foreclosure for clerks of superior court - unc school of ... foreclosure for clerks of superior...

TRANSCRIPT

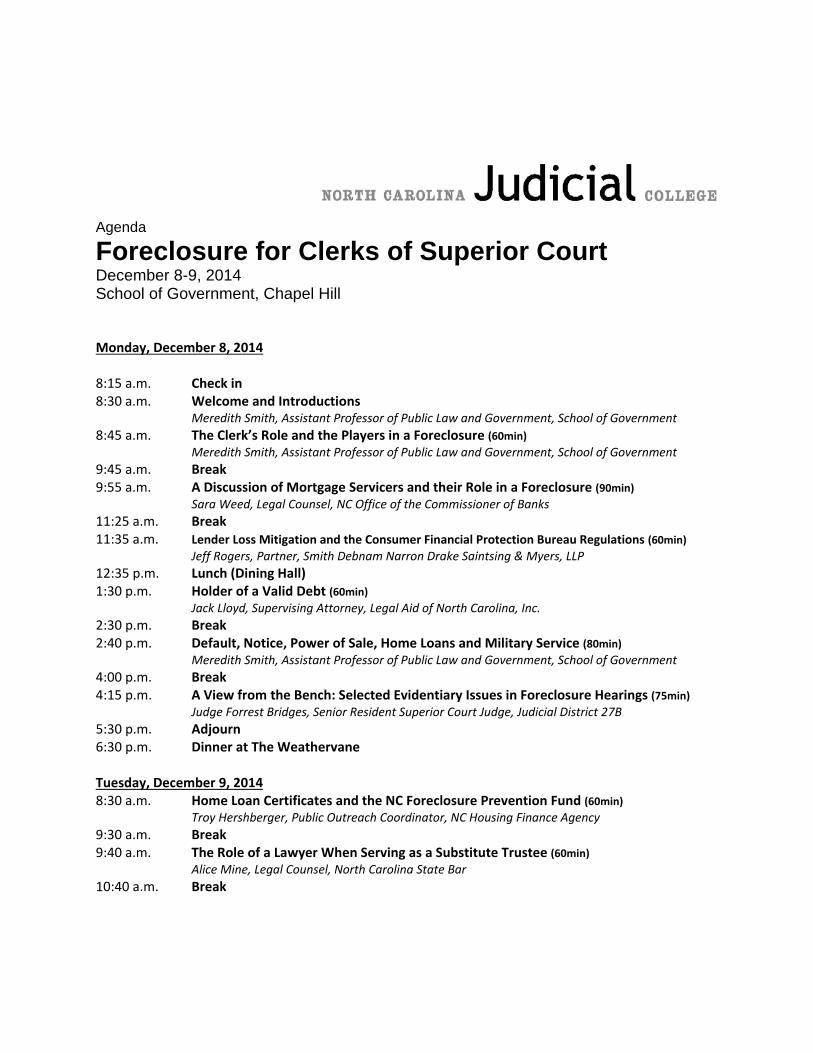

Agenda

Foreclosure for Clerks of Superior Court December 8-9, 2014 School of Government, Chapel Hill Monday, December 8, 2014 8:15 a.m. Check in 8:30 a.m. Welcome and Introductions Meredith Smith, Assistant Professor of Public Law and Government, School of Government

8:45 a.m. The Clerk’s Role and the Players in a Foreclosure (60min) Meredith Smith, Assistant Professor of Public Law and Government, School of Government

9:45 a.m. Break 9:55 a.m. A Discussion of Mortgage Servicers and their Role in a Foreclosure (90min) Sara Weed, Legal Counsel, NC Office of the Commissioner of Banks

11:25 a.m. Break 11:35 a.m. Lender Loss Mitigation and the Consumer Financial Protection Bureau Regulations (60min) Jeff Rogers, Partner, Smith Debnam Narron Drake Saintsing & Myers, LLP

12:35 p.m. Lunch (Dining Hall) 1:30 p.m. Holder of a Valid Debt (60min)

Jack Lloyd, Supervising Attorney, Legal Aid of North Carolina, Inc.

2:30 p.m. Break 2:40 p.m. Default, Notice, Power of Sale, Home Loans and Military Service (80min) Meredith Smith, Assistant Professor of Public Law and Government, School of Government 4:00 p.m. Break 4:15 p.m. A View from the Bench: Selected Evidentiary Issues in Foreclosure Hearings (75min) Judge Forrest Bridges, Senior Resident Superior Court Judge, Judicial District 27B

5:30 p.m. Adjourn 6:30 p.m. Dinner at The Weathervane Tuesday, December 9, 2014 8:30 a.m. Home Loan Certificates and the NC Foreclosure Prevention Fund (60min)

Troy Hershberger, Public Outreach Coordinator, NC Housing Finance Agency

9:30 a.m. Break 9:40 a.m. The Role of a Lawyer When Serving as a Substitute Trustee (60min) Alice Mine, Legal Counsel, North Carolina State Bar

10:40 a.m. Break

10:50 a.m. Panel Discussion: Conducting a Foreclosure Hearing (60min) Nicole Brinkley, Assistant Clerk of Superior Court, Wake County Fred Benson, Assistant Clerk of Superior Court, Mecklenburg County Johanna Finkelstein, Assistant Clerk of Superior Court, Buncombe County Teri Lawson, Assistant Clerk of Superior Court, Guilford County

Meredith Smith, Moderator, School of Government

11:50 a.m. Break 12:00 p.m. The Application of Rules of Civil Procedure to Foreclosure Hearings (30min) Ann Anderson, Assistant Professor, UNC School of Government

12:30 p.m. Box Lunches + Mock Hearing (90min) Meredith Smith, Assistant Professor of Public Law and Government, School of Government 2:00 p.m. Adjourn 12 Hours CEUs Applied for 12 General Hours of CLEs

1

Foreclosure for Clerks of Superior Court UNC School of Government

Chapel Hill, NC December 8‐9, 2014

EVALUATION

SESSION EVALUATION Monday, December 8, 2014 The Clerk's Role and the Players in Foreclosure Meredith Smith, Assistant Professor, School of Government

Strongly Strongly Please rate your instructor’s teaching: Disagree Neither Agree The instructor presented the material clearly. SD D N A SA The instructor was knowledgeable and well‐prepared. SD D N A SA The instructor’s pace was appropriate. SD D N A SA Overall, the session was skillfully done. SD D N A SA

Strongly Strongly Please rate the session content: Disagree Neither Agree The session content is important for my professional development. SD D N A SA

Was the content appropriate for your level of knowledge? Too difficult About right Too easy

Please share any additional comments about the instructor’s teaching and the session’s content. If you indicated that you were dissatisfied with one or more aspects of the instructor’s teaching or the session’s content, we are particularly interested in learning how we can do better in the future:

2

A Discussion of Mortgage Servicers and their Role in a Foreclosure Sara Weed, Legal Counsel, NC Office of the Commissioner of Banks

Strongly Strongly Please rate your instructor’s teaching: Disagree Neither Agree The instructor presented the material clearly. SD D N A SA The instructor was knowledgeable and well‐prepared. SD D N A SA The instructor’s pace was appropriate. SD D N A SA Overall, the session was skillfully done. SD D N A SA Strongly Strongly Please rate the session content: Disagree Neither Agree The session content is important for my professional development. SD D N A SA

Was the content appropriate for your level of knowledge? Too difficult About right Too easy Please share any additional comments about the instructor’s teaching and the session’s content. If you indicated that you were dissatisfied with one or more aspects of the instructor’s teaching or the session’s content, we are particularly interested in learning how we can do better in the future: Lender Loss Mitigation and the Consumer Financial Protection Bureau RegulationsJeff Rogers, Partner, Smith Debnam Narron Drake Saintsing & Myers, LLP

Strongly Strongly Please rate your instructor’s teaching: Disagree Neither Agree The instructor presented the material clearly. SD D N A SA The instructor was knowledgeable and well‐prepared. SD D N A SA The instructor’s pace was appropriate. SD D N A SA Overall, the session was skillfully done. SD D N A SA Strongly Strongly Please rate the session content: Disagree Neither Agree The session content is important for my professional development. SD D N A SA

Was the content appropriate for your level of knowledge? Too difficult About right Too easy Please share any additional comments about the instructor’s teaching and the session’s content. If you indicated that you were dissatisfied with one or more aspects of the instructor’s teaching or the session’s content, we are particularly interested in learning how we can do better in the future:

3

Holder of a Valid Debt Jack Lloyd, Supervising Attorney, Legal Aid of North Carolina, Inc.

Strongly Strongly Please rate your instructor’s teaching: Disagree Neither Agree The instructor presented the material clearly. SD D N A SA The instructor was knowledgeable and well‐prepared. SD D N A SA The instructor’s pace was appropriate. SD D N A SA Overall, the session was skillfully done. SD D N A SA

Strongly Strongly Please rate the session content: Disagree Neither Agree The session content is important for my professional development. SD D N A SA

Was the content appropriate for your level of knowledge? Too difficult About right Too easy

Please share any additional comments about the instructor’s teaching and the session’s content. If you indicated that you were dissatisfied with one or more aspects of the instructor’s teaching or the session’s content, we are particularly interested in learning how we can do better in the future:

Default, Notice, Power of Sale, Home Loans and Military Service Meredith Smith, Assistant Professor, School of Government

Strongly Strongly Please rate your instructor’s teaching: Disagree Neither Agree The instructor presented the material clearly. SD D N A SA The instructor was knowledgeable and well‐prepared. SD D N A SA The instructor’s pace was appropriate. SD D N A SA Overall, the session was skillfully done. SD D N A SA

Strongly Strongly Please rate the session content: Disagree Neither Agree The session content is important for my professional development. SD D N A SA

Was the content appropriate for your level of knowledge? Too difficult About right Too easy

Please share any additional comments about the instructor’s teaching and the session’s content. If you indicated that you were dissatisfied with one or more aspects of the instructor’s teaching or the session’s content, we are particularly interested in learning how we can do better in the future:

4

A View from the Bench: Selected Evidentiary Issues in Foreclosure Hearings Judge Forrest Bridges, Senior Resident Superior Court Judge, Judicial District 27B

Strongly Strongly Please rate your instructor’s teaching: Disagree Neither Agree The instructor presented the material clearly. SD D N A SA The instructor was knowledgeable and well‐prepared. SD D N A SA The instructor’s pace was appropriate. SD D N A SA Overall, the session was skillfully done. SD D N A SA

Strongly Strongly Please rate the session content: Disagree Neither Agree The session content is important for my professional development. SD D N A SA

Was the content appropriate for your level of knowledge? Too difficult About right Too easy

Please share any additional comments about the instructor’s teaching and the session’s content. If you indicated that you were dissatisfied with one or more aspects of the instructor’s teaching or the session’s content, we are particularly interested in learning how we can do better in the future:

Tuesday, December 9, 2014

Home Loan Certificates and the NC Foreclosure Prevention Fund Troy Hershberger, Public Outreach Coordinator, NC Housing Finance Agency

Strongly Strongly Please rate your instructor’s teaching: Disagree Neither Agree The instructor presented the material clearly. SD D N A SA The instructor was knowledgeable and well‐prepared. SD D N A SA The instructor’s pace was appropriate. SD D N A SA Overall, the session was skillfully done. SD D N A SA

Strongly Strongly Please rate the session content: Disagree Neither Agree The session content is important for my professional development. SD D N A SA

Was the content appropriate for your level of knowledge? Too difficult About right Too easy

Please share any additional comments about the instructor’s teaching and the session’s content. If you indicated that you were dissatisfied with one or more aspects of the instructor’s teaching or the session’s content, we are particularly interested in learning how we can do better in the future:

5

The Role of a Lawyer When Serving as a Substitute Trustee Alice Mine, Legal Counsel, North Carolina State Bar

Strongly Strongly Please rate your instructor’s teaching: Disagree Neither Agree The instructor presented the material clearly. SD D N A SA The instructor was knowledgeable and well‐prepared. SD D N A SA The instructor’s pace was appropriate. SD D N A SA Overall, the session was skillfully done. SD D N A SA

Strongly Strongly Please rate the session content: Disagree Neither Agree The session content is important for my professional development. SD D N A SA

Was the content appropriate for your level of knowledge? Too difficult About right Too easy

Please share any additional comments about the instructor’s teaching and the session’s content. If you indicated that you were dissatisfied with one or more aspects of the instructor’s teaching or the session’s content, we are particularly interested in learning how we can do better in the future:

Panel Discussion: Conducting a Foreclosure Hearing Nicole Brinkley, Asst. Clerk, Wake, Fred Benson, Asst. Clerk, Mecklenburg, Johanna Finkelstein, Asst. Clerk, Buncombe, Teri Lawson, Asst. Clerk, Guilford, Meredith Smith, Moderator, School of Government

Strongly Strongly Please rate your instructor’s teaching: Disagree Neither Agree The instructor presented the material clearly. SD D N A SA The instructor was knowledgeable and well‐prepared. SD D N A SA The instructor’s pace was appropriate. SD D N A SA Overall, the session was skillfully done. SD D N A SA

Strongly Strongly Please rate the session content: Disagree Neither Agree The session content is important for my professional development. SD D N A SA

Was the content appropriate for your level of knowledge? Too difficult About right Too easy

Please share any additional comments about the instructor’s teaching and the session’s content. If you indicated that you were dissatisfied with one or more aspects of the instructor’s teaching or the session’s content, we are particularly interested in learning how we can do better in the future:

6

The Application of Rules of Civil Procedure to Foreclosure Hearings Ann Anderson, Assistant Professor, School of Government

Strongly Strongly Please rate your instructor’s teaching: Disagree Neither Agree The instructor presented the material clearly. SD D N A SA The instructor was knowledgeable and well‐prepared. SD D N A SA The instructor’s pace was appropriate. SD D N A SA Overall, the session was skillfully done. SD D N A SA

Strongly Strongly Please rate the session content: Disagree Neither Agree The session content is important for my professional development. SD D N A SA

Was the content appropriate for your level of knowledge? Too difficult About right Too easy

Please share any additional comments about the instructor’s teaching and the session’s content. If you indicated that you were dissatisfied with one or more aspects of the instructor’s teaching or the session’s content, we are particularly interested in learning how we can do better in the future:

Box Lunches + Mock Hearing Meredith Smith, Assistant Professor, School of Government

Strongly Strongly Please rate your instructor’s teaching: Disagree Neither Agree The instructor presented the material clearly. SD D N A SA The instructor was knowledgeable and well‐prepared. SD D N A SA The instructor’s pace was appropriate. SD D N A SA Overall, the session was skillfully done. SD D N A SA

Strongly Strongly Please rate the session content: Disagree Neither Agree The session content is important for my professional development. SD D N A SA

Was the content appropriate for your level of knowledge? Too difficult About right Too easy

Please share any additional comments about the instructor’s teaching and the session’s content. If you indicated that you were dissatisfied with one or more aspects of the instructor’s teaching or the session’s content, we are particularly interested in learning how we can do better in the future:

7

COURSE EVALUATION Course Content Please rate the usefulness and length of each session:

Usefulness Session Length

Keep Session

OmitSession

Too Short Just Right Too Long

Clerk's Role & the Players in a Foreclosure

Discussion of Mortgage Servicers & their Role in Foreclosure

Lender Loss Mitigation & the Consumer Financial Protection Bureau Regulations

Holder of a Valid Debt Default, Notice, Power of Sale, Home Loans & Military Service

A View from the Bench: Selected Evidentiary Issues in Foreclosure Hearings

Home Loan Certificates & the NC Foreclosure Prevention Fund

The Role of a Lawyer When Serving as a Substitute Trustee

Panel Discussion: Conducting a Foreclosure Hearing

The Application of Rules of Civil Procedure to Foreclosure Hearings

Boxed Lunch & Mock Hearing

Are there any topics that we should add to the course? Strongly Strongly Please rate the course content: Disagree Neither Agree The course (as a whole) will be useful to me. SD D N A SA The course materials will be useful to me. SD D N A SA Please share any additional comments about course content. If you indicated that you were dissatisfied with one or more aspects of course content, we are particularly interested in learning how we can do better in the future: Strongly Strongly Please rate the logistics of the course: Disagree Neither Agree Registering for the course was simple and straightforward. SD D N A SA Before attending the course, I received appropriate and SD D N A SA

timely information about course logistics. The room set‐up was appropriate for this class. SD D N A SA On‐site School of Government staff was informed and helpful. SD D N A SA

8

Please share any additional comments about course logistics. If you indicated that you were dissatisfied with one or more logistical aspects of the course, we are particularly interested in learning how we can do better in the future:

How did you find out about the course? (please check all that apply)

___ Postcard Announcement ___ Email Announcement ___ School of Government Flyer ___ School of Government Website ___ School of Government Listserv Please specify: _______________________

___ Referral from Colleagues ___ Web Search ___ Advertisement ___ School of Government Blog Please specify: _______________________ ___ Other, Please specify: _________________

TAB 1:

The Clerk’s Role & the Players

in a Foreclosure

TAB 2:

Mortgage Servicers & their

Role in a Foreclosure

TAB 3:

Lender Loss Mitigation &

C.F.P.B. Regulations

Borr

ower

not

ice

mus

t:1.Indicate the specific reasons why

NO

OPT

ION

S

Borr

ower

not

ice

mus

t:1.Indicate which options are

offered

2.Give the Borrower 7

+ d

ays

to accep

t or reject offer.

WIT

H O

PTIO

NS

Borr

ower

not

ice

mus

t:1.Indicate which options are

offered

2.Give the Borrower 1

4+

day

s to accep

t or reject offer.

3.State the Borrower has the right

to appeal the determ

ination

within 1

4 d

ays

4.State the req

uirem

ents for an

appeal

WIT

H O

PTIO

NS

Bor

row

er n

otic

e m

ust

:

(i)

State the application is complete

(ii)

Give Borrower 1

4+

day

s to accep

t or reject loss m

itigation offer

(iii)

State the borrower has or will have the right to appeal determination.

(iv)

Instruct Borrower to contact servicers of any other m

ortgage loans

secured by the same property to discuss loss mitigation options.

Day 1

Day 2

Day 3

Day 4

Day 5

LOSS

MIT

IGAT

ION

APP

LICA

TIO

N R

ECEI

VED

90+

DAY

S BE

FORE

SCH

EDU

LED

FO

RECL

OSU

RE S

ALE

LOSS

MITI

GA

TION

PRO

CED

URES

September 2014

1.

Review and determ

ine

if application is

complete

(exc

ludi

ng le

gal p

ublic

hol

iday

s, Sa

turd

ays,

and

Sund

ays.)

2.

Notify Borrower of receipt in writing,

wit

hin

fiv

e d

ays

FOR

INCO

MPL

ETE

APP

LICA

TIO

NS

COM

PLET

EDA

PPLI

CATI

ON

S

If application

becomes complete

90

+ d

ays before

sched

uled

foreclosure sale

date…

follow step 2

for completed

applications.

If application becomes complete 3

8-

89

day

sbefore sched

uled

foreclosure sale date...

30

Day

Mark

Within 3

0 d

ays of

receiving the complete

application:

1.

Evaluate Borrower for all

loss m

itigation options

available

2.

Notify Borrower in

writingof determination.

Borr

ower

not

ice

mus

t:1.Indicate the specific reasons

why

2.State the Borrower has the right

to appeal the determ

ination

within 1

4 d

ays

3.State the req

uirem

ents for an

appeal

NO

OPT

ION

S

Within 3

0 d

ays of

receiving the complete

application:

1.

Evaluate Borrower for all

loss m

itigation options

available

2.

Notify Borrower in

writingof determination.

Bor

row

er n

otic

e m

ust

:

1.

State the application is

incomplete

2.

Provide a list of what is

required

to complete the

application

3.

Give Borrower a reasonable

deadline to submit missing

inform

ation.

4.

Instruct Borrower to contact

servicers of any other

mortgage loans secured by

the same property to discuss

loss m

itigation options.

NO

OPT

ION

SBo

rrow

er n

otic

e m

ust:

1.Indicate the specific reasons why

Borr

ower

not

ice

mus

t:1.Indicate which options are offered

2.Give the Borrower 7

+ d

ays to accep

t or reject offer.

WIT

H O

PTIO

NS

Bor

row

er n

otic

e m

ust

:

(i)

State the application is complete

(ii)

Give Borrower 7

+ d

ays to accep

t or reject loss m

itigation offer

(iii)

Instruct Borrower to contact servicers of any other m

ortgage loans

secured by the same property to discuss loss mitigation options.

Day 1

Day 2

Day 3

Day 4

Day 5

1.

Review and determ

ine

if application is

complete

(exc

ludi

ng le

gal p

ublic

hol

iday

s, Sa

turd

ays,

and

Sund

ays.)

2.

Notify Borrower of receipt in writing,

wit

hin

fiv

e d

ays

FOR

INCO

MPL

ETE

APP

LICA

TIO

NS

COM

PLET

EDA

PPLI

CATI

ON

S

If application becomes complete 3

8-8

9 d

aysbefore sched

uled

foreclosure sale date...

30

Day

Mark

Within 3

0 d

ays of

receiving the complete

application:

1.

Evaluate Borrower for

all loss mitigation

options available

2.

Notify Borrower in

writingof

determination.

Bor

row

er n

otic

e m

ust

:

1.

State the application is

incomplete

2.

Provide a list of what is

required

to complete the

application

3.

Give Borrower a reasonable

deadline to submit missing

inform

ation.

4.

Instruct Borrower to contact

servicers of any other

mortgage loans secured by

the same property to discuss

loss m

itigation options.

LOSS

MIT

IGAT

ION

APP

LICA

TIO

N R

ECEI

VED

45-

89 D

AYS

BEFO

RE S

CHED

ULE

D F

ORE

CLO

SURE

SAL

E

LOSS

MITI

GA

TION

PRO

CED

URES

September 2014

COM

PLET

EDA

PPLI

CATI

ON

S

NO

OPT

ION

S

Borr

ower

not

ice

mus

t:1.Indicate the specific reasons whyBo

rrow

er n

otic

e m

ust:

1.Indicate which options are offered

2.Give the Borrower 7

+ d

ays to accep

t or reject offer.

WIT

H O

PTIO

NS

Within 3

0 d

ays of receiving

the complete

application:

1.Evaluate Borrower for all loss

mitigation options available

2.Notify Borrower in

writingof

determination.

Loss m

itigation application

received

0 t

o 3

7 d

ays before

sched

uled foreclosure sale

You

are

not r

equi

red

to co

mpl

y w

ith a

ny o

f th

e lo

ss m

itiga

tion

requ

irem

ents

und

er 1

2 C.

F.R.

§10

24.4

1 (2

014)

.

LOSS

MIT

IGAT

ION

APP

LICA

TIO

N R

ECEI

VED

38-

44 D

AYS

BEFO

RE S

CHED

ULE

D F

ORE

CLO

SURE

SAL

E

LOSS

MITI

GA

TION

PRO

CED

URES

September 2014

NO

OPT

ION

S

WIT

H O

PTIO

NS

LOSS

MIT

IGAT

ION

APP

EALS

PRO

CESS

If Application becomes complete

90

+ d

ays

before sched

uled foreclosure sale, Borrower has the

right to appeal Servicer’s determination to deny

Borrower’s Loss M

itigation Application for any trial

or permanen

t loan

modification program

.

Borro

wer

mus

t be

perm

itted

to

subm

it an

app

eal w

ithin

14

day

s af

ter r

ecei

ving

the

offe

r not

ice.

With

in 3

0 d

ays

of re

ceiv

ing

Borr

ower

’s ap

peal

: 1.Have personnel (indep

endent of personnel who authorized

initial determ

ination) review

the appeal

2.Notify Borrower of whether a loss m

itigation option is being

offered based

upon appeal.

Borr

ower

not

ice

mus

t:

1.Indicate which options are

offered

2.State Borrower has 1

4+

day

s

to accep

t or reject the offer.

Borr

ower

not

ice

mus

t:

1.State no options are available

2.Provide Borrower specific reasons for den

ial

(optional)

LOSS

MITI

GA

TION

PRO

CED

URES

September 2014

LOSS

MIT

IGAT

ION

PRO

CED

URE

SSeptember 2014

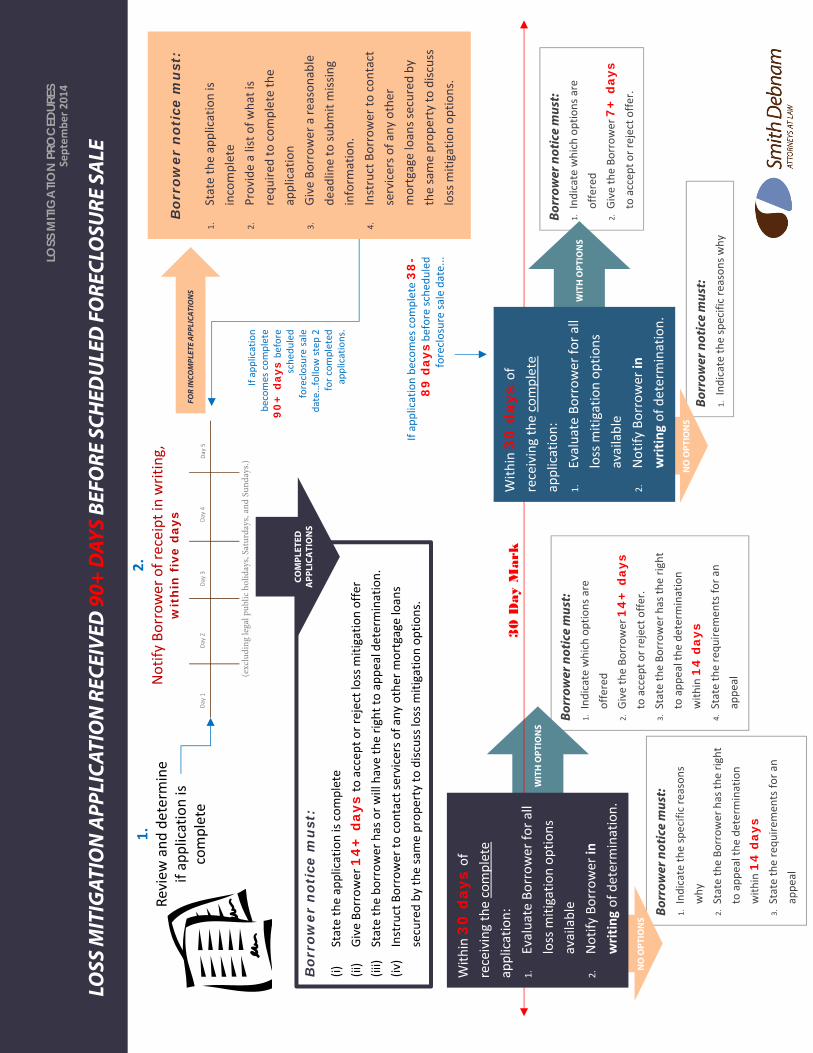

If, after notifying a Borrower of Borrower’s complete application status, a servicer

realizes that additional inform

ation or corrections are necessary to complete the

application, t

he fo

llow

ing

rule

s app

ly:

•The Servicer m

ust promptly request the missing inform

ation and give the Borrower a reasonable

opportunity to complete the application.

•The application is treated

as complete until the Borrower submits the missing inform

ation.

•If a Borrower does not accept an

offer within the deadline established

by the Servicer’s notice, the

Servicer m

ay consider the offer rejected.

•Borrowers are lim

ited

to one appeal.

Serv

icer

s mus

t exe

rcise

reas

onab

le d

iligen

ce in

ob

tain

ing

doc

umen

ts a

nd in

form

atio

n to

com

plet

e a

loss

miti

gatio

n ap

plic

atio

n.

In general, loss mitigation option offers should only be based on complete

applications. T

he fo

llow

ing

are

exce

ptio

ns to

that

rule

:

•If Servicer has exercised

reasonable diligence in obtaining documen

ts and inform

ation to complete

a Borrower’s loss m

itigation application, but the application rem

ains incomplete for a significant

period of time without further progress by the Borrower to m

ake the application complete,

Servicer m

ay evaluate the incomplete application and offer the Borrower any available loss

mitigation options.

•Servicers may offer a short‐term paymen

t forbearance program

to Borrowers based

upon an

evaluation of an

incomplete loss m

itigation application.

IMPORTANT NOTES

Smith Deb

nam

Narron Drake Saintsing & M

yers, LLP

Laur

en V

. Ree

ves

| A

ttorn

eyDirect Line: 919.250.2126

Email: lreeves@

smithdeb

nam

law.com

Sam

uel D

. Fle

der |

Atto

rney

Direct Line: 919.250.2238

Email: sfleder@sm

ithdeb

nam

law.com

Jeff

D. R

oger

s |

Partn

erDirect Line: 919.250.2112

Email: jrogers@sm

ithdeb

nam

law.com

Ba

nkru

ptcy

Fo

recl

osur

e

Litig

atio

n

Col

late

ral R

ecov

ery

Le

nder

Lia

bilit

y D

efen

se

CRE

DITO

RS’ R

IGHT

S PR

AC

TICE

ARE

A

Ba

nkru

ptcy

Fo

recl

osur

e

Col

lect

ions

Lit

iga

tion

C

olla

tera

l Rec

over

y

Lend

er L

iabi

lity

Def

ense

Fo

recl

osur

e

Litig

atio

n

Col

late

ral R

ecov

ery

Le

nder

Lia

bilit

y D

efen

se

Real

Est

ate

Law

We

invi

te y

ou to

con

tact

us i

f you

hav

e an

y qu

estio

ns o

r if y

ou w

ould

like

mor

e in

form

atio

n.

4601

Six

Fork

s Roa

d, S

uite

400

Rale

igh,

NC

276

09

TAB 4:

Holder of a Valid Debt

TAB 5:

Default, Notice, Power of Sale,

Home Loans & Military Service

TAB 6:

Selected Evidentiary Issues in

Foreclosure Hearings

TAB 7:

Home Loan Certificates & NC

Foreclosure Prev. Fund

Mar

y M

. Hol

der

NC

Hou

sing

Fin

ance

Age

ncy

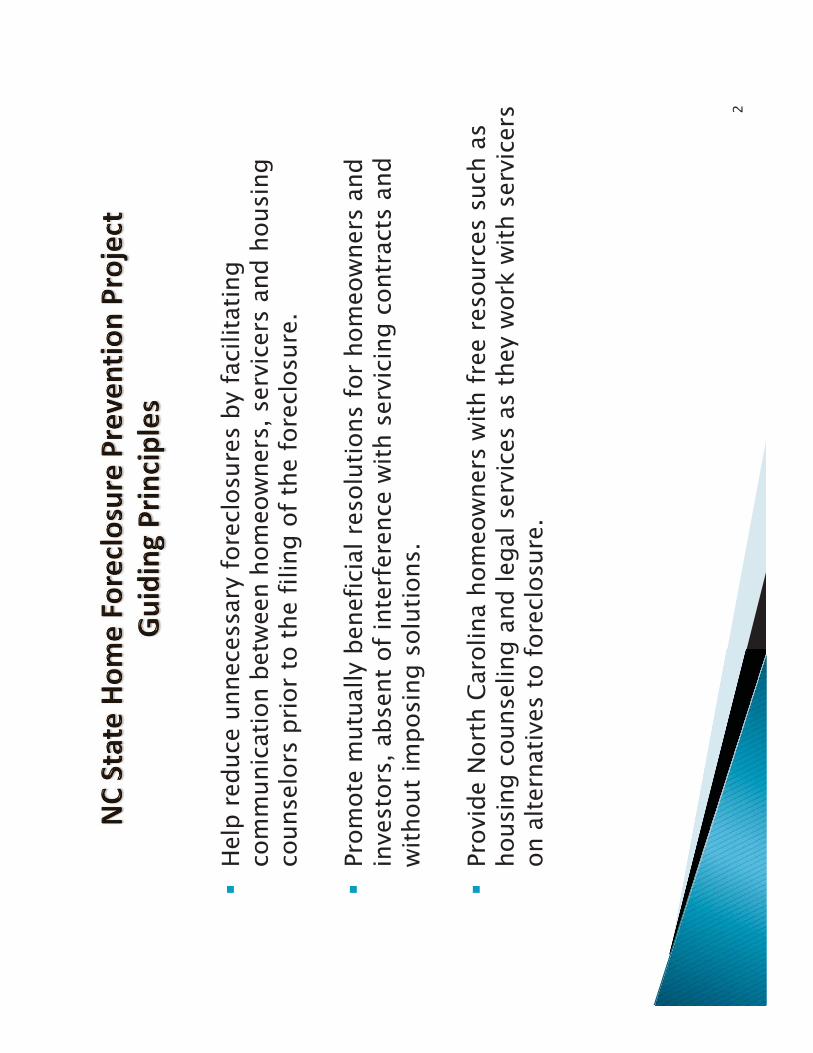

�

Hel

p re

duce

unn

eces

sary

fore

clos

ures

by

faci

litat

ing

com

mun

icat

ion

betw

een

hom

eow

ners

, ser

vice

rs a

nd h

ousi

ng

coun

selo

rs p

rior

to th

e fil

ing

of th

e fo

recl

osur

e.

�Pr

omot

e m

utua

lly b

enef

icia

l res

olut

ions

for

hom

eow

ners

and

in

vest

ors,

abs

ent o

f int

erfe

renc

e w

ith s

ervi

cing

con

trac

ts a

nd

with

out i

mpo

sing

sol

utio

ns.

�

Prov

ide

Nor

th C

arol

ina

hom

eow

ners

with

free

res

ourc

es s

uch

as

hous

ing

coun

selin

g an

d le

gal s

ervi

ces

as th

ey w

ork

with

ser

vice

rs

on a

ltern

ativ

es to

fore

clos

ure.

2

�N

C H

ousi

ng F

inan

ce A

genc

y (N

CHFA

) sen

ds a

“For

eclo

sure

Hel

p O

utre

ach

Lett

er” t

o ho

meo

wne

rs w

ith n

otic

e of

the

avai

labi

lity

of fr

ee

hous

ing

coun

selin

g.

�

Hom

eow

ners

cal

l the

SH

FPP

toll-

free

num

ber

(1-8

88-4

42-8

188)

an

d ar

e co

nnec

ted

to c

ouns

elin

g pa

rtne

rs b

y ca

ll ce

nter

re

pres

enta

tives

.

�N

CHFA

has

par

tner

ship

agr

eem

ents

with

36

HUD

app

rove

d ho

usin

g co

unse

ling

orga

niza

tions

to p

rovi

de a

ssis

tanc

e to

hom

eow

ners

.

�H

omeo

wne

r file

s ar

e as

sign

ed to

cou

nsel

ing

part

ners

usi

ng a

sys

tem

re

ferr

al w

izar

d to

dire

ct c

alls

acc

ordi

ng to

the

prop

erty

loca

tion

and

agen

cy c

apac

ity.

3

12

2008

13

,004

2009

65

,184

20

10

87,1

81

2011

12

0,97

6 20

12

81,4

84

2013

59

,148

2017

2013

2012

� 46

1,97

2 in

itial

filin

gs th

ru O

ctob

er 2

014

� 67

,585

hom

eow

ner c

ouns

elin

g se

ssio

ns h

ave

been

con

duct

ed

� 12

,788

fore

clos

ures

hav

e be

en p

reve

nted

� 9,

526

stat

utor

y 30

day

ext

ensi

ons

have

bee

n gr

ante

d

NC

Stat

e Ho

me

Fore

clos

ure

Prev

entio

n Pr

ojec

t

Prog

ram

Act

ivity

(In

itial

Sub

-Prim

e &

Hom

e Lo

an F

iling

s)

Thru

10/

14

34,9

95

• Su

b-pr

ime

Loan

s (2

005

thru

200

7)

• 2

Year

Sun

set

(Oct

. 201

0)

• 30

Day

Ext

ensio

n

Allo

wan

ce

SHFP

P es

tabl

ishe

d w

ith fo

cus o

n su

bprim

e lo

ans

(HB

2623

)

SHFP

P ex

pand

ed to

in

clud

e al

l ho

me

loan

s

(SB

1216

)

SHFP

P Ph

ase

I ad

min

istr

atio

n tr

ansf

erre

d fr

om N

CCO

B to

N

CHFA

(H

B 48

4)

SHFP

P Ph

ase

2 re

mai

ning

ad

min

istr

atio

n tr

ansf

erre

d to

N

CHFA

(S

B 82

6)

• Al

l Hom

e Lo

ans

• 2

½ Y

ear S

unse

t (M

ay 2

013)

• 3

0 Da

y E

xten

sion

Allo

wan

ce

• Fili

ng F

ee

( •

NCH

FA-

Coun

selin

g &

Pr

ogra

m S

taff

• N

CCO

B- F

iling

s &

Ext

ensio

n Ap

prov

als

(S(

• NCH

FA- F

iling

s &

Exte

nsio

n Ap

prov

als

• 45

Day

Pre

FC

prog

ram

cont

act

chan

ge to

NCH

FA

•Sun

set D

ate

Rem

oved

2012

20

11

2010

20

08

Proj

ect T

imel

ines

& P

rogr

am C

hang

es

N

C St

ate

Hom

e Fo

recl

osur

e Pr

even

tion

Proj

ect

�Fi

ling

Excl

usio

ns (§

45-

101)

(1b)

(a)

oEq

uity

line

of c

redi

t o

Cons

truc

tion

loan

s o

Reve

rse

mor

tgag

e

oBr

idge

loan

�N

on H

ome

Loan

Det

erm

inat

ion

(§ 4

5-10

1) (1

b) (d

) o

Loan

s th

at e

xcee

d th

e Fa

nnie

Mae

con

firm

ing

loan

siz

e ar

e de

emed

non

hom

e lo

ans

upon

filin

g

�Th

e 45

day

wai

t per

iod

does

not

app

ly

�N

o fil

ing

fee

is b

illed

�

Cond

ition

al c

ertif

icat

e of

com

plia

nce

avai

labl

e up

on fi

ling

(Non

Hom

e Lo

an C

ertif

icat

e)

�

Pre-

Fore

clos

ure

Not

ice

& El

ectr

onic

Fili

ngs

(§ 4

5-10

2 an

d 10

3)

o45

day

not

ice

requ

ired

oEl

ectr

onic

filin

g

oCo

nditi

onal

cer

tific

ate

of c

ompl

ianc

e av

aila

ble

45 a

fter

filin

g (e

arlie

st p

ossi

ble

cour

t fil

ing

date

) o

Filin

g fe

e bi

lled

(one

tim

e pe

r hom

e lo

an)

o30

day

ext

ensi

on a

llow

ance

(if g

rant

ed c

ertif

icat

e av

aila

ble

75 d

ays

afte

r fili

ng)

6

�Sy

stem

acc

ess

is g

rant

ed in

the

nam

e of

the

serv

icer

or

indi

vidu

al

note

hol

der

initi

atin

g th

e fo

recl

osur

e pr

ocee

ding

. �

Acce

ss fo

rms

can

be lo

cate

d at

: ht

tps:

//w

ww

.nch

fa.o

rg/S

HFP

POnl

ine/

fcs/

Com

pany

Logi

n.as

px

�Fo

rms

are

retu

rned

to N

CHFA

via

em

ail,

fax

or m

ail.

o

Scan

and

em

ail t

o Pr

eFCF

iling

Acce

ss@

nchf

a.co

m

oFa

x to

(919

) 981

-268

1, A

ttn:

SH

FPP

Acco

unt S

etup

Tea

m

oM

ail t

o SH

FPP

Acco

unt S

etup

Tea

m: P

.O. B

ox 2

8066

, Ral

eigh

, NC

2761

1

7

Serv

icer

Log

in L

ink:

htt

ps:/

/ww

w.n

chfa

.org

/SH

FPPO

nlin

e/fc

s/Co

mpa

nyLo

gin.

aspx

1st

Scr

een:

◦

Prop

erty

Add

ress

Info

rmat

ion:

◦

Addr

ess*

◦

City

* ◦

Stat

e*

◦Zi

p*

Loan

Info

rmat

ion:

◦

Orig

inal

Loa

n Da

te*

◦O

rigin

al P

rinci

pal B

alan

ce *

◦

Loan

Term

s (in

mon

ths)

* ◦

Lien

Sta

tus (

1st o

r 2nd

)*

◦Bo

rrow

er’s

Prin

cipa

l Dw

ellin

g at

Orig

inat

ion*

(yes

or n

o)

Prim

ary

Borr

ower

Info

rmat

ion:

◦

Firs

t Nam

e:*

◦La

st N

ame:

*

◦Bo

rrow

er's

Mai

ling

Addr

ess (

if di

ffere

nt fr

om th

e pr

oper

ty a

ddre

ss)

* Re

quire

d Fi

elds

8

2nd S

cree

n:

This

scre

en o

nly

com

es u

p if

the

filin

g is

dee

med

a H

ome

Loan

◦

Co-B

orro

wer

Info

rmat

ion:

◦

Firs

t Nam

e:

◦La

st N

ame:

◦

Borr

ower

's M

ailin

g Ad

dres

s (if

diffe

rent

from

the

prop

erty

add

ress

) Lo

an C

onfir

mat

ions

: ◦

Date

of 4

5-10

2 Pr

e-fo

recl

osur

e N

otic

e:*

◦Du

e Da

te o

f Las

t Sch

edul

ed P

aym

ent M

ade:

*

�N

otes

:

1)Th

e sy

stem

will

pro

vide

a c

onfir

mat

ion

that

the

filin

g w

as su

cces

sful

ly

subm

itted

incl

udin

g th

e as

signe

d ca

se n

umbe

r.

2)Th

e ho

me

loan

cer

tific

ate

is on

e pa

ge a

nd n

on h

ome

loan

cer

tific

ate

is tw

o pa

ges w

ith th

e se

cond

bei

ng a

n ou

tline

of l

oan

info

rmat

ion

subm

itted

. 3)

The

serv

icer

or d

esig

nate

d at

torn

ey h

as to

log

back

into

the

syst

em to

prin

t the

ce

rtifi

cate

of c

ompl

ianc

e, it

is n

ot m

aile

d by

NCH

FA.

4)Th

e fil

ing

fee

invo

ice

is ge

nera

ted

the

mon

th a

fter t

he su

bmiss

ion

and

mus

t be

pulle

d fr

om th

e sy

stem

, it i

s not

mai

led

by N

CHFA

.

9

�Pr

ogra

m “F

requ

ently

Ask

ed Q

uest

ions

” are

pub

lishe

d on

the

serv

icer

log

in s

cree

n an

d se

nt to

new

use

rs u

pon

acce

ss to

th

e sy

stem

.

�Pr

ogra

m C

onta

cts:

�

Cert

ifica

te q

uest

ions

: ce

rtfic

ates

@nc

hfa.

com

�

Filin

g fe

e In

quiri

es:

filin

gfee

s@nc

hfa.

com

�

Syst

em a

cces

s in

quiri

es: p

refc

filin

gacc

ess@

nchf

a.co

m

�Fi

ling

fee

cred

its: f

iling

feec

redi

ts@

nchf

a.co

m

�Fi

ling

stat

utor

y in

quiri

es: m

mho

lder

@nc

hfa.

com

�

Gen

eral

filin

g su

bmis

sion

inqu

iries

: cat

hyax

tell@

nchf

a.co

m

10

Que

stio

ns

11

Call 1‐888‐623‐8631 or visit our web

site www.foreclosureprevention.gov

for program

details

North Carolina Housing Finance Agency

NC FORECLO

SURE PREV

ENTION FUND

NC Foreclosure Prevention Fund

•18 states including NC received Fed

eral

Hardest Hit Funds in 2010

•NC Housing Finance Agency chosen to

administer Foreclosure Prevention Fund

Program

•40 HUD approved Counseling agen

cies

throughout the state

•Over 17,800 homeo

wners assisted

•Average 400 loans closed m

onthly

NC Foreclosure Prevention Fund

Program

s

•Mortgage Paymen

t Program

(MPP) –

pays monthly m

ortgage and m

ortgage

related expen

ses or reinstates a

mortgage

•Second M

ortgage Refinance Program

(SMRP) –refinances and extinguishes

an unaffordable second m

ortgage

Program

Eligible (Temporary) Financial

Hardship…

NCHFA

uses this term to describe an

event or condition that has caused a tem

porary red

uction in

income. This term can

encompass any of the following circumstances:

•Job loss due to no fault of their own

–Part‐tim

e/Full‐Time Req

uirem

ents

–Under‐employed with a 10% red

uction in

income from previous em

ployer

•Red

uction in

hours or income due to no fault of their own (>60 days)

–Part‐tim

e/Full‐Time Req

uirem

ents

–Em

ployer Furloughs

–Under‐employed with a 10% red

uction in

income from present

•Special H

ardships‐Which cause an employm

ent related hardship

–Illness or injury (temporary)

–Death of a co‐borrower

–Divorce or separation

–Military

MPP Types of Assistance

•Short Term Assistance ‐Job Search

–Up to $36,000 for up to 18 m

onths

•Long Term

Assistance ‐Job Training/Education

–Up to $36,000 for up to 36 m

onths

–Military Service M

embers: Enrolled in

VA‐sponsored program

or utilizing GI B

ill

enrolled in

a Vocational Reh

abilitation Program

or school are eligible for

Automatic 36 M

onths of assistance

•One‐Time Assistance –Reinstatem

ent

–Up to $36,000

–Also available to applicants receiving retirement, disability and social security

who experienced an employm

ent related hardship

0% interest, deferred paymen

ts, forgiven

after 10 years

MPP Population Served

Homeo

wner:

•experienced an employm

ent related financial

hardship on or after January 1, 2008

•able to search for a job, or attend school or

retraining, to secure employm

ent

•need help with m

onthly m

ortgage payment

SMRP Types of Assistance

Extinguish principal balance of second m

ortgage

Up to $30,000

0% interest, D

eferred Payments, N

OT forgiven

after 10 years

***A

lso available to applicants receiving retiremen

t,

disability and social security who experienced an

employm

ent related hardship

SMRP Population Served

Homeo

wner:

•experienced an employm

ent related financial

hardship on or after January 1, 2008

•recovered –full‐time permanent em

ploym

ent

•still need help ‐pay off second m

ortgage loan

Eligibility Criteria

Four Types

1.Basic Req

uirem

ents

2.Basic Exclusions

3.Property Req

uirem

ents

4.Underwriting Req

uirem

ents

Eligibility Criteria

1. B

asic Req

uirem

ents

Be a N.C. H

omeo

wner and a Legal U.S. Resident

Occupy home as primary residen

ce

Through

no fault of own experienced a program

eligible financial hardship on or after January 1,

2008

Military: Must be honorably discharged from

Active Duty (DD214 form

)

A homeowner must:

Eligibility Criteria

2. B

asic Exclusions

Been convicted

of a

mortgage related

felony

in last 10 years

Unpaid principal balances

on m

ortgages greater

than

$300,000

Seller financed m

ortgage

Curren

t pen

ding litigation

on primary residen

ce

mortgage

A homeowner who wishes to apply for MPP assistance m

ust

NOT HAVE:

Eligibility Criteria

3. Property Req

uirem

ents

The primary residen

cehome must be:

Located in North Carolina

Only one property in

addition to primary residen

ce

allowed

A single‐family home

Condominium/townhome (attached

or detached

)Manufactured or mobile home on foundation

permanen

tly affixed to real estate owned

by

homeo

wner

Duplex where owner occupies one unit as their

residen

ce

Eligibility Criteria

4. U

nderwriting Req

uirem

ents

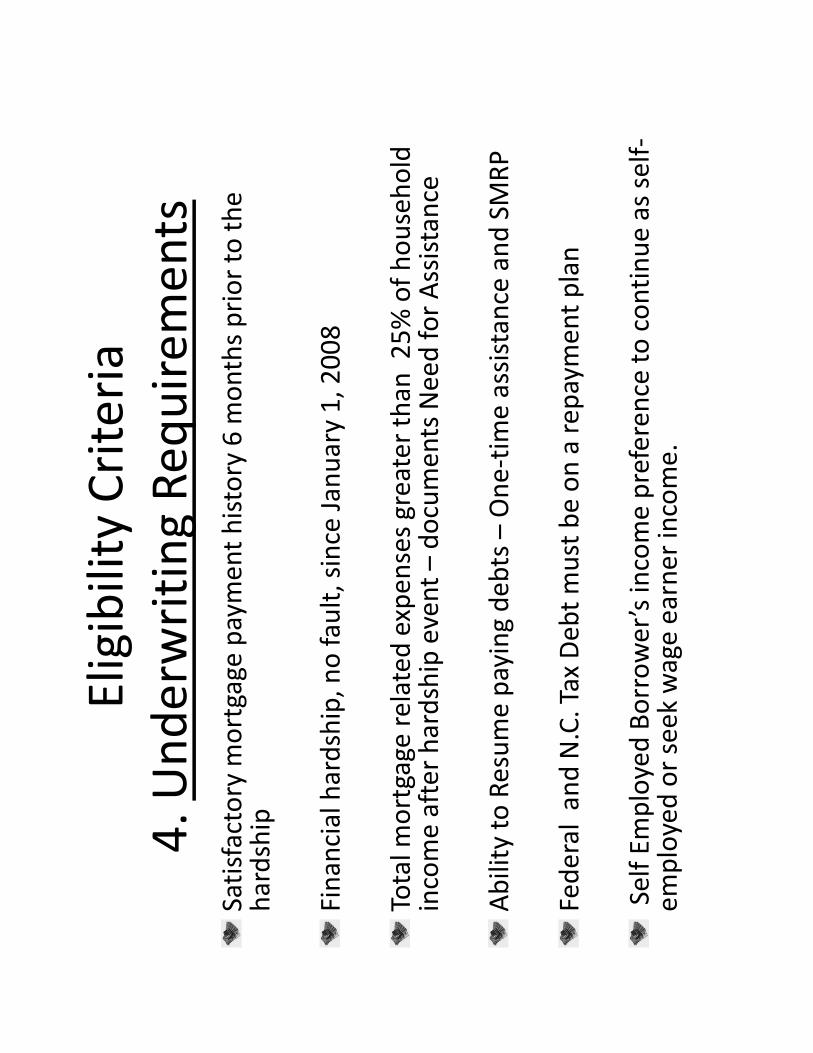

Satisfactory m

ortgage paymen

t history 6 m

onths prior to the

hardship

Financial hardship, no fault, since January 1, 2008

Total m

ortgage related

expen

ses greater than

25% of household

income after hardship event –documen

ts Need for Assistance

Ability to Resume paying deb

ts –One‐time assistance and SMRP

Federal and N.C. Tax Deb

t must be on a rep

aymen

t plan

Self Employed Borrower’s income preference to continue as self‐

employed or seek wage earner income.

Important Facts

Homeo

wner does not have to be delinquent on

mortgage, or in foreclosure to participate.

However, cannot be within 15 days of foreclosure sale.

A stay of foreclosure is provided

to stop a foreclosure for

120 days during NCFPF loan

process if

homeo

wner is 90 days or more delinquent.

Will not stop servicer contact.

Borrower should continue to pay m

ortgage payments.

•The NCFPF provides m

oney directlyto the

servicer (or tax collector, or insurance agency,

or homeo

wner’s association) on beh

alf of the

homeo

wner (borrower)

MPP and SMRP Assistance

Provided

as a Loan

NCHFA

transfers $$

Servicers and

other payees

receive $$

To Apply On line or Locate Counseling Agency

Http://w

ww.Ncforeclosureprevention.Gov

Contact Housing Counselor or

Borrower Direct

Freq

uently Asked

Questions

•Will you check my cred

it?

•How long does it take to get approved?

•What if I am

more than

6 m

onths beh

ind on my

mortgage?

•Is this program

only available in

my city?

•I w

as in the program

before, and still have not found a

job. May I reapply?

•I w

as den

ied previously due to an incomplete

application. May I reapply?

•How long will this program

be around?

•If I find a job, w

ill you cut my assistance?

•What if I am

approved for short‐term assistance, but

decide to go back to school? Can

I apply again?

NC Foreclosure Prevention Fund

Troy Hershberger

Outreach Specialist

tdhershberger@

nchfa.com

919.981.2647 (office)

TAB 8:

Role of Lawyer as a Substitute

Trustee

TAB 9:

Conducting a Foreclosure

Hearing

TAB 10:

Rules of Civil Procedure to

Foreclosure Hearings

TAB 11:

Mock Hearing