for the year ended 2014 - veritas · pdf filerepresents an increase of 11% on the forecast...

TRANSCRIPT

FOR THE YEAR ENDED

30 JUNE

2014

Contents

1 S A LV U S S T R A T E G I C I N V E S T M E N T S L I M I T E D A N N U A L R E P O R T 2 0 0 7 1V E R I T A S I N V E S T M E N T S L I M I T E D A N N U A L R E P O R T 2 0 1 4

Chairman’s Repor t

Director Profi les

Corporate Governance Statement

Directors’ Responsibi l i ty Statement

Financial Statements

Independent Auditor’s Repor t

Shareholder and Statutory Information

Corporate Directory

2

3

6

10

11

48

50

58

2 V E R I T A S I N V E S T M E N T S L I M I T E D A N N U A L R E P O R T 2 0 1 4

Chairman’s Report

Dear Shareholders

It is a pleasure to present to you the Annual Report for Veritas Investments Limited for the year ended 30 June 2014. This past year has been the key period for us to deliver on the prospective financial forecasts contained in our Prospectus and Investment Statement issued on 28 March 2013. We were delighted to report our audited FY2014 results on 26 August 2014 and that both the EBITDA and NPAT forecasts had been met. Further, the Board approved a fully imputed dividend at the top end of the policy range. The dividend represents an increase of 11% on the forecast full year dividend.

M A D B U T C H E RAs outlined in our market announcement on 27 February 2014, the unseasonal summer weather resulted in a slower trading period for Mad Butcher. However the year finished strongly with a positive fourth quarter helped by adapting our marketing approach and taking advantage of product opportunities. The business experienced growth with gross margin up on the previous year by 5.4% from $7.4 million to $7.8 million.

We have been pleased with how the Mad Butcher business has responded to various market challenges in the year.

K I W I P A C I F I C F O O D SIn December 2013 we acquired a 50% share in Kiwi Pacific Foods Limited, a joint venture company with Antares Restaurant Group, which operates the New Zealand Burger King franchise. This business produces and supplies meat patties for Burger King and a number of other high profile burger chains, both in New Zealand and internationally. We were pleased to see a positive contribution in the first trading period under our joint ownership and see further potential as markets are developed.

D I V I D E N DFull year dividends of $3.05 million have been approved by the Board against a forecast of $2.66 million. This includes the final dividend of 4.22 cents per share with a record date of 12 September 2014 and payable on 26 September 2014.

S H A R E P R I C EThe Board have been disappointed that Veritas shares have been trading at below issue price during the year despite forecasts being met and other acquisitions being announced. The Board is of the view that the shares have been trading under value at below their issue price. The Board remains focused on increasing shareholder value through improved performance in the Mad Butcher and other acquired businesses, as well as realising synergies between them. At the same time, it is reviewing its capital management strategies, and is reviewing options of buying back shares on market as an accretive move for shareholder value should they continue to trade at under value.

C H I E F F I N A N C I A L O F F I C E R During the year, we added a CFO role to Veritas and were delighted to have Adrienne Roberts join the team. Adrienne has listed company experience as CFO of Charlie’s Group and is a valuable addition to Veritas, especially as we continue to look for more acquisition opportunities.

N O S H F O O D M A R K E TAfter year end results were announced Veritas had confirmed it purchased the Nosh Food Market business from Nosh Management Limited. The new business will trade as Nosh Group Limited. Nosh has a strong brand and revenues, and fits well within our investment mandate. We have bank funding of $5 million to finance the purchase and the required working capital to give the business more impetus.We remain very focused on growing Veritas’ portfolio both organically with our existing businesses and through further acquisitions as the opportunities arise. We would like to thank shareholders and business partners for their on-going support. My personal thanks also go to the Board and staff of Group companies for their contributions to the successful year.

Mark DarrowChairman, Veritas Investments Limited

3V E R I T A S I N V E S T M E N T S L I M I T E D A N N U A L R E P O R T 2 0 1 4

Director Profiles

M A R K D A R R O W BBUS, CA, MINSTD

Independent Chairman

Mark Darrow is an experienced businessman and director, specialising in corporate governance.

Mark has held a number of directorships including Sime Darby Automobiles NZ Limited, Charlie’s Group Limited, Motor Trade Association (MTA), Motor Trade Group Investments Limited, GE Capital New Zealand Funding, the New Zealand Motor Industry Training Organisation (MITO), Vehicle Testing Group (VTNZ) and several private interest companies. He is also a Board Trustee for Macular Degeneration New Zealand (MDNZ). Mark has also held a number of senior executive positions including as Managing Director for Sime Darby New Zealand and Continental Car Services, General Manager of Peugeot New Zealand, Executive Director for GE Money and CEO for PGG Wrightson Finance Limited.

Mark was heavily involved in the 2011 sale of Charlie’s Group Limited to Asahi Group, the mergers of MITO with EXITO and Tranzqual, the sale of PGG Wrightson Finance Limited to Heartland New Zealand Limited, the acquisition of Water Dynamics and Aquaspec by PGG Wrightson and the sale of Vehicle Testing Group to Dekra SE.

Mark chaired the Finance and Audit Committee for Charlie’s Group Limited and MITO and currently chairs the Finance and Audit Committee for Veritas, and for MDNZ. He is Chairman for Kiwi Pacific Foods, a joint venture between Veritas and Antares Restaurant Group. He is also on the Finance and Audit Committee and Governance Committee for the Motor Trade Association.

Mark is a member of the New Zealand Institute of Chartered Accountants and a member of the New Zealand Institute of Directors.

T I M C O O K MINSTD

Non-Executive Director

Tim Cook is Managing Director of Collins Asset Management Limited; an Auckland based private equity and investment company. Collins Asset Management Limited has a number of investments in medical, technology, property, executive recruitment and the motor industry.

Tim has been with Collins Asset Management Limited since 2003, when he was initially a business advisor to the Chairman, and subsequently became a Director and CEO of Primecare Retirement Villages. He then oversaw the sale of that business in 2005, following which the Collins Group became a private equity organisation.

Tim is a director of a number of companies within and outside of the Collins Group. He is a Director of Cook Executive Recruitment Limited and Chairman of Team McMillan BMW Limited, Team MINI Limited and Rolls Royce Motor Cars Auckland. He is also Chairman of SaferSleep NZ Limited, SaferSleep USA and The Heart Institute Limited, New Zealand’s largest private cardiology practice. He is a Director of AHG Associated Practices Limited, MyWave Limited and MyWave Holdings Limited. His earlier management career includes senior retail and operational management roles in the supermarket, retail, franchising, food and fashion industry sectors. He chairs the Remuneration Committee for Veritas and is a member of the Finance and Audit Committee.

From 2006 to 2011 he was a Director of NZX listed Charlie’s Group Limited, representing Collins Asset Management who was the cornerstone shareholder at 19.69%. He was a member of the Finance and Audit Committee and Chairman of the Remuneration Committee. He was heavily involved in its sale to Asahi Group for $129 million in 2011.

4 V E R I T A S I N V E S T M E N T S L I M I T E D A N N U A L R E P O R T 2 0 1 4

DIRECTOR PROFILES CONTINUED

S T E F A N P R E S T O N BE (HONS), MBA (STANFORD)

Independent Director

Stefan has considerable experience with developing businesses and as a director.

Stefan is owner and principal of Ingenio – an active investment company that manages several innovative early-stage companies. Ingenio also consults to other companies primarily in the area of business design and innovation.

In his earlier career as a CEO, Stefan led a number of New Zealand Retail and consumer companies including Pacific Retail Group Limited, Whitcoulls Limited and Bendon Limited. While CEO at Bendon Limited, the company added operations in Europe, North America and the Middle East.

Stefan is also a Director of the Sleepyhead Group, Magic Memories, Flooring Brands and an Advisory Board member to the NZTE Beachheads Program and KEA.

M I C H A E L M O R T O N MBA (MASSEY)

Director

Michael Morton has extensive management experience and over 12 years’ experience as CEO of the Mad Butcher business.

Michael’s first management position was Assistant Manager at Stallone’s Pizza Delivery Company; a South Island based pizza chain which later became Eagle Boys Pizza. He was later appointed Operations Manager of that company.

Michael next worked for PepsiCo as Assistant Manager of KFC and then Operations Manager, before moving to Restaurant Brands New Zealand Limited to become Gene4ral Manager of the Pizza Hut business. In 2000, Michael left Restaurant Brands and joined the Mad Butcher Holdings Limited as CEO under Sir Peter Leitch’s ownership. In 2007, Michael completed the acquisition of the Mad Business Holdings Limited.

Since Michael joined the Mad Butcher business as CEO in 2000, the number of Mad Butcher stores throughout New Zealand has more than doubled to 36.

Following on from the successful acquisition of the Mad Butcher Holdings Limited by Veritas, Michael joined the Board of Veritas as continued his role as CEO of the Mad Butcher.

5V E R I T A S I N V E S T M E N T S L I M I T E D A N N U A L R E P O R T 2 0 1 4

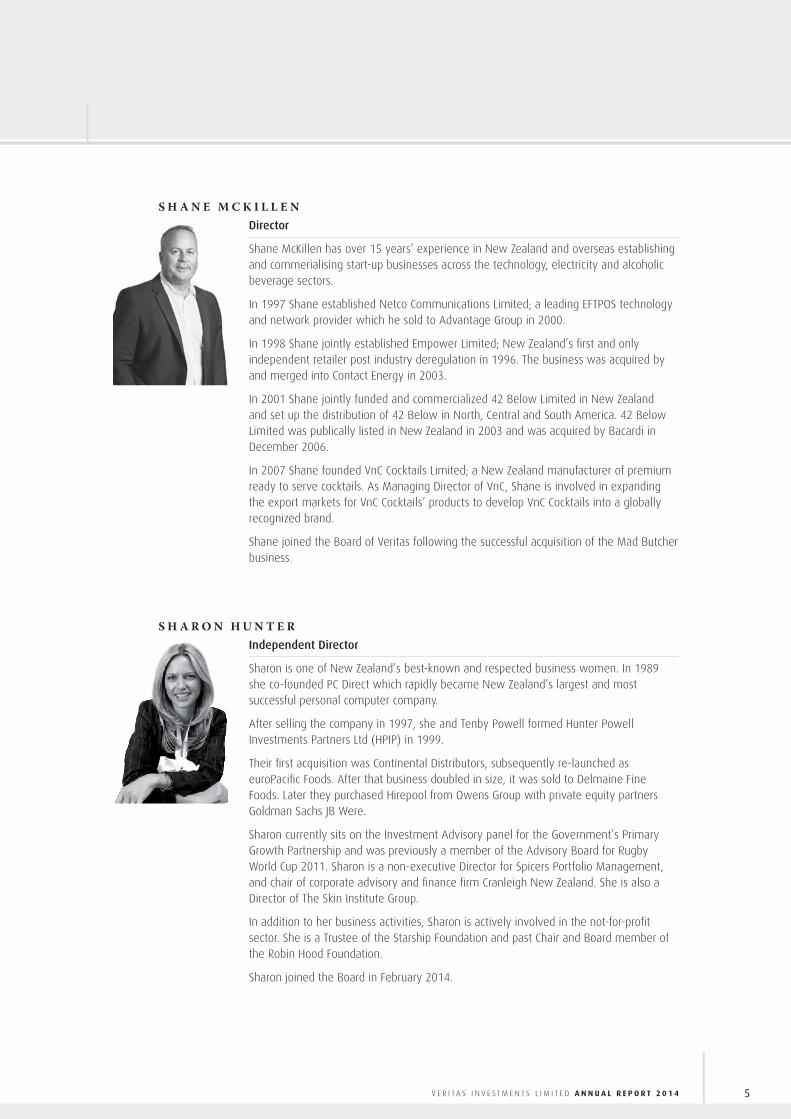

S H A N E M C K I L L E NDirector

Shane McKillen has over 15 years’ experience in New Zealand and overseas establishing and commerialising start-up businesses across the technology, electricity and alcoholic beverage sectors.

In 1997 Shane established Netco Communications Limited; a leading EFTPOS technology and network provider which he sold to Advantage Group in 2000.

In 1998 Shane jointly established Empower Limited; New Zealand’s first and only independent retailer post industry deregulation in 1996. The business was acquired by and merged into Contact Energy in 2003.

In 2001 Shane jointly funded and commercialized 42 Below Limited in New Zealand and set up the distribution of 42 Below in North, Central and South America. 42 Below Limited was publically listed in New Zealand in 2003 and was acquired by Bacardi in December 2006.

In 2007 Shane founded VnC Cocktails Limited; a New Zealand manufacturer of premium ready to serve cocktails. As Managing Director of VnC, Shane is involved in expanding the export markets for VnC Cocktails’ products to develop VnC Cocktails into a globally recognized brand.

Shane joined the Board of Veritas following the successful acquisition of the Mad Butcher business.

S H A R O N H U N T E RIndependent Director

Sharon is one of New Zealand’s best-known and respected business women. In 1989 she co-founded PC Direct which rapidly became New Zealand’s largest and most successful personal computer company.

After selling the company in 1997, she and Tenby Powell formed Hunter Powell Investments Partners Ltd (HPIP) in 1999.

Their first acquisition was Continental Distributors, subsequently re-launched as euroPacific Foods. After that business doubled in size, it was sold to Delmaine Fine Foods. Later they purchased Hirepool from Owens Group with private equity partners Goldman Sachs JB Were.

Sharon currently sits on the Investment Advisory panel for the Government’s Primary Growth Partnership and was previously a member of the Advisory Board for Rugby World Cup 2011. Sharon is a non-executive Director for Spicers Portfolio Management, and chair of corporate advisory and finance firm Cranleigh New Zealand. She is also a Director of The Skin Institute Group.

In addition to her business activities, Sharon is actively involved in the not-for-profit sector. She is a Trustee of the Starship Foundation and past Chair and Board member of the Robin Hood Foundation.

Sharon joined the Board in February 2014.

6 V E R I T A S I N V E S T M E N T S L I M I T E D A N N U A L R E P O R T 2 0 1 4

Corporate Governance Statement

The overall responsibility for ensuring that the Company is properly managed to enhance investor confidence through corporate governance and accountability lies with the Board of Directors.

The Board and Management are committed to ensuring that the Company maintains Corporate Governance structures which ensure that the Company operates efficiently and effectively in shareholders’ best interests.

The Company’s corporate governance processes do not materially differ from the principles set out in NZX’s Corporate Governance Best Practice Code. The Board will continue to monitor best practice in the governance area and update the Company’s policies to ensure it maintains the most appropriate standards.

R O L E A N D C O M P O S I T I O N O F T H E B O A R DThe business and affairs of the Company are managed under the direction of the Board of Directors, which has overall responsibility for decision making within the Company. At a general level, the Board is elected by the shareholders to:

Establish the Company’s objectives;

Develop major strategies for achieving the Company’s objectives;

Approve all material transactions relating to the Group;

Set investment parameters for the manager;

Monitor management’s performance with respect to these matters;

Ensure legislative compliance;

Communicate with shareholders and other stakeholders;

Approve the annual and half-year financial reports.

The Board of Directors currently consists of 3 Independent Directors and 3 Non-Independent Directors who all have a diverse range of experience and expertise (profiles of the individual Directors can be found on page 3-5) and are committed to use this to benefit the Company.

As at 30 June 2014, the Board consisted of:

Mark Darrow Chairman and Independent Director

Stefan Preston Independent Director

Sharon Hunter Independent Director

Tim Cook Director

Michael Morton Director

Shane McKillen Director

Phil Newland ceased to hold office as an Independent Director in October 2013.

A Director is “independent” when he or she does not have any direct or indirect interest or relationship with the Company which could reasonably influence, in a material way, that Director’s decisions relating to the Company. The Board will consider all relevant circumstances when determining independence, but in accordance with NZX Listing Rule, the Board is of the view that a Director cannot be independent where the Director, or an associated person of the Director:

is a substantial security holder in the Company; or

has a relationship with the Company (other than being a Director of the Company) under which the Director or associated person is likely to derive a substantial portion (generally 10% or more) of their annual revenue or income from the Company.

Q U A N T I T A T I V E B R E A K D O W N O F D I R E C T O R S A N D O F F I C E R S

As at As at 30 June 2014 30 June 2013Male 5 6Female 2 0TOTAL 7 6

N O M I N A T I O N A N D A P P O I N T M E N T O F D I R E C T O R SThe Board is responsible for identifying and recommending candidates. Directors may also be nominated by shareholders under NZX Listing Rule 3.3.5.

7V E R I T A S I N V E S T M E N T S L I M I T E D A N N U A L R E P O R T 2 0 1 4

A Director may be appointed by ordinary resolution and all Directors are subject to removal by ordinary resolution.

The Board may at any time appoint additional Directors. A Director appointed by the Board shall only hold office until the next annual meeting of the Company but shall be eligible for election at that meeting.

The procedures for the appointment and removal of Directors are governed by the Company’s constitution. The constitution provides for one third of the Company’s Directors (rounded down to the nearest whole number) to retire and stand for re-election at every Annual General Meeting. The Directors who must retire are those who have been in office the longest since last elected or deemed to be elected.

Any increase in the total Directors’ remuneration is approved by shareholders at the Company’s Annual Shareholders’ Meeting, upon the recommendation of the Board as a whole. Within that cap, the Board is responsible for determining the remuneration paid to each Director.

D I S C L O S U R E O F I N T E R E S T S B Y D I R E C T O R SThe Companies Act 1993 sets out the procedures to be followed where Directors have an interest in a transaction of proposed transaction or are faced with a potential conflict of interest requiring the disclosure of that conflict to the Board.

Veritas maintains an Interest Register that contains all the relevant and material directorships held by the members of the Board. Entries in the Interests Register made in the financial year ended 30 June 2014 are shown on pages 54 – 57.

E T H I C A L C O N D U C TThe Company has adopted a Code of Conduct, which sets out the ethical and behavioural standards expected of Veritas’ Directors and employees. The Code of Conduct outlines the Company’s policies in respect of conflicts of interest, competing corporate opportunities, maintaining confidentiality of information, acceptance of gifts and compliance

with laws and Company policies. Procedures for dealing with breaches of these policies are contained within the Code of Conduct, which forms part of each employee’s conditions of employment.

S H A R E D E A L I N G SVeritas’ Directors and employees must comply with the Company’s Securities Trading Policy and Procedures, to ensure that no trades in shares are effected whilst that person is in possession of material information which is not generally available to the market.

I N D E M N I F I C A T I O N A N D I N S U R A N C E O F D I R E C T O R S A N D O F F I C E R SThe Company has D&O insurance with Vero which ensures that generally, Directors and Officers will incur no monetary loss as a result of actions undertaken by them. The Company entered into an indemnity in favour of its Directors and Officers under a policy dated the 8th of May 2013 for the purpose of section 162 of the Companies Act 1993.

S H A R E H O L D E R R E L A T I O N SThe Company is committed to providing comprehensive and timely information to its shareholders. Shareholders are encouraged to participate in annual meetings and the Company encourages queries from shareholders outside formal meetings.

B O A R D P R O C E S S E SThe Board (past and current members) met formally 13 times for the financial year ended 30 June 2014 for the purpose of reviewing the progress of the Company, approving communications with shareholders and the maintenance of all internal procedures and governance.

These formal meetings included discussions relating to the Investment, Finance and Audit, and Remuneration Committees. There were a number of informal meetings throughout the financial year, but these are not included in the table overleaf.

8 V E R I T A S I N V E S T M E N T S L I M I T E D A N N U A L R E P O R T 2 0 1 4

Board Members Meetings Attended

Mark Darrow, Chairman 13Tim Cook 13Shane McKillen 13Michael Morton 12Stefan Preston 11Sharon Hunter (appointed February 2014) 6Phil Newland (resigned October 2013) 4

C O M M I T T E E SThe Board has 3 formally constituted committees. These committees, established by the Board, review and analyse policies and strategies as developed by the Board. The committees examine proposals and, where appropriate, make recommendations to the Board. Committees do not take action or make decisions on behalf of the Board unless specifically authorised to do so by the Board.

Finance and Audit CommitteeThe Company’s Finance and Audit Committee has been established to monitor audit and risk management processes (including treasury and financing policies). It specifically ensures adequate financial reporting and regulatory conformance. The committee is accountable to the Board for considering and, if necessary or desirable, adopting the recommendations of the external Auditor and addressing the adequacy of the external audit function.

The committee provides the Board with additional assurance regarding the accuracy of financial information for inclusion in the Group’s annual report, including all financial information released through NZX.

The Company utilises the accounting and administration services of Collins Asset Management (associated with Tim Cook) under the management of Mark Darrow (Chairman). A number of the Board

meetings incorporated Finance and Audit Committee discussions. For the financial year ended 30 June 2014, the Finance and Audit Committee had 3 formal meetings. These formal meetings are intended to continue for the financial year ending 30 June 2015.

Finance and Audit Meetings Committee Members Attended

Mark Darrow, Chairman 3Tim Cook 3Sharon Hunter (appointed February 2014) 1Phil Newland (resigned October 2013) 1

PricewaterhouseCoopers has provided the Company with taxation and accounting advice. KPMG has provided the Company with taxation advice in addition to its services as external Auditor. Notwithstanding this, the Company is currently satisfied with KPMG’s independence and the quality of the audit it provides.

The Company has adopted an External Financial Auditor’s Independence Policy designed to ensure the independence of its external financial auditors.

KPMG have undertaken the audit of the financial statements for the year ended 30 June 2014.

Investment CommitteeThe Board has a separate Investment Committee. A number of the Board meetings incorporated Investment Committee discussions. For the financial year ended 30 June 2014, the Investment Committee had 7 formal meetings. These formal meetings are intended to continue for the financial year ending 30 June 2015.

Investment Committee Meetings Members Attended

Stefan Preston, Chairman 7Michael Morton 7Shane McKillen (appointed February 2014) 3Phil Newland (resigned October 2013) 2

CORPORATE GOVERNANCE STATEMENT CONTINUED

9V E R I T A S I N V E S T M E N T S L I M I T E D A N N U A L R E P O R T 2 0 1 4

Remuneration CommitteeThe Remuneration Committee is responsible for overseeing management succession planning, establishing employee incentive schemes, reviewing and approving the compensation arrangements for the Executive Directors and senior management and recommending to the full Board the remuneration of Directors. A number of the Board meetings incorporated Remuneration Committee discussions. For the year ended 30 June 2014, the Remuneration Committee had no formal meetings. It has been agreed that these formal meetings will be held as and when required.

Members of the Remuneration Committee are Tim Cook (Chairman), Mark Darrow and Shane McKillen.

M A N A G I N G R I S KThe Board has overall responsibility for the company system of risk management and internal control and has procedures in place to provide effective control within the management and reporting structure. The Board has in place policies and procedures to identify significant business risks and to implement procedures for effectively managing those risks. Key risk management tools used by Veritas include the Finance and Audit Committee and Investment Committee functions, outsourcing of certain functions to experts, internal controls, financial and compliance reporting procedures and adequate insurance cover.

Management Reports are prepared monthly and reviewed by the Board to monitor performance against budget goals and objectives. The Board also requires management to identify and respond to risk exposures.

A structure framework is in place for capital expenditure, including appropriate authorisations and approval levels.

The Board maintains an overall view of the risk profile of the Company and is responsible for monitoring corporate risk assessment processes.

D I S C L O S U R EThe Company adheres to the NZX continuous disclosure requirements which govern the release of all material information that may affect the value of the Company’s listed shares. The Board and senior management team have processes in place to ensure that all material information is promptly provided to the Chairman and disclosed to the market as appropriate.

10 V E R I T A S I N V E S T M E N T S L I M I T E D A N N U A L R E P O R T 2 0 1 4

The Board of Directors have pleasure in presenting the financial statements and audit report for Veritas Investments Limited for the year ended 30 June 2014.

The Directors are responsible for presenting financial statements in accordance with New Zealand law and generally accepted accounting practice, which give a true and fair view of the financial position of the Group as at 30 June 2014, and the result of the Group’s operations and cash flows for the period ended on that date.

The Directors believe that proper accounting records have been kept which enable with reasonable accuracy, the determination of the financial position of the Group and facilitate compliance with the Financial Reporting Act 1993.

The Directors consider that they have taken adequate steps to safeguard the assets of the Group and to prevent and detect fraud and other irregularities. Internal control procedures are also considered to be sufficient to provide a reasonable assurance as to the integrity and reliability of the financial statements.

The Board of Directors of the Group authorised these financial statements presented on pages 12 to 47 for issue on 25 August 2014.

For and on behalf of the Board

Mark DarrowChairman, Veritas Investments Limited Finance and Audit Committee Chairman

Directors’ Responsibility Statement

11V E R I T A S I N V E S T M E N T S L I M I T E D A N N U A L R E P O R T 2 0 1 4 21 S A LV U S S T R A T E G I C I N V E S T M E N T S L A N N U A L R E P O R T 2 0 0 7

Financial Statements

S t a t e m e n t o f C o m p r e h e n s i v e I n c o m e 1 2

S t a t e m e n t o f F i n a n c i a l P o s i t i o n 1 3

S t a t e m e n t o f C h a n g e s i n E q u i t y 1 4

S t a t e m e n t o f C a s h F l o w s 1 6

N o t e s t o t h e F i n a n c i a l S t a t e m e n t s 1 7

I n d e p e n d e n t A u d i t o r ’ s R e p o r t 2 5

11V E R I T A S I N V E S T M E N T S L I M I T E D A N N U A L R E P O R T 2 0 1 4

12 V E R I T A S I N V E S T M E N T S L I M I T E D A N N U A L R E P O R T 2 0 1 4

Revenue 4 29,972,494 29,865,428 7,292 -

Expenses Carcass purchases 19,276,627 20,110,286 - - Advertising & marketing costs 2,866,918 2,376,963 - - Employee benefits expense 943,131 553,180 - - Other expenses 7 1,168,479 919,076 452,964 1,277,129 Depreciation & amortisation expense 10 68,530 102,238 - - (24,323,685) (24,061,743) (452,964) (1,277,129)

Other operating income 162,326 - - - Share of joint venture’s profit, net of tax 11.1 250,554 - - - Dividend from subsidiary - - 1,800,000 - Operating profit / (loss) 6,061,689 5,803,685 1,354,328 (1,277,129)

Finance income / (expense) - net 8 39,525 (110,355) 51,425 12,458 Other gains - 30,469 631,344 82,400 Non-trading transaction impact 7 - (4,800,506) - -

Profit / (loss) before income tax 6,101,214 923,293 2,037,097 (1,182,271)

Income tax expense 13 (1,611,783) (1,770,634) - -

Total comprehensive income / (loss) for the period from continuing operations 4,489,431 (847,341) 2,037,097 (1,182,271)

Net loss from operations held for sale 6 (136,012) - - -

TOTAL COMPREHENSIVE INCOME / (LOSS) FOR THE PERIOD 4,353,419 (847,341) 2,037,097 (1,182,271)

Earnings per Share (cents per share) 15 12.09 (4.56) (basic and diluted)

Statement of Comprehensive Income

FOR THE YEAR ENDED 30 JUNE 2014

2014note

2013VERITAS

The accompanying notes form part of and should be read in conjunction with the Financial Statements.

2014 2013GROUP

13V E R I T A S I N V E S T M E N T S L I M I T E D A N N U A L R E P O R T 2 0 1 4

Statement of Financial Position

The accompanying notes form part of and should be read in conjunction with the Financial Statements.

AS AT 30 JUNE 2014

20142014note

20132013GROUP VERITAS

ASSETSCash and cash equivalents 19 3,995,014 2,837,307 2,567,277 1,984,784 Restricted cash 19 75,000 75,000 75,000 75,000 Trade and other receivables 9 2,150,090 1,193,300 116,530 130,309 Assets from operations held for sale 6 416,357 - - - Total current assets 6,636,461 4,105,607 2,758,807 2,190,093

Property plant and equipment 10 108,591 101,734 - - Intangibles - computer software 10 64,517 31,255 - - Investments in subsidiaries 11 - - 43,450,155 39,938,375 Investments in joint venture 11.1 3,762,334 - - - Total non-current assets 3,935,442 132,989 43,450,155 39,938,375 TOTAL ASSETS 10,571,903 4,238,596 46,208,962 42,128,468

LIABILITIES Trade and other payables 12 1,669,581 1,502,587 469,923 355,238 Income tax payable 13 22,296 265,941 - - Liabilities from operations held for sale 6 127,827 - - - Total current liabilities 1,819,704 1,768,528 469,923 355,238

Borrowings 19 2,800,000 - 2,800,000 - TOTAL LIABILITIES 4,619,704 1,768,528 3,269,923 355,238 Net Assets / (Net Liabilities) 5,952,199 2,470,068 42,939,039 41,773,230

EQUITY Share capital 14 27,555,187 26,955,187 50,458,434 49,858,434 Retained earnings (21,602,988) (24,485,119) (7,519,395) (8,085,204)TOTAL EQUITY 5,952,199 2,470,068 42,939,039 41,773,230

For and on behalf of the Board of Directors, who authorised these Financial Statements for issue on 25 August 2014:

Mark Darrow Michael MortonChairman Director

14 V E R I T A S I N V E S T M E N T S L I M I T E D A N N U A L R E P O R T 2 0 1 4

FOR THE YEAR ENDED 30 JUNE 2014

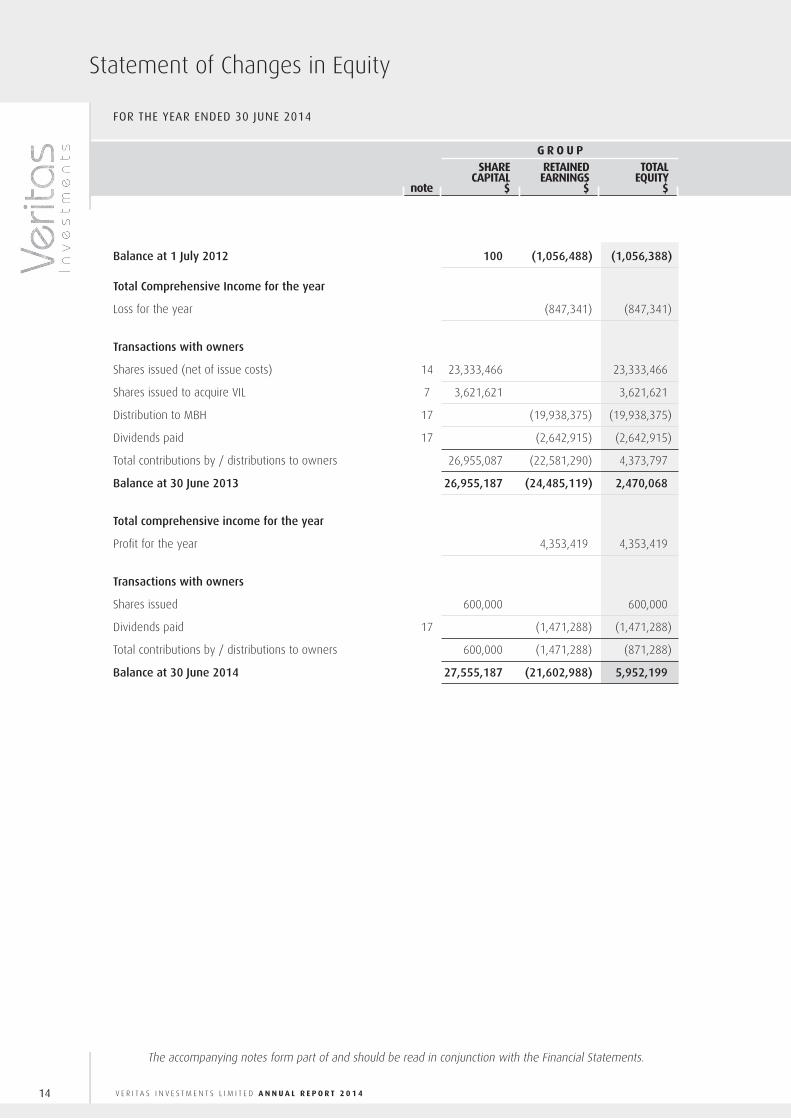

Statement of Changes in Equity

The accompanying notes form part of and should be read in conjunction with the Financial Statements.

RETAINED EARNINGS

$SHARE

CAPITAL $

TOTAL EQUITY

$

G R O U P

note

Balance at 1 July 2012 100 (1,056,488) (1,056,388)

Total Comprehensive Income for the year Loss for the year (847,341) (847,341)

Transactions with owners Shares issued (net of issue costs) 14 23,333,466 23,333,466 Shares issued to acquire VIL 7 3,621,621 3,621,621 Distribution to MBH 17 (19,938,375) (19,938,375)Dividends paid 17 (2,642,915) (2,642,915)Total contributions by / distributions to owners 26,955,087 (22,581,290) 4,373,797 Balance at 30 June 2013 26,955,187 (24,485,119) 2,470,068

Total comprehensive income for the year Profit for the year 4,353,419 4,353,419

Transactions with owners Shares issued 600,000 600,000 Dividends paid 17 (1,471,288) (1,471,288)Total contributions by / distributions to owners 600,000 (1,471,288) (871,288)Balance at 30 June 2014 27,555,187 (21,602,988) 5,952,199

15V E R I T A S I N V E S T M E N T S L I M I T E D A N N U A L R E P O R T 2 0 1 4

The accompanying notes form part of and should be read in conjunction with the Financial Statements.

RETAINED EARNINGS

$SHARE

CAPITAL $

TOTAL EQUITY

$

V E R I T A S

note

STATEMENT OF CHANGES IN EQUITY CONTINUED

Balance at 1 July 2012 7,511,571 (6,902,933) 608,638

Total Comprehensive Income for the year Loss for the year - (1,182,271) (1,182,271)

Transactions with owners Shares issued (net of issue costs) 14 42,346,863 - 42,346,863 Shares issued to acquire VIL 7 - - - Distribution to MBH 17 - - - Dividends paid 17 - - - Total contributions by / distributions to owners 42,346,863 - 42,346,863 Balance at 30 June 2013 49,858,434 (8,085,204) 41,773,230

Total comprehensive income for the year Profit for the year - 2,037,097 2,037,097

Transactions with owners Shares issued 600,000 - 600,000 Dividends paid 17 - (1,471,288) (1,471,288)Total contributions by / distributions to owners 600,000 (1,471,288) (871,288)Balance at 30 June 2014 50,458,434 (7,519,395) 42,939,039

16 V E R I T A S I N V E S T M E N T S L I M I T E D A N N U A L R E P O R T 2 0 1 4

The accompanying notes form part of and should be read in conjunction with the Financial Statements.

Statement of Cash Flows

FOR THE YEAR ENDED 30 JUNE 2014

20142014note

20132013GROUP VERITAS

Cash from customers 29,196,687 29,776,384 671,071 82,400 Cash paid to suppliers and employees (23,817,770) (25,669,102) (338,279) (1,138,697)Interest / dividends received 108,861 11,861 1,893,537 12,458 Interest paid (87,992) (121,747) (60,768) - Tax (paid) / refunded (1,855,428) (881,000) - 2,468 Discontinued operations - operating casflows (116,268) - - -

Net cash from / (used in) operating activities 22 3,428,090 3,116,396 2,165,561 (1,041,371)

Purchase of property plant and equipment (PPE) (20,964) - - - Discontinued operations - investing casflows (361,167) - - - Investment acquisition costs (2,911,780) - (2,911,780) (39,938,375)

Net cash from / (used in) investing activities (3,293,911) - (2,911,780) (39,938,375)

Proceeds from share issue - 23,333,466 - 42,285,237 Dividend to Vendor - purchase of Mad Butcher Business - (19,938,375) - - Dividend paid (1,471,288) (2,642,915) (1,471,288) - Bank borrowings drawn / (repaid) 2,800,000 (1,060,000) 2,800,000 - Franchisee advances (made) / repaid (305,184) 20,000 - -

Net cash from / (used in) financing activities 1,023,528 (287,824) 1,328,712 42,285,237 Net increase in cash and cash equivalents 1,157,707 2,828,572 582,493 1,305,491 Cash and cash equivalents at beginning of period 2,912,307 83,735 2,059,784 692,668 Cash and cash equivalents at end of period 4,070,014 2,912,307 2,642,277 1,998,159 Cash and bank balances 3,995,014 2,837,307 2,567,277 1,909,784 Restricted cash 75,000 75,000 75,000 75,000 4,070,014 2,912,307 2,642,277 1,984,784

17V E R I T A S I N V E S T M E N T S L I M I T E D A N N U A L R E P O R T 2 0 1 4

Notes to the Financial Statements

FOR THE YEAR ENDED 30 JUNE 2014

1 . G E N E R A L I N F O R M A T I O N1.1 Reporting entity

Veritas Investment Limited (“Veritas”, or the “Company”) is a company incorporated and domiciled in New Zealand, registered under the Companies Act 1993 and listed on the NZX Main Board operated by NZX Limited (“NZX”). The Company is an issuer in terms of the Financial Reporting Act 1993.

Financial statements for Veritas (separate financial statements) and consolidated financial statements are presented. The consolidated financial statements of the Company as at and for the year ended 30 June 2014 comprise the Company, its subsidiaries Mad Butcher Limited (“MBL”), Midas Foods Limited (“MFL”) and Kiwi Choice Limited (“KCL”), and its joint venture Kiwi Pacific Foods Limited (“KPF”), together referred to as the “Group”.

The Group is engaged in coordinating the national marketing and product procurement for the individual Mad Butcher franchises, as well as providing support for the franchisees, and in the manufacturing of burger patties for the domestic and export markets.

1.2 Basis of preparationMBL is the wholly-owned subsidiary of Veritas which was specifically incorporated for the purpose of acquiring the Mad Butcher Business (the “Business”). The Business is as defined in the Sale and Purchase Agreement whereby MBL acquired the Mad Butcher franchisor business and assets previously owned and operated by a separate and unrelated reporting entity, MBH Limited (“MBH”).

For financial reporting purposes, aspects of “reverse acquisition” accounting are relevant and the rules require that the Mad Butcher Business is treated as the acquirer of Veritas. The consolidated financial statements prepared following a “reverse acquisition” are issued under the name of the legal parent (Veritas) but described in the notes as a continuation of the financial statements of the Mad Butcher Business. Given that this was the acquisition of a business, MBL’s financial statements will be those of the Mad Butcher Business.

Therefore, the consolidated financial information provided for the year ended 30 June 2014 reflects 12 months of trading of the Mad Butcher Business plus Veritas, plus 7 months of trading for Midas Foods and Kiwi Choice, plus 7 months of trading for Kiwi Pacific Foods on an equity-accounting basis. The consolidated financial information provided for the comparative year ended 30 June 2013 reflects 12 months of trading from the Mad Butcher Business, plus Veritas trading from 8 May to 30 June 2013.

The financial statements of the Mad Butcher Business for the year ended 30 June 2013 have been extracted from the financial statements and the accounting records of MBH for the year ended 31 March 2013, and of MBH and MBL for the period ended 30 June 2013, and exclude certain income and expenses transactions, specific assets and liabilities recorded by MBH on the basis that they are not related to the Business (note 2.3). There have been no allocations of income, expenses, assets or liabilities in determining the components to be excluded. The adjustments required to exclude these transactions and balances are presented as distributions (dividends paid) to owner within equity.

These consolidated financial statements meet the definition of “combined financial statements” and have been prepared for the reporting periods stated to represent the continuation of the Mad Butcher Business after the acquisition of the Business described above.

These financial statements have been prepared on a historical cost basis.

18 V E R I T A S I N V E S T M E N T S L I M I T E D A N N U A L R E P O R T 2 0 1 4

1 . G E N E R A L I N F O R M A T I O N ( c o n t i n u e d )The principal accounting policies adopted in the preparation of the financial statements are selected and applied in a manner which ensures that the resulting financial information satisfies the concepts of relevance and reliability, thereby ensuring that the substance of the underlying transaction and other events is reported. These policies have been consistently applied to all the periods presented, unless otherwise stated.

1.3 Statement of complianceThe financial statements have been prepared in accordance with New Zealand Generally Accepted Accounting Practice (“GAAP”) and the requirements of the Companies Act 1993 and the Financial Reporting Act 1993. They comply with New Zealand equivalents to International Financial Reporting Standards (“NZ IFRS”) and other applicable Financial Reporting Standards, as appropriate for profit oriented entities.

The financial statements also comply with International Financial Reporting Standards (“IFRS”).

The financial statements were authorised for issue by the Board of Directors on 25 August 2014.

1.4 Critical accounting judgements and key sources of estimation uncertaintyIn the application of the Group’s accounting policies, the directors are required to make judgements, estimates and assumptions about the carrying amounts of assets and liabilities that are not readily apparent from other sources. The estimates and associated assumptions are based on historical experience and other factors that are considered to be relevant. Actual results may differ from these estimates.

The estimates and underlying assumptions are reviewed on an on-going basis. Revisions to accounting estimates are recognised in the period in which the estimate is revised if the revision affects only that period, or in the period of the revision and future periods if the revision affects both current and future periods.

Critical judgements in applying accounting policiesThe following are the judgements, apart from those involving estimation, that the directors have made in the process of applying the Group’s accounting policies and that have the most significant effect on the amounts recognised in these financial statements:

The exclusions applied above are consistent with the treatment of such expenses / income and assets / liabilities in the Prospective Financial Information for FY2013 and FY2014 presented in the Investment Statement and Prospectus dated 28 March 2013.

Equity is the residual after excluding the above transactions and balances. They have been included within distribution to owner in the Statement of Cash Flows.

1.5 Functional and presentation currencyBoth the functional and presentation currency of the Company is New Zealand Dollars ($). Transactions in foreign currencies are initially recorded in the functional currency by applying the exchange rates ruling at the date of the transaction. Monetary assets and liabilities denominated in foreign currencies are re-translated at the exchange rate at balance date. Non-monetary items that are measured in terms of historical cost in a foreign currency are translated using the exchange rate as at the date of the initial transaction.

NOTES TO THE FINANCIAL STATEMENTS CONTINUED

19V E R I T A S I N V E S T M E N T S L I M I T E D A N N U A L R E P O R T 2 0 1 4

2 . S U M M A R Y O F S I G N I F I C A N T A C C O U N T I N G P O L I C I E S

2.1 ConsolidationThe consolidated financial statements incorporate the financial statements of the Company and entities controlled by the Company (its subsidiaries) as at the reporting date, as modified by the “reverse acquisition” rules explained in Note 1 above. Control is achieved when the Company is exposed, or has rights, to variable returns from its involvement with the investee and has the ability to affect those returns through its power to direct the activities of the investee.

Subsidiaries are included in the consolidated financial statements using the acquisition method of consolidation. Where necessary, adjustments are made to the financial statements of subsidiaries to bring their accounting policies into line with those used by other members of the Group. Investments in subsidiaries are recorded at cost less any impairment in the Company’s financial statements. All intra-group transactions, balances, income and expenses are eliminated in full on consolidation.

The results of entities acquired or disposed of during the year are included in the profit or loss from the effective date of acquisition or up to the effective date of disposal, as appropriate.

2.2 Acquisitions / business combinations / joint venture / goodwillAs explained in Note 1, under “reverse acquisition” accounting the Business is treated as the acquirer of Veritas. Under these rules, the difference between the market capitalisation of Veritas as at the transaction date immediately prior to completion of the acquisition of the Business and the net assets of Veritas at that same time is a share-based payment (included in the “non-trading transaction impact” expense). Accordingly, the acquisition of the Business does not give rise to any goodwill to be carried at cost (less impairment losses) on the Consolidated Statement of Financial Position.

In the year ended 30 June 2014, Veritas acquired Midas Foods Limited (“MFL”) and Kiwi Choice Limited (“KCL”), both with effect from 1 December 2013.

MFL’s main asset is a 50% shareholding in Kiwi Pacific Foods Limited (“KPF”), a joint venture with Antares Restaurant Group (“ARG”), owner and operator of the Burger King restaurant chain in New Zealand. Veritas (through MFL) includes 50% of KPF’s results as from 1 December 2013 under the equity accounting method.

KCL’s main asset is a contract to manage KPF, under which KCL is remunerated by a percentage of KPF’s gross turnover.

The investment in KPF is held at cost by the investor, and interest in KPF is accounted for using the equity method in the consolidated financial statements.

Acquisitions of businesses are accounted for using the acquisition method. The consideration transferred in a business combination is measured at fair value, which is calculated as the sum of the acquisition-date fair values of the assets transferred by the Group, liabilities incurred by the Group to the former owners of the acquiree and the equity interests issued by the Group in exchange for control of the acquiree.

Goodwill is measured as the excess of the sum of the consideration transferred, the amount of any non-controlling interests in the acquiree, and the fair value of the acquirer’s previously held equity interest in the acquiree (if any) over the net of the acquisition-date amounts of the identifiable assets acquired and the liabilities assumed. If, after reassessment, the net of the acquisition-date amounts of the identifiable assets acquired and liabilities assumed exceeds the sum of the consideration transferred, the amount of any non-controlling interests in the acquiree and the fair value of the acquirer’s previously held interest in the acquiree (if any), the excess is recognised immediately in profit or loss as a bargain purchase gain.

20 V E R I T A S I N V E S T M E N T S L I M I T E D A N N U A L R E P O R T 2 0 1 4

2 . S U M M A R Y O F S I G N I F I C A N T A C C O U N T I N G P O L I C I E S ( c o n t i n u e d )When the consideration transferred by the Group in a business combination includes assets or liabilities resulting from a contingent consideration arrangement, the contingent consideration is measured at its acquisition-date fair value and included as part of the consideration transferred in a business combination.

Changes in the fair value of the contingent consideration that qualify as measurement period adjustments are adjusted retrospectively, with corresponding adjustments against goodwill. Measurement period adjustments are adjustments that arise from additional information obtained during the ‘measurement period’ (which cannot exceed one year from the acquisition date) about facts and circumstances that existed at the acquisition date.

The subsequent accounting for changes in the fair value of the contingent consideration that do not qualify as measurement period adjustments depends on how the contingent consideration is classified. Contingent consideration that is classified as equity is not remeasured at subsequent reporting dates and its subsequent settlement is accounted for within equity. Contingent consideration that is classified as an asset or a liability is remeasured at subsequent reporting dates in accordance with NZ IAS 39 – Financial Instruments: Recognition and Measurement, or NZ IAS 37 – Provisions, Contingent Liabilities and Contingent Assets, as appropriate, with the corresponding gain or loss being recognised in profit or loss.

When a business combination is achieved in stages, the Group’s previously held equity interest in the acquiree is remeasured to fair value at the acquisition date (i.e. the date when the Group obtains control) and the resulting gain or loss, if any, is recognised in profit or loss. Amounts arising from interests in the acquiree prior to the acquisition date that have previously been recognised in other comprehensive income are reclassified to profit or loss where such treatment would be appropriate if that interest were disposed of.

If the initial accounting for a business combination is incomplete by the end of the reporting period in which the combination occurs, the Group reports provisional amounts for the items for which the accounting is incomplete. Those provisional amounts are adjusted during the measurement period (see above), or additional assets or liabilities are recognised, to reflect new information obtained about facts and circumstances that existed at the acquisition date that, if known, would have affected the amounts recognised at that date.

2.3 Revenue recognitionRevenue comprises the fair value of the consideration received or receivable for the sale of goods and services, excluding Goods and Services Tax, rebates and discounts, to the extent that it is probable that the economic benefits will flow to the Group and the amount of the revenue can be reliably measured.

Sales of carcasses - The Business acts as principal for the sale of beef carcasses. Revenue from the sale of carcasses is recognised when the carcasses are received by the franchise stores.

Supplier rebates revenue - The Business acts as an agent for the sale of poultry, pork, lamb and beef products. Supplier rebates on these products are recognised as revenue when the goods are received by the franchise stores.

Advertising income and franchise fees - Contracted annual advertising charges and franchise fees are recognised on a straight line basis over the year.

Management fees – Kiwi Choice’s management fees are based on KPF’s turnover, and are recognised when KPF’s sales are recognised.

NOTES TO THE FINANCIAL STATEMENTS CONTINUED

21V E R I T A S I N V E S T M E N T S L I M I T E D A N N U A L R E P O R T 2 0 1 4

2.4 Interest bearing liabilitiesInterest bearing loans and borrowings are initially measured at fair value, less directly attributable transaction costs. After initial recognition, interest bearing loans and borrowings are subsequently measured at amortised cost using the effective interest method. Loans and borrowings are classified as current liabilities unless the Group has an unconditional right to defer settlement of the liability for at least 12 months after the reporting date.

2.5 Finance costs / incomeFinance costs include interest on external debt (borrowing costs). Borrowing costs incurred for the construction of any qualifying asset are capitalised during the period of time that is required to complete and prepare the asset for its intended use or sale.

Finance income includes interest on deposits and finance revenues. These are recognised as the interest or revenue accrues using the effective interest method.

2.6 Dividends receivedDividends arising in respect of shares held by the Group / Veritas are recognised as income when paid by the investee corporation.

2.7 Cash and cash equivalentsCash and cash equivalents in the statement of financial position and statement of cash flows comprise cash at bank and in hand, net of small temporary bank overdrafts, and short-term deposits with an original maturity of three months or less that are readily convertible to known amounts of cash and which are subject to an insignificant risk of changes in value. Short term deposits with an original maturity of greater than three months are also included within cash and cash equivalents if the term deposit can be terminated at an earlier date, without incurring penalties.

Restricted cash comprises deposits held by the NZX on behalf of Veritas.

2.8 Trade and other receivablesTrade receivables are amounts due from franchise stores for carcasses sold or services performed in the ordinary course of business. If collection is expected in one year or less, they are classified as current assets. If not, they are presented as non-current assets.

Trade receivables are recognised initially at fair value and subsequently measured at amortised cost using the effective interest method, less an allowance for impairment. Collectability of trade receivables is reviewed on an on-going basis and a provision for doubtful debts is made when there is objective evidence that the Group will not be able to collect all amounts due according to the original terms of the receivables. Financial difficulties of the debtor, or amounts significantly overdue are considered objective evidence of impairment. The amount of the loss is recognised in the profit and loss component of the statement of comprehensive income. Subsequent recoveries of amounts previously written off are credited in the profit and loss component of the Statement of Comprehensive Income.

22 V E R I T A S I N V E S T M E N T S L I M I T E D A N N U A L R E P O R T 2 0 1 4

2 . S U M M A R Y O F S I G N I F I C A N T A C C O U N T I N G P O L I C I E S ( c o n t i n u e d )2.9 Goods and Service Tax (“GST”)

The financial statements have been prepared so that all components are stated exclusive of GST, except:

when the GST incurred on a purchase of goods and services is not recoverable from the taxation authority, in which case the GST is recognised as part of the cost of acquisition of an asset or as part of the expense item as applicable; and trade receivables and payables, which include GST invoiced.

The net amount of GST recoverable from, or payable to, the taxation authority is included as part of receivables or payables in the statement of financial position. GST paid to the taxation authority is included within payments to suppliers and employees in the statement of cash flows.

Commitments and contingencies are disclosed net of the amount of GST recoverable from, or payable to the taxation authority.

2.10 Income taxThe income tax expense or benefit for the period is the tax payable on the current period’s taxable income adjusted by changes in deferred tax assets and liabilities attributed to temporary differences between the tax base of assets and liabilities and their carrying amounts in the financial statements.

Current tax assets and liabilities are measured at the amount expected to be recovered from or paid to the taxation authorities based on the current period’s taxable income. The tax rates and tax laws used to compute the amount are those that are enacted or substantively enacted at balance date.

Deferred tax assets and liabilities are recognised for temporary differences at the balance date between the tax base of assets and liabilities and their carrying amounts for financial reporting purposes.

Deferred income tax assets are recognised for all deductible temporary differences, carry-forward of unused tax credits and unused tax losses, to the extent that it is probable that taxable profit will be available against which the deductible temporary differences, and carry-forward of unused tax credits and unused tax losses can be utilised.

The carrying amount of deferred income tax assets is reviewed at each reporting date and reduced to the extent that it is no longer probable that sufficient taxable profit will be available to allow all or part of the deferred income tax asset to be utilised.

Deferred income tax assets and liabilities are measured at the tax rates that are expected to apply to the year when the asset is realised or the liability is settled, based on tax rates (and tax laws) that have been enacted or substantively enacted at balance date.

The income tax expense or revenue attributable to amounts recognised directly in equity are also recognised directly in equity. The associated current or deferred tax balances are recognised in these accounts as usual.

2.11 Property, plant and equipmentProperty, plant and equipment is initially recorded at cost, including costs directly attributable to bring the asset to its working condition, less accumulated depreciation and any accumulated impairment losses. Any expenditure that increases the economic benefits derived from the asset is capitalised. Expenditure on repairs and maintenance that does not increase the economic benefits is expensed in the period it occurs.

NOTES TO THE FINANCIAL STATEMENTS CONTINUED

23V E R I T A S I N V E S T M E N T S L I M I T E D A N N U A L R E P O R T 2 0 1 4

Depreciation of property, plant and equipment is calculated using the diminishing value method to allocate their cost, net of their residual values, over their estimated useful lives. The rates are as follows:

Plant and equipment* 14 – 48%Furniture and fittings* 12%Office equipment* 11.4 - 67% Motor vehicles 24 - 36%Computer equipment 33 - 60%*the business has very few furniture and fittings and office equipment, hence for disclosure purposes these two categories have been included together with plant and equipment.

The assets’ residual values and useful lives are reviewed, and adjusted if appropriate, at each balance date. An asset’s carrying amount is written down immediately to its recoverable amount if the asset’s carrying amount is greater than its estimated recoverable amount. Gains and losses on disposals are determined by comparing proceeds with carrying amount. These are included in the profit and loss component of the statement of comprehensive income.

An item of property, plant and equipment is derecognised upon disposal or when no further future economic benefits are expected from its use or disposal. When an item of property, plant and equipment is disposed of, the difference between net disposal proceeds and the carrying amount is recognised in profit or loss.

2.12 Other intangible assetsIntangible assets acquired separately are reported at cost less accumulated amortisation and accumulated impairment losses.

Computer software - Acquired computer software licences are capitalised on the basis of the costs incurred to acquire and bring to use the specific software. These costs are amortised over their estimated useful lives (three to five years). Software costs with a net book value of $30,705 were reclassified from property, plant and equipment to intangible assets in 2013. The associated amortisation was reclassified from depreciation to amortisation expense.

An intangible asset is derecognised on disposal, or when no future economic benefit is expected from use or disposal. Gains or losses arising from derecognition of an intangible asset, measured as the difference between the net disposal proceeds and the carrying amount of the asset are recognised in profit or loss when the asset is derecognised.

2.13 Impairment of tangible and intangible assets other than goodwillAt the end of each reporting period, the Group reviews the carrying amounts of its tangible and intangible assets to determine whether there is any indication that those assets have suffered an impairment loss. If any such indication exists, the recoverable amount of the asset is estimated in order to determine the extent of the impairment loss (if any). When it is not possible to estimate the recoverable amount of an individual asset, the Group estimates the recoverable amount of the cash-generating unit to which the asset belongs. When a reasonable and consistent basis of allocation can be identified, corporate assets are also allocated to individual cash-generating units, or otherwise they are allocated to the smallest group of cash-generating units for which a reasonable and consistent allocation basis can be identified.

Intangible assets with indefinite useful lives and intangible assets not yet available for use are tested for impairment at least annually, and whenever there is an indication that the asset may be impaired.

24 V E R I T A S I N V E S T M E N T S L I M I T E D A N N U A L R E P O R T 2 0 1 4

2 . S U M M A R Y O F S I G N I F I C A N T A C C O U N T I N G P O L I C I E S ( c o n t i n u e d )Recoverable amount is the higher of fair value less costs to sell and value in use. In assessing value in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset for which the estimates of future cash flows have not been adjusted.

If the recoverable amount of an asset (or cash-generating unit) is estimated to be less than its carrying amount, the carrying amount of the asset (or cash-generating unit) is reduced to its recoverable amount. An impairment loss is recognised immediately in profit or loss, unless the relevant asset is carried at a revalued amount, in which case the impairment loss is treated as a revaluation decrease.

When an impairment loss subsequently reverses, the carrying amount of the asset (or a cash-generating unit) is increased to the revised estimate of its recoverable amount, but so that the increased carrying amount does not exceed the carrying amount that would have been determined had no impairment loss been recognised for the asset (or cash-generating unit) in prior years. A reversal of an impairment loss is recognised immediately in profit or loss, unless the relevant asset is carried at a revalued amount, in which case the reversal of the impairment loss is treated as a revaluation increase.

2.14 Trade and other payablesTrade and other payables are carried at amortised cost and due to their short term nature they are not discounted. They represent liabilities for goods and services provided to the Group by suppliers in the ordinary course of business prior to the end of the financial year that are unpaid and arise when the Group becomes obliged to make future payments in respect of the purchase of these goods and services. The amounts are unsecured and are usually paid within 30 days of recognition.

2.15 Employee entitlementsLiabilities for wages, salaries and annual leave are recognised in the provision for employee benefits and measured at the amounts expected to be paid when the liabilities are settled. The employee benefit liability expected to be settled within twelve months from balance date is recognised in current liabilities.

2.16 ProvisionsProvisions are recognised when the Group has a legal or constructive obligation as a result of a past event, it is probable that a future sacrifice of economic benefits will be required and a reliable estimate can be made of the amount of the obligation.

Provisions are measured at the present value of management’s best estimate of the expenditure required to settle the present obligation at balance date using a discounted cash flow methodology. The increase in the liability as a result of the passage of time is recognised in finance costs.

2.17 LeasesThe determination of whether an arrangement is or contains a lease is based on the substance of the arrangement at inception date, whether the fulfilment of the arrangement is dependent on the use of a specific asset or assets or the arrangement conveys the right to use the asset, even if that right is not explicitly specified in an arrangement.

NOTES TO THE FINANCIAL STATEMENTS CONTINUED

25V E R I T A S I N V E S T M E N T S L I M I T E D A N N U A L R E P O R T 2 0 1 4

Operating leases – Group as lesseeWhere the Group is the lessee, leases where the lessor retains substantially all the risks and benefits of ownership of assets are classified as operating leases. Net rental payments, excluding contingent payments, are recognised as an expense in profit or loss on a straight-line basis over the period of the lease. Operating lease incentives are recognised as a liability when received and subsequently reduced by allocating lease payments between rental expense and reduction of the liability.

2.18 Classification as debt or equityDebt and equity instruments issued by a Group entity are classified as either financial liabilities or as equity in accordance with the substance of the contractual arrangements and the definitions of a financial liability and an equity instrument.

2.19 Contributed equityOrdinary shares are classified as equity. Incremental costs directly attributable to the issue of new shares or options are shown in equity as a deduction, net of tax, from the proceeds.

2.20 Earnings per shareThe Group presents basic and diluted earnings per share (EPS) data for its common shares. Basic EPS is computed based on the weighted average number of shares of common stock outstanding during the period. Diluted EPS is computed based on the weighted average number of shares of common stock plus the effect of dilutive potential common shares outstanding during the period.

2.21 Operating segmentsOperating segments are reported in a manner consistent with internal reporting provided to the chief operating decision-making body. The chief operating decision-making body responsible for allocating resources and assessing performance of operating segments is the Board of Directors.

2.22 Discontinued operations / assets held for saleA discontinued operation is a component of the Group’s business, the operations and cashflows of which can be clearly distinguished from the rest of the Group and which:

represents a separate major line of business or geographical area of operations; or is part of a single co-ordinated plan to dispose of a separate major line of business or geographical area of operations; or is a subsidiary acquired exclusively with a view to re-sale.

Classification as a discontinued operation occurs at the earlier of disposal or when the operation meets the criteria to be classified as held-for-sale.

When an operation is classified as a discontinued operation, the comparative statement of profit and loss and other comprehensive income is re-presented as if the operation had been discontinued from the start of the comparative year.

Non-current assets, or disposal groups comprising assets and liabilities, are classified as held-for-sale if it is highly probable that they will be recovered primarily through sale rather than through continuing use.

26 V E R I T A S I N V E S T M E N T S L I M I T E D A N N U A L R E P O R T 2 0 1 4

2 . S U M M A R Y O F S I G N I F I C A N T A C C O U N T I N G P O L I C I E S ( c o n t i n u e d )Such assets, or disposal groups, are generally measured at the lower of their carrying amount and fair value less costs to sell. Any impairment loss on a disposal group is allocated first to goodwill, and then to the remaining assets and liabilities on a pro rata basis, except that no loss is allocated to inventories, financial assets, employee benefit assets, investment property or biological assets, which continue to be measured in accordance with the Group’s other accounting policies. Impairment losses on initial classification as held-for-sale or held-for-distribution and subsequent gains and losses on remeasurement are recognised in profit or loss.

Once classified as held-for-sale, intangible assets and property, plant and equipment are no longer amortised or depreciated, and any equity-accounted investee is no longer equity accounted.

2.23 Non-GAAP reporting measuresAdditional reporting measures have been presented in the statement of comprehensive income or referenced to in the notes to the financial statements. The following non-GAAP measures are relevant to the understanding of the Group financial performance:

EBIT (a non-GAAP measure) represents earnings before income taxes (a GAAP measure), excluding interest income and expense, as reported in the financial statements; EBITDA (a non-GAAP measure) represents earnings before income taxes (a GAAP measure), excluding interest income, interest expense, depreciation and amortisation, as reported in the financial statements; EBITDA and non-trading transaction impact (a non-GAAP measure) represents earnings before income taxes (a GAAP measure), excluding interest income, interest expense, depreciation and amortisation, and non-trading transaction impact, as reported in the financial statements.

3 . N E W S T A N D A R D S , A M E N D M E N T S A N D I N T E R P R E T A T I O NStandards, amendments and interpretation effective in the current periodThe following are the new or revised standards, amendments and interpretations applicable to the Group which are in issue that are not yet required to be adopted by the Group in preparing its financial statements for the year ended 30 June 2014:

Standard / interpretation Effective for Expected annual reporting to be initially periods beginning applied in the on or after financial year ending

NZ IFRS 9 ‘Financial Instruments’ 1 January 2017 30 June 2018 - Addresses measurement and recognition of financial assets and liabilities

NZ IFRS 15 ‘Revenue from Contracts with Customers’ 1 January 2018 30 June 2019 - Establishes principles for reporting useful information to users of financial statements about the nature, amount, timing and uncertainty of revenues and cashflows from contracts with customers

The financial statement impact of adoption of these standards, amendments and interpretations are not expected to have a material impact on the financial statements reported by the Group.

NOTES TO THE FINANCIAL STATEMENTS CONTINUED

27V E R I T A S I N V E S T M E N T S L I M I T E D A N N U A L R E P O R T 2 0 1 4

Adoption of new and revised standards, amendments and interpretationsThe standards, amendments and interpretations listed below applicable to the Group became mandatory in the current year:

NZ IFRS 10 – Consolidated Financial Statements

NZ IFRS 11 – Joint Arrangements

NZ IFRS 12 – Disclosure of Interests in other Entities

NZ IFRS 13 – Fair Value Measurement

Revised NZ IAS 27 – Separate Financial Statements

The adoption of these new and revised standards, amendments and interpretations did not have a material impact on the results or position reported by the Group.

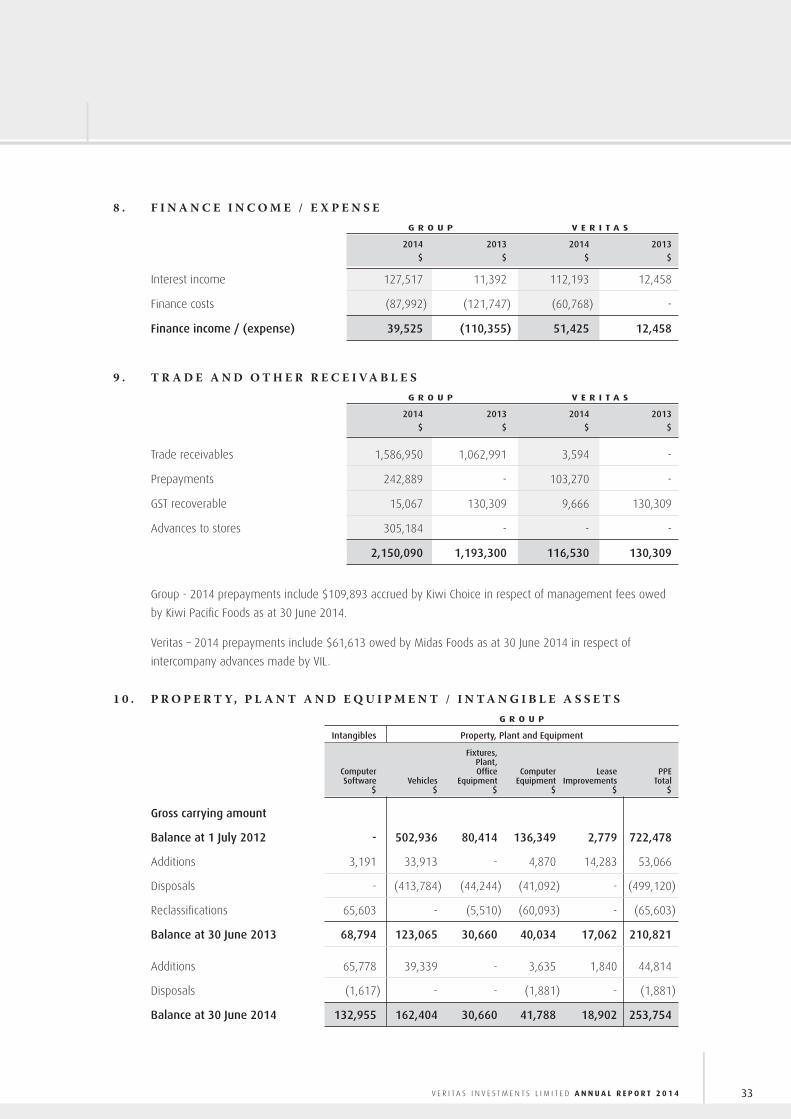

4 . R E V E N U E G R O U P V E R I T A S

2014 2013 2014 2013 $ $ $ $

Carcass income 20,691,094 21,357,436 - -

Suppliers rebates 4,980,620 4,636,928 - -

Advertising income 3,460,256 3,316,136 - -

Other income 840,524 554,928 7,292 -

29,972,494 29,865,428 7,292 -

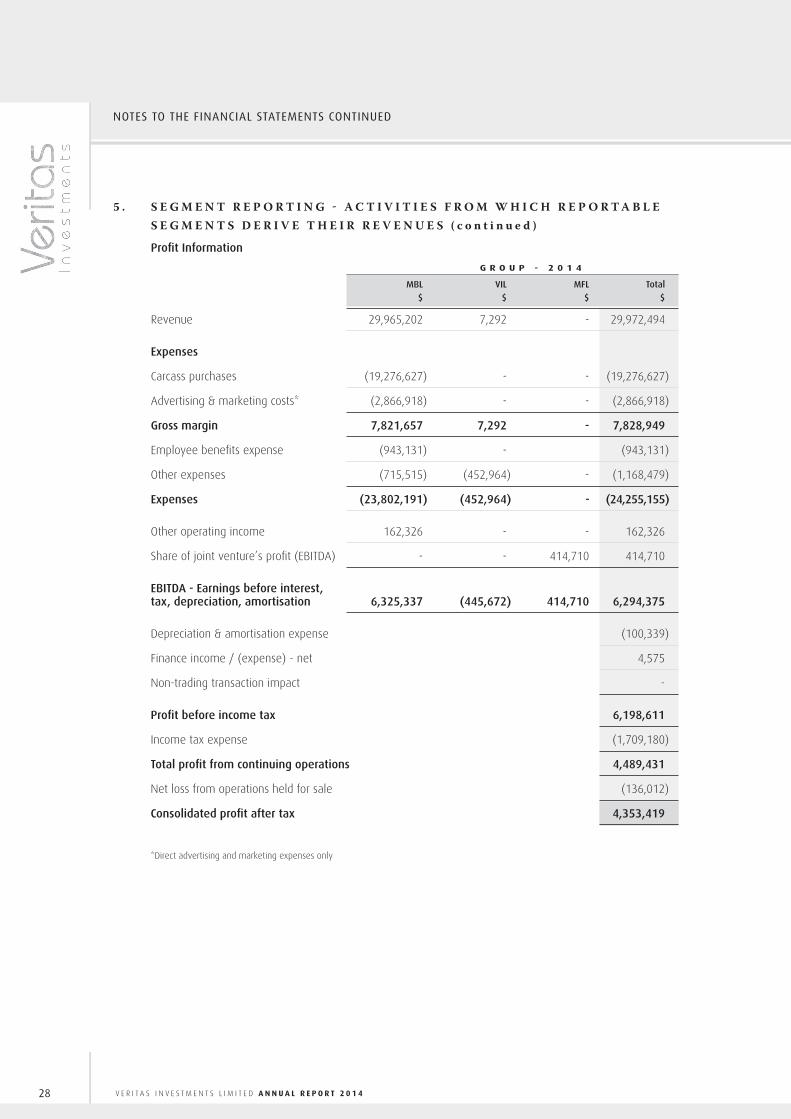

5 . S E G M E N T R E P O R T I N G - A C T I V I T I E S F R O M W H I C H R E P O R T A B L E S E G M E N T S D E R I V E T H E I R R E V E N U E S

Following Veritas legally acquiring the Mad Butcher business in 2013 and MFL and KCL in December 2013 it has been identified that the Chief Operating Decision Maker (“CODM”) for the Group is now the Board of Directors as they are now responsible for allocating resources and assessing performance across the Group. The Group has three reportable segments, which are the Group’s separate entities. For each of the entities the Board (the CODM) reviews management reports on a monthly basis.

Information regarding the results of each reportable segment in included below. Performance is measure based on segment EBITDA as included in the management reports that are reviewed by the Board. Segment EBITDA is used to measure performance as the Board believes that such information is the most relevant in evaluating the results of certain segments relative to other entities that operate within these industries.

28 V E R I T A S I N V E S T M E N T S L I M I T E D A N N U A L R E P O R T 2 0 1 4

NOTES TO THE FINANCIAL STATEMENTS CONTINUED

5 . S E G M E N T R E P O R T I N G - A C T I V I T I E S F R O M W H I C H R E P O R T A B L E S E G M E N T S D E R I V E T H E I R R E V E N U E S ( c o n t i n u e d )

Profit Information G R O U P - 2 0 1 4

MBL VIL MFL Total $ $ $ $

Revenue 29,965,202 7,292 - 29,972,494

Expenses

Carcass purchases (19,276,627) - - (19,276,627)

Advertising & marketing costs* (2,866,918) - - (2,866,918)

Gross margin 7,821,657 7,292 - 7,828,949

Employee benefits expense (943,131) - (943,131)

Other expenses (715,515) (452,964) - (1,168,479)

Expenses (23,802,191) (452,964) - (24,255,155)

Other operating income 162,326 - - 162,326

Share of joint venture’s profit (EBITDA) - - 414,710 414,710

EBITDA - Earnings before interest, tax, depreciation, amortisation 6,325,337 (445,672) 414,710 6,294,375

Depreciation & amortisation expense (100,339)

Finance income / (expense) - net 4,575

Non-trading transaction impact -

Profit before income tax 6,198,611

Income tax expense (1,709,180)

Total profit from continuing operations 4,489,431

Net loss from operations held for sale (136,012)

Consolidated profit after tax 4,353,419

*Direct advertising and marketing expenses only

29V E R I T A S I N V E S T M E N T S L I M I T E D A N N U A L R E P O R T 2 0 1 4

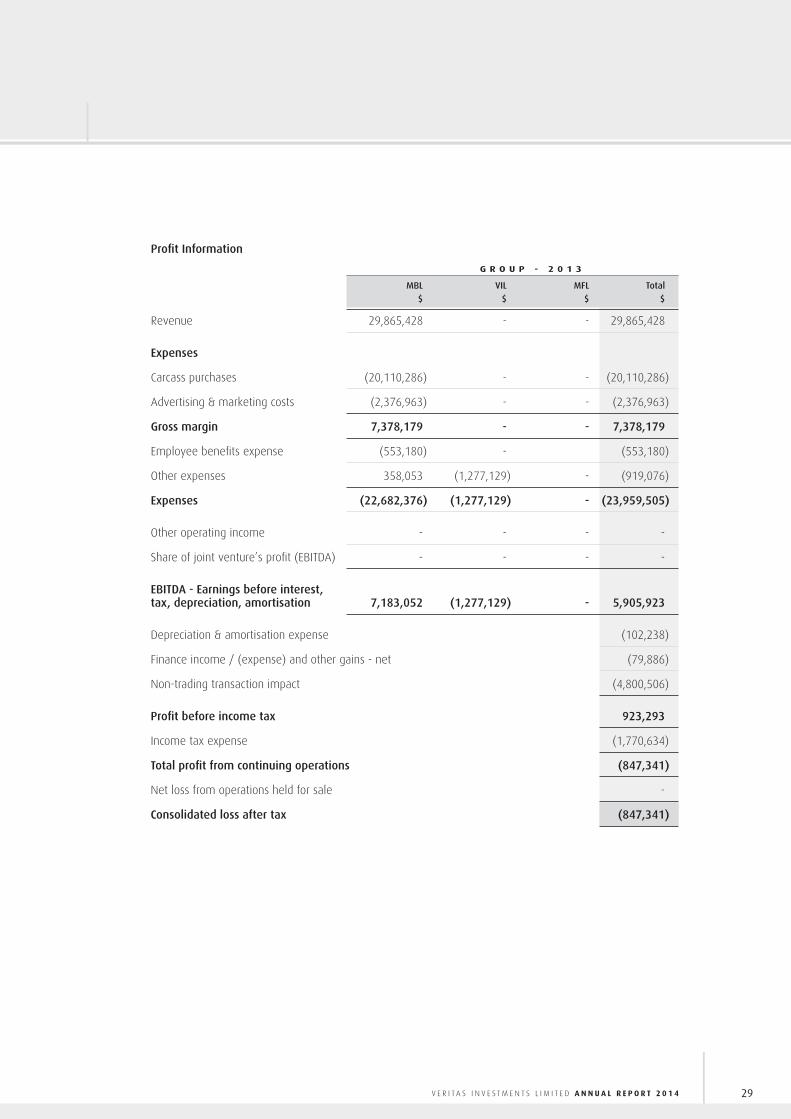

Profit Information G R O U P - 2 0 1 3

MBL VIL MFL Total $ $ $ $

Revenue 29,865,428 - - 29,865,428

Expenses

Carcass purchases (20,110,286) - - (20,110,286)

Advertising & marketing costs (2,376,963) - - (2,376,963)

Gross margin 7,378,179 - - 7,378,179

Employee benefits expense (553,180) - (553,180)

Other expenses 358,053 (1,277,129) - (919,076)

Expenses (22,682,376) (1,277,129) - (23,959,505)

Other operating income - - - -

Share of joint venture’s profit (EBITDA) - - - -

EBITDA - Earnings before interest, tax, depreciation, amortisation 7,183,052 (1,277,129) - 5,905,923

Depreciation & amortisation expense (102,238)

Finance income / (expense) and other gains - net (79,886)

Non-trading transaction impact (4,800,506)

Profit before income tax 923,293

Income tax expense (1,770,634)

Total profit from continuing operations (847,341)

Net loss from operations held for sale -

Consolidated loss after tax (847,341)

30 V E R I T A S I N V E S T M E N T S L I M I T E D A N N U A L R E P O R T 2 0 1 4

NOTES TO THE FINANCIAL STATEMENTS CONTINUED

5 . S E G M E N T R E P O R T I N G - A C T I V I T I E S F R O M W H I C H R E P O R T A B L E S E G M E N T S D E R I V E T H E I R R E V E N U E S ( c o n t i n u e d )

Asset / liability information G R O U P - 2 0 1 4

MBL VIL MFL Total $ $ $ $

Total assets for reportable segments 2,881,432 3,511,780 - 6,393,212

Equity accounted investee - - 3,762,334 3,762,334

Other assets - held for sale 416,357 - - 416,357

Consolidated total assets 3,297,789 3,511,780 3,762,334 10,571,903

Total liabilities for reportable segments 1,221,954 3,269,923 - 4,491,877

Other liabilities - held for sale 127,827 - - 127,827

Consolidated total liabilities 1,349,781 3,269,923 - 4,619,704

G R O U P - 2 0 1 3

MBL VIL MFL Total $ $ $ $

Total assets for reportable segments (37,889,872) 42,128,468 - 4,238,596

Equity accounted investee - - - -

Other assets - - - -

Consolidated total assets (37,889,872) 42,128,468 - 4,238,596

Total liabilities for reportable segments 1,413,290 355,238 - 1,768,528

Other liabilities - - - -

Consolidated total liabilities 1,413,290 355,238 - 1,768,528

5.1 Other information

GeographicalVeritas and its subsidiaries operate within New Zealand, and derived no revenue from foreign countries for the year ended 30 June 2014 (2013: nil).

Kiwi Pacific Foods derived revenue from foreign countries in the year ended 30 June 2014. As a joint venture, KPF is equity-accounted (from the date of acquisition), so its revenues are not consolidated and reported as Group revenues.

Information about major customersNo single customer contributed 10% or more to the Group’s revenue for the year ended 30 June 2014 (2013: nil).

31V E R I T A S I N V E S T M E N T S L I M I T E D A N N U A L R E P O R T 2 0 1 4

6 . D I S C O N T I N U E D O P E R A T I O N S - S T O R E H E L D F O R S A L EAs master franchisor, Mad Butcher selects towns and sites for new store openings and then manages the store fit-out (often, on a turn-key service). Finding a suitable site can take considerable time, and therefore Mad Butcher usually starts the franchisee selection process after a site has been leased and store fit-out started.

Mad Butcher identified a new store location in Invercargill and started fit-out early on in this financial year. However, negotiations with a prospective franchisee ultimately failed. Mad Butcher decided to go ahead with the store opening in November as planned, trading as owner of this store. From the commencement of trading the store has been treated as an operation held for sale, and its assets, liabilities and results have not been included in continuing operations.

Mad Butcher has been seeking a buyer for this store since the original prospect fell through. Negotiations are currently taking place with a prospective buyer, and a sale is expected to close by the end of September 2014.

As at 30 June 2014 $

Assets and liabilities held for sale

Plant and equipment 371,762

Inventories 42,653

Trade receivables 1,942

Assets held for sale 416,357

Trade payables 127,827

Liabilities held for sale 127,827

Impairment loss relating to assets and liabilities held for sale Assets and liabilities held for sale are stated at their book value. No impairment losses have been applied to reduce their carrying amounts.

November 2013 - June 2014 $

Results of Operation

Revenue 1,664,421

Cost of Sales (1,362,112)

Gross Profit 302,309

Expenses (491,214)

Loss before Tax (188,905)

Tax 52,893

Net loss for the period (136,012)

Cash flows used in Operation

Cash used in operating activities 116,268

Cash used in investing activities 361,167

Net cash outflow for the period 477,435

32 V E R I T A S I N V E S T M E N T S L I M I T E D A N N U A L R E P O R T 2 0 1 4

NOTES TO THE FINANCIAL STATEMENTS CONTINUED

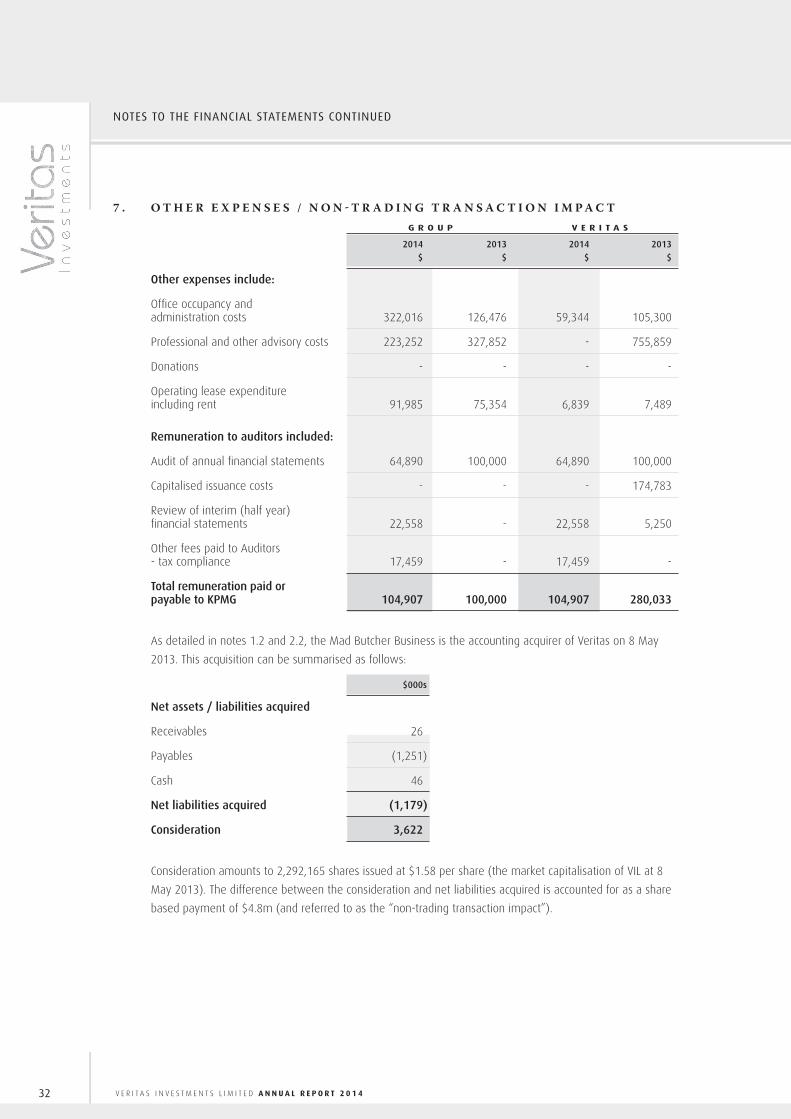

7 . O T H E R E X P E N S E S / N O N - T R A D I N G T R A N S A C T I O N I M P A C T G R O U P V E R I T A S

2014 2013 2014 2013 $ $ $ $

Other expenses include:

Office occupancy and administration costs 322,016 126,476 59,344 105,300

Professional and other advisory costs 223,252 327,852 - 755,859

Donations - - - -

Operating lease expenditure including rent 91,985 75,354 6,839 7,489

Remuneration to auditors included:

Audit of annual financial statements 64,890 100,000 64,890 100,000

Capitalised issuance costs - - - 174,783

Review of interim (half year) financial statements 22,558 - 22,558 5,250

Other fees paid to Auditors - tax compliance 17,459 - 17,459 -

Total remuneration paid or payable to KPMG 104,907 100,000 104,907 280,033

As detailed in notes 1.2 and 2.2, the Mad Butcher Business is the accounting acquirer of Veritas on 8 May 2013. This acquisition can be summarised as follows:

$000s

Net assets / liabilities acquired

Receivables 26

Payables (1,251)

Cash 46

Net liabilities acquired (1,179)

Consideration 3,622