final ppt mp_04.10.15_felipe_magofke_slideshare

TRANSCRIPT

1

MP Committee:

Rosemary Fernholz, Ph.D I Fernando Fernholz, Ph.D I Francis Lethem, Ph.D

Felipe Magofke April 10, 2015

2

Master’s Project

Fostering Innovation in Chile: Challenges in “Start-Up” to “Build-Up” Entrepreneurship

This is where CHILE needs to be

But are we going in the right direction?

3

RESEARCH FOR MASTER PROJECT: A GREAT JOURNEY!

CLIENT: CORFO (Vice. President Eduardo Bitran)

PROCESS MASTER PROJECT: More than 10 experts interviews 3 entrepreneurs surveys 3 workshops + 3 books More than 50 papers

PERSONAL EXPERIENCE: Working at the Ministry of

Economics and World Bank4

“The Production Development Corporation”, main agency of entrepreneurship and Innovation in Chile

INNOVATION+ACTION=START-UP TO BUILD -UP“The pure new idea is not adequate by itself to lead to implementation..... It

must be taken up by a strong character (entrepreneur) and implemented through his influence.” (Joseph A. Schumpeter)

• Small enterprises are more likely to innovate and face higher risk

• Ideas or inventions need to be translated into start-up businesses that build-up to continue and grow

5

Chile’s history of innovation highlights four main natural-resource based industries

OTHERCOPPER FISHERYFORESTRY

50%

#1 world producer

38% world’s reserves

Main export: raw

copper

Started 1820

#2 world’s producer of

salmon

40% world prod,

Start in 1973

10% 5% 35%

#10 world producer

75% subsidy

Exports start: 1974

Wine #5

Fruits

Other

CHILE IS KNOWN FOR INNOVATION IN SUCCESSFUL INDUSTRIES

Source: Pro Chile 2013 6

EXPORTS

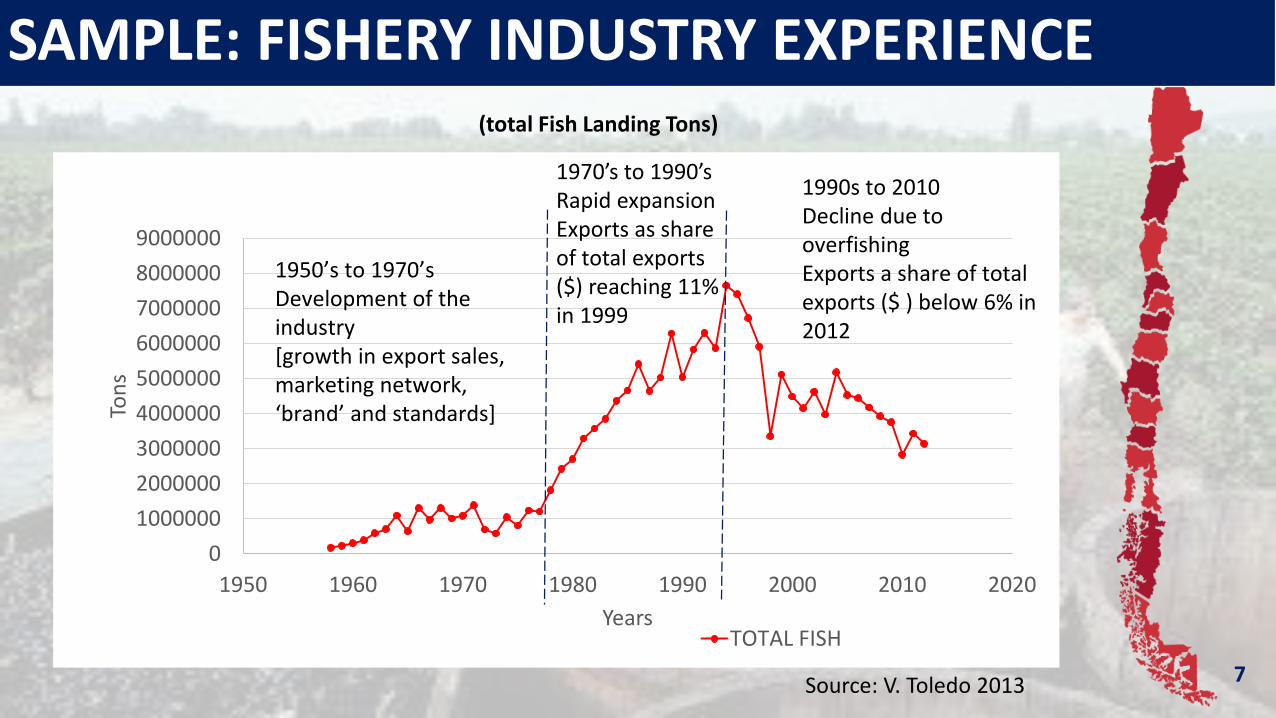

SAMPLE: FISHERY INDUSTRY EXPERIENCE

0

1000000

2000000

3000000

4000000

5000000

6000000

7000000

8000000

9000000

1950 1960 1970 1980 1990 2000 2010 2020

Ton

s

YearsTOTAL FISH

1950’s to 1970’sDevelopment of the industry[growth in export sales, marketing network, ‘brand’ and standards]

1990s to 2010Decline due to overfishingExports a share of total exports ($ ) below 6% in 2012

Source: V. Toledo 2013

1970’s to 1990’s Rapid expansionExports as share of total exports ($) reaching 11% in 1999

7

(total Fish Landing Tons)

POLICY CHALLENGE:

What policies could the Chilean Government design to ensure leadership in innovation and strengthen “start-up” to

“build-up” entrepreneurship?8

1. Background: Chile and Corfo

2. Ecosystem for entrepreneurs and innovation in Chile

i. Entrepreneurship Profile

ii. Ecosystem

iii. Current Government Approaches

3. Chilean Challenges: Innovation and Entrepreneurship

4. Analysis

5. Proposal for Start-Up to Build-Up

6. Implementation Strategy

Fostering Innovation in Chile: Challenges in Start-Up to Build-Up Entrepreneurship

9

1.5%1.0%

2.4%

1.9%2.5%

2.6%

2.9%

0.2%

0.7%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

1985-1997 1998-2009 2010-2012

GD

P G

row

thTFP

Capital

Labor

Source: Ministry of Treasury, Central Bank of Chile10

Source: Corfo 11

Main Government Agencies Main Government Programs

INCUBATORS

9%20%

31%

50%

25%

26%35%

4%

2009 2012

Large: +$5 millionMedium: $1 – $5 millionSmall: $150,000 – $1 millionMicro: $1 – $150,000

Source: Corfo12

98.69%

15.36%

48.56%37.45%

1.31%

84.64%

51.44%62.55%

0.00%10.00%20.00%30.00%40.00%50.00%60.00%70.00%80.00%90.00%

100.00%

N° ofcompanies

Total sales N° ofdependent

workers

Wagesdependent

workers(miles de UF)

SMB Large

Composition of Companies, sales, jobs, wages (2014)

0

20,000

40,000

60,000

80,000

0.00

1.00

2.00

3.00

4.00

5.00

6.00

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

Nu

mb

er o

f co

mp

anie

s p

er y

ear

New

Den

sity

Year

New Density New Firms

Density and number of new companies (2004-2012)

2.1. ENTREPRENEURSHIP PROFILE: MANY NEW COMPANIES, LOW PERCENT AND SALES OF SMEs

Source: SII

Source: World Bank

13

2.1. WHERE ARE THEIR BUSINESS?

RM (Capital), 35%

Center South, 32%

South, 20%

North, 13%

70% concentrated in the Central (around the Capital) region

Source: Ministry of Economics14

2.1 PROFILE OF THE CHILEAN ENTREPRENEURS AND THEIR ENTERPRISES (>70,000 IN 2012): HALF ARE NOT REGISTERED

31%%

369%

%

34-55 age (48%)

1,730,000 Entrepreneurs 49% are FormalMostly family-owned or not incorporated (80%)

28.4

53.7

14.5

3.4

0

10

20

30

40

50

60

%

38.8

24.1

37.1

0

10

20

30

40

50

Too small Don't findbenefits

Cost anddifficulties

%

51% Informal;(no official registration)

60% say that cost/difficulty of registering is higher than benefits

Source: Ministry of Economics

15

3. COMPANIES THAT FORMALLY REGISTER DO NOT ALWAYS START OPERATING

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

2006 2007 2008 2009 2010 2011 2012 2013

Nu

mb

er o

f co

mp

anie

s

New companies Companies starting operations

Companies out of business Net creationSource: SII I Felipe Magofke

16

3. LACK OF COLLABORATION AMONG COMPANIES

Companies Collaboration

No, 92.7

Yes, 7.3

Source: Ministry of Economics

17

3. R & D INVESTMENT IN CHILE IS CURRENTLY LOW

0.42

3.97

2.76

Chile Israel United States

Low % GDP Invested in R&D (2010)

Source: Ministry of Economics 18

Ecosystem for entrepreneurs and innovation in Chile: expert opinion (survey feedback) shows weaknesses such as R&D, education and financial support

Source: Global Entrepreneurship Monitor 2013

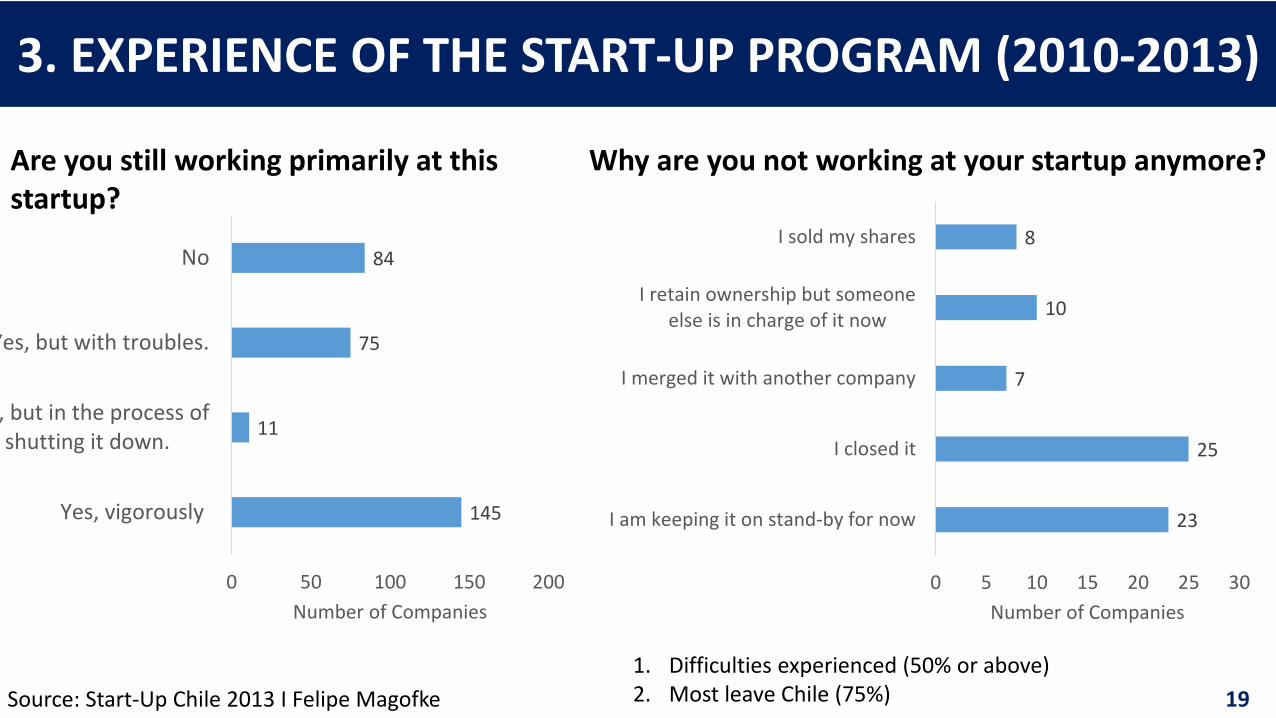

145

11

75

84

0 50 100 150 200

Yes, vigorously

Yes, but in the process ofshutting it down.

Yes, but with troubles.

No

Number of Companies

Are you still working primarily at this startup?

Why are you not working at your startup anymore?

23

25

7

10

8

0 5 10 15 20 25 30

I am keeping it on stand-by for now

I closed it

I merged it with another company

I retain ownership but someoneelse is in charge of it now

I sold my shares

Number of Companies

3. EXPERIENCE OF THE START-UP PROGRAM (2010-2013)

Source: Start-Up Chile 2013 I Felipe Magofke 19

1. Difficulties experienced (50% or above)2. Most leave Chile (75%)

Fostering Innovation in Chile: Challenges in Start-Up to Build-Up Entrepreneurship

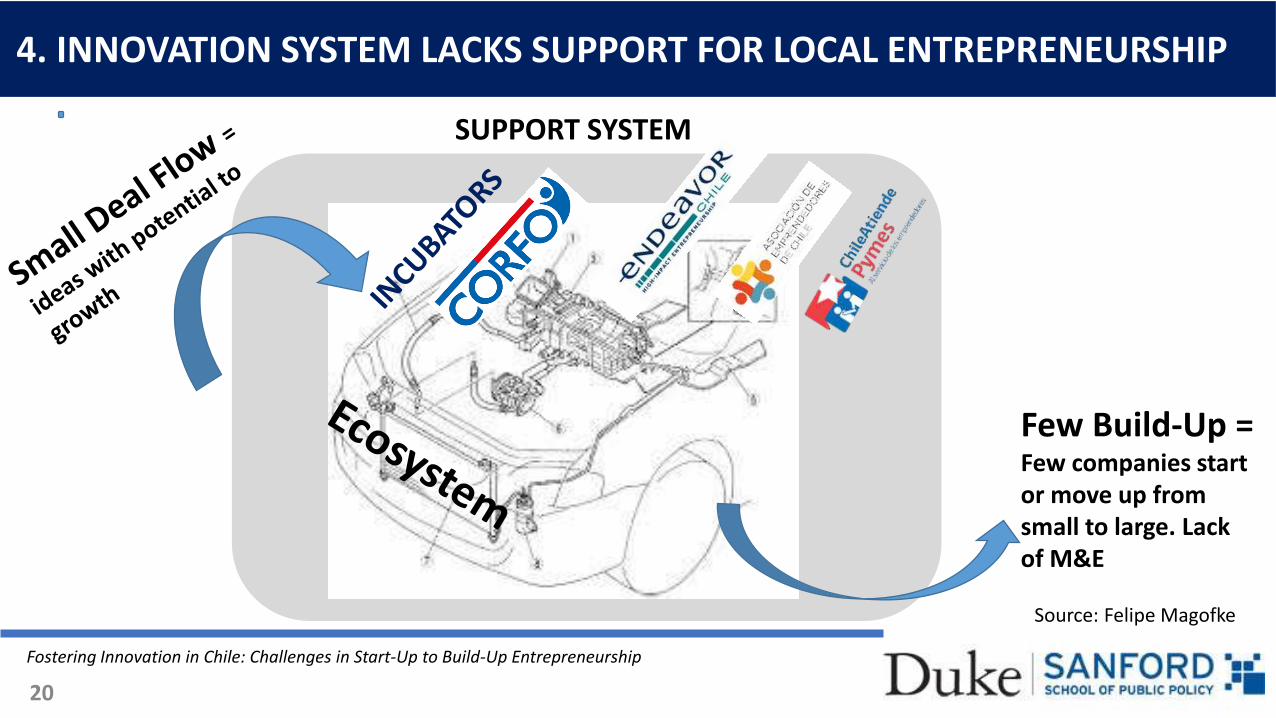

4. INNOVATION SYSTEM LACKS SUPPORT FOR LOCAL ENTREPRENEURSHIP

Few Build-Up = Few companies start or move up from small to large. Lack of M&E

Source: Felipe Magofke

20

SUPPORT SYSTEM

Fostering Innovation in Chile: Challenges in Start-Up to Build-Up Entrepreneurship

4. LOW RESPONSE FROM ENTREPRENEURS

Valley of Death

Rev

enu

e

Break even

• 70% own pocket • 10% FFF• 10% Bank• 10% Public

grants

• Low transition from S to M – L

• Most Start-up leave the country

• Just 15% of the sales

• Not enough $ support

• Few IPO• Few M&A

51% Informal

28.4

53.7

14.5

3.4

0

10

20

30

40

50

60

%

Source: Felipe Magofke

21

4. ENTREPRENEURS AND INNOVATION ECOSYSTEM IN CHILE: SWOT ANALYSIS

Solid, stable macroeconomic Good Governance

Financial Support (VC, R&D) Low Collaboration among

stakeholders (Academia, peers, etc.)

Low Education and Human Capital Measuring and tracking success Centralization

Become the Entrepreneurship and Innovation hub for LA

Foreign Networking through start-up Chile (exports)

Depreciation of local currency Latin American trap Others countries taking the lead Corruption among politician and

business (last couple of months) Natural disasters (Currently in the

North)

Inte

rnal

Ori

gin

Exte

rnal

Ori

gin

Helpful Harmful

22

4. LESSONS FROM ISRAEL AND US

Entrepreneurial culture and the mindset of people

Access to international financial markets and networks contribute to commercialization of research

A unique central government body for industrial R&D and innovation (Office of the Chief Scientist)

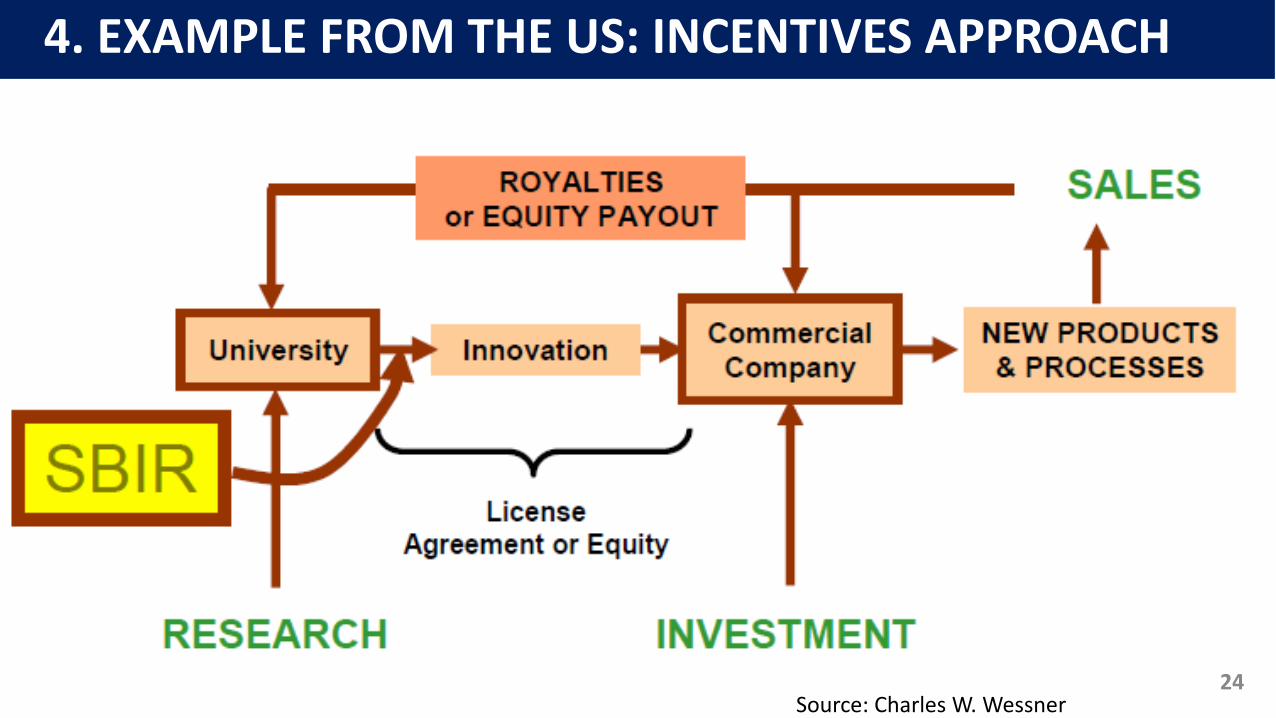

Small Business Innovation Research (SBIR)

Ecosystems and cluster models (Silicon Valley, Boston, Triangle, etc)

Advanced Technology ProgramStrong linkage with

universities and research

Source: World Bank & Charles W. Wessner23

4. EXAMPLE FROM THE US: INCENTIVES APPROACH

Source: Charles W. Wessner24

GOAL SHORT TERM MEDIUM AND LONG TERM

Research & Development Expand R&D: e.g. Small Business Innovation Research (SBIR)

Increase the investment in R&D by 30% each year until reach 2% of the GDP

Culture and Ecosystem Implement the week of Innovation and Entrepreneurship for each School in the country

Add to the requirement of “Becas Chile” to join teams of innovation or mentor entrepreneurs

Collaboration Create a committee in each macro zones to design cluster by region

Partnership with private sector and academia to launch 5 innovation labs

Measures and Evaluation Create an Ecosystem Map Promote accountability for each

program

Create a platform to evaluate impact, as well as, track projects’ performance (MIT)

Linkage with other agencies and SII

Incentives Launch a grant that promote association among SME, Academia and Large Companies

Implement the Innovation and Entrepreneurship award by region

Develop a new proposal law for Venture Capital

5. PROPOSAL: MOVING FROM START-UP TO BUILD-UP

25

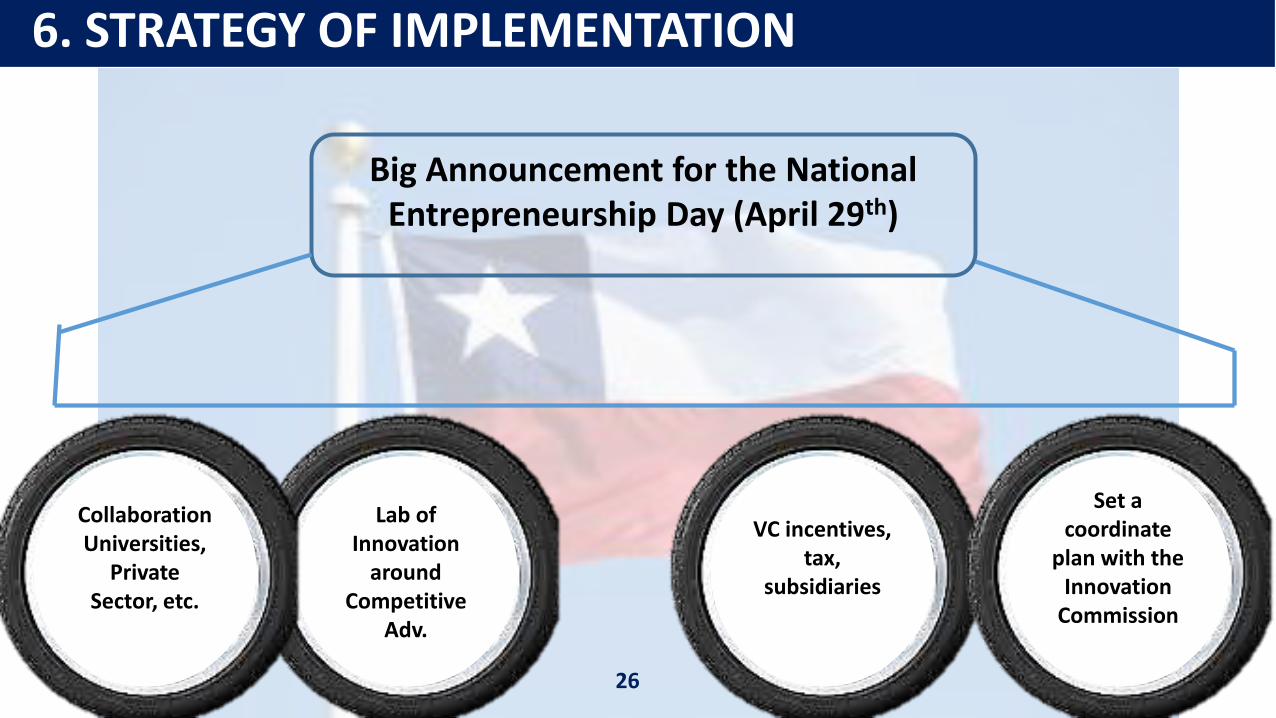

6. STRATEGY OF IMPLEMENTATION

Big Announcement for the National Entrepreneurship Day (April 29th)

Lab of Innovation

around Competitive

Adv.

VC incentives, tax,

subsidiaries

Set a coordinate

plan with the Innovation

Commission

Collaboration Universities,

Private Sector, etc.

26

MASTER PROJECT: FROM START UP TO BUILD UP

THANK YOU…

QUESTIONS?

MP Committee:

Rosemary Fernholz, Ph.D I Fernando Fernholz, Ph.D I Francis Lethem, Ph.D

Felipe Magofke April 10, 2015

Master’s Project

Fostering Innovation in Chile: Challenges in “Start-Up” to “Build-Up” Entrepreneurship