for the year ended 31 december 2011 annual report/media/files/f/... · for the year ended 31...

TRANSCRIPT

Falck Renewables S.p.A.Via Alberto Falck 4-16, 20099 Sesto San Giovanni (MI) ITALYph +39.02.24332360www.falckrenewables.eu - [email protected]

AN

NU

AL

REPO

RT F

OR

THE

YEA

R EN

DED

31

DEC

EMBE

R 20

11 ANNUAL REPORT

FOR THE YEAR ENDED 31 DECEMBER 2011

Annual report for the year ended 31 December 2011

2

Letter of the Chairman to the shareholders and stakeholders 4Letter of the Chief Executive Officer to the shareholders and stakeholders 6

1 Notice of annual general meeting 9

2 Company officers 12

3 Group structure 13

4 Consolidated financial highlights 14

5 Directors’ report

5.1 Falck Renewables group operating and financial review5.1.1 Falck Renewables group profile 175.1.2 Regulatory framework 185.1.3 Performance 255.1.4 Non-financial performance indicators 305.1.5 Share price performance 315.1.6 Performance of business sectors 315.1.7 Review of business in 2011 415.1.8 Employees 435.1.9 Environment, health and safety 445.1.10 Research and development activities 455.1.11 Risks and uncertainties 455.1.12 Significant events after the balance sheet date 545.1.13 Management outlook and going concern 545.1.14 Combined results 55

5.2 Operating and financial review of Falck Renewables SpA5.2.1 Financial highlights 605.2.2 Performance and review of business in 2011 605.2.3 Employees 615.2.4 Capital expenditure 615.2.5 Directors, statutory auditors, general managers and their interests 615.2.6 Related party transactions 615.2.7 Direction and coordination activities 635.2.8 Holding of own shares or parent company shares 635.2.9 Purchase and sale of own shares or parent company shares 635.2.10 Share schemes 635.2.11 Corporate governance and code of self-discipline 635.2.12 Legislative decree 231/01 635.2.13 Proposed appropriation of loss for the year 64

3

6 Consolidated financial statements6.1 Balance sheet 676.2 Income statement 686.3 Statement of comprehensive income 696.4 Cash flow statement 706.5 Statement of changes in equity 716.6 Notes to the consolidated financial statements 726.7 Additional disclosures regarding financial instruments in accordance with IFRS7 109

7 Supplementary information to the consolidated financial statements7.1 List of investments in subsidiaries and associates 125

8 Falck Renewables SpA separate financial statements8.1 Balance sheet 1298.2 Income statement 1308.3 Statement of comprehensive income 1318.4 Cash flow statement 1328.5 Statement of changes in equity 1338.6 Notes to the financial statements 1348.7 Additional disclosures regarding financial instruments in accordance with IFRS7 169

9 Supplementary information to the Falck Renewables SpA separate financial statements9.1 List of direct and indirect investments in subsidiaries and associates 1779.2 Summary of significant financial data from latest financial statements

of subsidiaries and associates 179

10 Certifications on consolidated and parent company financial statements pursuant toarticle 81-ter of Consob Regulation 11971 of 14 May 1999 as amended 185

11 Report of the board of statutory auditors to the annual general meeting 189

12 Independent auditors’ reports 197

Before commenting on the year that has justpassed, I would like to pause and reflect on aspecific day that was fundamental to achievingthis year’s results, more precisely 28 May 2010,the day on which the relevant boards of directorsapproved the extraordinary project to consolida-te all of the Falck Group’s renewable activities.

Numerous variables could have affected thischange, but I believed then, as I do now, thatbusiness is founded on the courage to embracechange. Falck Renewables was created on thisprinciple, which has always promoted change inthe Falck Group, and now we are delighted toillustrate the results of the previous year.

2011 was an exemplary year in terms of finalisedprojects and outstanding financial results thatare illustrated further in the Chief Executive Offi-cer’s letter.

Falck Renewables’ growth this year was unstop-pable, confirming once again that we chose theright direction and that the business plan isbased on sound assumptions and shows ampledevelopment potential.

As an example of our growth model and thevalues to which we aspire, it is worth highlightinganother longstanding business characteristicthat is apparent in the activities finalised thisyear: interaction and collaboration with the com-munities in which we work. Recent examples ofthis include: three quarters of the companiesthat worked on the construction of the Buddusò- Alà dei Sardi wind farm, which commencedoperations in 2011 boasting the largest installedcapacity in Italy, were local companies from Sar-dinia; a cooperative of young people is involvedin security and maintenance activities at the San

Sostene wind farm, providing an invaluablesource of employment in an area hit by highunemployment; more than 300 students visit ourTrezzo sull’Adda WtE plant every year.

We have also embarked on numerous social andenvironmental initiatives at our overseas opera-tions: at Cefn Croes in the UK, every year wesupport a countryside restoration plan thatincludes projects to safeguard a number of spe-cies of local wildlife and protect moorland andbog habitats, in Ben Aketil local species of birdsare monitored and in Kilbraur a conservationplan to maintain the existing natural habitat is inthe pipeline.

Falck Renewables is today the leading indepen-dent producer of renewable energy and I wouldlike to thank the Chief Executive Officer and themanagement team together with all of the staffwho, through their hard efforts, determinationand effectiveness, achieved significant andsustainable operating results. I also thank theboard of directors and the committees that pro-vided invaluable constructive support to thesegreat developments.

I am confident that the results achieved this yearhave provided the impetus for future develop-ment that we will build on together.

The ChairmanFederico Falck

4

Letter of the Chairman to the shareholders and stakeholders

5

6

2011 marked the“birth” of Falck Rene-wables, following themerger of the FalckGroup’s renewableenergy generatingactivities into onecompany.

This was a highly suc-cessful year for FalckRenewables that wit-nessed achievementsboth in terms of pro-jects developed andfinancial results, and

demonstrates the fact that we upheld and car-ried through all of our commitments to our sha-reholders and stakeholders with passion andconviction.

I personally would like to thank our manage-ment team and all of my colleagues for thedetermination and enthusiasm they showed incarrying out their work over the year and for thesupport they provided to the projects.

From a business perspective, Falck Renewa-bles increased its installed capacity from 498 to684 MW (+37%) in 2011, firmly cementing itsleadership position in the private independentrenewable energy production sector in Italy andEurope. This increase is thanks to the photo-voltaic plants of Cardonita, Spinasanta andSugherotorto in Sicily, amounting to a combined13 MW, the expansion of Kilbraur and Millen-nium in Scotland (35 MW) and the Buddusò -Alà dei Sardi wind farm (138 MW), all coming onstream this year. The latter is the largest windfarm in Italy with an estimated annual output ofapproximately 330 GWh that alone is able tomeet the energy needs of 110,000 average Ita-lian families. It was inaugurated last October

and took only 30 months to construct. Theincrease in installed capacity, together withimproved operating efficiency, cost synergies,better plant performance and careful manage-ment of our energy portfolio led to an increasein electricity generated from 1,147,000 MWh to1,560,000 MWh, corresponding to the energyrequirements of more than 500,000 Italian fami-lies and an outstanding improvement in thefinancial results compared to the combinedfigures for 2010.

This is a significant milestone, particularly inenvironmental terms, which we share with localcommunities: our clean energy meant thatapproximately 550,000 tons of CO2 emissionsto the atmosphere were avoided. The environ-mental and social, together with economic,responsibility of Falck Renewables’ projects is afundamental element of our corporate missionand an aspect on which we will focus evenmore in future in our pipeline of around 1,000MW of new projects across the UK, France andPoland. Over the next few years our efforts willbe concentrated on Poland due to its high rene-wable energy potential.

We also recorded 11% growth in the wastetreatment business, due to more effective main-tenance work on the Trezzo sull’Adda (20 MW)and Granarolo dell’Emilia (49% stake) plants,together with the impact of the full year’s con-solidation of Esposito Servizi Ecologici Srl andEcocentro Soluzioni Ambientali Srl that provideenvironmental services including waste selec-tion, treatment and transformation.

Financial growth exceeded expectations, recor-ding marked percentage increases: Ebitdaamounted to Euro 141.7 million (+49.9% on the2010 combined amount), which significantlysurpassed the estimated Euro 130 million com-municated to the market at the time of the share

Letter of the Chief Executive Officer to the shareholders and stakeholders

7

capital increase finalised in March. Revenuealso bettered expectations, equalling Euro248.6 million (+34.7% on the 2010 combinedamount), while profit for the year closed at Euro19.8 million, more than eight times the 2010combined amount. Profit for the year wouldhave reached Euro 32 million without the impactof the deconsolidation and impairment lossrecognised against Palermo Energia Ambiente,which is detailed in full in the Annual Report. Itake this opportunity to reassure those share-holders and stakeholders who read the report:the stake in Pea has been written off in full andas a consequence is no longer included in theGroup’s scope of consolidation.

The net financial position net of the fair value ofderivatives is a net indebtedness of approxima-tely Euro 765 million, even lower than expected.

All of the above results take on a new light whenconsidered in the context of the current econo-mic crisis and confirm the solidity of the projectimplemented at the end of 2010 to consolidatethe Falck Group’s renewable activities.

2011 was also a year in which we laid the foun-dations for future growth: we secured theauthorisations for the Spaldington Airfield (15MW) and West Browncastle (30 MW) windfarms, construction work commenced on theNutberry (15 MW) wind farm and we enteredtwo joint ventures with Photonike and L.E.D.Lighting and Renewable Energy Development,for the development of rooftop photovoltaicplants in Italy, in addition to launching initiativesto develop the future pipeline in areas of interestacross Europe.

With regard to the outlook for 2012 this willmark a year of growth for Falck Renewablesthanks to the full year impact of the Buddusò -Alà dei Sardi plant, the expansion of the Scot-

tish plants Millennium and Kilbraur and the pho-tovoltaic plants in Sicily. Other projects will alsocome on stream this year: the Petralia Sottanawind farm (22 MW) and the Ty Ru wind farm inFrance (10 MW) that, together with our existingoperating plants, we estimate will bring Ebitdato more than Euro 155 million.

I would like to provide a brief update on the2012-2014 business plan that was approved bythe Board of Directors together with the AnnualReport. The plan confirms the drivers of diffe-rentiating by production technology and bygeographical area and envisages sustainablegrowth centred on areas where there is a higherconcentration of renewable energy sources andon countries investing in the expansion of rene-wable energy.

We expect to have an installed capacity ofapproximately 950 MW by the end of 2014, with684 MW already in place at 31 December 2011and more than 100 MW in the pipeline inrespect of plants under construction or authori-sed plants. We estimate this will provide Ebitdaof around Euro 190 million, representing 34%overall growth.

To conclude, I renew my, and management’scommitment, to ensuring that Falck Renewa-bles maintains its outstanding strategic positionand continues to create value for its sharehol-ders in the years to come.

The Chief Executive OfficerPiero Manzoni

9

The shareholders are invited to attend the ordinary annual general meeting (AGM) at the Mediobanca offi-ces in Milan, Via Filodrammatici 3, at 10.30 a.m. on 7 May 2012 in first call and, where necessary, at the sametime and address on 9 May 2012 in second call, in order to discuss the following:

Agenda

Ordinary business:

1. The annual report for the year ended 31 December 2011; directors’ report, independent auditors’ reports,board of statutory auditors’ report: approval, related resolutions and resulting matters.

2. Proposed distribution of reserves.3. Appointment of a director to the board.4. Presentation of the remuneration report pursuant to articles 123-ter of Legislative Decree 58/1998 and84-quater of the Listing Rules and consultative vote on Section I;

5. Review of Reconta Ernst & Young SpA’s audit fees for the period 2011-2019: related resolutions and resul-ting matters.

Share capital and right to voteThe share capital of Falck Renewables SpA is Euro 291,413,891 issued and fully paid, consisting of291,413,891 shares with a nominal value of Euro 1 each, each share holding the right to one vote at theAGM. The company does not hold any own shares at today’s date.

Attendance and representation at the AGMThe following information is provided in respect of those shareholders who hold the right to attend and voteat the AGM (pursuant to article 125-bis of the Consolidated Finance Act):- In accordance with article 83-sexies of the Consolidated Finance Act, shareholders with the right toattend and vote at the AGM is confirmed in writing to the company by the intermediary, based on theinformation in the company’s register at the end of the accounting day on the seventh working day priorto the date established for the AGM in first call (specifically by 25 April 2012); those parties that becameshareholders after this date may not attend or vote at the AGM; the intermediary must provide the abovenotice to the company by the end of the third working day prior to the date set for the AGM in first call(specifically by 2 May 2012). The right to attend and vote will be upheld where notice is received by thecompany after this date but prior to work commencing on the shareholders’ meeting;

- Postal votes and electronic votes are not permitted;- All shareholders who have the right to attend the AGM may be represented by written proxy in com-pliance with current legislation, by completing a proxy form that may be requested from the relevantintermediaries or is available online on the company website www.falckrenewables.eu. The representati-ve who either delivers or transmits a copy of the proxy form to the company is required to certify boththe validity of the proxy and the identity of the shareholder;

- Notice of proxy may be sent by registered post to the company’s registered offices in Corso Venezia 16,Milan (20121), or by e mail to: [email protected];

- proxy may also be given, without any additional cost to the voter, by instructing the company Società perAmministrazioni Fiduciarie “SPAFID” S.p.A. to vote on some or all of the business on the agenda, for thepurpose designated by the company pursuant to article 135-undecies of the Consolidated Finance Act,on condition that the original is received by the second working day prior to the date set for the AGM(specifically by 3 May 2012) either by courier, AR recorded delivery or ordinary post to the premises in

1Notice of annual general meeting

Foro Buonaparte 10, Milan (20121); proxy will not be valid for those matters for which voting instructionswere not received. A proxy form may be obtained from the registered offices in Corso Venezia 16, Milanand the company website www.falckrenewables.eu; the proxy and voting instructions may be withdrawnby the above deadline (specifically by 3 May 2012).

Right to ask questionsShareholders may ask questions relating to items on the agenda prior to the meeting and up to the end ofthe second working day before the date set for the AGM in first call (specifically by 3 May 2012). These maybe put in writing and sent by registered post to the company’s registered offices in Corso Venezia 16, Milan(20121) or by e mail to the following address: [email protected], together with the inter-mediary notice confirming the shareholders’ validity; this notice is not required where prior notice has beenreceived from the intermediary regarding attendance at the AGM. The company may publish a response onthe company website www.falckrenewables.eu. or at the latest reply during the AGM and may avail of theoption to offer a single reply to more than one question pertaining to the same subject.

Amendments to the agendaIn accordance with law, shareholders who, either individually or jointly, represent at least one fortieth of theshare capital are entitled to propose, within ten days of the notice of the AGM being issued, additional agen-da, providing details of them in the request; requests must be filed in writing together with the interme-diary’s notice confirming the limit regarding the number of shares held is satisfied. Shareholders who pro-pose additional agenda prepare a report on the business to be discussed, which should be submitted to theboard of directors by the last date for filing amendments. Proposed amendments to the agenda are notadmitted in relation to matters, on which the AGM is required to deliberate in accordance with law, propo-sed by the board of directors or in relation to projects or reports prepared by them, other than those pur-suant to article 125-ter, paragraph 1, of the Consolidated Finance Act. Amendments to the agenda must besent by recorded delivery to the registered offices in Corso Venezia 16, Milan, or by e mail to: [email protected]. Any changes to the AGM’s agenda subsequent to these requests must be notified following the same pro-cedure as the notice calling the AGM, at least fifteen days before the date set for the AGM. The amendmentnotice will be made available to the public, using the same communication channels used to provide thedocumentation relating to the AGM, together with the shareholders’ report that gave rise to the amendmentand any comments by the board of directors.

***

Documentation Documentation relating to the AGM, required by existing legislation, will be made available to the public atthe company’s registered offices in Milan, Corso Venezia 16, Borsa Italiana SpA and the company websitewww.falckrenewables.eu within the time limits prescribed by law. Shareholders may view the filed docu-ments at the registered offices and copies will be provided on request for a fee.

10

11

More precisely:- the documentation relating to item 1 on the agenda comprising the report of the board of directors andproposed approval, the annual report for the year ended 31 December 2011, the directors’ report, the 2011report on corporate governance and ownership structure, the report of the board of statutory auditors andthe independent auditors’ reports, together with the board of directors’ report on the remuneration reportat item 4 of the agenda prepared pursuant to article 123-ter of the Consolidated Finance Act and theremuneration report itself, will be made available to the public by 16 April 2012 as noted above.

- the documentation supporting items 2, 3 and 5 on the agenda, specifically the board of directors’ propo-sed distribution of reserves (item 2), the board of directors’ report on items 3 and 5 of the agenda, toge-ther with the board of statutory auditors’ proposal and the proposal regarding the audit fees, will be madeavailable to the public by 7 April 2012 as noted above.

***

Shareholders entitled to attend the AGM are invited to arrive before the scheduled starting time for themeeting in order to facilitate registration procedures that will commence from 10.00 a.m. onwards; share-holders are also requested to present a copy of the intermediary notice in order to expedite the control pro-cess.

Milan, 30 March 2012

The ChairmanFederico Falck

The notice of the AGM was published in the Milano Finanza of 6 April 2012.

12

Board of directors

Federico Falck (*) Chairman

Guido Rosa (*) Deputy chairman

Piero Manzoni (*) Chief Executive Officer

Marco Agostini Directors

Guido Corbetta

Enrico Falck (*)

Elisabetta Falck

Giovanni Maria Garegnani (**)

William Jacob Heller

Andrea Merloni (**)

Libero Milone (**)

Barbara Poggiali (by co-option 24.2.2012) (**)

Bernardo Rucellai (**)

Claudio Tatozzi (**)

Sergio Ungaro

(*) Members of the Executive Committee(**) Independent members

Board of statutory auditors

Massimo Scarpelli Chairman

Aldo Bisioli Statutory auditors

Alberto Giussani

Massimo Foschi Substitute statutory auditors

Gianluca Pezzati

Independent auditors

Reconta Ernst & Young SpA

2Company officers

10

0%10

0%85

%

96.3

5%

86.7

7%

60%

Ele

ttro

ambi

ente

SpA

Tife

o En

ergi

aA

mbi

ente

Scp

Ain

liqu

idat

ion

Pla

tani

Ene

rgia

Am

bien

te S

cpA

in li

quid

atio

n

Ecos

esto

SpA

Prim

a S

rl

Am

bien

te20

00 S

rl

49% F

rullo

Ene

rgia

Ambi

ente

Srl

100%

Act

elio

sS

olar

SpA

100%

Sol

arM

esag

ne S

rl100%

Esp

osito

S

ervi

ziE

colo

gici

Srl

23.2

7%Pa

lerm

o En

ergi

aAm

bien

te S

cpA

in li

quid

atio

n

Fal

ckR

enew

able

sIt

alia

Srl10

0%

100%

100%

Eol

o3W

Min

ervi

noM

urge

Srl 10

0%

Eol

ica

Pet

ralia

Srl

Geo

pow

erSa

rdeg

na S

rl100% 20

%

FR

IE

nerg

etic

a S

rl

Eol

ica

Cal

abra

Srl

in li

quid

atio

n20%

Eol

ica

Sud

Srl

100%

Tasf

iye

Hal

inde

Ezse

Ele

ktrik

U

retim

Ltd

Sirk

eti

99.9

9%F

alck

Ren

ewab

les

Win

d Lt

d

100%

Par

c E

olie

n de

Sai

nte

Trep

hine

Sar

l

100%F

alck

Ene

rgie

sR

enou

vela

bles

Sas

100%

100%

SE

Ty

Ru

Sas

Par

c E

olie

n de

Bau

d S

arl

Par

c E

olie

n de

Plo

neve

z du

Fao

u S

arl

100%

Par

c E

olie

n d’

Ava

illes

–Li

mou

zin

Sarl

Par

c E

olie

n D

e M

oulis

mes

Sa

rl

100%

75%

75%

51%

Ecov

eol S

as

Con

solid

ated

by

prop

ortio

nal

met

hod

Valu

ed a

pply

ing

equi

ty m

etho

d

Valu

ed a

t cos

t

Con

solid

ated

lin

e-by

-line

Wte

, bio

mas

s an

d ph

otov

olta

ic s

ecto

r

Win

d se

ctor

FALC

K R

EN

EW

AB

LES

SpA

Boy

ndie

Win

dEn

ergy

Ltd 10

0%

Earls

burn

M

ezza

nine

Ltd

Cam

bria

n W

ind

Ene

rgy

Ltd

Falc

k R

enew

able

sU

K H

oldi

ngs

(No.

1) L

td100%

Falc

k R

enew

able

sFi

nanc

e Lt

d100%

100%

100%

100%

Earls

burn

Win

dEn

ergy

Ltd

Kilb

raur

Win

d E

nerg

y Lt

d100%

Kilb

raur

2 W

ind

Ene

rgy

Ltd10

0%

Mill

enni

um W

ind

Ene

rgy

Ltd10

0%

100% B

en A

ketil

Win

dE

nerg

y Lt

d

100% B

en A

ketil

2

Win

d E

nerg

y Lt

d

52% N

utbe

rry

Win

dEn

ergy

Ltd

Eol

ica

Cab

ezo

San

Roq

ue S

A

Par

que

Eol

ico

La C

arra

cha

SL

Nue

vos

Par

que

Eol

icos

La M

uela

AIE

95.5

1%

26%

50%

50%

26%

Par

que

Eol

ico

Plan

a de

Jarre

ta S

L

50%

Elek

trow

nie

Wia

trow

e Bo

nwin

dLy

szko

wic

eSp

. Z.o

.o.

50%

Elek

trow

nie

Wia

trow

e Bo

nwin

dKa

mie

nica

Sp. Z

.o.o

.

52% D

unbe

ath

Win

dEn

ergy

Ltd

Par

c E

olie

n du

Fou

y Sa

s

100%

100%

100%

52%

Nes

s W

ind

Ener

gy L

td

52%

Spal

ding

ton

Airf

ield

Win

dEn

ergy

Ltd

Cus

hnie

Win

dE

nerg

y Lt

d

Kin

gsbu

rn W

ind

Ene

rgy

Ltd

Par

c E

olie

nde

s C

rete

s S

as

100%

Esqu

enno

isE

nerg

ie S

as

100%

50%

Elek

trow

nie

Wia

trow

e Bo

nwin

dLe

szno

Sp. Z

.o.o

Act

elio

sE

tnea

Srl

100%

SE K

erne

bet S

as

13

Group structure3

14

(Euro thousands) 2011 2010 2009 2008

Revenue 248,650 99,196 94,923 97,699

Gross profit 118,062 37,257 32,826 40,977

EBITDA (1) 141,738 39,541 35,691 48,718

Operating profit 79,233 19,656 18,802 32,937

Profit for the year 19,844 4,643 5,734 19,462

Profit for the year attributable to owners of the parent 18,863 2,499 4,175 17,927

Earnings per share (Euro) (2) 0.070 0.031 0.062 0.265

No. of shares (average for the year) in thousands 269,402 79,812 67,680 67,680

No. of shares (at year-end) in thousands 291,414 161,897 67,680 67,680

- Net financial (assets)/liabilities 15,523 103,910 (162,407) (180,236)

- Non-recourse financing 749,680 601,213 65,371 79,841

Total net financial position - indebtedness/(asset) 765,203 705,123 (97,036) (100,395)

- Derivative financial instruments 60,913 23,228 1,778 1,612

Total net financial position including derivatives (asset) 826,116 728,351 (95,258) (98,783)

Total equity 451,826 335,333 349,652 354,994

Equity attributable to owners of the parent 444,913 327,988 343,849 350,063

Equity holders equity per share (Euro) (2) 1.651 4.110 5.081 5.172

Capital expenditure 177,995 89,047 13,687 17,070

Gross profit/revenue 47.5% 37.6% 34.6% 41.9%

EBITDA/revenue 57.0% 39.9% 37.6% 49.9%

Operating profit/revenue 31.9% 19.8% 19.8% 33.7%

Profit for the year/total equity 4.4% 1.4% 1.6% 5.5%

Net financial position/total equity 1.83 2.17 (0.27) (0.28)

Total number of group employees (no.) 241 210 145 140

(1) EBITDA = EBITDA is measured by the Falck Renewables group as profit for the year before income and costs from investments, net financeincome/costs, amortisation and depreciation, impairment, charges to risk provisions and income tax expense. This indicator was calculatedapplying best market practice taking into consideration the new group financing contracts. This method was applied to calculate EBITDA forthe previous years disclosed.

(2) Calculated using the average shares outstanding during the year.

Consolidated financial highlights4

Directors’ report5

16

Map of Falck Renewables’s plants

17

Dear Shareholders,

The parent company’s separate financial statements and the consolidated financial statements for the yearended 31 December 2011 have been prepared in accordance with International Financial Reporting Stan-dards (IFRS). These standards were adopted in 2005 for the first time in relation to the consolidated finan-cial statements and in 2006 for the parent company’s separate financial statements.

5.1 Falck Renewables group operating and financial review

5.1.1 Falck Renewables group profile

Falck Renewables SpA is an Italian limited company (“the Company” or “Falck Renewables”) with registe-red offices in Corso Venezia 16, Milan and its subsidiaries (hereinafter “the Falck Renewables Group” or the“Group”) essentially operate in Italy, the United Kingdom and France. Falck Renewables also holds invest-ments in three associated companies that operate two wind farms in Spain. A number of wind farms arecurrently under construction in Poland.

The Falck Renewables Group’s current structure is the outcome of the Consolidation Project that took placein the 2010 fourth quarter, whereby all of the renewable energy businesses of Falck SpA were transferred toFalck Renewables SpA, more specifically:

(i) the wind sector business of Falck Renewables Wind Ltd formerly Falck Renewables Plc (previously con-trolled by Falck SpA through Falck Energy SpA) and its subsidiaries; and

(ii) the WtE, biomass and photovoltaic businesses of Falck Renewables SpA (already controlled prior to con-clusion of the Consolidation Project by Actelios SpA) and its subsidiaries.

The Falck Renewables Group operates in the production of energy from renewable sources through windfarms and WtE, biomass and photovoltaic plants. Specialising in the renewable energy sector has allowedthe Falck Renewables Group to gain experience and acquire know-how in the operation and maintenance(O&M) of proprietary and third party-owned renewable energy power plants.

The Falck Renewables Group operates in the following two sectors:

• the wind sector, revenue from which derives mainly from the sale of Green Certificates, ROCs and elec-tricity generated by the Group’s wind farms;

• the WtE, biomass and photovoltaic sector, where revenue mainly derives from the sale of Green Certifi-cates and electrical and thermal energy and the operation and maintenance of third party renewableenergy power plants.

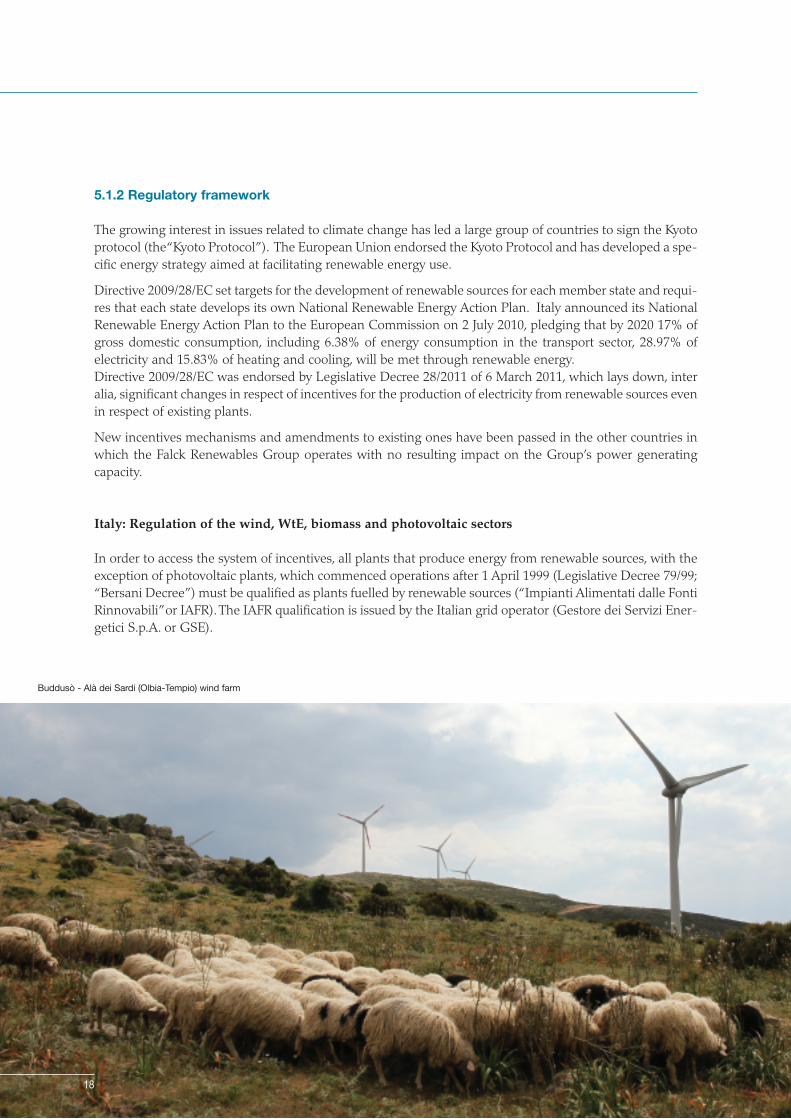

5.1.2 Regulatory framework

The growing interest in issues related to climate change has led a large group of countries to sign the Kyotoprotocol (the “Kyoto Protocol”). The European Union endorsed the Kyoto Protocol and has developed a spe-cific energy strategy aimed at facilitating renewable energy use.

Directive 2009/28/EC set targets for the development of renewable sources for each member state and requi-res that each state develops its own National Renewable Energy Action Plan. Italy announced its NationalRenewable Energy Action Plan to the European Commission on 2 July 2010, pledging that by 2020 17% ofgross domestic consumption, including 6.38% of energy consumption in the transport sector, 28.97% ofelectricity and 15.83% of heating and cooling, will be met through renewable energy. Directive 2009/28/EC was endorsed by Legislative Decree 28/2011 of 6 March 2011, which lays down, interalia, significant changes in respect of incentives for the production of electricity from renewable sources evenin respect of existing plants.

New incentives mechanisms and amendments to existing ones have been passed in the other countries inwhich the Falck Renewables Group operates with no resulting impact on the Group’s power generatingcapacity.

Italy: Regulation of the wind, WtE, biomass and photovoltaic sectors

In order to access the system of incentives, all plants that produce energy from renewable sources, with theexception of photovoltaic plants, which commenced operations after 1 April 1999 (Legislative Decree 79/99;“Bersani Decree”) must be qualified as plants fuelled by renewable sources (“Impianti Alimentati dalle FontiRinnovabili” or IAFR). The IAFR qualification is issued by the Italian grid operator (Gestore dei Servizi Ener-getici S.p.A. or GSE).

18

Buddusò - Alà dei Sardi (Olbia-Tempio) wind farm

19

The regulations on incentives for the production of electricity from renewable sources focus on severalmechanisms with different applications based on (i) the date the plant commenced operations, (ii) the typeof renewable resource used, and (iii) the plant’s capacity. The principal incentives are as follows:

a) CIP 6/92;

b) Green Certificates introduced by the Bersani Decree;

c) all-in rate introduced by Law 244 of 24 December 2007 (“All-in Rate”);

d) energy account governing photovoltaic plants (Ministerial Decree (MD) 6/08/2010).

a) CIP 6/92

This incentive system offers a direct incentive to producers of renewable and similar types of energy, and isstill effective for a number of operating plants, whereby under a specific agreement the producers soldenergy produced to ENEL (now the GSE) at a fixed price without participating in the feed in tariff marketmechanism. In particular, CIP 6/92 fixed the selling prices under which Enel purchased electricity, in accor-dance with the “avoided costs” criteria (of investment and combustibles) and offering incentives in relationto the higher costs incurred by generating electricity from renewable sources.Benefits terms have been fixed for 15 years, although the incentive element that increments avoided costsis guaranteed up to a maximum of 8 years.

b) Green certificates (GC)

From 2001, the Bersani Decree has required entities importing or producing more than 100 GWh per yearfrom conventional sources to feed into the grid (in the following year) not less than 2% of energy producedby renewable sources (for 2011 the minimum quota is 6.8%).

Cardonita (Enna) photovoltaic plant Spinasanta (Catania ) photovoltaic plant

The above mentioned emission quotas may bemet through the production of renewableenergy or alternatively the purchase of GC’sfrom other renewable energy producers. For each MWh of renewable energy the GSEawards the producer 1 GC. The GC’s are annual certificates of renewableproduction that producers receive (for 15 yearperiods) from the GSE based on productionlevels and the renewable source used. The cur-rent GC ratios applied to renewable energyproduction are:

. onshore wind farms: 1;

. offshore wind farms: 1.50;

. biodegradable waste and biomass plants notsourced from short chain: 1.3;

. agricultural biomass plants sourced fromshort chain supplies: 1.8.

The GC market becomes one of demand(minimum quotas) and supply (GC’s). TheLegislative Decree implementing Directive2009/28/EC states that the GC incentivemechanism will cease (with a transition periodup to 2015) and be replaced by a “Tariff” whe-reby the incentive element is determined

annually based on the market value of energy generated. The producers will therefore be involved in theelectricity market both in technical terms, through transmission (TERNA), and commercial terms, throughvaluation (the Electricity Account with the GME or bilateral contracts with operators or traders of standardproducts).The above mechanism applies to plants in operation at 31 December 2012.The GC system will continue through 2011-2015 and the GSE will buy in all excess GCs on the market. Thelegislative decree envisages an annual buy-in by the GSE of 78% (in Euro/MWh) of the difference between180 and the average annual electricity trading price published by the Regulatory Authority for Electricity andGas by 31 January each year. From 2016, a new FEED IN system will be applied to the remaining incentive years, the terms of which willbe defined in the forthcoming decree implementing Legislative Decree 28/2011.

c) All-in rate

The all-in rate is a form of incentive for energy produced from renewable sources that can be provided for15 years to certain types of plants with an average annual nominal capacity of up to 1 MW, as an alternati-ve to the Green Certificate mechanism. Producers who opt for this tariff option may not participate in the electricity market (FEED IN TARIFFmechanism). This tariff is not applicable to the Falck Renewables Group’s plants.

20

Work at the street sweeping recovery plant in Gorle (Bergamo)

d) Energy account

The energy account is the incentive for photo-voltaic plants and was originally governed byMinisterial Decree of 19 February 2007 andensuing amendments (replacing MinisterialDecree 28/07/05 and Ministerial Decree06/02/06). With regard to plants that commen-ced operations between 1 January 2008 and31 December 2010 the Ministerial Decree pro-vides tariff-based incentives for the energyproduced that vary based on the characteristicsof the plants (integrated, partially integrated ornon-integrated) and their nominal capacity (1-3 KW; 3 - 20 KW; over 20 KW). This incentiveis provided by GSE for a period of up to 20years. Under Legislative Decree 129 of 13 August2010, the incentive tariffs under the energyaccount governed by Ministerial Decree of19 February 2007 continue to apply to photo-voltaic systems including those that commen-ced operations after 31 December 2010, provi-ded that (i) by 31 December 2010 the photo-voltaic system had been installed and the rele-vant authorities notified of the completion ofwork, and (ii) the facilities came into operationby 30 June 2011.

The MD of 6/8/2010 sets a national target for systems installation totalling 8 GW by 2020. It also sets anincentives cap of 3 GW for solar photovoltaic plants, 300 MW for integrated plants with innovative featuresand 200 MW for concentrated photovoltaic plants. The MD of 6/8/2010 no longer distinguishes betweenplants in relation to their integration with existing buildings but identifies them as those “constructed onbuildings” and “other plants”.

The Legislative Decree implementing Directive 2009/28/EC specifies that the provisions of MD 06/08/10apply to plants that commenced operations prior to 31 May 2011. New Ministerial Decrees will be issuedfor subsequent periods.

• United Kingdom: regulatory framework in the wind sector

In line with Directive 2009/28/EC, the UK Government’s target is to achieve 30% of its energy consumptionfrom renewable sources by 2020.

The incentives schemes for the production of electricity from renewable sources fall under 2 incentives regi-mes:

a) NFFO Order (England, Wales and Scotland);b) Renewables Obligation Order.

21

Street sweeping recovery plant in Gorle (Bergamo)

a) NFFO (England, Wales and Scotland)

In England and Wales the legacy regime for the sale of electricity generated from renewable sources is regu-lated under the Electricity (Non-Fossil Fuel Sources) (England and Wales) Orders of 1994, 1997 and 1998(“NFFOEW Orders”). In Scotland it is regulated under the Electricity (Non-Fossil Fuel Sources) (Scotland)Orders of 1994, 1997 and 1999 (“NFFOS Orders”). There are also separate regulations for Northern Ireland.

Although the underlying legislation has been repealed, there is a saving in respect of existing projects whichcontinue to operate under the regulation until the expiry of the existing NFFO contracts (fixed price long-term sales contracts) with NFPA. For these plants the incentive mechanism is the feed in tariff. The CefnCroes plant continues to operate under the NFFOEW Orders.

b) Renewables Obligation Orders

The current regime to promote and support the generation of electricity from renewable sources in Englandand Wales and in Scotland is through separate Renewables Obligation Orders (“ROs”). The RenewablesObligation Order 2006 (England and Wales) and the Renewables Obligation (Scotland) Order 2007, respec-tively impose obligations on electricity suppliers to demonstrate that not less than a stipulated percentageof electricity produced was generated from renewable sources. The Office of Gas and Electricity Markets,OFGEM, issues Renewable Obligations Certificates (“ROCs”) and Scottish Renewable Obligations Certifi-cates (“SROCs”) on behalf of the Gas and Electricity Markets Authority (“GEMA”).

The ROs require electricity suppliers to source an increasing portion of their electricity supply from rene-wable sources (including onshore and offshore wind farms). The current target is set at 12.4% of all electri-city fed into the network in the period from 1 April 2011 to 31 March 2012.

Compliance under the RO scheme is regulated through a certification system using ROCs and SROCs.Renewable energy generators receive ROCs or SROCs for each MWh of electricity generated. ROCs andSROCs are tradable, are priced in the market and traded at a premium compared to the market price of asimilar quantity of energy (FEED IN PREMIUM mechanism).

Smaller wind farms (all of the Group’s wind farms except for Kilbraur and Millennium) are also entitled toother benefits. Renewables generating plants are typically connected to the low voltage regional electricitydistribution network rather than to the high voltage transmission network operated by the National Grid.Using the distribution network rather than the high voltage transmission network avoids the charges impo-sed by the National Grid. This is known as Triad Avoidance Benefit.

The Finance Act 2000 introduced the Climate Change Levy (“CCL”) which is a flat rate currently at £4.41 perMWh, charged on the supply of electricity to non-domestic customers. Eligible renewable generators areentitled to climate change levy exemption certificates (“LECs”). In order to meet the obligations of theFinance Act 2000, suppliers may either purchase LECs from a generator of qualifying renewable energywhich can then be submitted to OFGEM or pay the tax directly to OFGEM. Unlike ROCs (and SROCs), LECs are not fully tradable and the supplier must show they relate to a quan-tity of renewable electricity actually supplied to a specific industrial consumer.

22

23

• Spain: regulatory framework in the wind sector

Under Directive 2001/77/EC, Spain has targeted that 29% of gross electricity consumption be produced fromrenewable energy sources by 2010.

The main regulations in Spain comprise the 2004 and 2007 Royal Decrees. New regulations were approvedin July 2010 which do not affect the wind farms falling under the 2004 Royal Decree. The 2004 Royal Decree established that electricity generated could be sold at a price comprising a fixed ele-ment (or premium) and a variable element depending on the energy prices in the Spanish electricity mar-ket.

The 2004 Royal Decree was superseded by the 2007 Royal Decree. The 2007 Royal Decree maintains thefeed-in tariff regime and introduces a new pool price regime, which is subject to a floor and a cap to ensu-re wind farm owners are not under or over remunerated. The Group’s wind farms have elected to apply thepool price regime established in the 2004 Royal Decree until 31 December 2012, following which the newpool price regime established under the 2007 Royal Decree will apply. In addition to the pricing regimes, electricity generated from renewable sources is afforded priority access tothe transmission and distribution grid system, ensuring all power is purchased.

Royal Decree 1/2012 issued on 27 January 2012 temporarily suspends all economic incentives for the pro-duction of electricity from renewal sources in respect of projects not authorised at the date of issue of thedecree as Spain has already exceeded the level of installed capacity set out in the plan issued by the SpanishGovernment. This suspension will remain in force until a solution to the system’s tariff deficit is found anda new renewable sources remuneration model is established.

Pool price regime

The majority of Spain’s wind power is sold under the pool price regime. The Group’s wind farms apply thisregime.

Remuneration under the 2004 Royal Decree is calculated as the sum of the negotiated market price plus pre-mium, plus/minus a reactive power bonus, plus incentives, minus deviations.

The negotiated market price is calculated either (i) by reference to the settlement of demand and supply andother procedures carried out by OMEL (the market operator) or (ii) by reference to the price negotiated bet-ween the parties when the sale is made though bilateral agreements or forward market trading (“venta aplazo”).

The premium is set at 40% of the average or reference tariff, while the incentive is set at 10% of the avera-ge reference tariff.

Pursuant to the 2007 Royal Decree, remuneration is calculated as the sum of the negotiated market priceplus a premium of 2.9291 Euro c/Kwh. The market price plus the premium cannot be greater than 8.4944Euro c/Kwh nor less than 7.1275 Euro c/KWh. Moreover, the remuneration also includes a reactive powerbonus (calculated as a percentage of 7.8441 Euro c/KWh) in relation to the ability of the operator to controlreactive power. The premium will be reviewed annually, taking into consideration the Consumer Price Index(published monthly and at the end of every year by the Instituto Nacional de Estadisctica) minus 0.25% until2012 and minus 0.50% thereafter.

• France: regulatory framework in wind sector

Law 2000-198 of 10 February 2000 regarding theupgrade and development of public services andelectricity (and ensuing amendments under theLaws of 3 January 2003 and 15 July 2003 - theFrench Electricity Law) and Decree 2001-410 of10 May 2001, require Electricité de France (“EDF”)and local distributors to purchase electricity gene-rated by producers of energy from renewable sour-ces under a 15 year purchase agreement. Subsequent to the amendment of July 2005, thepurchase obligation applies to wind farms locatedwithin the perimeter of a wind farm developmentarea (zone de development de l’éolien or ZDE).

The conditions applicable to the purchase of elec-tricity generated by renewable energy plants areset out in the Arrété of 17 November 2008.

The Arrété specifies a fixed tariff regime (8.2 Euroc/KWh subject to indexation) for the first 10 yearsof generation, while the tariff for the last five yearsof the purchase contract is linked to the volume ofenergy produced in the first 10 year period. Low-wind sites (less than 2,400 hours of generation peryear) will continue to benefit from the same tarifffor the full 15 year period, whereas middle andhigh-wind speed sites will see a decrease in thepurchase tariff in the final five years of the con-tract.

The tariff applicable to a specific wind farm isdetermined using a coefficient (“k index”) depen-dent on the year in which the EDF received the fullapplication to enter into the electricity purchaseagreement. The k index is reviewed annually inline with a specific formula defined in the Arrété.The tariff, subject to an annual index, is guaran-teed for the 15 years following the start of opera-tions.

The Group’s plants are located in low wind speedareas.

24

Le Fouy (France) wind farm

Buddusò - Alà dei Sardi (Olbia-Tempio) wind farm

25

5.1.3 Performance

The consolidated results for the year ended 31 December 2010 comprised the full year’s results of the WtE,biomass and photovoltaic sector while the results of the wind sector (Falck Renewables Wind Ltd, formerlyFalck Renewables Plc) only related to the period 1.12.2010-31.12.2010, as it became part of the Falck Rene-wables Group in November 2010. The balance sheet comprised all of the assets and liabilities of both of the above sectors at 31 December2010.Consequently, the 2011 results of operations are not comparable with those for the year ended 2010 whilethe state of affairs and financial position at 31 December 2011 are comparable with those at 31 December2010.

(Euro thousands) 31.12.2011 31.12.2010Revenue 248,650 99,196Cost of sales (130,588) (61,939)Gross profit 118,062 37,257Operating profit 79,233 19,656EBITDA 141,738 39,541Profit for the year 19,844 4,643Profit for the year attributable to owners of the parent 18,863 2,499Invested capital net of provisions 1,277,942 1,063,684Total equity 451,826 335,333Net financial position - net indebtedness 826,116 728,351of which non-recourse financing 749,680 601,213Capital expenditure 177,995 89,047Group employees at year-end (no.) 241 210Ordinary shares (no.) 291,413,891 161,896,607

La Calce (Brindisi) photovoltaic plant Trezzo sull’Adda (Milan) WtE plant

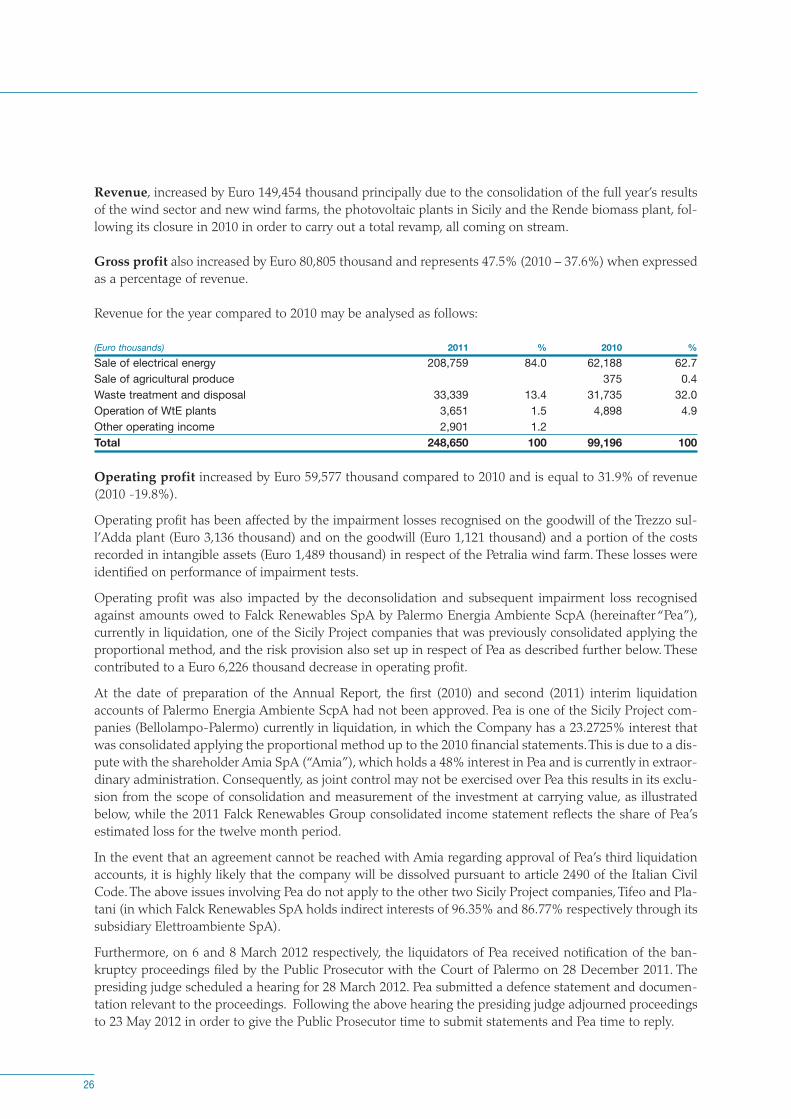

Revenue, increased by Euro 149,454 thousand principally due to the consolidation of the full year’s resultsof the wind sector and new wind farms, the photovoltaic plants in Sicily and the Rende biomass plant, fol-lowing its closure in 2010 in order to carry out a total revamp, all coming on stream.

Gross profit also increased by Euro 80,805 thousand and represents 47.5% (2010 – 37.6%) when expressedas a percentage of revenue.

Revenue for the year compared to 2010 may be analysed as follows:

(Euro thousands) 2011 % 2010 %Sale of electrical energy 208,759 84.0 62,188 62.7Sale of agricultural produce 375 0.4Waste treatment and disposal 33,339 13.4 31,735 32.0Operation of WtE plants 3,651 1.5 4,898 4.9Other operating income 2,901 1.2Total 248,650 100 99,196 100

Operating profit increased by Euro 59,577 thousand compared to 2010 and is equal to 31.9% of revenue(2010 -19.8%).

Operating profit has been affected by the impairment losses recognised on the goodwill of the Trezzo sul-l’Adda plant (Euro 3,136 thousand) and on the goodwill (Euro 1,121 thousand) and a portion of the costsrecorded in intangible assets (Euro 1,489 thousand) in respect of the Petralia wind farm. These losses wereidentified on performance of impairment tests.

Operating profit was also impacted by the deconsolidation and subsequent impairment loss recognisedagainst amounts owed to Falck Renewables SpA by Palermo Energia Ambiente ScpA (hereinafter “Pea”),currently in liquidation, one of the Sicily Project companies that was previously consolidated applying theproportional method, and the risk provision also set up in respect of Pea as described further below. Thesecontributed to a Euro 6,226 thousand decrease in operating profit.

At the date of preparation of the Annual Report, the first (2010) and second (2011) interim liquidationaccounts of Palermo Energia Ambiente ScpA had not been approved. Pea is one of the Sicily Project com-panies (Bellolampo-Palermo) currently in liquidation, in which the Company has a 23.2725% interest thatwas consolidated applying the proportional method up to the 2010 financial statements. This is due to a dis-pute with the shareholder Amia SpA (“Amia”), which holds a 48% interest in Pea and is currently in extraor-dinary administration. Consequently, as joint control may not be exercised over Pea this results in its exclu-sion from the scope of consolidation and measurement of the investment at carrying value, as illustratedbelow, while the 2011 Falck Renewables Group consolidated income statement reflects the share of Pea’sestimated loss for the twelve month period.

In the event that an agreement cannot be reached with Amia regarding approval of Pea’s third liquidationaccounts, it is highly likely that the company will be dissolved pursuant to article 2490 of the Italian CivilCode. The above issues involving Pea do not apply to the other two Sicily Project companies, Tifeo and Pla-tani (in which Falck Renewables SpA holds indirect interests of 96.35% and 86.77% respectively through itssubsidiary Elettroambiente SpA).

Furthermore, on 6 and 8 March 2012 respectively, the liquidators of Pea received notification of the ban-kruptcy proceedings filed by the Public Prosecutor with the Court of Palermo on 28 December 2011. Thepresiding judge scheduled a hearing for 28 March 2012. Pea submitted a defence statement and documen-tation relevant to the proceedings. Following the above hearing the presiding judge adjourned proceedingsto 23 May 2012 in order to give the Public Prosecutor time to submit statements and Pea time to reply.

26

27

In order to best represent Pea’s and its shareholders claims against the Sicily Regional Authorities, FalckRenewables SpA and Falck SpA, which together hold a 48% interest in Pea, signed an agreement with Peawhereby they agree to defer the receivables (both trade and financial) to allow payment of other creditorsand waive the same receivables in the event that following liquidation Pea does not have sufficient financialresources to pay the amounts in full. Also under this agreement, the shareholders Falck Renewables SpAand Falck SpA undertake to provide Pea with the funds required to settle certain creditors. A provision ofEuro 2,210 thousand was included in the sundry risks provision in the consolidated financial statements inorder to reflect this commitment. Pea’s other shareholders entered into separate agreements regarding thesettlement of receivables with Pea.

In light of this situation, which only involves Pea and in no way impacts on outstanding disputes betweenTifeo and Platani and the Sicily Regional Offices as confirmed by its legal advisors, the Falck RenewablesGroup carried out a valuation of the amounts arising after deconsolidation of Pea that resulted in recogni-tion of impairment losses, given the risk of dissolution of the company, against the carrying value of theinvestment in Pea and all receivables (trade and financial) due from it. Although there has been no sub-stantial change in the claims brought forward in the proceedings as no facts have emerged that would altersignificantly the outcome of the proceedings, certain risks and uncertainties regarding the corporate gover-nance of Pea exist that affect the risk of recoverability of the impaired amounts.

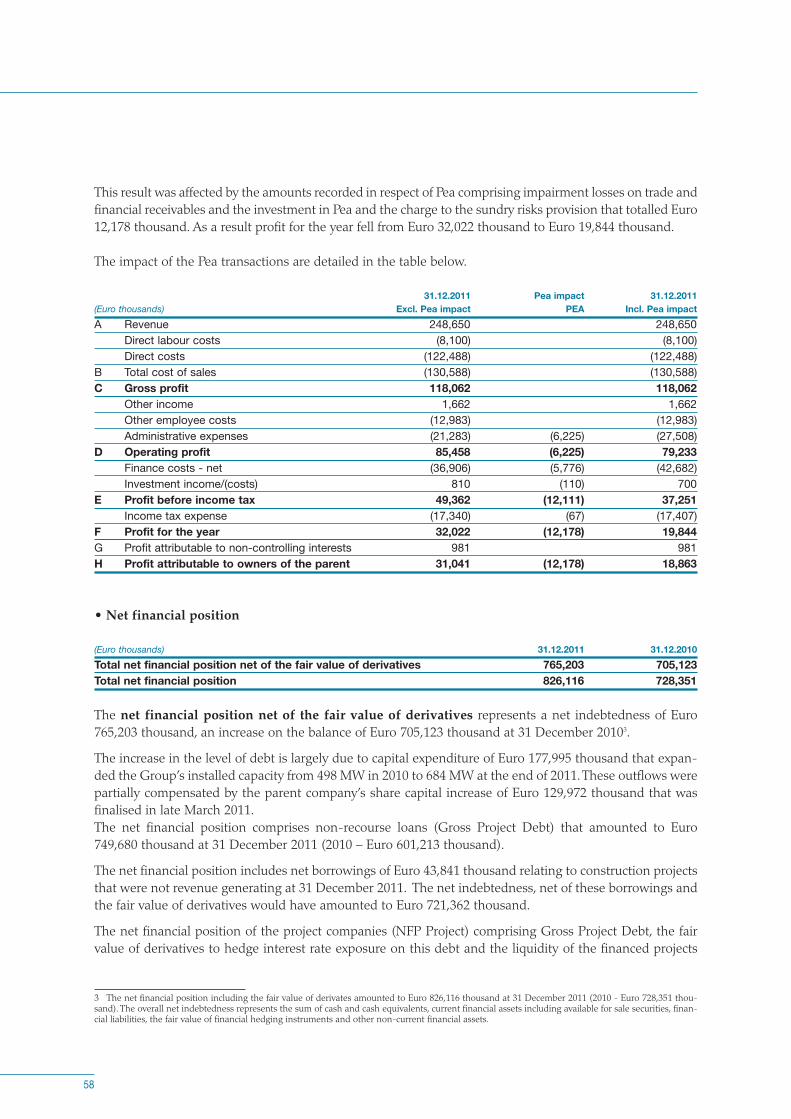

As a consequence, the consolidated results reflect an impairment loss of Euro 110 thousand, net of theamount arising on deconsolidation, recognised against the investment in Pea, an impairment loss of Euro4,015 thousand against trade receivables, an impairment loss recognised against financial receivables due tothe Falck Renewables Group from Pea, net of reversed capitalised interest, of Euro 5,776 thousand and the

Maintenance work on the Rende (Cosenza) biomass plant Control room of the Trezzo sull’Adda (Milan) WtE plant

abovementioned charge of Euro 2,210 thousand to the sundry risks provision. The total impact is Euro12,178 thousand, which is further detailed in the table below.

31.12.2011 Pea impact 31.12.2011(Euro thousands) Excl. Pea impact Incl. Pea impactA Revenue 248,650 248,650

Direct labour costs (8,100) (8,100)Direct costs (122,488) (122,488)

B Total cost of sales (130,588) (130,588)C Gross profit 118,062 118,062

Other income 1,662 1,662 Other employee costs (12,983) (12,983)Administrative expenses (21,283) (6,225) (27,508)

D Operating profit 85,458 (6,225) 79,233 Finance costs - net (36,906) (5,776) (42,682)Investment income/(costs) 810 (110) 700

E Profit before income tax 49,362 (12,111) 37,251 Income tax expense (17,340) (67) (17,407)

F Profit for the year 32,022 (12,178) 19,844 G Profit attributable to non-controlling interests 981 981 H Profit attributable to owners of the parent 31,041 (12,178) 18,863

The Group’s consolidated income tax expense increased on 2010 primarily due to the increase in profit forthe year but also due to the expiry of the tax benefits pursuant to the Tremonti-Ter Law tax that only appliedto the 2009 and 2010 results and contributed Euro 872 thousand in 2010. Electricity producers with morethan Euro 10 million of revenue and Euro 1 million of taxable income are subject to additional IRES (cor-poration tax) of 10.5% for 2011-2013, following which the additional tax will fall to 6.5%. The Group companies affected by the additional tax in 2011 were: Prima Srl, Frullo Energia Ambiente Srl,Eolica Sud Srl and Eolo 3W Minervino Murge Srl.

Moreover, the tax effect of the UK subsidiaries resulted in a Euro 4.6 million reduction in the total tax char-ge, principally due to a decrease in the tax rate (28% to 26.5%) and certain prior year costs (2008 and 2009)now being treated as deductions for tax purposes.

As a result of the above, profit for the year amounted to Euro 19,844 thousand, an increase of Euro 15,201thousand on 2010. The net result was affected by the impairment losses and charge to the sundry risks pro-vision in respect of Pea that totalled Euro 12,178 thousand.

The net financial position, excluding the fair value of derivatives1 was a net indebtedness of Euro765,203 thousand, an increase on the total net indebtedness of Euro 705,123 thousand at 31 December 2010.The increase in the level of debt is largely due to capital expenditure of Euro 177,995 thousand that expan-ded the Group’s installed capacity from 498 MW in 2010 to 684 MW at the end of 2011. These outflows werepartially compensated by the parent company’s share capital increase of Euro 129,972 thousand that wasfinalised in late March 2011. The net financial position comprises non-recourse loans (Gross Project Debt) that amounted to Euro749,680 thousand at 31 December 2011 (2010 – Euro 601,213 thousand).

28

1 The net financial position including the fair value of derivates amounted to Euro 826,116 thousand at 31 December 2011 (2010 - Euro 728,351 thou-sand). The overall net indebtedness represents the sum of cash and cash equivalents, current financial assets including available for sale securities, finan-cial liabilities, the fair value of financial hedging instruments and other non-current financial assets.

29

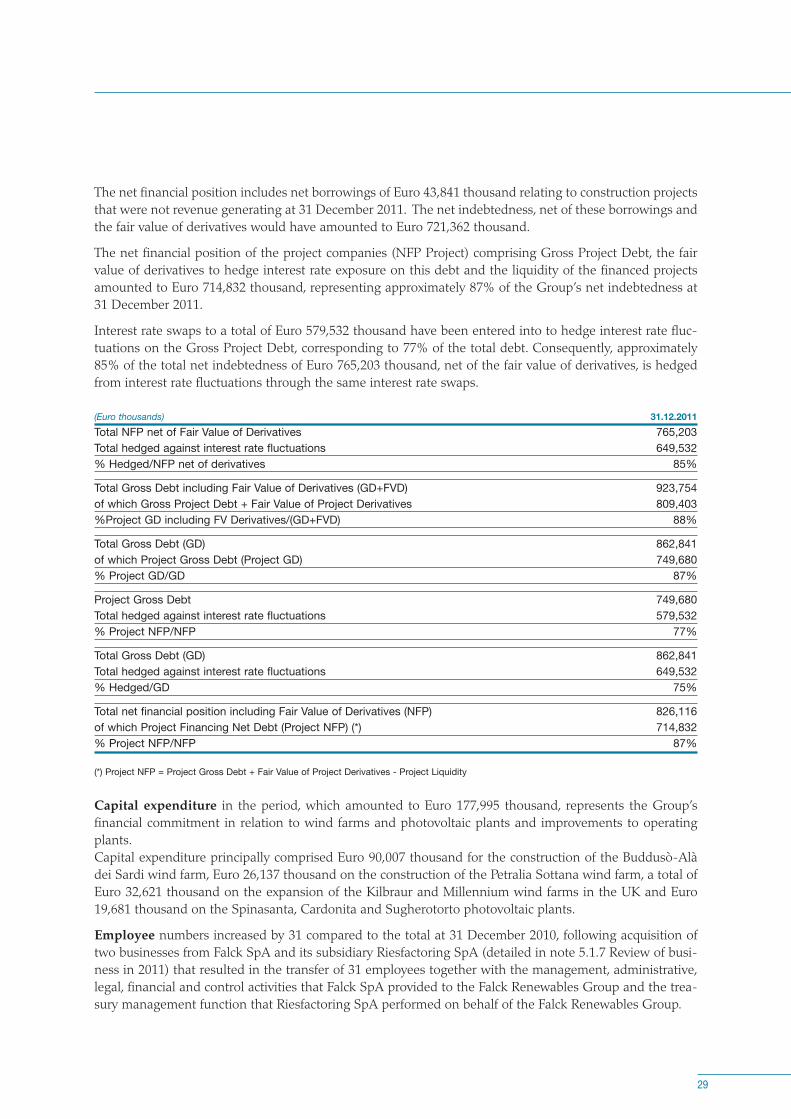

The net financial position includes net borrowings of Euro 43,841 thousand relating to construction projectsthat were not revenue generating at 31 December 2011. The net indebtedness, net of these borrowings andthe fair value of derivatives would have amounted to Euro 721,362 thousand.

The net financial position of the project companies (NFP Project) comprising Gross Project Debt, the fairvalue of derivatives to hedge interest rate exposure on this debt and the liquidity of the financed projectsamounted to Euro 714,832 thousand, representing approximately 87% of the Group’s net indebtedness at31 December 2011.

Interest rate swaps to a total of Euro 579,532 thousand have been entered into to hedge interest rate fluc-tuations on the Gross Project Debt, corresponding to 77% of the total debt. Consequently, approximately85% of the total net indebtedness of Euro 765,203 thousand, net of the fair value of derivatives, is hedgedfrom interest rate fluctuations through the same interest rate swaps.

(Euro thousands) 31.12.2011Total NFP net of Fair Value of Derivatives 765,203Total hedged against interest rate fluctuations 649,532% Hedged/NFP net of derivatives 85%

Total Gross Debt including Fair Value of Derivatives (GD+FVD) 923,754of which Gross Project Debt + Fair Value of Project Derivatives 809,403%Project GD including FV Derivatives/(GD+FVD) 88%

Total Gross Debt (GD) 862,841of which Project Gross Debt (Project GD) 749,680% Project GD/GD 87%

Project Gross Debt 749,680Total hedged against interest rate fluctuations 579,532% Project NFP/NFP 77%

Total Gross Debt (GD) 862,841Total hedged against interest rate fluctuations 649,532% Hedged/GD 75%

Total net financial position including Fair Value of Derivatives (NFP) 826,116of which Project Financing Net Debt (Project NFP) (*) 714,832% Project NFP/NFP 87%

(*) Project NFP = Project Gross Debt + Fair Value of Project Derivatives - Project Liquidity

Capital expenditure in the period, which amounted to Euro 177,995 thousand, represents the Group’sfinancial commitment in relation to wind farms and photovoltaic plants and improvements to operatingplants. Capital expenditure principally comprised Euro 90,007 thousand for the construction of the Buddusò-Alàdei Sardi wind farm, Euro 26,137 thousand on the construction of the Petralia Sottana wind farm, a total ofEuro 32,621 thousand on the expansion of the Kilbraur and Millennium wind farms in the UK and Euro19,681 thousand on the Spinasanta, Cardonita and Sugherotorto photovoltaic plants.

Employee numbers increased by 31 compared to the total at 31 December 2010, following acquisition oftwo businesses from Falck SpA and its subsidiary Riesfactoring SpA (detailed in note 5.1.7 Review of busi-ness in 2011) that resulted in the transfer of 31 employees together with the management, administrative,legal, financial and control activities that Falck SpA provided to the Falck Renewables Group and the trea-sury management function that Riesfactoring SpA performed on behalf of the Falck Renewables Group.

Reconciliation of equity attributable to owners of the parent and profit for the year

The consolidation reserve includes the differences arising from the elimination of the book value of conso-lidated investments against the related share of net equity.As a result the other equity headings correspond to the amounts disclosed in the parent company’s finan-cial statements.

The reconciliation of equity attributable to owners of the parent and profit for the year as at and for the yearended 31 December 2011 may be summarised as follows:

Share capital Profit Equityand reserves for the year attributable to

owners of(Euro thousands) the parentFalck Renewables SpA financial statements 558,412 (1,776) 556,636- Difference between adjusted net equity of consolidated entities

and carrying value of related investments (139,547) 36,114 (103,433)- Reversal of dividends from consolidated entities 15,811 (15,811)- Realised profits on sale of assets between Group companies net

of depreciation and amortisation (8,530) 104 (8,426)- Impairment losses recognised on consolidated equity investments (96) 232 136Group consolidated profit for the year and equity attributable to owners of the parent 426,050 18,863 444,913

5.1.4 Non-financial performance indicators

The key non-financial performance indicators are set out below:

Unit of measurement 31.12.2011 31.12.2010Gross electricity generated MWh 1,560,000 303,745Total waste treated tonn. 339,593 328,646

The total electricity generated in 2010 only includes production for the month of December in respect of thewind sector. Including wind sector production for the entire year would have resulted in gross electricitygenerated of 1,147,000 MWh.

30

31

5.1.5 Share price performance

The performance of the Falck RenewablesSpA share price, which is listed on theSTAR segment, is illustrated below.

The format of communications to sharehol-ders or prospective investors of Falck Rene-wables SpA is based on constant interac-tion and does not necessarily follow that ofpresentations or road shows. Investor rela-tions are in fact principally based on one toone meetings and issuing notices andexplanations even by e-mail or throughtelephone contact. The Company attendsconventions and financial discussions orga-nised by Borsa Italiana, enterprises orfinancial institutions.

Throughout 2011, and in the concludingstages of the share capital increase in thefirst quarter, road show presentations toboth Italian and overseas institutional investors were intensified, complementing the usual meetings withthe financial community aimed at illustrating the key elements of the Group’s business model, comprisingthe management and strategic development of new projects.

Particular care is taken by the Company to ensure that all communications are transparent and timely, alsothrough quarterly earnings conference calls.An effective communication tool available to investors is the website www.falckrenewables.eu, which meetsall of the criteria for companies listed on the STAR segment.

5.1.6 Performance of business sectorsThe Falck Renewables Group operates in the following business sectors:

- The wind sector through Falck Renewables Wind Ltd and its subsidiaries;

- The WtE and waste treatment, biomass and photovoltaic sector.

This paragraph therefore illustrates the principal results of operations, net assets and financial data of theGroup’s two sectors, supported by a brief commentary, while the notes to the financial statements report thefull results of operations and net assets of the sectors with separate disclosure of the amounts relating toFalck Renewables SpA which are commented on in a separate note.

Share price performance

• WtE, biomass and photovoltaic sector

The key financial highlights of this sector may be summarised as follows:

(Euro thousands) 31.12.2011 31.12.2010Revenue 106,216 89,948Cost of sales (66,134) (56,536)Gross profit 40,082 33,412Operating profit 32,748 28,735EBITDA 50,548 45,758Profit for the year 17,671 11,738Profit for the year attributable to owners of the parent 16,638 11,875Invested capital net of provisions 303,521 273,428Total equity 92,057 96,724Net financial position - indebtedness 211,464 176,704of which non-recourse financing 77,797 57,502Capital expenditure 21,789 50,369Employees at the year-end (no.) 134 135

This sector’s profit for the year increased by Euro 5,933 thousand compared to the 2010 result. Revenueincreased by Euro 16,268 thousand, which is largely due to the Rende biomass plant coming on stream fol-lowing its operating at reduced capacity until April 2010 and the subsequent closure to carry out a totalrevamp on the plant, the businesses of Esposito Servizi Ecologici and Ecocentro Soluzioni Ambientali thatwere consolidated in the previous financial statements commencing 1 June 2010, the photovoltaic plants inSicily coming on stream in March 2011 and the strong performance of the Trezzo sull’Adda and Granarolodell’Emilia WtE plants. The incentive tariffs pursuant to point 3 of CIP6/92 attributable to the Trezzo plantexpired in April 2011, while the avoided cost tariff is still in force. Similarly, the incentive element of the tariffin respect of the Granarolo dell’Emilia plant also expired from mid November 2011.

32

Trezzo sull’Adda (Milan) photovoltaic and WtE plants

33

There was marked growth in EBITDA (+ Euro 4,790 thousand), corresponding to 47.6% of revenue (2010 -50.9%).

The net indebtedness increased by Euro 34,760 thousand compared to the balance at 31 December 2010,principally due to capital expenditure on the photovoltaic plants in Sicily that came on stream in March. Thenet financial position comprises Euro 77,797 thousand of non-recourse borrowings.

Capital expenditure in the year amounted to Euro 21,789 thousand and largely related to the photovoltaicplants of Actelios Solar SpA located in Sicily.

• Wind sector

The key financial information for this sector may be summarised as follows:

(Euro thousands) 31.12.2011 31.12.2010Revenue 142,378 8,884Cost of sales (64,861) (5,310)Gross profit 77,517 3,574Operating profit 64,380 1,281EBITDA 101,859 3,934Profit/(loss) for the period 19,452 (2,632)Profit/(loss) for the period attributable to owners of the parent 19,504 (2,618)Invested capital net of provisions 959,960 781,999Total equity 53,411 31,364Net financial position - indebtedness 906,549 750,635of which non-recourse financing 671,883 543,711Capital expenditure 155,336 38,678Employees at the year-end (no.) 42 42

School trip to the Rende (Cosenza) biomass plant

Following the Demerger and Contribution of the wind energy business to Falck Renewables SpA, the con-solidated results of the wind sector for 2010 comprised the period 1.12.2010 - 31.12.2010, as it became partof the Falck Renewables Group in November 2010. Consequently, the results of operations for 2011 and are not comparable with those of 2010, while the stateof affairs and financial position at 31 December 2011 are comparable with those at 31 December 2010.

The consolidated financial statements comprise the results of the wind sector for the full year from 1 January2011 representing a profit for the year of Euro 19,452 thousand, and EBITDA of Euro 101,859 thousand, cor-responding to 71.5% of revenue.

The net indebtedness, which reflects the significant level of investment in wind farms, increased by Euro155,914 thousand compared to 31 December 2010, as did non-recourse borrowings that amounted to Euro671,883 thousand at 31 December 2011, an increase of Euro 128,172 thousand.

Capital expenditure for the year amounted to Euro 155,336 thousand and principally related to the Buddu-sò-Alà dei Sardi and Petralia in Sicily wind farms and the expansion of the Kilbraur and Millennium windfarms in Scotland.

• Sicily projects (Integrated projects for the management and WtE treatment of waste in Sicily)

The Group worked on three projects for the construction and management of integrated WtE plants whichwere to be located in Casteltermini (province of Agrigento) (the “Platani Project”), Augusta (province ofSyracuse) (the “Tifeo Project”) and Bellolampo (province of Palermo) (the “Palermo Project”), to be con-structed by project companies belonging to the Group (together the “Sicily Projects”).

34

Cefn Croes (GB) wind farm Boyndie (GB) wind farm

35

These projects commenced following the declaration of a state of emergency in the waste managementsector in Sicily by the Italian Prime Minister in the Decree dated 22 January 1999, resulting in theappointment of a Commissioner to deal with the emergency on 31 May 1999. Subsequently the Govern-ment identified the possibility of treating the municipal waste generated in the territory of the SicilyRegion using WtE technology, as this provided the opportunity to derive fuel from waste, improving theenergy content of the residual fraction of waste by increasing the dry portion.

Following publication of O.P.C.M. (Ordinance of the Prime Minister) 3190 of 22 March 2002, whichapproved, inter alia, the construction of WtE plants, the Commissioner published an invitation to enterinto conventions with a maximum 20 year duration, for the utilisation of the residual fraction of muni-cipal waste, net of recycled waste, generated in the territory of the Sicily Region pursuant to article 4 ofO.P.C.M. 2983, (subsequently replaced by article 5 of Ordinance 3190/02), with industrial operators thatwere able to treat the residual fraction of waste and recover energy through its use in dedicated WtEplants or industrial plants under their ownership.

At this time Elettroambiente SpA (Elettroambiente), formerly part of the Enel group, together with otherlocal and non-local companies, formed a temporary business association (ATI), in which it acted as leadagent, with the purpose of bidding for public tenders. Enel Produzione SpA (Enel) was also a memberof this ATI as it provided the required financial resources that the other members lacked.

In August 2002, the Company joined a group, with Elettroambiente acting as lead agent, to submit a bidin relation to the above tender for the treatment of waste through WtE for municipalities in the Palermoarea. Subsequently, Elettroambiente and Enel left the group in respect of the Palermo area and Falck SpAtook over as lead agent.

Under the new directive, the Commissioner published calls for tenders on 9 August 2002 that wereawarded on 2 May 2003; in the same month the members of the ATI formed the special-purpose enti-ties Palermo Energia Ambiente ScpA (Pea), Platani Energia Ambiente ScpA (Platani) and Tifeo EnergiaAmbiente ScpA (Tifeo) (hereinafter, the “Industrial Operators”).

On 17 June 2003 each of these project companies executed a 20 year convention with the President ofthe Sicily Region (then the Commissioner appointed by the Italian government to tackle the emergencywaste situation), to utilise the residual fraction of municipal waste, net of recycling, generated in themunicipalities of the Sicily Region as per article 4 of O.P.C.M. 2983, replaced by article 5 of Ordinance3190/02.

Also in 2003, Enel entered into an agreement with Italgest Energia SpA (Italgest) for the sale of Elet-troambiente (the holding company of Platani and Tifeo), and further to this Falck and Italgest executedan agreement on 5 August 2003 for the sale of Elettroambiente to the Company. This provides a brief outline of how the Company came to operate in Sicily from 2003 through the threeproject companies, Pea (23.27% stake), Platani (previously an 85.73% stake increased to 86.77% from 11June 2011, held through Elettroambiente and subject to direction and coordination activities by theCompany) and Tifeo (previously a 95.62% stake increased to 96.35% from 11 June 2011, held throughElettroambiente and subject to direction and coordination activities by the Company), which were incor-porated to construct and operate the Integrated Systems for waste management in Sicily after recycling.

The salient points of the Conventions included the information contained in a number of annexes sum-marising the key financial data and the 20 year business plan that supported the financial viability of theSicily Projects. These annexes expressly envisaged that the Industrial Operators would benefit from theincentives linked to the production of energy from renewable and comparable sources recognised byLaw 9 of 9 January 1991.

In the period between late 2004 and early 2006, the Industrial Operators received all of the authorisa-tions relating to the construction and operation of the plants comprised in the integrated systems andthose relating to emissions to the atmosphere, with work commencing officially in July 2006. A seriesof unforeseeable events that were beyond the control of the Industrial Operators had a significantimpact on the timing of construction work on the WtE plants and on the financial terms of the SicilyProjects and as a consequence on the realisation of the Sicily Projects themselves.

For example, in February 2007 the Industrial Operators were notified of a Joint Ministry Decree suspen-ding the authorisations following which work was suspended (appeals to the Regional AdministrativeCourt (TAR) in Lazio and the ruling issued by the Council of State resulted in cancellation of thesuspension decree); the 2007 Finance Act introduced significant changes to existing legislation creatinguncertainty regarding the continued application of the CIP/6 incentives (it was only at the end of 2008that the TAR in Lazio ruled on the appeals made by the Industrial Operators and declared illegitimatethe silence of the Ministry for Economic Development in relation to the statements filed by the plain-tiffs against the ministry decree on article 1, paragraphs 1117 and 1118 of Law 296/2006 relating to theright to be awarded the incentives under CIP 6/1992). The above events prevented the execution of the project financing contracts essential to the construc-tion of the plants. In a letter dated 21 March 2008 the Regional Department for Waste and Water(ARRA) notified the Industrial Operators that the European Court of Justice had previously passedjudgment on 18 July 2007 (case C-382/05) whereby it found that the Italian Republic had failed to ful-fil its publicity obligations regarding tenders as the Court regarded the Conventions as public servicecontracts rather than service concessions.

The Industrial Operators may not be held responsible for the breach of procedures that led to thesigning of the Conventions. The above-mentioned letters communicated that in order to comply withthis judgment a new call for tenders would be made in order to award the service. ARRA invited theIndustrial Operators to continue carrying out work despite this situation. The requirement to imple-ment the measures established in the judgement passed by the European Court of Justice gave rise toa long and complex negotiation process between the parties in order to identify the appropriatemethods and conditions required to reach a mutual solution to the Conventions.

These negotiations lasted almost a year and were finalised on 28 April 2009 with the execution of anagreement (the Agreement) between ARRA and each of the Industrial Operators and the respectiveshareholders. More precisely it was established that: (i) in the event that no bids were submitted inrelation to the new tender, the Industrial Operators would be required to take part in a “negotiated pro-cedure”, on condition that these procedures were “carried out based on tariffs and operating conditionsin line with those stipulated in the New Call for Tenders, provided that the financial viability of the cur-rent project was preserved” (Agreement art. 3); (ii) in any event the Industrial Operators and their sha-reholders would assign ownership of the Sicily Projects, the authorisations, sites and work carried outby the Industrial Operators and the shareholders against compensation for costs incurred to be certi-fied by an independent advisor (clause 6 of the Agreements). Calls for tenders were issued the follo-wing day (no bids were submitted) and on 23 July 2009 ARRA called for a “negotiated procedure” appl-ying the same terms as those of the call for tenders using open procedures, also inviting the IndustrialOperators.

The Industrial Operators notified ARRA that they were available to attend a meeting however, at thesame time brought to the attention of ARRA the fact that the basis for the negotiated procedure did notallow the financial terms of the Conventions to be met as required under clause 3 of the Agreementsdated 28 April 2009: this was supported by an independent expert opinion (professor Mario Massari ofBocconi University in Milan).

36

37