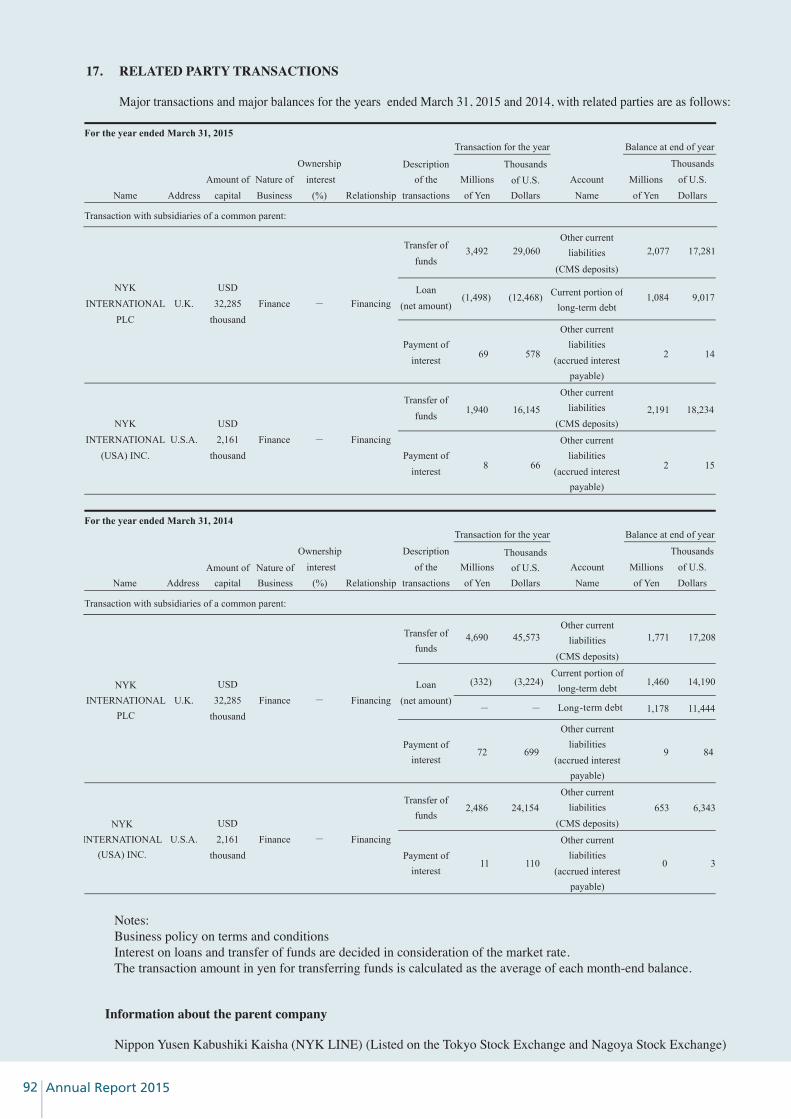

financial data notes to consolidated financial … logistics co., ltd. and consolidated subsidiaries...

TRANSCRIPT

Yusen Logistics Co., Ltd. and Consolidated Subsidiaries

Notes to Consolidated Financial Statements Year Ended March 31, 2015

1. BASIS OF PRESENTING CONSOLIDATED FINANCIAL STATEMENTS

The accompanying consolidated financial statements have been prepared in accordance with the provisions set forth in the Japanese Companies Act and Financial Instruments and Exchange Act and their related accounting regulations and in conformity with accounting principles generally accepted in Japan ("Japanese GAAP"), which are different in certain respects as to application and disclosure requirements of International Financial Reporting Standards.

In preparing these consolidated financial statements, certain reclassifications and rearrangements have been made to the consolidated financial statements issued domestically in order to present them in a form which is more familiar to readers outside Japan. In addition, certain reclassifications have been made in the 2014 financial statements to conform to the classifications used in 2015.

The consolidated financial statements are stated in Japanese yen, the currency of the country in which Yusen Logistics Co., Ltd. (the "Company") is incorporated and operates. The translations of Japanese yen amounts into U.S. dollar amounts are included solely for the convenience of readers outside Japan and have been made at the rate of ¥120.17 to $1, the approximate rate of exchange at March 31, 2015. Such translations should not be construed as representations that the Japanese yen amounts could be converted into U.S. dollars at that or any other rate.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

a. Consolidation—The consolidated financial statements as of March 31, 2015, include the accounts of the Company and its 71 significant (69 in 2014) subsidiaries (together, the "Group") listed below:

Consolidated Subsidiaries

EquityOwnership

Percentage*1 Capital Stock*1

Yusen Logistics (Americas) Inc. 51.00% USD 70,976 thousand Yusen Logistics (Hong Kong) Limited 100.00 HKD 55,000 thousand Yusen Air & Sea Service (China) Ltd. 100.00*2 HKD 11,000 thousand Yusen Logistics (Singapore) Pte.Ltd. 79.30 SGD 16,950 thousand Yusen Logistics (Benelux) B.V. 100.00*3 EUR 50 thousand Yusen Logistics (Deutschland) GmbH 100.00*3 EUR 2,638 thousand Yusen Air & Sea Service (U.K.) Ltd. 100.00*3 GBP 1,050 thousand Yusen Logistics (Australia) Pty.Ltd. 50.97*4 AUD 15,478 thousand Yusen Logistics (Canada) Inc. 100.00 CAD 5,000 thousand Yusen Logistics (France) S.A.S. 100.00*3 EUR 14,185 thousand Yusen Logistics (Taiwan) Ltd. 95.30*5 TWD 157,398 thousand Beijing Yusen Freight Service Co.,Ltd. 100.00*2 CNY 9,312 thousand Yusen Logistics (Italy) S.P.A. 100.00*3 EUR 3,326 thousand PT. Yusen Logistics Indonesia 67.62*6 USD 3,048 thousand Yusen Logistics (Europe) B.V. 53.69 EUR 39,493 thousand Yusen Logistics (Korea) Co.,Ltd. 100.00 KRW � 2,000 million Shanghai Yusen Freight Service Co.,Ltd. 100.00*2 CNY 16,457 thousand Yusen Air & Sea Service Management (Thailand) Co.,Ltd. 95.00*7 THB 10,000 thousand Yusen Logistics International (Vietnam) Co.,Ltd. 49.00*8 USD 600 thousand Yusen Logistics Philippines, Inc. 51.00 PHP 500,000 thousand Guangdong Yusen Freight Service Co.,Ltd. 100.00*2 CNY 8,009 thousand Yusen Logistics (India) Private Limited*26 51.00*9 INR 1,094 million Shanghai Yusen Logistics Service (W.G.Q.) Co.,Ltd. 100.00*2 CNY 5,380 thousand Suzhou Yusen Logistics Service Co.,Ltd. 100.00*2 CNY 6,844 thousand

Notes to Consolidated Financial StatementsFinancial Data

60 Annual Report 2015

Consolidated Subsidiaries

Equity Ownership

Percentage*1 Capital Stock*1

ETA TOO, INC. 100.00*10 USD 0 BRUNI INTERNATIONAL DE MEXICO,

S.A.DE C.V. 100.00*11 MXN 350 thousand Yusen Logistics (UK) Ltd. 100.00*3 GBP 44,130 thousand Yusen Logistics (Iberica) S.A. 100.00*3 EUR 585 thousand Yusen Logistics (Polska) Sp.z o.o. 100.00*3 PLN 2,400 thousand Yusen Logistics (Hungary) KFT. 100.00*3 HUF 12,420 thousand Yusen Logistics (Edam) B.V. 100.00*12 EUR 18 thousand Yusen Logistics (Czech) s.r.o. 100.00*3 CZK 431,729 thousand Yusen Logistics (Vietnam) Co.,Ltd. 99.00*13 VND 6,375 million NANHAI BUSINESS SOLUTIONS PTE LTD. 100.00*14 SGD 100 thousand Yusen Logistics & Kusuhara Lanka (Pvt.) Ltd. 51.00 LKR 6,500 thousand Yusen Logistics RUS LLC 100.00*3 RUB 1,000 thousand Yusen Logistics Center,Inc. 100.00*15 PHP 35,000 thousand Yusen Logistics (Thailand) Co.,Ltd. 87.80*16 THB 70,000 thousand PT. Puninar Yusen Logistics Indonesia 51.00 USD 13,000 thousand Yusen Logistics Do Brasil Ltda. 61.88 BRL 14,492 thousand Yusen Logistics (China) Co.,Ltd. 51.00 CNY 158,047 thousand PT. Yusen Logistics Solutions Indonesia 51.00 USD 5,100 thousand TASCO Berhad 53.19*17 MYR 100,000 thousand Baik Sepakat Sdn Bhd 100.00*18 MYR 100 thousand Tunas Cergas Logistik Sdn Bhd 100.00*18 MYR 100 thousand Emulsi Teknik Sdn Bhd 100.00*18 MYR 100 thousand TASCO Express Sdn Bhd 100.00*18 MYR 100 thousand Maya Kekal Sdn Bhd 100.00*18 MYR 2 Precious Fortunes Sdn Bhd 100.00*18 MYR 8,000 thousand Trans-Asia Shipping Pte Ltd 100.00*18 SGD 100 thousand Piala Kristal (M) Sdn Bhd 51.22*19 MYR 205 thousand Omega Saujana Sdn Bhd 51.22*19 MYR 205 thousand Titian Pelangi Sdn. Bhd. *25 100.00*18 MYR 3,380 thousand Shenzhen Yusen Freight Service Co.,Ltd. 100.00*2 CNY 11,430 thousand Double Wing Spirit Service Co.,Ltd. 80.00*20 THB 7,000 thousand Yusen Real Estate (Hai Phong) Co.,Ltd. 100.00*14 VND 126,216 million Yusen Logistics (Mexico), S.A. de C.V. *24 100.00*21 MXN 46,800 thousand Yusen Logistics Turkey Lojistik Hizmetleri Limited � Sirketi*24 100.00*22 TRY 14,680 thousand Yusen Logistics and Transportation (Vietnam) � Co.,Ltd.*24 49.00*8 VND 2,104 million Yusen Keihin Trans Co., Ltd. 100.00 JPY 36 million Yusen Logistics (Kitakanto) Co., Ltd. 100.00 JPY 50 million Yusen Logistics (Tsukuba) Co., Ltd. 100.00 JPY 50 million Yusen Logistics (Shinshu) Co., Ltd. 90.00 JPY 50 million Yusen Logistics (Tohoku) Co., Ltd. 100.00 JPY 30 million Yusen Logistics (Kyushu) Co., Ltd. 100.00 JPY 30 million Yusen Logistics (Chugoku) Co., Ltd. 80.00 JPY 30 million Yusen Logistics (Hokuriku) Co., Ltd. 100.00 JPY 20 million Yusen Logitec Co., Ltd. 100.00 JPY 20 million Yusen Travel Co., Ltd. 100.00 JPY 270 million Ryowa Diamond Air Service Co., Ltd. 99.17*23 JPY 50 million Yusen Loginet Co., Ltd. 100.00 JPY 20 million

*1 as of March 31, 2015 *2 owned 100.00% by Yusen Logistics (Hong Kong) Limited *3 owned 100.00% by Yusen Logistics (Europe) B.V. *4 owned 32.04% by the Company, 18.93% by Yusen Logistics (Singapore) Pte.Ltd. *5 owned 57.20% by the Company, 38.10% by Yusen Logistics (Hong Kong) Limited

61Annual Report 2015

*6 owned 8.88% by the Company, 58.74% by Yusen Logistics (Singapore) Pte.Ltd. *7 owned 49.00% by Yusen Logistics (Singapore) Pte.Ltd., 46.00% by Yusen Logistics (Thailand) Co.,

Ltd. *8 owned 49.00% by Yusen Logistics (Singapore) Pte.Ltd. *9 owned 31.53% by the Company, 19.47% by Yusen Logistics (Singapore) Pte.Ltd. *10 owned 100.00% by Yusen Logistics (Americas) Inc. *11 owned 99.71% by Yusen Logistics (Americas) Inc., 0.29% by Yusen Logistics (Mexico), S.A. de

C.V.*12 owned 100.00% by Yusen Logistics (Benelux) B.V. *13 owned 99.00% by Yusen Logistics (Singapore) Pte.Ltd *14 owned 100.00% by Yusen Logistics (Singapore) Pte.Ltd. *15 owned 100.00% by Yusen Logistics Philippines, Inc. *16 owned 33.46% by the Company, 10.80% by Yusen Air & Sea Service Management (Thailand) Co.,

Ltd.*17 owned 29.20% by the Company, 23.99% by Yusen Logistics (Singapore) Pte.Ltd. *18 owned 100.00% by TASCO Berhad *19 owned 51.22% by TASCO Berhad *20 owned 80.00% by Yusen Logistics (Thailand) Co., Ltd. *21 owned 74.8% by the Company, 12.60% by Yusen Logistics (Americas) Inc., 12.60% by ETA TOO,

INC.*22 owned 0.59% by the Company, 99.41% by Yusen Logistics (Europe) B.V. *23 owned 99.17% by Yusen Travel Co., Ltd. *24 became newly consolidated companies since materiality has increased *25 became newly consolidated company as the result of the acquisition of the stock *26 changed their company name in this fiscal year

Under the control or influence concept, those companies in which the Company, directly or indirectly, is able to exercise control over operations are fully consolidated, and those companies over which the Group has the ability to exercise significant influences are accounted for by the equity method.

Yusen Logistics Transporte S.A. de C.V. was merged into Yusen Logistics (Mexico), S.A. de C.V. and

excluded from the scope of consolidation. NYK LOGISTICS (AUSTRALIA) PTY.LTD. was excluded from the scope of consolidation due to liquidation.

Investments in three (three in 2014) unconsolidated subsidiaries and two (two in 2014) affiliated companies are accounted for by the equity method. Investments in the remaining unconsolidated subsidiaries and affiliated companies are stated at cost, which is determined by the moving-average method. If the equity method of accounting had been applied to the investments in these companies, the effect on the accompanying consolidated financial statements would not be material.

The excess of the cost of an acquisition over the fair value of the net assets of the acquired subsidiary at the date of acquisition is being amortized using the straight-line method principally over a period not exceeding 20 years.

All significant intercompany balances and transactions have been eliminated in consolidation. All material unrealized profit included in assets resulting from transactions within the Group is eliminated.

b. Unification of Accounting Policies Applied to Foreign Subsidiaries for the Consolidated Financial Statements—In May 2006, the Accounting Standards Board of Japan ("ASBJ") issued ASBJ Practical Issues Task Force (PITF) No. 18, “Practical Solution on Unification of Accounting Policies Applied to Foreign Subsidiaries for the Consolidated Financial Statements.” PITF No. 18 prescribes: (1) the accounting policies and procedures applied to a parent company and its subsidiaries for similar transactions and events under similar circumstances should in principle be unified for the preparation of the consolidated financial statements, (2) financial statements prepared by foreign subsidiaries in accordance with either International Financial Reporting Standards or the generally accepted accounting principles in the United States of America tentatively may be used for the consolidation process, (3) however, the following items should be adjusted in the consolidation process so that net income is accounted for in accordance with Japanese GAAP unless they are not material: 1) amortization of goodwill; 2) scheduled amortization of actuarial gain or loss of pensions that has been directly recorded in the equity; 3) expensing capitalized development costs of R&D; 4) cancellation of the fair value model accounting for property, plant, and equipment and investment properties and incorporation of the cost model accounting; and 5)

62 Annual Report 2015

exclusion of minority interests from net income, if contained.

c. Business Combination����In October 2003, the Business Accounting Council (“BAC”) issued a Statement of Opinion, “Accounting for Business Combinations,” and in December 2005, the ASBJ issued ASBJ Statement No. 7, “Accounting Standard for Business Divestitures” and ASBJ Guidance No. 10, “Guidance on Accounting Standard for Business Combinations and Business Divestitures.” The accounting standard for business combinations allowed companies to apply the pooling of interests method of accounting only when certain specific criteria are met such that the business combination is essentially regarded as a uniting-of-interests. For business combinations that do not meet the uniting-of-interests criteria, the business combination is considered to be an acquisition and the purchase method of accounting is required. This standard also prescribes the accounting for combinations of entities under common control and for joint ventures.

In December 2008, the ASBJ issued a revised accounting standard for business combinations, ASBJ Statement No. 21, “Accounting Standard for Business Combinations.” Major accounting changes under the revised accounting standard are as follows: (1) The revised standard requires accounting for business combinations only by the purchase method. As a result, the pooling of interests method of accounting is no longer allowed. (2) The previous accounting standard required research and development costs to be charged to income as incurred. Under the revised standard, in-process research and development costs (IPR&D) acquired in the business combination are capitalized as an intangible asset. (3) The previous accounting standard provided for a bargain purchase gain (negative goodwill) to be systematically amortized over a period not exceeding 20 years. Under the revised standard, the acquirer recognizes the bargain purchase gain in profit or loss immediately on the acquisition date after reassessing and confirming that all of the assets acquired and all of the liabilities assumed have been identified after a review of the procedures used in the purchase allocation. This standard was applicable to business combinations undertaken on or after April 1, 2010. The Company adopted this standard on April 1, 2010.

d. Cash Equivalents—Cash equivalents are short-term investments that are readily convertible into cash and that are exposed to insignificant risk of changes in value. Cash equivalents include time deposits which mature or become due within three months of the date of acquisition.

e. Investments in Securities—Securities are classified into three categories, depending on management's intent: trading, available-for-sale, or held-to-maturity. The Company classifies all investments in securities as available-for-sale securities. Marketable available-for-sale securities are reported at fair value, with unrealized gains and losses, net of applicable taxes, reported under accumulated other comprehensive income in a separate component of equity. Non-marketable available-for-sale securities are stated at cost determined by the moving-average method. For other than temporary declines in fair value, non-marketable investment securities are reduced to net realizable value by a charge to income.

f. Property, Plant and Equipment—Property, plant and equipment are stated at cost. Depreciation of property, plant and equipment of the Company and domestic consolidated subsidiaries is computed substantially by the declining-balance method at rates based on the estimated useful lives of the assets, except for the buildings and structures at the Toyooka distribution center, Iwata distribution center and Yusen Logi Fukumoto building, which are depreciated by the straight-line method. The depreciation of property, plant and equipment of foreign consolidated subsidiaries is generally computed by the straight-line method over the estimated useful lives of the assets. The range of useful lives is principally as follows:

Buildings and structures 3–60 years Furniture and fixtures 2–20 years Machinery, equipment and vehicles 4–6 years

g. Other Assets—Amortization of intangible assets included in other assets is computed by the straight-line method. Software for internal use is amortized over a five-year period.

h. Long-lived Assets—The Group reviews its long-lived assets for impairment whenever events or changes in circumstance indicate the carrying amount of an asset or asset group may not be recoverable. An impairment loss is recognized if the carrying amount of an asset or asset group exceeds the sum of the undiscounted future cash flows expected to result from the continued use and eventual disposition of the asset or asset group. The impairment loss is measured as the amount by which the carrying amount of the asset exceeds its recoverable amount, which is the higher of the discounted cash flows from the continued

63Annual Report 2015

use and eventual disposition of the asset or the net selling price at disposition.

i. Allowance for Doubtful Accounts—The Group provides an allowance for doubtful accounts based on the aggregated amount of estimated credit losses for doubtful receivables, plus an amount for receivables other than doubtful receivables calculated using historical write off experience over a certain period.

j. Accrued Bonuses to Employees—Employees are paid bonuses in July and December of every year. The bonuses include amounts for services rendered during the previous fiscal year which are recorded as accrued bonuses on the balance sheet as of the respective fiscal year-end.

k. Retirement and Pension PlansEmployee's retirement and pension plans—The Company and certain domestic consolidated subsidiaries have a non-contributory funded defined benefit pension plan and an unfunded retirement benefit plan. Certain of the Company’s domestic consolidated subsidiaries have a contributory funded defined contribution pension plan, while certain foreign consolidated subsidiaries have either a non-contributory funded defined benefit pension plan or a contributory funded defined contribution pension plan.

The liability for employees' retirement benefits is accounted for based on projected benefit obligations and plan assets at the balance sheet date.

Retirement allowance for directors and audit & supervisory board members—Retirement allowance for directors and audit & supervisory board members for certain subsidiaries are recorded to state the liability at the amount that would be required if all directors and audit & supervisory board members retired at each balance sheet date.

l. Provision for alleged antitrust law violation����The Company has recorded a provision against possible future losses that can be reasonably estimated at the present time associated with a class action lawsuit for alleged violation of the U.S. antitrust law in connection with freight forwarding services for international air cargo shipments.

m. Leases—In March 2007, the ASBJ issued ASBJ Statement No. 13, “Accounting Standard for Lease Transactions,” which revised the previous accounting standard for lease transactions issued in June 1993. The revised accounting standard for lease transactions was effective for fiscal years beginning on or after April 1, 2008.

Under the previous accounting standard, finance leases that were deemed to transfer ownership of the leased property to the lessee were capitalized. However, other finance leases were permitted to be accounted for as operating lease transactions if certain “as if capitalized” information was disclosed in the note to the lessee’s financial statements. The revised accounting standard requires that all finance lease transactions be capitalized to recognize lease assets and lease obligations in the balance sheet. In addition, the accounting standard permits leases which existed at the transition date and do not transfer ownership of the leased property to the lessee to continue to be accounted for as operating lease transactions.

The Company applied the revised accounting standard effective April 1, 2008. In addition, the Company continues to account for leases which existed at the transition date and does not transfer ownership of the leased property to the lessee as operating lease transactions.

All other leases are accounted for as operating leases.

n. Income Taxes—The provision for income taxes is computed based on the pretax income included in the consolidated statement of income. The asset and liability approach is used to recognize deferred tax assets and liabilities for the expected future tax consequences of temporary differences between the carrying amounts and the tax bases of assets and liabilities. Deferred taxes are measured by applying currently enacted tax laws to the temporary differences.

o. Treasury Stock—Under the Japanese Companies Act, the Company is allowed to acquire its own shares to the extent that the aggregate cost of treasury stock does not exceed the maximum amount available for dividends. Treasury stock is stated at cost in the equity of the accompanying consolidated balance sheet. Net gain on disposal of treasury stock is presented under "Capital surplus'' in the equity of the accompanying consolidated balance sheet.

64 Annual Report 2015

p. Foreign Currency Transactions—All short-term and long-term monetary receivables and payables denominated in foreign currencies are translated into Japanese yen at the exchange rates at the balance sheet date. The foreign exchange gains and losses from translation are recognized in the consolidated statement of income.

q. Foreign Currency Financial Statements—The balance sheet accounts of foreign consolidated subsidiaries and foreign subsidiaries accounted for by the equity method are translated into Japanese yen at the current exchange rate as of the balance sheet date except for equity, which is translated at the historical rate. Differences arising from such translations are shown as "Foreign currency translation adjustments" under accumulated other comprehensive income in a separate component of equity.

Revenue and expense accounts of foreign consolidated subsidiaries are translated into Japanese yen at the average exchange rates.

r. Derivatives—The Group uses derivative financial instruments to manage its exposures to fluctuations in foreign exchange and interest rates. Foreign exchange forward contracts are utilized by the Group. The Group does not enter into derivatives for trading or speculative purposes.

Derivative financial instruments and foreign currency transactions are classified and accounted for as follows: (1) all derivatives are recognized as either assets or liabilities and measured at fair value, and gains or losses on derivative transactions are recognized in the consolidated statement of income and (2) for derivatives used for hedging purposes, if derivatives qualify for hedge accounting because of high correlation and effectiveness between the hedging instruments and the hedged items, gains or losses on derivatives are deferred until maturity of the hedged transactions.

The foreign exchange forward contracts employed to hedge foreign exchange exposures in the Group's operating activities are measured at the fair value and the unrealized gains or losses are recognized in consolidated statement of income.

s. Accounting Changes and Error Corrections―In December 2009, the ASBJ issued ASBJ Statement No. 24 “Accounting Standard for Accounting Changes and Error Corrections” and ASBJ Guidance No. 24 “Guidance on Accounting Standard for Accounting Changes and Error Corrections.” Accounting treatments under this standard and guidance are as follows: (1) Changes in Accounting Policies - When a new accounting policy is applied with revision of accounting standards, the new policy is applied retrospectively, unless the revised accounting standards include specific transitional provisions. When the revised accounting standards include specific transitional provisions, an entity shall comply with the specific transitional provisions. (2) Changes in Presentations - When the presentation of financial statements is changed, prior-period financial statements are reclassified in accordance with the new presentation. (3) Changes in Accounting Estimates - A change in an accounting estimate is accounted for in the period of the change if the change affects that period only, and is accounted for prospectively if the change affects both the period of the change and future periods. (4) Corrections of Prior Period Errors - When an error in prior-period financial statements is discovered, those statements are restated.

This accounting standard and the guidance are applicable to accounting changes and corrections of prior- period errors, which are made from the beginning of the fiscal year that begins on or after April 1, 2011.

t. Per Share Information—Net assets per share are computed based on the outstanding shares of common stock at relevant balance sheet dates.

Basic net income per share is computed by dividing net income available to shareholders by the weighted-average number of shares of common stock outstanding for the period.

Diluted net income per share for the years ended March 31, 2015 and 2014, is not presented since the Company had no securities with a dilutive effect.

Cash dividends per share presented in the accompanying consolidated statement of income are dividends applicable to the respective years including dividends to be paid after the end of the year.

u.���� Change in Accounting Standard for Retirement Benefits—In May 2012, the ASBJ issued ASBJ

65Annual Report 2015

Statement No. 26, "Accounting Standard for Retirement Benefits" and ASBJ Guidance No. 25, "Guidance on Accounting Standard for Retirement Benefits," which replaced the accounting standard for retirement benefits that had been issued by the Business Accounting Council in 1998 with an effective date of April 1, 2000, and the other related practical guidance, and were followed by partial amendments from time to time through 2009.

(1) Under the revised accounting standard, actuarial gains and losses and past service costs that are yet to be recognized in profit or loss are recognized within equity (accumulated other comprehensive income), after adjusting for tax effects, and any resulting deficit or surplus is recognized as a liability (net defined benefit liability) or asset (net defined benefit asset).

(2) The revised accounting standard does not change how to recognize actuarial gains and losses and past service costs in profit or loss. Those amounts are recognized in profit or loss over a certain period no longer than the expected average remaining service period of the employees. However, actuarial gains and losses and past service costs that arose in the current period and have not yet been recognized in profit or loss are included in other comprehensive income and actuarial gains and losses and past service costs that were recognized in other comprehensive income in prior periods and then recognized in profit or loss in the current period, are treated as reclassification adjustments.

(3) The revised accounting standard also made certain amendments relating to the method of attributing expected benefit to periods, the discount rate, and expected future salary increases.

This accounting standard and the guidance for (1) and (2) above are effective for the end of annual periods beginning on or after April 1, 2013, and for (3) above are effective for the beginning of annual periods beginning on or after April 1, 2014, or for the beginning of annual periods beginning on or after April 1, 2015, subject to certain disclosure in March 2015, all with earlier application being permitted from the beginning of annual periods beginning on or after April 1, 2013. However, no retrospective application of this accounting standard to consolidated financial statements in prior periods is required.

The Company applied the revised accounting standard and guidance for retirement benefits for (1) and (2)

above, effective March 31, 2014, and for (3) above, effective April 1, 2014

With respect to (3) above, the Company changed the method of attributing the expected benefit to periods from a straight-line basis to a benefit formula basis, the method of determining the discount rate from using the period which approximates the expected average remaining service period to using a single weighted average discount rate reflecting the estimated timing and amount of benefit payment, and recorded the effect of (3) above as of April 1, 2014, in retained earnings. As a result, asset for retirement benefits and retained earnings as of April 1, 2014, increased by ¥857 million ($7,135 thousand), and ¥902 million ($7,502 thousand), respectively, and liability for retirement benefits as of April 1, 2014, decreased by ¥543 million ($4,522 thousand), and operating income and income before income taxes and minority interests for the year ended March 31, 2015 is immaterial. In addition, basic net assets per share for the year ended March 31, 2015, increased by ¥21.09 ($0.176) and basic net income per share for the year ended March 31, 2015 is immaterial.

v. New Accounting Pronouncements Accounting Standards for Business Combinations and Consolidated Financial Statements —On September 13, 2013, the ASBJ issued revised ASBJ Statement No. 21, "Accounting Standard for Business Combinations," revised ASBJ Guidance No. 10, "Guidance on Accounting Standards for Business Combinations and Business Divestitures," and revised ASBJ Statement No. 22, "Accounting Standard for Consolidated Financial Statements."

Major accounting changes are as follows:

(1) Transactions with non-controlling interest�A parent's ownership interest in a subsidiary might change if the parent purchases or sells ownership interests in its subsidiary. The carrying amount of minority interest is adjusted to reflect the change in the parent's ownership interest in its subsidiary while the parent retains its controlling interest in its subsidiary. Under the current accounting standard, any difference between the fair value of the consideration received or paid and the amount by which the minority interest is adjusted is accounted for as an adjustment of goodwill or as profit or loss in the consolidated statement of income. Under the revised accounting standard, such difference shall be accounted for as capital surplus as long as the parent retains control over its subsidiary.

66 Annual Report 2015

(2) Presentation of the consolidated balance sheet�In the consolidated balance sheet, "minority interest" under the current accounting standard will be changed to "non-controlling interest" under the revised accounting standard.

(3) Presentation of the consolidated statement of income�In the consolidated statement of income, "income before minority interest" under the current accounting standard will be changed to "net income" under the revised accounting standard, and "net income" under the current accounting standard will be changed to "net income attributable to owners of the parent" under the revised accounting standard.

(4) Provisional accounting treatments for a business combination�If the initial accounting for a business combination is incomplete by the end of the reporting period in which the business combination occurs, an acquirer shall report in its financial statements provisional amounts for the items for which the accounting is incomplete. Under the current accounting standard guidance, the impact of adjustments to provisional amounts recorded in a business combination on profit or loss is recognized as profit or loss in the year in which the measurement is completed. Under the revised accounting standard guidance, during the measurement period, which shall not exceed one year from the acquisition, the acquirer shall retrospectively adjust the provisional amounts recognized at the acquisition date to reflect new information obtained about facts and circumstances that existed as of the acquisition date and that would have affected the measurement of the amounts recognized as of that date. Such adjustments shall be recognized as if the accounting for the business combination had been completed at the acquisition date.

(5) Acquisition-related costs�Acquisition-related costs are costs, such as advisory fees or professional fees, which an acquirer incurs to effect a business combination. Under the current accounting standard, the acquirer accounts for acquisition-related costs by including them in the acquisition costs of the investment. Under the revised accounting standard, acquisition-related costs shall be accounted for as expenses in the periods in which the costs are incurred.

The above accounting standards and guidance for (1) transactions with non-controlling interest, (2) presentation of the consolidated balance sheet, (3) presentation of the consolidated statement of income, and (5) acquisition-related costs are effective for the beginning of annual periods beginning on or after April 1, 2015. Earlier application is permitted from the beginning of annual periods beginning on or after April 1, 2014, except for (2) presentation of the consolidated balance sheet and (3) presentation of the consolidated statement of income. In the case of earlier application, all accounting standards and guidance above, except for (2) presentation of the consolidated balance sheet and (3) presentation of the consolidated statement of income, should be applied simultaneously.

Either retrospective or prospective application of the revised accounting standards and guidance for (1) transactions with non-controlling interest and (5) acquisition-related costs is permitted. In retrospective application of the revised standards and guidance, the accumulated effects of retrospective adjustments for all (1) transactions with non-controlling interest and (5) acquisition-related costs which occurred in the past shall be reflected as adjustments to the beginning balance of capital surplus and retained earnings for the year of the first-time application. In prospective application, the new standards and guidance shall be applied prospectively from the beginning of the year of the first-time application.

The revised accounting standards and guidance for (2) presentation of the consolidated balance sheet and (3) presentation of the consolidated statement of income shall be applied to all periods presented in financial statements containing the first-time application of the revised standards and guidance.

The revised standards and guidance for (4) provisional accounting treatments for a business combination are effective for a business combination which occurs on or after the beginning of annual periods beginning on or after April 1, 2015. Earlier application is permitted for a business combination which occurs on or after the beginning of annual periods beginning on or after April 1, 2014.

The Company expects to apply the revised accounting standards and guidance for (1), (2), (3) and (5) above from April 1, 2015, and for (4) above for a business combination which will occur on or after April 1, 2015, and is in the process of measuring the effects of applying the revised accounting standards and guidance in future applicable periods.

67Annual Report 2015

neY fo snoilliM Thousands ofU.S. Dollars

5102 2014 2015

Proceeds from sale of available-for-sale securities ¥ 10 ¥ 95 $82 Total amount of gain on sale of available-for-sale securities 7 51 61 Total amount of loss on sale of available-for-sale securities – 3 –

3. LOSS ON IMPAIRMENT OF FIXED ASSET

The Group reviewed its long-lived assets for impairment as of the year ended March 31, 2015, and as a result, recognized an impairment loss of ¥369 million ($3,074 thousand) as other expenses. The impairment loss for the year ended March 31, 2015, was recorded on certain buildings and land in Osaka and Kobe, Japan. The Group reduced the book value of these assets to their recoverable amounts due to a significant decline in market value of certain fixed assets which were planned to be disposed of by sale. Assets in use comprised ¥155 million for buildings and ¥214 million for land. The recoverable amounts of those assets planned to be disposed by sale were measured at their net selling price determined by quotation from a third party vendor.

4. INVESTMENTS IN SECURITIES

The cost and aggregate fair values of the investments classified as "available-for-sale securities" at March 31, 2015 and 2014, are as follows:

(1) Available-for-sale securities for which market quotations are available:

(2) Proceeds from sale of available-for-sale securities and total amounts of gain and loss on sale of available-for-sale securities:

(3) The impairment losses on securities for the year ended March 31, 2015, amounted to ¥149 million ($1,241 thousand) for the securities of non-consolidated subsidiaries.

There were no impairment losses of securities for the year ended March 31, 2014.

Millions of Yen Thousands of U.S. Dollars 2015 2014 2015

Cost

Fair Value(Carrying Amount) Difference Cost

Fair Value(Carrying Amount) Difference Cost

Fair Value(Carrying Amount) Difference

Securities for which market value exceeds cost— Equity securities Government bonds Securities for which market value does not exceed cost— Equity securities 49

Total ¥ 413

5156(3)46 (5) 411 385 (26)

¥ 894 ¥ 481 ¥ 408 ¥ 697 ¥ 289 $ 3,434 $ 7,439 $ 4,005

¥ ¥ ¥304 788 484 ¥ 293 ¥ 586 ¥ 293 $ 2,529 $ 6,556 $ 4,027

60 60 0 59 60 1 494 498 4

68 Annual Report 2015

5. SHORT-TERM LOANS PAYABLE AND LONG-TERM DEBT

Short-term loans payable at March 31, 2015, consisted of notes to financial institutions and bank overdrafts. The weighted-average interest rates applicable to the short-term loans payable were 3.57% and 3.95% at March 31, 2015 and 2014, respectively.

Long-term debt at March 31, 2015 and 2014, consisted of the following:

Millions of Yen Thousands of U.S. Dollars

2015 2014 2015

Loans from banks and other financial institutions, due serially to 2025 with average interest rates of 1.14% (2015) and 0.93% (2014); Collateralized ¥ – ¥ – $ –

Unsecured 20,222 18,046 168,282 Finance lease obligation 379 253 3,153

Total 20,601 18,299 171,435 Less current portion (4,668 ) (5,359) (38,848 )

Long-term debt, less current portion ¥15,933 ¥12,940 $132,587

Annual maturities of long-term debt including financial lease obligation at March 31, 2015, were as follows:

Year Ending March 31 Millions of Yen

Thousands of U.S. Dollars

2016 ¥ 4,668 $ 38,848 2017 5,614 46,716 2018 1,365 11,355 2019 309 2,572 2020 and thereafter 8,645 71,944

Total ¥ 20,601 $171,435

As is customary in Japan, the Company maintains substantial deposit balances with banks with which it has borrowings. Such deposit balances are not legally or contractually restricted as to withdrawal.

General agreements with respective banks provide, as is customary in Japan, that additional collateral must be provided under certain circumstances if requested by such banks and that certain banks have the right to offset cash deposited with them against any long-term or short-term debt or obligation that becomes due and, in case of default and certain other specified events, against all other debt payable to the banks. The Company has never been requested to provide any additional collateral.

69Annual Report 2015

6. RETIREMENT AND PENSION PLANS

The Company and certain consolidated subsidiaries have severance payment plans for employees, directors, and audit & supervisory board members. Under most circumstances, employees terminating their employment are entitled to retirement benefits determined based on the rate of pay at the time of termination, years of service, and certain other factors. Such retirement benefits are made in the form of a lump-sum severance payment from the Company or from certain consolidated subsidiaries and annuity payments from a trustee. Employees are entitled to larger payments if the termination is involuntary, by retirement at the mandatory retirement age, by death, or by voluntary retirement at certain specific ages prior to the mandatory retirement age.

For the years ended March 31, 2015 and 2014

1. The changes in projected benefit obligation for the years ended March 31, 2015 and 2014, are as follows:

Millions of Yen Thousands of

U.S. Dollars 2015 2014 2015

Balance at beginning of year ¥ 18,191 ¥ 16,204 $ 151,383 � Cumulative effect of accounting change (1,400) – (11,657) Balance at beginning of year, as restated 16,791 16,204 139,726 � Current service cost 961 750 7,993 � Interest cost 444 502 3,694 � Actuarial gains and losses 1,607 (37) 13,370 � Benefits paid (954) (794) (7,942) � Past service cost 104 16 866 � Others 451 1,550 3,760 Balance at end of year ¥ 19,404 ¥ 18,191 $ 161,467

2. The changes in plan assets for the years ended March 31, 2015 and 2014, are as follows:

Millions of Yen Thousands of

U.S. Dollars 2015 2014 2015

Balance at beginning of year ¥ 12,922 ¥ 10,759 $ 107,532 Expected return on plan assets 461 401 3,834 � Actuarial gains and losses 1,231 58 10,242 � Contributions from the employer 955 895 7,944 � Benefits paid (623) (550) (5,180) Others 308 1,359 2,565 Balance at end of year ¥ 15,254 ¥ 12,922 $ 126,937

70 Annual Report 2015

3. Reconciliation between the liability recorded in the consolidated balance sheet and the balances of projected benefit obligation and plan assets as of March 31, 2015 and 2014

Millions of Yen Thousands of

U.S. Dollars 2015 2014 2015

Funded projected benefit obligation ¥ 15,126 ¥ 15,293 $ 125,875 Plan assets (15,254) (12,922) (126,937)

(128) 2,371 (1,062) Unfunded projected benefit obligation 4,278 2,898 35,592 Net liability (asset) for defined benefit obligation ¥ 4,150 ¥ 5,269 $ 34,530

Millions of Yen Thousands of

U.S. Dollars 2015 2014 2015

Net defined benefit liability ¥ 5,789 ¥ 5,553 $ 48,170 Net defined benefit asset (1,639) (284) (13,640) Net liability (asset) for defined benefit obligation ¥ 4,150 ¥ 5,269 $ 34,530

4. The components of net periodic benefit costs for the years ended March 31, 2015 and 2014, are as follows:

Millions of Yen Thousands of

U.S. Dollars 2015 2014 2015

Current service cost ¥ 961 ¥ 778 $ 7,993 Interest cost 444 502 3,694 Expected return on plan assets (461) (429) (3,834) Amortization of unrecognized actuarial loss 329 341 2,737 Amortization of past service cost 104 16 866 Others 0 4 1 � Net periodic benefit costs ¥ 1,377 ¥ 1,212 $ 11,457

5. Other comprehensive income on projected retirement benefit plans (before income tax effect) for the years ended March 31, 2015 and 2014

Millions of Yen Thousands of

U.S. Dollars 2015 2014 2015

Actuarial gains and losses ¥ 56 ¥ 8 $ 466 Total ¥ 56 ¥ 8 $ 466

71Annual Report 2015

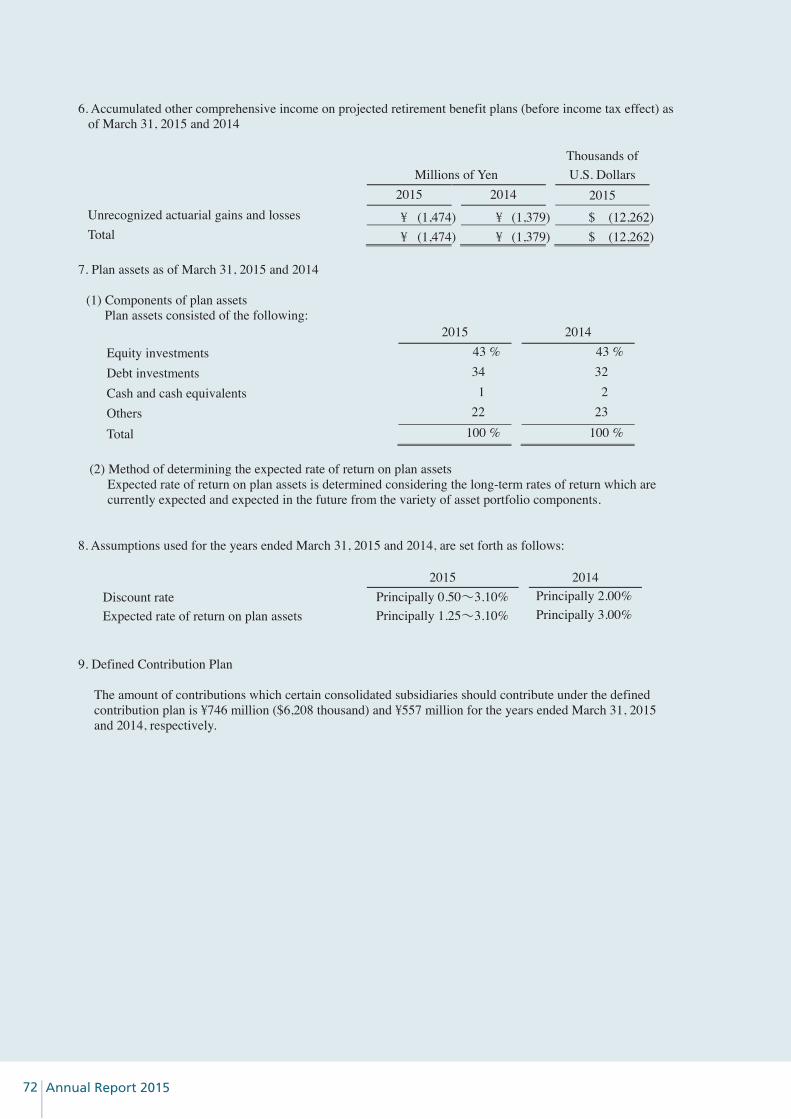

6. Accumulated other comprehensive income on projected retirement benefit plans (before income tax effect) as of March 31, 2015 and 2014

Millions of Yen Thousands of

U.S. Dollars 2015 2014 2015

Unrecognized actuarial gains and losses ¥ (1,474) ¥ (1,379) $ (12,262) Total ¥ (1,474) ¥ (1,379) $ (12,262)

7. Plan assets as of March 31, 2015 and 2014

(1) Components of plan assets Plan assets consisted of the following:

2015 2014 Equity investments 43 % 43 % Debt investments 34 32 Cash and cash equivalents 1 2 Others 22 23

Total 100 % 100 %

(2) Method of determining the expected rate of return on plan assets Expected rate of return on plan assets is determined considering the long-term rates of return which are currently expected and expected in the future from the variety of asset portfolio components.

8. Assumptions used for the years ended March 31, 2015 and 2014, are set forth as follows:

2015 2014 Discount rate Principally 0.50�3.10% Principally 2.00% Expected rate of return on plan assets Principally 1.25�3.10% Principally 3.00%

9. Defined Contribution Plan

The amount of contributions which certain consolidated subsidiaries should contribute under the defined contribution plan is ¥746 million ($6,208 thousand) and ¥557 million for the years ended March 31, 2015 and 2014, respectively.

72 Annual Report 2015

7. EQUITY

Japanese companies are subject to the Companies Act of Japan (the "Companies Act"). The significant provisions in the Companies Act that affect financial and accounting matters are summarized below:

a. Dividends

Under the Companies Act, companies can pay dividends at any time during the fiscal year in addition to the year-end dividend upon resolution at the shareholders meeting. For companies that meet certain criteria such as: (1) having a Board of Directors, (2) having independent auditors, (3) having an Audit & Supervisory Board, and (4) the term of service of the directors is prescribed as one year rather than two years of normal term by its articles of incorporation, the Board of Directors may declare dividends (except for dividends in kind) at any time during the fiscal year if the company has prescribed so in its articles of incorporation. The Company meets all the above criteria.

Semiannual interim dividends may also be paid once a year upon resolution by the Board of Directors if the articles of incorporation of the company so stipulate. The Companies Act provides certain limitations on the amounts available for dividends or the purchase of treasury stock. The limitation is defined as the amount available for distribution to the shareholders, but the amount of net assets after dividends must be maintained at no less than ¥3 million.

b. Increases/Decreases and Transfer of Common Stock, Reserve, and Surplus

The Companies Act requires that an amount equal to 10% of dividends must be appropriated as a legal reserve (a component of retained earnings) or as additional paid-in capital (a component of capital surplus) depending on the equity account charged upon the payment of such dividends until the total of aggregate amount of legal reserve and additional paid-in capital equals 25% of the common stock. Under the Companies Act, the total amount of additional paid-in capital and legal reserve may be reversed without limitation. The Companies Act also provides that common stock, legal reserve, additional paid-in capital, other capital surplus, and retained earnings can be transferred among the accounts under certain conditions upon resolution of the shareholders.

c. Treasury Stock and Treasury Stock Acquisition Rights

The Companies Act also provides for companies to purchase treasury stock and dispose of such treasury stock by resolution of the Board of Directors. The amount of treasury stock purchased cannot exceed the amount available for distribution to the shareholders which is determined by a specific formula.

Under the Companies Act, stock acquisition rights are presented as a separate component of equity.

The Companies Act also provides that companies can purchase both treasury stock acquisition rights and treasury stock. Such treasury stock acquisition rights are presented as a separate component of equity or deducted directly from stock acquisition rights.

73Annual Report 2015

8. INCOME TAXES

The Company and domestic consolidated subsidiaries are subject to Japanese national and local income taxes which, in the aggregate, resulted in a normal effective statutory rate of approximately 35.6% and 38.0% for the years ended March 31, 2015 and 2014, respectively.

The tax effects of significant temporary differences resulted in deferred tax assets and liabilities at March 31, 2015 and 2014, are as follows:

Millions of Yen Thousands of U.S. Dollars

2015 2014 2015 Deferred tax assets: � Net defined benefit liability ¥ 1,486 ¥ 1,650 $ 12,368

Accrued bonuses to employees 775 713 6,449 Accrued enterprise tax 86 59 712 Accrued pension and severance costs for directors

and audit & supervisory board members 126 108 1,052 Allowance for doubtful accounts 121 329 1,006 Depreciation 376 384 3,132 Tax loss carryforwards 3,129 2,574 26,035 Loss on impairment of fixed assets 99 15 821 Loss on revaluation of investments in securities 25 88 211 Loss on write-down of golf club membership 102 110 847

Stock of affiliated company 124 142 1,030 Provision for alleged antitrust law violation 580 – 4,828

Other 902 933 7,504 Total 7,931 7,105 65,995

Less valuation allowance (1,585 ) (1,688 ) (13,185 )

Total deferred tax assets 6,346 5,417 52,810

Deferred tax liabilities: Depreciation 1,191 819 9,914 � Net defined benefit asset 408 70 3,393

Other 574 532 4,776

Total deferred tax liabilities 2,173 1,421 18,083

Net deferred tax assets ¥ 4,173 ¥ 3,996 $ 34,727

74 Annual Report 2015

The reconciliation of the difference between the normal effective statutory tax rate and the actual effective tax rate reflected in the accompanying consolidated statements of income for the years ended March 31, 2015 and 2014 is as follows:

2015 2014

Normal effective statutory tax rate 35.6% 38.0% Adjustments: Entertainment expenses and other non-deductible permanent differences 3.1 4.7

Dividend income not taxable (6.0) (6.1 ) Effect of elimination of intercompany dividends received 9.6 8.8

Per share levy of local tax 0.6 1.0 Lower income tax rates applicable to income in certain

foreign countries (13.5) (7.1 ) Valuation allowance on deferred tax 4.6 0.7

Equity in earnings of affiliated companies and unconsolidated companies (0.3) (0.4 ) Effect of tax reduction 2.6 1.1 Amortization of goodwill 1.0 5.4 Foreign exchange adjustment for provision – (1.3) Tax credits (0.6) – Loss related to competition law case 0.9 –

Other—net 2.9 2.5

Actual effective tax rate 40.5% 47.3%

Adjustment of deferred tax assets and liabilities pursuant to the change in the corporate tax rate

New tax reform laws enacted in 2015 in Japan changed the normal effective statutory tax rate for the fiscal year beginning on or after April 1, 2015, to approximately 33.1% and for the fiscal year beginning on or after April 1, 2016, to approximately 32.3%. The effect of these changes was to decrease deferred tax assets, net of deferred tax liabilities, by ¥199 million ($1,655 thousand), decrease pension liability adjustment by ¥5 million ($45 thousand) and increase accumulated other comprehensive income for unrealized gain on available-for-sale securities by ¥8 million ($67 thousand) in the consolidated balance sheet as of March 31, 2015, and to increase income taxes—deferred in the consolidated statement of income for the year then ended by ¥202 million ($1,677 thousand).

9. LEASES

The Group has various lease agreements whereby the Group acts as lessee.

The minimum rental commitments under non-cancelable operating leases at March 31, 2015 and 2014, were as follows:

Thousands of

Millions of Yen U.S. Dollars 2015 � 2014 2015

Due within one year ¥ 10,718 ¥ 9,657 $ 89,189 Due after one year 20,851 20,743 173,511

Total ¥ 31,569 ¥ 30,400 $262,700

75Annual Report 2015

10. FINANCIAL INSTRUMENTS AND RELATED DISCLOSURES

In March 2008, the ASBJ revised ASBJ Statement No. 10 “Accounting Standard for Financial Instruments” and issued ASBJ Guidance No. 19 “Guidance on Accounting Standard for Financial Instruments and Related Disclosures.” This accounting standard and the guidance were applicable to financial instruments and related disclosures at the end of the fiscal years ending on or after March 31, 2010. The Group applied the revised accounting standard and the new guidance effective March 31, 2010.

(1) Group policy for financial instruments

The Group limits the use of financial instruments for fund management purposes to short-term bank deposits. It is the basic policy of the Group to use the cash management system operated within the Group and bank loans to fund its ongoing operations. Derivatives are used, not for speculative purposes, but to manage exposure to financial risks as described in (2) below.

(2) Nature and extent of risks arising from financial instruments

Receivables such as trade notes and trade accounts are exposed to customer credit risk. Although receivables in foreign currencies are exposed to the market risk of fluctuation in foreign currency exchange rates, the position, net of payables in foreign currencies, is hedged by using forward foreign currency contracts. Investment securities, mainly equity securities of customers and suppliers of the Group, are exposed to the risk of market price fluctuations.

Payment terms of payables, such as trade notes and trade accounts, are less than one year. Although payables in foreign currencies are exposed to the market risk of fluctuation in foreign currency exchange rates, those risks are netted against the balance of receivables denominated in the same foreign currency as noted above.

Loans, principally from financial institutions, in short-term loans payable are mainly for financing related to business transaction.

Loans, principally from financial institutions, in long-term debt are mainly for financing related to business integration and investment in property.

Derivatives, which are forward foreign currency contracts, are used to manage exposure to market risks from changes in foreign currency exchange rates of receivables and payables. Please see Note 11 for more details about derivatives.

(3) Risk management for financial instruments

Credit risk management

Credit risk is the risk of economic loss arising from a counterparty’s failure to repay or service debt according to the contractual terms. The Group manages its credit risk from receivables on the basis of internal guidelines, which include monitoring of payment term and balances of major customers by each business administration department to identify the default risk of customers in the early stage.

The maximum credit risk exposure of financial assets is limited to their carrying amounts as of March 31, 2015.

Market risk management (foreign exchange risk and interest rate risk)

Foreign currency trade receivables and payables are exposed to market risk resulting from fluctuations in foreign currency exchange rates. Such foreign exchange risk is hedged principally by forward foreign currency contracts. In addition, when foreign currency trade receivables and payables are expected from forecasted transactions, forward foreign currency contracts may be used under the limited contract term of a quarter of a year.

Investment securities are managed by monitoring market values and financial position of issuers on a regular basis.

The execution and management of derivative transactions are approved by the CFO or the board of directors according to the internal guidelines which prescribe the authority and the limit for each transaction. Counterparties to these derivative transactions are limited to major financial institutions in order to mitigate credit risks.

76 Annual Report 2015

Liquidity risk management

Liquidity risk comprises the risk that the Group cannot meet its contractual obligations in full on maturity dates. The Group manages its liquidity risk by holding adequate volumes of liquid assets, along with adequate financial planning by the corporate treasury department.

(4) Fair values of financial instruments

Fair values of financial instruments are based on quoted prices in active markets. If quoted prices are not available, other rational valuation techniques are used instead. As the valuation of financial instruments requires various assumptions, the fair values of financial instruments are subject to change when different assumptions are used. Please see Note 11 for fair value information for derivatives.

(a) Fair value of financial instruments

Millions of Yen

March 31, 2015 Carrying Amount � Fair Value �

Unrealized Gain/Loss

Cash and cash equivalents ¥ 32,107 ¥ 32,107 –Time deposits 4,496 4,496 –Trade notes and accounts receivable 93,641 93,641 –Investments in securities: �

Available-for-sale securities 894 894 –

Total ¥ 131,138 ¥ 131,138 –

Trade notes and accounts payable ¥ 46,939 ¥ 46,939 –Short-term loans payable 3,052 3,052 –Current portion of long-term debt 4,668 4,668 –Accrued income taxes 2,192 2,192 –Long-term debt 15,933 16,036 ¥ 103

Total ¥ 72,784 ¥ 72,887 ¥ 103� � � � � �� � � � � �

Millions of Yen

March 31, 2014 Carrying Amount � Fair Value �

Unrealized Gain/Loss

Cash and cash equivalents ¥ 27,694 ¥ 27,694 –Time deposits 2,522 2,522 –Trade notes and accounts receivable 76,193 76,193 –Investments in securities: �

Available-for-sale securities 697 697 –

Total ¥ 107,106 ¥ 107,106 –

Trade notes and accounts payable ¥ 39,010 ¥ 39,010 –Short-term loans payable 3,030 3,030 –Current portion of long-term debt 5,359 5,359 –Accrued income taxes 1,217 1,217 –Long-term debt 12,940 12,955 ¥ 15

Total ¥ 61,556 ¥ 61,571 ¥ 15

77Annual Report 2015

� � � � � �Thousands of U.S. Dollars

March 31, 2015 Carrying Amount � Fair Value �

Unrealized Gain/Loss

Cash and cash equivalents $ 267,177 $ 267,177 – Time deposits 37,413 37,413 – Trade notes and accounts receivable 779,239 779,239 – Investments in securities:

Available-for-sale securities 7,439 7,439 –

Total $1,091,268 $1,091,268 –

Trade notes and accounts payable $390,602 $390,602 – Short-term loans payable 25,398 25,398 – Current portion of long-term debt 38,848 38,848 – Accrued income taxes 18,238 18,238 – Long-term debt 132,587 133,441 $ 854

Total $605,673 $606,527 $ 854

Current assets and liabilities

The fair value of all current assets and liabilities (cash and cash equivalents, time deposit, trade notes and accounts receivable, trade notes and accounts payable, short-term loans payable, current portion of long-term debt, and accrued income taxes) is considered to be equivalent to their carrying amount due to their short-term maturities.

�

Investments in securities (available-for-sale securities)

The fair values of investments in securities are measured at the quoted market price of the stock exchange of the equity instruments, and at the quotes obtained from the financial institution for certain debt instruments. All investments in securities are classified as available-for-sale securities. The fair value information for investments in securities is included in Note 4.

�

Long-term debt

-Long-term loans payable

Long-term loans payable with variable interest rates are stated at book value as the interest rate on these loans reflects the market rate in the short term and their market values approximate book values. Long-term loans payable with fixed interest rates are stated at present value. The present value is calculated by discounting a periodically divided portion of the principal and interest of these loans*, using the assumed rate applied to a similar loan.

*As to the long-term loans payable related to the interest rate swap agreements that meet the requirements for exceptional accounting (Refer to Note 11, “Derivatives”), the total amount of principal and interest income at the post-swap rate is applied.

- Lease obligations

The fair value of lease obligations approximates carrying amount. �

78 Annual Report 2015

Derivatives

The fair value information for derivatives is included in Note 11.

(b) Financial instruments whose fair value cannot be reliably determined

Carrying Amount

Millions of Yen �Thousands of U.S. Dollars

Investments in equity instruments that do not have 2015 � 2014 2015 a quoted market price in an active market ¥ 324 ¥ 307 $2,693

(5) Maturity analysis for financial assets and securities with contractual maturities

Millions of Yen Due after Due after one year five years Due in one through through Due after

March 31, 2015 year or less five years ten years ten years Cash and cash equivalents ¥ 32,107 – – –Time deposits 4,496 – – –Trade notes and accounts receivable 93,641 – – –Investments in securities:

Available-for-sale securities with contractual maturities – ¥ 60 – –

Total ¥ 130,244 ¥ 60 – –

Millions of Yen Due after Due after one year five years

Due in one through through Due after March 31, 2014 year or less five years ten years ten years

Cash and cash equivalents ¥ 27,694 – – –Time deposits 2,522 – – –Trade notes and accounts receivable 76,193 – – –Investments in securities:

Available-for-sale securities with contractual maturities – ¥ 60 – –

Total ¥ 106,409 ¥ 60 – –

79Annual Report 2015

Thousands of U.S. Dollars Due after Due after one year five years Due in one through through Due after

March 31, 2015 year or less five years ten years ten years Cash and cash equivalents $267,177 – – –Time deposits 37,413 – – –Trade notes and accounts receivable 779,239 – – –Investments in securities:

Available-for-sale securities with contractual maturities – $499 – –

Total $1,083,829 $499 – –

80 Annual Report 2015

11. DERIVATIVES

The Group enters into foreign exchange forward contracts, interest rate swaps and currency swaps to reduce the exposure to fluctuations in interest rate risks and foreign exchange rates associated with certain assets and liabilities denominated in foreign currencies.

All derivative transactions are entered into to hedge interest and foreign currency exposures incorporated within the Group's business. Accordingly, market risk in these derivatives is basically offset by opposite movements in the value of hedged assets or liabilities.

Because the counterparties to these derivatives are limited to major international financial institutions, the Group does not anticipate any losses arising from credit risk.

Derivative transactions entered into by the Group have been made in accordance with internal policies which regulate their authorization.

The Group had the following derivative contracts outstanding at March 31, 2015 and 2014:

Derivative transactions to which hedge accounting is not applied.

Currency related

The contract or notional amounts of foreign currency forward contracts which are shown in the above table do not represent the amounts exchanged by the parties and do not measure the Group's exposure to credit or market risk. Fair values of currency swaps are calculated using the prices offered by transacting financial institutions.

Millions of Yen Thousands of U.S. Dollars

Contracts Contracts Contracts Outstanding Outstanding Outstanding

Contracts Due Over Fair Contracts Due Over Fair Contracts Due Over FairOutstanding One Year Value Outstanding One Year Value Outstanding One Year Value

Foreign currency forward contracts:

Selling U.S. dollarSelling euro

–––

– –– ––

– –

–

–

–

––

––

Selling British pound ––

¥ – 2,8665,868

– (87) – $Buying U.S. dollar

Buying Hong Kong dollar Buying Thai baht Buying euro

Currency swaps: Receipts - Singapore dollar, payments - U.S. dollar

2015 2014 2015

Buying Singapore dollar

261

Buying Canadian dollar

Receipts - Thai baht, payment - euro

¥ ¥

(4)2,169 $

¥ (2)¥

1¥

¥

(7)¥

(4)¥705 ¥ (14) ¥

715

¥ 185

473¥ 555

¥ 538

1,680(10) 13

$110

(114) – 7,343 $883

¥

¥ (39) (326)

–– 1,424 – $171 ¥ (1) (7)

1¥¥ 158 –– $ – $¥ ¥ (0) (2) 63 5241¥¥ 305

¥ 602

–– $ – $¥ ¥ (4) (32) 273 1,974–

–– –

–

–

$

$

$ $ $ $

$¥ ¥ (4) (29) 335 2,791

$ $¥ ¥ (95) (789) 685 ¥ 617 5,698 $ 5,136

$ $¥ ¥ 138 1,1441,110 9,237

¥¥ ¥ 344¥

–

–

81Annual Report 2015

Derivative transactions to which hedge accounting is applied.

(1) Currency related

(2) Interest related

Fair values are calculated using the prices offered by transacting financial institutions.

Fair values are calculated using the prices offered by transacting financial institutions.

Millions of Yen Thousands of U.S. Dollars

2015 2014 2015

2015 2014 2015

Contracts Contracts Contracts Outstanding Outstanding Outstanding Hedged Contracts Due Over Fair Contracts Due Over Fair Contracts Due Over Fair item Outstanding One Year Value Outstanding One Year Value Outstanding One Year Value

Derivative transactions qualifying for general accounting policies, deferral hedge accounting Currency swaps:

Receipts - U.S. dollar, payments - Malaysian Ringgit

Long-term debt

Receipts - Singapore dollar,

payments - U.S. dollar Long-term

loan ––– – – –Total

Millions of Yen Thousands of U.S. Dollars

Contracts Contracts Contracts Outstanding Outstanding Outstanding Hedged Contracts Due Over Fair Contracts Due Over Fair Contracts Due Over Fair item Outstanding One Year Value Outstanding One Year Value Outstanding One Year Value

Interest-rate swap derivative transactions qualifying for exceptional accounting Interest-rate swaps:

Receipts floating, payments fixed

Long-term debt

Total

¥ 1,867 ¥ 1,352 ¥209 ¥ 760

¥ 104

¥ 412

¥ 104

¥ 15

¥ (2)

$15,534 $11,250 $1,736

¥ 2,973 ¥ 2,865 ¥(47) ¥ 515 ¥ 463 ¥ (15) $24,743 $23,843 $(387)¥ 2,973 ¥ 2,865 ¥(47) ¥ 515 ¥ 463 ¥ (15) $24,743 $23,843 $(387)

¥ 1,867 ¥ 1,352 ¥209 ¥ 864 ¥ 516 ¥ 13 $15,534 $11,250 $1,736

82 Annual Report 2015

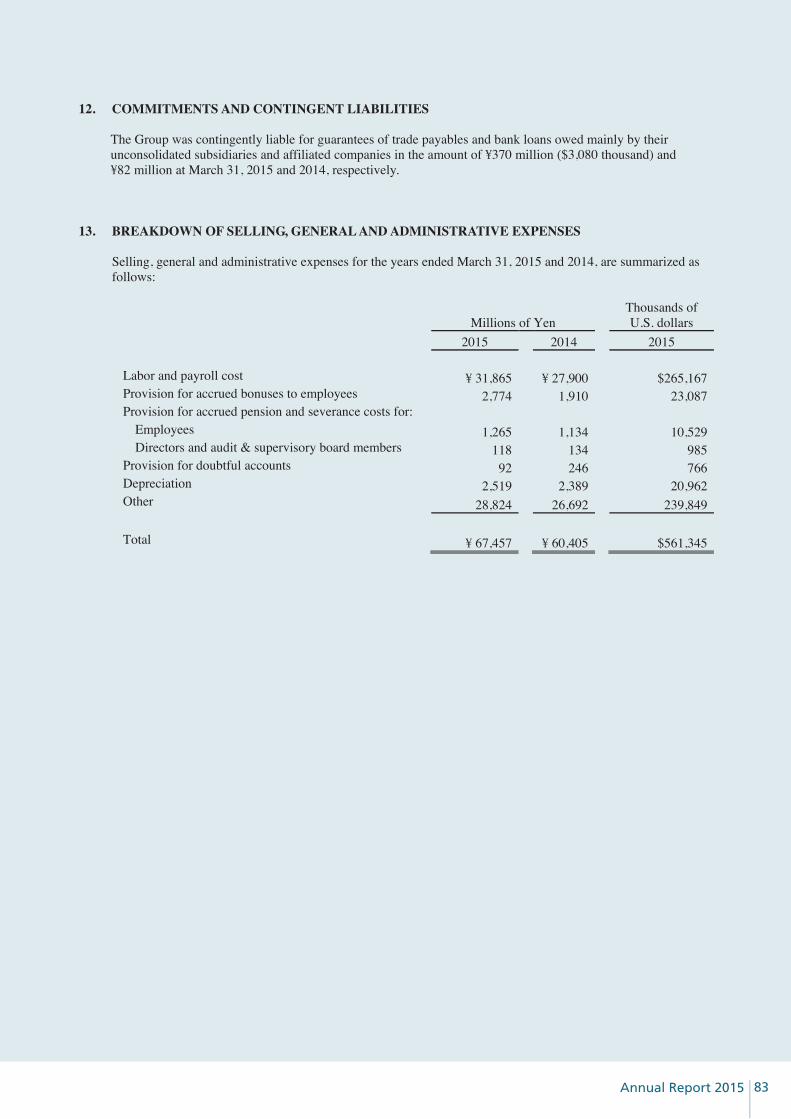

12. COMMITMENTS AND CONTINGENT LIABILITIES

The Group was contingently liable for guarantees of trade payables and bank loans owed mainly by their unconsolidated subsidiaries and affiliated companies in the amount of ¥370 million ($3,080 thousand) and ¥82 million at March 31, 2015 and 2014, respectively.

13. BREAKDOWN OF SELLING, GENERAL AND ADMINISTRATIVE EXPENSES

Selling, general and administrative expenses for the years ended March 31, 2015 and 2014, are summarized as follows:

Millions of Yen Thousands of U.S. dollars

2015 2014 2015

Labor and payroll cost ¥ 31,865 ¥ 27,900 $265,167 Provision for accrued bonuses to employees 2,774 1,910 23,087 Provision for accrued pension and severance costs for:

Employees 1,265 1,134 10,529 Directors and audit & supervisory board members 118 134 985

Provision for doubtful accounts 92 246 766 Depreciation 2,519 2,389 20,962 Other 28,824 26,692 239,849

Total ¥ 67,457 ¥ 60,405 $561,345

83Annual Report 2015

14. COMPREHENSIVE INCOME

For the years ended March 31, 2015 and 2014

The components of other comprehensive income consist of the following:

Millions of Yen Thousands of U.S. Dollars

2015 2014 2015

Unrealized gain (loss) on available-for-sale securities Gains arising during the year ¥ 200 ¥ 229 $ 1,662 Reclassification adjustments to profit or loss (8 ) (47) (61) Amount before income tax effect 192 182 1,601 Income tax effect (12 ) (48) (105) Total 180 134 1,496

Deferred gains or losses on hedges Gains arising during the year 11 5 93 Reclassification adjustments to profit or loss – – – Amount before income tax effect 11 5 93 Income tax effect – – – Total 11 5 93

Foreign currency translation adjustments Adjustments arising during the year 9,040 6,161 75,235 Reclassification adjustments to profit or loss – – – Amount before income tax effect 9,040 6,161 75,235 Income tax effect – – – Total 9,040 6,161 75,235

Share of other comprehensive income in associates Gains arising during the year 97 105 808

Pension liability adjustment Adjustments arising during the year (273 ) (258) (2,271) Reclassification adjustments to profit or loss 329 266 2,737 Amount before income tax effect 56 8 466 Income tax effect (51 ) (63) (426) Total 5 (55) 40

Gains or losses on change in shares in consolidated subsidiaries

Gains arising during the year 53 – 439 Reclassification adjustments to profit or loss – – – Amount before income tax effect 53 – 439 Income tax effect – – – Total 53 – 439

Total other comprehensive income ¥ 9,386 ¥ 6,350 $78,111

84 Annual Report 2015

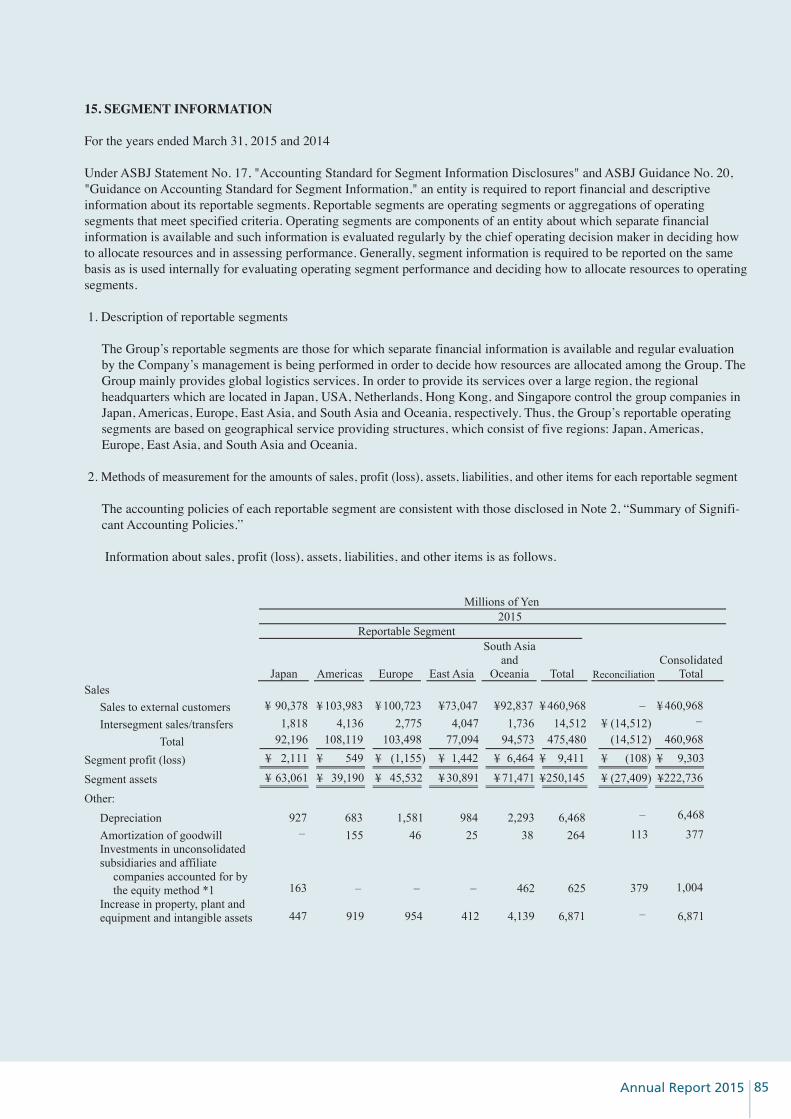

15. SEGMENT INFORMATION

For the years ended March 31, 2015 and 2014

Under ASBJ Statement No. 17, "Accounting Standard for Segment Information Disclosures" and ASBJ Guidance No. 20, "Guidance on Accounting Standard for Segment Information," an entity is required to report financial and descriptive information about its reportable segments. Reportable segments are operating segments or aggregations of operating segments that meet specified criteria. Operating segments are components of an entity about which separate financial information is available and such information is evaluated regularly by the chief operating decision maker in deciding how to allocate resources and in assessing performance. Generally, segment information is required to be reported on the same basis as is used internally for evaluating operating segment performance and deciding how to allocate resources to operating segments.

1. Description of reportable segments

The Group’s reportable segments are those for which separate financial information is available and regular evaluation by the Company’s management is being performed in order to decide how resources are allocated among the Group. The Group mainly provides global logistics services. In order to provide its services over a large region, the regional headquarters which are located in Japan, USA, Netherlands, Hong Kong, and Singapore control the group companies in Japan, Americas, Europe, East Asia, and South Asia and Oceania, respectively. Thus, the Group’s reportable operating segments are based on geographical service providing structures, which consist of five regions: Japan, Americas, Europe, East Asia, and South Asia and Oceania.

2. Methods of measurement for the amounts of sales, profit (loss), assets, liabilities, and other items for each reportable segment

The accounting policies of each reportable segment are consistent with those disclosed in Note 2, “Summary of Signifi-cant Accounting Policies.”

Information about sales, profit (loss), assets, liabilities, and other items is as follows.

Japan Americas Europe East Asia

South Asiaand

Oceania Total Reconciliation Consolidated

Total Sales

Sales to external customers Intersegment sales/transfers

Total Segment profit (loss) Segment assets Other:

Depreciation Amortization of goodwill Investments in unconsolidated subsidiaries and affiliate

companies accounted for by the equity method *1

Increase in property, plant and equipment and intangible assets

¥ 90,378

92,1961,818

927

163

447

¥ 2,111

¥ 63,061

Millions of Yen

Reportable Segment 2015

–

–

¥ 103,983

108,1194,136

683

919

¥ 549

¥ 39,190

155

–

¥ 100,723

103,4982,775

1,581

954

¥ (1,155)

¥ 45,532

46

–

––

–

–

¥73,047

77,0944,047

984

412

¥ 1,442

¥ 30,891

25

¥92,837

94,5731,736

2,293

4,139

462

¥ 6,464

¥ 71,471

38

¥ 460,968 ¥¥

460,968

460,968475,48014,512 (14,512)

¥¥

(14,512)

(27,409)

(108)

6,468 6,468

6,8716,871

625

¥ 9,411 ¥ 9,303

¥250,145 ¥222,736

264 113 377

1,004379

85Annual Report 2015

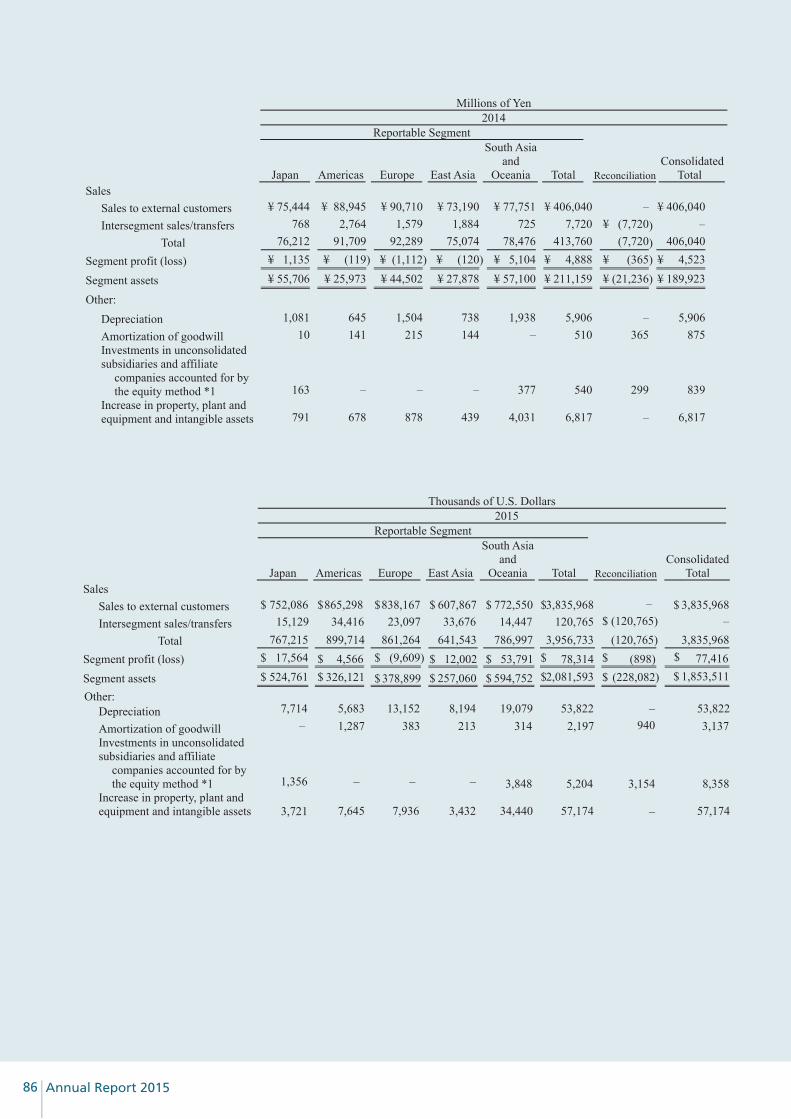

Thousands of U.S. Dollars

Reportable Segment

Japan Americas Europe East Asia

South Asiaand

Oceania Total ReconciliationConsolidated

Total Sales

Sales to external customers $ 752,086 865,298 Intersegment sales/transfers 15,129 34,416

4,566899,714

326,121

–

– Total 767,215

Segment profit (loss) $ 17,564 Segment assets $ 524,761

DepreciationAmortization of goodwill Investments in unconsolidated subsidiaries and affiliate

companies accounted for by the equity method *1

Increase in property, plant and equipment and intangible assets

Millions of Yen 4102 Reportable Segment

Japan Americas Europe East Asia

South Asiaand

Oceania Total Reconciliation Consolidated

Sales

Sales to external customers ¥ 75,444 ¥ 88,945 ¥ 90,710 ¥ 73,190 ¥ 77,751 ¥ 406,040 – ¥ 406,040Intersegment sales/transfers 768 2,764 1,579 1,884 725 7,720 ¥ (7,720) –

Total 76,212 91,709 92,289 75,074 78,476 413,760 (7,720) 406,040

Segment profit (loss) ¥ 1,135 ¥ (119) ¥ (1,112) ¥ (120) ¥ 5,104 ¥ 4,888 ¥ (365) ¥ 4,523

Segment assets ¥ 55,706 ¥ 25,973 ¥ 44,502 ¥ 27,878 ¥ 57,100 ¥ 211,159 ¥ (21,236) ¥ 189,923

Other:

Other:

Depreciation 1,081 645 1,504 738 1,938 5,906 – 5,906Amortization of goodwill 10 141 215 144 – 510 365 875Investments in unconsolidated subsidiaries and affiliate

companies accounted for by the equity method *1 163 – – – 377 540 299 839

Increase in property, plant and equipment and intangible assets 791 678 878 439 4,031 6,817 – 6,817

Total

2015

7,714

1,356

3,721

–

–

5,683

7,645

1,287

–

13,152

7,936

383

–

–

–

8,194

3,432

213

23,097 33,676

$$

$ 838,167

861,264

$ 607,867

641,543

$

(9,609)$

378,899$ 257,060$12,002$

19,079

34,440

3,848 3,154

31453,822

57,174

8,358

3,137940

14,447772,550

786,997

$

594,752 2,081,593$53,791

53,822

57,174

5,204

2,197

120,7653,835,968

3,956,733

$ 3,835,968

3,835,968

$

1,853,511$

(120,765)(120,765)

$

(228,082)$(898)$78,314$

$$ 77,416$

86 Annual Report 2015

*1: The reconciliation column for investments in unconsolidated subsidiaries and affiliated companies accounted for by the equity method contains investments which are not attributable to any reportable segments.

*2: The common assets mainly consisted of cash and deposits and investment securities.

Thousands of Millions of Yen U.S. Dollars

2015 2014 2015 Sales:

Elimination of intersegment transactions ¥ (14,512) ¥ (7,720) $ (120,765)

Total ¥ (14,512) ¥ (7,720) $ (120,765)

Thousands of Millions of Yen U.S. Dollars

2015 2014 2015 Segment profit:

Elimination of intersegment transactions – – –Amortization of goodwill ¥ (113) ¥ (365) $ (940)Others 5 0 42

Total ¥ (108) ¥ (365) $ (898)

Thousands of Millions of Yen U.S. Dollars

2015 2014 2015 Segment asset:

Elimination of intersegment receivables and payables ¥ (16,373) ¥ (10,834) $ (136,246)Elimination of intersegment investments and equity accounts (17,332) (16,208) (144,230)Common assets *2 6,383 5,893 53,114Others (87) (87) (720)

Total ¥ (27,409) ¥ (21,236) $ (228,082)

Notes: 1. The breakdown for the reconciliation of each item for the years ended March 31, 2015 and 2014, is as follows:

2. Segment profit (loss) is reconciled to operating income in the consolidated statement of income.

87Annual Report 2015

Related information

1. Information about services

2. Information about geographical areas

(1) Sales

Notes: (1) Sales are classified by country or region based on the location of customers. (2) Hong Kong is included in China.

The Group has omitted information about services as of March 31, 2015 and 2014, as sales to external customers in air and sea cargo is over 90% of consolidated sales.

Millions of Yen 2014

Japan Americas Europe East Asia South Asia

and Oceania Others Total U.S.A China

¥ 74,580 ¥ 73,418 ¥ 68,751 ¥ 78,063 ¥ 1 ¥ 406,040

Millions of Yen

2015

2015

Japan Americas Europe East Asia South Asia

and Oceania Others Total U.S.A China

¥ 89,308 ¥ 73,317

Thousands of U.S. Dollars

Japan Americas Europe East Asia South Asia

and Oceania Others Total U.S.A China

$ 743,183 $ 867,646 $ 3,835,968 $ 812,884 $839,676 $610,115 $564,707 $775,332 $16

¥ 104,265 ¥ 97,684 ¥100,904 ¥ 67,861 ¥ 93,172 ¥ 2 ¥ 460,968

¥ 89,137 ¥ 85,190 ¥ 90,841

88 Annual Report 2015

(2) Property, plant and equipment

(3) Information about major customers

The Group has omitted information about major customers, as sales to any particular customer is not over 10% of consolidated sales at March 31, 2015 and 2014.

(4) Information about loss on impairment of fixed assets

Millions of Yen 2015

Japan Americas Europe East Asia South Asia

and Oceania Total ¥ 369 – – – – ¥ 369

Millions of Yen 2014

Japan Americas Europe East Asia South Asia

and Oceania Total – – – ¥ 55 – ¥ 55

Thousands of U.S. Dollars 2015

Japan Americas Europe East Asia South Asia

and Oceania Total $3,074 – – – – $ 3,074

Change in presentationPrior to April 1, 2014, "Malaysia" was included in "South Asia and Oceania". Since the amount of property, plant and equipment in Malaysia become more than 10% of that in the consolidated balance sheet during the fiscal year ended March 31, 2015, such amount is disclosed separately. In accordance with this change in presentation, property, plant and equipment for the year ended March 31, 2014, was reclassified. The amount of "Malaysia" included in "South Asia and Oceania" for the year ended March 31, 2014 was ¥5,223 million.

Millions of Yen 2015

¥ 10,309 ¥ 7,817 ¥ 7,121 ¥ 14,017 ¥ 2,508 ¥ 20,391 ¥ 9,343 ¥ 5,223 ¥ 55,042

Millions of Yen 2014

Thousands of U.S. Dollars 2015

¥ 9,425 ¥ 9,394 ¥ 8,671 ¥ 12,862 ¥ 2,590 ¥ 25,065 ¥ 10,768 ¥ 6,912 ¥ 59,336

AmericasU.S.A Thailand Malaysia

Japan Europe East Asia South Asia and Oceania Total

$ 78,432 $ 78,175 $ 72,153 $ 107,034 $ 21,552 $ 208,576 $ 89,607 $ 57,523 $ 493,769

AmericasU.S.A Thailand Malaysia

Japan Europe East Asia South Asia and Oceania Total

AmericasU.S.A Thailand Malaysia

Japan Europe East Asia South Asia and Oceania Total

89Annual Report 2015

(5) Information about amortization of goodwill

Millions of Yen

5102

Amortization of goodwill

Goodwill at March 31, 2015

Japan Americas Europe East AsiaSouth Asia

and Oceania Elimination / Corporate Total

– ¥ 155 ¥ 46 ¥ 25 ¥ 38 ¥113 ¥ 377

– 1,696 491 515 – 230 2,932

Japan Americas Europe East AsiaSouth Asia

and Oceania Elimination / Corporate Total

¥10 ¥ 141 ¥215 ¥ 144 – ¥365 ¥ 875

– 1,598 581 487 – 296 2,962

Millions of Yen

4102

Amortization of goodwill

Goodwill at March 31, 2014

Thousands of U.S. Dollars

5102

Japan Americas Europe East AsiaSouth Asia

and Oceania Elimination / Corporate Total

Amortization of goodwill – $ 1,287 $ 383 $ 213 $ 314 $ 939 $ 3,136

Goodwill at March 31, 2015 – 14,110 4,089 4,285 – 1,917 24,401

90 Annual Report 2015

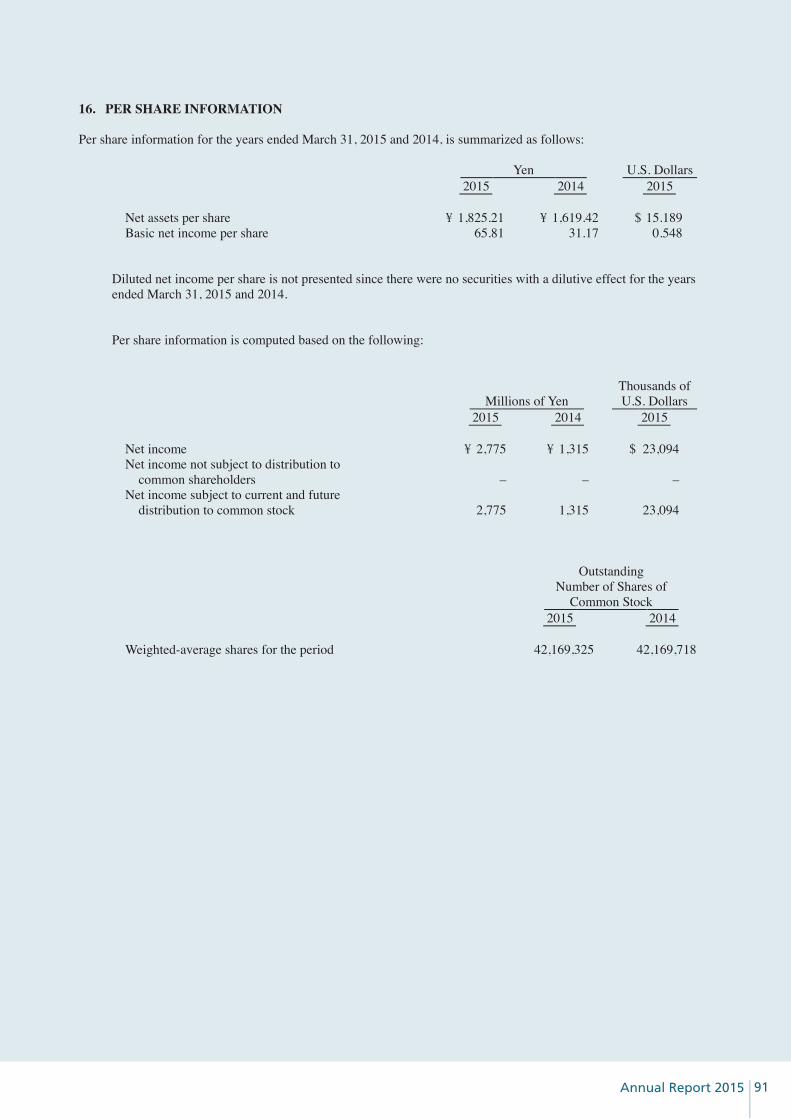

16. PER SHARE INFORMATION

Per share information for the years ended March 31, 2015 and 2014, is summarized as follows:

Yen U.S. Dollars 2015 2014 2015