fall 2008 version professor dan c. jones fina 4355 handouts

TRANSCRIPT

Fall 2008 VersionFall 2008 Version

Professor Dan C. Jones

FINA 4355

Handouts

Risk Management and Insurance: Perspectives in a Global EconomyRisk Management and Insurance: Perspectives in a Global Economy

9. Public-Sector Economic Security9. Public-Sector Economic Security

Professor Dan C. Jones

FINA 4355

Handouts

3

Study PointsStudy Points

Why private markets fail to provide some financial services

Selected public-based economic security services

The future of social insurance

Why Private Markets Fail

5

Market FailureMarket Failure

Market failure stemming fromFinancial intermediaries refusing to offer an otherwise demanded service

Prices being so high that no or only a modest market evolves

Causes of the failureFinancial intermediaries cannot adequately address the information problems that they encounter.

Positive externalities accompany the purchase.

Buyers have insufficient income.

Risk aversion is insufficient to motivate individuals to pay high loadings.

6

Cause – Information ProblemsCause – Information Problems

Financial markets are characterized by adverse selection and moral hazard problems.

Where the usual techniques for dealing with these information problems do not work well or at all, the private sector offers no solutions or offers them only at very high prices.

Also discussed in Chapters 2, 8 and 19.

7

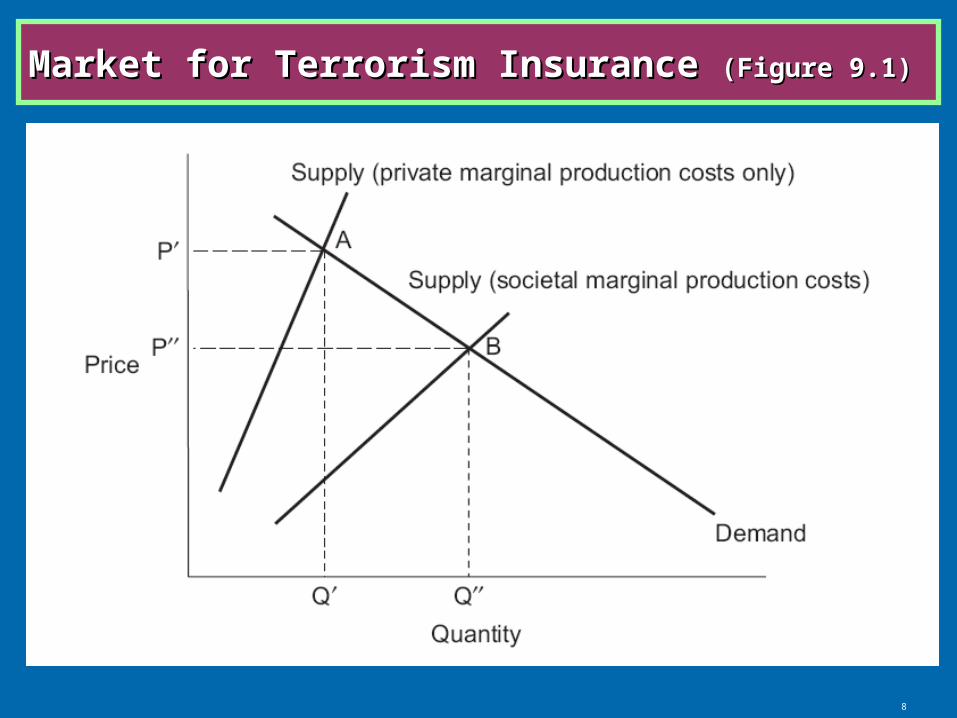

Cause – Fails to Capture Positive ExternalitiesCause – Fails to Capture Positive Externalities

To the extent that society receives positive spillovers from someone having acquired additional security, the price will be too high because it reflects only private producers’ marginal costs of production and fails to credit against those costs the marginal societal benefits.

As with all activities and products that exhibit positive externalities, individuals will consume too little (in society’s view) if they must pay the full private cost.

ExamplesThe market for terrorism insurance (figure 9.1)

Social insurance (figure 9.2)

8

Market for Terrorism Insurance Market for Terrorism Insurance (Figure 9.1)(Figure 9.1)

9

Social Insurance Social Insurance (Figure 9.2)(Figure 9.2)

10

Cause – Insufficient Buyer IncomeCause – Insufficient Buyer Income

Many individuals have income that are insufficient to pay for life’s necessities (immediate utility) and for financial security services (future utility).

The interest rate necessary to induce a poor person to forego current consumption for future consumption is exceptionally high, maybe even infinite.

In the absence of positive externalities, insufficient income provides no economic justification for government becoming a provider of financial security services. But,

Some economic security services do carry positive externalities.

Societies often choose to provide security services for non-economic reasons (e.g., concerns about fairness).

11

Cause – Insufficient Buyer Risk AversionCause – Insufficient Buyer Risk Aversion

Intermediaries incur expense and other cost loadings, which may be viewed high for several reasons

Illustration using insurance

Low-severity or high-frequency exposures

Correlated exposures

Exposure ambiguity

12

Public-based Economic Security ServicesPublic-based Economic Security Services

Social insuranceThe most important government-provided economic security services in most countries

Mandatory savings programs

Economic-needs-tested programs

The remaining part of the chapter discusses mainly social insurance. The other two discussed in page 228.

Social Insurance

14

FundamentalsFundamentals

Social insurance provides income security for individuals and is also an important public policy instrument

Government-sponsored economic security program that insures individuals and families against interruption or loss of earning power or health and which possesses three characteristics:

Economic security is provided for well-defined loss exposures.

Participation is compulsory for the target population.

Contributions usually are not adjusted for probability of loss.

15

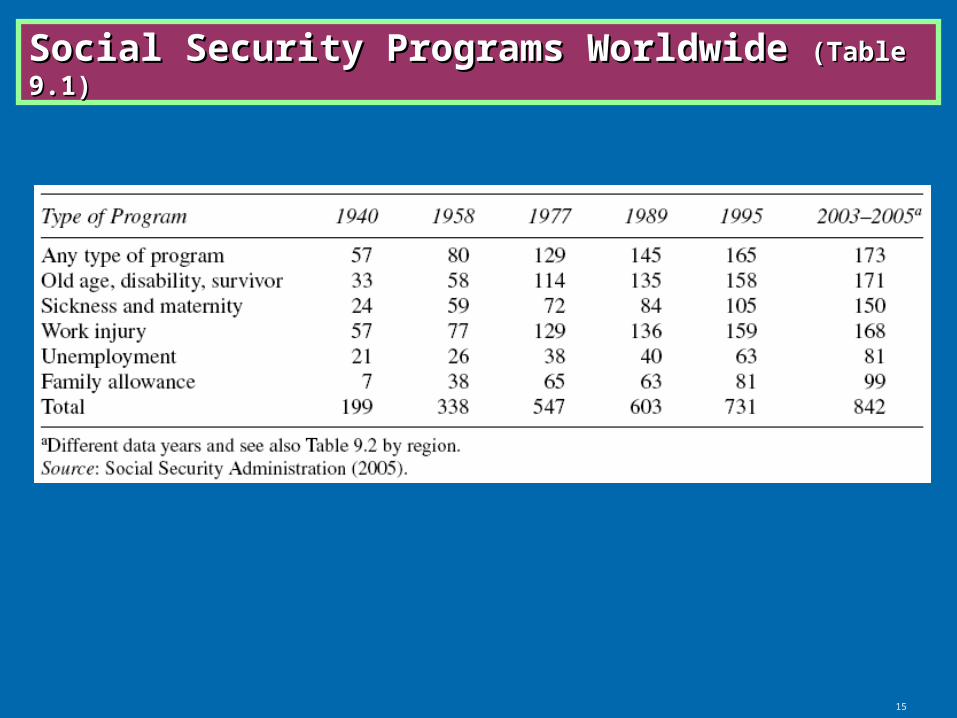

Social Security Programs Worldwide Social Security Programs Worldwide (Table 9.1)(Table 9.1)

16

Comparison of Programs by Region Comparison of Programs by Region (Table 9.2)(Table 9.2)

17

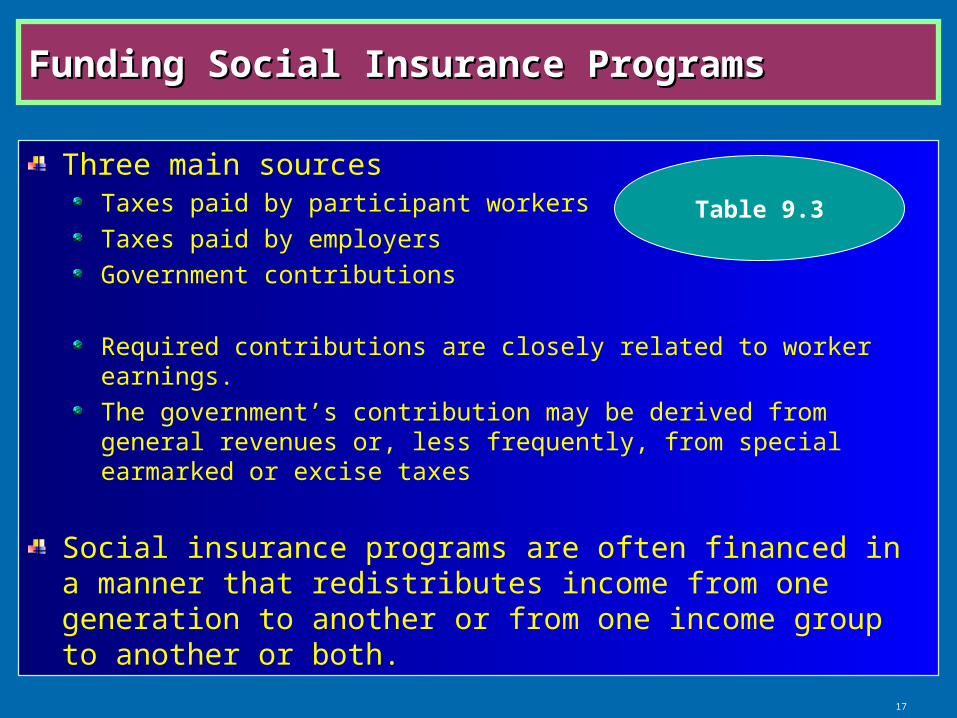

Funding Social Insurance ProgramsFunding Social Insurance Programs

Three main sourcesTaxes paid by participant workers

Taxes paid by employers

Government contributions

Required contributions are closely related to worker earnings.

The government’s contribution may be derived from general revenues or, less frequently, from special earmarked or excise taxes

Social insurance programs are often financed in a manner that redistributes income from one generation to another or from one income group to another or both.

Table 9.3

18

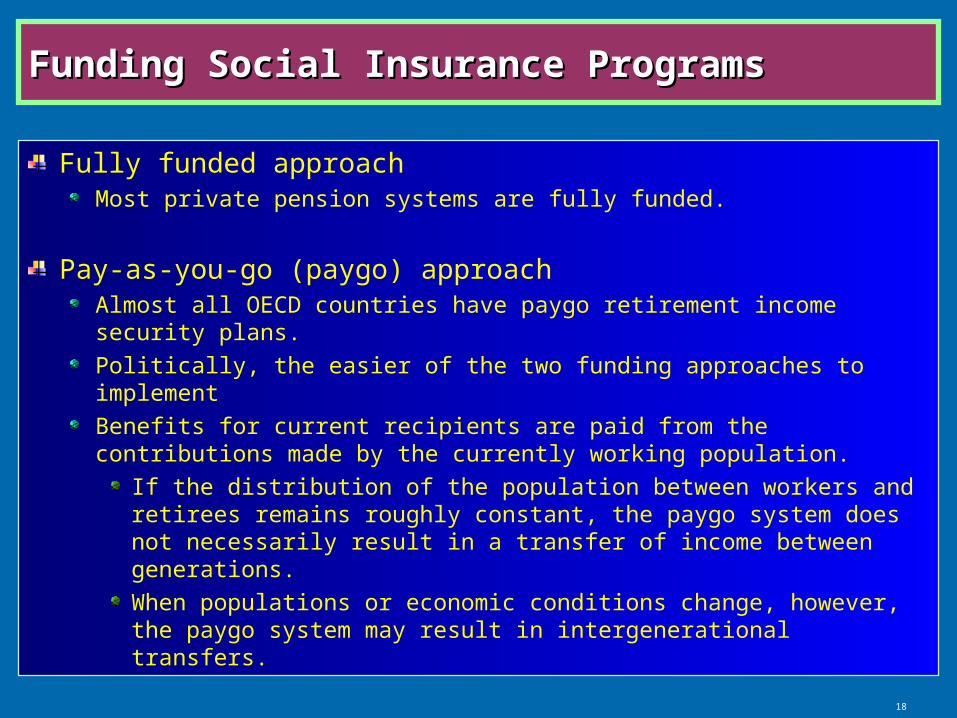

Funding Social Insurance ProgramsFunding Social Insurance Programs

Fully funded approachMost private pension systems are fully funded.

Pay-as-you-go (paygo) approachAlmost all OECD countries have paygo retirement income security plans.

Politically, the easier of the two funding approaches to implement

Benefits for current recipients are paid from the contributions made by the currently working population.

If the distribution of the population between workers and retirees remains roughly constant, the paygo system does not necessarily result in a transfer of income between generations.

When populations or economic conditions change, however, the paygo system may result in intergenerational transfers.

19

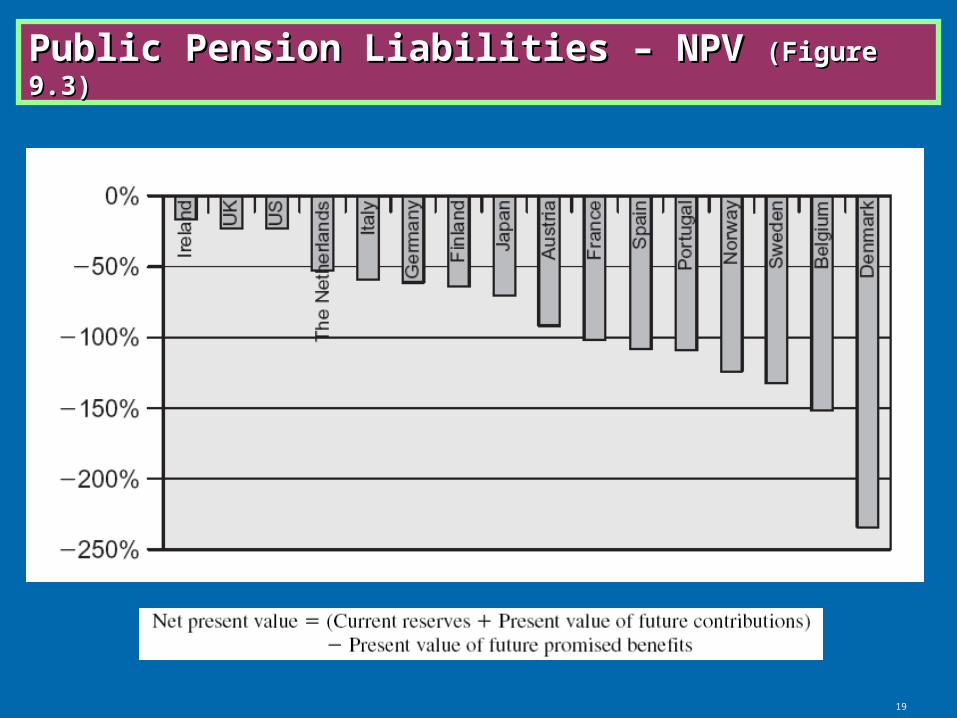

Public Pension Liabilities – NPV Public Pension Liabilities – NPV (Figure 9.3)(Figure 9.3)

20

Social Insurance BenefitsSocial Insurance Benefits

Retirement income

Survivor benefits

Health insurance

Unemployment insurance

21

Social Insurance Benefits – RetirementSocial Insurance Benefits – Retirement

Support for the elderly has been a prime focus of social insurance.

Individuals may not have the information needed to prepare adequately for retirement.

There are economies of scale in funding retirement benefits.

The elderly’s consumption is likely to have external benefits to society.

22

Social Insurance Benefits – RetirementSocial Insurance Benefits – Retirement

Scopes of CoverageOriginally available only to government employees and the military

Gradually extended first to private-sector workers in urban areas and then to virtually all wage earners and salaried employees

Initially excluded from coverage agricultural workers and the self-employed due mainly to administrative difficulty. Also commonly excluded were family workers, domestics and day workers.

The trend has been to cover these groups under separate funds or to bring them under the general system.

Even the non-employed may now be covered.

23

Social Insurance Benefits – RetirementSocial Insurance Benefits – Retirement

Plan design and reform objectivesProvide economic security against destitution in old age

Smooth the distribution of consumption spending over a lifetime

Provide for life’s requirements for those with exceptional longevity

Three distinct tiersThe first tier – provides poverty relief, normally in a public system funded on a paygo basis participation with mandatory

The second tier – provides for consumption smoothing over each person’s lifetime

The third tier – private, funded and voluntary

24

Social Insurance Benefits – RetirementSocial Insurance Benefits – Retirement

Plan design and reform – IMF’s proposals

All pension systems, no matter how financed, require strong and effective government to succeed.

The choice between government paygo and (private or public) funded schemes is of secondary importance to the government’s ability to manage the economy effectively, to promote adequate output growth, and to sustain a stable foundation for whatever pension system is adopted.

Within the limits of national economic and government capacity, countries have a wide range of choice over pension design. No one approach will prove superior.

25

Social Insurance Benefits – RetirementSocial Insurance Benefits – Retirement

Benefit qualification – eligibility requirementAttainment of a specified age and

Completion of a specified period of contributions or covered employment

Many programs have the same pensionable age for women as for men.

Nature of benefitsIn most countries, retirement benefits are wage-related and based also on formulas. For example,

A basic rate (e.g., 30%) of average earnings, plus an increment of 2% of earnings for each year of service in excess of a minimum number of years for qualification

26

Social Insurance Benefits – Survivor BenefitsSocial Insurance Benefits – Survivor Benefits

Most social insurance programs provide for some type of payment to dependents

Spouse and dependent children under a certain age

Patterned closely after their counterpart retirement income benefit programs

Funding for survivor benefits ordinarily follows that for retirement income benefits.

EligibilityThe deceased worker was a pensioner at death or have completed a minimum period of covered employment or contribution.

Certain additional conditions such as age requirement

27

Social Insurance Benefits – Survivor BenefitsSocial Insurance Benefits – Survivor Benefits

Periodic benefits for survivors of covered persons or pensioners are provided under most systems, although a few pay lump-sum benefits only.

Survivor benefits are paid to some categories of widows under nearly all programs.

The age limits for children’s benefits are often the same as for children’s allowances through retirement income or disability income benefit programs.

Benefits are payable under a number of programs to certain widowers of insured workers or pensioners.

28

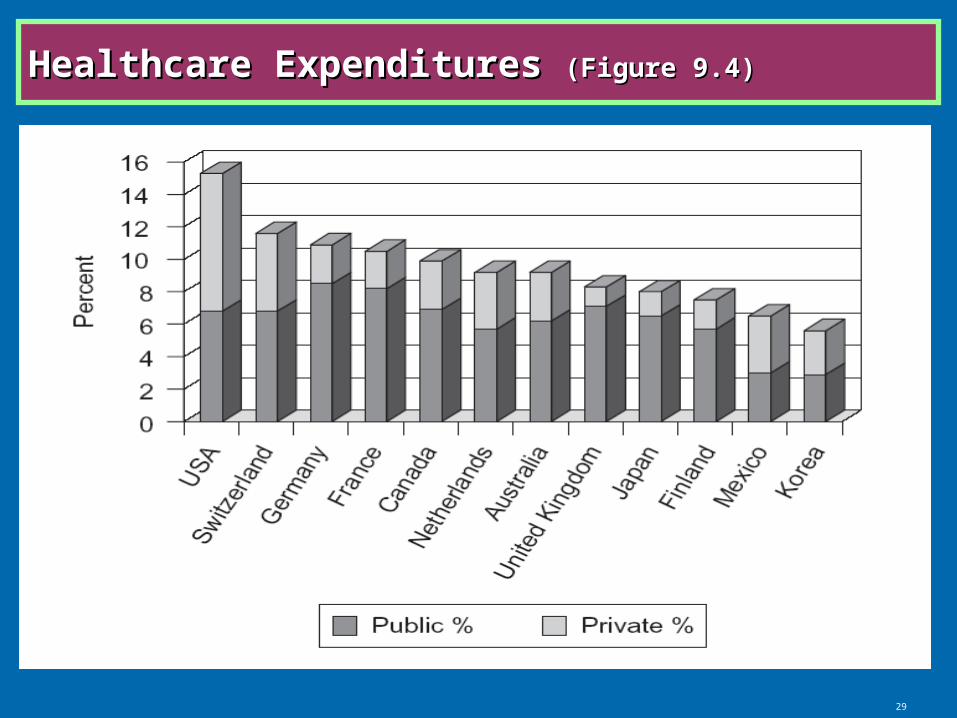

Social Insurance Benefits – HealthSocial Insurance Benefits – Health

The healthcare delivery and financing systems reflect the cultural, economic and political character of the nation.

Most industrialized countries place great value on equal access to healthcare across individuals, and provide basic universal coverage to all.

It is not the case in the U.S., which does not have a national healthcare program. The culture in the U.S. places relatively less value on social equity and relatively greater value on private-market solutions to financing healthcare.

29

Healthcare Expenditures Healthcare Expenditures (Figure 9.4)(Figure 9.4)

30

Economics of Healthcare – Market ImperfectionsEconomics of Healthcare – Market Imperfections

Difficulty in measuring marginal benefit of additional medical service on health

Buyers cannot purchase health per se but consume medical services to improve or maintain health.

Presence of information asymmetries, including adverse selection

Information asymmetry exists between buyers and sellers.

Information asymmetries exist with respect to the price of medical services.

Information asymmetries exist between insureds and insurers.

31

Economics of Healthcare – Market ImperfectionsEconomics of Healthcare – Market Imperfections

Problems of moral hazardThird-party payment for healthcare services not only reduces incentives for consumers to seek price information, but also increases the potential for moral hazard, another information asymmetry.

consumer behavior may change since insureds do not bear the full cost of medical care.

Demand for services induced by suppliersthe provider of medical services not only supplies medical services to consumers, but also advises them on what to demand.

Barriers to market entryHealthcare markets have barriers to entry.

32

Economics of Healthcare – Market ImperfectionsEconomics of Healthcare – Market Imperfections

Other considerations

Cultural beliefs

Growth of medical technology

Medical malpractice costs

33

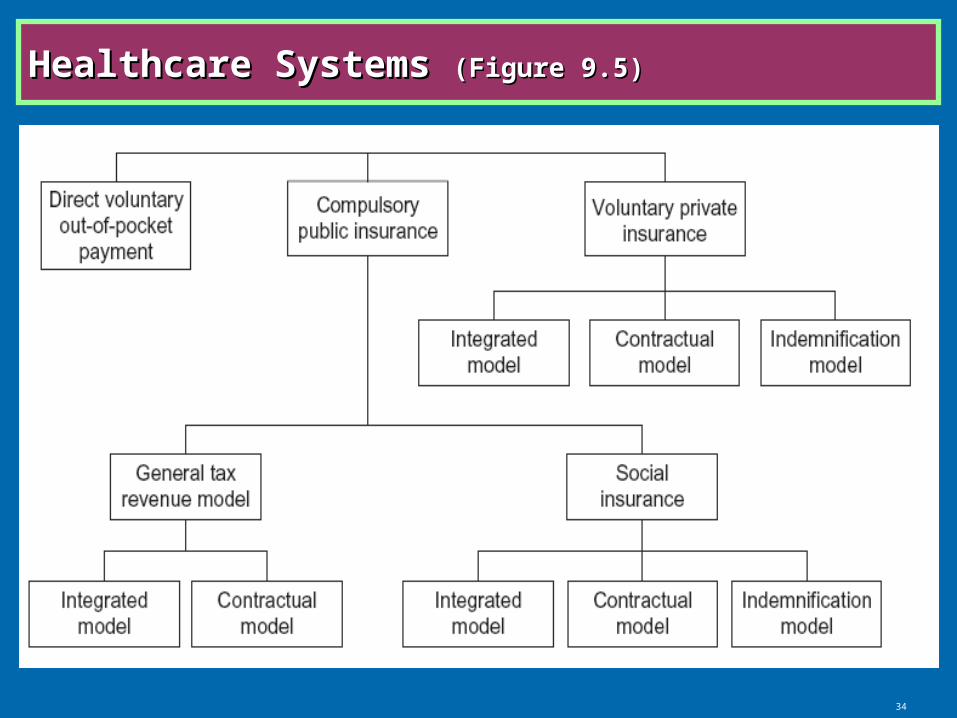

Healthcare SystemsHealthcare Systems

TrendsDeveloped countries have modern healthcare services available to most of the population. Developing countries tend to provide a higher

level of medical service to urban residents.

Delivery systems (Figure 9.5)Direct, voluntary out-of-pocket payment

Compulsory public insurance

General revenue tax model

Social insurance model

Voluntary private insurance

34

Healthcare Systems Healthcare Systems (Figure 9.5)(Figure 9.5)

35

Healthcare System Reform InitiativesHealthcare System Reform Initiatives

Increased use of the public contractual model

Greater use of third-party payers

Greater independence of hospital management

Enhanced use of managed care and cost sharing

36

Healthcare Spending and Health OutcomesHealthcare Spending and Health Outcomes

The prime determinant of differences in national spending for healthcare is national per capita income. Similarly, the variation in general health of populations is explained primarily by differences in income level.

A positive relationship between income and medical spending is expected, as is a positive relationship between education and income.

Nations with higher per capita incomes have longer life expectancy and lower infant mortality rates. Exceptions exist.

China, Sri Lanka and Vietnam

The U.S.

37

Social Insurance Benefits – DisabilitySocial Insurance Benefits – Disability

Most programs are structured such that those who participate in the retirement income plan also participate in the disability income plan.

Funding ordinarily follows that of retirement income benefit funding.

Benefit eligibility requirementsLoss of productive capacity and

Fulfillment of a minimum period of work or contributions

The qualifying period usually shorter than for an old age, retirement income benefit.

Table 9.5

38

Social Insurance Benefits – DisabilitySocial Insurance Benefits – Disability

Provisions for persons who are permanently disabled due to non-occupational causes are similar to those for retirement.

A relatively short waiting period (e.g., 2~7 days) is imposed.

Workers ordinarily may receive short-term benefits for up to 26 weeks.

39

Social Insurance Benefits – Occupational InjurySocial Insurance Benefits – Occupational Injury

Occupational-injury benefit programs – i.e., workers’ (workmen’s) compensation programs – are the oldest, most widespread type of social insurance.

Program structuresSocial insurance systems utilizing a public fund

Various forms of private or semiprivate arrangements required by law

Most countries maintain the work-injury programs that do not share a direct link with other social security programs.

In some other countries, the benefits are available under special provisions of the country’s social security programs.

40

Social Insurance Benefits – Occupational InjurySocial Insurance Benefits – Occupational Injury

Medical benefits: two variationsAll “necessary” medical services – unless specifically excluded in the law

A list of covered medical services

Income replacement benefitsA percentage of the (average) wage prior to disability, a stated monetary ceiling, or both

To minimize moral hazard and costs, most programs not offer full indemnification

Compensation varies according to the degree of disability:

Temporary disability

Permanent total disability

Permanent partial disability

Table 9.6

41

Social Insurance Benefits – Occupational InjurySocial Insurance Benefits – Occupational Injury

Survivor benefits

Customarily payable to a widow, regardless of her age, until her death or remarriage; to a disabled widower; and to dependent children below specified ages

Industrialization and occupational injury

Employment shifted from the manufacturing to the service sector

Claims associated with industrial injury and illness decreased

Growth in the number of recognized occupational diseases due to a greater understanding of the origins of certain diseases

42

Social Insurance Benefits – UnemploymentSocial Insurance Benefits – Unemployment

ObjectivesProvide periodic cash income to workers during temporary periods of involuntary unemployment

Help stabilize the economy during recessionary periods

Encourage employers to stabilize employment

Help the unemployed find jobs

The programs exist mainly in industrialized countries.About one-half of the compulsory unemployment programs cover the majority of employed persons, regardless of industry.

Table 9.7

43

Social Insurance Benefits – UnemploymentSocial Insurance Benefits – Unemployment

Program structuringMost are compulsory and fairly broad in scope.

Some countries rely on voluntary programs with no government mandate.

Some unemployment programs economic-needs tested

Some offer scheduled payments of benefits, and others provide lump-sum grants.

Contribution solely by employers is the typical method governments use to finance unemployment insurance.

The contribution usually as a fixed percentage of the covered payroll

44

Social Insurance Benefits – UnemploymentSocial Insurance Benefits – Unemployment

Benefit eligibilityCompletion of a minimum period of service in a covered employment

Involuntary unemployment

Nearly all unemployment insurance programs require that applicants be capable of and available for work.

BenefitsA percentage of the average wage during a recent period

Payable only after a waiting period

Several countries maintain unemployment assistance or similar means-tested programs supplementing regular unemployment insurance.

Mandatory Savings Programs

Economic-needs-tested Programs

46

Mandatory Savings ProgramsMandatory Savings Programs

Employees’ contribution toward their own personal retirement savings programs

Substitute for or complement paygo types of social insurance systems

The account holder often may purchase separate disability and survivors’ insurance coverages.

Little or no income redistribution among participantsThese programs do not meet our definition of social insurance.

Also known as provident funds

Table 9.8

47

Economic-needs-tested ProgramsEconomic-needs-tested Programs

Benchmarks each applicant’s resources to formula-based standards for subsistence need estimation and offers benefits only to applicants who satisfy the test

Different countries have different tests, but they commonly take into consideration

The net wealth and current income of the applicant and the familyHealth condition and age of the breadwinnerFamily sizePlace of living

If the program does not require contributions by the beneficiary, it is a social assistance (welfare) program intended to alleviate poverty.

It is not insuance.

48

The Future of Social InsuranceThe Future of Social Insurance

Selected factors affecting the insuranceRising healthcare costsLow birth ratesIncreasing life expectancyPaygo public pension systems preservation of economic security through equitable financing approachesSocial and political environmentsMacroeconomic performance

Transition into fully funded programs

Privatization of social insurance programsChileJapan

Discussion Questions

50

Discussion Question 1Discussion Question 1

Does flood insurance qualify as a social insurance program? Justify your answer.

51

Discussion Question 2Discussion Question 2

In the section on “Low-Severity or High-Frequency Exposures,” the authors discussed several types of loss exposures for which private insurance is unsuitable. What are the characteristics of exposures that insurers are willing to cover?

You may refer to Chapter 19 for a related discussion.

52

Discussion Question 3Discussion Question 3

Provide a rationale for instituting a paygo social insurance program.

53

Discussion Question 4Discussion Question 4

Discuss the implications of a successful social insurance program on a country’s finances.

54

Discussion Question 5Discussion Question 5

Compare public and private programs for providing retirement income. Who benefits under each type of program?