.3996

Distribution by financial year 2019 2020 2021**

Distribution (Sen) 1.77 1.96 0.99 Distribution Yield (%) 3.8 4.3 2.0

** Cumulative quarterly distribution for the month of Jan'21 - Jun'21

Asset/sector allocation# No. Asset/sector name % NAV

1 Financials 17.7 2 Information Technology 16.4 3 Real Estate 13.9 4 Materials 12.4 5 Consumer Discretionary 11.4 6 Industrials 9.5 7 Communication Services 7.0 8 Government 3.4 9 Others 6.3 10 Cash & Cash Equivalents 2.0

Geographical allocation# No. Geographical name % NAV

1 China 41.0 2 Australia 12.0 3 Taiwan 10.8 4 Others 34.2 5 Cash & Cash Equivalents 2.0

RM Class 3-year

Fund Volatility 10.0

Low Lipper Analytics

16 Jun 21

RM-Hedged Class 3-year

Fund Volatility 12.2

Moderate Lipper Analytics

16 Jun 21

July 2021 Factsheet Manulife Asia Pacific Income And Growth Fund

# MANULIFE ADVANCED FUND SPC - ASIA PACIFIC INCOME AND GROWTH FUND SEGREGATED PORTFOLIO

Fund type/category Feeder Fund (Mixed Assets) Fund objective To provide income and capital appreciation over the medium- to long-term. Investor profile This Fund is suitable for investors who seek regular income and capital appreciation, have a medium to long-term investment horizon and seek investment exposure in the Asia-Pacific ex Japan region. Fund manager Manulife Investment Management (M) Berhad 200801033087 (834424-U) Trustee HSBC (Malaysia) Trustee Berhad 193701000084 (1281-T) Fund information (as at 30 Jun 2021) NAV/unit (RM Class) RM 0.4959 NAV/unit (RM-Hedged Class)

RM 0.4856 Fund size USD 1.69 mil Units in circulation 14.31 mil Fund launch date 12 Dec 2017 Fund inception date 02 Jan 2018 Financial year 31 Dec Currency USD Management fee Up to 1.80% of NAV p.a. Trustee fee 0.04% of NAV p.a. excluding

foreign custodian fees and charges

Sales charge Up to 5.50% of NAV per unit Redemption charge Nil Distribution frequency Quarterly, if any Benchmark 60% MSCI AC Asia Pacific

ex Japan Index + 40% JP Morgan Asia Credit Index.

Fund review and strategy Since inception performance as at 30 June 2021*

——— Fund RM Class ——— Benchmark in RM

Given the growth recovery scenario and somewhat elevated inflation expectations, we prefer equities over fixed income at this point. Within fixed income, the focus remains on yield extraction through credit opportunities within the high-yield space while maintaining shorter duration profiles.

Total return over the following periods ended 30 June 2021*

1 month

6 month YTD 1 year 3 year 5 year Since

inception Fund RM Class (%) -0.36 5.21 5.21 12.22 19.36 - 14.50 Benchmark in RM (%) 0.66 7.49 7.49 20.34 36.98 - 32.05 Fund RM-Hedged Class (%) -0.86 2.60 2.60 16.94 18.15 - 13.73 Benchmark in USD (%) 0.00 4.15 4.15 24.21 33.29 - 28.73

Calendar year returns* 2016 2017 2018 2019 2020

Fund RM Class (%) - - -6.68 13.21 3.02 Benchmark in RM (%) - - -6.72 15.06 14.46 Fund RM-Hedged Class (%) - - -8.16 14.60 5.31 Benchmark in USD (%) - - -8.65 16.24 16.39

* Source: Lipper; Past performance is not necessarily indicative of future performance. The performance is calculated on NAV-to-NAV basis.

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

01/2018 04/2018 07/2018 10/2018 01/2019 04/2019 07/2019 10/2019 12/2019 03/2020 06/2020 09/2020 12/2020 03/2021 06/2021

Top 5 holdings# No. Security name % NAV

1 TAIWAN SEMICONDUCTOR MANUFAC 5.9

2 TENCENT HOLDINGS LTD 3.4 3 SAMSUNG ELECTRONICS-

PREF 3.4

4 ALIBABA GROUP HOLDING-SP ADR 2.9

5 HAOHUA 4 ⅛ 07/19/27 1.8 Highest & lowest NAV 2018 2019 2020

High 0.5005 0.4918 0.4962 Low 0.4460 0.4414 0.3996

Distribution by financial year 2019 2020 2021**

Distribution (Sen) 1.77 1.96 0.99 Distribution Yield (%) 3.8 4.3 2.0

** Cumulative quarterly distribution for the month of Jan'21 - Jun'21

Asset/sector allocation# No. Asset/sector name % NAV

1 Financials 17.7 2 Information Technology 16.4 3 Real Estate 13.9 4 Materials 12.4 5 Consumer Discretionary 11.4 6 Industrials 9.5 7 Communication Services 7.0 8 Government 3.4 9 Others 6.3 10 Cash & Cash Equivalents 2.0

Geographical allocation# No. Geographical name % NAV

1 China 41.0 2 Australia 12.0 3 Taiwan 10.8 4 Others 34.2 5 Cash & Cash Equivalents 2.0

RM Class 3-year

Fund Volatility 10.0

Low Lipper Analytics

16 Jun 21

RM-Hedged Class 3-year

Fund Volatility 12.2

Moderate Lipper Analytics

16 Jun 21

14

July 2021 Factsheet Manulife Asia Pacific Income And Growth Fund Market Review Asia ex Japan equity markets moved marginally lower in June. Two catalysts dominated global equity markets for the month. In mid-June, the US Federal Reserve Board (Fed)’s unexpectedly hawkish statement that rates might be raised twice in 2023 due to rising inflationary pressures bolstered the US dollar and roiled equity markets, particularly emerging markets. In addition, the spread of the Delta variant of Covid-19 notably increased caseloads globally, particularly in Southeast Asia where lockdowns were reinstated due to lower vaccination rates. As a result, only a handful of regional markets posted gains (mostly in Northeast Asia except for the Philippines and Vietnam), while all major regional currencies were flat or weakened against the US dollar). In the United States, Treasury yields declined on the back of mixed economic data and the Federal Open Market Committee meeting. The May non-farm payrolls report came in short of market expectations that the US economy added 559,000 jobs, while the headline consumer price index rose by 5% year-on-year in May, hitting the highest monthly gains since 2008. The Fed was generally viewed as hawkish after they kept rates unchanged and hinted at the likelihood of higher rate hikes. The Fed’s dot plot pointed to two hikes by the end of 2023, but the Fed did not issue guidance on tapering its asset purchases. Post-Fed meeting, Fed officials eased inflation fears and expected inflationary pressure to be transitory. Over the period, the 10-year Treasury yield fell from 1.59% to 1.47%. Asian credit markets posted positive returns over the month owing to lower US Treasury yields and positive carry, offsetting wider credit spreads in the high-yield space. The Asian high yield corporate segment underperformed Asian investment grade credit; the JP Morgan Asian High Yield Corporate Bond Index decreased by -1.27%, while the JP Morgan Asian Investment Grade Corporate Bond Index increased by 0.82% in US dollar terms. Chinese high-yield names were soft, dragged by financing pressure and policy tightening concerns on the Chinese property sector, whilst investment grade credit remained relatively resilient. In Malaysia, S&P affirmed its A- sovereign rating and maintained a negative outlook due to renewed Covid-19 cases, though it did not induce significant price action. China equities moved marginally lower for the month. While onshore indices were essentially flat, growth-related indices (ChiNext and STAR 50) notably outperformed. In terms of capital flows, northbound inflows totalled 15 billion renminbi for the month, notably down from the 56 billion renminbi in May. On the economic front, monthly data in retail sales, fixed asset investments, and industrial output suggested weaker activity as they failed to meet market consensus. Taiwan’s equity market moved higher for the month even as several factors drove technology shares lower: concerns over supply chain breaks due to Covid-19 restrictions, a less optimistic outlook for global smartphone sales, and lower price hikes expected in the panel sector. On the economic front, exports continued their strong run, moving up 38.6% (year-on-year) in May. South Korean equity markets posted gains for the month. Equities were boosted by the floating of several successful initial public offerings, as well as declining investor fears over inflation and moderately optimistic expectations for the second quarter earnings season. On the economic front, exports posted their best performance since August 1988, surging 46 percent (year-on-year) in May. Indian equities posted losses for the month despite the decreasing number of Covid-19 cases. The Indian government unveiled new measures to help the economy at the end of the month, including additional lending for loan guarantee schemes and a broadening of credit guarantees. The Reserve Bank of India also pledged to maintain ample liquidity for markets, announcing it would increase already aggressive purchases of government bonds in third quarter. ASEAN markets were all lower except for the Philippines where the equity market moved higher on optimism of the economic opening; areas outside the capital were opened despite further restrictions imposed around Manila. The central bank pledged an accommodative position until at least the first half of 2022, as inflationary pressures receded in May. In Indonesia, a notable increase in the number of Covid-19 cases that led to further lockdowns, coupled with a hawkish Fed statement, weakened the rupiah and sent equities sharply lower. Malaysian equity markets were lower as the national lockdown originally scheduled for the first two weeks of June was extended through July – no end date was given. In Thailand, a notable increase in Covid-19 cases resulted in the country’s parliament passing a bill to borrow US$16 billion for virus-related fiscal relief. Political instability also increased as protestors calling for constitutional reform headed back onto the streets of the capital. In Australia, equity markets posted losses for the month. Equity markets moved lower as commodity prices on key exports were mixed – iron ore moved higher while copper receded – and new administrative lockdowns were imposed due to the spread of the Delta variant. Feeder Fund Review In June, the Feeder Fund posted -0.36% versus the benchmark return of 0.66% for its RM class while returned -0.86% versus the benchmark return of 0.002% for its RM-Hedged class. The Fund’s equity portion detracted on the back of stock selection at the country and sector level and asset allocation decisions at the country level. Stock selection in China, Taiwan and South Korea and the overweight to Singapore were the primary detractors to performance. Partially offsetting the detraction was stock selection in India. Detracting from performance was the Fund’s holding in a Chinese cybersecurity software company over concerns of weak second quarter results due to a delay in the government’s tender. However, we believe that the long-term structural growth in cybersecurity remains intact and supportive government policies should help support future growth. Another detractor was a Hong Kong fixed line telecommunications company that guided toward lower-than-expected divided per share growth on the back of stalled economic activity in Hong Kong driven by the global Covid pandemic. Contributing positively was the Fund’s holding in a Chinese e-commerce company after recording record gross merchandise value during the most recent promotional sales season. The company continues to increase its new business investment which should drive its future earnings. Another contributor was a Taiwanese wafer manufacturer on the back of an improved demand/supply outlook. The company’s long-term agreements for wafer supply should provide visibility to its revenue and earnings stream considering a tighter supply/demand situation owing to increasing demand but limited supply increase. Over the period, the portfolio’s overall security selection contributed to performance with US dollar-denominated holdings of a Chinese chemical state-owned-enterprise and an Indonesian cooking oil manufacturer being the outperformers. However, underweight US dollar interest rate duration positioning detracted as Treasury yields fell over the period. Overweight to US dollar-denominated Asian corporate bonds also detracted as this segment underperformed the broad Asian credit market. Market Outlook Despite global equity market valuations looking elevated relative to history, low absolute interest rates and somewhat depressed earnings need to be kept in mind with multiples looking far more reasonable several years out. Asian equities continue to trade at a reasonable discount to global markets and we anticipate strong double-digit earnings recovery in 2021. Although 10-year bond yields have risen since the start of the year, equity dividend yields continue to look attractive compared to bond yields. We see scope for further reductions in valuation dispersions between high price-earnings growth stocks and stocks that have attractive yields as we enter a period of global economic recovery as vaccinations take hold across the region and around the world.

15

July 2021 Factsheet Manulife Asia Pacific Income And Growth Fund The strength in the anticipated economic recovery has led us to favour more cyclical yields such as within materials and ports for instance. The consumer spending recovery is also prompting us to increase our allocation towards the consumer discretionary sector particularly those who also have solid long-term growth prospects. Bond proxy equities are less favoured compared to last year given the recent steepening in the yield curve. Although real estate investment trusts can be considered as bond proxies, we maintain a strong allocation as a source of yield although we favour trusts that benefit from re-opening post-Covid lockdowns such as retail commercial trusts. We also continue to see strong value in many expressway companies which are seeing a dramatic increase in traffic post-Covid. Many companies we like that offer robust growth at a reasonable yield continue to be within the Taiwanese information technology sector which continues to benefit from ongoing chip shortages and ongoing structural growth profiles with solid cash flows and generous dividend payout ratios. We continue to hold several exposures within the banking sector. The steepening yield curve together with our view that many regional property markets should see a recovery in activity should lead to stronger earnings fundamentals. In terms of growth sectors, we see some value emerging back into the Chinese e-commerce sector which has corrected due to the anti-monopoly campaign. Compared to a few months ago, there is a lot more clarity on what the earnings impact would be from fines and alterations to business practices. Overall, the earnings growth profile continues to look attractive at much lower valuations. Given the growth recovery scenario and somewhat elevated inflation expectations, we prefer equities over fixed income at this point. Within fixed income, the focus remains on yield extraction through credit opportunities within the high-yield space while maintaining shorter duration profiles. Based on the Fund's portfolio returns as at 31 May 2021 the Volatility Factor (VF) for the Fund is as indicated in the table above and are classified as in the table (source: Lipper). "Very High" includes Funds with VF that are above 17.190, "High" includes Funds with VF that are above 14.310 but not more than 17.190, "Moderate" includes Funds with VF that are above 10.755 but not more than 14.310, "Low" includes Funds with VF that are above 3.645 but not more than 10.755 and "Very Low" includes Funds with VF that are above 0.000 but not more than 3.645 (source:FiMM). The VF means there is a possibility for the Funds in generating an upside return or downside return around this VF. The Volatility Class (VC) is assigned by Lipper based on quintile ranks of VF for qualified Funds. VF and VC are subject to monthly revision or at any interval which may be prescribed by FIMM from time to time. The Fund's portfolio may have changed since this date and there is no guarantee that the Funds will continue to have the same VF or VC in the future. Presently, only Funds launched in the market for at least 36 months will display the VF and its VC. The above information has not been reviewed by the SC and is subject to the relevant warning, disclaimer, qualification or terms and conditions stated herein. Investors are advised to read and understand the contents of the Master Prospectus dated 10 August 2020 and its First Supplemental Master Prospectus dated 10 August 2020 and its Second Supplemental Master Prospectus dated 27 January 2021 and its Third Supplemental Master Prospectus dated 5 April 2021 and all the respective Product Highlights Sheet(s) (collectively, the “Offering Documents”), obtainable at our offices or website, before investing. The Offering Documents have been registered with the Securities Commission Malaysia (SC), however the registration with the SC does not amount to nor indicate that the SC has recommended or endorsed the product. Where a unit split/distribution is declared, investors are advised that following the issue of additional units/distribution, the NAV per unit will be reduced from the pre-unit split NAV/cum-distribution NAV to post-unit split NAV/ex-distribution NAV; and where a unit split is declared, the value of your investment in the Fund’s denominated currency will remained unchanged after the distribution of the additional units. Past performances are not an indication of future performances. There are risks involved with investing in unit trust funds; wholesale funds and/or Private Retirement Schemes. Some of these risks associated with investments in unit trust funds; wholesale funds and/or Private Retirement Schemes are interest rate fluctuation risk, foreign exchange or currency risk, country risk, political risk, credit risk, non-compliance risk, counterparty risk, target fund manager risk, liquidity risk and interest rate risk. For further details on the risk profile of all the funds, please refer to the Risk Factors section in the Offering Documents. The price of units and income distribution may go down as well as up. Investors should compare and consider the fees, charges and costs involved. Investors are advised to conduct own risk assessment and consult the professional advisers if in doubt on the action to be taken.

16

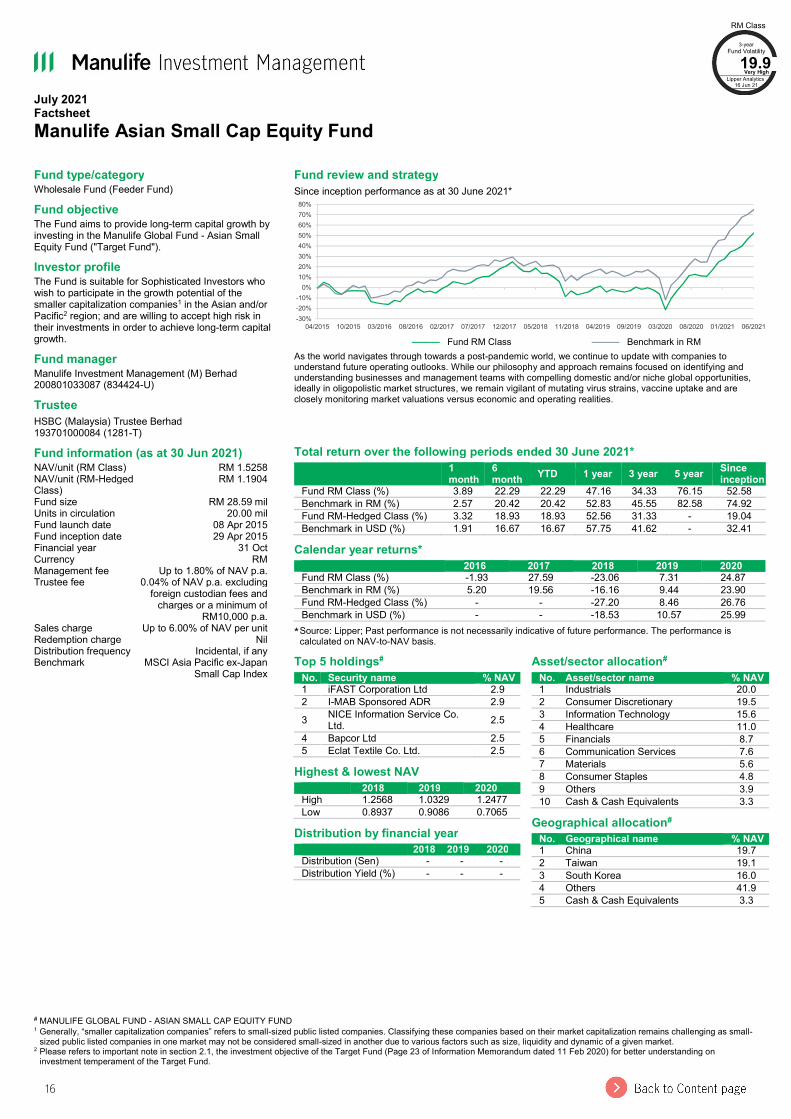

July 2021 Factsheet Manulife Asian Small Cap Equity Fund

# MANULIFE GLOBAL FUND - ASIAN SMALL CAP EQUITY FUND 1 Generally, “smaller capitalization companies” refers to small-sized public listed companies. Classifying these companies based on their market capitalization remains challenging as small-

sized public listed companies in one market may not be considered small-sized in another due to various factors such as size, liquidity and dynamic of a given market. 2 Please refers to important note in section 2.1, the investment objective of the Target Fund (Page 23 of Information Memorandum dated 11 Feb 2020) for better understanding on

investment temperament of the Target Fund.

Fund type/category Wholesale Fund (Feeder Fund) Fund objective The Fund aims to provide long-term capital growth by investing in the Manulife Global Fund - Asian Small Equity Fund ("Target Fund"). Investor profile The Fund is suitable for Sophisticated Investors who wish to participate in the growth potential of the smaller capitalization companies1 in the Asian and/or Pacific2 region; and are willing to accept high risk in their investments in order to achieve long-term capital growth. Fund manager Manulife Investment Management (M) Berhad 200801033087 (834424-U) Trustee HSBC (Malaysia) Trustee Berhad 193701000084 (1281-T) Fund information (as at 30 Jun 2021) NAV/unit (RM Class) RM 1.5258 NAV/unit (RM-Hedged Class)

RM 1.1904 Fund size RM 28.59 mil Units in circulation 20.00 mil Fund launch date 08 Apr 2015 Fund inception date 29 Apr 2015 Financial year 31 Oct Currency RM Management fee Up to 1.80% of NAV p.a. Trustee fee 0.04% of NAV p.a. excluding

foreign custodian fees and charges or a minimum of

RM10,000 p.a. Sales charge Up to 6.00% of NAV per unit Redemption charge Nil Distribution frequency Incidental, if any Benchmark MSCI Asia Pacific ex-Japan

Small Cap Index

Fund review and strategy Since inception performance as at 30 June 2021*

——— Fund RM Class ——— Benchmark in RM

As the world navigates through towards a post-pandemic world, we continue to update with companies to understand future operating outlooks. While our philosophy and approach remains focused on identifying and understanding businesses and management teams with compelling domestic and/or niche global opportunities, ideally in oligopolistic market structures, we remain vigilant of mutating virus strains, vaccine uptake and are closely monitoring market valuations versus economic and operating realities.

Total return over the following periods ended 30 June 2021*

1 month

6 month YTD 1 year 3 year 5 year Since

inception Fund RM Class (%) 3.89 22.29 22.29 47.16 34.33 76.15 52.58 Benchmark in RM (%) 2.57 20.42 20.42 52.83 45.55 82.58 74.92 Fund RM-Hedged Class (%) 3.32 18.93 18.93 52.56 31.33 - 19.04 Benchmark in USD (%) 1.91 16.67 16.67 57.75 41.62 - 32.41

Calendar year returns* 2016 2017 2018 2019 2020

Fund RM Class (%) -1.93 27.59 -23.06 7.31 24.87 Benchmark in RM (%) 5.20 19.56 -16.16 9.44 23.90 Fund RM-Hedged Class (%) - - -27.20 8.46 26.76 Benchmark in USD (%) - - -18.53 10.57 25.99

* Source: Lipper; Past performance is not necessarily indicative of future performance. The performance is calculated on NAV-to-NAV basis.

-30%-20%-10%

0%10%20%30%40%50%60%70%80%

04/2015 10/2015 03/2016 08/2016 02/2017 07/2017 12/2017 05/2018 11/2018 04/2019 09/2019 03/2020 08/2020 01/2021 06/2021

Top 5 holdings# No. Security name % NAV

1 iFAST Corporation Ltd 2.9 2 I-MAB Sponsored ADR 2.9 3 NICE Information Service Co.

Ltd. 2.5 4 Bapcor Ltd 2.5 5 Eclat Textile Co. Ltd. 2.5

Highest & lowest NAV 2018 2019 2020

High 1.2568 1.0329 1.2477 Low 0.8937 0.9086 0.7065

Distribution by financial year 2018 2019 2020

Distribution (Sen) - - - Distribution Yield (%) - - -

Asset/sector allocation# No. Asset/sector name % NAV

1 Industrials 20.0 2 Consumer Discretionary 19.5 3 Information Technology 15.6 4 Healthcare 11.0 5 Financials 8.7 6 Communication Services 7.6 7 Materials 5.6 8 Consumer Staples 4.8 9 Others 3.9 10 Cash & Cash Equivalents 3.3

Geographical allocation# No. Geographical name % NAV

1 China 19.7 2 Taiwan 19.1 3 South Korea 16.0 4 Others 41.9 5 Cash & Cash Equivalents 3.3

RM Class 3-year

Fund Volatility 19.9

Very High Lipper Analytics

16 Jun 21

July 2021 Factsheet Manulife Asian Small Cap Equity Fund

# MANULIFE GLOBAL FUND - ASIAN SMALL CAP EQUITY FUND 1 Generally, “smaller capitalization companies” refers to small-sized public listed companies. Classifying these companies based on their market capitalization remains challenging as small-

sized public listed companies in one market may not be considered small-sized in another due to various factors such as size, liquidity and dynamic of a given market. 2 Please refers to important note in section 2.1, the investment objective of the Target Fund (Page 23 of Information Memorandum dated 11 Feb 2020) for better understanding on

investment temperament of the Target Fund.

Fund type/category Wholesale Fund (Feeder Fund) Fund objective The Fund aims to provide long-term capital growth by investing in the Manulife Global Fund - Asian Small Equity Fund ("Target Fund"). Investor profile The Fund is suitable for Sophisticated Investors who wish to participate in the growth potential of the smaller capitalization companies1 in the Asian and/or Pacific2 region; and are willing to accept high risk in their investments in order to achieve long-term capital growth. Fund manager Manulife Investment Management (M) Berhad 200801033087 (834424-U) Trustee HSBC (Malaysia) Trustee Berhad 193701000084 (1281-T) Fund information (as at 30 Jun 2021) NAV/unit (RM Class) RM 1.5258 NAV/unit (RM-Hedged Class)

RM 1.1904 Fund size RM 28.59 mil Units in circulation 20.00 mil Fund launch date 08 Apr 2015 Fund inception date 29 Apr 2015 Financial year 31 Oct Currency RM Management fee Up to 1.80% of NAV p.a. Trustee fee 0.04% of NAV p.a. excluding

foreign custodian fees and charges or a minimum of

RM10,000 p.a. Sales charge Up to 6.00% of NAV per unit Redemption charge Nil Distribution frequency Incidental, if any Benchmark MSCI Asia Pacific ex-Japan

Small Cap Index

Fund review and strategy Since inception performance as at 30 June 2021*

——— Fund RM Class ——— Benchmark in RM

As the world navigates through towards a post-pandemic world, we continue to update with companies to understand future operating outlooks. While our philosophy and approach remains focused on identifying and understanding businesses and management teams with compelling domestic and/or niche global opportunities, ideally in oligopolistic market structures, we remain vigilant of mutating virus strains, vaccine uptake and are closely monitoring market valuations versus economic and operating realities.

Total return over the following periods ended 30 June 2021*

1 month

6 month YTD 1 year 3 year 5 year Since

inception Fund RM Class (%) 3.89 22.29 22.29 47.16 34.33 76.15 52.58 Benchmark in RM (%) 2.57 20.42 20.42 52.83 45.55 82.58 74.92 Fund RM-Hedged Class (%) 3.32 18.93 18.93 52.56 31.33 - 19.04 Benchmark in USD (%) 1.91 16.67 16.67 57.75 41.62 - 32.41

Calendar year returns* 2016 2017 2018 2019 2020

Fund RM Class (%) -1.93 27.59 -23.06 7.31 24.87 Benchmark in RM (%) 5.20 19.56 -16.16 9.44 23.90 Fund RM-Hedged Class (%) - - -27.20 8.46 26.76 Benchmark in USD (%) - - -18.53 10.57 25.99

* Source: Lipper; Past performance is not necessarily indicative of future performance. The performance is calculated on NAV-to-NAV basis.

-30%-20%-10%

0%10%20%30%40%50%60%70%80%

04/2015 10/2015 03/2016 08/2016 02/2017 07/2017 12/2017 05/2018 11/2018 04/2019 09/2019 03/2020 08/2020 01/2021 06/2021

Top 5 holdings# No. Security name % NAV

1 iFAST Corporation Ltd 2.9 2 I-MAB Sponsored ADR 2.9 3 NICE Information Service Co.

Ltd. 2.5 4 Bapcor Ltd 2.5 5 Eclat Textile Co. Ltd. 2.5

Highest & lowest NAV 2018 2019 2020

High 1.2568 1.0329 1.2477 Low 0.8937 0.9086 0.7065

Distribution by financial year 2018 2019 2020

Distribution (Sen) - - - Distribution Yield (%) - - -

Asset/sector allocation# No. Asset/sector name % NAV

1 Industrials 20.0 2 Consumer Discretionary 19.5 3 Information Technology 15.6 4 Healthcare 11.0 5 Financials 8.7 6 Communication Services 7.6 7 Materials 5.6 8 Consumer Staples 4.8 9 Others 3.9 10 Cash & Cash Equivalents 3.3

Geographical allocation# No. Geographical name % NAV

1 China 19.7 2 Taiwan 19.1 3 South Korea 16.0 4 Others 41.9 5 Cash & Cash Equivalents 3.3

RM Class 3-year

Fund Volatility 19.9

Very High Lipper Analytics

16 Jun 21

17