accounting principles 10th edition weygandt & kimmel chapter 2

DESCRIPTION

Accounting Principles 10th Edition Weygandt & Kimmel Chapter 2 - The Recording Process - Problem SolutionsTRANSCRIPT

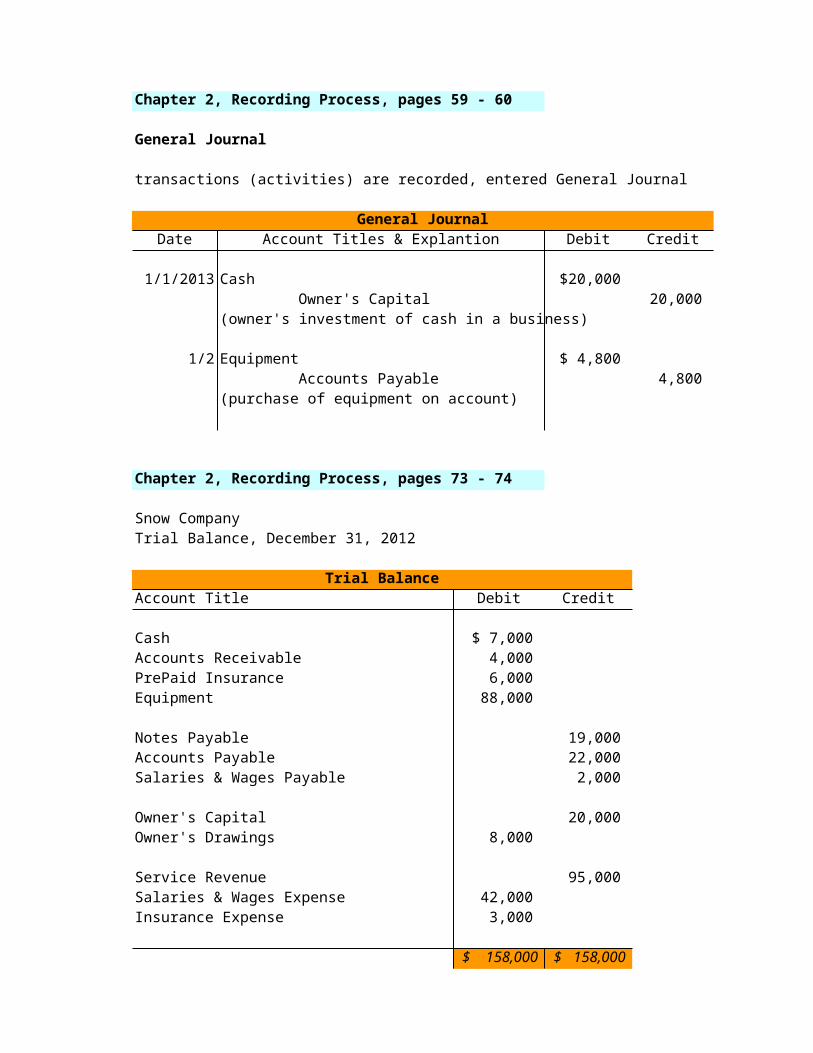

Chapter 2, Recording Process, pages 59 - 60

General Journal

transactions (activities) are recorded, entered General Journal

General JournalDate Account Titles & Explantion Debit Credit

11/1/2013 Cash $ 20,000

Owner's Capital 20,000 (owner's investment of cash in a business)

21/2 Equipment $ 4,800

Accounts Payable 4,800 (purchase of equipment on account)

3

Chapter 2, Recording Process, pages 73 - 74

Snow Company 4Trial Balance, December 31, 2012

Trial BalanceAccount Title Debit Credit 5

Cash $ 7,000 Accounts Receivable 4,000 PrePaid Insurance 6,000 6Equipment 88,000

Notes Payable 19,000 Accounts Payable 22,000 7Salaries & Wages Payable 2,000

Owner's Capital 20,000 Owner's Drawings 8,000 8

Service Revenue 95,000 Salaries & Wages Expense 42,000 Insurance Expense 3,000 9

$ 158,000 $ 158,000

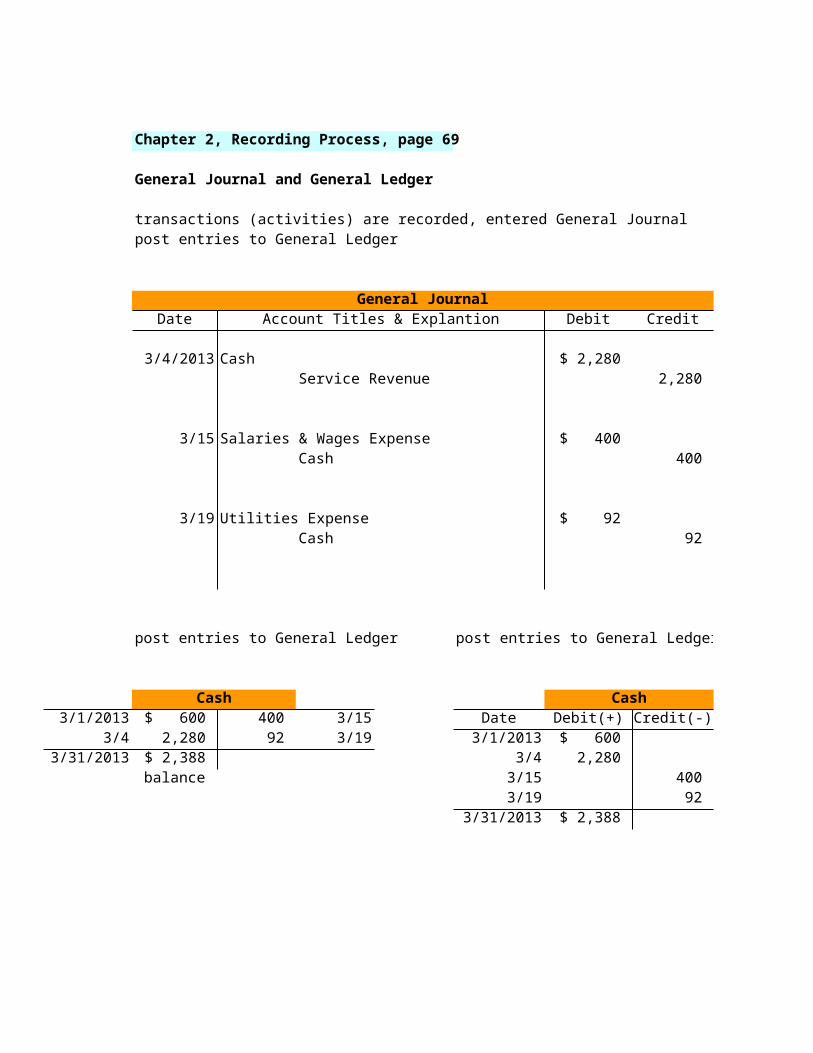

Chapter 2, Recording Process, page 69

General Journal and General Ledger

transactions (activities) are recorded, entered General Journalpost entries to General Ledger Date

10/1/201310/2

General Journal 10/3Date Account Titles & Explantion Debit Credit 10/4

10/203/4/2013 Cash $ 2,280 10/26

Service Revenue 2,280 10/31

3/15 Salaries & Wages Expense $ 400 Cash 400 Date

10/5/2013

3/19 Utilities Expense $ 92 Cash 92

Date10/4/2013

post entries to General Ledger post entries to General Ledger

Cash Cash Date3/1/2013 $ 600 400 3/15 Date Debit(+) Credit(-) Balance 10/1/2013

3/4 2,280 92 3/19 3/1/2013 $ 600 $ 600 3/31/2013 $ 2,388 3/4 2,280 2,880

balance 3/15 400 2,480 3/19 92 2,388

3/31/2013 $ 2,388 Date

10/1/2013

Date

10/5/2013

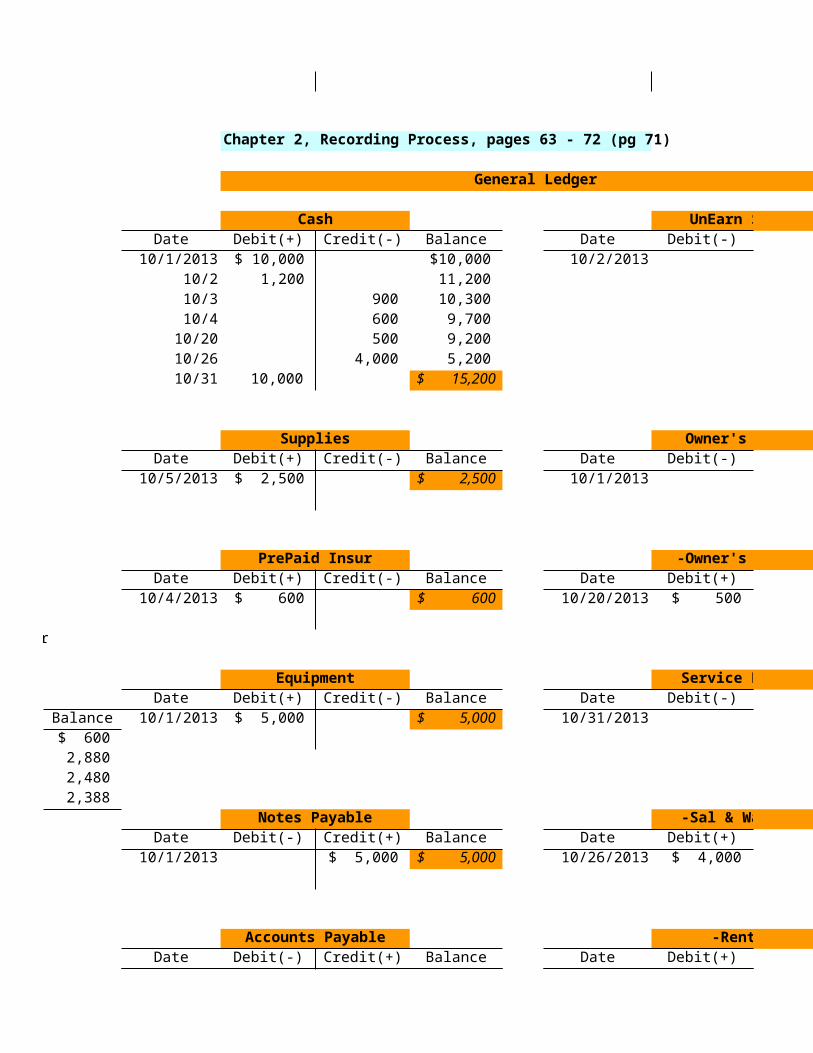

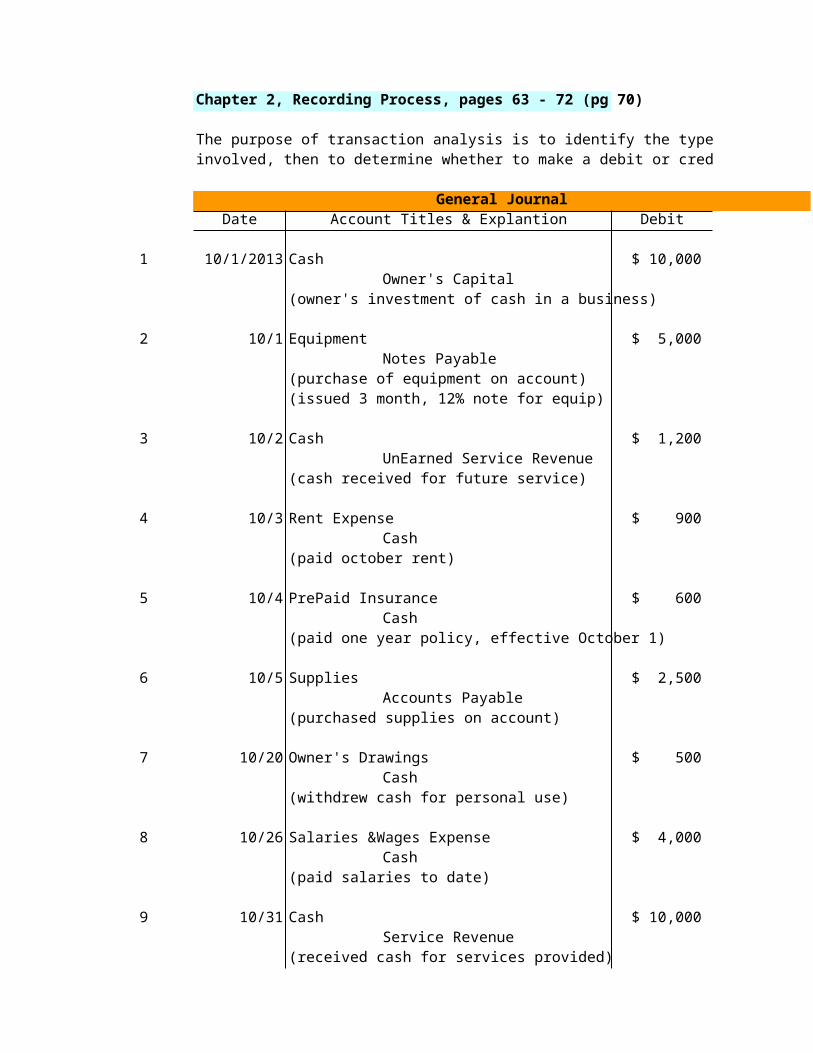

Chapter 2, Recording Process, pages 63 - 72 (pg 70)

The purpose of transaction analysis is to identify the type of accountinvolved, then to determine whether to make a debit or credit to the account

General JournalDate Account Titles & Explantion Debit Credit

10/1/2013 Cash $ 10,000 Owner's Capital 10,000

(owner's investment of cash in a business)

10/1 Equipment $ 5,000 Notes Payable 5,000

(purchase of equipment on account)(issued 3 month, 12% note for equip)

10/2 Cash $ 1,200 UnEarned Service Revenue 1,200

(cash received for future service)

10/3 Rent Expense $ 900 Cash 900

(paid october rent)

10/4 PrePaid Insurance $ 600 Cash 600

(paid one year policy, effective October 1)

10/5 Supplies $ 2,500 Accounts Payable 2,500

(purchased supplies on account)

10/20 Owner's Drawings $ 500 Cash 500

(withdrew cash for personal use)

10/26 Salaries &Wages Expense $ 4,000 Cash 4,000

(paid salaries to date)

10/31 Cash $ 10,000 Service Revenue 10,000

(received cash for services provided)

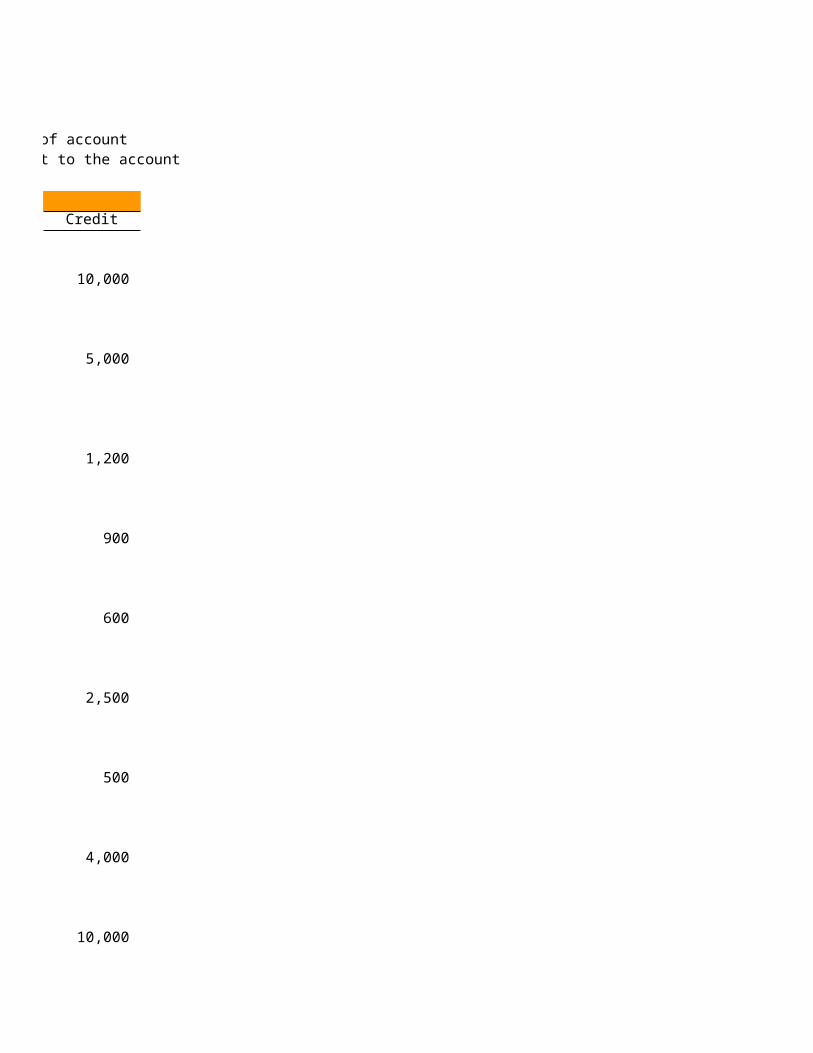

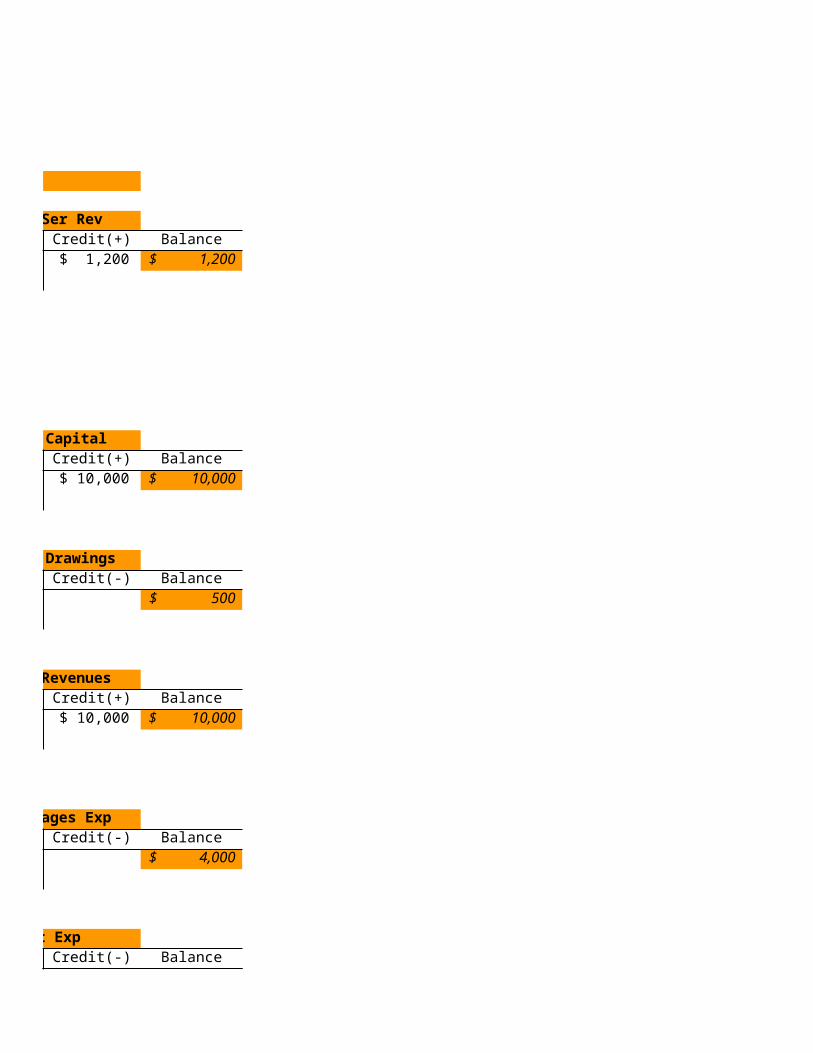

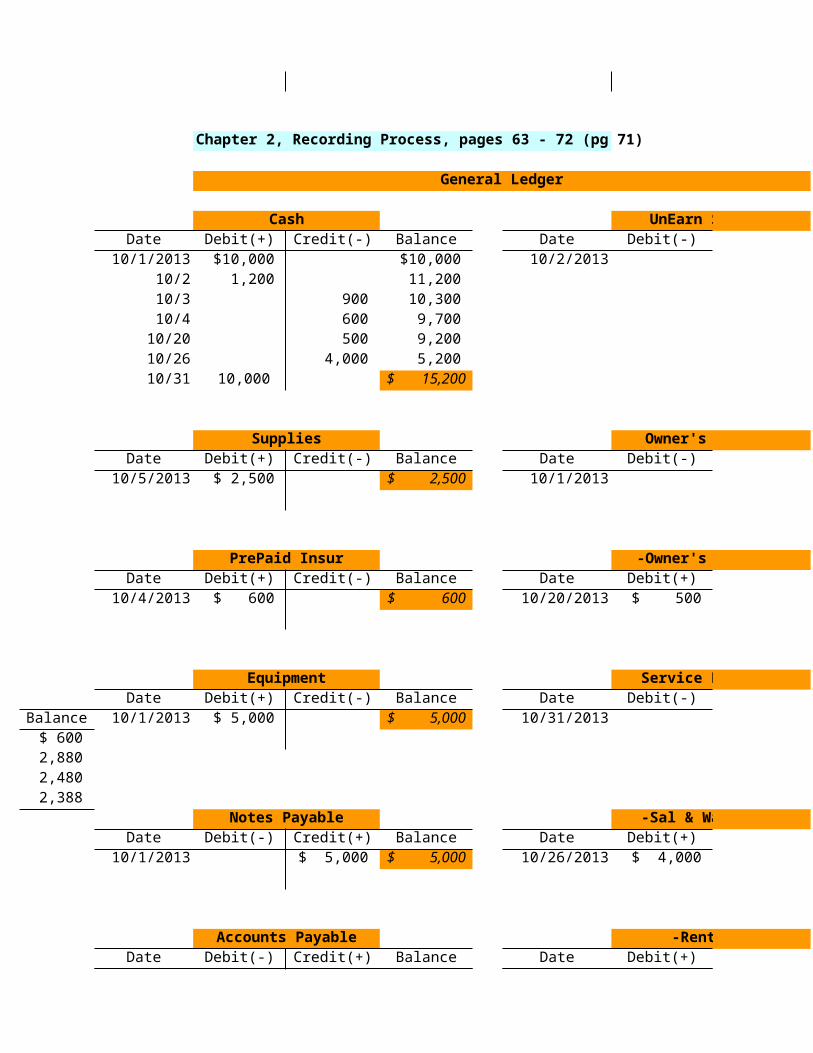

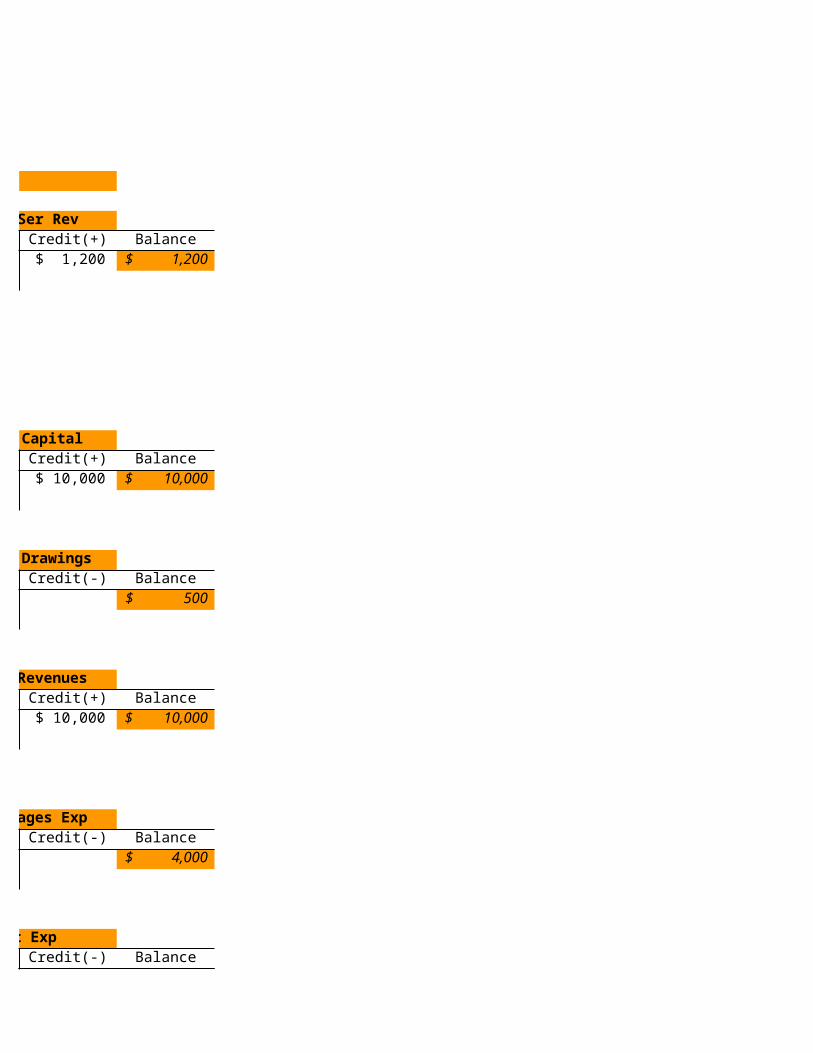

Chapter 2, Recording Process, pages 63 - 72 (pg 71)

General Ledger

Cash UnEarn Ser Rev Debit(+) Credit(-) Balance Date Debit(-) Credit(+) Balance

$ 10,000 $ 10,000 10/2/2013 $ 1,200 $ 1,200 1,200 11,200

900 10,300 600 9,700 500 9,200 4,000 5,200

10,000 $ 15,200

Supplies Owner's Capital Debit(+) Credit(-) Balance Date Debit(-) Credit(+) Balance

$ 2,500 $ 2,500 10/1/2013 $ 10,000 $ 10,000

PrePaid Insur -Owner's Drawings Debit(+) Credit(-) Balance Date Debit(+) Credit(-) Balance

$ 600 $ 600 10/20/2013 $ 500 $ 500

Equipment Service Revenues Debit(+) Credit(-) Balance Date Debit(-) Credit(+) Balance

$ 5,000 $ 5,000 10/31/2013 $ 10,000 $ 10,000

Notes Payable -Sal & Wages Exp Debit(-) Credit(+) Balance Date Debit(+) Credit(-) Balance

$ 5,000 $ 5,000 10/26/2013 $ 4,000 $ 4,000

Accounts Payable -Rent Exp Debit(-) Credit(+) Balance Date Debit(+) Credit(-) Balance

$ 2,500 $ 2,500 10/3/2013 $ 900 $ 900

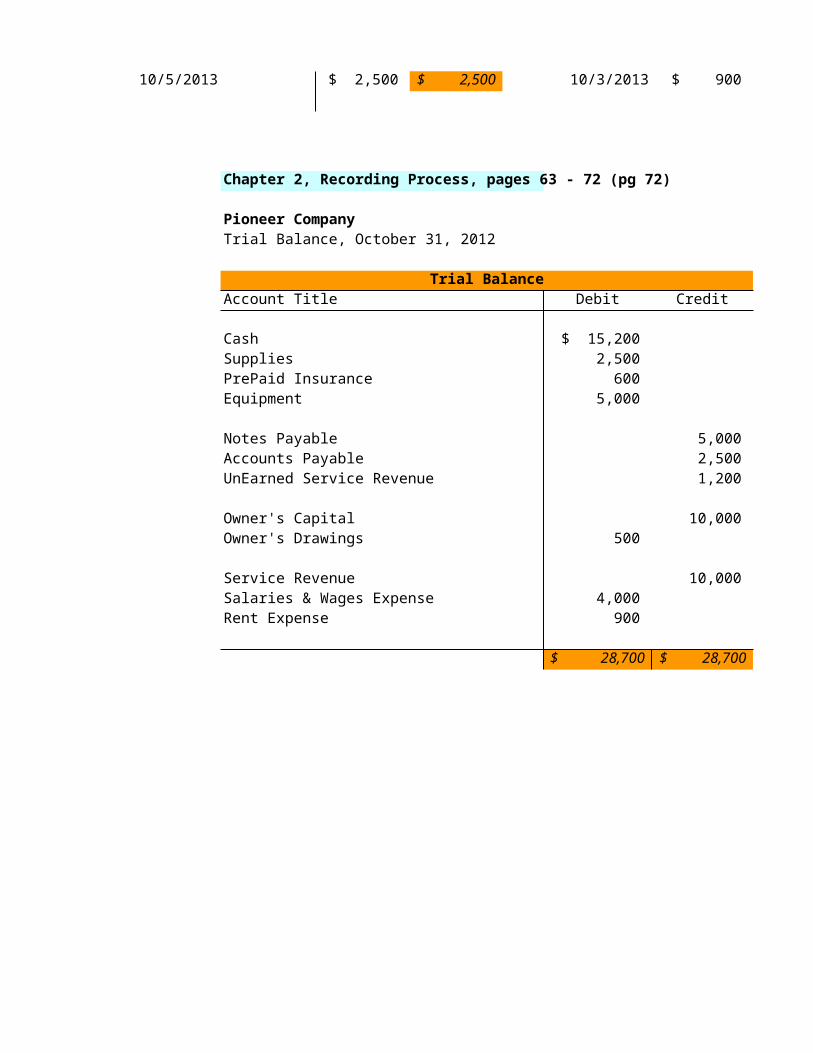

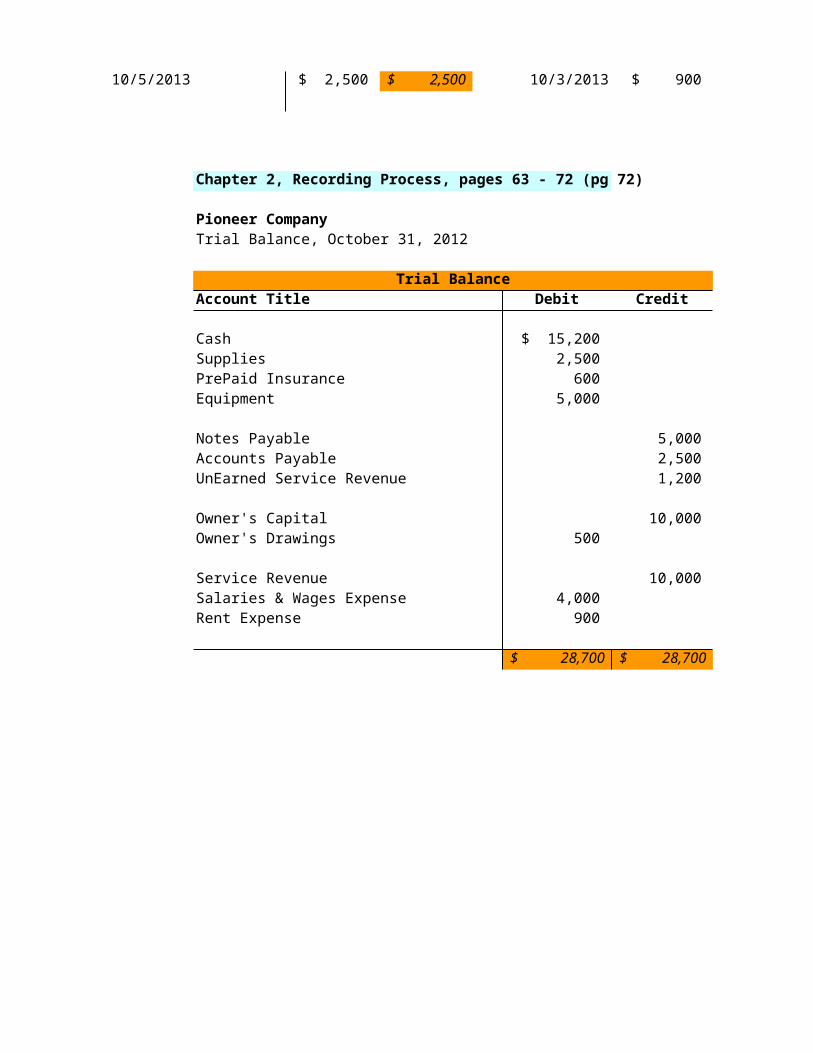

Chapter 2, Recording Process, pages 63 - 72 (pg 72)

Pioneer CompanyTrial Balance, October 31, 2012

Trial BalanceAccount Title Debit Credit

Cash $ 15,200 Supplies 2,500 PrePaid Insurance 600 Equipment 5,000

Notes Payable 5,000 Accounts Payable 2,500 UnEarned Service Revenue 1,200

Owner's Capital 10,000 Owner's Drawings 500

Service Revenue 10,000 Salaries & Wages Expense 4,000 Rent Expense 900

$ 28,700 $ 28,700

Chapter 2, Recording Process, pages 63 - 72 (pg 70)

The purpose of transaction analysis is to identify the type of accountinvolved, then to determine whether to make a debit or credit to the account

General JournalDate Account Titles & Explantion Debit Credit

1 10/1/2013 Cash $ 10,000 Owner's Capital 10,000

(owner's investment of cash in a business)

2 10/1 Equipment $ 5,000 Notes Payable 5,000

(purchase of equipment on account)(issued 3 month, 12% note for equip)

3 10/2 Cash $ 1,200 UnEarned Service Revenue 1,200

(cash received for future service)

4 10/3 Rent Expense $ 900 Cash 900

(paid october rent)

5 10/4 PrePaid Insurance $ 600 Cash 600

(paid one year policy, effective October 1)

6 10/5 Supplies $ 2,500 Accounts Payable 2,500

(purchased supplies on account)

7 10/20 Owner's Drawings $ 500 Cash 500

(withdrew cash for personal use)

8 10/26 Salaries &Wages Expense $ 4,000 Cash 4,000

(paid salaries to date)

9 10/31 Cash $ 10,000 Service Revenue 10,000

(received cash for services provided)

Chapter 2, Recording Process, pages 63 - 72 (pg 71)

General Ledger

Cash UnEarn Ser RevDate Debit(+) Credit(-) Balance Date Debit(-) Credit(+) Balance

10/1/2013 $ 10,000 $ 10,000 10/2/2013 $ 1,200 $ 1,200 10/2 1,200 11,200 10/3 900 10,300 10/4 600 9,700

10/20 500 9,200 10/26 4,000 5,200 10/31 10,000 $ 15,200

Supplies Owner's CapitalDate Debit(+) Credit(-) Balance Date Debit(-) Credit(+) Balance

10/5/2013 $ 2,500 $ 2,500 10/1/2013 $ 10,000 $ 10,000

PrePaid Insur -Owner's DrawingsDate Debit(+) Credit(-) Balance Date Debit(+) Credit(-) Balance

10/4/2013 $ 600 $ 600 10/20/2013 $ 500 $ 500

Equipment Service RevenuesDate Debit(+) Credit(-) Balance Date Debit(-) Credit(+) Balance

Balance 10/1/2013 $ 5,000 $ 5,000 10/31/2013 $ 10,000 $ 10,000 $ 600 2,880 2,480 2,388

Notes Payable -Sal & Wages ExpDate Debit(-) Credit(+) Balance Date Debit(+) Credit(-) Balance

10/1/2013 $ 5,000 $ 5,000 10/26/2013 $ 4,000 $ 4,000

Accounts Payable -Rent ExpDate Debit(-) Credit(+) Balance Date Debit(+) Credit(-) Balance

10/5/2013 $ 2,500 $ 2,500 10/3/2013 $ 900 $ 900

Chapter 2, Recording Process, pages 63 - 72 (pg 72)

Pioneer CompanyTrial Balance, October 31, 2012

Trial BalanceAccount Title Debit Credit

Cash $ 15,200 Supplies 2,500 PrePaid Insurance 600 Equipment 5,000

Notes Payable 5,000 Accounts Payable 2,500 UnEarned Service Revenue 1,200

Owner's Capital 10,000 Owner's Drawings 500

Service Revenue 10,000 Salaries & Wages Expense 4,000 Rent Expense 900

$ 28,700 $ 28,700

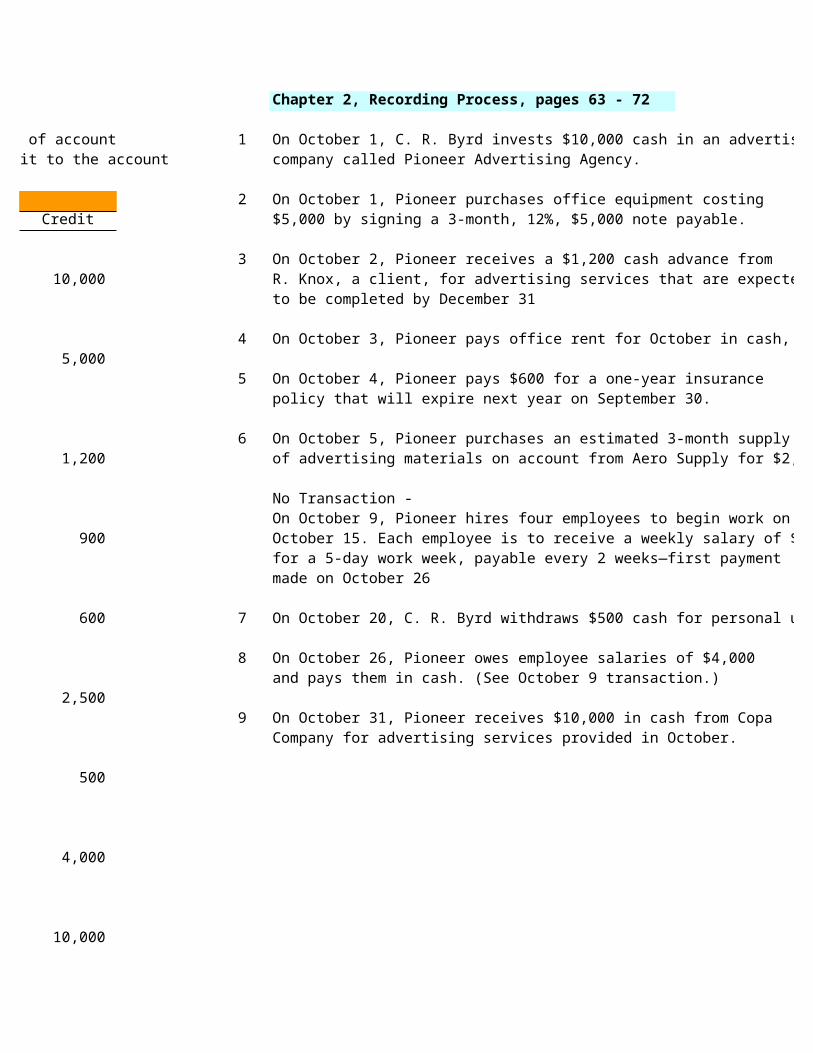

Chapter 2, Recording Process, pages 63 - 72

1 On October 1, C. R. Byrd invests $10,000 cash in an advertisingcompany called Pioneer Advertising Agency.

2 On October 1, Pioneer purchases office equipment costing$5,000 by signing a 3-month, 12%, $5,000 note payable.

3 On October 2, Pioneer receives a $1,200 cash advance fromR. Knox, a client, for advertising services that are expectedto be completed by December 31

4 On October 3, Pioneer pays office rent for October in cash, $900.

5 On October 4, Pioneer pays $600 for a one-year insurancepolicy that will expire next year on September 30.

6 On October 5, Pioneer purchases an estimated 3-month supplyof advertising materials on account from Aero Supply for $2,500.

No Transaction - On October 9, Pioneer hires four employees to begin work onOctober 15. Each employee is to receive a weekly salary of $500for a 5-day work week, payable every 2 weeks—first paymentmade on October 26

7 On October 20, C. R. Byrd withdraws $500 cash for personal use

8 On October 26, Pioneer owes employee salaries of $4,000and pays them in cash. (See October 9 transaction.)

9 On October 31, Pioneer receives $10,000 in cash from CopaCompany for advertising services provided in October.

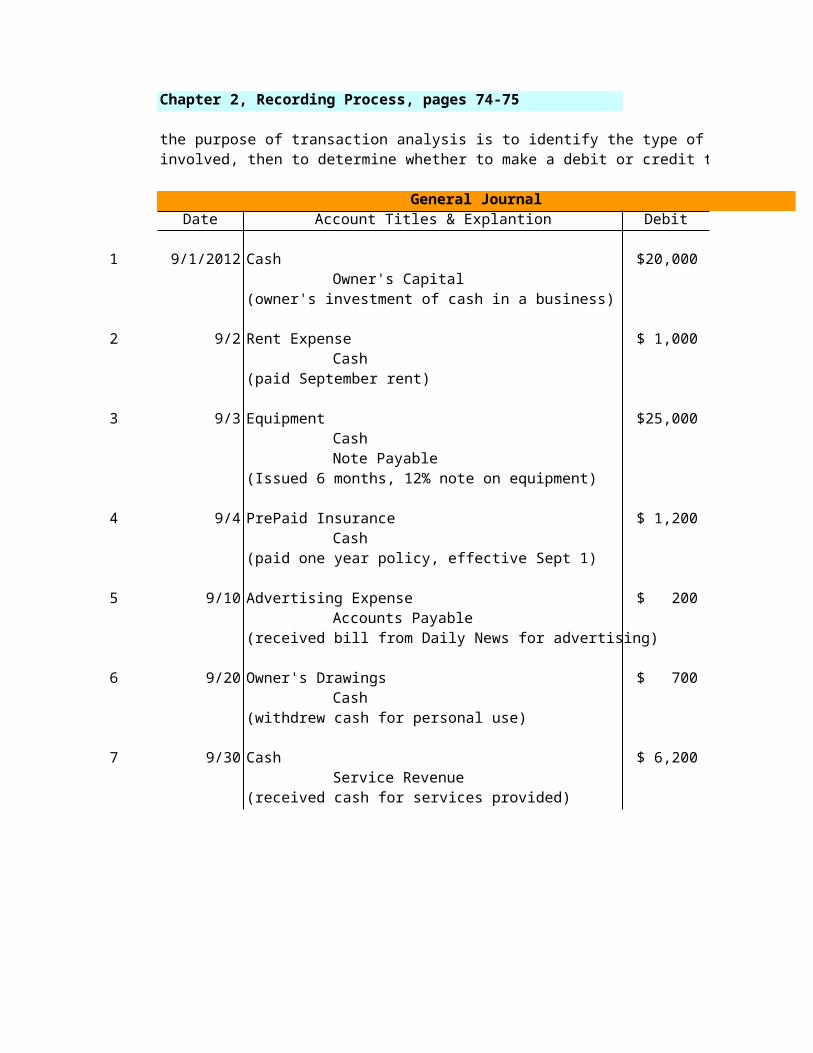

Chapter 2, Recording Process, pages 74-75

the purpose of transaction analysis is to identify the type of accountinvolved, then to determine whether to make a debit or credit to the account

General JournalDate Account Titles & Explantion Debit Credit

1 9/1/2012 Cash $ 20,000 Owner's Capital 20,000

(owner's investment of cash in a business)

2 9/2 Rent Expense $ 1,000 Cash 1,000

(paid September rent)

3 9/3 Equipment $ 25,000 Cash 10,000Note Payable 15,000

(Issued 6 months, 12% note on equipment)

4 9/4 PrePaid Insurance $ 1,200 Cash 1,200

(paid one year policy, effective Sept 1)

5 9/10 Advertising Expense $ 200 Accounts Payable 200

(received bill from Daily News for advertising)

6 9/20 Owner's Drawings $ 700 Cash 700

(withdrew cash for personal use)

7 9/30 Cash $ 6,200 Service Revenue 6,200

(received cash for services provided)

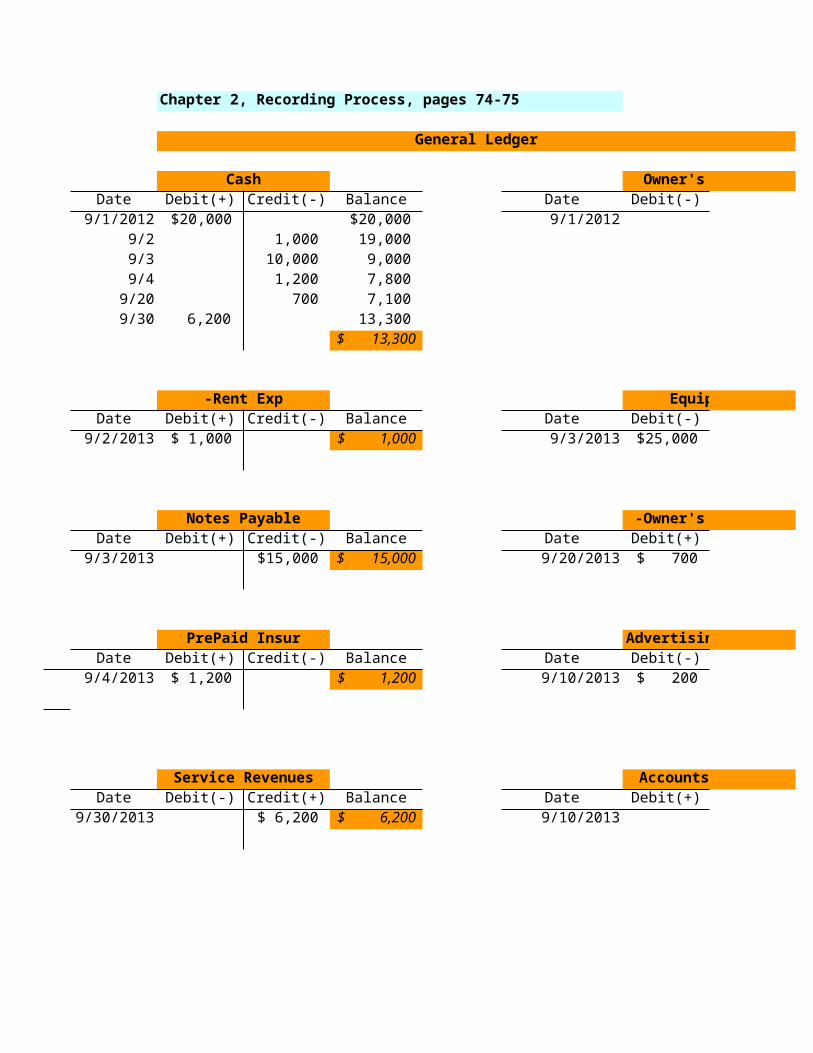

Chapter 2, Recording Process, pages 74-75

General Ledger

Cash Owner's CapitalDate Debit(+) Credit(-) Balance Date Debit(-) Credit(+) Balance

9/1/2012 $ 20,000 $ 20,000 9/1/2012 $ 20,000 $ 20,000 9/2 1,000 19,000 9/3 10,000 9,000 9/4 1,200 7,800

9/20 700 7,100 9/30 6,200 13,300

$ 13,300

-Rent Exp EquipmentDate Debit(+) Credit(-) Balance Date Debit(-) Credit(+) Balance

9/2/2013 $ 1,000 $ 1,000 9/3/2013 $ 25,000 $ 25,000

Notes Payable -Owner's DrawingsDate Debit(+) Credit(-) Balance Date Debit(+) Credit(-) Balance

9/3/2013 $ 15,000 $ 15,000 9/20/2013 $ 700 $ 700

PrePaid Insur Advertising ExpenseDate Debit(+) Credit(-) Balance Date Debit(-) Credit(+) Balance

9/4/2013 $ 1,200 $ 1,200 9/10/2013 $ 200 $ 200

Service Revenues Accounts PayableDate Debit(-) Credit(+) Balance Date Debit(+) Credit(-) Balance

9/30/2013 $ 6,200 $ 6,200 9/10/2013 $ 200 $ 200

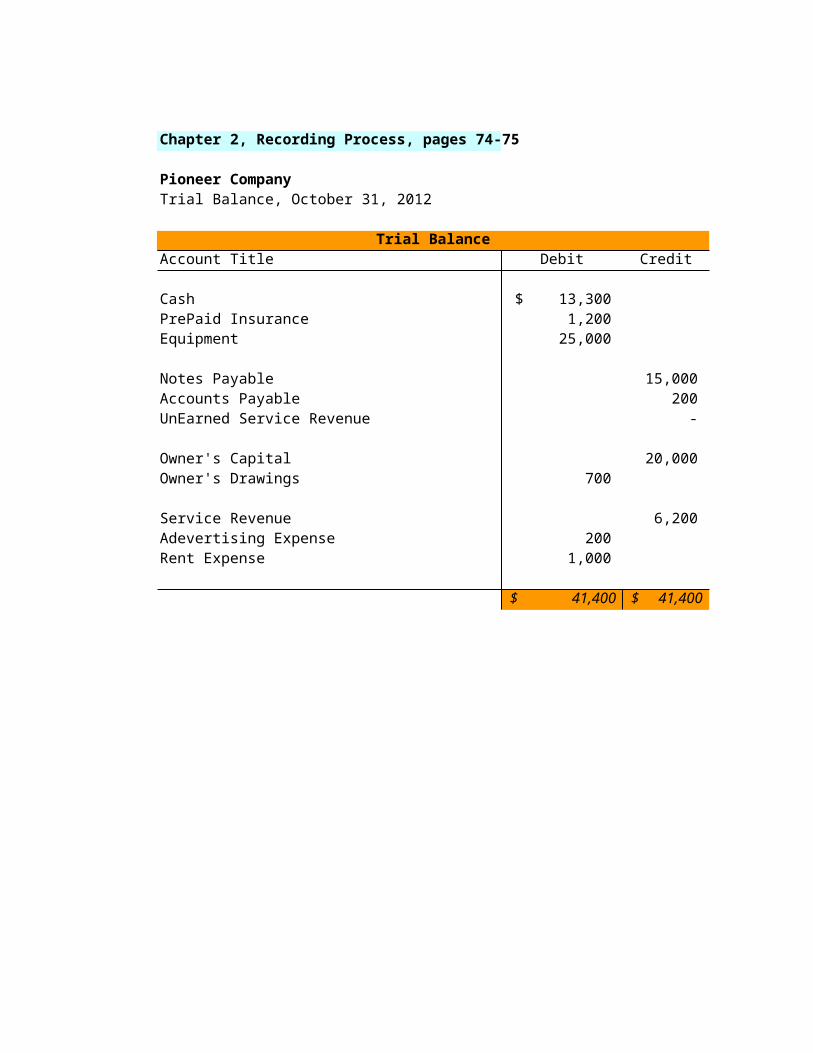

Chapter 2, Recording Process, pages 74-75

Pioneer CompanyTrial Balance, October 31, 2012

Trial BalanceAccount Title Debit Credit

Cash $ 13,300 PrePaid Insurance 1,200 Equipment 25,000

Notes Payable 15,000 Accounts Payable 200 UnEarned Service Revenue -

Owner's Capital 20,000 Owner's Drawings 700

Service Revenue 6,200 Adevertising Expense 200 Rent Expense 1,000

$ 41,400 $ 41,400

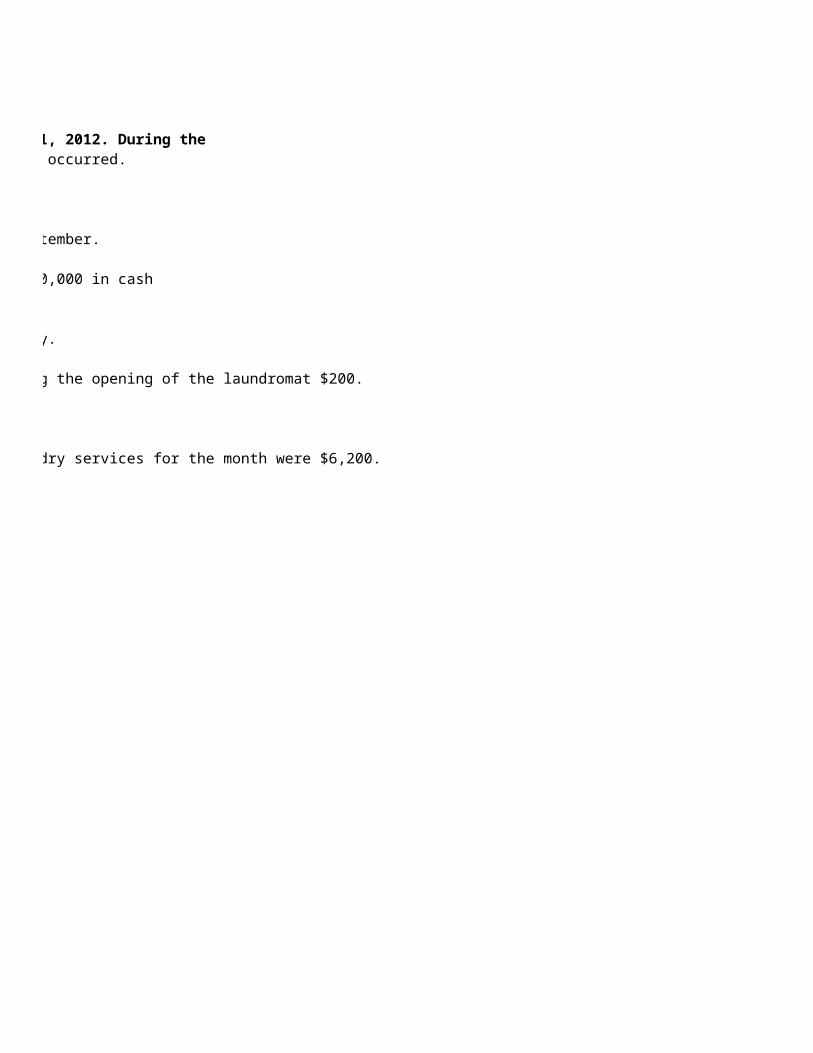

Chapter 2, Recording Process, pages 74-75

Bob Sample opened the Campus Laundromat on September 1, 2012. During thefirst month of operations, the following transactions occurred.

1 1 Sept. 1 Bob invested $20,000 cash in the business.

2 2 The company paid $1,000 cash for store rent for September.

3 3 Purchased washers and dryers for $25,000, paying $10,000 in cashand signing a $15,000, 6-month, 12% note payable.

4 4 Paid $1,200 for a one-year accident insurance policy.

5 10 Received a bill from the Daily News for advertising the opening of the laundromat $200.

6 20 Bob withdrew $700 cash for personal use.

7 30 The company determined that cash receipts for laundry services for the month were $6,200.

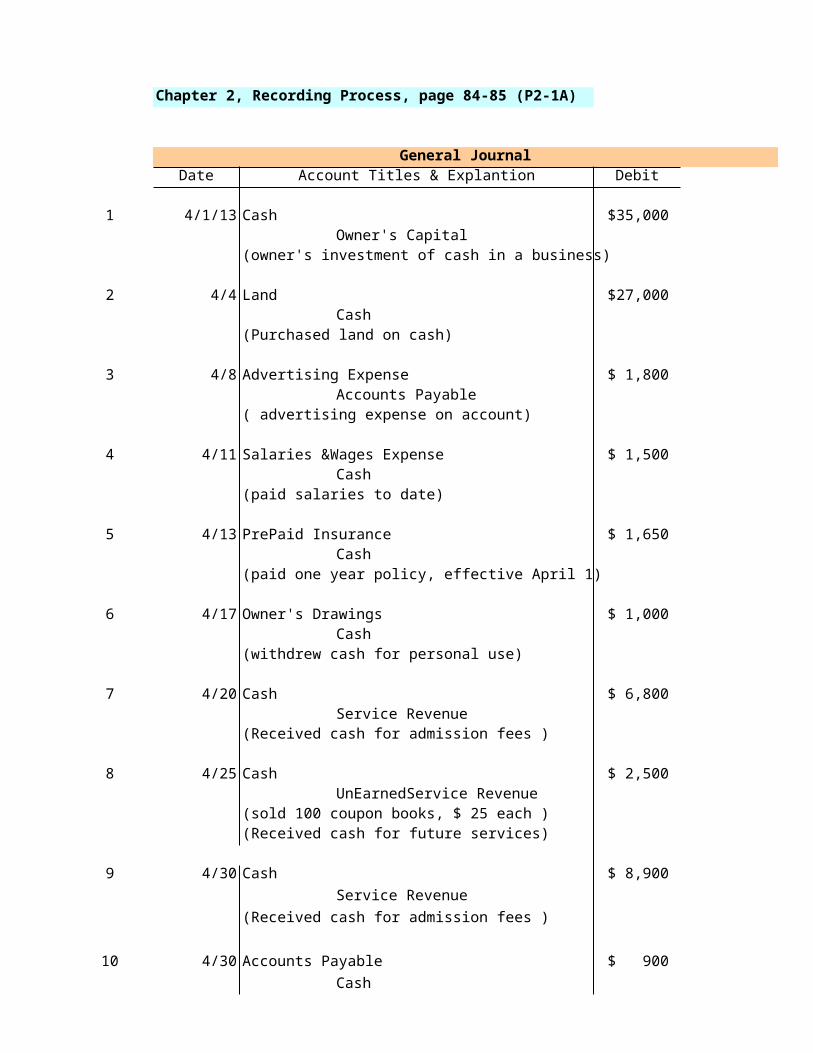

Chapter 2, Recording Process, page 84-85 (P2-1A)

General JournalDate Account Titles & Explantion Debit Credit

1 4/1/13 Cash $ 35,000 Owner's Capital 35,000

(owner's investment of cash in a business)

2 4/4 Land $ 27,000 Cash 27,000

(Purchased land on cash)

3 4/8 Advertising Expense $ 1,800 Accounts Payable 1,800

( advertising expense on account)

4 4/11 Salaries &Wages Expense $ 1,500 Cash 1,500

(paid salaries to date)

5 4/13 PrePaid Insurance $ 1,650 Cash 1,650

(paid one year policy, effective April 1)

6 4/17 Owner's Drawings $ 1,000 Cash 1,000

(withdrew cash for personal use)

7 4/20 Cash $ 6,800 Service Revenue 6,800

(Received cash for admission fees )

8 4/25 Cash $ 2,500 UnEarnedService Revenue 2,500

(sold 100 coupon books, $ 25 each )(Received cash for future services)

9 4/30 Cash $ 8,900 Service Revenue 8,900

(Received cash for admission fees )

10 4/30 Accounts Payable $ 900 Cash 900

(paid Adv expense incurred on Apr 18 )

Chapter 2, Recording Process, page 84-85 (P2-1A)

General Ledger

Cash UnEarnedService RevenuesDate Debit(+) Credit(-) Balance Date Debit(-) Credit(+) Balance

4/1/13 $ 35,000 $ 35,000 4/25/2013 $ 2,500 $ 2,500 4/4 27,000 8,000

4/11 1,500 6,500 4/13 1,650 4,850 4/17 1,000 3,850 4/20 6,800 10,650 4/25 2,500 13,150 4/30 8,900 22,050 4/30 900 $ 21,150

Land Owner's CapitalDate Debit(+) Credit(-) Balance Date Debit(-) Credit(+) Balance

4/4/2013 $ 27,000 $ 27,000 4/1/2013 $ 35,000 $ 35,000

PrePaid Insurance -Owner's DrawingsDate Debit(+) Credit(-) Balance Date Debit(+) Credit(-) Balance

4/13/2013 $ 1,650 $ 1,650 4/17/2013 $ 1,000 $ 1,000

Accounts Payable -Advertising ExpenseDate Debit(-) Credit(+) Balance Date Debit(+) Credit(+) Balance

4/8/2013 $ 1,800 $ 1,800 4/8/2013 $ 1,800 $ 1,800 4/30 $ 900 $ 900

Service Revenues -Salary & Wage ExpenseDate Debit(-) Credit(+) Balance Date Debit(+) Credit(-) Balance

4/20/2013 $ 6,800 $ 6,800 4/11/2013 $ 1,500 $ - $ 1,500 4/30 8,900 $ 15,700

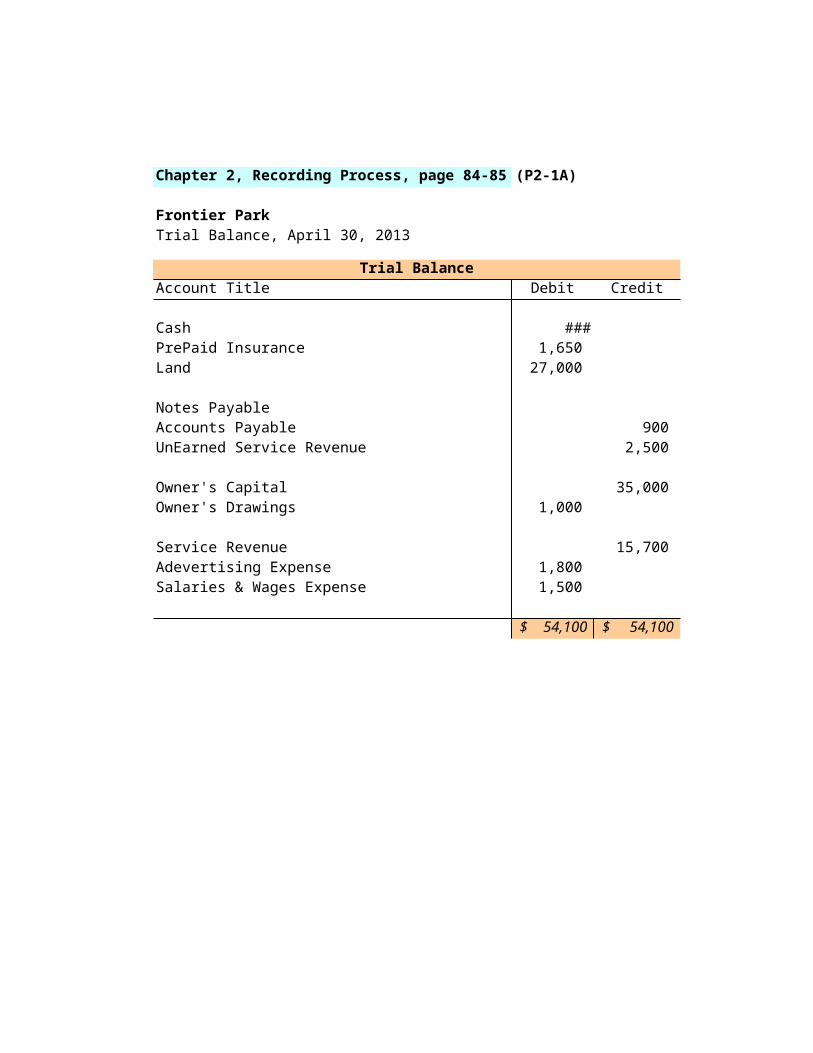

Chapter 2, Recording Process, page 84-85 (P2-1A)

Frontier ParkTrial Balance, April 30, 2013

Trial BalanceAccount Title Debit Credit

Cash $ 21,150 PrePaid Insurance 1,650 Land 27,000

Notes PayableAccounts Payable 900 UnEarned Service Revenue 2,500

Owner's Capital 35,000 Owner's Drawings 1,000

Service Revenue 15,700 Adevertising Expense 1,800 Salaries & Wages Expense 1,500

$ 54,100 $ 54,100

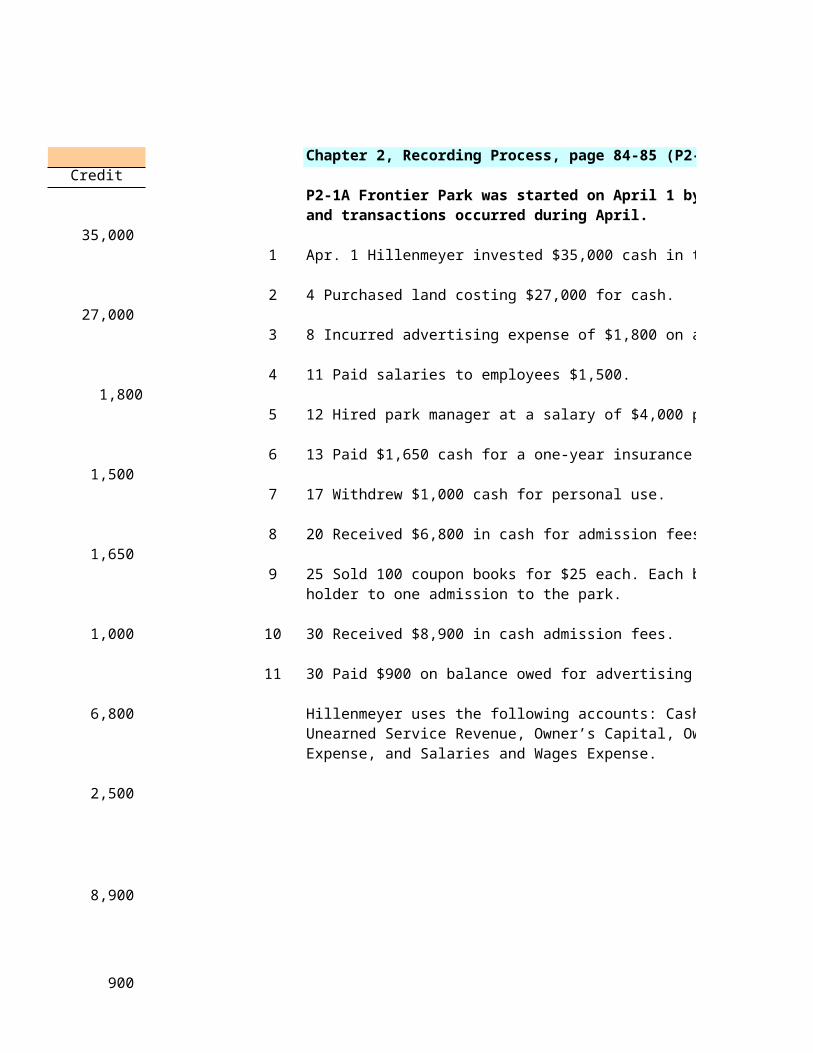

Chapter 2, Recording Process, page 84-85 (P2-1A)

P2-1A Frontier Park was started on April 1 by H. Hillenmeyer. The following selected eventsand transactions occurred during April.

1 Apr. 1 Hillenmeyer invested $35,000 cash in the business.

2 4 Purchased land costing $27,000 for cash.

3 8 Incurred advertising expense of $1,800 on account.

4 11 Paid salaries to employees $1,500.

5 12 Hired park manager at a salary of $4,000 per month, effective May 1.

6 13 Paid $1,650 cash for a one-year insurance policy.

7 17 Withdrew $1,000 cash for personal use.

8 20 Received $6,800 in cash for admission fees.

9 25 Sold 100 coupon books for $25 each. Each book contains 10 coupons that entitle theholder to one admission to the park.

10 30 Received $8,900 in cash admission fees.

11 30 Paid $900 on balance owed for advertising incurred on April 8.

Hillenmeyer uses the following accounts: Cash, Prepaid Insurance, Land, Accounts Payable,Unearned Service Revenue, Owner’s Capital, Owner’s Drawings, Service Revenue, AdvertisingExpense, and Salaries and Wages Expense.

Harjeet TutejaFn580

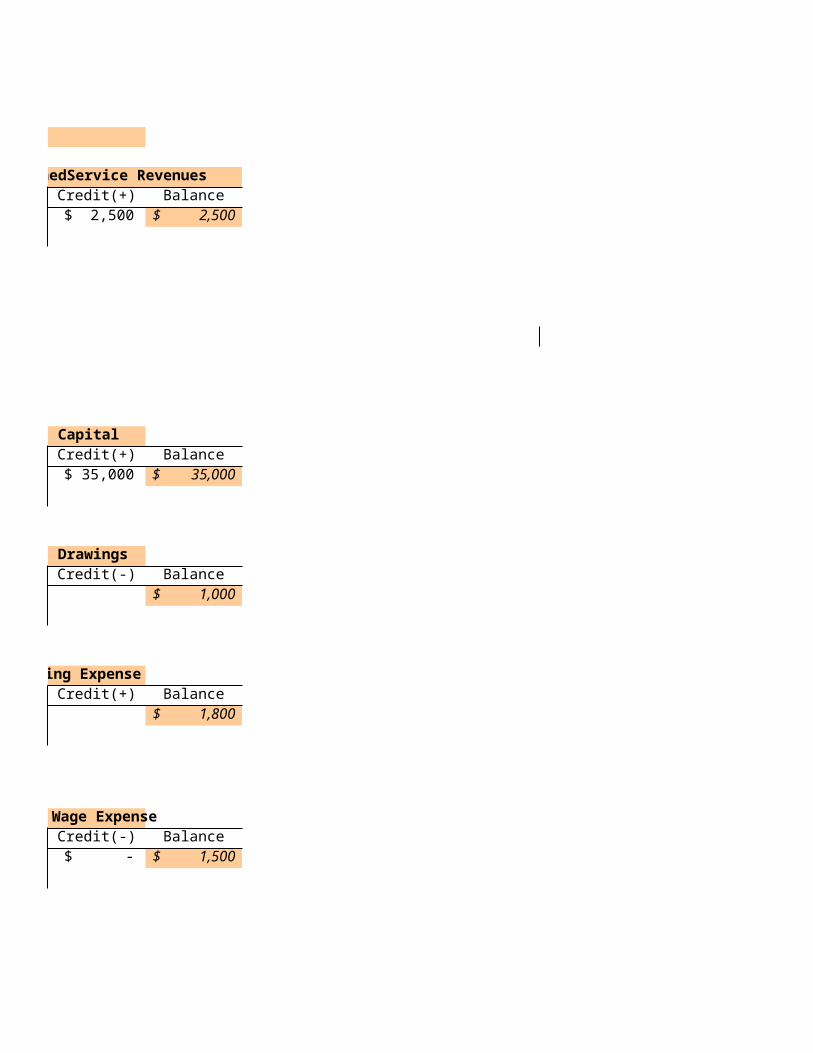

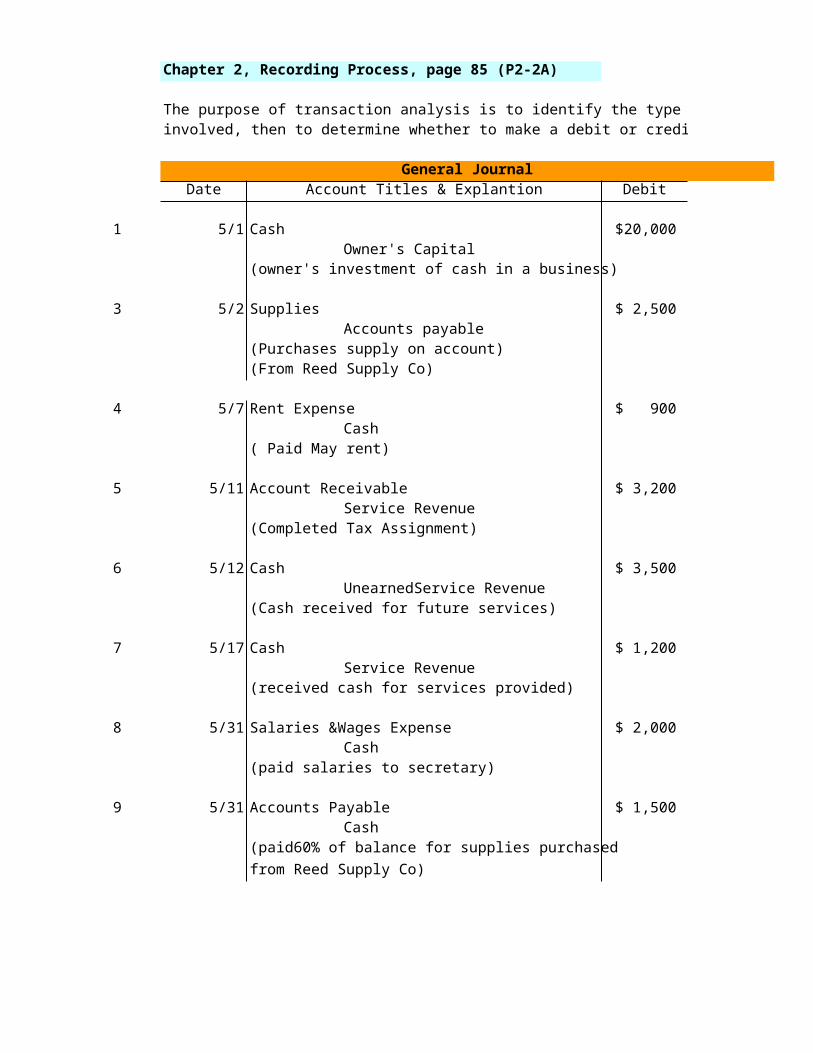

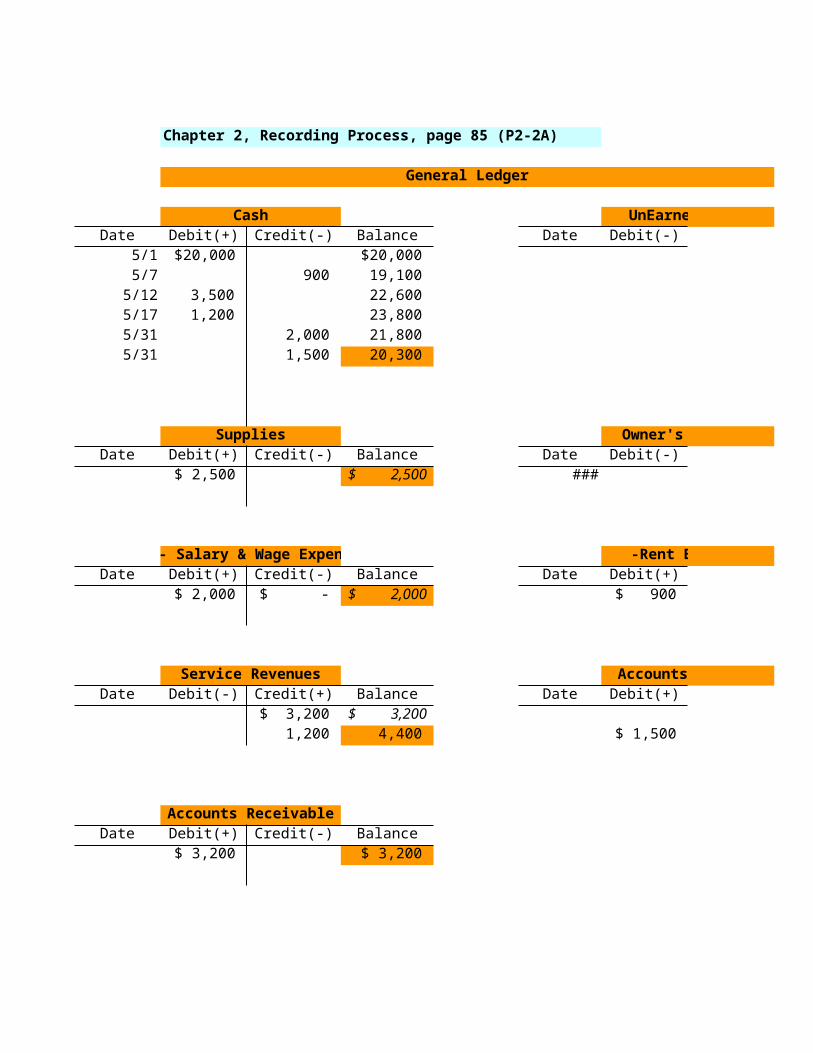

Chapter 2 - P2-1AChapter 2, Recording Process, page 85 (P2-2A)

The purpose of transaction analysis is to identify the type of accountinvolved, then to determine whether to make a debit or credit to the account

General JournalDate Account Titles & Explantion Debit Credit

1 5/1 Cash $ 20,000 Owner's Capital 20,000

(owner's investment of cash in a business)

3 5/2 Supplies $ 2,500 Accounts payable 2,500

(Purchases supply on account) (From Reed Supply Co)

4 5/7 Rent Expense $ 900 Cash 900

( Paid May rent)

5 5/11 Account Receivable $ 3,200 Service Revenue 3,200

(Completed Tax Assignment)

6 5/12 Cash $ 3,500 UnearnedService Revenue 3,500

(Cash received for future services)

7 5/17 Cash $ 1,200 Service Revenue 1,200

(received cash for services provided)

8 5/31 Salaries &Wages Expense $ 2,000 Cash 2,000

(paid salaries to secretary)

9 5/31 Accounts Payable $ 1,500 Cash 1,500

(paid60% of balance for supplies purchasedfrom Reed Supply Co)

Harjeet TutejaFn580

Chapter 2 - P2-1A

Chapter 2, Recording Process, page 85 (P2-2A)

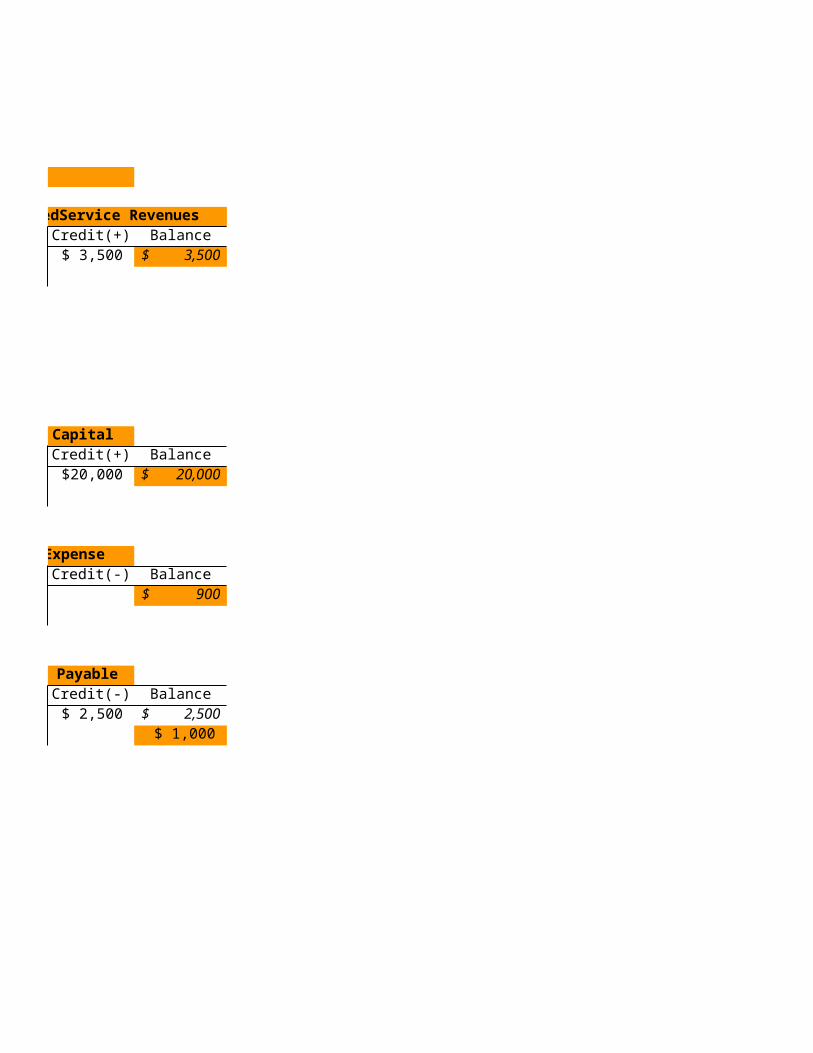

General Ledger

Cash UnEarnedService RevenuesDate Debit(+) Credit(-) Balance Date Debit(-) Credit(+) Balance

5/1 $ 20,000 $ 20,000 $ 3,500 $ 3,500 5/7 900 19,100

5/12 3,500 22,600 5/17 1,200 23,800 5/31 2,000 21,800 5/31 1,500 20,300

Supplies Owner's CapitalDate Debit(+) Credit(-) Balance Date Debit(-) Credit(+) Balance

$ 2,500 $ 2,500 ### $ 20,000 $ 20,000

'- Salary & Wage Expense -Rent ExpenseDate Debit(+) Credit(-) Balance Date Debit(+) Credit(-) Balance

$ 2,000 $ - $ 2,000 $ 900 $ 900

Service Revenues Accounts PayableDate Debit(-) Credit(+) Balance Date Debit(+) Credit(-) Balance

$ 3,200 $ 3,200 $ 2,500 $ 2,500 1,200 4,400 $ 1,500 $ 1,000

Accounts ReceivableDate Debit(+) Credit(-) Balance

$ 3,200 $ 3,200

Harjeet TutejaFn580

Chapter 2 - P2-1A

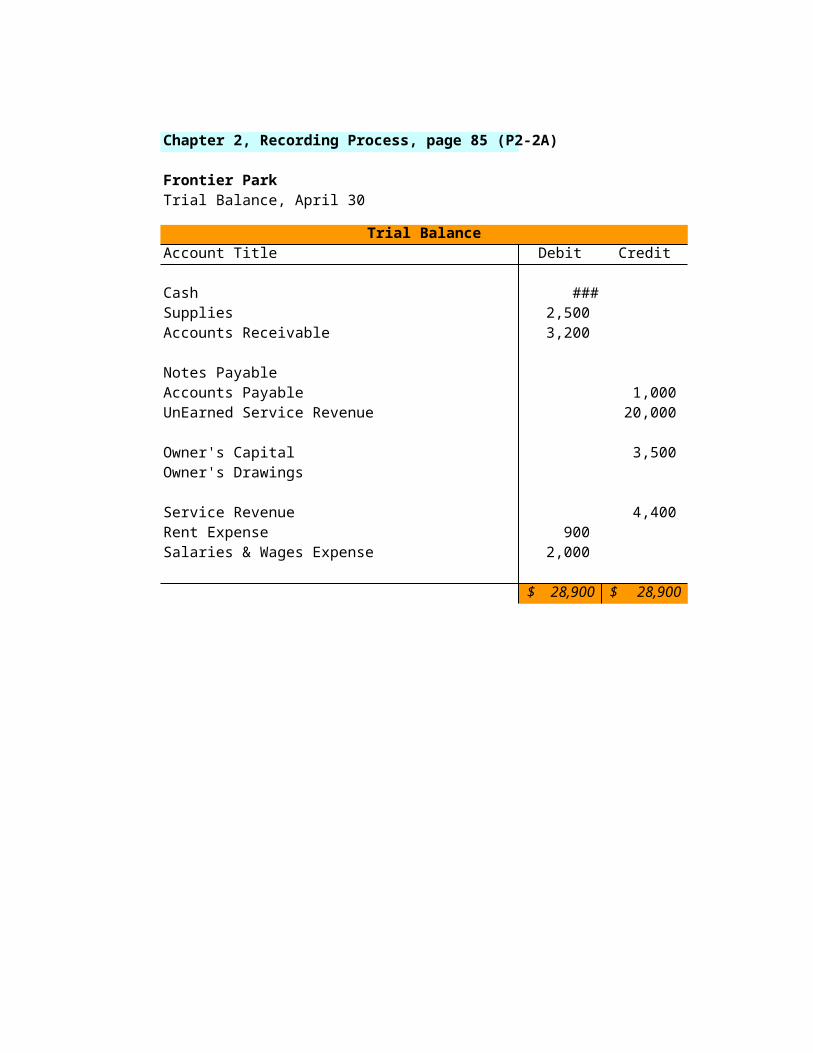

Chapter 2, Recording Process, page 85 (P2-2A)

Frontier ParkTrial Balance, April 30

Trial BalanceAccount Title Debit Credit

Cash $ 20,300 Supplies 2,500 Accounts Receivable 3,200

Notes PayableAccounts Payable 1,000 UnEarned Service Revenue 20,000

Owner's Capital 3,500 Owner's Drawings

Service Revenue 4,400 Rent Expense 900 Salaries & Wages Expense 2,000

$ 28,900 $ 28,900

Harjeet TutejaFn580

Chapter 2 - P2-1A

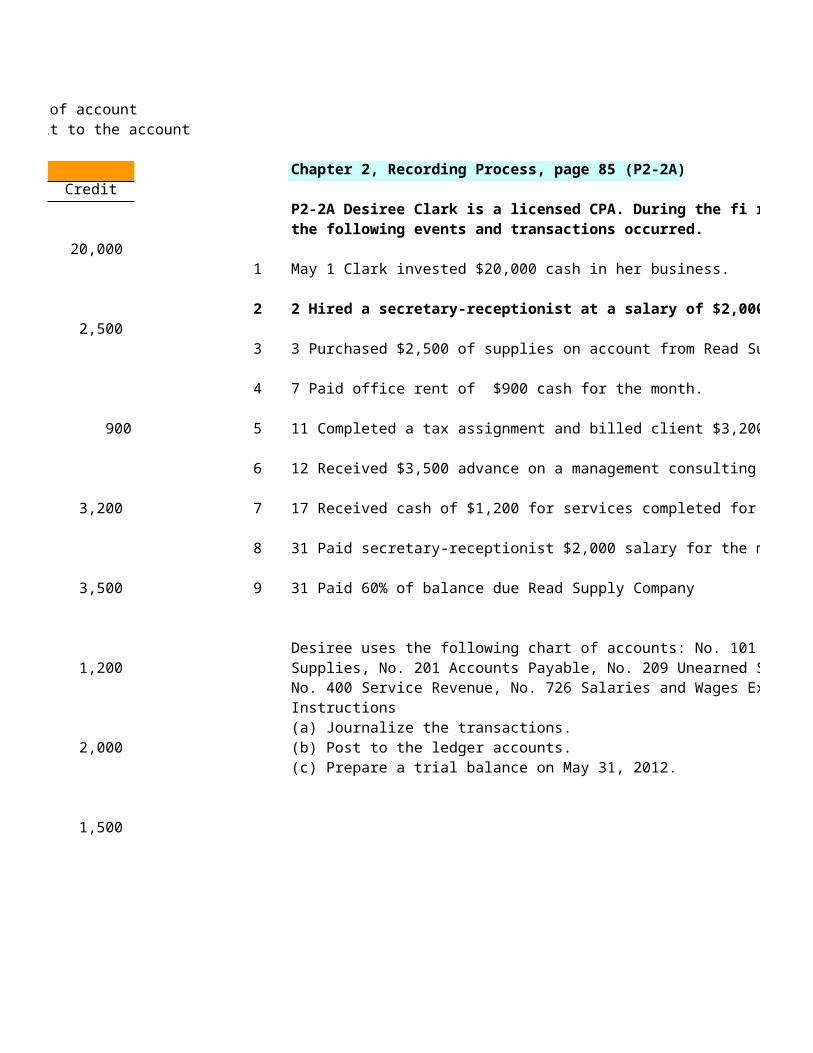

Chapter 2, Recording Process, page 85 (P2-2A)

P2-2A Desiree Clark is a licensed CPA. During the fi rst month of operations of her business,the following events and transactions occurred.

1 May 1 Clark invested $20,000 cash in her business.

2 2 Hired a secretary-receptionist at a salary of $2,000 per month.

3 3 Purchased $2,500 of supplies on account from Read Supply Company.

4 7 Paid office rent of $900 cash for the month.

5 11 Completed a tax assignment and billed client $3,200 for services provided.

6 12 Received $3,500 advance on a management consulting engagement.

7 17 Received cash of $1,200 for services completed for C. Desmond Co.

8 31 Paid secretary-receptionist $2,000 salary for the month.

9 31 Paid 60% of balance due Read Supply Company

Desiree uses the following chart of accounts: No. 101 Cash, No. 112 Accounts Receivable, No. 126Supplies, No. 201 Accounts Payable, No. 209 Unearned Service Revenue, No. 301 Owner’s Capital,No. 400 Service Revenue, No. 726 Salaries and Wages Expense, and No. 729 Rent Expense.Instructions(a) Journalize the transactions.(b) Post to the ledger accounts.(c) Prepare a trial balance on May 31, 2012.

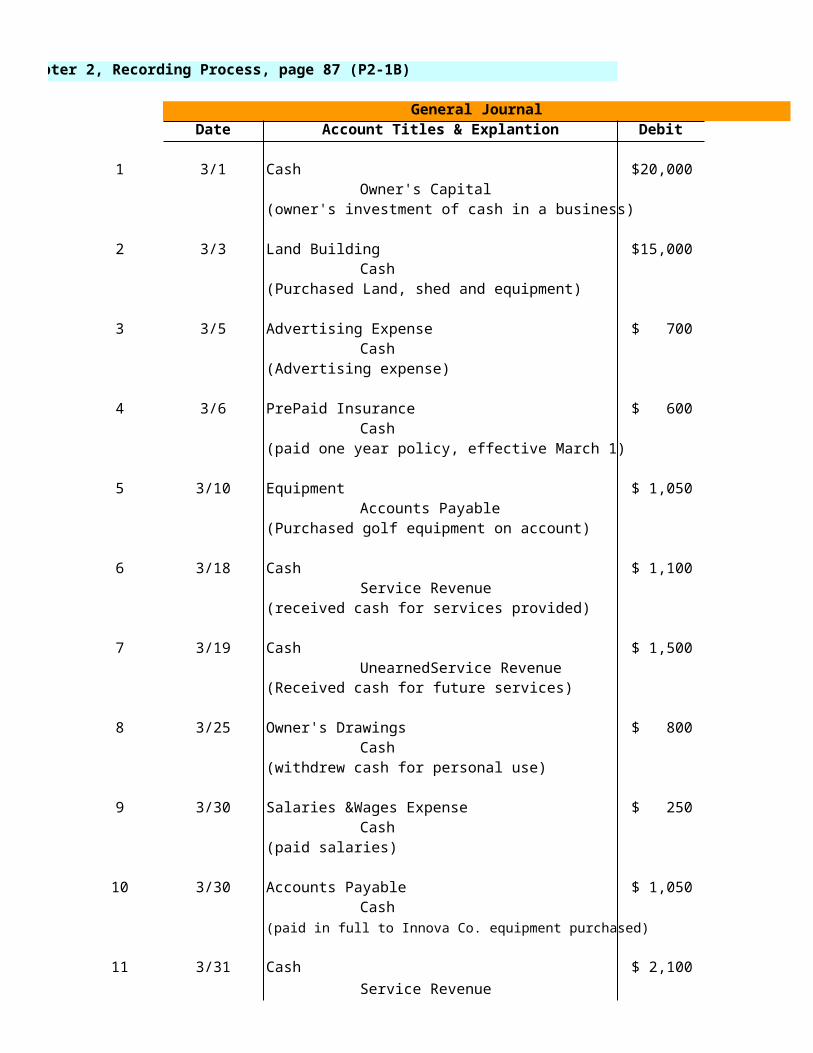

Chapter 2, Recording Process, page 87 (P2-1B)

General JournalDate Account Titles & Explantion Debit Credit

1 3/1 Cash $ 20,000 Owner's Capital 20,000

(owner's investment of cash in a business)

2 3/3 Land Building $ 15,000 Cash $ 15,000

(Purchased Land, shed and equipment)

3 3/5 Advertising Expense $ 700 Cash 700

(Advertising expense)

4 3/6 PrePaid Insurance $ 600 Cash 600

(paid one year policy, effective March 1)

5 3/10 Equipment $ 1,050 Accounts Payable 1,050

(Purchased golf equipment on account)

6 3/18 Cash $ 1,100 Service Revenue 1,100

(received cash for services provided)

7 3/19 Cash $ 1,500 UnearnedService Revenue 1,500

(Received cash for future services)

8 3/25 Owner's Drawings $ 800 Cash 800

(withdrew cash for personal use)

9 3/30 Salaries &Wages Expense $ 250 Cash 250

(paid salaries)

10 3/30 Accounts Payable $ 1,050 Cash 1,050

(paid in full to Innova Co. equipment purchased)

11 3/31 Cash $ 2,100 Service Revenue 2,100

(received cash for services provided)

Chapter 2, Recording Process, page 87 (P2-1B)

General Ledger

Cash Owner's CapitalDate Debit(+) Credit(-) Balance Date Debit(-) Credit(+) Balance

3/1 $ 20,000 $ 20,000 3/1/2013 $ 20,000 $ 20,000 3/3 15,000 5,000 3/5 700 4,300 3/6 600 3,700

3/18 1,100 4,800 -Owner's Drawings3/19 1,500 6,300 Date Debit(-) Credit(+) Balance3/25 800 5,500 3/25/2013 $ 800 $ 800 3/30 250 5,250 3/30 1,050 4,200 3/31 $ 2,100 6,300

Land Building UnEarnedService RevenuesDate Debit(+) Credit(-) Balance Date Debit(-) Credit(+) Balance

3/3/2013 $ 15,000 $ 15,000 3/19/2013 $ 1,500 $ 1,500

- Salary & Wage Expense -AdvertisingExpenseDate Debit(+) Credit(-) Balance Date Debit(+) Credit(-) Balance

3/30/2013 $ 250 $ 250 3/5/2013 $ 700 $ 700

Service Revenues Accounts PayableDate Debit(-) Credit(+) Balance Date Debit(+) Credit(-) Balance

3/18/2013 $ 1,100 $ 1,100 3/10/2013 $ 1,050 3/31 2,100 3,200 3/30 $ 1,050 $ -

Prepaid Insurance EquipmentDate Debit(+) Credit(-) Balance Date Debit(+) Credit(-) Balance

3/6/2013 $ 600 $ 600 3/10/2013 $ 1,050 $ 1,050

Chapter 2, Recording Process, page 87 (P2-1B)

Frontier ParkTrial Balance, April 30

Trial BalanceAccount Title Debit Credit

Cash $ 6,300 PrePaid Insurance 600 SuppliesAccounts ReceivableLand Building 15,000 Equipment 1,050

Notes PayableAccounts Payable - UnEarned Service Revenue 1,500

Owner's Capital 20,000 Owner's Drawings 800

Service Revenue 3,200 Rent ExpenseAdevertising Expense 700 Salaries & Wages Expense 250

$ 24,700 $ 24,700

Chapter 2, Recording Process, page 87 (P2-1B)

P2-1B Forte Disc Golf Course was opened on March 1 by Matt Forte. The following selectedevents and transactions occurred during March.

1 Mar. 1 Invested $20,000 cash in the business.2 3 Purchased Heeren’s Golf Land for $15,000 cash. The price consists of land $12,000,

shed $2,000, and equipment $1,000. (Make one compound entry.)3 5 Paid advertising expenses of $700.4 6 Paid cash $600 for a one-year insurance policy.5 10 Purchased golf discs and other equipment for $1,050 from Innova Company payable

in 30 days.6 18 Received $1,100 in cash for golf fees earned (Forte records golf fees as service

revenue).7 19 Sold 150 coupon books for $10 each. Each book contains 4 coupons that enable the

holder to play one round of disc golf.8 25 Withdrew $800 cash for personal use.9 30 Paid salaries of $250.

10 30 Paid Innova Company in full.11 31 Received $2,100 cash for fees earned.

Matt Forte uses the following accounts: Cash, Prepaid Insurance, Land, Buildings, Equipment,Accounts Payable, Unearned Service Revenue, Owner’s Capital, Owner’s Drawings, ServiceRevenue, Advertising Expense, and Salaries and Wages Expense.InstructionsJournalize the March transactions.

Chapter 2, Recording Process, page 85 (P2-2B)

General JournalDate Account Titles & Explantion Debit Credit

1 5/1 Cash $ 20,000 Owner's Capital 20,000 1

(owner's investment of cash in a business) 2

2 5/2 Rent expense $ 1,100 3Cash 1,100 4

(rent paid for the month) 56

3 5/2 Supplies $ 4,000 7Accounts payable 4,000 8

(purchased dental supply on account) 9

4 5/3 Accounts Receivable $ 5,100 Service Revenue 5,100

(Billed for services)

5 5/6 Cash $ 1,000 UnEarned Service Revenue 1,000

(cash received for future service)

6 5/11 Cash $ 2,100 Service Revenue 2,100

(Received cash for services)

7 5/30 Salaries &Wages Expense $ 2,800 Cash 2,800

(paid salaries to date)

8 5/30 Accounts Payable $ 2,400 Cash 2,400

(paid for supplies) $ 38,500 38,500

Chapter 2, Recording Process, page 85 (P2-2B)

General Ledger

Cash Owner's CapitalDate Debit(+) Credit(-) Balance Date Debit(-) Credit(+) Balance

$ 20,000 $ 20,000 $ 20,000 $ 20,000 1,100 18,900

$ 1,000 19,900 $ 2,100 22,000

2,800 19,200 -Rent Expense 2,400 16,800 Date Debit(-) Credit(+) Balance

$ 1,100 $ 1,100

Furniture & Equipmt UnEarnedService RevenuesDate Debit(+) Credit(-) Balance Date Debit(-) Credit(+) Balance

$ 1,000 $ 1,000

- Salary & Wage Expense SuppliesDate Debit(+) Credit(-) Balance Date Debit(+) Credit(-) Balance

$ 2,800 $ 2,800 $ 4,000 4,000

Service Revenues Accounts PayableDate Debit(-) Credit(+) Balance Date Debit(+) Credit(-) Balance

$ 5,100 5,100 $ 4,000 $ 4,000 2,100 7,200 $ 2,400 $ 1,600

Prepaid Insurance EquipmentDate Debit(+) Credit(-) Balance Date Debit(+) Credit(-) Balance

- Utility Expense Accounts ReceivableDate Debit(+) Credit(-) Balance Date Debit(+) Credit(-) Balance

$ 5,100 $ 5,100

Chapter 2, Recording Process, page 85 (P2-2B)

Victoria Hall DentistTrial Balance, April 30

Trial BalanceAccount Title Debit Credit

Cash $ 16,800 PrePaid InsuranceSupplies 4,000 Accounts Receivable 5,100 Land BuildingEquipment

Notes PayableAccounts Payable 1,600 UnEarned Service Revenue 1,000

Owner's Capital 20,000 Owner's Drawings

Service Revenue 7,200 utility ExpenseAdevertising ExpenseSalaries & Wages Expense 2,800 Rent Expense 1,100

$ 29,800 $ 29,800

Chapter 2, Recording Process, page 85 (P2-2B)

P2-2B Victoria Hall is a licensed dentist. During the fi rst month of the operation of her business,the following events and transactions occurred.

April 1 Invested $20,000 cash in her business.1 Hired a secretary-receptionist at a salary of $700 per week payable monthly.(No transaction) 2 Paid offi ce rent for the month $1,100.3 Purchased dental supplies on account from Smile Company $4,000.10 Provided dental services and billed insurance companies $5,100.11 Received $1,000 cash advance from Trudy Borke for an implant.20 Received $2,100 cash for services completed and delivered to John Carl.30 Paid secretary-receptionist for the month $2,800.30 Paid $2,400 to Smile Company for accounts payable due.

Victoria uses the following chart of accounts: No. 101 Cash, No. 112 Accounts Receivable, No. 126Supplies, No. 201 Accounts Payable, No. 209 Unearned Service Revenue, No. 301 Owner’s Capital,No. 400 Service Revenue, No. 726 Salaries and Wages Expense, and No. 729 Rent Expense.

Chapter 2, Recording Process, page 85 (P2-3B)

General JournalDate Account Titles & Explantion Debit Credit

1 5/1 Cash $ 40,000 Owner's Capital 40,000 1

(owner's investment of cash in a business)

2 5/1 Prepaid Rent expense $ 24,000 2Cash 24,000

(2 year rental agreement on WH) 3

3 5/1 Furniture & Equipment $ 30,000 4Cash 10,000Accounts payable 20,000

4 5/1 PrePaid Insurance $ 1,800 5Cash 1,800 6

(paid one year policy, effective May 1) 78

5 5/6 Supplies $ 500 9Cash 500 10

116 5/7 Supplies $ 1,500

Accounts payable 1,500

7 5/8 Cash $ 8,000 Accounts Receivable 12,000

Service Revenue 20,000

8 5/9 Accounts Payable $ 400 Cash 400

(paid for supplies)

9 5/10 Cash $ 3,000 Accounts Receivable 3,000 (Received cash in payment of account)

10 5/11 Utility Expense $ 350 Accounts Payable 350

11 5/12 Salaries &Wages Expense $ 6,100 Cash 6,100

Chapter 2, Recording Process, page 85 (P2-3B)

General Ledger

Cash Owner's CapitalDate Debit(+) Credit(-) Balance Date Debit(-) Credit(+) Balance

5/1 $ 40,000 $ 40,000 $ 40,000 $ 40,000 5/1 24,000 16,000 5/1 10,000 6,000 5/1 1,800 4,200 5/6 500 3,700 -Rent Expense5/8 8,000 11,700 Date Debit(-) Credit(+) Balance5/9 400 11,300 $ 24,000 $ - $ 24,000

5/10 $ 3,000 14,300 5/12 6,100 8,200

Furniture & Equipmt UnEarnedService RevenuesDate Debit(+) Credit(-) Balance Date Debit(-) Credit(+) Balance

$ 30,000 $ 30,000

- Salary & Wage Expense SuppliesDate Debit(+) Credit(-) Balance Date Debit(+) Credit(-) Balance

$ 6,100 $ 6,100 $ 500 $ 500 1,500 2,000

Service Revenues Accounts PayableDate Debit(-) Credit(+) Balance Date Debit(+) Credit(-) Balance

$ 20,000 20,000 $ 20,000 $ 20,000 1,500 $ 21,500

400 21,900 350 21,450

Prepaid Insurance EquipmentDate Debit(+) Credit(-) Balance Date Debit(+) Credit(-) Balance

$ 1,800 $ 1,800

- Utility Expense Accounts ReceivableDate Debit(+) Credit(-) Balance Date Debit(+) Credit(-) Balance

$ 350 $ 350 $ 12,000 $ 12,000 $ 3,000 $ 9,000

Chapter 2, Recording Process, page 85 (P2-3B)

Frontier ParkTrial Balance, April 30

Trial BalanceAccount Title Debit Credit

Cash 9 $ 8,200 PrePaid Insurance 1,800 Supplies 2,000 Accounts Receivable 9,000 Land BuildingEquipment 30,000

Notes PayableAccounts Payable 21,450 UnEarned Service Revenue

Owner's Capital 40,000 Owner's Drawings

Service Revenue 20,000 utility Expense 350 Adevertising ExpenseSalaries & Wages Expense 6,100 Rent Expense 24,000

$ 81,450 $ 81,450

Chapter 2, Recording Process, page 85 (P2-3B)

P2-3B San Jose Services was formed on May 1, 2012. The following transactions took placeduring the fi rst month

Transactions on May 1:1. Jarron Gilbert invested $40,000 cash in the company, as its sole owner.2. Hired two employees to work in the warehouse. They will each be paid a salary of $3,050 permonth. (No transaction) 3. Signed a 2-year rental agreement on a warehouse; paid $24,000 cash in advance for the fi rstyear.4. Purchased furniture and equipment costing $30,000. A cash payment of $10,000 was madeimmediately; the remainder will be paid in 6 months.5. Paid $1,800 cash for a one-year insurance policy on the furniture and equipment.

Transactions during the remainder of the month:

6. Purchased basic offi ce supplies for $500 cash.7. Purchased more offi ce supplies for $1,500 on account.8. Total revenues earned were $20,000—$8,000 cash and $12,000 on account.9. Paid $400 to suppliers for accounts payable due.10. Received $3,000 from customers in payment of accounts receivable.11. Received utility bills in the amount of $350, to be paid next month.12. Paid the monthly salaries of the two employees, totalling $6,100.

Instructions(a) Prepare journal entries to record each of the events listed. (Omit explanations.)(b) Post the journal entries to T accounts.(c) Prepare a trial balance as of May 31, 2012.Trial balance totals $81,450