for personal use only - asx.com.au · puma masterfund p-16 financial report income statement for...

TRANSCRIPT

\

PUMA MASTERFUND P-16A.B.N. 17 739385 144

Special purpose annual report of the Trust as an individual entityfor the period ended 31 March 2011

The Trust's registered office is:Perpetual Limited

Level 12 Angel Place1 23 Pitt Street

SYDNEY NSW 2000

For

per

sona

l use

onl

y

PUMA MASTERFUND P-16

2011 Special Purpose Annual ReportContents

Page

Financial Report ........................................................................................................ 3Income statement"",',.............................................................................................. 3Statement of comprehensive income..............................................,...,..................... 4Statement of financial position........................................................,......................... 5Statement of changes in equity................................................................................. 6Statement of cash flows............................................................................................ 7Notes to the financial statements.............................................................................. 8Note 1. Trust Information.................................................... .................................... 8Note 2. Summary of significant accounting policies ................................................ 8Note 3. Loss for the period........ ............................................................ ............... 12Note 4. Due from financial institutions (current assets) .......................................... 13Note 5. Other assets (current assets).................................................................... 13Note 6. Loan assets held at amortised cost......................................................... 13Note 7. Other liabilities (current liabilities) .............................................................. 13Note 8. Debt issued at amortised cost..... ............................ ................... ............. 13Note 9. Net liabilities attributable to unitholders (non-current) ................................ 14Note 10. Notes to the statement of cash flows....................................................... 14Note 11. Related party information......................................................................... 15Note 12. Contingent liabilities and assets................................................................ 15Note 13. Audit and other services provided by PricewaterhouseCoopers ............... 15Note 14. Events occurring after the reporting date.................................................. 15

Directors' declaration ... .......... ... .............................................................................. 16Independent auditor's report to the members of PUMA MASTERFUND P-16 ..... 17

Qlr§QtQrDirector

PUMA MASTERFUND P-16 2011 Financial Report 2

For

per

sona

l use

onl

y

PUMA MASTERFUND P-16

Financial Report

Income statementfor the period ended 31 March 2011

Notes2 September 2010to 31 March 2011

$

Interest and similar income

Interest expense and similar charges

Net interest income

3

3

28,646,758

(24,201,555)4,445,203

Fee and commission incomeFee and commission expenses

Net fee and commission expense 3

344,123

(1,149,610)

(805,487)

Net operating income 3,639,716

Distributions to unitholders

Operating loss for the period(3,811,588)

(171,872)

(171,872)Loss attributable to unitholders of PUMA MASTERFUND P-16

The above income statement should be read in conjunction with the accompanying notes.

PUMA MASTERFUND P-16 2011 Financial Report 3

For

per

sona

l use

onl

y

PUMA MASTERFUND P-16

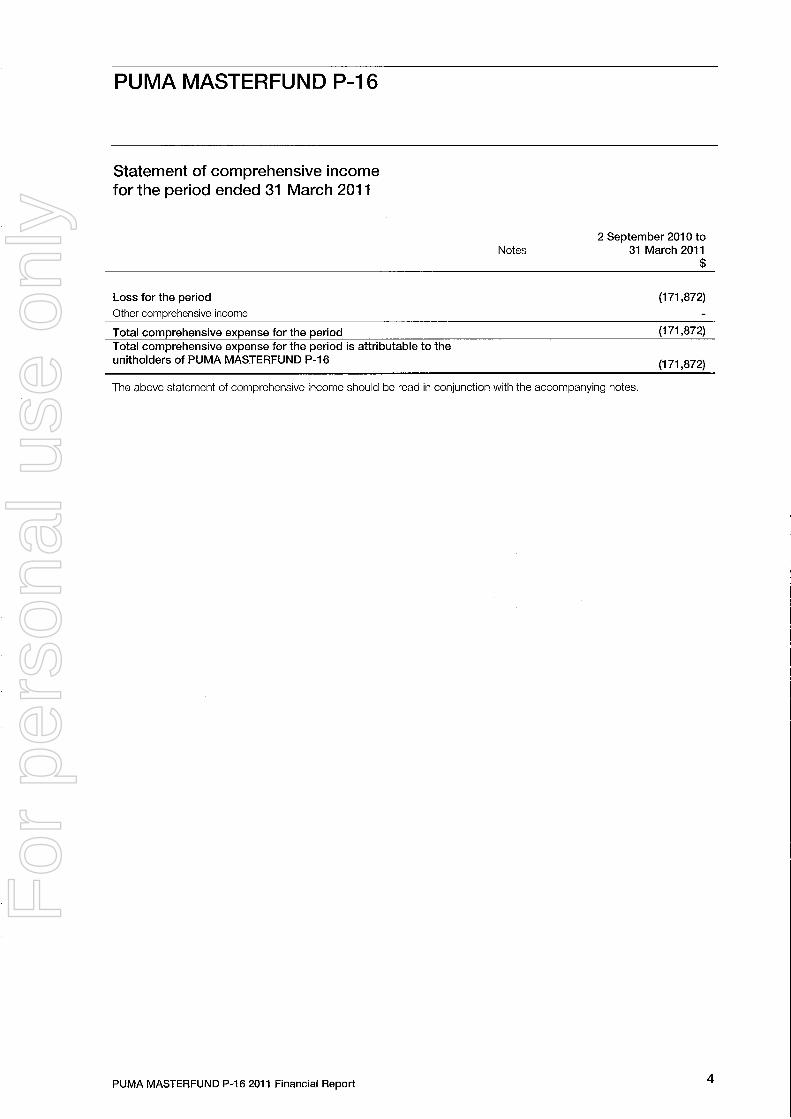

Statement of comprehensive incomefor the period ended 31 March 2011

Notes2 September 2010 to

31 March 2011

$

Loss for the periodOther comprehensive income

Total comprehensive expense for the periodTotal comprehensive expense for the period is attributable to theunitholders of PUMA MASTERFUND P-16

(171,872)

(171,872)

(171,872)

The above statement of comprehensive income should be read in conjunction with the accompanying notes.

PUMA MASTERFUND P-16 2011 Financial Report 4

For

per

sona

l use

onl

y

PUMA MASTERFUND P-16

Statement of financial positionas at 31 March 2011

Notes2011

$

AssetsDue from financial institutions

Other assets

Derivative financial instruments - positive values

Loan assets held at amortised cost

Total assets

4

5

21,574,701335,250542,911

647,831,432670,284,294

6

Liabilities

Distributions payable

Other liabilities

Derivative financial instruments - negative values

Debt issued at amortised cost

Total liabiliies (excluding net liabilities attributable to unitholders)Net liabilties attributable to unitholders

7

4,663,409523,171

732,458664,537,028670,456,066

(171,772)

8

9

The above statement of financial position should be read in conjunction with the accompanying notes.

PUMA MASTERFUND P-16 2011 Financial Report 5

For

per

sona

l use

onl

y

PUMA MASTERFUND P-16

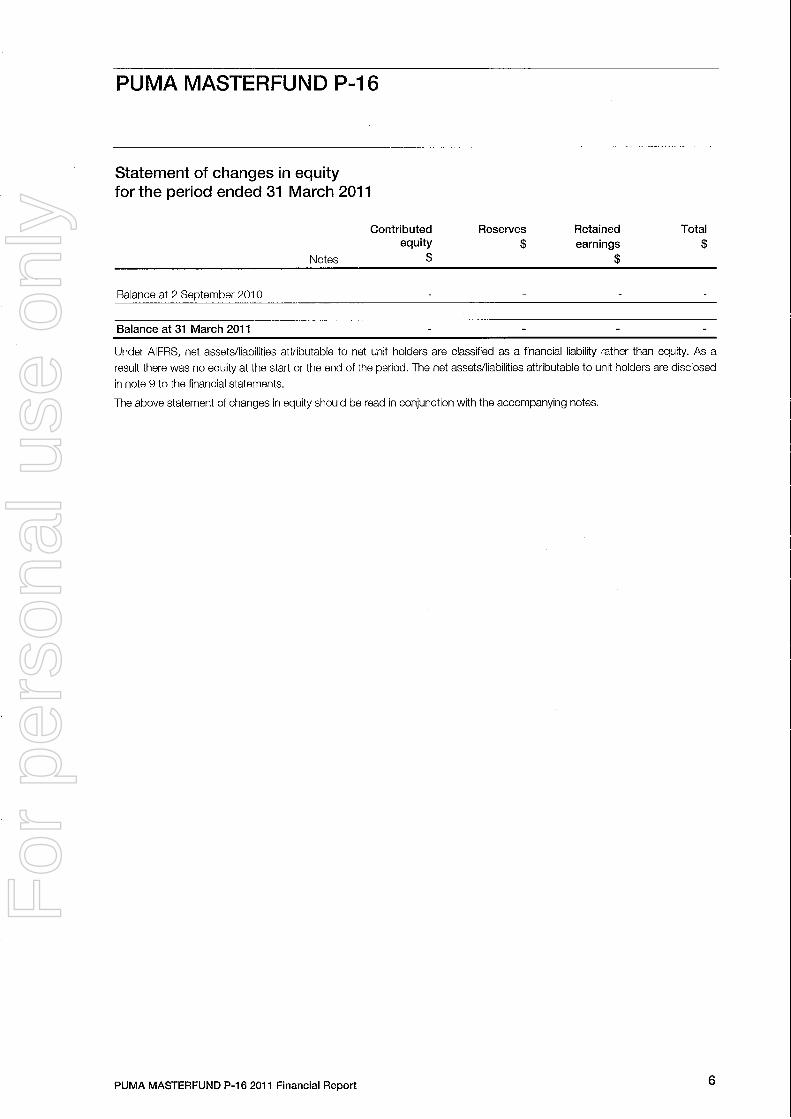

Statement of changes in equityfor the period ended 31 March 2011

Notes

Contributedequity

$

Reserves$

Retainedearnings

$

Total$

Balance at 2 September 2010

Balance at 31 March 2011

Under AIFRS, net assets/liabilties attributable to net unit holders are classified as a financial liability rather than equity. As a

result there was no equity at the start or the end of the period. The net assets/liabilities attributable to unit holders are disclosed

in note 9 to the financial statements.

The above statement of changes in equity should be read in conjunction with the accompanying notes.

PUMA MASTERFUND P-16 2011 Financial Report 6

For

per

sona

l use

onl

y

PUMA MASTERFUND P-16

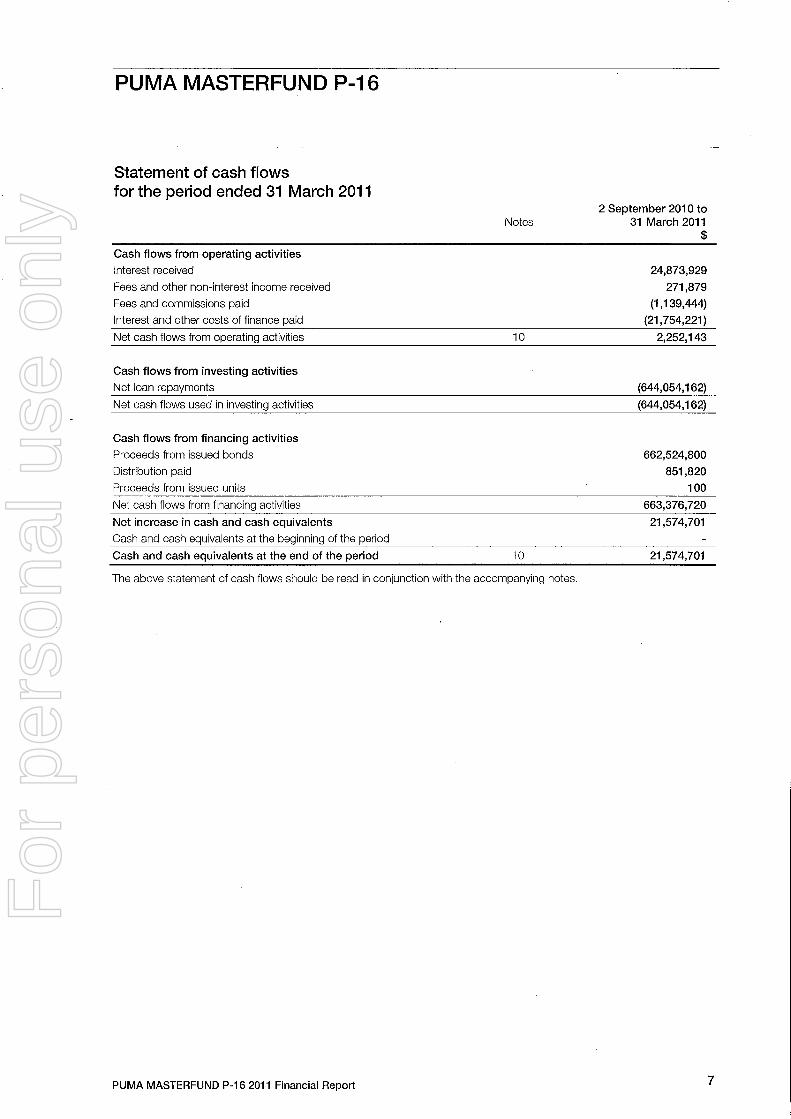

Statement of cash flowsfor the period ended 31 March 2011

Notes2 September 2010 to

31 March 2011

$

Cash flows from operating activitiesInterest receivedFees and other non-interest income received

Fees and commissions paid

Interest and other costs of finance paid

Net cash flows from operating activities 10

24,873,929271,879

(1,139,444)(21,754,221 )

2,252,143

Cash flows from investing activitiesNet loan repayments

Net cash flows used in investing activities(644,054,162)

(644,054,162)

Cash flows from financing activitiesProceeds from issued bonds

Distribution paid

Proceeds from issued units

Net cash flows from financing activities

Net increase in cash and cash equivalentsCash and cash equivalents at the beginning of the period

Cash and cash equivalents at the end of the period

662,524,800851,820

100

663,376,72021,574,701

10 21,574,701

The above statement of cash flows should be read in conjunction with the accompanying notes.

PUMA MASTERFUND P-16 2011 Financial Report 7

For

per

sona

l use

onl

y

PUMA MASTERFUND P-16

Notes to the financial statementsfor the period ended 31 March 2011

Note 1. Trust Information

The Trust is registered and domiciled in Australia. The address of the Trust's registered office is Perpetual Limited, Level 12Angel Place, 123 Pitt Street, Sydney NSW 2000

Note 2. Summary of significant accounting policies

i) Basis of preparation

The execution date of the Trust is 2 September 2010. These financial statements reflect its first period of operations with thefirst mortgages being originated in September 2010. However, the financial statements have been prepared for a period of 7months from the date of execution.

The Trust is not a reporting entity because, in the Directors' opinion, it is unlikely that users exist who are unable tocommand the preparation of reports tailored so as to satisfy, specificaliy, all of their information needs.

The principal accounting policies adopted in the preparation of this Financial Report are set out below.

This special purpose Financial Report has been prepared in compliance with the Trust Deed to prepare and distribute afinancial report. The Directors have determined that Generally Accepted Accounting Principles and practices are adopted asdeemed appropriate by the Trust Manager to meet the needs of the members. Disclosure requirements have not beenadopted with the exception of the following:

AASB 101: Presentation of Financial Statements. AASB 107: Cash Flow Statements. AASB 108: Accounting Policies, Changes in Accounting Estimates and Errors. AASB 1031: Materiality. AASB 1048: Interpretation and Application of Standards

The Directors have determined that the Trust need not comply with AASB 7 "Financial Instruments Disclosure" or AASB 139"Financial Instruments: Recognition and Measurement".

Historical cost convention

This Financial Report has been prepared under the historical cost convention, as modified by the revaluation of investment

securities available for sale and other certain assets and liabilities (including derivative instruments) at fair value.

Critical accounting estimates and significant judgements

The preparation of the Financial Report in conformity with Australian Accounting Standards requires the use of certain criticalaccounting estimates. It also requires management to exercise judgement in the process of applying the accountingpolicies. In preparation of these financial statements there were no areas involving a higher degree of judgement orcomplexity.

Estimates and judgements are continually evaluated and are based on historical experience and other factors, includingreasonable expectations of future events. Management believes the estimates used in preparing the Financial Report arereasonable. Actual results in the future may differ from those reported and therefore it is reasonably possible, on the basis of

existing knowledge, that outcomes within the next financial year that are different from our assumptions and estimates could

require an adjustment to the carrying amounts of the assets and liabilities reported.

PUMA MASTERFUND P-16 2011 Financial Report 8

For

per

sona

l use

onl

y

PUMA MASTERFUND P-16

Notes to the financial statements (continued)for the period ended 31 March 2011

Note 2. Summary of significant accounting policies (continued)

i) Basis of preparation (continued)

New Accounting Standards, amendments to Accounting Standards and Interpretations that are not yeteffective

When a new Accounting Standard is first adopted, any change in accounting policy is accounted for in accordance with thespecific transitional provisions (if any), otherwise retrospectively.The Trust's assessment of the impact of the key new Accounting Standards, amendments to Accounting Standards andInterpretations is set out below:

AASB 2010-7 Amendments to Australian Accounting Standards arising from AASB 9 (December 201 0)

In December 2010, the AASB re-issued AASB 9 Financial Instruments, which is effective for annual reporting periodsbeginning on or after 1 January 2013. Early adoption is permitted if all the requirements are applíed at the same time. Therevised AASB 9 includes the classification and measurement requirements for financial liabilities, and the recognition andderecognition requirements for financial instruments, in addition to the classification and measurement requirements forfinancial assets that appeared in the December 2009 version of the Standard.

In respect of financial liabilities, the change in fair value (for financial liabilities designated at fair value through profit or loss)

due to changes in an entity's own credit risk is to be presented in other comprehensive income, unless such presentationwould create an accounting mismatch. If a mismatch is created or enlarged, the entity is required to present all changes infair value (including the effects of changes in the credit risk of the liability) in profit or loss. All other key requirements forclassification and measurement of financial liabilities have been carried forward unamended from AASB 139 FinancialInstruments: Recognition and Measurement. The recognition and derecognition requirements in AASB 139 have also beenretained and relocated to the revised AASB 9 unamended. The entity will first apply AASB 9 in the financial year beginning 1

April 2013. The impact of AASB 9 on the entity's financial statements on initial application has not yet been assessed.

ii) Foreign currency translations

Functional and presentation currency

The Trust's financial statements are presented in Australian dollars (presentation currency), which is the Trust's functionalcurrency.

iii) Revenue recognition

Revenue is measured at the fair value of the consideration received or receivable. Revenue is recognised for the majorbusiness activities as follows:

Interest incomeInterest received as part of the interest premium that varies over the life of a stated income loan and deferred establishment

fees has been brought to account on an accruals basis. All other interest income arising from ioans and deposits is broughtto account using the effective interest method. The effective interest method calculates the amortised cost of a financialinstrument and allocates the interest income or expense over the relevant period. The effective interest rate is that rate thatexactly discounts estimated future cash payments or receipts through the expected life of the financial instrument or, when

appropriate, a shorter period to the net carrying amount of the financial asset or liability.

Originator fees charged by the Trust Manager over the life of the ioan, are recognised as interest income using the effective

interest method.

Fee and commission incomeFee and commission income Is brought to account on an accruals basis.

iv) Distributions

In accordance with the Trust Deed, the Trust distributes its distributable (taxable) income, and any other amountsdetermined by the Manager, to unitholders in cash. The distributions are recognised in the Income statement asdistributions to unitholders.

PUMA MASTERFUND P-16 2011 Financial Report 9

For

per

sona

l use

onl

y

PUMA MASTERFUND P-16

Notes to the financial statements (continued)for the period ended 31 March 2011

Note 2. Summary of significant accounting policies (continued)

v) Income tax

Under current income tax legislation, the Trust is not liable for income tax provided its taxable income is fully distributed tothe beneficiary.

vi) Derivative instruments

Derivative instruments entered into by the Trust include interest rate swaps. These derivative instruments are principally used

for the risk management of existing financial assets and liabilities.

All derivatives, including those used for statement of financial position hedging purposes, are recognised on the statement of

financial position and are disclosed as an asset where they have a positive fair value at balance date or as a liability wherethe fair value at balance date is negative.

Derivatives are initially recognised at fair value on the date a derivative contract is entered into and subsequently remeasured

to their fair value. Fair values are obtained from quoted market prices in active markets, including recent markettransactions, and valuation techniques, including discounted cash flow models and option pricing models, as appropriate.Movements in the carrying amounts of derivatives are recognised in the income statement, unless the derivative meets therequirements for hedge accounting.

The best evidence of a derivative's fair value at initial recognition is the transaction price, unless its fair value is evidenced by

comparison with other observable current market transactions in the same instrument or based on a valuation techniquewhose variables include only data from observable markets. Where such evidence exists, the Trust recognises profitsimmediately when the derivative is recognised.

vii) Investments and other financial assets

With the exception of derivatives which are classified separately in the statement of financial position, the remaininginvestments in financial assets are classified as loan assets held at amortised cost. The classification depends on thepurpose for which the investment was acquired, which is determined at initial recognition and, except for fair value thoughprofit or loss, is re-evaluated at each reporting date.

Loan assets held at amortised cost

Loan assets held at amortised cost are non-derivative financial assets with fixed or determinable payments that are notquoted in an active market.

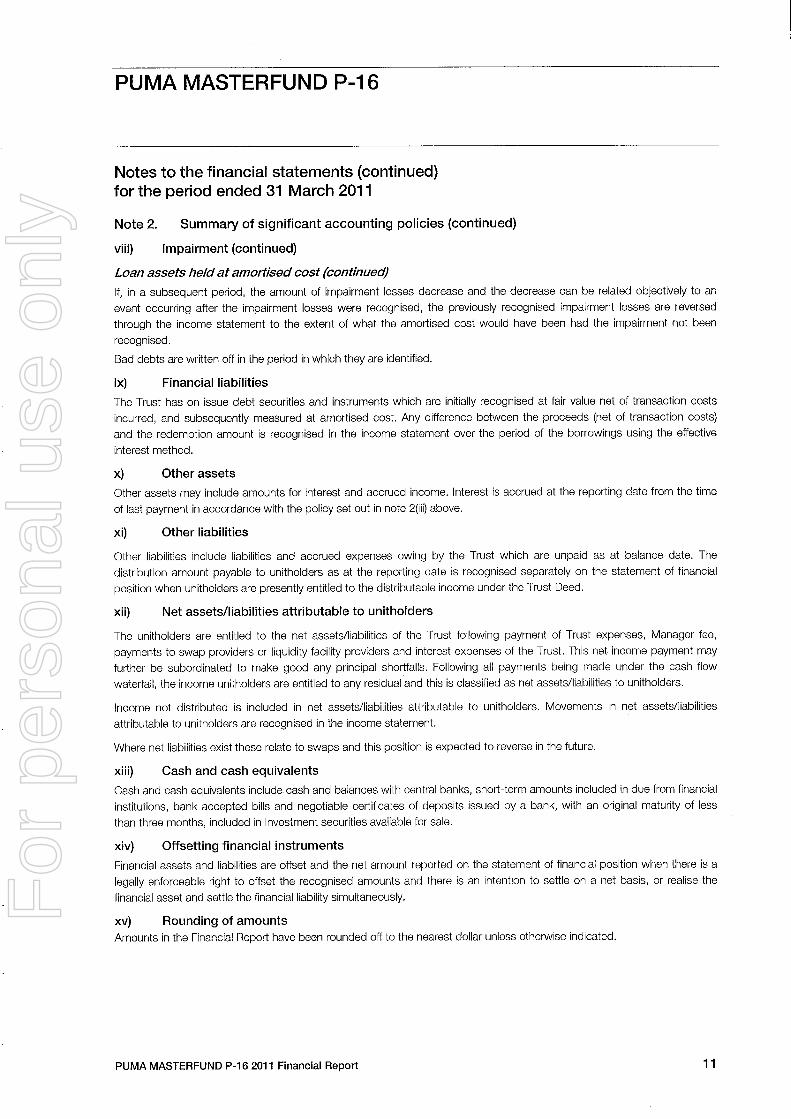

viii) Impairment

Loan assets held at amortised cost

Loan assets are subject to regular review and assessment for possible impairment. Provisions for impairment on loan assets

are recognised based on an incurred loss model and re-assessed at each reporting date. A provision for impairment isrecognised when there is objective evidence of impairment, and is caiculated based on the present value of expected futurecash flows, discounted using the original effective interest rate.

Specific provisions for impairment are recognised where impairment of individual loans is identified. The Trust makesjudgements as to whether there is any observable data indicating that there is a significant decrease in the estimated future

cash flows from a portfolio of loans before the decrease can be identified with an individual loan in that portfolio. Thisevidence may include observable data indicating that there has been an adverse change in the payment status of theborrowers in a group, or national or local economic conditions that correlate with defaults on assets in the group.Management uses estimates based on historical loss experience for assets with credit risk characteristics and objectiveevidence of impairment similar to those in the portfolio when scheduling its future cash flows. The methodology andassumptions used for estimating both the amount and timing of future cash flows are reviewed regularly to reduce anydifferences between loss estimates and actual loss experience. Changes in assumptions used for estimating future cashflows could result in a change in the estimated provisions for impairment on loan assets at reporting date.

PUMA MASTERFUND P-16 2011 Financial Report 10

For

per

sona

l use

onl

y

PUMA MASTERFUND P-16

Notes to the financial statements (continued)for the period ended 31 March 2011

Note 2. Summary of significant accounting policies (continued)

viii) Impairment (continued)

Loan assets held at amortised cost (continued)

If, in a subsequent period, the amount of impairment losses decrease and the decrease can be related objectively to anevent occurring after the impairment losses were recognised, the previously recognised impairment losses are reversedthrough the income statement to the extent of what the amortised cost would have been had the impairment not beenrecognised.

Bad debts are written off in the period in which they are identified.

ix) Financial liabilties

The Trust has on issue debt securities and instruments which are initially recognised at fair value net of transaction costsincurred, and subsequently measured at amortised cost. Any difference between the proceeds (net of transaction costs)and the redemption amount is recognised in the income statement over the period of the borrowings using the effectiveinterest method.

x) Other assets

Other assets may include amounts for interest and accrued income. Interest is accrued at the reporting date from the timeof last payment in accordance with the policy set out in note 2(iii) above.

xi) Other liabilties

Other liabilities include liabilities and accrued expenses owing by the Trust which are unpaid as at balance date. Thedistribution amount payable to unitholders as at the reporting date is recognised separately on the statement of financialposition when unitholders are presently entitied to the distributable income under the Trust Deed.

xii) Net assets/liabilities attributable to unitholders

The unitholders are entitled to the net assets/liabilities of the Trust following payment of Trust expenses, Manager fee,payments to swap providers or liquidity facility providers and interest expenses of the Trust. This net income payment mayfurther be subordinated to make good any principal shortfalls. Following all payments being made under the cash flowwaterfall, the income unitholders are entitled to any residual and this is classified as net assets/liabilities to unitholders.

Income not distributed is included in net assets/liabilities attributable to unitholders. Movements in net assets/liabilitiesattributable to unitholders are recognised in the income statement.

Where net liabilities exist these relate to swaps and this position is expected to reverse in the future.

xiii) Cash and cash equivalents

Cash and cash equivalents include cash and balances with central banks, short-term amounts included in due from financial

institutions, bank accepted bills and negotiable certificates of deposits issued by a bank, with an original maturity of lessthan three months, included in Investment securities available for sale.

xiv) Offsetting financial instruments

Financial assets and liabilities are offset and the net amount reported on the statement of financial position when there is a

legally enforceable right to offset the recognised amounts and there is an intention to settle on a net basis, or realise thefinancial asset and settle the financial liability simultaneously.

xv) Rounding of amounts

Amounts in the Financial Report have been rounded off to the nearest dollar unless otherwise indicated.

PUMA MASTERFUND P-16 2011 Financial Report 11

For

per

sona

l use

onl

y

PUMA MASTERFUND P-16

Notes to the financial statements (continued)for the period ended 31 March 2011

2 September 2010 to31 March 2011

$

Note 3. Loss for the period

Net interest incomeInterest and similar income

Interest expense and similar charges

Net interest income

28,646,758

(24,201,555)4,445,203

Fees and commission expensePenalty fees

Account management fees

Other fees income

Fees and commission expenseManagement fees' (931,282)Custody fees (19,521)Trustee fees (61,499)Other expenses (137,308)Net fee and commission expense (805,487). The manager fee has been calculated as 25 basis points (inclusive of GST) on the average month bond balance.

111,41356,962

175,748

PUMA MASTERFUND P-16 2011 Financial Report 12

For

per

sona

l use

onl

y

PUMA MASTERFUND P-16

Notes to the financial statements (continued)for the period ended 31 March 2011

2011$

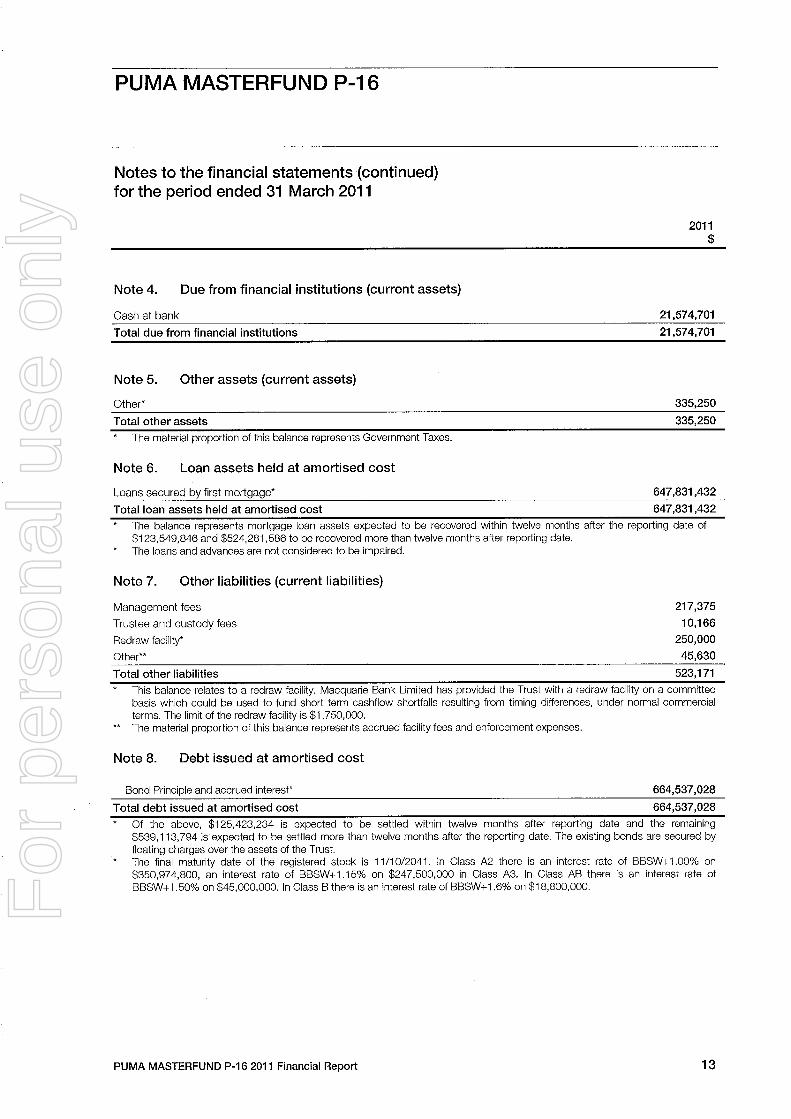

Note 4. Due from financial institutions (current assets)

Cash at bank

Total due from financial institutions

21,574,701

21,574,701

Note 5. Other assets (current assets)

Other*

Total other assetsThe material proportion of this balance represents Government Taxes.

335,250

335,250

Note 6. Loan assets held at amortised cost

Loans secured by first mortgage* 647,831,432Total loan assets held at amortised cost 647,831,432

The balance represents mortgage loan assets expected to be recovered within twelve months after the reporting date of$123,549,846 and $524,281,586 to be recovered more than twelve months after reporting date.The loans and advances are not considered to be impaired.

Note 7. Other liabilities (current liabilities)

Management fees 217,375Trustee and custody fees 10,166Redraw facility* 250,000Other" 45,630Total other liabilities 523,171

This balance relates to a redraw facility. Macquarie Bank Limited has provided the Trust with a redraw facility on a committedbasis which could be used to fund short term cashflow shortfalls resulting from timing differences, under normal commercialterms. The limit of the redraw facility is $1,750,000.The material proportion of this balance represents accrued facility fees and enforcement expenses.

Note 8. Debt issued at amortised cost

Bond Principle and accrued interest 664,537,028Total debt issued at amortised cost 664,537,028

Of the above, $125,423,234 is expected to be settled within twelve months after reporting date and the remaining$539,113,794 is expected to be settled more than twelve months after the reporting date. The existing bonds are secured byfloating charges over the assets of the Trust.The final maturity date of the registered stock is 11/10/2041. In Class A2 there is an interest rate of BBSW+ 1.00% on$350,974,800, an interest rate of BBSW+ 1.15% on $247,500,000 in Class A3. In Class AB there is an interest rate ofBBSW+ 1.50% on $45,000,000. In Class B there is an interest rate of BBSW+ 1.6% on $18,800,000.

PUMA MASTERFUND P-16 2011 Financial Report 13

For

per

sona

l use

onl

y

PUMA MASTERFUND P-16

Notes to the financial statements (continued)for the period ended 31 March 2011

2011$

Note 9. Net liabilities attributable to unitholders (non-current)

Net liabilities attributable to unitholders are represented by:

Opening balanceIssue of units

Net operating income

Distributions paid

Distributions payable

Total liabilities attributable to unitholders

The Income Unit holder is entitled to the residual income of the Trust.

1003,639,716

851,821

(4,663,409)

(171,772)

Note 10. Notes to the statement of cash flows

Reconcilation of cash and cash equivalents

Cash at the end of the period as shown in the cash flow statement is reconciled to related items in the statement of financial

position as follows:

Due from Financial Institutions'

Cash and cash equivalents at the end of the period

21,574,701

21,574,701

Reconciliation of profit to net cash flows from operating activities

Net operating profit

Changes in assets and liabilities

Change in fees and commissions receivable

Change in fees and commissions payable

Change in interest receivable

Change in interest payable

Change in trading securities and other financial instruments

Net cash flows from operating activities, Includes cash at bank as per Note 4.

3,639,716

(334,545)272,469

(3,777,270)2,262,228

189,547

2,252,143

PUMA MASTERFUND P-16 2011 Financial Report 14

For

per

sona

l use

onl

y

PUMA MASTERFUND P-16

Notes to the financial statements (continued)for the period ended 31 March 2011

Note 11. Related party information

Trust Manager

The Trust Manager of PUMA MASTERFUND P-16 is Macquarie Securitisation Limited (MSL). The immediate parent entity of

Macquarie Securitisation Limited is Macquarie Bank Limited and ultimate chief entity is Macquarie Group Limited.

Trustee

The Trustee of the Trust is Perpetual Limited.

Key Management Personnel

Key management personnel include persons who were Directors of Macquarie Securitisation Limited at any time during thefinancial year as follows:

Name Appointed

James Casey 3/03/2010

Jason Finlay 11/07/2008

Frank Nicholas Ganis 8/08/1995

Mark Hurford Brennan 3/03/2010

Adrian Philip Bentley 1/09/2009

Matthew James O'hare 10/03/2004

Resigned

24/05/2011

24/05/2011

2/05/2011

Remuneration to key management personnel

The KMPs did not receive any benefits or consideration in connection with the management of the Trust. All benefits thatwere received by the KMPs were solely related to other services performed with respect to their employment by MacquarieGroup Limited.

Transactions with related parties

Transactions between the Trust and Macquarie Securitisation Limited result from normal dealings with that company as theTrust Manager. Management fees paid or payable are disclosed in notes 3 and 7.

The sole income unitholder in the Trust is Macquarie Securitisation Limited.

There are derivative transactions entered for economic hedging on an arm's length basis through companies within theMacquarie Group.

The Trust has pre-approved redraw limits of $1,750,000 from Macquarie Bank Limited an entity in Macquarie Groupdisclosed in note 7. The Trust has drawn $250,000 out of this facility.

A related party is the holder of the class B notes.

All other transactions with related entities were made on normal commercial terms and conditions and at market ratesexcept where indicated.

Note 12. Contingent liabilities and assetsThe Trust has no commitments or contingent assets/liabilities which are individually material or a category of commitments

or contingent liabilities which are materiaL.

Note 13. Audit and other services provided by PricewaterhouseCoopersThe cost of auditors' remuneration for auditing services of $9,424 has been borne by Macquarie Group Services Australia

Pty Limited, a wholly-owned subsidiary within the Macquarie Group. The auditors received no other benefits.

Note 14. Events occurring after the reporting dateThere were no material post start events occurring after the reporting date requiring disclosure in these financial statements.

PUMA MASTER FUND P-16 2011 Financial Report 15

For

per

sona

l use

onl

y

PUMA MASTERFUND P-16

Directors' declaration

We report that in our opinion:

(a) The Trust has operated for the period ended 31 March 2011 in accordance with the provisions of the Trust Deed

dated 13 July 1990, as amended;

(b) the accompanying special purpose financial report of the Trust as set out on pages 3 to 15 are properly drawn up inaccordance with the Trust Deed so as to present fairly the financial position of the Trust as at 31 March 2011 and

the result of its operations for the financial period ended on that date; and

(c) there are reasonable grounds to believe that the Trust will be able to pay its debts as and when they become due

and payable.

The special purpose financial report of the Trust has been prepared in accordance with accounting policies described in

Note 2 and the requirements of the Trust Deed.

Signed in accordance with a resolution of the Directors of the Trust Manager on 28th June 2011.

Jli,,-yfÖ ÑFI r-Ur"-

Director

Sydney

28th June 2011

PUMA MASTERFUND P-16 2011 Financial Report 16

For

per

sona

l use

onl

y

fJcEWkRHOusf(mPERSIPricewaterhouseCoopersABN 52 780 433 757

Independent auditor's report to the unitholders of PUMAMASTERFUND P.16

Darling Park Tower 2201 Sussex StreetGPO BOX 2650SYDNEY NSW 1171DX 77 SydneyAustraliaTelephone +61 2 8266 0000Facsimile +61 282669999ww.pwc.com/au

Report on the financial report

We have audited the accompanying financial report, being a special purpose financial report, ofPUMA MASTERFUND P-16 (the "trust"), which comprise the statement of financial position as at31 March 2011, the statement of comprehensive income, statement of changes in net assetsattributable to unitholders and statement of cash flows for the year then ended, a summary ofsignificant accounting policies, other explanatory notes and the trustees' declaration.

The responsibility of the directors of the manager for the financial report

The directors of the manager of the trust, Macquarie Securitisation Limited, are responsible for thepreparation and fair presentation of the. financial report and have determined that the accountingpolicies described in Note 1 to the financial statements, which form part of the financial report, areappropriate to meet the requirements of the trust deed dated 21 December 2007. The responsibilityof the directors of the manager also includes establishing and maintaining internal control relevantto the preparation and fair presentation of the financial report that is free from materialmisstatement, whether due to fraud or error; selecting and applying appropriate accounting

policies; and making accounting estimates that are reasonable in the circumstances.

Auditor's responsibilty

Our responsibility is to express an opinion on the financial report based on our audit. No opinion isexpressed as to whether the accounting policies used, as described in Note 1, are appropriate tomeet the needs of the unitholders. We conducted our audit in accordance with Australian AuditingStandards. These Auditing Standards require that we comply with relevant ethical requirementsrelating to audit engagements and plan and perform the audit to obtain reasonable assurance

whether the financial report is free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts anddisclosures in the financial report. The procedures selected depend on the auditor's judgement,including the assessment of the risks of material misstatement of the financial report, whether dueto fraud or error. In making those risk assessments, the auditor considers internal control relevantto the trust's preparation and fair presentation of the financial report in order to design auditprocedures that are appropriate in the circumstances, but not for the purpose of expressing anopinion on the effectiveness of the trust's internal control. An audit also includes evaluating thereasonableness of accounting estimates made by the directors of the manager, as well asevaluating the overall presentation of the financial report.

The financial report has been prepared for distribution to unit holders for the purpose of fulfilling thefinancial reporting obligations of the directors of the manager under the trust deed. We disclaimany assumption of responsibility for any reliance on this audit report or on the financial report towhich it relates to any person other than the unitholders, or for any purpose other than that forwhich it was prepared.

Liability limited by a scheme approved under Professional Standards Legislation

For

per

sona

l use

onl

y

fJcfWTfRHOUsE(aJPERS I

Independent auditor's report to the unitholders of PUMA MASTERFUND P.16(continued)

Our audit did not involve an analysis of the prudence of business decisions made by the directorsor management of the manager of the trust.

,

We believe that the audit evidence we have obtained is sufficient and appropriate to provide abasis for our audit opinion.

Auditor's opinion

In our opinion, the financial report presents fairly, in all material respects, the financial position ofPUMA MASTERFUND P-16 as of 31 March 2011 and its financial performance for the year thenended in accordance with the accounting policies described in Note 1 to the financial statements.

Basis of Accounting and Restriction on Distribution and Use

Without modifying our opinion, we draw attention to Note 2 to the financial report, which describesthe basis of accounting. The financial report has been prepared to assist PUMA MASTERFUND P-16 to meet the requirements of the directors of the manager under the trust deed. As a result, thefinancial report may not be suitable for another purpose. Our report is intended solely for theunitholders of PUMA MASTERFUND P-16.

'V~pQ.PricewaterhouseCoopers

.tßc(lJCJ Heath

PartnerSydney

28th June 2011

For

per

sona

l use

onl

y