for personal use only - asx · for personal use only. disclaimer . this presentation does not...

TRANSCRIPT

Developing a Brazilian Iron Ore Business

Darren Gordon, Managing Director November, 2011

For

per

sona

l use

onl

y

Disclaimer

This presentation does not constitute investment advice. Neither this presentation nor the information contained in it constitutes an offer, invitation, solicitation or recommendation in relation to the purchase or sale of shares in any jurisdiction. This presentation does not take into account any person's particular investment objectives, financial resources or other relevant circumstances and the opinions and recommendations in this presentation are not intended to represent recommendations of particular investments to particular persons. All securities transactions involve risks, which include (among others) the risk of adverse or unanticipated market, financial or political developments. To the fullest extent permitted by law, the Company does not make any representation or warranty, express or implied, as to the accuracy or completeness of any information, statements, opinions, estimates, forecasts or other representations contained in this presentation. No responsibility for any errors or omissions from this presentation arising out of negligence or otherwise is accepted. This presentation may include forward looking statements. Forward looking statements are only predictions and are subject to risks, uncertainties and assumptions which are outside the control of Centaurus Metals. These risks, uncertainties and assumptions include commodity prices, currency fluctuations, economic and financial market conditions in various countries and regions, environmental risks and legislative, fiscal or regulatory developments, political risks, project delay or advancement, approvals and cost estimates. Actual values, results or events may be materially different to those expressed or implied in this presentation. Given these uncertainties, readers are cautioned not to place reliance on forward looking statements. Any forward looking statements in this presentation speak only at the date of issue of this presentation. Subject to any continuing obligations under applicable law and the ASX Listing Rules, Centaurus Metals does not undertake any obligation to update or revise any information or any of the forward looking statements in this presentation or any changes in events, conditions or circumstances on which any such forward looking statement is based. The information in this report that relates to Exploration Results and Mineral Resources is based on information compiled by Roger Fitzhardinge who is a Member of the Australasia Institute of Mining and Metallurgy and Volodymyr Myadzel who is a Member of Australian Institute of Geoscientists. Roger Fitzhardinge is a permanent employee of Centaurus Metals Limited and Volodymyr Myadzel is the Senior Resource Geologist of BNA Consultoria e Sistemas Limited, independent resource consultants engaged by Centaurus Metals. Roger Fitzhardinge and Volodymyr Myadzel have sufficient experience which is relevant to the style of mineralization and type of deposit under consideration and to the activity which they are undertaking to qualify as a Competent Person as defined in the 2004 Edition of the ‘Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserve’. Roger Fitzhardinge and Volodymyr Myadzel consent to the inclusion in the report of the matters based on their information in the form and context in which it appears. The information in this report that relates to Ore Reserves is based on information compiled by Beck Nader who is a professional Mining Engineer and a Member of Australian Institute of Geoscientists. Beck Nader is the Managing Director of BNA Consultoria e Sistemas Ltda and is a consultant to Centaurus. Beck Nader has sufficient experience, which is relevant to the style of mineralization and type of deposit under consideration and to the activity, which he is undertaking to qualify as a Competent Person as defined in the 2004 Edition of the ‘Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserve’. Beck Nader consents to the inclusion in the report of the matters based on their information in the form and context in which it appears.

2

For

per

sona

l use

onl

y

Bahia

Minas Gerais

Brazilian Iron Ore Business Centaurus Metals’ focus is to:

Develop & Operate a number of low cost mines.

Be known for high grade & consistent quality products.

Be one of a limited number of preferred suppliers to the Brazilian domestic steel industry.

Have commenced production at Jambreiro Project by end of 2013 at annualised production rate of at least 2mt of high grade hematite into the domestic market.

Complete Feasibility Study on Serra da Lontra Project based on export sales at initial rate of 1 to 2mtpa.

Secure new projects within trucking distance of the port/end customers to facilitate sales without incurring large amounts of capex on transport infrastructure.

Leverage off iron ore business to secure quality manganese projects.

3

For

per

sona

l use

onl

y

Company Structure

4

ASX CODE : CTM

* Ex prices from 3.125 cents to 28.5 cents (weighted average ex price 8.23 cents)

Shareholding

8%

Atlas Iron Ltd ** 19.9%

Directors & Management

Top 20 (Inc. Atlas Iron Ltd) 48%

Capital Structure

17.6m

$86.8m

Cash at bank (30 Sept 2011) $23.4m

Debt NIL

Enterprise Value $63.4m

Shares on Issue 133.5m

Options*

Share Price $0.65

Market Capitalisation

** Atlas Iron Ltd is an Australian iron ore exploring and producing company listed on the ASX (ASX code: AGO), currently producing at a rate of 6Mtpa. Since listing in 2004 Atlas has grown rapidly and is now a member of the S&P/ASX100 index. Atlas employs over 450 persons, has a market capitalisation of circa $3.0 billion, cash reserves of A$397 million (31 July 2011) and no debt.

For

per

sona

l use

onl

y

Centaurus Metals Board & Key Personnel DIDIER MURCIA Non-Executive Chairman 25 years corporate and resource industry experience. Specialises in strategic, corporate and commercial advice. Extensive iron ore experience as Director of Gindalbie Metals. Chairman of Rift Valley Resources and Director of ASX Listed, Gryphon Resources and London Listed, Aminex Plc. Didier is also Honory Consul in Australia for the Republic of Tanzania

DARREN GORDON Managing Director Chartered Accountant with over 16 years resource industry experience with particular emphasis on resource funding and structuring. 9 years experience as CFO of Gindalbie Metals. Has sound understanding of Brazil operating environment over the last 4 years

PETER FREUND Operations Director 40 years engineering experience with BHP, MIM, Thiess and Gindalbie. In charge of operating company that built the Alumbrera Copper project in Argentina. Most recently Chief Operating Officer for the Karara Iron Ore Project in the mid west region of WA. Strong knowledge of beneficiated iron ore, South American projects and bulk commodities

KEITH MCKAY Non-executive Director Geologist with 40 years technical and corporate experience. Previously Chairman of Gindalbie Metals and MD of Gallery Gold Ltd and Battle Mountain (Aust) Inc. Current Non Executive Director of Rift Valley Resources

RICHARD HILL Non-executive Director 20 years resource industry experience as both a solicitor and a geologist. Founding director of Centaurus Resources. Current director of YTC Resources with extensive network into Asian markets. Director of newly formed dedicated resource Investment Fund, Westoria Capital.

MARK HANCOCK Non-executive Director 25 years professional experience in senior financial roles with Lend Lease Corporation Ltd, Woodside Petroleum Ltd and Premier Oil plc. Since 2006 he has held senior roles at Atlas Iron Ltd, most recently as Chief Commercial Officer where he oversees management of the Company’s financial resources and iron ore customer base.

GEORGE JONES Strategic Consultant More than 35 years experience in the mining, banking and finance industries. Previously executive Chairman of Portman Mining Ltd and currently Chairman of two iron ore businesses, Gindalbie Metals (~600 million market cap) and Sundance Resources (~1.2 billion market cap).

5

Board holds strong equity position in the Company and is very

experienced in iron ore

For

per

sona

l use

onl

y

Centaurus Metals Board & Key Personnel

GEOFF JAMES - CFO & Company Secretary Chartered Accountant and Chartered Secretary with over 20 years financial experience. Previously Chief Financial Accountant for Clough engineering. Retains strong knowledge of Australian listing rules and International Accounting Standards

KLAUS PETERSEN - Chief Geologist – New Projects Brazilian national who has operated as Country Manager for CTM previously. Klaus hold a post doctorate in Geology from UWA and has over 20 years experience in the identification of new project opportunities within Brazil and other South American jurisdictions. Klaus retains a strong network of contacts within the mining industry in Brazil, particularly in Belo Horizonte. Strong English skills.

BRUNO SCARPELLI - GM – Environment & OH&S Brazilian national who previously worked for Vale in key environmental approvals post securing infrastructure approvals for the world class Carajas iron ore operations. Has previously worked for leading environmental consulting practice, Brandt, in Belo Horizonte. Bruno is a qualified translator having studied in the USA and fluent in English. Over 10 years environmental approvals experience

ROGER FITZHARDINGE - GM – Exploration & Evaluation Over 12 years experience as a geologist. Previously worked for Mirabela Nickel in Brazil for over 5 years and is fluent in Portuguese. Has previously worked for Rio Tinto as part of their iron ore operations in the Pilbara. Strong technical skills and very much a hands on approach to management of his geological team.

LUIZ CARLOS NORONHA JR. - Legal Counsel & Administrator Brazilian National, graduated from the Law School of Conselheiro Lafaiete, Minas Gerais State and has 12 years of experience, initially, in public and land administration with city hall and state government and then in private law practices dealing extensively with, tax, commercial law and land access for mining company clients.

DIOGENES VIAL Strategic Project Geologist Diogenes is highly regarded and well respected geologist with 35 years of experience in exploration management. Diogenes has extensive experience in training, development and management of teams, management of feasibility studies and the evaluation of mineral prospects. Diogenes spent 8 years as Chief Geologist for DOCEGEO (former exploration division of VALE) and 6 years as Iron and Manganese Exploration Manager/Coordinator in Brazil for VALE. He previously worked 6 years with Mineracao Morro Velho (now Anglo Gold) as underground geologist. He is fluent in Portuguese, English and Spanish.

6

Strong Management team predominantly based in the

Belo Horizonte office experienced in developing Brazilian resource projects

For

per

sona

l use

onl

y

Brazil

Latin America’s largest economy.

Rapidly growing population (currently ~200 million).

Over ~ 50% of population now considered middle class. ~4th largest car manufacturer.

Predicted growth of 4-5% in 2011.

US$830b infrastructure spend.

Hosting FIFA World Cup in 2014 and the Olympic Games in 2016.

Top 10 global steel producer (~ 39Mt).

Brazil exports > 300Mt per annum of iron ore.

Centaurus Metals is one of the few ASX listed companies providing direct exposure to the rapid development of Brazil

7

For

per

sona

l use

onl

y

International Investment into Brazil

A number of multi national companies have recently announced expansion plans into Brazil.

8

Spanish Telecom giant, Telefonica, to invest in growing telecommunication demand over next 3 years $14.6 billion

Foxconn (Apple’s IPad & IPhone manufacturer) to build new production facilities in Brazil $12.0 billion

Forbes & Manhattan to invest in a number of resource projects in Brazil through to 2016 $6.5 billion

Ford to expand manufacturing in Brazil through to 2015 $2.8 billion

Bunge – the world’s second largest sugar trader to boost sugar and ethanol production in Brazil over the next 5 years $2.5 billion

Fiat to invest in new factory in north east Brazil $1.8 billion

Renault & Volkswagen to expand manufacturing operations $1.2 billion

General Motors to increase Brazilian production capacity by 2012 $1.0 billion

Westfield to invest in shopping centres in Brazil $0.5 billion

For

per

sona

l use

onl

y

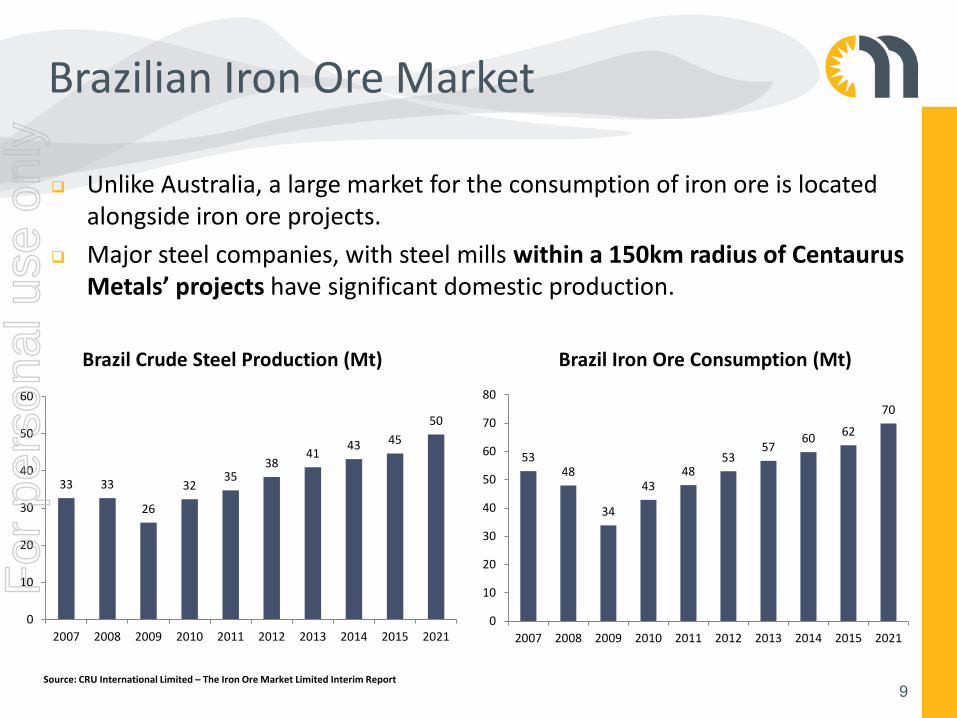

Brazilian Iron Ore Market

Unlike Australia, a large market for the consumption of iron ore is located alongside iron ore projects.

Major steel companies, with steel mills within a 150km radius of Centaurus Metals’ projects have significant domestic production.

9

33 33

26

32 35

38 41 43 45

50

0

10

20

30

40

50

60

2007 2008 2009 2010 2011 2012 2013 2014 2015 2021

Brazil Crude Steel Production (Mt)

53 48

34

43 48

53 57

60 62

70

0

10

20

30

40

50

60

70

80

2007 2008 2009 2010 2011 2012 2013 2014 2015 2021

Brazil Iron Ore Consumption (Mt)

Source: CRU International Limited – The Iron Ore Market Limited Interim Report

For

per

sona

l use

onl

y

Centaurus Metals’ Projects

10

For

per

sona

l use

onl

y

11

Domestic Iron Ore Business “Supplying Iron Ore to Brazil’s Steel Mills”

For

per

sona

l use

onl

y

Domestic Iron Ore Business

Targeting production from a number of low OpEx, low CapEx mines, in close proximity to established infrastructure.

Centaurus Metals is working towards: production at a rate of 2mtpa by the end of 2013 growing to 3mtpa, to be sold

into Brazil’s domestic steel mills for operating cash flows anticipated to be circa $150 million per annum.

becoming a consistent and reliable supplier of high quality, low impurity iron ore to domestic steel mills.

Current Focus: Jambreiro Iron Ore Project.

Other Domestic Project’s Passabem Iron Ore Project. Itambé Iron Ore Project.

12

For

per

sona

l use

onl

y

Itabirite Ore....

Metamorphosed iron formation composed of iron oxides with abundant quartz.

Iron Quadrangle itabirites typically comprise hematite.

Lower ROM grade than other sources of hematite (averaging 30-50% Fe).

Extremely well suited to low cost beneficiation.

Can be upgraded to 63-68% Fe via simple and low cost beneficiation processes.

Final product a high quality hematite product with low contaminants.

A major source of iron ore production in Brazil…

13

For

per

sona

l use

onl

y

Domestic Production - Jambreiro

14

For

per

sona

l use

onl

y

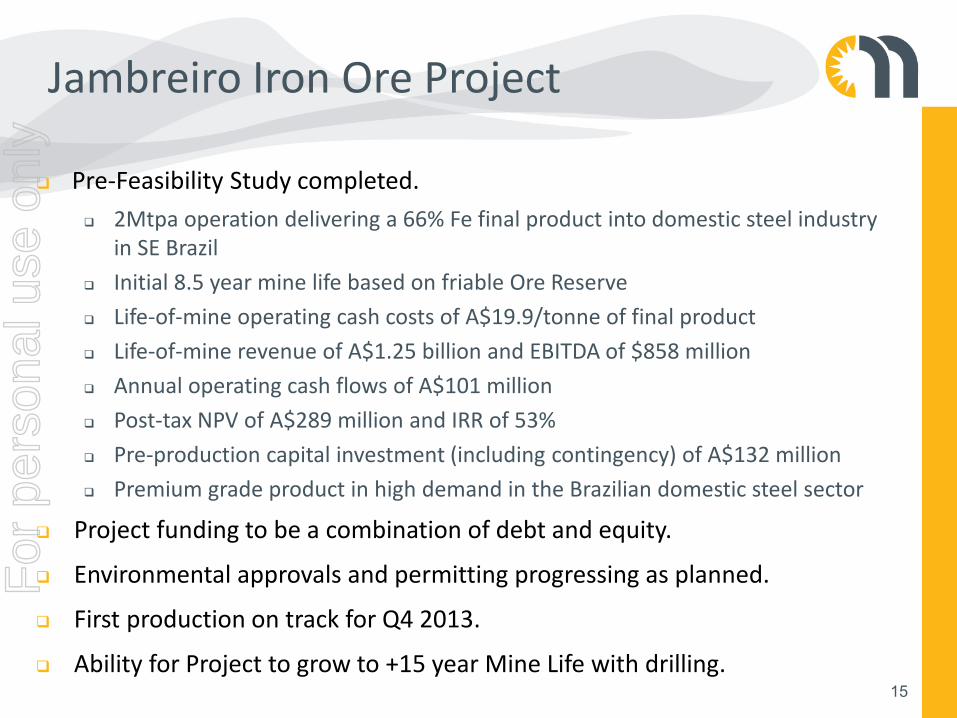

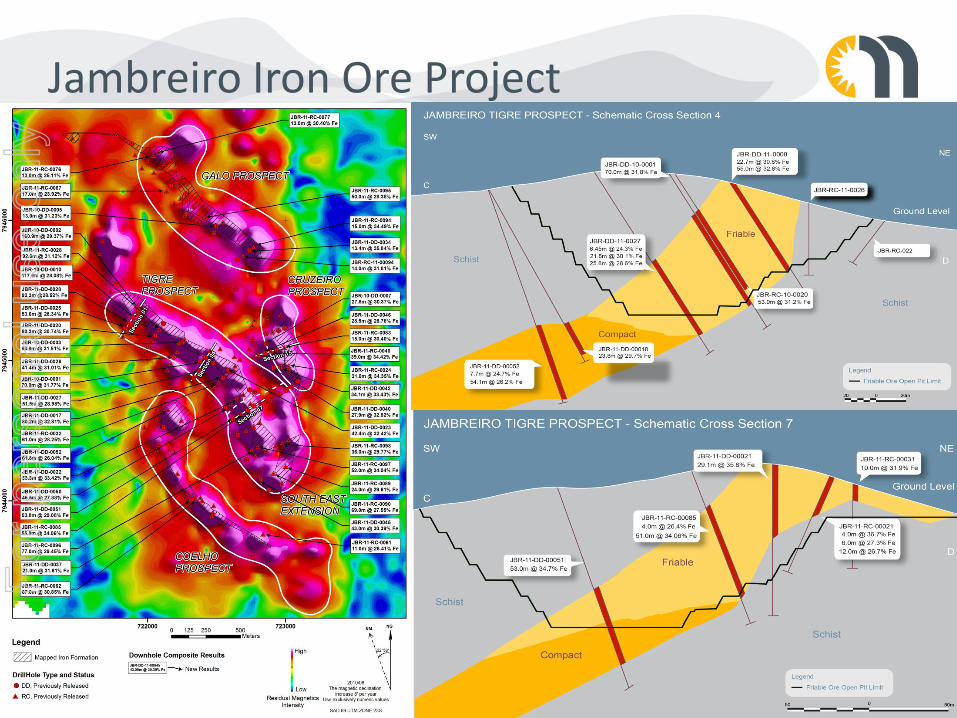

Jambreiro Iron Ore Project

Pre-Feasibility Study completed. 2Mtpa operation delivering a 66% Fe final product into domestic steel industry

in SE Brazil Initial 8.5 year mine life based on friable Ore Reserve Life-of-mine operating cash costs of A$19.9/tonne of final product Life-of-mine revenue of A$1.25 billion and EBITDA of $858 million Annual operating cash flows of A$101 million Post-tax NPV of A$289 million and IRR of 53% Pre-production capital investment (including contingency) of A$132 million Premium grade product in high demand in the Brazilian domestic steel sector

Project funding to be a combination of debt and equity.

Environmental approvals and permitting progressing as planned.

First production on track for Q4 2013.

Ability for Project to grow to +15 year Mine Life with drilling. 15

For

per

sona

l use

onl

y

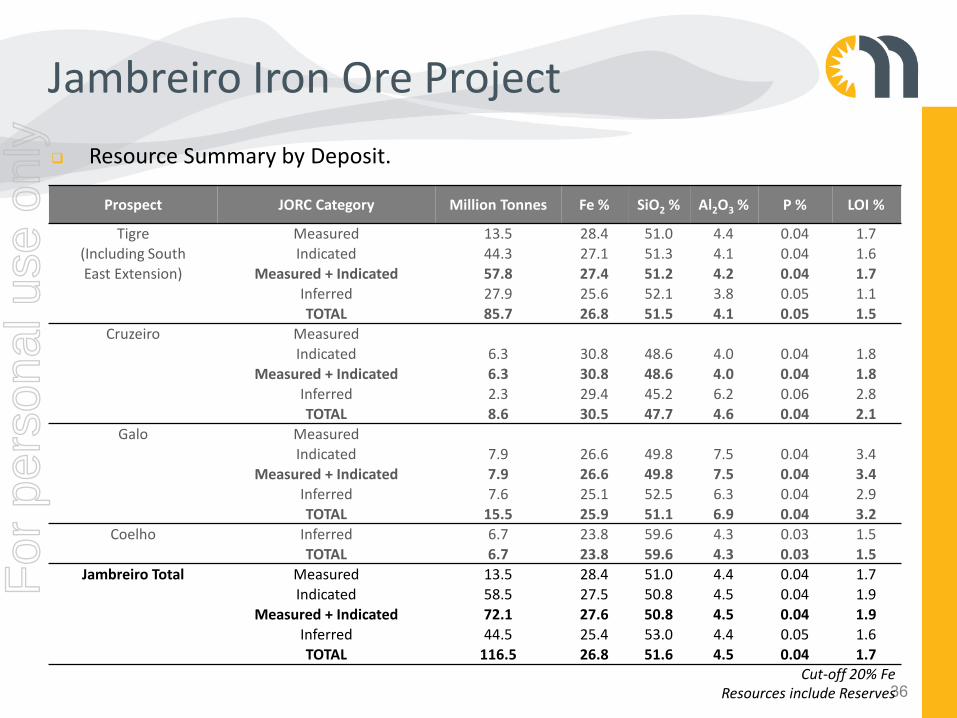

Jambreiro Iron Ore Project Mineral Resources

Ore Reserves

16

Prospect JORC Category Million Tonnes Fe % SiO2 % Al2O3 % P % LOI %

Jambreiro Friable Proven 12.0 28.6 51.2 4.5 0.03 1.7

Probable 37.0 28.0 51.0 5.2 0.04 2.2

TOTAL 49.0 28.2 51.1 5.0 0.04 2.1

Cut-off 20% Fe

Prospect JORC Category Million Tonnes Fe % SiO2 % Al2O3 % P % LOI %

Friable Measured 12.1 28.6 51.2 4.6 0.03 1.7 Indicated 39.9 27.9 51.1 5.3 0.04 2.2 Measured + Indicated 52.1 28.0 51.1 5.1 0.04 2.1 Inferred 15.0 24.9 55.2 5.3 0.04 2.1 TOTAL 67.0 27.3 52.0 5.1 0.04 2.1

Compact Measured 1.4 27.4 48.8 2.8 0.05 1.6 Indicated 18.6 26.6 50.2 3.0 0.06 1.2 Measured + Indicated 20.0 26.6 50.1 3.0 0.05 1.3 Inferred 29.5 25.7 51.9 4.0 0.05 1.3 TOTAL 49.5 26.1 51.1 3.6 0.05 1.3 TOTAL 116.5 26.8 51.6 4.5 0.04 1.7

Cut-off 20% Fe Resources include Reserves

For

per

sona

l use

onl

y

Jambreiro Iron Ore Project

17

For

per

sona

l use

onl

y

18

Product Quality Fe% SiO2% Al2O3% P% Mass Recovery %

PROCESS – WET MAGNETIC SEPARATION

FRIABLE ORE Head Grade 28.2 51.1 5.0 0.04 Beneficiated Product 66.6 2.8 0.7 0.02 37

COMPACT MINERALISATION Head Grade 25.0 55.9 2.2 0.07 Beneficiated Product 66.2 3.7 0.9 0.01 35

Jambreiro Iron Ore Project F

or p

erso

nal u

se o

nly

Jambreiro Iron Ore Project

Process Flowsheet

19

For

per

sona

l use

onl

y

Jambreiro Iron Ore Project

Key Pre-Feasibility Study Assumptions

20

Key Assumptions

Ore Reserves 49.0 Mt

Grade 28.2% Fe

Mass Recovery per dry tonne 37.6%

Reserve – Final Product 17.1 Mt

Grade 66% Fe

Waste Movement 46.0 Mt

Total Material Movement 95.0 Mt

Waste to Ore Ratio (LOM) 0.94 to 1

Production Rate 2Mtpa

BRL to AUD Exchange Rate 1.65 to 1

AUD to USD Exchange Rate 1 to 1

Sales Price – Mine Gate US$73 per DMT

Discount Rate 8%

For

per

sona

l use

onl

y

Jambreiro Iron Ore Project

Site Layout

Three pits and waste dump

Processing Plant

Administration Area

Tailings Dam

21

For

per

sona

l use

onl

y

Jambreiro Iron Ore Project Capital and Operating Costs

22

Operating Costs A$ per Tonne Product

Mining (Including Equipment Leasing) 8.1

Sizing, Screening & Beneficiation 8.8

Administration 1.4

Contingency 1.6

OPERATING CASH COST 19.9

Capital Equipment Total (A$ M)

DIRECT COSTS

Sizing & Screening 20.9

Beneficiation 38.4

Product Handling 10.0

Tails Management & Water Recovery 9.4

Water Supply 6.8

Power Supply 5.1

Site Infrastructure & Support Services 15.0

Commissioning, Spares & First Fill 6.1

TOTAL DIRECT CAPEX 111.7

Detailed Engineering & Construction Management 8.1

Contingency 11.8

TOTAL CAPEX 131.6

A$66/t of annual production capacity.

Main processing in WHIMS circuit.

Approximately half of capex cost is physical equipment items.

Capex and Opex benefits from highly friable, naturally liberated, iron ore at Jambreiro.

Key opex inputs:

- Power A$0.09 per Kw/h

- Diesel A$1.06/Litre

For

per

sona

l use

onl

y

Jambreiro Iron Ore Project

Base Case Pricing Assumption – US$73 per tonne of Product

Sensitivity Analysis

23

175 200 225 250 275 300 325 350 375 400

Capital Expenditure

Operating Expenditure

Discount Rate

Foreign Exchange

Price (FOB Mine)

NPV (A$M)

NPV Sensitivity

For

per

sona

l use

onl

y

Resource Summary – Domestic Projects Centaurus has assembled a strong project and resource base in Brazil of

Itabirite mineralisation that upgrades to a high grade hematite product.

At a Mass Recovery of 35%, using a 2 stage magnetic separation process, In Situ Resources generate over 55Mt of high grade hematite product (+66% Fe).

Beneficiation test work shows high grade hematite product can be produced from all Domestic projects.

Development Capex to be low by international standards as little to no infrastructure costs.

24

Project M&I Component Million Tonnes Fe % SiO2 % Al2O3 % P % LOI %

Jambreiro* 62% 116.5 26.8 51.6 4.50 0.04 1.70

Passabém** 7% 39.0 31.0 53.6 0.82 0.07 0.13

Itambé** 47% 10.0 36.6 39.1 3.98 0.05 2.38

TOTAL 165.5 28.4 51.3 3.60 0.05 1.37 *20% Fe cut-off grade applied ** 27% Fe cut-off grade applied

For

per

sona

l use

onl

y

Export Business “Supplying Carbon Steel Products to the

World Market”

25

For

per

sona

l use

onl

y

Export Business

26

For

per

sona

l use

onl

y

Export Business – Ilhéus Export Hub

Most Brazilian focussed iron ore companies have exploration targets of +1bn tonnes. Small projects close to key infrastructure have been overlooked. Centaurus is developing a tenement package around the Serra da Lontra Project that

is less than 150 kilometres from:

An existing port ; Ilhéus A planned port; Porto Sul Sealed Roads An open access railway currently under

construction.

Ongoing assessment of new Project opportunities to support Ilheus Export Hub business.

27

For

per

sona

l use

onl

y

Serra da Lontra Iron Ore Project

28

For

per

sona

l use

onl

y

Serra da Lontra Iron Ore Project

Mapping and sampling has shown a higher grade nature of itabirite mineralisation at Serra da Lontra. Average grade 45% to 47% Fe.

29

For

per

sona

l use

onl

y

Serra da Lontra Iron Ore Project

Newly acquired Project; cornerstone of the Ilhéus Export Hub.

140 kilometres by sealed road from export port of Ilheus.

Provides opportunity to start a relatively low capex export business at 1-2 Mtpa.

Exploration Target – 30 to 50 Mt @ 35 to 45% Fe.

Potential to produce 15 to 25 Mt of high grade hematite.

Estimate costs to port US$40 to US$50 per tonne of concentrate.

Bahia State Government very supportive of CTM and strong desire to build iron ore industry in Bahia.

Exploration work underway. Drilling to commence in December 2011 on receipt of drilling licence.

30

For

per

sona

l use

onl

y

Centaurus- 2011/2012 Activities

In 2012 Centaurus Metals main areas of focus will be:

Feasibility studies at the Jambreiro Project.

LOI’s from domestic iron ore consumers.

Exploration drilling at existing Ilhéus Export Hub projects.

Exploration drilling on Manganese Projects

Adding to identified prospects within Ilhéus Export Hub.

Securing access to port capacity for export projects.

Progressing Environmental & Department of Mines approvals for all Projects.

Seeking further near term production assets.

31

For

per

sona

l use

onl

y

Summary

Strong results of Jambreiro Pre-Feasibility Study show excellent value equation for investors.

Highly experienced team with strong global experience in the financing, development and operation of iron ore projects.

Very supportive major shareholder experienced in delivery of low capex iron ore projects.

Newly acquired export project opportunity close to existing common user port.

2mpta domestic production rate by the end of 2013 with export production initially targeting 1-2mtpa in late 2014.

Continuously assessing other opportunities (Fe and Mn) to grow the Brazilian carbon steel business.

32

Centaurus Metals is one of the few ASX listed companies providing direct exposure to the rapid

development of Brazil.

For

per

sona

l use

onl

y

Developing a Brazilian Iron Ore Business

Contacts: Darren Gordon Peter Freund Managing Director Operations Director [email protected] [email protected] (+618) 9420 4000 (+5531) 3262 2037

For

per

sona

l use

onl

y

APPENDICES

For

per

sona

l use

onl

y

Jambreiro Iron Ore Project

35

Reserve Summary by Deposit.

Prospect JORC Category Million Tonnes Fe % SiO2 % Al2O3 % P % LOI %

Tigre Proven 12.0 28.6 51.2 4.5 0.03 1.7

Probable 25.7 27.8 51.7 4.9 0.04 1.9

TOTAL 37.7 28.0 51.6 4.8 0.04 1.9

Cruzeiro Proven

Probable 4.5 31.0 49.1 3.9 0.04 1.8

TOTAL 4.5 31.0 49.1 3.9 0.04 1.8

Galo Proven

Probable 6.8 27.1 49.5 7.4 0.04 3.3

TOTAL 6.8 27.1 49.5 7.4 0.04 3.3

Jambreiro Total Proven 12.0 28.6 51.2 4.5 0.03 1.7

Probable 37.0 28.0 51.0 5.2 0.04 2.2

TOTAL 49.0 28.2 51.1 5.0 0.04 2.1

Friable Proven 12.0 28.6 51.2 4.5 0.03 1.7

Probable 37.0 28.0 51.0 5.2 0.04 2.2

TOTAL 49.0 28.2 51.1 5.0 0.04 2.1 Cut-off 20% Fe

For

per

sona

l use

onl

y

Jambreiro Iron Ore Project

36

Resource Summary by Deposit.

Prospect JORC Category Million Tonnes Fe % SiO2 % Al2O3 % P % LOI %

Tigre Measured 13.5 28.4 51.0 4.4 0.04 1.7 (Including South Indicated 44.3 27.1 51.3 4.1 0.04 1.6 East Extension) Measured + Indicated 57.8 27.4 51.2 4.2 0.04 1.7

Inferred 27.9 25.6 52.1 3.8 0.05 1.1 TOTAL 85.7 26.8 51.5 4.1 0.05 1.5

Cruzeiro Measured Indicated 6.3 30.8 48.6 4.0 0.04 1.8

Measured + Indicated 6.3 30.8 48.6 4.0 0.04 1.8 Inferred 2.3 29.4 45.2 6.2 0.06 2.8 TOTAL 8.6 30.5 47.7 4.6 0.04 2.1

Galo Measured Indicated 7.9 26.6 49.8 7.5 0.04 3.4

Measured + Indicated 7.9 26.6 49.8 7.5 0.04 3.4 Inferred 7.6 25.1 52.5 6.3 0.04 2.9 TOTAL 15.5 25.9 51.1 6.9 0.04 3.2

Coelho Inferred 6.7 23.8 59.6 4.3 0.03 1.5 TOTAL 6.7 23.8 59.6 4.3 0.03 1.5

Jambreiro Total Measured 13.5 28.4 51.0 4.4 0.04 1.7 Indicated 58.5 27.5 50.8 4.5 0.04 1.9

Measured + Indicated 72.1 27.6 50.8 4.5 0.04 1.9 Inferred 44.5 25.4 53.0 4.4 0.05 1.6

TOTAL 116.5 26.8 51.6 4.5 0.04 1.7 Cut-off 20% Fe

Resources include Reserves

For

per

sona

l use

onl

y