for personal use only - asx · 3 financial performance full year 2015 • ebitda of $20.2m •...

TRANSCRIPT

Geoff Lewis, CEO and Dean Langenbach, COO/CFOAugust 2015

FY15 Results

1

For

per

sona

l use

onl

y

Company Overview

2

ASX code: ASZ

Number of Shares on Issue: 206,720,839

Share Price:$1.04

Market Capital: $215 million

Ian Campbell: Chairman

Geoff Lewis: Managing Director, CEO

Stephen Johnston: Non Executive Director

Grant Pestell: Non Executive Director

Peter Torre: Company Secretary

The ASG Board

The ASG Executive Team

Geoff Lewis: Managing Director, CEO

Dean Langenbach: COO, CFO

Gerald Strautins: Executive - Strategy

For

per

sona

l use

onl

y

3

Financial PerformanceFull Year 2015

• EBITDA of $20.2m• Revenue up 3%, services revenue up 4%• EPS up 6.2%• NPAT up 6%• New contract establishment impacts EBITDA• H2 operating cash strong at $14m

Contract wins

Outlook

FY15 – Delivering on the New World

• Over $200m of contracts signed in 12 months:Western PowerCimicDepartment of CommunicationsSynergyState SuperDepartment of Primary & Environment Industries (DEPI)Lockheed Martin (Defence)Australian Transport Safety Bureau (ATSB)AusGroup (AGC)Australian Maritime Safety Authority (AMSA)

• Target EBITDA of 14% • $160m locked in revenue for FY16• FY16 Revenue guidance of $180m - $190m• Net debt of $11.4m, on track for FY16 target

For

per

sona

l use

onl

y

FY15 Financial Summary

4

$m FY15 FY14 Movement

Revenue 164.3 160.1 2.6%

EBITDA 20.2 22.0 (8.1%)

NPBT 11.6 12.6 (7.6%)

NPAT 9.5 9.0 6.3%

EBITDA Margins 12.3% 13.7% (1.4%)

EPS 4.61c 4.34c 6.2%

• Revenue up 3%, services Revenue up 4%• H2 core operating EDITDA stronger than H1• Revenue impacted by new Managed Service commencement

delays, contracted revenue now commencing in Q1 FY16• Additional $2.1m of bid and contract establishment costs as

record amount of contracts signed in FY15

For

per

sona

l use

onl

y

FY15 H1 v H2 Operating EBITDA

5

$m H1 H2 FY15 Total

Reported EBITDA 11.1 9.1 20.2

- Profit on Data Centre(1.0) 0.4 (0.6)

- R&D credit(0.8) 0.0 (0.8)

- Acquisition Payment0.0 0.4 0.4

- Share Based Payments0.1 0.3 0.4

Operating EBITDA 9.4 10.2 19.6

• H2 run rate strong, despite soft old world project revenue and higher contract ramp up costs

• Data Centre profit on sale reduced in H2 due to timing delay of new contracts coming on board.

For

per

sona

l use

onl

y

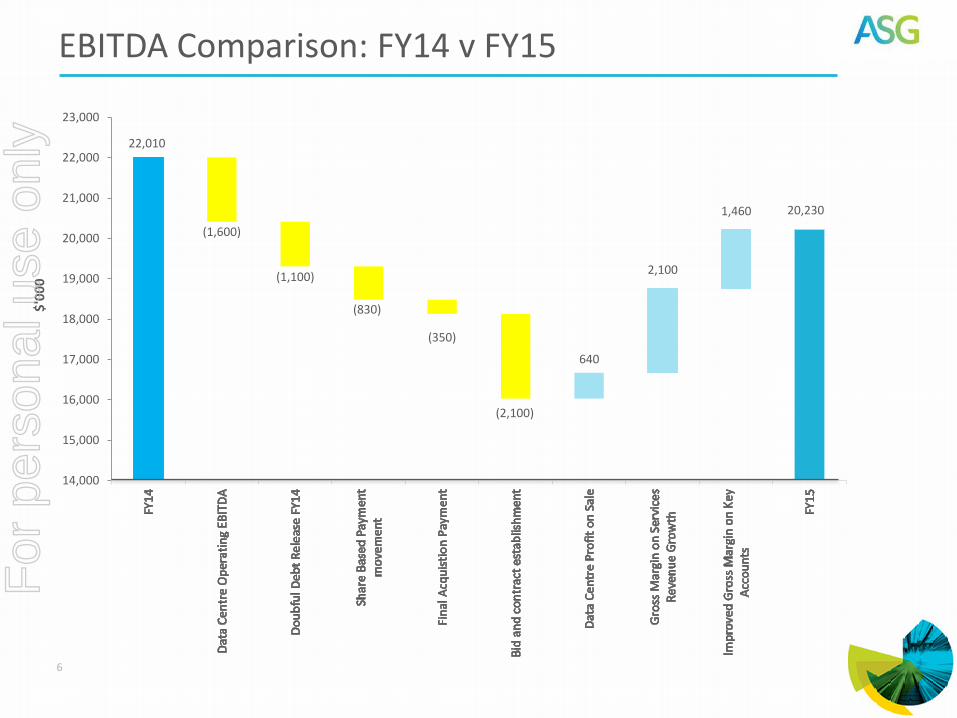

6

22,010

(1,600)

(1,100)

(830)

(350)

(2,100)

640

2,100

1,460 20,230

14,000

15,000

16,000

17,000

18,000

19,000

20,000

21,000

22,000

23,000

EBITDA Comparison: FY14 v FY15 $

'00

0F

or p

erso

nal u

se o

nly

EBITDA to Net Operating Cash

7

$m FY15 FY14

EBITDA 20.2 22.0

Finance Costs (1.7) (2.9)

Income Tax (1.7) (0.0)

R&D credit – non cash (0.8) (0.9)

Data centre profit – investing activity (0.6) 0.0

Debtors: early Govt. payments in June 2014 (4.1) 4.1

Debtors: SAP project milestone delay (2.0) 0.0

Other: sundry non-cash and creditor movement (0.8) (0.3)

Net Operating Cash 8.5 22.0

Net Operating Cash % EBITDA 40% 100%

• ASG targeting 70% - 75% Net Operating Cash % EBITDA • Average over FY14 and FY15 periods = 70%• $14m operating cash turnaround from H1

For

per

sona

l use

onl

y

Operating Cash Flow

8

• $2m milestone payment delay on SAP project. Payment received in August 2015

• Early Debtor receipts of $4.1m in FY14 impacted FY15• Future Operating Cash Flow consistent with EBITDA less interest and tax

53

68

48

73

61

-20

-10

0

10

20

30

40

50

60

70

80

-10.0

-

10.0

20.0

30.0

40.0

FY13 H1 FY14 FY14 H1 FY15 FY15

DA

YS

$M

Debtor Days Operating Cash Flow

For

per

sona

l use

onl

y

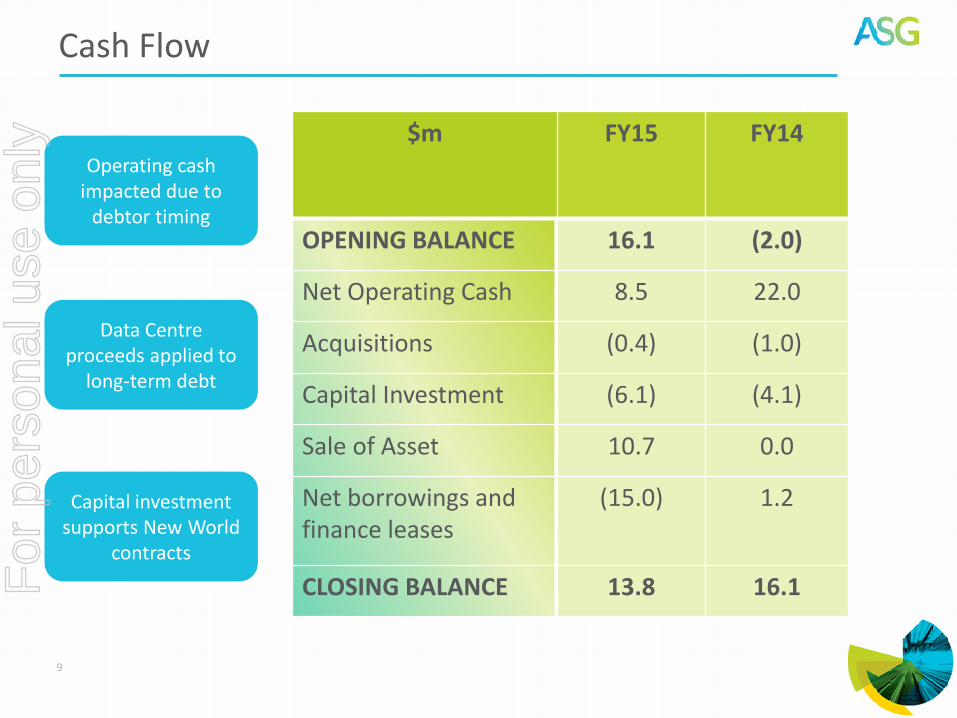

Cash Flow

9

$m FY15 FY14

OPENING BALANCE 16.1 (2.0)

Net Operating Cash 8.5 22.0

Acquisitions (0.4) (1.0)

Capital Investment (6.1) (4.1)

Sale of Asset 10.7 0.0

Net borrowings and finance leases

(15.0) 1.2

CLOSING BALANCE 13.8 16.1

Operating cash impacted due to

debtor timing

Data Centre proceeds applied to

long-term debt

Capital investment supports New World

contracts

For

per

sona

l use

onl

y

Balance Sheet Strengthening

10

$m June 2015 June 2014

Current Assets

Cash 13.8 16.1

Receivables 33.2 28.0

Other Current Assets 1.9 11.9

Total Current Assets 49.0 56.0

TOTAL ASSETS 177.1 179.8

Current Liabilities

Trade and other payables 33.6 33.1

Borrowings 5.9 8.8

Total Current Liabilities 46.4 50.9

Non-Current Borrowings 19.3 29.0

TOTAL LIABILITIES 73.8 86.3

NET ASSETS 103.3 93.5

Strengthened by operating performance

and Data Centre sale

Net Current Asset improvement (excluding

Data Centre sale)

Continued focus on debt reduction and liquidity

improvement

For

per

sona

l use

onl

y

Debt Reduction Focus

11

• FY15 Net Debt of $11.4m against target of <$10m• Higher than anticipated bid costs of $2.1m• Milestone delay on SAP project

• FY16 Target: Surplus cash reserves exceed debt• Remains on track despite unprecedented contract success

FY16 Target

FY14 Target

FY14 Actual

FY15 ActualFY15 Target

-35

-30

-25

-20

-15

-10

-5

0

5

10

$M

For

per

sona

l use

onl

y

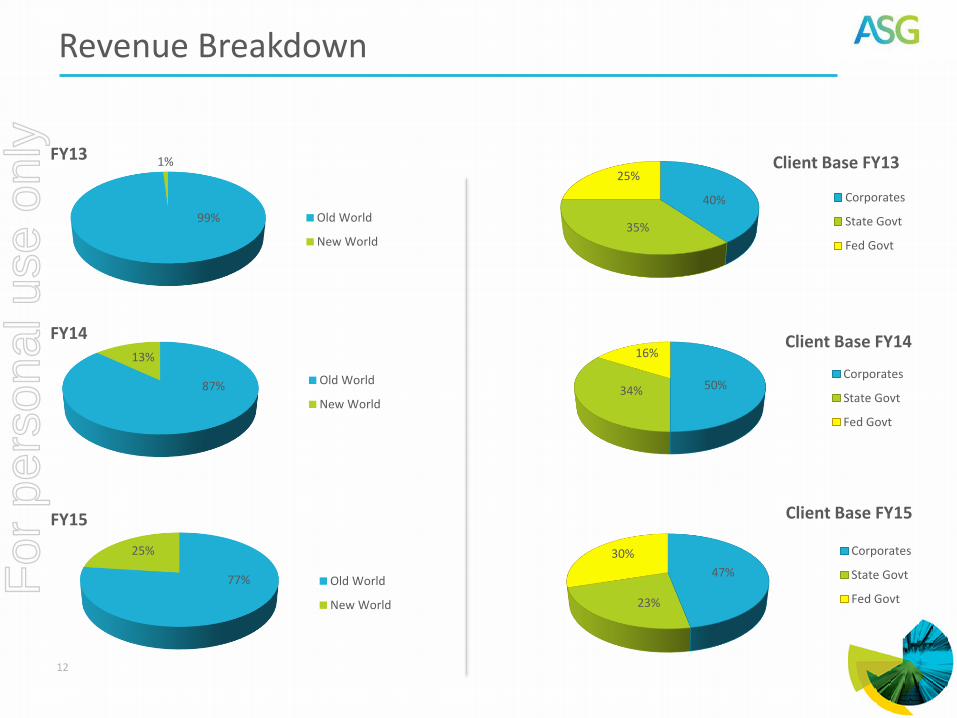

77%

25%

FY15

Old World

New World

Revenue Breakdown

12

99%

1%FY13

Old World

New World

87%

13%

FY14

Old World

New World

50%34%

16%Client Base FY14

Corporates

State Govt

Fed Govt

47%

23%

30%

Client Base FY15

Corporates

State Govt

Fed Govt

40%

35%

25%Client Base FY13

Corporates

State Govt

Fed Govt

For

per

sona

l use

onl

y

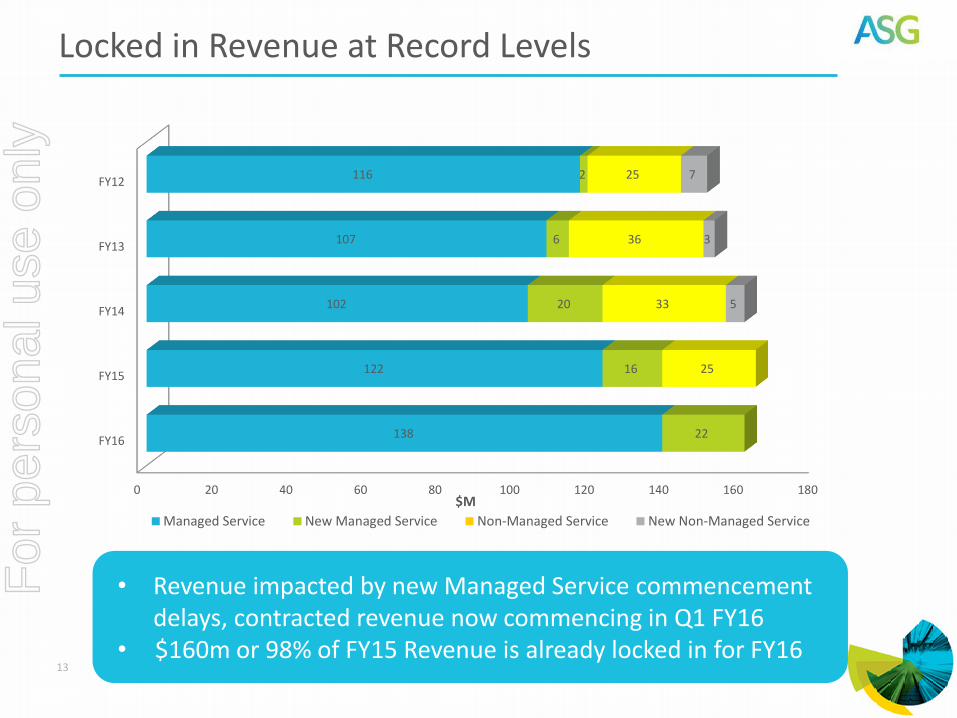

Locked in Revenue at Record Levels

13

• Revenue impacted by new Managed Service commencement delays, contracted revenue now commencing in Q1 FY16

• $160m or 98% of FY15 Revenue is already locked in for FY16

0 20 40 60 80 100 120 140 160 180

FY16

FY15

FY14

FY13

FY12

138

122

102

107

116

22

16

20

6

2

25

33

36

25

5

3

7

Managed Service New Managed Service Non-Managed Service New Non-Managed Service

$M

For

per

sona

l use

onl

y

Record Contract Wins – Over $200m in 12 Months

14

Customer TypeContractPeriod

Western Power Renewal + additional scope 3 + 2 + 2 years

Cimic New 5 years

Department of Communications Renewal + conversion to New World 5 years

Synergy Renewal + additional scope 3 + 3 years

State Super New 3 + 2 years

Department of Primary & Environment Industries (DEPI)

New 3 years

Lockheed Martin (Defence) New 8 years

Australian Transport Safety Bureau (ATSB)

New 4 years

AusGroup (AGC) New 5 + years

Australian Maritime Safety Authority (AMSA)

New 5 + 3 years

• $150m of new clients, $50m of existing clients• Average contract length 4 years plus 4 year renewal

For

per

sona

l use

onl

y

Pipeline

NSW$60m

WA$45m

VIC$85m

ACT$140m

QLD$15m

TOTAL$345m

For

per

sona

l use

onl

y

Transition to the Next Generation Technology Services Model

16

Buyer Side Push:• Pay for results (vs.

efforts)/outcome based• More predictability• Faster time to market

Vendor Side Pull:• Technological advances• Headcount issues• Wage inflation

As software, services and infrastructure continue to converge, buyers and sellers of IT services are moving rapidly towards the adoption of outcome-based services offering where the value proposition is defined

by IP

Traditional Services Offering(Capacity on Demand)

Managed Services Offering(Capability on Demand)

Role

Verticalisation

Intellectual Property

Methods / Tools / Accelerators

Labour

Role

Verticalisation

Intellectual Property

Methods / Tools/Accelerators

Labour

Current State Future State

Role

Verticalisation

Intellectual Property

Methods / Tools / Accelerators

Labour

For

per

sona

l use

onl

y

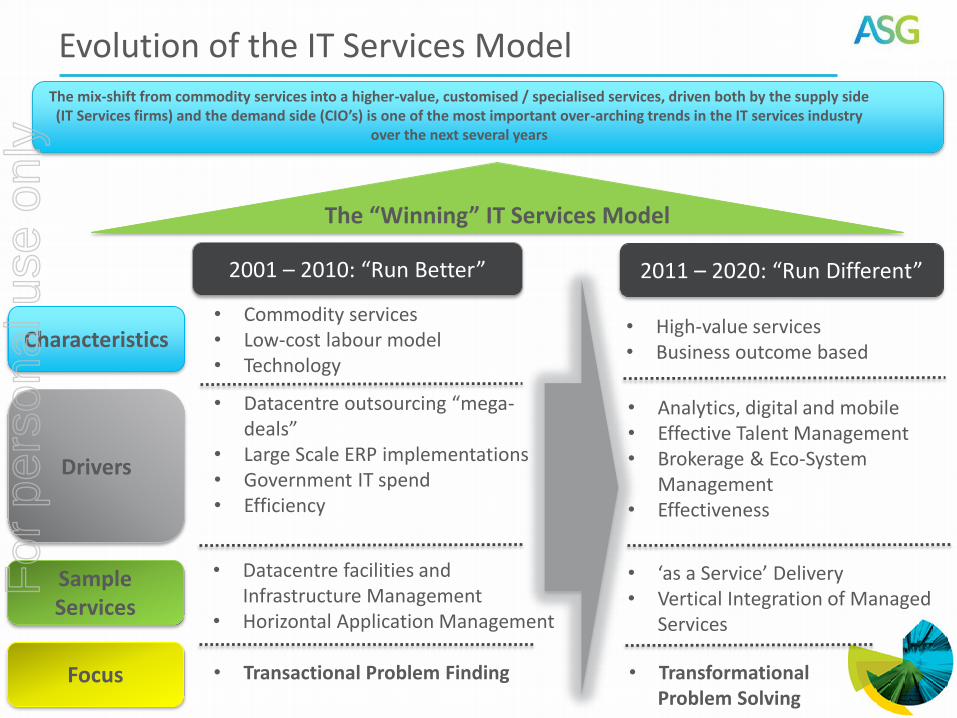

Evolution of the IT Services Model

17

The mix-shift from commodity services into a higher-value, customised / specialised services, driven both by the supply side(IT Services firms) and the demand side (CIO’s) is one of the most important over-arching trends in the IT services industry

over the next several years

The “Winning” IT Services Model

2001 – 2010: “Run Better” 2011 – 2020: “Run Different”

Characteristics

Drivers

SampleServices

Focus

• Commodity services• Low-cost labour model• Technology

• Datacentre outsourcing “mega-deals”

• Large Scale ERP implementations• Government IT spend• Efficiency

• Datacentre facilities and Infrastructure Management

• Horizontal Application Management

• Transactional Problem Finding

• High-value services• Business outcome based

• Analytics, digital and mobile• Effective Talent Management• Brokerage & Eco-System

Management• Effectiveness

• ‘as a Service’ Delivery• Vertical Integration of Managed

Services

• Transformational Problem Solving

For

per

sona

l use

onl

y

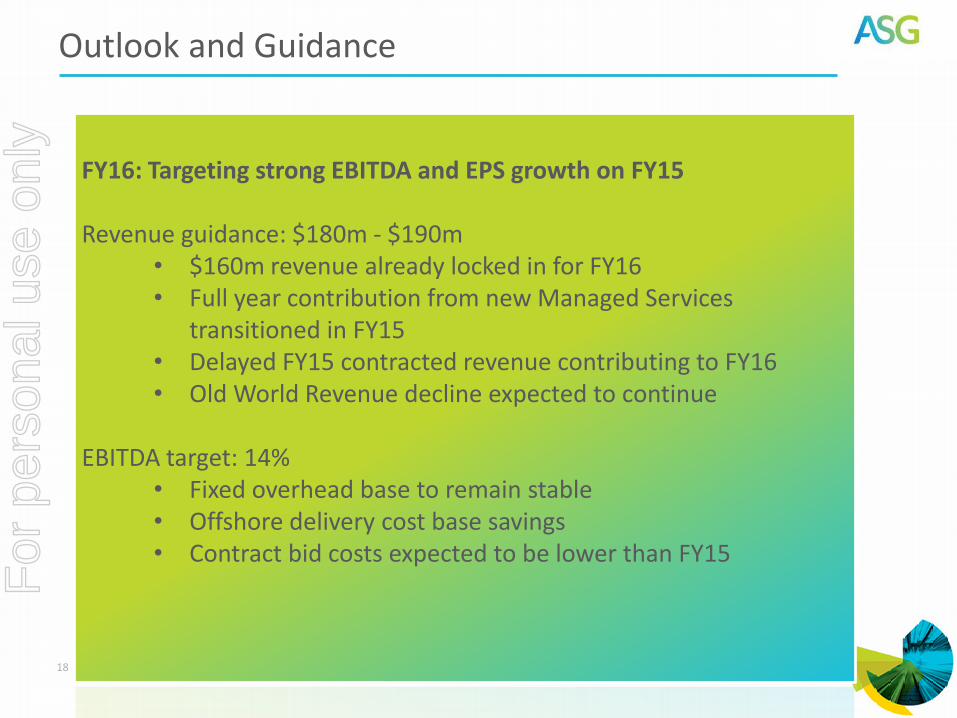

Outlook and Guidance

18

FY16: Targeting strong EBITDA and EPS growth on FY15

Revenue guidance: $180m - $190m• $160m revenue already locked in for FY16• Full year contribution from new Managed Services

transitioned in FY15• Delayed FY15 contracted revenue contributing to FY16• Old World Revenue decline expected to continue

EBITDA target: 14%• Fixed overhead base to remain stable• Offshore delivery cost base savings • Contract bid costs expected to be lower than FY15

For

per

sona

l use

onl

y

Q&A

19

For

per

sona

l use

onl

y