financial performance characteristics of successful listed ... · financial performance...

TRANSCRIPT

FINANCIAL PERFORMANCE CHARACTERISTICS OF SUCCESSFUL LISTED REAL ESTATE COMPANIES

Executive Summary

In this paper, we hypothesize three main determinants of firm value for real estate companies to be growth, profitability and leverage and investigate a total of 11 different company specific characteristics as potential indicators of superior performance. We find that successful real estate companies are generally of larger size and command attractive market valuation relative to their underlying book value. They are usually profitable and are more likely to take advantage of positive financial leverage effects, contributing to higher sustainable growth and profitable growth in the longer term. In addition, the financial variables that influence successful performance are largely similar for all countries and regions, but differ in degree and in some cases the influence works in the opposite direction. This indicates a potential gain in portfolio diversification across the global real estate markets. 1. Background and Motivation

This paper examines two issues with respect to the key financial performance characteristics of

successful listed real estate companies in 24 countries and three continents over the period 2000 through

2006. First, we test the hypothesis that the three main determinants of firm value for real estate companies

are growth, profitability and leverage; and second, we investigate which financial variables are most

important in explaining and predicting the level of two measures of stock market success, i.e., the Sharpe

ratio and Jensen’s alpha. Our motivation is to search for common elements between companies with a view

to determine whether there are similar characteristics that successful listed real estate companies share.

As an extension of the prior real estate studies such as Ling and Naranjo (2002), Bond et al. (2003)

and Hamelink and Hoesli (2004) which examine cross-sectional differences in commercial real estate

market returns, this paper adopts a corporate finance -based approach. Specifically, the literature on value-

based planning, which regards shareholder value creation as the central premise, provides motivation and

intuition for our study. Under this theory, two main determinants of value; namely profitability and growth

are identified (Varaiya et al. 1987). The key idea here is that corporate management seeks to create

shareholder value by ensuring that the warranted market value, MV, of the equity capital invested in the

firm by the shareholders exceeds the book value, BV, of equity. Therefore, value is created for shareholders

if MV>BV or MV/BV>1; value is destroyed if MV<BV or MV/BV<1 and value is sustained if MV=BV or

MV/BV=1. In addition, financial leverage is included as the third value driver in our expanded model

because many real estate firms are capital intensive (Chiang et al. 2002). Only Ooi and Liow (2004)’s work

has some similarities to the present study. They examine the performance of real estate stocks of seven East

1

Asia developing countries over 1992-2002 using Sharpe Index (SI). Employing OLS panel regression

technique, they find that size, book-market value ratio, capital structure and market diversification have

significant influence on the firms’ SI performance.

We investigate the key financial (including operational, asset investment and financing) of the

listed real estate companies in a multiple number of countries from 2000-2006, benchmarked against

equivalent performance indicators for other major domestic, regional and world real estate companies. In

reference to the value-based planning, four main corporate performance equations (i.e. market-book ratio,

sustainable growth, profitability, capital structure as endogenous variables) will be modeled using system-

equation approach. Finally, we will link the stock market and financial performance of the companies and

investigate main key financial performance indicators of successful real estate companies.

In identifying the contribution of successful listed real estate companies to their shareholders and

the real estate industries in Asia, Europe and North America, our paper brings four contributions to the

extant literature. First, we extend the knowledge of the performance of global listed real estate companies

which are expected to become an increasingly important component of institutional investors’ asset

portfolios. Although not intended to be part of this paper, our additional review on their risk-return and

correlation dynamics confirms the observation made by Eichholtz and Koedijk (1996) that the global teal

estate securities market has developed significantly over the last decade, both in the market capitalization

and the number of listed companies, and is set to continue to grow. Second, a larger and more varied

sample of 336 listed real estate companies from 24 countries and 3 regional markets allow us to examine

whether any findings about one or two countries from other business fields can be generalized to real estate

companies that have their underlying asset value in the direct property sector. Our approach recognizes

there are probably significant regional, country and sector factors contributing to differences in the

financial performance of successful real estate companies since real estate is mainly a local business. Third,

an added contribution of this paper is that a system multivariate regression methodology is employed to

link the four key performance measures simultaneously. Compared to the Ordinary Least Square (OLS)

regression approach, the use of the iterated two-stage least square (IT2SLS) system estimation considers

the endogeneity and interactions of the financial variables and is able to produce more efficient coefficient

estimates regarding the three main determinants of firm value, i.e., growth, profitability and capital

2

structure. Finally, we measure real estate company performance from a portfolio manager’s viewpoint by

linking two conventional risk-adjusted return indicators, i.e. Sharpe index (SI) and Jensen’s alpha (JI) to the

financial performance indicators. The results from a binary logit model will provide evidence of strong

predictive power of those indicators of successful real estate companies. To the authors’ best knowledge,

this is probably the first empirical study which investigates the main determinants of the value creation in

global listed real estate companies. Results from this study can provide interesting and practical insights to

global investors and fund managers in including successful real estate companies to their investment

portfolios.

Our results suggest successful real estate companies are generally of larger size and command

attractive market valuation relative to their underlying book value. They are usually profitable and are more

likely to take advantage of positive financial leverage effects, contributing to higher sustainable growth

rates (SGRs) and profitable growth in the longer term. Moreover, the financial variables that influence

successful performance are largely similar for all countries and regions, but differ in degree and in some

cases the influence works in the opposite direction. This indicates a potential gain in portfolio

diversification across the global real estate markets. Our results provide practical insights to global

investors and fund managers in including successful real estate companies into their investment portfolios.

This paper is organized as follows. Section 2 presents the real estate company dataset and key

financial indicators. Section 3 explains the empirical procedures that include the system modeling and logit

regression. Then, we discuss the results and implications in Section 4. The article ends with a summary of

the key findings and highlights the limitations of they study in Section 5.

2. Data sources and sample characteristics

The dataset includes 336 public real estate investment and development firms for the period 2000

through 2006. Based on market capitalization (in US dollar term) as of December 31, 2006, all real estate

companies available from Osiris database1 were ranked in the descending order. This gives rise to a total of

1 Osiris is a comprehensive database of listed companies, banks and insurance companies around the world. In addition to the income statement, balance sheet, cash flow statement and ratios it contains a wide range of complementary information such as news, ownerships, subsidiaries, M & A activities and ratings. Osiris contains information on 38,000 companies from over 130 countries including 30,000 listed companies and 8,000 unlisted or de-listed companies.

3

336 real estate companies that were continuously listed from 2000-2006 and had an equity capitalization of

at least USD 1 million from 24 securitized real estate markets across Asia, Europe and North America.

Among them, The US property equity market is the largest real estate securities market in the world. Most

property companies are structured as tax exempt real estate investment trusts (REITs), but real estate

operating companies (ROECs) that do pay tax also exists. The British real estate securities market is by far

the largest in Europe, both in numbers and size. It is followed by France and Netherlands, which has the

second and third largest market capitalization in Europe. Lastly, Japan is the largest and one of the very two

developed (the other market is Australia) real estate securities markets in Asia. It has long history of real

estate companies. Other markets such as Hong Kong and Singapore have established track record of

property investment and development companies in their respective stock markets.

The financial data and ratios of the 336 companies were derived from Osiris. The stock market

index and return data comes from Datastream. We are aware that our sampling procedure will introduce

survivorship bias; however this might be unavoidable to be in line with the objective of assessing

successful real estate companies over the longest period (i.e. 2000-2006) that the data permit.

Each of the 336 real estate firms has a market capitalization of at least USD 1.5 million as of

Financial Year 2006. Exhibit 1 provides the 2006 key financial indicators of the companies grouped by

country. The largest real estate company (by market capitalization) is Japan’s Mitsubishi Estate which has a

MV of USD35736.26 million as of December 2006. The next 14 largest global listed real estate companies

are: Sun Hung Kai Properties (HK), Cheung Kong Holdings (Hong Kong), Mitsui Fudason (Japan), British

Land (UK), Metrovacesa (Spain), Sacyr Vallehermoso (Spain),Sumitomo Realty & Development (Japan),

Rodamco Europe (Netherlands), Gecina (France), CapitaLand (Singapore), Henderson Land Development

(Hong Kong), Sino Land (Hong Kong), Hang Lung Properties (Hong Kong) and Liberty International (UK)

(Exhibit 1 here)

We include eleven financial indicators to assess and identify financial successful real estate

companies. These financial indicators are popular measures of real estate firms’ success considered by

analysts as well as extensively documented in the literature. They are briefly discussed below. Exhibit 2

provides the mean, median and standard deviation of these variables over the entire sample period (2000-

2006).

4

(a) Market- to Book ratio (MV/BV)

The use of this ratio is in line with the findings of Fama and French (1992)’s book-to market ratio

(BV/MV), who show that the BV/MV of individual stocks can explain cross-sectional variation in stock

returns. This ratio (or its reciprocal) is widely used as a measure of a firm’s growth opportunities through

value-based planning models which argue that at maximum, a firm’s management chooses strategies that

produce the largest MV, given BV.

(b) SIZE (MV)

Company size is another popular variable that explain stock return. Large firms are typically more

diversified and less risky. The seminal work of Fama and French (1992) shows that stock returns are

related to size and positively related to book-to-market ratio. Research by Laporta et al. (1997) reveals that

the relation between size and stock returns is similar for financial and non-financial firms. The variable is

measured here as the natural log of market capitalization and is used as a controlled variable in the

simultaneous equations.

(c) Sustainable growth rate (SGR)

Corporate finance theories suggest that companies need to trade off with the inherent constraints

with respect to policies regarding leverage and dividend payout in planning for its future growth. For

example, a real estate company may decide to retain a greater portion of its earnings in its reserve and

finance new projects or acquisitions out of the retained earnings. By doing so, the firm may not need to

increase its gearing and at the same time avoid give a signal to the market about its investment plan. The

sustainable growth rate (SGR) is the highest growth rate a firm can maintain without increasing its financial

leverage. This indicator was proposed by Higgins (1977) to relate a firm’s growth with its financial stability.

This rate depends on the firm’s return on equity (ROE) and earnings retention ratio (ERR); i.e.

SGR=ROE*ERR. The higher the sustainable growth, the more financial flexibility the firm has to expand

through organic growth or acquisitions. Liow (1998) finds the actual growth rate (AGR) of many Singapore

real estate companies were higher than their SGR. Consequently, these real estate firms relied on increasing

financial leverage to sustain their high growth.

(d) Return on equity (ROE)

5

This is a summary indicator that links a firm’s “net earnings’ from its Profit & Loss account and

“shareholders’ fund” from its balance sheet. It thus measures the profitability of investment from the

perspective of shareholders. It is a key driver of SGR and is measured as the product of ROA and debt ratio

(i.e. ROE = ROA* DEBTR)

(e) Debt ratio (DEBTR)

Capital structure measured as the ratio of long-term debt to total assets (DEBTR) is a proxy for

leverage. While the expected common stock returns are positively related to the ratio of debt to equity after

controlling for beta and firm size due to positive leverage effect, Fama and French (1992) find a negative

relation between debt and firm value. At higher levels of debt, the shareholders-bondholders’ agency

problems arise when debt is risky predict a negative relationship between leverage and profitability. This

ratio is highly relevant for many real estate firms which are very capital intensive

(f) Cost of equity (K e)

The cost of equity (K e) is the minimum return that shareholders of the firm demand consistent

with the riskiness of their investment in the firm. Value is created (destroyed) when a firm adopts strategies

that produce a return which exceeds (falls short of) its cost of equity. It is measured by the earnings yield

(reciprocal of price-earning ratio) of the firm in Year t.

(g) Spread

The magnitude of the percentage spread, (ROE – Ke), expected to be earned, implies that a

positive ROE alone is not a sufficient indicator of a profitable business. Instead, positive spread (i.e. ROE –

K e >0) implies profitable growth and hence the higher a firm’s value (MV/BV); where negative spread

implies unprofitable growth.

(h) Fixed tangibility (FA/CA)

Tangible fixed assets reduce the likely costs of financial distress, so firms with significant tangible

assets (such as real estate companies) would be expected to employ more debt. It is defined in this study as

ratio of fixed assets to current assets. Further, those firms with higher fixed tangibility such as real estate

firms could have lower profit level due to higher operating leverage.

(i) Earnings retention ratio (ERR)

6

This ratio is measured as (1- dividend payout ratio). Finance theory postulates that when a firm

pays out less of its earnings as dividend (i.e. lower payout ratio), it will accumulate more of its retained

earnings (higher ERR) to build up its reserve. Consequently, this firm is able to accrue higher SGR (as

SGR =ROE*ERR) and requires lesser debt financing (DEBTR) to supports its expansion or asset

acquisitions.

(j) Actual growth rate (AGR)

This represent the annual growth level experienced by a firm in Year t, and is measured as the %

change in total assets from year to year.

(k) Profitability (ROA)

Return on assets (ROA) is an asset utilization ratio that indicates how effectively or efficiently a

firm uses its assets. Usually the higher the ROA, the higher the growth potential of the firm

(Exhibit 2 here) 3. Methodology

With the selected financial variables, our empirical procedures comprise three steps.

First, we test the hypothesis that the three main determinants of firm value (measured by the

MV/BV ratio) for real estate companies are growth, profitability and leverage. We run four separate

simultaneous equations on the pooled data from 2000 to 2006 for the 24 countries, 3 continents and 6 years

using Iterated Weighted Two-stage Least Square (ITW2SLS) estimation method. This system approach is

necessary because financial variables are related in ways that makes it difficult, if not impossible, to

determine causality, and that they are often simultaneously determined by each other. The correlation

results reported in Exhibit 3 indicate that many of the financial variables are reasonably correlated. A

specific example is that in corporate finance, it is known that capital structure is endogenous to

performance; sustainable growth is endogenous to performance, capital structure and dividend policy.

Compared to the OLS regression approach, the use of the ITW2SLS system estimation method considers

the endogeneity of the financial variables and is able to generate more efficient coefficient estimates.

Before estimation, we have manually checked the financial data for outliers. They include zero

values for variables such as MV and earnings yield; negative values for MV/BV, DEBTR, ERR and

FA/CA ratios as well as extraordinarily large observations for any of the variables (defined as more than

7

three standard deviations away from the mean). Consequently, a number of firms for which these

observations occurred have been removed from the samples, so the final test sample contains 1131 firm-

observations (48.1% - with complete data for all financial indicators) during the period 2000-2006. The

four simultaneous equations of the system model are specified as:

(1) MV/BV = f (MV, SGR, ROE – K e, FA/CA)

(2) SGR = f (MV, MV/BV, FA/CA, ROA, DEBTR, ERR)

(3) ROA = f (MV, FA/CA, DEBTR, SGR)

(4) DEBTR = f (MV, FA/CA, ROA, AGR, ERR)

(Exhibit 3 here)

Equation (1) tests the three main determinants of firm value, MV/BV, to be (a) the spread (ROE –

K e), (b) sustainable growth rate (SGR) and (c) fixed tangibility (FA/CA). There are two main predictions:

(a) the higher the spread, ceteris paribus, the higher a firm’s MV/BV; (b) the higher the SGR, ceteris

paribus, the higher a firm’s value, MV/BV, if the spread is positive. Conversely, the higher the SGR, the

lower will be a firm’s value if the spread is negative. The MV variable is used as a controlled variable in

the four equations. Equation (2) is an expanded SGR model that includes the main determinants of Higgins

(1977)’s original SGR model (i.e. ROA, DEBTR and ERR) and extra variables (MV/BV, FA/CA and MV).

The profitability (Equation 3) and capital structure (Equation 4) variables are interrelated; with Chiang et al.

(2002) find that capital structure is positively related to asset but negatively with profitability for Hong

Kong property and construction firms. The trade-off model postulate profitable firms can use more debt to

derive more tax shelter benefits. In contrast, the pecking order theory suggests that more profitable firms

have less need for external debt financing.

Second, we use two conventional measures of investment performance, i.e. the Sharpe index (SI)

and Jensen’s alpha (JI) to measure firms’ success from the capital market perspective. The SI is closely

associated with the CAPM and measures excess return per unit of risk. A positive JI indicates the

occurrence of positive abnormal returns. Similarly, negative JIs indicate returns below the level anticipated

by the CAPM according to the risk-free rate, systematic risk and market risk premium. With the possible

indicators for identifying financially successful real estate companies (as explained above), an OLS

8

regression model investigates which financial variables are most important in explaining the level of the

two measures of stock market success, i.e. SI and JI. The two estimating equations are:

(a) SI = f {intercept, LNMV, LN(MV/BV), SGR, ROA, D/E, SPREAD, DREG1, DREG2,

DREG4}

(b) JI = f {intercept, LNMV, LN(MV/BV), SGR, ROA, D/E, SPREAD, DREG1, DREG2,

DREG4}

Where: DREG i = dummy variable if firm i is in Group X, X = 1 (Asia-Pacific developed /matured

markets: Australia, New Zealand, Japan, Singapore, Hong Kong), 2 (Asia-Pacific developing markets:

Malaysia, Thailand, Philippines, Indonesia and China), 3 (European markets: UK, France, Germany, etc) or

=0, otherwise; Intercept is the SI (or JI) mean values for Group 4 (North Americas markets: Canada and

USA)

Finally, we estimate two binary logit models to predict whether each measure of financial

performance will beat the average value of JI (SI) for the firms in the sample. In the JI model, the

dependent variable is a dummy variable representing one if JI is positive and zero otherwise. In the SI

model, the dependent variable is a dummy variable representing one if the value of SI is greater than the

average for the final 170 firms (average SI is 2.1522) and zero otherwise. The logit model predicts correctly

when the predicted probability for a firm, derived from the log of the odds, is greater than 0.5 and the

dependent variable for the firm is one. Similarly the model predicts correctly when the predicted

probability is less than or equal to 0.5 and the dependent variable for the firm is zero.

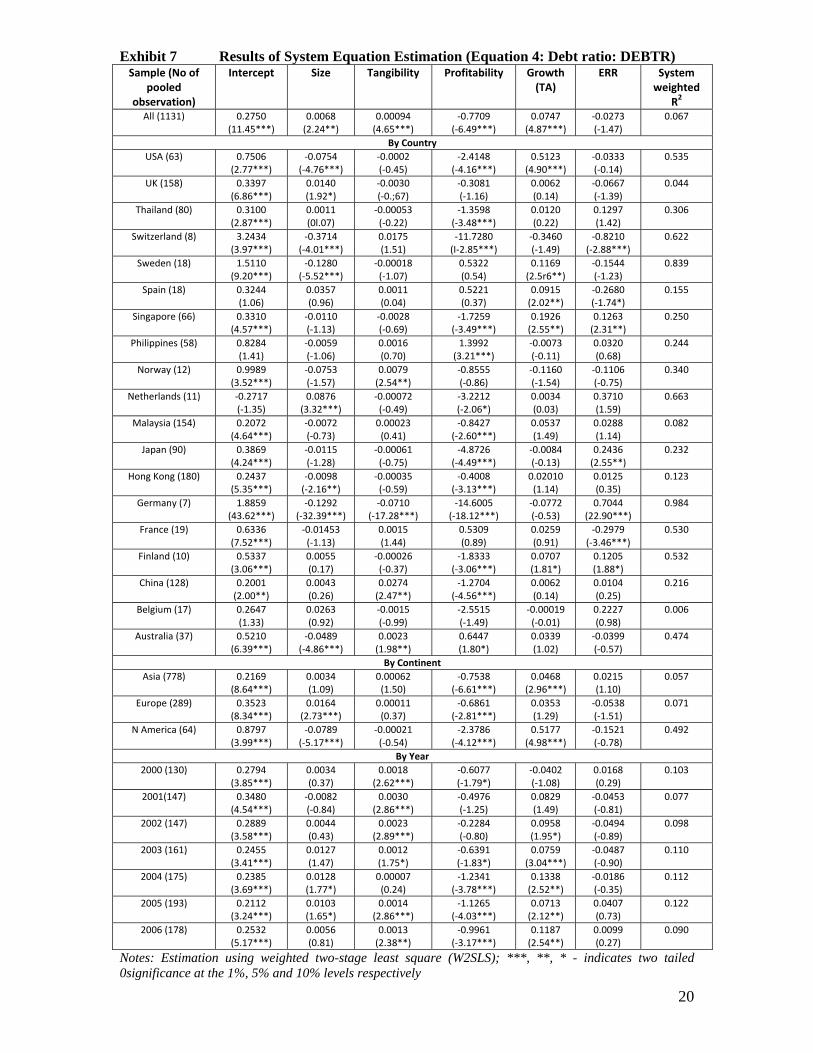

4. Results

The simultaneous regression estimation results are reported in Exhibits 4 -7. For each equation,

the regressions are run for the overall pooled sample, 19 country- pooled models, 3 regional- pooled

models and 6 yearly - pooled models. This approach hopes to test the robustness of the results.

(Exhibits 4 to 7 here)

After controlling for the endogeneity and simultaneity of firm value, sustainable growth rate,

profitability and capital structure, we find significant and important co-movements in the variables as well

as the directions of influence in most cases are consistent with the various hypotheses. Another observation

9

is that the financial variables that influence the performance are largely similar for all countries, regions

and different periods; but differ in degree and in some cases the influence works in the opposite direction.

This indicates a potential gain in portfolio diversification across the global real estate securities markets.

Firm value (represented by the MV/BV ratio) is positively influenced by the market capitalization

(SIZE) significantly except Sweden, Norway and France where the coefficients are insignificantly negative.

That is to say, larger real estate firms are able to capture higher stock market valuation, evidence which

appears inconsistent with that of Fama and French (1992). Contrary to the overall sample that documents a

positive relationship between the sustainable growth rate (SGR) and firm valuation, the influence is

significantly negative for Germany and France; insignificantly negative for the USA, Thailand and Sweden;

and insignificantly positive for Philippines, Norway and China. Similarly, spread is found to have a

significantly positive effect on firm value for the overall sample. However, the coefficient is insignificantly

negative in Thailand, Switzerland, Norway, Germany, China and Australia implying that in these real estate

securities market, unprofitable growth (i.e. negative spread) has a negative effect on firm value. In contrast,

the influence of the spread variable is significantly positive in the USA, UK, Spain, Singapore, Netherlands,

Malaysia, Japan, Hong Kong, France, Finland and Belgium implying that (highly) profitable growth of real

estate firms in these markets contribute significantly to higher stock market valuation. Finally, tangibility

has a moderately negative impact on firm valuation since higher operating leverage (due to higher fixed

asset such as property ownership) reduces firm value. This negative coefficient holds except for the USA,

Sweden, Malaysia and China.

Of the six financial variables that are hypothesized to affect the SGR, the most influencing

variables are firm valuation (significantly positive), profitability (significantly positive) and earnings

retention ratio (significantly positive). These positive effects are not surprising based on the SGR literature.

The majority of the individual ERR coefficients are significantly positive, suggesting that the higher the

ERR (the lower the dividend payout ratio), the higher the SGR. This is consistent with the observation that

many high-growth real estate companies usually pay low or no dividends to their shareholders and instead

use these retained earnings to invest in positive NPV projects which in turn contribute to higher SGR of the

companies. The profitability coefficients for 10 countries are significantly positive confirming that higher

SGR can be achieved from higher profitability; in other cases the coefficients are mostly positive but

10

insignificant. Finally, in 6 of the 22 firms’ MV/BV coefficient, we confirm the significant and positive

relationship between MV/BV and SGR. However, this result is not conclusive as the remaining 16

countries (regions) coefficients are either insignificantly positive or insignificantly negative, indicating that

the difference in the dynamic relationship between firm value and sustainable growth needs to be exploited

For Asian and European real estate firms, the influence of SIZE and SGR on profitability is both

significantly positive indicating larger and higher growth real estate firms are associated with higher return

on assets (ROA); these two coefficients are also positive and yet statistically insignificant for the North-

American real estate firms. Tangibility also has a positive and significant effect on the profitability

performance for Asian and North-American firms; the positive effect is nevertheless weaker for European

firms. Finally, for real estate firms in all three regions, profitability is consistently and negatively

influenced by the capital structure (represented by DEBTR). That is to say, higher debt level contributes

negatively to return on assets. This result is not surprising as borrowing interests are the first charge and

reduces the profit of the business. Contrary to other countries, higher debt level contributes to higher

profitability in France and Australia.

Lastly, the results reported in Exhibit 7 clearly indicate that the negative and significant

relationship between profitability and capital structure exists for real estate firms from the three regions.

Two notable exceptions are the Philippines and Australia where their DEBTR coefficients are significantly

positive. Firm size has a positive effect on borrowing by European and Asian real estate firms. Whilst the

positive coefficient is significant for the European firms, it is statistically indistinguishable from zero for

the Asian firms. Hence, in general, larger real estate firms are able to borrow more (in percentage term of

total assets) compared to smaller firms. In general, both the tangibility and actual growth rate variables

have a positive effect each on capital structure. Specifically, Asian and North-American real estate firms

have an average positive and significant AGR indicating that higher growth (in total assets) requires higher

borrowing. In contrast, the average positive effect of the tangibility variable is not clear in the regional and

country analyses since many of the coefficients are either insignificantly positive or insignificantly

negative ; only Norway, China and Australia have a significantly positive debt ratio coefficient indicating

that tangible assets (/properties) contribute to borrowing level because of the collateral role it plays. Finally,

11

although there is a negative relationship shown between the ERR and DEBTR, this negative relationship is

statistically indistinguishable from zero in many instances.

In summary, our system modeling and analyses have reasonably established the main financial

characteristics of successful real estate companies. In particular, successful (measured by higher firm value,

MV/BV) real estate companies are usually larger and are associated with higher sustainable growth and

positive spread as well as higher fixed tangibility (in percentage term). In addition, these companies are

usually profitable and nevertheless maintain a higher plough back (earnings retention) ratio as well as able

to borrow more (in percentage term of total assets) to support their continued growth. Our empirical work

also reveals the financial variables that influence successful real estate company performance are largely

similar for all countries, regions and in different periods, but differ in degree and in some cases the

influence works in the opposite direction. This indicates a potential gain in portfolio diversification across

the global real estate markets. However, some country results must be interpreted with cautions. This is

because no meaningful results can be obtained from countries like Switzerland, Finland, Norway and

Germany etc with only up to three companies. They are probably not going to provide adequate parameter

stability due to the too few firms within the samples.

For the capital market analysis, .the source data are the 336 firms for the last three years (2004 -

2006). In addition, those firms with one or more missing values for the variables gathered were excluded.

This leaves us with a total of 170 firms (50.6%) with complete data for the 3-year period. The regression

results are reported in Exhibit 8. The intercepts represent a test of the hypothesis that the mean SI (JI) for

Group 4 countries is zero. The other DREG coefficients represent tests for significant differences in the

means for SI and JI against the means for Group 4. Focusing on the financial variables, the results indicate

that five indicators (MV, MV/BV, SGR, ROA and DEBTR) are significant (up to 5 percent level) in

explaining successful JI performance. The SI results indicate that two indicators are statistically significant

in contributing to successful real estate company performance: market capitalization of equity (MV) and

profitability (ROA). Overall the results provide strong evidence that large size and highly profitable real

estate companies have on average superior investment performance. Other factors such as capital structure

(DEBTR ratio), sustainable growth rate (SGR) and profitability (ROA) also contribute to the real estate

firm’s stock market success.

12

(Exhibit 8 here)

Finally, the results for the two logit models reported in Exhibit 9 provide reasonably strong

evidence of the predictive power of the defined indicators of successful real estate companies. They predict

correctly in about 84 percent of the cases with respect to JI and about 77 percent for SI. The binary logit

models indicate that successful real estate companies (i.e. with positive JI and above-average SI

performances) are generally of larger size and command attractive market valuation relative to their

underlying book value. They are profitable and are more likely to take advantage of positive financial

leverage effects, contributing to higher SGR and profitable growth in the longer term.

(Exhibit 9 here)

One last comment is in order regarding the impacts of current financial/liquidity crisis on

corporate financial performance. As the global financial landscape has changed considerably since 2006,

one question that may be of interest to readers is how well these successful real estate companies are doing

now. Some guesses are that a number of these firms are probably in great financial difficulties coupled

with their unfavorable market valuations (in term of MV/BV). Some are probably even on the verge of

collapse – particularly in regard to the negative financial leverage effect. Under these difficult market

conditions, one view is that these companies have to re-think and re-manage their sustainable growth rates

(SGRs) in relation to the firms’ growth and financial stability; i.e. while struggling to improve their return

on asset (ROAs) through more efficient asset utilization, they should probably pursue a zero-growth (or

even negative-growth) strategies so as to cut down /minimize their debts. By doing so, they hope to

maintain/improve the bottom lines as well as reduce their financial and bankruptcy risks due to high

financial gearing. With more data available, this research can be extended to evaluate and compare the

financial characteristics of the successful real estate companies before and after the present financial crisis

and derive important lessons that can be learnt in regard to the corporate financial management under crisis

situations.

5. Conclusion

To conclude, we find that successful real estate companies (i.e. with positive JI and above-average

SI performances) are generally of larger size and command attractive market valuation relative to their

13

underlying book value. They are usually profitable and are likely to take advantage of positive financial

leverage effects, contributing to higher SGR and profitable growth in the longer term. Moreover, the

financial variables that influence successful performance are largely similar for all countries and regions,

but differ in degree and in some cases the influence works in the opposite direction. This indicates a

potential gain in portfolio diversification across the global real estate securities markets. This information is

very useful for international investors and portfolio managers to understand better the dynamics of growth

and value creation in real estate companies. With the increasing significance of securitized real estate as

property investment vehicles for international investors to gain real estate exposure globally (Worzala and

Sirmans, 2003), this study on global real estate company performance is timely and has significant

implications for ongoing international real estate investment strategies and academic research in the

financial performance dynamics of listed real estate companies. It would probably generate a lot of interest

among both academics and practitioners, alike – in terms of determining common characteristics of listed

property around the world.

Some limitations of this study are also noted. First, in order to include as many as real estate firms

possible and at the same time ensure that the time period is long enough for any meaningful conclusion (s)

to be drawn, we adopt a compromised time span of seven-year (2000-2006) bearing in mind that a longer

time-series of financial data would help improve the power of analysis. Second, only real estate firms that

are continuously listed during the entire period are included. Like most other studies, our sampling

procedure is thus subject to survivorship bias (which is largely unavoidable) and care must be taken to

interpret the results generated from the study. Third, there is large number of missing as well as negative

ratios especially for some variables like DEBTR, ERR and earnings yield, resulting in only 48.1 percent of

the usable sample. Finally, we might not have included all important financial and stock market

performance indicators in the study.

14

REFERENCES Bond, S., Karolyi, A. and A. Sanders, International real estate returns: a multifactor, multicountry approach. Real Estate Economics, 2003, 31(3), 481-500 Chiang, Y.H., Chan, P.C.E. and Hui, C.M.E., Capital structure and profitability of the property and construction sectors in Hong Kong, Journal of Property Investment and Finance 2002, 20(6), 434-453 Eichholtz, P.M.A. and K.G. Koedijk, The global real estate securities market, Real Estate Finance, 1996, 13(1), 76-82 Fama, E.F. and French, K., The cross-section of expected stock returns, Journal of Finance, 1992, 47, 427-466 Hamelink, F. and Hoesli, M., What factors determine international security returns? Real Estate Economics, 2004, 32(3), 437-462 Higgins, R.C., How much growth can a firm afford? Financial Management, 1977, Fall, 7-15 Laporta, R., Lakonishok, J., Shleifer, A. and Vishny, R., Good news for value stocks, further evidence on market efficiency, Journal of Finance , 1997, 52(2), 859-883 Ling, D, and Naranjo, A., Commercial real estate return performance: a cross-country analysis, Journal of Real Estate Finance and Economics, 2002. 24(1/2), 119-142 Liow, K.H., An empirical investigation of corporate growth of property companies, Journal of Financial Management of Property and Construction, 1998, 3(3), 5-16 Liow, K.H., The Dynamics of Return Volatility and Systematic Risk in International Real Estate Security Markets, Journal of Property Research, 2007, 24(1), 1-29 Ooi, JTL and Liow, K.H., Risk-adjusted performance of real estate stocks: evidence from developing countries, Journal of Real Estate Research, 2004, 26(4): 371-395 Varaija, N., Kerin, R.A. and Weeks, D., The relationship between growth, profitability and firm value”, Strategic Management Journal 8(5): 487-497 Worzala, E. and C.F. Sirmans, Investing in international real estate stocks: a review of the literature, Urban Studies, 2003, 40, 1115-1149

15

Exhibit 1 Key Financial Indicators of Global Real Estate Companies (as of FY2006)

Continent Country Number of firms Total assets ('million)

Book equity ('million)

Market capi-talization ('million)

Net profit after tax ('million)

Current Liabilities ('million) Fixed Assets ('million)

Asia AUSTRALIA 10 2846.41 1575.77 2324.53 270.75 583.37 2399.78CHINA 35 559.28 212.80 360.53 17.36 235.02 178.60

HONGKONG 57 2774.73 1769.77 2103.56 196.37 251.93 1832.18INDONESIA 4 268.69 130.56 216.72 19.72 97.96 92.16

JAPAN 23 5143.52 1407.17 4875.28 136.98 1259.62 3486.29MALAYSIA 53 274.86 157.71 119.43 10.10 102.17 270.28

NZ 1 53.80 52.72 60.26 7.67 0.74 29.20PHILIPPINES 31 320.91 171.74 343.40 13.19 77.61 210.98SINGAPORE 18 2281.49 1052.40 1916.46 103.62 442.49 1487.15THAILAND 17 351.31 144.42 219.04 56.19 110.79 216.91

AVERAGE 249 1487.50 667.51 1253.92 83.20 316.17 1020.35Europe AUSTRIA 1 3572.76 1591.01 1693.92 78.71 150.25 2888.07

BELGIUM 4 1974.11 1135.68 1332.76 158.90 188.18 1850.32FINLAND 2 2914.39 761.42 1182.64 114.12 360.57 1189.40FRANCE 4 8494.19 3966.68 5632.93 858.32 643.08 5113.82

GERMANY 3 2509.00 755.91 1795.01 82.98 519.39 1983.91ITALY 1 6132.03 2397.31 2677.52 271.95 191.15 5157.32

NETHERLANDS 3 7384.23 4391.38 5931.34 970.10 490.61 7271.72NORWAY 2 3134.06 956.20 1480.41 198.20 235.30 2990.73

SPAIN 3 21704.18 3399.55 12869.99 1114.18 4639.88 16129.81SWEDEN 3 3604.26 1460.47 2017.94 288.80 578.28 3535.06

SWITZERLAND 2 1797.28 655.71 762.60 44.71 553.83 1676.39UK 39 2555.98 1363.18 1493.64 342.36 159.47 2336.04

AVERAGE 67 5481.37 1902.87 3239.22 376.94 725.83 4343.55North America CANADA 1 2626.69 782.28 846.34 39.44 91.11 2582.53

US 19 1371.11 346.79 784.30 73.42 81.77 596.29AVERAGE 20 1998.90 564.53 815.32 56.43 86.44 1589.41

Source: derived from Osiris and Datastream

16

Exhibit 2 Descriptive statistics of key financial ratios for Global Real Estate Companies: 2000-2006

Financial variables No of valid observations

Mean Median Std deviation

Market capitalization (‘m) 2246 795.99 128.72 2645.48

Sustainable growth rate 2063 0.0202 0.0292 0.3003

Return on equity 2213 0.0505 0.0540 0.1692

Debt ratio 1890 0.2999 0.2754 0.1857

Spread (ROE‐ cost of capital) 1698 ‐0.0057 ‐0.0031 0.1422

Cost of capital (earnings yield) 1718 0.0829 0.0610 0.0808

Earnings retention ratio 1979 0.7961 0.8990 0.2767

Tangibility (Fixed assets / current assets)

2278 9.0942 2.2183 21.3987

Growth (change in total assets) 2271 0.2756 0.0492 5.2517

Market‐to‐book value ratio 2195 1.3092 0.8675 1.8303

Return on capital 2304 0.0220 0.0245 0.6256

Source: derived from Osiris and Datastream Exhibit 3 Correlation analysis of financial ratios: 2000-2006 Correlation MV SGR ROE DEBTR SPREAD EP ERR FACA GTA MB

MV 1

SGR 0.082 1

ROE 0.274**

0.358*** 1

DEBTR ‐0.248** 0.0391 ‐0.158 1

SPREAD

0.365*** 0.203 0.655*** ‐0.471*** 1

EP ‐0.175 0.124 0.234* 0.435*** ‐0.581*** 1

ERR ‐0.704*** ‐0.007 ‐0.178 0.221* ‐0.342*** 0.249** 1

FACA ‐0.071 0.087 0.126 ‐0.223* 0.127 ‐0.028 ‐0.138 1

GTA 0.166 ‐0.070 0.364*** 0.201 0.173 0.170 ‐0.130 0.046 1

MB 0.839*** 0.047 0.310** ‐0.305** 0.499*** ‐0.309** ‐0.675*** 0.065 ‐0.018 1

ROA ‐0.027 0.168 0.703*** ‐0.478*** 0.574*** 0.019 0.007 0.375*** 0.131 0.126

Notes: ***, **, * - indicates two tailed significance at the 1, 5 and 10% levels respectively

17

Exhibit 4 Results of system equation estimation (Equation 1: Market-book ratio, MV/BV) Sample (No of pooled

observation) Intercept Size Sustainable

Growth Spread Tangibility System

weighted R2

ALL (1131) ‐0.9661 (‐13.22***)

0.1599 (12.50***)

0.7965 (4.30***)

1.7879 (9.40***)

‐0.0016 (‐1.95*)

0.272

By country

USA (63) ‐0.4844 (‐1.95*)

0.1901 (3.60***)

‐0.5980 (‐1.17)

2.8744 (3.79***)

0.0004 (0.32)

0.472

UK (158) ‐0.3452 (‐3.34***)

0.0288 (1.63*)

1.1383 (2.87***)

1.1871 (3.92***)

‐0.0021 (‐2.03**)

0.288

Thailand (60) ‐2.4694 (‐7.71***)

0.5983 (8.24***)

‐0.9357 (‐1.57)

‐0.1156 (‐0.27)

‐0.0276 (‐2.87***)

0.576

Switzerland (8) ‐1.3077 (‐5.44***)

0.2376 (7.95***)

0.8572 (2.17*)

‐0.3937 (‐0.63)

‐0.0120 (‐2.66**)

0.972

Sweden (18) 0.4861 (0.71)

‐0.0597 (‐0.54)

‐0.2922 (‐0.30)

1.2338 (1.24)

0.0023 (1.64)

0.260

Spain (18) ‐2.2761 (‐6.03***)

0.3600 (6.58***)

0.6956 (2.09**)

1.9409 (5.15***)

‐0.1299 (‐4.13***)

0.901

Singapore (66) ‐0.5651 (‐2.49**)

0.0821 (2.34**)

1.0471 (2.25**)

5.0240 (5.79***)

‐0.0388 (‐2.83***)

0.473

Philippines (58) ‐2.1257 (‐6.90***)

0.3166 (5.04***)

2.0821 (1.05)

1.8961 (1.21)

‐0.0021 (‐0.08)

0.472

Norway (12) 1.9706 (2.98***)

‐0.2518 (‐1.04)

1.1273 (1.11)

‐0.0486 (‐0.07)

‐0.0092 (‐1.15)

0.374

Netherlands (11) ‐0.6261 (‐2.88***)

0.0959 (2.78**)

1.4291 (2.79**)

1.8579 (2.07*)

‐0.0054 (‐2.01*)

0.774

Malaysia (154) ‐1.3718 (‐7.46***)

0.2102 (4.87***)

0.8948 (2.67***)

1.8514 (3.75***)

0.0017 (0.71)

0.329

Japan (90) ‐1.2180 (‐5.94***)

0.2275 (7.34***)

0.6743 (1.88*)

2.3080 (4.30***)

‐0.0051 (‐1.82*)

0.492

Hong Kong (180) ‐1.3363 (‐8.38***)

0.1392 (5.86***)

1.3622 (3.52***)

1.1084 (3.31***)

‐0.0098 (‐3.05***)

0.423

Germany (7) ‐2.8213 (4.85***)

0.6140 (10.11***)

‐10.1704 (‐6.07***)

‐0.7436 (‐1.23)

‐0.1440 (‐3.16)

0.972

France (19) 0.6907 (1.57)

‐0.0042 (‐0.07)

‐9.6919 (‐3.16***)

3.8528 (1.89*)

‐0.0058 (‐1.11)

0.464

Finland (10) ‐3.1708 (‐9.17***)

0.5028 (9.05***)

‐0.6344 (‐0.85)

1.7298 (3.32***)

0.0015 (1.08)

0.975

China (128) ‐1.6770 (‐3.20***)

0.4381 (4.58***)

1.0430 (1.18)

‐0.3026 (‐0.57)

0.0845 (1.22)

0.176

Belgium (17) ‐1.2675 (‐6.48***)

0.1844 (5.93***)

‐0.3989 (‐0.49)

1.7517 (3.39***)

‐0.0024 (‐1.46)

0.749

Australia (37) ‐1.0050 (‐2.69***)

0.1959 (2.87***)

‐0.5322 (‐0.57)

‐0.0767 (‐0.07)

‐0.0122 (‐1.43)

0.220

By continents

Asia (778) ‐1.1882 (‐12.56***)

0.2059 (12.132***)

0.8747 (3.72***)

1.7367 (7.24***)

‐0.0096 (‐4.40***)

0.296

Europe (289) ‐0.6118 (‐6.63***)

0.0919 (6.26***)

0.8895 (2.92***)

1.3787 (5.18***)

‐0.0014 (‐2.00**)

0.362

N America (64) 0.4758 (‐1.91*)

0.1838 (3.42***)

‐0.5451 (‐1.07)

2.9092 (3.83***)

0.0046 (0.33)

0.463

By Year

2000 (130) ‐0.8787 (‐3.62***)

0.1490 (3.52***)

0.8098 (1.49)

2.5139 (3.95***)

‐0.0041 (‐1.39)

0.254

2001 (147) ‐1.0128 (‐3.99***)

0.1688 (3.81***)

3.3528 (3.26***)

0.2487 (0.38)

‐0.0091 (‐1.97**)

0.213

2002 (147) ‐1.0083 (‐4.56***)

0.1665 (4.14***)

‐0.1558 (‐0.28)

1.8569 (3.51***)

‐0.0040 (‐1.15)

0.217

2003 (161) ‐0.7466 (‐4.09***)

0.1157 (3.50***)

1.4061 (3.02***)

3.1759 (5.78***)

‐0.0018 (‐0.74)

0.358

2004 (175) ‐1.0057 (‐6.83***)

0.1341 (5.29***)

2.2088 (5.53***)

2.6770 (6.08***)

0.0008 (0.82)

0.440

2005 (193) ‐1.0542 (‐7.12***)

0.1817 (6.94***)

‐0.0355 (‐0.10)

1.1471 (3.22***)

‐0.0016 (‐0.86)

0.299

2006 (178) ‐1.0987 (‐5.91***)

0.2050 (6.84***)

0.2825 (0.58)

1.0222 (2.03**)

‐0.0021 (‐0.96)

0.317

Notes: Estimation using weighted two-stage least square (W2SLS); ***, **, * - indicates two tailed significance at the 1%, 5% and 10% levels respectively

18

Exhibit 5 Results of system equation estimation (Equation 2: Sustainable growth rate: SGR) Sample (No of

pooled observation)

Intercept Size MV/BV Tangibility Profitability Debt ratio Earnings retention (ERR)

System weighted R2

ALL (1153) ‐0.0187 (1.04) 0.0022 (1.03) 0.0175 (3.91***) 0.00006 (0.45) 0.5922 (7.72***) 0.00019 (0.01) 0.0622 (3.17***) 0.103

By Country

US (63) 0.1519 (0.57) ‐0.0005 (‐0.03) ‐0.0156 (‐0.53) 0.00005 (0.17) 0.8106 (1.33) 0.0327 (0.32) ‐0.0892 (‐0.38) 0.037

UK (158) ‐0.0231 (‐0.88) 0.0036 (1.14) 0.0380 (2.71***) ‐0.00019 (‐0.98) 0.5154 (4.43***) ‐0.0019 (‐0.05) 0.0783e (3.80***) 0.393

Thailand (60) ‐0.1093 (‐0.72) 0.0509 (2.08**) ‐0.0426 (‐1.35) ‐0.0030 (‐1.19) 0.7312 (1.72*) 0.0635 (0.48) ‐0.1264 (‐1.37) 0.267

Switzerland (8) 0.0351 (0.64) ‐0.0124 (‐1.56) 0.0042 (0.16) ‐0.0011 (‐2.74**) 3.0451 (17.47***) 0.0384 (4.05***) 0.01541 (1.87*) 0.967

Sweden (18) ‐0.0965 (‐1.36) 0.0650 (1.06) 0.0215 (0.27) ‐0.00013 (‐0.31) 0.6131 (0.36) 0.5681 (1.01) 0.4616 (2.27**) 0.414

Spain (18) 0.2339 (0.60) ‐0.0619 (‐1.09) 0.1618 (1.68*) 0.0438 (1.86*) ‐0.9140 (‐0.89) 0.2044 (1.07) 0.2387 (1.85*) 0.274

Singapore (66) 0.1570 (2.01**) ‐0.0237 (‐2.56**) 0.0231 (0.83) ‐0.0037 (‐0.98) 0.0002 (0.01) ‐0.1543 (‐1.41) 0.1547 (3.02***) 0.219

Philippines (58) ‐0.1024 (‐2.62***) 0.0073 (1.73*) ‐0.0110 (‐1.18) 0.00047 (0.32) 1.5128 (5.24***) 0.0567 (0.66) 0.0543 (1.88*) 0.446

Norway (12) ‐0.6250 (‐2.56**) 0.0567 (1.89*) ‐0.0531 (‐0.54) ‐0.0036 (‐1.17) 1.4667 (2.60**) 0.4982 (1.83*) 0.1937 (2.29**) 0.596

Netherlands (11) ‐0.0025 (‐0.01) ‐0.0066 (‐0.22) 0.1814 (1.79*) 0.0011 (1.09) 0.8133 (0.62) 0.00088 (0.01) ‐0.0139 (‐0.07) 0.399

Malaysia (154) 0.0070 (0.11) 0.0138 (1.20) 0.0294 (1.40) ‐0.00035 (‐0.57) 0.0676 (0.18) ‐0.0982 (‐1.12) 0.0236 (0.87) 0.064

Japan (90) 0.1205 (1.06) ‐0.0067 (‐0.53) ‐0.0019 (‐0.06) ‐0.00038 (‐0.44) 0.9458 (0.74) ‐0.0692 (‐0.63) ‐0.0211 (‐0.21) 0.028

Hong Kong (180) 0.0497 (0.91) ‐0.0018 (‐0.35) 0.0493 (3.92***) 0.00066 (1.14) 0.3043 (2.52**) ‐0.1916 (‐2.66**) 0.0780 (2.27**) 0.225

Germany (7) NC NC NC NC NC NC NC NC

France (19) ‐0.0276 (‐0.74) 0.0025 (0.87) ‐0.0102 (‐0.85) ‐0.00043 (‐1.61) 0.5576 (4.02***) 0.0215 (0.37) 0.0597 (2.36**) 0.853

Finland (10) ‐0.4752 (‐1.74***) 0.0739 (2.50**) ‐0.0948 (‐1.50) 0.00054 (2.41**) 0.0413 (0.10) ‐0.0124 (‐0.07) 0.1427 (5.52***) 0.807

China (128) ‐0.0793 (‐1.31) 0.0141 (1.49) 0.0116 (1.44) ‐0.0017 (‐0.27) 0.6140 (3.55***) ‐0.0867 (‐1.55) 0.0733 (3.21***) 0.233

Belgium (17) ‐0.0833 (‐0.76) ‐0.0083 (‐0.70) ‐0.0504 (‐0.80) 0.00040 (0.84) 0.924 (1.69*) 0.2202 (2.41**) 0.1138 (1.70*) 0.700

Australia (37) 0.1311 (0.64) ‐0.0044 (‐0.19) ‐0.0122 (‐0.34) 0.00003 (0.02) ‐0.073 (‐0.13) ‐0.2907 (‐1.13) 0.0359 (0.33) 0.061

By continent

Asia (778) 0.0322 (1.39) 0.00031 (0.11) 0.0186 (3.54***) ‐0.00018 (‐0.54) 0.4749 (5.02***) ‐0.0910 (‐3.15***) 0.0367 (2.37**) 0.079

Europe (289) ‐0.0766 (‐3.35***) 0.0030 (1.11) 0.0430 (4.29***) ‐0.00005 (‐0.40) 0.5681 (5.49***) 0.0733 (0.79***) 0.1180 (7.92***) 0.428

N. America (64) 0.0248 (0.11) 0.00060 (0.04) ‐0.0083 (‐0.31) 0.000098 (0.26) 0.7249 (1.26) 0.0213 (0.21) 0.0415 (0.22) 0.035

By Year

2000 (130) 0.0377 (0.66) ‐0.0052 (‐0.75) 0.0118 (0.92) 0.00013 (0.27) 0.6093 (2.27**) ‐0.1008 (‐1.53) 0.0978 (2.47**) 0.123

2001(147) 0.0047(0.15) ‐0.00093 (‐0.24) 0.0248 (3.77***) 0.00035 (0.89) 0.6690 (4.55***) ‐0.0246 (‐0.80) 0.0398 (1.91*) 0.226

2002 (147) ‐0.0425 (‐0.68) 0.0087 (1.23) ‐0.0071 (‐0.56) 0.00008 (0.15) 0.2414 (1.32) ‐0.0243 (‐0.44) 0.0355 (0.95) 0.025

2003 (161) 0.0054 (0.09) 0.0019 (0.32) 0.0408 (3.20***) 0.00012 (0.29) 0.4061 (1.68*) ‐0.0208 (‐0.40) 0.0417 (1.17) 0.136

2004 (175) 0.0578 (1.39) ‐0.0122 (‐2.61***) 0.0519 (4.59***) ‐0.000003 (‐0.02) 0.2997 (1.53) 0.0706 (1.68*) 0.0711 (2.31**) 0.173

2005 (193) ‐0.0708 (‐1.21) 0.0143 (2.31**) 0.0029 (0.19) 0.000059 (0.15) 0.4430 (1.87*) ‐0.0838 (‐1.41) 0.0752 (1.66*) 0.086

2006 (178) ‐0.0222(‐0.64) ‐0.0047 (‐0.98) 0.0137 (1.28) ‐0.000055 (‐0.17) 0.9890 (5.17***) 0.1567 (3.64***) 0.0644 (3.01***) 0.232

Notes: Estimation using weighted two-stage least square (W2SLS); ***, **, * - indicates two tailed significance at the 1%, 5% and 10% levels respectively, NC-non-convergence

19

Exhibit 6 Results of system equation estimation (Equation 3: Profitability: ROA) Sample (No of

pooled observation)

Intercept Size Tangibility Debt ratio Sustainable growth

System weighted R2

ALL (1131) 0.0159 (3.66***)

0.0048 (6.90***)

0.0002 (4.17***)

‐0.0406 (‐5.79***)

0.0861 (8.02***)

0.133

By country

USA (63) 0.0529 (3.06***)

0.0002 (0.09)

0.0002 (2.55**)

‐0.0680 (‐3.43***)

0.0325 (1.23)

0.321

UK (158) 0.0281 (2.05***)

0.0029 (1.42)

‐0.00002 (‐0.19)

‐0.0397 (‐1.83*)

0.2886 (6.69***)

0.272

Thailand (60) 0.0538 (2/.06**)

0.0105 (2.16**)

‐0.0004 (‐1.54)

‐0.1404 (‐4.12***)

0.0766 (2.10**)

0.433

Switzerland (8) 0.0084 (1.15)

0.0016 (1.71)

0.0003 (3.46***)

‐0.0152 (‐6.15***)

0.3035 (29.99****)

0.987

Sweden (18) 0.1074 (1.09)

0.0030 (0.31)

‐0.00007 (‐1.23)

‐0.1454 (‐2.05**)

0.1248 (4.07***)

0.725

Spain (18) 0.0730 (1.48)

‐0.0035 (‐0.51)

0.0084 (1.99**)

‐0.0107 (‐0.27)

‐0.0331 (‐0.69)

0.201

Singapore (66) 0.1547 (3.02***)

0.0473 (2.47***)

0.0020 (0.79)

‐0.0689 (‐2.61)

0.0186 (0.60)

0.184

Philippines (58) ‐0.0017 (‐0.21)

0.0017 (1.05)

0.0005 (0.64)

0.1083 (2.80***)

0.2354 (4.46***)

0.461

Norway (12) 0.0063 (0.05)

0.0082 (0.48)

0.0003 (0.34)

‐0.0825 (‐0.96)

0.1674 (1.43)

0.410

Netherlands (11) 0.0708 (0.84)

‐0.0011 (‐0.07)

0.0006 (1.06)

‐0.0801 (‐0.75)

0.2897 (2..21**)

0.640

Malaysia (154) 0.0040 (0.04)

0.0103 (4.57***)

‐0.000007 (‐0.05)

‐0.0478 (‐2.51**)

0.0136 (0.76)

0.189

Japan (90) 0.0409 (4.99***)

‐0.0003 (‐0.32)

‐0.0001 (‐1.13)

‐0.0412 (‐4.03***)

0.0087 (0.79)

0.173

Hong Kong (180) ‐0.0071 (‐0.38)

0.0088 (3.66***)

0.0008 (2.22**)

‐0.0989 (‐2.31**)

0.1396 (3.35***)

0.212

Germany (7) 0.0492 (0.83)

‐0.0001 (‐0.02)

‐0.0042 (‐1.35)

‐0.0151 (‐0.48)

0.0940 (0.78)

0.678

France (19) ‐0.0092 (‐0.22)

0.0006 (0.16)

0.0001 (0.50)

0.0267 (0.50)

0.8815 (6.55***)

0.826

Finland (10) 0.0612 (1.25)

0.0191 (2.15**)

0.0002 (0.88)

‐0.2650 (‐3.80***)

0.1468 (1.01)

0.813

China (128) ‐0.0099 (‐0.43)

0.0090 (2.20**)

‐0.0037 (‐1.18)

‐0.0978 (‐4.04***)

0.1244 (3.10***)

0.279

Belgium (17) 0.0330 (1.20)

0.0061 (1.43)

0.0002 (0.71)

‐0.1083 (‐2.78***)

0.3898 (4.70***)

0.732

Australia (37) ‐0.0472 (‐1.13)

0.0113 (2.37**)

‐0.0002 (‐0.41)

0.1300 (1.53)

‐0.0068 (‐0.15)

0.152

By continents

Asia (778) 0.0195 (3.55***)

0.0044 (4.95***)

0.0002 (1.74*)

‐0.0556 (‐5.34***)

0.0677 (5.18***)

0.109

Europe (289) 0.0364 (3.83***)

0.0032 (2.35**)

0.00005 (1.26)

‐0.0616 (‐4.71***)

0.1994 (7.89***)

0.245

N America (64) 0.0527 (3.09***)

0.0003 (0.11)

0.0002 (2.57**)

‐0.0677 (‐3.47***)

0.0322 (1.24)

0.322

By Year

2000 (130) 0.0137 (1.06)

0.0038 (1.92*)

0.00004 (0.26)

‐0.0282 (‐1.45)

0.0580 (2.13**)

0.079

2001 (147) ‐0.0066 (‐0.59)

0.0044 (2.36**)

0.0002 (1.06)

‐0.0140 (‐0.84)

0.1667 (4.14***)

0.159

2002 (147) ‐0.0129 (‐0.84)

0.0067 (2.56**)

0.00006 (0.26)

‐0.0035 (‐0.14)

0.0428 (1.14)

0.055

2003 (161) 0.0272 (2.60***)

0.0014 (0.75)

0.0001 (0.77)

‐0.0217 (‐1.26)

0.0764 (2.97***)

0.067

2004 (175) 0.0372 (3.88***)

0.0030 (1.91*)

0.0001 (1.56)

‐0.0600 (‐3.70***)

0.0593 (2.21**)

0.109

2005 (193) 0.0463 (4.77***)

0.0028 (1.77*)

0.0004 (3.04***)

‐0.0606 (‐3.55***)

0.0442 (2.06**)

0.139

2006 (178) 0.0195 (2.02**)

0.0060 (4.29***)

0.0004 (3.76***)

‐0.0640 (‐3.98***)

0.1317 (5.16***)

0.303

Notes: Estimation using weighted two-stage least square (W2SLS); ***, **, * - indicates two tailed significance at the 1%, 5% and 10% levels respectively

20

Exhibit 7 Results of System Equation Estimation (Equation 4: Debt ratio: DEBTR) Sample (No of

pooled observation)

Intercept Size Tangibility Profitability Growth (TA)

ERR System weighted

R2

All (1131) 0.2750 (11.45***)

0.0068 (2.24**)

0.00094 (4.65***)

‐0.7709 (‐6.49***)

0.0747 (4.87***)

‐0.0273 (‐1.47)

0.067

By Country

USA (63) 0.7506 (2.77***)

‐0.0754 (‐4.76***)

‐0.0002 (‐0.45)

‐2.4148 (‐4.16***)

0.5123 (4.90***)

‐0.0333 (‐0.14)

0.535

UK (158) 0.3397 (6.86***)

0.0140 (1.92*)

‐0.0030 (‐0.;67)

‐0.3081 (‐1.16)

0.0062 (0.14)

‐0.0667 (‐1.39)

0.044

Thailand (80) 0.3100 (2.87***)

0.0011 (0l.07)

‐0.00053 (‐0.22)

‐1.3598 (‐3.48***)

0.0120 (0.22)

0.1297 (1.42)

0.306

Switzerland (8) 3.2434 (3.97***)

‐0.3714 (‐4.01***)

0.0175 (1.51)

‐11.7280 (I‐2.85***)

‐0.3460 (‐1.49)

‐0.8210 (‐2.88***)

0.622

Sweden (18) 1.5110 (9.20***)

‐0.1280 (‐5.52***)

‐0.00018 (‐1.07)

0.5322 (0.54)

0.1169 (2.5r6**)

‐0.1544 (‐1.23)

0.839

Spain (18) 0.3244 (1.06)

0.0357 (0.96)

0.0011 (0.04)

0.5221 (0.37)

0.0915 (2.02**)

‐0.2680 (‐1.74*)

0.155

Singapore (66) 0.3310 (4.57***)

‐0.0110 (‐1.13)

‐0.0028 (‐0.69)

‐1.7259 (‐3.49***)

0.1926 (2.55**)

0.1263 (2.31**)

0.250

Philippines (58) 0.8284 (1.41)

‐0.0059 (‐1.06)

0.0016 (0.70)

1.3992 (3.21***)

‐0.0073 (‐0.11)

0.0320 (0.68)

0.244

Norway (12) 0.9989 (3.52***)

‐0.0753 (‐1.57)

0.0079 (2.54**)

‐0.8555 (‐0.86)

‐0.1160 (‐1.54)

‐0.1106 (‐0.75)

0.340

Netherlands (11) ‐0.2717 (‐1.35)

0.0876 (3.32***)

‐0.00072 (‐0.49)

‐3.2212 (‐2.06*)

0.0034 (0.03)

0.3710 (1.59)

0.663

Malaysia (154) 0.2072 (4.64***)

‐0.0072 (‐0.73)

0.00023 (0.41)

‐0.8427 (‐2.60***)

0.0537 (1.49)

0.0288 (1.14)

0.082

Japan (90) 0.3869 (4.24***)

‐0.0115 (‐1.28)

‐0.00061 (‐0.75)

‐4.8726 (‐4.49***)

‐0.0084 (‐0.13)

0.2436 (2.55**)

0.232

Hong Kong (180) 0.2437 (5.35***)

‐0.0098 (‐2.16**)

‐0.00035 (‐0.59)

‐0.4008 (‐3.13***)

0.02010 (1.14)

0.0125 (0.35)

0.123

Germany (7) 1.8859 (43.62***)

‐0.1292 (‐32.39***)

‐0.0710 (‐17.28***)

‐14.6005 (‐18.12***)

‐0.0772 (‐0.53)

0.7044 (22.90***)

0.984

France (19) 0.6336 (7.52***)

‐0.01453 (‐1.13)

0.0015 (1.44)

0.5309 (0.89)

0.0259 (0.91)

‐0.2979 (‐3.46***)

0.530

Finland (10) 0.5337 (3.06***)

0.0055 (0.17)

‐0.00026 (‐0.37)

‐1.8333 (‐3.06***)

0.0707 (1.81*)

0.1205 (1.88*)

0.532

China (128) 0.2001 (2.00**)

0.0043 (0.26)

0.0274 (2.47**)

‐1.2704 (‐4.56***)

0.0062 (0.14)

0.0104 (0.25)

0.216

Belgium (17) 0.2647 (1.33)

0.0263 (0.92)

‐0.0015 (‐0.99)

‐2.5515 (‐1.49)

‐0.00019 (‐0.01)

0.2227 (0.98)

0.006

Australia (37) 0.5210 (6.39***)

‐0.0489 (‐4.86***)

0.0023 (1.98**)

0.6447 (1.80*)

0.0339 (1.02)

‐0.0399 (‐0.57)

0.474

By Continent

Asia (778) 0.2169 (8.64***)

0.0034 (1.09)

0.00062 (1.50)

‐0.7538 (‐6.61***)

0.0468 (2.96***)

0.0215 (1.10)

0.057

Europe (289) 0.3523 (8.34***)

0.0164 (2.73***)

0.00011 (0.37)

‐0.6861 (‐2.81***)

0.0353 (1.29)

‐0.0538 (‐1.51)

0.071

N America (64) 0.8797 (3.99***)

‐0.0789 (‐5.17***)

‐0.00021 (‐0.54)

‐2.3786 (‐4.12***)

0.5177 (4.98***)

‐0.1521 (‐0.78)

0.492

By Year

2000 (130) 0.2794 (3.85***)

0.0034 (0.37)

0.0018 (2.62***)

‐0.6077 (‐1.79*)

‐0.0402 (‐1.08)

0.0168 (0.29)

0.103

2001(147) 0.3480 (4.54***)

‐0.0082 (‐0.84)

0.0030 (2.86***)

‐0.4976 (‐1.25)

0.0829 (1.49)

‐0.0453 (‐0.81)

0.077

2002 (147) 0.2889 (3.58***)

0.0044 (0.43)

0.0023 (2.89***)

‐0.2284 (‐0.80)

0.0958 (1.95*)

‐0.0494 (‐0.89)

0.098

2003 (161) 0.2455 (3.41***)

0.0127 (1.47)

0.0012 (1.75*)

‐0.6391 (‐1.83*)

0.0759 (3.04***)

‐0.0487 (‐0.90)

0.110

2004 (175) 0.2385 (3.69***)

0.0128 (1.77*)

0.00007 (0.24)

‐1.2341 (‐3.78***)

0.1338 (2.52**)

‐0.0186 (‐0.35)

0.112

2005 (193) 0.2112 (3.24***)

0.0103 (1.65*)

0.0014 (2.86***)

‐1.1265 (‐4.03***)

0.0713 (2.12**)

0.0407 (0.73)

0.122

2006 (178) 0.2532 (5.17***)

0.0056 (0.81)

0.0013 (2.38**)

‐0.9961 (‐3.17***)

0.1187 (2.54**)

0.0099 (0.27)

0.090

Notes: Estimation using weighted two-stage least square (W2SLS); ***, **, * - indicates two tailed 0significance at the 1%, 5% and 10% levels respectively

21

Exhibit 8 OLS Regression Results

Jensen ‘s alpha (JI) Sharpe Index (SI) Variables Coefficient t-statistic Coefficient t-statistic

Intercept ‐0.01356*** ‐2.90 0.64576 0.70

LN (market value) 0.00195*** 2.69 0.40993*** 4.18

LN (Market equity / Book equity) 0.00415*** 3.20 0.28657 0.98

Sustainable growth rate (SGR) 0.03848*** 7.75 ‐0.44880 ‐0.38

Profitability (ROA) 0.04326** 2.25 8.09315** 2.01

Capital structure (D/E) 0.00299** 2.02 ‐0.38674 ‐0.96

Spread (return on equity – cost of equity)

0.00182 0.19 1.64655 1.18

DREG1 0.00382 1.13 ‐0.29675 ‐0.45

DREG2 ‐0.00358 ‐1.20 ‐1.83137*** ‐2.82

DREG3 0.00732*** 2.63 1.44638** 2.46

Adjusted R2 0.547 0.575

F‐stat 23.73 26.37

Prob (F‐stat) 0.0000 0.0000 Notes: ***, ** - indicates two-tailed statistical significance at the 1% and 5% levels; DREG i = dummy variable if firm i is in Group X, X = 1 (Asia-Pacific developed /matured markets: Australia, New Zealand, Japan, Singapore, Hong Kong), 2 (Asia-Pacific developing markets: Malaysia, Thailand, Philippines, Indonesia and China), 3 (European markets: UK, France, Germany, etc) or =0, otherwise; Intercept is the SI (or JI) mean values for Group 4 (North Americas markets: Canada and USA)

Exhibit 9 Binary Logit Regression Results

Prediction Evaluation (cutoff for success C = 0.5) Jensen’s alpha (JI) Sharpe Index (SI)

Prob (dep = 1) <=C 51 69

No correct 33 46

% correct 64.71 66.67

Prob (dep = 1)>=C 119 101

No correct 109 85

% correct 91.60 84.16

Total 170 170

No correct 142 131

% correct 83.53 77.06 Note: (a) “correct” classifications are obtained when the predicted probability is less than or equal 0.5 and the observed dependent variable =0, or when the predicted probability is greater than 0.5 and observed dependent variable = 1, (b) For JI, the dependant dummy is 1 if JI is positive; and is 0 when JI is negative, (c) For SI, the dependant dummy is I if SI >2.1522 (sample average), or o otherwise