financial services & wealth management...financial services & wealth management david clarke...

TRANSCRIPT

ST

RA

TE

GY

BR

IEF

ING

, S

TR

AT

EG

Y B

RIE

FIN

G, A

ugust 2001A

ugust 2001

0

Financial Services &Wealth Management

David ClarkeGroup Executive

13 August 2001

ST

RA

TE

GY

BR

IEF

ING

, S

TR

AT

EG

Y B

RIE

FIN

G, A

ugust 2001A

ugust 2001

1

DisclaimerDisclaimer

The material contained in the following presentation isintended to be general background information on WestpacBanking Corporation and its activities as at 13 August 2001.

The information is supplied in summary form and is thereforenot necessarily complete. Also, it is not intended that it berelied upon as advice to investors or potential investors, whoshould consider seeking independent professional advicedepending upon their specific investment objectives, financialsituation or particular needs.

ST

RA

TE

GY

BR

IEF

ING

, S

TR

AT

EG

Y B

RIE

FIN

G, A

ugust 2001A

ugust 2001

•• Current SituationCurrent Situation•• StrategyStrategy

ST

RA

TE

GY

BR

IEF

ING

, S

TR

AT

EG

Y B

RIE

FIN

G, A

ugust 2001A

ugust 2001

3

High return and high growthHigh return and high growthwealth management businesswealth management business

90 101

148

254

149

1997 1998 1999 2000 1H 2001

NPAT $m

Source: Westpac Financial Services Group Statutory Accounts

29% CAGR*195

Embedded value uplift * Excluding accounting impacts

ST

RA

TE

GY

BR

IEF

ING

, S

TR

AT

EG

Y B

RIE

FIN

G, A

ugust 2001A

ugust 2001

4

42.830.5 24.8

17.2 13.8

CB

A(C

olo

nia

l)

NA

B(M

LC

)

AM

P

BT

Wes

tpac

But not top tier in FUMBut not top tier in FUM

$bn $bn

Source: ASSIRT as at March 2001

94.6

72.4

47.135.9 33.3

21.6

CB

A(C

olo

nia

l)

AM

P

NA

B

(MLC

)

BT

DB

Wes

tpac

Total Funds Under Management Retail Funds Under Management

1. 2. 3. 4. 5. 8. 1. 2. 3. 4. 5.

ST

RA

TE

GY

BR

IEF

ING

, S

TR

AT

EG

Y B

RIE

FIN

G, A

ugust 2001A

ugust 2001

5

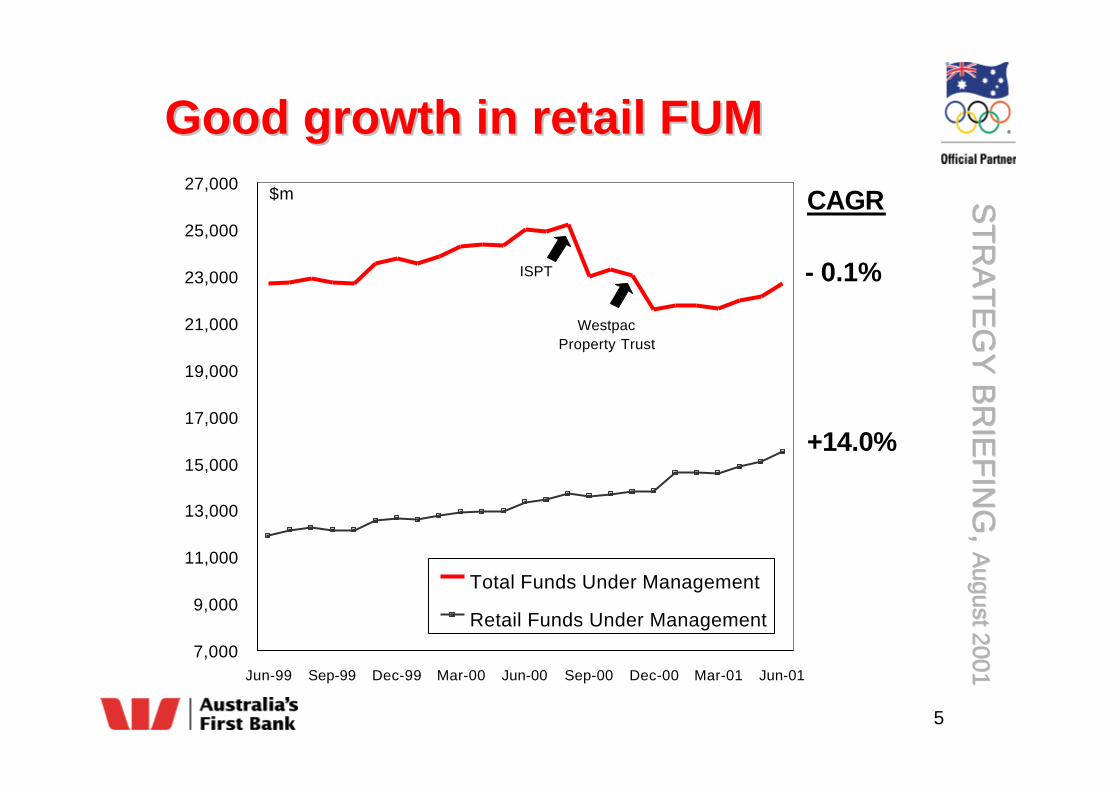

Good growth in retail FUMGood growth in retail FUM

7,000

9,000

11,000

13,000

15,000

17,000

19,000

21,000

23,000

25,000

27,000

Jun-99 Sep-99 Dec-99 Mar-00 Jun-00 Sep-00 Dec-00 Mar-01 Jun-01

Total Funds Under Management

Retail Funds Under Management

ISPT

WestpacProperty Trust

$m

+14.0%

- 0.1%

CAGR

ST

RA

TE

GY

BR

IEF

ING

, S

TR

AT

EG

Y B

RIE

FIN

G, A

ugust 2001A

ugust 2001

6

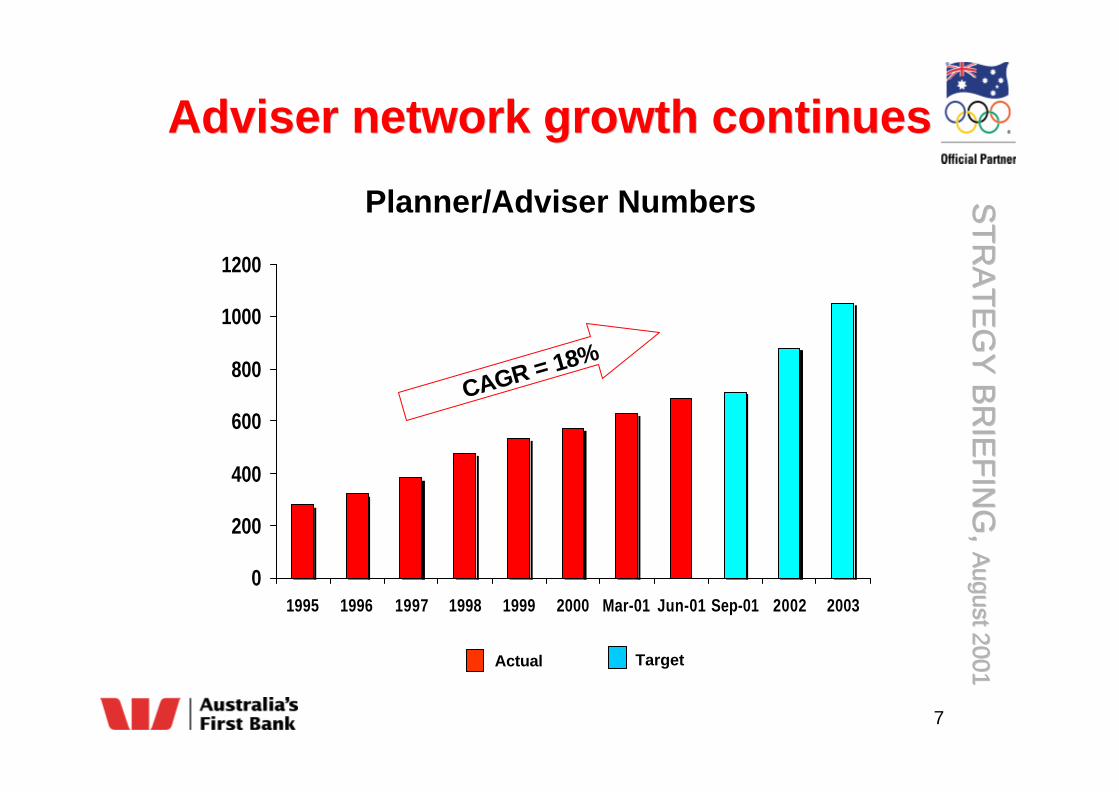

Sound foundations for growthSound foundations for growth

• Growth in adviser network

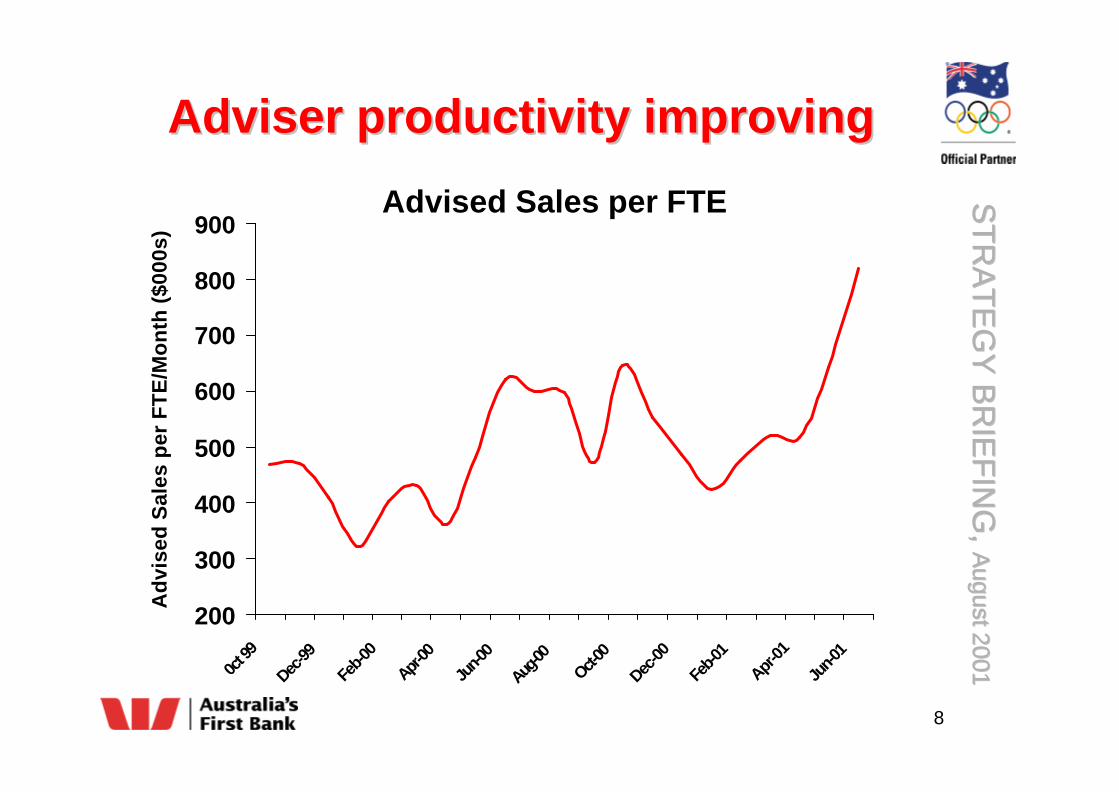

• Adviser productivity improving

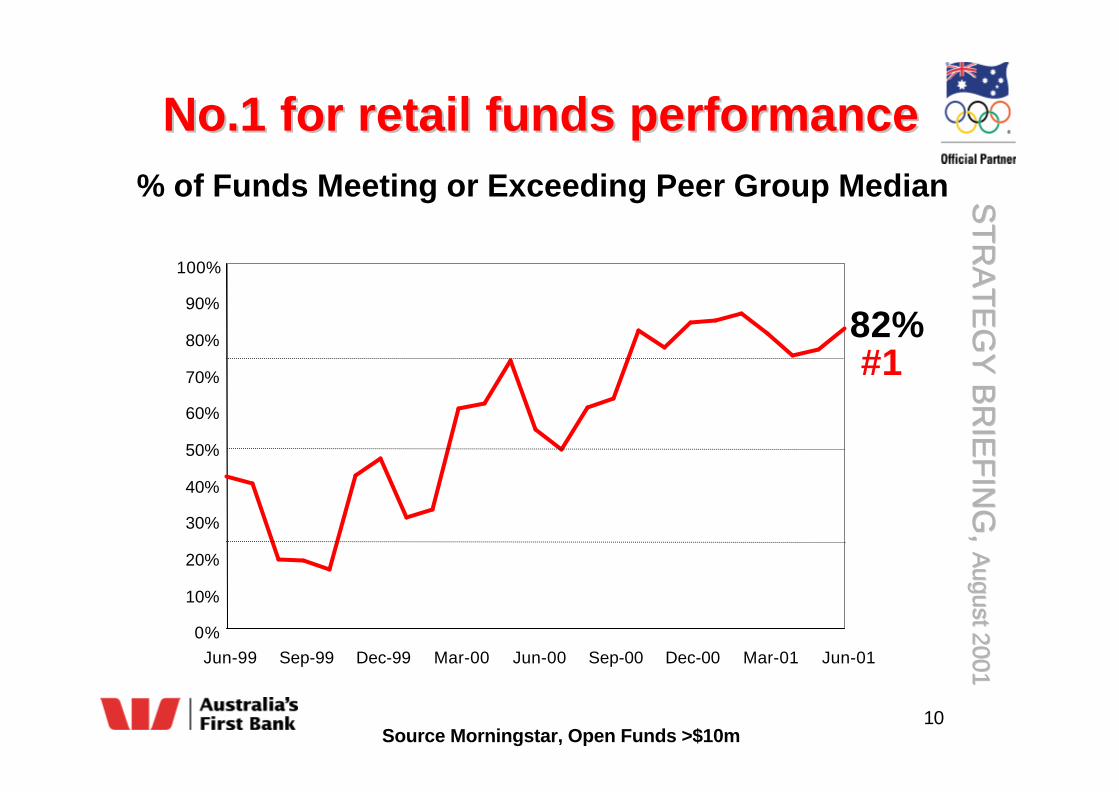

• Fund performance - No.1 over 1 year

ST

RA

TE

GY

BR

IEF

ING

, S

TR

AT

EG

Y B

RIE

FIN

G, A

ugust 2001A

ugust 2001

7

0

200

400

600

800

1000

1200

1995 1996 1997 1998 1999 2000 Mar-01 Jun-01 Sep-01 2002 2003

Adviser network growth continuesAdviser network growth continues

Planner/Adviser Numbers

Actual Target

CAGR = 18%

ST

RA

TE

GY

BR

IEF

ING

, S

TR

AT

EG

Y B

RIE

FIN

G, A

ugust 2001A

ugust 2001

8

200

300

400

500

600

700

800

900

0ct 9

9

Dec-99

Feb-0

0

Apr-00

Jun-0

0

Aug-00

Oct-00

Dec-00

Feb-0

1

Apr-01

Jun-0

1

Adviser productivity improvingAdviser productivity improving

Advised Sales per FTEA

dvi

sed

Sal

es p

er F

TE

/Mo

nth

($0

00s)

ST

RA

TE

GY

BR

IEF

ING

, S

TR

AT

EG

Y B

RIE

FIN

G, A

ugust 2001A

ugust 2001

9

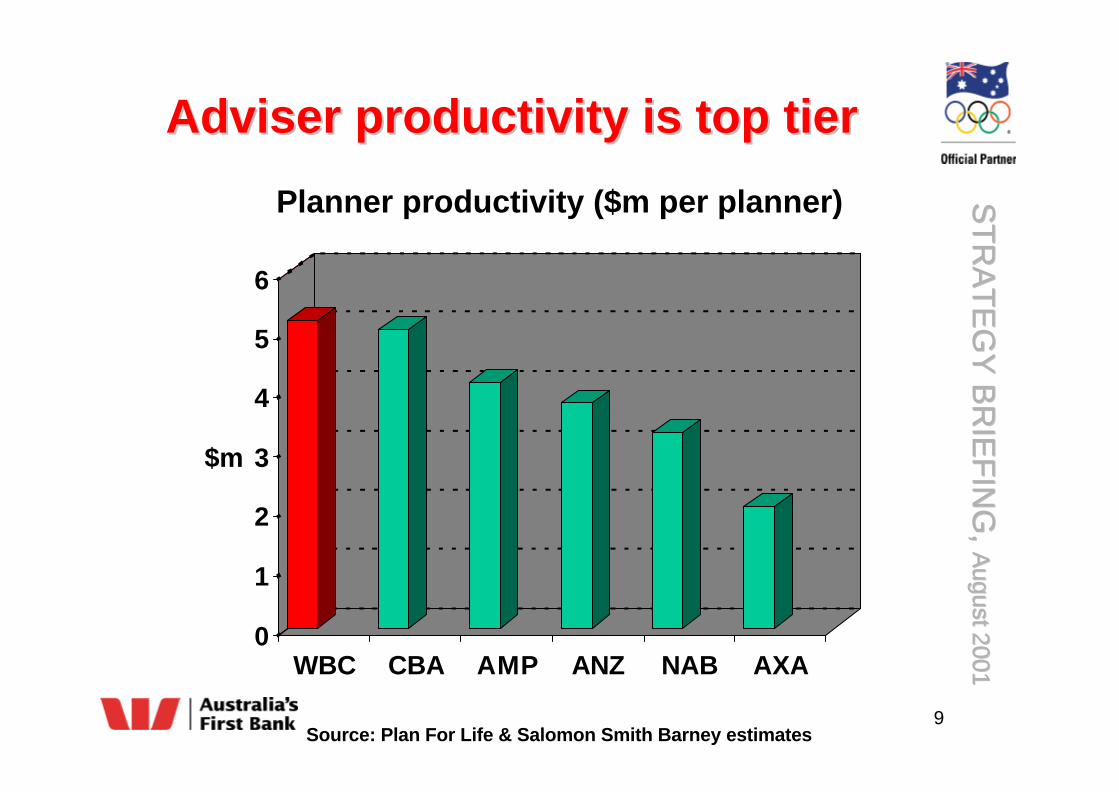

Adviser productivity is top tierAdviser productivity is top tier

Planner productivity ($m per planner)

0

1

2

3

4

5

6

WBC CBA AMP ANZ NAB AXA

$m

Source: Plan For Life & Salomon Smith Barney estimates

ST

RA

TE

GY

BR

IEF

ING

, S

TR

AT

EG

Y B

RIE

FIN

G, A

ugust 2001A

ugust 2001

10Source Morningstar, Open Funds >$10m

No.1 for retail funds performanceNo.1 for retail funds performance% of Funds Meeting or Exceeding Peer Group Median

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Jun-99 Sep-99 Dec-99 Mar-00 Jun-00 Sep-00 Dec-00 Mar-01 Jun-01

82%#1

ST

RA

TE

GY

BR

IEF

ING

, S

TR

AT

EG

Y B

RIE

FIN

G, A

ugust 2001A

ugust 2001

11

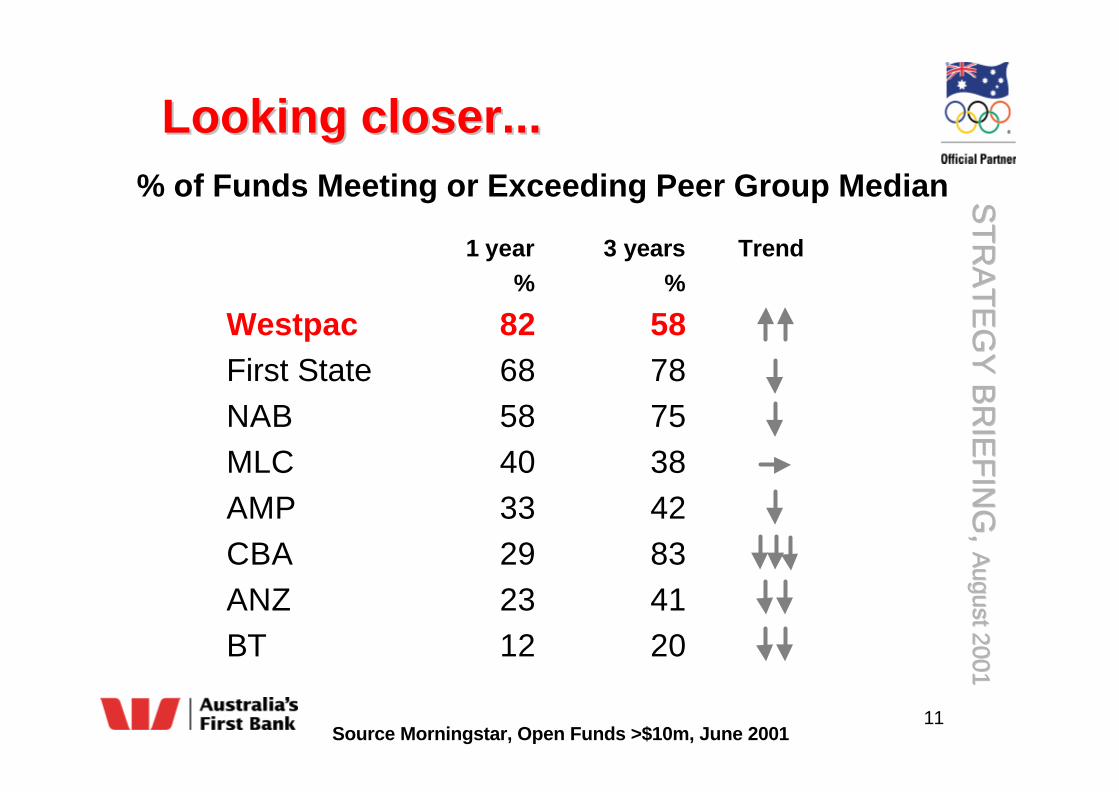

Looking closer...Looking closer...

1 year 3 years Trend% %

Westpac 82 58First State 68 78NAB 58 75MLC 40 38AMP 33 42CBA 29 83ANZ 23 41BT 12 20

Source Morningstar, Open Funds >$10m, June 2001

% of Funds Meeting or Exceeding Peer Group Median

ST

RA

TE

GY

BR

IEF

ING

, S

TR

AT

EG

Y B

RIE

FIN

G, A

ugust 2001A

ugust 2001

12

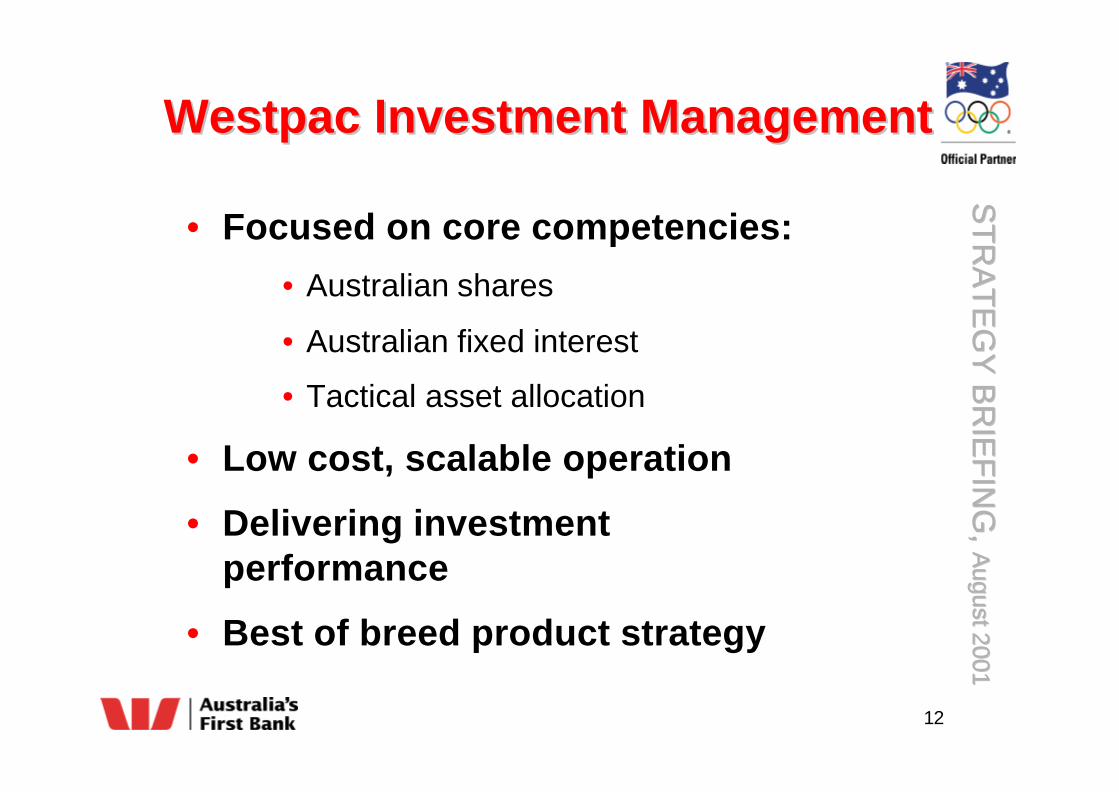

Westpac Investment ManagementWestpac Investment Management

• Focused on core competencies:

• Australian shares

• Australian fixed interest

• Tactical asset allocation

• Low cost, scalable operation

• Delivering investmentperformance

• Best of breed product strategy

ST

RA

TE

GY

BR

IEF

ING

, S

TR

AT

EG

Y B

RIE

FIN

G, A

ugust 2001A

ugust 2001

13

0

100

200

300

400

500

600

Quarterly Retail Inflow Trend

Retail inflows improving stronglyRetail inflows improving strongly

Mar`99 Jun`99 Sep`99 Dec`99 Mar`00 Jun`00 Sep`00 Dec`00 Mar`01 Jun`01

$m

ST

RA

TE

GY

BR

IEF

ING

, S

TR

AT

EG

Y B

RIE

FIN

G, A

ugust 2001A

ugust 2001

•• Current SituationCurrent Situation•• StrategyStrategy

ST

RA

TE

GY

BR

IEF

ING

, S

TR

AT

EG

Y B

RIE

FIN

G, A

ugust 2001A

ugust 2001

15

AcquisitionsAcquisitions

• Not interested in profitless growth

• Must add shareholder value

• Watching brief

• Our strategy is not dependent onacquisitions

ST

RA

TE

GY

BR

IEF

ING

, S

TR

AT

EG

Y B

RIE

FIN

G, A

ugust 2001A

ugust 2001

16

Our wealth management strategyOur wealth management strategy

• Leveraging our comparative advantage

– large customer base, warm leads andreduced search costs

• Expanding distribution size andcapability

• Accessing & integrating ‘best of breed’products

• Balancing growth and profitable returns

ST

RA

TE

GY

BR

IEF

ING

, S

TR

AT

EG

Y B

RIE

FIN

G, A

ugust 2001A

ugust 2001

17

The opportunity is large...The opportunity is large...

• 81% of Priority Customers don’t hold a

Westpac wealth management product

• 94% of Business Customers have their

super with another financial institution

– 39% of these have their super with

another Bank

ST

RA

TE

GY

BR

IEF

ING

, S

TR

AT

EG

Y B

RIE

FIN

G, A

ugust 2001A

ugust 2001

18

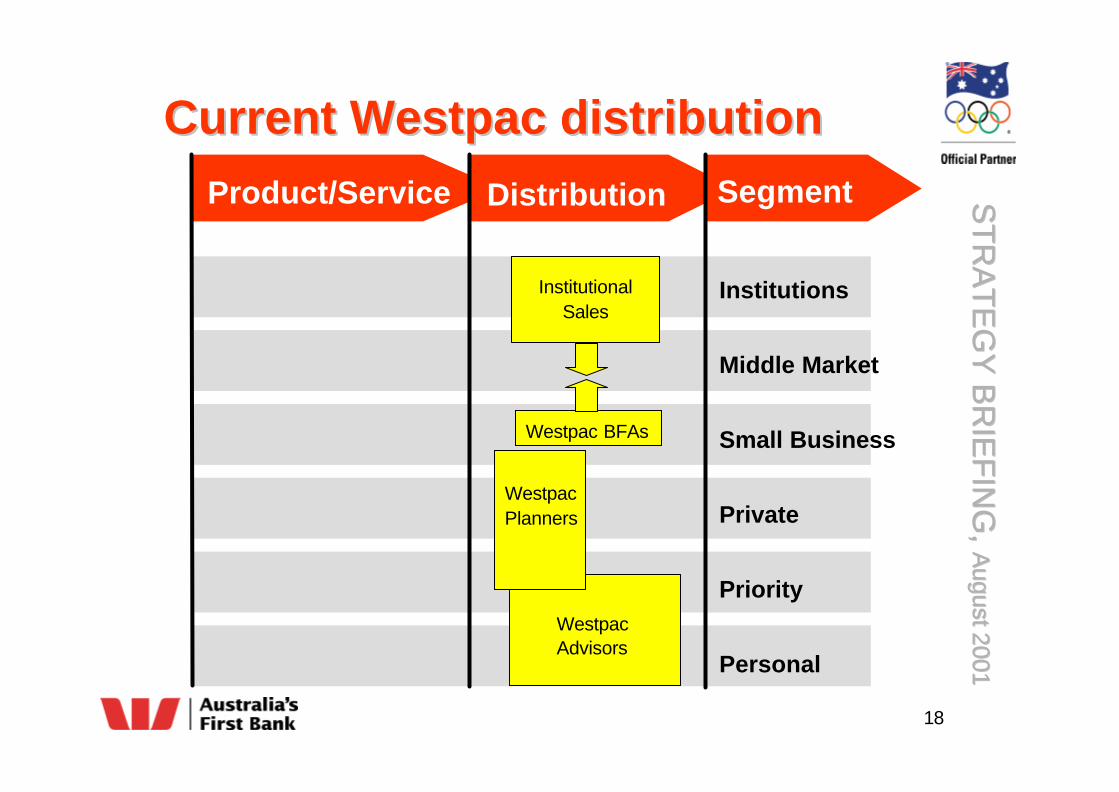

Current Westpac distributionCurrent Westpac distribution

Institutions

Middle Market

Small Business

Private

Priority

Personal

InstitutionalSales

Westpac BFAs

WestpacAdvisors

WestpacPlanners

Product/Service Distribution Segment

ST

RA

TE

GY

BR

IEF

ING

, S

TR

AT

EG

Y B

RIE

FIN

G, A

ugust 2001A

ugust 2001

19

Distribution opportunitiesDistribution opportunities

InstitutionalSales

Westpac BFAs

WestpacAdvisors

WestpacPlanners

Product/Service Distribution Segment

IFAs

HPJDV

Institutions

Middle Market

Small Business

Private

Priority

Personal

ST

RA

TE

GY

BR

IEF

ING

, S

TR

AT

EG

Y B

RIE

FIN

G, A

ugust 2001A

ugust 2001

20

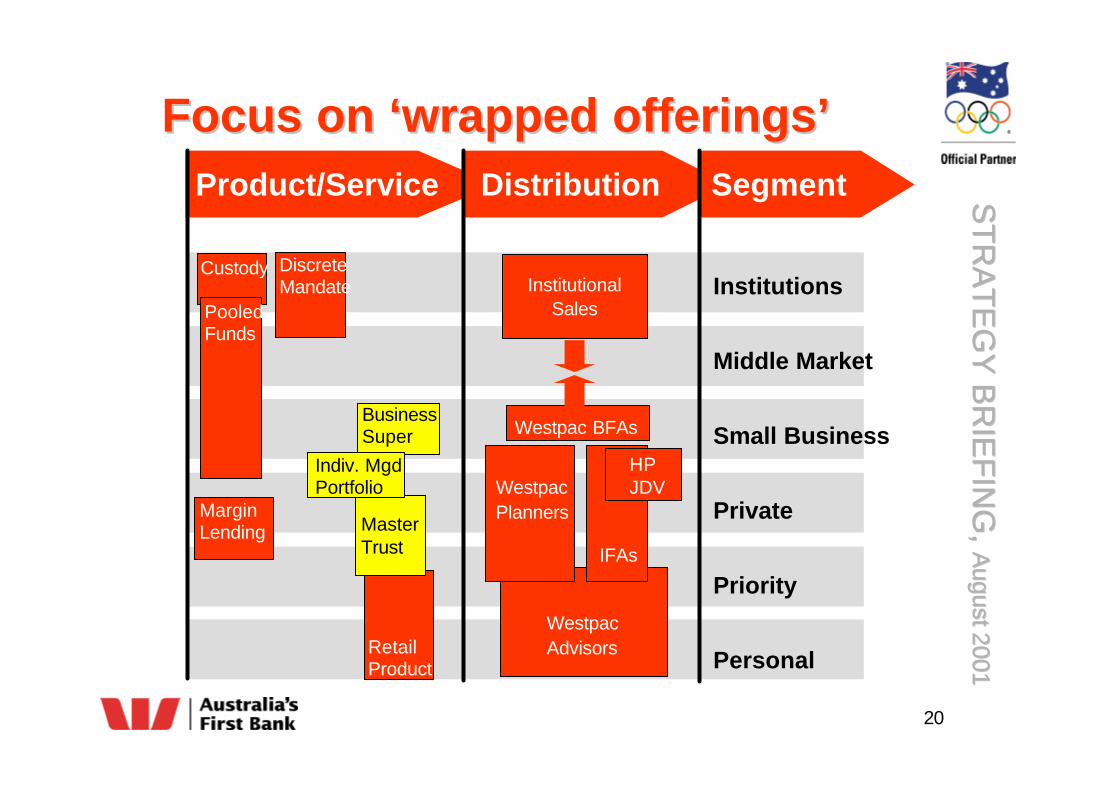

Focus on ‘wrapped offerings’Focus on ‘wrapped offerings’

Institutions

Middle Market

Small Business

Private

Priority

Personal

DiscreteMandate

BusinessSuper

RetailProduct

MasterTrust

MarginLending

Custody

PooledFunds

Product/Service Distribution Segment

Indiv. MgdPortfolio

InstitutionalSales

Westpac BFAs

WestpacAdvisors

WestpacPlanners

IFAs

HPJDV

ST

RA

TE

GY

BR

IEF

ING

, S

TR

AT

EG

Y B

RIE

FIN

G, A

ugust 2001A

ugust 2001

21

In summary...In summary...

• High growth and high return business

• Leveraging our comparative advantages

• Expanding distribution size and

capability

• Providing best of breed products

ST

RA

TE

GY

BR

IEF

ING

, S

TR

AT

EG

Y B

RIE

FIN

G, A

ugust 2001A

ugust 2001

22