forecasting and budgeting - curtis blakely & co., pc · forecasting and budgeting presented by:...

TRANSCRIPT

FORECASTING AND BUDGETING

Presented By:Darrell Spence, CPA/ABVCurtis Blakely & Co., P.C.

P.O. Box 5486Longview, TX 75608

(903) [email protected]

2

Forecasting and Budgeting

Everybody knows what a budget is, of course: It’s a way of figuring out how much you are going to spend on essentials and incidentals.It’s a lot easier to put together a budget if you have some basic financial information to work with.For your company, this kind of basic financial information resides in its financial statements.

3

Forecasting and Budgeting

These financial statements – income statements, balance sheets, statements of cash flows – are fairly straightforward, because they’re based on how your company performed last year or the year before. Unfortunately, historical information is not always adequate when preparing a budget.

4

Forecasting and Budgeting

In order to effectively create a budget, a company must first create a financial forecast from which the budget can be prepared.

5

Financial Forecasts

Profound words about the future and about whether we should try to predict it have often been spoken.Our expectations, no matter how far off the mark they are, encourage us to set objectives, to move forward, and to achieve our goals somewhere down the road.

6

Financial Forecasts

You can think about the future of your company in much the same way. Assumptions about your own industry and marketplace – that you’ll have no new competitors, that a new technology will catch on, or that customers will remain loyal –provide a framework to plan around.Forecasts assist a company in capturing these assumptions.

7

Uses of Forecasts - Budgeting

Forecasts provide a moving picture of your financial situation tomorrow, next month, next year, and even three to five years out.Your financial picture is likely to be much clearer in the near term, of course, and much cloudier the farther out you try to look.Fortunately, you can use the best of your forecasts to make near-term decisions about where, when, and how much money to spend on your company in the near future. This is the budgeting process.

8

Uses of Forecasts –Long Range Planning

A forecast will assist in determining the long term viability of a company.A forecast assists in evaluating capital expenditures. Will they pay for themselves? Can the company service the new debt relative to capital expenditures? Should capital expenditures be financed with debt or internally generated funds?

9

Uses of Forecasts –Long Range Planning

A forecast assists in planning dividend/capital credit payments. Will the company have cash flow available to pay these?A forecast assists in monitoring earnings. Will the company meet the financial performance required by lenders? Will the company meet regulatory requirements?

10

Uses of Forecasts– New Business

Forecasts are needed to prove the feasibility of potential new businesses.A forecast can be used to obtain financing for new businesses.Forecasts help to determine cash needs in the start-up phase of a new business.

11

Uses of Forecasts - Valuations

Forecasts are used for valuations in potential sales of businesses.Forecasts are needed for valuation of potential acquisitions.Forecasts are used for valuations in estate planning.

12

Constructing Financial Forecasts–Identifying Key Assumptions

You want to be clear about what your business assumptions are and where they come from, because your assumptions are as important the numbers themselves when it comes to making a financial prediction.Several key assumptions are revenue sources, inflation rate, capital borrowing and repayment, subscriber/customer growth, and capital expenditures.

13

Constructing Financial Forecasts–Establishing a Base Year

For existing businesses, the most common base year used in constructing a financial forecast is the last full fiscal year’s financial statements. However, some forecasts will use the current year annualized for a base year.Whichever is used, adjustments should be made for known and measurable changes such as revenue stream changes, pay raises, new employees hired, changes in benefits provided, additional debt borrowed or repaid.

14

Constructing Financial Forecasts–Establishing a Base Year

Although existing businesses can use their track records and financial histories as starting points for the base year in the forecast, care should be taken. It is all too easy to get a bad case of forecasting laziness where last year’s data is simply grown at an inflationary rate with no adjustments made for nonrecurring items, etc.

15

Constructing Financial Forecasts–Establishing a Base Year

For start-up businesses, the base year is developed from scratch. Revenues are computed based on projected customers times the appropriate per customer revenue amounts and expenses are often driven by customer numbers also. However, general and administrative expenses are often driven by number of employees, and other factors which would apply to G & A costs.

16

Constructing Financial Forecasts –Determine Factors Which Drive Revenue and Expense

For telephone companies, revenues are often based on the number of customers/access lines, unit sales and sales price, rate base and expenses, and minutes of use.

17

Constructing Financial Forecasts –Determine Factors Which Drive Revenue and Expense

For telephone companies, inflation, a plant growth rate and subscriber growth are often used for the following: plant specific expense – inflation and plant growth, plant nonspecific expense – inflation, depreciation – plant balances, customer expense – inflation and subscriber growth, corporate expense –inflation and subscriber growth.

18

Constructing Financial Forecasts –Determine Factors Which Drive Revenue and Expense

The above works well for ILEC’s still operating in a regulated atmosphere. However, CLEC’s and other nonregulated entities might consider using different methods for forecasting.

19

Constructing Financial Forecasts –Determine Factors Which Drive Revenue and Expense

Examples of these includes calculating actual cost of services sold, forecasting known expenditures (consulting, legal, etc.), forecasting salary and benefit requirements as employee headcounts increase, and obtaining departmental forecasts such as sales, network, customer, and administrative.

20

Constructing Financial Forecasts –Capturing Data in Financial Statement Form

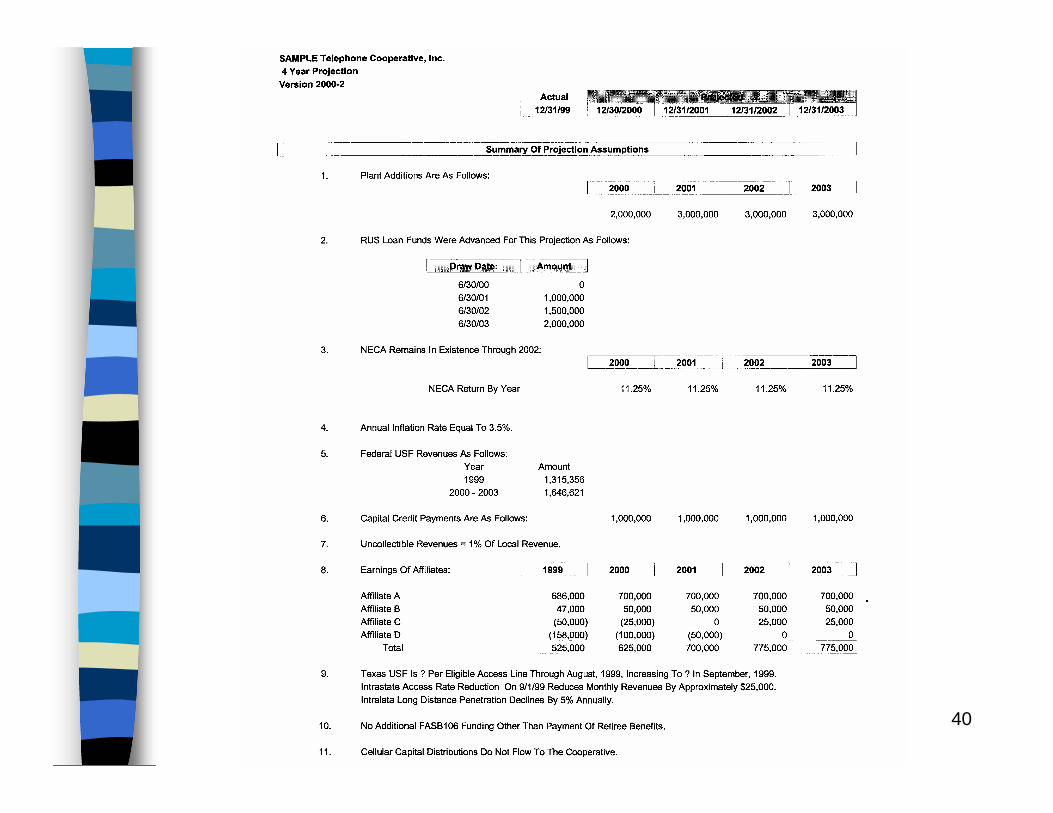

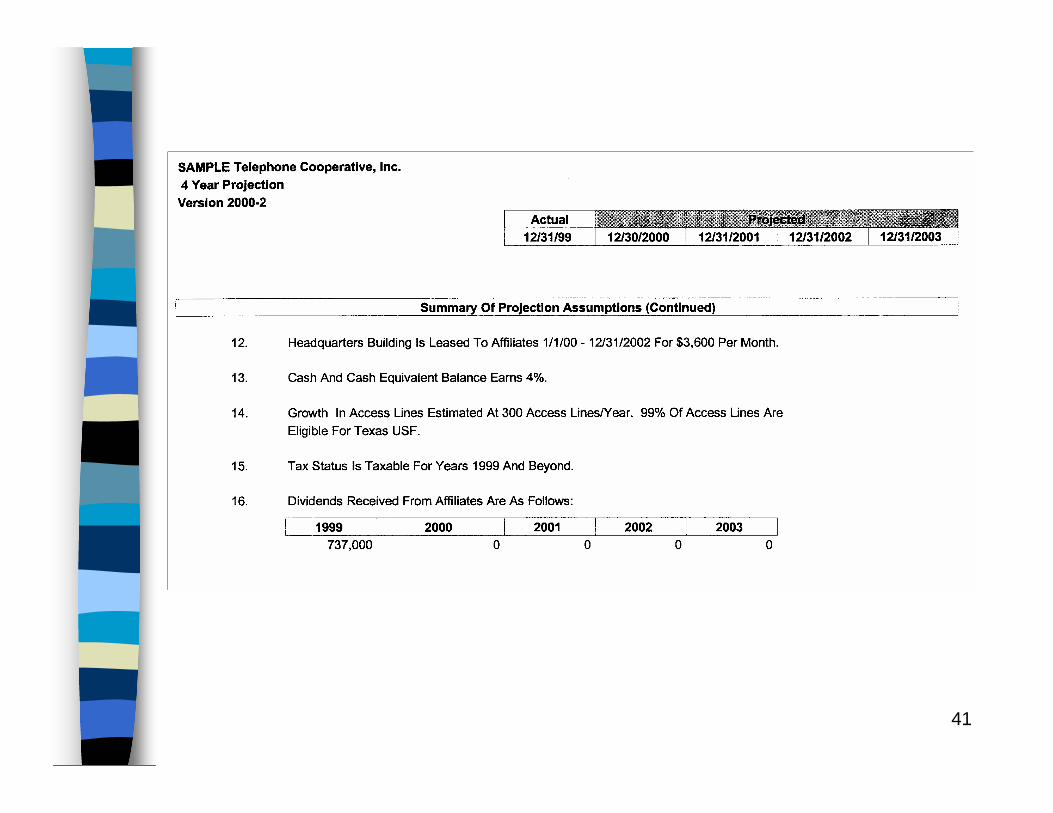

After identifying assumptions, establishing a base year, and determining factors which drive revenues and expenses, forecasted financial statements should be prepared.Most companies get a spreadsheet program involved in the analysis at this point.An example of a forecast prepared using Lotus 123 is attached.

21

Creating a Budget - Overview

Making a budget for your company is one of the most important steps that you’ll take in fulfilling your business plan.Your budget spells out exactly where your company’s resources will come from and where they’re going to go, and helps ensure that you make the right financial decisions.

22

Creating a Budget –Use as a Business Tool

A budget is a business tool that helps you communicate , organize, monitor, and control what’s going on in your business.A budget requires managers to communicate with one another so that they can agree on specific financial objectives, including revenue levels and spending targets.A budget establishes roles and responsibilities for managers, based on how much money they’re in charge of bringing in and how much they’re allowed to spend.

23

Creating a Budget –Use as a Business Tool

A budget creates a standard way of measuring and monitoring management performance by keeping track of how well the revenue targets and spending limits are met.A budget promotes the efficient and effective use of your financial resources by making sure that all your resources point toward a common set of business goals.

24

Creating a Budget –What’s Inside the Budget

A rough outline of your company’s budget looks a lot like your forecasted financial statements.Your budget turns your financial forecast into a specific plan. In fact, many companies simply take their forecasted first year numbers and divide by twelve for budgeted monthly numbers. These are then compared to actual numbers and variances are calculated.

25

Creating a Budget –What’s Inside the Budget

Other companies will use their forecast as a guide in calculating more detailed actual budgeted amounts. These are then compared to actual and variances are calculated.

26

Creating a Budget –What’s Inside the Budget

Small companies might have one master budget, while larger companies might have operating, administrative, financial, capital, and development budgets. For these companies, a master budget is prepared by combining all of the individual budgets mentioned.

27

Types of Budgeting Approaches – Top-down Budgeting

Top-down budgeting is done by the top people – owners or senior managers – and works best in small companies.Whoever is preparing the forecast should meet with the company’s decision-makers to take time to discuss general expectations about the future. The business assumptions that go into the forecast and the key predictions and estimates are discussed here.The forecast should then be prepared.

28

Types of Budgeting Approaches – Top-down Budgeting

Meet again to explore the results of the forecast. Consider different sets of business assumptions and weigh their potential effects on the forecast. Continue to meet until the group can agree on a reasonable forecast.Establish revenue and expense targets for your company’s major functional areas based on the forecast.Meet one last time after the budget is in place to review the numbers and get it approved.

29

Types of Budgeting Approaches – Top-down Budgeting

Once approved, the budgeted numbers should be implemented either using your accounting software or a spreadsheet application.

30

Types of Budgeting Approaches –Bottom-up Budgeting Approach

Bottom-up budgeting involves all management levels, which can mean more realistic revenue targets and spending limits. Typically works best in larger companies.The bottom-up approach to creating your budget really is just an expanded version of the top-down process, taking into account the demands of a bigger company and of more people who have something to say.

31

Types of Budgeting Approaches –Bottom-up Budgeting Approach

You still want to begin putting together your budget by meeting with the company’s decision makers.That group should still spend time coming to a general understanding of, and agreement on, your company’s financial forecast, along with the business assumptions and expectations for the future that go with it. But rather than forcing a budget from the top, this approach allows you to build the budget from the bottom.

32

Types of Budgeting Approaches –Bottom-up Budgeting Approach

Managers and supervisors at all levels in the organization should meet and start with a recap of the budget guidelines, but discussions should focus on setting revenue and expense targets. After all, these managers are the ones who actually have to achieve the numbers and stay within the spending limits.

33

Types of Budgeting Approaches –Bottom-up Budgeting Approach

Summarize the results of the budget negotiations. If necessary, get the decision makers together again to discuss revision in the financial objectives, based on the insights, perceptions, and wisdom of the company’s entire management team.Go through the process again, if you have to, so that everyone at every level of the organization is on board (or at least understands the reasoning behind the budget and its numbers).

34

Types of Budgeting Approaches –Bottom-up Budgeting Approach

Approve the budget at the top. Make sure that everybody in the company understands what the budget means, applying the budget not only to financial objectives but also to larger business goals.Once approved, the budgeted numbers should be implemented either using your accounting software or a spreadsheet application.

35

Forecasting and Budgeting -Summary

Unfortunately, the uncertain future that makes your financial forecast and budget necessary in the first place is unpredictable enough to require constant attention.You should monitor your financial situation and revise the parts of your forecast and budget that change when circumstances –and your own financial objectives – shift.

36

Forecasting and Budgeting -Summary

The entire financial forecast should be updated regularly, keeping track of when past predictions were on target or off, and extending your projections another month, quarter, or year.

37

Sample Telephone Cooperative, Inc.

4 Year ProjectionVersion 2000-2

38

39

40

41