four different groups of recursive tests forward recursive tests

Post on 22-Dec-2015

257 views

TRANSCRIPT

Four different groups of recursive tests

Forward recursive tests

Recursively calculated trace tests

Recursively calculated trace tests

Recursively calculated eigenvalues

Recursively calculated eigenvalues

Log transformed eigenvalues

The fluctuations test

A detailed discussion of the test procedure will be given in Chapter 12

The max test of beta.

Tests of known beta. Reference period: full sample

Tests of known beta. Reference period: 1986:1-2003:1

Tests of known beta. Reference period: 1973:2-1986:1

One-step ahead prediction tests

One-step-ahead prediction tests for the system

Prediction tests for each variable: X-form VAR

Prediction tests for each variable. R-form VAR

Backward recursive test of loglikelihood function

Test for Constancy of the Log-Likelihood

1973 1974 1975 1976 1977 1978 1979 1980 1981 1982 1983 1984 19850.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5X(t)

R1(t)

5% C.V. (1.36 = Index)

Backwards recursively calculated trace tests

Backwards calculated log transformed eigenvalues

Backwards calculated fluctuations tests

Eigenv alue Fluctuation Test

Tau(Ksi) = C(T)| |Ksi(t)-Ksi(T)| |

1973 1975 1977 1979 1981 1983 19850.00

0.25

0.50

0.75

1.00X( t )R1( t )5% C. V. (1. 36 = I ndex)

Tau(Ksi(1))

1973 1975 1977 1979 1981 1983 19850.00

0.25

0.50

0.75

1.00X( t )R1( t )5% C. V. (1. 36 = I ndex)

Tau(Ksi(2))

1973 1975 1977 1979 1981 1983 19850.00

0.25

0.50

0.75

1.00X( t )R1( t )5% C. V. (1. 36 = I ndex)

Tau(Ksi(3))

1973 1975 1977 1979 1981 1983 19850.00

0.25

0.50

0.75

1.00X( t )R1( t )5% C. V. (1. 36 = I ndex)

Tau(Ksi(1)+...+Ksi(3))

The max test of parameter constancy

Test of Beta Constancy

1973 1974 1975 1976 1977 1978 1979 1980 1981 1982 1983 1984 19850.00

0.25

0.50

0.75

1.00X(t)R 1(t)5% C .V. (3.92 = Index )

Q(t)

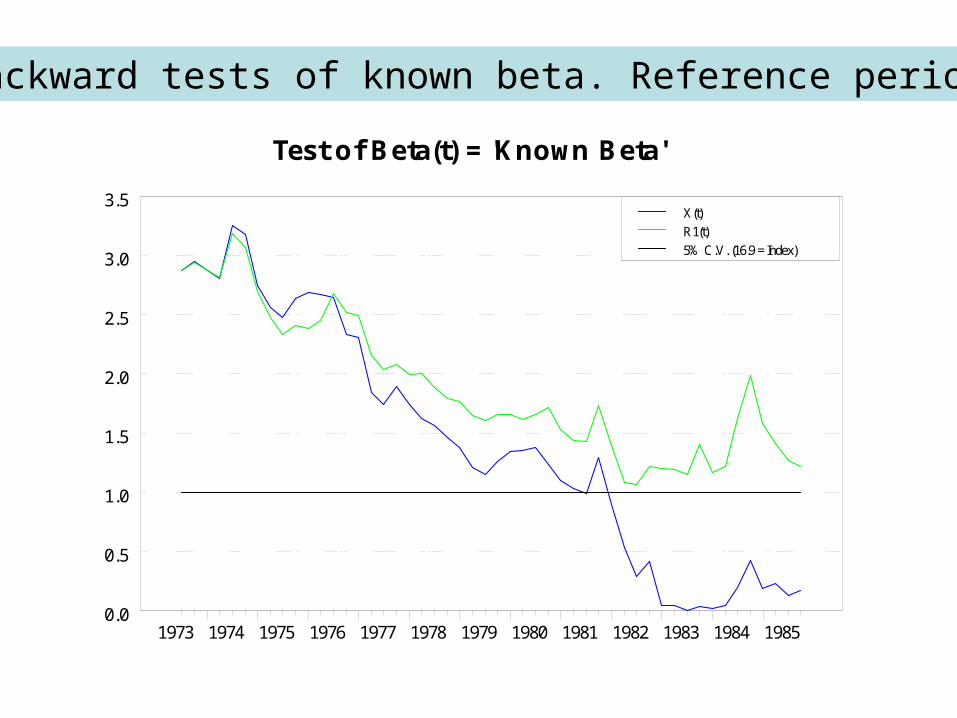

Backward tests of known beta. Reference period ?

Test of Beta(t) = 'Known Beta'

1973 1974 1975 1976 1977 1978 1979 1980 1981 1982 1983 1984 19850.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5X(t)

R1(t)

5% C.V. (16.9 = Index)

Recursively back-casting the system

Recursively back-forecasting each variable. X-form VAR

Back-forecasting each of the variables based on the VAR in R-form