for discussion on - 香港特別行政區立法會 -...

TRANSCRIPT

For discussion on

14 May 2012

Legislative Council Panel on Education

Improvement Measures to Student Financial Assistance Schemes

for Post-secondary Students

Purpose

This paper seeks Members’ views on the implementation of a

package of measures to improve the operation of the Non-means-tested Loan

Schemes (NLS) upon completion of the NLS Review and related

improvement measures on the means-tested assistance schemes, namely the

Tertiary Student Finance Scheme – Publicly-funded Programmes (TSFS) and

the Financial Assistance Scheme for Post-secondary Students (FASP)

administered by the Student Financial Assistance Agency (SFAA).

Members’ support is also sought on the creation of a Principal Executive

Officer (PEO) post in SFAA to strengthen the directorate support for

implementing the above-mentioned improvement measures.

Non-means-tested Loan Schemes

The Scheme

2. The NLS was first introduced in the 1998/99 academic year to

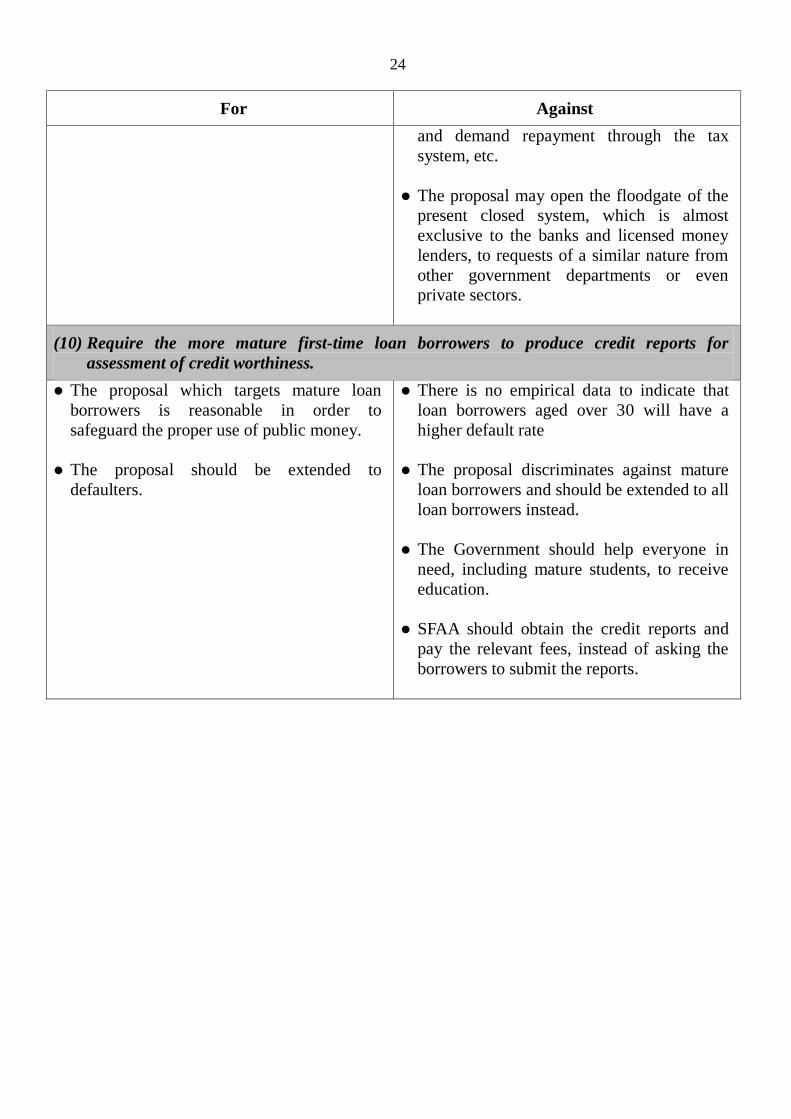

provide an alternative source of finance to tertiary students who did not wish

or failed to go through the means test under TSFS1 to assist them to pursue

studies.

3. The ambit of the scheme has been expanded over the years. At

present, SFAA administers three NLS targeting different categories of

students –

(a) Non-means-tested Loan Scheme for Full-time Tertiary

Students (Scheme A) – for full-time students pursuing

publicly-funded post-secondary programmes (from the sub-degree

to the postgraduate level), who are eligible to apply for

means-tested grants and loans under TSFS.

1 Formerly known as Local Student Finance Scheme before the 2007/08 academic year

LC Paper No. CB(2)1922/11-12(02)

2

(b) Non-means-tested Loan Scheme for Post-secondary Students

(Scheme B) – for full-time students aged 25 or below pursuing

self-financing, locally-accredited sub-degree and degree

programmes, who are eligible to apply for means-tested grants and

loans under FASP.

(c) Extended Non-means-tested Loan Scheme (Scheme C) – for

students pursuing a wide and diverse range of full-time and

part-time post-secondary and continuing and professional education

courses.

4. Borrowers of NLS loans do not need to go through any means test,

or provide security for the loans. For safeguarding public resources, NLS

operate on a no-gain-no-loss and full-cost recovery basis. Interest starts to

accrue upon loan drawdown. The interest rate comprises a no-gain-no-loss

(NGNL) interest rate2, and a 1.5% risk-adjusted-factor (RAF) to cover the

Government’s risks in disbursing unsecured loans. The current interest rate

is 3.174% per annum. Loans should be repaid within 10 years after the end

of studies. Loan borrowers with repayment difficulties may apply for

deferment of loan repayment. Those who default payment of two or more

consecutive quarterly instalments will be considered defaulters.

Phase 1 Public Consultation and Proposed Measures

5. We launched Phase 1 public consultation in mid 2010 to collect

initial public’s views on various issues relating to the operation of NLS.

Taking into account the views received, we proposed a package of 10

improvement measures for Phase 2 public consultation. The proposed

measures aim to (i) ease the repayment burden of student loan borrowers; (ii)

reduce excessive borrowing of loan borrowers and induce enhancement in

quality assurance of eligible courses; and (iii) tackle the student loan default

problem more effectively. They are -

Ease the repayment burden of student loan borrowers

(1) Reduce the RAF rate of the three schemes from 1.5% to zero, and

review the situation after three years;

2 The no-gain-no-loss interest rate is set at a certain percentage below the average best lending rate

(BLR) of the note-issuing banks. The percentage is the average differential between the BLRs and

the 12-month Hong Kong Dollar Inter-bank Offered Rates over a 10-year period, and is reviewed

biennially. The no-gain-no-loss interest rate is currently 1.674% per annum.

3

(2) Extend the standard repayment period of non-means-tested loans

from 10 years to 15 years;

(3) Relax the deferment arrangements such that those borrowers whose

applications for deferment have been approved would be allowed an

extension of loan repayment period without interest during the

approved deferment period, subject to a maximum of two years;

(4) Revise the repayment interval from quarterly to monthly basis;

Prevent excessive borrowing of loan borrowers and induce enhancement in

quality assurance of eligible courses

(5) Cap the loan amount in respect of each programme at the level of

tuition fee payable for all the three schemes;

(6) Impose a life-time combined maximum loan limit of $300,000

under Schemes A and B; and a separate life-time maximum limit of

$300,000 under Scheme C, with annual price adjustment

mechanism;

(7) Remove the age limit from Scheme B;

(8) Suitably revise the course eligibility criteria of Scheme C to restrict

the eligible courses to those with a reasonable degree of quality

assurance;

Tackle the student loan default problem more effectively

(9) Share the negative credit data of defaulters with the credit reference

agency (CRA) under clearly defined circumstances; and

(10) Require the more mature first-time loan borrowers to produce credit

reports for assessment of credit worthiness.

Phase 2 Public Consultation

6. Phase 2 public consultation took place between 14 November 2011

and 29 February 2012. We consulted major stakeholders including the

Legislative Council (LegCo) Panel on Education, the Joint Committee on

4

Student Finance (JCSF)3, Federation of Continuing Education in Tertiary

Institutions, Hong Kong Federation of Students (HKFS), Junior Chamber

International Hong Kong, education institutions, student groups, course

providers and loan borrowers, etc, and received 61 written submissions.

The views received are summarised at Annex A. In addition, we have also

received 1 743 views through an on-line survey on a dedicated website.

The views collected from the on-line survey are summarised below -

Proposal

For Against

1 Reduce the RAF rate of the three NLS from 1.5% to zero, and

review the situation after three years.

90% 10%

2 Extend the standard repayment period of NLS loans from 10

years to 15 years.

76% 24%

3 Relax the deferment arrangements such that those borrowers

whose applications for deferment have been approved would

be allowed an extension of loan repayment period without

interest during the approved deferment period, subject to a

maximum of two years.

89% 11%

4 Revise the repayment interval from quarterly to monthly basis.

73% 27%

5 Cap the loan amount in respect of each programme at the level

of tuition fee payable for all NLS.

75% 25%

6 Impose two life-time loan limits each of $300,000, one for

Schemes A and B and one for Scheme C, with annual price

adjustment mechanism.

77% 23%

7 Remove the age limit from Scheme B.

82% 18%

8 Suitably revise Scheme C’s course eligibility criteria to restrict

the eligible courses only to those with a reasonable degree of

quality assurance.

79% 21%

9 Share the negative data of defaulters with the CRA under

clearly defined circumstances.

62% 38%

10 Require the more mature first-time loan borrowers to produce

credit reports for assessment of credit worthiness.

56% 44%

3 JCSF advises the Government on the operation of TSFS and NLS. JCSF comprises lay members from

the community, institutional and student representatives of the eight University Grants

Committee-funded institutions, Vocational Training Council and Hong Kong Academy for Performing

Arts.

5

7. The results of Phase 2 public consultation revealed that all 10

proposals received majority support. In particular, Proposals 1 to 8 have

each garnered over 70% support from respondents. Having considered the

views received, we have drawn up recommendations on taking forward the

various proposals as set out in the ensuing paragraphs.

Proposals 1 to 4 on easing the repayment burden of loan borrowers

8. Proposals 1 and 2 on reducing RAF to zero and extending the

repayment period from 10 years to 15 years can significantly reduce the

monthly repayment of borrowers by up to 40%. Based on the current

NGNL, the interest rate will be reduced from 3.174% to 1.674%. Taking

into account the strong public support received, we propose that all new and

existing loan borrowers will benefit from these proposals. As the proposed

extended repayment period of 15 years means that borrowers will pay more

interest, new and existing borrowers may choose if they wish to repay in 10

or 15 years. Irrespective, all borrowers may repay their loans early at any

time to save interest.

9. The relaxed deferment arrangement under Proposal 3 can provide

necessary relief to needy loan borrowers as the approved deferment period

will be interest-free during the extended repayment period, subject to a

maximum of two years, meaning that for these needy loan borrowers, their

entire repayment period can be up to 17 years. Loan borrowers who have

difficulty in repaying their loans on grounds of financial hardship, further

full-time study or serious illness and who have not benefited from the

one-off relief measure on deferment of loan repayment introduced in August

2009 will benefit from this proposal.

10. We propose to implement Proposals 1 to 3 in the 2012/13 academic

year. For Proposal 4 on revising the repayment interval from quarterly to

monthly which can facilitate better financial management of loan borrowers,

we propose to implement it in the 2013/14 academic year as it involves

substantial system enhancement.

Proposals 5 to 7 on preventing excessive borrowing

11. Proposals 5 to 7 also received strong public support. These

proposals can ensure that reasonable financial support is provided to

students pursuing post-secondary and continuing & professional education

while discouraging unreasonably high tuition fees and preventing excessive

borrowing. Upon implementation of the proposals, loans available to

students under all the three schemes will be aligned and capped at the level

6

of tuition fee payable. There will be no age limit under the three schemes.

We propose to implement these proposals in the 2012/13 academic year.

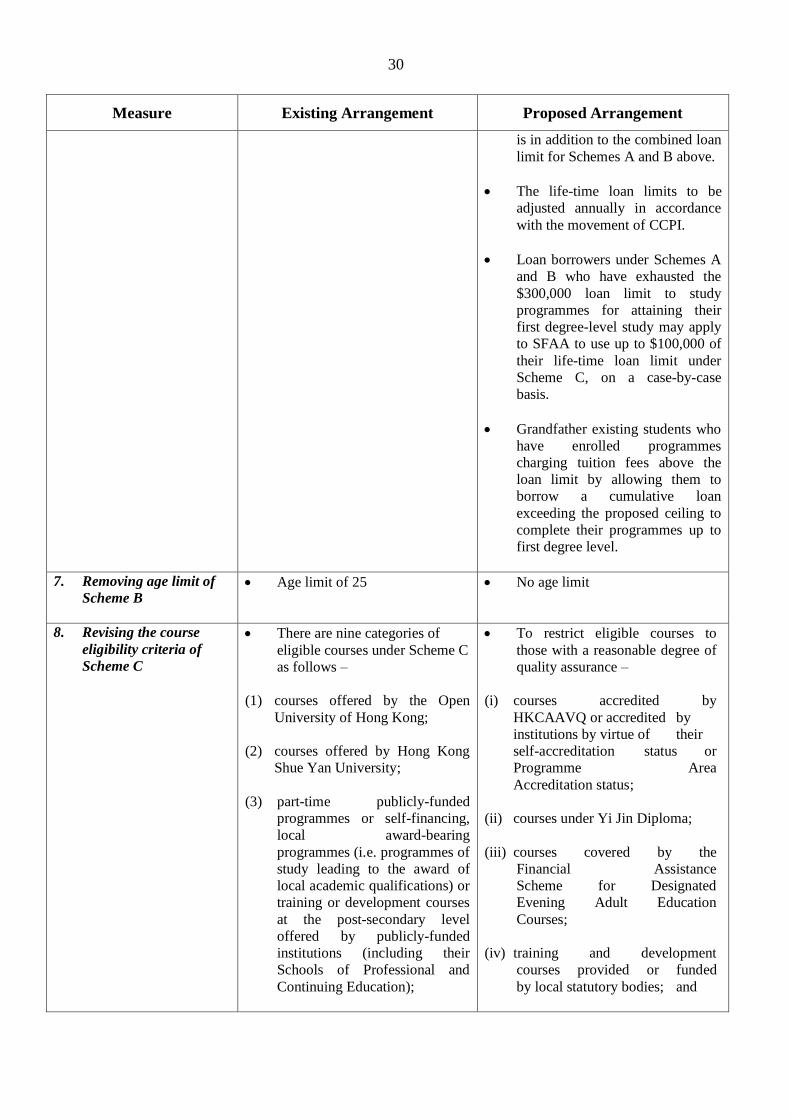

12. Proposal 6 proposes a combined cap of $300,000 for Schemes A

and B and a separate, additional life-time maximum loan limit of $300,000

for Scheme C. The cap is a life-time maximum loan limit for each eligible

loan borrower and it will be price-adjusted annually in accordance with the

Composite Consumer Price Index (CCPI). Over 99% of the loan accounts

of NLS activated in the 2010/11 academic year incurred a total loan amount

below $300,000. The loan ceiling will be applied to the loans disbursed to

loan borrowers from the 2012/13 academic year and onwards and the NLS

loans they obtained prior to the 2012/13 academic year will not be counted

towards the loan ceiling.

13. Some stakeholders have expressed concerns about whether the

life-time loan limit of $300,000 is sufficient, in particular having regard to

the rising trend of tuition fee levels of self-financing programmes. In some

cases, some students may need to take out NLS loans in order to complete

their associate degree and first degree programmes. In response to these

concerns, we propose that loan borrowers under Schemes A and B who have

exhausted the $300,000 loan limit for studying programmes for attaining

their first degree-level study may apply to SFAA to use up to $100,000 of

their life-time loan limit under Scheme C, on a case-by-case basis. SFAA

will consider factors such as whether the students are studying for their first

degree-level study and the tuition fee level of the course, etc.

14. We also note that there are some locally-accredited self-financing

programmes that charge very high tuition fees e.g. the total course fee for a

four-year degree programme offered by an arts and design college amounts

to around $1 million. Having consulted the relevant Bureaux with policy

responsibilities for arts & culture and innovation industries, we do not

recommend giving exceptional treatment for students of these institutions.

We have also been advised that a number of local universities are currently

providing comparable courses and choices are available for students

pursuing these areas of study. Nevertheless, for those students who have

already borrowed NLS loans to finance their study in these programmes, we

reckon that the proposed loan ceiling is not adequate to finance them to

complete their programmes. As these students may have reasonable

expectation that they can rely on NLS loans to complete their study, we

propose to grandfather these students by allowing them to borrow a

cumulative loan exceeding the proposed ceiling in order to complete their

programmes up to first degree level.

7

Proposal 8 on inducing enhancement in quality assurance of eligible courses

15. Proposal 8 which aims to induce enhancement in quality assurance

of courses under Scheme C received nearly 80% support. We propose to

implement this proposal in the 2012/13 academic year. Scheme C now

provides loans for students pursuing a wide and diverse range of

post-secondary and continuing & professional education courses. Many of

them are not yet locally-accredited. Some Scheme C course providers have

expressed concern about tightening the course eligibility criteria, as it takes

time for existing courses to obtain local accreditation status.

16. We propose a transitional arrangement for existing non-accredited

courses. Initially, a 3-month provisional qualified status will be given to

existing courses providers. They should, within this period, submit a

Statement of Intent (SOI) to Hong Kong Council for Accreditation of

Academic and Vocational Qualifications (HKCAAVQ) seeking

accreditation. Upon confirmation of the receipt of the SOI from

HKCAAVQ, the provisional qualified status will be extended for one year to

allow the course providers concerned to proceed with the accreditation

process. If the courses have yet to be accredited at the expiry of the

one-year provisional qualified period, the provisional qualified period may

be further extended for another year if the course providers can demonstrate

that they are actively seeking accreditation i.e. they have signed a Service

Agreement with HKCAAVQ and made payment of the initial accreditation

fee. Further extension of the provisional qualified period would be

considered only on an exceptional basis on the merits of individual case.

Nevertheless, if the number of courses seeking accreditation is higher than

expected, HKCAAVQ will need more time to process them. In this case,

we are prepared to extend the provisional qualified period to course

providers so affected. We also propose a grandfathering arrangement to

enable existing students to complete their study programme in case the

course being pursued fails to obtain the accreditation during the transitional

period.

Proposal 9 on sharing negative credit data of defaulters with CRA

17. While attracting a slight majority support, the proposal of sharing

negative credit data of defaulters with CRA remains one with divided views

among the stakeholder groups reflecting their different perspectives and

interests. Little surprise therefore is the strong opposition of the HKFS.

Furthermore, the Privacy Commissioner of Personal Data (PCPD) has

expressed reservations about the proposal, mainly for fear of opening up a

floodgate for similar requests from other Government departments in future.

8

PCPD’s concerns and the Administration’s response are at Annex B.

18. We consider that, given the similarity between SFAA’s student

loans and the unsecured personal loans offered by licensed banks and

financial institutions (and probably to the same loan borrowers too), it

should be in the overall public interest to prevent defaults involving

Government loans (hence public money), in the same way as we are

protecting the private sector from excessive lending by allowing licensed

banks and financial institutions by means of the sharing of negative credit

data of defaulters with the existing CRA under the Personal Data (Privacy)

Ordinance (PD(P)O). Not to pursue the proposal may inadvertently send a

wrong message that public funds are less deserving of prudent use and less

deserving of safeguard against abuse than private sector funds. Also

important is the message on responsible financial management that we wish

to send to students.

19. Our proposal is similar to the on-going sharing of negative credit

data of defaulters with the existing CRA amongst licensed banks and

financial institutions, which is being regulated under the PD(P)O and in

particular the Code of Practice on Consumer Credit Data. We are also

prepared to subject SFAA to a series of more stringent regulatory measures

than those currently applicable to licensed banks and financial institutions

on the handling of consumer credit data. Furthermore, the scope of our

proposal is far more restricted. Specifically, our initial proposal on the

provision of negative credit data by SFAA is restricted to the relatively more

serious default cases, say, those loan borrowers owed more than $100,000

and have ceased repayment for more than a year and who have failed to

respond to our reminders or to provide any reasonable justification for

delayed repayments. As of now, there are about 600 such cases out of

13 000 default cases, as all loan borrowers who have reached agreement

with SFAA on deferment arrangements would not be counted as defaulters.

20. We will have further consultation with stakeholders, LegCo

members and political parties on this issue. Since the PCPD’s agreement

to exercise his statutory authority under the PD(P)O is the prerequisite for

implementing our proposal, we are planning to put up a detailed

implementation proposal to PCPD to address his concerns and arguments.

Proposal 10 on requiring the more mature loan borrowers to produce credit

reports

21. The proposal of requiring the more mature first-time loan borrowers

to produce credit reports in applying for loans received marginal majority

9

support. There are concerns about the absence of empirical data indicating

that loan borrowers aged 30 or above have a higher default rate. Since the

views received are rather diverse, we propose that we should monitor and

analyse, with reference to age distribution of the defaulters, the default

situation of various schemes after the implementation of the improvement

proposals. If the default rate of Scheme C should remain much higher than

other schemes upon review, we would then, based on the evidence collected,

consider whether, and if so, how this proposal should be taken forward.

Other Views Collected

22. There are other views received during the consultation period,

including charging no interest during the study period, capping the monthly

repayment to a percentage of income, and permanently abolishing RAF or

charging a different RAF based on the default situation of individual loan

schemes.

Study interest

23. We consider that charging no interest during the study period goes

against the fundamental no-gain-no-loss principle of NLS and will

encourage excessive borrowing. With the proposal to reduce the RAF rate

from 1.5% to 0%, subject to review in three years’ time and other proposals,

the interest rate for students during the study period will already be reduced

by almost half and the monthly repayment amount would be reduced by

around 40%. The additional interest savings for students from abolishing

the study interest is only about $20 per month4. However, the waiving of

study interest on all existing loan borrowers would lead to a substantial

interest loss of around $33.7 million each year for the Government. This

may also induce some to take advantage of the interest-free loans,

potentially leading to unnecessary and/or excessive borrowing and increased

default cases in the future.

Capping the monthly repayment amount to a percentage of income

24. We consider that lowering the interest rate and extending the

repayment period are the most effective means of reducing the monthly

repayment burden of borrowers. As Hong Kong lacks a “pay-as-you-go”

taxation system, SFAA, being the administrator of the payment and

repayment of student loans, does not have information on the monthly

income of loan borrowers to facilitate calculation of the amount they should 4 Based on the assumption that a student has borrowed $100,000 to pursue a 4-year programme, the

repayment period is 15 years and the interest rate is 1.674%.

10

repay. Bearing in mind the tendency for fresh graduates to change jobs

rather frequently, the possible salary revisions and the complex

remuneration structures of some companies, the administrative implications

and costs would be very significant. In addition, a self-reporting

mechanism, whereby borrowers need to report to SFAA their employment

status and income and to update SFAA whenever there is any change, is of

dubious reliability at best. A sample check of self-reported incomes would

still require substantial administrative work and might also involve issues of

privacy. We have therefore decided not to pursue this option.

Permanently abolishing the RAF

25. Abolishing the RAF effectively means that the Government would

absorb the loss from writing off irrecoverable debts. Therefore, reviewing

the RAF in three years’ time, taking into account the default situation and

the amount of irrecoverable debts then, is a prudent approach. In the

review, we will also consider whether we should charge a different RAF

based on the default situation of individual loan schemes.

Means-tested Financial Assistance Schemes

The Schemes

26. At present, needy post-secondary students can apply for financial

assistance under two means-tested assistance schemes, namely TSFS and

FASP. TSFS covers students pursuing University Grants

Committee-funded and exclusively publicly-funded programmes while

FASP covers students pursuing locally-accredited, self-financing

programmes. Eligible students who pass the means test of the SFAA will

be offered grants and/or loans under the TSFS and FASP as appropriate.

Grants cover tuition fees and academic expenses and loans are to cover

living expenses. Students who do not receive full level of assistance can

apply for NLS loan to make up the shortfall.

Improvements to FASP

27. In connection with the NLS Review, we have proposed in the Phase

2 public consultation specifically three improvement measures for FASP to

further enhance the support to needy students pursuing self-financing

post-secondary education programmes. They are -

11

Relax the age limit for FASP from 25 to 30

28. FASP, introduced in the 2001/02 academic year, provides grants for

tuition fees (subject to a ceiling) and academic expenses as well as loans for

living expenses to full-time students aged 25 or below pursuing

self-financing and locally-accredited sub-degree and degree programmes.

Having regard to the need to provide adequate support for those who have

had a late start in taking up post-secondary education or have to take a

longer time to complete their studies, we propose to relax the age limit for

FASP from 25 to 30. According to the enrolment statistics on relevant

self-financing post-secondary programmes in the 2010/11 academic year, the

relaxed age limit will cover around 99% of the students.

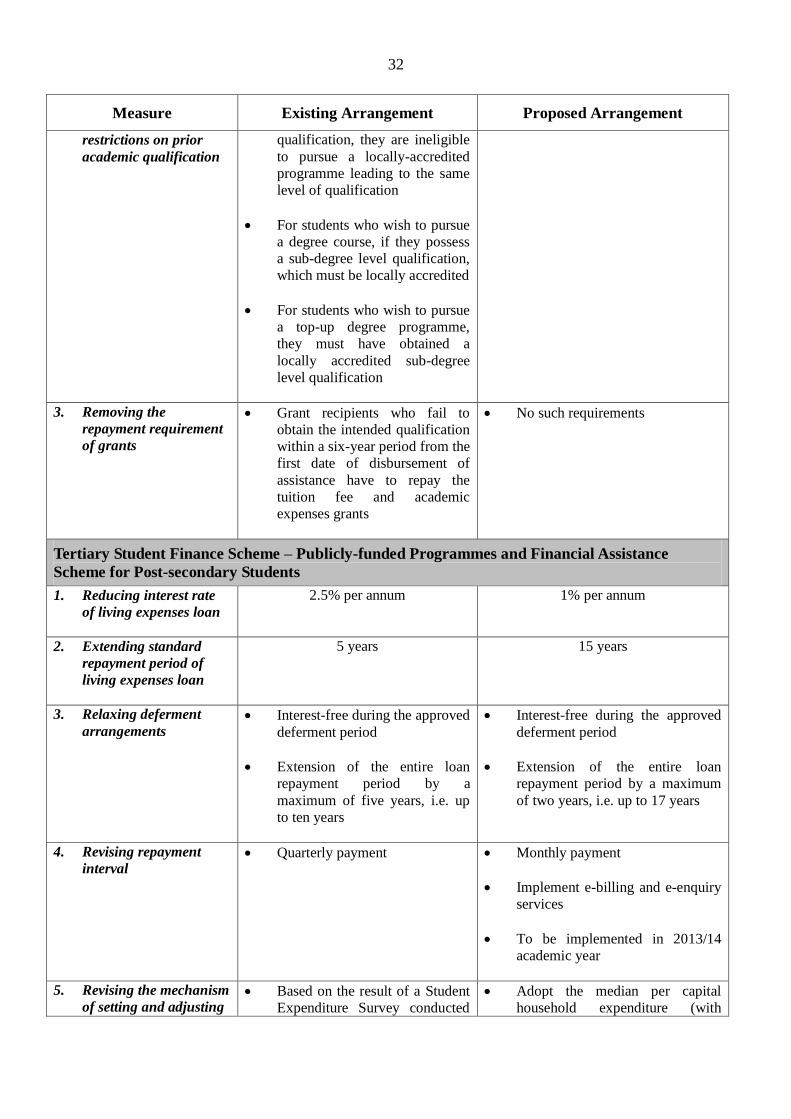

Remove the requirements / restrictions on prior academic qualification for

the purpose of applying for assistance

29. According to the current eligibility criteria of FASP, needy students

who have obtained sub-degree / degree level qualifications are ineligible for

assistance under FASP to pursue locally-accredited programme leading to the

same level of qualification. If a needy student wishes to apply for FASP

assistance to pursue a degree course and if he/she possesses a sub-degree

level qualification, that qualification must be locally-accredited; if a student

wishes to apply for FASP assistance to pursue a top-up degree programme,

he/she must have obtained a locally-accredited sub-degree level qualification.

We consider that such requirements / restrictions have posed unnecessary

constraints for needy students to obtain assistance for pursuing studies under

FASP/Scheme B. In order to allow these students more flexibility in

planning their study pathways, we propose to remove all requirements/

restrictions relating to prior academic qualifications from FASP and

Scheme B. This improvement will bring the requirements / restrictions on

par with needy students enrolled in publicly-funded programmes and apply

for assistance under TSFS.

Remove the grant repayment requirement

30. FASP grant recipients are currently required to obtain the intended

qualification within a six-year period from the first date of disbursement of

assistance, failing which they have to repay the tuition fee and academic

expenses grants. To put students receiving FASP grants on par with their

counterparts receiving grants under TSFS who are not subject to this

requirement, we propose to remove this requirement for FASP grant

recipients. Specifically, FASP grant recipients from the 2012/13 academic

12

year onwards will not be required to repay the grants received5 even if they

fail to obtain their intended qualification. The improvement will further

enhance our support to needy students pursuing self-financing programmes

and expedite the process of releasing grants to them. We also propose that

for those students who have terminated/withdrawn from studies before

2012/13 and are required to repay the grants received according to the

prescribed terms and conditions, they may apply to SFAA for waiver of

repayment of their outstanding grant if their cessation of studies was

involuntary due to special circumstances beyond their control, e.g. suffered

from mental illness or serious injury in accidents. We propose that SFAA

will consider and approve such applications on a case-by-case basis.

Further Improvements to Means-tested Loans offered under the TSFS and

FASP

31. Currently, the interest rate of means-tested living expenses (LE)

loans under both TSFS and FASP is fixed at 2.5% per annum. Interest is

not accrued while studying but upon commencement of the loan repayment

period. The current repayment period is five years (could be extended to

10 years). Assuming that a student pursues a four-year programme and

repays the loans in five years after graduation, the effective interest rate is

1.23%. For a student who has taken out the median loan amount of

$40,1106, the monthly repayment amount is $713 which includes an average

interest amount of $45.

32. In anticipation of the longer study period under the new academic

structure, students may need to take out a larger amount of LE loans and may

in return increase their repayment burden. The Financial Secretary

announced in the 2012-13 Budget that we would review the interest rate

mechanism of the means-tested loans. We have completed the review. In

conjunction with the recommendations of the NLS review, the proposed

improvement measures on means-tested loans are described in the ensuing

paragraphs.

5 Including the grants received prior to 2012/13 by continuing students of a FASP/TSFS programme (some

students may switch from FASP to TSFS programmes), who have not terminated their studies and been

demanded for repayment according to the prescribed terms and conditions. Students with grant paid

before 2012/13 who have terminated their studies and been demanded to repay the grant according to the

prescribed terms and conditions will have their outstanding grant waived if they can obtain the intended

qualifications in 2012/13 or after. Otherwise, they are required to continue to repay their grant as

demanded. 6 This median loan amount is based on the TSFS as at the end of 2010/11 only. Living expenses loans

were only provided to FASP beneficiaries since 2008/09. Hence, the bulk of the living expenses loan

repayment accounts (34 231 out of 37 840) are under the TSFS. The median for the loan accounts

under FASP is $35,670 as at end 2010/11.

13

Reduction of interest rate and extension of repayment period

33. In tandem with the improvement proposals of NLS loans, we

propose to revise the interest rate of means-tested loans from the existing

2.5% to 1% and extend the repayment period from the existing 5 years to 15

years7. The combined effect of the above improvement measures will

further alleviate the repayment burden of loan borrowers. Taking the

median loan amount of $40,110 as illustration, the monthly repayment

amount will be reduced significantly from $713 to $240 (about a 66%

reduction). The monthly repayment amount of a borrower under FASP,

with the median loan amount of $35,670, will be reduced from $634 to $214,

which is also a 66% reduction. When taken together with the other

proposals of NLS Review to ease the repayment burden of loan borrowers

(i.e. Proposals 3 and 4), the maximum two-year relaxed deferment

arrangement will also be applied to eligible means-tested loan borrowers (i.e.

they have difficulty in repaying their loans on grounds of financial hardship,

further full-time study or serious illness and have not benefited from the

one-off relief measure on deferment of loan repayment introduced in August

2009), and the repayment intervals of means-tested loans will also be revised

from quarterly to monthly.

34. Same as for NLS loans, we propose that all new and existing loan

borrowers will benefit from the proposal. As for the loan repayment period,

since the proposed extended repayment period of 15 years will result in

higher interest charges, new and existing loan borrowers may choose if they

accept this option or not. They may also, as allowed under the current

arrangement, make early or partial repayment at any time during the

repayment period.

Improvement to the Mechanism of Setting and Adjusting the Maximum

Living Expenses Loan and Academic Expenses Grant under the TSFS

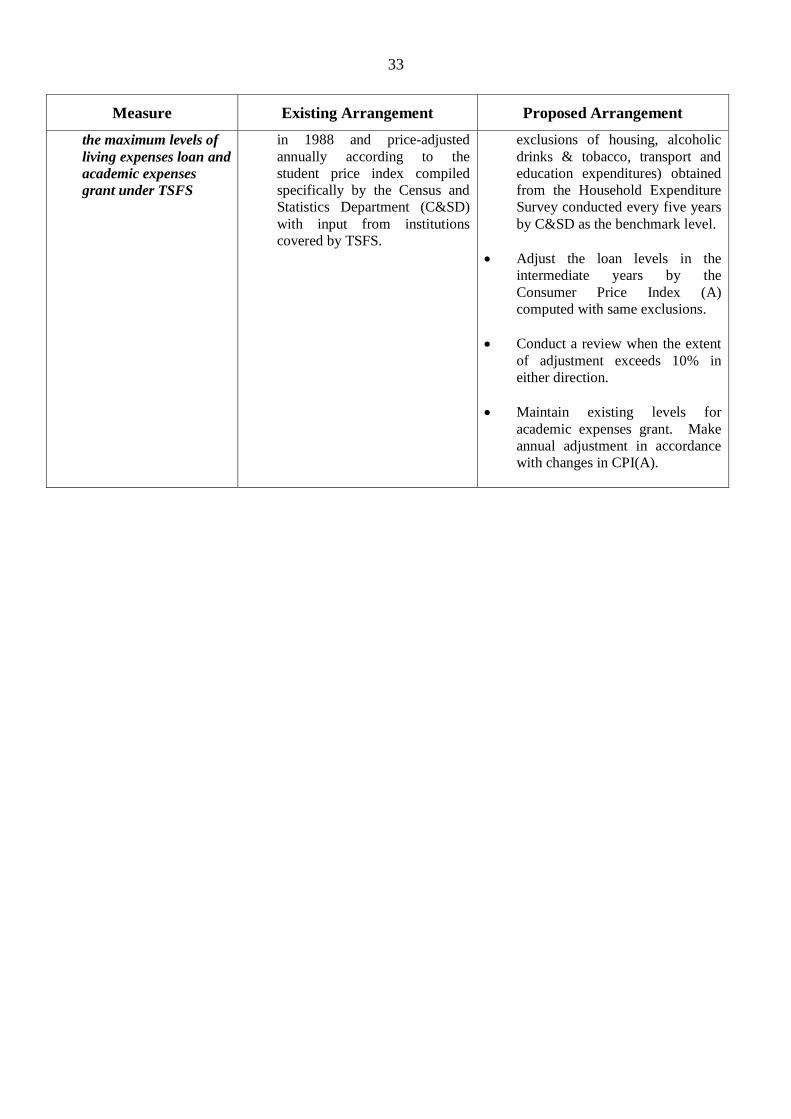

35. At present, the levels of maximum LE loan (currently at $37,960)

and academic expenses grant (depends on the discipline of study, varying

from $5,800 to $28,340) under TSFS are based on a direct application of the

results of a Student Expenditure Survey (SES) conducted in 1988 and

price-adjusted annually according to the student price index compiled

specifically by the Census and Statistics Department (C&SD) with input

7 The reduction of interest rate and extension of repayment period should also be applicable to the FASP

tuition fee loans borrowers/ grant repayers. As at the end of 2010/11, there are about 7 400 repayment

accounts with outstanding tuition fee loans amounting to about $160 million. For repayment of grants,

there are about 2 700 repayment accounts with outstanding loan amount of about $99 million.

14

from institutions covered by the scheme. The maximum level of LE loan is

also applicable to eligible FASP students. Another SES was conducted in

1999/2000. The findings revealed that the average expenditure of surveyed

students was about 70% higher than the maximum loan offered at that time.

Moreover, students with TSFS assistance spent an average of around 13%

more than those without. The survey results thus gave rise to doubts on the

usefulness and reliability of the SES, and also brought about the question of

whether it is appropriate to link the level of financial support to the actual

living expenses of students rather than to the need of students or to a level of

support the public generally considers reasonable.

36. Upon the advice of the JCSF, the results of the 1999/2000 SES were

shelved. A consultancy study was subsequently commissioned with a view

to recommending a new mechanism which is simpler, more objective, more

sustainable and acceptable by stakeholders.

37. Taking into account the results of the consultancy study, we propose

to revise the mechanism of setting the maximum LE loan level by adopting

the median per capita household expenditure (with exclusions of housing,

alcoholic drinks & tobacco, transport and education expenditures) obtained

from the Household Expenditure Survey (HES) conducted every five years

by C&SD as the benchmark level. The LE loan levels in the intermediate

years between the conduct of HESs will be adjusted by the Consumer Price

Index (A) (CPI(A)) computed with similar exclusions. To avoid drastic

changes to the LE levels during economically turbulent years, we will

initiate a review on the mechanism when the extent of adjustment to the

prevailing maximum LE loan level on the basis of the benchmark level from

the HES exceeds 10% in either direction, and will adjust the maximum LE

amount in subsequent years in accordance with CPI(A) pending completion

of the review.

38. According to the revised mechanism, the maximum LE loan

derived from the latest HES results (i.e. 2009-10 HES8) is $37,980, which is

very close and comparable to the current maximum level of $37,960 under

the existing mechanism.

39. As for the maximum academic expenses grant levels, we accept the

recommendation of the consultancy study to maintain the existing amounts

in view of the on-going changes in the teaching and learning activities

amidst the development of the new academic structure. It is also proposed

that the annual updating of the maximum academic expenses grant levels to

8 the results of the 2009-10 HES were released in late April 2011

15

be based on the CPI(A) instead of the resources-consuming student price

index compiled annually by the C&SD with institutions’ input.

Report on the Operation of the Relaxed Means Test Mechanism

40. At the LegCo Panel on Education meeting on 9 May 2011,

when examining the proposal on relaxation of means test mechanism

administered by SFAA, Members raised concern about the impact of the

implementation of the statutory minimum wage (SMW) on the eligibility of

the means-tested financial assistance schemes. This is to report the

situation after the implementation of the relaxed means test mechanism.

41. Since the implementation of the relaxed means test mechanism

with effect from the 2011/12 academic year, up to end March 2012, about

354 000 students, from pre-primary to post-secondary levels, have received

means-tested financial assistance, representing about one-third of the

relevant student population. Among them, about 209 000 students (59%)

receive full level of assistance, which is a substantial increase as compared to

about 30% in 2010/11 before the relaxation.

42. Taking heed of Members’ concern about the impact of the

implementation of SMW on the eligibility of the means-tested financial

assistance schemes, we have compared the relaxed income thresholds for

full level of assistance for the 2012/13 application cycle with the latest

median household income of different family sizes as shown in Annex C.

On the whole, students from families with monthly income at around 50% to

60% of the median household income would be eligible for full level of

assistance while those from families with monthly income at around the

median household income would be eligible for assistance. This is in line

with the proposal made by the Administration when the relaxed means test

mechanism was presented to the Panel in May 2011. We consider that the

relaxed means test mechanism operates effectively and has provided

enhanced support to needy students.

Examination Fee Remission Scheme

43. Separately, we will take into account the views on expanding

the scope of the Examination Fee Remission Scheme administered by SFAA

to enable needy non-Chinese speaking (NCS) students in secondary schools

to sit for other overseas Chinese language examinations when mapping out

the implementation details to further motivate both schools and NCS

students to cross over different learning levels at different stages of

development leading to multiple progression pathways

16

Staffing Implications

44. Additional manpower support is required to implement the package

of proposals to the NLS and means-tested assistance schemes mentioned

above. Specifically, SFAA will need additional staff to handle the options

to be exercised by loan borrowers on extension of their repayment period,

handle an increasing number of loan accounts and deferment applications,

plan for and implement the change of repayment intervals from quarterly to

monthly, plan and implement a course registration system to tighten the

course eligibility criteria under Scheme C, and process applications from

existing grant repayers under FASP for waiving the repayment requirement

etc. After critically reviewing the existing manpower, we propose to create

32 new non-directorate posts9 to enhance SFAA’s processing capacity.

45. At present, the management structure of SFAA consists of only one

directorate officer (Senior Principal Executive Officer (SPEO) at D2 level)

as the Head of Department, designated as Controller, SFAA (C, SFAA),

underpinned by three non-directorate Chief Executive Officers and one

Senior Treasury Accountant as deputies to oversee the administration of

student financial assistance schemes, and another two Chief Executive

Officers and one Senior Systems Manager to oversee general administration

matters and other specific functions. Since the post of Controller, SFAA (C,

SFAA) was upgraded from Principal Executive Officer (PEO) at D1 level to

SPEO in 1996, SFAA has experienced substantial increase in the scope and

complexity of its functions, as illustrated by the following developments

from 1996-97 to 2010-2011 -

(a) the departmental expenditure (excluding grants/loans disbursed) of

SFAA has increased from $7.8 million to $126 million;

(b) the number of financial assistance schemes has increased from six

to 14;

(c) the number of applications for student financial assistance has

increased from 568 000 to 952 000, with the amount of grants and

funds disbursed increasing from $2,820 million to $5,080 million

and the number of loan accounts increasing from around 58 000 to

around 220 000; and 9 The 32 non-directorate posts will comprise of four Executive Officer II (EOII), five Clerical Officer,

12 Assistant Clerical Officer (ACO) and one Clerical Assistant posts on a permanent basis from 1 July

2012; two EOII and two ACO posts on a permanent basis from 1 April 2013; one Senior Executive

Officer, one Executive Officer I, two EOII and two ACO posts on a time-limited basis from 1 July

2012 to 31 March 2014.

17

(d) the number of staff, including civil service and non-civil service

staff, has increased from 110 to 935.

46. With the implementation of various improvement measures of the

financial assistance schemes coming on stream in addition to the existing

major initiative of charting a major organisation restructuring of SFAA in

tandem with the roll-out of the Integrated Student Financial Assistance

System, it is necessary to enhance the staffing support of SFAA at the

directorate level. This will be conducive to the effective governance of the

Agency and sustainable supervision of the expanded functions and major

initiatives to be implemented. We therefore propose to create one

permanent PEO post at D1 rank on 1 July 2012 to strengthen the senior

management structure of SFAA and in particular to oversee the

implementation of the improvement proposals to the means-tested and non

means-tested loan schemes.

Financial Implications

47. The proposals would have financial implications as analysed below -

Non-means-tested Loans

(a) The overall loan balance is projected to increase by $513 million

from $7,859 million in the 2013/14 academic year to $8,372 million

in 2022/23 (i.e. an average increase of $57 million per year over

these nine years), mainly as a result of the extension of loan

repayment period from 10 to 15 years. This is partly offset by the

restriction of loan coverage in Scheme B and change in course

eligibility criteria of Scheme C;

(b) The interest received from RAF seeks to cover the Government’s

risk in disbursing unsecured loans. The reduction of the RAF

interest rate to zero will effectively mean that the Government

would have to absorb the loss arising from irrecoverable default

loans under all the three Schemes. As at end of 2010/11 academic

year, there were about 13 000 defaulters under the NLS, involving

$213 million in arrears and a total outstanding amount of about

$652.7 million. Taking into account the results of SFAA’s latest

efforts in tackling default loans, the estimated amount of

irrecoverable student loans is around $52.3 million. Following the

implementation of the improvement measures, we estimate that the

18

amount of irrecoverable debt would be around $15-20 million each

year;

(c) The relaxation of deferment arrangement would bring about interest

loss comprising interest waived and interest income forgone,

estimated to be around $41.2 million and $14.610

million

respectively each year, based on the number of approved deferment

cases in the 2009/10 academic year and before the implementation

of proposals specified in the paper;

Means-tested Assistance

(d) The improvement measures of FASP would give rise to additional

recurrent expenditure on means-tested grants and LE loans to

eligible needy students. It is estimated that the relaxation of age

limit to 30 and removal of requirements/restrictions relating to prior

academic requirements would lead to an increase of about $17

million for means-tested grants and about $5 million for

means-tested LE loans each year from the 2012/13 academic year

onwards. The removal of grant repayment requirements would

lead to an estimated amount of grants repayment and interest income

forgone at about $44 million and $6 million each year respectively;

(e) As at the end of 2010/11 academic year, there were about 38 000

means-tested LE loan repayment accounts. The proposal to reduce

the interest rate from 2.5% to 1% and extend the standard repayment

period from five to 15 years will have financial implications of

$63.3 million per year; and

(f) Under the new mechanism for setting and adjusting the LE loan

ceiling, it is estimated that an additional loan expenditure of about

$0.4 million per year will be incurred from 2012/13 onwards. As

only minor alteration of annual adjustment is proposed for the

academic expenses grants, no additional recurrent expenditure is

expected for the item.

Manpower resources

(g) The proposed 32 non-directorate posts (including six time-limited

posts and 26 permanent posts) will bring about an additional total

non-recurrent staff cost of $4,379,865 in 2012-13 and 2013-14 and a

10

$1.8 million of the interest forgone is due to deferment of means-tested loans.

19

recurrent staff cost of $6,858,300 in a full year based on the notional

annual mid-point salary (NAMS) value. The proposed creation of

the PEO post will bring about an additional notional annual salary

cost at mid-point of $1,357,200 and full annual average staff cost,

including salaries and staff on-cost, at $1,900,080.

Implementation Timetable

48. For the NLS, we propose to implement the proposals by phases as

follows -

(a) Proposals 1 to 3 and 5 to 8 in the 2012/13 academic year;

(b) Proposal 4, which involves substantial system enhancement, in the

2013/14 academic year;

(c) For Proposal 9, we will continue to deliberate and engage PCPD as

well as the other relevant parties with a view to identifying an

effective way to deter and tackle defaults; and

(d) For Proposal 10, we will monitor the default situation of the loan

schemes and the age profile of defaulters before deciding whether,

and if so, how to take forward this proposal.

49. As regards the proposed improvements to FASP, the means-tested

LE loans and the mechanism of setting and adjusting the maximum levels of

LE loan and academic expenses grant under TSFS, we propose to implement

the measures as detailed in paragraphs 27 to 39 above from the 2012/13

academic year.

Advice Sought

50. Subject to Members’ views, we would seek approval from the

Finance Committee on the improvement proposal to student assistance

schemes and raising the NAMS and establishment ceiling of SFAA to

accommodate the proposed additional non-directorate posts on 8 June 2012.

A summary of the proposals is at Annex D. Subject to Members’ views,

we will also make a submission to the Establishment Subcommittee of the

Finance Committee on 6 June 2012 on the proposed creation of the PEO

post.

20

Education Bureau

May 2012

Annex A

Summary of Views and Comments received during

Phase 2 Public Consultation on Improvement Proposals of

Review of Non-means-tested Loan Schemes

For Against

(1) Reduce the risk-adjusted factor (RAF) rate of the three schemes from 1.5% to zero, and

review the situation after three years

The reduction can ease the repayment

burden of loan borrowers, in particular those

new graduates whose starting salaries are

relatively low.

It is not fair to request those who repay

timely to pay RAF on top of the repayment

interest for the purpose of covering the

actual deficit or the potential loss arising

from default cases.

The RAF should be removed permanently

instead of retaining it and reviewing it three

years later.

A reduced interest rate may induce

excessive borrowing and possible abuse.

(2) Extend the standard repayment period of non-means-tested loans from 10 years to 15

years

The reduction of the instalment repayment

amount resulting from the extension of the

standard repayment period can alleviate the

repayment burden of loan borrowers, in

particular those new graduates whose

starting salaries are relatively low.

The extension is not an effective measure to

solve the repayment difficulties of loan

borrowers but will increase the total interest

expenses.

15 years are too long as loan borrowers

would have other financial commitments to

deal with and hence may increase the risk of

default.

More options on the length of standard

repayment period should be provided.

(3) Relax the deferment arrangements such that those borrowers whose applications for

deferment have been approved would be allowed an extension of loan repayment period

without interest during the approved deferment period, subject to a maximum of two years

The relaxation can effectively help those

who are facing repayment difficulties but

some consider the two-year interest-free

period too short.

The extended standard repayment period of

15 years is already too long and hence no

need to allow further extension.

22

For Against

The interest-free provision may induce

unjustified deferment applications and

appears unfair to those loan borrowers who

repay on time.

(4) Revise the repayment interval from quarterly to monthly basis

It is easier to manage monthly repayment

and also to get in line with the usual practice

of many other bills or credit card payment.

Auto-pay and other convenient payment

options should be provided to facilitate the

new monthly repayment arrangement so as

to reduce the administrative cost.

The change of repayment interval will not

be of significant difference in maintaining

timely repayment.

Options on monthly, quarterly and even

half-yearly repayment interval should be

provided.

(5) Cap the loan amount in respect of each programme at the level of tuition fee payable for

all non-means-tested loan schemes

The alignment can prevent excessive

borrowing and abuse of loan on

non-academic related expenses, such as

travel and investment, etc.

The Government should secure proper use

of public money to assist students in paying

tuition fees but not on their living expenses.

Full-time students should not be deprived

from receiving quality higher education by

being compelled to engage in other activities

to earn their living.

Academic expenses which are study-related

should be provided.

(6) Impose a life-time loan limit, with annual price adjustment mechanism

The proposed $300,000 loan limit should be

adequate for most of the loan borrowers to

finance their studies.

The loan limit can be set lower to prevent

excessive borrowing and ensure the

affordability of loan borrowers for future

repayment.

There should not be a loan limit so as to

encourage continuing and lifelong

education.

The loan limit may not be sufficient to

pursue self-financing programmes even up

to first degree level having regard to the

increasing trend in tuition fee level.

There are also worries that the limit may

inadvertently prevent students from

receiving quality education which may

reasonably charge relatively higher tuition

fee.

23

For Against

(7) Remove the age limit from that imposed on the non-means-tested loan scheme for

students pursuing full-time self-financed locally-accredited programmes

The proposal can remove age discrimination

and provide financial assistance to those

mature students who enroll full-time studies

at latter stage.

Financial assistance may easily be abused as

those aged over 25 are working adults who

should be capable of paying for their studies.

(8) Suitably revise the course eligibility criteria to restrict the eligible courses to those with a

reasonable degree of quality assurance

It is essential to tighten up the eligibility of

course providers and so as to ensure the

quality of programmes from which loans can

be borrowed under NLS.

It is hard to determine a set of objective

assessment criteria for the eligibility of

courses.

The new measure may reduce loan

borrowers’ choices of courses and hence

hinder their study path.

Existing course providers show concerns on

the proposal as it takes time and resources

for existing courses to obtain local

accreditation status.

(9) Share the negative data of defaulters with the credit reference agency under clearly

defined circumstances

The proposal has deterrent effect and can

prevent abuse and excessive borrowing.

Irresponsible loan borrowers should bear the

consequence themselves.

The data can provide good reference to other

credit providers.

Student loan borrowers should not be treated

differently from other private loan

borrowers.

The circumstances of sharing negative credit

data should be clearly defined and made

known to loan borrowers at an initial stage

to enhance the transparency of the policy.

The loan is for education purpose and

students may have genuine difficulty in

repaying upon graduation.

There will be great impact on students’

future.

The proposal is too “commercial” and

Government loan should not be linked to the

private financial sector.

The credit data are confidential personal

data and may be misused by private sector.

The Government should use other means,

e.g., restrict the emigration rights of

defaulters, expedite legal recovery actions,

liaise with the defaulters more proactively

24

For Against

and demand repayment through the tax

system, etc.

The proposal may open the floodgate of the

present closed system, which is almost

exclusive to the banks and licensed money

lenders, to requests of a similar nature from

other government departments or even

private sectors.

(10) Require the more mature first-time loan borrowers to produce credit reports for

assessment of credit worthiness.

The proposal which targets mature loan

borrowers is reasonable in order to

safeguard the proper use of public money.

The proposal should be extended to

defaulters.

There is no empirical data to indicate that

loan borrowers aged over 30 will have a

higher default rate

The proposal discriminates against mature

loan borrowers and should be extended to all

loan borrowers instead.

The Government should help everyone in

need, including mature students, to receive

education.

SFAA should obtain the credit reports and

pay the relevant fees, instead of asking the

borrowers to submit the reports.

Annex B

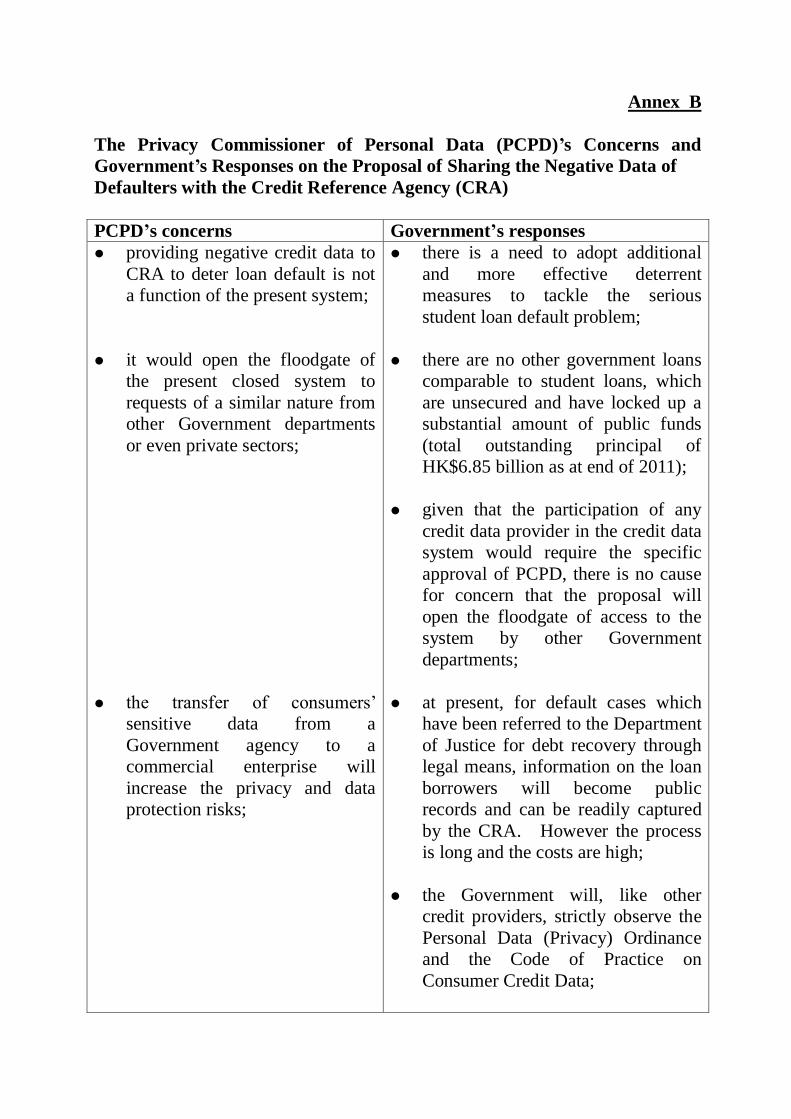

The Privacy Commissioner of Personal Data (PCPD)’s Concerns and

Government’s Responses on the Proposal of Sharing the Negative Data of

Defaulters with the Credit Reference Agency (CRA)

PCPD’s concerns Government’s responses

providing negative credit data to

CRA to deter loan default is not

a function of the present system;

it would open the floodgate of

the present closed system to

requests of a similar nature from

other Government departments

or even private sectors;

the transfer of consumers’

sensitive data from a

Government agency to a

commercial enterprise will

increase the privacy and data

protection risks;

there is a need to adopt additional

and more effective deterrent

measures to tackle the serious

student loan default problem;

there are no other government loans

comparable to student loans, which

are unsecured and have locked up a

substantial amount of public funds

(total outstanding principal of

HK$6.85 billion as at end of 2011);

given that the participation of any

credit data provider in the credit data

system would require the specific

approval of PCPD, there is no cause

for concern that the proposal will

open the floodgate of access to the

system by other Government

departments;

at present, for default cases which

have been referred to the Department

of Justice for debt recovery through

legal means, information on the loan

borrowers will become public

records and can be readily captured

by the CRA. However the process

is long and the costs are high;

the Government will, like other

credit providers, strictly observe the

Personal Data (Privacy) Ordinance

and the Code of Practice on

Consumer Credit Data;

26

as how the CRA assigns a credit

score to individual consumers is

not disclosed, whether the

proposal would produce an

insignificant or a

disproportionately negative

effect on the borrower cannot be

assessed;

if the disclosure is not a purpose

directly related to the original

one of collecting personal data of

student loan borrowers for

processing loan applications,

“voluntary” prescribed consent

has to be obtained from the data

subject, i.e. existing loan

borrowers;

even if the proposal will only

cover new loan applicants and

SFAA will take all practicable

steps to inform the applicants of

the transfer in the event of

default, the question whether the

borrower’s personal data are

collected by means which are

fair in the circumstances of the

case may be relevant. That is,

whether NLS is the only secured

source from which students

irrespective of family

backgrounds can obtain funds to

finance their education;

as revealed by the findings of a

survey commissioned by PCPD,

the percentage of interviewees

supporting the proposal dropped

from 60% to 35% after relevant

privacy concerns had been

explained to them.

only the negative credit data of the

more serious default cases would be

shared with CRA, say, those which

owed more than $100,000 and had

ceased repayment for more than a

year and who had failed to respond

to SFAA’s reminders or to provide

any reasonable justification for the

delayed repayments;

SFAA will ensure that the data

protection principles are fully

complied with;

SFAA is prepared to be subject to a

series of more stringent regulatory

measures than those currently

applicable to licensed banks and

financial institutions on the handling

of consumer credit data;

SFAA will introduce measures to

screen cases by an independent panel

such that only very essential/limited

data will be shared.

given the similarity between SFAA’s

student loans and the unsecured

personal loans offered by licensed

banks and financial institutions, it

should be in the overall public

interest to prevent defaults involving

Government loans (hence public

27

money) in the same way as we are

protecting the private sector from

excessive lending by means of

sharing of such data under the Code

of Practice on Consumer Credit

Data.

28

Annex C

Adjusted Family Income (AFI) Thresholds and

Equivalent Monthly Family Income Limits

for the 2012/13 academic year

Compared with

Median Household Income of Different Family Sizes

Family

size

AFI

threshold for

full level of

assistance

Equivalent

monthly family

income limit

for full

assistance

% of median monthly

household income

[2011whole year]

(% before relaxation)

AFI

threshold

for any

assistance

Equivalent

monthly

family

income limit

for any

assistance

% of median

monthly household

income

[2011whole year]

1 $31,403 $5,233 75% (55%)

$60,722

$10,120 145%

2 $31,403 $7,850 53% (38%) $15,180 102%

3 $38,016 $12,672 63% (40%) $20,240 101%

4 $34,975 $14,573 56% (38%) $25,301 98%

5 $31,403 $15,701 47% (37%) $30,361 90%

6 $31,403 $18,318 48% (39%) $35,421 93%

29

Annex D

Summary of Proposals

to Improve the Non-means-tested Loan Schemes and

the Means-tested Assistance Schemes

vis-à-vis the Existing Arrangements

Measure Existing Arrangement Proposed Arrangement

Non-means-tested Loan Schemes

1. Reducing RAF rate 1.5% per annum

Effective Interest Rate = 3.174% per

annum

0% per annum

Effective Interest Rate = 1.674% per

annum

(subject to review in 3 years’ time)

2. Extending standard

repayment period

10 years 15 years

3. Relaxing deferment

arrangements Interest charged during the

approved deferment period

Upon expiry of deferment

period, balance of the loan

including the interest accrued

has to be repaid within the

remaining compressed period of

less than 10 years at a higher

amount per instalment

Interest-free during the approved

deferment period

Extension of the entire loan

repayment period by a maximum

of two years

4. Revising repayment

interval Quarterly payment

Monthly payment

Implement e-billing and e-enquiry

services

To be implemented in 2013/14

academic year

5. Aligning loan coverage Schemes A & C: Loan amount

of a course capped at tuition fee

payable

Scheme B: Maximum loan

amount equals to tuition fee

payable plus academic expenses

and living expenses assistance

Schemes A, B & C: Loan amount

of a course capped at tuition fee

payable

6. Imposing loan limits No loan limit over life time

under each scheme

Impose a combined life-time loan

limit of $300,000 under Schemes

A and B

Impose a life-time loan limit of

$300,000 under Scheme C which

30

Measure Existing Arrangement Proposed Arrangement

is in addition to the combined loan

limit for Schemes A and B above.

The life-time loan limits to be

adjusted annually in accordance

with the movement of CCPI.

Loan borrowers under Schemes A

and B who have exhausted the

$300,000 loan limit to study

programmes for attaining their

first degree-level study may apply

to SFAA to use up to $100,000 of

their life-time loan limit under

Scheme C, on a case-by-case

basis.

Grandfather existing students who

have enrolled programmes

charging tuition fees above the

loan limit by allowing them to

borrow a cumulative loan

exceeding the proposed ceiling to

complete their programmes up to

first degree level.

7. Removing age limit of

Scheme B

Age limit of 25

No age limit

8. Revising the course

eligibility criteria of

Scheme C

There are nine categories of

eligible courses under Scheme C

as follows –

(1) courses offered by the Open

University of Hong Kong;

(2) courses offered by Hong Kong

Shue Yan University;

(3) part-time publicly-funded

programmes or self-financing,

local award-bearing

programmes (i.e. programmes of

study leading to the award of

local academic qualifications) or

training or development courses

at the post-secondary level

offered by publicly-funded

institutions (including their

Schools of Professional and

Continuing Education);

To restrict eligible courses to

those with a reasonable degree of

quality assurance –

(i) courses accredited by

HKCAAVQ or accredited by

institutions by virtue of their

self-accreditation status or

Programme Area

Accreditation status;

(ii) courses under Yi Jin Diploma;

(iii) courses covered by the

Financial Assistance

Scheme for Designated

Evening Adult Education

Courses;

(iv) training and development

courses provided or funded

by local statutory bodies; and

31

Measure Existing Arrangement Proposed Arrangement

(4) programmes offered under the

Project Yi Jin;

(5) registered courses and exempted

courses under the Non-local

Higher and Professional

Education (Regulation)

Ordinance (Cap. 493);

(6) post-secondary courses, adult

education courses, continuing

and professional education

courses offered by a school

registered under section 13(a) or

exempted from registration

under section 9(1) of the

Education Ordinance (Cap.

279);

(7) courses offered by a Post

Secondary College registered

under the Post Secondary

Colleges Ordinance (Cap. 320);

(8) training or development courses

provided or funded by statutory

bodies; and

(9) continuing and professional

education courses offered by

any institution approved by the

Controller, SFAA in accordance

with the criteria concerned.

(v) registered courses and

exempted courses under the

Non-local Higher and

Professional Education

(Regulation) Ordinance

(Chapter 493).

Provide a transitional period for

existing non-accredited course

providers/courses to obtain

accreditation.

Grandfather existing students by

allowing them to complete their

study programme in case the

course being pursued fails to

obtain accreditation during the

transitional period.

9. Sharing negative credit

data of defaulters with

credit reference agency

No such arrangement

To deliberate and engage PCPD as

well as the other relevant parties

with a view to identifying an

effective way to deter and tackle

defaults.

10. Requiring more-mature

loan applicants to

produce credit reports

No such requirement

To monitor the default situation of

the loan schemes and the age

profile of defaulters before

deciding whether, and if so, how

to take forward this proposal.

Financial Assistance Scheme for Post-secondary Students

1. Relaxing the age limit Age limit of 25

Age limit of 30

2. Removing the

requirements/ For students who have obtained

sub-degree/degree level

No such requirements/ restrictions

32

Measure Existing Arrangement Proposed Arrangement

restrictions on prior

academic qualification

qualification, they are ineligible

to pursue a locally-accredited

programme leading to the same

level of qualification

For students who wish to pursue

a degree course, if they possess

a sub-degree level qualification,

which must be locally accredited

For students who wish to pursue

a top-up degree programme,

they must have obtained a

locally accredited sub-degree

level qualification

3. Removing the

repayment requirement

of grants

Grant recipients who fail to

obtain the intended qualification

within a six-year period from the

first date of disbursement of

assistance have to repay the

tuition fee and academic

expenses grants

No such requirements

Tertiary Student Finance Scheme – Publicly-funded Programmes and Financial Assistance

Scheme for Post-secondary Students

1. Reducing interest rate

of living expenses loan

2.5% per annum

1% per annum

2. Extending standard

repayment period of

living expenses loan

5 years 15 years

3. Relaxing deferment

arrangements Interest-free during the approved

deferment period

Extension of the entire loan

repayment period by a

maximum of five years, i.e. up

to ten years

Interest-free during the approved

deferment period

Extension of the entire loan

repayment period by a maximum

of two years, i.e. up to 17 years

4. Revising repayment

interval Quarterly payment

Monthly payment

Implement e-billing and e-enquiry

services

To be implemented in 2013/14

academic year

5. Revising the mechanism

of setting and adjusting Based on the result of a Student

Expenditure Survey conducted

Adopt the median per capital

household expenditure (with

33

Measure Existing Arrangement Proposed Arrangement

the maximum levels of

living expenses loan and

academic expenses

grant under TSFS

in 1988 and price-adjusted

annually according to the

student price index compiled

specifically by the Census and

Statistics Department (C&SD)

with input from institutions

covered by TSFS.

exclusions of housing, alcoholic

drinks & tobacco, transport and

education expenditures) obtained

from the Household Expenditure

Survey conducted every five years

by C&SD as the benchmark level.

Adjust the loan levels in the

intermediate years by the

Consumer Price Index (A)

computed with same exclusions.

Conduct a review when the extent

of adjustment exceeds 10% in

either direction.

Maintain existing levels for

academic expenses grant. Make

annual adjustment in accordance

with changes in CPI(A).