Four different groups of recursive tests

Forward recursive tests

Recursively calculated trace tests

Recursively calculated trace tests

Recursively calculated eigenvalues

Recursively calculated eigenvalues

Log transformed eigenvalues

The fluctuations test

A detailed discussion of the test procedure will be given in Chapter 12

The max test of beta.

Tests of known beta. Reference period: full sample

Tests of known beta. Reference period: 1986:1-2003:1

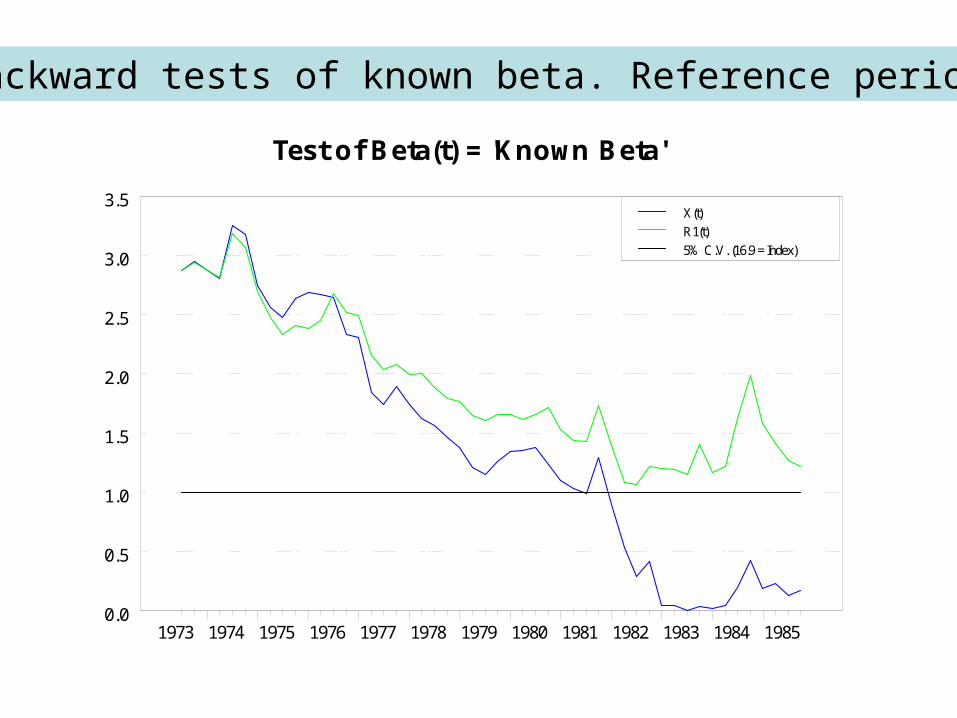

Tests of known beta. Reference period: 1973:2-1986:1

One-step ahead prediction tests

One-step-ahead prediction tests for the system

Prediction tests for each variable: X-form VAR

Prediction tests for each variable. R-form VAR

Backward recursive test of loglikelihood function

Test for Constancy of the Log-Likelihood

1973 1974 1975 1976 1977 1978 1979 1980 1981 1982 1983 1984 19850.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5X(t)

R1(t)

5% C.V. (1.36 = Index)

Backwards recursively calculated trace tests

Backwards calculated log transformed eigenvalues

Backwards calculated fluctuations tests

Eigenv alue Fluctuation Test

Tau(Ksi) = C(T)| |Ksi(t)-Ksi(T)| |

1973 1975 1977 1979 1981 1983 19850.00

0.25

0.50

0.75

1.00X( t )R1( t )5% C. V. (1. 36 = I ndex)

Tau(Ksi(1))

1973 1975 1977 1979 1981 1983 19850.00

0.25

0.50

0.75

1.00X( t )R1( t )5% C. V. (1. 36 = I ndex)

Tau(Ksi(2))

1973 1975 1977 1979 1981 1983 19850.00

0.25

0.50

0.75

1.00X( t )R1( t )5% C. V. (1. 36 = I ndex)

Tau(Ksi(3))

1973 1975 1977 1979 1981 1983 19850.00

0.25

0.50

0.75

1.00X( t )R1( t )5% C. V. (1. 36 = I ndex)

Tau(Ksi(1)+...+Ksi(3))

The max test of parameter constancy

Test of Beta Constancy

1973 1974 1975 1976 1977 1978 1979 1980 1981 1982 1983 1984 19850.00

0.25

0.50

0.75

1.00X(t)R 1(t)5% C .V. (3.92 = Index )

Q(t)

Backward tests of known beta. Reference period ?

Test of Beta(t) = 'Known Beta'

1973 1974 1975 1976 1977 1978 1979 1980 1981 1982 1983 1984 19850.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5X(t)

R1(t)

5% C.V. (16.9 = Index)

Recursively back-casting the system

Recursively back-forecasting each variable. X-form VAR

Back-forecasting each of the variables based on the VAR in R-form