fast moving consumer goods industryxa.yimg.com/kq/groups/22151721/1625926202/name/fm… · ·...

TRANSCRIPT

FAST MOVING CONSUMER GOODS

INDUSTRY

ISSUE 1H 2010

ISI Analytics – the Business research arm of ISI Emerging Markets

A Euromoney Institutional Investor Company www.securities.com

India In

dustry

Research

ISI A

nalytic

s

1. Industry Profile 1

1.1 Industry Overview 1.2 General Economic Environment 1.3 India’s FMCG Industry Overview 1.3.1 Food Inflation 1.3.2 Food and Beverages Industry 1.3.3 Household Care 1.3.4 Personal Care

2. Market Trends and Outlook 2.1 Union Budget 2010-11 2.2 e-Choupal 2.3 Growth in Rural Market 2.4 Regulatory Issues 2.4.1 National Food Processing Policy 2.4.2 FDI Policy in Retail Trading (Single Brand) 2.4.3 Government Policies and Initiatives

11

3. Leading Players and Comparative Matrix 3.1 Leading Players 3.1.1 Hindustan Unilever Ltd (HUL) 3.1.2 Nirma Ltd 3.1.3 Dabur India Ltd (DIL) 3.1.4 Colgate-Palmolive India Ltd (CPIL) 3.1.5 Godrej Consumer Products Ltd (GCPL) 3.2 Comparative Matrix 3.3 SWOT Analysis

19

Notes: 1 RMB = INR 6.5539 1 NZD = INR 31.5560 1 USD = INR 44.7415 1 lakhs = 100,000 units 1 crores (cr) = 10,000,000 units

FMCG

ISI Analytics

FMCG india

1. Industry Profile

1.1 Industry Overview Fast Moving Consumer Goods (FMCG) - alternatively known as consumer packaged goods (CPG) are products that are sold quickly and generally consumed at a regular basis, as opposed to durable goods such as kitchen appliances that are replaced over a period of years. The FMCG industry primarily engages in the production, distribution and marketing operations of CPG. FMCG product categories comprise of food and dairy products, pharmaceuticals, consumer electronics, packaged food products, household products, drinks and others. Meanwhile, some common FMCG include coffee, tea, detergents, tobacco and cigarettes, soaps and others. The big names in this sector include Sara Lee, Nestle, Reckitt Benckiser, Unilever, Procter & Gamble, Coca-Cola, Carlsberg, Kleenex, General Mills, Pepsi, Mars and others. FMCG in Vietnam urban area grew 19% in 2008 as a result of the rising number of young and sophisticated consumers.

Approximately 50% of consumers in Vietnam are under the age of 30 and this figure is projected to increase to 70mn by 2018. In addition, the number of high income earners (from USD500 per month) has trebled over the past six years while the number of low income earners (under USD250 per month) decreased from 62% in 1999 to 9% in 2008 in major cities such as Hanoi and Ho Chi Minh City. In China, statistics compiled by the China Chain Store and Franchise Association showed that 100 major FMCG firms reaped sales income of RMB530bn in 2006 after sound growth of 20% over figures obtained in the previous year. Sixteen out of the 100 examined firms are foreign-funded firms that garnered RMB168.8bn in sales volume. Improved efficiency also contributed significantly to average sales growth of 27% yoy. Meanwhile, the remaining 84 domestic firms reaped RMB360.8bn in sales after a 17% growth.

1

Chart 1: FMCG Value Growth in 2008 in Selected ASEAN Countries

Sources: Asean Affairs; TNS Media Vietnam

ISI Analytics

FMCG india

New Zealand’s FMCG plays a vital role in its economy, in which it accounted for 5% of GDP, 31% of manufacturing GDP and 26% of manufacturing employment, while offering 63,000 full time jobs to its people. The nation’s export for food and beverage (F&B) trebled over the past 17 years, growing from NZD6.96bn in 1990 to NZD21.43bn in 2008. Dairy, meat, seafood, fruits and vegetables, wine as well as specialty food industries are among the main categories of the country’s F&B industry. Dairy industry that produces goods ranging from high quality basics (milk powders, butter and etc.) to specialty foods (ice-cream, artisan cheeses and etc.) is responsible for 22% of total exports, while dairy exports in 2008 amounted to NZD9.29bn. In Malaysia, total FMCG expanded 8.2% in 2007 with average prices increasing by 4.2% as inflation kicks in. Malaysians continued to purchase convenient and indulgent products in spite of inflationary pressures, whereby new launches for ice cream and snacks as well as innovative products such as ice cream minis were signs of successful convenient indulgence. In addition, fabric softener and air freshener experienced notable growth. A survey that involved 1,000 Malaysians indicated that Malaysians continue to be loyal to brands despite the global financial slowdown, particularly in FMCG goods such as dairy products (76%), staple food (78%), soft drinks (61%), canned products (68%), healthcare (78%) and cosmetic products (74%).

1.2 General Economic Environment India is one of the economies that shrugged off the effects of the recent global financial crisis with a growth of 7.87% during July-September 2009, up from 6.1% during the previous quarter. Analyst projected that the nation’s economic growth is projected to grow between 7-7.5% in 2010-11 and could be the world’s fastest expanding economy within the next four years relying on higher pool of savings to help finance development in the country to surpass China. Expanding at an average GDP of 7.1% over the decade through the third quarter of 2009, it is possible for the Indian economy to experience a double-digit growth within the next four years. The country’s finance ministry reported that its fast-growing USD1.2tr economy currently has saving rate of 32.5% of GDP compared to 28% in Japan, 30% in South Korea and 38% in Malaysia. With the support of growing population in its workforce (220mn people by 2030) as well as increasing savings by young working Indians that will add momentum to the nation’s growth. According to estimates published by the Index of Industrial Production (IIP), index for electricity, manufacturing and mining each registered growth rates of 7.5%, 9.2% and 9.5% during the second quarter of 2009-10.

GDP (yoy)

Inflation (yoy)

Inward FDI

Export Import

Population Population Growth yoy

% % USD mn USD mn USD mn Person mn %

Mar-08 8.63 7.87 2,838 17,254 23,574 2002-03 1,056 1.54

Jun-08 7.8 7.69 -618 19,181 28,951 2003-04 1,072 1.52

Sep-08 7.75 9.77 1,159 15,789 31,136 2004-05 1,089 1.59

Dec-08 5.8 9.7 1,392 13,368 19,456 2005-06 1,106 1.56

Mar-09 5.76 8.03 1,067 12,916 16,597 2006-07 1,122 1.45

Jun-09 6.13 9.29 2,824 12,972 22,166 2007-08 1,138 1.43

Sep-09 7.87 11.64 6,607 13,608 21,377 2008-09 1,154 1.41

Table 1: Key Economic Indicators

Source: CEIC

2

ISI Analytics

FMCG india

Indian remains a resilient market for overseas investors and local consumers. Overseas investment inflows into India’s stock market totaled to USD816.69mn during the first trading week of 2010, while local currency rating outlook was raised from ‘stable’ to ‘positive’ by Moody’s Investors Service as the country demonstrates resilience to the global financial meltdown as well as positive outlook that its economy will resume high levels of economic growth. Among the BRIC countries, China’s unemployment rate of 4.3% is the lowest among these markets while India’s IT-driven growth path is projected to provide job opportunities that will lower the country’s current unemployment rate of 7.2%. Russia and Brazil’s current jobless rate are at 9.9% (mid-2009) and 8.1% respectively. On the other hand, Brazil’s jobless rate is projected to decline steadily as a result of its diversified economy. The World Bank estimated that 41.6% of India’s population lives below USD1.25 on a

daily basis and 75.6% live with less than USD2 per day. In the Union Budget 2009-10, INR39,100cr was allocated for rural employment programmes, up 144% over the 2008-09 budget. During the first half of 2010, India’s Finance Minister expanded microfinance programmes through the budget 2010-11 by doubling the allocation of INR400cr to the Micro-Finance Development and Equity Fund. According to India’s Economic Survey, a reduction in unemployment rate is expected to take place during the end of the 11th Five Year Plan (2007-12). The Survey also projected that the country’s labour force from 2007 to 2012 is expected to be around 45mn (unemployment rate to fall below 5% by 2012) against 58mn employment opportunities that would be created during its 11th Five Year Plan. During April-June 2009, employment rate fell by 131,000, with declines in employment rate of 38,000 in April and 157,000 a month later before increasing 64,000 in June.

Chart 2: Gross Domestic Saving – Household

Source: CEIC

3

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2004/05 2005/06 2006/07 2007/08 2008/09

INR bn

28

28.5

29

29.5

30

30.5

% of Personal Disposable

Income (%)

Financial Savings

Physical Savings

% of Personal Disposable Income

ISI Analytics

FMCG india

1.3 India’s FMCG Industry Overview India’s FMCG sector was valued at INR60,000cr in 2004 after a growth of 4% during 2003-04. According to a report by the Federation of Indian Chambers of Commerce and Industry (FICCI), several FMCG registered double-digit growth in value terms, for example, shaving cream (20%), deodorant (40%), branded coconut oil (10%), anti-dandruff shampoos (15%), hair dyes (25%) and cleaners and repellents (20%). On the contrary, negative growth of up to 8% was registered in products such as personal healthcare, laundry soaps, dish wash, toilet soap, toothpaste and toothpowder. In 2008, India’s FMCG sector had a value of INR86,000cr and analysts projected a growth of 15% in 2010 (2009: 12%) as the economy shows signs of recovery. According to the FICCI-Technopak report, the FMCG sector will grow at a rate of 10-12% within the next decade to reach INR206,000cr by 2013 and INR355,000cr by 2018. The implementation of the proposed Goods and Services Tax (GST) and the less restrictive foreign direct investment (FDI) policies are expected to contribute to the growth of the FMCG sector to INR225,000cr by 2013 and INR456,000cr by 2018.

With a total market size in excess of USD14.7bn, India’s FMCG industry is the fourth largest sector in its economy and plays a vital role in India’s socio-economic front with nearly eight million stores selling FMCG and employing some 25mn people as wholesalers, distributors and others. Besides that, the FMCG sector purchases nearly INR9,600cr worth of agricultural products and processes them into value-added products while the sector accounted for nearly 40% of the media industry’s revenue. Sales in the FMCG sector grew by a staggering 14.8% during the six-month period ended September 2009 but only expanded 7% during the two-month period ended November 2009. As a result of lower growth in the sector, India’s top 10 FMCG companies experienced deceleration in sales growth from 9.9% during the first half of the financial year (April-September 2009) to a growth of 3.3% during the October-November period. In addition, contributing factors such as price increase of 50-100% for most agri-commodities as well as higher crude oil prices caused operating margin to fall during the October-December quarter.

Table 2: FMCG Category and Products

Source: India Brand Equity Foundation (IBEF)

Category Products

Food and Beverages

Health beverages; soft drinks; staples/cereals/ bakery products (biscuits, bread, cakes); snack food; chocolates; ice cream; tea; coffee; soft drinks; processed fruits; vegetables; dairy products; bottled water; branded flour; branded rice; branded sugar; juices etc.

Household Care

Fabric wash (laundry soaps and synthetic detergents); household cleaners (dish/utensil cleaners, floor cleaners, toilet cleaners, air fresheners, insecticides and mosquito repellents, metal polish and furniture polish).

Personal Care Oral care; hair care; skin care; personal wash (soaps); cosmetics and toiletries; deodorants; perfumes; feminine hygiene; paper products.

4

ISI Analytics

FMCG india

1.3.1 Food Inflation As a result of the 2007-08 food price crisis, international food prices reached its peak in 2008 but fell drastically a year later. Developing countries were largely affected by the hike in food prices, where share of expenditure on food accounts for a large proportion of total consumer spending. According to Chart 3, developing countries such as Indonesia, India and China each spent 41.9%, 34.9% and 33.0% of their consumer spending on food in 2008. In 2010, due to speculation that the Indian central bank may hike interest rates after instructing banks to raise more cash reserves, the nation’s food prices inflated for a second week. An index that measures wholesales prices of lentils, rice, vegetables and other food products jumped 17.56% in the week to January 23 over the previous

year. In addition, food inflation hiked 19.95% in the week to December 5, 2009, indicating the most significant increase since December 1998. Inevitably, high food inflation could restrict consumers’ demand and pricing flexibility for FMCG while lowering consumers’ purchasing power that diverts purchases away from certain FMCG. Table 3 indicated that retail price for rice in Bangalore had the most drastic hike in price, where its price increased two-fold from INR12 per kg in 2007 to INR36 per kg two years later. The only price drop shown in the table is the wheat price in Ahmedabad, in which its price fell 6.5% from INR12.3 per kg in 2007 to INR11.5 per kg the next year before rising a staggering 30.43% to INR15 per kg in 2009. Another notable increase is the price for rice in Ahmedabad, where a hike of INR10.2 per kg to INR23 per kg in 2009 from INR12.8 per kg two years earlier.

34.9

33.0

11.8

5.9

41.9

24.0

18.6

0.0 5.0 10.0 15.0 20.0 25.0 30.0 35.0 40.0 45.0

Indonesia

India

China

Brazil

South Africa

EU

USA

% of total spending

Chart 3: Share of Expenditure on Food in Total Consumer Spending in 2008

Sources: Euromonitor; OECD; Eurostat

INR per kg

Rice Wheat Atta

2007 2008 2009 2007 2008 2009 2007 2008 2009

Delhi 16.0 22.0 23.0 12.0 13.0 15.5 13.0 14.0 17.5

Ahmedabad 12.8 16.5 23.0 12.3 11.5 15.0 13.0 13.5 16.0

Mumbai 15.3 17.5 19.0 15.5 16.0 20.0 16.0 17.0 22.0

Bangalore 12.0 17.0 36.0 16.0 16.0 21.0 16.0 17.0 21.0

Hyderabad 11.0 14.0 19.0 12.0 14.0 19.0 16.0 17.0 17.0

Chennai 15.0 18.0 22.0 17.0 18.0 21.0 18.0 20.0 22.0

Table 3: Agriculture Retail Price in Selected Cities

Source: CEIC

5

ISI Analytics

FMCG india

1.3.2 Food and Beverages Industry India’s food industry accounted for nearly 65% of the nation’s retail market and has an estimated value of USD182bn, while exports of fresh and processed vegetables, fruits, livestock and cereals hike 10% to reach USD8.67bn in 2008-09. According to a report by Associated Chambers of Commerce and Industry of India (ASSOCHAM), India’s food market (includes processed F&B) has a current market size of INR7,198cr after a 17% growth in 1Q 2009-10 and is projected to grow 19% during 2Q FY10. Agricultural and Processed Food Products Export Development Authority (APEDA) projected that India’s farm product exports in the global trade will expand from its current 2% to more than 5%, and India’s exports of agricultural products might double to hit USD20.6bn within the next five years. Each year, India produces 105 tonnes of milk (highest in the world), 150 tonnes of fruits and vegetables (second largest), 485 mn livestock (highest), 230 mn tonnes of food-grain (third largest) and 7m tonnes of fish (third largest). • Spices In spite of a challenging economic environment, spice exports for India rose 6% in dollar terms to its all-time high of USD11.68bn (or 470,520 tonnes) in 2008-09, up from USD11.01bn (or 444,250 tonnes) during the previous fiscal. • Food Processing On the food processing front, the Indian market has an estimated value of USD13.05bn that includes biscuits, chocolates, ice-cream, confectionery, snacks, cheese and butter. With major global companies such as Britannia, Nestle, Amul, ITC Foods, Parle, Kellogg’s, GlaxoSmithKline and others, this sector

exhibited sound growth of 14-15% over the past three years. A total of USD143.8mn of FDI flowed into India’s food processing industry in 2007-08, up USD138.1mn from previous fiscal of USD5.7mn. In order to allow the food processing sector to prosper, the Indian government formulated the Vision-2015 action plan. In which it plans to treble the size of this industry from nearly USD70bn to USD210bn, thus increasing the level of processing of perishables from 6% to 20%, thus expanding value addition from 20% to 35% as well as strengthening the nation’s share in global food market from 1.5% to 3%. Moreover, the government introduced a blueprint for enhancing growth in the country’s food processing sector through the formulation of the National Food Processing Policy, infrastructure improvements in the rural areas as well as the simplification of tax structures. • Snacks and Confectionery This market is poised for steady growth of 15-20% with an estimated worth of USD3bn. The branded snack market has an estimated value of USD1.34bn, while the unorganized market has an estimated value at USD1.56bn with a potential growth rate of 7-8%. • Health Food FMCG companies forayed into India’s growing branded health food sector. Hindustan Unilever Ltd’s (HUL) health food brand - Kissan Amaze is being marketed on a trial basis in three southern states in India. Meanwhile, joint venture partnership between Godrej Food & Beverages Ltd and Hershey Company - Godrej Hershey Foods & Beverages Ltd (GHFBL) has plans to introduce several brands from its international portfolio into the Indian branded health food sector.

6

ISI Analytics

FMCG india

• Dairy Dairy India 2007 projected that India’s current dairy sector is USD62.67bn with a 5% yoy growth, of which its exports increased from USD210.5bn in 2007-08 to USD113.57bn a fiscal year later. India’s position as the world’s largest milk producer was maintained with production of 110mn tonnes in 2008-09. • Beverages India’s market size for carbonated drinks was nearly USD1.5bn, while the juice and juice-based drinks market size was nearly USD0.25bn. The fruit-drink market is an expanding market that has a growth rate of 25% while sports and energy drinks category have potential to expand due to its low penetration in the domestic market. As a result of rising disposable income among the Indian population, growth in foreign tourists

as well as favourable government policies, India’s alcoholic beverages category saw consistent growth over the years (9% CAGR by 2013) with its wine industry expanding at a rate of 25% yoy growth. • Outlay, Expenditure and Investments Investments play an important role for growth of India’s food sector, particularly in the food processing industry. The food processing industry currently employs some 48 mn people (direct employment: 13mn; indirect employment 35mn). And in 2004-05, this sector contributed INR280,000cr (or nearly 14%) to manufacturing GDP. Outlay and expenditure for this sector each increased 60.21% and 72.06% from 2004-05 to 2008-09. On the contrary, inflow FDI contracted 26.9% from 2007-08 to the next fiscal when global financial crisis adversely affected inward investments (Chart 4).

Chart 4: Outlay, Expenditure and Inflow FDI for Food Processing Industry

0

2

4

6

8

10

2004-05 2005-06 2006-07 2007-08 2008-09

Outlay & Expenditure

(in INR cr)

0

100

200

300

400

500

600

700

Inflow FDI (in INR cr)

Outlay Expenditure Inflow FDI

Source: Ministry of Food Processing Industries (MOFPI)

Table 4: Production of Selected Food Products

Biscuits Chocolate and Sugar

Confectionary Malted Food

Milk Powder

Wheat Flour and Maida

Sugar Salt

Tonnes Tonnes Tonnes Tonnes Tonnes

th Tonnes

th Tonnes

th

2007 1,248,081 55,898 82,115 17,992 2,169 26,905 18,388

2008 1,378,157 61,787 61,821 17,889 2,146 26,025 17,425

Mar-09 355,344 17,079 13,421 51,253 547 7,875 5,433

Jun-09 377,363 13,635 12,847 27,467 572 701 11,428

Source: CEIC

7

ISI Analytics

FMCG india

1.3.3 Household Care As a result of rapid urbanisation and emergence of small packs and sachets, this segment saw high level of penetration, in which it is projected to grow at a CAGR of 2% from 2005 to 2010. Detergent production in India expanded 66.92% from 639,472 tonnes in 1999 to 1,067,415 tonnes in 2007 before contracting 6.18% to 1,001,454 tonnes a year later. In 2010, Procter & Gamble (P&G) and HUL were engaged in a price war. With the lower

priced version of Tide introduced by P&G, HUL retaliated by slashing prices by 10-30% for its detergent products, namely Rin and Surf where HUL cut the price for Rin from INR70 to INR50 per pack. As for Surf Excel Blue, prices were brought down from INR91 to INR82 for a 500gm pack. Contributing close to one-fourth (in FY2009) of its total sales, the detergent segment remains a key market for HUL. With P&G’s new urgency in this segment, the company promoted Tide Natural with smart advertising as well as through volume discounts.

Chart 5: Exports of Selected Food Products

Source: CEIC

Chart 6: Production for Selected Beverages Products

Source: CEIC

0

100

200

300

400

500

600

700

Jun-07

Aug-07

Oct-07

Dec-07

Feb-08

Apr-08

Jun-08

Aug-08

Oct-08

Dec-08

Feb-09

Apr-09

Jun-09

Beer (Litre th)Coffee (Ton)Tea (Ton)Soft Drinks and Soda (Bottle mn)

8

0

50

100

150

200

250

300

350

2003

2004

2005

2006

2007

2008

Mar-09

Jun-09

Sep-09

Dairy Products, Processed Fruits &

Juices and Processed Vegetables

(in USD m

n)

0

200

400

600

800

1,000

1,200

1,400

1,600

Spices (in USD m

n)

Dairy Products

Processed Fruits and Juices

Processed Vegetables

Spices

ISI Analytics

FMCG india

1.3.4 Personal Care This segment of FMCG has been experiencing growth for the past few years and has an estimated worth of USD4bn. Key segments of India’s personal care industry include personal hygiene products, hair care, skin care, colour cosmetics, and fragrances. In addition, the largely dominated bar soap segment saw annual growth of approximately 5% for the past four years. ASSOCHAM reported that India’s INR3,360cr oral care market (includes toothbrush and tooth powder) experienced a 10.8% growth during the first quarter of 2009-10. Analysts estimated that this market will grow 11.5% during the second quarter of 2009-10 with a projected market size of INR3,450cr. However, the INR18.5bn skin care and cosmetics market that includes skin/fairness creams, shaving creams and deodorants, experienced a 11.52% growth during the first quarter of 2009-10 and is projected to see a 12% growth during 2Q FY10. Meanwhile, the hair care market size (includes hair oils, shampoos, creams, conditioners, hair dyes

and etc.) was approximately INR8,000cr with strong growth of 14.68% in the first quarter of 2009-10 and is expected to post sound growth of 16% in 2Q FY10. The key trend in the personal care segment is moving away from health products towards beauty products, hence consumers are switching demand from basic products (such as soaps, shampoos, hair oils and etc.) to specialized products (such as skin whitening cream, anti-ageing products, sun block lotions and etc.). With rising disposable income from USD2,720 in 2008 to an estimated USD3,482 in 2012 as well as growing female population (2008: 178mn; 2012: estimated 191mn) between the age group 25-44 years will definitely boost this market segment. Sales of whitening cream outpaced those of Coca-Cola and tea in India as most Indians consider having fair-complexions an asset. As a consequence, the country’s market for whitening cream expanded at a whopping 18% yoy growth while analysts predicted that it will grow to nearly 25% in 2010 with an estimated market worth of USD432mn.

6%

1%

46%

31%16%Hair Care

Bath & Show er

Products

Colour Cosmetics

Fragrances

Skin Care

Chart 7: Market Share of Personal Care Products

Source: Tata Strategic Management Group

9

ISI Analytics

FMCG india

Table 5 shows that industrial production of hair oil and Ayurvedic hair oil in India jumped 192.06% from 7.52mn litres in 2004 to 21.97mn litres a year later and saw a growth of 56.99% from figures in 2005 to 34.49mn litres in 2008. Industrial production of soap (IPP) shrank 30.9% from 584,414 tonnes in 2003 to a low of 403,833 in 2007 before gradually rising 41,832 tonnes to 445,665 tonnes a year later. On the contrary, production of soap (SSI) grew 6.24% from 3,592,000 tonnes in 2003 to 3,816,000 tonnes in 2008. Production for toothpaste expanded 249.57% from 19,061 tonnes in 2003 to 66,632 tonnes in 2008 while production for toothpowder contracted 22.58% from its peak of 8,382 tonnes in 2004 to a low of 6,489 tonnes in 2007. In 2009, one of the FMCG companies – Marico Ltd (Marico) test marketed new products (Nihar Naturals Cooling Oil and Parachute Advanced Cooling Oil) in order to gain greater market share. In addition to launching new products, Marico increased its

presence in the Indian market through increased penetration in the rural markets. The company has a 21% market share in the INR2,200cr hair oil segment and aims to increase market share in this lucrative segment through cooling hair oil products. In 2010, Mumbai-based VVF Ltd acquired three brands from Chennai-based Henkel India (Henkel) – a FMCG company, namely Aramusk and Moloy soaps as well as Mahobringol hair oil. Three months after the acquisition, VVF - one of the world’s largest contract manufacturers of bar soaps bought Henkel’s plant in Tiljala, Calcutta, in which the cost of acquisition is estimated INR23cr while the plant accounted for INR18cr. The acquired brands are estimated to yield little turnover at a national level but brands such as Aramusk is famous in its domestic market as it is one of the oldest male deodorant soaps in India with a loyal consumer base. Meanwhile, Moloy sandalwood soap and Mahabringol hair oil are popular brands in eastern India.

Table 5: Industrial Production of Selected Personal Care Products

Hair Oil & Ayurvedic Hair Oil

Soap (IPP) *

Soap (SSI) **

Toothpaste Toothpowder

Litre th Tonnes Tonnes th Tonnes Tonnes

2003 2,127 584,414 3,592 19,061 7,744

2004 7,521 502,045 3,647 17,673 8,382

2005 21,966 480,811 3,651 32,771 8,233

2006 26,308 484,775 3,697 48,189 7,237

2007 30,636 403,833 3,761 53,129 6,489

2008 34,485 445,665 3,816 66,632 7,802

Mar-09 9,248 135,270 960.2 17,097 2,018

Jun-09 10,055 156,102 961.4 18,731 2,052

* IPP = Independent Power Producer ** SSI = Small Scale Industries Source: CEIC

10

ISI Analytics

FMCG india

2.1 Union Budget 2010-11 The FMCG industry is expected to yield higher growth on the back of higher disposable income led by income tax cuts, while FMCG prices are expected to hike. Prices of daily use products such as soaps, talcum powder, shampoos, hair dyes, diapers and sanitary napkins are expected to increase by 2-5%, while diapers and sanitary napkins that were previously fully exempt from excise are now slapped with a 10% duty. However, prices of deodorants and perfumes are expected drop by 5% while

duty charges on medicinal and toilet preparations will be reduced from 16% to 10%. Most FMCG companies including HUL, Colgate-Palmolive, Nestle, Reckitt Benckiser and Dabur India Ltd have large manufacturing plants in excise-free zones that are not affected by a hike or cut in excise duty, while higher cost of production will inevitably cause price hike. Also, the establishment of five additional food parks will no doubt boost the food processing industry.

2. Market Trends and Outlook

11

Table 6: Union Budget 2010-11: Central Plan Outlay by Sectors

in INR cr 2009-10 Budget

Estimates 2009-10 Revised

Estimates 2010-11 Budget

Estimates

Agriculture and Allied Activities 10,629 10,123 12,308

Rural Development * 51,769 51,560 55,190

Irrigation and Flood Control 439 404 526

Energy 115,574 109,685 146,579

Industry and Minerals 35,740 30,694 39,019

Transport ** 94,306 88,948 101,997

Communications 16,731 16,099 18,529

Science Technology and Environment 11,207 9,908 13,677

General Economic Services 6,270 5,446 7,554

Social Services *** 103,856 101,370 127,570

General Services 1,400 1,353 1,535

Grand Total 447,921 425,590 524,484

* Includes provision for rural housing but excludes provision for rural roads ** Includes provision for rural roads *** Excludes provision for rural housing

Source: Ministry of Finance

• Fertilizer Subsidy: Effective from 1st April, 2010, a Nutrient Based Policy for this sector will enhance agricultural productivity as well as provide better returns for Indian farmers, hence reducing the volatility in demand for fertilizer subsidy.

• Foreign Direct Investment: Clear definition in the calculation of indirect foreign investments in Indian companies simplifies the FDI regime. Also, complete liberalisation of pricing and payment of technology transfer fee and trademark, brand name and royalty payments will ease the process of FDI.

ISI Analytics

FMCG india

• Agricultural Growth: (a) Agricultural Production: 1. The provision of INR400cr to strengthen

green revolution in Eastern India, namely Bihar, Chattisgarh, Jharkhand, Uttar Pradesh, Bengal and Orissa.

2. The provision of INR300cr for rain-fed areas to organise 60,000 pulses and oil seed villages and also the provision of water harvesting watershed management as well as soil health to increase productivity of dry farming areas.

3. The provision of INR200cr for conservation farming that sustained the gains made in the green revolution areas. It involves concurrent attention to soil health, water conservation as well as preservation of biodiversity.

(b) Reduction in Wastage of Produce: 1. Government will address the issue

regarding the opening up of retail trade that will close the gap between farm gate, wholesale and retail prices.

2. An ongoing scheme for private sector participation will lower deficit in storage capacity.

(c) Credit Support to Farmers: 1. Banks are to meet target of

INR375,000cr set for agriculture credit flow.

2. In view of drought and floods in some states, repayment period of the loan amount owed by farmers are to be extended by six months from 31st December, 2009 to 30th June, 2010 under the Debt Waiver and Debt Relief Scheme for Farmers.

3. Farmers who promptly repay short-term crop loans will receive additional incentive of 2% (instead of 1%) for 2010-11.

(d) Impetus to the Food Processing Sector: 1. The government will add another five

mega food parks, hence bringing India’s food parks to a total of fifteen.

2. Cold storage and cold room facilities (including farm level pre-cooling and preservation or storage of agricultural and allied produce, marine products and meat) will be available through External Commercial Borrowings.

• Infrastructure: A whopping INR173,552cr

was allocated for infrastructure development, while allocation for road transport and railway transport each amounted to INR19,894cr and INR16,752cr.

• Energy: Allocation for the power sector

(excluding Rajiv Gandhi Grameen Vidyutikran Yojana) doubled to INR5,130cr in 2010-11, up from INR2,230cr in 2009-10. The Coal Regulatory Authority was introduced to allow fair competition in the coal sector, in which the Ministry of New and Renewable Energy’s plan outlay rose 61.29% to INR1,000cr in 2010-11, up from INR620cr. In addition, projects that involve solar, small hydro and micro power are to be established in Jammu and Kashmir at a cost of INR500cr.

• Education: Allocation for school

education was increased from INR26,800cr in 2009-10 to INR31,036cr in 2010-11, thus showing a 15.81% growth. Moreover, under the Thirteenth Finance Commission grants for 2010-11, states are entitled to some INR3,675cr for elementary education purposes.

• Rural Development: The Mahatma

Gandhi National Rural Employment Guarantee Scheme and rural development were allocated INR40,100cr and INR66,100cr respectively. Besides

12

ISI Analytics

FMCG india

that, allocated funds for Backward Region Grant Fund expanded 25.86% from INR5,800cr in 2009-10 to INR7,300cr in 2010-11, while additional central assistance of INR1,200cr will be provided for drought mitigation in Bundelkhand.

2.2 e-Choupal e-Choupal was developed by India’s conglomerate, Indian Tobacco Co. (ITC). Prior to the introduction of this facility, farmers were restricted to selling their products in the local mandi through a middleman, hence the low earnings. The availability of e-Choupal allowed farmers to be trained to manage the Internet kiosk that allows them to yield the best price through the access of daily prices of crops in India as well as overseas. Apart from changing the quality of farmers’ lives, e-Choupal provides information regarding weather forecasts, farming techniques, crop insurance and others. Covering ten states across 40,000 villages, e-Choupal allows 4mn farmers (of which constitutes a majority of 75% of the population living below poverty line) across India to obtain relevant information that helps improve rural economy. The network of 6,500 e-Choupal centres expanded the spectrum of commodities such as wheat, rice, pulses, soya, maize, spices, coffee,

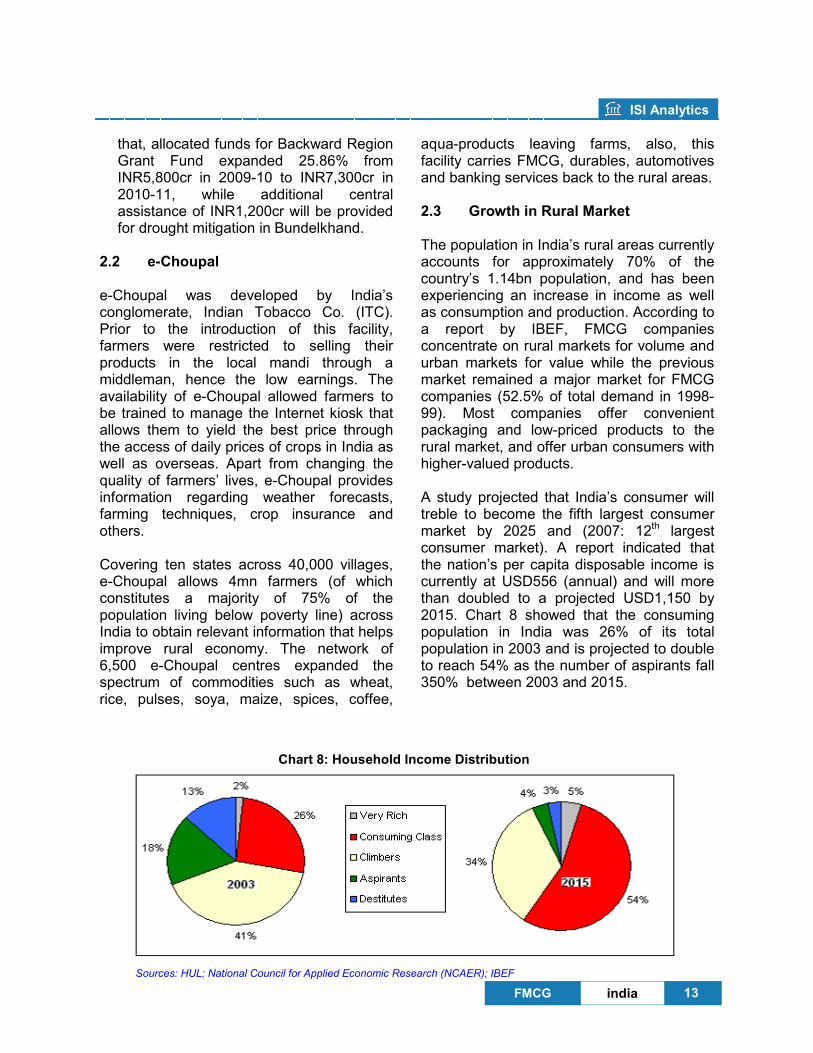

aqua-products leaving farms, also, this facility carries FMCG, durables, automotives and banking services back to the rural areas. 2.3 Growth in Rural Market The population in India’s rural areas currently accounts for approximately 70% of the country’s 1.14bn population, and has been experiencing an increase in income as well as consumption and production. According to a report by IBEF, FMCG companies concentrate on rural markets for volume and urban markets for value while the previous market remained a major market for FMCG companies (52.5% of total demand in 1998-99). Most companies offer convenient packaging and low-priced products to the rural market, and offer urban consumers with higher-valued products. A study projected that India’s consumer will treble to become the fifth largest consumer market by 2025 and (2007: 12th largest consumer market). A report indicated that the nation’s per capita disposable income is currently at USD556 (annual) and will more than doubled to a projected USD1,150 by 2015. Chart 8 showed that the consuming population in India was 26% of its total population in 2003 and is projected to double to reach 54% as the number of aspirants fall 350% between 2003 and 2015.

Chart 8: Household Income Distribution

Sources: HUL; National Council for Applied Economic Research (NCAER); IBEF

13

ISI Analytics

FMCG india

2.4 Regulatory Issues 2.4.1 National Food Processing Policy India’s food processing sector has enormous importance in the nation’s development and with India being the second largest food producer in the world, this sector has solid growth potential. Food production is expected to double within the next decade to accommodate the rising consumption of value added food products. Benefits such as economic growth, growing agricultural yields, higher productivity and job creation will definitely raise the living standards of the Indian community, especially those living in the rural areas. This policy will facilitate the establishment of cold chain, low cost pre-cooling facilities that are located near farms, cold stores and grading, sorting as well as packing facilities so that wastage levels can be lowered whilst improving quality and shelf life of those products. New technologies in the food processing and packaging will be developed

in order to provide mechanism to facilitate the process of technology transfer through a network of R&D institution. In addition, agro food parks will be built to facilitate the food production process. The following will have greater priority and special consideration in view of policy and plans: • The North Eastern Region, the Hilly

Areas, and ITDP (Initiative for Transportation and Development Programmes) areas in India shall be given priority in terms of attention and consideration.

• Fiscal incentives (such as excise duty or sales tax concession and tax holidays) are to be given to the above mentioned areas as well as areas that are established outside these areas near the market centre.

• Food processing units can enjoy tax holiday (excluding liquor, cigarettes and aerated drinks and similar luxury products) for a period of 10 years.

Table 7: Challenges, Constraints and Concerns

Potential Growth India is a major food producer with more than 600 mn tonnes of food products under its production. It has growth potential to become the largest food producer in the world.

Wastage Processing level is currently very low while wastage level is high that shrinks national wealth.

Value Addition Value addition to raw products in India is only at a 7% and this figure is considered low when compared to China’s 23% and Philippines’ 45%.

Small Scale and Unorganized Sectors

These sectors account for 75% of the food processing industry and only has local presence in which it lacks access to knowledge, technology and marketing network.

Low Demand The price gap between farmers’ realization and consumers’ final price is very big – caused by low productivity, high cost of production, spoilage due to poor infrastructure and high cost of borrowing.

Marketing Efforts The marketability of processed food is low despite vast domestic market size. However, this market has growth potential should awareness and educational campaigns are held.

Source: Confederation of Women Entrepreneurs (CoWe)

14

ISI Analytics

FMCG india

2.4.2 FDI Policy in Retail Trading (Single Brand) In February 2010, ministers in India advocated that its retail market lacks competition for a check on prices as well as liberalisation of the industry. The share of FDI inflow to the retail trading (single brand) sector has been increasing over the years, in which it accounted for 0.18% of India’s INR469,364.98cr FDI inflows from April 2000 to December 2009. However, from April 2000 to December 2008, FDI inflow to the retail trading sector only accounted for 0.03% of total FDI inflow of INR338,384.74cr. The key driving forces for retail growth are banks, capital goods, engineering, FMCG, software services, oil marketing, power, two-wheelers and telecommunication companies. On July 2009, FDI inflows of retail trading (single brand) hit an approximate

USD46.6mn, meanwhile India’s retail sector is expected grow to a market size of USD833bn by 2013 and USD1.3tn by 2018 with a CAGR of 10%. The nation’s retail market saw exponential growth as developments take place in major cities, metros as well as tier-II and tier-III cities across India. The 51:49 joint venture partnership between UK-based Marks & Spencer and India-based Reliance Retail Ltd has 15 retail stores spanned across India while plans are being laid out to open as many as 35 stores over the next five years. Besides that, Europe’s largest retail – Carrefour S.A. is expected to commence its wholesale operations in India by 2010. This retail giant also plans to establish its first wholesale cash and carry outlet in the National Capital Region and the company currently exports USD170mn worth of products from India.

Table 8: Sector-wise FDI Inflows

* Processing and warehousing coffee and rubber Source: Department of Industrial Policy and Promotion

FDI Inflows (in INR cr) Apr 2000 to Dec 2009

Apr 2000 to Dec 2008

Apr 2000 to Dec 2007

Agriculture Services 7,123.17 785.44 741.22

Food Processing Industries 4,388.45 3,422.26 2,786.23

Retail Trading (Single Brand) 822.70 107.47 6.64

Soaps, Cosmetics & Toilet Preparations 680.50 498.49 434.18

Agricultural Machinery 668.95 664.91 639.98

Vegetable Oils and Vanaspati 605.63 376.92 175.88

Tea and Coffee * 381.38 377.43 142.21

Sugar 183.90 183.66 160.98

15

ISI Analytics

FMCG india

2.4.3 Government Policies and Initiatives

Removal of Quantitative Restrictions and Reservation Policy

The abolishment of most of the food and agro-processing industries (except for alcohol, cane sugar, hydrogenated animal fats and oils etc. and items reserved for the exclusive manufacture in the SSI sector) as well as the removal on quantitative restrictions in 2001 led to market expansion in the FMCG industry.

Central and State Initiatives

State government such as Himachal Pradesh, Uttaranchal and Jammu and Kashmir provided companies with fiscal incentives (such as allotment of land at concessional rates, 100% subsidy on project reports and 30% capital investment subsidy on fixed capital investment up to USD63,000) that encouraged them to establish manufacturing plants in their respective regions. The reduction of excise and import duty allows most of the processed food products to be exempted from excise duty.

Location (District) in Andhra Pradesh Name of Park

Chittoor Food processing park (existing)

Ranga Reddy Agri-biotech park (existing)

Guntur, Khammam and Nellore Food processing park (upcoming)

Location (District) in Uttar Pradesh Name of Park

Barabanki and Varanasi Agro park

Food Processing Policy, 2004-2009

• Targets to facilitate better returns for farmers and attract investment in this sector.

• Will emphasize on employment opportunities as well as minimise wastage on agri-products.

Sugar Policy, 2004

• Incentives and concessions such as exemption of entry tax on sugar, reimbursement of administrative charge and trade tax on molasses to establish sugar mills in Uttar Pradesh.

Location (District) in Madhya Pradesh Name of Park

Mandideep, Pillukhedi, Borgaon and Maneri Food Park

Biotechnology Policy, 2003

• Targets to conserve the state’s biodiversity and the sustainable use of its biotic resources.

• Production of high-yielding, draught and pest resistant seeds for agriculture and horticulture crops that is suitable for different agro-climatic areas.

Sources: HUL; NCAER; IBEF

Table 9: Sector-specific Infrastructure

16

ISI Analytics

FMCG india

2.4.3.1 Milk and Milk Powder Control Order, 1992 (MMPO) With intentions to maintain and increase the supply of liquid milk that are of desired quality in view of public interest, the central government of India introduced the MMPO in order to regulate the production, supply and distribution of milk and milk products, whereby ‘milk’ carries the meaning of milk of cow, buffalo, sheep, goat or a mixture thereof, raw or processed in any form and includes pasteurised, sterilised, recombined, flavoured, acidified, skimmed, toned, double toned, standardised or full cream milk. The functions of this board are as follows: • Provide assistance and advise the

central government on any matter that concerns the production, manufacture, sale, purchase and distribution of milk and milk products.

• Registering authorities or other officials authorised by it may carry out periodic inspection of any premises that manufacture or process milk or milk products, or business in which milk or milk products are carried out. This is to ensure compliance that are stated in the Order as well as genuine and proper supply of milk or milk products to consumers.

• Without prejudice to the provisions of the previous provision, the board shall advise the central government on matters relating to:

(a) Facilitation of the supply of availability of

liquid milk, through balancing uneven distribution supplies in different regions and seasons.

(b) Maintenance or increase in supplies of milk as well as balance the distribution of milk and milk products.

(c) Establishment of appropriate standards and norms for controlling and handling milk and milk products.

(d) Maintenance of proper sanitary and hygiene standards during the

manufacturing process of milk and milk products.

(e) Establishment, promotion or registration of any industry that is relatable to milk products.

2.4.3.2 Meat Food Product Order, 1973 This Order came into effect from 15th July, 1975 with instructions stating that no person shall conduct business his/her business as a manufacturer except under and in compliance with the terms and conditions of a license granted to him/her under this Order. As stated in the Order, sanitary and other requirements are to be complied with by a licensee are as follows: • All parts of the factory shall always be

kept clean, lighted, ventilated and should be cleaned, disinfected and deodourised at a regular basis.

• All factories shall be equipped with adequate cold storage facilities, efficient drainage as well as plumbing systems.

• The factory shall be constructed and maintained as to allow hygienic production. All operations relating to the preparation or packing of meat food products shall be carried out with strict hygienic procedures and the factory premises shall not be utilized for living or sleeping purposes provided that it is separated from the factory by a wall.

• Meat used for the preparations of meat food products (if it is not slaughtered in the factory) should only be obtained from slaughter houses in which ante-mortem and post-mortem inspections have been conducted in compliance with rules prescribed and so certified by the local authority.

• All parts of the internal surface above the floor or pavement of the slaughter house shall be washed with hot lime wash within the first ten days of March, June, September and December. Meanwhile, any blood or liquid refuse or filth in the slaughter house shall be thoroughly washed and cleaned with water and

17

ISI Analytics

FMCG india

deodorant or disinfectant within three hours after the completion of slaughter.

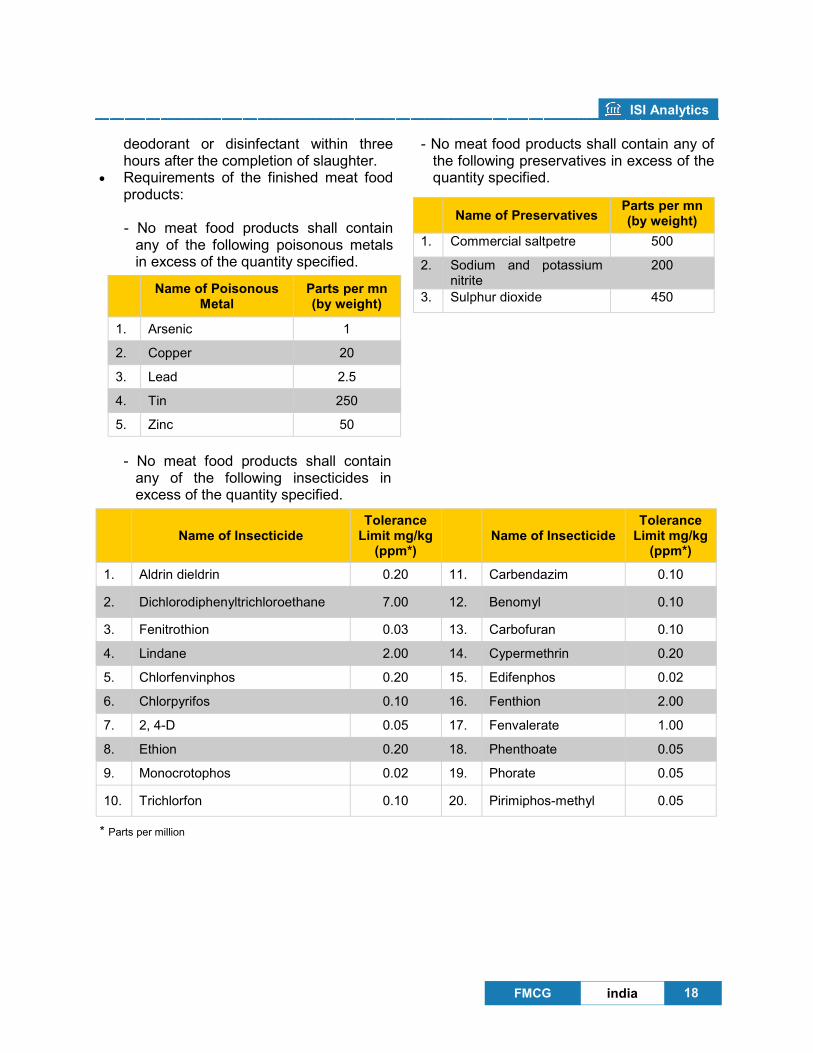

• Requirements of the finished meat food products:

- No meat food products shall contain

any of the following poisonous metals in excess of the quantity specified.

- No meat food products shall contain any of the following preservatives in excess of the quantity specified.

18

Name of Poisonous

Metal Parts per mn (by weight)

1. Arsenic 1

2. Copper 20

3. Lead 2.5

4. Tin 250

5. Zinc 50

Name of Preservatives

Parts per mn (by weight)

1. Commercial saltpetre 500

2. Sodium and potassium nitrite

200

3. Sulphur dioxide 450

- No meat food products shall contain any of the following insecticides in excess of the quantity specified.

Name of Insecticide Tolerance Limit mg/kg

(ppm*) Name of Insecticide

Tolerance Limit mg/kg

(ppm*)

1. Aldrin dieldrin 0.20 11. Carbendazim 0.10

2. Dichlorodiphenyltrichloroethane 7.00 12. Benomyl 0.10

3. Fenitrothion 0.03 13. Carbofuran 0.10

4. Lindane 2.00 14. Cypermethrin 0.20

5. Chlorfenvinphos 0.20 15. Edifenphos 0.02

6. Chlorpyrifos 0.10 16. Fenthion 2.00

7. 2, 4-D 0.05 17. Fenvalerate 1.00

8. Ethion 0.20 18. Phenthoate 0.05

9. Monocrotophos 0.02 19. Phorate 0.05

10. Trichlorfon 0.10 20. Pirimiphos-methyl 0.05

* Parts per million

ISI Analytics

FMCG india

3.1.1 Hindustan Unilever Ltd (HUL) Sunlight and Lifebuoy soaps were introduced in 1888 and 1895 respectively. And in 1895, Lever Brothers appointed agents in cities such as Mumbai, Chennai, Kolkata and Karachi. Several products were introduced by this FMCG giant – Pears soap (1902), Brooke Bond Red Label tea (1903), Lux flakes (1905), Vim scouring powder (1913), Vinolia soap (1914), Rinso soap powder (1922) and others. In 1924, Gibbs dental preparations were introduced and a year later North West Soap Co. was fully under the control of Lever Brothers. Unilever was later established in 1930 through the merger between Lever Brothers and Margarine Unie. In 1931, Unilever’s first subsidiary in India was established under the name Hindustan Vanaspati Manufacturing Co., followed by Lever Brothers India Ltd (1933) and United Traders Ltd (1935). The merger between these three companies resulted in the establishment of HUL in 1956. India’s trade liberalisation in 1991 benefited HUL’s growth as less trade restrictions allowed this FMCG giant to explore different opportunities

without production capacity constraints. With the Ayush range and Ayush Therapy Centres, HUL made its foray into the Ayurvedic health and beauty segment in 2002 and a year later, the company launched Hindustan Lever Network through the acquisition of the Amalgam Group. In 2007, the company was renamed to Hindustan Unilever Ltd. HUL’s soaps and detergents portfolio registered sound sales growth of 54% with annual segmental margin slightly shrinking by 20 basic points. Despite cost pressures, fabric wash remains its growth momentum and brands such as Surf, Rin, Sunlight and Wheel registered strong value and volume growth. On the personal products front, HUL comprises categories such as hair care, skin care, toothpaste, toothbrush, deodorants and colour cosmetics, while its well-positioned shampoo segment has a powerful brand portfolio that accommodates consumers’ needs from different income groups - Clinic is a mass market brand, Sunsilk falls into the mid-price market while Dove is in the premium segment.

3. Leading Players and

Comparative Matrix

19

3.1 Leading Players

Table 10: India’s Top 5 FMCG Companies (as at FY2009)

Industry Total Revenue (in INR th)

1. Hindustan Unilever Ltd (HUL) Food manufacturing, beverage and tobacco production, chemical manufacturing, and others

210,952,300

2. Nirma Ltd Chemical manufacturing 30,700,300

3. Dabur India Ltd (DIL) Food manufacturing, chemical manufacturing 28,522,700

4. Colgate-Palmolive India Ltd (CPIL) Chemical manufacturing 17,886,700

5. Godrej Consumer Products Ltd (GCPL) Chemical manufacturing 14,365,800

Company

Source: EMIS

ISI Analytics

FMCG india

Following the detergent price war between P&G and HUL, the latter’s stock was downgraded by a majority of brokerage firms in March 2010. P&G indirectly decreased the price of Tide Naturals by increasing grammage (25% across stock-keeping units) and adding an extra 50g to a 200g pack of Tide Naturals for the same price of INR10, while 100g would be added to a 400g pack of Tide Naturals at the same price of INR20. Share price at HUL fell 8.75% over 11th and 12th March and closed at INR219.60 at the end of the week. Analysts estimated that HUL’s detergent segment could be rendered as the detergent price war intensifies, in which the segment accounts for 10-12% of the company’s earnings before income tax. Also in March 2010, analysts indicated that HUL has been an underperformer over the

past one year; in fact, it has underperformed most of its smaller rivals since the past consecutive 12 months. HUL’s current operating margin of 14% is lower than its peak operating margin registered at 18% in 2002. FMCG giants such as Colgate and HUL are projected to have substantial control of nearly 85% of India’s toothpaste market. With soaring demand in the whitening cream segment in which HUL’s Fair & Lovely is the segment leader. The company’s cutting-edge skin-lightening technology is known to be the best in the world and has nearly 250mn consumers spanned across 30 countries. This product contains no bleach or harmful ingredients and was rated as the 12th Most Trusted Brand in India by ACNielsen ORG-MARG in 2003.

Chart 9: Share Price of HUL

Source: Bombay Stock Exchange

3.1.2 Nirma Ltd Nirma started its one-man operation in 1969 and at present, the company has grew into a 14,000 employee-base with annual turnover of more than INR2,500cr. Its operations started off with door-to-door selling of Dr. Karsanbhai Patel’s detergent powder that was priced at a shocking INR3 per kg while the cheapest brand in the market was priced at INR13 per kg. Through innovative and

low-profile marketing operations, a new domestic marketplace for the detergent segment was created.

During the 1980s, Nirma’s brand was well ahead of its closest rival – HUL’s Surf, in which Nirma offered a perfect match of product, price, promotion and place, hence capturing a greater slice of market share in its domestic market. Currently, Nirma has the largest share in India’s detergent market

20

ISI Analytics

FMCG india

(38%) and the second largest share toilet soap market (20%). Nirma witnessed a challenging FY2009 when the world’s financial system crumbled over, triggering poor economic performance in most developed countries. Nirma’s consolidated revenue was mainly contributed by soaps and surfactants, processed minerals as well as pharmaceutical with net sales growing from INR2,684.46cr in FY2007-08 to INR4,574.82cr during the next fiscal. Soaps and surfactants accounted for 57.64% of net sales for FY2009, down 20.23% from previous year’s 77.87%.

Worldwide recession impacted the company’s processed minerals segment as global demand for soda ash deteriorated following contractions in the construction and auto industries, whereby the glass industry accounted for nearly 50% of worldwide demand for soda ash. Processed minerals are manufactured in the US and are mainly marketed in markets such as the US, Latin America, Europe, China, Japan and Gulf countries. In order to counter the effects of the recessionary pressure in the US market, Nirma sought alternative markets, reallocated its employees, as well as introduced maintenance programmes.

Chart 10: Production of Selected Goods

640.28

59.88

78.71

57.37

86.74

692.74

0 200 400 600 800

Detergents

Toilet Soap

Linear Alkyl

Benzene

Tonnes (in th)

2007-08

2008-09

Source: Company’s Annual Report

3.1.3 Dabur India Ltd (DIL) DIL was established in 1884 with its manufacturing plant set up two years later and further expanded to setting up its research laboratories in 1919. DIL was restructured into a public limited company in 1986 and entered into a joint venture partnership with Spain-based Agrolimen to manufacture and market confectionary products in its domestic market. With its oncology formulation centre, DIL entered the specialised healthcare area of cancer treatment in 1993. Two years later, DIL

entered into joint venture agreements with Israel-based Osem for food and France-based Bongrain for cheese and other dairy products. In 2003, Dabur demerged its pharmaceutical operations from the FMCG operations so that each entity can focus on their respective operations. With this, DIL’s FMCG business comprises of personal care products, healthcare products as well as Ayurvedic specialities. In addition, its pharmaceutical business includes allopathic, oncology formulations and bulk drugs. And in

21

ISI Analytics

FMCG india

2005, DIL adopted an inorganic growth strategic through the acquisition of Mumbai-based Balsara’s oral care and household care product in a INR143cr all-cash deal and added brands such as Promise, Babool, Sanifresh and Odonil to its product range. Also, the acquisition allows DIL to expand its scale of operation through synergies in its marketing, sales, distribution and procurement activities. A year later, DIL crossed the USD2bn mark in market capitalisation and in line with its commitment to adhere global best practices and highest standards of transparency as well as governance, DIL adopted the US GAAP (the US Generally Accepted Accounting Principles). In 2007, the company entered the organised retail business through H&B Stores Ltd – a wholly-owned subsidiary of DIL. In order to increase presence in its domestic retail market, DIL will invest INR140cr by 2010 with aims to establish a chain of stores selling health and beauty products.

Despite a challenging year that saw a slowdown in the economy, DIL financial performance showed a positive trend during the FY2008-09. In which consolidated revenue increased to INR2,834.1cr after a 18.3% growth while consolidated net profit grew by 17.5% to INR391.2cr. Also, during FY2008-09, the company had four divisions, namely, consumer care, international business, consumer health, and others and these divisions generated consolidated sales of 72.8%, 18.5%, 7.3% and 1.4% respectively. Due to consistent profitable growth and improved market position, credit rating agency Crisil upgraded DIL’s rating in terms of its long-term bank facilities as well as non convertible debentures from AA+ to the highest grade in long-term rating of AAA. This upgrade also reflected DIL’s successful integration of its operations following the acquisition of a major player in the women’s skin care market – Fem Care Pharma Ltd as well as DIL’s strong market presence in the herbal products segment.

Chart 11: Category-wise Share of Consumer Care Division Sales

Source: Company’s Website

22

ISI Analytics

FMCG india

3.1.4 Colgate-Palmolive India Ltd (CPIL) Colgate’s business was established in 1806 when William Colgate started a starch, soap and candle business in New York City. In 1820, a starch factory located in New Jersey was built. However, the company was restructured and renamed as Colgate & Co. in 1857. Within the next two decades, Colgate introduced perfumed soaps and toothpastes in jars. Wisconsin-based B.J. Johnson Co. was producing soaps in 1864 but Palmolive Soap was only introduced in 1898. Owing to the popularity of Palmolive soaps, the company was renamed as Palmolive Co. and was later engaged in a merger with Kansas-based soap producer known as the Peet Brothers to become Palmolive-Peet in 1926. Two years later, Colgate-Palmolive-Peet Co. was established through a merger while Colgate was listed on the New York Stock Exchange in 1930. Again, the company was renamed as Colgate-Palmolive in 1953 and it acquired Hill’s Pet Nutrition in 1976, whereby the latter is currently the global leader in pet nutrition. The joint venture partnership between Hong Kong-based Hawley & Hazel – a leading oral care company and Colgate-Palmolive allowed the latter to strengthen its position in major markets in the Asian region. Today, the FMCG giant has sales that surpassed USD15bn with core business that include

oral care, personal care, home care as well as pet nutrition and its products are sold in more than 200 countries. Colgate-Palmolive (India) Ltd (CPIL) was established in 1937 using hand-carts to distribute its dental cream. Today, CPIL distributes its products through 3.5mn retail outlets spanned across India. The Mumbai-based FMCG company has strong presence in the oral care segment, in which it has approximately 46% market share in that segment. The company’s high sales volume was supported by the introduction of lower price-points variants and improved rural distribution. Driven by the discount brand - Cibaca, India’s rural market currently accounts for nearly 35% of its revenue. As a result of low per capita toothpaste consumption of 108-110gms (developed nations: 400-450gms; other Asian countries: 200-250gms), the Indian market offers growth opportunities in the toothpaste segment. In addition, its rural market offers attractive growth opportunities. During the third quarter ended 31st December, 2009, CPIL recorded net sales of INR490.6cr, showing a growth of 17% over the corresponding a year ago. Similarly, net profit for the third quarter of FY2009-10 hit INR116.4cr after a 29.77% growth against INR89.7cr (qoq).

Chart 12: Index Comparison

Source: Bombay Stock Exchange

23

ISI Analytics

FMCG india

During the end of 2009, Oral Health Month - a joint campaign by CPIL and the Indian Dental Association was successful in concluding its 6th edition oral health awareness with an aim to promote the importance of good oral care habits. This awareness campaign was brought together with the support of 17,500 dental professionals and was successful in covering 1,000 towns across India. In addition, mobile dental vans were used to reach underprivileged areas and provide more than 1.2lakhs free dental check-ups through 37 cities. 3.1.5 Godrej Consumer Products Ltd

(GCPL) Godrej Group was established in 1897 and has since grown into a group that has a turnover of USD2.5bn with seven major companies operating in real estate, FMCG, industrial engineering, appliances, furniture, security, agri care and other businesses. Nearly 20% of the group’s business is conducted abroad and has market presence in more than 60 countries. With its personal and home care products, GCPL is one of the leading companies in India’s FMCG sector. GCPL offers products such as Cinthol, No. 1, Expert, Ezee and etc. to its domestic market. In order to ensure that it has market coverage in the pan-India area, GCPL has established branch offices in Mumbai, Delhi, Kolkata and Chennai while its factories are located in Malanpur (Madhya Pradesh), Thana (Himachal Pradesh), Katha (Himachal Pradesh), Guwahati (Assam) and Sikkim so that the company’s diverse product portfolio can accommodate different requirements. Moreover, GCPL has several international brands and trademarks in Europe, Australia, Canada, Africa and the Middle East.

In 2005, UK-based Keyline Brands Ltd (KBL) was acquired by Godrej Group, in which the former operates in the toiletries and personal care segment and its portfolio comprises of several niche brands such as Cuticura, Aapri, Erasmic, Nulon and Inecto. With major customers such as Boots, Superdrug, Tesco, Asda, Sainsbury, and Morrisons in the UK, KBL has a current turnover of nearly GBP20mn. Also during the end of 2009, GCPL announced that it will concentrate on three core brands, namely No. 1 (soaps), Cinthol (soaps, talcum powder and deodorant) and Expert (hair colour). These three brands will receive higher investments to further innovate their brands. During the quarter ended 30th September, 2009, the company achieved a staggering 167.78% growth in consolidated net profit to reach INR93cr over INR34.73cr during the same quarter a fiscal before. The surge in profit was mainly contributed by volume growth in soaps and hair-care segments as well as lower cost of production such as palm oil. In March 2010, GCPL entered an agreement to acquire Nigeria-based Tura from Tura Group – a leading personal care manufacturer and distributor of high quality personal care products in several African markets. Tura is one of the leading beauty products in Nigeria and this acquisition will build GCPL’s pan-African presence as well as introduce its portfolio into other Western African countries. The fact that Tura is a well-established beauty company that has offered consumers with high quality products in the personal care segment over the past 20 years will help provide GCPL a platform for value creation in the pan-African region.

24

ISI Analytics

FMCG india

Chart 13: Sales Turnover (Net of Excise Duty) for Selected Segments

Source: Company’s Website

71,379.77

29,249.84

4,284.81

3,519.80

56,661.66

26,219.20

3,846.63

1,940.94

0 20,000 40,000 60,000 80,000

Soaps

Hair colour and other

toiletries

Detergents

Fatty acids and glycerine

INR lakhs

FY2007-08

FY2008-09

3.2 Comparative Matrix

HUL Nirma DIL CPIL GCPL

Mar 2009 * Mar 2009** Mar 2009** Mar 2009** Mar 2009**

Total Revenue 21,059.20 4,644.75 2,852.27 1,788.67 1,436.58

Net Profit 2,504.51 126.60 391.21 285.78 172.62

Net Profit Margin (%) 11.89 2.73 13.72 15.98 12.02

Return on Equity (%) 11.49 1.59 4.52 21.01 6.72

Return on Assets (%) 28.94 2.40 20.71 35.40 14.62

Debt / Equity Ratio (x) 29.90 34.12 12.37 43.53 23.90

EPS (INR) 11.46 12.85 4.548 20.89 6.83

Current Ratio (x) 0.98 3.79 1.18 0.86 2.22

Share Equity 217.98 79.57 86.51 13.60 25.70

Total Assets 8,653.97 5,276.53 1,889.11 807.22 1,180.81

Current Assets 5,786.78 2,341.64 950.80 500.05 732.75

Total Liabilities 6,516.50 2,715.06 1,070.30 591.95 613.96

Current Liabilities 5,883.94 619.74 807.65 583.52 329.89

Market Capitalisation (as at 26/03/10)

51,836.88 2,886.60 14,306.49 9,465.78 8,187.07

* Period length of 15 months ** Period length of 12 months Sources: Reuters; EMIS

Table 11: Financial Highlights (in INR cr unless otherwise stated)

25

ISI Analytics

FMCG india

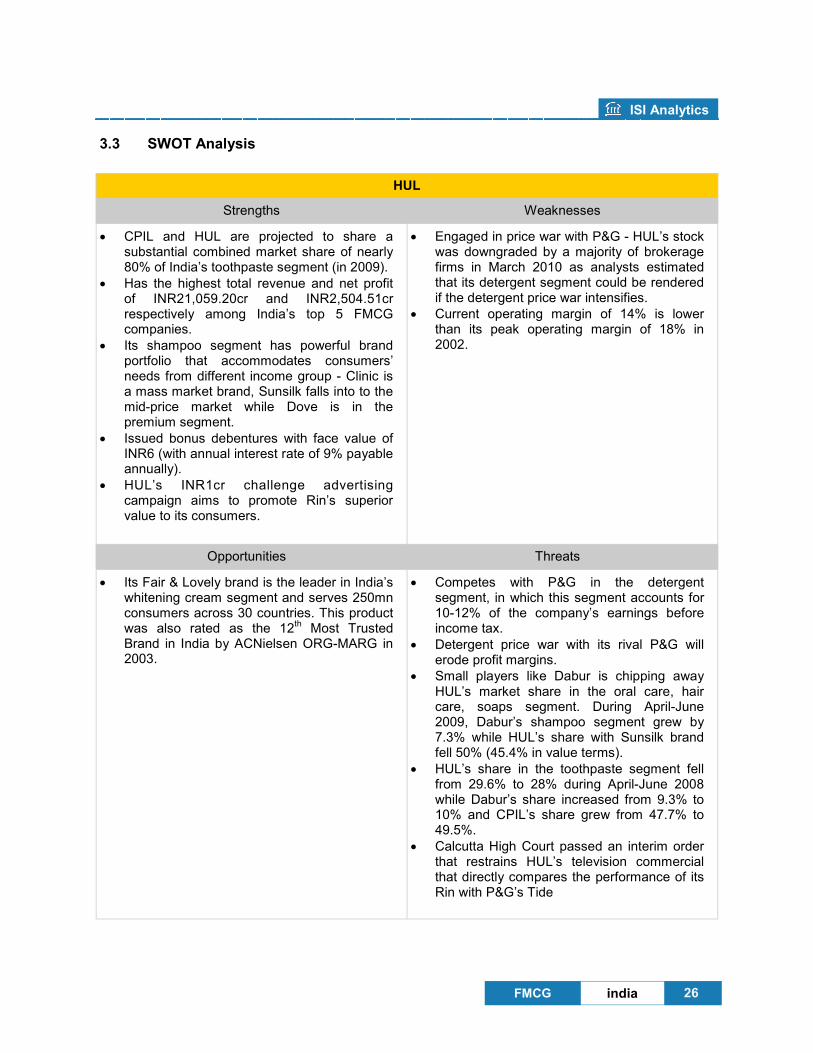

Strengths Weaknesses

• CPIL and HUL are projected to share a substantial combined market share of nearly 80% of India’s toothpaste segment (in 2009).

• Has the highest total revenue and net profit of INR21,059.20cr and INR2,504.51cr respectively among India’s top 5 FMCG companies.

• Its shampoo segment has powerful brand portfolio that accommodates consumers’ needs from different income group - Clinic is a mass market brand, Sunsilk falls into to the mid-price market while Dove is in the premium segment.

• Issued bonus debentures with face value of INR6 (with annual interest rate of 9% payable annually).

• HUL’s INR1cr challenge advertising campaign aims to promote Rin’s superior value to its consumers.

• Engaged in price war with P&G - HUL’s stock was downgraded by a majority of brokerage firms in March 2010 as analysts estimated that its detergent segment could be rendered if the detergent price war intensifies.

• Current operating margin of 14% is lower than its peak operating margin of 18% in 2002.

Opportunities Threats

• Its Fair & Lovely brand is the leader in India’s whitening cream segment and serves 250mn consumers across 30 countries. This product was also rated as the 12

th Most Trusted

Brand in India by ACNielsen ORG-MARG in 2003.

• Competes with P&G in the detergent segment, in which this segment accounts for 10-12% of the company’s earnings before income tax.

• Detergent price war with its rival P&G will erode profit margins.

• Small players like Dabur is chipping away HUL’s market share in the oral care, hair care, soaps segment. During April-June 2009, Dabur’s shampoo segment grew by 7.3% while HUL’s share with Sunsilk brand fell 50% (45.4% in value terms).

• HUL’s share in the toothpaste segment fell from 29.6% to 28% during April-June 2008 while Dabur’s share increased from 9.3% to 10% and CPIL’s share grew from 47.7% to 49.5%.

• Calcutta High Court passed an interim order that restrains HUL’s television commercial that directly compares the performance of its Rin with P&G’s Tide

HUL

3.3 SWOT Analysis

26

ISI Analytics

FMCG india

Strengths Weaknesses

• Nirma currently has the largest market share in India’s detergent market (38%) and the second largest share in toilet soap segment (20%).

• Sought alternative markets, reallocated its employees and introduced maintenance programmes to counter the effects of the recessionary pressure in the US market.

• Net sales grew from INR2,684.46cr in FY2007-08 to INR4,574.82cr during the next fiscal.

Opportunities Threats

• Nirma’s consolidated revenue was mainly contributed by the soaps and surfactants, processed minerals and pharmaceutical segments - the company could further invest in India’s toothpaste segment as it offers potential growth opportunities (low per capital toothpaste consumption).

• Worldwide recession impacted Nirma’s processed minerals segment as global demand for soda ash shrank due to contractions in the construction and auto industries.

Nirma

3.3 SWOT Analysis (Cont’)

27

ISI Analytics

FMCG india

3.3 SWOT Analysis (Cont’)

28

Strengths Weaknesses

• Demerged its pharmaceutical operations from FMCG segment so that each entity can focus on their respective operations.

• Adopted an inorganic growth strategy through the acquisition of Mumbai-based Balsara’s oral care and household care product in a INR143cr all-cash deal, thus adding brands such as Promise, Babool, Sanifresh and Odonil to its product range as well as expand its scale of operation through synergies.

• Consolidated revenue ballooned 18.3% to INR2,834.1cr during the FY2008-09 while consolidated net profit grew 17.5% to INR391.2cr.

• During April-June 2009, Dabur’s shampoo segment grew by 7.3%

• Lack financial stability and market presence to compete with multinationals like CPIL and HUL in the oral care market - both CPIL and HUL are estimated to enjoy a combined market share of 85% in India while DIL has a 10% share.

Opportunities Threats

• Entered the organised retail business through H&B Stores Ltd.

• Will invest INR140cr by 2010 to establish a chain of stores selling health and beauty products.

• Seek to acquire South African hair care company - Isoplus that generates sales of nearly INR100cr.

• Competes with FMCG giants like HUL and CPIL in India’s INR16,000cr oral care segment.

DIL

ISI Analytics

FMCG india

3.3 SWOT Analysis (Cont’)

29

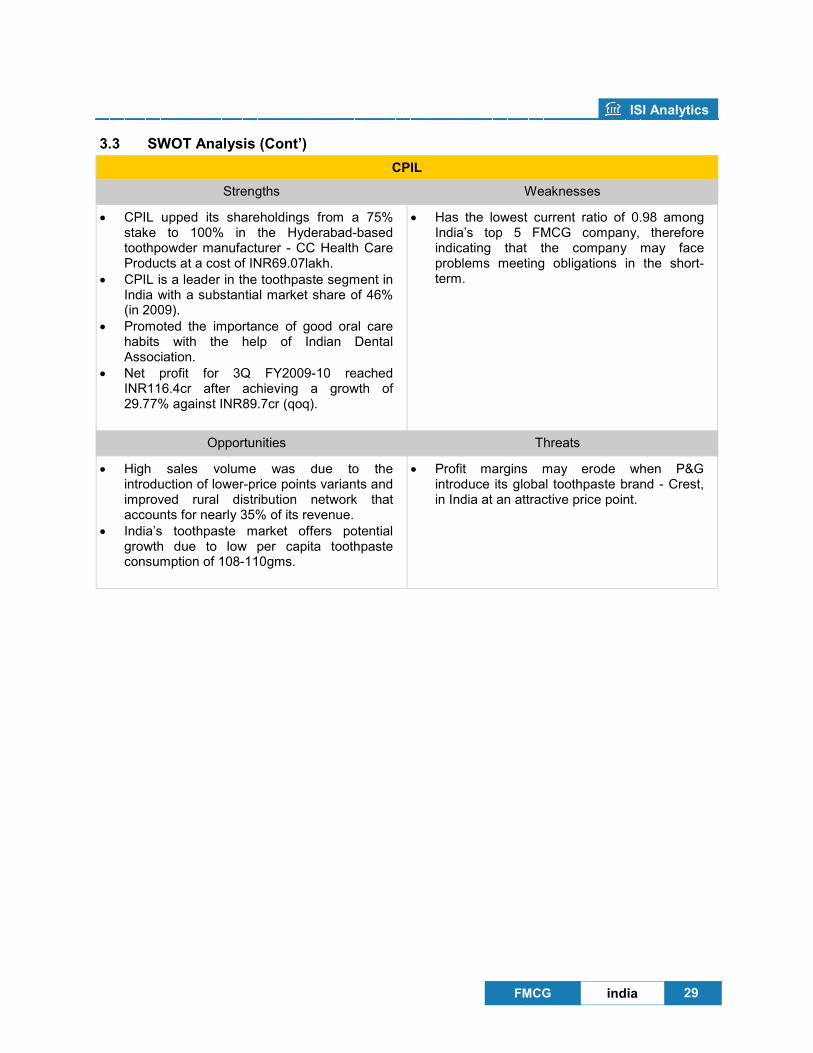

Strengths Weaknesses

• CPIL upped its shareholdings from a 75% stake to 100% in the Hyderabad-based toothpowder manufacturer - CC Health Care Products at a cost of INR69.07lakh.

• CPIL is a leader in the toothpaste segment in India with a substantial market share of 46% (in 2009).

• Promoted the importance of good oral care habits with the help of Indian Dental Association.

• Net profit for 3Q FY2009-10 reached INR116.4cr after achieving a growth of 29.77% against INR89.7cr (qoq).

• Has the lowest current ratio of 0.98 among India’s top 5 FMCG company, therefore indicating that the company may face problems meeting obligations in the short-term.

Opportunities Threats

• High sales volume was due to the introduction of lower-price points variants and improved rural distribution network that accounts for nearly 35% of its revenue.

• India’s toothpaste market offers potential growth due to low per capita toothpaste consumption of 108-110gms.

• Profit margins may erode when P&G introduce its global toothpaste brand - Crest, in India at an attractive price point.

CPIL

ISI Analytics

FMCG india

3.3 SWOT Analysis (Cont’)

30

Strengths Weaknesses

• Branches offices and factories are located in various parts of India so that the company’s diverse product portfolio can accommodate different requirements.

• GCPL also have several international brands and trademarks in Europe, Australia, Canada, Africa and the Middle East.

• During the quarter ended 30th September,

2009, GCPL’s net profit grew 167.78% to INR93cr.

• Too much diversification may steer the company away from its core business operations.

Opportunities Threats

• UK-based Keyline Brands Ltd was acquired by the Group, thereby allowing the Group to diversify country risks.

• Surge in net profit was a result of lower palm oil price.

• Acquired Nigeria-based Tura to penetrate markets in the pan-African region.

• Competes with other FMCG giants like HUL and CPIL that has vast experience in global FMCG segment.

GCPL

The research report is based on material compiled from data considered to be reliable at the time of

writing. However, information and opinions expressed will be subject to change without notice. We do

not accept any liability directly or indirectly that may arise from investment decision-making based on

this report.