financial management meaning of financial...

TRANSCRIPT

Management Chapter I

Management of funds is an important aspect of financial management.

Meaning of Financial Management

- Financial management is that managerial activity which is concerned

with planning and controlling of the firm’s financial resources. - It is concerned with acquiring, financing and managing assets to

accomplish the overall goal of a business enterprise (mainly to maximise

the shareholder’s wealth). - Financial management comprises the forecasting, planning, organizing,

directing, coordinating and controlling of all activities relating to

acquisition and application of the financial resources of an undertaking in keeping with its financial objective.”

- Financial Management is concerned with the managerial decisions that result in the acquisition and financing of short term and long term credits for the firm.

- Financial Management is concerned with efficient acquisition (financing) and allocation(investment in assets, working capital etc) of funds

What does Financial Management mean-

Efficient use of economic resources namely capital funds.

According to Phillippatus, "Financial management is concerned with the

managerial decisions that result in the acquisition and financing of short

term and long term credits for the firm".

Here it deals with the situations that require selection of specific assets

(or combination of assets), the selection of specific size and growth of an enterprise.

Here the analysis deals with the expected inflows and outflows of funds and their effect on managerial objectives.

So the analysis simply states two main aspects of financial management namely procurement of funds and an effective use of funds

to achieve business objectives.

Procurement of funds:

As funds can be obtained from different sources, the procurement of funds is considered as an important aspect of business concerns.

Funds procured from different sources have different characteristics in terms of risk, cost and control.

Funds raised by issue of equity shares are the best from the point of view of risk for the company, as there is no question of repayment of equity

capital except when the company is under liquidation.

From the cost point, equity capital is the most expensive source of funds

as dividend expectations of shareholders are normally higher than the prevalent interest rates.

Financial management constitutes risk, cost and control. The cost of funds should be at minimum for a proper balancing of risk and control.

In the Globalised competitive scenario mobilization of funds plays a very significant role.

Funds can be raised either through domestic market or international market. Foreign Direct Investment (FDI) as well as Foreign Institutional

Investors (FII) is two major sources of raising funds. The mechanism of procurement of funds has to be modified in the light of requirements of foreign investors.

Utilization of Funds:

1. Effective utilization of funds is an important aspect of financial management as it avoids the situations where funds are either kept idle or under-utilised.

2. Funds procured involve a certain cost and risk.

3. If the funds are not used properly, then running business will have difficulties.

4. In case of dividend decisions we also consider this. So it is crucial to employ the funds properly and profitably.

How do we measure the wealth of a company ?

Value of a firm is represented by the market price of the company's

common stock. The market price of a firm's stock represents the focal judgment of

all market participants as to what the value of the particular firm is.

It takes into account present and prospective future earnings per share,

the timing and risk of these earnings, the dividend policy of the firm and many other factors that bear upon the market price of the stock.

The market price serves as a performance index or report card of the

firm's progress. It indicates how well management is doing on behalf of stockholder

Investment Decisions :

Decisions relate to the selection of assets in which funds will be invested by a firm. Funds procured from different sources have to be invested in various kinds of assets.

Long term funds are used in a project for various fixed assets and also for current assets.

The investment of funds in a project has to be made after careful assessment of the various projects through capital budgeting.

Part of the long term funds is also kept for financing the working

capital requirements. Asset management policies are to be laid down regarding various

items of current assets. The inventory policy would be determined by the production

manager and the finance manager, keeping in view the

requirement of production and the future price estimates of raw materials and the availability of funds.

Financing decisions:

Decisions relate to acquiring the optimum finance to meet financial objectives and seeing that fixed and working capital are effectively

managed. The financial manager needs to possess a good knowledge of the

sources of available funds and their respective costs and needs to

ensure that the company has a sound capital structure, i.e. a proper balance between equity capital and debt.

Managers need to have a very clear understanding as to the

difference between profit and cash flow, bearing in mind that profit is of little avail unless the organisation is adequately supported by

cash to pay for assets and sustain the working capital cycle. Financing decisions also call for a good knowledge of evaluation of

risk, e.g. excessive debt carries high risk for an organization’s

equity because of the priority rights of the lenders. A major area for risk-related decisions is in overseas trading,

where an organisation is vulnerable to currency fluctuations, and the manager must be well aware of the various protective procedures such as hedging (it is a strategy designed to minimize,

reduce or cancel out the risk in another investment available to him).

Dividend decisions:

Decisions relate to the determination as to how much and how frequently cash can be paid out of the profits of an organisation as income for its owners/shareholders.

The owner of any profit-making organization looks for reward for his investment in two ways, the growth of the capital invested and the cash paid out as income; for a sole trader this income would be

termed as drawings and for a limited liability company the term is dividends.

What is the importance of Financial Management?

The importance of good financial management is to describe some of the tasks that it involves:-

Avoidance of over investment in the fixed assets Balancing cash-outflow with cash-inflows

Ensuring that there is a sufficient level of short-term working capital

Setting sales revenue targets that will deliver growth

Increasing gross profit by setting the correct pricing for products or services

Controlling the level of general and administrative expenses by finding more cost efficient ways of running the day-to-day business

operations Tax planning that will minimize the taxes a business has to pay.

What are scopes of Financial Management ?

Determination of size of the enterprise and determination of rate of growth.

Determining the composition of assets of the enterprise. Determining the mix of enterprise’s financing i.e. consideration of level of

debt to equity, etc.

Analysis, planning and control of financial affairs of the enterprise. A sound financial management is essential in all types of organizations

whether it may be profit or non-profit.

Financial management is essential in a planned Economy as well as in a capitalist set-up as it involves efficient use of the resources.

From time to time, it is seen that many firms have been liquidated not because their technology was obsolete or because their products were not in demand or their Labour was not skilled and motivated but there

was a complete mismanagement of financial affairs. Even in a boom period, when a company make high profits there is also a

fear of liquidation because of bad financial management. Financial management optimizes the output from the given input of

funds.

In the country like India where resources are scarce and the demand for funds are many, the need of proper financial management is required.

In case of newly started companies with a high growth rate it is more

important to have sound financial management since finance alone guarantees their survival.

Financial management is very important in case of non-profit organizations, which do not pay adequate attentions to financial management.

However a sound system of financial management has to be cultivated among bureaucrats, administrators, engineers, educationalists and public at a large.

Present Value

- “Present Value” is the current value of a “Future Amount”.

- It can also be defined as the amount to be invested today (Present Value) at a given rate over specified period to equal the “Future Amount”.

Annuity

- An annuity is a stream of regular periodic payment made or received for

a specified period of time.

- In an ordinary annuity, payments or receipts occur at the end of each period.

Perpetuity

Perpetuity is an annuity in which the periodic payments or receipts begin on a fixed date and continue indefinitely or perpetually.

Fixed coupon payments on permanently invested (irredeemable) sums of

money are prime examples of perpetuities.

Financial Management In India

In the country like India there is a changing scenario of financial

management.

As the economy is opening up and global participation is increasing very fast, the opportunities have no limits.

Presently financial management passes through an era of experimentation as a larger part of finance activities are carried out.

Highlights Context:

Interest rates are free from regulations. Rupee is fully convertible in current account.

Optimum debt equity mix is possible. Maintaining share prices are also crucial. In liberalized scenario the

capital market is an important avenue of funds for business. Ensuring management control is vital especially in the light of foreign

participation.

Financial Management Objectives

1) Profit Maximization:

Objective of financial management is same as the objective of a company

that is to earn profit.

But profit maximization cannot be the sole objective of a company. It is a

limited objective.

If profits are given undue Importance then problems may arise as

discussed below.

The term profit is vague and it involves much more contradictions. Profit maximization has to be attempted with a realization of risks

involved. A positive relationship exists between risk and profits. So both risk and profit objectives should be balanced.

Profit Maximization does not take into account the time pattern of

returns. Profit maximization fails to take into account the social considerations

2) Wealth Maximization:

- It is commonly agreed that the objective of a firm is to maximize value or

wealth.

- Value of a firm is represented by the market price of the company's

common stock.

The market price of a firm's stock represents the focal judgement of all

market participants as to what the value of the particular firm is.

It takes in to account present and prospective future earnings per share, the timing and risk of these earning, the dividend policy of the firm and

many other factors that bear upon the market price of the stock. Market price acts as the performance index or report card of the firm's progress.

- Prices in the share markets are largely affected by many factors like

general economic outlook, outlook of particular company, technical factors

and even mass psychology.

Normally this value is a function of two factors as given below,

The anticipated rate of earnings per share of the company The capitalization rate.

The likely rate of earnings per shares (EPS) depends upon the assessment as to how profitably a company is growing to operate in the future.

The capitalization rate reflects the interest of the investors for the company. Methods of Financial Management:

In the field of financing there are various methods to procure funds.

Funds may be obtained from long-term sources as well as from short-term sources.

Long-term funds may be availed by owners that are shareholders, lenders by issuing debentures, from financial institutions, banks and public at large.

Short-term funds may be availed from commercial banks, public

deposits, etc. Financial leverage or trading on equity is an important method by which a finance manager may increase the return to common shareholders.

At the time of evaluating capital expenditure project, methods like average rate of return, pay back, internal rate of returns, net present

value and profitability index are used.

A firm can increase its profitability without affecting its liquidity by an efficient management of working capital and utilization of the current

resources at the disposal of the firm.

Similarly for the evaluation of a firm's performance there are different

methods.

Ratio analysis is a popular technique to evaluate different aspects of a firm.

An investor takes in to account various ratios to know whether investment in a particular company will be profitable or not.

These ratios enable him to judge the profitability, solvency, liquidity and growth aspect of the firm.

LIQUIDITY:

Is defined as ability of the business to meet short-term obligations.

It shows the quickness with which a business/company can convert its assets into cash to pay what it owes in the near future.

It measures a company’s ability to meet expected as well as unexpected requirements of cash to expand its assets, reduce its liabilities and cover

up any operating losses.

Liquidity is assessed through the use of ratio analysis. liquidity ratio

provides an insight into the present cash solvency of a firm and its ability to remain solvent in the event of financial crisis.

Liquidity of receivables is assessed through Average collection period(ACP) as it tells us the average number of days receivables are

outstanding i.e., the average time a bill takes to convert into cash.

The ratio, reveals the following:

Too low an ACP may suggest excessively restricted credit policy of a

company.

Too high an ACP may indicate too liberal a credit policy. A large number

of receivables may remain due and outstanding, resulting in less profits and more chances of bad debts.

PROFITABILITY:

When it becomes essential for a company to examine profit per unit of

sale - it is done by estimating profitability per rupee sales. It is used as measure of comparison and standard of performance.

Profitability to sales ratio reflects the company’s ability to generate profits per unit of sales.

FINANCIAL DISTRESS AND INSOLVENCY:

In managing business risk, the firm has to cope with the variability of the demand for its products, their prices, etc.

It has also to keep a tab on fixed costs.

As regards financial risk, high proportion of debt in the capital structure

entails a high level of interest payments.

If cash inflow is inadequate, the firm will face difficulties in payment of

interest and repayment of principal.

If the situation continues long enough, a time will come when the firm

would face pressure from creditors.

Failure of sales can also cause difficulties in carrying out production

operations.

The firm would find itself in a tight spot.

Investors would not invest further. Creditors would recall their loans.

Capital market would heavily discount its securities.

Thus, the firm would find itself in a situation called distress.

When the sale proceeds is inadequate to meet outside liabilities, the firm is said to have failed or become bankrupt or (after due processes of law

are gone through) insolvent.

FUNCTIONS OF FINANCIAL EXECUTIVE:

Forecasting of cash flow Raising funds

Managing the flow of internal funds To facilitate cost control To facilitate pricing of product lines and services

Forecasting profits Measuring required return

Managing assets Managing funds

FINANCIAL SECTOR REFORMS IN INDIA:

Following key areas of reforms:

Reforms of structure of financial systems

Policies and regulations to deal with insolvency and liquidity of financial intermediaries

The development of markets for short and long term financial instruments

The role of institutional elements in development of financial systems

The link between financial sector and the real sectors, particularly in the case of restructuring financial and industrial institutions or enterprises

The dynamics of financial systems management in terms of stabilization and adjustment, and

Access to international markets.

The financial sector reforms in India seeks to achieve the following:

Suitable modifications in the policy framework

Improvement in the financial health and competitive capabilities Building financial infrastructure

Up gradation of the level of managerial competence and the quality of human resource of banks by reviewing to recruitment, training, and placement.

Capital budgeting is concerned with decisions which each return on investment

over a period of time in future. For evaluation of investment proposal an

estimation of the future benefits accruing from the investment proposal is

required to be made. To quantify the benefits, two alternative criteria are

available and they are accounting profit and cash flows. The basic

differentiating factor is the inclusion of certain non-cash expenses in the profit

and loss account such as, depreciation. The accounting profit is to be adjusted

for these non-cash expenditure to determine the actual cash inflow. The cash

flow approach of measuring the future benefits of a project is superior to the

accounting approach as cash flows are theoretically better measures of the net

economic benefits of costs associated with a proposed project, because of the

following three reasons.

- It considered economic value which is determined by the economic

outflows and inflows.

- The use of cash flows avoids accounting ambiguities.

- The cash flow approach takes into account the time value of money

whereas the accounting approach ignores it.

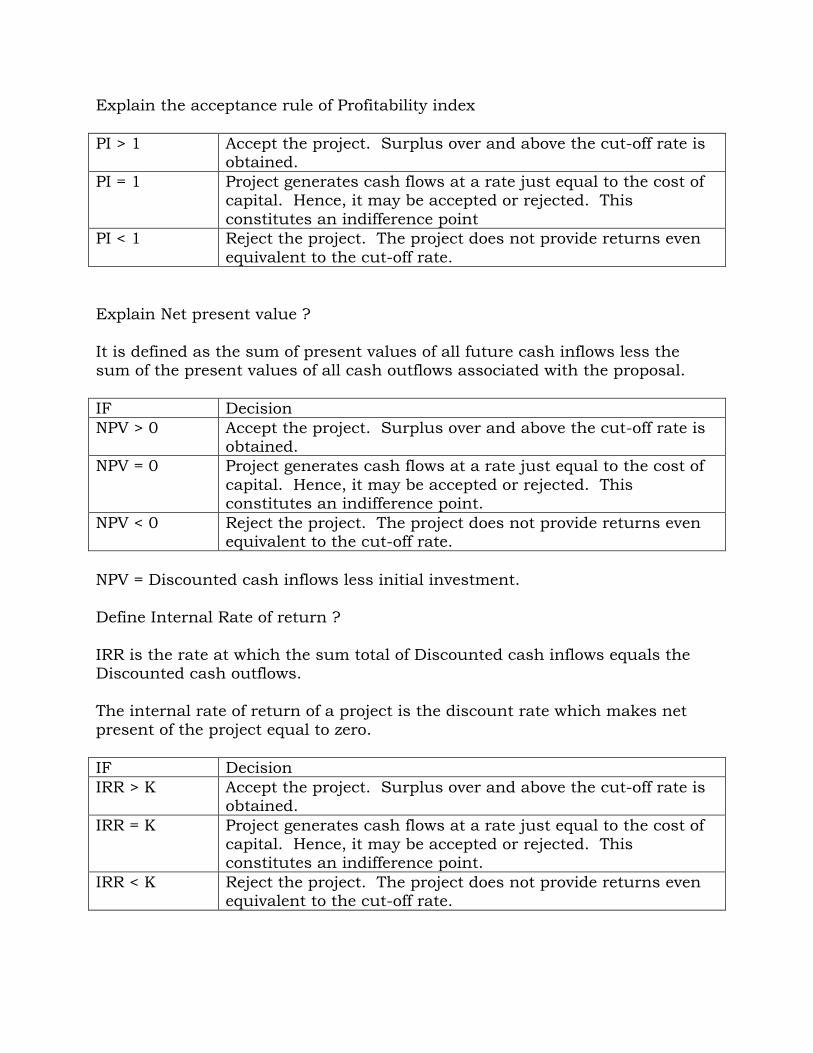

Net Present Value :

- It is a process of calculating the present value of cash flows(inflows and

outflows) of an investment proposal, using the cost of capital as the

appropriate discounting rate and finding out the net present value by

subtracting the present value of cash outflows from the present value of

cash inflows.

- The decision criteria using NPV method is to accept the investment

project if its present value is positive or equal to zero.

Internal Rate of return :

- It is that rate of discount which equates the present value of cash inflows

with the present value of cash outflows of an investment. In other words,

it is the rate at which the NPV of the investment is zero.

- It is a percentage figure which will not indicate the financial

attractiveness of the project in percentage term.

SOURCES OF FINANCE CHAPTER IV

What is Equity shares ?

- Funds raised by the issue of equity shares are the best in the risk point

of view for the firm, since there is no question of repayment of equity capital except when the firm is under liquidation.

- However, equity capital is usually the most expensive source of funds from the cost point of view. This is because the dividend expectations of

shareholders are normally higher than prevalent interest rate and also because dividends are an appropriation of profit, not allowed as an expense under the Income Tax Act.

- Also the issue of new shares to public may dilute the control of the

existing shareholders. What is Debenture ?

- Debentures as a source of funds are comparatively cheaper than the

shares because of their tax advantage.

- The interest the company pays on a debenture is free of tax, unlike a dividend payment which is made from the taxed profits.

- However, even when times are hard, interest on debenture loans must be paid whereas dividends need not be.

- However, debentures entail a high degree of risk since they have to be

repaid as per the terms of agreement. Also, the interest payment has to be made whether or not the company makes profits.

Recourse factoring :

- Under recourse factoring, the factor provides all types of factoring services except assumption of the credit risk of the debts. Consequently, if the customer makes default in payment of the debt on maturity for any

reason, the factor is entitled to recover from the client the amount

advanced against such debt, in all other respects, recourse factoring is akin to full factoring.

Loan syndication :

- Loan syndication involves obtaining commitment for term loans from the

financial institutions and banks to finance the project.

- It refers to the services rendered by merchant bankers in arranging and procuring credit from financial institutions, banks and other lending and investment organization or financing the client project cost or working

capital requirements. Process of loan syndication involves the following usual formalities :

(a) Preparation of project details. (b) Preparation of loan application.

(c) Selection of financial institutions for loan syndication. (d) Issue of sanction letter of intent from financial institutions

(e) Compliance of terms and conditions for availment of the loan (f) Documentation (g) Disbursement of the loan

Source of Real estate funding :

- Two major instruments of real estate financing are mortgage loans/ mortgages and real estate leases.

- Mortgages are instruments that conveys real estate as security for debt. - The debt is evidenced by a promissory note or bond representing a

personal promise to repay.

- A lease conveys to the ‘lessee’ (tenant) the right to possess and use another’s property for a period of time. During this time, the ‘lessor’ (land lord or fee owner) possesses a ‘reversion’ that entitles him to retake

possession at the end of the lease period. - Apart from own resources, there are a host of financial institutions

engaged in real-estate funding. In fact, the Govt itself is an important source of real estate finance. In Indian context, the sources of finance include state housing boards, loans from employers, loans from co-op

housing societies, HDFC, housing schemes of banks, LIC - There are a host of informal mortgage lenders called ‘financiers’ who are

also engaged in real estate counseling and finance. Financing cost escalation :

- Cost escalation results in the increase in project cost for many reasons

viz., delay in implementation of project and inflationary pressure on

corporate purchasing are the main reasons for cost escalation.

- Financing cost escalation will depend upon the corporate arrangements as to how the project cost has originally been financed. There may be

two different aspects to treat the financing of cost escalation as discussed below :

(1) Firstly, financing cost escalation in the case when the project is new and financed by owner fund only. In such cases, the raising of equity is costly but issue of right shares to existing shareholder could be

planned and this cost be met out. There may be another situation when the company is existing company and project cost is being financed by its internal funds. In this case, the company can use its

reserves and surplus in financing cost escalation. (2) In second situation, where the company has been using borrowed

sums in addition to equity capital for financing the project cost, it can always make request for additional funds to the lending institutions to meet the cost escalation or over runs in the project cost. In case the

cost escalation is of greater magnitude then the company will have to go to raise funds from equity holders besides raising loans from the

institutions so as to maintain the debt equity ratio in the existing balanced and planned proportions.

CAPITAL STRUCTURE CHAPTER III

MEANING:

- Capital structure of a firm is a reflection of the overall investment and financing strategy of the firm.

- Capital structure can be of various kinds as described below:

Horizontal capital structure: the firm has zero debt

component in the structure mix. Expansion of the firm takes through equity or retained earnings only.

Vertical capital structure: the base of the structure is formed by a small amount of equity share capital. This

base serves as the foundation on which the super structure of preference share capital and debt is built.

Pyramid shaped capital structure: this has a large proportion consisting of equity capital and retained

earnings.

Inverted pyramid shaped capital structure: this has a

small component of equity capital, reasonable level of retained earnings but an ever-increasing component of debt.

SIGNIFICANCE OF CAPITAL STRUCTURE:

- Reflects the firm’s strategy - Indicator of the risk profile of the firm

- Acts as a tax management tool - Helps to brighten the image of the firm.

FACTORS INFLUENCING CAPITAL STRUCTURE:

- Corporate strategy - Nature of the industry

- Current and past capital structure

CAPITAL STR.

- It relates to long-term capital deployment for creation of long-term assets.

- It is the core element of the

financial structure. It can exist without the current liabilities and in such cases

FINANCIAL STR

- involves creation of both long term and short term assets

- CS shall be equal to the

financial structure

- The components of the

Capital structure may be used to build up the level of current assets but the

current liabilities should not be used to finance acquisition of fixed assets.

- FS of a firm is considered to

be a balanced one if the amount of current liabilities is less than the capital

structure net outside debt because in such cases the long-term capital is

considered sufficient to pay current liabilities in case of

sudden loss of current assets.

PLANNING AND DESIGNING OF CAPITAL STRUCTURE:

- Attributes of a well planned capital structure - Designing a capital structure

- Design should be functional - Design should be flexible - Design should be confirming statutory guidelines

DETERMINANTS OF CAPITAL STRUCTURE:

- Minimization of risk

- Maximization of profit - Nature of the project

- Control of the firm

COST OF CAPITAL:

Factors determining cost of capital:

- General economic conditions: fluctuations in interest rates occur as a result of changes in the demand supply equilibrium of ingestible

funds.

- Risk profile of the project: a project considered risky would attract capital at a higher cost than a project in the same industry having

lesser risk.

COST OF DEBT:

- Concerned essentially with the long-term debt of the firm. - The long-term debt has been used to finance long-term projects.

- We denote cost of debt by the symbol k (d). It is calculated in different ways depending upon whether the debt is a rolling or a term debt redeemable at the expiry of the term.

COST OF PREFERENCE SHARE CAPITAL:

- The preference dividend is equal to the interest payment and

redemption of preference capital is equivalent to redemption of debt.

- Its inclusion in the share capital component is primarily done to bring

down the borrowings of the firm in the balance sheet.

- Cost of preference share capital is arrived at by equating the aggregate of present value of the periodic dividend payments and the redemption amount.

LEVERAGE ANALYSIS

The term “Leverage” in general refers to a relationship between two interrelated

variables In Financial analysis it represents the influence of one financial variable over

some other related financial variable Leverage is used by business firms to quantify the risk-return relationship by

different alternative capital structures.

The operating profits i.e. Earnings before Interest and taxes depends upon Investment Decisions of the firm. Irrespective of the level of EBIT or change therein, a fixed amount of interest must be paid to the debt investors.

Consequently, the residual profit (which is available to equity investors) also

varies in response to change in EBIT. The relationship between change in operating profits and earning for shareholders is known as leverage analysis.

These types of leverages can be ascertained as follows :

Operating leverage

It is defined as the firm’s ability to use fixed operating costs to magnify effects of changes in sales on its EBIT.

It may be defined as the employment of a asset with a fixed cost in the

hope that sufficient revenue will be generated to cover all the fixed and variable costs.

The use of assets for which a company pays a fixed cost is called operating leverage.

A change in sales will lead to a change in profit i.e. EBIT. However,

variable costs will change in proportion to sales while fixed costs will remain constant.

Hence a change in sales will lead to a more than proportional change in EBIT. The effect of change in sales on EBIT is measured by OL.

When Sales increases, Fixed Costs will remain the same irrespective of

the level of output, and so, the percentage increase in EBIT will be higher than increase in sales. This is the favourable effect of OL.

Operating leverage is the ratio of net operating income before fixed

charges to net operating income after fixed charges. Degree of OL is equal to the percentage increase in the net operating

income to the percentage increase in the output.

OL is a function of three factors :

(i) Rupee amount of fixed cost (ii) Variable contribution margin (iii) Volume of sales

Operating leverage = % change in EBIT

---------------- % change in sales

Or

Contribution / EBIT

The OL studies effect of change in sales on EBIT of the firm.

Financial leverage :

FL is defined as the ability of a firm to use fixed financial charges

(interest) to magnify the effect of changes in EBIT, on the firm’s EPS.

FL is defined as the use of funds with a fixed cost in order to increase EPS.

FL occurs when a company has debt content in its capital structure and fixed financial charges. These fixed charges do not vary with EBIT. They

are fixed and are to be paid irrespective of level of EBIT. When EBIT increases, the interest payable on debt remains constant and

hence residual income available to equity shareholders will also increase

more than proportionately. Hence, an increase in EBIT will lead to a higher percentage increase in

EPS. This is measured by FL.

Degree of FL is the ratio of the percentage increase in EPS to the percentage increase in EBIT.

Financial leverage = % change in EPS

-------------------

% change in EBIT OR

EBIT / PBT OR EBIT

----- PBT – PD / (1-t)

The FL studies the effect of change in EBIT on EPS of the firm.

Combined Leverage :

It is used to measure the total risk of the firm i.e. operating risk and

financial risk. It is defined as the potential use of fixed costs, both operating and

financial, which magnifies the effect of sales volume change on the EPS

of the firm. Effect of fixed operating costs is measured by OL. Effect of fixed interest

charges is measured by FL. Combined effect of these is measured by Combined leverage.

Degree of combined leverage is ratio of percentage change in EPS to the

percentage change in sales. It indicates the effect of change in sales on EPS.

Combined leverage = % change EBIT x% change in EPS = % change in EPS % change in sales % change in EB IT % change in sales

OR C x EBIT C ----- ------ ----

EBIT PBT PBT

OR OL x FL

EBIT – EPS analysis

Capital structure can also be analyzed with reference to the effect of financing pattern on the return available to the shareholders. The financing pattern will affect the apportionment of EBIT over different suppliers of funds and in

particular affect the return to the equity shareholders. This is due to the fact that different combinations of debt, preference capital and equity capital have different tax implications. Given a level of EBIT, a particular combination of

different sources will have a particular EPS and for different financing patterns there will be different EPS.

FINANCIAL BREAK EVEN LEVEL

A financial breakeven level is that level of EBIT at which the EPS is zero. If the EBIT reduces below this level, the EPS would be negative.

Financial break even of EBIT = Interest + Pref Div / (1 – t)

Indifference level Indifference level of EBIT is one at which the EPS under two different debt

equity mix is same. In other words, an indifference level of EBIT is such level of EBIT terms. The indifference level of EBIT can be ascertained either

graphically or with the help of finding the value of EBIT in any of the following equations :

(EBIT – Int.1) x (1 – t) – PD.1 (EBIT – Int.2) x (1 – t) – PD.2 ----------------------------------- = -----------------------------------

N.1 N.2

POINTS TO REMEMBER

- The total funds needed by the firm depend upon the investment

decisions of the firm. However, the next step is to determine the best mix of different sources of funds. The process that leads to the choice of capital mix is referred to as capital structure planning.

- There are different techniques of analysing the risk return characteristics of different alternative capital structure. The leverage analysis and EBIT-

EPS analysis are two such techniques.

- In leverage analysis, the relationship between two inter-related variables is established. In FM, there are two types of leverages calculated. These

are OL & FL. A CL may also be calculated.

- The OL establishes the relationship between sales and EBIT. It measures the effect of change in sales revenue on the level of EBIT. OL

appears as a result of fixed cost. If there is no fixed cost, there will be no OL.

- The FL measures the responsiveness of the EPS for a given change in

EBIT. The FL appears as a result of fixed financial charge i.e interest and preference dividend.

- CL may also be ascertained to measure the % change in EPS for a % change in the sales.

- EBIT-EPS Analysis is another way of looking at the effects of different

types of capital structures. EBIT-EPS analysis considers the effect on EPS of different types of capital mix.

- Given a level of EBIT, a particular combination of different sources (i.e.

Debt, Pref share capital and equity share capital) will result in a particular level of EPS, and therefore, for different financing patterns, there would be different levels of EPS.

- For a given level of EBIT, higher the degree of financial leverage, i.e. higher the level of debt financing, greater would be the EPS (provided ROI is more than cost of debt). However, if the ROI is less than cost of debt,

then the effect of increase in leverage of EPS would be negative.

- Financial breakeven level of EBIT is that level of EBIT at which the EPS

of the firms is zero.

- Indifference level of EBIT is one at which the EPS remains same under two different financial plans. At the indifference level of EBIT, the firm

would be indifferent whether the funds are raised by one capital mix or another because both will have same level of EPS.

- Indifference level of EBIT may be ascertained graphically or with the help

of mathematical formulation.

DIVIDEND POLICY CHAPTER V

THE POLICY:

- This determines what portion of earnings will be paid out to stockholders and what will be retained in the business to finance long-term growth.

- Dividend constitutes the cash flow that accrues to equity holders whereas retained earnings are one of the most significant sources of

funds for financing the corporate growth.

FORMS OF DIVIDEND:

- The most common type of dividend is in the form of cash

- Public companies usually pay cash dividend, sometimes a regular cash dividend and sometimes an extra cash dividend

- Paying a cash dividend reduces the corporate cash and retained

earnings. - It is also paid in the form of shares of stock and this is referred as

stock dividend or bonus shares.

STABLE DIVIDEND POLICY THEORY:

The stability could take three forms:

- Keep dividends at a stable rupee amount but allow its payout

ratio to fluctuate, or

- Maintain stable payout ratio and let the rupee dividend fluctuate, or

- Set low regular dividend and then supplement it with year-end

“extras” in years when earnings are high. As earnings of the firm increase the customary dividend will not be altered but a year-end “extras” will be declared.

RESIDUAL THEORY OF DIVIDEND POLICY:

- Dividend policy is strictly a financing decision; the payment of cash

dividend is a passive residual.

- The amount of dividend payout will fluctuate from period to period in

keeping with fluctuations in the amount of acceptable investment opportunities available to the firm.

- If the firm is unable to find out profitable investment opportunities, payout will be 100%.

- The theory implies that investors prefer to have the firm retain and reinvest earnings rather than pay them out in dividends if the return

on re-invested earnings exceeds the rate of return the investors could themselves obtain on other investments of comparable risks.

IRRELEVANCE OF DIVIDEND:

- Investors are indifferent to dividends and capital gains and so

dividends have no effect on the wealth of shareholders.

- They argue that the value of the firm is determined by the earning power of firms assets or its investment policy.

- The manner in which earnings are divided into dividends and retained earnings does not affect this value.

DETERMINANTS OF DIVIDEND POLICY:

- Legal: dividends must be paid out of firm’s earnings/ current earnings

- Financial: a firm can pay dividend only to the extent that it has cash to disburse

- Economic constraints

- Nature of business conducted by a company

- Existence of the company: length of existence of the company.

- Type of company Organisation: pvt. Or public

- Financial needs of the company.

- Market conditions

- Financial arrangements

- Change in government policies

LEGAL ASPECTS OF DIVIDENDS:

1. Dividends to be paid only out of profits:

- It is necessary for a company to declare and pay dividend only out of

profits for that year arrived at after providing for depreciation in accordance with the provisions of section 205(2) of the Companies

Act.

- A dividend could be declared out of profits of the company for any

previous financial year or years arrived after providing for depreciation in accordance with those provisions and remaining undistributed.

- The dividend can also be declared out of moneys provided by the central govt. or a state govt. for the payment of dividend in pursuance

of guarantee given by that govt.

- The company is required to transfer to the reserves such percentage

of its profits for that year not exceeding 10% in addition to providing for depreciation as required under section 205(2A) of the Companies Act.

2. Unpaid dividend to be transferred to special dividend account:

- Dividends are to be paid within 30 days from the date of the declaration

- If they are not paid the company is required to transfer the unpaid dividend to unpaid account within 7 days of the expiry of the period of

30 days.

- The company is required to open this account in any scheduled bank

as required under section 205-A of the Companies Act, 1956

3. Dividend is to be paid only to registered shareholders or to their order or their bankers

TRANSFER OF UNPAID/UNCLAIMED DIVIDEND TO INVESTOR EDUCATION AND PROTECTION FUND:

1. Any money transferred to the unpaid dividend account of a company in pursuance of section 205A(5) which remains unpaid or unclaimed for a

period of 7 years from the date of such transfer to unpaid dividend account, shall be transferred by the company to the investor education and protection fund established under sub-section (1) of section 205C

2. Sub-section (1A) of section 205 stipulates that the board of directors may declare interim dividend and the amount of dividend including interim

dividend is to be such deposited in a separate bank account within 5 days from the date of declaration.

3. Failure to do so, every director of the company, shall, if knowingly a

party to the default, be punishable with simple imprisonment for a term which may extend to 3 years and shall also liable to a fine of rupees for everyday during which such default continues and

4. The company shall be liable to pay simple interest at a rate of 18% p.a. during the period for which such default continues.

WORKING CAPITAL MANAGEMENT AND CONTROL CHAPTER VI

BASIC CONCEPTS AND FORMULAE

1. Working Capital Management

a. Working Capital Management involves managing the balance between

firm’s short term assets and its short-term liabilities. b. From the value point of view, Working Capital can be defined as:

i. Gross Working Capital: It refers to the firm’s investment in current assets.

ii. Net Working Capital: It refers to the difference between current

assets and current liabilities. c. From the point of view of time, working capital can be divided into:

i. Permanent Working Capital: It is that minimum level of investment in the current assets that is carried by the business at all times to carry out minimum level of its activities.

ii. Temporary Working Capital: It refers to that part of total working capital, which is required by a business over and above permanent working capital.

2. Factors To Be Considered While Planning For Working Capital Requirement

Nature of business

Market conditions

Demand conditions

Operating efficiency

Credit policy

3. Finance manager has to pay particular attention to the levels of current assets and their financing. To decide the levels and financing of current

assets, the risk return trade off must be taken into account. In determining the optimum level of current assets, the firm should balance the profitability – Solvency tangle by minimizing total costs.

4. Working Capital Cycle Working Capital Cycle indicates the length of time between a company’s paying for materials, entering into stock and receiving the cash from sales of

finished goods. It can be determined by adding the number of days required for each stage in the cycle.

5. Computation of Operating Cycle a. Operating Cycle = R + W + F + D – C Where,

R = Raw material storage period W = Work-in-progress holding period

F = Finished goods storage period D = Debtors collection period. C = Credit period availed.

The various components of operating cycle may be calculated as shown below:

Average cost of rawmaterial consumption per day Raw material storage period Average stock of raw material

Work - in- progress holdingperiod Average cost of production per day

Average work - in - progress inventory

Average cost of goods soldper day

Finished goods storage period Average stock of finished goods

Average Credit Sales per day

Debtors collection period Average book debts

Average credit purchases per day Credit period availed Average trade creditors 6. Treasury Management

Treasury management is defined as ‘the corporate handling of all financial matters, the

generation of external and internal funds for business, the management of currencies and cash flows and the complex, strategies, policies and procedures of corporate

finance”. 7. Management of Cash It involves efficient cash collection process and managing payment of cash both

inside the organisation and to third parties.

Financial Management 7.3 The main objectives of cash management for a business are:-

i. Provide adequate cash to each of its units; ii. No funds are blocked in idle cash; and

iii. The surplus cash (if any) should be invested in order to maximize returns for the business.

8. Cash Budget Cash Budget is the most significant device to plan for and control cash receipts and

payments. This represents cash requirements of business during the budget period. The

various purposes of cash budgets are: i. Coordinate the timings of cash needs. It identifies the period(s) when there might

either be shortage of cash or an abnormally large cash requirement; ii. It also helps to pinpoint period(s) when there is likely to be excess cash;

iii. It enables firm which has sufficient cash to take advantage like cash discounts on its

accounts payable; iv. Lastly it helps to plan/arrange adequately needed funds (avoiding

excess/shortage of cash) on favorable terms. 9. Preparation of Cash Budget

The Cash Budget can be prepared for short period or for long period. Cash budget for short period: Preparation of cash budget month by month would

require the following estimates: (a) As regards receipts:

Receipts from debtors; Cash Sales; and Any other source of receipts of cash (say, dividend from a subsidiary

company) (b) As regards payments:

Payments to be made for purchases; Payments to be made for expenses; Payments that are made periodically but not every month;

(i) Debenture interest; (ii) Income tax paid in advance;

(iii) Sales tax etc. Management of Working Capital 7.4

Special payments to be made in a particular month, for example, dividends to shareholders, redemption of debentures, repayments of loan, payment of

assets acquired, etc. Cash Budget for long period: Long-range cash forecast often resemble the projected

sources and application of funds statement. The following procedure may be adopted to prepare long-range cash forecasts:

(i) Take the cash at bank and in the beginning of the year: (ii) Add: (a) Trading profit (before tax) expected to be earned; (b) Depreciation and other development expenses incurred to be written off; (c) Sale proceeds of assets’;

(d) Proceeds of fresh issue of shares or debentures; and (e) Reduction in working capital that is current assets (except cash) less

current liabilities. (iii) Deduct:

(a) Dividends to be paid. (b) Cost of assets to be purchased.

(c) Taxes to be paid.

(d) Debentures or shares to be redeemed. (e) Increase in working capital.

10. Cash Management Models William J. Baumol’s Economic Order Quantity Model, (1952): According to

this model, optimum cash level is that level of cash where the carrying costs and transactions costs

are the minimum. The formula for determining optimum cash balance is: S

C 2U P

Miller-Orr Cash Management Model (1966): According to this model the net cash flow is completely stochastic.

When changes in cash balance occur randomly the application of control theory serves a

useful purpose. The Miller-Orr model is one of such control limit models. Financial Management 7.5

11. Management of Marketable Securities Management of marketable securities is an integral part of investment of cash as this may

serve both the purposes of liquidity and cash, provided choice of investment is made

correctly. As the working capital needs are fluctuating, it is possible to park excess funds in some short term securities, which can be liquidated when need for cash is

felt. The selection of securities should be guided by three principles.

Safety: Return and risks go hand in hand. As the objective in this

investment is ensuring liquidity, minimum risk is the criterion of selection.

Maturity: Matching of maturity and forecasted cash needs is essential. Prices of

long term securities fluctuate more with changes in interest rates and are therefore, more risky.

Marketability: It refers to the convenience, speed and cost at which a

security can be converted into cash. If the security can be sold quickly without loss of

time and price it is highly liquid or marketable. 12. Inventory Management Inventory management covers a large number of problems including fixation of

minimum and maximum levels, determining the size of inventory to be carried, deciding

about the

issues, receipts and inspection procedures, determining the economic order quantity,

proper storage facilities, keeping check over obsolescence and ensuring control over

movement of inventories. 13. Management of Receivables

The basic objective of management of sundry debtors is to optimise the

return on investment on these assets known as receivables.

Large amounts are tied up in sundry debtors, there are chances of bad

debts and there will be cost of collection of debts. On the contrary, if the investment in

sundry debtors is low, the sales may be restricted, since the competitors may offer more

liberal terms. Therefore, management of sundry debtors is an important issue and

requires proper policies and their implementation. There are basically three aspects of management of sundry debtors:

(i) Credit policy: The credit policy is to be determined. It involves a trade off

between the profits on additional sales that arise due to credit being extended on the one hand and the cost of carrying those debtors and bad debt losses on the other. This seeks to decide credit period, cash discount and other relevant

matters. (ii) Credit Analysis: This requires the finance manager to determine as to how

risky it is to advance credit to a particular party. (iii) Control of Receivables: This requires finance manager to follow up debtors

Management of Working Capital 7.6 and decide about a suitable credit collection policy. It involves both laying

down of credit policies and execution of such policies.

Important Sources of Financing of Receivables (i) Pledging: This refers to the use of a firm’s receivable to secure a short term loan.

(ii) Factoring: In factoring, accounts receivables are generally sold to a financial

institution (a subsidiary of commercial bank-called “Factor”), who charges commission and bears the credit risks associated with the accounts receivables purchased by it.

14. Management of Payables Management of Payables involves management of creditors and suppliers. Trade creditor is a spontaneous source of finance in the sense that it arises

from

ordinary business transaction. But it is also important to look after your creditors -

slow payment by you may create ill-feeling and your supplies could be disrupted and

also create a bad image for your company. Creditors are a vital part of effective cash management and should be

managed

carefully to enhance the cash position. 15. Financing of Working Capital

It is advisable that the finance manager bifurcates the working capital

requirements between permanent working capital and temporary working capital.

The permanent working capital is always needed irrespective of sales fluctuations, hence should be financed by the long-term sources such as debt and equity.

On the contrary, temporary working capital may be financed by the short-term sources

of finance.

Broadly speaking, the working capital finance may be classified between the

two categories: (i) Spontaneous Sources: Spontaneous sources of finance are those which

naturally arise in the course of business operations. Trade credit, credit from employees, credit from suppliers of services, etc. are some of the examples

which may be quoted in this respect. (ii) Negotiable Sources: On the other hand the negotiated sources, as the name

implies, are those which have to be specifically negotiated with lenders say, commercial banks, financial institutions, general public etc. Financial Management

7.7 UNIT – I : MEANING, CONCEPT AND POLICIES OF WORKING CAPITAL

Question 1 Discuss the factors to be taken into consideration while determining the requirement of working capital. (November 2008) Answer

Factors to be taken into consideration while determining the requirement of working capital: (i) Production Policies (ii) Nature of the business

(iii) Credit policy (iv) Inventory policy (v) Abnormal factors (vi) Market conditions (vii) Conditions of supply (viii) Business cycle

(ix) Growth and expansion (x) Level of taxes (xi) Dividend policy (xii) Price level changes

(xiii) Operating efficiency. Question 2

Discuss the liquidity vs. profitability issue in management of working capital. (November 2010) Answer Liquidity versus Profitability Issue in Management of Working Capital Working capital management entails the control and monitoring of all

components of working capital i.e. cash, marketable securities, debtors, creditors etc. Finance manager has to pay

particular attention to the levels of current assets and their financing. To decide the level of

financing of current assets, the risk return trade off must be taken into account. The level of current assets can be measured by creating a relationship between current assets and

fixed assets. A firm may follow a conservative, aggressive or moderate policy.

Management of Working Capital 7.8 A conservative policy means lower return and risk while an aggressive policy

produces higher return and risk. The two important aims of the working capital management are profitability and

solvency. A liquid firm has less risk of insolvency i.e. it will hardly experience a cash shortage or a

stock out situation. However, there is a cost associated with maintaining a sound liquidity position. So, to have a higher profitability the firm may have to sacrifice solvency and

maintain a relatively low level of current assets. Question 3

Discuss the estimation of working capital need based on operating cycle process. (November 2010) Answer Estimation of Working Capital Need based on Operating Cycle One of the methods for forecasting working capital requirement is based on the

concept of operating cycle. The determination of operating capital cycle helps in the

forecast, control and management of working capital. The length of operating cycle is the indicator of performance of

management. The net operating cycle represents the time interval for which the firm has to negotiate for Working Capital from its Bankers. It enables to determine

accurately the amount of

working capital needed for the continuous operation of business activities. The duration of working

capital cycle may vary depending on the nature of the business. In the form of an equation, the operating cycle process can be expressed as

follows: Operating Cycle = R + W + F +D – C Where,

R = Raw material storage period. W = Work-in-progress holding period. F = Finished goods storage period.

D = Debtors collection period. C = Credit period availed.

Question 1

Explain briefly the functions of Treasury Department. (May 2008; June 2009; November 2002) Answer The functions of treasury department management is to ensure proper usage, storage and risk

management of liquid funds so as to ensure that the organisation is able to meet its obligations, collect its receivables and also maximize the return on its investments.

Towards this end the treasury function may be divided into the following:

Management of Working Capital 7.34

(i) Cash Management: The efficient collection and payment of cash both inside the organization and to third parties is the function of treasury department.

Treasury normally manages surplus funds in an investment portfolio.

(ii) Currency Management: The treasury department manages the foreign currency risk exposure of the company. It advises on the currency to be used when invoicing

overseas sales. It also manages any net exchange exposures in accordance with the

company policy. (iii) Fund Management: Treasury department is responsible for planning and sourcing the

company’s short, medium and long-term cash needs. It also participates in the decision on capital structure and forecasts future interest and foreign currency rates.

(iv) Banking: Since short-term finance can come in the form of bank loans or through the

sale of commercial paper in the money market, therefore, treasury department carries out

negotiations with bankers and acts as the initial point of contact with them. (v) Corporate Finance: Treasury department is involved with both acquisition

and disinvestment activities within the group. In addition, it is often responsible for investor relations.

Question 2 Explain Baumol’s Model of Cash Management. (May 2008) Answer

William J. Baumol developed a model for optimum cash balance which is normally used in

inventory management. The optimum cash balance is the trade-off between cost of holding cash (opportunity cost of cash held) and the transaction cost (i.e. cost of converting

marketable securities in to cash). Optimum cash balance is reached at a point where the

two opposing costs are equal and where the total cost is minimum. This can be explained with the following diagram:

Transaction Cost Holding Cost Cost

(Rs.) Total Cost

Optimum Cash Balance Financial Management 7.35

The optimum cash balance can also be computed algebraically. Optimum Cash Balance = H

2 AT A = Annual Cash disbursements

T = Transaction cost (Fixed cost) per transaction H = Opportunity cost one rupee per annum (Holding cost) The model is based on the following assumptions:

(i) Cash needs of the firm are known with certainty. (ii) The cash is used uniformly over a period of time and it is also known with

certainty. (iii) The holding cost is known and it is constant. (iv) The transaction cost also remains constant.

Question 3 Explain with example the formula used for determining optimum cash balance according to Baumal’s cash management model. (November 2009) Answer

Formula for Determining Optimum Cash Balance according to Baumol’s Model

C = S

2UP Where, C = Optimum cash balance

U = Annual cash disbursement P = Fixed cost per transaction S = Opportunity cost of one rupee p.a.

Example A firm maintains a separate account for cash disbursement. Total

disbursements are Rs.1,05,000 per month or Rs.12,60,000 per year. An Administrative and transaction cost of transferring cash to

disbursement account is Rs. 20 per transfer. Marketable securities yield is 8% per annum.

Determine the optimum cash balance according to William J. Baumol model. Solution The optimum cash balance C = Rs. 25,100

0.08 2 Rs.12,60,000 Rs.20 Management of Working Capital

7.36 Question 5

Write short note on Different kinds of float with reference to management of cash. (May 1998 & 1999) Answer

Different Kinds of Float with Reference to Management of Cash: The term float is used to refer to the periods that affect cash as it moves through the different stages of the

collection process. Four kinds of float can be identified:

(i) Billing Float: An invoice is the formal document that a seller prepares and sends to the purchaser as the payment request for goods sold or services provided. The time

between the sale and the mailing of the invoice is the billing float.

(ii) Mail Float: This is the time when a cheque is being processed by post office, messenger

service or other means of delivery. (iii) Cheque processing float: This is the time required for the seller to sort, record and

deposit the cheque after it has been received by the company. (iv) Bank processing float: This is the time from the deposit of the cheque to the

crediting of

funds in the seller’s account. Question 6

Write short note on William J. Baumal vs. Miller-Orr Cash Management Model. (May 2004) Answer William J Baumal vs Miller- Orr Cash Management Model: According to William J Baumal’s

Economic order quantity model optimum cash level is that level of cash where the carrying costs and transactions costs are the minimum. The carrying costs refer to the cost of

holding cash, namely, the interest foregone on marketable securities. The transaction costs

refers to the cost involved in getting the marketable securities converted into cash. This happens when the firm falls

short of cash and has to sell the securities resulting in clerical, brokerage, registration and other

costs. The optimim cash balance according to this model will be that point where these two costs are

equal. The formula for determining optimum cash balance is : Management of Working Capital 7.38

C = S

2 U P , Where, C = Optimum cash balance

U = Annual (monthly) cash disbursements P = Fixed cost per transaction S = Opportunity cost of one rupee p.a. (or p.m)

Miller-Orr cash management model is a net cash flow stochastic model. This model is designed to

determine the time and size of transfers between an investment account and cash account. In this model control limits are set for cash balances. These limits may consist of h as

upper limit, z as the return point, and zero as the lower limit.

When the cash balances reach the upper limit, the transfer of cash equal to h-z is invested in marketable securities account. When it touches the lower limit, a transfer from

marketable securities account to cash account is made. During the period when cash balance stays between

(h,z) and (z, o ) i.e high and low limits no transactions between cash and marketable securities

account is made. The high and low limits of cash balance are set up on the basis of fixed cost

associated with the securities transactions, the opportunity cost of holding cash and the degree of

likely fluctuations in cash balances. These limits satisfy the demands for cash at the lowest possible total costs.

Question 7 Describe the three principles relating to selection of marketable securities. (November 2009) Answer Three Principles Relating to Selection of Marketable Securities

The three principles relating to selection of marketable securities are: (i) Safety: Return and risk go hand-in-hand. As the objective in this

investment is ensuring

liquidity, minimum risk is the criterion of selection. (ii) Maturity: Matching of maturity and forecasted cash needs is essential.

Prices of longterm securities fluctuate more with changes in interest rates and are, therefore, riskier. (iii) Marketability: It refers to the convenience, speed and cost at which a

security can be converted into cash. If the security can be sold quickly without loss of time and

price, it is highly liquid or marketable.

FINANCIAL SERVICES CHAPTER VIII

MONEY MARKET CONCEPT OF MONEY MARKET

1. It is the market for dealing in monetary assets of short term nature (one

year) 2. Financial assets which are equivalent to money having characteristics of

liquidity, minimum transaction cost and no loss in value

3. Money market enables the raising of short term funds for meeting temporary shortages of cash & obligation and temporary deployment of

excess funds for returns 4. The major constituents are Banks, Financial Institutions, Large

corporations & RBI.

5. The instruments dealt in are Treasury bills, commercial bills, certificate of deposits, commercial paper etc.,

FEATURES OF MONEY MARKET

1. Deals with raising and deploying short term funds 2. Provides institutional source for providing working capital 3. Operates as a wholesale market and has sub-markets – call market, bill

market, treasury bills market, commercial paper market, certificate of deposits market etc.,

4. Volume of transactions is very large 5. Transactions are on telephone etc., later confirmed 6. Same day settlement basis

7. Highly liquid, safety 8. Large size instruments (Rs.1 lacs for bills, Rs.25 lacs for Commercial

deposit & commercial paper).

OBJECTIVES OF MONEY MARKET

1. To provide balancing mechanism for short term surplus and deficiencies 2. To provide liquidity in the economy

3. To provide reasonable access to users of short term funds at reasonable price/cost

DIFFERENCE BETWEEN MONEY MARKET VS. CAPITAL MARKET

MONEY MARKET CAPITAL MARKET

- It deals with raising and deployment of funds for short term

- Deals with long term financing

- Provides the instruction source for providing working capital

- long term capital for financing fixed assets

- Operates as a wholesaler

market and has number of inter-related sub-markets, FI etc are main players:

– regulate money supply – Statutory lending ratio(SLR), -Cash reserve ratio (CRR)

– liquidity etc.

- Equity/debt market regulated

by SEBI Capital appreciation

STRUCTURE OF INDIAN MONEY MARKET

- The Indian money market consists both organised & unorganised segments

- The unorganized sector consists of – indigenous bankers, money

lenders, chit funds etc, where interest rates are higher.

- The organised sector consists of - RBI, SBI, Public Sector banks, Private sector banks, Foreign banks, Regional Rural Banks, Non-Scheduled

banks, Non Banking Financial corporations, LIC, GIC, UTI etc., MONEY MARKET INSTRUMENTS

1. GOVT SECURITIES:

a) Dated Securities : Fixed maturity instruments with pre-decided coupon rate payable semi annually. Issued at par with fixed tenure (issued at face value, redeemable at par)

b) Zero Coupon bonds : Issued at discount and are redeemed at par, after a fixed tenure. The difference between issue price and redemption is interest

c) Partly paid stocks : Repayment in instalments over the fixed tenure (issued at face value coupons issued).

d) Floating rate bonds : Interest rate is linked to a bench mark index. Fixed tenure, Interest rate changes based on the movement in bench mark index(bank rate).

e) Bonds with call put option : option is exercisable after a fixed period. Holder can sell/buy back the bond to/from Government of India.

f) Capital Indexed Bonds : These are fixed tenure instruments where

the interest & principal are fixed as %age of wholesale price index.

ADVANTAGES OF GOVT SECURITIES

- Zero default risk - No Tax deduction at source on interest

- Low volatility - Qualifies for SLR - Highly liquid

METHODS OF ISSUANCE OF G.SECURITIES

- Auctions

- On tap issue

- Fixed coupon issue (carrying fixed rate)

- Private placement

- Open market operations

2. TREASURY BILLS( T-BILLS)

a. Shorter rupee denominated obligation issued by RBI on behalf of GOI. These instruments have sovereign rating and issue with a minimum

denomination of Rs.10000 and in multiple of Rs.10000. The transaction size will be 50 to 100 million. T-bills are issued 14 /91/ 182/ 364 days.

Recently 14 /182 days T-bills have been discontinued.

b. It is a discounted instrument issued in the form of zero coupon instruments at discount face value and redeemable at par. The amount

on repayment is credited to current account of the investor held with RBI.

c. They form part of SLR investments and used for short term liquidity.

d. No tax impact, zero default risk, liquidity, simple settlement.

Futures of T-bills

a) Bids are made for a minimum of Rs.25,000 and multiple thereof. b) Instruments are paid at par on maturity c) Available both in primary and secondary market

3. Call money / notice money / term money /fixed deposit

a) It is an amount borrowed or lent for a short period. b) If the period is more than 1 day and into 14 days it is called notice

money, Otherwise it is called call money c) Money lend for 15 days to one year is called term money or fixed

deposit

d) Sundays and holidays are excluded e) No collateral security

f) Interest is payable on maturity g) No brokers in the call money market

h) Trading is done Over the Counter (OTC) i) Settlement is done between participants through current account with

RBI

4. REPOSE / REVERSE REPOSE

- It is a transaction in which two parties agree to sell and re-purchase the same security.

- Under the agreement the seller sells specified securities for re-purchase the same at mutually decided future date and price

- The buyer purchases with an agreement to resell the same to the seller

on an agreed date at pre-determined price

- Such transactions are called repo when viewed from the sellers point of view and reverse repo when viewed from buyers perspective.

- Repo /reverse repo are used to meet shortfall in cash positions, to augment returns on funds held and to borrow securities to meet

regulatory requirement

- An SLR surplus bank and CRR deficit bank can use the repo deals for adjusting CRR / SLR positions

- RBI uses repo / reverse repo for adjusting liquidity in the system.

- The securities eligible for trading are Govt Sec, T-bills, PSU bonds,FI bonds, corporate bonds etc.,

- Repo transactions are done in the market lots of Rs.5 crores 5. CERTIFICATE OF DEPOSITS (CDs)

- CD are rupee denominated secure promissory notes, freely transferable on endorsement & delivery

- Comml Banks / FI can issue CDs

- CDs are not required to be rated

- They are issued at a discount at face value and are redeemable at par on

maturity

- Eligible investors in CDs are banks, corporates, individuals, insurance companies, PF etc.,

- NRI can invest in CD on non-repatriable and non-transferable basis.

- Minimum size of CD is Rs.1 lac

- Used by Banks to maintain reserve requirements (CRR & SLR)

- Maturity period for CDs issued by bank from 15 days to one year, whereas it is one to three years for CDs issued by FI.

6. INTER BANK PARTICIPATION (IBP)

- These instruments are used by banks for 90 days only

- The issuing banks show participation as borrowing, while participating banks show it has advances to Banks

- It is more flexible, but it is not transferable

- No provision for pre-matured redemption

7. MONEY MARKET MUTUAL FUNDS (MMMFs)

- MMMFs invest money in money market instruments

- They are regulated by SEBI and follow the guidelines as are applicable to

any other fund 8. COMMERCIAL BILLS

- CB are negotiable instruments accepted by buyers for goods or services obtained by them on credit

- Such bill of exchange can be kept upto the due date and encashed by the seller or may be endorsed to third party

- The seller who gets the bills of exchange discounts it with Banks or FI or

bill discounting house and collects the money.

9. COMMERCIAL PAPER (CP)

- CP is a rupee denominated, short term, unsecured, negotiable promissory notes with a fixed maturity issued by well rated companies. It is sold on a discount basis

CPs are issued by corporate or as an alternate source of working capital CPs are issued at a discount to face value and are redeemable at par on

maturity Eligible investors in CPs are individuals, corporates, insurance companies and banks.

NRI can invest in CP on repatriable non-transferable basis. Banks & Companies are the common investors. CPs are subjected to stamp duty (0.25%) and concessional rate of 0.05%

for banks

ISSUER Corporates, Financial Institutions are permitted to issue CPs when networth is more than Rs.4 crores. Banks sanction working capital limit

to companies. Its account is classified as standard by Financial Institutions & banks

CREDIT RATING

- All CPs are to be rated mandatorily. Minimum rating is P2 equivalent

- Corporate issues are rated P1 MATURITY

- Minimum 7 days and maximum one year

DENOMINATION

- Rs.5 lacs or multiples thereof.

- Amount invested by single investor should not be less than Rs.5 lacs face value

ISSUING AND PAYING AGENT

- The issuing & paying agent are scheduled commercial banks.

- Issuer to ensure legal framework for CP issues is complied with.

- Issuing & paying agent will check that the issuer has minimum credit rating, verifies all documents and reports to RBI.

- Any default are reported to RBI.

- Credit rating agencies to abide by Code of Conduct of SEBI and determine the validity period of rating and closely monitor the rating.

10. GILT EDGED SECURITIES

- Govt securities issued by central , state and semi – government

authorities, port trusts, electricity boards, housing boards, Financial institutions etc.,

- GES are issued to meet the short term fund requirement of Government

- Budgeted amount is collected through trenches over the period of the year

- Process of issue and redemption is continuous

- It is not auctioned

- GES are eligible for SLR purpose

- Default risk is negligible as it is backed by the Govt

- The rate of interest is low

- These securities are issued by public debt office of RBI

- Major buyers of GES are banks, insurance companies, PF etc.,

11. BILL RE-DISCOUNTING

- It is a source of temporary finance for banks

12. INTER CORPORATE DEPOSITS (ICD)

- ICD is an unsecured loan extended by one corporate to another.

- This market allows surplus funds of one corporate lends to other companies.

MERCHANT BANKING:

The merchant bankers undertake the following activities:

- Managing of public issue of securities - Underwriting connected with the aforesaid public issue management

business

- Managing/advising on international offerings of debt/equity i.e., GDR, ADR, BONDS and other instruments

- Private placement of securities - Primary or satellite dealership of government securities - Corporate advisory services related to securities market including

takeovers, acquisition and disinvestment - Stock broking - Advisory services for projects

- Syndication of rupee term loans - International financial advisory services

MUTUAL FUNDS:

- These funds are the institutions, which provide small investors with avenues of investment in the capital market.

Advantages:

- Professional management

- Diversification - Convenient administration - Return potential

- Low costs - Liquidity

- Transparency

Types:

Open ended mutual funds:

- Is a fund with a non-fixed number of out standing shares, that stands ready at any time to redeem shares on demand

- The fund itself buys back the shares surrendered and is ready to sell new shares.

- Generally the transaction takes place at the net asset value (NAV) which is calculated on a periodical basis

Close-ended funds:

- It is the fund where mutual fund management sells a limited number of shares and does not stand ready to redeem them.

- The shares of such funds are traded in the secondary markets.

- The requirement for listing is laid down to grant liquidity to the

investors who have invested with the mutual fund.

- These funds are more like equity shares.

VENTURE CAPITAL:

- Is a form of equity financing, which is specially designed for funding high risk and high reward projects

- It is direct investment in securities of new and unseasoned enterprises by way of private placement.

- Is the capital that is invested in equity or debt securities (with equity conversion terms) of young unseasoned companies promoted by

technocrats who attempts to break new path.

- It is a source of finance for new or relatively new, high risk, high profit potential products as the projects belong to untried segments or technologies.

Venture capital generally provides following services:

- Finance new and rapidly growing companies - Typically knowledge-based, sustainable, up scalable companies

- Purchase equity/ quasi-equity securities - Assist in the development of new products or services

- Add value to the company through active participation - Take higher risks with the expectation of higher rewards - Have a long term orientation

Problem areas facing the industry are:

- There is insufficient understanding of venture capital as a commercial activity

- The support to the venture capital industry, by the government is in

inadequate - The exit options available to the venture capitalist are limited

- Market limitations hinder the growth of venture capital; and - The inadequacy of the legal framework for venture capital industry.

LOAN SYNDICATION:

- Arrange/ procure finance on request for the projects that come up for counseling.

- A pre-requisite would require arrangement of funds that would involve,

o Assessing the quantum and nature of funds required