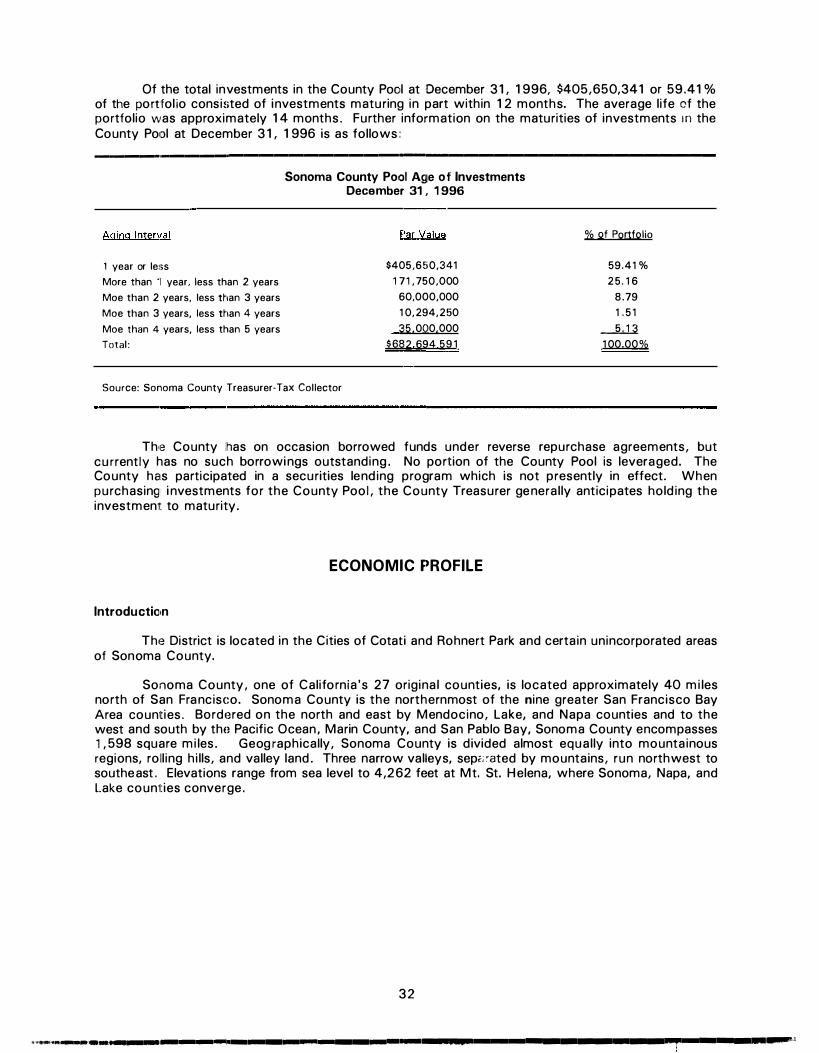

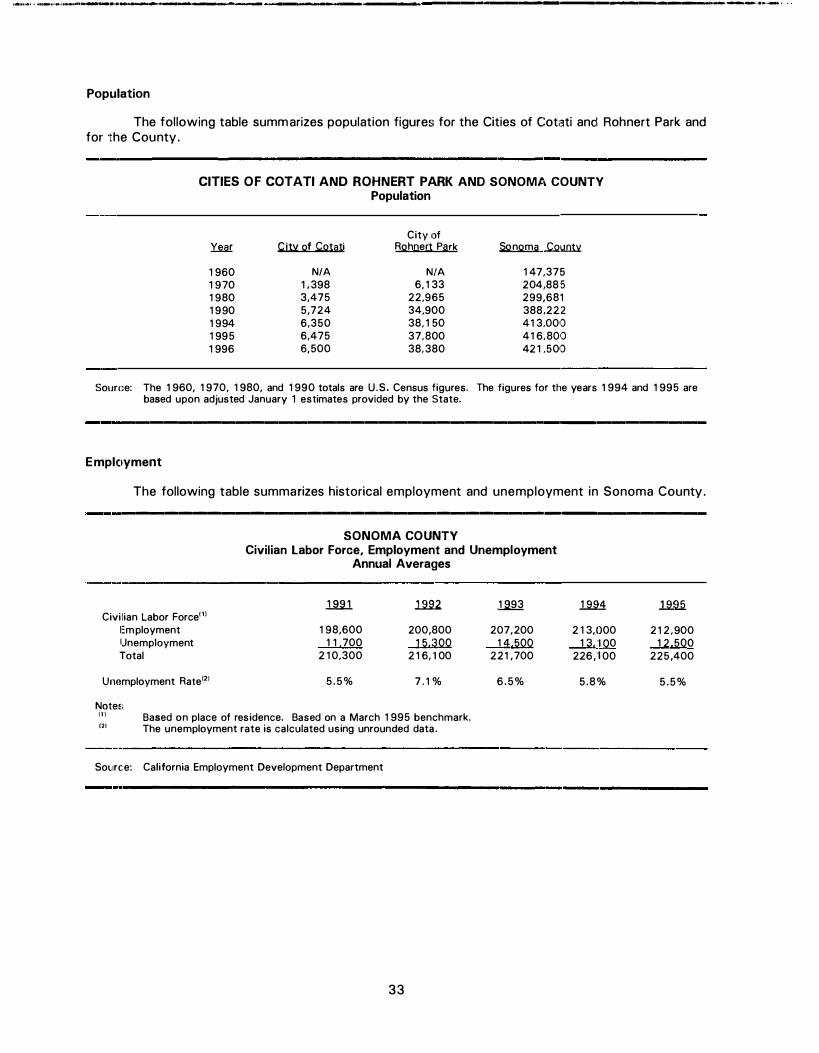

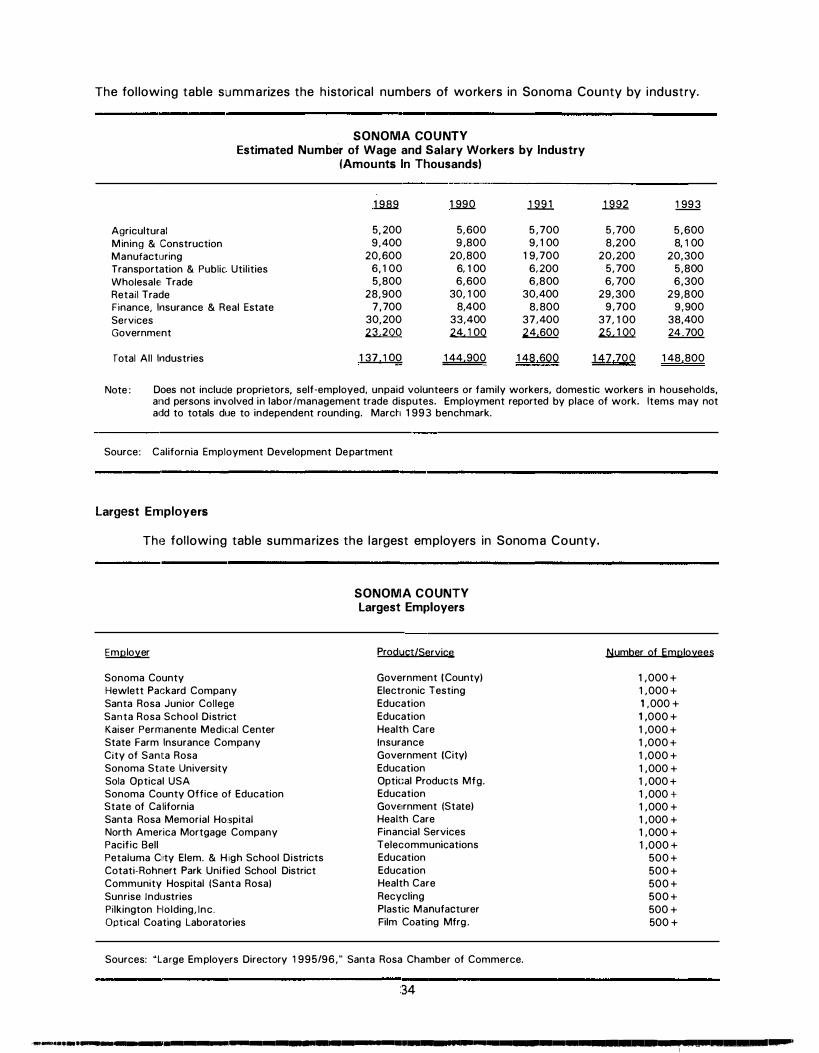

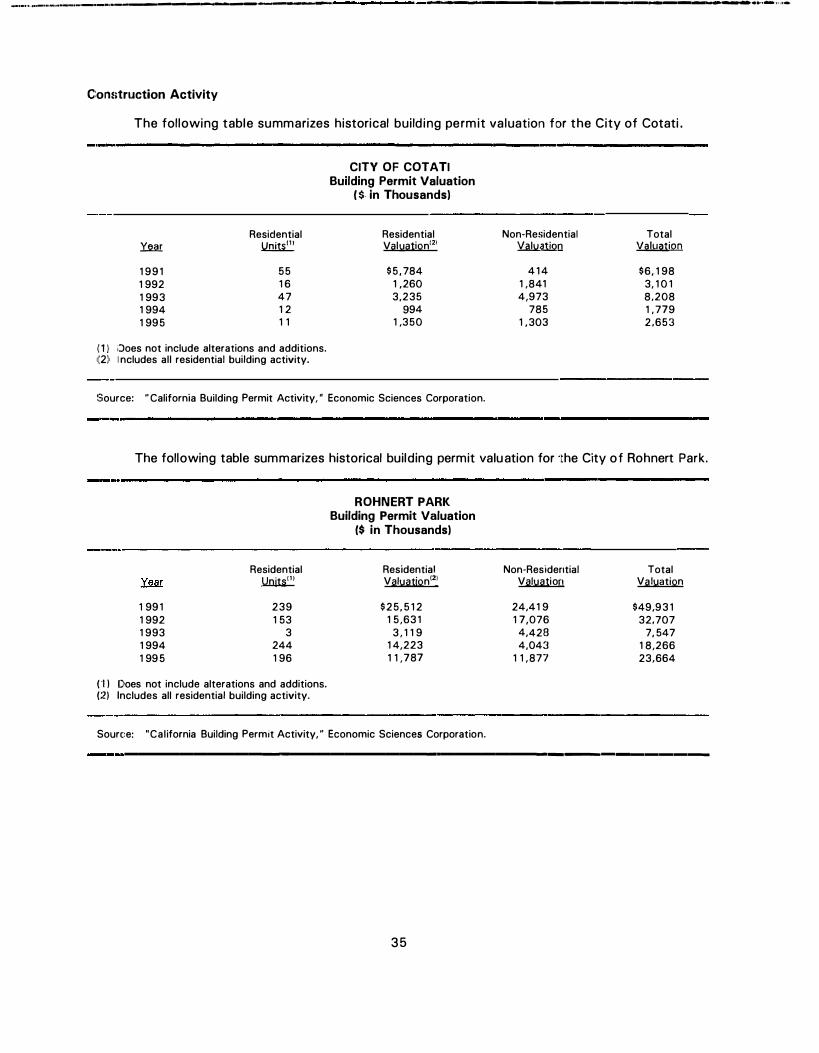

Download - tlilt;. Company - CA.gov

•lllllll,1•-•,,dl-1111Httllj••i.il ............. t. __________ ·--------------------·-----------.................. ...._;.,, ...

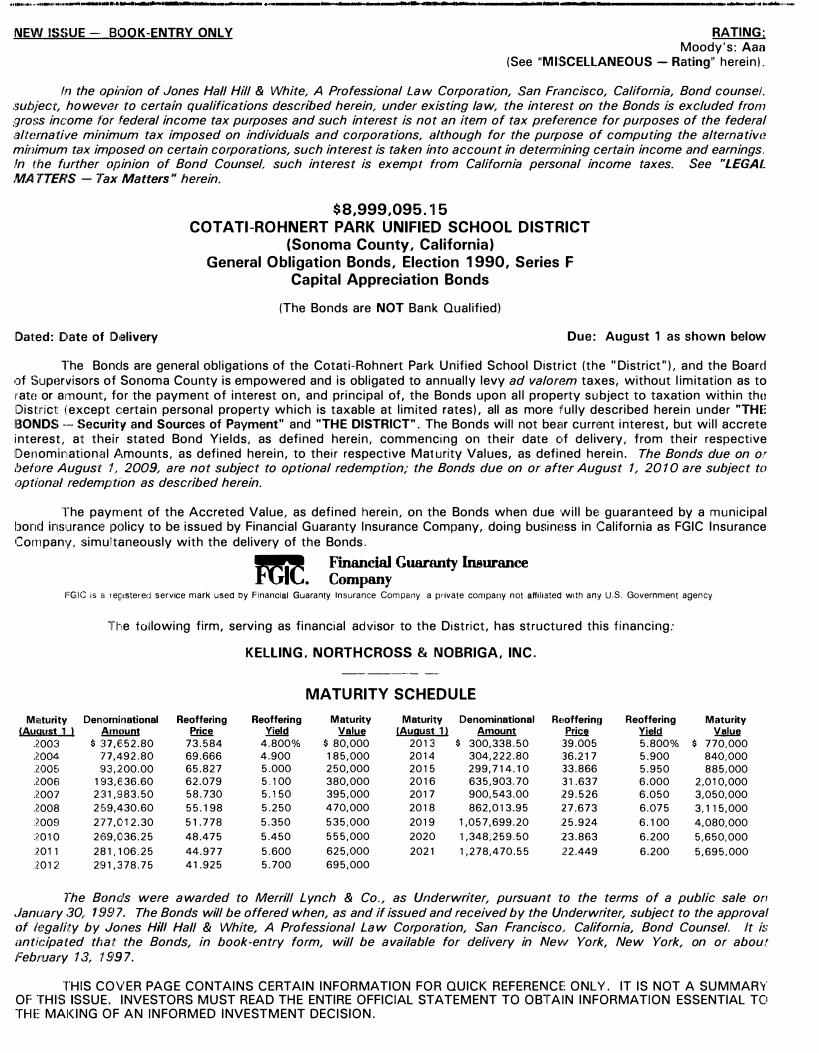

1NEWi�SUE -·_BOOK-ENTRY ONLY RATING� Moody's: Aaa

(See "MISCELLANEOUS - Rating" herein).

ln the opk1ion of Jones Hall Hill & White, A Professional Law Corporation, San Francisco, California, Bond counsel. subject, howevc�r to certain qualifications described herein, under existing law, the intewst on the Bonds is excluded from gross income for .federal income tax purposes and such interest is not an item of tax preference for purposes of the federal alternative minimum tax imposed on individuals and corporations, ;.llthough for the purpose of computing the alternative minimum tax imposed on certain corporations, such interest is taken into account in determining certain income and earnings. ln the further opinion of Bond Counsel, such interest is exempt from California personal income taxes. See "LEGAi. MATTERS - Tax Matters" herein.

IDated: Date of ID1elivery

$8,999,095. '15 COTATI-ROHNERT PARK UNIFIED SCHOOL DISTRICT

(Sonoma County, California) General Obligation Bonds, Election 1990, Series F

Capital Appreciation Bonds

(The Bonds are NOT Bank Qualified)

Due: August 1 as shown below

The Bonds are general obligations of the Cotati-Rohnert Park Unified School District (the "District"), and the Board of Supervisors of Sonoma County is empowered and is obligated to annually levy ad valorem taxes, without limitation as to rate or amount, for the payment of interest on, and principal of, the Bonds upon all property subject to taxation within tho District (except certain personal property which is taxable at limited rates), all as more fully described herein under "THE: IBONDS -- Security and Sources of Payment" and "THE DISTRICT". The Bonds will not bear current interest, but will accrete interest, at their stated Bond Yields, as defined herein, commencing on their date of delivery, from their respective Denominational Amounts, as defined herein, to their respective Maturity Values, as defined herein. The Bonds due on or before August t.. 2009, are not subject to optional redemption; the Bonds due on or after August 1, 2010 are subject to optionc1/ redemption as described herein.

The payment of the Accreted Value, as defined herein, on the Bonds when due will be guaranteed by a municipal bond insurance policy to be issued by Financial Guaranty Insurance Company, doing business in California as FGIC Insurance Company, simul1taneously with the delivery of the Bonds.

""-"' Financial Guaranty Insurance tlilt;. Company

FGIC is a rer11stered service mark used by Financial Guaranty Insurance Company. a private company not affiliated with any U.S. Government agency

Me1turity {�!!.QLISt_U

2003

2004

.WOE, 2006

2007

2008

2009

2010

:2011

:2012

The following firm, serving as financial advisor to the District, has structured this financing:

Denominational Reoffering /!!!!!)Unt Price

$ :37 ,€,52.80 73.584

77,492.80 69.666

93,200.00 65.827

193,636.60 62.079

2:31,983.50 58.730

2!59,430.60 55.198

277,012.30 51. 778

2159,036.25 48.475

281, 106.25 44.977

291,378.75 41.925

KELLING, NORTHCROSS & NOBRIGA, INC.

Reoffering Yield

4.800%

4.900

5.000

5.100

5.150

5.250

5.350

5.450

5.600

5.700

--·------ --··

MATURITY SCHEDULE

Maturity Maturity Denominational Value IAuaust_jJ Amount

$ 80,000 2013 $ 300,338.50

185,000 2014 304,222.80

250,000 2015 299,714.10

380,000 2016 635,903.70

395,000 2017 900,543.00

470,000 2018 862,013.95

535,000 2019 1,057,699.20

555,000 2020 1,348,259.50

625,000 2021 1,278,470.55

695,000

RE1offerin1J Reoffering fr.iJa Yield

39.005 5.800%

36.217 5.900

33.866 5.950

31 .637 6.000

.29.526 6.050

27.673 6.075

.25.924 6.100

:23.863 6.200

:22.449 6.200

Maturity Value

$ 770,000

840,000

885,000

2,010,000

3,050,000

3, 115,000

4,080,000

5,650,000

5,695,000

The Bonds were awarded to Merrill Lynch & Co., as Underwriter, pursuant to the terms of a public sale on January 30,. 1 g97_ The Bonds will be offered when, as and if issued and received by the Underwriter, subject to the approval of legality by Jones Hill Hall & White, A Professional Law Corporation, San Francisco .. California, Bond Counsel. It is anticipated that the Bonds, in book-entry form, will be available for delivery in New York, New York, on or about February 13, t !}9 7.

THIS COVER PAGE CONTAINS CERTAIN INFORMATION FOR QUICK REFEREI\ICE ONLY. IT IS NOT A SUMMARY OF THIS ISSUE. INVESTORS MUST READ THE ENTIRE OFFICIAL STATEMENT TO OBTAIN INFORMATION ESSENTIAL TO THE MAl<ING OF AN INFORMED INVESTMENT DECISION.

Michael Cale Supervisor, District

Paul Kelley Supervisor, District 4

SONOMA COUNTY

County Board of Supervisors

Ernie Carpenter Chairman, District 5

Tim Smith Supervisor, District 3

James Harberson Supervisor, District 2

COTATI-ROHNERT PARK UNIFIED SCHOOL DISTRICT

George Steffensen Clerk

Kim Butler Member

Board of T1rustees

Terri Palladino-King Presidtmt

District Administration

Janice L. Heffron Superintendent

Ann Huber Assistant Superintendent,

Business Services

PROFESSIONAL SERVICES

Finandal Advisor

Kelling, Northcross & Nobriga, Inc. Oakland, California

Bond Counsel

Eric Kirchmann Member

Ed Gilardi Member

Jones Hill Hall & White, A Professional Law Corporation San Francisco,, California

Paying Agent

First Trust of California, National Association Los Angeles, California

,,....,,...., ... ----·-1--1,• -------------!----------------.---------

.11111i1,i,11•t ,., ... nllH"'�*'·ililllll•l_l_Ml .. -lll>N __ __......_,. ____ -o,,,, ___ _,.. .. .........,,. __ _ _______ , ___________ ........ ......_, ............. ...

TABLE OF CON'TENTS

INTRODUCTION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 The District . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 Authority for Issuance of the Bonds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 Sources of Payment for the Bonds . ; . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 Purpose of the Bonds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2 Description of the Bonds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2 Payment of The Bonds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2 Definitions Regarding the Bonds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2 Tax Matters . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3 Professionals Involved in the Offering . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4 Offering and Delivery of the Bonds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4 Continuing Disclosure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4 Other Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

THE: :BONDS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6 Authority for Issuance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6 Purpose of The Bonds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6 Estimated Sources and Uses of Funds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6 Investment of Bond Proceeds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6 Security and Sources of Payment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7 Description of the Bonds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . 8 Redemption . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8 Form, Denomination and Payment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9 Book-Entry System . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9 Discontinuation of Book-Entry System; Payment to Beneficial Owners . . . . . . . . . . . . 11

BON[) INSURANCE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

CONSTITUTIONAL AND STATUTORY PROVISIONS AFFECTING DISTRICT REVENUES AND APPROPRIATIONS . . . . . . . . . . . . . . . . . . . . 12 Article XIIIA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13 Legislation Implementing Article XIIIA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 3 Unitary Property . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13 Proposition 62 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14 Article XIIIB . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14 Propositions 98 and 111 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 5 Proposition 187 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16 Proposition 218 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 7 Applications of Constitutional and Statutory Provisions . . . . . . . . . . . . . . . . . . . . . . . 18 Future Initiatives . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

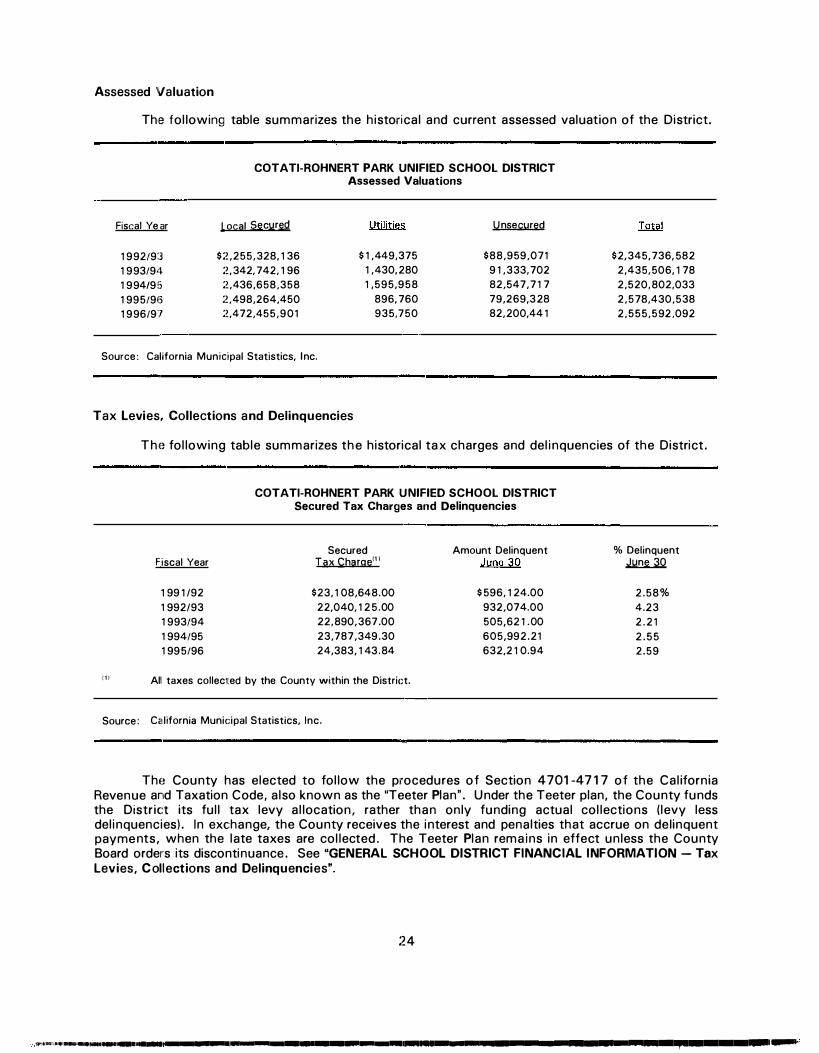

Gl:MERAL SCHOOL DISTRICT FINANCIAL INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . 18 State Funding of Education . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18 State Budget . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 8 State Lottery . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 9 Ad Valorem Property Taxation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19 Assessed Valuation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19 Tax Levies, Collections and Delinquencies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20 Budget Process . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21 Accounting Practices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

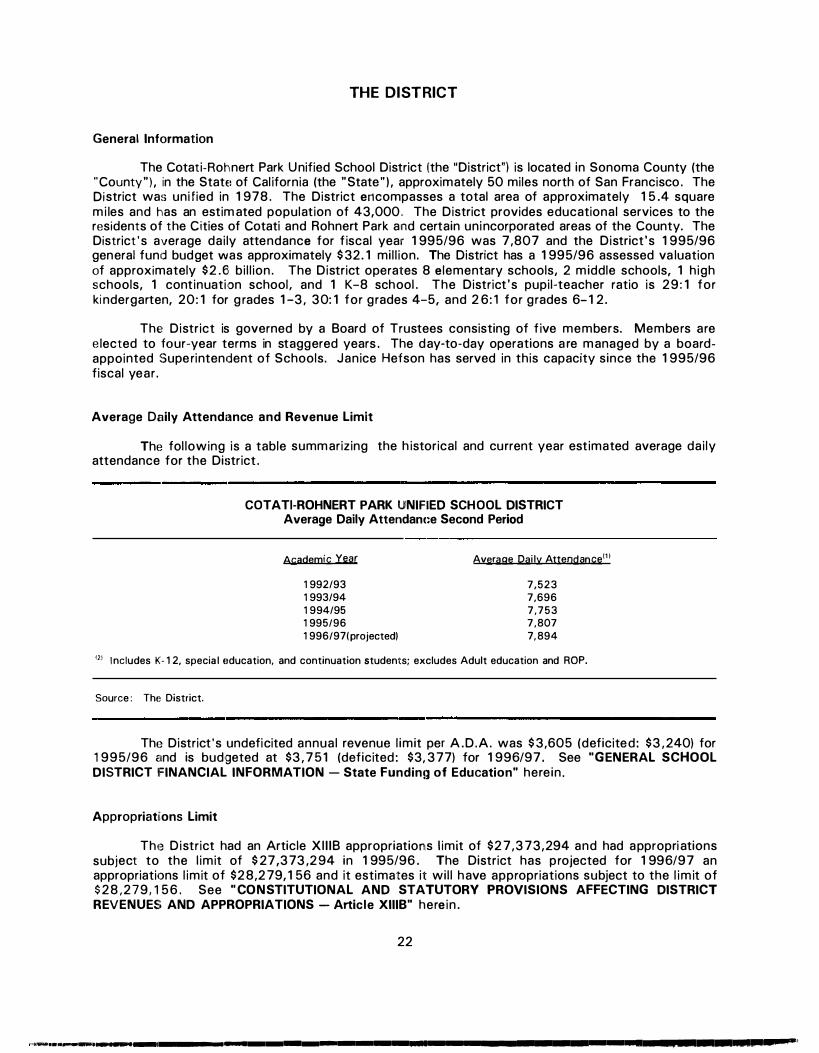

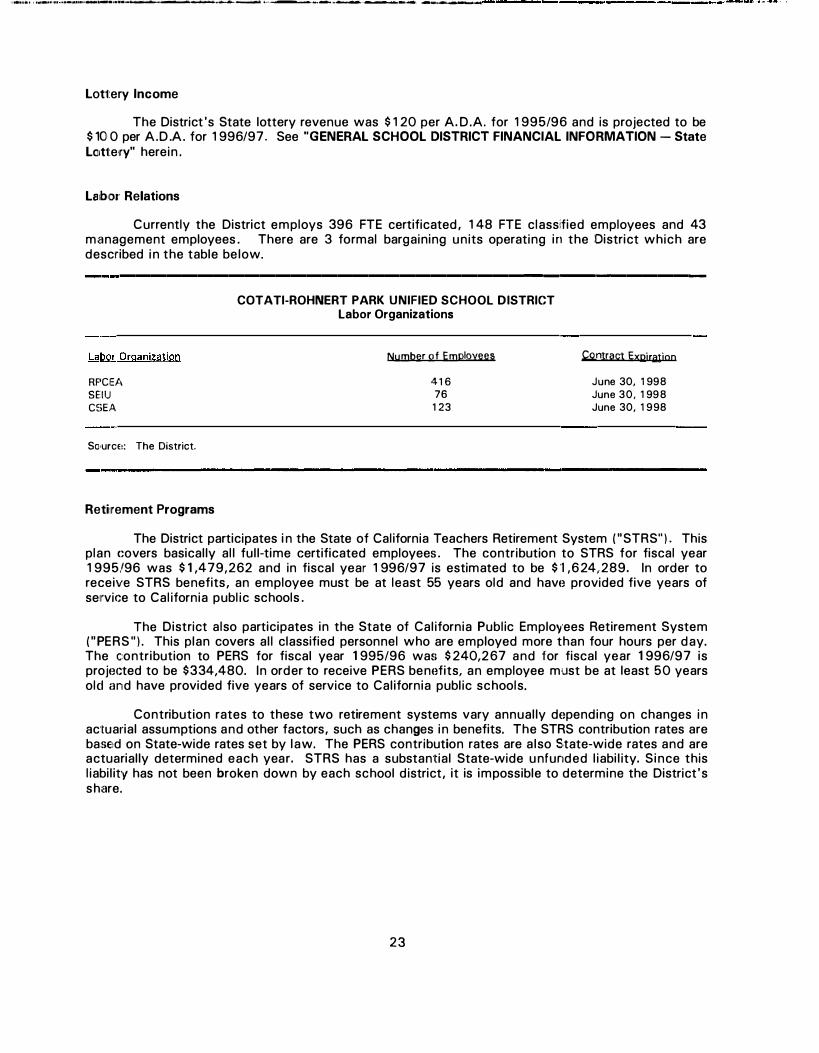

THE: DISTRICT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22 General Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22 Average Daily Attendance and Revenue Limit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

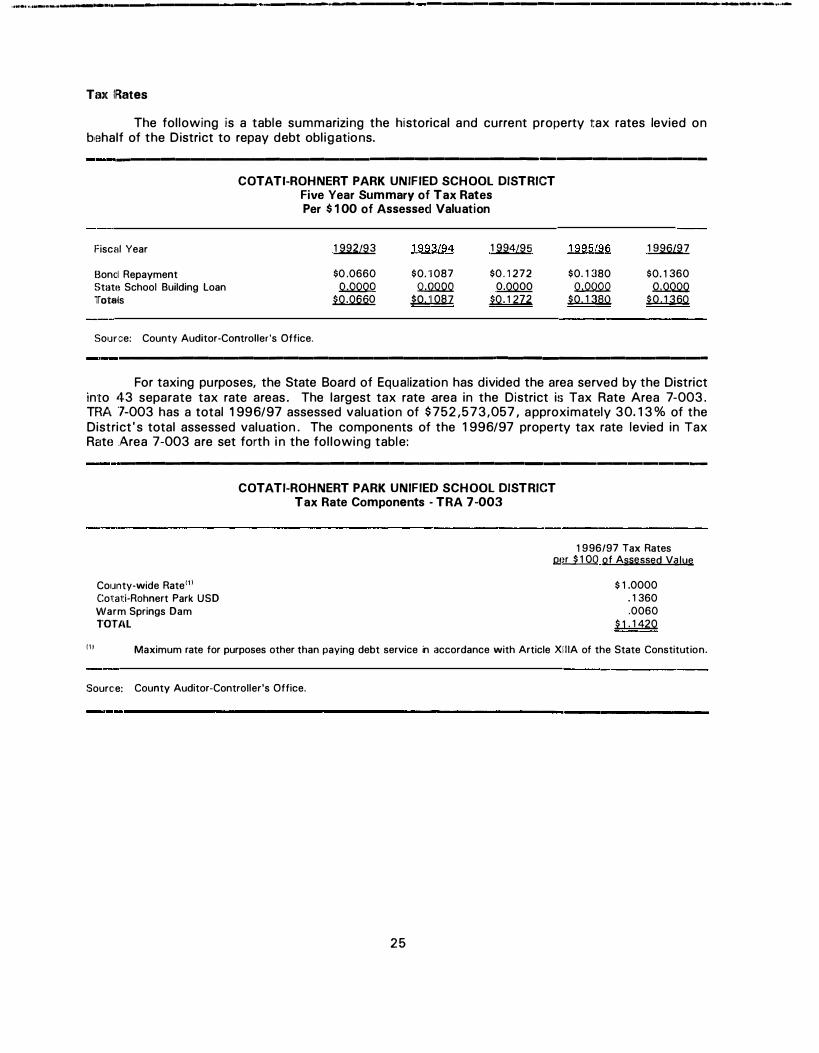

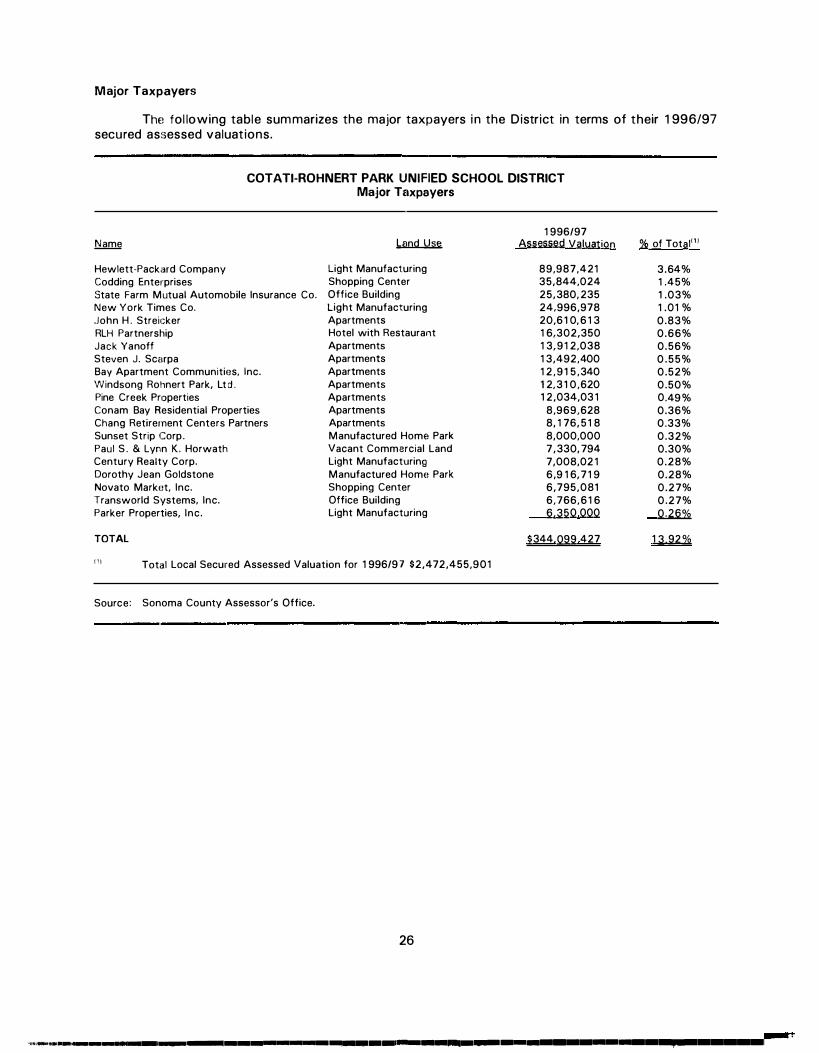

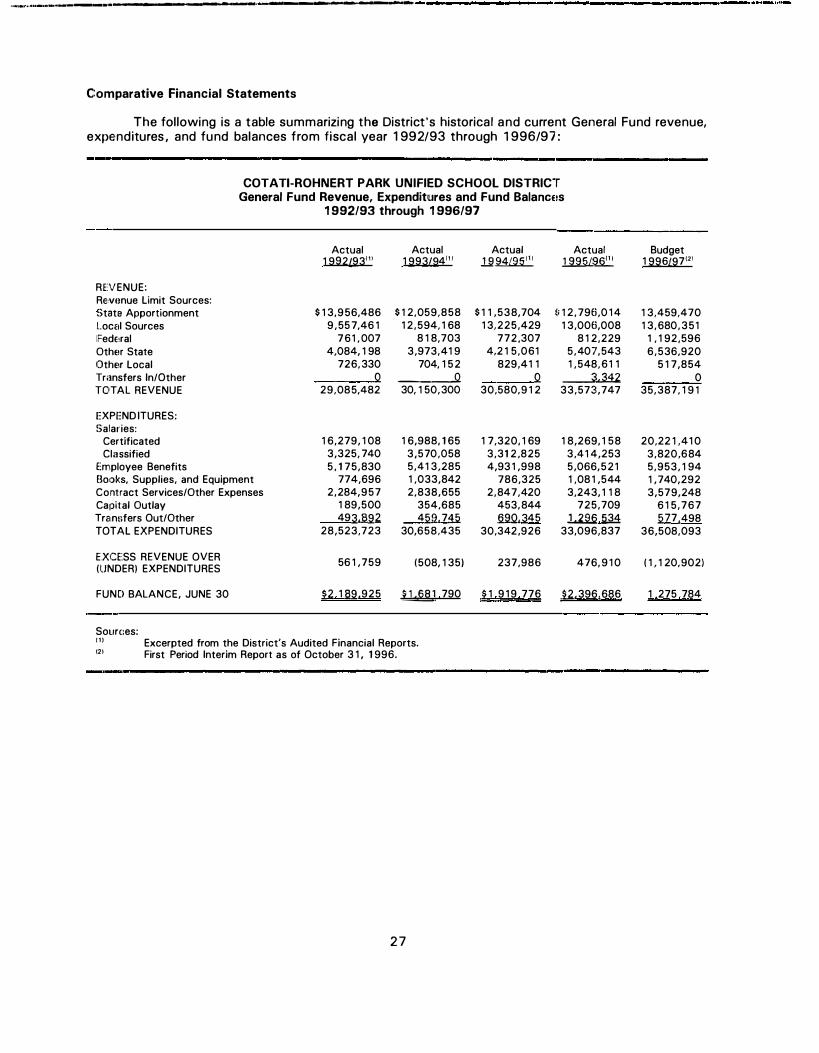

Appropriations Limit . . . . . . . . . . . . . . .. . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22 Lottery Income . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23 Labor Relations . . . . . . . . . . . . . . . . . .. . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23 Retirement Programs . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23 Assessed Valuation . . . . . . . . . . . . . . .. . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24 Tax Levies, Collections and Delinquencies . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24 Tax Rates . . . . . . . . . . . . . . . . . . . . . .. . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25 Major Taxpayers .. . . . ..... ... , . . .. . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26 Comparative Financial Statements . . . . .. . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27 District Debt Structure . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28 Statement of Direct and Overlapping Debt . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29 Investment of District Funds . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

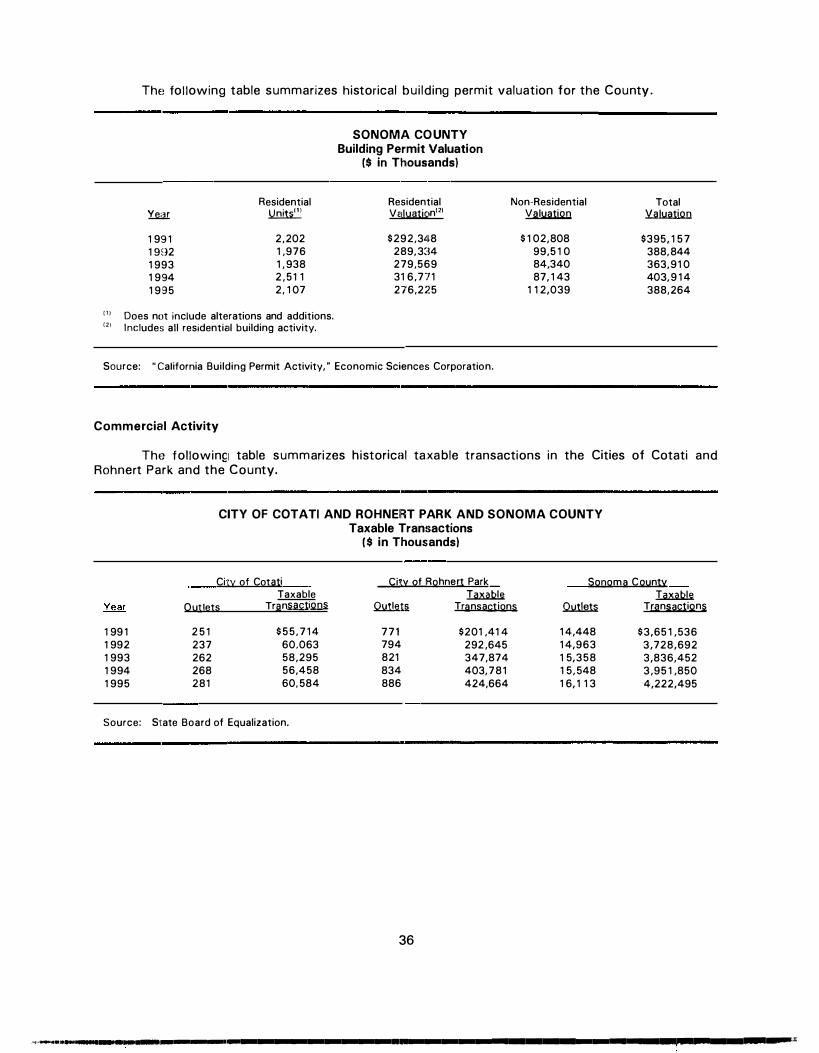

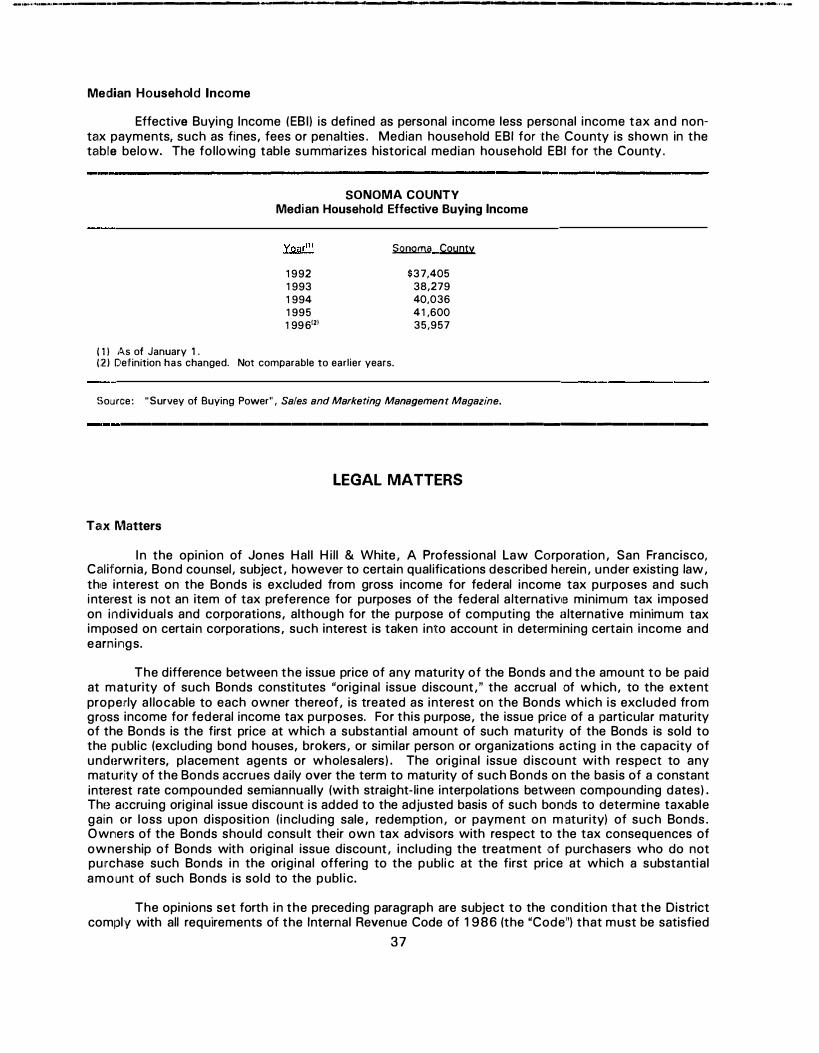

ECONOMIC PROFILE . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32 Introduction . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32 Population . . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33 Employment . . . . . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33 Lar9est Employers . . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34 Construction Activity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35 Commercial Activity . . . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36 Median Houseihold Income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

LEGAL MATTERS .. .. . .... .. .... .. .... ........ .... ..................... 37 Tax Matters . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37 No Litigation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38 Legality for Investment in California . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38 Legal Opinion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

MISCELLANEOUS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38 Rating . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38 Underwriting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39 Closing Papers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39 Continuing Disclosure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39 Additional Information . . . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

APPENDIX A - FORM OF LEGAL OPINION ................... .. ......... . .. .. .. A- 1 APPENDIX B - EXCERPTS FROM 1 995/96 AUDITED FINANCIAL STATEMENTS ........... 8-1 APPENDIX C - FORM OF CONTINUING DISCLOSURE CERTIFICATE .... ................ C-1 APPENDIX D - BOND YIELD ACCRETED VALUE TABLES ....... .................. .. D- 1 APPENDIX E - REOFFERING YIELD ACCRETED VALUE: TABLES ............... . .. .. .. E-1 APPENDIX F - SPECIMEN OF BOND INSURANCE POLICY . . . . . . . . . . . . . . . . . . . . . . . . . . . F- 1

,'if'm��r��""J�·._1_._... ____ ._. ______ I ______________ �----.... __._

....... ,,, .. ........ ,1 •• �1,, .. , ........ -........... ,,.-,--..,. .. .............,..._ .. _,..,.. -- •····--· .. ·-�-·----- ____ .,......,.., __ ....... ___ ...... ___ , ___________ ,,___: ·�-1-l

OFFICIAL ST A TEMENT

$8,999,095. 15 COT A Tl-ROHNERT PARK UNIFIED SCHOOL DISTRICT

(Sonoma County, California) General Obligation Bonds, Election 1990, Series F

Capital Appreciation Bonds (Bank Qualified)

INTRODUCTION

This introduction is not a summary of this official statement (the "Officic1I Statement'?. It is only a brief description of and guide to, and is qualified by, more complete and detailed information contained in the entire Official Statement, including the cover page and appendices hereto, and the documents summarized or described herein. A full review should be made of the entire Official Statement. The offering of the Bonds to potential investors is made only .by means of the entire Offich1I Statement.

The Official Statement, which includes the cover page and appendices hereto, is provided to furnish information in connection with the sale of $8,999,095.15 principal amount of Cotati-Rohnert Park Unified School District (Sonoma County, California), General Obligation Bonds, Election 1990, SeriHs F, Capital Appreciation Bonds (the "Bonds"), as described more fully herein.

The District

The Cotati-Rohnert Park Unified School District (the "District") is located in Sonoma County (the "County"), in the State of California (the "State"), approximately 50 miles north of San Francisco. The District was unified in 1978. The District encompasses a total area of approximately 15.4 square miles and has an estimated population of 43,000. The District provides educational services to the residents of the Cities of Cotati and Rohnert Park and certain unincorporated areas of the County. The District's average daily attendance for fiscal year 1995/96 was 7,807 and the District's 1995/96 general fund budget was approximately $32.1 million. The District has a 1995/96 assessed valuation of approximately $2.6 billion. See "THE DISTRICT" herein.

Authority for Issuance of the Bonds

The Bonds are issued pursuant to certain provisions of the State of California Education Code (the "Education Code") and pursuant to resolutions adopted by the Board of Trustees of the District and the Board of Supervisors of the County. See "THE BONDS - Authority 1'or Issuance" herein.

Sources of Payment for the Bonds

The Bonds represent a general obligation of the District, and the Board of Supervisors of the County is empowered and is obligated to annually levy ad va/orem taxes, without limitation as to rate or amount, for the payment of the interest on and principal of the Bonds, upon all property subject to taxation within the District (except certain personal property which is taxable1 at limited rates) . See "TlliE BONDS - Security and Sources of Payment," and "THE DISTRICT" herein.

1

Purpose 011' the Bonds

The net procieeds of the Bonds are expected to be used for improvements to the Mountain Shadows rv1iddle School , the purchase of portable classrooms for the Phoenix High School , the upgrade of portable bu i ld ings at the Marguerite Hahn Elementary School , construction of a performing arts center at Flancho Cotate High Schoo l , and general improvements throughout the District . See "THE BONDS - Purpose of the Bonds" here in .

Description of the Bonds

The Bonds wi!I I be issued as fully registered bonds without coupons in denominations of $5 ,000 each Maturity Value, as defined below, or any integral multiple thereof. The Bonds wi l l be registered initially in the name of Cede & Co . , as nominee of the Depository Trust Company, New York, New York ( " DTC" ) . DTC will act as securities depository for the Bonds. See "THE BONDS - Form, Denomination and Paym1:mt; Book-Entry System and Discontinuation of Book-Entry System; Payment to Beneficial Owners" here in . So long as OTC, or Cede & Co . , as its nominee, is the registered owner of a l l the Bonds, payments on the Bonds wi l l be made d i rectly to DTC, and disbursement of such payments to the DTC Participants (defined below) wi l l be the responsibi l ity of OTC, and disbursement of such payments to the Benefic ia l Owners (defined below) wil l be the responsibi l ity of the OTC Participants, as more fu l ly described hereinafter .

The Bonds maturing on and after August 1 , 201 0, may be redeemed prior to maturity at the opt ion of the D istrict, beg inning on August 1 , 2009. See "THE BONDS - Redemption" here in .

Payment of The Bondls

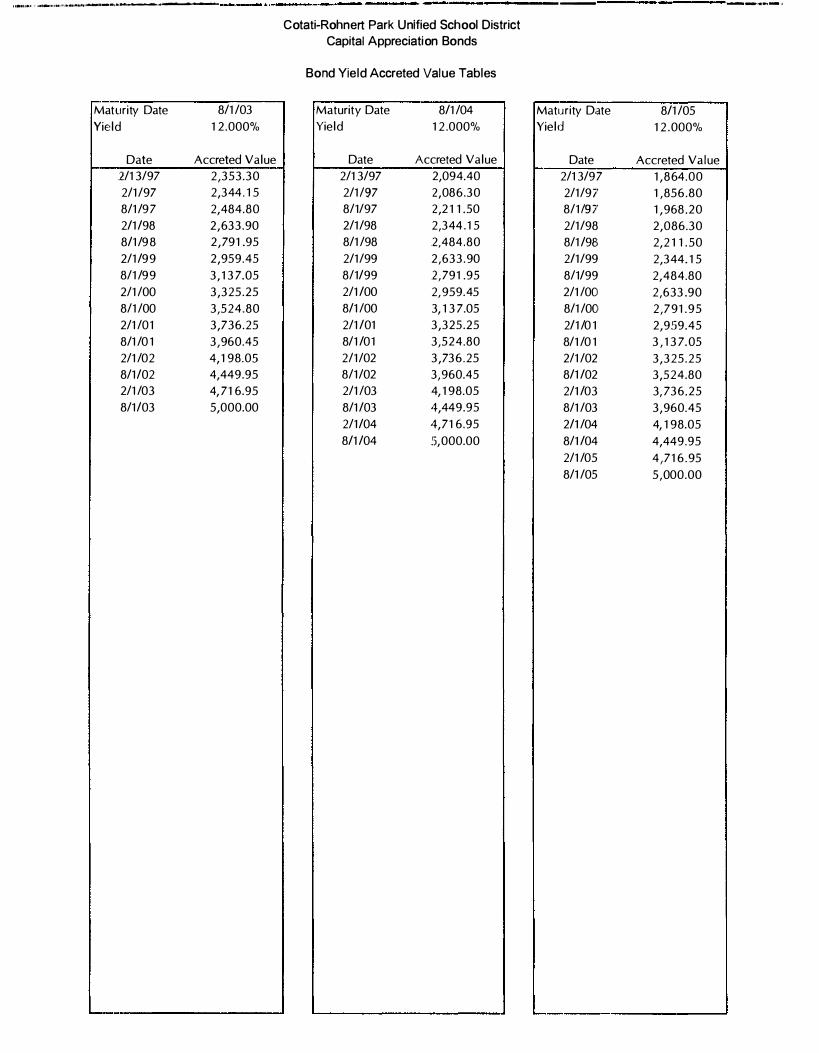

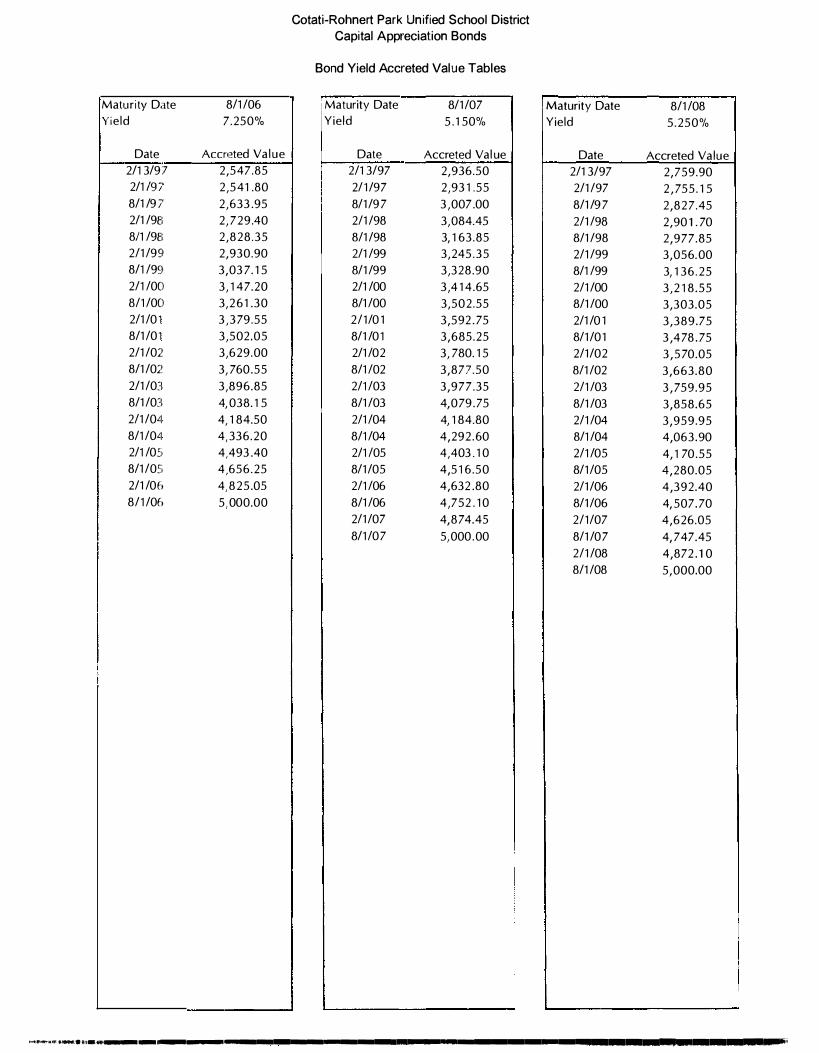

ThH Bonds wi l l not bear current interest, but wi l l accrete in value, commencing on their date of de livery, from their respective Denominational Amounts to their respective Maturity Values, compounding on a semiannual basis as described below and set forth in Tables of Accreted Values i n APPENDIX D here in . The Maturity Value for each Bond represents the Accreted Value thereof, as described below and defined in the Resolutions, calculated as of its respective August 1 maturity date . Accreted Value is payable only at maturity or upon prior redemption . See "THE BONDS - Form, Denominat1ion and Payment" herein .

Definitions Regarding the Bonds

The terms set forth below have the fol lowing meanings:

Accreted lnMrest means the difference, as of the date of calculation, between the Denominati1onal Amount and its Accreted Value, as these terms are defined below.

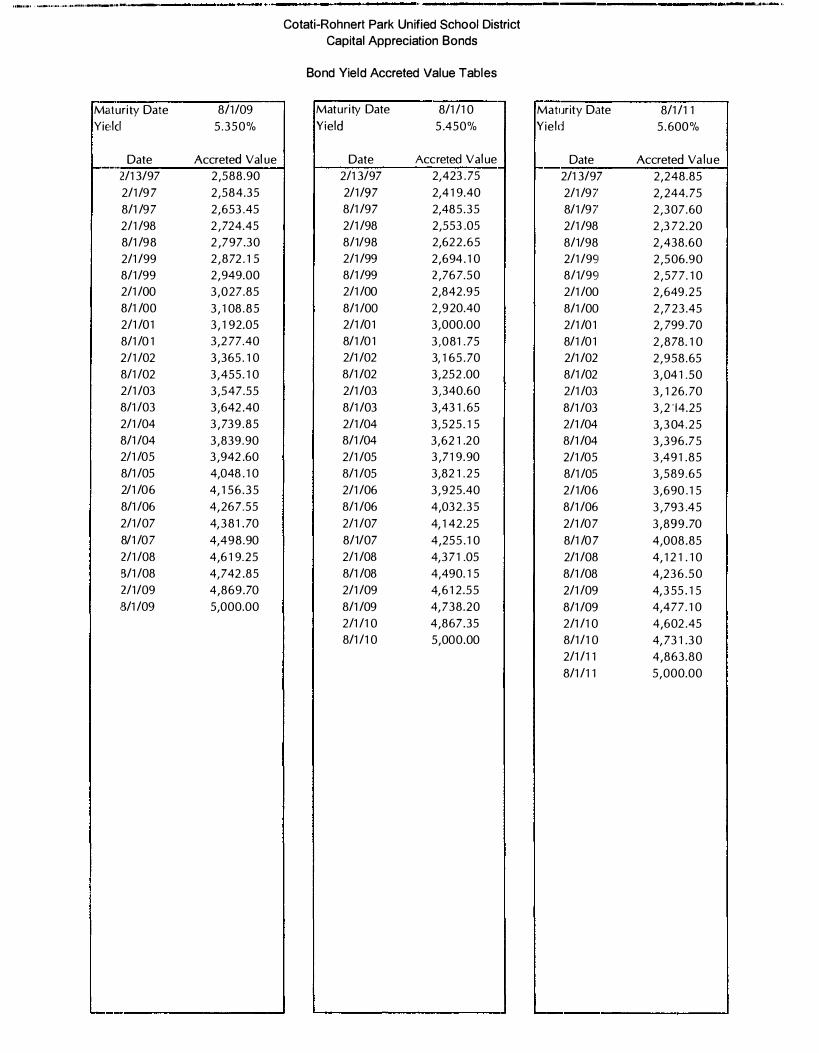

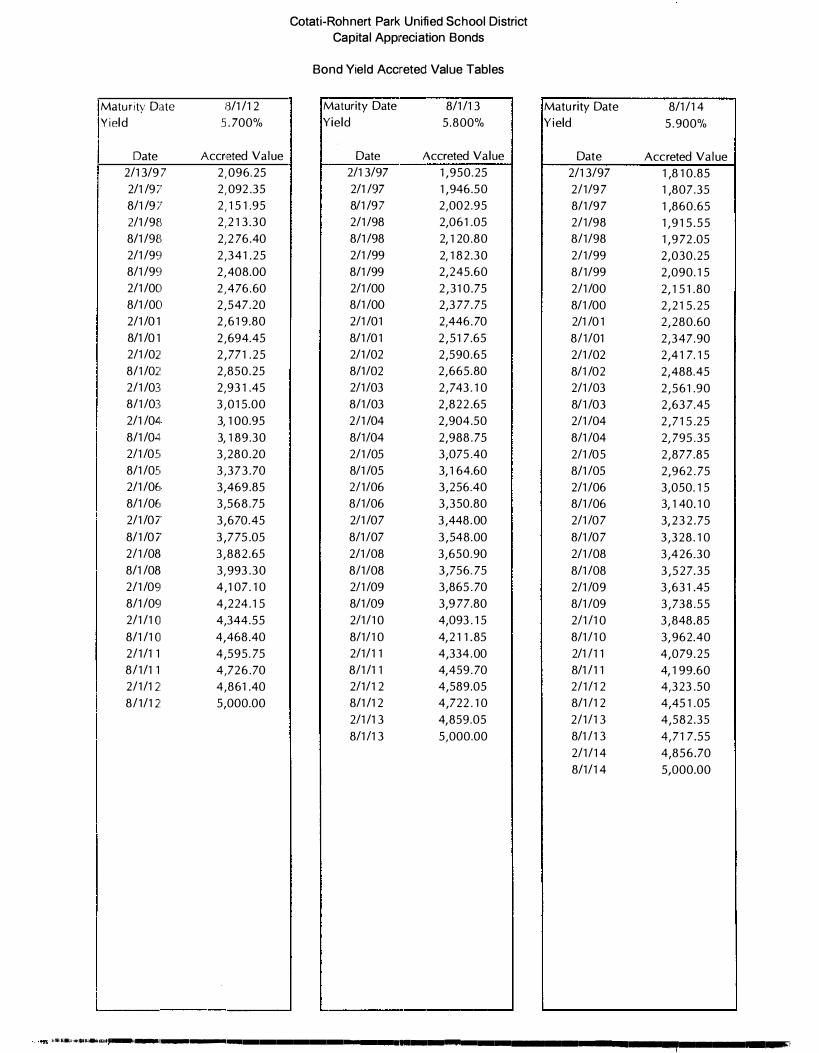

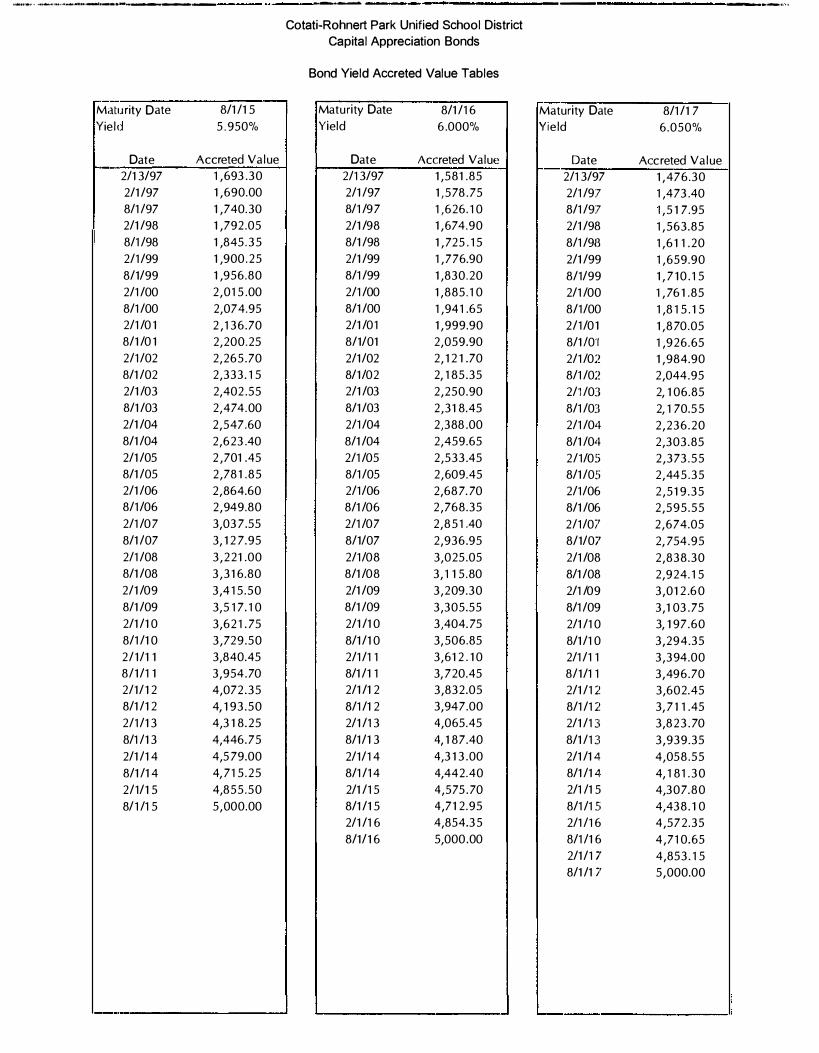

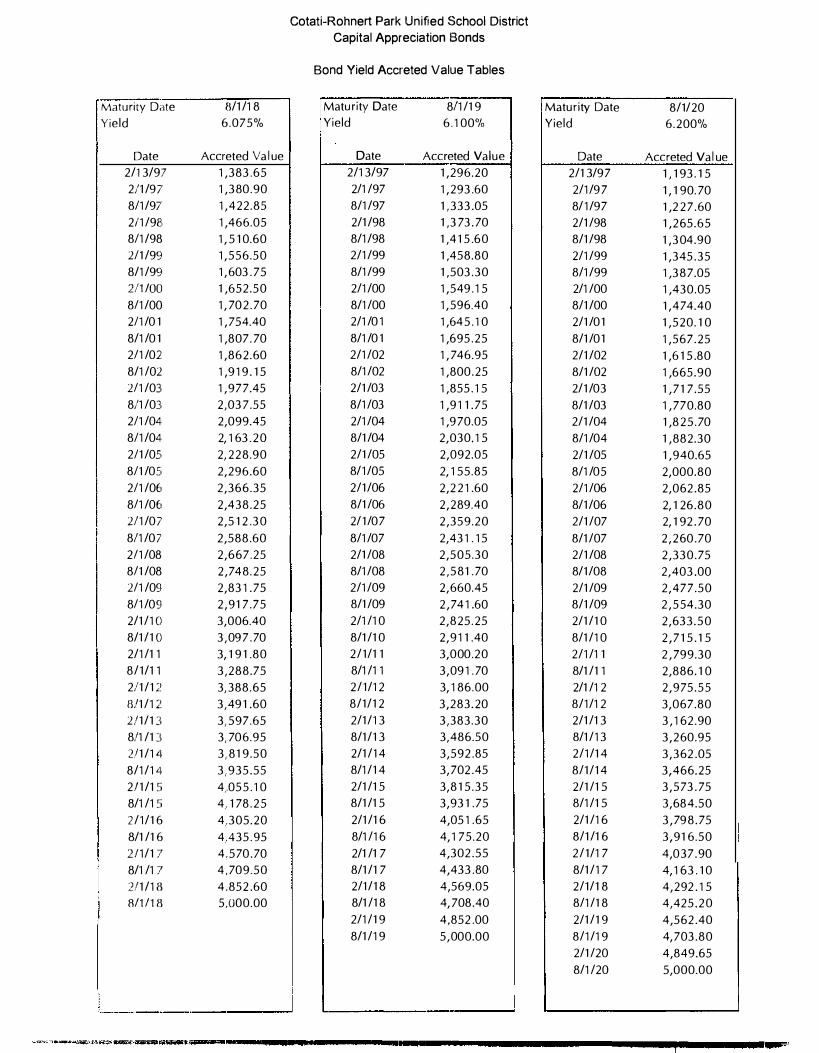

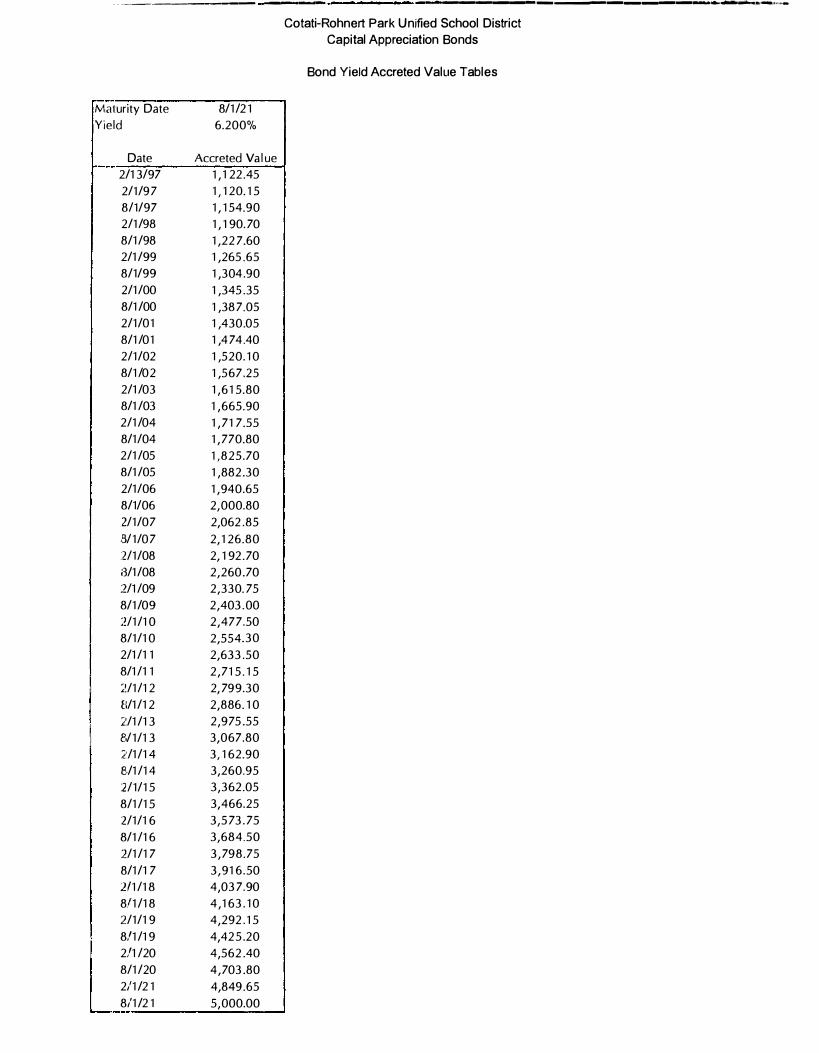

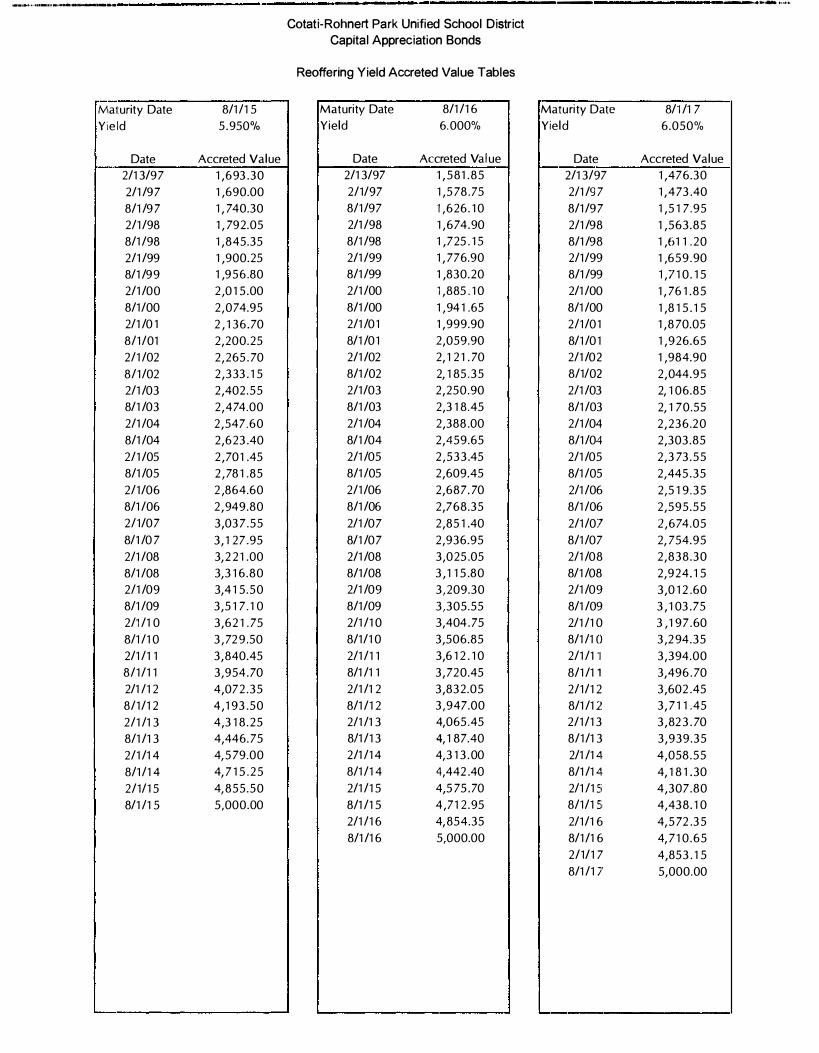

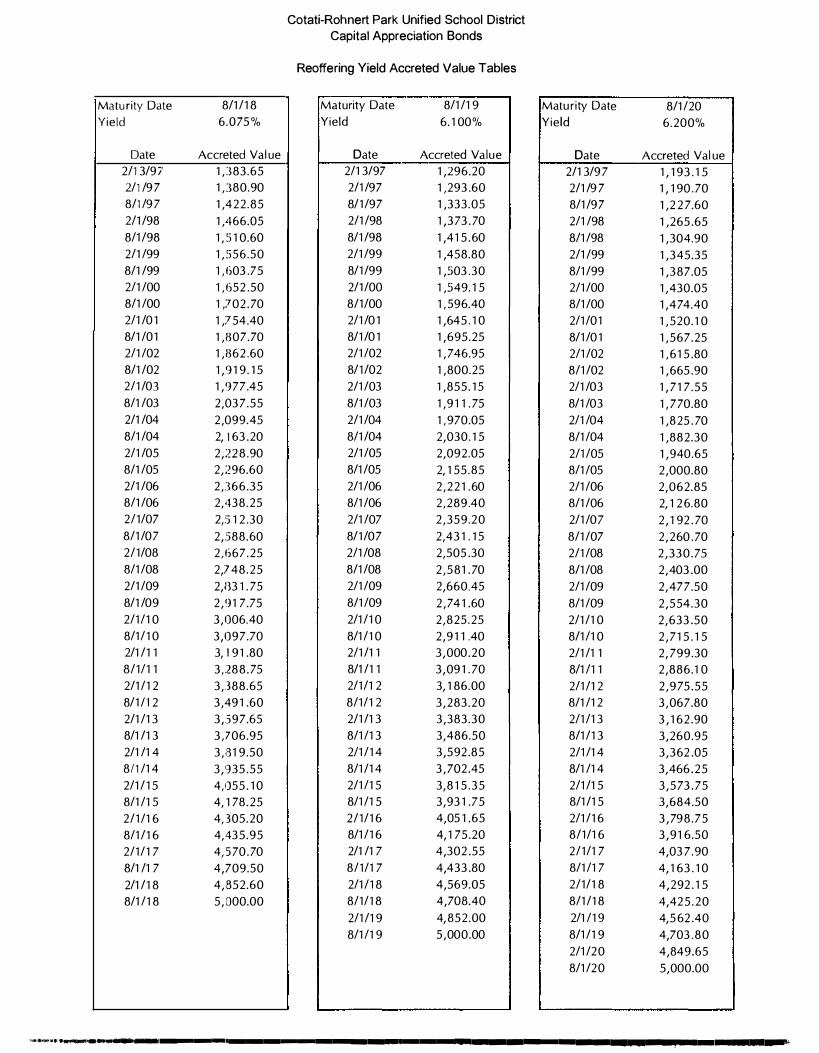

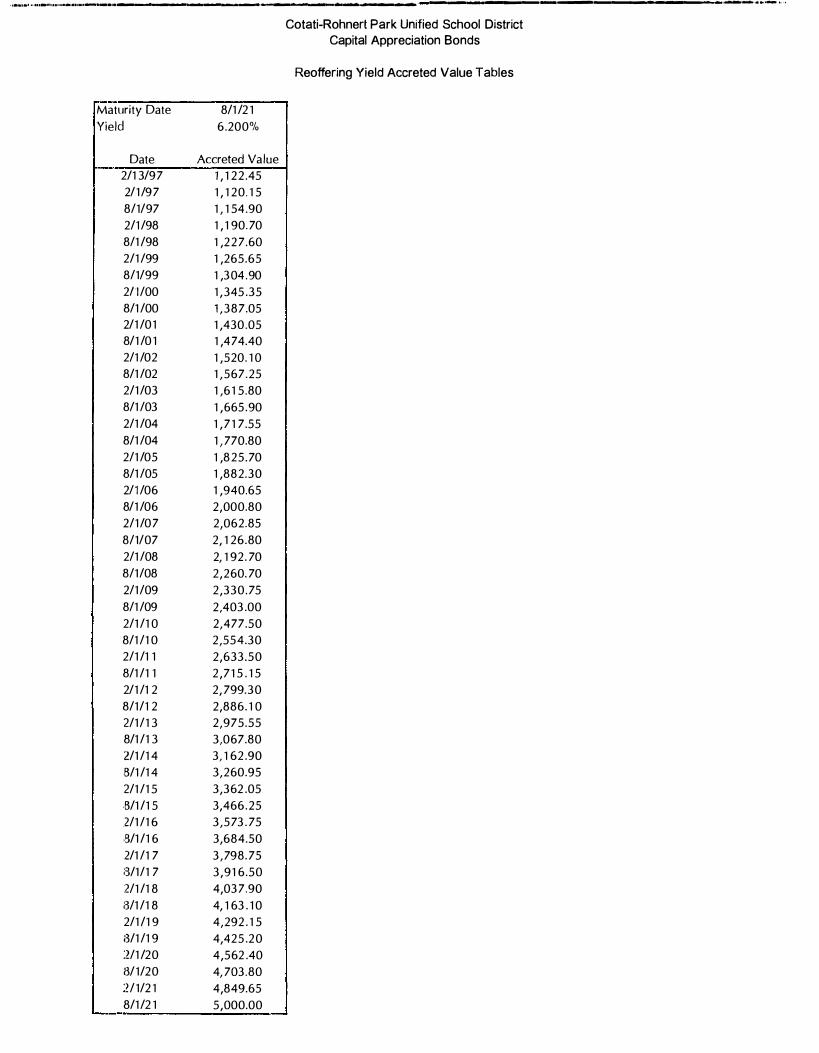

Accreted Value means, as of the date of calculation, the calculated value of a Bond upon discountinu its Maturity Value semiannual ly at its Bond Yield to said calcu lation date, assuming that with i n any such semiannual period Accreted Value i ncreases in equal daily amounts to its Accreted Value on its next semi.annual discounting date on the basis of a 360-day year of twelve 30-day months . The semiannual compounding dates for calculating Accreted Value for the Bonds are February 1 and August 1 . Tables of Accreted Values on February 1 and August 1 for the Bonds appear in APPENDIX D herein .

Bond Yield means the yield which discounts the Maturity Value of any Bond to its Denominatiional Amoui nt, as these terms are defined below. Bond Yield is calculated on the basis of a 360-day vear of twelve 30-day months, d iscounted semiannually on February 1 and August 1 . Bond Yields for the Bonds a1ppear in APPENDIX D herein .

2

-� . .i.,,� t11*i>l•""'���"'*-' ____ , ___________ I_I_IIMII ______________ .. _____ I

Capital Appreciation Bond means a bond with zero stated interest rate that accretes in value on the basis of its Bond Yield, compounding semiannually, as described below under "Accreted Value".

Denominational Amount means the initial purchase price of any Bond at which it is purchased by the Underwriter, as hereinafter defined.

Maturity Value means the Accreted Value of any Bond on its maturity date.

Reoffering Price means the price at which a Bond is initially reoffered to the public by the Underwriter.

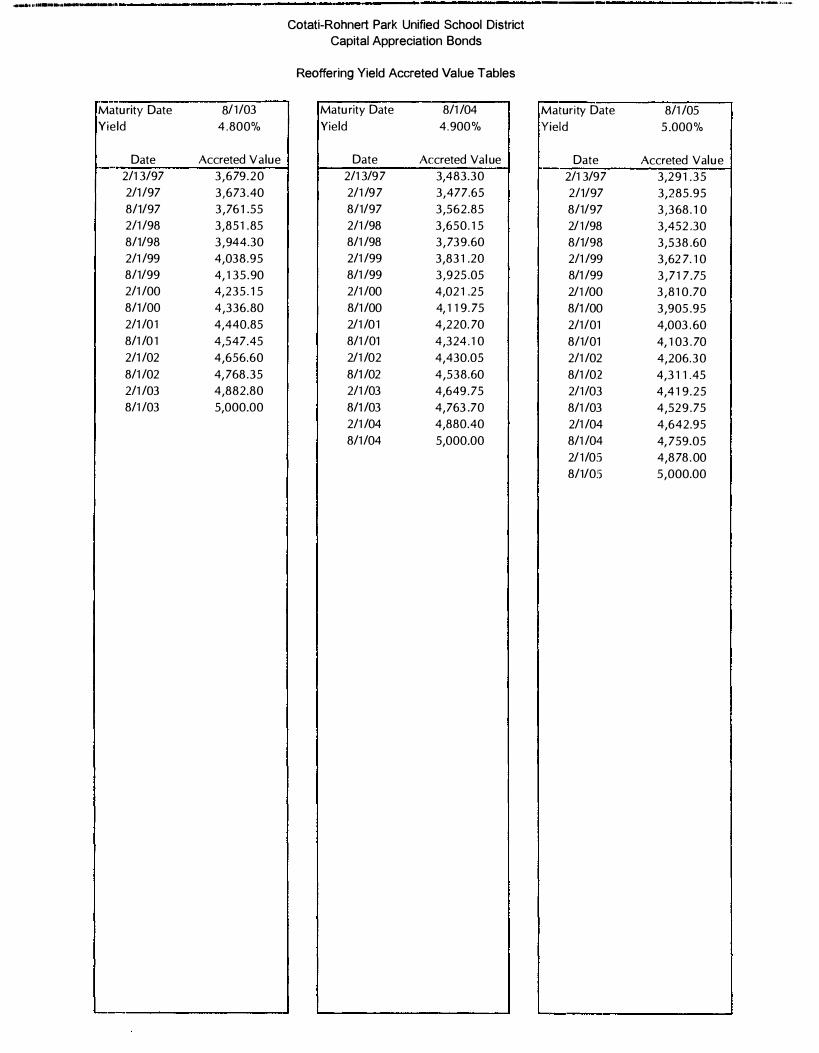

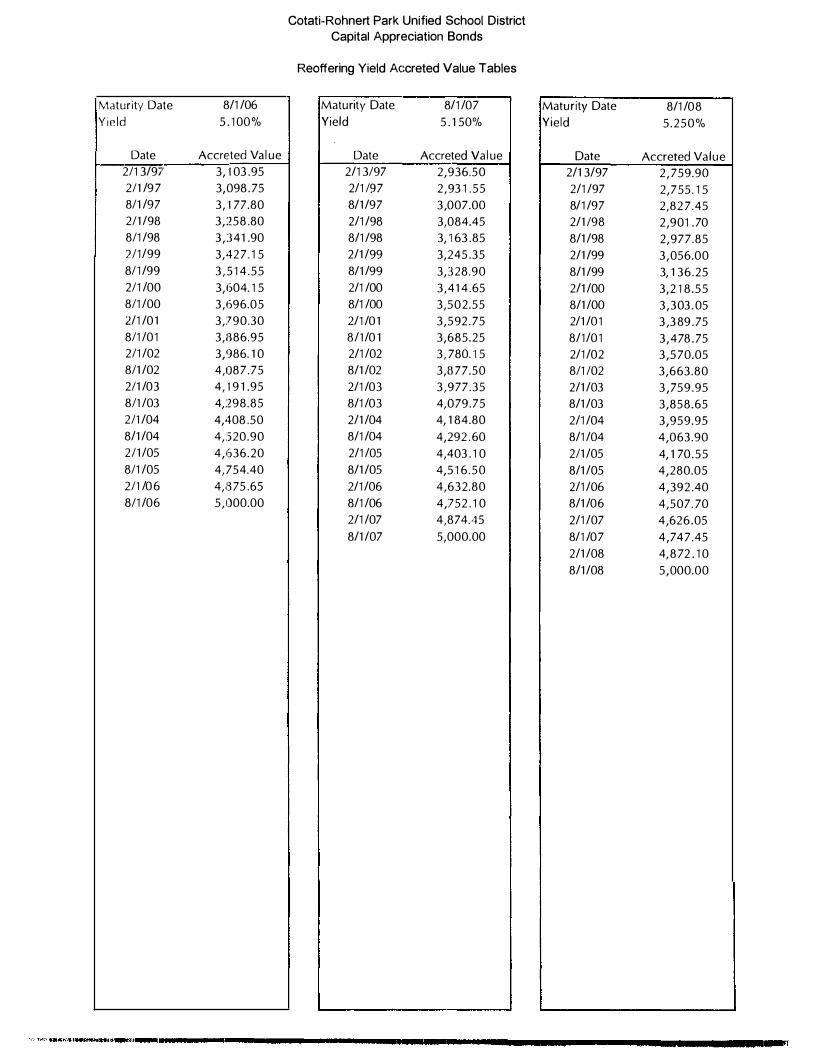

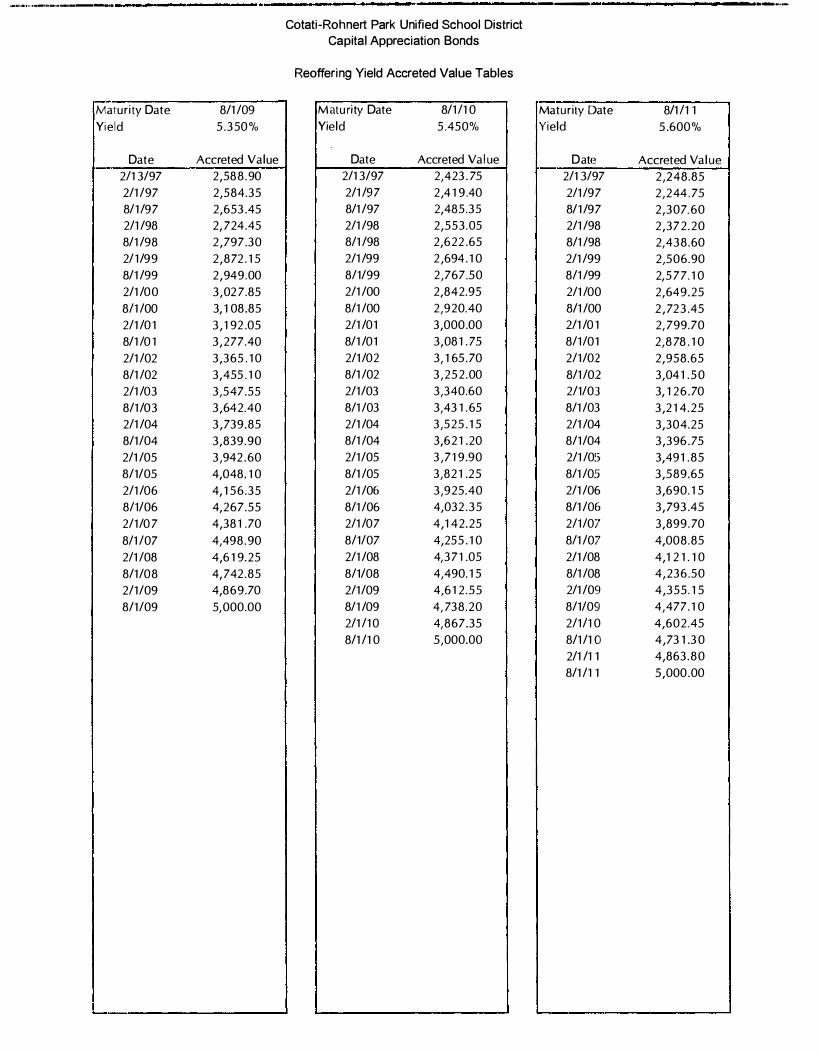

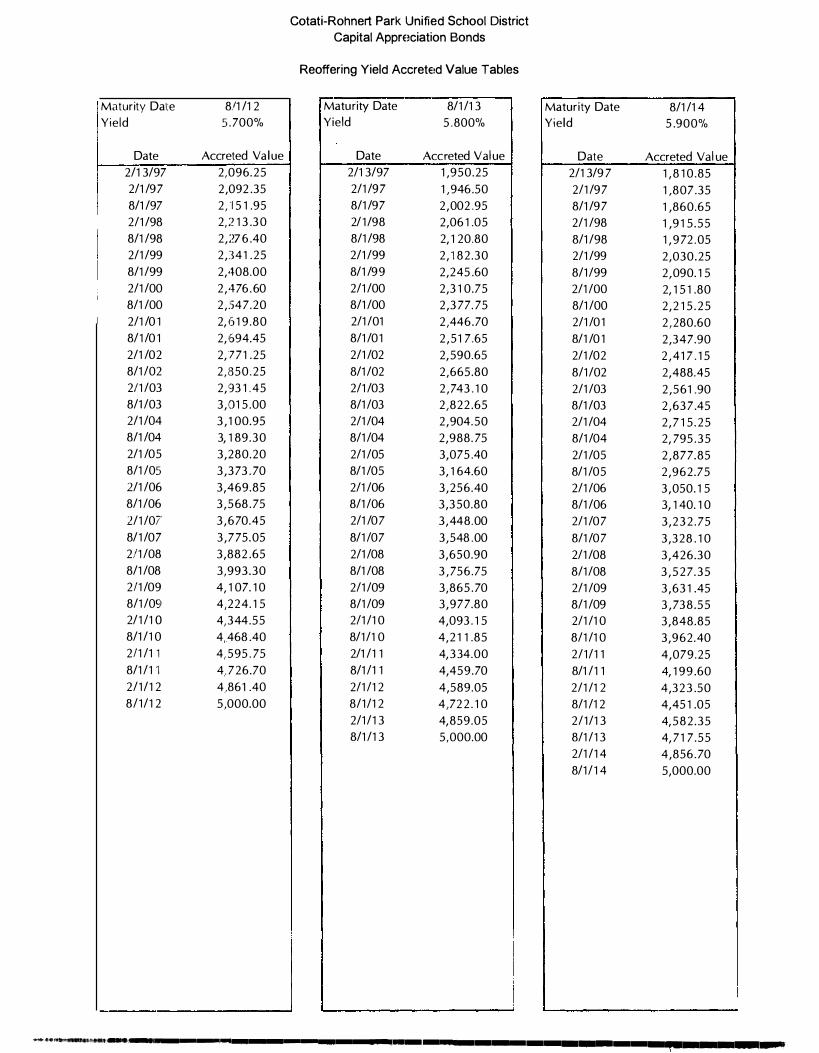

Reoffering Yield means the yield which discounts the Maturity Value of any Capital Apprnciation Bond to its Reoffering Price. Reoffering Yield is calculated on the, basis of a 360-day year o1' twelve 30-day months discounted semiannually on February 1 and August 1. Reoffering Yields on the Bonds appear on the cover page hereof and in APPENDIX E herein .

Reoffering Yield Accreted Value means, as of the date of calculation, the calculated value of a Bond upon discounting its Maturity Value semiannually at its Reoffering Yield to said calculation date , assuming that within any such semiannual period Reoffering Yield Accreted Value increases in equal daily amounts to its Reoffering Yield Accreted Value on its next semiannual compounding date on the basis of a 360-day year of twelve 30-day months . The semiannual discounting dates for calculating Reoffering Yield Accreted Value for the Bonds are February 1 and August 1 . Tables of REwffering Yield Accreted Values on February 1 and August 1 for the Bond:s appear in APPENDIX E heimin.

Transfer Amount means with respect to any Bond, the Maturity Value.

Tax Matters

In the opinion of Jones Hall Hill & White, A Professional Law Corporation, San Francisco, California, Bond Counsel, subject, however to certain qualifications described herein, under existing law, the interest on the Bonds is excluded from gross income for federal income tax purposes, such interest is not an item of tax preference for purposes of the federal alternative mini mum tax imposed on individuals and corporations, although for the purpose of computing the .alternative minimum tax imposed on certain corporations, such interest is taken into account in determiining certain income and earnings. In the further opinion of Bond Counsel, such interest is exempt from California personal income taxes . See "LEGAL MATTERS - Tax Matters " herein.

Under federal income tax rules currently in effect, gain or loss upo11 sale of the Bonds would bei recognized in part by reference to the Reoffering Yield Accreted Value. S·ee "LEGAL MATTERS -Tax Matters " herein. Tables of Reoffering Yield Accreted Values on February 1 and August 1 for the Bonds appear in APPENDIX D herein.

Bank Qualification

The Bonds are mil "qualified tax-exempt obligations" within the meaning of the Internal Reivenue Code of 1986.

3

Professionals Involved in the Offering

Kelling, Northcross & Nobriga, Inc., Oakland, California , is the District 's financial advisor with respect to the Bonds. Jones Hill Hall & White, A Professional Law Corporation, San Francisco, California, is the District's bond counsel with respect to the Bonds. First Trust of California, National Association , Los Angeles, California, will act as the District 's paying agent, registrar and transfer agent (the "Payin!� Agent") with respect to the Bonds. Kellino, Northcross & Nobriga, Inc. and Jones Hill Hall & White willl receive compensation from the District contingent upon the sale and delivery of the Bonds.

Offering and Delivery of the Bonds

The Bonds will be offered when, as and if issued and received by the Underwriter, subject to approval as to their legality by Bond Counsel. It is anticipated that the Bonds, in book-entry form, wil l be available for delivery through DTC in New Yori<, New York on or about February 6 , 1 997.

Continuing Disclosure

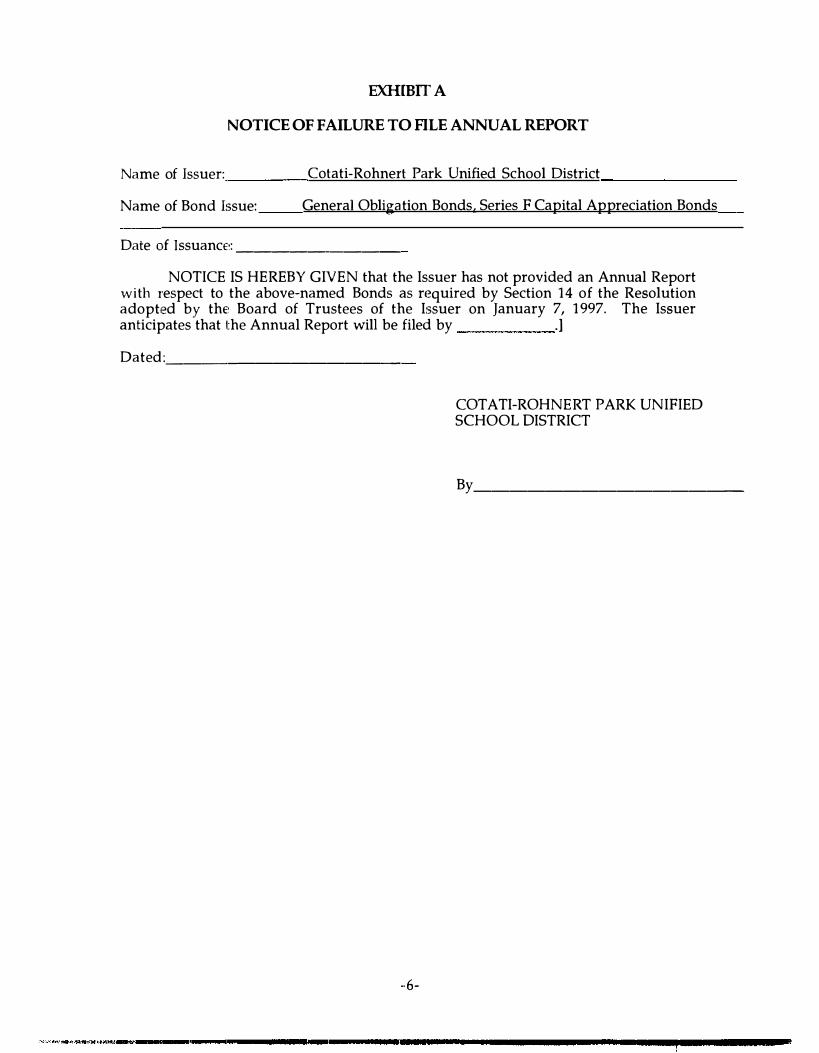

The District has covenanted for the benefit of the holders and beneficial owners of the Bonds to provide certain financial information and operating data relating to the District (the "Annual Report") and to provide notices of the occurrence of certain enumerated events, if material . See " MISCELLANEOUS - Continuing Disclosure" and "APPENDIX C - Form of Continuing Disclosure Certificate"' herein.

Other Information

This Official Statement speaks only as of its date, and the information contained herein is subject to change.

Copies of documents referred to herein and information concerning the Bonds are available from the Business Manager, Cotati-Rohnert Park Unified School District, 1 60 1 East Cotati Avenue, Rohnert Park , California 94928 telephone : (707) 792-47:20. The District may impose a charge for copying, mailing and handling .

No dealer, broker, salesperson or other person has been authorized by the Districts to give any information or to make any representations other than as contained herein and, if given or made, such other information or representations must not be rnlied upon as having been authorized by the District . This Official Statement does not constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sale of the Bonds by a person in any jurisdiction in which it is unlawful for such person to make such an offe1r, solicitation or sale .

This Official Statement is not to be construed as a contract with the purchasers of the Bonds. Statements contained in this Official Statement which involve estimates, forecasts or matters of opinion, wlhether or not expressly so described herein, are intended solely as such and are not to be construed as representations of fact . The summaries and references to documents, statutes and constitutional provisions referred to herein do not purport to be comprehensive or definitive, and are qualified in their entireties by reference to each such document , statute and constitutional provision.

The information set forth herein has been obtained from sources which are believed to be reliable , but is not guaranteed as to accuracy or completeness, and is not to be construed as a representation by thei District . The information and expressions of opinions herein are subject to change witlhout notice and neither delivery of this Official Statement nor any sale made hereunder shall, under any circumstances, create any implication that there has been no change in the affairs of the District since the date hereof. This Official Statement is submitted in connection with the sale of the Bonds referred to herein and may not be reproduced or used, in whole or in part , for any other purpose .

4

_____ , ___________ .. ,..,, ._ , . . , ,

IN CONNECTION WITH THIS OFFERING, THE UNDERWRITER MAY OVERALLOT OR EFFECT TH.L\I\ISACTIONS WHICH STABILIZE OR MAINTAIN THE MARKET PRICE OF THE BONDS AT A LEVEL ABOVE THAT WHICH MIGHT OTHERWISE PREVAIL IN THE OPEN MARKET. SUCH STABILIZING, IF COMMENCED, MAY BE DISCONTINUED AT ANY TIME. THE UNDERWRITER MAY OFFER AND SELL THE BONDS TO CERTAIN DEALERS AND DEALER BANKS AND BANKS ACTING AS AGENT AT PRICES LOWER THAN THE PUBLIC OFFERING PRICE STATED ON THE COVER PAGE HEREOF AND SAID PUEILIC OFFERING PRICE MAY BE CHANGED FROM TIME TO TIME BY THE UNDERWRITER.

END OF INTRODUCTION

5

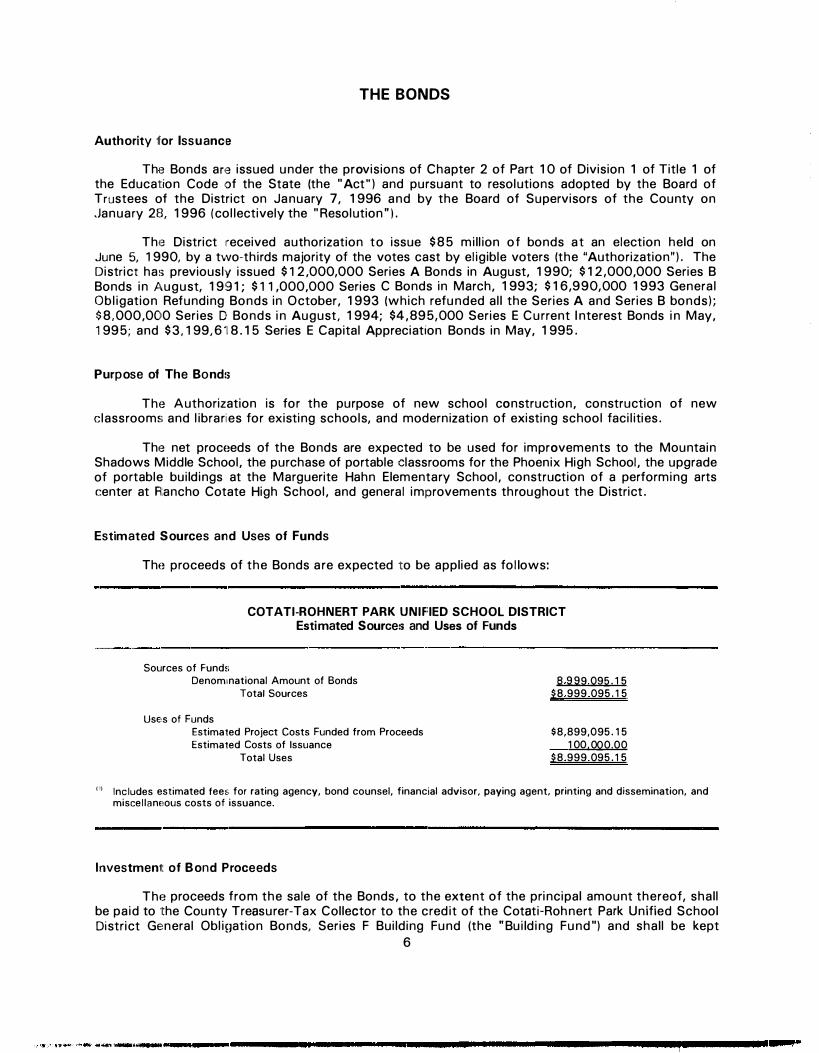

THE BONDS

Authority for lssuanc,e

The Bonds am issued under the provisions of Chapter 2 of Part 1 0 of Division 1 of Title 1 of the Education Code of the State (the "Act") and pursuant to resolutions adopted by the Board of Trustees of the District on January 7, 1 996 and by the Board of Supervisors of the County on .January 2B, 1 996 (collectively the "Resolution").

The District received authorization to issue $85 million of bonds at an election held on June 5, 1 990, by a two-thirds majority of the votes cast by eligible voters (the "Authorization"). The District has previously issued $ 1 2,000,000 Series A Bonds in August, 1 990; $ 1 2,000,000 Series B Bonds in ,t:1,ugust, 1 99 1 ; $ 1 1 ,000,000 Series C Bonds in March, 1 993; $ 1 6,990,000 1 993 General Obligation Refunding Bonds in October, 1 993 (which refunded all the Series A and Series B bonds); $8,000,000 Series D Bonds in August, 1 994; $4,895,000 Series E Current Interest Bonds in May, 1 995; and $3, 1 99,6 '1 8 . 1 5 Series E Capital Appreciation Bonds in May, 1 995 .

Purpose of The Bonds

The Authorization is for the purpose of new school construction, construction of new classrooms and libraries for existing schools, and modernization of existing school facilities .

The net proceeds of the Bonds are expected to be used for improvements to the Mountain Shadows Middle School, the purchase of portable classrooms for the Phoenix High School, the upgrade of portable buildings at the Marguerite Hahn Elementary School, construction of a performing arts center at R:ancho Cotate High School, and general improvements throughout the District .

Estimated Sources and Uses of Funds

Tht� proceeds of the Bonds are expected to be applied as follows:

COTATI-ROHNERT PARK UNIFIED SCHOOL DISTRICT Estimated Sources and Uses of Funds

Sources of Funds

Denommational Amount of Bonds

Total Sources

Use,s of Funds

Estima1ed Project Costs Funded from Proceeds

Estima1ed Costs of Issuance

Total Uses

B 999 095. 1 5 $8 999 095 . 1 5

$8,899,095 . 1 5 1 00,000.00

$8 999 095 . 1 5

Pi Inc ludes estimated fees for rating agency, bond counsel, financial advisor, paying agent, printing and dissemination, and misce l laneous costs of issuance.

Investment of Bond Proceeds

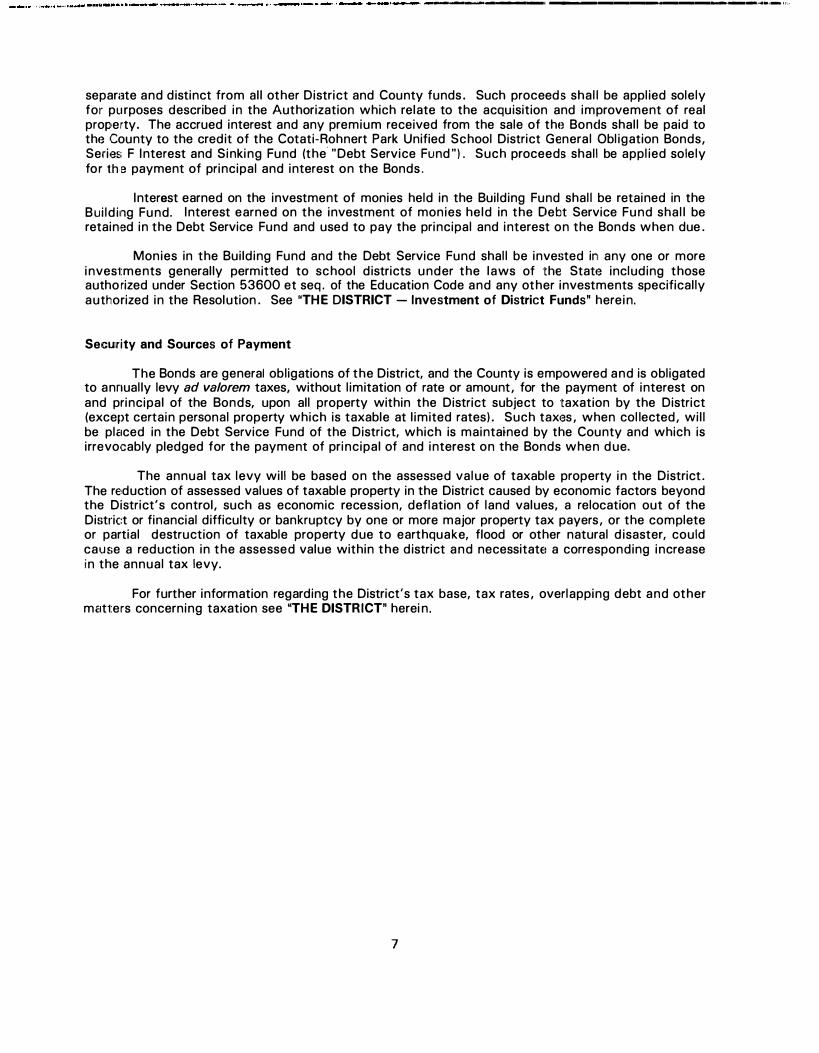

The proceeds from the sale of the Bonds, to the extent of the principal amount thereof, shall be paid to the County Treasurer-Tax Collector to the credit of the Cotati-Rohnert Park Unified School District General Obli{Jation Bonds, Series F Building Fund (the "Building Fund") and shall be kept

6

___ ,. ____ , ___________ -...i•·- 1···

separate and distinct from all other District and County funds. Such proceeds shall be applied solely foir pu rposes described in the Authorization which relate to the acquisition and improvement of real property. The accrued interest and any premium received from the sale of the Bonds shall be paid to the County to the credit of the Cotati-Rohnert Park Unified School District General Obligation Bonds, Series F Interest and Sinking Fund (the· "Debt Service Fund") . Such proceeds shall be applied solely for the payment of principal and interest on the Bonds .

Interest earned on the investment of monies held in the Building Fund shall be retained in the Building Fund. Interest earned on the investment of monies held in the Debt Service Fund shall be retained in the Debt Service Fund and used to pay the principal and interest on the Bonds when due .

Monies in the Building Fund and the Debt Service Fund shall be invested in any one or more investments generally permitted to school districts under the laws of the State including those authorized under Section 53600 et seq . of the Education Code and any other investments specifically authorized in the Resolution . See "THE DISTRICT - Investment of District Funds" herein.

Security and Sources of Payment

The Bonds are general obligations of the District, and the County is empowered and is obligated to annually levy ad valorem taxes, without limitation of rate or amount, for the payment of interest on and principal of the Bonds, upon all property within the District subject to taxation by the District (except certain personal property which is taxable at limited rates) . Such taxes, when collected, will be placed in the Debt Service Fund of the District, which is maintained by the County and which is irrevocably pledged for the payment of principal of and interest on the Bonds when due.

The annual tax levy will be based on the assessed value of taxable property in the District . The reduction of assessed values of taxable property in the District caused by economic factors beyond the District's control, such as economic recession, deflation of land values, a relocation out of the District or financial difficulty or bankruptcy by one or more major property tax payers, or the complete or partial destruction of taxable property due to earthquake, flood or other natural disaster, could cause a reduction in the assessed value within the district and necessitate a corresponding increase in the annual tax levy.

For further information regarding the District's tax base, tax rates, overlapping debt and other matters concerning taxation see "THE DISTRICT" herein.

7

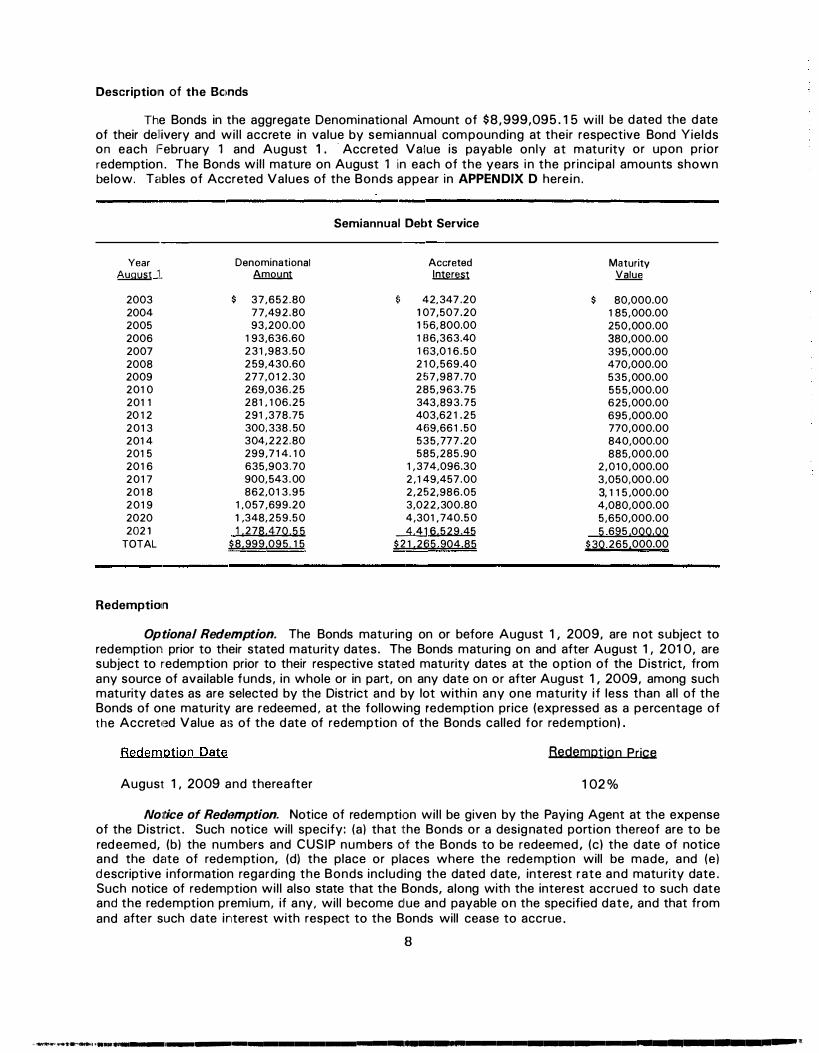

Description of the Bc1nds

The Bonds in the aggregate Denominational Amount of $8, 999,095. 1 5 wil l be dated the date of their dellivery and wi l l accrete in value by semiannual compounding at their respective Bond Yields on each February 1 and August 1 . · Accreted Value is payable only at maturity or upon prior redemption . The Bonds wil l mature on August 1 in each of the years in the principal amounts shown below. Tables of Accreted Values of the Bonds appear in APPENDIX D here in .

Year August l

2003 2004 2005 2006 2007 2008 2009 201 0 201 1 20 1 2 201 3 201 4 201 5 201 6 201 7 201 8 201 9 2020 202 1

TOTAL

Redemptioin

Denominational Amount

$ 37,652.80 77,492 .80 93,200.00

1 93,636.60 231 ,983.50 259,430.60 277,0 1 2 .30 269,036 .25 281 , 1 06 .25 291 ,378.75 300,338 .50 304,222.80 299,7 1 4. 1 0 635,903.70 900,543 .00 862,01 3 .95

1 ,057,699.20 1 ,348,259 .50

1 .278.470.55 $8.999,095 . 1 5

Semiannual Debt Service

Accreted �

�· 42, 347 .20 1 07 ,507 .20 1 !i6, 800.00 1 B6,363.40 H,3,0 1 6 .50 2 1 0,569.40 2 !i7 ,987.70 285,963.75 343,893 .75 403,62 1 .25 469,66 1 .50 535,777 .20 585,285 .90

1 ,374,096.30 2 , 1 49,457.00 2,252,986.05 3,022,300.80 4,301 , 740.50

_Ml 6.529.45 $2 1 .265 904.85

Maturity Value

$ 80,000.00 1 85,000.00 250,000.00 380,000.00 395,000.00 470,000.00 535,000.00 555,000.00 625,000.00 695 ,000.00 770,000.00 840,000.00 885,000.00

2,01 0,000.00 3,050,000.00 3, 1 1 5 ,000.00 4,080,000.00 5,650,000.00 5 695 .000.00

$30 265.000.00

Optional Rediimption. The Bonds maturing on or before August 1 , 2009, are not subject to redemption prior to their stated maturity dates. The Bonds maturing on and after August 1 , 201 0, are subject to redemption prior to their respective stat,ed maturity dates at the option of the District, from any source of available funds, in whole or in part, on any date on or after August 1 , 2009, among such maturity dates as are selected by the District and by lot with in any one maturity i f less than all of the Bonds of one maturity are redeemed , at the following redemption price (expressed as a percentage of the Accret11�d Value as of the date of redemption of the Bonds called for redemption) .

Redemption Price

August 1 , 2009 and thereafter 1 02 %

Notice of Redt1mption. Notice of redemption wil l be given by the Paying Agent at the expense of the District . Such notice will specify: (al that the Bonds or a designated portion thereof are to be redeemed, (bl the numbers and CUSIP numbers of the Bonds to be redeemed, (c) the date of notice and the date of redemption, (d) the place or places where the redemption will be made, and (el descriptive information regarding the Bonds including the dated date, interest rate and maturity date . Such notice of redemption wil l also state that the Bonds, along with the interest accrued to such date and the redemption premium, if any, wil l become dlue and payable on the specified date, and that from and after such date interest with respect to the Bonds will cease to accrue .

8

,·�·-'1"'�1,··----,-------------,---------------..---------1-'l'

_______ , __________ ............ ·-�···· ···

Notice of redemption will be made by registered or otherwise secured mail,. postage prepaid, to (a) the registered owners of the Bonds being redeemed (or, if such owner is a syndicate, to the managing member of such syndicate), (b) a municipal registered securities depository,. and (c) a national information service that disseminates securities redemption notices. Notice of redemption will be at least thirty days, but not more than sixty days, prior to the redemption date. Neither failure to receive such notice nor any defect in the content of such notice will affect the sufficiency of the proceeding for the redemption of the Bonds.

Form, Denomination and Payment

The Bonds will be issued as fully registered bonds, without coupons, and will be in denominations of $5,000 Maturity Value each, or any integral multiple thereof. The Bonds shall bear interest at the rates shown on the cover hereof computed on the basis of a 360-day year of twelve 30-day months. Each bond will accrete in value by semiannual compounding at its respective stated Bond Yield on February 1 and August 1 from the date of delivery, and will be payable in the amount so accreted, as Maturity Value at maturity or Accreted Value upon prior redemption. The difference between the Denominational Amount and Accreted or Maturity Value of a Bond is its Accreted Interest as of the date of such calculation. No separate interest will be paid.

The Bonds, when issued, will be registered initially in the name of Cede & Co. , as nominee of OTC. So long as OTC, or Cede & Co. , as its nominee, is the registered owner of all the Bonds, principal and interest payments on the Bonds will be made directly to OTC, disbursement of such payments to th1:i OTC Participants (defined below) will be the responsibility of OTC, and disbursement of such payments to the Beneficial Owners (defined below) will be the responsibility of the OTC Participants, as more fully described hereinafter. See "THE BONDS - Book-Entry System" and " -- Discontinuation of Book-Entry System; Payment to Beneficial Owners" below.

Bool<··Entry System

The information in this section concerning DTC and DTC 's book-tmtry system has been obtained from sources that the District believes to be reliable, but the District takes no responsibility tor the accuracy thereof. The District cannot and does not give any assurances that DTC, DTC Participants or Indirect Participants will distribute to the Beneficial Owners (t1) payments of interest, pnhcipal or premium, if any, with respect to the Bonds, (b) certificates representing ownership interest in or other confirmation or ownership interest in the Bonds, or (c) redemption or other notices sent to DTC or Cede & Co., its nominee, as the registered owner of the Bonds, or that they will so do on a timely basis or that DTC, DTC Participants or DTC Indirect Participants will act in the manner described in this Official Statement. The current "Rules " applicable to DTC are on file with the Securities and Exchange Commission and the current "Procedures " of DTC to be followf.'d in dealing with DTC Participants are on file with DTC.

DTC will act as securities depository for the Bonds. The Bonds will be issued as fully-registered securities registered initially in the name of Cede & Co. (DTC's partnership nominee). One fullyregistered Bond certificate for each maturity will be issued for the Bonds in the aggregate principal amount of each maturity, and will be deposited with OTC.

DTC is a limited-purpose trust company organized under the New York Banking Law, a "banking organization" within the meaning of the New York Banking Law, a member of the Federal Reserve System, a "clearing corporation" within the meaning of the New York Uniform Commercial Code, and a " dearing agency" registered pursuant to the provisions of Section 17 A of the Securities Exchange Act of 1 934 . OTC holds securities that its participants ( " Participants" ) deposit with OTC. OTC also fac:ilitates the settlement among Participants of securities transactions, such af; transfers and pledges, in de1posited securities through electronic computerized book-entry changes in Participants' accounts, thereby eliminating the need for physical movement of securities certificat,es. Direct Participants inc!ud,e securities brokers and dealers, banks, trust companies, clearing corporntions, and certain other

9

organizations. DTC is owned by a number of i ts Direct Part;cipants and by the New York Stock Exchange, Inc., the American Stock Exchange, Inc., and the National Association of Securities Dealers, Inc. Access to the DTC system is also available to others such as securities brokers and dealers, banks, and trust companies that clear through or maintain a custodial relationship with a Direct Participant , either dirnctly or indirectly ( "Indirect Participants"). The Rules applicable to DTC and its Participants are on fil e with the Securities and Exchange Commission.

Purchases of Bonds under the OTC system must be made by or through Direct Participants, which will receive a credit for the Bonds on DTC's records. The ownership interest of each actual purchaser of each Bond ( "Beneficial Owner") is in turn to be recorded on the Direct and Indirect Participants' records. Beneficial Owners wil l not receive written confirmation from OTC of their purchase, but Beneficial Owners are expected to receive written confirmations providing details of the transaction, as wel l as periodic statements of their holdings, from the Direct or Indirect Participant through which the Beneficial Owner entered into the transaction. Transfers of ownership interests in the Bonds are to be accomplished by entries made on the books of Participants acting on behalf of Beneficial Owners. Beneficial Owners will not receive certificates representing their ownership interests in Bonds , except in the event that use of the book-entry system for the Bonds is discontinued.

To facilitate subsequent transfers, all Bonds deposited by Participants with OTC are registered in the name of DTC 's partnership nominee, Cede & Co. The deposit of Bonds with OTC and their registration in the name of Cede & Co . effect no change in beneficial ownership. OTC has no knowledge of the actual Beneficial Owners of the Bonds; DTC's records reflect only the identity of the Direct Participants to whose accounts such Bonds are credited, which may or may not be the Beneficial Owners. The Participants will remain responsible for keeping account of their holdings on behalf of their customers.

Conveyance of notices and other communications by OTC to Direct Participants, by Direct Participants to Indirect Participants, and by Direct Participants and Indirect Participants to Beneficial Owners wii l l be goveirned by arrangements among them, subject to any statutory or regulatory requirements as may be in effect from time to time.

Redemption notices shall be sent to Cede & Co. If less than all of the Bonds within an issue are being redeemed, IDTC' s practice is to determine by lot the amount of the interest of each Direct Participant in such issue to be redeemed.

Neither DTC nor Cede & Co. wil l consent or vote with respect to Bonds . Under its usual procedures , DTC mails an Omnibus Proxy to the District as soon as possible after the record date. The Omnibus Proxy assigns Cede & Co.'s consenting or voting rights to those Direct Participants to whose accounts the Bonds are credited on the record date (identified in a listing attached to the Omnibus Proxy) .

Principal and interest payments on the Bonds will be made to DTC. DTC's practice is to credit Direct Participants' accounts on a payable date in accordance with their respective holdings shown on DTC ' s records unless OTC has reason to believe that it wil l not receive payment on a payable date. Payments by Participants to Beneficial Owners will be governed by standing instructions and customary practices, as is the case with securities held for the accounts of customers in bearer form or registered in "street name, " and will be the responsibility of such Participant and not of OTC, the Paying Agent, the District or the County, subject to any statutory or n�gulatory requirements as may be in effect from time to time. Paymen1t of principal and interest to DTC is the responsibi lity of the County or the Paying Agent, disbursement ,of such payments to Direct Participants shall be the responsibility of OTC, and disbursement of such payments to the Beneficial Owners shall be the responsibi l ity of Direct and Indirect Participants.

OTC may discontinue providing its services as securities depository with respect to the Bonds at any time by giving reasonable notice to the County or the Paying Agent, or the District may decide to discontinue use of the system of book-entry transfers through OTC. Under such circumstances, in

1 0

, _a.0c->••••"-••---------·--------------------------lml!II-----I-"

the event that a successor securities depository is not obtained, Bond certificates are requ ired to be printeid and delivered .

Disc:ontinuation of Book-Entry System; Payment to Beneficial Owners

In the event that the book-entry system described above is no longer used with respect to the Bonds, the fol lowing provisions wil l govern the payment, reg istration, transfer, exchange and replacement of the Bonds.

The principal of the Bonds and any premium upon the redemption thereof pr ior to the maturity wi l l be payable in lawful money of the United States of America upon presentation and surrender of the Bonds at the principal corporate trust office of the Paying Agent. I nterest on the Bonds wil l be paid by th,e Paying Agent by check mailed to the person whose name appears on the reg istration books of the Paying Agent as the registered owner, and to that person's address appeari ng on the registration books as of the close of business on the 1 5th day of the month next preceding an I nterest Payment Date . At the option of the registered owner of at least $ 1 ,000,000 in aggregate principal amount, upon written request given at least three days prior to the applicable I nterest Payment Date, interest wii l l be tra nsmitted by wire transfer to an account designated by such owner.

Any Bond may be exchanged for Bonds of any authorized denomination upon presentation and su rrender at the principal corporate trust office of the Paying Agent, in Los Angeles, California, together wii th a request for exchange signed by the registered owner or by a person l egal ly empowered to do so in a form satisfactory to the Paying Agent. A Bond may be transferred only on the Bond registration books upon presentation and surrender of the Bond at the principal corporate trust office of the Paying A1Jent together with an assignment executed by the registered owner or by a person legal ly empowered to do so in a form satisfactory to the Paying Agent . Upon exchange or transfer, the Paying Agent shal l complete , authenticate and deliver a new Bond or Bonds of any authorized denomination or de1norninations requested by the registered owner or by a person legally empowered to do so , equal in the aggregate to the unmatured principal amount of the Bond surrendered and bearing interest at the same rate and maturing on the same date.

Neither the District, the County nor the Paying Agent wil l be requi red to exchange or transfer any Bond during the period from the sixteenth day of the month next preceding any I nterest Payment Dat,e or date of redemption and ending with the close of business on that Interest Payment Date or dato of redemption.

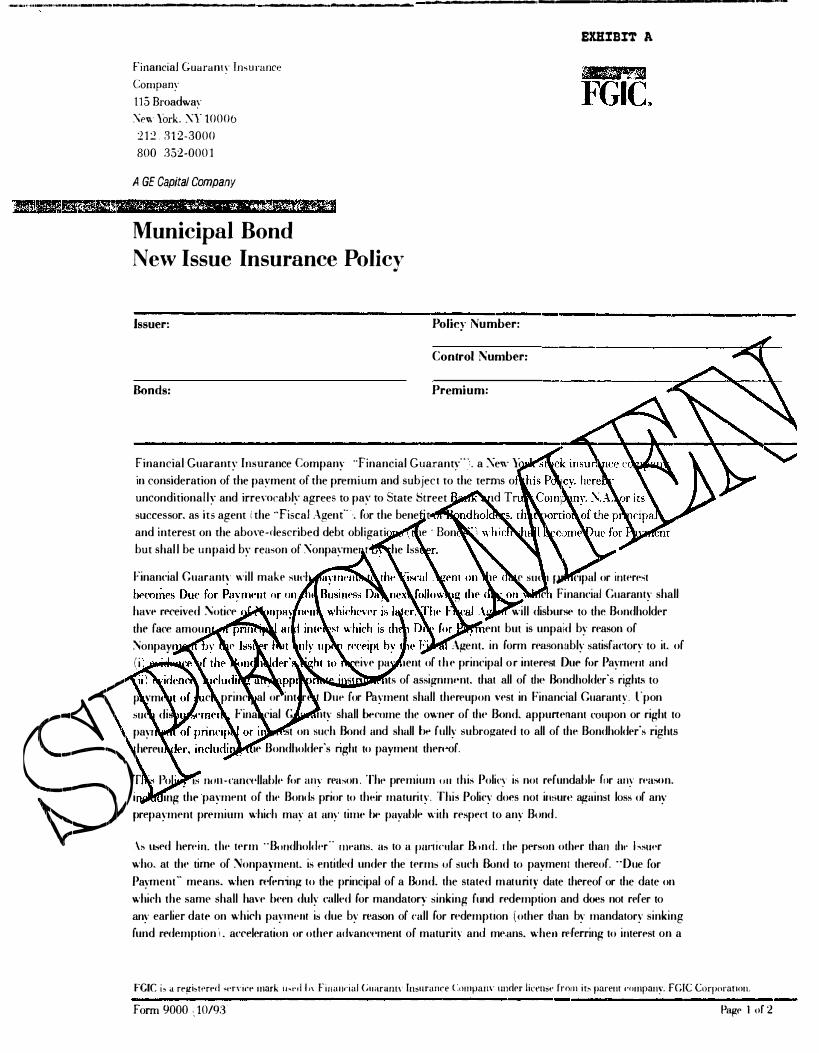

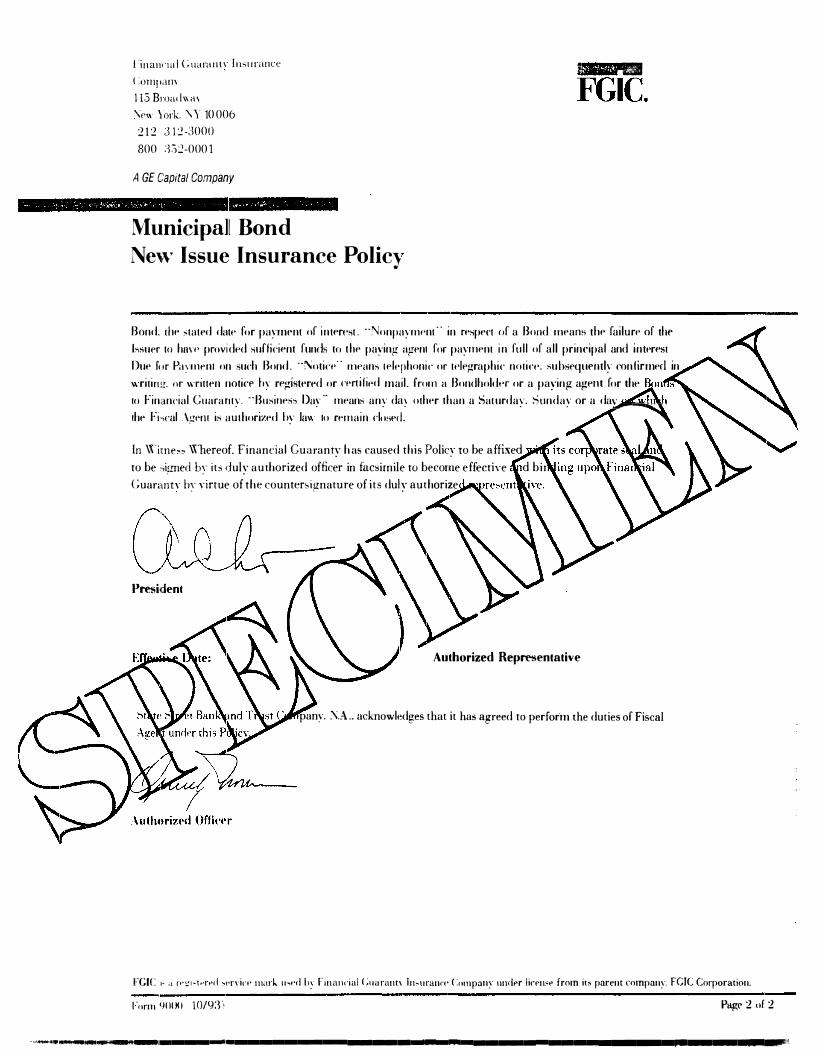

BOND INSURANCE

The following information has been furnished by Financial Guaranty Insurance Company for use in this Official Statement. The District takes no responsibility for the accuracy thereof. Reference is m.flde to APPENDIX F for a specimen of their Municipal .Bond New Issue Insurance Policy.

Concurrently with the issuance of the Bonds, Financial Guaranty I nsurance Company, doing busiiness in Cal ifornia as FG IC Insurance Company ("Financial Guaranty" ) , wil l issue its Mun icipal Bond N1�w Issue I nsurance Pol icy for the Bonds (the "Policy"} . The Policy unconditionally guarantees the payment of that portion of the pri ncipal (or accreted value in the case of capital appreciation bonds) of and i nterest on the Bonds which has become due for payment, but shall be unpaid by reason of nonpayment by the District. Financial Guaranty wi l l make such payments to State Street Bank and Trust Company, N .A. , or its successor as its agent (the "Fiscal Agent"} , on the later of the date on which such principal (or accreted value in the case of capital appreciation bonds} and i nterest is due or on the business day next following the day on which Financial Guaranty shal l have received tele1Phonic or telegraphic notice, subsequently confirmed in writ ing, or written notice by registered or certified mai l , from an owner of Bonds or the Paying Agent of the nonpayment of such amount by the District. The Fiscal Agent wil l disburse such amount due on any Bond to its owner upon receipt by the

1 1

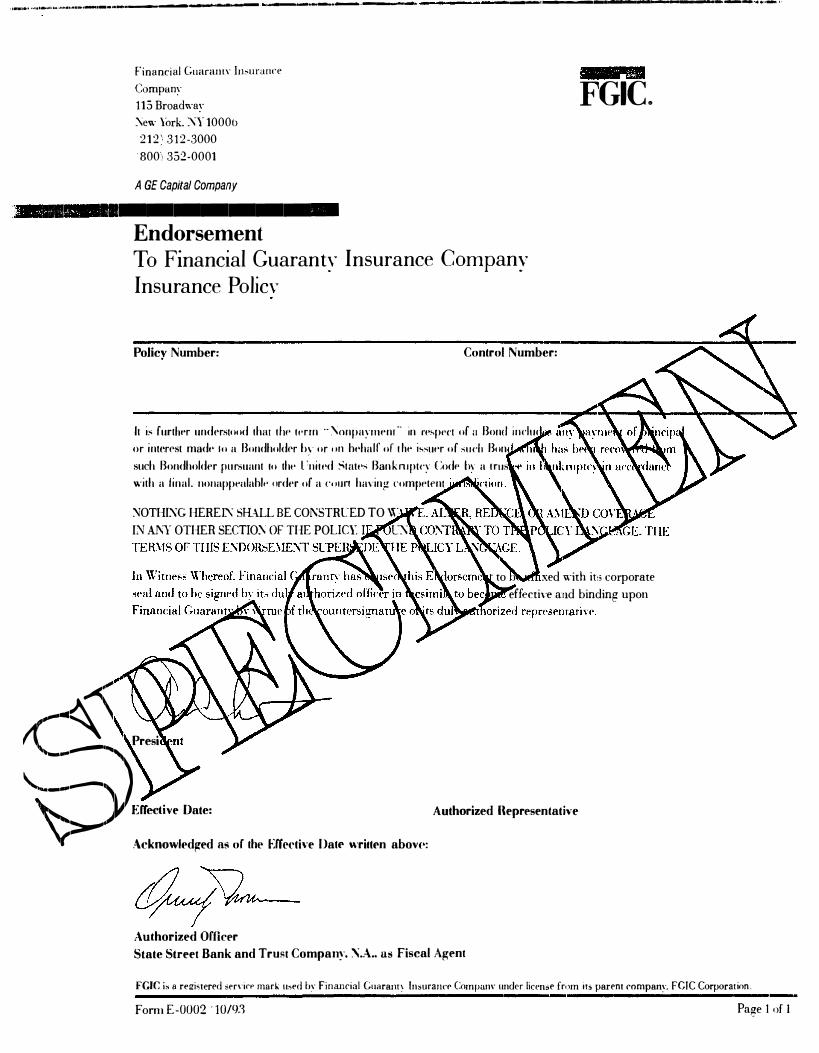

Fiscal Agent of evidence satisfactory to the Fiscal Agent of the owner's right to receive payment of the principal (or accreted value in the case of capital appreciation bonds) and interest due for payment and evidence, including any appropriate instruments of assignment, that all of such owner's rights to payment o'f such princ:ipal (or accreted value in the case of capital appreciation bonds) and interest shall be vested in Financial Guaranty . The term "nonpayment" in respect of a Bond includes any payment of principal (or accreted value in the case of capital appreciation bonds) or interest made to an owner of a Bond which has been recovered from such owner pursuant to the United States Bankruptcy Code by a trustee in bankruptcy in accordance with a final, nonappealable order of a court having competent jurisdiction .

The Policy is non-cancelable and the premium will be fully paid at the time of delivery of the Bonds. The Policy covers failure to pay principal (or the accreted value in the case of capital appreciation bonds) 01f the Bonds on their respective stated maturity dates, or dates on which the same shall have been duly called for mandatory sinking fund redemption, and not on any other date on which the Bonds may have been accelerated, and covers the failure to pay an installment of interest on the stated date for its payment.

This Official Statement contains a section regarding the ratings assigned to the Bonds and reference should be made to such section for a discussion of such ratings and the basis for their assignment to the Bonds. Reference should be made to the description of the District for a discussion of the ratings, if any, assigned to such entity's outstanding parity debt that is not secured by credit enhancement .

Thi� Policy is not covered by the Property/Casualty Insurance Security Fund specified in Article 76 of the New York Insurance Law.

Financial Guaranty is a wholly-owned subsidiary of FGIC Corporation (the "Corporation"), a Delaware holding company. The Corporation is a subsidiary of General Electric Capital Corporation ("GE Capital"). Neither the Corporation nor GE Capital is obligated to pay the debts of or the claims against Financial Guaranty. Financial Guaranty is a monol1ine financial guaranty insurer domiciled in the State of New York and subject to regulation by the State of New York Insurance Department. As of September 30, 1 9916, the total capital and surplus of Financial Guaranty was approximately $ 1 ,097 ,600, 1 90. Financial Guaranty prepares financial statements on the basis of both statutory accountin�11 principles and generally accepted accounting principles. Copies of such financial statements may be obtained by writing to Financial Guaranty at 1 1 5 Broadway, New York, New York 1 0006, Attention: Communications Department (telephone number: (21 2) 3 1 2-3000) or to the New York State Insurance Department at 1 60 West Broadway, 1 8th Floor, New York, New York 1 00 1 3, Attention: Financial Condition Property/Casualty Bureau (telephone number (21 2) 602-0389) .

CONSTITUTIONAL AND .STATUTORY PROVISIONS

AFFECTING DISTRICT REVENUES AND APPROPRIATIONS

Principal of and interest on the Bonds are payable from the proceeds of an ad valorem tax required to be levied by the Board of Supervisors of the County for the payment thereof. (See 'THE BONDS - Security a.nd Sources of Payment 11 herein.) Articles XII/A and X/1/B of the Constitution, Propositions 62, 98, 1 1 1, 187, and 2 18 and certain other provisions of law discussed below, are included in this section to describe the potential effect of these Constitutional and statutory measures on the ability of the District to levy taxes and spend tax proceeds for operating and other purposes, and it should not be inferred from the inclusion of such materials that these laws impose any limitation on the ability of the District to levy taxes for payment of the Bonds. The tax levied by the County for payment of the Bonds was approved by the District's voters in compliance with the California Constitution and all applicable laws.

·1 2

,,.........,,,i.,.-,4 ............. .-0IHF l ___ l __ i ___________ , _________________ 1111111 ________ �,

Articlle XIIIA

Article XIIIA of the Constitution of the State of California (the "State") limits the amount of ad vc1/orem taxes on real property to 1 % of "full cash value" as determined by the county assessor. Article XIIIA defines "full cash value" fo mean "the county assessor's valuation of real property as shown on the 1 975/76 tax bill under ' full cash value' or, thereafter, the appraised value of real propeirty when purchased, newly constructed, or a change in ownership has occurred after the 1 97 5 assessment, " subject to exemptions in certain circumstances of property transfer o r reconstruction. The "full cash value" is subject to annual adjustment to reflect increases, not to exceed 2% for any ye,ar, or decreases in the consumer price index or comparable local data, or to reflect reductions in propeirty value caused by damage, destruction or other factors.

Article XIIIA requires a vote of two-thirds of those voting in an election in a city, county, special district or other public agency to impose special taxes, and except for ad vaJ'orem taxes described in the next sentence, prohibits the imposition of any additional ad valorem, sales or transaction taxes on real property. Article XIIIA exempts from the 1 % tax limitation any taxes above that level required to pay debt service (a) on any indebtedness approved by the voters prior to July 1 , 1 978, and (bl as the result of an amendment approved by State voters on June 3, 1 986, on ariy bonded indebtedness approved by two-thirds of the votes cast by the voters for the acquisition or improvement of real property on or after July 1 , 1 978. In addition, Article XIIIA requires the approval of two-thirds of all members of the State Legislature to change any State taxes for the purpose of increasing tax revenues, while prohibiting the imposition by the State Legislature of any new ad va/or,<Jm, sales or transaction taxe1s on real property.

Legislation Implementing Article XIIIA

Legislation has been enacted and amended a number of times since 1 978 to implement Article XWA. Under current law, local agencies are no longer permitted to levy directly any property tax (except to pay voter-approved indebtedness) . The 1 % property tax is automatically levied by the county and distributed according to a formula among taxing agencies. The formula apportions the tax roughly in proportion to the relative shares of taxes levied prior to 1 989.

That portion of annual property tax revenues generated by increases in assessed valuations within each tax rate area within a county, subject to redevelopment agencv, if any, claims on tax increment and subject to changes in organization, if any, of affected jurisdictions, is allocated to each jurisdiction within the tax rate area in the same proportion that the total property tax revenue from the ta>e rate area for the prior year was allocated to such jurisdictions.

Beginning in the 1 98 1 /82 fiscal year, assessors in the State no longer record property values on tax rolls at the assessed value of 25 % of market value. All taxable property is now shown at "full cas:h value" on the tax rolls. The tax rate is expressed as $ 1 per $ 1 00 of taxable value.

Unitary Property

AB 454 (Chapter 921 , Statutes of 1 9871 provides that revenues de1rived from most utility property assessed by the State Board of Equalization ( "Unitary Property" ) , commencing with the 1 988/89 fiscal year, are allocated as follows: (a) each jurisdiction will receive up to 1 02% of its prior year State-assessed revenue; and (bl if county-wide revenues generated from Unitary Property are less than the previous year 's revenues or greater than 1 02% of the previous year 's revenues, each jurisdiction will share the burden of the shortfall or the benefit of the excess revenues by a specified formula . This provision applies to all Unitary Property except railroads, whose valuation will continue to be allocated to individual tax rate areas.

The provisions of AB 454 do not constitute an elimination of the asnessment of any Stateasse:ssed properties nor a revision of the methods of assessing utilities by the State Board of

1 3

Equal ization . Generally, AB 454 allows valuation growth or decl ine of Un itary Property to be shared by al l jurisd ictions in a county.

Several major State-assessed util ities have challenged the legal ity of property valuation theories and the val ues assessed by the State Board of Equalization, which administers the assessment of publ ic util ities for property taxation purposes. The chal lenge was precipitated by the superior court decision i n A T& T Communications of California, et al. v. State Board of Equalization in which the valuation method used by the State Board of Equal ization to value unitary util ity property was declared il legal and a new method of va luation was imposed , result ing in significantly lower property taxes . Several counties and util ity companies whose unitary property valuations could be affected by the principles announced in the superior court decision signed a settlement agreement i n 1 993. The agreement ' s effective ness, however, is dependent on the fulfi l lment of certai n conditions. If effective, this settlement would have only prospective fiscal impact on uti l ity assessments, which would be phased down gradual ly over the next several years .

Proposition 62

A statutory initiative ("Proposition 62") was adopted by the voters at the November 4, 1 986, general elei:::tion, which requires voter approval for new or higher taxes by local government entities.

The District does not receive tax revemue from any measure adopted in violation of Proposition 62.

Article XI I IB

Article XI I IB oi: the State Constitution, as subsequently amended by Propositions 98 and 1 1 1 , l im its the an nual appropriations of the State and of any city, county, school d istrict, authority or other political subdivision of the State, to the level of appropriations of the particular governmental entity for the prior fiscal year, a:s adjusted for changes in the cost of living and in population, for transfers in the f inancia l responsibi l ity for provid ing services, and for certa in declared emergencies. As amended, Article X l l l ll3 defi nes:

(a l "chan1;1e i n the cost of l iving" with respect to school d istricts to mean the percentage change in California per-capita i ncome from the preced ing year, and

(bl "chan1Je in population" with respect to a school d istrict to mean the percentage change in the average daily attendance of the school d istrict from the preceding fiscal year.

For fiscal yearn beginn ing on or after July 1 , 1 990, the appropriations l imit of each entity of government shall be the appropriations l imit for the 1 986/87 fiscal year adjusted for the changes made from that fiscal year pursuant to the provisions of Article XI I IB, as amended .

The appropriations of an entity of local government subject to Article X I I IB l im itations i nclude the proceeds of taxes levied by or for that entity and the proceeds of certain State subventions to that entity . " Proceeds of taxes" include, but a re not Hmited to , all tax revenues and the proceeds to the entity from (a) regulatory licenses, user charges and user fees ( but only to the extent that these proceeds exceed the reasonable costs in provid ing the regulation, product or service) , and (bl the investment of tax revenues.

Appropriations subject to l imitation do not i nclude (a) refunds of taxes, (b) appropriations for debt servic,e, (c) appropriations required to comply with certa in mandates of the courts or the federal government, (d) appropriations of certain special d istricts, (el appropriations for al l qual ified capital outlay projects as defined by the leg islature, (f) appropriations derived from certain fuel and vehicle taxes and {g) appropriations derived from certa i n taxes on tobacco products .

1 4

���* ........... ...., ......... 11 .............................................................................................. 1�·

........ _,, .. , ................... ----------------------.. --------,----------� ............ , ... ....

Article XIIIB includes a requirement that all revenues received by an entity o:f government other than the State in a fiscal year and in the fiscal year immediately following it in excess of the amount piermitted to be appropriated during that fiscal year and the fiscal year immodiately following it shall b1e re,turned by a revision of tax rates or fee schedules within the next two subsequent fiscal years. If a1 school district receives any proceeds of taxes in excess of its appropriations limit, it may, by resolution of the school district 's governing board, increase its appropriations limit to equal that amount, provided that the State has sufficient excess appropriations limit in that fiscal year.

Article XIIIB also includes a requirement that fifty percent of all revenues received by the State in a fiscal year and in the fiscal year immediately following it in excess of the amount permitted to be appropriated during that fiscal year and the fiscal year immediately following it shal l be transferred and al located to the State School Fund pursuant to Section 8.5 of Article XVI 01f the State Constitution. See '"Pro positions 98 and 1 1 1 " below.

Propositions 98 and 1 1 1

On November 8, 1 988 the voters approved Proposition 98, an initiative constitutional amendment and statute called "The Classroom Instructional Improvement and Accountability Act" ("Proposition 98" ) . In addition to adding certain provisions to the Education Code, Proposition 98 also ameinded Article XIIIB and Section 8 of Article XVI of the State Constitution and added Section 8.5 of Article XVI to the State Constitution, the effects of which are to establish a minimum level of State funding for school districts, to al locate to school districts, within limits, State revenues in excess of th1e State's appropriations limit and to exempt such excess funds from school district appropriations limits ..

On June 5, 1 990, the voters approved Proposition 1 1 1 (Senate Constitutional Amendment No. 1 ) cal led the "Traffic Congestion Relief and Spending Limit Act of 1 990" ("Proposition 1 1 1 ") which furthe,r modified Article XIIIB and Sections 8 and 8.5 of Article XVI of the State Constitution with respect to appropriations limitations and school funding priority and allocation .

Article XIIIB, as amended by both Proposition 98 and Proposition 1 1 1 , hs discussed above under "Article XIIIB ."

The provisions of Sections 8 and 8 .5 of Article XVI, as added 1to and/or amended by Propositions 98 and 1 1 1 , may be summarized as follows :

a) State Funding of Schools !Section 8). Monies to be applied by the State for the support of school districts must be at a level equal to the greater of the following "tests" :

( i ) The amount which, as a percentage of the State general fund ("General Fund") revenues which may be appropriated pursuant to Article Xl 11IB, equals the percentage of General Fund revenues appropriated for school districts in fiscal year 1 986/87;

(ii) The amount actually appropriated to school districts in the prior fiscal year from General Fund proceeds and from allocated local proceeds of taxes (excluding any excess state revenues allocated pursuant to Section 8.5) , adjusted for changes in enrollment and for the change in the cost of living (operative only in a fiscal year in which the percentage growth in California per capita personal income is less than or equal to the percentage growth in per capita General Fund revenues plus one-half of one percent) ;

(iii) The amount actually appropriated to school districts in the prior fiscal year from General Fund proceeds and from allocated local proceeds 01' taxes (excluding any excess State revenues allocated pursuant to Section 8 .5) adjusted for changes in enrol lment and for the change in per capita General Fund revenues, and, in addition,

1 5

an am ount equal to one-half of one percent times the prior year appropriations (excluding any excess State revenues) adjusted for changes in enrollment (operative only in a fiscal year in which the percentage growth in California per capita personal income is greater than the percentage growth in per capita General Fund revenues plus one-half of one percenti.

If the third test is used in any year the difference between the third test and the second test will become a "credit" to schools which will be paid in future years when the General Fund revenue growth exceeds personal income growth.

The State legislature by a two-thirds vote of both houses, with the Governor 's concu1rrence, may suspend for one year the minimum funding provisions for school districts as provided for in Section 8.

b) Allocations to the State School Fund (Section 8.5l. In addition to the amounts applied to school districts under the tests discussed above, the State Controller is directed to allocate available excess State revenues (pursuant to Article XIIIB) to the State School Fund. However, no such allocation is required at any time that the Director of Finance and the Superintendent of Public Instruction mutually determine that current annual expenditures per student equal or exceed the average annual expenditures per student of the 1 0 states with the highest annual expenditures per student and the average class size equals or is less than the average class size of the 1 0 states with the lowest class �.ize.

Such allocations do not constitute appropriations subject to Article XIIIB limitations and are to be made in an equal amount per enrollment.

Proposition 1 87

At the November 1 994 general election, State voters approved Proposition 1 87. Proposition 1 87 makes persons with foreign citizenship who have entered the State illegally ineligible for public social serviices, public health care services (unless an emergency) , and public school educat ion at elementary, secondary , and post-secondary levels. Further, Proposition 1 87 requires every school district to verify the status of every child enrolling for the first time on or after January 1 , 1 995. By January 1 , 1 996, evi,Hy school district is required to have verified the legal status of every student enrolled in the school district as well as the legal status of the student's parents or guardian. If any student, parent, or guardian is not legally in the United States, the school district must report the student to the United States Immigration and Naturalization Service ("INS") and certain other parties. Proposition 1 87 also prohibits a school district from providing education to a student it does not verify as either a United States citizen or a person legally admitted to the U nited States.

Opponents of Proposition 1 87 have filed at least eight lawsuits challenging the constitutionality and validity of the measure. On November 2, 1 995, a United States District Court judge struck down the central provisions of Proposition 1 87 by ruling that parts of Proposition 1 87 conflict with federal power over immigrat ion. The ruling concluded that states may not enact their own schemes to "regulate immigration or devise immigration regulations which run parallel or purport to supplement federal immigration law. " As a consequence of the ruling, students may not be denied public education and may not be asked about their immigration status when enrolling in public schools . Further, the ruling stru c:k down the requirements of Proposition 1 87 that teachers and district employees report information on the immigrant status of students, parents, and guardians. An appeal has been filed. It cannot be predicted what the nature or outcome of such appeal will be or the ultimate fiscal impact of Proposition 1 87.

If ultimately upheld, Proposition 1 87 could have a significant impact on funding for California school districts. For every student that the District excludes under Proposition 1 87 and for every student who does not attend school in the District as a result of Proposit ion 1 87, the District may lose

1 6

.,.,�.ii;-··j�---li----·------------.. ----------------.------1

�•'*'••••• , i••-•*'1• .. ··� ..... , ..... m....,.•-•••_..•_..,._ ______ ·---- -------·----------.......................

a portion of the State revenue it receives based on average daily attendance. lin addition, to the extent that the exclusion of students and the verification and reporting requirements are found to be at odds with various federal laws, the District may lose all or a portion of any federal revenue it receives. Furtlher, the cost of compliance with the verification and reporting requirements may prove significant .

Prop1osition 2 1 8

Under the California Constitution, the power of initiative is reserved to the voters for the purpose of enacting statutes and constitutional amendments. Over the past 113 years, the voters have exierc:ised this power through the adoption of Proposition 13 and similar measures, the most recent of which was approved as Proposition 218 in the general election held on November 5, 1996.

On November 5, 1996, California voters approved Proposition 218 -- Voter Approval for Local Government Taxes - Limitation on Fees, Assessments, and Charges - Initiative Constitutional Ameindment . Proposition 218 added articles XIIIC and XIIID to the California Constitution, imposing certain vote requirements and other limitations on the imposition of new or increased taxes, assessments and property-related fees and charges. Proposition 218 states that all taxes imposed by loc:al governments shall be deemed to be either general taxes or special taxes. Special purpose districts, including school districts, have no power to levy general taxes. No local government may impose, extend or increase any general tax unless and until such tax is submitted to the electorate and approved by a majority vote. No local government may impose, extend or increase any special tax unless and until such tax is submitted to the electorate and approved by a two-thirds vote.

Proposition 218 also provides that no tax, assessment, fee or charge slhall be assessed by any ag1ency upon any parcel of property or upon any person as an incident of property ownership except: ( i ) the ad valorem property tax imposed pursuant to Article XIII and Articlo XIIA of the California Constitution, ( ii) any special tax receiving a two-thirds vote pursuant to the California Constitution, and ( ii i ) assessments, fees and charges for property related services as provided in Proposition 218. Proposition 218 then goes on to add voter requirements for assessments and fees and charges imposed as an incident of property ownership, other than fees and charges for sewer, water, and refuse collection services. In addition, all assessments ad fees and charges imposed a:; an incident of property ownership, including sewer, water, and refuse collection services, are subjected to various additional procedures, such as hearings and stricter and more individualized benefit requirements and findings. The effect of such new provisions will presumably be to increase the difficulty a local agency will have in imposing, increasing or extending such assessments, fees and charges .

Proposition 218 also provides that the initiative power shall not be prohibited or otherwise limited in matters of reducing or repealing any local tax, assessment, fee or charge. This provision is not limited to taxes imposed on or after November 6, 1996, the effective date of Proposition 218, and could result in retroactive repeal or reduction in any existing taxes, assessments, fees and charges, subj(wt to overriding federal constitutional principles relating to the impairments of contracts.

Like its antecedents, Proposition 218 is likely to undergo both judicial and legislative scrutiny beforn its impact on the District and its obligations can be determined. Certain provisions of Proposition 218 may be examined by the courts for their constitutionality under both State and federal constitutional law. The District is not able to predict the outcome of any suc:h examination.

The foregoing discussion of Proposition 218 should not be considered an exhaustive or authoritative treatment of the issues. The District does not expect to be in a position to control the consideration or disposition of these issues and cannot predict the timing or outcome of any judicial or legislative activity in this regard. Interim rulings, final decisions, legislative proposals and legislative enactments may all affect the impact of Proposition 218 on the Bonds as wull as the market for the Bonds. Legislative and court calendar delays and other factors may prolong any uncertainty regarding the offects of Proposition 218.

1 7

Applications of Constitutional and Statutory Provisions

The appl i cation of Proposition 98 and other statutory regu lations has become increasingly d ifficult to predict accurately in recent years . For a d iscussion of how these provisions of Proposition 98 have been applied to school funding see "GENERAL SCHOOL DISTRICT FINANCIAL INFORMATION" herein.

Future lniti1atives

Article X I I IA, Article XI I IB, Proposition 62, Proposition 98, Proposition 1 1 1 , Proposition 1 87 and Proposition 2 1 8 were each adopted as measures that qual ified for the bal lot pursuant to the State's i n itiative process . Frnm time to t ime other in itiative measures could be adopted, further affecting District revenues or the District 's abil ity to expend revenues. The nature and impact of these measures cannot be anticipated by the District .

GENERAL SCHOOL DISTRICT FINANCIAL INFORMATION

Tht:! information in this section concerning the state funding of public education is provided to supplement information regarding the District's finances discussed elsewhere in this Official Statement, and it should not be inferred from the inclusion of this information in this Official Statement that the principal ol or interest on the Bonds is payable from State revenues. The Bonds are payable from the proceeds of an ad valorem tax required to be levied by the County Board of Supervisors in an amount sufficient to make such payments.

State Funding of Edu,cation

As a whole, State school districts receive a significant portion of their funding from State appropriations. As a result, decreases in State revenues can significantly affect appropri ations made by the legislature to school districts.

Aninual State apportionments of basic and equal ization aid to school d istricts for general pu rposes are computed up to a revenue l imit per unit of average dai ly attendance (the "A.D .A . " ) . Generally, these appoirtionments amount to the d i-fference between the school district 's revenue l imit and its property tax al location. The revenue l imit calculations are adjusted annually in accordance with a number of factors designed primari ly to provide cost of l iving increases and to equal ize revenues among all State school d istricts of the same type . SHe "THE DISTRICT - Average Daily Attendance and Revenue Limit" here in .

State Budget