forecasting foreign exchange volatility for …398471/fulltext01.pdf · forecasting foreign...

TRANSCRIPT

1

UPPSALA UNIVERSITY Jan 31, 2010 Department of Statistics Uppsala

Bachelor’s Thesis Fall Term 2010 Advisor: Lars Forsberg

F O R E C A S T I N G F O R E I GN E X CHA N G E VO L A T I L I T Y F O R

V A L U E A T R I S K

CAN REALIZED VOLATILITY OUTPERFORM GARCH PREDICTIONS?

David Fallman1 & Jens Wirf2

ABSTRACT

In this paper we use model-free estimates of daily exchange rate volatilities employing high-frequency intraday data, known as Realized Volatility, which is then forecasted with ARMA-models and used to produce one-day-ahead Value-at-Risk predictions. The forecasting accuracy of the method is contrasted against the more widely used ARCH-models based on daily squared returns. Our results indicate that the ARCH-models tend to underestimate the Value-at-Risk in foreign exchange markets compared to models using Realized Volatility.

KEYWORDS: Realized volatility, volatility forecasting, exchange rates, high-frequency data, value-at-risk.

2

CONTENT

1. Introduction ................................................................................................................................. 3

2. Volatility Models ........................................................................................................................ 4

2.1 ARCH ......................................................................................................................................... 4

2.2 Realized Volatility ............................................................................................................... 5

2.3 ARMA ........................................................................................................................................ 6

2.4 Value-at-Risk ......................................................................................................................... 7

3. Data .................................................................................................................................................. 8

3.1 Data Construction ............................................................................................................... 8

3.2 Data Description .................................................................................................................. 9

4. Results ......................................................................................................................................... 13

4.1 In-Sample Fit ...................................................................................................................... 13

4.2 Out-of-Sample Forecast Evaluation .......................................................................... 15

4.3 Value-at-Risk: Practical Application ......................................................................... 18

5. Conclusion ................................................................................................................................. 20

6. References ................................................................................................................................. 22

Appendix .......................................................................................................................................... 23

3

1. INTRODUCTION

It is widely acknowledged in academic literature that financial asset prices are

difficult, if not impossible, to predict, much due to their seemingly random

nature. However, ever since Engle’s seminal contribution of the Autoregressive

Conditional Heteroskedasticity framework in 1982, much progress has been

made in modeling the dynamics of the conditional volatility. This modeling has

spurred significant interest among academics and financial market

practitioners alike as volatility is a core measure of the risk associated with

holding a financial asset. Accurately predicting volatility is instrumental to

making informed risk management decisions and bears implications for

numerous areas in financial economics.

Although unobserved and inherently time-varying, financial asset volatility is

well documented to display serial dependence [volatility clustering], which

means it has predictable features. The prevailing methodology for modeling and

forecasting asset volatility stems from Engle’s (1982) ARCH framework and the

plethora of variants that have since followed. Notably the Generalized ARCH

(GARCH) by Bollerslev (1986) has become standard practice in many financial

institutions.

A more recent and competing approach to modeling volatility is Realized

Volatility, popularized by among others Talyor & Xu (1992) and Andersen,

Bollerslev, Diebold & Labys (1999). Following the increasing availability of

high-frequency data, RV has become an increasingly popular method. It is a

model-free methodology which harnesses the information contained in higher

frequency data, i.e. intraday data such as five or ten minute returns. It has the

advantage that it can be modeled with parsimonious standard time series

models rather than the arguably more complex ARCH-family of models.

In this paper, we consider the practical task of forecasting one-day-ahead

foreign exchange volatility and compare the predictive ability of a number of

GARCH and RV based models. The objective is to determine whether RV can

outperform standard practice in forecasting procedures and so assess whether

there is real merit to using computer intensive high-frequency data. To this aim

we analyze four major exchange spot rates, namely the Euro versus the U.S.

Dollar, Japanese Yen, Great British Pound and Swedish Krona over the period

Jan 2009 to Oct 2010. As a practical application of volatility forecasting we also

4

consider the task of calculating one-day-ahead Value-at-Risk for a hypothetical

FX portfolio.

The remainder of this paper is organized as follows; in Section 2 the theoretical

underpinnings of the models are explored conceptually, In Section 3 the data is

described in detail together with a discussion of how the raw data has been

treated. In Section 4, we document the results of the study, followed by a

conclusion in Section 5.

2. VOLATILITY MODELS

Modeling financial market volatility is essential for trading and risk

management, however since volatility is a random variable that is unobserved,

it must be modeled and there are different approaches to doing that. In this

section, we explore the theoretical properties of two such approaches, the

ARCH-framework and Realized Volatility. Finally, we also describe how Value-

at-Risk is calculated.

2.1 ARCH

Engle’s (1982) Autoregressive Conditional Heteroscedasticity (ARCH) model was

not directly meant for the financial markets but it was soon realized that it had

potential in the field. The ARCH models calculate variance with the assumption

of heteroscedasticity in the residuals unlike most other models which require

homoscedasticity to produce unbiased estimators. The ARCH model was

groundbreaking and has proved so useful that Engle received the Economic

Sciences Price in memory of Alfred Nobel in 2003. The ARCH models use the

fact that volatility clustering leads to autocorrelation which can be modeled by

including past values as weights for the forecast estimate. It thereby assumes

that the conditional variance is dependent on the variance from previous days.

The weights are most commonly calculated through maximum likelihood

estimation that will give the most accurate estimates for the given sample. But

since volatility is not a directly observed variable, the ARCH models use squared

past returns as its input and since daily returns does not contain information

about the volatility within the day, there is a limit to how accurate estimates the

model can produce. However, it outperformed the rolling standard deviation

5

model which was the regularly used method before Engle discovered the ARCH

application for financial data.

The Generalized Autoregressive Conditional Heteroscedasticity (GARCH) model

introduced by Bollerslev (1986) is by far the most used application of the ARCH

model. Formally denoted as GARCH(p,q) where q are the ARCH-term which

refers to how many autoregressive lags the model are using and the p refers to

the GARCH-term i.e. the number moving average lags that the model will

include.

The conditional variance ( can be modeled using previous day’s variance and

return ( as follows with a GARCH(1,1) process

. (1)

The unconditional variance can be found by rearranging the model to

(2)

with the restriction that .The GARCH model with its long memory

through declining weights that never reach zero has proven so successful that it

has replaced the ARCH as the standard practice model.

The exponential GARCH model is further extensions by Nelson (1991) which

avoids the non-negative restrictions on the weights of the GARCH by modeling

instead of . In addition the volatility can react asymmetrically. EGARCH is

a logarithmic variation of the GARCH model where

∑

∑

(3)

where is defined as | | | | which allows to have

asymmetric effect on the volatility, where

if

2.2 REALIZED VOLATILITY

As previously mentioned, the most common method is to use statistical models

from the ARCH family, but there exists also an alternative model-free approach

which is called Realized Volatility.

Summing up high frequency squared realizations will result in a good estimate

for the variance of a random i.i.d variable (Merton, 1980). Realized volatility is

6

an extension of this where squared intraday returns is used to construct a time

series of the variance. Realized volatility is defined as

[∑ ]

(4)

This can also be written as

[∑

] { [ ]

[ ] (5)

where ri,t is the returns for each observation which is calculated as

( ) ( ) . (6)

If the assumptions above are fulfilled and if the returns are distributed with

fixed and even intervals each day will make RV(t) an consistent and unbiased

estimator of the daily variance (Andersen et al. 2000a), A higher frequency of

returns would normally be ideal but can introduce unwanted effect due micro

market effects such as bid-ask bounces etc. To determine the appropriate

frequency can be tricky as where a too high frequency will introduce bias and

while a too low frequency loses much of the information you normally would

want to model. When determining this, the stocks and currency’s volume of

trading should be taken in consideration as a higher trading volume results in

that a higher interval frequency can be chosen.

2.3 ARMA

Since RV is a consistent measure of volatility we can treat it as “observed”. As

such, it can be modeled and forecasted using standard time series techniques.

The Autoregressive Moving Average (ARMA) model, which we have opted to

use, is applied to stationary and autocorrelated time series data. The model

contains two parts, the autoregressive (AR) part and the moving average (MA).

Part. Both parts can be modeled by themselves to describe time series of data.

The AR(p) model is defined as:

∑ (7)

Where is a observed time series and are the parameters which have

restrictions for the model to be stationary, for example of | | , in the case

7

of an AR(1). Each observation is made of a random error shock that is a linear

combination of prior observations. The MA(q) model is defined as

∑ (8)

where are the MA parameters and is a constant. Each observation here is

made up of a random error shock that is a linear combination of prior random

shocks. ARMA(p,q) refers to the merger of the two models and has the same

assumptions and conditions. The ARMA process is modeled as

∑ ∑

(9)

2.4 VALUE-AT-RISK

Value-at-Risk is an intuitive and easily understood measure of risk. Take for

example, a 5% VaR on a portfolio of assets. Value-of-risk states the least amount

of money the portfolio is expected to lose in the worst 5% of the trading days.

Risk management has gone through a revolution since the introduction of

Value-at-Risk (VaR) in the early 1990s. VaR is now used to control, manage and

measure market risk. The most common use of VaR is to calculate 1% or 5%

probabilities for a given portfolio of assets. VaR can be calculated in a few

different ways depending on if it uses daily volatility or average volatility. One

way of defining VAR is

(10)

where loss is denoted L and c is the confidence level. We will mainly be focusing

on the one day ahead VaR for this essay and for that specification to be valid do

we need to identify the quantile’s distribution and estimate the volatility for

.

The one day ahead VaR is defined as

size. (11)

The VaR adjusted for given time horizon is defined as

√ ⁄ (12)

The financial asset return distributions quantile is an important part of Value-

at-Risk model. A big problem today is that the Gaussian distribution is often

8

used even though daily returns often tend to be more leptokurtic relative to the

Gaussian distribution. This will inevitably lead to inaccurate risk management.

One approach to mitigating the problem is standardizing the returns with the

conditional standard deviation estimate derived from Realized Volatility or

from another model such as GARCH. Returns can theoretically be decomposed

as:

(13)

Assuming that returns are uncorrelated with the conditional variance and that

. However since is not a directly observable variable we have to

use to the next best thing, our Realized Volatility estimate. Standardizing the

returns can be done by simple rearranging the former decomposition to:

(14)

This should in theory result in a Gaussian distribution but due to noise in the ,

the tails may sometimes be fatter. Student-t is normally the distribution that is

used to handle a fat-tailed distribution, but if you have a large number of

observations, this will reduce the noise in which allows the Normal

distribution to be used anyway.

3. DATA

In this section we document how the raw data has been manipulated and the

series of interest constructed. Last in this section, some key data is plotted in

graphs.

3.1 DATA CONSTRUCTION

As previous mentioned, the empirical analysis is focused around four FOREX

spot rate series, namely the Euro versus the Swedish Krona, Great British

Pound, U.S. Dollar and the Japanese Yen. The data3 spans over the period

3 The data provider is Forex Rate at forexrate.co.uk.

9

January 1st 2009 through October 29th 2010, which is a total of 476 active

trading days. We have opted for two sampling frequencies, daily and ten minute

evenly spaced intervals. This means there is one low and one high frequency

sampling for use in comparing the modeling frameworks.

Regarding the high-frequency sampling intervals, there is an inherent tradeoff

between choosing ultra-high frequencies such as tick or second data and semi-

high frequencies such as 20, 30, 60 minutes data. The problem is essentially that

ultra-high frequencies has microstructure bid/ask frictions which distorts the

data, and while lower frequencies avoids this problem, more and more

information is lost with the longer sampling intervals. In this paper, we rely on a

10 min interval, as previously mentioned, which seems a reasonable tradeoff.

The raw data are global 24-hour trading day quotes. To achieve continuity in

the sampling and avoid irregularities in the number of observations per day

around weekends, we follow Bollerslev (2002) and let a five-day trading week

span from Sunday to Friday, where each trading day runs from 21:00 GMT to

21:00 GMT the next day. This gives around 68’300 observations in the higher

frequency series. To then transform the spot rates into returns we calculate the

first difference of the logarithm of the close-to-close prices.4

3.2 DATA DESCRIPTION

Graph 3.1 depicts the raw price series of the different exchange rates. At a first

glance, it seems that three of the series lack a clear trend, whereas the SEK has

an downward trend in the sample period. Notably, there is a fair bit of

fluctuation in all four series over the 15 months we have sampled.

4 The dataset can be obtained by sending a request to [email protected].

10

GRAPH 3.1 – PLOT OF PRICE DATA

The volatility of the exchange rate series becomes more observable when we

look at the constructed RV series in Graph 3.2, recalling that this operation

visualizes volatility. The four series have a similar pattern in the first half of

2009 where they all seem to display a decreasing volatility level. From the mid

of 2009 through the mid 2010 there is relatively stable period with a lower

level of activity. For three of the series, the GBP, JPY and USD, this is followed by

a major spike in volatility in the summer of 2010. The SEK only shows a slight

tendency of this event, in an otherwise exceptionally low volatility period.

.80

.84

.88

.92

.96

I II III IV I II III IV

2009 2010

EUR / GBP

100

110

120

130

140

I II III IV I II III IV

2009 2010

EUR / JPY

9.0

9.5

10.0

10.5

11.0

11.5

12.0

I II III IV I II III IV

2009 2010

EUR / SEK

1.1

1.2

1.3

1.4

1.5

1.6

I II III IV I II III IV

2009 2010

EUR / USD

11

GRAPH 3.2 – PLOT OF REALIZED VOLATILITY

Regarding the forecastability of the series, a key component is arguably the

autocorrelation pattern. Graph 3.3 plots a correlogram of a hundred lags. Across

all the series, there appears to be a lot of serial dependence. Generally it seems

to start at around 0.6, yet decaying in somewhat dissimilar fashions. The USD,

JPY and GBP appear to decay exponentially, whereas then SEK decays almost

linearly.

.00000

.00002

.00004

.00006

.00008

I II III IV I II III IV

2009 2010

EUR / GBP

.00000

.00004

.00008

.00012

.00016

.00020

.00024

.00028

I II III IV I II III IV

2009 2010

EUR / JPY

.00000

.00005

.00010

.00015

.00020

I II III IV I II III IV

2009 2010

EUR / SEK

.00000

.00005

.00010

.00015

.00020

.00025

.00030

I II III IV I II III IV

2009 2010

EUR / USD

12

GRAPH 3.3 REALIZED VOLATILITY CORRELOGRAM

The distributional characteristics of returns standardized by the square root of

RV, which is important for the calculation of VaR is plotted in Graph 3.4. In

Table 3.1 the moments are also tabulated.

GRAPH 3.4 – DISTRIBUTION OF STANDARDIZED RETURNS

.0

.2

.4

.6

.8

10 20 30 40 50 60 70 80 90 100

EUR / USD

.0

.2

.4

.6

.8

10 20 30 40 50 60 70 80 90 100

EUR / JPY

.0

.2

.4

.6

.8

10 20 30 40 50 60 70 80 90 100

EUR / SEK

.0

.2

.4

.6

.8

10 20 30 40 50 60 70 80 90 100

EUR / GBP

0

10

20

30

40

50

60

-3 -2 -1 0 1 2 3

Fre

quency

EUR / GBP

0

10

20

30

40

50

60

-5 -4 -3 -2 -1 0 1 2 3

Fre

quency

EUR / JPY

0

20

40

60

80

100

-3 -2 -1 0 1 2 3

Fre

quency

EUR / SEK

0

10

20

30

40

50

-1.6 -1.2 -0.8 -0.4 0.0 0.4 0.8 1.2

Fre

quency

EUR / USD

13

TABLE 3.1 – DISTRIBUTION OF STANDARDIZED RETURNS

Returns standardized by √ as estimate of σ

EUR/BGP EUR/SEK EUR/USD EUR/JPY

Mean -0.03606 -0.05715 -0.00315 -0.01624

Skewness -0.00377 -0.04603 -0.05969 -0.33878

Kurtosis 2.45123 3.18318 2.64013 3.34074

Jarque-Bera 5.97387 0.83368 2.85117 11.4085

Probability

0.05044 0.65912 0.24036 0.00333

4. RESULTS

In the first part of the empirical results we focus on the in-sample model

estimation, specifically the model parameters and how well the models fit the

data in question. In the second part, we turn to the actual forecasting of

volatility and compare the models predictive abilities.

4.1 IN-SAMPLE FIT

As a first step in our analysis we examine the RV data set for each of the four

exchange rate series. The idea is to fit a number of standard parametric time

series models to this data, in order capture the serial dependence described in

the data section. To this aim, we employ number of ARMA-type models, namely

one autoregressive, one moving average and one mixed model. These models

are also applied to the logarithm and square root of RV. Since we use a rolling

one-year in-sample window for forecasting, explained in detail in the section,

there are a total of 216 forecasts per series. This of course involves 216

regression estimation results per series and per model, totaling around 7’700

estimations for the RV dataset alone. Naturally, the results of this quantity of

estimations are difficult to portray in any comprehensible way. Which is why

we have only summarized some schematic aspects of the estimations, seen in

Table 4.1. The statistics reported show the range of coefficients as well as the

stability of the parameters. Furthermore we consider the fit of the models by

looking at both the adjusted R-Squared and the Breusch-Godfrey Portmanteau

test for residual autocorrelation. Whether or not there is any serial dependence

left in the residual is of course a key indicator of whether the model has

successfully captured the information contained the series.

14

What is seen in Table 4.1 is that all the AR-models generally leave a lot of

residual autocorrelation as is indicated by the Breusch-Godfrey test. This also

applies to the MA-models which seem to leave serial dependence almost all the

time. The most successful models are the ARMA models which have the highest

R-squared values and least residual autocorrelation. The most successful

transformation alternates between the logarithm and square root. It however

also seems that the coefficients in the ARMA models vary a lot more than the

single models as the window rolls.

TABLE 4.1 - IN-SAMPLE RV ESTIMATION DIAGNOSTICS

√ AR MA ARMA AR MA ARMA AR MA ARMA

EUR/SEK

Coef * 0.53 0.40 0.97 -0.81 0.78 0.59 0.98 -0.66 0.69 0.51 0.98 -0.75

(StDev) 0.21 0.18 0.11 0.21 0.12 0.12 0.02 0.18 0.13 0.14 0.01 0.17

Adj-R2 ** 0.32 0.21 0.47 0.62 0.40 0.70 0.50 0.32 0.62

B-G ***

1.00 1.00 0.32 1.00 1.00 0.14 1.00 1.00 0.26

EUR/GBP Coef * 0.47 0.33 0.56 -0.26 0.46 0.34 0.93 -0.74 0.49 0.37 0.82 -0.54 (StDev) 0.12 0.19 0.31 0.39 0.10 0.06 0.04 0.11 0.11 0.07 0.13 0.28

Adj-R2 ** 0.24 0.16 0.27 0.22 0.15 0.30 0.25 0.18 0.31

B-G ***

0.37 1.00 0.17 0.93 0.99 0.00 0.41 1.00 0.00

EUR/JPY Coef * 0.52 0.41 0.76 -0.32 0.70 0.54 0.86 -0.34 0.65 0.51 0.80 -0.26 (StDev) 0.20 0.16 0.16 0.48 0.05 0.05 0.03 0.08 0.11 0.11 0.07 0.27

Adj-R2 ** 0.31 0.23 0.34 0.49 0.34 0.51 0.43 0.31 0.46

B-G ***

0.69 1.00 0.01 0.80 1.00 0.03 0.44 1.00 0.10

EUR/USD

Coef * 0.65 0.51 0.84 -0.39 0.60 0.42 0.91 -0.59 0.65 0.48 0.88 -0.49 (StDev) 0.07 0.07 0.11 0.33 0.06 0.04 0.05 0.14 0.06 0.05 0.07 0.22

Adj-R2 ** 0.43 0.29 0.49 0.37 0.23 0.43 0.42 0.28 0.48

B-G ***

0.96 1.00 0.65 1.00 1.00 0.29 0.98 1.00 0.55

*Statistic reported: Mean, Standard Devivation of coefficients. **Mean adjusted R-squared. ***Percentage of cases where a null hypothesis of ‘no residual autocorrelation’ is rejected at 5% significance, lag length=5. Bold font indicates highest R-Squared and Italic font is the lowest B-G result.

The second set of models is the ARCH-type models. Note here that these models

use the daily return data and not the higher frequency RV data. We have opted

to fit three different ARCH-model specifications, namely the ARCH(1), the

GARCH(1,1) as well as the EGARCH(1,1). As with the previous set of data we

evaluate to what extent these models are able to capture the information

contained within the in-sample period. Again, the shear amount estimation

outputs associated with the models means we need summarize the results. We

15

present selected aspects the models coefficient stability and fit. Results are

found in Table 4.2. The diagnostics indicate, if anything, that the EGARCH model

leaves the least residual autocorrelation. The models otherwise appear very

similar.

TABLE 4.2 - IN-SAMPLE GARCH ESTIMATION DIAGNOSTICS

ARCH GARCH EGARCH

EUR/SEK Coefficients* 5.7E-06 4.2E-07 0.0813 -1.8083 0.1326

Std Error* 2.4E-06 7.7E-07 0.0719 2.7703 0.1140

ARCH LM** 0.4354 0.7033 0.6810

EUR/GBP

Coefficients* 6.7E-06 5.4E-07 0.0186 -13.688 -0.0218

Std Error* 4.1E-07 6.6E-07 0.0311 10.283 0.0955

ARCH LM** 0.3666 0.6737 0.6792

EUR/JPY

Coefficients* 1.5E-05 3.1E-06 0.0400 -7.3843 -0.0122

Std Error* 1.6E-06 5.9E-06 0.0505 2.6496 0.0424

ARCH LM** 0.8845 0.7208 0.8545

EUR/USD

Coefficients* 8.5E-06 1.5E-07 0.0172 -5.8725 0.0274

Std Error* 9.6E-07 1.3E-07 0.0353 5.9908 0.0531

ARCH LM** 0.4394 0.5836 0.6526

**Probability of the F-value’s mean for a LM-test with 5 lags. Bold font indicates highest L-M result.

4.2 OUT-OF-SAMPLE FORECAST EVALUATION

The performance of volatility forecasts are crucial to many finance applications,

including VaR discussed in this paper, which is why the overall objective is to

evaluate which models predict volatility with the highest accuracy over a

certain horizon.

We test the predictive accuracy of our various models by producing one-day-

ahead static forecasts from a rolling window of one year, or 260 active trading

days, which means the out-of-sample period starts January 2nd 2010. That is,

an entire year of observations is used to produce a forecast of the day

immediately ahead. The in-sample of one year is then rolled forward one day, in

order to forecast the next day and yet so son. There are therefore a total of 216

predictions per series and model to be compared and statistically evaluated.

16

The idea is to compare the models both within respective classes i.e. ARCH-

types and the RV based, as well as contrast them against each other.

In comparing the forecasts we use three standard forecast error measurements,

namely MAE, MAPE and RMSE5. Note that, to calculate the forecast error, we

contrast the forecast with actual RV, as is customary. This also applies to the

ARCH-models. These loss functions are widely used and seem a good base for

discussion of performance. Although, assessing the quality of out-of-sample

forecasts is not entirely straightforward since numerical indications such these

may be misleading. It may be the case, if there for example are extreme outliers

in the series that some models get a disproportionate large mean error which

fails to describe forecasting performance in the absence of extreme outliers.

What this means is that these measures should only be interpreted in company

with the forecast graph.

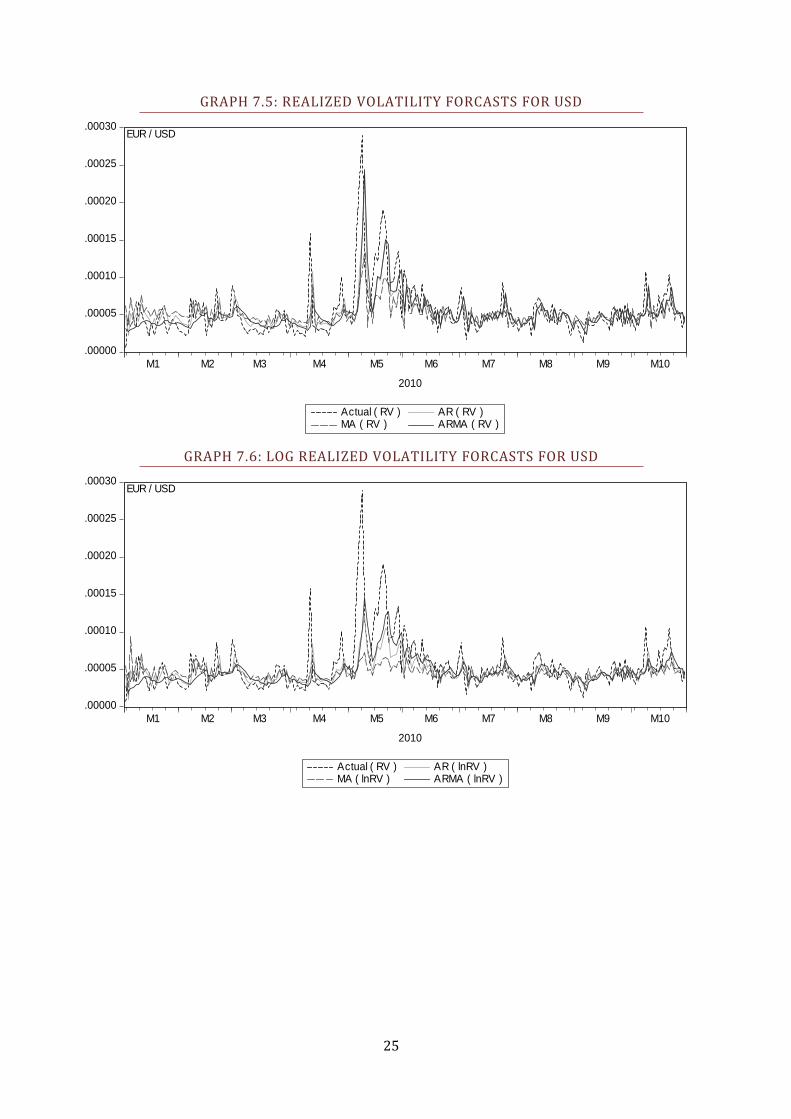

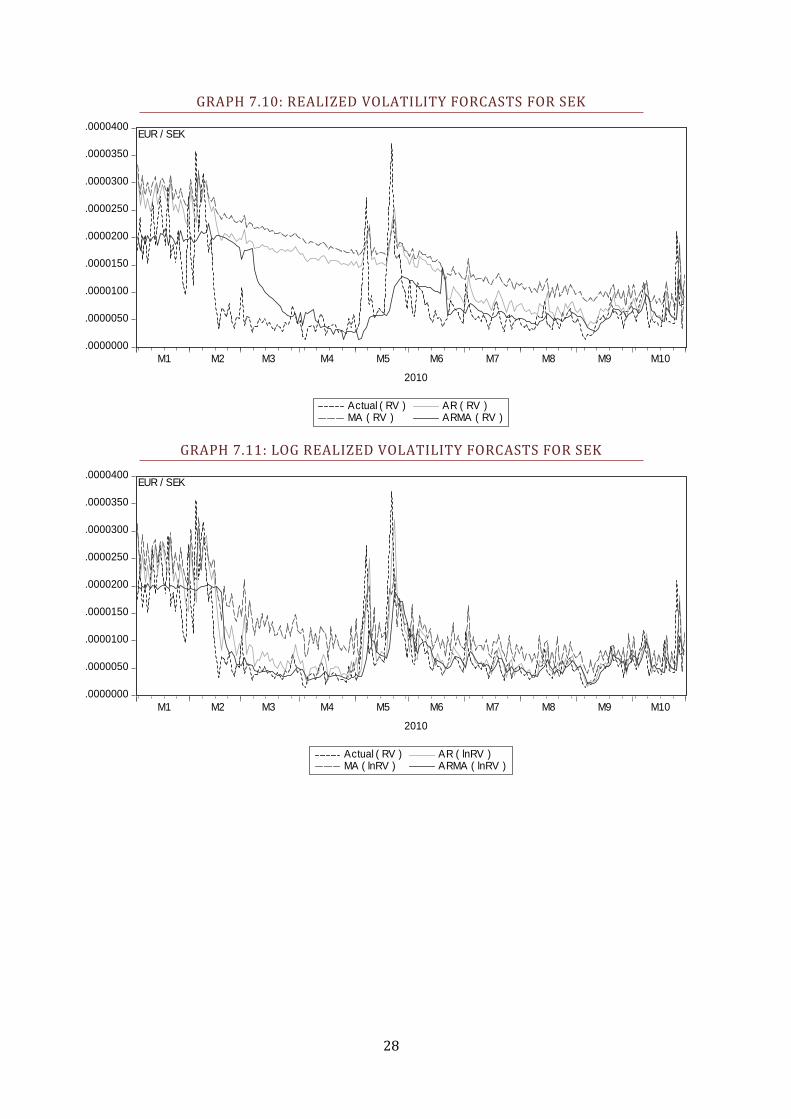

First, we look at how the total of nine RV models performs in the one-day-ahead

forecasts, results seen in Table 4.3. Notably, it seems one particular model, the

ARMA based on the logarithm of RV, quite consistently give the superior

forecasts. The ARMA on the square root of RV also performs admirably.

TABLE 4.3 - RV FORECAST EVALUATION

√ AR MA ARMA AR MA ARMA AR MA ARMA

EUR/SEK

MAE 7.0E-06 9.3E-06 3.8E-06 3.1E-06 5.3E-06 2.6E-06 4.2E-06 7.0E-06 2.3E-06

MAPE 1.4203 1.8938 0.6154 0.4548 0.9917 0.3459 0.7205 1.3832 0.4105

RMSE 8.6E-06 1.0E-05 6.0E-06 4.7E-06 6.6E-06 4.5E-06 5.6E-06 8.2E-06 4.9E-06

** *

EUR/JPY

MAE 8.7E-06 9.8E-06 8.4E-06 8.3E-06 9.7E-06 8.2E-06 8.2E-06 9.3E-06 8.1E-06

MAPE 0.4737 0.5594 0.4108 0.3742 0.4297 0.3532 0.3961 0.4648 0.3749

RMSE 2.0E-05 2.2E-05 2.1E-05 2.1E-05 2.4E-05 2.1E-05 2.0E-05 2.3E-05 2.0E-05

* * *

EUR/GBP

MAE 2.5E-06 2.9E-06 2.4E-06 2.5E-06 2.7E-06 2.3E-06 2.5E-06 2.7E-06 2.4E-06

MAPE 0.3616 0.4285 0.3359 0.3168 0.3518 0.2866 0.3338 0.3784 0.3031

RMSE 5.2E-06 5.9E-06 5.3E-06 5.5E-06 5.7E-06 5.5E-06 5.3E-06 5.6E-06 5.3E-06

* **

EUR/USD

MAE 1.8E-05 2.0E-05 1.8E-05 1.8E-05 2.0E-05 1.7E-05 1.8E-05 1.9E-05 1.8E-05

MAPE 0.3751 0.4267 0.3515 0.3371 0.3756 0.3169 0.3542 0.3944 0.3320

RMSE 2.7E-05 3.0E-05 2.8E-05 2.9E-05 3.4E-05 2.9E-05 2.8E-05 3.2E-05 2.8E-05

* **

MAE: Mean Absolute Error, MAPE: Mean Absolute Percentage Error, RMSE: Root Mean Squared Error Bold font indicates lowest error. Note that the logged and square rooted series are anti-logged and squared respectively prior to evaluation.

5 Mean Absolute Error, Mean Absolute Percentage Error and Root Mean Squared Error

17

Next, we have a look at the corresponding results for the ARCH-type models,

Table 4.4. It is clear to see that the GARCH specification most often give the top

forecasts, although the ARCH model is not far behind.

TABLE 4.4 – GARCH FORECAST EVALUATION

ARCH GARCH EGARCH NAIVE

EUR/SEK MAE 3.9E-06 4.5E-06 4.7E-06 1.1E-07

MAPE 0.4844 0.4053 0.4446 0.3506

RMSE 6.2E-06 7.9E-06 8.0E-06 4.9E-06

** *

EUR/JPY

MAE 1.1E-05 1.0E-05 1.2E-05 -3.2E-08

MAPE 0.5383 0.4470 0.5050 0.4210

RMSE 2.5E-05 2.6E-05 2.5E-05 2.0E-05

* **

EUR/GBP

MAE 2.9E-06 2.5E-06 3.3E-06 -3.3E-10

MAPE 0.3648 0.2751 0.3954 0.3788

RMSE 6.2E-06 5.9E-06 6.4E-06 5.7E-06

***

EUR/USD

MAE 4.5E-05 4.5E-05 4.6E-05 -2.2E-08

MAPE 0.7913 0.7954 0.8118 0.3837

RMSE 5.7E-05 5.6E-05 5.7E-05 2.9E-05

* ** MAE: Mean Absolute Error, MAPE: Mean Absolute Percentage Error, RMSE: Root Mean Squared Error. Bold font indicates lowest error.

We now turn our attention to comparing the alternative forecasting

frameworks. Recall that the GARCH(1,1) is widely used as the standard for

many financial practitioners and it is hence the benchmark against which the

competing models should measure up. In Table 4.5 we have documented the

improvement in forecasting errors for a selection of the top models against the

GARCH(1,1).

TABLE 4.5 – MODEL COMPARSION AGAINST GARCH

ARCH EGARCH AR-RV LOG-ARMA SQ-ARMA

EUR/SEK 13% -4% -55% 42% 49%

EUR/JPY -10% -20% 13% 18% 19%

EUR/GBP -16% -32% 0% 8% 4%

EUR/USD 0% -2% 60% 62% 60%

Statistics reported: Percentage improvement in RMSE (i.e. lower forecast error) over the benchmark GARCH(1,1) result. Bold font indicates highest improvement for respective series.

18

4.3 VALUE-AT-RISK: PRACTICAL APPLICATION

We now turn to the practical application of the results attained in the paper.

Take, for instance, a portfolio with 100’000 Euro invested in each of the four

currencies. The following information is necessary to calculate the desirable

VaR:

Portfolio size, which in this case is 100’000 Euro for each currency.

Volatility forecast for given day (e.g. √ from a Log-ARMA(1,1)

which we recognized as the ideal model (see Table 4.3) for one day

ahead forecasts).

Confidence level which in this case is 99% since we will be calculating

the standard VaR (1%).

Time period of trading (we will be using one day ahead).

The distribution for each exchange rate series (see Table 3.1).

As seen in Table 3.1 all currencies pass as normally distributed except the

Japanese Yen series. Since the Yen series was not normal we proceeded with a

robustness check in the form of a Monte Carlo simulation6. However, it is

noteworthy that only the left tail of the distribution matters in VaR calculations.

Therefore, it is only necessary for the Monte Carlo values on that particular side

that need to correspond to the Gaussian distribution if you want use it. The

conclusion from the simulation is that the critical value taken from the Monte

Carlo simulation is only marginally different to the Gaussian’s 1 percent

quantile (2.33).When comparing VaR(1%) calculated with the Gaussian

distribution, the student-t distribution and with the results of a Monte Carlo

simulation we get what is seen in Graph 4.1.

6 Monte Carlo simulation is a method which calculates distributions with information from the sample. As this did not change our results we will not dwell on it, but the interested reader is referred to Jackel, P. (2002), Monte Carlo – Methods in finance, John Wiley & Sons, 1st edition, Somerset, NJ, USA.

19

GRAPH 4.1 – VAR DISTRIBUTION SIMUALTION COMPARISON

We can now calculate one day ahead VAR (1%) for each series with a rolling in-

sample with one trading years observation with volatility forecasts taken from

the log-ARMA(1,1) model.

GRAPH 4.2 – 1% VAR WITH 100’000 EURO PORTFOLIO

400

800

1,200

1,600

2,000

2,400

2,800

M1 M2 M3 M4 M5 M6 M7 M8 M9 M10

2010

Monte Carlo

Gaussian distribution

T distribution with 10 d.f

EUR / JPY

1% VAR with 100 00 Euro portfolio with different distribution assumtions:

1,000

1,500

2,000

2,500

3,000

3,500

M1 M2 M3 M4 M5 M6 M7 M8 M9 M10

2010

EUR / USD

400

600

800

1,000

1,200

1,400

M1 M2 M3 M4 M5 M6 M7 M8 M9 M10

2010

EUR / SEK

400

800

1,200

1,600

2,000

2,400

M1 M2 M3 M4 M5 M6 M7 M8 M9 M10

2010

EUR / JPY

500

600

700

800

900

1,000

1,100

M1 M2 M3 M4 M5 M6 M7 M8 M9 M10

2010

EUR / BGP

1% VAR with 100 000 EUR portfolio

20

This is only the probability for each series in an absolute value for each day,

remember that it is only 1% for this to actually happen a given day. As seen in

the graph (note the axis scale) above is it much safer to invest in British Pound

compared to U.S Dollar as when the actual 1-percent-day come so will the losses

for USD probably exceed GBP.

TABLE 4.6 – LOG-ARMA/GARCH VAR COMPARISON

The Log-ARMA model produces much higher and precise volatility estimates

which as seen in Table 4.6 leads to much higher VaR-values. The GARCH model

is heavily underestimates the risk which is particularly worrying since forecast

models have tendencies to predict lower values that the actual observation. So

the GARCH model will have an even higher differential against the actual VaR-

value compared to when it is matched against the Log-ARMA.

5. CONCLUSION

The objective of this paper was to document whether forecasting models based

on realized volatility could outperform those of the more widely used ARCH-

family, in the case of exchange rate series. Furthermore, we set out to analyze

the implications of the different modeling strategies in a practical application,

namely Value-at-Risk calculations.

The results of the study indicate that the RV based models consistently produce

superior forecasts to those of the ARCH-models and offer a forecasting accuracy

improvement of up to 50 percent. This seems to confirm the notion that there

may be valuable information contained within intraday price data when

forecasting short horizons. Therefore, practitioners interested in forecasting FX

rate volatility ought to regard using RV as a highly pertinent alternative to

ARCH. As for the practicality of either modeling framework, the high-frequency

data is admittedly more complicated to attain and handle. However, the

EUR/SEK +23%

EUR/JPY +3%

EUR/GBP +4%

EUR/USD +56%

Average VaR difference in percent between LOG-ARMA and GARCH with 1% VaR calculated with 100’000 Euro as portfolio. A positive number indicates that Log-ARMA has a larger VaR-value.

21

convenience of using standard time series ARMA methodology should not be

overlooked. It is of course also possible that the potential gains in forecasting

precision afforded by the RV methodology alone can outweigh the cost and

inconvenience of using intraday data.

As for the Value-at-Risk, we found that the RV models generally predicated

higher volatilities and thus estimated greater values at risk. That is, the results

indicate that the frequently used ARCH models tend to seriously underestimate

the risk associated with holding a given portfolio of assets. If so, our results

bears the implication that risk managers may justifiably need to upgrade their

VaR numbers, in order to accurately portray their real risk.

On a final note, it is worth noting that the ARMA models we used to model the

RV, were the most simplistic available. For completeness and potential further

gains in predictive accuracy, higher orders and more flexible models ought to be

evaluated. In a further study, it would be interesting to see if the residual serial

dependence of the ARMA models could be regularly reduced to near zero.

22

6. REFERENCES

Articles:

Andersen, T.G. & Bollerslev, T. & Diebold F.X. & Labys, P. (2001), ”The

Distribution of Realized Exchange Rate Volatility”, Journal of the American

Statistical Association, No. 96, pp. 42-55.

Andersen, T.G. & Bollerslev, T. & Diebold F.X. & Labys, P. (2000), ”Exchange rate

returns standardized by Realized Volatility are (nearly) Gaussian”,

Multinational Finance Journal, No. 4, pp. 159-179.

Andersen, T.G. & Bollerslev, T. & Diebold F.X. & Labys, P. (2002), ”Modeling and

forecasting Realized Volatility”, Econometrica, No. 71, pp. 529-626.

Frinjs, B. & Margaritis, D. (2008), “Forecasting daily volatility with intraday

data”, The European Journal of Finance, Vol. 14, No. 6, pp. 523-540.

Gardner, Jr. E.S. (2006), “Exponential smoothing: The state of Art – Part ll”,

International Journal of Forecasting, vol. 22, issue 4, pp. 637-666.

Teräsvirta, T. (2006), “An Introduction to Univariate GARCH models”, SSE/EFI

Working Papers in Economics and Finance, No. 646.

Books:

Alexander, C. (2008), Practical Financial Econometrics, 1st ed., John Wiley &

Sons Inc, Hoboken, USA.

Jäckel, P. (2002), Monte Carlo – Methods in finance, 1st ed., John Wiley & Sons

Inc, Hoboken, USA.

Philippe, J. (2007), Value At Risk: The New Benchmark for Managing Financial

Risk, 3rd ed., The McGraw-Hill Companies Inc, NY, USA.

23

APPENDIX

GRAPH 7.1: OUT-OF-SAMPLE ARCH MODELS FORECAST FOR GBP

GRAPH 7.2: OUT-OF-SAMPLE ARCH MODELS FORECAST FOR JPY

.00000

.00001

.00002

.00003

.00004

.00005

.00006

.00007

.00008

25 50 75 100 125 150 175 200

Actual ( RV ) ARCH GARCHEGARCH NAIVE

EUR / BGP

.00000

.00004

.00008

.00012

.00016

.00020

.00024

.00028

M1 M2 M3 M4 M5 M6 M7 M8 M9 M10

2010

Actual ( RV ) ARCH GARCHEGARCH NAIVE

EUR / JPY

24

GRAPH 7.3: OUT-OF-SAMPLE ARCH MODELS FORECAST FOR USD

GRAPH 7.4: OUT-OF-SAMPLE ARCH MODELS FORECAST FOR SEK

.00000

.00005

.00010

.00015

.00020

.00025

.00030

25 50 75 100 125 150 175 200

Actual ( RV ) ARCH GARCHEGARCH NAIVE

EUR / USD

.00000

.00001

.00002

.00003

.00004

.00005

.00006

.00007

.00008

25 50 75 100 125 150 175 200

Actual ( RV ) ARCH GARCHEGARCH NAIVE

EUR / SEK

25

GRAPH 7.5: REALIZED VOLATILITY FORCASTS FOR USD

GRAPH 7.6: LOG REALIZED VOLATILITY FORCASTS FOR USD

.00000

.00005

.00010

.00015

.00020

.00025

.00030

M1 M2 M3 M4 M5 M6 M7 M8 M9 M10

2010

Actual ( RV ) AR ( RV )MA ( RV ) ARMA ( RV )

EUR / USD

.00000

.00005

.00010

.00015

.00020

.00025

.00030

M1 M2 M3 M4 M5 M6 M7 M8 M9 M10

2010

Actual ( RV ) AR ( lnRV )MA ( lnRV ) ARMA ( lnRV )

EUR / USD

26

GRAPH 7.6: SQUARE ROOT REALIZED VOLATILITY FORCASTS FOR USD

GRAPH 7.7: REALIZED VOLATILITY FORCASTS FOR GBP

.00000

.00005

.00010

.00015

.00020

.00025

.00030

M1 M2 M3 M4 M5 M6 M7 M8 M9 M10

2010

Actual ( RV ) AR ( sqrt RV )MA ( sqrt RV ) ARMA ( sqrt RV )

EUR / USD

.00000

.00001

.00002

.00003

.00004

.00005

.00006

.00007

.00008

M1 M2 M3 M4 M5 M6 M7 M8 M9 M10

2010

Actual ( RV ) AR ( RV )MA ( RV) ARMA ( RV )

EUR / BGP

27

GRAPH 7.8: LOG REALIZED VOLATILITY FORCASTS FOR GBP

GRAPH 7.9: SQUARE ROOT REALIZED VOLATILITY FORCASTS FOR GBP

.00000

.00001

.00002

.00003

.00004

.00005

.00006

.00007

.00008

M1 M2 M3 M4 M5 M6 M7 M8 M9 M10

2010

Actual ( RV ) AR ( lnRV )MA ( lnRV ) ARMA ( lnRV )

EUR / BGP

.00000

.00001

.00002

.00003

.00004

.00005

.00006

.00007

.00008

M1 M2 M3 M4 M5 M6 M7 M8 M9 M10

2010

Actual ( RV ) AR ( sqrt RV )MA ( sqrt RV ) ARMA ( sqrt RV )

EUR / BGP

28

GRAPH 7.10: REALIZED VOLATILITY FORCASTS FOR SEK

GRAPH 7.11: LOG REALIZED VOLATILITY FORCASTS FOR SEK

.0000000

.0000050

.0000100

.0000150

.0000200

.0000250

.0000300

.0000350

.0000400

M1 M2 M3 M4 M5 M6 M7 M8 M9 M10

2010

Actual ( RV ) AR ( RV )MA ( RV ) ARMA ( RV )

EUR / SEK

.0000000

.0000050

.0000100

.0000150

.0000200

.0000250

.0000300

.0000350

.0000400

M1 M2 M3 M4 M5 M6 M7 M8 M9 M10

2010

Actual ( RV ) AR ( lnRV )MA ( lnRV ) ARMA ( lnRV )

EUR / SEK

29

GRAPH 7.12: SQUARE ROOT REALIZED VOLATILITY FORCASTS FOR SEK

GRAPH 7.13: REALIZED VOLATILITY FORCASTS FOR JPY

.0000000

.0000050

.0000100

.0000150

.0000200

.0000250

.0000300

.0000350

.0000400

M1 M2 M3 M4 M5 M6 M7 M8 M9 M10

2010

Actual ( RV ) AR ( sqrt RV )MA ( sqrt RV ) ARMA ( sqrt RV )

EUR / SEK

.00000

.00004

.00008

.00012

.00016

.00020

.00024

.00028

M1 M2 M3 M4 M5 M6 M7 M8 M9 M10

2010

Actual ( RV ) AR ( RV )MA ( RV ) ARMA ( RV )

EUR / JPY

30

GRAPH 7.14: LOG REALIZED VOLATILITY FORCASTS FOR JPY

GRAPH 7.15: SQUARE ROOT REALIZED VOLATILITY FORCASTS FOR JPY

.00000

.00004

.00008

.00012

.00016

.00020

.00024

.00028

M1 M2 M3 M4 M5 M6 M7 M8 M9 M10

2010

Actual ( RV ) AR ( lnRV )MA ( lnRV ) ARMA ( lnRV )

EUR / JPY

.00000

.00004

.00008

.00012

.00016

.00020

.00024

.00028

M1 M2 M3 M4 M5 M6 M7 M8 M9 M10

2010

Actual ( RV ) AR ( sqrt RV )MA ( sqrt RV ) ARMA ( sqrt RV )

EUR / JPY