financial accounting mgt101 power point slides lecture 39

TRANSCRIPT

Financial Accounting

1

Lecture – 39

Solution

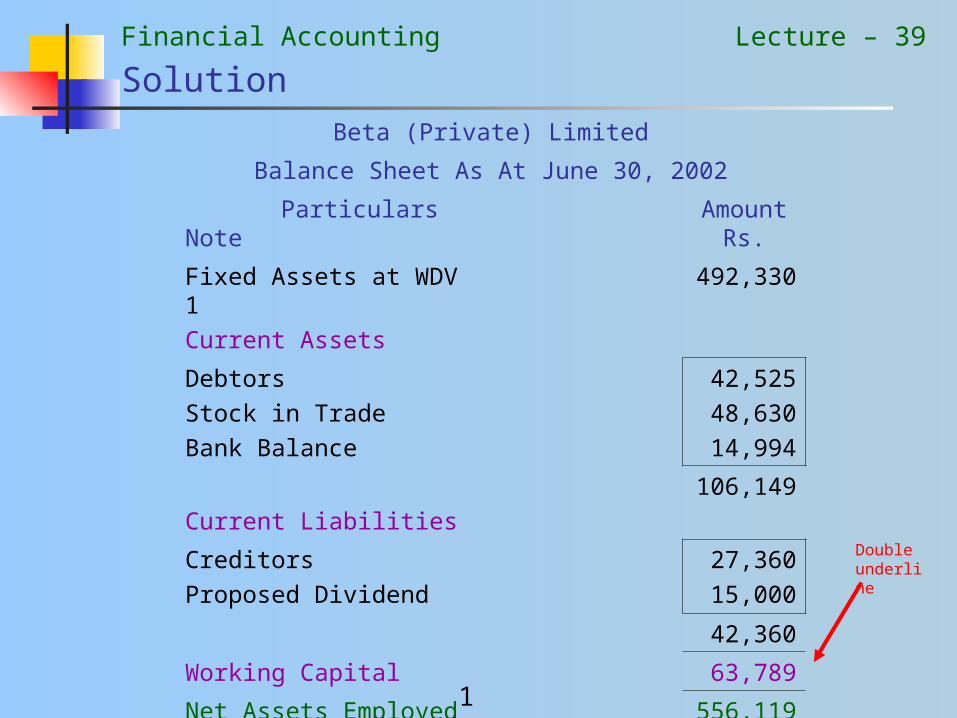

Beta (Private) Limited

Balance Sheet As At June 30, 2002

Particulars Note Amount Rs.

Fixed Assets at WDV 1Current Assets

492,330

DebtorsStock in TradeBank Balance

42,52548,63014,994

Current Liabilities106,149

CreditorsProposed Dividend

27,36015,000

42,360

Working Capital 63,789

Net Assets Employed 556,119

Double underline

Financial Accounting

2

Lecture – 39

Solution

Financed By:

Authorized Capital50,000 Shares of Rs. 10 each 500,000

Paid Up Capital30,000 Shares of Rs. 10 eachGeneral ReserveAccumulated Profit and Loss Account 2

300,0008,0008,119

Share Holders EquityDebentures

316,119240,000

Total 556,119

Double underline

Double underline

Note: Slide 1 and 2 will be shown together and then zoomed one by one as done in earlier lectures.

Financial Accounting

3

Lecture – 39

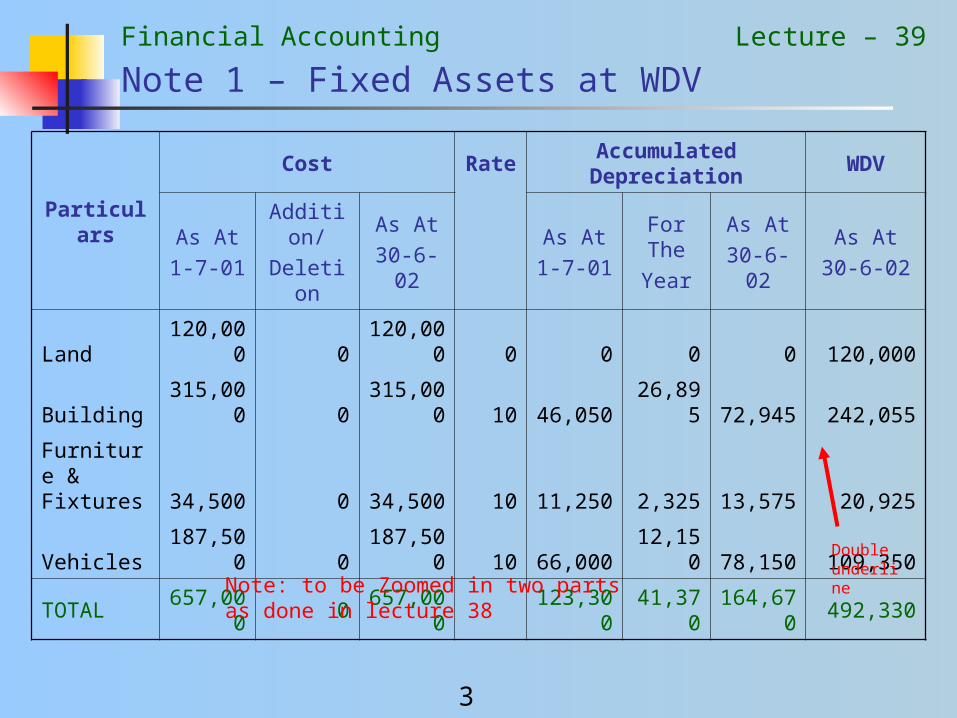

Note 1 – Fixed Assets at WDV

Particulars

Cost Rate Accumulated Depreciation WDV

As At

1-7-01

Addition/

Deletion

As At

30-6-02

As At

1-7-01

For The

Year

As At

30-6-02

As At

30-6-02

Land 120,000 0 120,000 0 0 0 0 120,000

Building 315,000 0 315,000 10 46,050 26,895 72,945 242,055

Furniture & Fixtures 34,500 0 34,500 10 11,250 2,325 13,575 20,925

Vehicles 187,500 0 187,500 10 66,000 12,150 78,150 109,350

TOTAL 657,000 0 657,000 123,300 41,370 164,670 492,330

Note: to be Zoomed in two parts as done in lecture 38

Double underline

Financial Accounting

4

Lecture – 39

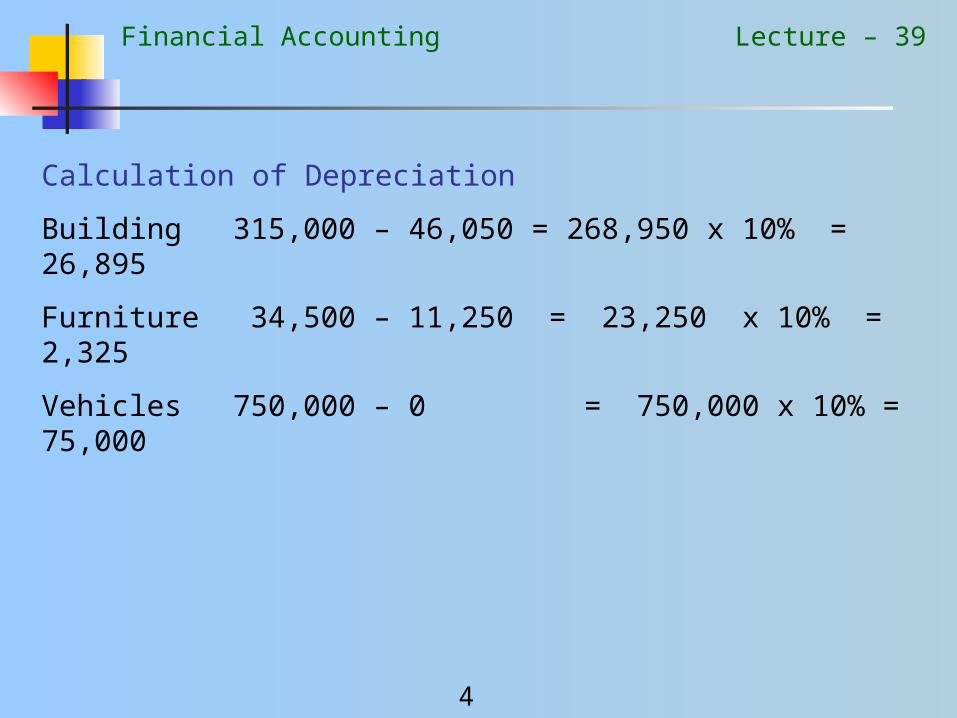

Calculation of Depreciation

Building 315,000 – 46,050 = 268,950 x 10% = 26,895

Furniture 34,500 – 11,250 = 23,250 x 10% = 2,325

Vehicles 750,000 – 0 = 750,000 x 10% = 75,000

Financial Accounting

5

Lecture – 39

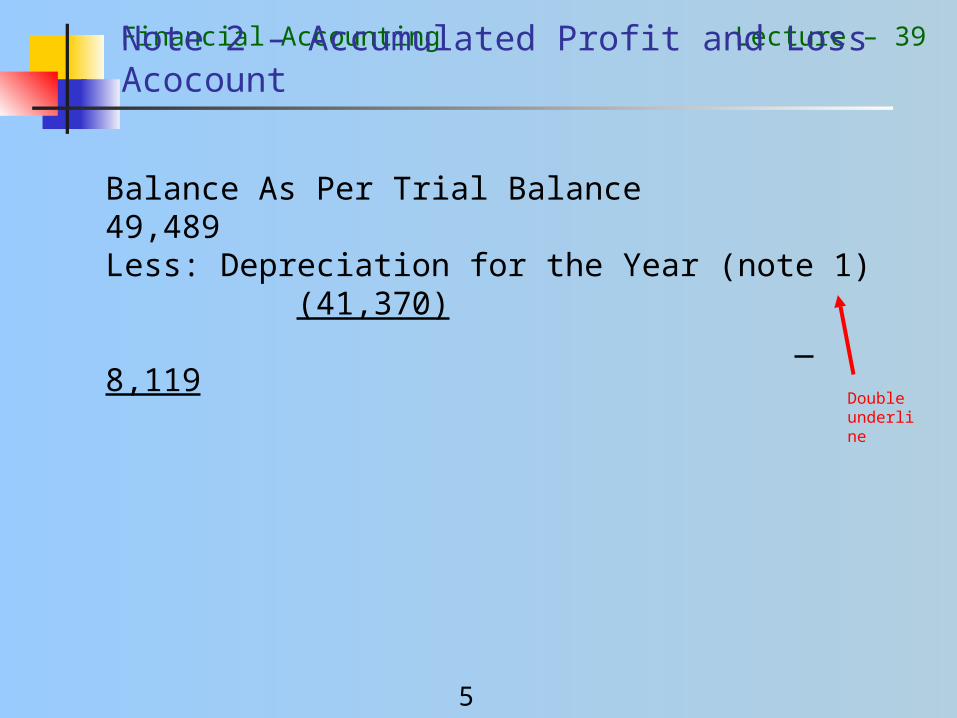

Note 2 – Accumulated Profit and Loss Acocount

Balance As Per Trial Balance 49,489Less: Depreciation for the Year (note 1)(41,370)

8,119

Double underline

Financial Accounting

6

Lecture – 39

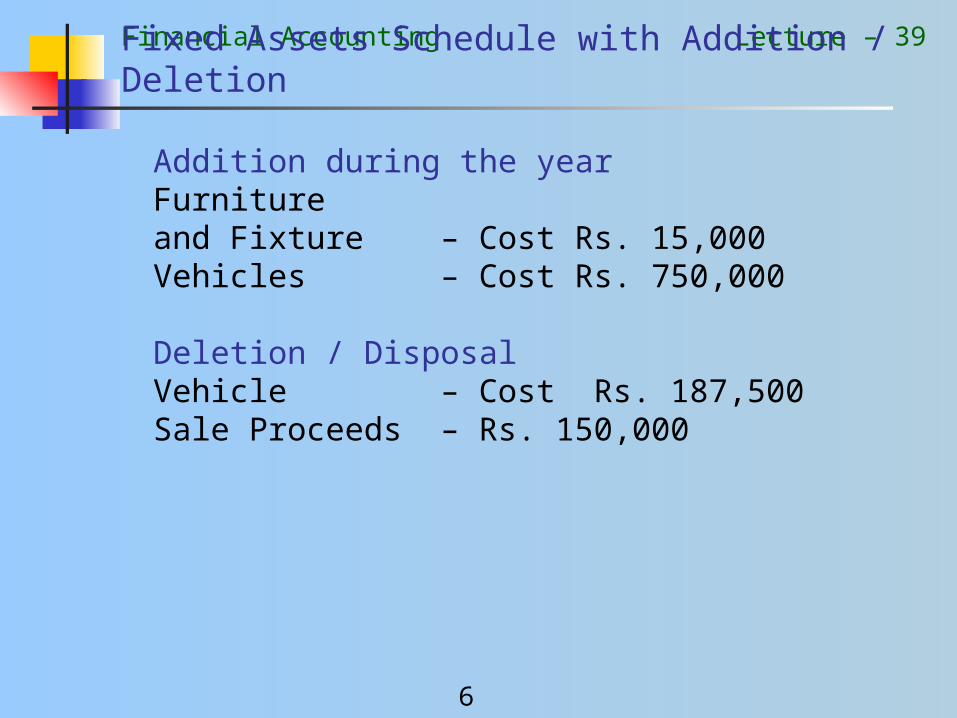

Fixed Assets Schedule with Addition / Deletion

Addition during the yearFurnitureand Fixture – Cost Rs. 15,000Vehicles – Cost Rs. 750,000

Deletion / DisposalVehicle – Cost Rs. 187,500Sale Proceeds – Rs. 150,000

Financial Accounting

7

Lecture – 39

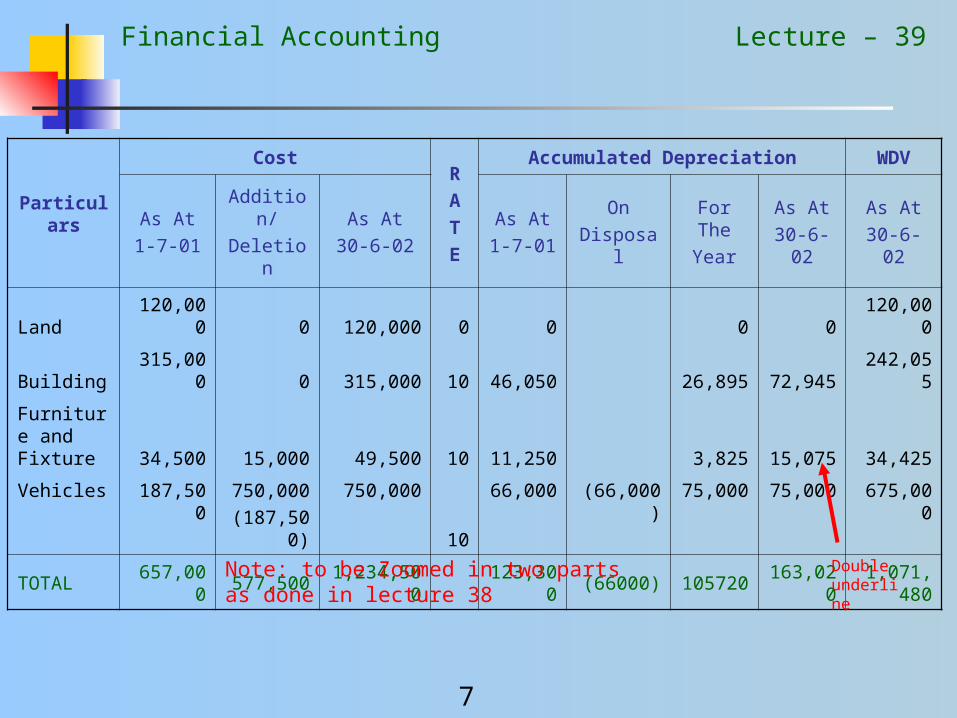

Particulars

CostR

A

T

E

Accumulated Depreciation WDV

As At

1-7-01

Addition/

Deletion

As At

30-6-02

As At

1-7-01

On

Disposal

For The

Year

As At

30-6-02

As At

30-6-02

Land 120,000 0 120,000 0 0 0 0 120,000

Building 315,000 0 315,000 10 46,050 26,895 72,945 242,055

Furniture and Fixture 34,500 15,000 49,500 10 11,250 3,825 15,075 34,425

Vehicles 187,500 750,000

(187,500)

750,000

10

66,000 (66,000) 75,000 75,000 675,000

TOTAL 657,000 577,500 1,234,500 123,300 (66000) 105720 163,020 1,071,480

Note: to be Zoomed in two parts as done in lecture 38

Double underline

Financial Accounting

8

Lecture – 39

Calculation of DepreciationBuilding 315,000 – 46,050 = 268,950 x 10% = 26,895Furniture 34,500 – 11,250 = 23,250 x 10% = 2,325

+ 15,000 x 10% = 1,500

OR 49,500 – 11,250 = 38,250 x 10% =

3,825

Vehicles 750,000 – 0 = 750,000 x 10% = 75,000

Financial Accounting

9

Lecture – 39

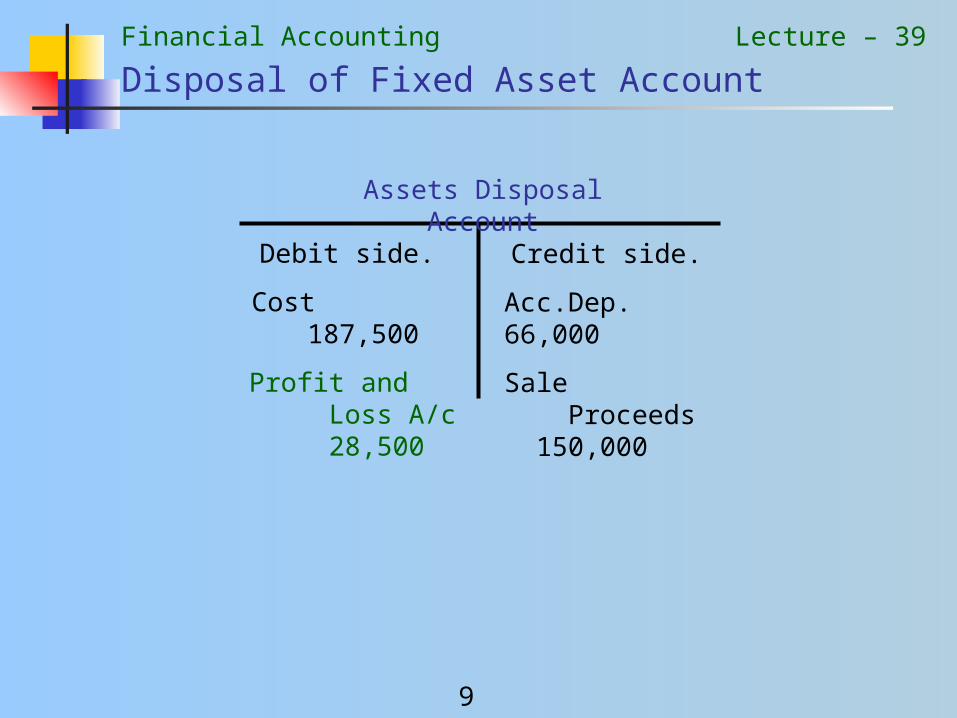

Disposal of Fixed Asset Account

Assets Disposal Account

Debit side.

Cost 187,500

Profit and Loss A/c 28,500

Credit side.

Acc.Dep. 66,000

Sale Proceeds 150,000

Financial Accounting

10

Lecture – 39

Question

• The following trial balance has been extracted from the books of Delta Limited as on June 30, 2002.

• You are required to prepare the profit and loss account for the year and the Balance Sheet as at June 30, 2002.

Financial Accounting

11

Lecture – 39

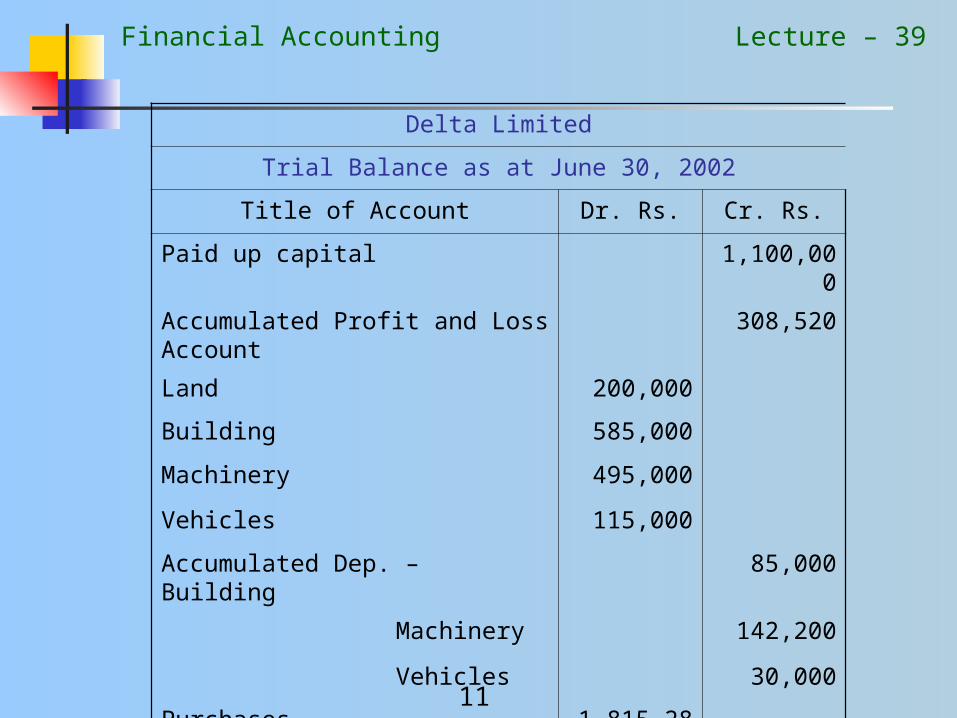

Delta Limited

Trial Balance as at June 30, 2002

Title of Account Dr. Rs. Cr. Rs.

Paid up capital 1,100,000

Accumulated Profit and Loss Account 308,520

Land 200,000

Building 585,000

Machinery 495,000

Vehicles 115,000

Accumulated Dep. – Building 85,000

Machinery 142,200

Vehicles 30,000

Purchases 1,815,282

Financial Accounting

12

Lecture – 39

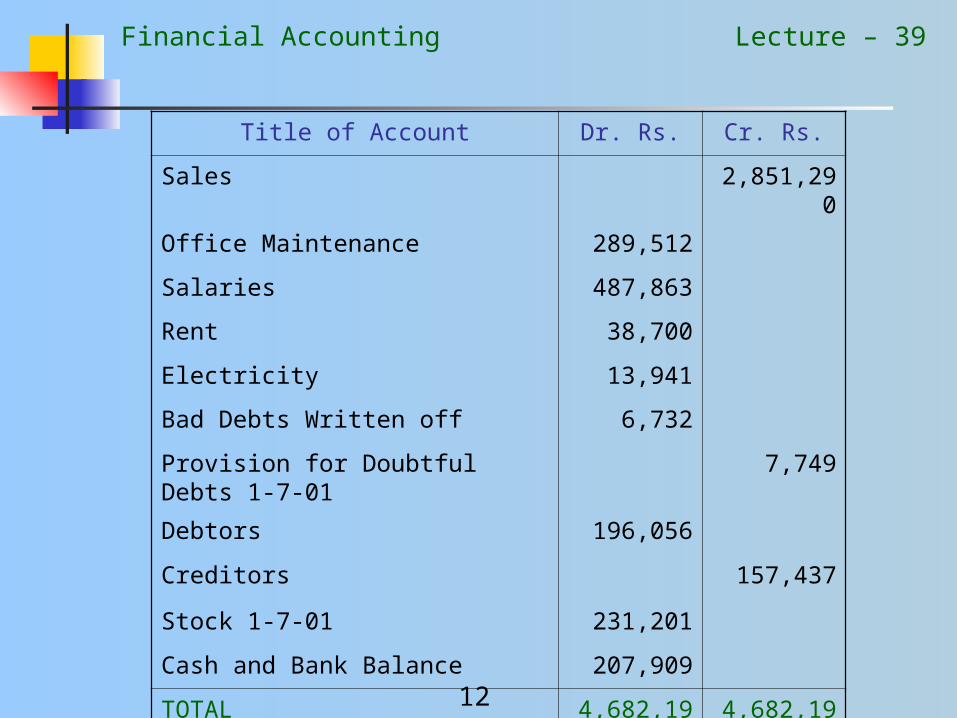

Title of Account Dr. Rs. Cr. Rs.

Sales 2,851,290

Office Maintenance 289,512

Salaries 487,863

Rent 38,700

Electricity 13,941

Bad Debts Written off 6,732

Provision for Doubtful Debts 1-7-01 7,749

Debtors 196,056

Creditors 157,437

Stock 1-7-01 231,201

Cash and Bank Balance 207,909

TOTAL 4,682,196 4,682,196

Financial Accounting

13

Lecture – 39

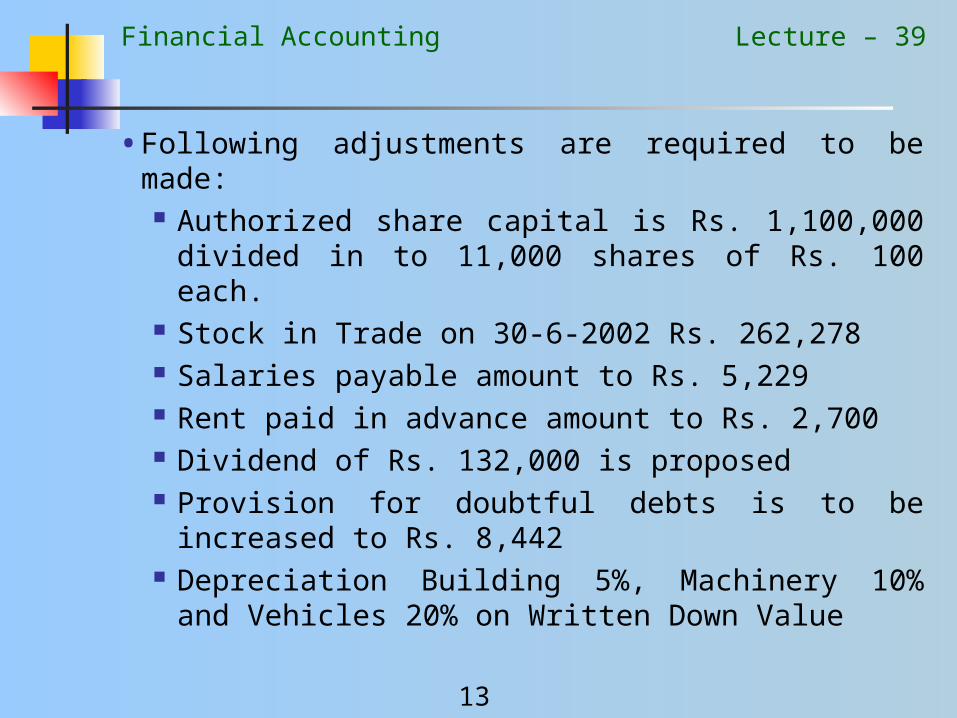

• Following adjustments are required to be made: Authorized share capital is Rs. 1,100,000 divided in to

11,000 shares of Rs. 100 each. Stock in Trade on 30-6-2002 Rs. 262,278 Salaries payable amount to Rs. 5,229 Rent paid in advance amount to Rs. 2,700 Dividend of Rs. 132,000 is proposed Provision for doubtful debts is to be increased to Rs.

8,442 Depreciation Building 5%, Machinery 10% and Vehicles

20% on Written Down Value

Financial Accounting

14

Lecture – 39

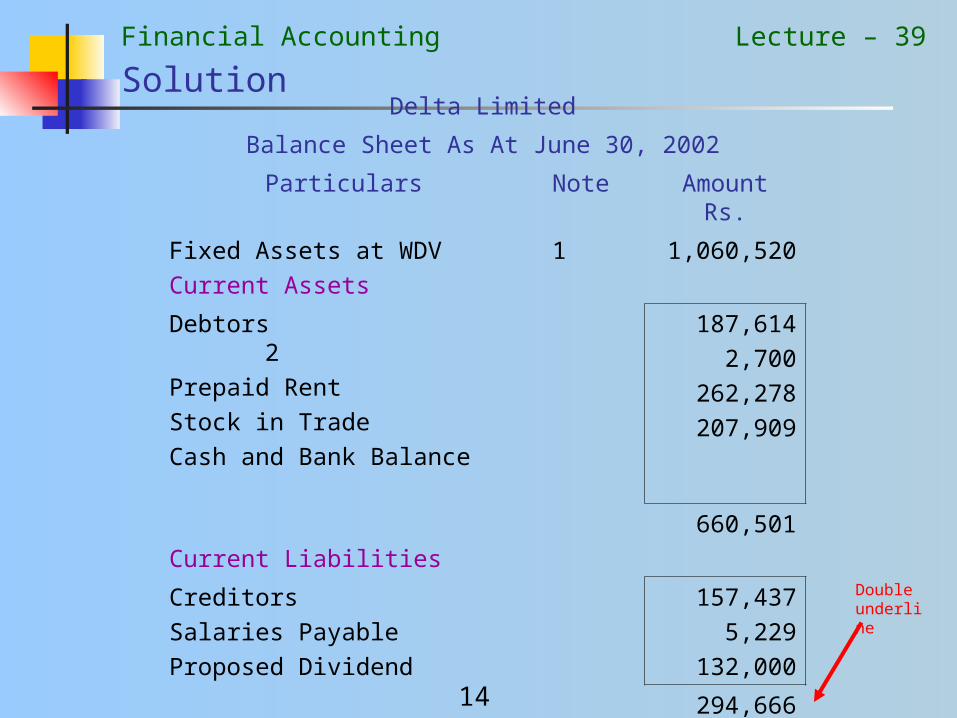

SolutionDelta Limited

Balance Sheet As At June 30, 2002

Particulars Note Amount Rs.

Fixed Assets at WDV 1

Current Assets

1,060,520

Debtors 2

Prepaid Rent

Stock in Trade

Cash and Bank Balance

187,614

2,700

262,278

207,909

Current Liabilities

660,501

Creditors

Salaries Payable

Proposed Dividend

157,437

5,229

132,000

294,666

Working Capital 365,835

Net Assets Employed 1,426,355

Double underline

Financial Accounting

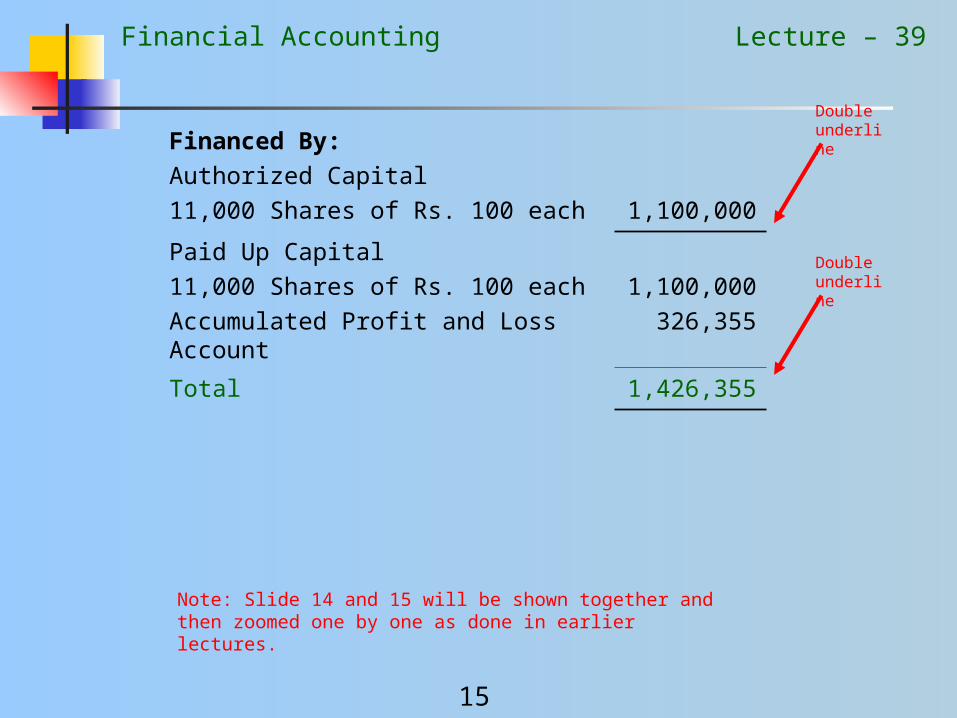

15

Lecture – 39

Financed By:

Authorized Capital11,000 Shares of Rs. 100 each 1,100,000

Paid Up Capital11,000 Shares of Rs. 100 eachAccumulated Profit and Loss Account

1,100,000326,355

Total 1,426,355

Note: Slide 14 and 15 will be shown together and then zoomed one by one as done in earlier lectures.

Double underline

Double underline

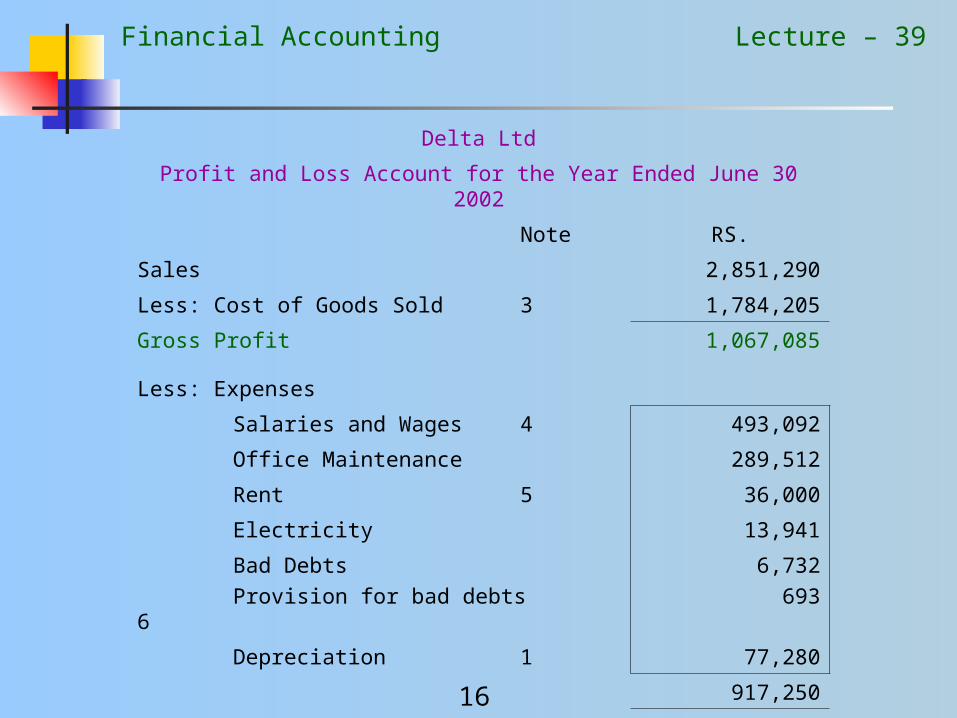

Financial Accounting

16

Lecture – 39

Delta Ltd

Profit and Loss Account for the Year Ended June 30 2002

Note RS.

Sales 2,851,290

Less: Cost of Goods Sold 3 1,784,205

Gross Profit 1,067,085

Less: Expenses

Salaries and Wages4 493,092

Office Maintenance 289,512

Rent 5 36,000

Electricity 13,941

Bad Debts

Provision for bad debts 6

6,732

693

Depreciation 1 77,280

917,250

Net Profit 149,835

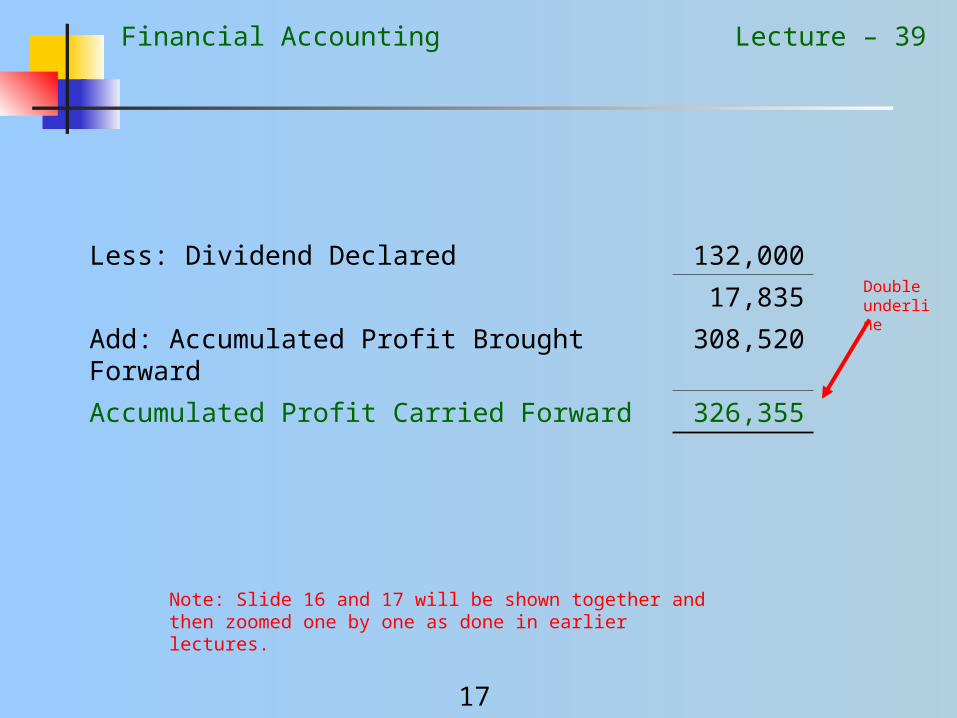

Financial Accounting

17

Lecture – 39

Less: Dividend Declared 132,000

17,835

Add: Accumulated Profit Brought Forward 308,520

Accumulated Profit Carried Forward 326,355

Double underline

Note: Slide 16 and 17 will be shown together and then zoomed one by one as done in earlier lectures.

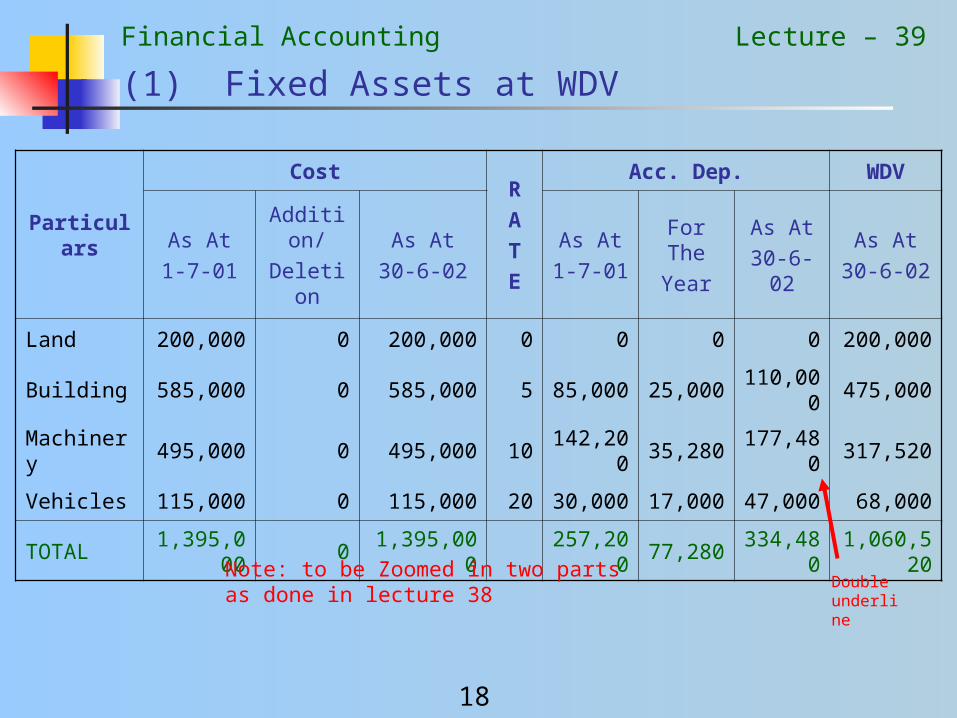

Financial Accounting

18

Lecture – 39

(1) Fixed Assets at WDV

Particulars

CostR

A

T

E

Acc. Dep. WDV

As At

1-7-01

Addition/

Deletion

As At

30-6-02

As At

1-7-01

For The

Year

As At

30-6-02

As At

30-6-02

Land 200,000 0 200,000 0 0 0 0 200,000

Building 585,000 0 585,000 5 85,000 25,000 110,000 475,000

Machinery 495,000 0 495,000 10 142,200 35,280 177,480 317,520

Vehicles 115,000 0 115,000 20 30,000 17,000 47,000 68,000

TOTAL 1,395,000 0 1,395,000 257,200 77,280 334,480 1,060,520

Double underline

Note: to be Zoomed in two parts as done in lecture 38

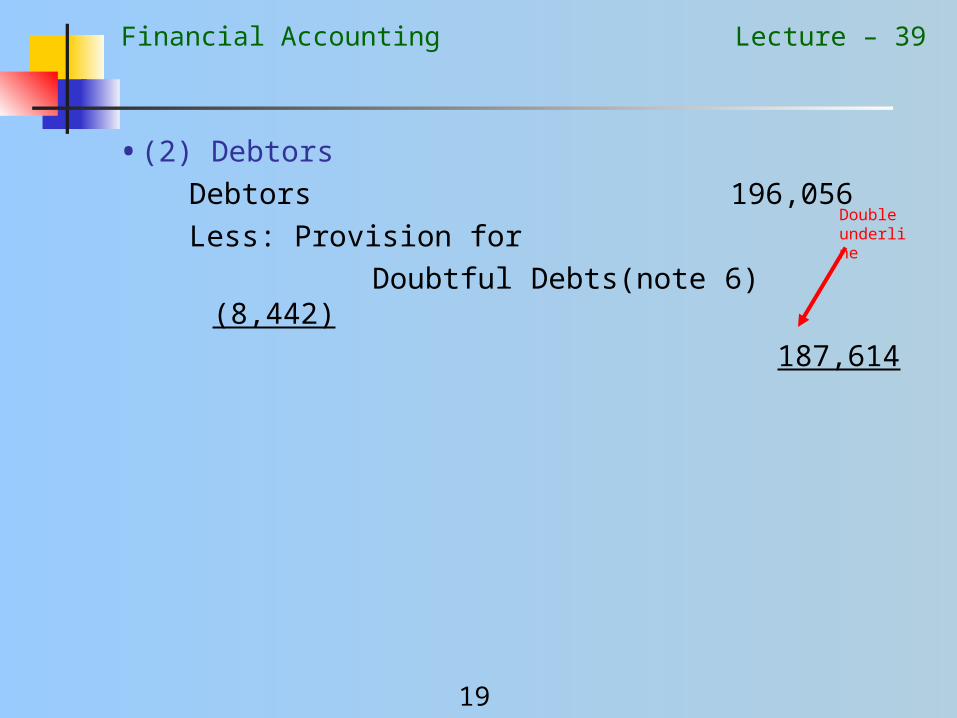

Financial Accounting

19

Lecture – 39

• (2) Debtors

Debtors 196,056

Less: Provision for

Doubtful Debts(note 6) (8,442)

187,614

Double underline

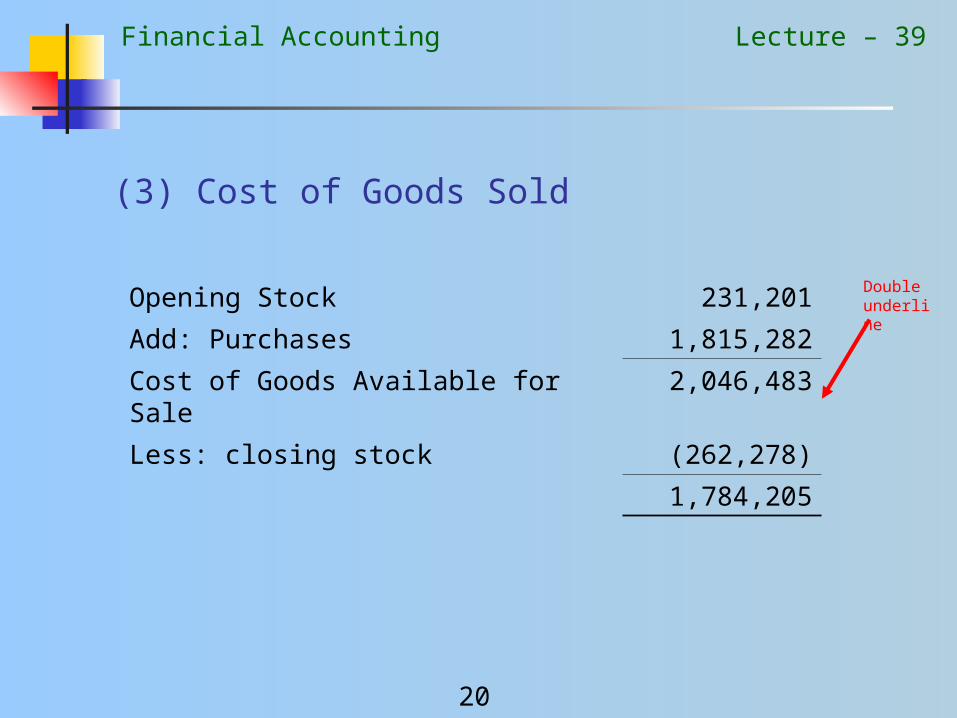

Financial Accounting

20

Lecture – 39

(3) Cost of Goods Sold

Opening Stock 231,201

Add: Purchases 1,815,282

Cost of Goods Available for Sale 2,046,483

Less: closing stock (262,278)

1,784,205

Double underline

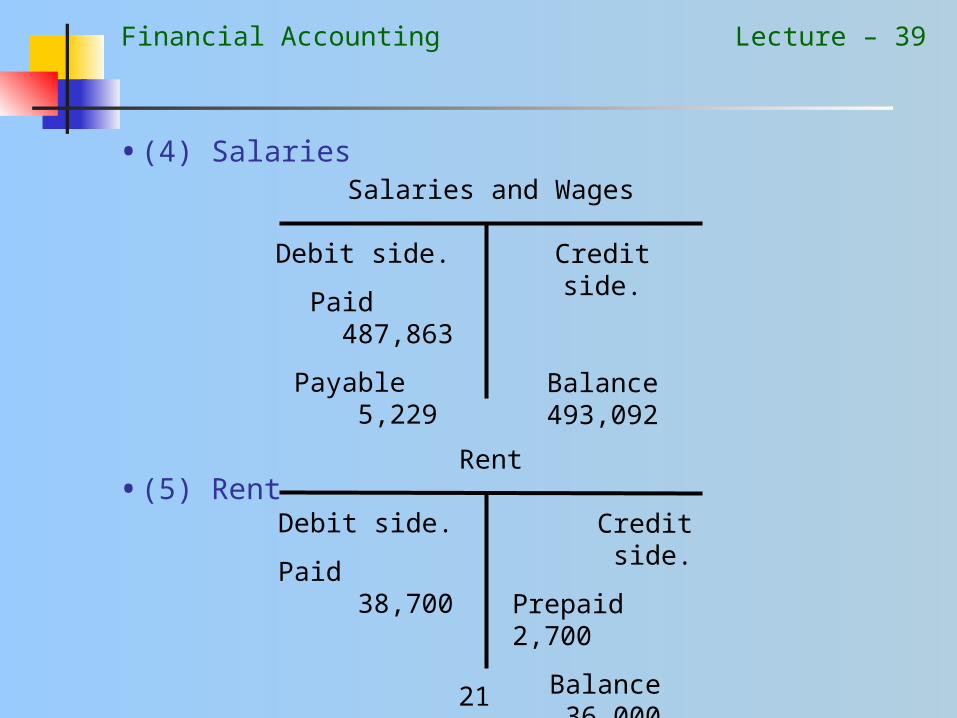

Financial Accounting

21

Lecture – 39

• (4) Salaries

• (5) Rent

Salaries and Wages

Debit side.

Paid 487,863

Payable 5,229

Credit side.

Balance 493,092

Rent

Debit side.

Paid 38,700

Credit side.

Prepaid 2,700

Balance 36,000

Financial Accounting

22

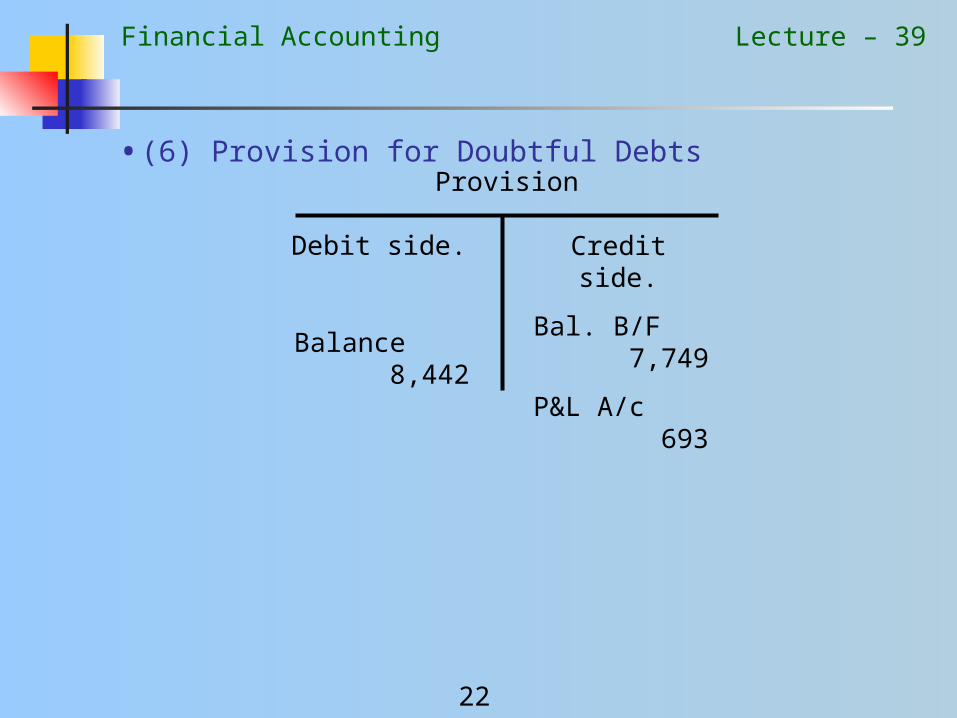

Lecture – 39

• (6) Provision for Doubtful DebtsProvision

Debit side.

Balance 8,442

Credit side.

Bal. B/F 7,749

P&L A/c 693