food and sustainability: will the seed bear fruit? · food and sustainability: will the seed bear...

TRANSCRIPT

Sustainable Swiss Private Banking since 1841.

Food and sustainability: Will the seed bear fruit?

Sustainability study:

Ratings and key themes

December 2010

Content

Sustainability ratings – Danone, Unilever and

Heinz lead the field 1

Health and enjoyment – the industry's dilemma 5

Raw materials – a vital interest in sustainable

farming 9

Factory and field – slow to introduce fair

working conditions 12

Acknowledgements 16

Contacts 17

Publications 18

Food industry 2010 – Sustainability study

1

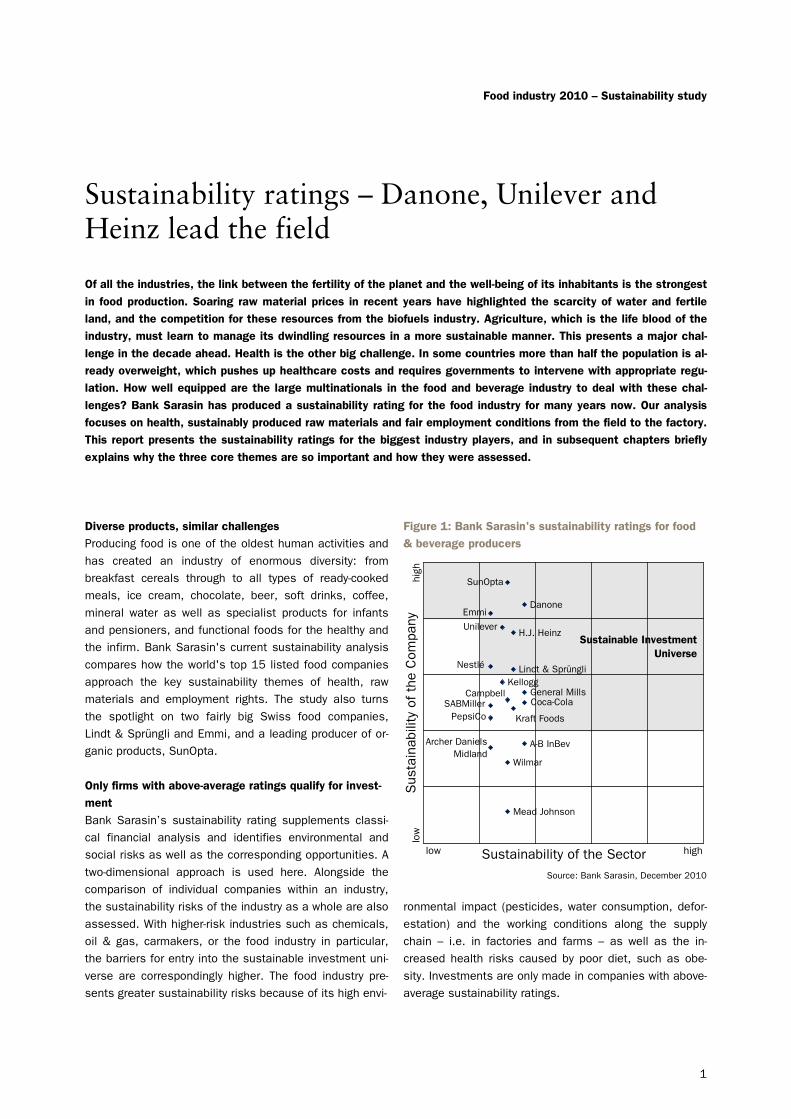

Sustainability ratings – Danone, Unilever and Heinz lead the field

Of all the industries, the link between the fertility of the planet and the well-being of its inhabitants is the strongest

in food production. Soaring raw material prices in recent years have highlighted the scarcity of water and fertile

land, and the competition for these resources from the biofuels industry. Agriculture, which is the life blood of the

industry, must learn to manage its dwindling resources in a more sustainable manner. This presents a major chal-

lenge in the decade ahead. Health is the other big challenge. In some countries more than half the population is al-

ready overweight, which pushes up healthcare costs and requires governments to intervene with appropriate regu-

lation. How well equipped are the large multinationals in the food and beverage industry to deal with these chal-

lenges? Bank Sarasin has produced a sustainability rating for the food industry for many years now. Our analysis

focuses on health, sustainably produced raw materials and fair employment conditions from the field to the factory.

This report presents the sustainability ratings for the biggest industry players, and in subsequent chapters briefly

explains why the three core themes are so important and how they were assessed.

Diverse products, similar challenges

Producing food is one of the oldest human activities and

has created an industry of enormous diversity: from

breakfast cereals through to all types of ready-cooked

meals, ice cream, chocolate, beer, soft drinks, coffee,

mineral water as well as specialist products for infants

and pensioners, and functional foods for the healthy and

the infirm. Bank Sarasin's current sustainability analysis

compares how the world's top 15 listed food companies

approach the key sustainability themes of health, raw

materials and employment rights. The study also turns

the spotlight on two fairly big Swiss food companies,

Lindt & Sprüngli and Emmi, and a leading producer of or-

ganic products, SunOpta.

Only firms with above-average ratings qualify for invest-

ment

Bank Sarasin’s sustainability rating supplements classi-

cal financial analysis and identifies environmental and

social risks as well as the corresponding opportunities. A

two-dimensional approach is used here. Alongside the

comparison of individual companies within an industry,

the sustainability risks of the industry as a whole are also

assessed. With higher-risk industries such as chemicals,

oil & gas, carmakers, or the food industry in particular,

the barriers for entry into the sustainable investment uni-

verse are correspondingly higher. The food industry pre-

sents greater sustainability risks because of its high envi-

Figure 1: Bank Sarasin's sustainability ratings for food

& beverage producers

Source: Bank Sarasin, December 2010

ronmental impact (pesticides, water consumption, defor-

estation) and the working conditions along the supply

chain – i.e. in factories and farms – as well as the in-

creased health risks caused by poor diet, such as obe-

sity. Investments are only made in companies with above-

average sustainability ratings.

SABMiller

Lindt & Sprüngli

PepsiCo

Nestlé

Mead Johnson

Kraft Foods

Kellogg

H.J. Heinz

General Mills

EmmiDanone

Coca-ColaCampbell

Wilmar

Archer Daniels

MidlandA-B InBev

Sustainability of the Sector

Susta

inability

of th

e C

om

pany

high

low

hig

h

low

SunOpta

Unilever

Sustainable Investment

Universe

Food industry 2010 – Sustainability study

2

Danone, Unilever, Heinz, Nestlé: strong in raw materials

In the current year's sustainability ratings, Danone, Unile-

ver and Heinz take the lead, followed by Nestlé (see Fig-

ure 1). Danone achieves an above-average rating for all

the major sustainability criteria. Unilever and Heinz – and

Nestlé to a slightly lesser degree – have significant

strengths in the promotion of sustainably produced raw

materials. However, Heinz and Unilever are only slightly

better than average when it comes to the health aspects

of their products, while Nestlé is relatively well posi-

tioned.

Unilever and Nestlé: poor record in employment rights

One major area for improvement both at Unilever and

Nestlé is the lack of employment rights in the numerous

production facilities in developing countries. This year

Unilever, after a prolonged period of disputes, agreed to

enter into a collaboration with the international union of

the sector. Nestlé is still at the start of this process, but

is meant to have signalled its willingness to commence a

dialogue with the unions.

Controversial business activities rated as risks: formula

milk and bottled water are prime examples

Danone and Nestlé are both market leaders in two areas

which repeatedly attract controversy: infant formula milk

and bottled water. With formula milk, the main area of

conflict is the health aspect (see Chapter 2), while with

bottled water the main problem is its environmental foot-

print compared with normal tap water and the privatisa-

tion of a public resource. Companies repeatedly fall into

the media spotlight. These business activities influence

our risk assessment: the rating has to be adjusted to re-

flect their contribution to group sales and also the com-

pany’s market leadership.

Significant room for progress

In the broad midfield of company rankings very little pro-

gress has so far been achieved (with a few exceptions) in

the major sustainability issues. This means that the in-

dustry needs to make its products far more healthy, pro-

vide more transparent information to consumers and

market products in a more responsible way. In the USA

especially, the challenges are enormous. Independent in-

stitutions are assessing nutritional value and marketing

practices, and politics is getting involved. Raw materials

need to be procured in a more sustainable manner as

well. There is already a lot of activity in this area on the

other side of the Atlantic. In recent years virtually every

large multinational has launched new initiatives, drawn

up suitable strategies and entered into collaborations

with environmental organisations such as the WWF or

Rainforest Alliance.

Figure 2: What the major food & beverage companies

produce (2009)

Source: company details

Organic food companies pioneered the way in raw mate-

rials

Our investment universe also includes a number of com-

panies selling organic products, such as Canada's Sun-

Opta, one of the world's biggest suppliers of organic raw

materials. With its closed-loop systems and the avoid-

ance of problematic agrochemicals, organic farming pro-

vides solutions for some of the environmental problems

associated with conventional farming, such as the signifi-

cant ecological impact on groundwater and the reduction

of soil fertility. These companies therefore perform very

well as far as raw materials are concerned.

Controversial and disputed health benefits

Consumers generally believe that organic products offer

added value – whether from an environmental or health

Company Sales

USD bn

Employ-

ees

Main products

Campbell Soup 7.59 17,000 Soups and sauces

Danone 21.5 81,000 Dairy products, bottled water,

babyfood

General Mills 14.8 33,000 Pre-cooked meals, breakfast cereals,

snacks, biscuits

H.J. Heinz 10.5 29,600 Ketchup, sauces, pre-cooked meals,

snacks, babyfood

Kellogg 12.6 31,000 Breakfast cereals, snacks

Kraft Foods 40.4 97,000 Confectionery, snacks, drinks, cheese,

pre-cooked meals

Nestlé 103.7 278,100 Coffee, dairy, pre-cooked meals,

chocolate, petfood, bottled water

Unilever 50.1 163,000 Ice cream (no. 1), tea, soups, marga-

rine, laundry & personal care products

Anheuser-Busch

InBev

36.8 116,000 World’s biggest beer producer, soft

drinks (10% of sales)

Pepsico 43.2 203,000 World’s biggest snacks producer,

leading soft drinks seller

SABMiller 26.3 70,100 Second-biggest beer producer, soft

drinks as well (10% of sales)

Coca Cola 31.0 92,800 World’s biggest producer of soft drinks

Mead Johnson

Nutrition

2.8 5,600 Infant and baby food

Archer Daniels

Midland

35.9 25,600 Wholesaler of cereals and rapeseed,

palm oil, soya and cocoa

Wilmar 23.9 70,000 World’s biggest grower and processor

of palm oil and soya (mainly)

Food industry 2010 – Sustainability study

3

perspective. In Asia and especially in China, where nu-

merous food scandals have unsettled consumers, the

term organic has now become synonymous with safe

products (i.e. free of toxins). There is also evidence to

suggest that certain organic raw materials, such as milk,

contain a higher proportion of healthy fatty acids. Health

benefits are generally a controversial and disputed area

within the food industry. It remains to be seen which sus-

tainability strategies will bear fruit.

4

Food industry 2010 – Sustainability study

5

Health and enjoyment – the industry's dilemma

Food and exercise are vital factors for good health. For many centuries, a little extra weight was no bad thing. De-

cent nutrition and living standards have ultimately increased life expectancy. But this model has been turned on its

head over the past 30 years: the glut of food on offer in our part of the world has encouraged people to become

overweight and obese. This can decrease life expectancy by up to 10 years. In many OECD countries more than

50% of the population are already overweight, and in transitional economies such as Brazil and Russia – and even

China - the proportion is already higher than 25%. These figures highlight the extent of the problem. The food and

beverage industry is part of this problem, and is keen to make a bigger contribution to the solution, under the ban-

ner of health. Bank Sarasin assesses whether the industry is moving towards healthier products, and the concrete

steps it is taking in this direction.

Food: universally available and cheaper than ever

Our food – measured in terms of calories – is better value

for money than ever before, our everyday world is flooded

with appealing food offers and ready-cooked meals are

becoming more and more prevalent in our weekly food

shop. Along with other changes to our lifestyle, a recent

OECD report shows that this has led to a dramatic rise in

the number of overweight and obese people (see Figure

3). While this trend seems to be flattening out in some

countries, the rate is actually increasing in developing

countries especially. And it is alarmingly high in children

as well, which will be an enormous burden in future.

Soaring healthcare costs

Obesity pushes up the cost of treating overweight pa-

tients by up to 25%. Diabetes, cardiovascular and other

associated diseases frequently only come to light years

afterwards, however. In the UK, health authorities esti-

mate that the costs of obesity could inflate healthcare

spending by 70% up to 2015, and by as much as 240%

by 2025. However, the OECD report cited says that it is

uncertain whether obesity will actually push up healthcare

costs across the economy as a whole, as allowances

also need to be made for the reduced life expectancy of

overweight people.

Active government, aware consumers

Recent years have shown that the state is keen to take a

more proactive role. There has already been a wide ban

of unhealthy products in schools. Taxes on sugary drinks

or preventing their purchase with food tokens are just

some of the measures being considered in the USA. The

First Lady is also attempting to get leading companies to

Figure 3: Obesity on the increase – percentage of over-

weight people in the adult population

Source: OECD „Obesity and the Economics of Prevention“, 2010

commit to binding targets for reducing the calorie content

of their products. In Europe the discussion has centred

on clearer labelling of fat, sugar and other ingredients, as

well as tougher regulation on the health claims made in

advertising. Consumers have also changed, and health

has become a much more important consideration when

making their purchases.

Overweight and obesity are measured by the Body Mass

Index. A male adult of average height (1.75m) is classed

as overweight if he weighs over 77 kilos, and obese if

more than 92 kilos. For a female adult with an average

height of 1.65m the respective figures are 68 and 82 ki-

los.

USA

UK

Australia

France

Spain

Korea

0%

25%

50%

75%

100%

1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

Food industry 2010 – Sustainability study

6

Health and enjoyment: getting the balance right

The food industry is increasingly looking for ways to find a

better balance between health and enjoyment. For dec-

ades the amount of sugar, fat and salt contained in prod-

ucts has given them their characteristic taste. Many chil-

dren's products have in particular successfully estab-

lished themselves in this way. Prepared meals and fast

foods are usually too high in fat and salt and often tend

to contain too much sugar as well. By contrast, vital in-

gredients such as fibre or vitamins are often missing al-

together. The main challenge facing companies is there-

fore to come up with healthier products that still taste

good.

Product mix presents both opportunities and risks

Bank Sarasin's sustainability rating attaches huge impor-

tance to the health of the company's product portfolio, as

it is an indicator of how well the company is equipped to

deal with the opportunities and risks presented by the

growing healthy lifestyle trend. So far, however, the in-

dustry has no commonly accepted standard for the nutri-

tional value of products, which seems rather astonishing

given the importance of this topic. Some companies, for

example, have stricter rules in this area, while others are

more lax. Given the lack of reliable data, we have studied

general criteria such as the fat, salt and sugar content,

as well as making an assessment of the unhealthy, im-

proved and healthy products, augmented by the opinions

of selected experts and institutions.

Danone, Kellogg and Nestlé have the best profile

Danone comes top of our ratings of the biggest food

groups (Figure 4). Kellogg and Nestlé also have a rela-

tively well balanced risk/opportunity profile. With the

other companies, the proportion of healthy product

groups is significantly smaller, but strategies for reformu-

lating products are a priority. Going forward, the key

questions are: Will binding standards for nutritional value

be introduced soon in some markets? And will the com-

panies be able to meet these tougher standards or will

products have to be upgraded at significant expense?

And will companies strive for adequate standards when

developing new products?

Alcohol viewed in a critical light

With beverage companies, alcohol is another factor to

consider. Following the words of Paracelsus "The dose is

what makes the poison", it is the consumer who decides

Figure 4: Health risks of the product portfolio

(as a % of sales)

Sources: Own and estimates of experts of the IASO; Rudd Center for Food

Policy & Obesity, 2009; Dexia, 2009

whether to drink in moderation or to excess. But there

has been a significant shift in drinking habits in recent

decades. More and more young people, along with other

sections of the population in developing countries with lit-

tle experience of drink, are now consuming more alcohol.

In addition to chronic diseases such as liver damage,

road accidents through drunk driving are another very un-

fortunate consequence. There are signs of tighter regula-

tion of alcohol, such as taxation or restrictions on the

sale or advertising of drink at sports events, for example.

Bank Sarasin therefore makes a critical assessment of

companies' portfolio of alcoholic drinks.

Responsible advertising

In addition to the risks and opportunities presented by

the product mix, Bank Sarasin also assesses how well

the theme of health and nutrition is integrated into the

corporate and product strategy. And because the food

and beverage industry has such a massive advertising

budget, we also examine how responsibly companies

market their products. Here formula milk is one of the

lines of business that is repeatedly the centre of contro-

versy.

Formula milk, children's products and other controver-

sies

Heavily targeted by marketing activities for decades, the

percentage of mothers that breastfeed their babies has

fallen dramatically in Asia especially, against recommen-

dations of the World Health Organization. Furthermore it

is still unclear whether there might be a link between

formula milk and subsequent overweight children. Bank

0%

25%

50%

75%

100%

Dan

one

Kello

gg

Nes

tlé

Gen

eral M

ills

Heinz

Cam

pbell

Unileve

r

Kraf

t

Coca

-Cola

Unhealthy Improved Healthy products groups

Food industry 2010 – Sustainability study

7

Sarasin assesses this aspect along with other frequent

areas of controversy such as genetically modified ingredi-

ents or aggressive advertising aimed at children as a risk

for industry that needs to find a new balance between

health and pleasure.

8

Food industry 2010 – Sustainability study

9

Raw materials – a vital interest in sustainable farming

The rate of population growth and urbanisation over the past 50 years would be unthinkable had it not been possi-

ble to significantly increase our food production at the same time. This has been facilitated by mechanisation, fer-

tilisers, intensive irrigation methods and better crop protection, as well as higher-yielding crop varieties. But fertile

land and clean water are becoming increasingly scarce, while fertilisers and pesticides cause significant damage to

the environment. The large food and beverage producers have realised that the long-term supply of agricultural

products is becoming increasingly precarious. Bank Sarasin assesses their strategies and the concrete steps they

are taking in procuring their main raw materials from more sustainable sources.

Biggest cause of environmental damage

Agriculture – once an emblem of prudent management of

natural resources – has now become the biggest culprit

in causing environmental damage. It is responsible for

90% of global deforestation, whether for arable or pas-

ture land. Farming is also the biggest consumer of

chemicals, generates the highest volume of greenhouse

gases, consumes roughly 70% of the planet's freshwater

resources – mostly in a very inefficient manner – and is

responsible for a dramatic loss of fertile soil through ero-

sion, salinisation or overuse, as well as the run-off of fer-

tilisers polluting local groundwater.

Canvassing for raw materials

The impressive increase in productivity and yields has

created an environmental footprint that is completely un-

sustainable. The large food producers have recognised

the portents of future shortages. They are therefore fo-

cusing their attention not only on price but increasingly on

the long-term secure supply of raw materials. In the past

Coca-Cola relied on the spot market for around 70% of its

raw materials, but nowadays roughly half its supplies

come from long-term delivery contracts. Large multina-

tionals such as Unilever, Nestlé, Kraft and Heinz together

purchase significant amounts of the global harvest of cer-

tain crops: 15-20% of coffee, more than 10% of the

world’s tea, tomatoes and peas, and 5% of the palm oil.

The industry has realised that it needs to invest in the

mainstay of its products: agriculture.

Organics evolving from a niche …

For a long time organic farming was considered to be the

Figure 5: New sustainability standards for raw materials

and their share of global production

The 4C Standard was developed under the auspices of the Deutsche Ge-

sellschaft für Technische Zusammenarbeit (GTZ). MSC, RSPO, RTRS, BSI

and ASC are backed by the WWF.

Sources: latest data from Rainforest Alliance, Unilever, 4C, WWF

only alternative to conventional agriculture. Although or-

ganic farming methods are good for the planet, more than

50 years on they still only account for less than 1% of

farmland worldwide. Even though strong growth can be

seen in Asia, and some countries in Europe now have

more than 10% of their land farmed organically, organic

farming has still not established itself in the cultivation of

environmentally problematic and commercially important

crops such as soya, palm oil or sugarcane.

Standard Agricultural

goods

Certified

percentage

(worldwide)

Rainforest Alliance Bananas 15%

Tea estimated 5%

Coffee 1.3%

4C Coffee no data

Marine Stewardship Fish: wild catch

Council (MSC) White fish 43%

Tuna fish 0.5%

Roundtable on

Sustainable Palmoil

(RSPO)

Palm oil 6.3%

Round Table on

Responsible Soy (RTRS)

Soya under development

Better Sugarcane

Initiative (BSI)

Sugarcane under development

Aquaculture

Stewardship Council

(ASC)

Fish: farmed under development

Food industry 2010 – Sustainability study

10

… to a mass-produced product: new sustainability stan-

dards gain importance

More and more new sustainability standards are now be-

ing introduced by organisations such as the Rainforest Al-

liance or the WWF. Their intention is to improve the envi-

ronmental situation by targeting the mass market, adopt-

ing a less rigorous approach where appropriate. The pos-

sibility of curbing the destruction of rainforests for the

cultivation of soya in Brazil or palm oil in Malaysia, for

example, represents an important step forward. Respect-

ing the needs of indigenous people in these regions is

another important aspect that can be incorporated in

these new standards. The WWF's Market Transformation

Initiative specifically targets these key agricultural com-

modities such as palm oil, soya, sugarcane, fish, beef

and milk.

Roundtable: progress through compromise

The roundtable provides the key to this. The idea is to

negotiate verifiable sustainability standards with all the

leading industry players. The farmers and traders involved

account for more than half the global production volume

in some cases, and not just major buyers but environ-

mental and human rights organisations and farmers’ as-

sociations are being consulted as well. The FSC and MSC

standards for sustainable forestry and combating over-

fishing are already widely known. Sustainably produced

palm oil has become more important for the food indus-

try. Figure 5 shows that some important raw materials

have already been widely certified, but many initiatives

are still at an early stage. Negotiations on soya, for ex-

ample, repeatedly falter because of the difficulty in agree-

ing binding control mechanisms. Standards for beef or

fish farming – both areas with pressing environmental

problems – are only just being developed.

Long-term supply and reputation at stake

We see the ability to procure raw materials increasingly

from sustainable sources as being one of the industry's

biggest challenges. Here it is not simply a question of a

long-term secure supply and environmental responsibility.

As consumer companies with a host of leading global

brands, themes that fall under the media spotlight, such

as the clearance of rainforests to grow palm oil or soya,

play a vital role in the brand’s image. Recently Nestlé has

even had to defend itself in social media such as Face-

book after Greenpeace launched a campaign against

palm oil sourced from areas created by cutting down the

rainforest.

Green genetic engineering: benefits and risks

Green genetic engineering is another theme that crops up

when discussing raw materials. At present, this essen-

tially means using seeds that have been genetically modi-

fied to make them resistant to herbicides or pests.

Nowadays significant transgenic crops mainly include

soya, maize, rapeseed and cotton. Researchers are also

looking to modify seeds to include additional properties

such as resistance to drought. The main benefits of this

are higher crop yields and less use of crop protection

agents, or at least switching to agents that are kinder on

the environment. At the same time, this technology is ex-

tremely controversial. There are undesirable effects and

reservations that question important concepts of green

GMOs. The International Assessment of Agricultural

Knowledge, Science and Technology for Development

(IAASTD), which in 2009 published a report on the future

of agriculture, is very cautious in its assessment of the

opportunities provided by genetic engineering techniques

for agricultural purposes.

Acceptance problems …

Environmental organisations and (primarily) European

consumers are sceptical as well. Based on the knowl-

edge currently available, unknown risks for the environ-

ment and for our food chain cannot be ruled out. The lack

of clear findings creates uncertainty. Consumers want

transparency, and organisations such as Greenpeace

have compiled consumer advice on how to avoid products

containing GMOs.

… and risks outweigh in our opinion

Given this stalemate, Bank Sarasin thinks the risks out-

weigh the opportunities for the time being and excludes

the seed producers from its investment universe. With

food producers, the use of GM ingredients is rated as

critical. Here most of the big companies follow a regional

policy: they avoid GMOs altogether in Europe, but other-

wise place no restrictions on their use. Only the organic

food producers studied completely avoid the use of

GMOs. The Swiss dairy producer Emmi has also imposed

a ban on the use of genetically modified animal feed.

Food industry 2010 – Sustainability study

11

Sustainable raw materials: assessment of strategy and

implementation

Bank Sarasin essentially assesses two aspects of sus-

tainable raw material procurement: Firstly, is there a clear

strategy in place for procuring the most important materi-

als increasingly from sustainable sources (see figure 6)?

Where does the company stand in relation to the imple-

mentation of the strategy? Are suitable standards used

and does the company have the necessary expertise?

And secondly, what proportion of raw materials already

comes from sustainable sources? For example, member-

ship of one of the roundtables mentioned earlier does not

in itself mean that a company is really serious about pro-

curing its raw materials from sustainable sources. Here it

is important to dig below the surface. There still needs to

be a significant shift in corporate reporting away from

simply anecdotal information to hard facts.

Figure 6: Clear strategy for procuring important raw

materials from sustainable sources

(as % of maximum score)

Source: Bank Sarasin, December 2010

Both small and large companies follow good practices

For companies committed to organic farming methods,

raw materials from land that has been farmed in a sus-

tainable manner are the business model to some extent.

For this reason the Canadian company SunOpta scores

the highest rating when it comes to raw material strate-

gies. Apart from these industry minnows, however, some

of the food giants also have very ambitious goals and ex-

tensive know-how. Heinz is the world's biggest consumer

of processed tomatoes and for the past decades has

pioneered the cultivation of tomato varieties requiring

fewer pesticides. Clear targets are set for water con-

sumption and the amount of greenhouse gas emissions

for growing tomatoes. Unilever is also a veteran in this

area. It has its own comprehensive standards and is in-

creasing using independent schemes: by 2015 it wants

to procure all its palm oil and tea from certified sustain-

able sources (Unilever purchases 12% of the world's tea

harvest and 3% of palm oil).

Increasingly binding targets …

Other companies that score better than average include

Danone and Nestlé, who are the world's biggest purchas-

ers of milk and coffee. Both companies have defined

binding targets for procuring raw materials from sustain-

able sources. In the case of dairy products there are no

recognised standards, apart from organic milk – they are

currently still under development. However, Danone has

reached agreements with its major suppliers on the re-

duction of greenhouse gas emissions, which is a major

problem for the dairy industry. The amount of methane

produced by cows, for example, can be reduced by chang-

ing the composition of their cattle feed.

… and cooperations predominate

Many of the large US companies are also increasingly ac-

tive, working on strategies to promote raw materials pro-

duced by sustainable farming methods. Some of them

have even entered into cooperations with leading envi-

ronmental organisations. With their support, the aim is to

identify the major sources of potential: Which raw mate-

rial should the company target, and how? Some large

corporations are also involved in the roundtable negotiat-

ing sustainability standards. It is likely that companies

such as Coca-Cola and Kraft will perform better in this

area in future.

0% 25% 50% 75% 100%

SunOpta

Unilever

Heinz

Danone

Nestlé

Pernod Ricard

Campbell

Diageo

SABMiller

Coca-Cola

General Mills

PepsiCo

Kellogg

Kraft Foods

A-B InBev

Food industry 2010 – Sustainability study

12

Factory and field – slow to introduce fair work-ing conditions

The environmental risks in our food chain have been the focus of much attention and the industry is showing in-

creasing awareness of its responsibility. But working conditions – whether in the companies' own factories or in

the many pre-production stages in farming – still leave a lot to be desired. Two main trends can be identified: an in-

creased use of precarious work, which is leading to a deterioration in employment rights and working conditions.

What’s more, consumers are only slowly becoming aware of the social conditions under which branded products

are manufactured. Fairtrade and child labour in cocoa-growing regions have both attracted a lot of public attention,

for example. Companies are taking initial steps to try and influence the working and living conditions of farmers

and farm labourers. Bank Sarasin assesses how committed companies are to promoting decent working conditions

and employment rights not just in their own workforce, but along the entire supply chain.

Important employers

The food industry, along with the very extended agricul-

tural supply chain, is one of the world's biggest employ-

ers. The scope of the industry ranges from highly quali-

fied staff working in laboratories and soft commodity

dealers, through to factory workers (with or without per-

manent employment contracts) and even small or large-

scale farmers with scores of unskilled labourers working

in fields and plantations.

Increase in the use of precarious work in factories

With big companies such as Unilever, Danone, Nestlé or

Coca-Cola, around half the workforce works in factories,

and just as many often work in developing and newly in-

dustrialised countries. Here there are some factories

where more than half the workforce have no fixed em-

ployment contract. Food companies use contract workers

or a temporary company, and outsource production to

subcontractors of all stripes, or through other mecha-

nisms. Trade unions no longer have access to these

workers, their wages generally tend to be lower and the

insecure employment conditions represent a drastic ero-

sion of social benefits and lack of protection in the event

of sickness or accidents.

What do branded products stand for?

More and more workers involved in the production of

branded products for the large food multinationals no

longer have a fixed (or adequate) employment relation-

ship with the company. This is increasingly the case even

in Europe and the USA. As a result, companies are

gradually moving away from their social responsibility to

provide decent working conditions and employment

rights. This trend, which is being monitored both by the

International Labour Organisation (ILO) and the Interna-

tional Union of Food (IUF), is rather worrying: increasingly

precarious work conditions in the value chain of branded

products pose a number of risks, as experiences in other

industries have shown. Companies are also being scruti-

nised more closely by NGOs and the media. Bank Sarasin

therefore assesses whether companies provide adequate

reporting of insecure employment relationships or trade

union representation, and to what extent they support

important labour rights.

Figure 7: Global trade unions: new negotiation part-

ner for multinational companies

Source: IUF, 2010 and ILO, 2010

Global rights and global labour: out of sync

The basic impression that comes across when analysing

companies is that the globalisation of the workforce is

Group management

Local management

Employees

Local union

Global union

Group management

Local management

Employees

Local union

Global union

Food industry 2010 – Sustainability study

13

not moving along at the same pace as the global protec-

tion of important labour rights. Globally valid codes of

conduct do certainly exist, but in most cases there are no

suitable mechanisms for reviewing and resolving conflicts

with employees, and transparency regarding these

themes is often very poor. For example, only two large

companies, Danone and Perod Ricard, publish details on

the percentage of workers with no fixed employment con-

tract.

International framework agreement: one of the solutions

Danone is in fact the only big multinational to have

signed a framework agreement with the IUF on globally

applicable employment standards. Coca-Cola and Chi-

quita have close relationships with the IUF, while Unilever

is more reluctant to engage. Danone's global agreement

is now in its fifth year and has been hailed as a success

by both parties. A global works council was set up in

2009 and Danone's awareness of pressing problems has

increased significantly. At the moment, for example, an

agreement is currently being drawn up on dealing with

stress.

Global trade unions as mediators

The experience of Danone and companies from other in-

dustries shows that global trade unions can play a valu-

able role as mediators between group management and

the local unions when it comes to negotiating a more

even balance between the interests of the company and

the employees (see Figure 7). They also have extensive

experience in resolving conflicts in different areas of the

world. Furthermore, they act as an additional information

source and negotiating partner for group management

when it comes settling local labour disputes. Quite often

the incumbent management and the local unions are too

entrenched in their respective positions. Mediation is

therefore vital.

Employment conditions in agriculture: precarious work

for subsistence level pay

What are working conditions like at the agricultural end of

the food chain? A prevalence of seasonal workers during

harvest time, subsistence risks through crop failure and

price collapse, frequent accidents and illnesses caused

by agrochemicals, and generally casual employment rela-

tionships. The International Labour Organisation also es-

timates that around 60% of the world's child labour is

concentrated in farming. Here it is quite common for chil-

dren to be helping out on the family farm, with no pay,

and the work is often dangerous. But farming and fishing

is still the main source of employment for most of the

population in many countries. It is therefore one of the

most important drivers of economic development in poor

countries.

Market power allows companies to have an influence

Commodities such as cocoa and coffee are produced by

millions of small growers. In this complex supply chain, is

it actually possible for large multinationals to have any in-

fluence at all on working conditions? For many raw mate-

rials, the answer is yes. Large corporations have enor-

mous market power and a well-established network of

suppliers. The banana supply chain for the UK market

clearly demonstrates this concentration (see Figure 8).

These types of market structure not only allow companies

to set prices, but also to dictate other conditions. To

bring some light into the last mile of the supply chain is

certainly a challenge, but numerous initiatives show there

are opportunities to do so.

Figure 8: Bottleneck market structure – five large compa-

nies purchase bananas for the UK from 15,000 growers

Source: Vorley, 2003 from ILO Global Agri-Food Chains, 2008

Two main starting points: price and yield

With child labour, there are two starting points for achiev-

ing a positive improvement in the long run: safeguarding

farmers' subsistence by paying higher prices for agricul-

tural goods and services, and providing technical and

structural support for farmers to enable them to achieve

better yields and boost their income in the process. This

reduces pressure on farmers to fall back on children as a

free source of labour.

Consumers 60 million

Retailers 5 retailers

(70% market share)

Ripeners/Distributers 5 companies such as

Dole, Chiquita

15‘000 small-medium scale

Production farmers with

400‘000 plantation workers

Food industry 2010 – Sustainability study

14

Price premiums: transparency and Fairtrade

With the help of an independent organisation, Lindt &

Sprüngli has established a system that allows it to trace

the cocoa from Ghana back to the original grower. This

transparency, and the accompanying quality assurance,

provides farmers with a premium – an important inde-

pendent initiative by the company to safeguard the exis-

tence of farmers and combat the use of child labour.

Cadbury, now owned by Kraft, has a high proportion of

Fairtrade products on the market – a strategy that is gain-

ing traction in the UK market especially. On the one hand

farmers receive a guaranteed base price which covers the

cost of sustainable soil management. They also receive a

Fairtrade premium. This goes to cooperatives to be used

for investment in production equipment such as irrigation

systems or the provision of basic essentials for the local

community, such as building a new school. In return,

buyers such as Cadbury receive certified raw materials for

which the agreed conditions can be verified, and it can

also use the Fairtrade label when marketing its products.

Know-how helps to boost yields and drive development

Many companies such as Heinz, Nestlé and Coca-Cola

now increasingly purchase their main raw materials di-

rectly, for example from farming cooperatives. This direct

relationship allows programs to be set up to improve

farmers' know-how and technical skills. The goal is to

boost yields and at the same time to improve quality as

well. Large multinationals can work alongside research

institutions to look for more resilient crop varieties, pro-

mote new techniques in soil and plant protection and

support the establishment of farmers' cooperatives.

Credibility of long-term engagement: a pressing chal-

lenge

It remains to be seen whether the seed of these social

measures will bear fruit with respect to the key chal-

lenges facing the industry. With such complex issues as

child labour, it is unrealistic to expect rapid results. But

now more than ever, food companies need to ensure

transparency and credibility.

15

Food industry 2010 – Sustainability study

16

Acknowledgements

The author would like to thank the following experts for providing

valuable information for this study:

Tim Lobstein, policy director of the International Association of the

Study of Obesity (IASO) and member of the International Obesity

Taskforce, advises governments and the World Health Organization,

and has also collaborated on the OECD report cited in this docu-

ment.

Jayson Clay, prolific sustainability expert in the field of agriculture,

in charge of the WWF's Market Transformation Initiative for negotiat-

ing sustainability standards with central players in the major agricul-

tural commodities. Thanks also to Helen van Hoeven, coordinator of

the initiative.

Ron Oswald, General Secretary of the International Union of Food,

Agricultural, Hotel, Restaurant, Catering, Tobacco and Allied Work-

ers' Associations (IUF), has many years of trade union experience

and has played a key role in the development of the international

framework agreement. The IUF represents around 10 million indus-

try workers worldwide.

Rabobank Food & Agribusiness Research, which made its exten-

sive expertise available on the individual agricultural commodities.

Author:

Dr. Gabriella Ries Hafner

+41 61 277 71 66

Basel, December 2010

Copyright fee: CHF 50 / EUR 35

Food industry 2010 – Sustainability study

17

Contacts

Andreas Knörzer Tel. +41 61 277 74 77

Head Sustainable Investment [email protected]

Yvonne Emmerich-Weissflog Tel. +41 61 277 70 24

Management Support [email protected]

Bianca Maier Tel. +41 61 277 79 08

Business Development [email protected]

Gabriela Pace Tel. +41 61 277 73 31

Assistant [email protected]

Sustainability Research

Dr. Eckhard Plinke Tel. +41 61 277 75 74

Head Sustainability Research [email protected]

Machinery, Electronics,

Electrical Engineering

Makiko Ashida Tel. +41 61 277 74 70

Insurance, Consumer Goods, [email protected]

Trade, Software

Thomas Dietzi Tel. +41 61 277 42 49

Business Services, Real Estate, [email protected]

Construction and Building Materials,

Telecommunication

Dr. Matthias Fawer Tel. +41 61 277 73 03

Energy [email protected]

Antje Greiner Tel. +41 61 277 79 35

Banks, Financial Services [email protected]

Andreas Holzer Tel. +41 61 277 70 38

Chemicals, Paper, Mining, Media, [email protected]

Medical & Healthcare, Water Utilities

Klaus Kämpf Tel. +41 61 277 77 80

Real Estate, Water, [email protected]

Recycling & Waste Management

Transport Infrastructure

Balazs Magyar Tel. +41 61 277 73 66

Countries, Institutions, Energy [email protected]

Dr. Gabriella Ries Hafner Tel. +41 61 277 71 66

Food, Automobiles, Transport [email protected]

Dr. Mirjam Würth Tel. +41 61 277 73 42

Tourism, Support [email protected]

Bank Sarasin & Co. Ltd [email protected]

Sustainable Investment www.sarasin.ch/sustainability

CH-4002 Basel

Client Services

Erol Bilecen Tel. +41 61 277 75 62

Head Client Services [email protected]

Institutional Clients

Dr. Michaela Collins Tel. +41 61 277 77 68

Private Clients, Churches [email protected]

Susanne Gessler Tel. +41 61 277 42 59

Administration, Private Clients [email protected]

Alexander Mülhaupt Tel. +41 61 277 73 07

Institutional Clients [email protected]

Sonia Wagner Tel. +41 61 277 73 64

Private Clients [email protected]

Nahrungsmittel 2010 – Nachhaltigkeitsstudie

18

Publications

Solar Energy 2010 Solar industry - Entering new dimensions. Matthias Fawer, Balazs Magyar, November 2010

Renewable Energy Renewable energies: evolving from a niche to a mass market. Matthias Fawer, August 2010

Emerging Countries Emerging Sustainability – Sustainability analysis of emerging market companies. Andreas Holzer,

May 2010

Country Sovereign Bonds The world in a dilemma between prosperity and resource protection - Sustainability rating of sovereign

bonds 2010. Balazs Magyar, March 2010

Solar Energy 2009 Solar industry – The first green shoots of recovery. Matthias Fawer, November 2009

Automotive Automotive: An industry powers ahead – Sustainability research report: Key themes and company ratings.

Gabriella Ries Hafner, September 2009

Real Estate Sustainable Real Estate – Investing in bricks and mortar. Sustainability as a criterion for investing in the

real estate sector. Klaus Kämpf, Thomas Dietzi, September 2009

Renewable Energy Renewable energies: sunnier times ahead, once storms have cleared the air. Matthias Fawer, June 2009

Solar Energy 2008 Solar Energy 2008 – Stormy weather will give way to sunnier periods. Matthias Fawer, November 2008

Energy Efficiency Energy efficiency – hidden capital. How investors can benefit from the "cheapest source of energy".

Eckhard Plinke, June 2008

Commodities Commodities – still a responsible investment? Eckhard Plinke, Dominique Ehrbar, Andreas Holzer,

Gabriella Ries, June 2008

Solar Energy 2007 Solar Energy 2007 – The industry continues to boom. Matthias Fawer, November 2007

Medicinal Technology A healthy future? An analysis of the sustainability of the medical technology industry. Andreas Holzer,

October 2007

Company Rating Assessing corporate sustainability – Methodology of the Sarasin company rating. Eckhard Plinke,

July 2007

Railway A multi-track future – An analysis of the social and environmental aspects of railways and public

transport. Gabriella Ries, March 2007

Solar Energy 2006 Solar energy 2006 – Light and shade in a booming industry. Matthias Fawer, December 2006

Banks Banking on sustainability: An analysis of the social and environmental aspects of international banks.

Klaus Kämpf, November 2006

Industry Rating The Sarasin industry rating – Methodology and results of sector sustainability analysis. Eckhard Plinke,

September 2006

Biofuels Biofuels – transporting us to a fossil-free future? Matthias Fawer, July 2006

Retail Trade Buying into sustainability – Environmental and social challenges in Trading, Distribution and Retailing.

Michaela Collins, June 2006

Textiles, Clothing & Luxury Goods "Just do it" – but responsibly. An analysis of the environmental and social aspects of the apparel, textile

and luxury goods industry. Makiko Ashida, March 2006

Solar Energy 2005 Solar Energy 2005 – Bridging the gap between shrinking natural resources and booming demand.

Matthias Fawer, November 2005

Pharmaceuticals Always read the label. An analysis of the social and environmental impacts of the pharmaceutical

industry. Andreas Holzer, October 2005

Mortgage Bonds The Sustainability of Covered Bonds. Klaus Kämpf, March 2005

Country Sovereign Bonds Emerging country sovereign bonds: A sustainable investment? Michaela Collins, June 2005

To order copies of reports, please see contact address on previous page.

Trademark information

Sarasin (Logo), Sarasin Sustainable Investment and Sarasin Sustainability-Matrix are trademarks of the Sarasin Group

and are registered in a number of jurisdictions.

Important notice

This publication has been prepared by Bank Sarasin & Co. Ltd, Switzerland, (hereafter "BSC") for information pur-

poses only. It is not produced by our Research Department. Therefore, the Directives on the "Independence of Finan-

cial Research" of the Swiss Bankers Association were not applied. This publication contains selected information and

does not purport to be complete. This document is based on publicly available information and data ("the Informa-

tion") believed to be correct, accurate and complete. BSC has not verified and is unable to guarantee the accuracy

and completeness of the Information contained herein. Possible errors or in-completeness of the Information do not

constitute legal grounds (contractual or tacit) for liability, either with regard to direct, indirect or consequential dam-

ages. In particular, neither BSC nor its shareholders and employees shall be liable for the opinions, estimations and

strategies contained in this document. The opinions expressed in this document, along with the quoted figures, data

and forecasts, are subject to change without notice. A positive historical performance or simulation does not consti-

tute any guarantee for a positive performance in the future. Discrepancies may emerge in respect of our own financial

research or other publications of the Sarasin Group relating to the same financial instruments or issuers. It is impos-

sible to rule out the possibility that a business connection may exist between a company which is the subject of re-

search and a company within the Sarasin Group, from which a potential conflict of interest could result.

This document does not constitute either a request or offer, solicitation or recommendation to buy or sell investments

or other specific financial instruments, products or services. It should not be considered as a substitute for individual

advice and risk disclosure by a qualified financial, legal or tax advisor.

This document is intended for persons working in countries where the Sarasin Group has a business presence. BSC

does not accept any liability whatsoever for losses arising from the use of the Information (or parts thereof) contained

in this document.

© Copyright Bank Sarasin & Co. Ltd. All rights reserved.

Bank Sarasin & Co. Ltd

Elisabethenstrasse 62

P.O. Box

CH - 4002 Basel

Switzerland

Tel + 41 (0)61 277 77 77

Fax + 41 (0)61 272 02 05

www.sarasin.ch

Printed on 100% recycled paper

better life? have a

longer one?

childrenWill your

Or just a

By 2050, about two billion people will be over 60 years old, 62 percent of them in Asia alone. It’s an enormous challenge for

the healthcare services and all the other companies involved. This is also interesting in terms of thematic investments. This is where Bank Sarasin has decades of experience and know-how that are available to you as our client whenever you need them.

www.sarasin.com

Sustainable Swiss Private Banking since 1841.