financial accounting, 10th edition solutions manual harrison · chapter 4 internal control &...

TRANSCRIPT

Chapter 4 Internal Control & Cash 4-1

Financial Accounting, 10th Edition Solutions Manual Harrison

Completed downloadable package SOLUTIONS MANUAL for Financial

Accounting, 10th Edition by Walter T. Harrison, Charles T. Horngren , C.

William Thomas. Solutions Manual, Answer key, Instructor's Resource Manual

for all chapters are included. Download link:

https://testbankreal.com/download/financial-accounting-10th-edition-

solutions-manual-harrison-horngren-thomas/

Chapter 4

Internal Control & Cash

Short Exercises

(5 min.) S 4-1

Fraud is an intentional misrepresentation of facts, made for the purpose

of persuading another party to act in such a way that causes injury or

damage to that party.

The Three Components of the Fraud Triangle 1. Motive — Fraud generally results from either critical need or greed on

the part of the perpetrator. Regardless of whether the driving force is

need or greed most perpetrators are driven to attempt to acquire

something that belongs to others.

2. Opportunity — The opportunity to commit fraud usually arises through

weak internal controls.

3. Rationalization — The perpetrator(s) is (are) convinced, in their own

minds, that they deserve the object of the fraudulent behavior. They may

Financial Accounting 10/e Solutions Manual 4-2

believe no one else will ever know or even that everybody else is engaging

in fraudulent behavior

Chapter 4 Internal Control & Cash 4-3

(5 min.) S 4-2 Clyde should report the errors to Lusk because Lusk is Clyde’s

supervisor, and Lusk is responsible for the errors. If Lusk fails to take

action, then Clyde should report the errors to Lusk’s supervisor in the

organization. Clyde should keep going up the chain of command until the

errors are corrected. In any event, outsiders who are relying on Otto

Brothers Limited’s financial statements must be made aware of the need

to correct the reported net income figure.

(10 min.) S4-3 A computer virus enters program code without your consent and

performs destructive action to your computer files or programs.

A Trojan Horse is a malicious computer program that hides inside a

legitimate program and works like a virus to corrupt your computer files

or programs.

A phishing expedition can be a Web site that attracts visitors who may be

tricked into revealing their account numbers, social security numbers,

passwords, or other valuable data. The creator of the Web site then uses

the unsuspecting Web-site visitors’ data to steal from them and for other

illicit purposes.

Financial Accounting 10/e Solutions Manual 4-4

(5-10 min.) S 4-4

COMPONENTS OF INTERNAL CONTROL

1. Control environment — Top managers must set the “tone at the top” to

establish a control environment.

2. Risk assessment — Each company must identify its own risks, based

upon its particular line of business, and establish procedures to minimize

the risks.

3. Control procedures — Specific procedures are needed for a good

system of internal control.

4. Monitoring of controls — Auditors can monitor a company’s actions

and its financial statements. Controls can also be programmed into the

information system.

5. Information system — Accurate information is essential for success in

business. Accounting information enters and exits through the

information system.

Student responses may vary for the descriptions.

(5-10 min.) S 4-5

Separation of duties is essential for safeguarding assets. The person who

has custody of an asset should not also account for the asset. A person

who performs both duties can steal the asset and hide the theft by making

a false entry in the accounting records.

Student responses may vary.

Chapter 4 Internal Control & Cash 4-5

(5-10 min.) S 4-6

There are several major internal control procedures as discussed in the

chapter besides separation of duties:

1. Smart hiring practices. The company should be careful to hire both

competent and honest personnel. Smart hiring practices involve

conducting background checks on job applicants, as well as training and

supervision on the job.

2. Comparisons and compliance monitoring. No person or department

should be allowed to completely process a transaction from beginning to

end without being checked by another person or a computer program.

Examples of comparisons and compliance monitoring are the use of

operating and cash budgets. Also, in key functions, one employee (or a

computer program) double checks the work of another for accuracy.

3. Adequate records help to assure that sufficient hard copy documents

or electronic information is kept by the entity to support the validity of

transactions that were processed. Examples include sales invoices,

purchase orders, shipping records, and customer remittance advices.

Among the benefits of adequate records is the ability to provide an audit

trail later for internal or external auditors to follow in auditing the entity’s

financial statements.

4. Limited access goes hand in hand with separation of duties to assure

that only authorized individuals are allowed access to (a) the assets of

Financial Accounting 10/e Solutions Manual 4-6

(continued) S 4-6

the company, such as cash or inventory; and (b) the records. Generally,

only people with custodial responsibilities (such as the cashier or the

warehouse personnel) should be allowed access to assets (such as cash

or inventory). Only people with recordkeeping responsibilities (such as

accountants) should have access to the company’s journals and ledgers.

5. Proper approvals. No transaction should be processed without

management’s general or specific approval. Generally, the larger the

transaction, the higher the organizational level of approval necessary.

Notice that the first letters of these attributes spell the acronym SCALP.

That’s an easy and comprehensive way to remember the control

procedures involved in internal controls.

(20-30 min.) S 4-7

Cash is important not because of its amount as reported on the balance

sheet, but because of its effect on a business. All transactions ultimately

affect cash. Businesses purchase assets and must pay cash. They make

sales and collect cash. All expenses ultimately require cash. Also, cash is

susceptible to theft because it is a medium of exchange. These factors

combine to give cash more importance than its account balance would

suggest.

Student responses may vary.

Chapter 4 Internal Control & Cash 4-7

(20-30 min.) S 4-8

Punching a hole through supporting documents reduces the

opportunity for fraud. Without this control procedure, a dishonest

employee could resubmit documents for payment a second time. The

employee could change the payee’s address and have the check sent

to an address the employee controls. Or the employee could arrange

to have the second payee split the payment with the employee.

Canceling the documents makes it difficult to get approval for a

duplicate payment.

Student responses may vary.

Financial Accounting 10/e Solutions Manual 4-8

(10 min.) S 4-9

Vincente Corp. Bank Reconciliation

August 31, 2014

BANK BOOKS

Balance, August 31 $4,775 Balance, August 31 $3,640

Add: Deposit in transit 300 Add: Bank collection 685

5,075 Interest revenue 20

4,345

Less: Less:

Outstanding checks (800) Service charge (15)

NSF check (55)

Adjusted bank balance $4,275 Adjusted book balance $4,275

Vincente has cash of $4,275.

(5 min.) S 4-10

Journal

DATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT

Aug. 31 Cash……………………………………….. 685 Accounts Receivable………………... 685 Collection on account. 31 Cash……………………………………….. 20 Interest Revenue……………………... 20 Interest earned on bank balance. 31 Miscellaneous Expense………………... 15 Cash……………………………………. 15 Bank service charge. 31 Accounts Receivable…………………… 55 Cash…………………………………….. 55 NSF check.

Chapter 4 Internal Control & Cash 4-9

(5 min.) S 4-11

It appears that the employee has stolen $710 (adjusted book balance,

$3,300 − adjusted bank balance, $2,590). The adjusted bank balance is the

company’s true cash balance, and the company books show more cash

on hand. Therefore, the books must be incorrect.

(5 min.) S 4-12

Sims will notice a gap in the sequence of sales receipts for the receipt that

Young destroyed. This knowledge will lead Sims to investigate what

happened to the missing receipt and what happened to the related cash.

(10 min.) S 4-13

1. Paying by check carries three controls over cash:

The check provides a record of the payment.

The check must be signed by an authorized official.

Before signing the check, the official should study the evidence

supporting the payment.

2. A dishonest purchasing agent could:

Purchase goods and have them delivered to his home or other location

that he controls.

Approve payment by the company for goods that he spent too much on,

and then split the excess with the supplier.

Companies avoid this internal control weakness by separating the

following duties related to the purchase of, and payment for, goods:

purchasing goods

receiving goods

approving and paying for goods

Financial Accounting 10/e Solutions Manual 4-10

(5-10 min.) S 4-14

Farm-to-Market (FM)

Cash Budget Year 2015

Millions

Cash balance, beginning $ 7

Estimated cash receipts—total 103

110

Estimated cash payments—total (97)

Cash available (needed) before new financing 13

Budgeted cash balance needed (11)

Cash available for additional investments $ 2

(5 min.) S 4-15

“Cash and cash equivalents” includes liquid assets such as time

deposits, certificates of deposit, and high-grade U.S. or foreign

government securities that are very close to maturity (three months or

less at the time of purchase). Besides cash, all of these listed are

considered to be “cash equivalents”—items quickly and easily converted

to cash.

Chapter 4 Internal Control & Cash 4-11

Exercises

(5-20 min.) E 4-16A

a. Higaredo has access to the cash collected, and he also prepares the

cash report. With access to both items, Higaredo can steal cash and

falsify his cash report to conceal his theft.

b. Valdez prepares the purchase order and also receives the goods. She

can add some items to the purchase order and have these extra items

shipped to a location she controls. When the goods come in, she

checks the incoming shipment, so there’s no outside party to learn of

her dishonesty.

Student responses may vary.

(10 min.) E 4-17A

Cash payments: a. Strong internal control. There is a good separation of duties.

Supervisors request equipment, and the home office purchases the

equipment.

b. Weak internal control. Supervisors request, purchase, and pay for

equipment with little oversight by the home office.

Cash receipts: a. Weak internal control. There is not a good separation of duties. The

accountant both handles cash and accounts for cash.

b. Strong internal control. There is a good separation of duties. Different

people handle cash and account for cash.

Financial Accounting 10/e Solutions Manual 4-12

(10 min.) E 4-18A

To prevent Munson’s embezzlement, Downtown Columbia’s board of

directors could have:

a. Not permitted Munson to write checks for Downtown Columbia.

Instead, appoint a board member to write the checks.

b. Not permitted Munson to receive cash that came to Downtown

Columbia. Have subscriber checks sent to a post office box

belonging to a bank and have the bank collect the checks.

c. Supervised Munson’s work by examining Downtown Columbia’s

documents such as paid checks.

d. Had an audit of Downtown Columbia’s transactions and financial

statements.

Student responses may vary.

Chapter 4 Internal Control & Cash 4-13

(10-20 min.) E 4-19A

F.L. Callan

Bank Reconciliation March 31, 2015

BANK:

Balance, March 31 $ 409

Add: Deposit in transit 1,325

Less: Outstanding checks:

Check No.

626 $ 90

627 270 (360)

Adjusted bank balance $1,374

BOOKS:

Balance, March 31 $1,472

Less:

Correction of book error —

Recorded $81 check as $18 $ 63

NSF check 28

Service charge 7 (98)

Adjusted book balance $1,374

Financial Accounting 10/e Solutions Manual 4-14

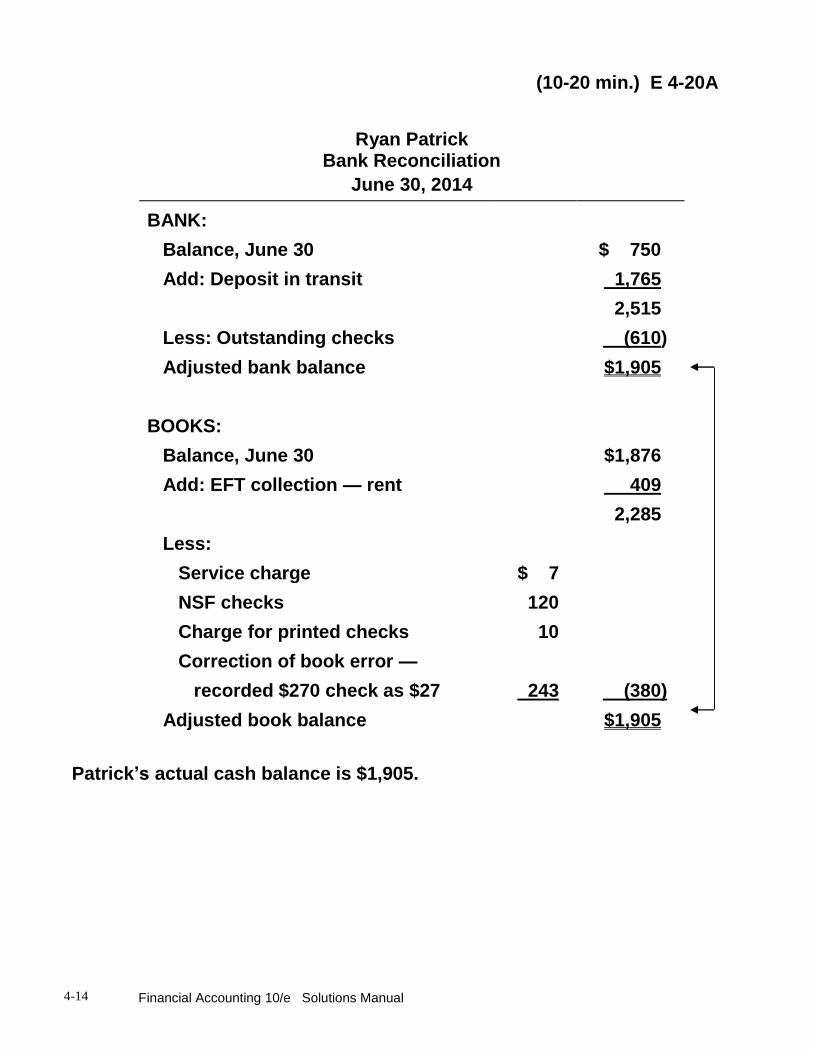

(10-20 min.) E 4-20A

Ryan Patrick

Bank Reconciliation

June 30, 2014

BANK:

Balance, June 30 $ 750

Add: Deposit in transit 1,765

2,515

Less: Outstanding checks (610)

Adjusted bank balance $1,905

BOOKS:

Balance, June 30 $1,876

Add: EFT collection — rent 409

2,285

Less:

Service charge $ 7

NSF checks 120

Charge for printed checks 10

Correction of book error —

recorded $270 check as $27 243 (380)

Adjusted book balance $1,905

Patrick’s actual cash balance is $1,905.

Chapter 4 Internal Control & Cash 4-15

(10-15 min.) E 4-21A

Journal DATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT

June 30 Cash .............................................................. 409 Rent Revenue .......................................... 409 EFT collection of rent. 30 Miscellaneous Expense ($7 + $10) .............. 17 Cash......................................................... 17 Bank service charge and charge for printed checks. 30 Accounts Receivable ................................... 120 Cash......................................................... 120 NSF checks returned by bank. 30 Salary Expense ($270 − $27) ....................... 243 Cash......................................................... 243 Correction of book error.

Financial Accounting 10/e Solutions Manual 4-16

(10-15 min.) E 4-22A

TO: Store Manager

FROM: Student

SUBJECT: Evaluation of internal control and plan for improvement

There is a weakness in internal control over cash receipts. The cash

registers do not keep a record of sales. With no record, there is no way to

determine how much cash should be in the cash drawer. This omission

makes it easy for the cashier to steal cash and not get caught.

To improve internal control, the company should use cash registers that

record each sale, and tabulate total cash sales each day. The manager can

prove the amount of cash in the cash drawer against this recorded

amount.

Chapter 4 Internal Control & Cash 4-17

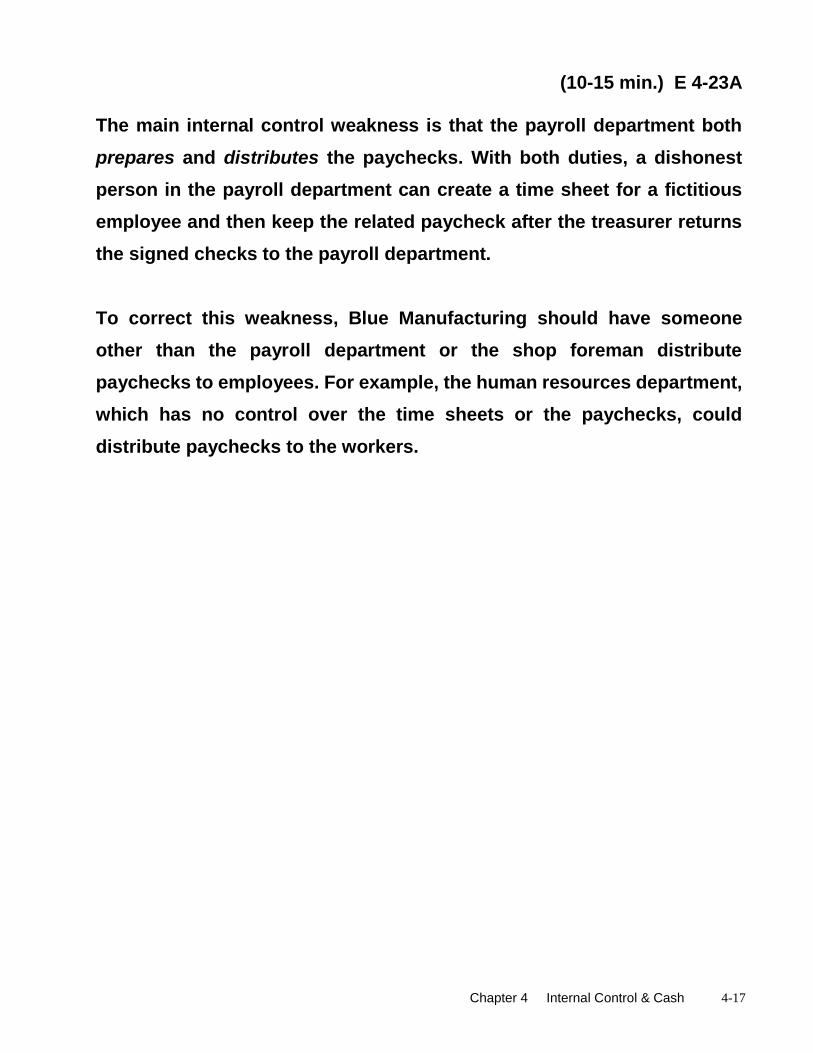

(10-15 min.) E 4-23A The main internal control weakness is that the payroll department both

prepares and distributes the paychecks. With both duties, a dishonest

person in the payroll department can create a time sheet for a fictitious

employee and then keep the related paycheck after the treasurer returns

the signed checks to the payroll department.

To correct this weakness, Blue Manufacturing should have someone

other than the payroll department or the shop foreman distribute

paychecks to employees. For example, the human resources department,

which has no control over the time sheets or the paychecks, could

distribute paychecks to the workers.

Financial Accounting 10/e Solutions Manual 4-18

(20-30 min.) E 4-24A

Dexter Communications, Inc.

Cash Budget

Year Ended December 31, 2015

Millions

Cash balance, December 31, 2014 $ 68

Budgeted cash receipts:

Collections from customers 11,325

Sale of assets 157

11,550

Budgeted cash payments:

Payments for cost of

services and products $6,196

Payments of operating expenses 2,553

Investment in equipment 1,822

Payment of debt 538

Payment of dividends 348 11,457

Cash available (needed) before financing 93

Budgeted cash balance, December 31, 2015 (70)

Cash available for additional investments, or

(New financing needed) $ 23

Dexter Communications expects to have cash available for additional

investments of $23 million during 2015.

Chapter 4 Internal Control & Cash 4-19

(5-20 min.) E 4-25B a. Kennedy has access to the cash collected, and he also prepares the

cash report. With access to both items, Kennedy can steal cash and

falsify his cash report to conceal his theft.

b. Morales prepares the purchase order and also receives the goods. She

can add some items to the purchase order and have these extra items

shipped to a location she controls. When the goods come in, she

checks the incoming shipment, so there’s no outside party to learn of

her dishonesty.

Student responses may vary.

(10 min.) E 4-26B

Cash payments:

a. Strong internal control. There is a good separation of duties.

Supervisors request equipment, and the home office purchases the

equipment.

b. Weak internal control. Supervisors both request, purchase, and pay for

equipment with little oversight by the home office.

Cash receipts:

a. Weak internal control. There is not good separation of duties. The

accountant both handles cash and accounts for cash.

b. Strong internal control. There is a good separation of duties. Different

people handle cash and account for cash.

Financial Accounting 10/e Solutions Manual 4-20

(10 min.) E 4-27B

To prevent Henry’s embezzlement, Downtown Huntsville’s board of

directors could have:

a. Not permitted Henry to write checks for Downtown Huntsville. Instead,

appoint a board member to write the checks.

b. Not permitted Henry to receive cash that came to Downtown Huntsville.

Have customer checks sent to a lock box belonging to the bank and

allow the bank to get the checks from the lock box.

c. Supervised Henry’s work by examining Downtown Huntsville’s

documents such as paid checks.

d. Had an audit of Downtown Huntsville’s transactions and financial

statements.

Student responses may vary.

Chapter 4 Internal Control & Cash 4-21

(10-20 min.) E 4-28B

A.C. Mazanek Bank Reconciliation

May 31, 2014

BANK:

Balance, May 31 $ 405

Add: Deposit in transit 1,320

Less: Outstanding checks:

Check No.

626 $ 75

627 265 (340)

Adjusted bank balance $1,385

BOOKS:

Balance, May 31 $1,452

Less:

Correction of book error —

Recorded $85 check as $58 $ 27

NSF check 37

Service charge 3 (67)

Adjusted book balance $1,385

Financial Accounting 10/e Solutions Manual 4-22

(10-20 min.) E 4-29B

Joe Donney

Bank Reconciliation

August 31, 2014

BANK:

Balance, August 31 $ 638

Add: Deposit in transit 1,695

2,333

Less: Outstanding checks (756)

Adjusted bank balance $1,577

BOOKS:

Balance, August 31 $1,620

Add: EFT collection — rent 375

1,995

Less:

Service charge $ 9

NSF checks 137

Charge for printed checks 20

Correction of book error —

recorded $280 check as $28 252 (418)

Adjusted book balance $1,577

Donney’s actual cash balance is $1,577.

Chapter 4 Internal Control & Cash 4-23

(10-15 min.) E 4-30B

Journal

DATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT

Aug 31 Cash ......................................................... 375 Rent Revenue ..................................... 375 EFT collection of rent. 31 Miscellaneous Expense ($9 + $20) ......... 29 Cash.................................................... 29 Bank service charge and charge for printed checks. 31 Accounts Receivable .............................. 137 Cash.................................................... 137 NSF checks returned by bank. 31 Salary Expense ($280 − $28) .................. 252 Cash.................................................... 252 Correction of book error.

Financial Accounting 10/e Solutions Manual 4-24

(10-15 min.) E 4-31B TO: Store Manager

FROM: Student

SUBJECT: Evaluation of internal control and plan for improvement

There is a weakness in internal control over cash receipts. The cash

registers do not keep a record of sales. With no record, there is no way to

determine how much cash should be in the cash drawer. This omission

makes it easy for the cashier to steal cash and not get caught.

To improve internal control, the company should use cash registers that

record each sale and tabulate total cash sales each day. The manager can

prove the amount of cash in the cash drawer against this recorded

amount.

Chapter 4 Internal Control & Cash 4-25

(10-15 min.) E 4-32B

The main internal control weakness is that the payroll department both

prepares and distributes the paychecks. With both duties, a dishonest

person in the payroll department can create a time sheet for a fictitious

employee and then keep the related paycheck after the treasurer returns

the signed checks to the payroll department.

To correct this weakness, Quick Kick should have someone other than

the payroll department or the shop foreman distribute paychecks to

employees. For example, the human resources department, which has no

control over the time sheets or the paychecks, could distribute paychecks

to the workers.

Financial Accounting 10/e Solutions Manual 4-26

(20-30 min.) E 4-33B

Carron Communications, Inc.

Cash Budget

Year Ended December 31, 2015

Millions

Cash balance, December 31, 2014 $ 72

Budgeted cash receipts:

Collections from customers 11,233

Sale of assets 108

11,413

Budgeted cash payments:

Payments for cost of

services and products $6,129

Payments of operating expenses 2,756

Investment in equipment 1,543

Payment of debt 611

Payment of dividends 316 11,355

Cash available (needed) before financing 58

Budgeted cash balance, December 31, 2015 (65)

Cash available for additional investments, or

(New financing needed) $ (7)

Carron expects to need new financing of $7 million during 2015.

Chapter 4 Internal Control & Cash 4-27

Quiz

Q4-34 c

Q4-35 a

Q4-36 b

Q4-37 d

Q4-38 b

Q4-39 c

Q4-40 c

Q4-41 d

Q4-42 a

Q4-43 d

Q4-44

Q4-45

c [$14,000 + $81,000 − $44,000 − $34,000 − $25,000 −

$13,000 = ($21,000); arrange financing for this

amount.]

e

Financial Accounting 10/e Solutions Manual 4-28

Problems

(15-20 min.) P 4-46A

The internal control weaknesses in English Imports’ system are:

1. O’Hara controls the content of the invoices. With no supervision of her

work, O’Hara could have the suppliers overstate their prices and then

arrange to have them split the excess with her after English Imports

pays the invoices.

2. Luck has both cash handling and accounting duties. With both

responsibilities, Luck could steal incoming cash and cover her theft by

manipulating the accounting records.

As with all small businesses, the key to effective internal control is

more owner involvement. Kregg could:

1. Make the purchase and pay arrangements with the English artisans

who supply English Imports’ products. Let O’Hara keep locating new

products, but don’t let her arrange for the purchases and payment.

2. Kregg could assign either cash handling or accounting duties to Luck

and then hire someone else to do the other (accounting or cash-

handling) duties. Also Kregg needs to perform the bank reconciliation

to keep her eye on cash receipts and cash payments.

Chapter 4 Internal Control & Cash 4-29

(10-20 min.) P 4-47A

Requirement 1 Requirement 2 Requirement 3

Missing Internal Control

Characteristic Possible Problem Solution a. Separation of

duties Theft of diamonds — the purchasing agent could have diamonds sent to a location he controls.

Separate purchasing, approval, and check-signing duties.

b. Assignment of

responsibility Lost revenue, because too many employees are managing the office and neglecting their duties.

Assign a single employee to manage the office when the owner is absent.

c. Separation of

duties Theft of cash. Separate

accounting and cash-handling duties.

Financial Accounting 10/e Solutions Manual 4-30

(20-30 min.) P 4-48A

Req. 1

Richmond Automotive

Bank Reconciliation

June 30, 2014

BANK:

Balance, June 30, 2014 $ 9,142

Add: Deposits in transit ($982 + $2,804) 3,786

12,928

Less: Outstanding checks —

Check No.

3119 $ 542

3120 987

3121 277

3122 2,406 (4,212)

Adjusted bank balance, June 30, 2014 $ 8,716

BOOKS:

Balance, June 30, 2014 $ 7,298

Add: EFT collection of rent $ 525

Bank collection of note receivable 1,375

Book error — $1,380 check

recorded as $1,830 450 2,350

9,648

Less: EFT payment of insurance $ 467

Unauthorized signature check 455

Service charge 10 (932)

Adjusted book balance, June 30, 2014 $ 8,716

Chapter 4 Internal Control & Cash 4-31

(continued) P 4-48A

Req. 2 (entries based on the reconciliation)

Journal

DATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT

June 30 Cash .................................................................. 525

Rent Revenue .............................................. 525

EFT deposit for rent revenue earned.

30 Cash .................................................................. 1,375

Note Receivable .......................................... 1,375

Note receivable collected by bank.

30 Cash .................................................................. 450

Accounts Payable ....................................... 450

Correction for check #3115 recorded incorrectly.

30 Insurance Expense ........................................... 467

Cash ............................................................. 467

EFT for payment of insurance.

30 Accounts Receivable ....................................... 455

Cash ............................................................. 455

US customer check returned by bank.

30 Miscellaneous Expense ................................... 10

Cash ............................................................. 10

Bank service charge.

Financial Accounting 10/e Solutions Manual 4-32

(continued) P 4-48A

Req. 3

A bank account helps control cash by providing a place for safekeeping.

The bank also provides a detailed list of the company’s cash transactions

that managers can compare to the company’s own cash records and

thereby correct any book errors quickly.

The bank reconciliation helps control cash by ensuring that the company

accounts for its cash transactions correctly and that the bank and book

records of cash are correct. Also, the bank reconciliation establishes the

balance of cash to report on the balance sheet.

Chapter 4 Internal Control & Cash 4-33

(30-45 min.) P 4-49A

Dallas Wireless

Cash Budget

2015

Thousands

Cash balance, beginning $ 1,600

Budgeted cash receipts:

Collections from customers ($61,000 × 1.25) 76,250

Receipt of interest 400

78,250

Budgeted cash payments:

Cash paid for inventory ($46,000 × 1.26) $57,960

Cash paid for operating expenses 13,200

Purchases of equipment 4,500

Purchases of investments 800

Payment of dividends 500

Payment of long-term debt 200 (77,160)

Cash available (needed) before financing 1,090

Budgeted cash balance, ending (4,675)

Cash available for additional investments, or

(New financing needed) $ (3,585)

Financial Accounting 10/e Solutions Manual 4-34

(15-20 min.) P 4-50B

The internal control weaknesses in Finnish Imports’ system are:

1. Martin controls the content of the invoices. With no supervision of her

work, Martin could have the suppliers overstate their prices and then

arrange to have them split the excess with her after Finnish Imports

pays the invoices.

2. Moore has both cash handling and accounting duties. With both

responsibilities, Moore could steal incoming cash and cover her theft

by manipulating the accounting records.

As with all small businesses, the key to effective internal controls is

more owner involvement. Ferguson could:

1. Make the purchase and pay arrangements with the artisans who supply

Finnish Imports’ products. Let Martin keep locating new products, but

don’t let her arrange for the purchases and payment.

2. Ferguson could assign either cash handling or accounting duties to

Moore and then hire someone else to do the other (accounting or cash-

handling) duties. Also Ferguson needs to perform the bank

reconciliation to keep her eye on cash receipts and cash payments.

Chapter 4 Internal Control & Cash 4-35

(10-20 min.) P 4-51B

Requirement 1 Requirement 2 Requirement 3

Missing Internal Control

Characteristic Possible Problem Solution a. Separation of duties Theft of cash or

diamonds by the purchasing agent.

Have a manager, not the purchasing agent, approve invoices for payment and sign the checks.

b. Assignment of

responsibilities Lost revenue due to delay of architectural drawings.

Assign one senior architect to fulfill management duties while Klepper is absent. Other senior architect should focus on producing architectural drawings.

c. Separation of duties Theft of cash. Keep accounting and

cash handling duties separate.

Financial Accounting 10/e Solutions Manual 4-36

(20-30 min.) P 4-52B Req. 1

Big City Automotive

Bank Reconciliation

July 31, 2014

BANK:

Balance, July 31, 2014 $ 9,693

Add: Deposits in transit ($986 + $2,801) 3,787

13,480

Less: Outstanding checks

Check No.

3119 $ 563

3120 972

3121 265

3122 2,831 (4,631)

Adjusted bank balance, July 31, 2014 $ 8,849

BOOKS:

Balance, July 31, 2014 $ 6,958

Add: EFT collection of rent $ 850

Bank collection of note receivable 1,350

Book error — $1,390 check recorded

as $1,930

540 2,740

9,698

Less: Unauthorized signature check $ 417

EFT payment of insurance 407

Service charge 25 (849)

Adjusted book balance, July 31, 2014 $ 8,849

Chapter 4 Internal Control & Cash 4-37

(continued) P 4-52B

Req. 2 (entries based on the reconciliation)

Journal

DATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT

July 31 Cash ................................................................... 850

Rent Revenue ............................................... 850

EFT deposit for rent revenue.

31 Cash ................................................................... 1,350

Note Receivable ........................................... 1,350

Note receivable collected by bank.

31 Cash ................................................................... 540

Accounts Payable ........................................ 540

Correction for check #3115 recorded incorrectly.

31 Accounts Receivable ........................................ 417

Cash .............................................................. 417

US customer check returned by bank.

31 Insurance Expense ........................................... 407

Cash .............................................................. 407

EFT for payment of insurance.

31 Miscellaneous Expense .................................... 25

Cash .............................................................. 25

Bank service charge.

Financial Accounting 10/e Solutions Manual 4-38

(continued) P 4-52B

Req. 3

A bank account helps control cash by providing a place for safekeeping.

The bank also provides a detailed list of the company’s cash transactions

that Big City Automotive managers can compare to the company’s own

cash records and thus correct any book errors quickly.

The bank reconciliation helps control cash by ensuring that the company

accounts for its cash transactions correctly and that the bank and book

records of cash are correct. Also, the bank reconciliation establishes the

balance of cash to report on the balance sheet.

Chapter 4 Internal Control & Cash 4-39

(30-45 min.) P 4-53B

Tampa Wireless

Cash Budget

2015

Cash balance, beginning $ 1,500

Budgeted cash receipts:

Collections from customers ($66,000 × 1.25) 82,500

Receipt of interest 100

84,100

Budgeted cash payments:

Cash paid for inventory ($50,000 × 1.24) $62,000

Cash paid for operating expenses 13,400

Purchase of equipment 4,800

Purchases of investments 400

Payment of dividends 200

Payments of long-term debt 600 (81,400)

Cash available (needed) before financing 2,700

Budgeted cash balance, ending (4,750)

Cash available for additional investments, or

(New financing needed) $ (2,050)

Financial Accounting 10/e Solutions Manual 4-40

Challenge Exercises and Problem

(15-25 min.) E 4-54

Wood could be: Brown could investigate by: 1. Writing business checks to

herself. 1. Performing the bank

reconciliation and examining all checks written by the business.

2. Submitting purchase invoices a

second time for duplicate payment, perhaps altering the mailing address on the duplicate invoice and sending the check to a post office box that Wood controls.

2. Examining purchase invoices for authenticity and comparing invoices to receiving reports to determine that the business received all goods it paid for. Any invoice with a hole indicates it was paid earlier. Calling the suppliers directly to inquire about any questionable invoices.

3. Paying suppliers excess

amounts and arranging for suppliers to kick back part of the excess to Wood.

3. Comparing the business’s ratio of cost of goods sold to retail selling price to the cost-to-retail ratio in the past. A kickback scheme would show up in higher cost figures and a lower profit percentage.

4. Making small cash payments to

herself. 4. Examining all cash records and

comparing the records to actual quantities of supplies and other items needed by the business.

Student responses may vary.

Chapter 4 Internal Control & Cash 4-41

(20-30 min.) E 4-55 Req. 1

Gateway Golf, Inc.

Cash Budget

Year Ended December 31, 2015

Thousands

Cash balance, December 31, 2014 $ 145

Budgeted cash receipts:

Collections from customers 20,400

Issuance of stock 632

21,177

Budgeted cash payments:

Purchases of inventory items $14,245

Payment of operating expenses 2,849

Purchase of property and equipment 1,588

Payment of long-term and short-term debt 990

Payment of dividends 307 (19,979)

Cash available (shortage) before financing 1,198

Budgeted cash balance, December 31, 2015 (135)

Cash available for additional investments $ 1,063

Req. 2

Current ratio = Total current assets

= $7,576

= 1.74 Total current liabilities $4,360

Debt ratio = Total liabilities

= $11,588

= 0.51 Total assets $22,677

I would lend $95 thousand to Gateway Golf because the company’s ratio

values are strong. Also, the cash budget indicates strong cash flows

during 2015.

Financial Accounting 10/e Solutions Manual 4-42

P 4-56

The Pembrook Company

Bank Reconciliation

December 31

BANK:

Balance, December 31 (corrected for erroneous

November outstanding checks)

$ 3,668

Add: Deposit in transit

Actual amount of December 30 deposit 650

4,318

Less: Outstanding checks

Check No.

1560 $185

1901 842

1902 168 (1,195)

Adjusted bank balance, December 31 $ 3,123

BOOKS:

Balance, December 31 $ 9,455

Add: Checks #1880, #1882, and #1883 recorded in both November and December

$1,155

EFT receipt from customer 52

Interest revenue 6 1,213

10,668

Less: NSF check $ 135

EFT payment of utility bill 755

Book error (overstatement of Dec. 24 deposit)

3,000

Unexplained difference 3,655 (7,545)

Adjusted book balance, December 31 $ 3,123

Chapter 4 Internal Control & Cash 4-43

(continued) P 4-56

Checks No. 1880, 1882, and 1883 were outstanding in November so should

not also be deducted from Cash in December. The unexplained difference

of $3,655 consists of $1,155 erroneous November outstanding checks and

the $2,500 difference between deposit in transit listed on the original

reconciliation and the amount of the deposit in transit listed on the books.

It is possible that the $3,000 difference between the December 23 deposit

on the books and the December 24 receipt on the bank statement was

intentional and used to cover up the missing cash.

Financial Accounting 10/e Solutions Manual 4-44

Decision Cases

(20-30 min.) Decision Case 1

Environmental Concerns, Inc.

Bank Reconciliation

September 30

BANK:

Balance, September 30 $ 8,224

Add: Deposit of September 30 in transit 3,794

12,018

Less: Outstanding checks ($116 + $150 +

$853 + $990 + $206 + $145) (2,460)

Adjusted bank balance, September 30 $ 9,558

BOOKS:

Balance, September 30 $10,402

Add: Bank collection 200

10,602

Less: Service charge $ 8

NSF check 36 (44)

Adjusted book balance, September 30 $10,558

Based on the above reconciliation, it appears the bookkeeper has stolen

$1,000, the difference between the adjusted bank and book amounts

($9,558 − $10,558). He understated the total of outstanding checks by

$1,000 to cover his theft.

Adjusted

balances

do not

agree.

Chapter 4 Internal Control & Cash 4-45

(continued) Decision Case 1

Benz should assign an employee with no cash-handling duties to prepare

the bank reconciliation. The bookkeeper should not perform this

duty, because a person who handles cash and also prepares the

reconciliation can steal cash and manipulate the reconciliation to cover

the theft. Perhaps Benz should prepare the reconciliation himself.

Financial Accounting 10/e Solutions Manual 4-46

(15-30 min.) Decision Case 2

The internal control weakness in this case is a lack of separation of duties.

The foreman performs too many duties.

1. The foreman hires the workers.

2. The foreman controls workers’ employment documents.

3. The foreman fills out workers’ time sheets and transmits all

documents to the home office.

4. The foreman passes out paychecks to workers.

5. The workers never go to the home office, so home-office personnel

do not even know whether all workers exist.

The foreman could steal from the company as follows: 1. The foreman could enter a fictitious worker into the payroll system

and fill out bogus time sheets for the fictitious employee. Then the

foreman could pocket the pay check written to the employee.

2. The foreman could enter more time than actually worked by an

employee and arrange to split the extra pay received by the worker.

3. The foreman could pad his own hours to receive pay for time that he

did not work.

The following actions will correct the internal control weakness:

1. The home office could have the construction workers come to the

office for processing their employee documents. Then the home

office would at least know that all the workers exist.

2. Have employees sign their own time sheets.

Chapter 4 Internal Control & Cash 4-47

(continued) Decision Case 2

3. Don’t allow Pickins to pass out paychecks. Have employees pick up

paychecks at corporate office or have another corporate employee go

and pass out paychecks. The check distributor should ask for a picture

identification.

4. Have a home-office employee compare signatures on the workers’ time

sheets to their signatures on file and, occasionally, to their

endorsements on the backs of their paychecks.

5. Occasionally — or always — have a home-office employee go to the

construction site to pass out paychecks.

6. Have a home-office employee go to the construction site occasionally

to “take attendance” of workers on duty that day. Then match the

names of workers on duty to the time sheets turned in at the end of the

week.

Financial Accounting 10/e Solutions Manual 4-48

Ethical Issues

Ethical Issue 1

1. Identify the ethical issue. You must decide whether it is ethical for the

auditor not to require the bank to record the loss.

2. What are the alternatives? Require the client to record the loss, or

permit the client not to record the loss.

3. Identify the stakeholders. The auditor, the bank, and the public at large

can be affected. The auditor’s reputation is on the line. The bank’s

financial statements are in question. The public can be affected if the

bank issues financial statements that include erroneous amounts.

Assess the possible outcomes. If the auditors require the bank to

record the loss, the auditor will keep his or her reputation intact. But

the auditor will lose the client and also lose the revenue from this large

audit. The accounting firm may then be unable to expand the firm as it

had hoped to do.

If the auditors okay the bank’s financial statements even after the bank

did not record the loss, the auditor would keep the bank as a client,

earn the audit revenue, and be able to expand the firm as planned. But

the bank’s financial statements would report erroneous amounts for

the notes receivable. People relying on the bank’s financial statements

may suffer losses as a result. The accounting firm’s reputation would

be hurt.

(continued) Ethical Issue 1

Chapter 4 Internal Control & Cash 4-49

4. Make the decision. The auditor should require the bank to record the

loss even if that means losing the bank as a client. By sticking to its

belief that the bank should record the loss, the auditors’ reputation will

not be harmed as it would by okaying financial statements that include

errors. It’s far better to lose a client than to lose your reputation.

Financial Accounting 10/e Solutions Manual 4-50

Ethical Issue 2

1. Identify the ethical issue. Galvin’s ethical issue is whether to use his

knowledge of The Salvation Army’s plans and of Nadar’s situation to

either party’s advantage (or disadvantage). Should Galvin help The

Salvation Army buy the land at the lowest price? Should he help Nadar

sell the land at the highest price? Galvin’s position presents him with

a conflict of interest.

2. What are the alternatives? There are several:

(a) Let other members of the Salvation Army board of directors know

of Nadar’s situation in order to help The Salvation Army buy the

land at a bargain price.

(b) Disclose Nadar’s situation to fellow board members and insist

that The Salvation Army pay market price ($3.6 million) for the

land.

(c) Advise Nadar of The Salvation Army’s plans and encourage her

to hold out for a high price on the sale of the land.

(d) Reveal nothing to The Salvation Army’s board or to Nadar and

take no part in the negotiation between the two parties.

(e) Take a temporary leave of absence from The Salvation Army

board for unspecified “personal reasons.”

3. Identify the stakeholders involved. Galvin, The Salvation Army, Nadar,

and Community Banks.

Assess the possible consequences. Disclosing Nadar’s weakened

condition to The Salvation Army board may help The Salvation Army

buy the land at a low price, depending on the ethical bearing of

Chapter 4 Internal Control & Cash 4-51

(continued) Ethical Issue 2

fellow board members. This would help The Salvation Army and hurt

Nadar, relative to her ability to sell the land at market value of $3.6

million. Insisting that The Salvation Army offer market price for the land

would seem fair to both parties, but that would betray the trust of Nadar.

And it may or may not sway the board to go along with a $3.6 million

offer for the land.

Making Nadar aware of The Salvation Army’s plans may help Nadar get

a higher price for the land than she would get otherwise. This would

betray the trust of other members of The Salvation Army’s board.

Remaining silent would preserve Galvin’s integrity. However, if either

The Salvation Army or Nadar ever learned of Galvin’s relationship with

the other party, they would wonder whether Galvin used the

information against them.

Taking a temporary leave of absence would preserve Galvin’s integrity

and remove him from the conflict of interest. It would also preserve

Galvin’s reputation for fairness and the reputation of Community Bank

for keeping depositor information confidential.

4. Make the decision. The authors would take the leave of absence and

hope other Salvation Army board members do not probe Galvin’s

“personal reasons.” This way neither The Salvation Army nor Nadar

can accuse Galvin of using inside information to the advantage of the

other party.

Ethical Issue 3

Financial Accounting 10/e Solutions Manual 4-52

1. Identify the ethical issue. French’s ethical issue is whether to tell IMS

personnel about Snicker Foods’ possible bankruptcy.

2. What are the alternatives?

(a) Keep quiet and let nature take its course, or

(b) Tell IMS’s top managers of Snicker’s possible

bankruptcy.

3. Identify the stakeholders involved. IMS, Snicker Foods, Community

Bank, and everyone connected to these organizations — owners,

employees, creditors, depositors, and their communities.

Assess the possible consequences. Telling IMS about Snicker’s

possible bankruptcy may help IMS avoid wasted effort on Snicker. This

may enable IMS to seek more profitable ventures and aid IMS’s

recovery. In turn, this may help IMS pay its loan to Community Bank.

4. Make the decision. French should not tell IMS of Snicker’s financial

difficulties (after all, Snicker isn’t bankrupt yet). French should let

nature take its course. Then she will protect the bank’s (and her own)

reputation for keeping client information confidential. In her aiding IMS

through the loan-restructuring process, French may try to help IMS find

other customers that can take up the slack if the sale to Snicker doesn’t

go through.

Chapter 4 Internal Control & Cash 4-53

Focus on Financials: Amazon.com, Inc.

(20-30 min.)

Req. 1 Cash equivalents include assets that are slightly less liquid than cash, but

similar enough to be reported together. Cash equivalents must be readily

convertible to known amounts of cash and close to maturity (with an

original maturity of three months or less at the time of purchase).

Req. 2 Amazon.com, Inc. includes in its cash equivalents highly liquid

instruments with an original maturity of three months or less at the time

of purchase.

Req. 3 Yes, Note 2- CASH, CASH EQUIVALENTS, AND MARKETABLE

SECURITIES

Cash equivalents and marketable securities include money market funds

and equity securities, foreign government and agency securities, U.S.

government and agency securities, corporate debt securities, asset-

backed securities, and other fixed income securities. Note 2 provides this

list of cash equivalents and marketable securities. The company does not

separately identify the cash equivalents.

Req. 4 Yes, this is cash or cash equivalents required to be restricted as collateral

for debt and other agreements. Stockholders should be aware of what

cash is actually available to the company and which cash is restricted.

Restricted cash is less liquid. From Note 2, restricted cash, cash

equivalents, and marketable securities equal $99 million at December 31,

2012.

Financial Accounting 10/e Solutions Manual 4-54

Focus on Analysis: YUM! Brands, Inc.

(20-30 min.)

Req. 1

1. Net income of $1,608 million, in the operating section.

2. Capital spending, which used $1,099 million, in the investing

section.

3. Repurchase of shares of common stock, which used $965 million,

in the financing section.

4. Depreciation and amortization, which provided $645

million. Actually, these are expenses that do not use cash, so they

are added back to income to arrive at cash provided by operations.

5. Dividends paid on common stock, which used $544 million, in the

financing section.

6. Acquisitions, which used $543 million, in the investing section.

7. Proceeds from refranchising of restaurants, which provided $364

million, in the investing section.

Req. 2

The following items mentioned in Item 9A (following the footnotes), are

also mentioned in the chapter:

“Management is responsible for establishing and maintaining

adequate internal control over financial reporting”. Management

concluded that internal control over financial reporting was

effective as of the end of the year.

An accounting firm evaluated the internal controls and reported on

their effectiveness.

Student responses will vary.

Chapter 4 Internal Control & Cash 4-55

Group Project

Student responses will vary. Reference download links: financial accounting 10th edition solutions financial accounting 10th edition pdf financial accounting 10th edition harrison pdf financial accounting harrison 10th edition financial accounting harrison pdf financial accounting 10th edition solutions manual financial accounting 10th edition harrison horngren and thomas pdf harrison financial accounting 11e